HowtheFed'sRateDecisionAffectsYourMoney

On May 1, the US Federal Reserve maintained interest rates at their highest level in 23 years for the sixth consecutive meeting, aiming to combat persistent inflation. The US central bank unanimously decided to keep the benchmark lending rate steady at 5 25 to 5.50 percent, citing a "lack of further progress" towards its 2 percent inflation target.

The Fed indicated it would not consider lowering rates until it had "greater confidence" that inflation was sustainably moving toward its target. Federal Reserve Chair Jerome Powell stated in a press conference, "It is likely that gaining such greater confidence will take longer than previously expected " While the US central bank is prepared to maintain high rates as long as necessary, Powell also mentioned that another rate hike is "unlikely" in the near future.

How Will This Affect Us?

Singapore's interest rates are influenced by global rates and foreign exchange market expectations, generally aligning with the direction set by other central banks, particularly the US Fed.

With a Fed rate cut, Singapore's domestic interest rates might follow a downward trend due to the global search for yield. This reduction in interest rates can lead to cheaper borrowing costs for businesses and consumers, stimulating economic activity. However, MAS will also consider other factors, such as domestic inflation and economic conditions, in its policy decisions

A decrease in interest rates generally leads to lower returns on savings deposits. Some banks in Singapore have already lowered the interest rates on their flagship savings accounts.

Fixed deposits interest rates have already fallen and are unlikely to increase, even though the Fed has paused its rate hikes.

“We won’t see the promotional interest rates that we saw previously last year. That’s when everyone was rushing to a bank,” said Mr Thum, senior research analyst at Phillip Securities Research. “I don’t think we’ll see that because of the uncertainty.”

Veronica.joan@manulifefa.com.sg | +65 9763 2325 | https://www.linkedin.com/in/veronica-joan-moreira/

MONEY MATTERS

Q2 2024 CLIENT UPDATES

A Federal Reserve rate cut has widespread implications for global economies, including Singapore. Lower U.S. interest rates can lead to capital inflows, a stronger SGD, and lower domestic interest rates in Singapore. For savers, this environment means lower returns on deposits but potential gains in higheryielding investments and property.

Strategic Considerations for Singapore Savers

Diversification:

In a low-interest-rate environment, diversifying across asset classes can help manage risk and enhance returns. This includes balancing between equities, bonds, real estate, and other investments.

Exploring Higher-Yield Investments:

Savers should explore higher-yielding investment options such as corporate bonds, dividend-paying stocks, and real estate investment trusts (REITs) to compensate for lower returns on savings accounts.

Reviewing Financial Goals:

Assessing and adjusting financial goals in response to changing interest rates can ensure savers remain on track to meet their long-term objectives. This might involve increasing investment contributions or reallocating assets

Let's meet for coffee to discuss adjusting your financial goals in response to changing interest rates. Use this opportunity to take advantage of our current promotions and ensure you’re on track for your long-term financial goals!

Source:https://www channelnewsasia com/singapore/fed-interest-rates-banksloans-savings-fixed-deposit-cna-explains-4309016

Veronica.joan@manulifefa.com.sg | +65 9763 2325 | https://www.linkedin.com/in/veronica-joan-moreira/

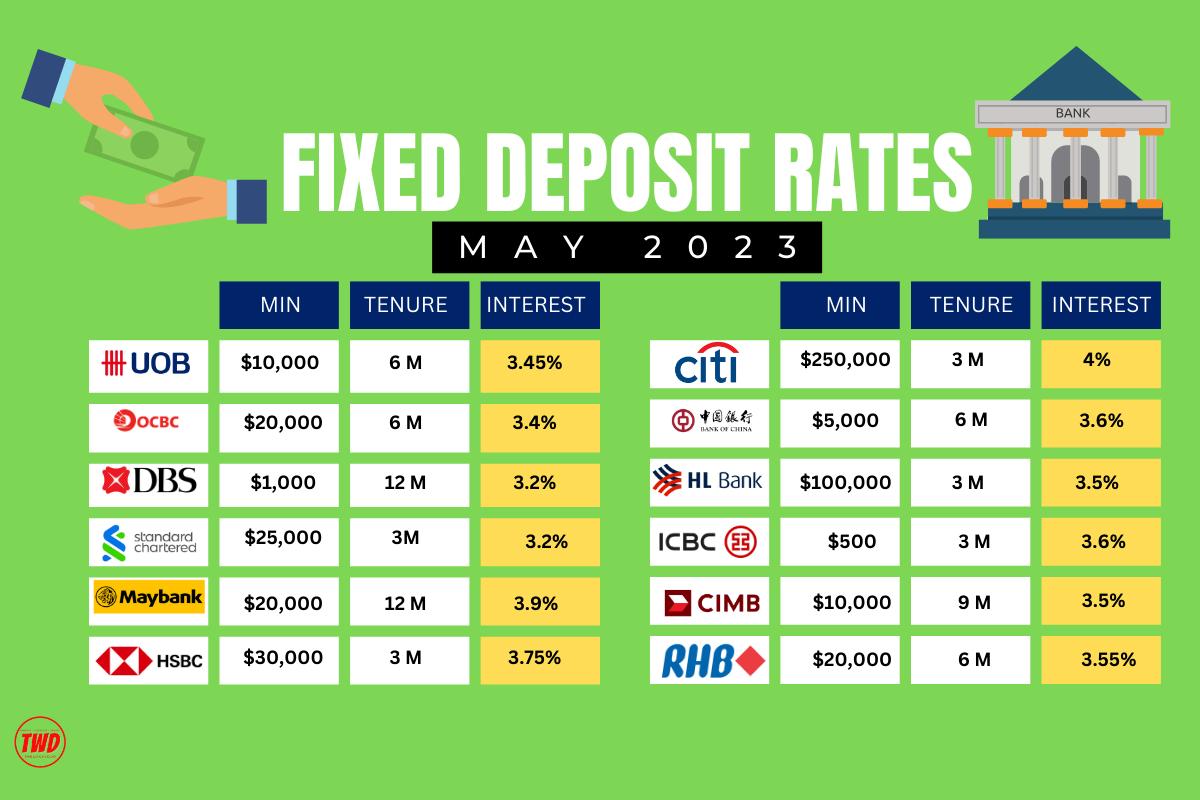

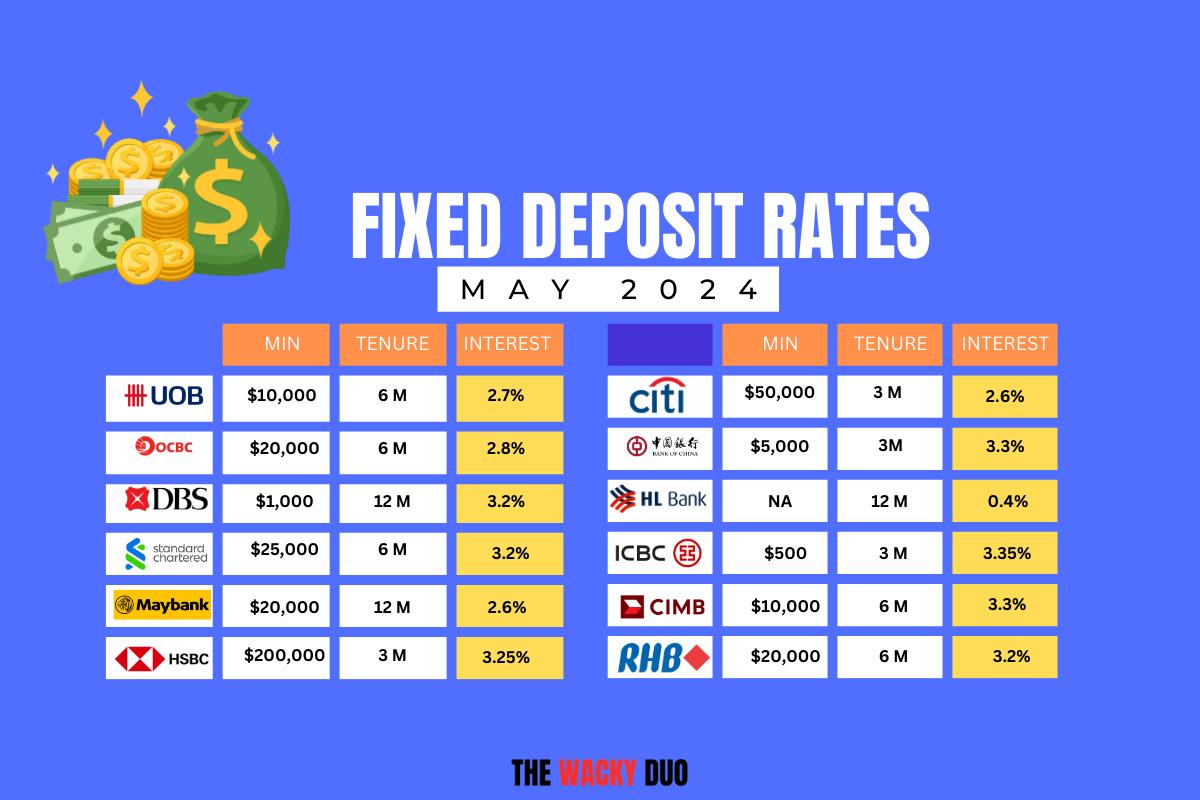

of 2023 vs 2024 fixed deposit rates [Source:https://www thewackyduo com/]

Comparison

Q2 2024 CLIENT UPDATES MARKET INDICES (Source: https://finance yahoo com/world-indices/?guccounter=1&guce referrer=aHR0cHM6Ly93d3cuZ29vZ2xlLmNvbS8&guce referrer sig=AQAAADerD 3dmgl78HRpMGz11xZkC4EqHqDW-xvNIMY178NiwWUlh9G29uCoMW- CLuCOcHn0otTlbhFKJNTsGwORmbU1RsKA81BuDBDTOWyA8IAGldbveHGXh-zQOPFIY5UCQ4Bs0T99BArbNg3SRJf6Oe1JQO6lmyxGuPo9I4e03y Veronica.joan@manulifefa.com.sg | +65 9763 2325 | https://www.linkedin.com/in/veronica-joan-moreira/

MONEY MATTERS

MONEY MATTERS

Q2 2024 CLIENT UPDATES

From 2025, the Special Account will be scrapped for those aged 55 and above. When that happens, savings from members’ Special Account will be transferred to their Retirement Account, up to the Full Retirement Sum (currently set at S$213,000 for 2025). Any remaining Special Account savings will be transferred to their Ordinary Account, which currently earns 2.5 per cent per annum.

CPF members, particularly those who have substantial SA savings after turning age 55 are reviewing their retirement plans. They will probably look for alternatives to beat the performance of 2.5% risk-free, which is offered by the CPF-OA.

Here are some of our suggestions:

Transfer OA savings to RA up to the new ERS amount:

You will be able to enjoy higher monthly CPF Life payouts as this will be 4 times of BRS from 2025, which translates to $426,000

Source: https://www.mof.gov.sg/docs/librariesprovider3/budget2024/download/pdf/annexf1.pdf

However, take note that this method is irreversible and the transferred funds can no longer be withdrawn.

Invest OA monies under the CPF Investment Scheme (CPFIS):

Members can use OA monies to invest in T-bills, fixed deposits, insurance plans, unit trusts, and so on, depending on risk profile, financial knowledge, and objectives. When the investment is liquidated, the proceeds return to OA.

An example would be the 6-month T-bill issued by the Singapore government, which sits at a yield of 3.65% at the time of writing. The biggest benefit? It’s relatively liquid with a short lock-in period of only six months and offers a respectable yield, while having low counterparty risk (which is the Singapore government).

The downside? The reinvestment risk due to the short-term nature of the T-bill Considering that the US Fed has intentions of lowering rates in the near future, the Singapore T-bill yield is not expected to stay at such a high rate for long, and investors will have to bear the consequences of reinvestment risk – six months later, how are you going to allocate the capital?

Veronica.joan@manulifefa.com.sg | +65 9763 2325 | https://www.linkedin.com/in/veronica-joan-moreira/

CPFSPECIALACCOUNTCLOSURE:ALOOKATALTERNATIVE INVESTMENTS

MONEY MATTERS

Q2

2024 CLIENT UPDATES

Withdraw savings (beyond the FRS) for investments and/or insurance that are not covered under CPFIS:

Private insurers do offer Retirement Income plan which provides a monthly income during retirement. In addition, such plans provide Insurance coverage and more flexibility compared to CPF Life. The other option is Investment Linked Plan (ILP) and/or investment into unit trusts, ETF and shares to generate potentially higher returns, with higher risk too.

Reachouttometoday tounderstandmore abouttheCPFchanges andtheinvestment alternativesavailable!

Veronica.joan@manulifefa.com.sg | +65 9763 2325 | https://www.linkedin.com/in/veronica-joan-moreira/

MONEY MATTERS

Q2 2024 CLIENT UPDATES

SQ321 TURBULENCE – REMINDER TO TRAVELLERS

Air travellers everywhere must have followed news of turbulence-hit

Singapore Airlines (SIA) flight SQ321 with a shudder - another one of the many fears about flying that have become reality recently.

Travel insurance can provide financial cover for many eventualities and situations that travellers might encounter when abroad. This can include:

Accidental death and permanent disability and dismemberment

Medical expenses (paying for medical treatment whilst you are abroad)

Medical repatriation (return you to your home country)

Loss/damage or theft of luggage, money, passport or personal possessions

The 229 crew and passengers on board Flight SQ321 were violently shaken by sudden and extreme turbulence as the Boeing 777 aircraft was en-route from London to Singapore, forcing the jet to make an emergency landing in Bangkok on Tuesday afternoon.

Several dozen people suffered traumatic, and potentially life-changing, injuries:

Some patients encountered paralysis

22 patients are being treated for spinal and spinal cord injuries.

6 are being treated for skull and brain trauma.

A 73-year-old Briton died of a suspected heart attack.

This unfortunate incident, has highlighted the importance for travellers to obtain travel insurance.

Cancellation or curtailment of trip

Expenses for a close relative or friend to stay with you or travel from the home country to accompany you

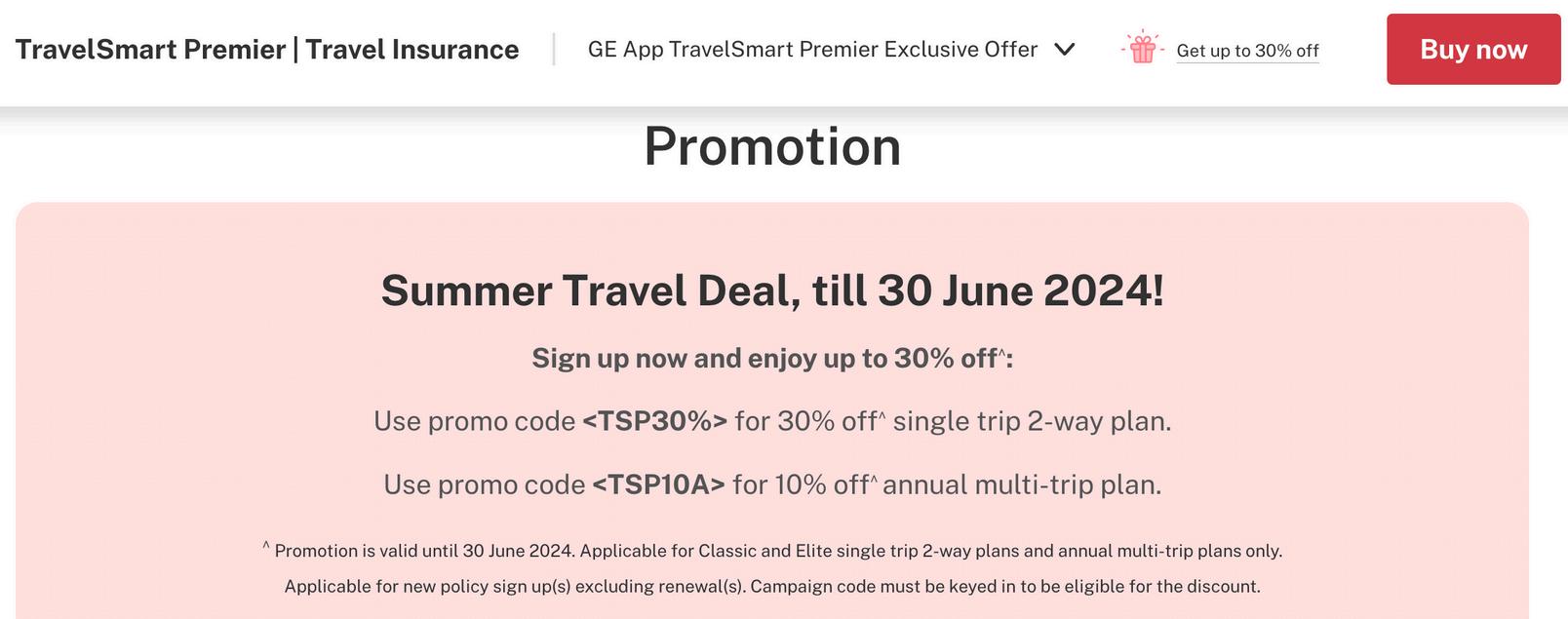

Travel insurance will give you peace of mind while travelling. Take advantage of these travel insurance promotions and safeguard your upcoming trips:

Veronica.joan@manulifefa.com.sg | +65 9763 2325 | https://www.linkedin.com/in/veronica-joan-moreira/

UPCOMING EVENTS MONEY MATTERS

Q1 2024 CLIENT UPDATES

Being our valued clients, you are entitled to join our exclusive seminars and events, and here are our upcoming events; focusing on your retirement and estate planning goals.

Writing a will and having a lasting power of attorney are crucial steps in ensuring your wishes are respected and your affairs are managed effectively.

A will outlines how you want your assets distributed after your death, providing clarity and preventing potential disputes among beneficiaries

A lasting power of attorney, on the other hand, designates someone to make decisions on your behalf if you become incapacitated, ensuring your financial and health care preferences are upheld.

Together, they offer comprehensive protection and peace of mind, covering both end-of-life asset distribution and management of your affairs during your lifetime if you cannot do so yourself

Take control of your future today— register with me to get a spot and find out more!

Veronica.joan@manulifefa.com.sg | +65 9763 2325 | https://www.linkedin.com/in/veronica-joan-moreira/