Make ever y epic writing journey a cosy one Hobbiton handcraft from the makers of the world’s most magical pens.

Nestled by the coast of Lusail sits the splendor of Raf es and Fairmont Doha, where luxury is rooted in even the smallest details. Open the doors to mesmerizing hospitality and make memories in a world of sophistication.

BOLD FOR THE BOLD

↑ María Paula Rodríguez, Senior Business Innovation Manager at Luker Chocolate

BUSINESS UNUSUAL

40 2026 will be the year of ‘Quiet Climate’ What does that mean for founders?

42 Tony Matharu: Planting Trees for the LongTerm Insights from the city guide his longterm vision

56 Building a Business Case for Decarbonisation

Action

STARTUP SPOTLIGHT

60 Chipping in for the Planet CHIPX rethinks tech for lower impact 63 Start-ups are already building Britain’s green future The country must catch up

Prosperity or the planet?

48 Net Zero Britain Ambition meets delivery

52 Governance is the New Green Environmentally driven businesses can lead markets 54 The Cost of Exclusion Why ignoring racial equality hurts the bottom line

FEATURES EDITOR Patricia Cullen patricia.cullen@bncb2b.com

CEO Wissam Younane wissam@bncpublishing.net

MANAGING DIRECTOR Rabih Najm rabih@bncpublishing.net

ART DIRECTOR Simona El Khoury

EDITORIAL TEAM Tamara Pupic, Aalia Mehreen Ahmed

MEDIA SALES MANAGER Olha Kovalova olha.kovalova@bncb2b.com

GENERAL MANAGER Daniel Malins daniel@bncb2b.com

REGIONAL DIRECTOR Andy B. andy@bncb2b.com

CONTRIBUTING EDITOR Omar Hamdi

CONTRIBUTING WRITERS

Alice Veldtman, Juliette Devillard, Charlotte Keenan, Dr Marcelle Moncrieffe-Newman, Sam Stark, Goutam Challagalla, Frederic Dalsace, Pip Wilkins and James Mesina SUBSCRIBE

Contact subscriptions@bncb2b.com to receive Entrepreneur United Kingdom every issue. COMMERCIAL ENQUIRIES sales@bncb2b.com

Access fresh content daily on our website

RETHINKING BUSINESS, TECHNOLOGY, AND A GREEN ECONOMY

Entrepreneur United Kingdom

Welcome to the February issue of Entrepreneur UK magazine, which asks how business and technology are changing not just what we do, but how we see and understand the world around us.

Through a New Lens, our cover story, takes that question literally. XPANCEO is a deep-tech company developing an invisible, weightless smart contact lens as the next generation of computing and interface between humans and technology. We trace the work of founders Roman Axelrod and Dr. Valentyn Volkov, who are not merely innovating, but shaping how humans experience and connect with technology. That same spirit of rethinking runs through the rest of this issue. The green economy is no longer abstract; it is a

practical, urgent concern for business and policy alike. This edition examines how companies can take tangible, responsible actions to address environmental challenges.

The analysis of Unilever’s sustainability strategy shows how even well-intentioned approaches can falter under organisational complexity and market pressures, offering lessons for leaders seeking to embed environmental responsibility at the core of decision-making.

Entrepreneur UK talks to Tony Matharu, founder of Integrity International Group and Blue Orchid Hotels, whose hotel developments and initiatives like Here to Help London show that business success and civic responsibility can grow together. Additionally, Hannah Gilbert, director of sustainability at the British Business Bank, emphasises the role of finance in scaling innovation and enabling smaller firms to participate meaningfully in the net zero transition. In her feature, Charlotte Keenan, global head of corporate engagement at Goldman Sachs, shows how small businesses are thriving despite economic challenges and offers strategies readers can apply to grow their own. Across founders, financiers and sustainability leaders, the stories in this issue make a clear point: decarbonisation is not a symbolic gesture but a structural, strategic imperative.

Taken together, the features in this month’s issue ask readers to look beyond conventional measures of progress, showing that innovation isn’t simply about new tools - it’s about new ways of seeing, acting, and challenging the rules we’ve long accepted.

Thanks for reading.

Patricia Cullen Features Editor, Entrepreneur United Kingdom

REGISTRATION IS NOW LIVE

LENS THROUGH A NEW

XPANCEO’s bold vision for the future

by PATRICIA CULLEN

XPANCEO forward: Founders Roman Axelrod and Dr Valentyn Volkov

→ Smart Contact

prototype

As technology advances at an unprecedented rate, few companies are on the verge of reshaping daily life as radically as XPANCEO. Founded in 2021 by entrepreneur Roman Axelrod and scientist Dr. Valentyn Volkov, this Dubai-based deep-tech firm is breaking new ground in human-technology interaction. XPANCEO is developing a smart contact lens for AI-powered XR computing — delivering visuals directly to the retina, without screens, frames, or headsets. With capabilities like XR vision, real-time health monitoring, colour correction, and next-gen biometric verification, this invisible lens could redefine content consumption, social media, industrial applications, sports, and healthcare.

EXPANSION IS WHAT DRIVES ME. EXPANSION OF HUMAN CAPABILITIES, PERCEPTION, INTELLIGENCE, AND PRESENCE IN THE UNIVERSE. THIS IDEA BECAME SO CENTRAL THAT MY WIFE CAME UP WITH THE PORTMANTEAU

The genesis of XPANCEO

The concept behind XPANCEO was born from an unexpected moment of reflection. Axelrod, in the final stages of selling his previous company, found himself at a crossroads. “I finally had the space to think about the mission of my life, and I formulated it as exploring the unknown,” he said, “like the moment in a computer game when you step into an unexplored grey area on the map and realise that there are no hints, no instructions, and no guarantees. You either move forward and open something new, or you stay where you are.” Axelrod decided on the former. This period of introspection led to a realisation: human potential could be expanded by connecting people with an intuitive, ever-present cognitive layer - deeply embedded in daily life - that acts as a personal assistant always at hand. “AI wasn’t much back then, but I was sure, intuitive, omnipresent assistance would come. The question was: where should it live?” Axelrod’s worldview is deeply influenced by transhu-

manism. He sees the fusion of humans and technology as inevitable - it’s the next evolutionary step for both civilization and computing. The outcome, greater than the sum of its parts, will be a new kind of human - capable of truly controlling AI and using it for good. The form it takes, however, remains a choice.

“Expansion is what drives me”, says Axelrod. “Expansion of human capabilities, perception, intelligence, and presence in the universe. This idea became so central that my wife came up with the portmanteau “XPANCEO.” I felt such a strong connection to it that it became my Instagram handle. And the funniest thing. When we decided to start the project, we needed a name for a pitch deck. We tried to come up with something new, but nothing felt right or truthful. Eventually, we decided to simply use my username.”

Axelrod believes technology should enhance, not hinder, the human experience. “The current generation of gadgets does not fit that future,” he says. “Phones, laptops and tablets pull our attention away from reality, harm our health, and deteriorate the quality of everyday life. More importantly, they are fundamentally unsuitable for humanity’s long-term goals. You cannot explore Mars, build complex off-planet systems, live longer, healthier lives, or coexist with advanced intelligence while relying on devices designed for scrolling and tapping,” he adds. This led him to see the human eye as the perfect interface for a new habitat for intelligence. A moment of

WE’VE BEEN RECOGNISED BY NATURE INDEX AS ONE OF THE TOP THREE START-UPS GLOBALLY IN PHYSICS, BUILT 26 FUNCTIONAL PROTOTYPES, AND FILED 19 PATENT-PENDING APPLICATIONS. THIS LEVEL OF DEMONSTRATED PROGRESS SENDS A CLEAR SIGNAL TO INVESTORS”

inspiration - a Pinterest image of a woman astronaut with unusually vivid eyes - convinced him that vision was the most authentic and intuitive place to start.

It was at this juncture that XPANCEO was born. However, creating a smart contact lens - a device capable of embedding technology into the human body - was not just an act of innovation; it was a technical challenge that required unprecedented breakthroughs in materials science, biotechnology, and AI systems. For this,

Axelrod needed to find a partner who could turn the vision into reality.

The Scientific Challenge

Enter Dr. Valentyn Volkov, a physicist with extensive experience in advanced materials science and nano-optics.

Volkov had spent more than 20 years working in some of the most prestigious research laboratories in Europe, leading high-level scientific teams focused on novel materials. Initially, Volkov was reluctant to leave academia and join a start-up. However, after

several discussions with Axelrod, Volkov recognised the enormity of the challenge and the potential impact the smart contact lens could have on society.

“When Axelrod first approached me with the idea, I didn’t say yes immediately. But at some point my impression shifted from he might be crazy to he definitely has an unusual idea,” Volkov says. The more they discussed it, the more the partners realised that this wasn’t just about creating a product - it was about advancing fundamental science

and tackling problems no one had even imagined. The collaboration between Axelrod and Volkov set the stage for XPANCEO to begin its journey of deep-tech development. The first task was to build the first prototype of the smart contact lens - no small feat, given the numerous scientific and engineering hurdles involved. Traditional electronics and displays couldn’t fit into such a tiny, flexible form factor, so the team had to look beyond existing solutions.

“Our journey began by breaking the problem down to its fundamental principles,” says Volkov. “Instead of following existing solutions,

→ XPANCEO Laboratory

→ Dr Valentyn Volkov, founder and CTO of XPANCEO

we engineered the lens from scratch, grounded in core physics and materials science. The first challenge was to develop flexible electronics that could be both thin and transparent. At the same time we needed to rethink how optics, biosensing, and data processing could be embedded into something as small and delicate as a contact lens.”

Over the years, XPANCEO developed cutting-edge technologies, including quasi-2D materials for transparent conductors, micro-optical projection systems, and biosensing technologies capable of tracking health data through the wearer’s tears. The result is 26 prototypes that demonstrate visual AR interface, wireless data and power transfer, several approaches for detection of vital biomarkers such as glucose, for diabetes patients and others requiring continuous blood sugar monitoring, IOP (Intra-Ocular Pressure) for glaucoma treatment and prevention, and vision enhancement such as color correction for those with color blindness. This research does not come cheap. “We had to prove to the

“XPANCEO CHANGES THE WAY PEOPLE RELATE TO TECHNOLOGY AT A VERY FUNDAMENTAL LEVEL”

world that what we’re building is not only possible but will inevitably change the world,” the partners emphasise. “Not just as a concept, but as something investors could believe in, something that could be funded and built at scale. And it worked. First, we raised $40m, then 250m at a $1.35bn valuation.” Volkov says the funding doesn’t alter the company’s roadmap but instead reinforces it, noting that key prototypes for most planned features are already in place. “What the funding does is remove friction. We managed to expand our team with Nobel-class scientists and engineers, bringing new state-of-the-art equipment, growing our capabilities,” he says. Their lab team has already doubled. The funding will allow them to conduct the necessary human and medical trials. “This is all on the timeline we’d mapped out from the beginning,” he adds

XPANCEO’s rapid rise in the deep-tech landscape has been underscored by successful funding rounds. “Our recent funding is the largest Series A round in the MENA region across all industries, and worldwide in AR/VR/XR and wearables. But most importantly, it shows tangible progress” highlights Axelrod. “We’ve been recognised by Nature Index as one of the top three start-ups globally in physics, built 26 functional prototypes, and filed 19 patent-pending applications. This level of demonstrated progress sends a clear signal to investors. When they see a team that’s not just ambitious but actually delivering at this pace, capital follows.”

This valuation places XPANCEO among the ranks of highly coveted unicorns, companies that have attracted significant investor confidence despite the long development timelines and technical risks that characterise deep-tech ventures. But for Axelrod and Volkov, the funding isn’t just a validation of their vision - it’s a tool that removes

→ XPANCEO Laboratory

friction from their development roadmap. The investment has allowed them to expand their R&D teams, accelerate development, and scale their laboratory capabilities, moving closer to their ultimate goal. “By the end of 2026, we aim to integrate everything we’re working on into a single prototype, showcasing the range of main features: image projection, health monitoring, and wireless power. That was always the plan,” the founders say.

A Paradigm Shift in Human-Technology Interaction

The implications of XPANCEO’s smart contact

phones, laptops, and wearables. However, we still interact with this intelligence through screens, keyboards, and headsets, which disrupt our connection to the real world. “Today, technology constantly asks for our attention. We look down at screens, switch between devices, and mentally separate the digital world from the real one. Over time, this creates friction, distraction, and cognitive overload. Our goal is to

technology to consumer markets, XPANCEO has been strategic in first testing the lens in high-stakes B2B environments, such as aerospace, healthcare, and industrial sectors. These demanding fields provide an ideal proving ground for the lens’s capabilities.

Market Applications

The real-world applications for the smart contact lens are wide-ranging. By being placed directly on the eye, it ensures a wider, unobstruct-

lens extend far beyond the realm of personal convenience. While other companies are working to bring AR to market through smart glasses or headsets, XPANCEO is pushing the envelope by developing a technology that is fundamentally invisible, ambient, and non-invasive. “XPANCEO changes the way people relate to technology at a very fundamental level,” Axelrod explains. In the 20th century, computers were standalone devices, containing all their processing power and connecting externally only for specific tasks. By the 21st century, computing evolved into a cloud-based ecosystem, accessed via

remove that friction.”

At the heart of XPANCEO’s philosophy is a shift in the human-technology interactions. The company believes that true human-AI symbiosis can only be achieved when technology is seamlessly integrated into the human body and our daily experiences. While the ultimate goal is to bring this

ed experience - ideal for piloting vehicles, highspeed movement, sport performance, space, and aviation. In healthcare, the lens could become nextgeneration personal lab and hospital located directly on the cornea, shifting from episodic doctor visits to continuous monitoring of glucose, intraocular

→ Roman Axelrod, founder and managing partner of XPANCEO

→ Dr Valentyn Volkov, founder and CTO of XPANCEO

BY THE END OF 2026, WE AIM TO INTEGRATE EVERYTHING WE’RE WORKING ON INTO A SINGLE PROTOTYPE, SHOWCASING THE RANGE OF MAIN FEATURES: IMAGE

PROJECTION, HEALTH MONITORING, AND WIRELESS POWER”

pressure, and other biomarkers in tear fluid, while dispensing medications in precise doses and delivering AR-guided medical instructions in real time. But the optical system can be used not only in lenses, but also in the implant for vision restoration that XPANCEO has developed together with Intra-Ker, which uses similar technology of image projection that are used in our contact lenses.

“Our prototype addresses corneal blindness by bypassing damaged or opaque corneas entirely,” Valentyn says. “Our implant uses the same microdisplay technology we’re exploring for the smart contact lenses, but this time embedded in place of the damaged cornea, delivering visual information directly to the retina. We’ve already tested a proof of concept in a donor human eye, and it successfully delivered sharp visual content to the retina.”

Space is the ultimate test for any technology. If it works there, it can work anywhere. In aerospace, the

smart contact lens could revolutionise the way astronauts interact with their environment. Today, astronauts rely on bulky systems to access mission-critical data. XPANCEO’s technology would provide a hands-free, AR interface, allowing astronauts to access real-time data without compromising their focus on the task at hand. “We’ve developed a projection system prototype integrated into a real spacesuit, aligned with our collaboration with the Mohammed Bin Rashid Space Centre in the UAE,” the founders explain. “These developments push the limits of human interfaces in the most demanding environments imaginable.”

The potential for other environments - from elite sports to industrial applications - also looms large. In these fields, the ability to provide real-time, unobtrusive data to users who cannot afford distractions is invaluable. For instance, a surgeon could wear the smart lens during an operation to access critical data

without taking their hands off the tools, while a pilot could benefit from enhanced navigation assistance during high-speed flights in low-visibility conditions.

Future focus

With its clear vision and cutting-edge technology, XPANCEO is on the cusp of a major paradigm shift. Looking to the future, Axelrod says they are focused on refining the smart contact lenses for use in a variety of real-life scenarios, building on the B2B collaborations they’ve already been testing across different sectors.

“Success in those applications will prove that society is ready for smart contact lenses to be used in real life,” he adds. The world may still be several years away from fully embracing smart contact lenses as the primary interface for AI-powered XR, but XPANCEO’s commitment to pushing the boundaries of human-machine integration positions it as a pioneer in the next wave of computing.

In the Loop /

BUILDING THE GREEN FUTURE

Inside the Minds of Sustainability Entrepreneurs

by PATRICIA CULLEN

Across industries and continents, sustainability has moved from optional virtue signaling to an urgent business imperative. Yet as companies chase green credentials, the path from innovation to real-world impact is rarely straightforward. Five leaders, each tackling environmental challenges from cocoa farms in Colombia to the skies above, from skincare jars in the UK to off-grid Himalayan schools, reveal what it truly takes to transform ideas into systems, impact, and jobs—and the barriers that still hinder meaningful change.

TURNING WASTE INTO VALUE

In the sun-baked cocoa fields of Colombia, the majority of the fruit -the pods, pulp, and husks - is discarded. For many, this is a byproduct of inefficiency. For London based María Paula Rodríguez, Senior Business Innovation Manager at Luker Chocolate, a Colombian B Corp chocolate manufacturer, it is an opportunity. “Turning a significant industry waste issue - the 81.7% of the cocoa pod that is usually wastedinto economic and environmental value,” she says, is the core of her work.

At Luker, a B Corp producing cocoa for some of the world’s leading chocolate brands,

Rodríguez has overseen the transformation of this waste into ingredients for the food and beverage sector. “This came from sustained R&D, pilot testing at one of our own farms, and working with partners beyond the chocolate sector - and it’s now in the market thanks to the creativity of a number of clients.”

Her approach embodies a principle that resonates across sectors: sustainability cannot be an afterthought. “Sustainability is something you always design into the system, not something you add on later,” she asserts.

Beyond the chocolate factory, her ambition is systemic: “A real shift would be farmers benefiting from more of what

Senior Business

→ María Paula Rodríguez,

Innovation Manager at Luker Chocolate

→ Andrew Symes, CEO of OXCCU

The players I respect most in this space are converging on the same playbook: electrify what you can, generate clean power on-site where it reduces risk and cost, and instrument everything so performance is visible and financeable”

they grow, so that cocoa remains a viable livelihood despite mounting climate and economic pressure.” By finding ways to use the whole cocoa fruit, Rodríguez is helping create models where economic and environmental benefits are more evenly shared, while consumers gain the ability to choose products reflecting sustainable practices, not just taste.

Aviation’s Green Horizon

From the fields of Colombia to the high skies, Andrew Symes, CEO of OXCCU, a University of Oxford spin-out developing scalable sustainable aviation fuel, is tackling a different challenge: the carbon footprint of aviation. “The most meaningful impact has been taking years of academic research and progressing it into a technology that can be tested and validated beyond the lab,” he explains. OXCCU is developing sustainable aviation fuel (SAF) from waste carbon. The OX1

demonstration plant has already generated operating data for the larger OX2 facility, set to produce fuel for further testing this year. Symes emphasises that aviation decarbonisation depends on scalable, credible solutions. “Each stage of development is grounded in evidence and can support the next step towards commercial deployment,” he says. Transparency, he notes, is key: “Being open about both progress and remaining challenges builds trust, and that trust allows partners, investors and policymakers to get behind the technology and move it forward.”

His vision for the next decade is ambitious: “I would like to see sustainable aviation fuel treated as essential infrastructure rather than a constrained alternative.” He welcomes regulatory expansion into pathways such as power-to-liquids and gasification, which promise greater resource availability. For Symes, the lesson is clear: systemic, evidence-driven

In the Loop /

innovation, coupled with long-term regulatory support, is what distinguishes temporary trends from transformative outcomes.

Rethinking Beauty: Education and Sustainability in Skincare

While Symes focuses on the skies, Julie Macken is revolutionising what people put on their faces. In an industry dominated by over-formulation and marketing hype, Macken, founder of Neve’s Bees, a natural skincare brand, advocates for simplicity and education. “Most skincare products are around 80% water, plus processing chemicals used to keep that water stable. Water isn’t a moisturiser -it evaporatesand many of the added emulsifiers, preservatives and stabilisers can actually disrupt the skin barrier,” she says. Her innovation lies in concentrated, waterless formulations that treat skin as a living organ. “The most meaningful impact of my work has been educating

people about waterless skincare and redefining what healthy skin really is,” Macken explains. By promoting barrier health and simpler routines, she reduces both environmental waste and unrealistic beauty pressures.

away from over-formulation, unrealistic beauty standards, and misleading marketing toward skin literacy and thoughtful product design. For Macken, sustainable entrepreneurship is inseparable from consumer empowerment.

highlights systemic failures in the UK’s approach to decarbonising buildings. “We are actively investing in infrastructure that produces vast amounts of usable waste heat, especially data centres. Failing to connect that heat to homes and communities

Everything she does starts with education: “If people understand why something works -and why it mattersthey make better choices without needing to be persuaded.” Over the next decade, she hopes the industry will mirror the scrutiny applied to ultraprocessed food, moving

Heating Homes with Waste Heat: The Long Game for Net Zero

Back on the ground, Simon Kerr, Head of Heat Networks at EnergiRaven, an energy management company and platform focused on helping organisations monitor, analyse, and optimise energy use,

is a missed opportunity,” he warns. The UK’s Future Homes Standard, once a potential turning point for green housing, has been diluted, and even small measures like mandated batteries risk rollback. Heating buildings remains the UK’s largest single source of carbon emissions,

↑ Julie Macken, founder of Neve’s Bees

→ Nick Spicer, CEO of Your Eco

If people understand why something works -and why it matters - they make better choices without needing to be persuaded”

yet massive investments in data centres and industry could provide abundant usable waste heat. Kerr argues for treating heat as core infrastructure: “A Net Zero built environment would look like homes and neighbourhoods heated by clean, locally sourced heat.

→ Simon Kerr, Head of Heat Networks at EnergiRaven

Gas boilers would increasingly disappear, replaced by Heat Interface Units connected to publicly owned heat networks.”

Crucially, financing must be patient and long-term. “Small, fragmented projects struggle to attract serious capital, whereas large, coordinated schemes can unlock institutional investment and deliver impact at pace,” Kerr explains. For him, the challenge is less technological than systemic: aligning finance, regulation, and planning to ensure that climate-positive projects are investable and scalable.

Power to the People

Nick Spicer, CEO of Your Eco, a renewable energy company, extends this focus on systemic solutions into humanitarian terrain. In the Himalayas, he reconnected a school cut off after an earthquake; in the Caribbean, he supported an off-grid media centre,

opened by Richard Branson. “The most meaningful impact has been using clean infrastructure to restore capability and dignity where energy access is the difference between opportunity and isolation,” he reflects.

For Spicer, sustainability scales only when treated as core infrastructure. “The players I respect most in this space are converging on the same playbook: electrify what you can, generate clean power on-site where it reduces risk and cost, and instrument everything so performance is visible and financeable.” His vision extends beyond individual projects: smarter grids, integrated design, and robust delivery frameworks could generate thousands of skilled green jobs while reducing global emissions.

A Pattern Emerges: Systems, Patience, and Scale

Across these diverse sectors, a pattern emerges. Innovation alone is insufficient. Real change demands:

} Integration: Sustainability must be designed into systems, whether a chocolate supply chain, an aviation fuel process, or a heating network.

} Evidence and Transparency: Symes’ SAF plant and Rodríguez’s cocoa upcycling are grounded in pilot data and R&D, building credibility that attracts investment.

} Patient Capital: Kerr’s heat networks and Spicer’s renewable projects highlight the need for long-term

financing rather than short-term gains.

} Education and Trust: Macken’s waterless skincare demonstrates that consumers and communities can be allies, not passive recipients, if equipped with understanding.

Yet obstacles persist. Policy inconsistency, regulatory fragmentation, short-term finance, and cultural inertia continue to slow adoption. Rodríguez notes that for cocoa farmers, climate and economic pressures threaten livelihoods; Kerr warns of diluted home-building standards; Spicer stresses that infrastructure projects fail without disciplined delivery and alignment. Even with clear solutions, translating ambition into action remains a struggle. For these entrepreneurs, sustainability is not a marketing slogan or a CSR checkbox - it is a framework for reshaping value, infrastructure, and opportunity. Across sectors - from upcycling cocoa waste to producing sustainable aviation fuel, from redesigning skincare to building resilient energy systems - the lesson is consistent: meaningful environmental change demands systems thinking, long-term commitment, and disciplined execution. In their hands, sustainability becomes more than a technical or commercial challenge; it is a blueprint for resilient economies, empowered communities, and a planet better equipped to face the decades ahead.

Middle Managers: The Unsung Heroes of the Net Zero Transition?

by ALICE VELDTMAN

Net zero commitments are now a common feature of business strategy. Across all sectors organisations are developing decarbonisation plans in response to investor expectations, regulatory pressure and other demands. In the UK, the consequences of climate change, particularly vulnerability to storms and flooding, pose a material risk to business. Conversely, cutting emissions is often motivated by opportunities to drive cost efficiencies and enhance brand reputation. Yet although net zero ambitions are widespread and the risks and opportunities are clear, achieving it is not easy. Whilst technology and data are important for measuring, reducing and reporting emissions, reaching net zero requires organisational change management, for which middle managers play an essential but often overlooked role.

Net zero: strategy is easy, execution is hard

Setting a net zero target is a strategic decision. Delivering it requires organisations to rethink how they manufacture products, manage supply chains, allocate capital and make every day operational decisions. Transformation at this scale aligns with the definition of change management, yet net zero is rarely cited as a reason for enacting strategic change programmes.

Classic strategic change models, emphasise the need to create urgency and mobilise leadership coalitions as a first two steps for driving successful

transition. However, research also warns that urgency alone can backfire if leadership teams lack the capacity or capability to guide change initiatives. This tension is especially felt when it comes to sustainability. Despite calls for urgent global action to mitigate the climate crisis within the business context, achieving net zero by 2050 may feel like a distant ‘nice to do’ versus commercial pressures prioritised in the shortterm.

However, with the net zero goals set, responsibility for “making it happen” typically falls to those tasked with translating strategy into action: middle managers.

Why middle managers matter more than most leaders realise

There is a wide body of research acknowledging the importance of middle managers for delivering strategic change. Positioned between top managers and frontline employees, middle managers occupy a central position to be able to make sense of change directed by senior managers Additionally, they are often more immersed in operational understanding allowing them to “sense give” on the implementation of change to wider employees.

Middle managers are central to:

}Making sense of strategic intent and translating new ideas

}Adapting messages to engage different audiences

on change

}Building informal networks that help mobilise support for change

}Informal knowledge sharing, which supports organisational learning

Much of this influence happens outside formal governance structures, through everyday decisions, peer-to-peer conversations and what some researchers describe as “water cooler learning”. This makes the contribution of middle managers both powerful and easy to overlook. When it comes to delivering sustainability targets research found conflicting rationales between profit and purpose goals can create challenges. Middle managers are often the ones required to reconcile these tensions in practice. One study found middle managers cope by mentally separating the individual requirements of commercial and social goals then integrate and sense-make, requiring emotional and behavioural capabilities.

Middle Managers can be powerful accelerators for achieving net zero

For entrepreneurs and business leaders serious about net zero, the opportunity is clear. Middle managers can play a powerful role in accelerating changes required to meet net zero goals, depending on how they are engaged and supported.

Research points to several practical priorities:

}Involve middle managers early in shaping strategic change required to reach net zero.

}Align incentives and performance measures to reduce conflicts between commercial and environmental goals.

}Invest in capability-building, through targeted recruitment, or training particularly in carbon management or climate literacy and change leadership.

}Create psychological safety allowing honest communication about capacity trade-offs and conflicting goals.

}Build broad guiding coalitions at all levels to mobilise change.

}Align ethical values to unite sensemaking across the business and help deliver non-profit goals.

By embedding sustainability into the organisation’s purpose, values and operating model, rather than treating it as an add-on, middle managers can be better equipped to help deliver change across the organisation.

The real opportunity in the net zero transition

Net zero will not be delivered through targets, dashboards or annual reports alone. It will be delivered, or not, through thousands of everyday decisions made across the organisation.

Middle managers sit at the point where ambition meets reality. They translate strategy into action, navigate competing

“For entrepreneurs and business leaders serious about net zero, the opportunity is clear. Middle managers can play a powerful role in accelerating changes required to meet net zero goals, depending on how they are engaged and supported ”

demands and shape how employees experience change. They are often the unsung heroes of transformation.

For leaders willing to recognise and invest in this role, the net zero transition is not just a compliance exercise, it is an opportunity to build more resilient, adaptive and future-ready organisations.

Alice Veldtman, Carbon Management Consultant,

Nottingham Business School, Nottingham Trent University.

In the Loop / Why Tech Show London Matters in the Age of Intelligent Scale

by JAMES MESINA

Technology leaders are operating in a moment of contradiction. Innovation is accelerating. AI is reshaping decision-making at speed. Expectations around performance, resilience, and sustainability continue to rise. At the same time, trust in systems, data, and the institutions that deploy them is under greater scrutiny than ever.

This is the context in which Tech Show London has become increasingly important. More than a technology exhibition, Tech Show London reflects the reality facing modern organisations. Progress today sits at the intersection of ambition and responsibility. Leaders are no longer asking what is possible. They are asking what is scalable, secure, and sustainable. Across cloud, data, cybersecurity, infrastructure, and DevOps, the challenges shaping enterprise strategy are converging. AI performance depends on resilient infrastructure. Digital trust relies on secure, sovereign systems. Data-driven insight requires governance that enables innovation rather than constraining it. These are not siloed issues. They demand joined-up thinking.

That is why Tech Show London’s approach extends beyond technology alone. Its 2026 programme brings together technical expertise with broader perspectives on power, ethics, and human impact. For senior leaders, this is what sets Tech Show London apart. It is a space to step back from day-to-day execution and engage with the wider forces shaping technology decisions. These include responsible AI, cyber resilience, infrastructure sustainability, and organisational culture. Performance still matters. ROI still matters. But organisations that will lead over the next decade are those that treat trust as a strategic asset. It is something built deliberately and protected as they scale.

Tech Show London exists to support that shift. Not by prescribing answers, but by creating the conditions for better conversations. Conversations that are informed, challenging, and grounded in real-world leadership. In an era where technology decisions shape business outcomes and societal impact alike, Tech Show London

“MORE THAN A TECHNOLOGY EXHIBITION, TECH SHOW LONDON REFLECTS THE REALITY FACING MODERN ORGANISATIONS”

is no longer just a date in the calendar. It is a moment of reflection and direction.

To find out more, visit https://www.techshowlondon.co.uk/

James Mesina is a Marketing Executive at Tech Show London, playing a key role in shaping campaigns that connect global technology leaders with innovative audiences. With a passion for digital marketing, events, and emerging tech, Mesina helps drive engagement and amplify the voice of one of the UK’s leading technology events.

→ Delegates at Tech Show London 2025

→ Tech Show London Highlights

→ Inside a previous Tech Show London event

GREEN GAINS

The billion-dollar business strategy of the future by ENTREPRENEUR UK STAFF

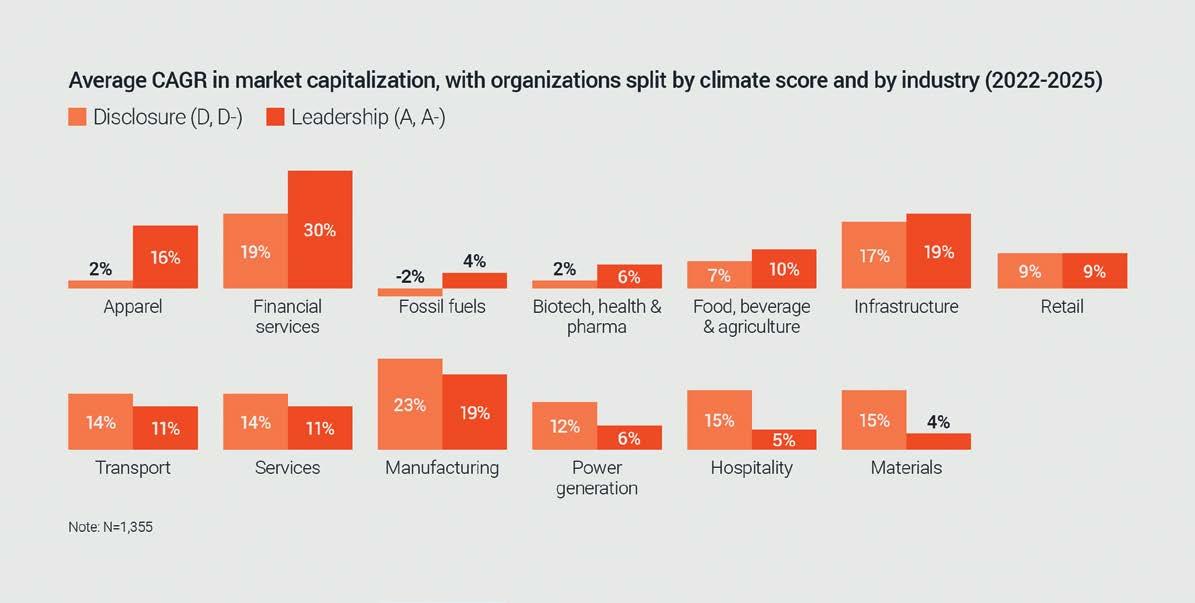

As geopolitical tensions escalate and economic uncertainty grips global markets, the role of environmental action in business strategy has evolved from an ethical consideration to a driver of resilience, capital allocation, and long-term competitiveness. The latest findings from the CDP Corporate Health Check 2026 reveal a compelling truth: companies that prioritise environmental leadership

aren’t just protecting the planetthey’re securing their financial futures. The study, conducted in partnership with Oliver Wyman, highlights how a select group of global companies is seizing the opportunity presented by environmental responsibility, unlocking a staggering US$218bn in financial value in just the past year. These leaders are cutting emissions at four times the rate of their peers, proving that the link between sustainability and profitability is no longer a theoretical ideal but a hard reality for businesses who understand the power of environmental stewardship.

A NEW WAVE OF ENVIRONMENTAL LEADERSHIP

The findings from CDP’s 2026 analysis indicate that just 15% of companies worldwide are now embracing environmental action as a core business strategy. This cohort is leading the charge on climate, water, and forest issues, setting an ambitious pace that is, in many cases, outpacing traditional financial metrics.

Companies in this group reduced their emissions at an average compound annual growth rate (CAGR) of 4%, compared to only 1% among those in the lower-performing category. This is a staggering difference in progress - one that speaks volumes about the long-term viability of aligning corporate performance with the planet’s wellbeing. Sherry Madera, CEO

→ CDP's CEO, SHERRY MADERA

of CDP, aptly puts it: “Climate and nature loss are no longer distant risks - they are already reshaping markets, supply chains, and investment decisions.” This shift is more than a trend. It’s a transformation in how companies are thinking about their bottom line. As the study suggests, the competitive advantage now lies with those who have integrated climate, water, and forest considerations into their core strategies, using them as levers to not only reduce risks but also drive financial opportunity.

THE RISING ECONOMIC CASE FOR SUSTAINABILITY

The report is clear: there is undeniable economic value in environmental action. Sectors such as financial services, infrastructure, and apparel have seen stronger market capitalisation growth among environmen-

“CLIMATE AND NATURE LOSS ARE NO LONGER DISTANT RISKS - THEY ARE ALREADY RESHAPING MARKETS, SUPPLY CHAINS, AND INVESTMENT DECISIONS”

dividends in the form of market share, stronger brand reputation, and resilience to shocks. This shift in perspective is reshaping entire industries and forcing a rethinking of how businesses engage with environmental data.

REGIONAL DIVERGENCE: A TALE OF TWO MARKETS

tal leaders compared to their less proactive peers.

For example, financial services companies that lead on sustainability have outperformed their competitors by 30% versus 19% in market growth since 2022. In the infrastructure sector, the difference stands at 19% versus 17%, and in apparel, the environmental

leaders have grown 16% while others have barely moved the needle at 2%.

This underscores a pivotal point: environmental performance is no longer an ancillary factor in a company’s success. It is central to its financial outcomes. Sustainability isn’t a cost to be managed but an investment that pays

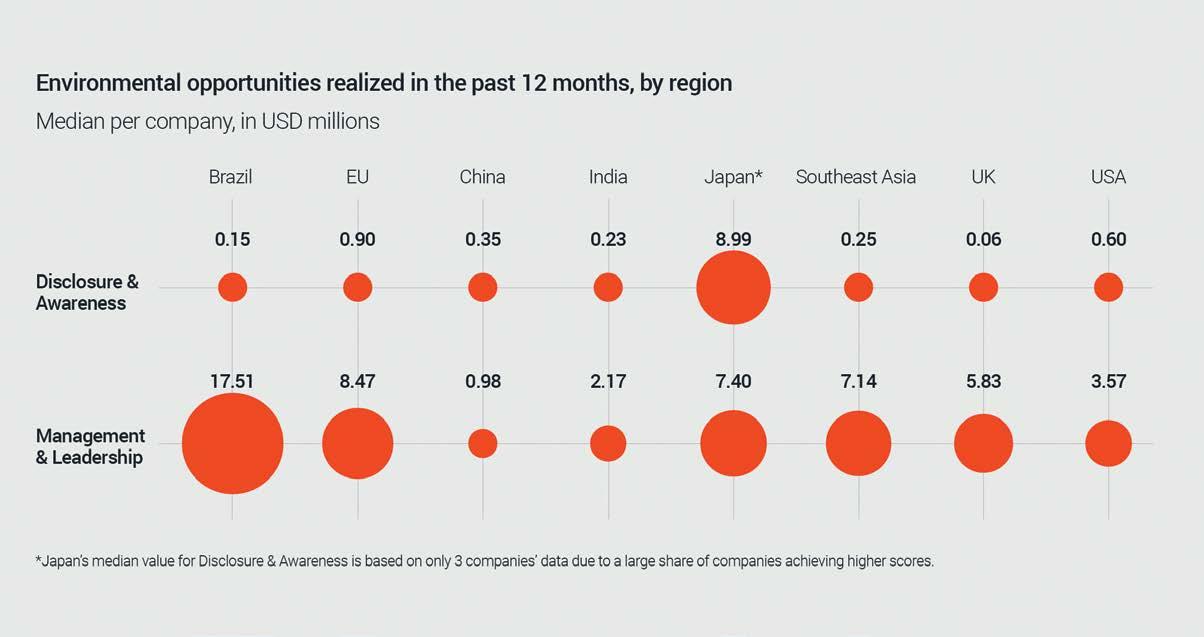

While environmental leadership is growing, the pace of progress varies significantly across regions. In particular, Japan stands out as the clear global leader, with 22% of Japanese companies achieving leadership status on climate action. This contrasts sharply with the US, where only 5% of companies are meeting top-tier environmental standards.

Europe continues to perform strongly, with 52% of companies in the EU27

“MOMENTUM FOR THE TRANSITION IS UNDENIABLE, YET

BUSINESSES FACE A

LEVEL OF POLITICAL AND MACROECONOMIC

UNCERTAINTY

NOT SEEN IN A GENERATION”

reaching the top two performance levels in environmental metrics, compared to just 31% in the US. However, the study also highlights the growing momentum in China and

Southeast Asia, where companies are beginning to catch up rapidly. In fact, China has now surpassed the US in terms of environmental leadership, with 54% of Chinese companies

reporting strong performance across climate, water, and forests. The findings suggest a clear need for regional collaboration and innovation if the global business community is to bridge the environmental divide. As Nick Studer, CEO of Oliver Wyman, notes, “Momentum for the transition is undeniable, yet businesses face a level of political and macroeconomic uncertainty not seen in a generation.” In such a volatile environment, businesses that remain firmly committed to environmental goals are showing that resilience and foresight are just as important as short-term profit margins.

WHAT NEXT?

While mitigation efforts, reducing emissions and protecting ecosystems, are

the focus of most companies at present, adaptation is quickly emerging as the next frontier of environmental action. According to the report, businesses have identified US$1.47tn in physical environmental risks, with more than a quarter of those risks materialising in the near term. Despite this, only US$84.5bn has been invested in adaptation efforts, underscoring the significant opportunity that still exists for businesses to safeguard their operations against the physical impacts of climate change. Companies that invest in climate adaptation are better positioned to protect their value in the face of extreme weather, resource scarcity, and shifting regulatory environments. The report suggests that those who fail to act may find themselves

exposed to greater financial instability, making proactive resilience strategies not just a moral imperative, but a financial one as well.

INCENTIVISING ENVIRONMENTAL LEADERSHIP

One of the most significant findings of the report is the role of governance in driving environmental performance. The most successful companies are linking executive pay directly to environmental outcomes, with 78% of water and forest leaders aligning compensation with sustainability targets. This ensures that environmental objectives are integrated into the very fabric of corporate decision-making, creating an intrinsic motivation for leaders to push the boundaries of what’s possible in terms of emissions reductions and resource management. Moreover, the research shows that companies with clear transition plans aligned to 1.5°C targets are not only

reducing their environmental footprint but also creating a blueprint for other businesses to follow. By adopting robust environmental strategies that consider both the risks and opportunities of climate change, these companies are securing long-term profitability in an increasingly complex global market.

THE FUTURE OF ENVIRONMENTAL BUSINESS STRATEGY

The key takeaway from the CDP Corporate Health Check 2026 is that environmental action is no longer peripheral to business strategy; it is now a core driver of competitiveness and financial performance. As Sherry Madera so aptly puts it, “Earth-positive is no longer peripheral to business strategy; it is becoming a core driver of long-term competitiveness.” Companies that integrate sustainability into their DNA -whether through emissions reductions, value-chain engage-

“EARTH-POSITIVE IS NO LONGER PERIPHERAL TO BUSINESS STRATEGY; IT IS BECOMING A CORE DRIVER OF LONG-TERM COMPETITIVENESS. THE CHALLENGE NOW IS SCALE –MAKING THIS THE NORM RATHER THAN EXCEPTION”

ment, or adaptation investments -are positioning themselves not just for survival, but for success in the new green economy.

As we look to the future, the challenge is not just for businesses to act on these insights, but for them to scale their efforts. As the global economy continues to face unpredictable headwinds, the companies that thrive will be those that recognise environmental leadership as an opportunity to build resilience, drive growth, and create lasting value for both shareholders and society. It is no longer about doing less harm -it is about doing more good. Environmental action is now more than just a risk management strategy; it is a competitive edge that defines the next generation of corporate leadership.

In the Loop / Greener Pastures

The

UK’s next growth story by

PATRICIA CULLEN

→ Hannah Gilbert, Director of Sustainability at the British Business Bank

With renewable energy and clean tech leading the charge, Entrepreneur UK speaks to Hannah Gilbert, Director of Sustainability at the British Business Bank.

Which green sectors show the strongest growth potential for UK businesses, based on current economic data?

The Office for National Statistics (ONS) publishes

data on the environmental goods and service sector (EGSS), which shows economic activity (as measured by Gross Value Added- GVA) has doubled between 2010 and 2022 (100% increase).

Specific EGSS sectors have grown even more including renewable energy (140% increase), environmental education (347% increase) and low emission vehicles, carbon capture and storage, and inspections and control (109% increase). The number of jobs in EGSS

sectors have also increased by 37% to 479,800 in 2022. Despite a slowdown in equity funding conditions over recent years, investors still see potential for investing in the clean tech sector. 43% of UK VC fund managers surveyed in our latest UK VC Financial Returns report currently consider investing in clean energy. The Bank’s UK Business angel survey also shows a shift in business angel investor preferences towards the clean tech sector. The proportion of business angels investing in energy, environment and clean tech increased from 20% in 2019 to 35% in 2025. Our Small Business Equity Tracker 2024 report looked at equity investment and comparisons between the UK and US across sectors. It found that the UK’s relative position in green tech sectors has improved significantly in recent years, with the UK share of the global market increasing from 2.6% to 4.5% over the past decade.

What trends are you seeing in SME access to finance for green initiatives?

Our recently published ‘SMEs and Net Zero’ report explores in detail the extent to which smaller businesses in the UK understand and are engaged with net zero. The research shows that a

majority of SMEs (57%) see a lack of available finance or grants as a key barrier for progressing to net zero. The Bank’s own SME finance survey suggests the proportion of firms who prioritise environmental sustainability reporting access to external finance as a barrier to becoming environmentally sustainable has been largely flat over the last few years, with between 26-28% of those firms prioritising environmental sustainability reporting access to finance to be a barrier in 2022-2024 surveys. The SMEs and Net Zero report findings also showed that demand for finance for green initiatives remains muted among smaller businesses as they face many near-term competing priorities. Whilst smaller businesses generally perceive there to be benefits to their organisation of progressing towards net zero (63% see at least one benefit), transitioning to net zero is a low priority for most smaller businesses over the next 12 months, including most of those in high-emitting sectors. 6% of SMEs are currently accessing green finance or grants and a further 9% have plans to access green finance or grants in the future. This rises to 14% among medium-sized businesses with a further

15% of medium-sized businesses planning to access green finance or grants in the future. Smaller businesses in the utilities, waste and energy supply sectors are the most likely to prioritise working towards net zero with 39% of businesses in these sectors stating achieving net zero was a high priority and a further 33% stating it is a medium priority.

How is the UK financial system adapting to support sustainable innovation?

The UK is consistently ranked first in the world for sustainable finance. Supporting British industry and creating good, skilled jobs up and up down the country is core to the government’s industrial strategy and plan to grow the economy, ensuring businesses can take

THE NUMBER OF JOBS IN EGSS SECTORS HAVE ALSO INCREASED BY 37% TO 479,800 IN 2022. DESPITE A SLOWDOWN IN EQUITY FUNDING CONDITIONS OVER RECENT YEARS, INVESTORS STILL SEE POTENTIAL FOR INVESTING IN THE CLEAN TECH SECTOR.

THE UK IS CONSISTENTLY RANKED FIRST IN THE WORLD FOR SUSTAINABLE FINANCE”

advantage of the transition to new low carbon technologies as they reduce their emissions and that

they have the finance to innovate, adopt and enable the opportunities in the transition to net zero. As

noted earlier, we have already seen a high number of new jobs created in EGSS sectors. Our research shows that investment value and investor appetite has risen in green sectors, including clean tech, green tech and energy-related industries in the last few years:

} Our Small Business Equity Tracker reports look at equity finance for smaller businesses in the UK. The report published in 2023 looks specifically at clean tech companies and shows that equity investment in clean tech companies in the UK has been on the rise the last few years to reach a record £0.9bn in 2022, though it

has since reversed some of this progress in recent years. The Bank welcomes the growth of the clean tech industry in the UK given the scale of investment that is needed for the transition to a net zero economy.

} Our Small Business Equity Tracker 2024 report looked at equity investment and comparisons between the UK and US across sectors. It found that the UK’s relative position in green tech sectors has improved significantly in recent years, with its share of the global market increasing from 2.6% to 4.5% over the past decade. The report also found green tech-focused companies are more likely

In the Loop /

to raise follow on funding than companies in the overall UK equity market (49% of green tech focused companies raised a second round of funding compared to 45% for the overall market), which was an improvement compared to previous start up cohorts.

} However, the report also found that deal sizes to green tech-focused companies are not scaling up to the same extent as businesses in other sectors. Average deal sizes for green tech focused companies are larger than the overall equity market over the first three funding rounds. Over rounds four to six though, green tech-focused deals are smaller than comparable deals in the overall equity market which could signify a possible funding gap as this sector is generally more capital intensive than other sectors.

} Our latest Small Business Equity Tracker report, published in 2025, shows that there is also an increased focus from angel investors on energyrelated industries. The proportion of angel investors surveyed investing in energy, environment and cleantech rose from 20% to 35% between 2019 and 2025, whilst 43% of UK VC fund managers surveyed in our UK VC Financial Returns 2025 report currently consider investing in clean energies.

From an economic perspective, how resilient are UK green businesses to market shocks?

It is not possible to assess how resilient UK green businesses are to market shocks compared to other sectors, as no data source covers this information, though there are some indications from bank surveys. For example, a recent survey undertaken by Rabobank among its SME customers found that SMEs with low ESG performance were about twice as likely as high performers to run into arrears over the year. The SME Finance monitor survey suggests around 22% of SMEs overall in H1 2025 described themselves as struggling, with revenue falling short of

WE EXPECT THE BRITISH BUSINESS BANK’S INDUSTRIAL STRATEGY GROWTH CAPITAL TO THEREFORE DELIVER AROUND £16BN OF CAPITAL TO INVEST ACROSS THE EIGHT SECTORS OVER THE NEXT FOUR YEARS.

outgoings. Over time, the proportion of SMEs reporting that they are struggling has increased from 18% in Q1 2023 to 24% in Q2 2025.

Which government policies or programs are proving most effective at stimulating green entrepreneurship?

The Government announced its Modern Industrial Strategy in 2025, setting out eight growth-driving sectors. Four of these sectors are -vital to stimulating green entrepreneurshipClean Energy, Advanced Manufacturing, Digital and Technologies and Financial Services, which includes sustainable finance. As part of the Government’s announcement, the British Business Bank will be committing £4bn across the eight sectors,

crowding in c. £12bn of private capital. We expect the British Business Bank’s Industrial Strategy Growth Capital to therefore deliver around £16bn of capital to invest across the eight sectors over the next four years.

Looking at the data, what key indicators should entrepreneurs track when building a sustainable business? From an entrepreneur’s perspective, relevant key indicators will depend on the size of the business, funding stage, sector and business model. We supported a toolkit for start-ups and their investors last year, which helps businesses to understand and improve their ESG performance and includes a free library of resources. You can find the toolkit here: toolkit.esgvc.co.uk/

Accelerating Growth in 2026

Three Lessons from Thriving Entrepreneurs. by CHARLOTTE KEENAN

While headlines focus on economic headwinds, thousands of small businesses across Britain are quietly defying the trend. They’re growing faster, hiring more people, and achieving higher productivity than their peers. Goldman Sachs has had a front-row seat to more than 2,500 of these success stories, as we enter the sixteenth year of our 10,000 Small Businesses (10KSB) UK programme. In our latest Impact Report, published in December, the Enterprise Research Centre at Aston University examined the trajectories of the 2,509 high-growth businesses that have graduated from 10KSB UK and compared them to businesses of a similar size and growth profile. The findings are striking. Within three years of completing

Pair learning with real-world guidance

The 10KSB UK programme centres on globally renowned business education delivered by Oxford University’s Saïd Business School – it is essentially a mini-MBA-style programme delivered over three months and refined over 15 years designed to equip small business owners with the frameworks to understand markets, manage finances, and develop a strategy for growth. But what transforms this education into results is pairing it with individualised support. Each participant works with a dedicated “Growth Expert” – experienced business practitioners who help apply classroom frameworks to real challenges. While a module might cover market entry strategy, a

10KSB UK, our alumni outperform their peers by increasing their revenues by 43% and number of people employed by 35% on average, as well as achieving approximately 14% higher productivity. If this effect was replicated for all 153,000 comparable businesses across the UK, then we could see almost one million new jobs created and over £100bn in estimated additional revenue. We’ve learned that this success rests on three pillars: combining rigorous business education with tailored, one-to-one support; building networks that can create lasting commercial value; and creating the space for strategic thinking. These lessons offer a roadmap not just for 10KSB UK alumni, but for any business owner seeking to accelerate their own growth in 2026 and beyond.

FOR 2026, BUSINESS OWNERS SHOULD ACTIVELY PRIORITISE INVESTING IN THESE PEER RELATIONSHIPS – WHETHER THROUGH BUSINESS EDUCATION, ATTENDING INDUSTRY GROUPS, OR WORKING WITH OTHERS TO CREATE PEER ADVISORY CIRCLES”

Growth Expert helps you navigate entering your specific market with your particular constraints.

John McArthur, whose company McArthur BDC designs grain storage systems for cereal farmers and distillers, credits this combination with transforming his business.

“Without the financial organisation I learnt, we’d have been flailing during Covid,” he says. “The access to finance information and grant application

advice meant we were wellstructured and stayed financially robust.” The programme also gave him confidence to pursue acquisitions, buying both a supplier and a customer, with one of his advisors from the programme still sitting on his board. For any entrepreneur, it’s a demonstration that structured learning matters, but so does having someone who can help you translate general principles

→ John McArthur, founder of McArthur BDC

into specific actions. Seek out mentors or advisors who know your industry and can provide practical guidance on applying what you’re learning to the particular challenges your business faces.

Build networks to open new doors

10KSB UK graduates consistently report that relationships formed during the programme prove as valuable as the education. Businesses from their cohort become customers, suppliers, and collaborators. They recommend each other’s services and sometimes launch ventures together.

Paris Blackwell, who runs Pario Holiday Parks in

“INVEST IN STRUCTURED LEARNING AND FIND ADVISORS WHO CAN HELP YOU APPLY IT. BUILD NEW RELATIONSHIPS WITH FELLOW ENTREPRENEURS WHO UNDERSTAND YOUR CHALLENGES. AND CARVE OUT TIME TO STEP BACK AND THINK STRATEGICALLY ABOUT WHERE YOUR BUSINESS IS HEADING”

North Wales, exemplifies the lasting power of these connections. “Eight years after our time on the 10KSB UK programme,

our cohort are still in regular communication. We ask questions and share stresses that other entrepreneurs can relate to.”

These aren’t just professional contacts –they’re personal relationships built on shared entrepreneurial experience. And increasingly, they extend internationally.

Connections with our US and French programmes have opened export markets and cross-border relationships for UK alumni, creating opportunities they wouldn’t have discovered in isolation.

There is so much value in connecting with people who understand your challenges and can become collaborators or guides into new markets. For 2026, business owners should actively prioritise investing in these peer

→ Paris Blackwell, Director at Pario Holiday Parks

→ Naynesh Karia, Co-founder of Food Attraction Limited

relationships – whether through business education, attending industry groups, or working with others to create peer advisory circles.

Make time to work on your business rather than in it

The 10KSB UK programme also creates dedicated time for business owners to step back and think strategically. When you’re immersed in daily operations it can be difficult to maintain the broader perspective needed to spot bottlenecks, identify growth opportunities, or develop coherent plans.

Naynesh Karia discovered this when he joined the programme in 2016. His family food business, Food Attraction, had £2.5m in annual sales and 25 staff, but was hitting a ceiling. “The opportunity came just at the right time. It gave me the mental capacity to be pragmatic and realise we needed to start hiring to grow.”

Stepping back allowed him to see that he couldn’t be an expert in everything. He recruited key

managers and formed a board of senior management, freeing himself and his brother to focus on marketing and product development. Today the business employs 130 people with £15m in revenues.

Creating this space deliberately is something all entrepreneurs should seek to do. Block out time regularly – monthly or quarterly – to work on your business rather than in it. Use it to assess what’s working, identify constraints, and explore opportunities you’ve been too busy to consider.

Three things you can control

The year ahead will bring challenges no business owner can predict or control. But amid the unpredictability, there are concrete actions you can take right now. Invest in structured learning and find advisors who can help you apply it. Build new relationships with fellow entrepreneurs who understand your challenges. And carve out time to step back and think strategically

about where your business is heading. These three priorities won’t insulate you from every headwind, but the evidence from 2,500 growing businesses shows they can put you in a stronger position to navigate whatever 2026 brings. The businesses most likely to thrive this year will be the ones that start now.

Charlotte Keenan is the Head of the Office of Corporate Engagement International at Goldman Sachs and leads Goldman Sachs 10,000 Small Businesses UK, a programme which provides business and management training to highgrowth small businesses in the UK to create jobs and economic opportunity. The information and statistics in this article are drawn from the Impact Report. The case studies and examples set forth herein are for illustrative purposes only and should not be considered a prediction or assurance of future performance, nor a guarantee of actual results.

2026 will be the year of Climate’‘Quiet

What does that mean for founders?

by JULIETTE DEVILLARD

Something shifted for climate founders over the past year. In 2024, building a “climate tech” company was, in itself, a strong positioning. It helped attract talent, capital, and attention. It signalled ambition and values. For a while, that was enough to open doors. In 2025, that changed. With Trump’s election, the rollback of climate policy in the US and a growing backlash against ESG, many companies quietly softened their language on net zero or stepped back from public sustainability commitments altogether. As political will waned, funding became tighter, both from investors and potential customers.

The need for climate action didn’t stop, but leading with climate became harder. As the start-up world continues to adapt, I predict that 2026 will be the year of “Quiet Climate”. Quiet Climate doesn’t mean building different solutions. It means talking about them differently. Founders will keep working on electrification, efficiency, resilience, low-carbon materials and cleaner infrastructure. However, fewer decks will open with the word “climate”; they’ll instead open with margins, efficiency, payback periods and risk reduction.

For years, climate innovation was often pitched as being mission-first. The assumption was that customers would pay a premium for sustainability, or that being greener was, on its own, a competitive advantage. In today’s economy, that assumption no longer holds. When budgets are under pressure, businesses buy what saves them money and what reduces risk - what helps them deliver on their core objectives. That doesn’t make climate solutions less relevant, but it does change how they need to be sold.

The strongest climate-driven businesses won’t ask customers to make a values-based choice. They’ll offer a clear upgrade, lower energy costs, more reliable operations, faster deployment or easier compliance, or all of the above. Emissions reduction is now the outcome of a better product, not the headline. This is especially important for mission-driven founders to internalise because most climate startups aren’t selling to sustainability teams. They’re selling to CFOs, operations leaders and procurement teams. These buyers care about cost, reliability and performance. If a business’ solution delivers on those metrics, decarbonisation becomes a powerful added benefit. It may feel painful to be inwardly motivated by impact, but outwardly selling efficiency, but this shift is now a necessity.

This trend has already played out in venture. Funds that once branded themselves explicitly as “climate” are now leaning into adopting language like “efficiency”, “industrial innovation”, “deep tech” or “energy security”. The portfolios of start-ups they invest in still look

strikingly similar, but the framing has changed because the market has changed.

Founders are making the same move. Pitch decks that once led with tonnes of CO2 saved now lead with unit economics. Case studies that used to highlight emissions reductions now open with cost savings and operational impact. The climate story is still there, but it’s no longer doing the heavy lifting on its own. There’s a resilience benefit here too. Businesses that can clearly articulate their commercial value are less exposed to political cycles or public backlash. If a solution stands up on cost and performance alone, it’s harder to dismiss.

→ Juliette Devillard, founder, Climate Connect

However, Quiet Climate comes with a real risk. We can’t allow this “quiet” era to become an excuse to stop measuring, stop reporting or stop being honest about the climate impact of these products. If the startup world teaches us anything, it’s that attention moves in cycles. Climate will return to the centre of public conversation, and the work done now needs to be robust enough to stand up to scrutiny when it does. If we care about long-term impact, Quiet Climate needs to be about message discipline, not lower standards.

So what should founders be doing in practice in 2026? First, pressure-test value propositions. If the climate benefit disappeared from a startups’ pitch, would the offer still be compelling? If not, founders need to find the hook. That might be energy cost, reliability, compliance, throughput, waste reduction, safety or labour constraints. Second, build

“

Businesses that can clearly articulate their commercial value are less exposed to political cycles or public backlash. If a solution stands up on cost and performance alone, it’s harder to dismiss”

for adoption, not applause. At the early stage, many startups optimise for winning awards or sounding good on stage - not surprisingly given this can help attract angels and early funders. With scale though, the focus needs to shift away from shiny awards, and towards the mundane but essential task of fitting seamlessly into customer procurement processes. These include fast integration, clear ROI and credible case studies over vanity metrics. Third, learn to be bilingual. Founders need to speak “customer” and “climate” fluently without mixing the messages. Customers want operational outcomes. Investors, regulators and strategic partners want credible data. Teams still want purpose. Surviving and thriving in an era of Quiet Climate means knowing which language to use, and when. Fourth, don’t worry about the labels. Whether the market calls it climate tech, energy tech, resilience tech or industrial innovation, the underlying opportunity is the same: rebuilding how the world makes, moves and powers things. Finally, don’t quit. The toughest years are when the future gets decided. When easy money disappears and scrutiny increases, genuinely strong solutions have room to stand out. The founders and investment funds who stick with climate during this downturn are the ones who will shape the next cycle of growth.

The climate crisis remains a multi-decade challenge that will reshape supply chains, infrastructure, insurance markets and geopolitics. Businesses will keep needing cleaner power, more efficient operations and more resilient systems. Those forces are bigger than any election cycle, so let’s not let ourselves be sidetracked by a single climatedenying President.

Juliette is a climate connector and ecosystem builder. Prior to founding Climate Connect, she spent 4 years in the US working in early-stage startup creation at the intersection of climate and deep tech. Juliette is also a public speaking coach, leadership coach, and mental health awareness advocate.

TONY MATHARU: Planting Trees for the Long Term

WHEN THE PANDEMIC EMPTIED LONDON’S STREETS AND SILENCED ITS THEATRES, CAFES, AND BARS, IT REVEALED A TRUTH OFTEN OVERLOOKED: THE CITY’S VITALITY DEPENDS AS MUCH ON HUMAN MOBILITY AS ON THE GRANDEUR OF ITS ARCHITECTURE. FEW UNDERSTOOD THIS MORE VISCERALLY THAN TONY MATHARU, THE BRITISH PROPERTY DEVELOPER AND ENTREPRENEUR WHOSE WORK SPANS HOTELS, HOSPITALITY GROUPS, AND COMMUNITY INITIATIVES.

My initial interest in starting a business,”

Matharu recalls, “began as a small seed that germinated in an environment created and nurtured by my mother who encouraged me to start something of my own, since there was no family business existing.” That first venture blossomed into a chain of 18 hotels in central London. Growth brought new opportunities and challenges: ultimately a difference of vision and ambition with minority shareholders led Tony to restructure, step away, and embark on a fresh chapter unencumbered by con-

→ Tony Matharu, Board Member of the London Chamber of Commerce and Industry and Chairman of its Asian Business Association

straints imposed by others. From that transition emerged the Integrity International Group and its multi award winning Blue Orchid Hospitality subsidiary, models of resilience and longterm strategic thinking. Matharu says his philosophy mirrors

that of Warren Buffett: thinking longterm and ‘planting trees.’ The benefits of shade and protection others enjoy, he notes, come from investments nurtured over time. In practical terms, this means patient, deliberate growth: acquiring sites, navigating planning,

developing buildings, stabilising income streams and creating long term value. These are stages measured not in quarters but in years.

The arrival of COVID-19 provided an unexpected test of this philosophy.

Central London’s vibrancy is predicated on movement: office workers commuting, tourists wandering, theatregoers gathering, diners circulating. Without that mobility, the city’s economy stalled. “Just take the Square Mile,”

Matharu explains, “five or six hundred thousand people coming into that one square mile every day… when they’re not coming in, there’s an impact… the whole infrastructure shudders to a halt.”

In response, he founded Here to Help London, a charitable initiative aimed at alleviating lockdown hardships, which then evolved into the Central London Alliance, a community interest company. It was a recognition that the private sector, par-

→ The Rochester, a luxury hotel in London, included in the Blue Orchid Hospitality portfolio

→ Atlas House, a Grade II‑listed historic office building in the City of London

ticularly hospitality, has obligations beyond profit.

“When you start a business, you’re part of a multifaceted interdependent community,” Matharu notes. Hotels, pubs, and restaurants are not mere commercial entities; they are nodes in a social network, providing employment, culture, and cohesion.

Matharu’s reflections extend beyond London’s streets to the broader ethos of entrepreneurship. Public goodwill, he observes, has the capacity to sustain cities in ways government interventions cannot. From the volunteers of London 2012 to the frontline responders applauded during the pandemic, civic spirit underpins resilience. “Human beings are generally well meaning and public spirited… but some-

times this gets pushed to the background.” His vision for business is similarly integrative: profitability should serve society, not merely shareholders. This sense of social responsibility is rooted in Matharu’s personal values, particularly the Sikh principle of seva - “doing something positive for somebody or some group of people every day without seeking selfbenefit or self-aggrandisement.” He has woven this ethos into his business philosophy, seeing no contradiction between generating profit and promoting social good. “Many people regard doing good as good for business… but

if you’re still doing good, that’s a positive thing, even if individual or collective rewards might also result” he notes. In a city that thrives on mobility, diversity, and culture, such an approach may be the most sustainable investment of all. “Entrepreneurs just want the right environment to create and scale their businesses and to generate value. It’s not too much to ask, is it?”

Sustainability has also become a strategic priority. In an era of carbon-conscious development, Matharu favours retrofitting over demolition wherever feasible. “The local planning authorities are

→ The Wellington, a Westminster‑based boutique hotel is part of Tony Matharu’s Blue Orchid Hospitality portfolio

now adopting a retrofit-first approach… rather than demolish and destroy, one can take benefit from the quality of the historic fabric and materials.” The decision is never binary: market needs, regulations, and building characteristics determine whether retrofitting is viable, but the guiding principle remains - extract life from existing structures before creating new ones.

For aspiring entrepreneurs, Matharu offers practical counsel. Understanding demand and aligning supply is fundamental. If you understand the market’s needs and can meet them profitably, you’ve solved the first puzzle of entrepreneurship.” Equally critical is removing obstacles. “Anything that quells or inhibits ambition is counterproductive and you need a “stable and certain environment to stimulate and reward risk.” Excessive taxation, complex

“MANY PEOPLE REGARD DOING GOOD AS GOOD FOR BUSINESS… BUT IF YOU’RE STILL DOING GOOD, THAT’S A POSITIVE THING, EVEN IF INDIVIDUAL OR COLLECTIVE REWARDS MIGHT ALSO RESULT”

regulations, and volatile policy environments can discourage investment and scaling. Matharu does not mince words: “Why take risks, borrow lots of money, invest your time and other resources, when at the end all of that the value you have created and possibly more will simply be removed and given to the tax man?” Business rates, stamp duties, and inheritance taxes can collectively erode the rationale for growth, prompting entrepreneurs to scale back or sell, reducing employment and competition in the process.

Undeterred by these pressures, Matharu is advancing a robust pipeline of developments. He is developing another all suite apartment hotel in the City of London, with a hundred apartments,

alongside a boutique Grade II-listed hotel near Guildhall and Bank, complete with spa and pool. He has also secured a site in St James’s Park for over 500 rooms with extensive facilities. “I have at least five years of development in place and I am determined to continue, although the environment is more challenging than I can ever remember,” he admits. The challenges he cites are not abstract. London’s hospitality sector faces disproportionate burdens: business rates for hotels in the UK are set to increase by an average of 115% and more in London, according to UK Hospitality, while restaurants, venues and pubs have also faced steep rises. Energy costs, employment taxes, increased employment regulation,

“THE GOVERNMENT MAY HAVE BACKTRACKED ON CERTAIN PLANS BUT A DECISIVE U-TURN IS STILL NEEDED ON THE ‘21ST CENTURY WINDOW TAX’ WHICH IS TODAY’S BUSINESS RATES REGIME AND ON THE PROPOSED REMOVAL OF BUSINESS

PROPERTY RATES RELIEF/ INHERITANCE TAX”

and other regulatory measures compound the strain. Matharu sees these pres-

sures as potentially calamitous. “UK hospitality is on the brink - approximately

six hospitality businesses are set to go under every day. Independent operators are disappearing, leaving the field to global brands who do not have the same community and long term interests as independent concerns and especially family owned businesses, and they do not have to factor in or consider inheritance taxes, for example. We need to do far better.” Inheritance tax is critical looming threat. “If 20% to 40% of your total asset base is subject to inheritance tax as a result of the proposed removal of

business property tax relief, it becomes the opposite of scaling. Heirs would potentially be forced to sell and break up carefully curated businesses. This affects independent familyowned enterprises just like the farmers where careful assembly and stewardship of assets is being punished by the removal of agricultural property tax relief. Many are rightly alarmed - without intervention, we face disaster: reduced investment, scaled-back operations, and fewer jobs with less money in the Treasury coffers.” With the