This Benefit Guide is provided for sta to have a comprehensive resource for the YMCA of Greater Pittsburgh health and wellness benefits. This Benefit Guide is not intended to be a contract (expressed or implied), nor is it intended to otherwise create any legally enforceable obligations on the part of the YMCA of Greater Pittsburgh, its agents, or its sta . The included information is intended as a benefit summary only. It does not include all of the benefit provisions, limitations, and qualifications. If this information conflicts in any way with the contract, the contract will prevail. The purpose of this Benefit Guide is to summarize the YMCA of Greater Pittsburgh’s sta benefits and the policies and procedures regarding these benefits. For the most detailed and up-to-date information, please refer to the appropriate plan document, evidence of

or contract, as well as

Visit ybenefits.org for a comprehensive overview of the YMCA benefits.

INTRODUCTION AND ELIGIBILITY

The YMCA of Greater Pittsburgh is pleased to provide our sta and their dependents with a comprehensive benefits package that addresses their personal health and financial well-being. We encourage sta to examine this summary carefully to fully understand the benefits available. This summary is designed to give general information about each option and an overview of the benefit plans. The many benefits the YMCA of Greater Pittsburgh o ers are summarized in the following sections. The YMCA of Greater Pittsburgh contributes a significant portion to Medical and Dental benefits o ered. Other benefits are provided to you at no cost, and some are fully paid by you.

Eligibility

The YMCA of Greater Pittsburgh provides benefits to all full-time sta members and their dependents. New full-time and newly benefit eligible full-time sta will be eligible for group benefits on the first of the month following 30 days of employment.

Eligible Dependents

Eligible dependents for medical coverage are your legally married spouse and dependent children up to age 26. Children who are disabled are covered up to any age. Dental coverage applies for children until their 19th birthday or their 25th birthday if they are a student.

Part- time sta

Part-time sta averaging a minimum of 30 working hours per week may be eligible for medical insurance benefits. The YMCA of Greater Pittsburgh uses an initial 12-month look back measured period to determine eligibility for medical insurance benefits.

HEALTH BENEFITS

For 2026, the YMCA of Greater Pittsburgh is o ering the following.

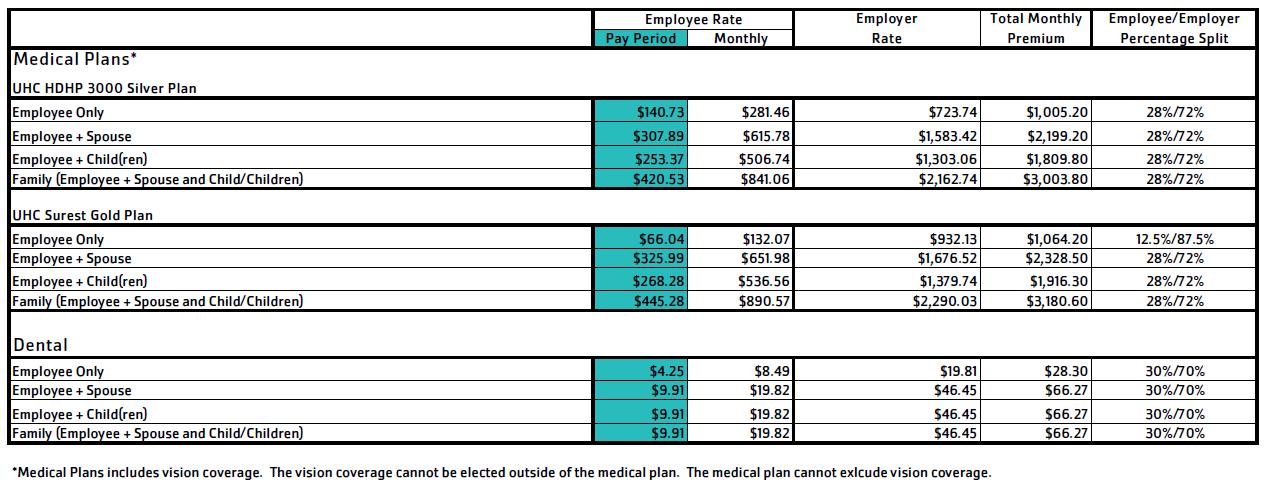

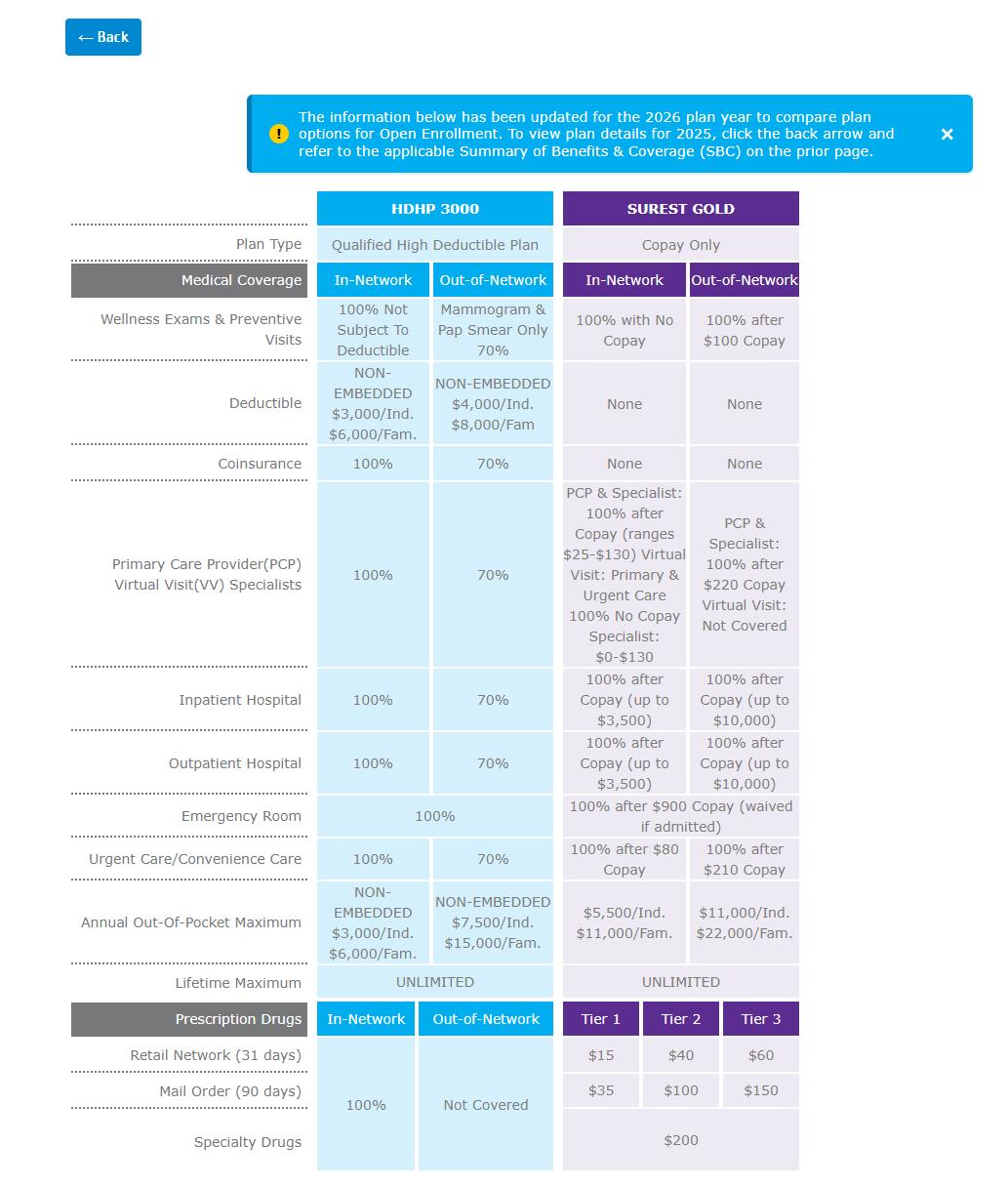

Medical Benefits through United Healthcare

High Deductible Health Plan (HDHP 3000 ) (Surest Gold Plan)

Vision through EyeMed is included in both health plan choices A 2026 Medical Plans Comparison Chart can be found on page ___for review

Along with the medical plan we also have the option for tax-advantaged financial accounts which are: Health Savings Account (HSA) - Available if on United Healthcare HDHP 3000Plan

Flexible Spending Account (FSA) - Available if on the Surest Gold Plan or also if opting out of a medical plan

Dental Benefit through Delta Dental PPO

1 plan Available

Additional Benefits o ered:

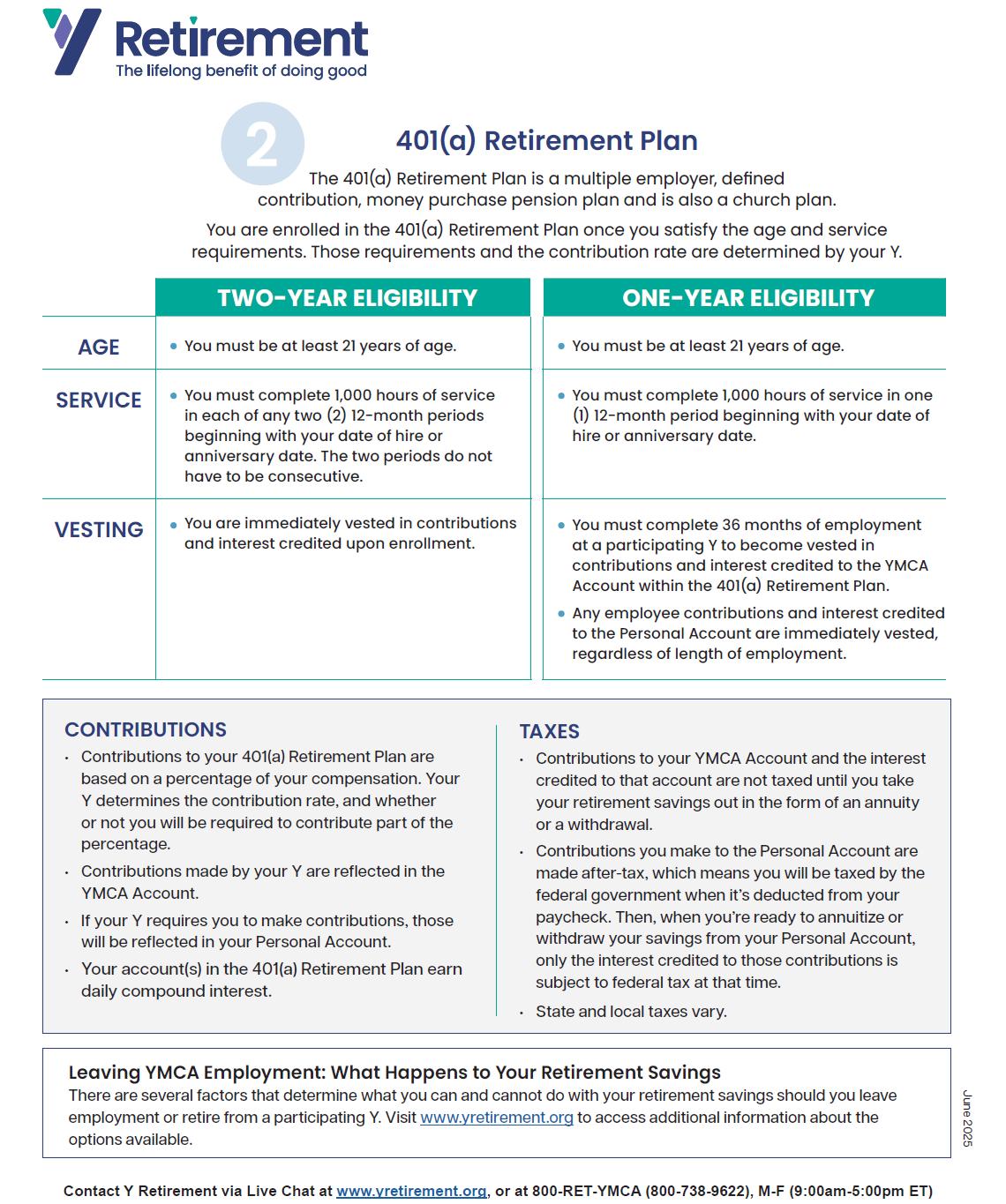

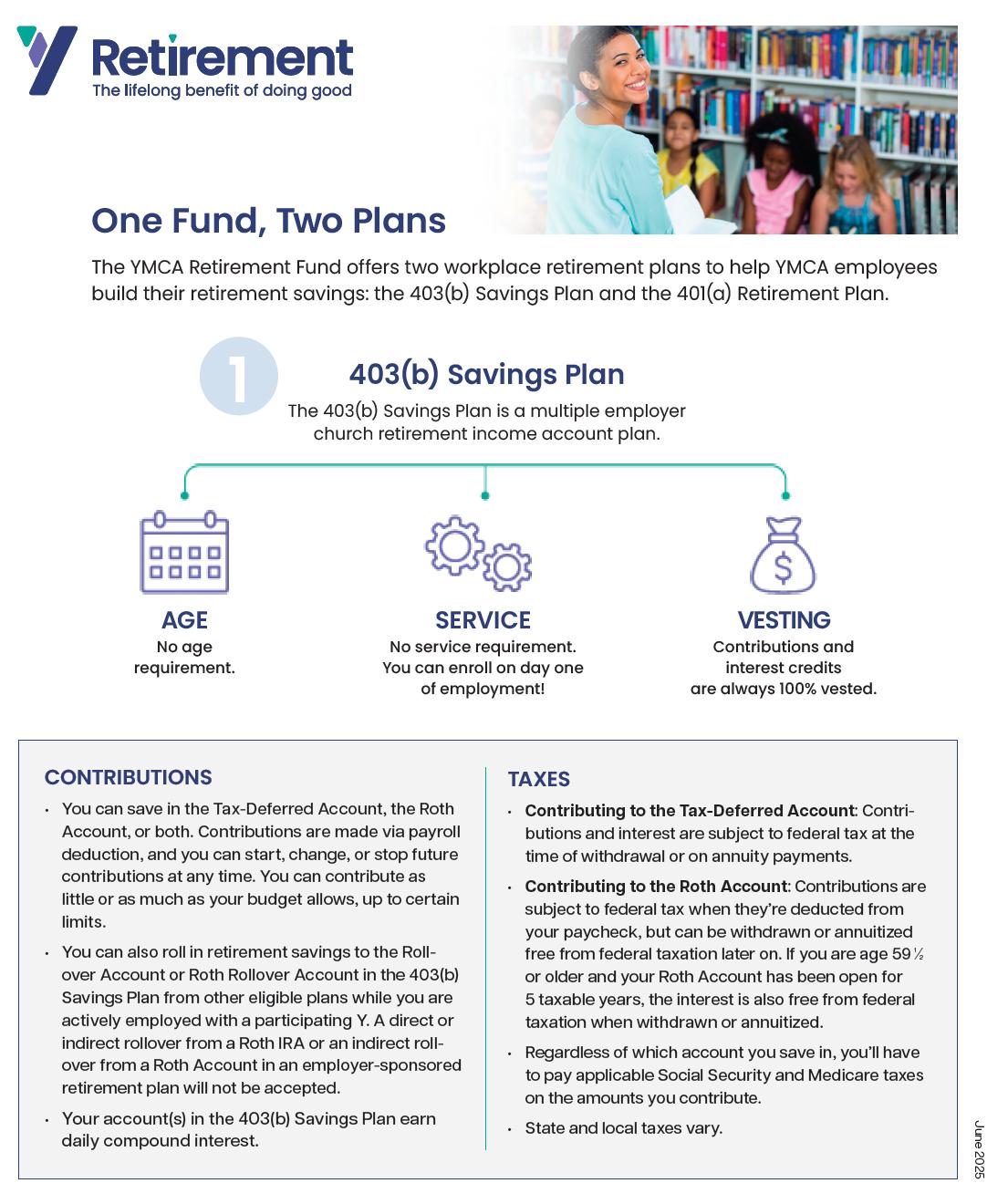

403(b) Retirement Savings

ROTH Account

11% Employer retirement Contribution (once eligible after full time for 2 years) Free YMCA Membership Free Programs or at a discounted rate

Long Term Disability Short Term Disability Paid Time O 11 Paid Holidays

Basic Life & AD&D

Optional Life & Dependent Life Insurance Employee Assistance Program (EAP) Visit ybenefits.org for a comprehensive overview of the YMCA Benefits. You can choose

Qualifying Life event

A qualifying life event (QLE) refers to a significant change in your circumstances that can impact your eligibility for health insurance. These events allow you to enroll in health insurance outside the regular yearly Open Enrollment Period. Here are some examples of qualifying life events:

Loss of Health Coverage:

Losing existing health coverage, including job-based, individual, or student plans. Losing eligibility for Medicare, Medicaid, or CHIP. Turning 26 and losing coverage through a parent’s plan.

Changes in Household:

Getting married or divorced. Having a baby or adopting a child. Experiencing a death in the family.

Other Qualifying Events:

Gaining membership in a federally recognized tribe or status as an Alaska Native Claims Settlement Act (ANCSA) Corporation shareholder. Becoming a U.S. citizen. and Leaving incarceration (jail or prison).

Consolidated Omnibus Budget Reconciliation Act (COBRA)

Federal law provides for the continuation of benefits for employees or dependents who lose their health coverage. This temporary extension provides eligible employees/dependents continuation of benefits on a private-pay basis (group rate plus a 2% administrative fee) for up to 18 months. In some circumstances, this benefit can be continued for 36 months. Qualifying events for COBRA coverage include, but are not limited to, employees who leave The YMCA or are terminated (except for gross misconduct), employees who lose coverage due to the reduction of hours, or circumstances in which covered dependents lose coverage.

2026 BENEFIT PLAN RATES

COBRA 2026 Rates

The Consolidated Omnibus Budget Reconciliation Act (COBRA) gives workers and their families who lose their health benefits the right to choose to continue group health benefits provided by their group health plan for limited periods of time under certain circumstances such as voluntary or involuntary job loss and other life events. Rates are 102% of the full premium, as shown below:

UNDERSTANDING YOUR OPTIONS HDHP 3000

Why Choose a Health Plan from YMCA Employee Benefits:

Regardless of which plan you choose, a health plan from YMCA Employee Benefits guarantees you’ll have access to a large network of physicians and specialists, and comprehensive coverage for you and/or your family. With any of our plans, you’ll have the freedom of using any doctor or facility you want without needing a referral—though you’ll typically save a significant amount of money using doctors and/or facilities that are in-network. Choosing a plan from YMCA Employee Benefits means you’ll also have access to:

Preventive Care Covered at 100%

No copay, co-insurance, or deductible—as long as care is received from a network provider

Tools and Services to Make Informed Decisions

Enrollment in a YMCA Employee Benefits medical plan means you’ll have access to resources to help you estimate costs, find providers, and compare your options

Personal Support and Helpful Programs to Improve Your Health

Access to registered nurses, Wellness Coaching, personal health support advocates, and more—all at no extra cost to you

Additional benefits of choosing the HDHP 3000 plan:

High Deductible Health Plans (HDHPs) o er many features that aren’t available with other plan options, including:

Lower premium

Typically, the premium for a High Deductible Health Plan is lower. That means you’ll usually pay less up front for the cost of your plan. It may be a good idea to set aside a portion of that savings to contribute to your deductible if you need it.

High deductible up front, except for preventive services

You’ll be responsible for paying the full cost of medical care you receive until you’ve met your deductible. The only exception is for innetwork wellness and/or preventive care, which is covered at 100% beginning on your first day of coverage.

Tax-free savings with a Health Savings Account (HSA)

One of the biggest advantages of an HDHP is the ability to open and contribute to an HSA. The money in your HSA can be spent on any qualified medical expense*, including your deductible! Plus, any interest earned is tax-free and some HSAs allow you to invest in stocks or mutual funds to grow your account even further.

Please Note: This plan features a non-embedded design, meaning that, for those with dependents covered, the individual deductible is NOT embedded inside the family deductible. If you enroll any dependents in the plan, the full family deductible must be met before the plan will cover any costs. Similarly, once the full family out-of-pocket maximum is met, the plan will cover 100% of any additional covered expenses.

SUMMARY OF BENEFITS

YMCA: HDHP 3000

Summary of Benefits and Coverage: What this Plan Covers & What You Pay For Covered Services

Coverage Period: 01/01/2026-12/31/2026

Coverage for: Individual / Individual + Family | Plan Type: PPO

The Summary of Benefits and Coverage (SBC) document will help you choose a health plan. The SBC shows you how you and the plan would share the cost for covered health care services. NOTE: Information about the cost of this plan (called the premium) will be provided separately. This is only a summary. For more information about your coverage, or to get a copy of the complete terms of coverage, go to www.ybenefits.org or call 877-BEN-YMCA For general definitions of common terms, such as allowed amount, balance billing, coinsurance, copayment, deductible, provider, or other underlined terms see the Glossary. You can view the Glossary at www.ybenefits.org or call 877-BEN-YMCA to request a copy.

What is the overall deductible?

Are there services covered before you meet your deductible?

Network: $3,000 Individual / $6,000 Family

Non-Network: $4,000 Individual / $8,000 Family Per calendar year

Yes. The deductible does not apply to preventive care.

Are there other deductibles for specific services? No

What is the out-of-pocket limit for this plan?

What is not included in the out-of-pocket limit?

Will you pay less if you use a network provider?

Network: $3,000 Individual / $6,000 Family

Non-Network: $7,500 Individual / $15,000 Family

Per calendar year

Premiums, balance-billing charges, health care this plan doesn’t cover, and penalties for failure to obtain prior authorization

Yes. For a list of network providers, see www.myuhc.com or call the Member Services number on the back of your ID Card.

Generally, you must pay all of the costs from providers up to the deductible amount before this plan begins to pay. If you have other family members on the plan, the overall family deductible must be met before the plan begins to pay.

This plan covers some items and services even if you haven’t yet met the deductible amount. But a copayment or coinsurance may apply. For example, this plan covers certain preventive services without cost-sharing and before you meet your deductible. See a list of covered preventive services at https://www.healthcare.gov/coverage/preventive-care-benefits/.

You don’t have to meet deductibles for specific services.

The out-of-pocket limit is the most you could pay in a year for covered services. If you have other family members on the plan, the overall family out-of-pocket limit must be met

Even though you pay these expenses, they don’t count toward the out-of-pocket limit

This plan uses a provider network. You will pay less if you use a provider in the plan’s network. You will pay the most if you use an out-of-network provider, and you might receive a bill from a provider for the difference between the provider’s charge and what your plan pays (balance billing). Be aware, your network provider might use an out-of-network provider for some services (such as lab work). Check with your provider before you get services.

Primary care visit to

If you visit a health care provider’s office or clinic

Preventive care/screening/ immunization No charge

What You Will Pay

If you have a test

Common Medical Event Services You May Need

If you need drugs to treat your illness or condition More information about prescription drug coverage is available at www.myuhc.com

If you have outpatient surgery

Mammograms and pap smears: 30% coinsurance

All other services: Not covered

You may have to pay for services that aren’t preventive. Ask your provider if the needed services are preventive, then check what your plan will pay for.

Some outpatient diagnostic tests require authorizationrefer to the SPD for details

If you use a non-network provider and fail to get authorization, you are subject to a $500 benefit reduction.

Authorization is required for imaging-refer to the SPD for details

If you use a non-network provider and fail to get authorization, you are subject to a $500 benefit reduction.

What You Will Pay

If you need immediate

a 90 day supply Tier 3 drugs

up to a 31 day supply Mail order: up to a 90 day supply

Authorization is required and specialty drugs must be filled through the designated Specialty Pharmacy. Information is available on www.myuhc.com or by calling 877-BENYMCA.

Authorization is required for outpatient surgeries-refer to the SPD for details.

If you use a non-network provider and fail to get authorization, you are subject to a $500 benefit reduction.

Authorization is required for outpatient surgeries-refer to the SPD for details

If you use a non-network provider and fail to get authorization, you are subject to a $500 benefit reduction.

You must notify UHC within 48 hours if admitted to a nonnetwork hospital, or on the same day of admission if reasonably possible If you are admitted to a non-network hospital and fail to notify UHC, you may be subject to a $500 benefit reduction. Refer to the SPD for more details.*

If you have a hospital stay

If you are pregnant

Authorization is required for all scheduled admissions. If you are admitted to a non-network facility and fail to get authorization, you are subject to a $500 benefit reduction.

Authorization is required for all scheduled admissions. If you are admitted to a non-network facility and fail to get authorization, you are subject to a $500 benefit reduction.

Authorization is required for partial hospitalization/day treatment, intensive outpatient program treatment, outpatient electro-convulsive treatment, psychological testing, transcranial magnetic stimulation, extended outpatient treatment visits beyond 45 - 50 minutes in duration (with or without medication management), and intensive behavioral therapy, including Applied Behavior Analysis (ABA).

If you use a non-network provider and fail to get authorization, you are a subject to a $500 benefit reduction.

Authorization is required for inpatient services (including services at a residential treatment facility)

If you use a non-network provider and fail to get authorization, you are subject to a $500 benefit reduction.

Depending on the type of services, a copayment, coinsurance, or deductible may apply. Maternity care may include tests and services described elsewhere in the SBC (i.e. ultrasound).

None

*For more information about limitations and exceptions, see the Summary Plan Description (SPD) at www.ybenefits.org

What You Will Pay

Limitations, Exceptions, & Other Important Information

Authorization is required for maternity stays exceeding 48 hours for normal vaginal delivery and 96 hours for cesarean section delivery

If you use a non-network facility and fail to get authorization, you are subject to a $500 benefit reduction.

Authorization is required, 60 visit limit per calendar year

If you use a non-network provider and fail to get authorization, you are subject to a $500 benefit reduction.

Outpatient: 30 visit limit per calendar year (not applicable with a mental health/substance use disorder diagnosis)

Inpatient: Authorization is required, 120 day limit per calendar year

If you use a non-network provider and fail to get authorization for inpatient rehabilitation or skilled nursing facility services, you are subject to a $500 benefit reduction.

Outpatient: 30 visit limit per calendar year (not applicable with a mental health/substance use disorder diagnosis)

Authorization is required, 120 day limit per calendar year

If you use a non-network provider and fail to get authorization, you are subject to a $500 benefit reduction.

If your child needs dental or eye care

Authorization is required for items obtained by a nonnetwork provider that cost more than $1,000 to purchase or rent There is a $2,000 calendar year limit for disposable medical supplies.

If you use a non-network provider and fail to get authorization, you are subject to a $500 benefit reduction.

If you use a non-network provider and fail to get authorization, you are subject to a $500 benefit reduction.

Children’s eye exam No charge Not covered 1 visit per calendar year, up to age 6

Children’s glasses Not covered Not covered None

Children’s dental check-up Not covered Not covered None

Excluded Services & Other Covered Services:

Services Your Plan Generally Does NOT Cover (Check your policy or plan document for more information and a list of any other excluded services.)

Cosmetic surgery

Children’s glasses

Dental care

Hearing aids

Long-term care

Non-emergency care when traveling outside the U.S.

Routine foot care

Weight loss programs

Other Covered Services (Limitations may apply to these services. This isn’t a complete list. Please see your plan document.)

Acupuncture

Bariatric surgery

Chiropractic care

Fertility treatment

Private duty nursing

Routine eye care

Your Rights to Continue Coverage: Contact your Human Resources department. In addition, there are agencies that can help if you want to continue your coverage after it ends. The contact information for those agencies is: U.S. Department of Labor’s Employee Benefits Security Administration at 1-866-444EBSA(3272) or www.dol.gov/ebsa/healthreform Other coverage options may be available to you too, including buying individual insurance coverage through the Health Insurance Marketplace For more information about the Marketplace, visit www.HealthCare.gov or call 1-800-318-2596.

*For more information about limitations and exceptions, see the Summary Plan Description (SPD) at www.ybenefits.org

Your Grievance and Appeals Rights: There are agencies that can help if you have a complaint against your plan for a denial of a claim. This complaint is called a grievance or appeal. For more information about your rights, look at the explanation of benefits you will receive for that medical claim. Your plan documents also provide complete information to submit a claim, appeal, or a grievance for any reason to your plan. For more information about your rights, this notice, or assistance, contact the number on the back of your ID card, or The Department of Labor’s Employee Benefits Security Administration at 1 -866-444-EBSA(3272) or www.dol.gov/ebsa/healthreform

Does this plan provide Minimum Essential Coverage? Yes

Minimum Essential Coverage generally includes plans, health insurance available through the Marketplace or other individual market policies, Medicare, Medicaid, CHIP, TRICARE, and certain other coverage. If you are eligible for certain types of Minimum Essential Coverage, you may not be eligible for the premium tax credit

Does this plan meet the Minimum Value Standards? Yes

If your plan doesn’t meet the Minimum Value Standards, you may be eligible for a premium tax credit to help you pay for a plan through the Marketplace

Language Access Services:

Spanish (Español): Para obtener asistencia en Español, llame al 877-BEN-YMCA

Tagalog (Tagalog): Kung kailangan ninyo ang tulong sa Tagalog tumawag sa 877-BEN-YMCA

To see examples of how this plan might cover costs for a sample medical situation, see the next section

6 of 8

About these Coverage Examples:

This is not a cost estimator. Treatments shown are just examples of how this plan might cover medical care. Your actual costs will be different depending on the actual care you receive, the prices your providers charge, and many other factors. Focus on the cost sharing amounts (deductibles, copayments and coinsurance) and excluded services under the plan. Use this information to compare the portion of costs you might pay under different health plans Please note these coverage examples are based on self-only coverage.

Peg is Having a Baby (9 months of in-network pre-natal care and a hospital delivery)

Managing Joe’s type 2 Diabetes (a year of routine in-network care of a wellcontrolled condition)

Mia’s Simple Fracture (in-network emergency room visit and follow up care)

Diagnostic tests (ultrasounds and blood work)

Specialist visit (anesthesia)

This EXAMPLE event includes services like:

Primary care physician office visits (including disease education)

Diagnostic tests (blood work)

Prescription drugs

Durable medical equipment (glucose meter)

This EXAMPLE event includes services like:

Emergency room care (including medical supplies)

Diagnostic test (x-ray)

Durable medical equipment (crutches)

Rehabilitation services (physical therapy)

The plan would be responsible for the other costs of these EXAMPLE covered services.

of

HEALTH SAVINGS ACCOUNT (HSA)

Sta who enroll in a High Deductible Health Plan (HDHP) medical plan may be eligible to enroll in a Health Savings Account (HSA) through OMEGA Federal Credit Union.

An HSA is a tax-favored account that allows contributions on a pre-tax basis; funds may be used to pay for eligible medical expenses for you and your legal tax dependents, as determined by the IRS, enrolled in a HDHP. Your HSA funds, if not spent, rollover, accumulate year-to-year, and belong to you beyond employment with the YMCA of Greater Pittsburgh.

The Y contributes $875 to your HSA for Employee Only or $1750 for Employee + Family. This amount may be prorated if you become an eligible employee outside of the Open Enrollment period. See the HSA contribution schedule on page 16 for additional information.

2026

Annual Contribution Limits

Single: $4400

Family: $8750

Sta aged 55 and older are eligible for a catch-up contribution of $1,000 annually on top of the regular contribution limits

Who can have an HSA?

To be an eligible individual and qualify for an HSA, the taxpayer must meet the following requirements: Be covered by a high-deductible health plan (HDHP) on the first day of the month

Not be covered by other health insurance

Not be enrolled in Medicare (the individual can be HSA-eligible for the months before being covered by Medicare)

Not be eligible to be claimed as a dependent on someone else’s tax return

Shop for HSA eligible items online at hsastore.com

If you decide to enroll in HSA, contact Ashbourn Cramer (acramer@ymcapgh.org). You will be required to complete an HSA Enrollment in Dayforce, an online Omega Credit Union Membership Application and an Omega Credit Union HSA Application. To ensure your requested deductions are accurate, this process should be completed in a timely manner.

HSA CONTRIBUTION SCHEDULE

Employee Only HSA: Full Employer Contribution is $875 for eligible employees

Employee Eligibility Date Approx. ($) Approx. (%) Date Contributed

January 1st

February 1st

2nd Pay Date in January OR 1st Pay Date in February

1st Pay Date in February

March 1st 729.14 83.33% 1st Pay Date in March

April 1st

May 1st

1st Pay Date in April

1st Pay Date in May June 1st

1st Pay Date in June July 1st

1st Pay Date in July August 1st

1st Pay Date in August

1st Pay Date in September

October 1st 218.75 25.00% 1st Pay Date in October

November 1st

1st Pay Date in November

Employee + Family HSA: Full Employer Contribution is $1750 for eligible employees

Employee Eligibility Date

1st Pay Date in February

March 1st 1458.28 83.33% 1st Pay Date in March

April 1st 1312.50 75.00% 1st Pay Date in April

May 1st

66.67% 1st Pay Date in May June 1st

1st Pay Date in June July 1st 875 50.00% 1st Pay Date in July

August 1st 729.05 41.66% 1st Pay Date in August

September 1st 583.28 33.33% 1st Pay Date in September

October 1st 437.50 25.00% 1st Pay Date in October

November 1st 291.55 16.66% 1st Pay Date in November

December 1st 145.60 8.32% 1st Pay Date in December

UNDERSTANDING YOUR OPTIONS

Surest Gold

Why Choose a Health Plan from YMCA Employee Benefits:

Regardless of which plan you choose, a health plan from YMCA Employee Benefits guarantees you’ll have access to a large network of physicians and specialists, and comprehensive coverage for you and/or your family. With any of our plans, you’ll have the freedom of using any doctor or facility you want without needing a referral—though you’ll typically save a significant amount of money using doctors and/or facilities that are in-network. Choosing a plan from YMCA Employee Benefits means you’ll also have access to:

Preventive Care Covered at 100%

No copay, co-insurance, or deductible—as long as care is received from a network provider

Tools and Services to Make Informed Decisions

Enrollment in a YMCA Employee Benefits medical plan means you’ll have access to resources to help you estimate costs, find providers, and compare your options

Personal Support and Helpful Programs to Improve Your Health

Access to registered nurses, Wellness Coaching, personal health support advocates, and more—all at no extra cost to you

Additional

Benefits

of Choosing the Surest Gold plan:

Our Surest Gold plan is a ‘copay only’ plan, meaning there is no deductible to satisfy before benefits are paid, and no surprise costs later. When you need care, or a procedure, search the Surest member website for a provider near you and see your exact cost (copay) before you go.

No deductible

Your plan pays for covered services right away, no up-front deductible that needs to be met first

Doctor visits

Pay one flat copay for in-network visits to a primary doctor or specialist, or have a Virtual Visit using Doctor on Demand for free! No copays are required for in-network wellness/preventive care visits.

Low copays for prescription drugs

Pay a flat $15, $40, or $60 copay (depending on tier) for eligible prescription drugs at in-network retail pharmacies. Or save even more by ordering a 90-day supply through the mail. The copay for specialty drugs is $200.

How Would This Plan Cover Costs?

Your annual medical costs are unique to your health needs, family size, and financial situation. Choosing the right plan is a personal decision that only you can make. See below for examples of how this plan provides benefits to cover three individuals and their specific medical claims.

Dan is Dealing with Diabetes

Dan’s Type 2 Diabetes is well-controlled, but he still needs to see his doctor several times a year and has ongoing costs for medication and blood work to maintain control of his condition throughout the year. Knowing he has recurring costs to manage his diabetes, Dan prefers to set aside some money up front for estimated outof-pocket costs.

On this plan, Dan can estimate his annual expenses by multiplying his o ce visit and prescription drug copays by his expected usage. Since he has a good idea of these expected costs up front, he decides to contribute that amount into a Flexible Spending Account (FSA) to take advantage of the tax-saving benefits.

Penelope is Planning a Pregnancy

Penelope is hoping to get pregnant in the next year. She knows that she may have plenty of doctor’s visits to plan for throughout a pregnancy, plus regular screenings and ultrasounds—and not to mention the cost of delivery!

Penelope searches “maternity” on the Surest website and finds a list of options for delivering her baby nearby. On this plan, she finds that she will only be responsible for one flat copay for all standard covered services during both the pregnancy and the delivery of her baby and the amount of that copay depends on which birthing facility she chooses.

Carol is Calculating Costs

Carol and her family are generally in good health, but she knows illnesses or injuries aren’t always predictable. She and her husband have some money saved up just in case they need to pay for something unexpected during the year. Lo and behold, her daughter ended up in the emergency room with a broken leg!

Her daughter’s injury couldn’t have been predicted, but with this plan, Carol’s insurance covered the majority of the unexpected costs and she was only responsible for a copay for the ER visit, plus additional copays for follow-up o ce visits and tests/services. But she had enough money in her savings account to cover it.

IN SUMMARY

EXAMPLE COST $5,600

Includes a year of routine in-network o ce visits, diagnostic tests (blood work), prescription drugs, and durable medical equipment (glucose

Includes routine

The Surest Gold plan from YMCA Employee Benefits encourages members to check costs and compare options for doctors and procedures before making an appointment. Prices for health services that often occur together (like labs or x-rays ordered by your doctor) are bundled into a single copay to avoid suprise bills months later. Unlike other industries where you’re used to getting what you pay for, the Surest pricing model actually applies lower costs to higher-value care. This results in better savings opportunities, keeping the premium cost that you pay for coverage lower and helping you reduce your out-of-pocket costs throughout the year!

These breakdowns are meant as examples only to show what one may pay after enrolling in the Surest Gold plan. You should always compare all plans available to you (including deductibles, copays and out of pocket maximums) and take into consideration your financial well-being (your premium costs and ability to pay for unexpected claims) before selecting your health coverage.

The Summary of Benefits and Coverage (SBC) document will help you choose a health plan. The SBC shows you how you and the planw ould share the cost for covered health care services. NOTE: Information about the cost of this plan(called the premium) will be provided separately. This is only a summary. For more information about your coverage, or to get a copy of the complete terms of coverage, visit Join.Surest.com,Surest mobile appor call Surest Member Servicesat 1-866-683-6440. For general definitions of common terms, such as allowed amount,balance billing, coinsurance, copay, deductible, provider, or other underlinedterms,see the Glossary. You can view the Glossary at Healthcare.gov/sbc-glossary/ or call 1-866-487-2365to request a copy.

Important Questions Answers

What is the overalldeductible? $0

Are there services covered before you meet yourdeductible? Yes. Preventive Care.

Why This Matters

See the Common Medical Events chart below for yourcosts for services thisplancovers.

This plancovers some items and services even if you haven’t yet met the deductible amount. But a copayor coinsurancemay apply. For example, thisplan covers certain preventive serviceswithoutcost-sharingand before you meet your deductible . See a list of coveredpreventive servicesat Healthcare.gov/coverage/preventive-care-benefits/ Are there other deductiblesfor specific services? No

What is the out-of-pocket limitfor thisplan?

What is not included in the out-of-pocket limit?

Will you pay less if you use a network provider?

Fornetwork providers:

$5,500individual / $11,000family

Forout-of-network providers:

$11,000individual / $22,000family

Premiums,balance billingcharges and health care thisplandoesn’t cover.

Yes. See Join.Surest.com or call 1-866-683-6440for a list of network providers.

Do you need a referralto see a specialist? No

You don’thave to meetdeductiblesfor specific services.

The out-of-pocket limitis the most you could pay in a year for covered services.

If you have other family members in this plan, they have to meet their own out-of-pocket limitsuntil the overall family out-o f-pocket limithas been met.

Even though you pay these expenses, they don't count toward theout-of-pocket limit.

Thisplanuses aprovidernetwork. You will pay less if you use aproviderin the plan's network. You will pay the most if you use an out-of-networkprovider, and you might receive a bill from aproviderfor the difference between theprovider’scharge and what yourplan pays (balance billing). Be aware,yournetwork providermight use anout-of-network providerfor some services (such as lab work). Check with yourproviderbefore you get services.

You can see thespecialistyou choose without areferral.

What You Will Pay

Allcopaymentandcoinsurancecosts shown in this chart are after your deductiblehas been met, if a deductibleapplies. Common Medical Event Services You May Need

Non-routine diagnostic test: Up to$3,150 copay/visit

$150-$1,900copay/visit Up to $5,700copay/visit

Limitations, Exceptions, & Other Important Information*

Certain procedures performed in the office may have a higher office visit copay.

Copaysare listed as a range. Providersare assigned copays within the range based on treatment outcomes and cost information that identifies network providersthat provide costefficient care.

*Cost share applies to any other Telehealth service based on provider type. If you receive services in addition to office visit, additional copaysmay apply.

You may have to pay for services that are not preventive. Ask your providerif the services needed are preventive. Then check what your planwill pay for.

Copaysare listed as a range. Providersare assigned copays within the range based on treatment outcomes and cost information that identifies network providersthat provide costefficient care.

Prior authorizationis required for certain Non-routine diagnostic testsor there may be no coverage.

Copaysare listed as a range. Providersare assigned copays within the range based on treatment outcomes and cost information that identifies network providersthat provide costefficient care.

Prior authorization is required for certain imaging tests or there may be no coverage.

If you need drugs to treat your illness or condition

31-Day Supply

$15 copay

90-Day Supply

$35 copay

31-Day Supply

$40 copay

90-Day Supply

$100 copay

31-Day Supply

More information about prescription drug coverage is available at Optumrx.com Preventive Pharmacy 90-Day Supply No charge

$60 copay

90-Day Supply

$150 copay

31-Day Supply

$200 copay

If you need immediate medical attention

Physician/surgeon fees No charge No charge

Emergency room care

If you have a hospital stay Facility

$900 copay/visit

$900 copay/visit

Physician/surgeon fees No charge No charge

Certain Tier 1 drugs are available with no charge, including prescribed generic contraceptives and tobacco cessation medications.

To learn more about drug tiers and about copays for specific drugs, visit Optumrx.com website.

Prior authorization is required for certain drugs or there may be no coverage.

Specialty drugs are not covered at a 90-day supply.

Prior authorization is required for certain specialty drugs or there may be no coverage.

Copays are listed as a range. Providers are assigned copays within the range based on treatment outcomes and cost information that identifies network providers that provide costefficient care.

Prior authorization is required for certain outpatient surgery or there may be no coverage.

Copay is waived if admitted within 24 hours. Outof-network emergency room care visit copay applies to the in-network out-of-pocket limit.

Prior authorization is required for non-emergency medical transportation or there may be no coverage. Out-of-network emergency medical transportation copay applies to the in-network outof-pocket limit.

Copays are listed as a range. Providers are assigned copays within the range based on treatment outcomes and cost information that identifies network providers that provide costefficient care.

Prior authorization is required for non-emergency facility admissions and inpatient surgery or there may be no coverage.

Home/Office: $195 copay/visit

Outpatient Facility: $390 copay/visit

Certain procedures/services in the outpatient setting may have a lower copay.

Prior authorization is required for certain outpatient services or there may be no coverage. Inpatient services $2,000 copay/stay $6,000 copay/stay

Certain procedures/services in the inpatient setting may have a lower copay.

Prior authorization is required for certain inpatient services or there may be no coverage.

Cost sharing does not apply to preventive services with network providers.

If you are pregnant

Office visits No charge

$195 copay/visit

Childbirth/delivery professional services No charge No charge

Depending on the type of service, a copay may apply.

One copay for all covered services related to childbirth/delivery, including the newborn, unless discharged after mother.

Copays are listed as a range. Providers are assigned copays within the range based on treatment outcomes and cost information that identifies network providers that provide costefficient care.

Cost sharing does not apply to certain preventive services.

Prior authorization is required for inpatient stays beyond 48 hours following a normal vaginal delivery or 96 hours following a cesarean section delivery or there may be no coverage.

is required for certain home health care services or there may be no coverage.

are a combination of network providers

providers per person per plan

Copays are listed as a range. Providers are assigned copays within the range based on treatment outcomes and cost information that identifies network providers that provide costefficient care.

Excluded Services & Other Covered Services:

Services Your Plan Generally Does NOT Cover (Check your plan document for more information and a list of any other excluded services.)

Cosmetic surgery

Dental care (Adult)

Hearing aids Long term care

Non-emergency care when traveling outside the U.S

Weight loss programs

Other Covered Services (Limitations may apply to these services. This isn’t a complete list. Please see your plan document.)

Acupuncture (No visit limit)

Bariatric surgery

Chiropractic care (No visit limit)

Fertility treatment (Limitations apply)

Private duty nursing

Routine eye care (Adult) (limited to one exam per person per plan year.)

Routine foot care (for certain conditions)

Your Rights to Continue Coverage: There are agencies that can help if you want to continue your coverage after it ends. The contact information for those agencie s is: the Department of Labor’s Employee Benefit Security Administration at 1-866-444-EBSA (3272) or dol.gov/ebsa/healthreform. You may also contact Surest Member Services at 1-866-683-6440. Other coverage options may be available to you too, including buying individual insurance coverage through the Health Insurance Marketplace. For more information about the Marketplace, visit HealthCare.gov or call 1-800-318-2596.

Your Grievance and Appeals Rights: There are agencies that can help if you have a complaint against your plan for a denial of a claim. This complaint is called a grievance or appeal. For more information about your rights, look at the explanation of benefits you will receive for that medical claim. Your plan documents also provide complete information on how to submit a claim, appeal, or a grievance for any reason to your plan. For more information about your rights, this notice, or assistance, contact: Surest Member Services at 1-866-683-6440, or the Department of Labor’s Employee Benefits Security Administration at 1-866-444-EBSA (3272) or dol.gov/ebsa/healthreform

Does this plan provide Minimum Essential Coverage? Yes

Minimum Essential Coverage generally includes plans, health insurance available through the Marketplace or other individual mar ket policies, Medicare, Medicaid, CHIP, TRICARE, and certain other coverage. If you are eligible for certain types of Minimum Essential Coverage, you may not be eligible for the premium tax credit. Does this plan meet the Minimum Value Standards? Yes

If your plan doesn’t meet the Minimum Value Standards, you may be eligible for a premium tax credit to help you pay for a plan through the Marketplace. Language Access Services:

Spanish (Español): Para obtener asistencia en Español, llame al [1-866-633-2446]

Pennsylvania Dutch (Deitsch): Fer Hilf griege in Deitsch, ruf [1-866-633-2446] uff.

Tagalog (Tagalog): Kung kailangan ninyo ang tulong sa Tagalog tumawag sa [1-866-633-2446]

Samoan (Gagana Samoa): Mo se fesoasoani i le Gagana Samoa, vala’au mai i le numera telefoni [1-866-633-2446]

Carolinian (Kapasal Falawasch): ngere aukke ghut alillis reel kapasal Falawasch au fafaingi tilifon ye [1-866-633-2446]

Chamorro (Chamoru): Para un ma ayuda gi finu Chamoru, å’gang [1-866-633-2446].

To see examples of how this plan might cover costs for a sample medical situation, see the next section.

About these Coverage Examples:

This is not a cost estimator. Treatments shown are just examples of how this planmight cover medical care. Your actual costs will be different depending on the actual care you receive, the prices your providerscharge, and many other factors. Focus on the cost sharingamounts (deductibles, copayments,and coinsurance) and excluded servicesunder the plan. Use this information to compare the portion of costs you might pay under different health plans. Please note these coverage examples are based on self-only coverage.

FLEXIBILE SPENDING ACCOUNT (FSA)

A Flexible Spending Account (FSA) may be used to make pre-tax payroll deductions for qualified health expenses. An FSA allows employees to decrease their taxable income, due to funds being deducted on a pre-tax basis. FSA accounts only allow reimbursements for legal tax dependents of the sta , as determined by the IRS. This service is provided by ISOLVED.

2026 Annual Contribution Limits for Healthcare FSA: $3400

The Healthcare FSA allows for a rollover of funds up to $680. The regular Healthcare FSA covers medical, prescription, dental, vision and over the counter (OTC) medications/supplies. OTC medications/supplies are covered only with a prescription.

Who can have an FSA?

Anyone can contribute to an FSA if:

You have coverage under the Surest plan

You have waived YMCA benefits

Shop for FSA eligible items online at fsastore.com

additional complete pair of prescription eyeglasses non-covered items, including nonprescription sunglasses

INCLUDED WITH MEDICAL PLANS

YMCA - Select

SUMMARY OF BENEFITS

STANDARD PLASTIC LENSES

Find an eye doctor (Select Network)

• eyemed.com

• EyeMed Members App •For LASIK, call 1.800.988.4221

Heads up

You may have additional benefits. Log into eyemed.com/member to see all plans included with your benefits.

CONTACT LENSES

Contacts - Conventional

OTHER

- Disposable

Hearing Care from Amplifon network

Discounts on hearing exam and aids; call 1.877.203.0675 Not covered

Lasik or PRK From U.S. Laser Network 15%

FREQUENCY

Exam Once every 12 months Frame

Lenses

Contact Lenses

(Plan allows member to receive either contacts and frame, or frames and lens services)

Frame, lens and lens options must be purchased in the same transaction to receive full discount. Items purchased separately will be discounted at 20% off the retail price.

EyeMed reserves the right to make changes to the products available on each tier. All providers are not required to carry all brands on all tiers. For current listing of brands by tier,

Keep smiling Delta Dental PPO™

Save with PPO

Visit a dentist in the PPO1 network to maximize your savings.2 These dentists have agreed to reduced fees, and you won’t get charged more than your expected share of the bill.3 Find a PPO dentist at deltadentalins.com

Set up an online account

Get information about your plan, check benefits and eligibility information, find a network dentist and more. Sign up for an online account at deltadentalins.com

Check in without an ID card

You don’t need a Delta Dental ID card when you visit the dentist. Just provide your name, birth date and enrollee ID or Social Security number. If your family members are covered under your plan, they’ll need your information. Prefer to have an ID card? Simply log in to your account to view or print your card.

Save with a PPO dentist

Coordinate dual coverage

If you’re covered under two plans, ask your dental o ce to include information about both plans with your claim — we’ll handle the rest.

Understand transition of care

Generally, multi-stage procedures are covered under your current plan only if treatment began after your plan’s e ective date of coverage.4 Log in to your online account to find this date.

Get LASIK and hearing aid discounts

With access to QualSight and Amplifon Hearing Health Care5, you can receive significant savings on LASIK procedures and hearing aids. To take advantage of these discounts, call QualSight at 855-248-2020 and Amplifon at 888-779-1429.

1 In Texas, Delta Dental Insurance Company provides a dental provider organization (DPO) plan.

2 You can still visit any licensed dentist, but your out-of-pocket costs may be higher if you choose a non-PPO dentist. Network dentists are paid contracted fees.

3 You are responsible for any applicable deductibles, coinsurance, amounts over annual or lifetime maximums and charges for non-covered services. Out-of-network dentists may bill the difference between their usual fee and Delta Dental’s maximum contract allowance.

4 Applies only to procedures covered under your plan. If you began treatment prior to your effective date of coverage, you or your prior carrier is responsible for any costs. Group- and state-specific exceptions may apply. If you are currently undergoing active orthodontic treatment, you may be eligible to continue treatment under Delta Dental PPO. Review your Evidence of Coverage, Summary Plan Description or Group Dental Service Contract for specific details about your plan.

5 Vision corrective services and Amplifon’s hearing health care services are not insured benefits. Delta Dental makes the vision corrective services program and hearing health care services program available to you to provide access to the preferred pricing for LASIK surgery and for hearing aids and other hearing health services.

West Virginia: Learn about our commitment to providing access to a quality dentist network at deltadentalins.com/about/legal/index-enrollee.html

Benefit Highlights: Delta Dental PPO

REWARDING HEALTHY BEHAVIOR

WellnessWorks Program MEMBER INCENTIVES

August 1, 2025 - July 31, 2026

Help your YMCA lower the cost of coverage and earn up to $350 in gift card rewards!

Your rewards program has moved to Rally Engage!

Starting August 1, 2025, wellness rewards will no longer be accessible on the previous Rally website/app. You must log in to the new website or mobile app to access your wellness rewards for the 2025-2026 incentive period.

Visit ymca.rallyengage.com or download the Rally Engage mobile app and log in with your HealthSafe ID® .

Once you’re in the new site, take the Health Survey to get started and you’ll be on your way to earning up to $350 in gift card rewards!

HOW IT WORKS: LOG IN TO RALLY ENGAGE

Our wellness rewards program has moved to a new platform called Rally Engage. Visit ymca.rallyengage.com or download the Rally Engage mobile app and log in with your HealthSafe ID®

TAKE THE HEALTH SURVEY

Once you’re logged in, take the Health Survey to earn your first $50 in rewards and unlock all the other programs/activities. Once the survey is complete, you’ll also get a Rally Health Score, which measures where you are in your overall health journey.

CHOOSE YOUR PATH

Select from the programs and activities below to earn the remaining $300 of your gift card rewards. You’ll also earn digital Rally points that can be used to enter online sweepstakes for even more rewards. Once the program/activity has been completed, log back in to Rally Engage to redeem your rewards for e-gift cards from a large list of online vendors. Some activities are rewarded automatically once the claim has been received and may take a few weeks to show up as complete. After you’ve selected your gift card, you’ll receive an email with the code, or you can access it on the Rewards page.

All covered employees, retirees, and spouses/domestic partners are eligible to earn the gift card rewards. Adult children dependents over the age of 18 may create an account on Rally Engage and participate in the activities/programs below, however they are NOT eligible to earn gift card rewards.

Take the Rally Health Survey to unlock the options below

Complete three Rally Missions 2

Watch video about the Employee Assistance Program (EAP) benefit

Take two (2) Rally quizzes to learn more about your benefits

Set goals and track your daily steps with Rally Stride

Meet your goal at least 12 times during any calendar month to earn the reward for that month $25 per month!

NEW! Enroll in Wellos and attend 3 coaching sessions 2

Get an applicable preventive screening: 2

Annual Physical/Wellness Exam ( ≥18 yrs old)

Colorectal Cancer Screening ( >45 yrs old) 1

Mammogram Screening (Females ≥40 yrs old) 1

Cervical Cancer Screening (Females 21-65 yrs old) 1

Get a biometric screening (in-person or using an at-home kit from LetsGetChecked)

Complete 12 sessions of the YMCA’s Diabetes Prevention Program 2

Complete LIVESTRONG at the YMCA ® program for cancer survivors 2

Complete at least 9 sessions of the Real Appeal weight loss program 2

NEW! Complete the Quit for Life® tobacco cessation program 2

Participate in Virta to lose weight, or to reverse or prevent Type 2 diabetes and prediabetes Enroll in the treatment program - $50 Participate for at least 6 months - $100

CONDITIONAL ALTERNATIVE

The reward will be triggered after your doctor submits the claim.

If a medical condition makes it unreasonably di cult for a participant to achieve the standards for the incentives under this program, or if it is medically inadvisable for a participant to attempt to achieve the standards for the incentives under this program, participants may call the Senior Client Manager at 312-419-8786 to request a reasonable alternative.

Here

EMPLOYEE ASSISTANCE PROGRAM (EAP)

When you have a long list of stressors — and a longer list of to-dos

When you’re dealing with the pressures of ever yday life, it can be easy to simply smile and say, “I’m fine.” But sometimes, emotions like stress, sadness or even anger can linger

In those moments, Emotional Wellbeing Solutions is here for you. It’s a modern, flexible employee assistance program (EAP) that offers support for ever yday life. Call anytime to speak with an Emotional Wellbeing Specialist who’ll listen to your needs and connect you with resources that can help. It’s available to all members of your household, including children living away from home.

24/7 availability No cost to you

Support for

To learn more, scan the QR code or visit

To find the right support for you, register with your HealthSafe ID or enter your company access code: 9622

EmotionalWellbeing Solutionsisavailable24/7

Emotional Wellbeing Specialists are available by phone to provide help with a range of life concerns and stressors, including:

This includes referrals, seeing network providers, access to and initial consultations with Or sign in to This program should not be

Once eligible, the YMCA of Greater Pittsburgh contributes 11% of your gross annual salary into your retirement account.

SHORT TERM DISABILITY, LONG TERM DISABILITY AND FMLA

Short-Term Disability YMCA's Short Term Disability (STD) policy is set-up for any full-time employee who needs to be out of the workplace for more than 5 days due to: serious illness (example cancer) surgery, injury (not work related) or birth of a child (the mother).

Our STD policy is as follows

DAYS OF

0-5 DAYS

1ST FOUR WEEKS

2ND FOUR WEEKS

3RD FOUR WEEKS

4TH FOUR WEEKS - Up to 6 Months

LONG-TERM DISABILITY

Pay covered by STD

Employee must use PTO days

Employee is paid at 100%

Employee is paid at 80%

Employee is paid at 70%

Employee is paid at 60%

The YMCA o ers a long-term disability insurance plan to full-time employees. Long-term disability begins after short-term disability has been exhausted, which is a total of six (6) months for a personal illness, serious illness or injury. Medical documentation is required.

The plan pays 60% of your basic monthly earnings not to exceed a maximum monthly benefit of $5,000. Please refer to your plan manual for detailed information. Coverage is through the National Y Employee Benefits Plan.

FAMILY & MEDICAL LEAVE ACT (FMLA)

This policy is intended to comply with the Family and Medical Leave Act of 1993 (the “Act”) and shall be construed consistently with the Act and any applicable regulations

Eligibility

Employees are eligible for unpaid family and medical leave (“FMLA leave”) under this policy if they have been employed by The YMCA for at least 12 months and have worked at least 1,250 hours during the 12-month period immediately preceding the commencement of the FMLA leave

Coverage

When Leave Can Be Taken Eligible employees are entitled to FMLA leave for one or more of the following reasons:

For the birth of a child to an employee, and to care for such newborn child;

For placement with the employee of a son or daughter for adoption or foster care;

To care for the employee’s spouse, son, daughter, or parent with a serious health condition; or because of a serious health condition that makes the employee unable to perform the functions of the employee’s job.

A qualifying exigency arising out of the fact that an employee’s spouse, child or parent is called up for or is on active duty in the Armed Forces in support of a military contingency operation as defined by law and the employee’s circumstances justify his/her need for leave . . . . .

Parental Leave

The YMCA of Greater Pittsburgh will provide up to 12 weeks of paid parental leave to employees following the birth of an employee’s child or the placement of a child with an employee in connection with adoption or foster care. The purpose of paid parental leave is to enable the employee to care for and bond with a newborn or a newly adopted or newly placed child. This policy will run concurrently with Family and Medical Leave Act (FMLA) leave and in accordance with our Short-Term Disability payment schedule as applicable. This policy will be in e ect for births, adoptions or placements of foster children.

LIFE AND AD&D

At no cost to you, the YMCA of Greater Pittsburgh provides Basic Life and Accidental Death & Dismemberment (AD&D) insurance through Lincoln Financial Group. You are insured 2x your base annual salary to a maximum of $500,000. You can also purchase additional supplemental Life and Accidental Death & Dismemberment (AD&D) insurance through Lincoln Financial Group, for you, your spouse, and dependent children.

Additional Coverage Sta Can Purchase Up to 2x your base annual salary not to exceed $500,000 Dependent Spouse up to $10,000 Dependent Child(ren) up to $10,000

PAID TIME OFF (PTO) and HOLIDAYS

See The YMCA of Greater Pittsburgh Sta Handbook for more information about PTO and Holidays.

OTHER BENEFITS OFFERED BY YMCA GP

EMPLOYEE MEMBERSHIPS AND DISCOUNTS

A complimentary membership is a benefit o ered to our full-time, part-time and seasonal sta members. All sta who wish to use our facilities are required to have an active membership, including membership card and photo on file, and follow the same rules as our facility members.

Please review the qualifications for your discounted sta membership based on current employment type:

FULL-TIME EMPLOYEES

All exempt and non-exempt full-time employees are eligible for a free Association-Wide Family membership. Everyone on the full-time employee’s membership must live in the same household as the employee. There is a maximum of two adults (19+) permitted on the membership. Young Adults may remain on the membership in accordance with current IRS Guidelines at the time of sign-up.

PART-TIME EMPLOYEES

All part-time employees are eligible for a free Association-Wide Individual membership. Part-Time employees have the option to upgrade to an Association-Wide Family Membership for an additional $25 per month. There is a maximum of two adults (19+) permitted on the membership. Young Adults may remain on the membership in accordance with current IRS Guidelines at the time of sign-up.

EMPLOYEE DISCOUNTS

All active employees receive a 25% discount on programs for either themselves or members of their household, dependent upon their active membership type.

Additional discounts available to YMCA of Greater Pittsburgh employees:

Employee Discounts Keep more money in your pocket

Car Rental

Enterprise Holdings offers a discount on leisure/personal travel. Check with your organization for other codes if you are doing business travel. Savings is off the base rental price of vehicles. Taxes, fees, and insurance are NOT included. 1. Go to https://www.nationalcar.com 2. Fill out the reservation information 3. Use the Contract ID: XZ78989

Retail Discounts

Create an account with Staples to easily order online using your organization’s discounted pricing, pay with a personal credit card, and have items shipped directly to your home. Register your account online. The address you indicate when registering will be your delivery/shipping address. You will receive a Welcome email from

second email prompting you to add a phone used at checkout in any U.S. Staples retail store to receive the organization’s pricing or the in-store price – whichever is lower. For questions, contact Staples Customer Service by phone at 877-826-7755 or by email at support@staplesadvantage.com.

Corporate Shopping is an online site that conveniently combines several great deals and discounts to major retail stores all in one place. Create an account at:

our partnership with HealthTrust and program vendors. Please note, discounts are based off of full retail price. Some local sales or other promotions may provide more competitive pricing from time-to-time.

Discount codes should NOT be shared with anyone other than staff at your organization or posted publicly online.

To take advantage of this offer, visit http:// pbpp.sherwin-williams.com/hpg-memberemployees/ You will be able to print a discount card that can be used at Sherwin Williams stores nationwide on a number of paint products and supplies. Offer excludes Duration & Emerald Coatings and spray equipment.

Prescriptions

FamilyWize offers a free program that saves consumers an average of 42% on prescription medications. It covers all FDA-approved drugs and can be used at over 60,000 pharmacies nationwide. Discounts can be used with or without existing insurance coverage. Visit https://www.familywize.org to look up anticipated savings by drug name or type and to get access to the prescription discounts.

HELPFUL BENEFITS TERMS AND CONDITIONS

Co-insurance - A percentage of a health care cost—such as 20 percent—that the covered employee pays after meeting the deductible.

Co-payment-The fixed dollar amount—such as $25 for each doctor visit—that the covered employee pays for medical services.

Deductible- A fixed dollar amount that the covered employee must pay out of pocket each calendar year before the plan will begin reimbursing for non preventative health expenses. Plans usually require separate limits per person and per family.

Formulary- A list of prescription drugs covered by the health plan, often structured in tiers that subsidize low-cost generics at a higher percentage than more expensive brand-name or specialty drugs.

Health savings account (HSA) - HSAs may be opened by employees who enroll in a high-deductible health plan. Employees can put money in an HSA up to an annual limit set by the government, using pre-tax dollars. Employers may also contribute funds to these accounts within the prescribed limit. HSA funds may be used to pay for medical expenses whether or not the deductible has been met, and no tax is owed on funds withdrawn from an HSA to pay for medical expenses. HSAs are individually owned and the account remains with an employee after employment ends.

High-deductible health plan (HDHP)- An HDHP features higher annual deductibles than traditional health plans, such as a preferred provider organization (PPO) or health maintenance organization (HMO) plan. With the exception of preventive care, covered employees must meet the annual deductible before the plan pays benefits. HDHPs, however, may have significantly lower premiums than a PPO, HMO or other traditional plan.

In-network- Doctors, clinics, hospitals and other providers with whom the health plan has an agreement to care for its members. Health plans cover a greater share of the cost for in-network health providers than for providers who are out-of-network.

Out-of-network- A health plan will cover treatment for doctors, clinics, hospitals and other providers who are out-of-network, but covered employees will pay more out-of-pocket to use out-of-network providers than for in-network providers.

Out-of-pocket limit- The most an employee could pay during a coverage period (usually one year) for his or her share of the costs of covered services, including co-payments and co-insurance.

Premium- The amount that must be paid for a health insurance plan by covered employees, by their employer, or shared by both. A covered employee's share of the annual premium is generally paid periodically, such as monthly, and deducted from his or her paycheck.

MEDICARE PART D CREDITABLE COVERAGE NOTICE

Important Notice from The YMCA of Greater Pittsburgh about Your Prescription Drug Coverage and Medicare

Please read this notice carefully and keep it where you can find it. This notice has information about your current prescription drug coverage with The YMCA of Greater Pittsburgh and about your options under Medicare’s prescription drug coverage. This information can help you decide whether or not you want to join a Medicare drug plan. If you are considering joining, you should compare your current coverage, including which drugs are covered at what cost, with the coverage and costs of the plans o ering Medicare prescription drug coverage in your area. Information about where you can get help to make decisions about your prescription drug coverage is at the end of this notice.

There are two important things you need to know about your current coverage and Medicare’s prescription drug coverage: Medicare prescription drug coverage became available in 2006 to everyone with Medicare. You can get this coverage if you join a Medicare Prescription Drug Plan or join a Medicare Advantage Plan (like an HMO or PPO) that o ers prescription drug coverage. All Medicare drug plans provide at least a standard level of coverage set by Medicare. Some plans may also o er more coverage for a higher monthly premium.

The YMCA of Greater Pittsburgh has determined that the prescription drug coverage o ered by the The YMCA of Greater Pittsburgh is, on average for all plan participants, expected to pay out as much as standard Medicare prescription drug coverage pays and is therefore considered Creditable Coverage. Because your existing coverage is Creditable Coverage, you can keep this coverage and not pay a higher premium (a penalty) if you later decide to join a Medicare drug plan.

When Can You Join A Medicare Drug Plan?

You can join a Medicare drug plan when you first become eligible for Medicare and each year from October 15th to December 7th. However, if you lose your current creditable prescription drug coverage, through no fault of your own, you will also be eligible for a two (2) month Special Enrollment Period (SEP) to join a Medicare drug plan.

What Happens To Your Current Coverage If You Decide to Join A Medicare Drug Plan?

If you decide to join a Medicare drug plan while enrolled in The YMCA of Greater Pittsburgh’s coverage as an active employee, please note that your The YMCA of Greater Pittsburgh’s coverage will be the primary payer for your prescription drug benefits and Medicare will pay secondary. As a result, the value of your Medicare prescription drug benefits will be significantly reduced. Medicare will usually pay primarily for your prescription drug benefits if you participate in The YMCA of Greater Pittsburgh’s coverage as a former employee.

You may also choose to drop your The YMCA of Greater Pittsburgh’s coverage. If you do decide to join a Medicare drug plan and drop your current The YMCA of Greater Pittsburgh’s coverage, be aware that you and your dependents may not be able to get this coverage back.

When Will You Pay A Higher Premium (Penalty) To Join

A Medicare Drug Plan?

You should also know that if you drop or lose your current coverage with The YMCA of Greater Pittsburgh and don’t join a Medicare drug plan within 63 continuous days after your current coverage ends, you may pay a higher premium (a penalty) to join a Medicare drug plan later.

If you go 63 continuous days or longer without creditable prescription drug coverage, your monthly premium may go up by at least 1% of the Medicare base beneficiary premium per month for every month that you did not have that coverage. For example, if you go nineteen months without creditable coverage, your premium may consistently be at least 19% higher than the Medicare base beneficiary premium. You may have to pay this higher premium (a penalty) as long as you have Medicare prescription drug coverage. In addition, you may have to wait until the following October to join

For more information about Medicare prescription drug coverage: Visit www.medicare.gov

Call your State Health Insurance Assistance Program for personalized help 1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048.

If you have limited income and resources, extra help paying for Medicare prescription drug coverage is available. For information about this, visit Social Security on the web at www.socialsecurity.gov, or call them at 1-800-772-1213 (TTY 1-800-325-0778

PROVIDERS CONTACT INFORMATION

Refer to this list if you need to contact one of your benefit providers. For general information about your benefits, contact Ashbourn Cramer (acramer@ymcapgh.org)