Deepening Roots in Europe & the U.S., Bullish on Southeast Asia's Potential

Linkwell, with its full range of fasteners, multi-site (including Taiwan, China, Indonesia, Malaysia, Vietnam, etc.) production lines, and one-stop services, has been deeply rooted in the construction and industrial markets for 49 years, earning high praise and trust from numerous global clients. In 2025, the fastener industry faced unprecedented political and economic turbulence, with fluctuating demand in Europe and America impacting orders for Taiwanese suppliers. However, Linkwell relies on its business resilience to continue providing stable supply to its European and American clients. President Kosky Yen stressed: "Drawing on nearly half a century of global trade experience, we've observed that overseas fastener demand fluctuates but follows an overall upward trend. Europe and America remain the largest demand markets and won't disappear—we will always be the most reliable backbone for our clients there!"

SUNNY HILL

CHINA

FASTWELL

Competitive Supply System Enables Global Adaptability

Moreover, Linkwell has long laid out its strategy in the Asian market, optimistic about the steady continuous growth in Southeast Asian fastener demand in recent years. It has established factories in Malaysia, Vietnam, and Indonesia, positioning them as a solid foundation for stable business growth—a clear positive for Linkwell.

Southeast Asian countries, particularly Indonesia, Malaysia, Vietnam, and Thailand, impose extremely strict environmental regulations on foreign-invested factories. Linkwell's factories in these Southeast Asian nations have been cultivated for years, with their fastener products meeting high self-standards in environmental technology and quality, giving the company a key competitive edge in the Southeast Asian market. The Taiwan headquarters leverages support from diverse partner factories to achieve a complete production supply chain. By integrating sites in Taiwan, China, and Southeast Asia, Linkwell has built a onestop supply chain that flexibly meets global clients' diverse needs in quality, cost, environmental protection and volume.

Responding to Energy Savings & Carbon Reduction with Digital Systems

To comply with the EU's CBAM, Linkwell engaged professional consultants for guidance and required all factories to jointly promote energy savings and carbon reduction. Meanwhile, in response to client demands, it actively introduced ERP systems into its plants and production processes, demonstrating its commitment to sustainable operations.

Brand Management Drives Business Upgrades

Facing various competitions and uncertainties from U.S.China trade tensions, Kosky believes that the "strength of stability" and "solidifying brand reputation" are the keys to a company's sustainability. Therefore, Linkwell is upgrading equipment automation to reduce labor costs and enhance quality stability. Looking ahead to future challenges, Linkwell looks forward to forging even closer ties with its partners to achieve new successes.

High Drilling Speed and StabilityALEX SCREW’s Self-drilling Screw Technology Stands Out from Peers

Self-drilling screws are commonly used fasteners in many outdoor and construction fastening operations, but their performance sometimes may not meet customer expectations due to insufficient technical expertise from manufacturers. Recognizing the potential market demand and application advantages of self-drilling screws, Alex Screw Industrial Co., Ltd., with its extensive screw manufacturing knowledge, has invested heavily in selfdrilling screw technology in recent years, in addition to window screws and building screws. It aims to provide global customers with product solutions that combine performance and durability through its superior technology and design capabilities.

Penetrating Through 12 mm Thick Steel Plates in 15 Seconds

mong various short, medium, and long self-drilling screws, the one with a #5 point is arguably the most technically demanding. Previously, customers often encountered inconsistent penetration performance or fluctuating penetration times when using these screws for fastening sheet metal. However, Alex Screw's technical team conducted in-depth research into the shape and processing steps of self-drilling screws, introduced professional appearance measurement fixtures, and carried out precise control of mold service life, successfully developing the self-drilling screws whose penetration speed and stability have amazed customers. These screws will be also showcased at the Taiwan International Fastener Show 2026. "Making self-drilling screws with good quality is not easy, but making a longer #5 point self-drilling screw is even more difficult! Thanks our #5 point self-drilling screw can penetrate a 12 mm thick steel plate in 1516 seconds, demonstrating excellent drilling speed and high stability, and has received extremely high praise from many of our clients. Not only does it have a differentiated technological advantage, but it is also more pricecompetitive compared to other major manufacturers' products," Sales Manager Anne of Alex Screw said.

Quality Control Fully Upgraded to the "Bluetooth

nderstanding the differences in customers' knowledge of products and two-way communication skills, Alex Screw skilled in customer communication can tailor the most suitable solutions for customers, covering materials, specifications, and technology, and can also create greater value for customers through quality control upgrades and shortened delivery times. Starting with rigorous control over associate service providers for heat treatment, electroplating, and surface treatment, it implements inspection step by step. In addition to purchasing X-ray film thickness and salt spray testing machines to control quality, its QC personnel have fully switched to Bluetooth-interconnected instruments to integrate accurate data directly into the ERP system, avoiding human-made errors and inaccurate reports. "Quantitative data make it easier for us to analyze and improve. In the future, we will gradually replace large instruments that have exceeded their service life to create a more complete interconnected quality control system," Sales Manager Anne said.

Flexible Delivery Capacity- the Top Choice for Customers in Emerging Markets

In addition to stable deliveries to mature markets such as Europe, Alex Screw continues to focus on the needs of customers in emerging markets such as the Middle East, Russia, and Central/Eastern Europe who demand "good prices but not low quality," and also has suitable products to meet the needs of various building projects or structural fastening applications. "Emerging markets have significant demand for self-drilling screws, but their ordering and inquiry patterns differ greatly from those of customers in Europe and the U.S. We can flexibly adjust shipments from our own factories in China or Taiwan to suit the regulations and customer requirements of different markets, and we are happy to offer customers discounts without compromising quality while maintaining reasonable profits. We hope to expand our presence in emerging markets while fully satisfying our customers' needs," Sales Manager Anne said.

Copyright owned by Fastener World

Article by Gang Hao Chang, Vice Editor-in-Chief

Self-drilling

Customers Travel Great Distances to Seek Cooperation.

KWANTEX Wins Market

Dominance Through "Innovation"

"If you're looking for unreleased leading products and technologies, look no further than Kwantex in Taiwan!" This statement from an overseas customer not only highlights Kwantex's successful investment over the past 30 years, transforming from packaging & wire drawing to R&D in fasteners, but also demonstrates its long-established leadership at a different level among its Taiwanese counterparts in terms of product development, technological innovation, and brand positioning.

In recent years, Kwantex has consistently conveyed its focus on R&D and its strong R&D capabilities to the international market. Its outstanding innovation is reflected in its annual product development, with many products receiving recognition such as the German Red Dot Design Award, the Fastener Innovation Award from U.S. Worldwide Fastener Sources, the Best Booth Award at IFE 2025, etc. Furthermore, Kwantex actively keeps pace with environmental protection and carbon reduction trends, such as achieving ESG certification in 2024 and planning to release its latest ESG report in 2026, demonstrating its significant commitment and responsibility to environmental friendliness and sustainable development.

Incredibly Eye-catching Products! A New Product is Adopted Every 5 Years

"To turn the market around, there's no chance without innovation," Kwantex President Jack Lin said. Kwantex develops over 100 improved, innovative, and patented products annually, with R&D and patent maintenance costs reaching tens of millions NTD. For Kwantex, a product's ability to revolutionize the market requires a balance of functional and aesthetic innovation, along with optimal adjustments to meet customer needs. President Lin believes, "Only innovative products can give us pricing power." Therefore, since securing its 1st European customer order, Kwantex has been working at full speed. Through continuous development, testing, and product refinement, an average of 1 new product is adopted by customers every 5 years, with some new products already surpassing the design and functionality of many well-known European and U.S. brands.

5 Major Features of Kwantex Wood Screws and Industrial Assembly Screws: Quick Fastening, Force-saving, Anti-split, Shear-resistant, and High Pull-out Strength

The relatively poor rust and deformation resistance of traditional industrial steel beams has led markets in Europe, USA, and Japan to shift towards Cross Laminated Timber (CLT) construction, thereby driving demand for wood screws. Coupled with rising labor costs, the demand for

President Jack Lin ▼

wood screws that can meet automated & rapid fastening requirements without cracking or insufficient anti-loosening force, as well as industrial assembly and construction screw sets with high clamping force and easy maintenance & reuse, is also increasing daily.

These needs can now be met through Kwantex's full-size and high-performance product offerings, such as wood screws that offer quick & easy fastening and anti-split performance while maintaining a clean and aesthetical finish; the TTX® Drive & Bit series, which fasten securely when turned (including the patented TTX® Drive with its 6-lobe hook design to prevent slippage and which won the Worldwide Fastener Sources Fastener Innovation Award in 2022); the Cutters series, a leading brand in the Nordic and N. American furniture/construction markets, known for its ease of use and crack resistance; and the Torpedo series, which allows for quick tapping

(including the KTX-Torpedo Plastic Decking Screw, which fastens wood surfaces without cracking edges and features reverse threads to prevent mushrooming); the 3rd-generation Archimedes’ Secret Threads (AS’) series (the best alternative to the TY-17, double cut design and Torpedo thread) that can prevent wood cracking without damaging the wood fibers and reducing driving torque, and maintain high pull-out force; the KTX Convex (VK) Head that can replace traditional hex washer heads and prevent slippage and wear after installation (suitable for various steel structure, wood structure, and concrete screws and bolts, which are easy to use with VN nuts); the KTX-Jig (for Hidden Decking Screw System) that can create a clean, fastener-free surface by side fastening, which won the Worldwide Fastener Sources Fastener Innovation Award in 2025; and the stainless steel KTX Terrace (IPE) Screw that can drill into extremely hard wood without pre-drilling and snapping-off.

Kwantex Still Achieves a 20% Growth Amid Market Sluggishness

"Kwantex products have consistently achieved positive results in each market. A high percentage of customers who have used our products become our agents or use our patents for private label sales. When customers are experiencing economic downturns or excessive market competition and shift towards product upgrades, it presents an opportunity for us to leap forward. With hundreds of product improvements and innovations every year, we still achieved growth of over 20% in

2025." President Lin said. Kwantex's innovation extends from product design to subsequent packaging and logistics, and it aims to integrate concepts such as environmental protection, storage, and reuse with users' home life. Kwantex will celebrate its 30th anniversary in 2026. President Lin also announced that in the 2nd half of 2026 the company will present more groundbreaking innovations to global customers in product design, packaging, and

logistics, showcasing Kwantex's worldclass R&D capabilities and quality strength on par with international giants. "When Kwantex received the Best Booth Award at IFE 2025, the judges praised us as 'an industry leader and a model of innovation in Taiwan.' I believe that a large part of the reason we won this award is based on our consistent efforts to demonstrate the core value of our products and our forward-looking vision of future market trends," President Lin said.

Focusing on ESG, Ensuring Environmental Sustainability, and Caring for Employees

In addition to its commitment to product innovation, Kwantex also values environmental protection and carbon reduction. The company's representative color “purple” conveys Kwantex's aspiration to maintain its business development while striving to reduce pollution in the screw manufacturing process and coexist sustainably with the Nature, because screws are not just products, but an integral part of everyone's life. "Kwantex products are certified by the EU CE/ETA, US ICC, and SGS quality management systems. They can be reused in various fields such as industrial assembly, civil engineering, bridges, vehicles, ships, and aviation, eliminating the problem of needing to scrap a large number of screws due to failure. This perfectly aligns with the spirit of ESG environmental protection and carbon reduction," President Lin said. Regarding corporate responsibility, Kwantex creates a safe workplace for its employees. In addition to

professional safety and fitness managers stationed at the factory, there are also dedicated factory nurses and external occupational physicians providing employees with regular medical check-ups and assistance. On the occasion of the company's 30th anniversary, President Lin said, "We will continue to focus on product innovation and corporate sustainability, so that our employees can work with peace of mind and we can attract more customers from more countries to adopt Kwantex products or our brand."

Pointmaster Machinery has researched self-drilling screws for nearly 30 years. At its founding, it had only one machine model, but has always sticked to co-developing with clients and listening to their needs, continually developing new products. It is currently the most comprehensive manufacturer of self-drilling screw formers.

Founded in November 1998, Pointmaster reached a milestone on January 8, 2019 with the 1,000th self-drilling screw former shipped, and the 1,500th one shipped on April 11, 2024. Looking back, there used to be words that Pointmaster would close its doors, along with shareholder disputes, a factory auction crisis, and three years of legal battles. General Manager Mr. Chi-Wei Liao recalls with mixed emotions, “It is winning the court case at that time that culminates to Pointmaster’s success today.” With the 1,633rd machine shipped to this day, Pointmaster’s commitment to quality and service remains the constant tenet for 27 years.

Diverse Specifications, Durable & Robust Design

Self-drilling screw formers are essentially for self-drilling screws production only, so they have a relatively smaller market demand than other fastener machines. Yet this has not dimmed Pointmaster’s passion for manufacturing selfdrilling screw formers. It continually researches in this field, and whenever clients report deficiencies, Pointmaster tests and improves the designs. No matter how much time and energy is required, they insist on delivering the best.

Pointmaster’s current self-drilling screw formers are available in single or double-stroke structures, with sizes categorized by the fastener size they produce. The doublestroke design is intended for stainless steel screws, while the single-stroke model mainly produces carbon steel screws. The models include popular PM-100, PM-100S, PM-200, and PM-210S, reaching production speeds of up to 600 pieces

Email: tforever@ms29.hinet.net

per minute. Besides standard models, custom machines are available, such as the PM-W250S tailored to client requests. The largest model can produce self-drilling screws up to 600 mm in length. Pointmaster’s R&D has yielded multiple patents; the use of different cast iron materials strengthens the machines’ rigidity and robustness, delivering a tonnage output about 1.25 times higher than competitors.

Pointmaster utilizes a patent “dual clutch control system” that can rapidly disengage the front flywheel inertia, allowing instant braking even at high speeds. This prevents quality issues from misfeed or empty-die collisions and also protects the dies, boosting production efficiency. Even many Chinese manufacturers prefer Pointmaster’s forming machines over cheaper locally-made options. All models have CE certification, with quality recognized in EU countries.

Efficient After-Sales Service, Expansion into Emerging Markets

Pointmaster does not skimp on after-sales service. To rapidly diagnose and resolve client issues, it operates a service center in Gangshan of Kaohsiung, Taiwan’s fastener heartland. For Chinese clients, to avoid the need for on-site technicians, there are authorized service partners in Guangzhou and Zhejiang, China, to provide after-sales service. The company continually trains its technicians, and should there be problems that cannot be resolved remotely, head office personnel can fly abroad to provide global clients with support.

Currently, its sales are primarily export-driven. In recent years, as production prerequisites in emerging markets mature, demand has surged, especially in Vietnam, Indonesia, and India where Pointmaster’s orders continue to rise. Pointmaster does not have exclusive distributors for the time being but welcomes interested parties to discuss collaborations.

Copyright owned by Fastener World / Article by Dean Tseng

Pointmaster Machinery’s contact: Mr. Chi-Wei Liao, General Manager

Jern Yao's 12,560 sqm New Factory Inaugurated Massive Investment to Build “Self-use Parts” Processing Plant

Jern Yao Enterprises, one of the world's largest manufacturers of mid-to-high-end screw, nut, and part formers, with cumulative global sales nearing 5,000 units, officially inaugurated its self-use parts processing plant in Rende (Tainan) at the end of 2024. Unlike the original Plant 1, handling assembly, outsourcing, quality assurance, warehousing, and maintenance, the primary mission of Jern Yao's 2nd new plant will be to “increase the percentage of self-use parts production” and “enhance the precision, speed, and stability of machined parts.”

Nearly 50 Five-face and Advanced Milling Machines Now Operational, Securing Its Lead in High-Precision Product Manufacturing

The 12,560 sqm second plant dedicated to producing self-use parts represents a significant endeavor that sets Jern Yao apart from its competitors in the former manufacturing industry. The percentage of Jern Yao's self-use parts production was previously ~30%, primarily consisting of small-batch custom orders. Considering the challenges such as emerging succession gaps among partner factories, equipment upgrades, and parts lead times increasingly failing to meet the industry's stricter demands, coupled with the company's own desire to accelerate production schedules and enhance finished product precision, Jern Yao made a substantial investment in introducing 45 advanced and 4 fiveface milling machines. This initiative aims to rapidly elevate Jern Yao's product precision and manufacturing capacity to a level unmatched by competitors within a short timeframe. At a time when an increasing number of former manufacturers are heard to directly source cheap yet questionable-quality parts from China and have them assembled in Taiwan to “wash the origin” for cost reduction, Jern Yao not only refuses to follow suit by steadfastly rejecting Chinese raw materials and parts that fail to meet its high-standard quality requirements, but also invests heavily in acquiring dozens of advanced milling machines to enhance its self-use parts production capabilities, demonstrating Jern Yao’s unwavering commitment in recent years to actively frame itself as the world's premier former brand and solidify its position as the global leader.

“Currently, few Taiwanese former manufacturers possess five-face milling machines. Unlike traditional CNC machines, the advantage of five-face machines lies in eliminating the need to flip workpieces, significantly boosting machining capacity. It can operate with only a single setup, reducing humanmade errors while enabling us to execute more complex designs and achieve higher precision levels. To ensure precision for both tooling and workpieces, we even maintain our plant air conditioning at a constant 28°C. With the introduction of five-face milling machines, we now have the opportunity to further increase our core part self-sufficiency ratio to a 5:5 split, ” stated President Alec Tsai.

JernYao currently offers machine models ranging from 2-die to 8-die configurations. To meet customer demands for automated processing speed and efficiency, it actively integrates AI into product design (e.g., machine troubleshooting functions). It also recalibrates existing models (e.g., increasing their production from 240 pcs of M8 screws per min. to 300pcs) and accelerates die change efficiency through external adjustment of male/female dies. These measures comprehensively address increasingly stringent customer requirements for precision, speed, and stability.

“Price cutting represents Jern Yao's most significant challenge at present. However, the superior performance, the capability to produce more precise products, and the stability of our machines remain unmatched by competitors. Moving forward, we will strive to gain greater customer recognition by reducing unnecessary costs in the manufacturing process, ensuring smoother production line operations, and shortening lead times, in order to pave the way for Jern Yao's next era of successes,” added President Tsai.

New Plant Welcomes

President Alec Tsai to Office; Jern Yao Ready to Sail with New Management

Jern Yao, which has dominated the industry for 32 years with its exceptional high-

back simply because someone is a supervisor. He believes that eliminating the hierarchical distance that inhibits openness will enable smoother progress across all company operations.

President Tsai stated: “I aspire to build Jern Yao into a company where employees are genuinely motivated to work hard and even feel a sense of belonging, like it's their home. Traditional industries in central and southern Taiwan often adopt a management style where criticism

performance machines, welcomed new leadership in July 2024 as Alec Tsai formally took over the helm from former President Ted Tsai. His first initiative was a sweeping overhaul of Jern Yao's corporate culture, aiming to introduce Western management philosophies emphasizing “frank communication and treating managers as partners.” While the initial implementation proved challenging, the shift in corporate atmosphere is evident today. When employees now feel comfortable addressing President Tsai directly as “Alec,” it signals a departure from the previous era where management dictated every detail.

constructive suggestions, fearing they might be held accountable for any shortcomings. Instead, I prefer a collaborative approach where we sit down together to discuss problems and find solutions, encouraging everyone to voice ideas that benefit the company's future development."

Before assuming the role of President, Alec had served at Jern Yao for over a decade, gaining deep familiarity with all departments. His years of study, work, and life in the US and Canada also instilled in him a strong emphasis on fostering open communication between employees and management holding different viewpoints. Therefore, in his first year in office, he vigorously promoted reforms in the company's internal management culture. He hopes to eliminate the corporate atmosphere of the older generation that overly emphasizes hierarchical systems, allowing Western management thinking that encourages bold expression of opinions and mutual growth and progress to further take root in all departments. President Tsai believes: “The invisible distance between employees and supervisors hinders corporate growth and progress. This barrier prevents employees from promptly voicing concerns or suggestions, resulting in valuable input failing to reach management and issues not being resolved through timely team brainstorming.”

To bridge the gap with employees, President Tsai himself frequently addresses staff and managers by their first names in a friendly manner at the company. He actively encourages them to speak up whenever issues arise, emphasizing that even urgent matters can be brought directly to him for discussion—there's no need to hold

Corporate culture and employees determine a company's future trajectory. To strengthen employees' sense of identification and belonging with the company, President Tsai has actively promoted knowledge transfer and technical training across departments. His goal is to equip the company team with more robust capabilities to tackle future market challenges. Under his leadership philosophy that “new equipment demands new ways of thinking,” Jern Yao stands ready to secure a decisive victory for the next 30 years.

Jern Yao’s contact: Mike Huang, Sales Section Chief Email: mike@jernyao.com

Copyright owned by Fastener World

Article by Gang Hao Chang, Vice Editor-in-Chief

The largest five-face milling machine in the plant

Five-face milling machines

President Alec Tsai

Upgrade and Transformation No Price Cutting!

Despite the bleak market atmosphere, with Taiwanese businesses complaining that reduced customer demand and lower unit prices have led to lower-than-expected overall order volume and profitability, is the situation really that bad?

Looking at the export data for the first 11 months of 2025, Taiwanese fastener industry is fortunate to have maintained a stable export volume of over 1.1 million tons. Compared to the same period in 2024 (approximately 1.2 million tons), exports to developed countries (such as Germany, Japan, Canada, Poland, France, Sweden, Denmark, Slovakia, Finland, and the Czech Republic) and emerging markets (such as Thailand, India, Saudi Arabia, Vietnam, Brazil, and the Philippines) have shown varying degrees of growth, with some countries even experiencing increases of several tens of percent. This conveys a message: the sluggish market does not mean that fastener demand is shrinking in all countries; some countries or regions are still experiencing growth against the trend.

In a market where opportunities and pressures coexist, businesses that can uncover potential opportunities others haven't yet seen to offset the enormous challenges posed by external pressures, amplify their unique advantages over competitors, and accelerate the adjustment of their development strategies, can definitely break through against the odds, attract customers to switch orders, and continue to achieve excellent performance.

Price Cutting Ignites Global Trade Protectionism;

Transformation is the Best Risk Mitigation Strategy

The massive dumping of Chinese products at below-market prices is gradually disrupting the existing balance of supply chains in many countries. The overwhelming influx of low-priced goods into local markets is causing substantial damage to local businesses, forcing many countries to seriously consider whether to impose protective import tariffs or high AD measures on manufacturers from China and other countries. This means that the era of trade liberalization created by the WTO framework is gradually coming to an end, and may also have ripple effects on Taiwan and other export-oriented fastener producing countries.

According to the foreign trade data released by China's General Administration of Customs, China's total import and export value for the first 11 months of 2025 reached US$5.75 trillion, a year-on-year increase of 2.9% (of which exports were US$3.41 trillion, a year-on-year increase of 5.4%; and imports were US$2.34 trillion, a year-on-year decrease of 0.6%). The overall trade surplus was approximately US$1.07 trillion (approximately NT$33.3 trillion), exceeding the US$1 trillion mark for the first time and surpassing the surplus for

the entire year of 2024. Many industries (not only fasteners) in China operate on a large-scale dumping competition model, with exports often exceeding hundreds of thousands of tons, making it extremely difficult for competitors to compete on price alone. Under such circumstances, if one would like to maintain profit margins and avoid losing orders, it's essential to find breakthroughs beyond price. With the low-price competition for market share seemingly a dead end, many industry associations in Taiwan are calling for a rapid pace of transformation and upgrading.

This includes accelerating product differentiation, digitizing production lines, and reducing carbon emissions to promote industrial upgrading. In addition, increasing participation in international exhibitions to solidify customer loyalty in Europe and the United States and expanding brand awareness in emerging markets will help alleviate the pressure caused by low-price competition or trade protectionism.

Rate Fluctuations of NTD Become Stabilized, Temporarily Alleviating the Profit Erosion Crisis

Industry

policies and foreign exchange market adjustments. In contrast, the NTD experienced a sharp appreciation in a short period of time. This is quite unfavorable for Taiwan's traditional industries and fastener industry, which rely heavily on exports. In particular, Taiwan has fewer domestic resources compared to other countries, and it cannot compete with China's strong dumping and subsidized prices for steel raw materials and wire rods. Various unfavorable conditions for competition have left many businesses in a difficult position.

Therefore, Taiwanese government should play a key role in considering the difficulties faced by industrial development and doing its utmost to maintain the stability of the NTD exchange rate without being regarded as a currency manipulator .

2026 is a Crucial Year for the Development of Taiwanese Fastener

Historical data show that Taiwanese fastener industry has remained stable despite fluctuations in the past two years. With the support of the government and related industry associations, it is estimated that exports would still hover around 1.2 million tons in 2025. However, it is important to note that although there are no signs of deterioration in exports at present, some countries may further implement AD duties due to trade protectionism or competition from Chinese manufacturers. Furthermore, the EU's CBAM and the U.S. tariffs on steel and aluminum pursuant to Section 232, and even the potential expansion of trade protection policies by Canada, Mexico, the EU, or Japan, will inevitably have varying degrees of impact on major markets, and Taiwan cannot be excluded from these scenarios.

Some manufacturers believe that the impact of the U.S. Section 232 may last for at least 5 years. In other words, the next year or two will be a critical period for the survival of Taiwanese businesses. If they do not upgrade and transform, and actively seek potential development opportunities, their advantages may soon be overtaken by competitors from China and emerging countries.

2025 has passed. Although the overall economic environment remains uncertain, if we look ahead to 2026 and even 2027, the market still holds a lot of potential and development opportunities. Facing economic cycles and external challenges, businesses and individuals inevitably experience pressure; however, this is not the time to be discouraged or to stop moving forward. Only by continuously striving to improve your capabilities, strengthening your professional skills and competitive advantages can you maintain the foundation during downturns. Through continuous learning, adjusting strategies, and accumulating energy, you can seize opportunities and make the best preparations for future growth and breakthroughs when the overall economy gradually improves.

When the NTD appreciated to NT$28-29 to 1 USD, it wiped out the profits of many Taiwanese manufacturers. Fortunately, it has recently recovered to a more stable level of NT$31-32, which has temporarily alleviated businesses' concerns about the continued erosion of profits by the exchange rate. For the past 2 decades, the NTD exchange rate has been closely influenced by fluctuations in the U.S., China, Japan, and S. Korea. However, observing the changes in the Japanese yen, Korean won, and Chinese yuan against the US dollar in 2025, the Japanese yen fluctuated significantly but did not form a one-way sharp appreciation or depreciation trend throughout the year. The Korean won also fluctuated moderately within a range. The Chinese yuan appreciated moderately due to the influence of Chinese Copyright owned by Fastener World / Article by Gang Hao Chang, Vice Editor-in-Chief

EMERGING FASTENER MARKETS NEWS

全球新興市場新聞

compiled by Fastener World

Association News

The Fasteners Cooperative Association of Kansai Visits Manila, Philippines

The Overseas Information Committee of Fasteners Cooperative Association of Kansai (Western Japan) led a delegation of 7 members on a tour to Manila, Philippines, from October 22 to 24, 2025. The purpose was to gain insights into local market dynamics and business environment while exploring potential future collaboration opportunities.

The group departed from Kansai International Airport and, upon arriving in Manila, they first toured the historic Intramuros district to experience remnants of the Philippine colonial era. The following day, the delegation visited Yamaguchi Nut Philippines Corporation (affiliated with Japan's Yamaguchi Nut Company), where they received a company overview and details on future development plans. Discussions focused on Philippine market trends and business challenges, followed by a tour of the nut factory to examine production processes. The group then proceeded to Philippines Ogami Corporation (affiliated with Japan's Ogami Co.), listened to a company briefing, and conducted an tour of the mold factory to gain a deeper understanding of local operations. After concluding the tour, the delegation returned home from Manila. This activity not only gathered valuable overseas information but also strengthened ties between Japanese and Philippine companies, contributing to the association's future internationalization efforts.

2.0

Trump’s Steel Tariffs Stifle India’s Metal Industry Amid Global Trade Tensions

For years, the US has been a major market for Aditya Garodia, director of Corona Steel Industry Pvt Ltd, exporting over 100 steel products like fasteners from his West Bengal factory. However, after US President Trump imposed tariffs, business slowed significantly. Garodia said clients delayed orders and payments, with 30 percent of orders canceled after the tariff increase. Domestic demand also dropped due to cheaper Chinese competition. He stressed that India’s future steel exports depend on negotiating lower US tariffs.

Foundry owners across India report a steep decline in orders from US clients, describing the tariffs as a “nail in the coffin” for their businesses. Despite vigorous efforts by Indian industry representatives and the government to secure tariff exemptions and explore alternative markets, the trade restrictions remain firmly in place. With ongoing challenges from global trade tensions and economic instability, the tariffs exacerbate pressures on India’s metal industry. The situation highlights the broader risks facing exporters amid shifting international trade policies under US administration changes. Indian foundries are now forced to innovate and seek new opportunities, but the shadow of the tariffs continues to limit growth and profitability. The persistence of these tariffs serves as a cautionary tale about the long-term consequences of protectionist trade policies on global supply chains and developing economies.

Market Watch: Trump Tariff

Market Watch:CBAM

CBAM Takes Effect: Thailand's Steel Industry to Bear the Brunt

CBAM上路

With CBAM effective on January 1, 2026, Thai analysts predict that Thailand's iron and steel sector will face the heaviest impact. K-Research estimates the mechanism will affect 3.8% of Thailand's exports to the EU, equivalent to 28 billion bahts. Iron and steel, along with aluminum, will be hit first; in 2024, Thailand exported US$95.1 million worth of iron and steel to the EU and US$56.7 million in aluminum. Cement and fertilizer exports are negligible, while electricity and hydrogen have no sales to the EU.

Thai steelmakers are already under pressure from cheap Chinese imports and the US decision to raise steel and aluminum tariffs from 25% to 50%. CBAM will further erode competitiveness. Analysts warn that while initial financial burdens are limited, failure to adjust quickly could undermine Thailand's manufacturing edge. To support exporters, the Thai government is advancing the climate change bill approved by the cabinet on December 2, 2025, demonstrating Thailand's commitment to global decarbonization. The Federation of Thai Industries chairman stated: "This bill will bolster industry and exports, protect Thai products in international markets, and prevent lagging behind global climate standards." He emphasized that if Thailand fails to keep pace with CBAM and similar regulations, it risks declining export competitiveness, slower economic growth, and widening industry inequality.

European High-Energy-Intensive Industries Criticize: Carbon Border Tax Too Lenient on China's "Dirty Imports"

Starting in 2026, the EU imposes carbon fees on cement, iron, steel, aluminum, and fertilizers imported from countries with weaker emissions standards, ensuring "dirty" imports do not gain unfair advantages. EU domestic products must pay around €80 per ton of CO₂. European highenergy-intensive industries are deeply concerned that the CBAM is too soft on heavily polluting imports from China, Brazil, and the US, undermining the mechanism's original purpose. The main challenge lies in foreign producers not providing precise emissions data, so the EU plans to use default formulas for calculations. Drafts show that default emissions values for Chinese steel products are even lower than EU equivalents, sparking industry criticism. Green steelmaker Stegra is surprised that some EU production routes have "higher emissions than China" and suggests adjusting the values.

Industry warns that low default values will weaken incentives for clean production, allowing high-emission imports to enter the market at low carbon costs, potentially backfiring. CBAM Alliance Acting Chair Leon de Graaf stresses that default values should be set high to "punish" those not reporting real data, or importers will lack motivation to comply. Incorrect values could harm EU producers for two years. In response, Chinese media reports that these European industry figures overlook China's steel sector's green transformation achievements, claiming that by 2024, China's steel industry had 660 million tons of capacity engaged in energy efficiency benchmarking, saving 105,000 tons of standard coal annually per 10 million tons of capacity—totaling 10.5 million tons saved and 27.5 million tons of carbon reduced yearly, equivalent to the annual carbon sink of 570 million trees. China's Ministry of Commerce has urged the EU to uphold fairness, transparency, WTO rules, minimize trade disruptions, and avoid protectionism and green trade barriers.

Industry Development

Canada Imposes 25% Additional Tariff on Steel Derivative Products

The Canadian government has issued an official announcement imposing a 25% surtax on specified steel derivative products effective December 26, 2025. This measure applies to steel derivatives imported from all countries worldwide, aimed at protecting the domestic steel industry. Importers must declare and pay through the Canada Border Services Agency (CBSA). Goods in transit on the effective date are exempt. Affected fastener HS codes include: 731811, 731812, 731813, 731814, 731815, 731816, 731819, 731821, 731822, 731823, 731824, 731829.

EMERGING FASTENER MARKETS NEWS

Exemptions: Goods covered by existing surtax orders (e.g., China/U.S. steel surtax orders), casual goods, Chapter 98 goods, and in-transit goods. Temporary Exemptions: Until July 1, 2026, goods for manufacturing motor vehicles or vehicle chassis, or parts/ accessories thereof; goods for aircraft, ground flight simulators, or spacecraft, or parts thereof.

Remissions: Case-by-case relief available for goods unavailable domestically or causing severe economic impact. Existing U.S. import remissions temporarily extended through January-June 2026 (depending on use). 中國螺絲出口量前11個月衝破510萬噸

China's Fastener Exports Exceed 5.1 Million Tons in First 11 Months of 2025 Despite Price Decline

Despite persistently falling export prices, China's fastener industry demonstrates strong resilience. According to the latest data, China's fastener exports reached 5.107 million tons in the first 11 months of 2025, up 7.5% year-over-year. Full-year exports are projected to grow substantially for the second consecutive year, though the average price stood at just USD 1.921 per kg, down 2.7% from the previous year. January's exports soared to 587,339 tons, setting a historical single-month record. Volumes contracted sharply to 249,243 tons in February and fell further to 411,424 tons in October—the second-lowest monthly figure of the year. November saw a rebound to 493,438 tons, up 19.93% month-over-month and 4.31% year-over-year, approaching the 500,000-ton mark and signaling demand recovery.

On pricing, August 2024 plunged to USD 1.85 per kg— the lowest in 6 and half years. In 2025, January dipped to USD 1.857 per kg, while March briefly rose to USD 2.008 per kg, ending nine straight months below the USD 2 threshold. October and November slid again to USD 1.893 and USD 1.874 per kg, respectively, both annual lows. By contrast, December 2022 peaked at a record USD 3.278 per kg, with March 2023 at the second-high USD 3.205 per kg. In 2024, full-year exports totaled 5.289 million tons, up 16.66%, but prices crashed 14.3% to USD 1.97 per kg. Analysts note that low pricing remains a key competitive edge, driving volume growth amid price-volume divergence. Historical lows, like February 2023's 190,000 tons, underscore volatility, yet the overall upward trend bolsters China's global market share.

Vietnam’s Auto Parts Industry Accelerates

As of May 2025, Vietnam boasts 858 enterprises and manufacturing facilities certified to International Automotive Task Force (IATF) standards—a 22-fold increase in just 18 months—signaling rapid industry maturation. Vietnamese manufacturers now produce advanced components such as electric motors and electronic modules, moving beyond the so-called "screw curse" of only basic parts.

With a growing domestic auto market, experts urge a strategic push to develop the full supply chain, attracting foreign direct investment and supporting local SMEs. For example, Ho Chi Minh City’s An Thinh Technology shifted from household electrical goods to automotive wiring and jacks in 2019, achieving double-digit sales growth annually. Vnines Innovation in Dong Nai focuses on EV motors and controllers, exporting to North America, Europe, and Asia. Amphenol RF Vietnam, established in 2024, assembles automotive RF connectors.

Vietnam’s auto parts sector is increasingly integrated globally, valued at USD4.5 billion in 2023 and forecasted to exceed USD 13 billion by 2032. Despite challenges in skilled labor and environmental compliance, companies are expanding capacity and diversifying products, driving fastpaced growth.

Industry Leaders Unite to Drive Asia’s First Carbon Capture and Storage Initiative

產業巨頭攜手推動亞洲首個碳捕捉與封存計劃

A pioneering cross-industry consortium comprising global steelmakers, energy giants, and mining companies has initiated Asia's first independent, industry-led study to explore Carbon Capture, Utilization, and Storage (CCUS) hubs across the region. Participants include BHP, ArcelorMittal Nippon Steel India, JSW Steel, Hyundai Steel, Chevron, and Mitsui & Co. The study aims to identify large-scale CCUS projects with strong potential for CO2 storage and commercial use, focusing on hard-to-abate sectors like steelmaking. By leveraging shared infrastructure and economies of scale, the initiative targets cost reduction and economic viability. The year-long project will also examine regulatory frameworks, cross-border CO2 transport, and commercialization pathways. This landmark effort seeks to accelerate decarbonization efforts in Asia’s steel sector and create practical solutions that contribute to regional climate goals while supporting economic growth and industrial sustainability.

Companies Development

Avlock International India Inaugurates Manufacturing Facility in Mumbai

India啟用位於新孟買的扣件製造廠

On July 21, 2025, Avlock International India Pvt Ltd, a South African Joint Venture in India, inaugurated its new state-of-the-art fastener manufacturing plant in Rabale, Navi Mumbai. The event was led by founding member Mr. Lachhman Kewalramani and attended by Country Head Mr. Nishant Bagwe alongside key officials and partners.

The facility is equipped with advanced CNC and hydraulic machinery as well as in-house R&D, significantly boosting production capabilities to serve domestic and global markets. This move supports India’s "Make in India" initiative by strengthening local manufacturing and reducing import dependency. Products include lockbolts, blind fasteners, rivet nuts, and hydraulic and pneumatic installation tools, serving critical industries such as automotive, railways, renewable

energy, oil & gas, and more. Director Mr. Sameer Bulchandani highlighted that the Rabale plant marks a new chapter for scaling production and fostering innovation, efficiency, and sustainability, aligning with the company’s vision to become a globally recognized fastener brand.

BSRM to Invest Tk400 Crore in Fastener Plant

孟加拉BSRM公司投資

BSRM Group, Bangladesh’s steelmaker, has announced a Tk400 crore investment in building a state-of-the-art fastener manufacturing plant under BSRM Wires Limited at Mirsharai in Chattogram. The plant will produce high-quality bolts and nuts, reducing reliance on imports. Investment comes from both BSRM Limited and BSRM Steel, each contributing Tk200 crore. Construction will take over a year, creating at least 200 new jobs.

This strategic move enhances BSRM’s position in the steel value chain, aiming to support large infrastructure, shipbuilding, and energy projects while strengthening Bangladesh’s regional market competitiveness.

EMERGING FASTENER MARKETS NEWS

Businesses Including Deepak Fasteners Plan Rs 15,000 Crore Investment in Madhya Pradesh

Deepak Fasteners等多家企業將在 中央邦投資1500億盧比

Sundram Fasteners Announces New Global Engine Program

Sundram Fasteners 宣布全新全球引擎計畫

Newly inducted Punjab Industry Minister Sanjeev Arora faces a challenge as several Ludhiana-based industrialists plan to invest Rs 15,000 crore in Madhya Pradesh (MP) over the next five years. This surge follows MP Chief Minister Dr. Mohan Yadav’s recent visit to Ludhiana, where discussions with business leaders led to this investment boost. Concerned about Punjab’s investment outflow, MP Vikram Sawhney stressed the need to build a strong local ecosystem with world-class infrastructure and industrial zones to retain investment and jobs.

The move threatens Punjab’s economy. Gurmeet Singh Kular, president of the Federation of Industrial and Commercial Organizations (FICO), criticized the Punjab government for insufficient support, citing issues with promised fiscal incentives and refund schemes excluding major sectors. Shiromani Akali Dal president Sukhbir Badal highlighted lawlessness and gang violence in Punjab as reasons for the exodus, accusing political instability of damaging the state’s economy.

Key investors committing to MP include Deepak Fasteners (Rs 1,300 crore) and others, with expected employment for 20,000 youth. An industrialist noted better subsidies and safer conditions in MP compared to Punjab, influencing investment decisions.

Marmon Fastener Leases Factory in Southern Vietnam

Marmon Fastener公司租用越南南部工廠 擴展製造鏈

Marmon Fastener will lease a 6,000-square-meter readybuilt factory in Dong Nai Province, southern Vietnam, to manufacture screws for the North American market. The deal was facilitated by property firm Savills Vietnam. After two years of studying the country, Vietnam was chosen for its first investment, according to Chairman Steve Semmler. Leasing a ready facility reduces deployment time and leverages Vietnam’s skilled labor, stable investment environment, and competitive costs, while strengthening global manufacturing capacity and diversifying supply chains beyond North America.

Savills HCMC’s industrial services manager Phan Cuu Chi said this move reflects growing American investor confidence in Vietnam as a manufacturing hub within Asia’s supply chain. Vietnam’s advantages in cost, human resources, and location continue to attract multinational expansion.

Automotive components leader Sundram Fasteners recently unveiled a new global internal combustion engine (ICE) program and expressed a positive outlook for the coming months. This strategy capitalizes on robust domestic industry momentum and export recovery potential. The company revealed a long-term initiative set to launch between 2029-2031, demonstrating its innovation commitment and ability to secure future business amid automotive industry transformation.

Q4 and Q1 order schedules are expected to optimize, with management optimistic about the next six months, driven by:

• Strong domestic industry conditions

• Potential export market recovery

• Increased customer orders in Q1 and Q2

New products account for over 20% of revenue, developed over the past three years, showcasing market adaptability. Stainless steel and railway fasteners are key growth areas, targeting double-digit annual growth next year. The wind energy segment matches automotive profitability with superior capital return, focused on domestic markets, highlighting successful diversification.

Despite export challenges, management anticipates recovery within six months, with customers planning increased Q1-Q2 orders to significantly boost overall performance. Through the global engine program, product innovation, and diversification, Sundram Fasteners solidifies its growth foundation. Positive domestic and export outlooks plus strong wind energy results signal achievable targets, with investors watching quarterly financials closely.

Nitto

Seiko

Meets with Haryana State Chief Minister to Deepen Business Expansion in India

日本日東精工與印度哈里亞納邦首相會面,強化日印合作

On October 7, 2025, Nitto Seiko (Japan) held a significant meeting with Nayab Singh Saini, Chief Minister of Haryana State, India, during the "India Haryana State Investment Promotion Roadshow." Facilitated by Nippon Indo Cultural and Economic center, this meeting marked an important opportunity to strengthen India-Japan economic cooperation.

Since Mr. Saini took office in March 2024, bilateral economic collaboration has deepened. Earlier this year, Nitto Seiko completed the acquisition of Vulcan Forge Private Limited and Vulcan Cold Forge Private Limited subsidiaries in India to leverage local manufacturing and supply chain integration. The meeting featured an introduction of the Vulcan Group based in Haryana and acknowledged by the Chief Minister through a commemorative gift symbolizing a lasting friendship. Looking ahead, Nitto Seiko plans to expand business in India, deepen local partnerships, enhance technology exchange, and accelerate its global growth strategy.

UK-Ghana Industrial Partnership Strengthened as British High Commissioner Visits Springs and Bolts Factory

英國高級專員訪問Springs and Bolts工廠,

英國與非洲加納工業合作再添新章

British High Commissioner Harriet Thompson visited Springs and Bolts Co. Ltd. in Kumasi, Ghana, marking a significant milestone in UK-supported investments in Ghana’s manufacturing sector during her farewell tour in the Ashanti Region. The visit underscored the UK’s role in advancing Ghana’s ambitions as a competitive manufacturing hub in West Africa. Through the UK’s Jobs and Economic Transformation (JET) program, implemented by the Palladium Group, Springs and Bolts received technical support and grant funding, enhancing its capacity and enabling investor readiness. Early this year, the company secured significant follow-on investment via the Ghana Investment Support Programme (GhISP), enabling construction of a new, modern factory for large-scale production of automotive leaf springs and launching Ghana’s first fasteners manufacturing plant. This expansion will boost local value chains, create over 200 skilled jobs, and expand exports to five new West African markets.

CEO Derrick Asamoah Boahen praised UK support for enhancing investor confidence and enabling growth and diversification. Commissioner Thompson highlighted the factory as a prime example of British investment fostering local businesses, innovation, and stronger UK-Ghana ties. Springs and Bolts has begun full production since the end of 2025.

Coastal Steel and Fasteners Launches in Beerwah Industrial Park, Australia

Coastal Steel and Fasteners公司

在澳洲Beerwah工業園區開業

A fresh player in steel supplies and fasteners has opened its doors in Beerwah's expanding industrial estate, delivering premium products and dedicated service to the local Hinterland area. Situated conveniently in the new industrial zone off Roy's Road (adjacent to Reece Plumbing), Coastal Steel and Fasteners is now serving customers with an extensive selection of steel materials, fasteners, and bespoke cutting services designed for projects big and small.

Owner and founder Brendan Flesser, a certified boilermaker with more than 10 years of practical expertise, guarantees professional guidance, accurate fabrication, and dependable support. "Our goal is to equip local tradespeople, companies, and DIY enthusiasts with top-grade materials and tailored solutions," Brendan shared.

He invites nearby residents and professionals to stop by, discuss their needs, and browse the inventory. "We're building more than a business—we're becoming a community staple. I'm eager to partner on turning ideas into reality." Emphasizing knowledge, customer care, and real partnership, Coastal Steel and Fasteners is set to establish itself as the go-to local resource for the long haul.

Global Fastener Supply Chains Operate with Close Collaboration Emerging Nations Gradually Exert Greater Influence

全球扣件供應鏈合作緊密 新興國家漸展影響力

Emerging Fastener Market

Emerging markets outside advanced economies like Europe, the United States, and Japan (including Southeast Asia, South Asia, Central Asia, Central and South America, the Middle East, and Africa) have actively participated in the global fastener industry supply chain in recent years. Their contribution to the global fastener industry continues to rise, with specific countries accumulating influence annually that has even begun exerting intangible pressure on competitors from other nations. As many of these emerging markets are developing countries, their economic growth momentum has been relatively stronger compared to other mature economies. Coupled with local governments accelerating infrastructure development to catch up with advanced nations and improve living standards, they have allowed foreign investment for building manufacturing plants. Furthermore, substantial official resources have been allocated to support domestic industries in developing sectors such as automobiles, motorcycles, 3C electronics, renewable energy, machine tools, and CNC precision machining products. This dual approach enables these nations to not only manufacture and supply relevant fastener products for other countries, but also generates significant demand for fasteners required to meet the manufacturing needs of these emerging industries. This article will further explore the collaborative relationship between these emerging markets and the fastener (HS Code 7318) supplydemand dynamics of Europe, USA, and Japan, analyzing the shifting influence of these emerging markets within the import-export landscape of these mature fastener markets.

USA (Unit: million USD / ranked by 2025 data / data published through August 2025 / source: U.S. DoC)

Import

Among the top 10 import sources for the U.S., emerging economies include India and Mexico, ranked 8th and 9th respectively. India also recorded the most significant year-on-year growth rate (24.73%) among the top 10 import sources, with the cumulative import reaching US$189 million in the first eight months of 2025. Its import scale was comparable to that of South Korea (ranked 6th) and Italy (ranked 7th); Imports from Mexico also saw a modest 4.61% increase compared to the same period in 2024, reaching US$129 million. Among the top ten import sources, Mexico’s growth rate was only second to India and Italy.

Export

Among the top 10 export destinations for the U.S., emerging economies include Mexico, Brazil, and Singapore, ranking 1st, 7th, and 10th respectively. While Mexico remained the largest export destination for U.S. fasteners, with its export reaching US$1.285 billion in the first eight months of 2025, representing a slight 5.77% decline compared to the same period in 2024. Brazil, however, showed strong performance, with the export in the first eight months of 2025 surging 20.02% year-on-year to US$106 million, ranking second among the top ten export destinations in growth rate (behind French 41.33%); exports to Singapore experienced a notable 15.17% decline in the first eight months of 2025, marking the largest decrease among the top ten export destinations.

Import

Among Canada's top 10 import sources, emerging economies include Vietnam and India, ranked seventh and eighth respectively. Vietnam's import value reached approximately US$28.5 million in the first eight months of 2025, a significant 22.81% increase compared to the same period in 2024. This growth rate was only second to France, which ranked 10th. India also saw notable double-digit growth, with the import in the first eight months of 2025 rising 13.71% year-on-year to approximately US$25 million.

Export

Among Canada's top 10 export destinations, emerging economies include Mexico, Singapore, Australia, and Brazil. The export to Mexico during the first eight months of 2025 saw a significant 22.41% decline compared to the same period in 2024, reaching US$13.61 million. This marks the secondlargest contraction among the top 10 export destinations and the only decline among the aforementioned four emerging economies; the export to Singapore reached US$3.73 million in the first eight months of 2025, marking a 15.43% increase compared to the same period in 2024; the exports to Australia increased by 58.19% to US$2.41 million in the first eight months of 2025, marking the highest growth rate among the top ten export destinations. The export to Brazil rose by 11.02% to US$2.35 million in the first eight months of 2025 compared to the same period in 2024.

Import

EU’s fastener imports also receive significant support from suppliers of emerging countries, including Turkey with its geographical advantage, as well as Vietnam, India, Thailand, and Malaysia in Asia. Turkey ranked as the EU's third-largest fastener import source, with the 2024 imports totaling 335,800 metric tons, a mere 4.31% decrease compared to the same period in 2023; Vietnam

Canada (Unit: US dollars / ranked

EU (In

INDUSTRY FOCUS

in 2024; imports from India plummeted 22.55% to 88,000 metric tons in 2024, marking the steepest decline among the top ten import sources; imports from Thailand also declined by 15.26% in 2024 to 60,000 tons, marking the second-largest decrease among the top 10 import sources; Malaysia's imports reached 24,000 tons in 2024, showing a slight increase of 1.25% compared to the same period in 2023.

Export

Among the EU's top 10 export destinations, emerging economies include Mexico, Turkey, Brazil, India, and Morocco. Mexico, the fourth-largest market, imported 40,000 metric tons from the EU in 2024, marking a slight 6.86% decrease compared to the same period in 2023; the export to Turkey was comparable to Mexico's, reaching 39,000 tons, a 3.27% decrease from the same period in 2023; Brazil showed the most impressive performance among the top 10 countries, with the export surging 15.04% to 31,400 tons in 2024 compared to 2023; India procured approximately 20,300 metric tons from the EU in 2024, a slight decrease of 1.32% compared to the same period in 2023. Morocco in North Africa is particularly noteworthy, as its 2024 procurement of fasteners from the EU not only reached 18,100 metric tons (approaching India's scale) but also recorded the second-highest growth rate among the top 10 countries (9.64%).

Japan (Ranked by weight of 2025 / data published through October 2025 / source: Ministry of Finance, Japan)

Import

Japan's fastener imports originated not only from China and Taiwan, but also significantly from emerging nations such as Vietnam, Thailand, Malaysia, and India. From January to October 2025, Japan imported 12,400 metric tons from Vietnam, a slight decrease of 3.20% compared to the same period in 2024; imports from Thailand, though only 3,500 metric tons, saw a substantial increase of 14.03% year-on-year; imports from Malaysia totaled 1,249 tons, a slight decrease of 1.81% compared to the same period in 2024; among the top ten import sources, India showed the strongest growth, surging by 92.42% year-onyear.

Export

Thailand, Indonesia, India, Mexico, Brazil, Malaysia, and Turkey were among Japan's top 10 export partners for fasteners. From January to October 2025, fastener exports to Thailand totaled approximately 27,700 metric tons, marking a slight 1.07% increase compared to the same period in 2024; the export to Indonesia reached 14,900 metric tons, showing a significant 10.23% decline; the export to India was comparable to Indonesia at 14,500 metric tons, down 2.79% year-on-year; the export to Mexico reached 13,800 tons, down 11.50% year-on-year; the export to Brazil totaled 9,129 tons in the first ten months of 2025, an increase of 6.11%, making it the best performer among emerging markets; the exports to Malaysia amounted to approximately 5,855 tons, a slight decrease of 3.73% compared to the same period in 2024;

Turkey recorded the steepest year-on-year decline among the aforementioned emerging markets, falling 18.29% to 4,053 tons in the first ten months of 2025.

Taiwan (Ranked by weight in 2025 / data published through October 2025 / source: Taiwan's Bureau of Foreign Trade)

Import

Although Taiwan is a fastener export-oriented country, it also imports certain fasteners. Among emerging import sources are Vietnam, the Philippines, Malaysia, and Thailand. Vietnam, the thirdlargest source, reached 969 metric tons in the first ten months of 2025, a 32.67% decrease compared to the same period in 2024; the import from the Philippines totaled 436 metric tons during the same period, down 15.58% year-on-year; the import from Malaysia reached 307 tons in the first ten months of 2025, a decrease of 19.37% compared to the same period in 2024. Thailand saw the most significant year-on-year decline among all emerging countries, decreasing by 49.34% compared to the same period in 2024.

Export

Among Taiwan's top 10 export destinations, only Mexico is an emerging economy. From January to October 2025, Taiwan's exports of fasteners to Mexico reached 25,400 metric tons, a 9.25% decrease compared to the same period in 2024. This represents the second-largest decline among its top 10 export destinations.

Conclusions

The global fastener supply and demand industry chain maintains close cooperative relationships. Many developed countries, responding to high domestic manufacturing and labor costs, increasingly shift procurement orders to emerging-market supply chains capable of producing competitively priced products while meeting their technical standards and after-sales service requirements. This trend has inadvertently fostered the gradual growth and development of fastener suppliers in these emerging economies. Although the demand for fasteners in advanced economies like Europe, the U.S., and Japan is still largely met by manufacturers from China and Taiwan, emerging players from Southeast Asia, Latin America, and Turkey with support from local government policies and through collaborations with clients to acquire more technical expertise and experience have been gaining traction in recent years, making them successfully penetrate the industrial supply chains of Europe, the U.S., and Japan and capture a significant share of the market. Many manufacturers in Europe, the U.S., and Japan are also attempting to diversify their procurement sources to mitigate risks amid pressures from geopolitical tensions, import tariffs, and regulatory changes.

In terms of exports, a significant portion of exports from Europe, the U.S., and Japan is also destined for emerging economies, indicating that the demand for mid-to-high-end fasteners is also growing in these markets, which may be attributed to either the needs of overseas factories established by European, U.S. and Japanese companies in emerging economies or the increased focus of emerging economies on developing mid-to-high-end industries. However, while Taiwanese fastener manufacturers are striving to enter the mid-to-high-end market segment, their primary export partners remain predominantly European and American countries based on the data. This indicates that there is still room for improvement in developing emerging markets.

Copyright owned by Fastener World / Article by Gang Hao Chang, Vice Editor-in-Chief

“Government Policies Support”

“Collaborations with Clients”

Guatemala

Introduction

Guatemala is not a headline fastener market in the way Mexico or Brazil is, but it is quietly attractive for suppliers and investors who know how to win in mid-sized, import-dependent, project-driven economies. Demand is anchored in construction and infrastructure, industrial maintenance, light manufacturing, and the constant need for reliable MRO supply across logistics, utilities, and commercial facilities. What makes Guatemala interesting is not just consumption. It is the combination of importled supply, fragmented distribution, and predictable demand categories where a focused player can build share without needing large local production from day one.

Macro and Investment Context That Matters to Fasteners

Guatemala’s growth profile has been relatively steady, which matters more to fasteners than headline growth numbers. Stability supports continuous building activity, ongoing facility expansion, and steady maintenance spend rather than boom-bust cycles. From a fastener perspective, that translates into recurring orders for general-purpose bolts and screws, anchors and fixing systems, washers, and MRO replenishment lines.

Infrastructure is also a direct demand multiplier. Road rehabilitation and upgrading programs are fastener-intensive through guardrails, signage, drainage systems, bridge works,

temporary works, and contractor maintenance cycles. Even when fasteners are not the largest bill-of-material item, they are embedded across installation and repair tasks.

Nearshoring adds another layer. Guatemala has positioned itself as a complementary Central American destination for selected manufacturing investments. The practical impact for the fastener industry is less about one plant opening and more about the lifecycle demand that follows: construction, equipment installation, then long-run MRO.

What Trade Data Says About Guatemala’s Fastener Supply Base

Trade data confirms that Guatemala’s fastener market is fundamentally import-led. Domestic production exists, but it is limited in scale and largely concentrated on basic hardware and small-batch fabrication. It does not materially offset demand generated by construction, infrastructure works, industrial maintenance, or commercial facilities. As a result, competitive advantage in the Guatemalan fastener market is shaped primarily by import sourcing strategies, inventory positioning, and downstream distribution reach, rather than by local manufacturing capacity.

Copyright owned by Fastener World / Article by Shervin Shahidi Hamedani

INDUSTRY FOCUS

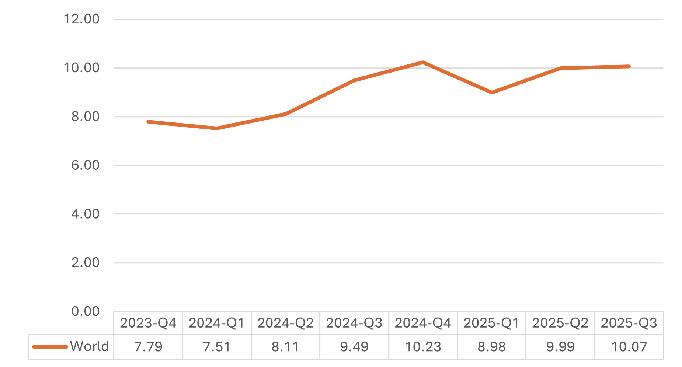

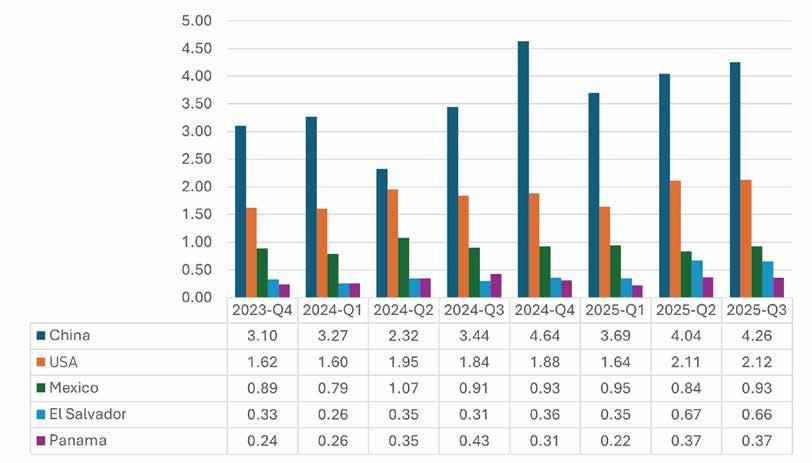

▼ Chart 1. Quarterly Import Values (Million USD) to Guatemala from the World

Chart 2 shows quarterly import values (million USD) to Guatemala from the five largest exporting countries, China, the United States, Mexico, El Salvador, and Panama, from 2024-Q1 to 2025-Q3. China consistently accounts for the largest share of imports and absorbs most incremental demand as the market expands. Its quarterly import values range from USD 2.32 million to USD 4.64 million, representing roughly 40-45 percent of total imports in most quarters and reaching about 45 percent in 2024Q4. This confirms China’s role as the reference supplier for standard, price-sensitive fasteners and the primary source used by distributors to reset inventory when volumes rise.

The United States plays a more stable, specificationdriven role. US imports generally remain between USD 1.60 million and USD 2.12 million per quarter, with less volatility than China. This pattern aligns with demand from industrial facilities, infrastructure projects, and MRO applications where reliability, documentation, and standards compliance matter more than unit price.

Chart 1 shows quarterly import values (million USD) to Guatemala from the global market (“World”) from 2024-Q1 to 2025-Q3. Imports increased steadily through 2024, rising from USD 7.51 million in 2024Q1 to a peak of USD 10.23 million in 2024-Q4. In 2025, imports eased temporarily to USD 8.98 million in Q1, before rebounding to USD 10.07 million by Q3. This pattern indicates a structural shift toward a higher and more stable import baseline rather than a one-off surge driven by short-term stocking.

▼ Chart 2. Quarterly Import Values (Million USD) to Guatemala from the 5 Largest Exporting Countries

Mexico functions as a practical regional supplier, with quarterly imports typically in the USD 0.84-1.07 million range. Its importance lies less in cost leadership and more in logistics efficiency, including shorter lead times, mixed shipments, and predictable replenishment cycles for distributors and contractors.

El Salvador stood out as the most notable mover in 2025. Imports from El Salvador rose sharply to around USD 0.67 million in 2025-Q2 and USD 0.66 million in 2025-Q3, roughly doubling its earlier quarterly range. This shift highlights the growing importance of regional suppliers when speed and responsiveness become critical, particularly in periods of tight project schedules or inventory pressure.

Panama remains a smaller but recurring supplier, consistent with a regional logistics and redistribution role. Its imports peaked at USD 0.43 million in 2024-Q3 and returned to about USD 0.37 million in 2025-Q2 and Q3, reinforcing the role of Central American trade hubs in supporting regional fastener supply chains.

Exports in Context

In contrast, Guatemala’s fastener exports remained modest and regionally concentrated. Total exports to the world typically ranged between USD 0.24 million and USD 0.39 million per quarter, a small fraction of import volumes. The majority of exports were directed to neighbouring Central American markets. El Salvador was consistently the largest destination, with quarterly exports commonly around USD 0.14-0.18 million, followed by Honduras at approximately USD 0.06-0.11 million, and Nicaragua at lower levels, often below USD 0.04 million per quarter. These figures suggest that exports are driven by regional redistribution and limited cross-border demand, rather than by Guatemala functioning as a production or export hub.

The imbalance between imports and exports reinforces a clear conclusion for suppliers and investors: Guatemala is primarily a consumption and distribution market for fasteners. The most attractive opportunities therefore lie in import optimization, local and regional warehousing, inventory reliability, and channel execution, rather than in export-oriented manufacturing strategies.

Where Demand Comes From: Key Opportunity Zones

Guatemala’s fastener demand is generated across several stable and recurring use cases rather than a single dominant sector. Construction remains the largest volume driver, supported by urban development, commercial buildings, and housing repairs. Demand in this channel centers on fast-moving items such as wood screws, anchors, general-purpose bolts, and washers, where availability, correct sizing, and practical packaging outweigh brand considerations.

Infrastructure and road works contribute a second layer of demand. Fasteners are embedded throughout guardrails, signage, drainage systems, bridge maintenance, and temporary works. Although rarely a headline cost item, fasteners are operationally critical, creating opportunities for suppliers that can deliver reliably and support contractors across project phases.

Industrial maintenance, repair, and operations represents a smaller but higher-value segment. Utilities, logistics facilities, food processing plants, and light manufacturing sites require consistent replacement supply to avoid downtime. In this segment, correct specifications, fast response, and inventory reliability matter more than the lowest unit price. Nearshoringrelated industrial parks add incremental demand. Even modest manufacturing investments generate fastener requirements across construction, equipment installation, and ongoing maintenance, often with higher standards and reliability expectations.

Overall, Guatemala’s demand is steady, fragmented, and execution-driven, favoring suppliers that align inventory and logistics closely with end-user needs.

Competitive Landscape and Strategic Implications

Competition in Guatemala’s fastener market reflects its import-led structure. Asian suppliers, led by China, dominate commodity fasteners and set reference pricing for standard items. Regional suppliers, particularly from Mexico and Central America, compete on speed, flexibility, and mixed shipments, which are critical when lead time matters. US and selected European suppliers focus on specification-driven demand in industrial and infrastructure applications. The most effective market strategies combine these approaches. Cost-efficient sourcing for core volumes, regional supply for responsiveness, and selective higher-spec offerings for industrial customers tend to outperform single-origin or price-only models.

What Investors and Suppliers Should Watch

Guatemala is best viewed as a consumption and distribution market, not a manufacturing or export hub. Trade data shows imports operating at a higher and more stable level since late 2024, with China anchoring volume supply and regional suppliers gaining importance where responsiveness is critical. The most attractive opportunities lie in import optimization, local and regional warehousing, inventory discipline, and strong distributor relationships. In Guatemala, suppliers that reduce friction for buyers through availability and reliability are more likely to build durable market positions than those competing solely on price.

GLOBAL FOOTPRINTS in 2025

International Fastener Expo 2025 09/16-17

Mandalay Bay Convention Center

Fastener Fair USA 2025 05/28-29

Music City Center

Fastener Fair Global 2025 03/25-27

Messe Stuttgart

Fastener Poland 2025 10/15-16

Expo Krakow

METALCON 2025 10/21-23

Las Vegas Convention Center

Egypt Projects 2025 09/06-08

Egypt International Exhibition Center

SteelFab 2025 01/13-16

Expo Centre Sharjah

IFS China 2025 05/22-24

Shanghai World Expo Exhibition & Convention Center (SWEECC)

Fastener Trade Show Suzhou & NEV Parts Exhibition 2025 10/22-24

Suzhou International Expo Center

Manufacturing Expo 2025 06/18-21 BITEC

Fastener Expo Shanghai 2025 06/17-19

National Exhibition and Convention Center (Shanghai)

Korea Metal Week 2025 10/29-31

KINTEX Exhibition Hall

Vietnam Hardware & Hand Tools Expo 2025 12/04-06

Saigon Exhibition and Convention Center (SECC)

Manufacturing World Japan 2025 07/09-11

Makuhari Messe

Fastener Fair India 2025 05/08-10

Exhibition Centre

TiTE x IHT 2025 10/21-23

Taichung International Convention & Exhibition Center METALEX 2025 11/19-22

MTA Vietnam 2025 07/02-05

Fastener and Fixing

Vietnam 2025 08/06-08

VEC Hanoi

Saigon Exhibition and Convention Center (SECC)

▶ Fastener Expo Frankfurt 2026

2026德國法蘭克福緊固件專業展

03/23-25

Messe Frankfurt