08 There is a deadly truth behind Pakistan’s growing rice exports

10 Treet Corp is banking on Lithium-ion batteries needed for EVs and solar. What is their gameplan?

12 What makes Pakistan’s $5 billion consumer lending market tick

18 Why Pakistan Never Built its Petrochemical Backbone Asif Saad

20 Pakistan’s IT exports are rising. Why is this, and how can it continue to grow?

27 Fast Cables believes in the adage that if you build it, they will come

31 UBL and Jazz just broke new ground in Pakistan’s financial markets

33 K-Electric’s battle for control: Al-Jomaih and Denham take Pakistan to court

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Usama Liaqat Shahab Omer | Zain Naeem | Nisma Riaz | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi)

Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

There is a deadly truth behind Pakistan’s growing rice exports

he increase in exports is led majorly by non-Basmati varieties as Pakistan pivots towards selling cheaper rice to low-value markets. Behind the increase is a major water crisis waiting to happen

By Abdullah Niazi

Last week, Pakistan’s rice exports surged past Vietnam to make Pakistan the third largest rice exporter in the world behind only Thailand and India. Pakistan exported 4.89 lakh tonnes of rice to the world compared to Vietnam’s 3.87 lakh tonnes in December 2025.

The increase is the result of a number of factors. On the international market, increased production in India has brought prices down and increased the demand for rice. Domestically, Pakistani farmers are turning towards rice production in greater numbers. Areas that are not traditionally rice growing regions have started growing high-yield non-Basmati variants. As a result, Pakistan’s exports to regions like Central Asia are growing significantly. While these are new markets for Pakistan and can contribute significantly to our exports and easing the trade deficit, there is a massive cost to these exports.

A major reason for farmers turning towards rice is the availability of cheap solar panels. They have allowed farmers to run their

tubewells at near-zero cost during the day to get the water needed to feed what is a water guzzling crop. This increased water consumption is fast depleting the water table in agricultural districts and will cause a massive strain on Pakistan’s water resources in the coming years. On top of this, farmers are also turning towards different varieties such as Kainta, which is branded and sold as Basmati in markets like Central Asia and Africa. This means Pakistani farmers are fast abandoning traditional Basmati, which can be a designer high-value export if marketed properly.

More rice, more exports, less water

Pakistan has been growing more rice in recent years. According to Faisal Jahangir, Chairman of the Rice Exporters Association of Pakistan (REAP), the overall rice cultivation area has increased by 20% compared to last year. The increase in area has even allowed rice farmers to avoid the worst of the damage caused by last year’s floods.

The total expected production of rice this year is around 1.1 crore metric tons. With the Pakistan Bureau of Statistics estimating domestic consumption at 20-25 lakh metric tonnes, that leaves Pakistan with a surplus of around 80 lakh metric tons that can be exported. This would be a significant increase from exports in FY 2024-25, which totaled 58 lakh mt, a 3.5% decline compared to FY 2023-24.

But the increase in rice exports has come at the expense of Pakistan’s traditional Basmati variety. According to a report of the United States Department of Agriculture (USDA), this shift is causing serious strain on Pakistan’s water resource. “Higher yielding hybrid varieties, especially in non-Basmati, have replaced the older non-hybrid varieties. However, growth is modest in basmati production as the basmati area is limited to a few districts in Punjab and few new high yielding varieties have been introduced in recent years,” reads the report.

The report goes on to specify the ongoing increase in rice cultivation is depleting available irrigation water, which is already diminished due to dam sedimentation. “To obtain more water, farmers have relied more on

The overall rice cultivation area has increased by 20% compared to last year. The increase in area has even allowed rice farmers to avoid the worst of the damage caused by last year’s floods

Faisal Jahangir, Chairman of the Rice Exporters Association of Pakistan (REAP)

digging wells, resulting in a drop in the water table. Future growth in rice area and production will depend on the increased availability of irrigation water.”

The digging of wells and usage of groundwater through tubewells has become financially feasible for farmers because of the glut of solar panels in the country. According to a Reuters report from October 2025, farmers are increasingly ditching diesel and grid power for sun-powered tube wells. “There are no recent official estimates on the number of tube wells in Pakistan, which doesn’t require their registration. But so widespread is their use that farmers choosing to power the devices with solar are set to drive a 45% collapse in the amount of grid electricity consumed by the agriculture sector in the three years through 2025, said energy economist Ammar Habib, who serves as an advisor to Pakistan’s power minister. His estimate was based on consumption data published by the national energy authority,” reads the report.

According to the data, some 400,000 tube wells that once relied on grid electricity have switched to solar. Farmers using solar panels have likely purchased an additional 250,000 tube wells since 2023, signalling that the sun now powers roughly 650,000 such devices across Pakistan.

“When you export crops like rice and sugarcane, you are not exporting the crops, you are exporting water,” says Khalid Khokhar,

the Chairman of the Kissan Ittehad, which is Pakistan’s largest advocacy collective for farmers. Mr Khokhar, who is a cotton farmer from South Punjab, claims the increase in sugarcane and rice production is very burdensome on water resources and will have serious consequences in the future. “We are giving up on cotton, which we once called White Gold, and are replacing it with white poison.

Faisal Hassan, a traditional Basmati farmer from Hafizabad, says that Basmati farmers of Central Punjab have had their livelihoods decimated in the recent floods. “Pests and weather conditions have had a deep effect. I was estimating production of 50-60 mounds but we are barely getting 10 mounds,” he says. Mr Hassan is a second generation Basmati farmer and his father developed the famous “Kernal Basmati” variant back in the 1960s. However, since then the development of Basmati varieties has all but stopped, and farmers have turned towards varieties like Japonica and Kainat.

The Kainat variety is actually similar in some respects to Basmati and has been branded and sold as Basmati in many parts of the world.

New markets

Another factor in the growing exports is Pakistan’s pivot towards new markets. Last month, the UAE remained the top destination

for Pakistani rice, importing 74,897 tonnes, including 16,850 tonnes of Basmati. China followed closely with 74,685 tonnes, while other major destinations included African countries. Saudi Arabia imported 16,032 tonnes, including 5,350 tonnes of Basmati, the EU and UK combined imported 21,100 tonnes, including 15,600 tonnes of Basmati.

However, exports to Kazakhstan exceeded 17,000 tonnes, including 10,300 tonnes of Basmati, while shipments to Uzbekistan stood at 10,382 tonnes. The growing exports to Central Asia are significant, but exporters remained cautious of the reporters.

One major exporter from Karachi speaking on the condition of anonymity told Profit the increasing exports were a function of selling “fragrant” rice varieties and branding them as Basmati. “There is a big difference. Fragrant rice is varieties like Kainat which are not Basmati, but Central Asian markets and other regions do not know the difference. Traditional Basmati can only be grown in certain districts and if branded correctly can be sold at a premium in the EU and American markets,” he claims. “But because it is easier to grow the other varieties, the government and export associations often collude to sell new non-Basmati varieties that also use up more water.”

When you export crops like rice and sugarcane, you are not exporting the crops, you are exporting water

Khalid Khokhar, Chairman of the Kissan Ittehad

Pakistan was once a bigger rice exporter than India. However, the failure to brand its rice led to Indian exporters in the 1980s buying Basmati rice from Pakistan and selling it in Europe and America as Basmati where it became famous. Today, Pakistani Basmati does not have anywhere near the branding that Indian Basmati has, which has led us to focus on exporting non-Basmati varieties.

The potential of premium Basmati is massive, but traditional growers claim it will require seed research, proper categorisation and definition of what is Basmati, and a concentrated effort to market Pakistan’s superior Basmati rice in high value markets such as the EU, United Kingdom, USA, and Canada where there is a great demand for Basmati. n

Treet Corp is banking on Lithium-ion batteries needed for EVs and solar. What is their gameplan?

With the rising trend of electric vehicles and the collapse of solar net metering for domestic consumers, Treet wants to be an early mover in what will certainly be a booming market

By Usama Liaqat

Last week, the federal government announced it had finalised a draft of the National Lithium-Ion Battery Manufacturing Policy 2026–2031. The ambitious policy lays out a roadmap by which Chinese firms will help Pakistan set up assembling and manufacturing facilities for Lithium-ion batteries in deals potentially worth $558 million.

The timing of this is vital. Pakistan is fast seeing the adoption of electric vehicles, particularly with the introduction of Chinese EV brands such as BYD which have launched to a resounding response from buyers. At the same time, Pakistan is fast shifting towards solar. Not only do industrial consumers want to shift towards solar, rooftop solarisation has become a lifeline for both urban and rural domestic consumers.

Up until a few years ago, Pakistan’s battery demand was largely restricted to small Valve-Regulated Lead-Acid (VRLA/AGM) batteries. These are engineered for short-term, instant power backup and are the batteries used with the UPS in homes and offices and in traditional combustion engine vehicles. However, EVs and solar setups require daily, and irregular charging cycles which can only be achieved by Lithium-ion batteries.

With the growing trend of EVs and plug-in hybrids as well as the government’s continued assault on its own net-metering policy for solar households, there is an increasing anxiety among people to go off the grid — something that can only be achieved through lithium-ion batteries.

Pakistan’s current battery landscape has a number of players including Exide, Osaka, Phoenix, Atlas and others. The Treet Corporation is also a strong challenger in this segment selling Daewoo brand batteries.

However, Lithium-ion batteries are a whole different ball game and require technical knowledge as well as more state of the art facilities. While Treet is more famous for their shaving products, the company is hoping to use their existing experience in lead-acid batteries (where they have revenues of Rs 8.8 billion last year) to enter this emerging market.

Whether this attempt of Treet’s is successful or not will depend not only on how the company is able to deal with challenges in setting up such a plant on its own, but also on the clarity and consistent implementation of the government’s policies towards encouraging this ecosystem. If successful, it would have significant implications for the future of energy consumption in Pakistan – by not only driving solar adoption by reducing prices, but also contributing to an array of green technologies that will be indispensable to achieve Pakistan’s Green objectives.

Treet’s Bid

Currently, Pakistan is reliant upon imports for Lithium-ion batteries. According to an IEEFA report from 2025, Pakistan imported approximately 1.25 gigawatt-hours (GWh) of lithium-ion battery packs in 2024. Given that the same report estimates that this import could reach up to 8.75 GWh by 2030, if the trends stay on, it is likely to present a big problem for Pakistan’s current account deficit.

And Treet is stepping in to help fill this gap. Talking to Profit, the CEO of Treet Corporation, Syed Sheharyar Ali, highlighted the key infrastructural requirements for setting up such a production plant. “Controlled assembly environments; advanced electrical and thermal testing facilities; strong quality and traceability systems; trained personnel with lithium-specific safety expertise,” he says. At the same time, setting up such systems “Pakistan needs BESS-specific standards aligned with international norms” on the regulatory side.

In order to kickstart this process, Treet is collaborating with Highstar Digital Energy Technology, a Chinese manufacturer of Lithium-ion batteries. Initially, this partnership would involve the import and sale of Lithium-ion batteries, but the nature of the partnership is “strategic and technology-driven,” averred Syed Sheharyar Ali. In fact, import is only part of the partnership.

The aim is to eventually start and sustain local pack assembly and system integration, while relying on sourcing the core cell chemistry globally. This partnership with Highstar is a step that is envisioned to lead to this stage. It is supposed to be a three-phase roadmap: “(i) initial import of proven lithium-ion energy storage systems; (iii) local assembly and system integration; and (iii) gradual localization as volumes and economics allow”.

The potential, if this thing works out, is massive. In fact, beyond simply assisting the consumer demand for solar energy, lithium-ion battery storage could also assist in helping ease the load of electricity grids and support the transition to a green economy.

Read This: Treet Battery Limited partners with Highstar to introduce lithium-ion batteries in Pakistan

Utility-scale Battery Energy Storage Systems (BESS) represent one such example. Think of these essentially as massive UPS systems for the electricity grid. When the electricity supply is high, for example, excess energy would be stored in these mega battery systems. And, when the demand is high, this stored charge could then be released to meet this pressure. This is a way to achieve peak shaving (shaving is a specialty of Treet!), while also promoting grid stability. And developing a local lithium-ion

The demand for energy storage – driven by solar adoption and grid challenges – is large enough for multiple players

Syed Sheharyar Ali, CEO of Treet Corporation

production infrastructure would help achieve such promises at better price points.

Coming to the issue of price, enabling local production would likely push down prices for rooftop solar consumers. As Syed Sheharyar Ali noted, local assembly would reduce supply chain risks and hedge against the fluctuations in the currency value. Moreover, it would reduce lead times, as well as after-sales and warranty costs. The net effect, he noted, could result in “10–15% system-level cost reductions over time,” which would make such solar-plus-storage solutions more affordable.

What Stands in the Way?

Well, first of all, it’s the investment. Cells alone, as Syed Sheharyar pointed out, represent 60-70% of the total cost of the system, and these cells are priced globally, vulnerable to the vicissitudes of global market and politics. Then there is the investment that goes into setting up an industry-standard safety and testing infrastructure. But that’s mainly for the investor to finance, though the government can certainly help with subsidies and other measures to share the risk.

More important, however, are the structural constraints. The local regulatory infrastructure, to put it mildly, is elementary. Not only are local certification mechanisms lacking, but the batter recycling infrastructure is also practically absent. The latter is of key concern, because although lithium-ion batteries last longer (up to 10 years) than the lead-acid ones (usually 2 to 5 years), the infrastructure for the former is not particularly developed, even in developed countries. And the risk improper wastage of these systems would pose, might rack up as the usage increases, and come to bite Pakistan back.

Other than these concerns, the government’s policies to encourage the local produc-

tion of these systems are in the early stages, and it remains to be seen how effectively and consistently they are applied.

Syed Sheharyar Ali, for instance, highlighted what he thinks are the key measures needed to facilitate the local production of Lithium-batteries. He would like to see the explicit recognition of battery energy storage as a critical infrastructure element. At the same time, rationalised and consistent trade duties on cells, BMS, and safety components are required, so that there is clarity regarding production metrics, enabling better business planning and risk management.

Moreover, he emphasised the encouragement of clear safety, installation, and recycling standards, and urged that the government should provide incentives for phased localisation. Above all, however, Syed Sherharyar Ali stressed, “policy continuity is essential”.

In this context, we can also consider the government’s announcement from last month, where it announced that it was planning to encourage the development of BESS systems to stabilise the national grid. That is all well and good, but a lot hinges on how this move ties in with the recent plans to encourage local production of lithium-ion batteries. Success in this context would require an overarching energy policy that facilitates these both (and other) initiatives, and also need a stable political and economic environment for this policy to catch on.

At this stage, however, Treet is only one company, and this initiative could do with a push from more private actors taking up the challenge. And this fact was also recognised by Syed Sheharyar Ali, who noted that the “demand for energy storage – driven by solar adoption and grid challenges – is large enough for multiple players”. Perhaps, more government incentives are needed to encourage more local players to invest in this infrastructure, which might soon be one of the key determinants of whether the government is able to succeed in its environmental objectives or not. n

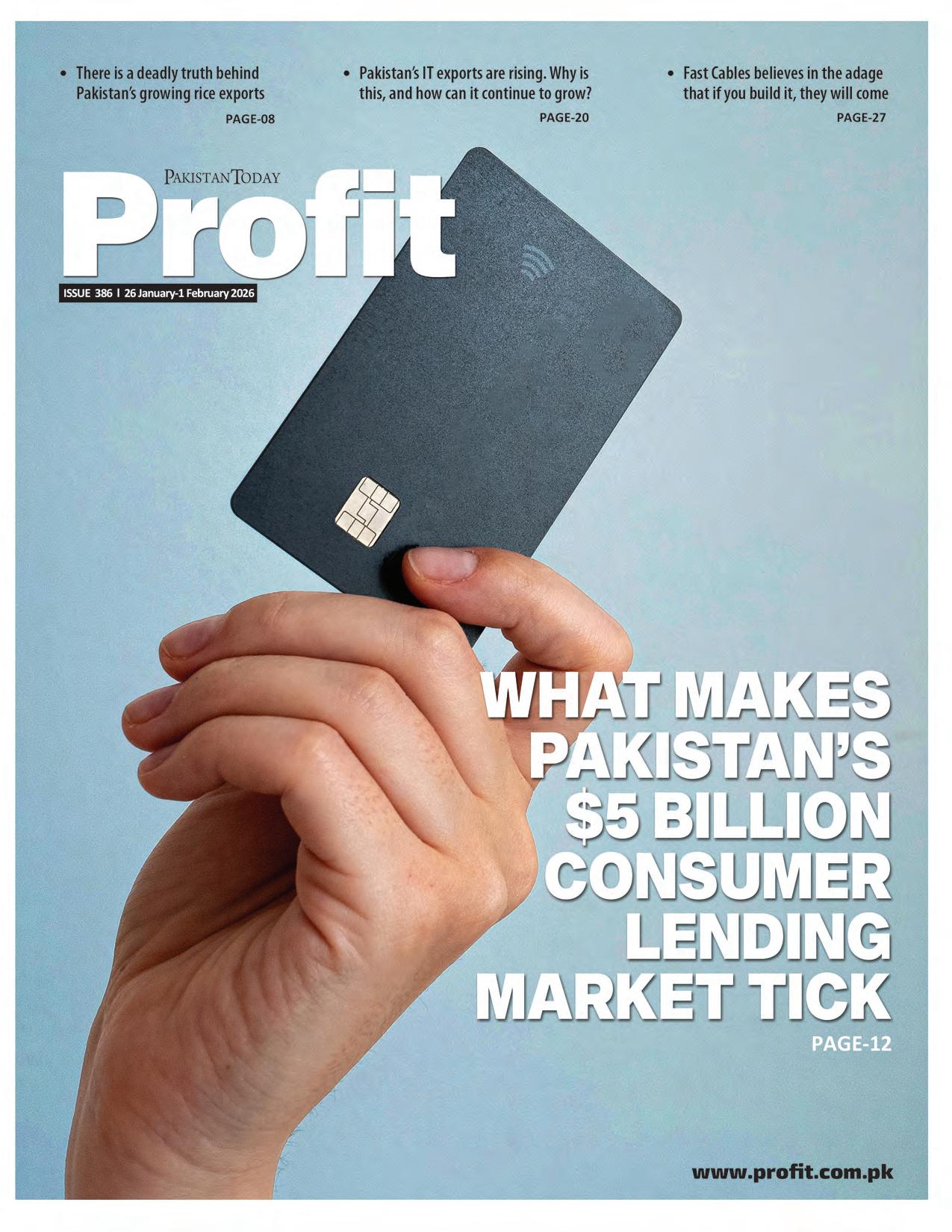

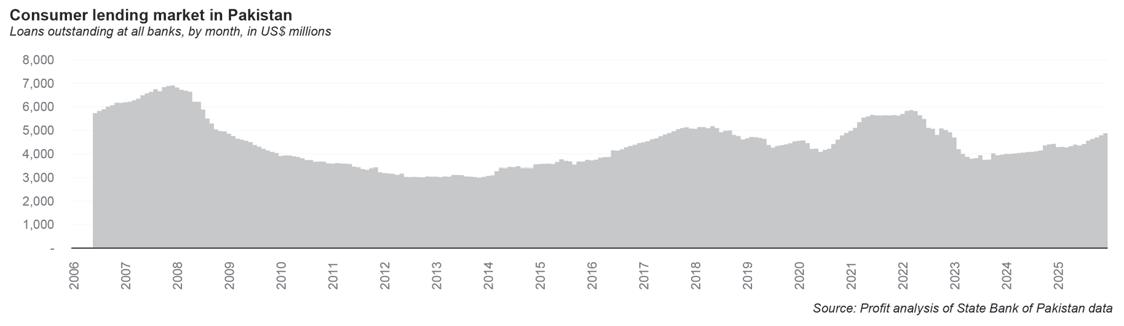

What makes Pakistan’s $5 billion consumer lending market tick

The sector is bigger than it looks, and while it has yet to surpass it Musharraf-era heyday, it is on a stronger economic footing than ever before

By Farooq Tirmizi

For a sector that is stereotyped as being highly risk averse, it appears that the Pakistani banking sector has learned how to lend to consumers, at least in small quantities. Some time over the course of the next year, total bank lending to non-employees will hit over Rs1 trillion. Unto itself, this is may simply be a psychological barrier, but the trend lines it represents belie the image of an otherwise staid financial services sector that has sworn off high-risk lending altogether.

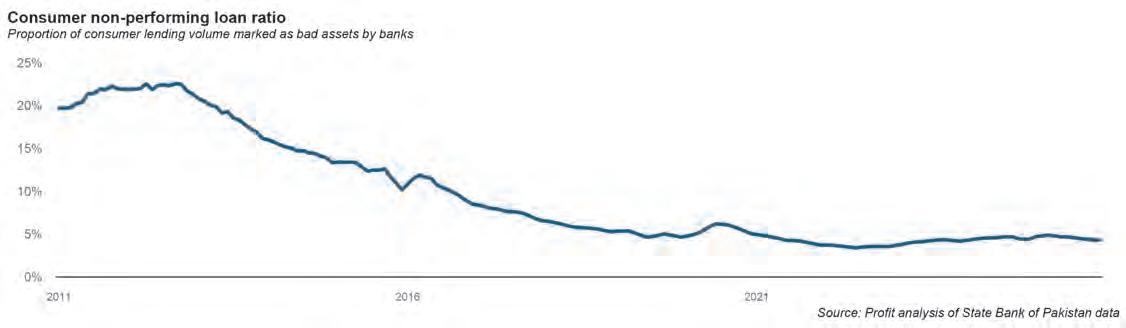

For instance, most people probably would not realize that the total size of the consumer lending market in Pakistan is about to hit $5 billion in total loans outstanding, and that non-performing loan ratio of this loan book is under 5% and has been for the last five years. Or that the total size of consumer lending doubled in rupee terms over just two years (2020 through 2022) but that non-performing loans did not go up during this time, or afterwards, despite interest rates skyrocketing past 20% during this period.

These are not data points that one is used to associating with the Pakistani banking sector. They sound like facts about a banking sector that actually knows how to lend. Of course, there is a flip side to this story as well, which we will also be exploring. But the picture of a credit squeezed Pakistani consumer, and a lazy banking sector that plows all deposits into government bonds, while mostly true, does have some complications that are interesting enough to explore in their own right.

This is a story of a banking sector that went in all guns blazing into consumer lending during the Musharraf era, got burned very badly – to the tune of several banks being merged out of existence – and has only now started to find its way back towards lending to its own consumer clients, enabled by a slowly transforming underlying economic reality.

Simply put, the Musharraf era consumer lending boom was about 30 years too early, and the true bonanza in consumer lending in Pakistan has yet to come.

To understand why this all matters, and why we may be headed towards a radically different financial services sector (eventually), it is important to understand a bit of financial history: where the Pakistani banking sector started, the impact of nationalization, the 1990s first privatization wave and the long shadow of Citigroup, the Musharraf era bank liberalization, and the nearly two-decade-long trough since.

That then lays the context of what the banking sector has been able to achieve over the past few years, and the past five years in particular. From there, we will be able to understand what comes next and why consumer lending is an important nut for the banking sector to crack.

Nawaz, Musharraf, and the two

privatization waves

Pakistan’s banking sector for the first three decades of its existence was highly simple, and largely geared towards deposit gathering. A handful of local banks, along with a surprising-

ly larger number of branches of foreign banks, constituted the entirety of the banking sector, taking in retail deposits and lending mainly to the finance international trade.

Then came the absolute train wreck that was nationalization, which brought nearly the entirety of the banking sector (minus the foreign banks) under direct government control. Banks took in deposits and gave out corrupt loans to politicians that were never paid back, causing the government to bail out banks every single year the way it bails out the railways or other moribund state-owned companies today.

The nationalization era was the predictable disaster that one would expect it to be. By 1988, the five nationalized banks collectively cost the government of Pakistan 8.8% of the country’s GDP in what had by then become the annual tradition of bank bailouts.

The annual bank bailouts were a central policy challenge in the late 1980s, which is what prompted the first of two waves of bank privatization. When the center-right Pakistan Muslim League Nawaz, led by Prime Minister Nawaz Sharif, first came to power in 1990, bank privatization was high on their agenda. Within weeks they had privatized Muslim Commercial Bank (now MCB Bank), selling it off to a consortium led by industrialist Mian Muhammad Mansha. Allied Bank was also put on the auction block but was bought by its management and employees.

The second wave of privatization came under the Musharraf era, when four of the big five banks were privatized, and banking regulations significantly liberalized to allow for far more private sector banks to operate in the country.

This fundamentally transformed the banking sector in Pakistan. Far from being a basket case that needed bailouts every single year, it became a major employer and taxpayer. Political loans had been the bane of the economy in the 1970s and 1980s and were featured prominently in the 1996 video of the Junoon song Ehtesaab. They practically vanished, almost overnight, as a problem.

The consumer experience of banking improved significantly. Debit cards and automated teller machines (ATMs) became prominent in the late 1990s, with the entire country’s ATM network being unified in 2004. As the economy grew, deposits started flowing in, which led to the obvious question of: who do the bank lend to now that they were no longer under pressure to lend to politicians and their friends?

The long shadow of Citibank

It may be hard to remember these days, but for about 70 years following the end of World War II in 1945, the world had a simple formula for economic and political success: emulate America. In Pakistani banking, this had the effect of the relatively small presence Citibank having a disproportionately large impact on the shape of the country’s financial services sector.

In the early 1990s, as Pakistan was liberalizing its banking sector, American companies were gearing

up for another wave of globalization and committing more resources to their operations outside their home countries and the developed economies of Western Europe and Japan. For Citibank, this meant beefing up its presence in Karachi, and the man who led that effort was Shaukat Tarin.

Tarin and the team he built in the early 1990s are legendary: they invented Pakistani consumer finance as we know it, introducing the country’s first credit cards and personal unsecured loans, and significantly altering the nature of the mortgage market. They never had a major market share, but the products they introduced – and the manner in which they operate inside banks – are what is available to Pakistani consumers today.

Why go after consumer finance? Because Citibank is an American bank, and it brought over American assumptions about how finance is supposed to operate. In the United States, retail banks take in retail deposits and lend out money in large part to retail borrowers. According to the Federal Reserve Bank of St Louis, about 39% of bank lending in the United States is either consumer mortgages or other consumer lending (auto loans, credit cards, etc.). And much of the remainder is to smaller businesses that are retail-adjacent lending.

It works this way in the United States

because the US has unmatched depth and diversity in its financial services sector. In America, the major investment banks serve the needs of its largest corporations, alongside large corporate banks, some of which do not even have any retail presence at all. It has a whole slew of lending companies and banks to serve mid-sized companies, and then what we would recognize as a retail banking sector that serves individual consumers and small businesses.

This kind of financial depth exists literally nowhere else on the planet, but American bankers nonetheless have a habit of trying to apply that mold no matter where they go. This is why the Citibank global management tried to advance consumer finance all over the globe, including at its limited branch network in Pakistan.

That push for consumer lending was taken forward by several other banks in the country in the late 1990s and particularly after the ex-Citibanker Shaukat Aziz became finance minister under President Pervez Musharraf in 1999.

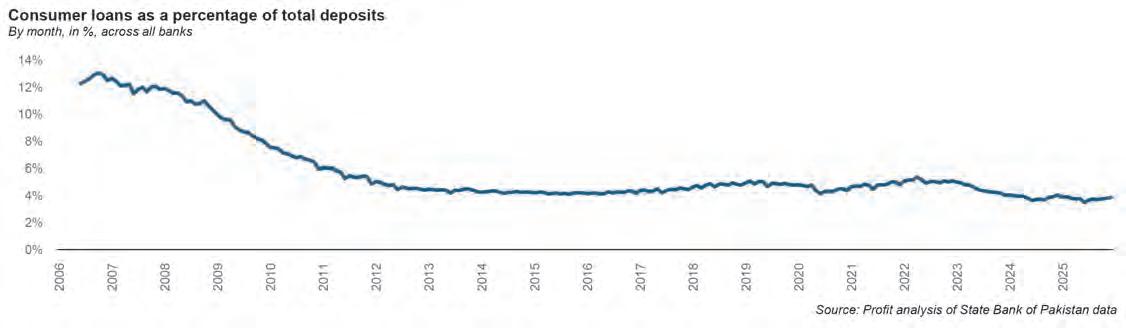

Relative to the total size of the economy – and even in just US dollar terms – the latter half of the Musharraf era (about 2004 through 2008) represented the peak of consumer finance in Pakistan. In December 2007, the total amount of consumer loans outstand -

ing at Pakistani banks was $6.9 billion, still the highest amount ever recorded if measured in US dollars, according to Profit’s analysis of data from the State Bank of Pakistan.

For most of 2006 and 2007, one out of every eight rupees deposited into a Pakistani bank was being lent to consumers, with personal loans and auto loans forming the bulk of the lending.

Then came the global economic crash of 2008, and non-performing loans as a percentage of the total consumer lending book skyrocketed, peaking in September 2012 at 22.6% of all consumer lending in the country. In other words, banks were lending a lot to consumers, but did not have a good sense of who they should be lending to, or how much.

The long retrenchment, and the slow recovery

From a peak of Rs425 billion in December 2007, the banking sector began pulling back on consumer lending for the next five years, shrinking the consumer loan book to as little as Rs282 billion ($3 billion) in April 2012. It was effectively impossible to get even a car loan during this time, let alone a mortgage.

Banks often simply shut down their entire consumer lending teams.

From that low point in 2012 began a long, and very slow recovery. Consumer lending grew, but tended to stay comfortably below the 5% mark that the State Bank’s new regulations deemed as prudent. In other words, having shrunk their consumer lending from about 13% of deposits in 2006 down to about 4.5% in 2012, banks basically kept the number there, and only grew consumer lending as the overall balance sheet and deposit base grew.

Between 2012 and 2020, consumer lending in Pakistan doubled in rupee terms, but barely grew in US dollar terms, and stayed completely flat as a percentage of total deposits.

The recent rise in lending

Then came a small, but noticeable surge starting around 2020, and coinciding with the Imran Khan Administration’s policies to make both mortgages and auto loans easier to obtain. On the mortgage front, there were the government subsidies for consumers to enable home ownership among the middle class. And on the auto loan front, the government allowed

banks to issue loans with tenures as long as 7 years, reducing monthly payments and making it more affordable for more people to buy cars using auto loans.

These changes were mild tweaks and only marginally increased the share of consumer lending on the banks’ books from about 4% of total deposits in 2020 to about 5% in 2022. But that small increase in share – coupled with general inflation and high growth in deposits – meant that the rupee-denominated consumer loan book doubled in size.

It has since plateaued as the government tightened regulations on auto lending and scaled back the subsidies on mortgage financing. But consider the following: the State Bank of Pakistan’s discount rate was as low as 7% for most of 2021 – when this surge of lending was happening – and went up to 22% by June 2023. One would think that this would cause the many people to start defaulting on their loans, especially since the banks had grown their loan books rather rapidly.

But the non-performing loan ratio for consumer loans in Pakistan has stayed at or below 5% for the entire time. A surge in lending, combined with a very rapid increase in interest rates would have been the perfect storm for a sharp rise in loan losses for the banks. So why did this not happen?

A larger, more stable middle class

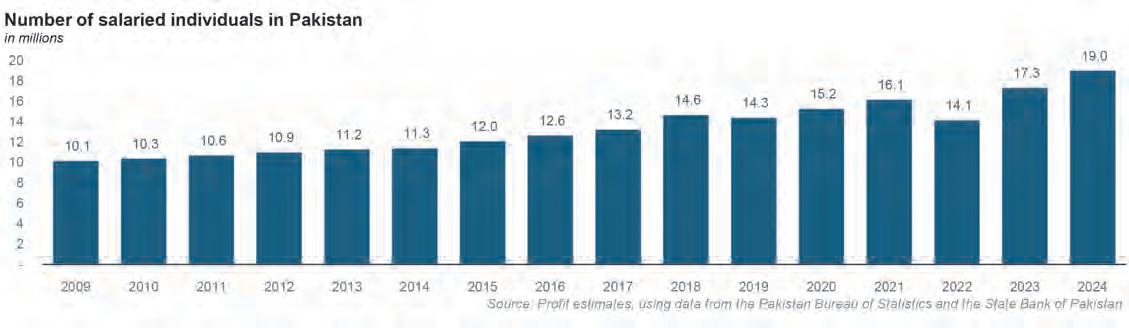

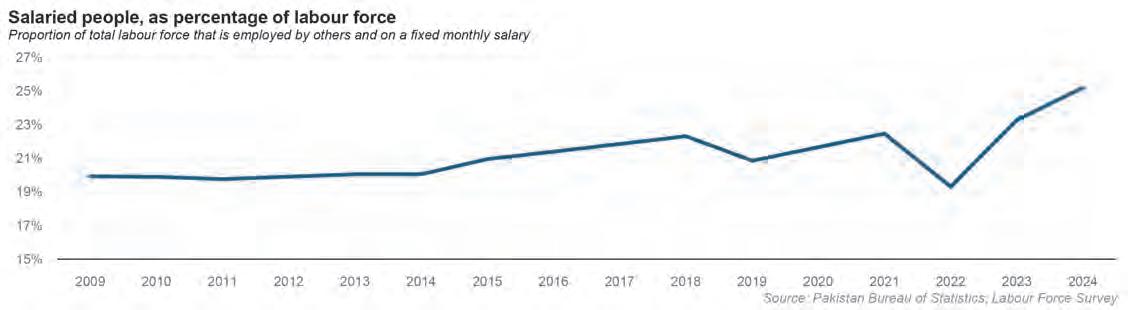

The answer appears to be two-fold. The first has to do with the fact that Pakistan’s labour force has considerably more stability with respect to their incomes, particularly as it relates to a fixed monthly salary.

According to the 2021 Labour Force Survey, the most recent one conducted by the Pakistan Bureau of Statistics, about 22.5% of Pakistan’s labour force consists of employed individuals who receive a regular monthly salary. While the PBS has not historically tracked this number for previous years, Profit’s analysis of the data – as well as other data sources –suggests that this number is rising, and with it changing the composition of what being employed in Pakistan means.

In the 15 years between 2009 and 2024, again using a combination of PBS data and Profit’s projections, we estimate that the Pakistani economy has created 19.8 million net new jobs. Of those, 8.9 million jobs – or about 45% of the total created – were fixed monthly salary jobs. In absolute terms, the number of people with fixed monthly salary jobs almost doubled between 2009 and 2024.

This has enormous implications for the nature of the Pakistani economy, and specif-

ically, the banking sector. Not only will this result in a significant increase in deposits over time, it also means that there are far more people who can take out a loan that requires a fixed monthly payment because they know how much their income will be every month.

There are a total of 31.2 million bank accounts owned by salaried individuals in Pakistan as of December 31, 2024, according to data from the State Bank of Pakistan, a number that has more than doubled over the past five years. That rapid growth is likely due to the fact that a large number of Pakistani companies require employees to open bank accounts at the bank in which the company maintains its corporate bank account in order to receive a salary, which means that people often have to create a new bank account every time they switch jobs.

The average balance in these salaried accounts is Rs144,000 and since the bulk of these are likely current accounts, the cost of deposits for banks is likely to remain relatively low. The average deposit amount has actually risen over the past five years from around Rs102,000 in 2019, which suggests that the rise in number of accounts may not just be a case of individuals having to open more and more accounts as they switch jobs.

And then there is the fact that Pakistan’s upper middle class appears to be expanding faster than ever before.

Let us start by defining the upper middle

class: people who make more than $1,000 a month, or about $12,000 a year. There are now almost 1.5 million people in the country who make more than that – as individuals. They represent a little over 1.3% of the total labour force, which is the highest it has ever been. If you use a slightly lower definition of upper middle class, and make it people who make more than $10,000 a year, the number of individuals in Pakistan who fit that category comes out to about 2.2 million people, or about 2% of the labour force. This number is also the highest ever recorded.

Now, let us go one level higher, and take a look at the number of Pakistanis who make more than $20,000 a year. These are people who might reasonably be called part of the global consumer middle class. In purchasing power terms, these people make the equivalent of someone making $71,000 a year in the United States.

The total number of people who fit this description is about 407,000 people, or about 0.37% of the labour force. Both the absolute number and proportion of labour force of people who are part of this category is the highest it has ever been.

Less than half a million people being part of the global consumer class is hardly something to get excited about, but the absolute number is starting to get close to being interesting.

And from a banks’ perspective, the fact

that the vast majority of these people have become part of the upper middle class only recently means that they are likely in the market for both consumer goods that signal that recent elevation in economic status, as well as the financial leverage needed to acquired those consumer goods. That is good for the banks’ ability to find good borrowers to lend profitably to.

More to come?

This consumer lending boom, in short, was smaller than the one that took place under the Musharraf era, but also a more stable one, in part because the banks appear to have learned their lessons and the regulator only marginally loosened some of its tightest post-2008 rules, and in part because the underlying macroeconomic conditions of the country are significantly better than they used to be.

What will be interesting is how the industry evolves as this middle class continues to grow and both the deposit base as well as demand for consumer loans rises. The banks have been able to profitably push their loan books right up until the brink of the SBP’s lending limits.

What would happen if the SBP incrementally started increasing those limits? Can the banks continue to find good borrowers and not risk an increase in bad loans? That remains to be seen, but the early signs are encouraging. n

Why Pakistan Never Built its Petrochemical Backbone Asif Saad

It was demand fragility, energy uncertainty, and a refusal to think in decades- not a lack of expertise

or ambition

Every few years, Pakistan rediscovers petrochemicals. A potential new investor ponders a fresh investment opportunity. A new policy paper is published. A delegation visits the Gulf or East Asia. Somebody points to China and India and wonders why not us?

As someone who has personally worked in this industry and seen its stagnation over the years, I find this question puzzling. In this article, I aim to put together a complete picture of our predicaments in this sector, based on my own experience and learning.

Pakistan has a large population, proximity to energy producers, and decades of industrial ambition. Yet it remains stuck importing the very molecules that underpin modern manufacturing – xylenes, polymers, intermediates, while countries with similar starting points moved decisively upstream.

The usual explanations are familiar: lack of capital, policy inconsistency, IMF constraints, energy shortages. All true, but

The writer is a strategy consultant who has previously worked at various C-level positions for national and multinational corporations

incomplete.

The real reason Pakistan never built a petrochemical spine is simpler and more uncomfortable. It never made demand inevitable. Demand in this case is not volume. It is a certainty.

When people talk about demand, they usually mean consumption volumes. How many tonnes of polyester, how much plastic packaging, how many downstream units. By that measure, Pakistan does have demand. Its textile sector is large, its cities are growing, and its population is sizable.

But petrochemicals are not built on volume. They are built on certainty.

A petrochemical complex does not ask whether demand exists today. It asks whether demand can disappear tomorrow. And in Pakistan, the answer has unfortunately always been yes.

Demand for petrochemicals in Pakistan is cyclical, income-sensitive, export-dependent, and vulnerable to shocks. When foreign exchange tightens, imports stop. When energy prices jump, factories shut. When global demand slows, textile orders vanish. Each shock breaks the chain. Contrast this with countries that built large upstream capacity. Their demand was not necessarily richer, but it was inescapable. Food had to be packaged. Housing had to be built. Everyday goods had to move through formal supply chains. Consumption became part of daily life, not just export statistics.

Pakistan never crossed that threshold.

The missing anchor: consumption beyond textiles

Pakistan’s industrial demand is narrow. Textiles dominate, but textiles alone cannot anchor a petrochemical chain. Textiles are export-led, price-sensitive, and globally substitutable. When margins compress, buyers move. When recessions hit, orders fall. That makes textile demand a weak foundation for long-gestation, capital-intensive upstream investments.

Countries that succeeded widened the base. Petrochemicals flowed into food packaging, FMCG, construction materials, pipes, insulation, household goods, automotive components and through all of these into the mundane infrastructure of daily life.

In Pakistan, much of this consumption remains informal. Food is unpackaged. Housing is unstandardised. Retail is fragmented. Plastics exist, but not at the density required to justify scale.

Energy: the non-negotiable precondition

Petrochemicals can tolerate low margins, but they cannot tolerate uncertainty. A petrochemical plant needs to run continuously. Every shutdown destroys economics. Pakistan’s energy system has never offered that assurance. Infrastructure monopolies, gas shortages, power interruptions, tariff shocks, retrospective levies, each episode teaches investors the same lesson: your plant may exist, but it may not run.

No amount of fiscal incentive compensates for that risk. This is why energy and related logistics must be locked before capacity is built. Long-term contracts, stable and globally competitive tariffs, and protected captive power are not luxuries; they are entry requirements.

Pakistan treated energy as a crisis to manage, not infrastructure to guarantee. The petrochemical sector paid the price.

Foreign exchange: the invisible tripwire

Petrochemicals are import-heavy in their early years. Feedstocks, catalysts, spare parts, even expertise arrive in dollars before domestic substitution or exports mature.

Pakistan’s repeated balance-of-payments crises created a fatal loop. FX shortages led to LC restrictions, which halted feedstock imports, which shut plants, which weakened downstream industry, which worsened exports, which deepened the FX crisis. This

cycle does more than hurt margins. It destroys confidence. Until FX exposure is structurally ring-fenced through dollar-linked pricing, offshore retention, and automatic import approvals, large-scale upstream investment will always look reckless.

Policy was present. Continuity was not.

Pakistan did not lack petrochemical policies. It lacked time. In every serious petrochemical story elsewhere, the state made one crucial commitment: it refused to change its mind midstream. Losses were expected. Overcapacity was tolerated. Political cycles were subordinated to industrial ones. Pakistan, by contrast, renegotiated the rules constantly. Tariffs shifted. Protections were granted and withdrawn. Energy pricing was revisited. Each adjustment was rational in isolation and devastating in aggregate.

Petrochemicals punish cleverness. They reward boredom.

Another uncomfortable truth is about capital itself. Pakistan’s private capital is entrepreneurial, agile, and opportunistic. It thrives in trading, services, real estate, and short-cycle manufacturing. It does not naturally gravitate toward projects that demand ten years of patience before meaningful returns appear.

In countries that built petrochemical backbones, one or two anchor investors were willing, and able, to absorb early losses, betting that scale and time would eventually discipline costs and unlock demand.

Pakistan never enabled such a bet. Fragmented capital, overcautious banks, and policy reversals ensured that no single player could

credibly carry the burden of incubation.

This is ultimately a sequencing failure. Pakistan tried to build upstream capacity while energy was unstable, FX was scarce, demand was narrow, and policy was negotiable. It asked petrochemicals to succeed where every structural condition was hostile.

The correct sequence is unglamorous but clear: First, lock energy, then, insulate FX exposure, then enable one or two anchor investors. Then, widen downstream consumption. Only then does upstream scale make sense.

At its core, this is not a technical failure. It is a philosophical one. Petrochemical chains are built by societies willing to lose money before they make it, to tolerate criticism before results appear, and to think in decades rather than budgets.

Pakistan has not lacked intelligence or capability. It has lacked patience.If every investment must justify itself within an electoral / power cycle, every policy must survive an IMF review, and every project must promise early profitability, upstream petrochemicals will remain permanently uneconomic. They are not uneconomic. They are impatiently judged.

If Pakistan ever wants to revisit this path seriously, it must first decide something fundamental. Is it willing to lock energy, capital, FX and policy long enough for demand to become inevitable? In other words, is it willing to bet on Pakistan itself? If the answer is no, importing polymers and intermediates will always appear cheaper and often will be.

But if the answer is yes, the conversation changes entirely. Not overnight, not painlessly, but structurally. Petrochemicals do not reward hope. They reward commitment. n COMMENT

Pakistan’s IT exports are rising. Why is this, and how can it continue to grow?

Government incentives, including changes to Exporters’ Specialised Foreign Currency Accounts, along with expanding global reach and increased IT literacy, have fueled the surge in IT exports

By Usama Liaqat

Recently, it was reported that December 2025 recorded the highest-ever monthly value of IT exports for Pakistan. In a report by Topline Research, it

was stated that this figure amounted to $437 million, which was a 22.7% increase over the amount in November 2025. Compared to December 2024, the value represented a 25% increase. At the same time, according to the report, IT exports during the first half of FY26 totalled Usd 2.2 billion, a 20 percent

increase over the corresponding period in the previous year.

There is an obvious trend, then. Pakistan’s IT exports are growing.

Headed mostly towards the Gulf region, these exports ordinarily involve the export of computer software, BPO services such as

call centre services, IT consultancy services for both software and hardware, information services, and maintenance and repair services for computers.

The reasons behind this surge, however, are some government incentives, particularly the reduction in the allowable permissible retention limit in Exporters’ Specialised Foreign Currency Accounts, as well as allowing exporters to use part of that money to make foreign investments. At the same time, the expanding global footprint of major IT exporters has also contributed to this increase, and so has the rise in IT literacy and the increased accessibility of the internet and internet-compatible devices to the population.

But the government is looking for steep upsides. According to the reports, under the “Uraan Pakistan” plan, the target for IT exports by 2028-29 has been set to Usd 10 billion. Given that estimates for exports this year range from Usd 4 to 5 billion, it is hard to envision such a rapid growth in a mere 3 years. Regardless of whether the aim is achieved or not, perhaps what is more important is the government-led and -encouraged development on local IT infrastructure. Part of this is happening, but perhaps more is needed – not only different in quantity, but also in kind – to really give the industry a push.

The Reasons for Increasing IT Exports

According to the report, one of the main reasons why IT exports are rising is that the State Bank of Pakistan had relaxed the maximum retention limit in Exporters’ Specialised Foreign Currency Accounts (ESFCAs) from 35% to 50%. The measure was instituted through a notification by the Exchange Policy Department of the State Bank, dated 23 October 2023. Its stated aim was, in fact, to “encourage the exporters of Software, Information Technology (IT) and IT-enabled Services (ITeS) and freelance services” in order to “boost their export earnings and bring additional foreign exchange into the country”.

Now, these accounts are essentially accounts in which IT exporters (including freelancers) can deposit a portion of their export proceeds to not only hedge against currency fluctuations, but also to cover business expenses. These expenses could include, for example, imports, acquisition of services from abroad, profit/dividend repatriation against registered shares, etc. And these expenses could then be made without the need for the State Bank’s approval.

One type of such expenses is the use of EFSCA funds in order to engage in capital and equity transactions, such as equity

investment abroad and foreign currency loan repayments, although appropriate procedure must be followed if these are being repatriated. The ability to prosecute this provision is also supported by the State Bank’s updated guidelines, which it published in 2024. These rules streamlined the process of acquiring stakes in foreign entities and granted permission to IT sector companies to expand their footprint abroad and create subsidiary or branch offices abroad.

These measures, obviously, are intended to encourage IT companies to access global markets and to enable them to use their earnings from those transactions to further their international presence. The end result can be envisioned, where increased international penetration leads to greater exports – a model that could be sustainable – and ultimately helps reduce the country’s trade deficit.

Then, there are major IT companies like Systems Limited, which have been expanding their footprint abroad. Systems, which is a Rs231 billion company, and brought in annual revenues of Pkr 38.5 billion in 2024, made 87% of its total earnings as part of exports.

In fact, according to their annual report 2025, the major market was the Middle East, Africa & Others region, which accounted for 59% of the total revenue. 21 percent came from North America, 13% from Pakistan, and 4% and 3% came from Europe and the Asia Pacific, respectively.

Moreover, the company is aiming to increase the share of export-led revenue. It is already planning to establish its own subsidiary in the United Kingdom. At the same time, it is growing its footprint in the Middle East, focusing on the acquisition of enterprise clients and offering specialised supply centre capabilities. Systems Limited has also ventured in the Business Process Outsourcing (BPO) space, whereby it offers cost-effective shared services in accounting, HR, and legal functions.

The success of companies like these – such as Contour Software, ibex, Strategic Systems, etc. – is surely a major driver of the increase in Pakistan’s exports. They have –and are building more – capacity to take up any facilitations the government has to offer.

And then there are the freelancers. Encouraged by the access to cheaper internet services (though sometimes with aberrant availability), cheaper compatible devices, and a more accessible IT education, IT-whizzes have been building up their profiles on freelancing platforms, and looping in foreign clients for a host of different IT services. In FY 2024, freelancers brought in a total of $400 million. Their contribution by the end of the current financial year is expected to cross $0.8 to $1 billion. Not bad.

Will IT be the “IT” sector?

Currently, the IT sector’s contribution to the export of total services from Pakistan represents around 45% of the total Rs2.3 trillion. The IT sector is the main driver in this case, and it is no wonder that the government is keen to present it as one of the key drivers of the push towards economic ability. In fact, it has been reported that the government is targeting to achieve $10 billion in IT exports by 2028-29, under the ‘Uraan Pakistan’ national economic plan. That, in such a short time, is ambitious, to put it mildly. This is especially the case if we consider that currently the country is welcoming reaching the IT export value of $2.2 billion in the first six months of the current fiscal year. The signs are encouraging, no doubt, and there is, of course, an upward trend. But the fact is, there are some constraints on the growth that can be relieved by the government’s investment in more long-term capability building.

Let’s take Systems Limited as an example, and its geographical spread of exports. The European market is a mere 4 percent, while APAC stands at 3 percent. These are also massive and lucrative markets, which have been little explored. In order to better enter these markets, a government-led, and private-driven partnership that is dedicated to the upskilling on the local talent, especially in terms of automation, smart systems, and AI-related infrastructure, is needed, which is likely to help Pakistan access a greater share in these markets, as well as increase its share in the Middle East and North American economies. At the same time, government-led partnerships – especially with advanced IT economies – aiming not only to develop and encourage the local tech ecosystem, but also to facilitate their export-readiness seems also a step that would help usher Pakistan’s IT exports to the next level.

Currently, the IT exports sector is dominated by Systems Limited, but not every IT company is as big. And the economies of scale accessible to Systems Limited might not be what’s available to most of the sector. There is, therefore, a great need for government encouragement of smaller companies, and it can do so by, for example giving incentives for infrastructure build-up, facilitating partnerships with bigger companies in the region, and equipping companies for higher-value exports. For instance, in terms of computing and processing hardware manufacturing, Pakistan too lacks behind. Though capitalising on such initiatives would likely take years, it might also be a pertinent way of bringing Pakistan’s exports to the next level. Initially, for example, such initiatives could be developed with international technology partners – from China, for instance – and these enterprises could gradually lead to local adoption and assembly. n

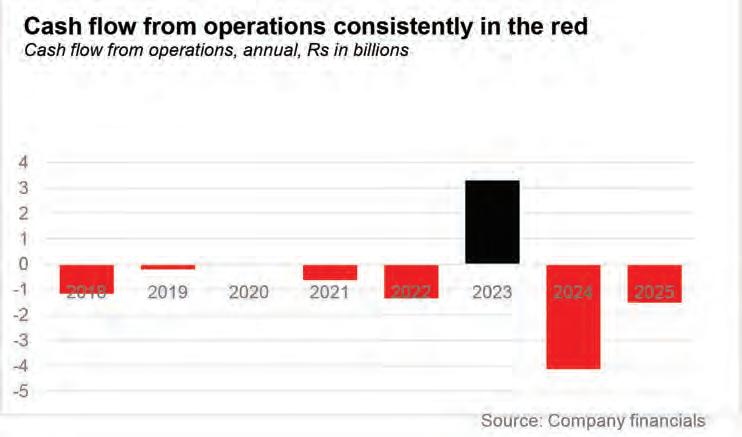

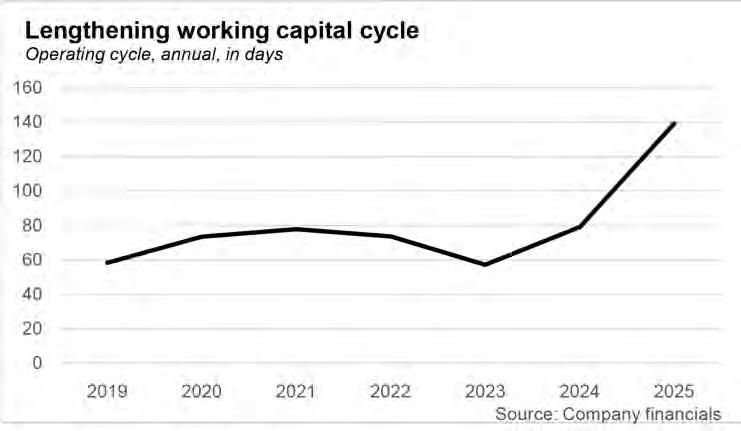

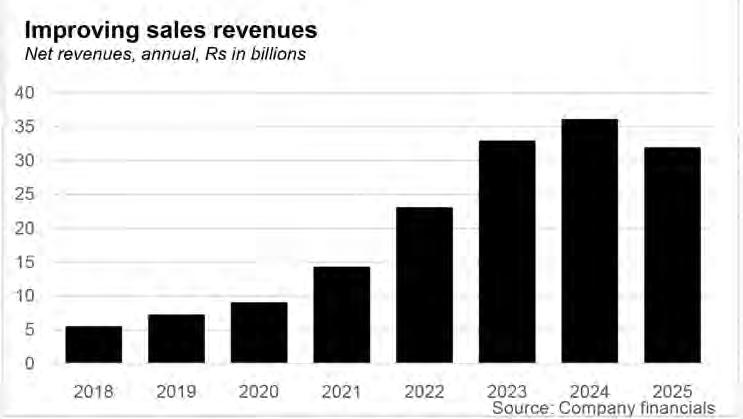

Pakistan’s soda ash industry gets anti-dumping protections

Margins are expected to expand for industry hit by cheaper Turkish and Kenyan competition after government rules foreign competitors were found to be in violation of regulations.

Pakistan’s domestic soda ash producers have won a significant, if time-limited, reprieve from import pressure after the National Tariff Commission (NTC) imposed provisional anti-dumping duties on disodium carbonate (soda ash) imports originating in and/or exported from Türkiye and Kenya. The move follows a preliminary finding that these imports were being dumped into Pakistan and had caused material injury to local industry.

Under the preliminary determination, the NTC has applied provisional duties for four months at differentiated rates: 5.58% on most Turkish exporters, 3.49% on selected Turkish producers, and 12.54% on exporters from Kenya, according to the equity research note and local reporting.

For investors, the immediate focus is what “frictions” mean for the two listed companies that dominate the market: Lucky Core Industries Limited (LCI) and Olympia Chemical Limited. The sector note argues that duties should provide structural support to the domestic soda ash industry, especially after several years in which import competition appears to have forced local players to defend volumes and accept weaker pricing. In the

broker’s framing, that pressure has been visible in falling gross margins within soda ash businesses – with LCI’s soda ash gross margin cited at 23% in FY25, down from 31% in FY22, while Olympia’s comparable margins also trended downwards in recent years.

The mechanics are straightforward: soda ash is a commodity input, so if dumped material is undercutting local selling pricestend to either match those prices (hurting margins) or lose share (hurting utilisation). The NTC’s preliminary findings point to precisely those channels – higher import volumes, price undercutting and price depression, loss of market share, lower capacity utilisation and profitability pressure – as key indicators of injury.

However, the margin uplift is not “automatic”. Even this provisional relief contains important **carve-o waived for imports used as inputs for export-oriented products, and for imports used in foreign grant-in-aid projects or those covered under applicable schemes. Those exemptions, while policy-consistent, matter because they can preserve an import channel for some of the largest industrial consumers – limiting how much pricing power local producers can regain.

This case has been building for months –and, in some respects, for years.

The NTC investigation was initiated on 18 July 2025, after LCI andlication alleging dumping of soda ash from Türkiye and Kenya. The investigated product falls under PCT Code 2836.2000, and is a critical input for downstream industries including glass, detergents, chemicals, paper, metallurgy and purification plants.

The sector note usefully sets out the evidentiary windows the regulator examined: the injury analysis covered FY22–FY25, while dumping was assessed over FY24–FY25. In those periods, the NTC’s preliminary view was that the domestic industry was being harmed in the ways trade-remedy frameworks typically look for: imports undercut, and local firms facing depressed prices and weaker profitability.

Import patterns cited in the research note underscore why the producers pushed for relief. Carbonates imports to Pakistan rose sharply in FY24 and continued elevated levels in FY25. In FY24, the total listed value reached $6.25 million (including $5.50 million from Turkey), while FY25 still shows $5.30 million, with Kenya’s share rising to $3.18 million.

The timeline also reflects how difficult it can be to secure definitive relief through Pakistan’s trade-remedy process. The note points out that a previous anti-dumping investigation

initiated in 2021 against Turkish soda ash imports – also on a petition by LCI and Olympia – was terminated in 2022 without duties.

That history is relevant because it frames the current duties as a renewed attempt to correct a perceived imbalance in a market that is effectively a domestic duopoly. The same research note estimates the soda ash market is led by LC (~30%) and around ~10% imports. PACRA has also described the local market as a “duopoly”, reinforcing the idea that when imports become disruptive, there are only two domestic balance sheets that can absorb the shock.

LCI is the larger and more diversified of the two players – and soda ash is both a legacy business and a meaningful earnings driver.

The company’s origins go back to Pakistan’s earliest industrial period: it traces its heritage to the Khewra Soda Company, built around the raw material advantages of the Khewra salt range. Over decades, the business evolved under the ICI Pakistan banner, before eventually becoming part of the Lucky/ Yunus-associated corporate ecosystem ucky Core Industries**. The company’s own published legacy timeline documents multiple expansions in soda ash capacity, alongside major investments in other chemical value chains.

Today, LCI operates as a broad chemicals and materials group, and the soda ash line sits alongside other segments. In the sector note, LCI’s soda ash capacity is cited at 560,000 tonnes per annum, and soda ash is described as contributing roughly 30% of the company’s value.

That “value share” explains why import competition has become a market story rather than a technical trade dispute. The same research note states that during FY25, LCI’s soda ash business fell 15% YoY, while the segment’s gross margin dropped to 23%, down from 31% in FY22 – a compression the analyst explicitly links to dumping pressure during the injury period.

Strategically, LCI is also the kind of company that feels second-order effects. If soda ash margins improve, management can either bank the uplift or reinvest in downstream capabilities – including refined grades and bicarbonate products demanded by consumer and industrial supply chains. Equally, if the relief proves temporary or porous, it may reinforce a more cauton posture in commodity-linked lines.

Olympia is the smaller competitor, but still a scaled industrial operator in its own right – and more concentrated on soda ash and sodium bicarbonate than LCI.

PACRA’s profile of the company states Olympia Chemicals was incorporated in Pakistan on 1 January 1995 and is headquartered on Davis Road, Lahore, with manufacturing facilities at **Warcha (Districter unit near

Multan Road (Tehsil Pattoki, District Kasur). It describes Olympia as a prominent manufacturer of light and dense soda ash and refined sodium bicarbonate, serving a broad range of industries.

The equity research note pegs Olympia’s soda ash capacity at 306,000 tonnes per annum, and assigns it roughly 30% of the national soda ash market.

For Olympia, anti-dumping relief can be even more material because its earnings are less “diversified away” into other chemical verticals. Yet the same caveats apply: exemptions for export-oriented users and grant-funded projects may preserve an import window for key buyers, and the provisional duty is not the final word.

Still, Olympia’s positioning has some inherent advantages. Its Warcha location, close to salt and other input sources, mirrors the original logic of Pakistan’s soda ash industrial geography – and PACRA notes a history of phased expansions over time. In a commodity business, the low-cost producer with stable utilisation tends to be the one that best translates trade protection into profits.

The soda ash decision fits into a broader pattern: Pakistan’s use of trade remedies has become more visible as local manufacturers struggle with cyclical demand, exchange-rate volatility and the persistent temptation for overseas producers to clear excess inventory in price-sensitive markets.

Th docket of anti-dumping investigations shows how wide the net has become –spanning chemicals, steel, paper and packaging, tiles, and even consumer items. Recent and ongoing cases listed by the regulator include investigations involving PVC (suspension grade), sulphonic acid, hydrogen peroxide, and phthalic anhydride in chemicals; and cold rolled coils/sheets, galvanised coils/sheets, and other steel products in metals.

In that context, soda ash is not an outlier; it is part of a wider industrial push for “rules-based protection” rather than ad hoc bans. These processes are typically framed around WTO-consistent tools: a domestic industry submits a complaint, the regulator tests the evidence, and provisional measures are applied only after a preliminary finding of dumping and injury.

Policy changes around exemptions have also shaped how these measures play out in practice. In 2025, Pakistan enacted amendments giving retrospective effect to exemptions from anti-dumping duties for products imported under foreign grant-in-aid projects, a policy choice that shows up again in the soda ash case via waivers for such imports.

For downstream industries, this “selective shielding” matters. It can protect the domestic producer’s core market while avoid-

ing unintended cost shocks for export sectors and development projects – but it also means the relief for local manufacturers can be less sweeping than headline duty rates suggest.

For all the excitement around margin expansion, the key phrase is “provisional”.

The NTC’s current action is explicitly framed as a preliminary determination with provisional duties imposed for a period of four months, effective from publication of the notice.

That means LCI and Olympia are not yet operating under a settled, multi-year protective regime. Over the next several months, several variables can alter the real-world impact

Final duty rates may differ. Provisional measures can be adjusted up or down after deeper verification and hearings.

Exemptions may dilute the benefit. The sector note highlights exemptions for export-oriented inputs and grant-in-aid projects; the broader legal framework also embeds provisional measures within a process aimed at balancing domestic injury claims with wider economic needs.

Importers may front-load shipments or alter sourcing. Where a market has multiple exporter options, duty differentials can redirect trade flows, changing which countries and firms dominate the import channel.

Diplomatic and legal pushback can emerge. Trade remedies often attract formal objections from exporting countries and their producers, adding political noise to what is meant to be a technical, evidence-based process.

For Pakistan’s soda ash duopoly, the more subtle risk is that a short window of protection encourages a short window of behaviour. Producers may raise prices to rebuild margins; buyers may respond by seeking exemptions, lobbying, stockpiling, or – if the duty window closes – reverting to imports. That dynamic can make the “relief” feel like a temporary patch rather than a durable investment signal.

Yet even temporary relief can matter. If the duties succeed in reducing undercutting for a quarter, it can stabilise utilisation and cash flows, giving both listed producers room to plan and invest – and, crucially, to negotiate with large buyers from a stronger position.

The soda ash episode, then, is best read as a marker of where Pakistan’s industrial policy is currently heading: more reliance on formal trade-remedy channels, more attention to the fine print of exemptions, and a continuing tugof-war between protecting domestic producers and keeping input costs manageable for downstream industry. Whether LCI and Olympiaths of breathing room into a longer-term advantage will depend less on the headline duty rates –and more on what the NTC decides when the provisional window closes. n

In 2026, Sazgar aims to expand its SUV market share

A new full sized premium SUV model takes the company further upmarket at a time when Pakistani consumer tastes are getting more discerning

Sazgar Engineering Works Ltd (PSX: SAZEW) has begun 2026 with a clear signal that it wants to move deeper into Pakistan’s fast-growing SUV market – and do so from the premium end. The Lahore-based assembler has announced it will open bookings for locally assembled (CKD) versions of the Tank 500 Hi4 T 4×4 2.0L Turbo AT from Monday, 26 January 2026, offering the model in both plug in hybrid (PHEV) and hybrid (HEV) variants.

That matters because the Tank 500 is not simply another mid-size urban crossover aimed at first-time SUV buyers. It is being positioned as a premium full-size SUV – the sort of vehicle Pakistani consumers typically associate with status, road presence and long-distance comfort – but with a modern electrified drivetrain and a pricing strategy designed to undercut the “imported luxury” end of the segment. In its recent research note, Arif Habib Limited (AHL) describes the Tank 500 as combining luxury, advanced hybrid technology and off-road capability, with a 2.0L turbo petrol hybrid powertrain, a 9 speed automatic transmission and 4WD.

AHL’s analysis also frames the Tank 500 as a direct challenational nameplates. The brokerage argues the model “sits comfortably” against Toyota’s Land Cruiser Prado and Fortuner, pitching it as a hybrid-enabled alternative to the Fortuner and a value-for-money proposition versus the Prado – an important distinction in a market where the badge still matters, but where buyers are increasingly comparing features, drivetrains and “what you get for the money”.

The Tank 500 launch is not intended to stand alone. The com investors that it plans to roll out two additional plug in hybrid products by the end of March 2026: Tank 500 and Cannon PHEVs. The disclosure, carried by Business Recorder from the company’s annual report, notes that after the successful launch of a CKD PHEV Haval H6 1.5L on 16 August 2025, Sazgar is planning CKD rollouts of Tank 500 and Cannon PHEVs by 31 March 2026 as part of a broader push into “new energy vehicles” (NEVs).

The other model – the Cannon Alpha – is a strategic bet on a different kind of Pakistani

demand: the dual use pick up category that serves both lifestyle buyers and working fleets. AHL expects Sazgar to roll out the Cannon Alpha 4×4 PHEV in the near term, noting that an earlier 4QFY26 launch (if it happens) could add upside to earnings.

From an investor’s perspective, the attraction of these launches is not only branding – it is the prin products and a broader line-up that can keep showrooms busy in different parts of the consumer cycle. AHL estimates initial Tank 500 deliveries of 200 units in 4QFY26, with an incremental Rs5.3 per share contribution to earnings, and suggests that scaling to 700 units in FY27 could lift the contribution to roughly Rs17.6 per share.

Sazgar is often described today as “tretail investors – but it is, in fact, a diversified industrial business that has evolved over three decades.

According to the Pakistan Stock Exchange’s company profile, Sazgar was incorporated in Pakistan on 21 September 1991 (later converted into a public limited company in 1994) and is engaged in the manufacture and

sale of automobiles, automotive parts and household electric appliances.

On the ground, that has historically meant three main lines:

Sazgar’s roots are in the three-wheeler market, and its corporate site continues to highlight the segment through products such as the “Deluxe Mini Cab Luxury” category and the company’s “eVe” electric three-wheeler branding.

Over the past few years, Sazgar’s four-wheeler business has become the growth engine – a transition reflected in official disclosures and market data. The company’s annual report disclosures cited by local business press describe Sazgar as manufacturing and marketing four-wheelers under HAVAL and JOLION, while also importing/marketing under TANK 500 and ORA, alongside three-wheelers under SAZGAR.

Sazgar also operates in tractor wheel rims, listed directly among its product categories on its corporate site. That segment, however, has faced a tougher demand environment: Business Recorder reported the company warning that the tractor wheel segment is “struggling” due to weaker tractor demand.

Just as notable is what Sazgar is stepping away from. In a sign of strategic focus – and arguably of the opportunity cost created by the rapid expansion of its automotive operations –the company has disclosed that its board decided to discontinue the home appliances business effective 1 September 2025, explicitly to focus resources on core and more profitable segments.

Financially, the scale of Sazgar’s transformation is visible in PSX-published figures. The PSX data for the year 2025 shows sales of Rs108.7bn, up from Rs57.6bn in 2024, while profit after taxation rose to Rs16.34bn from Rs7.94bn over the same period – alongside EPS growth that underscores just how significant the SUV-driven ramp-up has been.

Operationally, Sazgar remains very much a Lahore-centred manufacturer, with its registered office at Ali Town, Thokar Niaz Baig and factory facilities on Raiwind Road. And it has not abandoned exports: in late 2025, Nukta reported that the company planned to enter three new export markets – the Philippines, Mexico and Afghanistan – for its three-wheelers, even as domestic demand for four-wheelers accelerated.

In short: Sazgar is no longer merely a legacy three-wheeler maker that happened to find a hot SUV franchise. It is increasingly presenting itself as a multi-category automaker spanning internal-combustion, hybrid, plug in hybrid and electric models – with aftersales and parts economics that typically become more attractive as the vehicle parc grows.

Sazgar’s timing is not accidental. The broader Pakistani market has been tilting toward SUVs for years – first in the compact and

mid-size crossover range, and now increasingly into higher-priced, higher-feature segments.

AHL’s research note captures the scale of the shift in a single statistic: SUVs averaged 18% of total auto sales in CY25 (per PAMA), and when non-PAMA players are included, the share rises to nearly 28–30% – up from 9% in CY21.

PakWheels’ breakdown of 2025 market volumes offers a useful illustration of where consumer attention is concentrated. In its year-end overview, the portal reported that total SUVs and pick-ups sales were 32,914 units, with Haval (Sazgar) posting combined sales of 13,943 units – ahead of the combined Toyota Fortuner and Hilux series figure of 9,547 units in that tally. Even allowing for the inevitable caveats around category definitions and reporting, the direction is clear: the SUV is no longer a niche upgrade; it is becoming the default aspiration.

This is the context in which a premium full-size hybrid SUV like the Tank 500 arrives. It is designed to capture the buyer who has either “graduated” from the compact SUV category or wants the road presence of a Prado-style vehicle – but is prepared to consider alternatives if the value proposition is strong enough.

Pakistan’s high-end SUV market is unusual: it is both highly aspirational and structurally constrained.

At the very top end, prices for iconic imports can be staggering. For example, PakWheels lists the Toyota Land Cruiser at Rs9.5 crore (ex-factory/estimated listing format on the site), placing it far beyond the reach of all but the wealthiest buyers and corporate fleets.

One rung below that, the Toyota Prado remains a defining status symbol – and PakWheels lists the Toyota Prado 2026 between Rs55,000,000 and Rs60,000,000 (ex-factory price range on the site).

Those numbers matter because they frame the “space” Sazgar is trying to occupy: customers who want a big-body SUV experience but are not necessarily wedded to paying a Prado-level premium.

Meanwhile, the locally assembled/official-channel premium space is more populated – and more competitive – than it was a few years ago. The Toyota Fortuner, often treated as the benchmark for a rugged, high-resale, three-row SUV, is listed on PakWheels at Rs14.939m to Rs20.499m (ex-factory). The KIA Sorento –more urban-luxury oriented and available in hybrid form – is listed at Rs13.649m to Rs16.699m (ex-factory).

This is where Sazgar’s Tank 500 pricing looks deliberately provocative. AHL cites the Tank 500 at Rs20.5m (HEV) and Rs22.5m (PHEV) – essentially placing the hybrid full-size newcomer around the top end of Fortuner pricing, while remaining far below Prado territory.

The brokerage’s peer comparison also suggests Sazgar is not simply trying to match

incumbents feature-for-feature, but to reframe the comparison around size and electrified performance. In AHL’s table, the Tank 500 is listed at 5,078mm length versus 4,795mm for the Fortuner, with the Tank 500 variants showing substantially higher listed horsepower figures (Tank 500 PHEV 402 HP, Tank 500 HEV 342 HP, Fortuner 201 HP in the comparison).

If that positioning holds in real-world customer experience – and if aftersales support keeps pace – the Tank 500 could carve out a distinct niche: the buyer who wants a large, premium-feeling SUV with new-energy credentials, but who still wants a brand-backed, locally assembled ownership proposition rather than the uncertainty and cash outlay of a high-tax impnon Alpha pick-up, meanwhile, speaks to a parallel premiumisation trend: pick-ups are no longer only workhorses. AHL notes Pakistan’s pick-up market averages roughly 11,000 units annually and models a base case where Sazgar could deliver 1,000 units in 4QFY26, with larger volumes in FY27 already incorporated into forecasts.

In practice, this is a play for buyers who want Hilux-style utility, but are increasingly open to elecnd higher cabin specification. Investors have not missed the transformation – or the ambition.

As of 23 January 2026, the PSX quote page lists SAZEW at Rs1,953.64 per share, with a 52 week range of Rs947.00 to Rs2,094.18. The same PSX snapshot shows a 1 year change of 94.30%, underscoring how strongly the market has rerated the company as it shifted from legacy categories into high-growth SUVs and hybrids. The earnings trajectory helps explain why. PSX-published financials show that in 2025 Sazgar reported sales of Rs108.7bn and profit after taxation of Rs16.34bn, compared to Rs57.6bn salesrofit after tax in 2024.

In other words: the company’s SUV-era scale-up has not been incremental; it has been step-change.

Sell-side analysts are leaning into that narrative. In its January 2026 note, AHL reiterates a BUY stance with a Dec’26 target price of Rs2,566, implying upside from the prevailing market level at the time of the report – with the bullish case anchored on product mix improvement, expanding hybrid offerings and continued exposure to SUV demand.

What will determine whether the share price momentum is sustained in 2026 is less about hype and more about execution: keeping localisation on track, protecting margins as policy incentives evolve, ensuring parts availability and aftersales quality, and managing delivery timelines as bookings rise. But the direction of travel is clear: Sazgar is trying to become a full-spectrum SUV player – from mass-market crossovers to premium hybrid 4x4s – and the market is currently rewarding that ambition. n

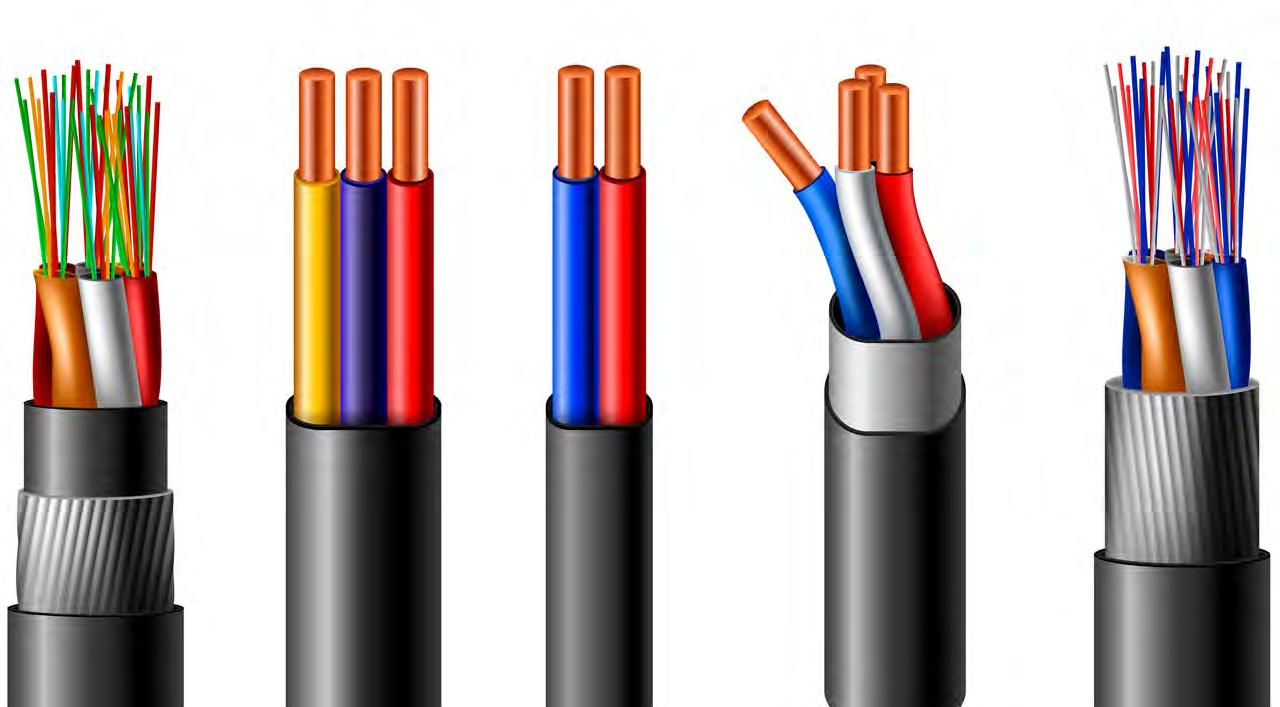

Fast Cables believes in the adage that if you build it, they will come

The company has big expectations from the future after laying down the ground work

By Zain Naeem

When the bidding for Pakistan International Airline was being carried out on the 23rd of December 2025, the ripple

effects of this privatization were expected to go far wider into the economy as a whole. The bidding was the last step in setting the price of the privatization but this was going to set off a beginning of a process that would see many such transactions taking place in the future. There was an air of anticipation in the banquet hall at the plush hotel where the Arif Habib

Consortium was able to win the bidding war. At a distance of 300 kilometers, a similar sense of anticipation was being seen on the factory floors and conference rooms of Fast Cables which was putting the finishing touches on their recently established production unit. A process that started nearly two years ago was reaching completion and Fast was opening

up its doors to the new reality. A reality that they had worked hard for and which would finally come to bear fruit in the near future. This is the story of how Fast Cables laid down the ground work and established a launch pad to blast off into the future. The literal realization of its tag line “Taaroun sai Sitaaroun tak”.

History of Fast Cables