• Automate Interactions & Notifications to Streamline Hand-offs Between Parties

To lead what’s next, you need to think differently now.

Investment professionals leading today’s markets aren’t just knowledgeable—they bring clarity, judgment, and a deep understanding of where capital is moving next.

The CAIA Charter gives you all three.

If you want to stay relevant, build influence, and earn the confidence to navigate what’s coming next, CAIA is where you start.

Learn more at caia.org.

Next isn’t coming. It’s here.

The Power of Integrating Technology and Investment Operations

by Frank Caccio, OpsCheck

Brian Goldblatt, Prager Metis Strategic Audit Selection for Investment Funds: The Six-Factor Framework for Success

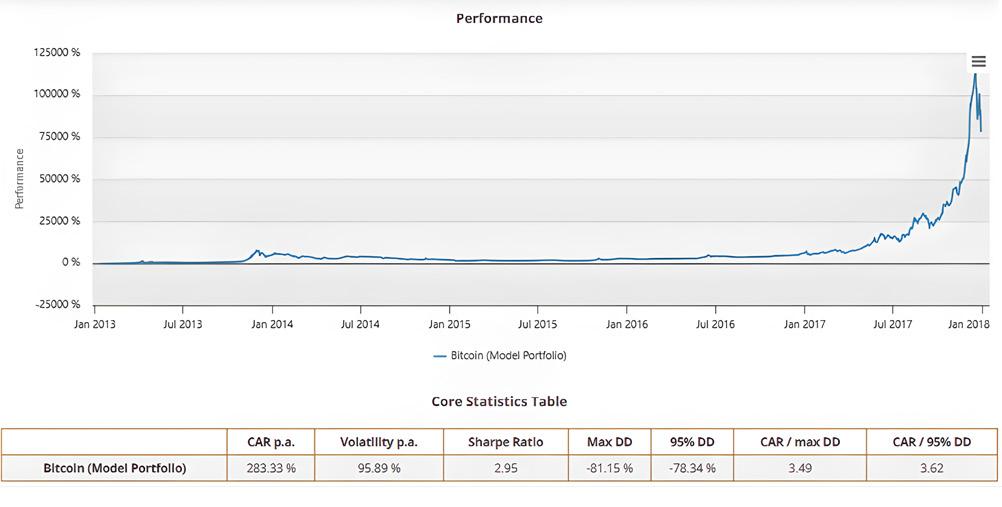

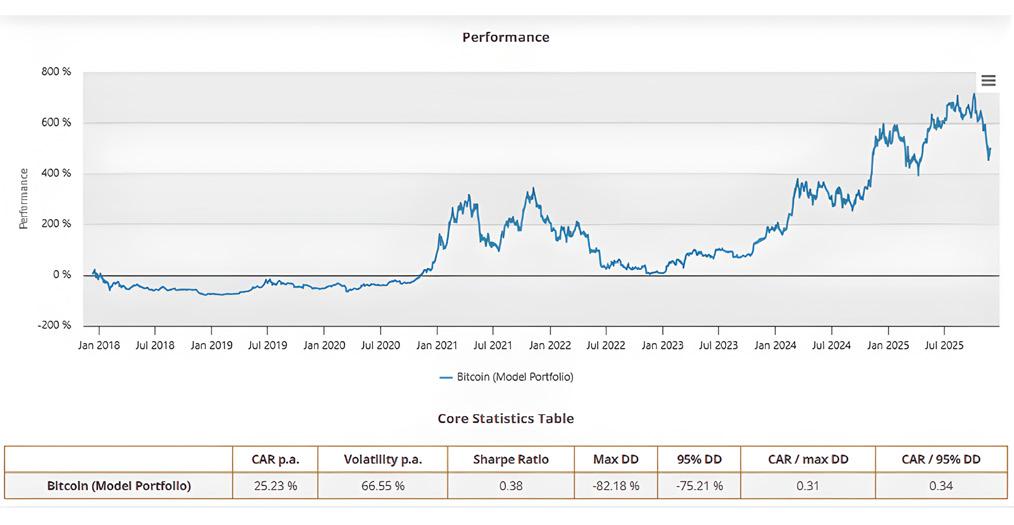

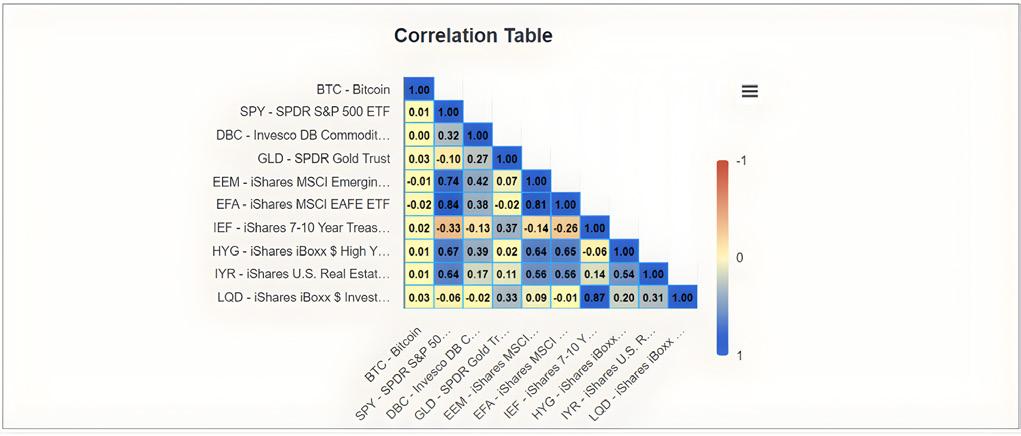

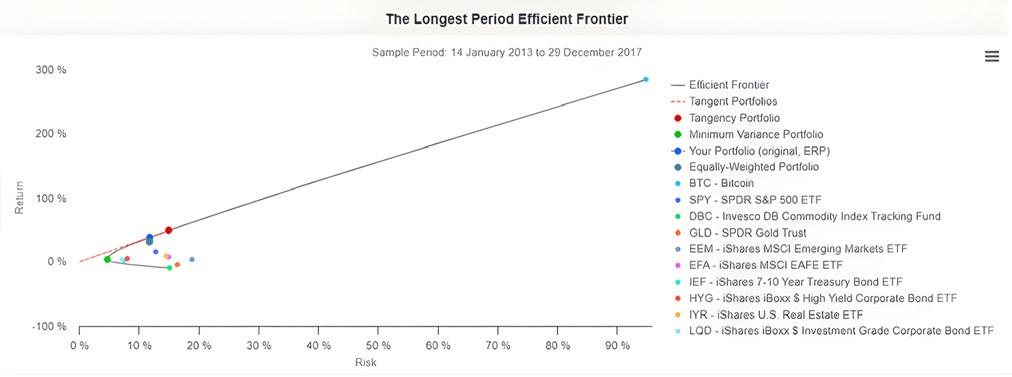

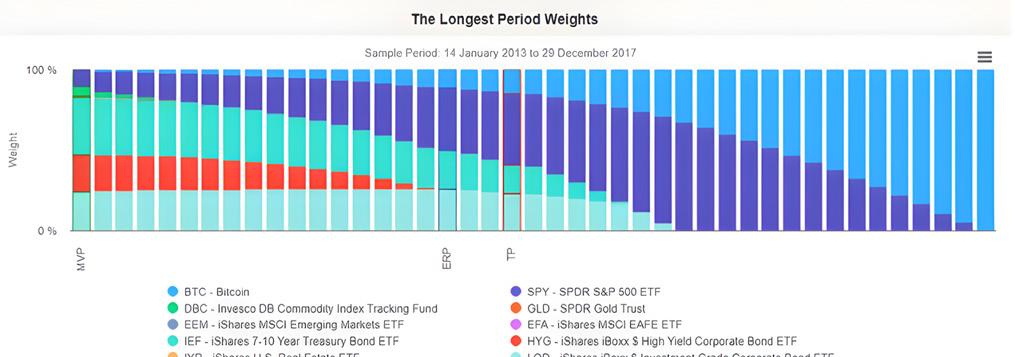

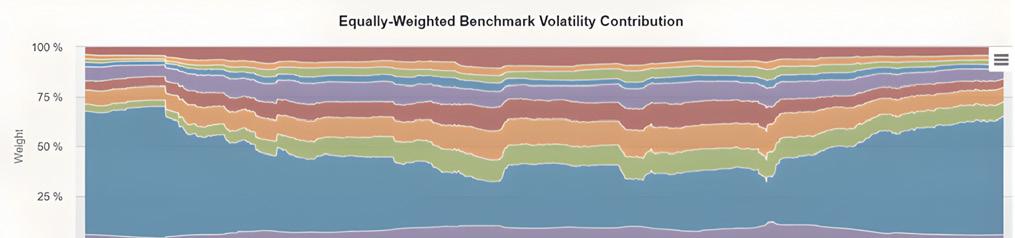

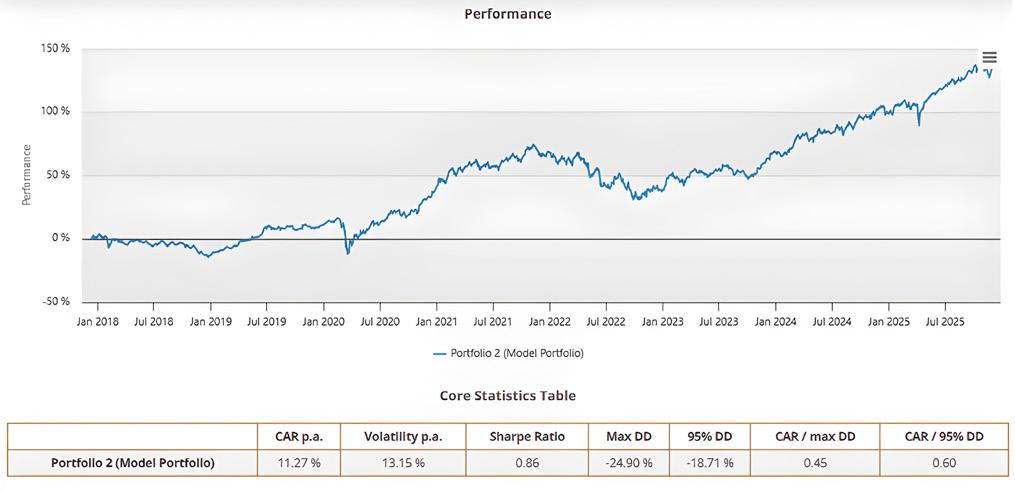

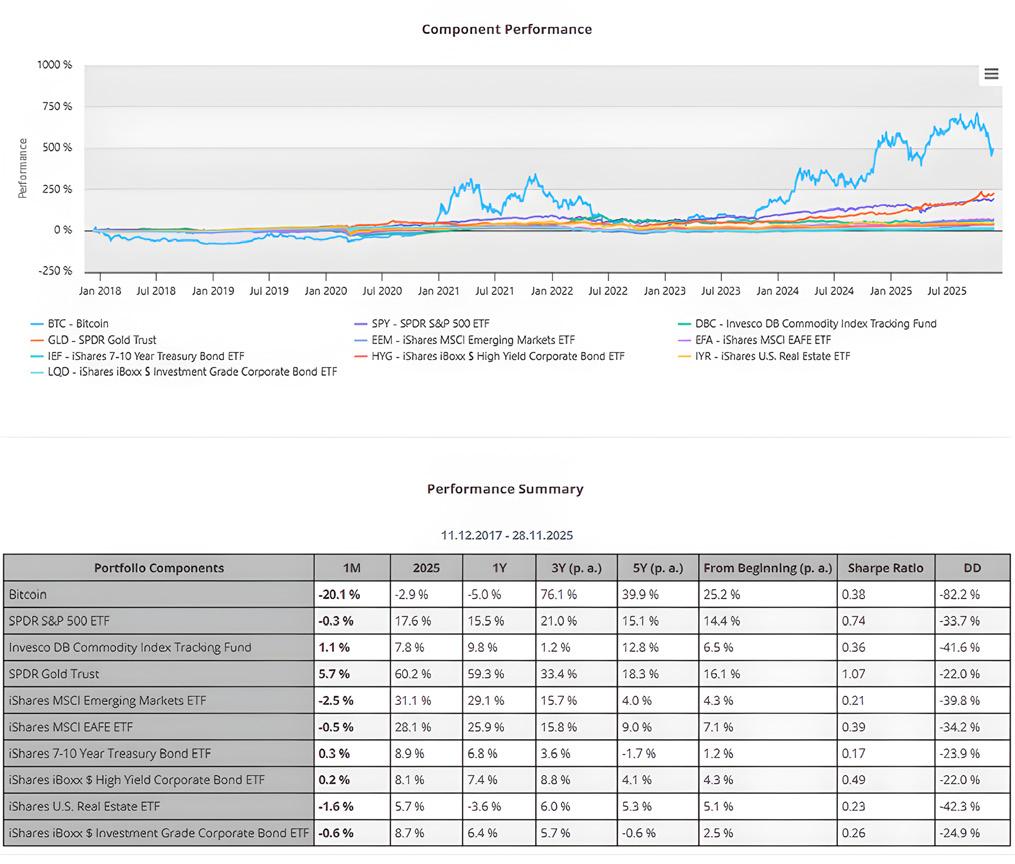

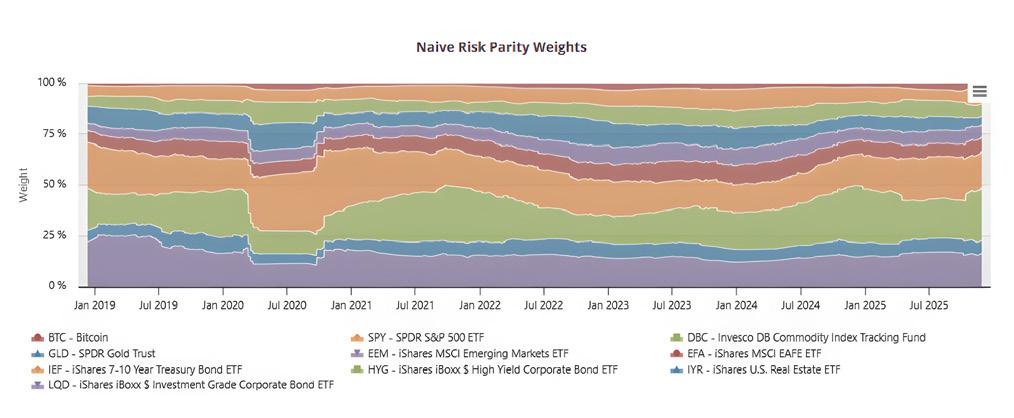

Radovan Vojtko, Quantpedia What Is the Optimal Passive Allocation to Bitcoin in a Diversified Portfolio?

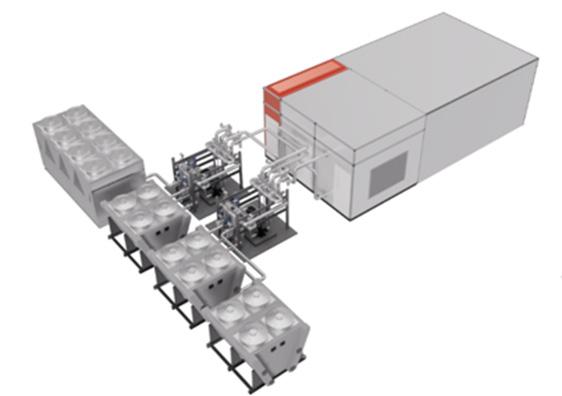

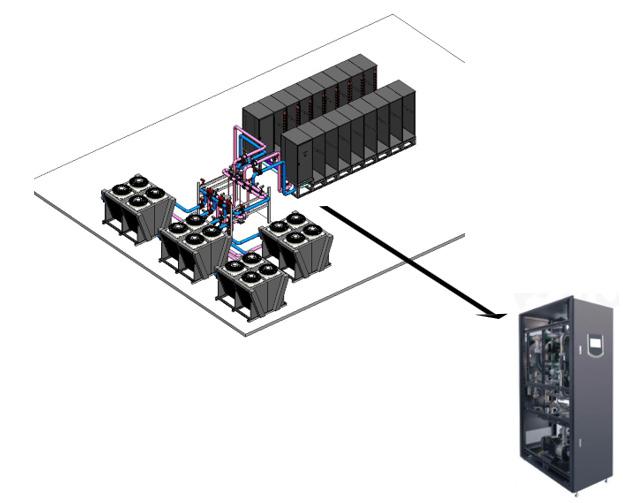

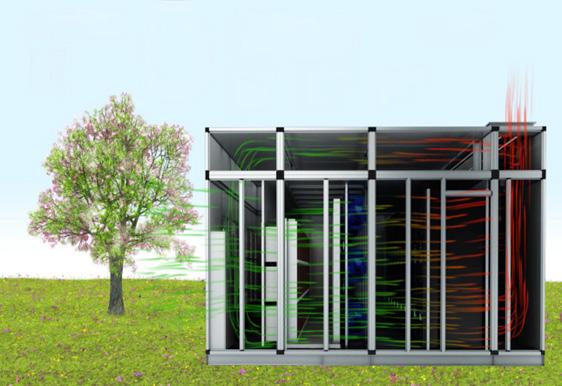

Daniel Robbins, RakworX The Future of Modular Data Centers for AI Systems

John Pavia, Siena Lane Partners Italy is on Everyone’s Shortlist? Really?

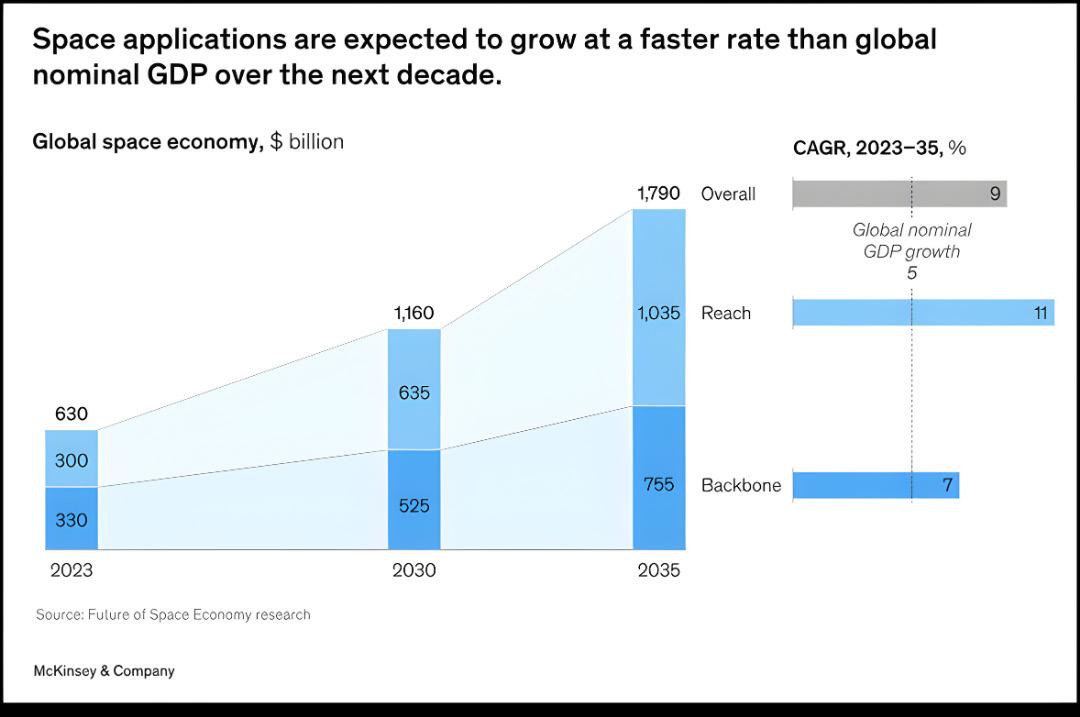

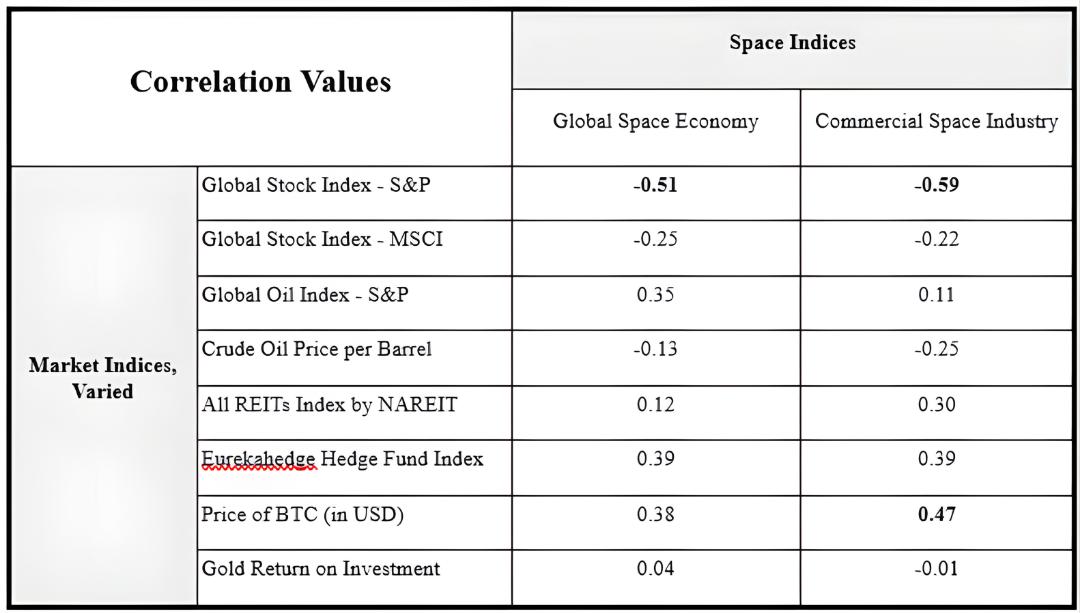

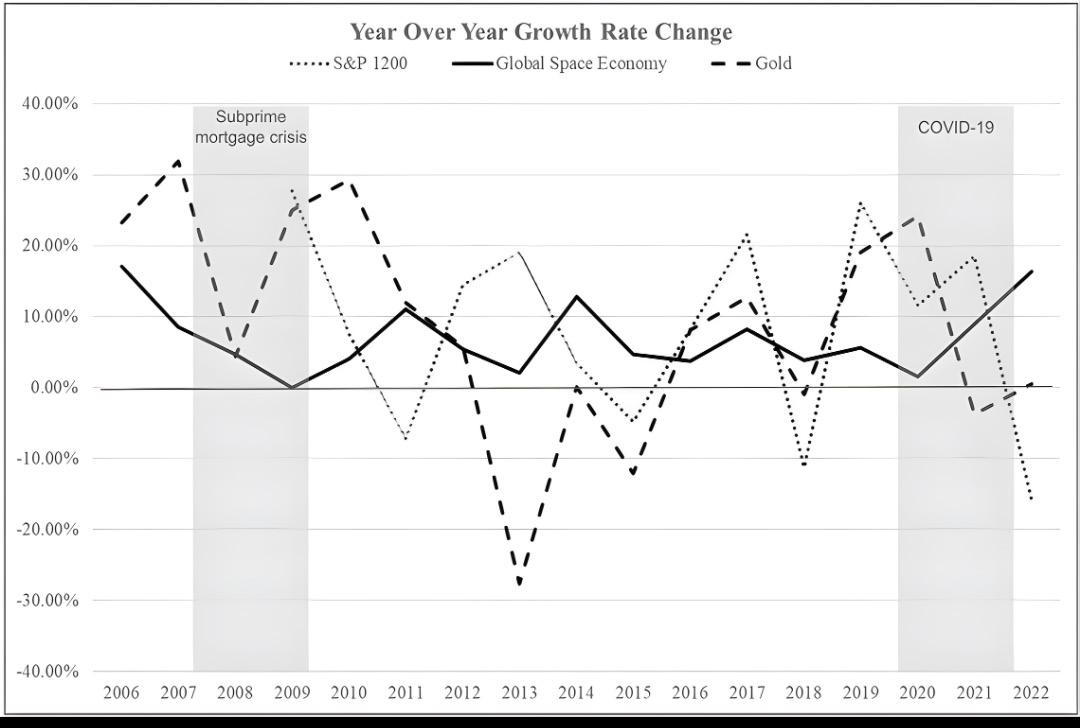

Meagan Murphy Crawford, SpaceFund

Chuck Stormon, StartFast Ventures The 2026 AI Investor's Playbook: Where Alpha Actually Lives

Adam Cohn, TradeStation Liquidity in Motion: The New Market Structure Shaking Up Alternative Assets

James Putra, TradeStation Trading Interfaces in the Age of AI: Why LLMs Might Make Them Obsolete

Intermediary Arms Race: Using Differentiated Alts to Defend Against the $124T Wealth Churnture Shaking Up

Peter Murrugarra & Geoff Marcus, IntiOne

David X Martin & Enrico Dallavecchia, Arctium

SEEKING CARIBBEAN ALPHA IN 2026

BY ADAM GREENFADER & NATHAN WHIGHAM AG&T and EN Capital

What Was the Lock, and What Is Now Opening

The Caribbean has never been an easy market for traditional capital. Even in stable cycles, the region demands patience, local knowledge, and flexible structuring. Regulation is extensive, traditional lenders maintain conservative risk tolerance, and the region’s geographic diversity limits the ability of large institutions to scale efficiently.

Why The Caribbean Works for Investors

For investors, the Caribbean opportunity increas-

ingly lies in high yield with controlled risk. When risk is assessed based on observed default behavior rather than perception, well structured Caribbean real estate often performs more defensively than traditional markets. Assets rarely fail in isolation. In close knit island markets, long term relationships and reputation strongly influence sponsor behavior. Lending terms in the Caribbean often reflect this dynamic. Transparency and direct communication between sponsors and lenders are not optional. They are part of the market culture. Caribbean loans also tend to be structured with tighter oversight, clearer cash control mechanisms, and more frequent lender reporting. These features provide lenders with earlier visibility into asset performance and

allow issues to be addressed before they escalate.

Risk is further mitigated by high barriers to entry Limited land availability, restrictive zoning, environmental protections, coastal constraints, and rising replacement costs make it difficult for competing projects to quickly come online. In many islands, new supply is structurally constrained, supporting long term pricing power and asset values.

This combination of tangible collateral, multiple exit paths, and constrained competition creates return profiles that are both yield enhanced and structurally resilient. As a result, private credit, preferred equity, and structured equity strategies tied to these markets are attracting increased attention from private wealth and institutional investors.

From Capital Contraction to Transition

The period from 2023 through 2025 marked one of the most restrictive credit environments in recent memory. Bank failures in 2023, combined with the full implementation of Basel III capital requirements, forced traditional lenders to hold higher reserves and reduce exposure to non core markets. By 2026, the environment has shifted. Inflation has moderated, interest rates are trending downward, and capital markets are gradually reopening. This easing improves feasibility, but it does not signal a return to pre 2020 lending behavior. Instead, it marks a transition toward more disciplined, structured, and sponsor focused capital deployment.

The Cost of Capital in a Lower Rate Environment

As rates decline, the cost of capital is easing, but it remains structurally higher than historical lows. Construction costs, insurance premiums, and climate risk pricing continue to influence underwriting decisions. In 2024, a typical Caribbean hotel construction loan carried interest rates near 11.5 percent, with loan to cost ratios around 55 percent from traditional lenders, and higher pricing from private credit and family office capital. By 2026, borrowing costs are improving, but lenders remain selective, prioritizing projects with strong sponsorship, realistic phasing, and multiple layers of capital

protection.

Insurance remains a critical variable. Rising premiums and climate related underwriting constraints continue to shape deal structures, with increasing emphasis on resiliency, mitigation strategies, and long term operational sustainability.

Who Is Providing Caribbean Capital in 2026

While many traditional institutions paused during the tightening cycle, private capital continued to adapt. In 2026, the Caribbean capital stack is increasingly supported by:

• Private credit and private debt funds

• Family offices and high net worth capital

• Structured equity and preferred equity investors

• Fintech enabled and non bank lenders

These groups are not replacing banks entirely. They are filling gaps where traditional lending remains constrained.

A More Complex Capital Stack Is the New Normal

A five star Caribbean resort now routinely requires five to seven capital sources. For example, a US$250 million capital stack may include senior debt, development finance institution tranches, private credit, family office equity, tokenized equity, and sponsor capital. Complexity is no longer a liability. It is a competitive advantage.

What Lenders Are Requiring Today

Stronger sponsors and guarantees. Experience matters. Lenders prioritize sponsors with demonstrated Caribbean track records and asset class expertise. Personal and corporate guarantees, completion guarantees, and bonding remain common, reinforcing alignment between sponsors and lenders.

Land valuation discipline. Land lift has largely disappeared. Lenders typically underwrite land at original cost, not projected appreciation, requiring sponsors to carry true equity risk.

Presales and capital reduction strategies. In hospitality and mixed use projects, condo hotel presales remain attractive. Presale thresholds typically range from 35 to 65 percent, reducing total capital requirements while demonstrating market acceptance.

Loan syndication and risk bifurcation. To manage exposure, lenders increasingly syndicate loans or bifurcate risk. Large hospitality financings are often structured with separate debt instruments for hotel and residential or condo hotel components, allowing differentiated risk profiles within the same project.

Where Capital Is Still Flowing

Despite tighter underwriting, capital continues to support mission driven developments. These projects benefit from:

• Unique cultural or historical positioning

• Scarce coastal or gateway locations

• Strong lifestyle and tourism demand

• Alignment with sustainability and resiliency themes

These attributes help projects stand out in a more selective capital environment.

Three Alternative Capital Trends Defining Caribbean Real

Estate in 2026

The next phase of Caribbean capital is being shaped by three structural trends now consistent across the region.

1. Funds Are Replacing Fragmented Buyers

Developers are increasingly partnering with debt and equity funds to purchase residential, hospitality, and branded units in bulk, both during pre-construction and post completion. Bulk takeouts are no longer viewed as distressed solutions. They are strategic tools.

For developers, bulk transactions accelerate liquidity, reduce sellout risk, and improve balance sheet visibility. For lenders, they enhance absorption certainty and cash flow clarity. For funds, they offer scale, pricing efficiency, and exposure to real assets with defined operating strategies.

2. Private Equity Is Reshaping Island Markets

Private equity and alternative capital are no longer supplemental. In 2026, they are foundational. By aligning capital horizons with development timelines and asset life cycles, investors are reshaping not only individual assets, but entire island destinations. Rather than pursuing short term yield, this capital is underwriting multi year transformations. Puerto Rico illustrates this shift clearly. Through Act 60, private equity has enabled full recapitalization and long term repositioning of legacy resort assets, requiring patient capital, flexible structures, and long term alignment.

3. Cross Border Capital Is Redefining Caribbean Real Estate

International capital is increasingly active across the Caribbean. European investors, particularly from the Netherlands, are deploying capital into markets such as Sint Maarten, Aruba, and Curaçao. One prime example is the Setai in Sint Maarten that secured construction capital from a large Dutch pension fund. These investments reflect confidence in jurisdictions with established legal frameworks, stable tourism demand, and economies linked to the euro and U.S. dollar. For sponsors, cross border capital brings scale and longer horizons, while raising expectations around governance, transparency, and execution.

The Landowner as a Capital Partner

A critical but often overlooked dynamic is the landowner’s role in helping to finance hotel development. Rising costs and thinner margins have elevated landowners into active capital partners through land leases, phased transactions, equity contributions, subordinated positions, and performance based participation. In today’s environment, land is not just an asset. It is a financing tool.

Resilience, Sustainability,

and the Next Wave of Capital

Resiliency is no longer a cost center. It is a source of capital. DFIs, multilaterals, impact funds, and tokenized investors increasingly reward credible sustainability frameworks with better pricing, longer tenors, and greater flexibility.

Final Reflection: A New Era Demands a New Lens

Caribbean development can no longer rely on one or two financing channels. The future belongs to those who can design smarter capital stacks, integrate diaspora capital, embrace tokenization, collaborate with landowners, and structure resiliency as a performance driver.

In the Caribbean, success in 2026 will favor teams that understand both local execution and global capital expectations. Navigating layered capital stacks, cross border investors, landowner partnerships, and increasingly complex underwriting requires experience that spans development, finance, and transaction execution.

This is where the combined experience of AG&T and EN Capital matters. Together, we bring decades of on the ground Caribbean development experience, deep relationships across private wealth and institutional capital, and a proven ability to structure and close complex transactions across hospitality, mixed use, and destination driven assets.

AG&T’s long standing presence across the Caribbean provides insight into local markets, regulatory environments, and development realities. EN Capital’s capital markets expertise brings disciplined structuring, access to diverse capital sources, and the ability to align projects with the right investors at the right point in the cycle.

In a market shaped by alternative capital, private equity, and global investors, execution matters more than ever. The next phase of Caribbean investment will not be led by those waiting for simpler conditions, but by teams prepared to structure smarter, partner broadly, and deliver Alpha across cycles.

Nathan Whigham Founder and President

EN

Capital

EN Capital is a capital advisory firm focused on commercial real estate, renewable energy and space compa- nies The firm is active across the United States, Puerto Rico, other Caribbean Markets and LATAM. ENC provides advisory on project capitalization, corporate credit & M&A. Nathan Whigham is the Founder and President of EN Capital. He has been in the capital markets and finance industries since 2006 and has been involved in over $1B of transactions up and down the capital stack across a variety of transaction types in corporate credit, commercial real estate, renewable energy and other market segments.

Adam Greenfader Chairman AG&T

Since 1993, AG&T is a premier Caribbean real estate development and advisory firm headquartered in Miami, Florida. AG&T has played an integral role in over 55 high-profile development projects valued over $1.5 billion, including master-planned communities, luxury hotels, affordable housing, and private island resorts. Key markets include Puerto Rico, Sint Maarten, Jamaica, USVI, Costa Rica, and Mexico. AG&T proudly serves a clientele that includes developers, hedge funds, private equity firms, and various institutional capital groups. Adam Greenfader is the Chairman of AG&T. He has notably chaired the Caribbean Council at the Urban Land Institute (ULI) and currently serves as the Florida Liaison for the Puerto Rico Builders Association. His recent work, the 2025 edition of “Why Puerto Rico Now: A Masterplan for Resurgence, Re- siliency, and Long-Term Economic Growth,” encapsulates his vision for a vibrant, forward-thinking future for Puerto Rico.

CONSIDERATIONS FOR STARTING A PRIVATE EQUITY FUND

BY E. GEORGE TEIXIERA Anchin

As private equity firms continue to succeed and become ever prevalent in the alternative investment space, more aspiring portfolio managers are joining the race to launch their own fund. While today there are many successful large private equity firms, many of the firms in this space are small or mid-sized shops with employees ranging from single digits to several hundred. The following summarizes several steps that managers should follow to launch a private equity fund.

Outline Your Business Strategy

Establishing a business strategy requires a significant investment of time, effort, and research to determine and answer many questions. For example, will your fund have a specific industry, sector, or geographic (US/

abroad) focus? Ultimately, potential investors want to know more about your fund’s strategy, so being prepared to address these and other relevant questions will go a long way in helping you raise capital for your new fund.

Setting up Operations and a Business Plan

Starting your own private equity fund is in many ways like starting any other business. You’re going to need a business plan which, among other things, calculates expected cash flow and establishes your fund’s timeline, including the capital-raising period. Private equity funds generally have an average life of 7 to 10 years1, although this varies based on a manager’s discretion and the execution of a solid business plan. A sound business plan contains growth strategies, a marketing plan, and a detailed executive summary that ties

all these areas together.

Once a business plan has been completed, you should begin to meet with external service providers and consultants, such as accountants, attorneys, and other industry specialists, who can assist you with effectively and efficiently refining and executing your business plan.

Another important step is to form a firm to manage the fund and name the fund. The fund manager must decide on the roles and titles of the firm’s leadership, such as the role of partner or portfolio manager as well as the establishment of a management team, including the CEO, CFO, CIO, and CCO. At launch, however, it may be wise to outsource some of these functions to execute your plan in a more cost-efficient manner.

Legal Needs

If you plan to raise a fund in the U.S., you may already know that fundraising is heavily regulated. There are numerous legal and regulatory requirements that a fund manager must adhere to in order to comply with securities laws. The Securities & Exchange Commission (SEC) takes compliance very seriously and a qualified attorney needs to be involved in the process early to make you aware of the rules and regulations associated with fundraising, investing, and managing the fund. Below are some key questions to discuss with your attorney.

Who will I be able to raise money from? Regulations impact how a fund manager raises money, primarily depending on, and related to, the type of investors, the type of marketing, and the amounts being raised.

How can I raise money? In addition to understanding which investors can participate in a fund, a manager needs to understand the rules regarding how investors may be contacted and approached to solicit investment. The fund manager will need to think carefully about the message, and the delivery thereof.

What kind of money can be invested? Another concern is the type of money that a fund or fund manager can receive. There are a variety of restrictions in this area, but the two most common are investments from retirement accounts and investments from foreign accounts. Each of these areas creates potential issues regarding how a fund manager can invest, manage and

report results to investors.

How much will the legal work cost? Every fund and attorney are unique, but you can expect start-up legal costs to be upwards of $50,000, and in some cases exceed $100,000.

By limiting the fact-finding phase of fund formation, a fund manager can focus their attorney’s time on key compliance questions and avoid expensive discussions and rewrites. Having your fund’s marketing materials, a draft of its investment strategy, and fee structure ready for review as you begin the legal process will also help to control legal costs as you look to launch your private equity fund.

Setting Up Your Fund Structure

In the U.S., a fund is typically organized as a limited partnership (LP) or a limited liability company (LLC). As a founder of the fund, you will be a general partner or managing member with the authority to represent the fund and allocate capital. Your investors will be limited partners who will not have the right to make any decisions on behalf of your fund or fund investments. The structure of a private equity fund is dependent on several tax, regulatory and financial considerations, usually driven by the tax needs of the investors. Some private equity fund features and potential structures are discussed briefly below.

Closed-End Structure

Private equity funds are usually closed-end investment vehicles, which means that there is a limited window to raise capital, and once this window has expired, no further capital can be raised. Investor capital is typically committed at the onset of the fund and is called by the manager periodically as investments are made. Investors in closed-end funds are generally not permitted to make withdrawals or additional capital contributions during the life of the fund and after the committed capital period. Some funds may provide for additional contributions for follow on investments in portfolio companies in which they already own a piece of. Once funded, an investor’s capital will typically be returned upon the sale or restructuring of fund portfolio companies, or profit distributions from operations of

portfolio companies

With a closed-end fund, once an investment is sold, the sale proceeds generally cannot be reinvested in that fund. Rather, the fund manager would create a separate continuation fund to allow investors to reinvest. The cost of launching these funds can be significantly less than the initial fund since less legal assistance is required, and an administrative infrastructure is already in place.

Fund Structure Options

Most private equity funds domiciled in the U.S. are organized as LPs since such a structure generally avoids double taxation of investment returns and grants limited partners (your investors) limited liability protection, thus shielding them from losing more than their investment. An onshore fund is a U.S.-based investment fund structure that typically includes an LP as the fund vehicle, an LLC as the investment manager of the fund (although an LP or an S corporation may be used depending upon tax considerations), and a general partner of the fund (managing member in the case of an LLC).

An offshore fund, often called a blocker fund, blocks offshore and tax-exempt U.S. investors from direct U.S. tax exposure. There are several ways to structure your offshore fund and the best option for you will depend mainly on the location of the fund manager, types of investors in your fund, and the type of investments that the fund will make. The three most common structures used for offshore funds are briefly described below.

Offshore Only – An offshore standalone fund is a structure where only one fund is used and that fund is offshore (commonly in Cayman, Bermuda, or BVI). This structure is used by managers who have no U.S. presence and whose fund is solely geared towards nonU.S. investors and tax-exempt U.S.-based investors who seek to avoid unrelated business taxable income (UBTI).

Master-Feeder – A master-feeder structure is generally used where there is a U.S. presence, and a manager is looking to raise capital from both foreign and domestic, or tax-exempt U.S. investors. This structure includes a master fund (an offshore fund which is either an LP or corporation, often referred to as an LTD, which elects to be treated as a partnership for U.S. tax purposes), which conducts the fund’s activity, and an

onshore feeder and offshore feeder that invest all their assets into the master fund.

The onshore feeder will generally be structured as a U.S. LP or LLC and is where the U.S. taxable investors will invest. Using an LP or LLC, which are passthrough entities for U.S. tax purposes, allows the master fund’s profits and losses to be allocated to the U.S. investors and thus taxed at the investor level. The master fund incurs no tax in the offshore jurisdiction, thereby avoiding double taxation.

The offshore feeder is structured as an offshore fund (see Offshore Only section above) and is where the non-U.S. and U.S. tax-exempt investors invest. Investment into the offshore feeder means that any U.S. tax exposure that arises, typically from the master’s investment in U.S. trades or businesses, does not affect the offshore feeder investors themselves. Foreign investors who are otherwise not required to file U.S. tax returns, prefer to invest through an offshore fund to avoid exposure to any U.S. tax or filing obligations. If a foreign investor were to invest directly into a fund structured as a partnership, they could be deemed to be engaged in the business of the fund and, to the extent that this includes any U.S. trades or business, could be required to file a U.S. tax return and be liable to pay U.S. taxes. For similar reasons, U.S. tax-exempt investors often prefer to invest through the offshore feeder. Tax-exempt U.S. investors could be liable for income tax on income from U.S. trades or businesses which are not substantially related to their tax-exempt purpose, known as UBTI.

Side-by-Side – Similar to a master-feeder structure, a side-by-side structure is used when a manager is looking to raise capital from both U.S. investors and nonU.S. or tax-exempt U.S. investors who have differing tax concerns. In this structure, two funds, an offshore and domestic U.S. fund are formed, and are managed and operated in the same way. The main reason for choosing the side-by-side structure over the master-feeder structure is to enable tax structuring measures for one fund independent of the other. A side-by-side structure generally includes a U.S.-based fund and an offshore-based fund that parallel each other in their trading/investing objectives and share the same investment manager but have flexibility to allow for differences in portfolio composition.

Fund Expenses, Fees and Distribution Waterfall

One of the most important areas to address when forming your private equity fund is to set the fees that will be charged to your investors. Well-thought-out and sound private equity fund offering documents contain terms that look to protect the fund manager and that are amenable to potential investors. Accordingly, the following will focus on private equity fund industry best practices regarding fund expenses, fee terms, and distribution waterfalls.

Fund Expenses – Expenses such as legal, fund administration, tax preparation, and audit fees are generally the costs incurred to set up and run a private equity

fund. The fund generally bears expenses directly related to forming and operating the fund. Overhead expenses are typically the responsibility of the fund manager. Your fund documents should clearly state which expenses will be borne by the fund and its investors and which by the fund manager. Quite often an expense cap is placed on the amount of expenses that can be charged to the fund, with the excess to be paid by the fund manager.

Management & Incentive Fees – Private equity fund managers generally charge their investors an annual management fee, as well as an incentive fee (also known as performance fee or carried interest). Management fees typically range from 1.25% to 2% and are generally charged on committed capital, regardless of whether the capital has been called or invested. Incen-

tive fees generally range from 15% to as high as 30% and represent an allocation of appreciation of assets or net profits by the fund. However, for the fund manager to begin receiving carried interest, the fund must first achieve a stated hurdle rate (also known as the preferred return).

Distribution Waterfall – Defines the economic relationship between the fund manager (general partner) and the investors (limited partners). There are four primary components to a distribution waterfall:

Return of Capital – All distributions go to the fund investors until they have received back their full committed capital contributed to the fund.

Preferred Return – Fund investors will continue to receive all distributions until the fund has achieved its preferred return (or hurdle rate). These percentages can range from 6% to 12% of the investor’s contributed capital, are compounded annually, and are generally defined in the fund’s offering documents.

Catch-up Provision – Once the fund has returned all capital to its investors as well as the preferred return, the fund manager (general partner) is then able to start collecting carried interest. This is generally calculated by going back to the first dollar of net profits of the fund and allows the fund manager to retain most of the fund’s future profits until it has received its stated share (assume 80% if the carried interest rate was 20%).

Remaining Distributions – After the fund manager has received its carried interest for fund returns beyond the preferred return, all remaining distributions are then allocated between the limited partners and the fund manager at the rate specified in the fund offering documents. For example, if the carried interest percentage is 20%, the remaining distributions would be allocated 80% to the limited partners and 20% to the fund manager.

While the above four components are standard across most private equity funds, some variations are worth mentioning. The most common variations are the European waterfall and the American waterfall. The European waterfall is where the carried interest is calculated at the fund level across all portfolio company deals. In this scenario, the fund manager does not begin to take any carried interest until the fund has returned all limited partner contributions across all port-

folio company deals as well as exceeded the preferred return. The American waterfall is calculated on a dealby-deal basis whereby the fund manager is compensated for each successful deal. This allows the fund manager to begin taking carried interest earlier in the life of the fund but can also result in the fund manager receiving carried interest despite failing to reach the preferred return across its portfolio. This can occur if there are individual portfolio companies with successful exits, but unrealized losses on current holdings. For funds that use the American waterfall, a clawback provision is needed and should be included in the fund offering documents. This allows investors to recoup the carried interest at the end of the fund’s life if the fund underperformed in total and the fund manager collected excess incentive fees.

Raising Capital

Raising money for a new private equity fund manager can be a formidable task and requires preparation. Items such as the offering memorandum, subscription agreement, fee terms, marketing materials, and due diligence questionnaires should be prepared in advance of meeting with potential investors.

Potential investors will also want to see a “meaningful” contribution from the fund manager (or fund management group) to better align their interests. Based on our experience and industry standards, fund managers have generally provided at least 1% to 3% of the fund’s total capital commitments.

At some point, while raising capital for your fund, you will most likely be asked by one or more potential investors to enter into a side letter. A side letter is an agreement between the fund and an investor to vary the terms of the limited partnership agreement concerning that particular investor. Some of the most common side letter requests from investors are for a partial or complete waiver of the fund’s fees (management fee, carried interest, or both), to reduce the lock-up requirements (which would give them the right to withdraw capital at an earlier date than other investors) and “most favored nation” clauses (which would, in essence, give that investor the right to obtain any benefit granted to other investors via a side letter). Tread lightly and carefully when assessing each side letter request from potential investors and seek legal assistance in drafting and nego-

tiating such agreements.

Audits and Taxes

You will need to engage an accounting firm to perform an annual audit of your fund and to prepare the fund’s tax returns (including Schedule K-1s that you will need to provide to your fund’s investors). It is prudent to meet with a firm like Anchin, which has vast experience with start-up private equity funds, before you finalize your legal documents so that you can discuss and better understand the unique tax landscape created by your fund strategy, investors and portfolio. Services include reviewing fund and related-entity structures, identifying requisite Federal and state tax filings, potential issues related to foreign investors, foreign investments, retirement plans, beneficial tax elections, your plan for manager and employee compensation, and the overall tax impact of running your fund. Preferably, you should look to hire a firm to partner with that not only covers your basic accounting needs but is also capable of helping as your fund grows and expands. The firm should be actively working with you to minimize tax exposure and to consult and advise on your operations. Look for a firm with a strong reputation for working with emerging managers, as larger accounting firms may not be initially focused on your start-up needs. A coordinated and experienced audit and tax team focused on your business and personal needs are imperative as you launch your new fund.

In Conclusion

Starting a private equity fund can be challenging, especially for those who don’t have any experience in doing so. It requires partnering with experienced professionals and a tremendous effort to refine your business strategy, develop your business plan and build your team. The above steps can be used as a roadmap for establishing a successful fund. For more information, please reach out to E. George Teixeira2, Partner and Practice Leader of Anchin’s Financial Services Group.

E. George Teixeira

Partner and Practice Leader of Anchin’s Financial Services Group Anchin

Anchin is a leading accounting, tax, and advisory firm specializing in the needs of privately held companies, investment funds, and high-net-worth individuals and families. Its highly focused industry specialization helps clients overcome challenges and achieve their financial objectives confidently. Consistently recognized in respected “best of” lists for service, firm management, and employee satisfaction, Anchin prioritizes partner-level engagement and commitment to employee retention.

Our Financial Services Practice includes eight partners and a team of approximately 55 professionals, serving over 400 clients in the alternative investment space, private equity and venture capital funds, hedge funds, fund-of-funds, and other asset managers. Clients range from emerging managers to institutional-backed firms with more than $1 billion in assets under management. This breadth of experience provides us with a comprehensive understanding of operational and regulatory complexities.

As a full-service firm with about 600 professionals, including more than 65 partners and principals, Anchin offers assurance, financial reporting, tax, and advisory services. We operate offices in New York City, Uniondale (NY), Boca Raton (FL), and Palm Beach Gardens (FL), and are proud members of BKR International.

Recalculate what’s possible by visiting us online at www. anchin.com.

HUNTING FOR CONVEXITY

BY BRIAN FOOTE, CFA

Broadway Capital Management, LLC

Financial markets exist to compensate investors for bearing uncertainty. Yet, the characteristic of uncertainty today differs markedly from even a generation ago. Capital flows instantaneously. Information—both useful and fabricated— spreads virally. Allocation decisions are increasingly dictated by rules-based systems rather than judgment.

At the same time, valuations in key market segments have stretched to extremes. As of early January 2026, the Shiller CAPE ratio sits near 40, a level reached

only during the peak of the dot-com era. Whether one chooses to label this a “bubble” is beside the point. These conditions will reward neither blind optimism nor superficial analysis. This regime demands preparation, humility, and a clear understanding of how markets behave at extremes.

A robust capital allocation framework begins here, shaped either by experience across cycles in my case, or experiencing them second hand through reading about them.

We all know that professional investing is not about forecasting a single future—indeed, it is not about forecasting at all—but about navigating a range of possible futures, including those most people prefer to dismiss as improbable. Perspective comes naturally when the dot-com bust, the Global Financial Crisis, and the collapse of Long-Term Capital Management all form part of one’s professional memory. Babies born during the GFC are now adults. Markets have evolved, but human behavior has not.

Markets do not fail at the average; they fail at the tails. Most lasting portfolio damage is not caused by routine volatility, but by rare, violent episodes dismissed as unlikely until they arrive—the so-called “six-sigma” events that somehow recur every decade. Any process that does not explicitly account for tails remains incomplete, regardless of how elegant it appears on paper.

The Fragility of Concentration

One of the defining structural changes of this era is the rise of passive investing. Passive strategies now hold nearly 60% of U.S. equity fund assets, up from roughly 50% just a few years ago. What was originally, and correctly, conceived as a way for the average investor to match the market at the lowest possible cost is now a potential source of risk. The road to hell was possibly paved with this great intention. Capital is increasingly allocated by index weight and market capitalization rather than business fundamentals, creating feedback loops in which quotational success attracts ever more capital regardless of valuation. Entire segments of the market outside the largest benchmarks are systematically neglected.

This dynamic is compounded by extreme concentration at the top with the so-called Magnificent Seven now representing roughly 34–35% of the S&P 500, rivaling historical extremes in market leadership concentration. When leadership narrows this dramatically, the market becomes more fragile, not more stable. Risk is disguised as diversification, and familiarity is mistaken for safety. At elevated valuations, even modest deviations from expectations can trigger sharp repricing as crowded trades attempt to exit simultaneously. Crowded markets exit through narrow doors. Nav-

igating this environment does not require precise prediction—only the recognition that protection is cheap relative to potential damage. Concentration amplifies tail risk, and tail risk is where convex strategies earn their keep.

Convexity in Practice

Probability, properly understood, is not about precision but about structure. A simple probability tree drawn on a whiteboard forces uncomfortable but necessary questions. What if growth slows instead of accelerates? What if liquidity dries up just as valuations compress? What if correlations spike precisely when diversification is most needed?

Each branch carries a probability. While those probabilities are never assigned perfectly, the exercise itself imposes discipline. It reminds investors that outcomes are not binary and that the most consequential paths often lie far from the center of the distribution. This probabilistic framing naturally leads to a search for convexity. When outcomes are asymmetric—when downside can be swift and severe while upside accrues gradually—portfolios must be constructed asymmetrically as well. Convexity recognizes that a small, consistent cost can protect against catastrophic loss, and that optionality has value precisely because the future is unknowable. Linear portfolios assume smooth paths. Markets do not oblige.

Options and hedging translate this insight into practice. They shape payoff distributions, explicitly clipping the most damaging downside paths. Protective structures are built when complacency makes them cheap. Periods of suppressed volatility are not signs of safety but invitations to prepare. Far out-of-the-money puts can hedge tails at modest cost, while collars protect concentrated exposures without surrendering all upside. Convexity is architecture, not theory.

Inefficiency and Opportunity

Away from the crowded center of the market, small- and micro-cap equities continue to offer something increasingly rare: inefficiency. These segments are poorly covered, lightly owned, and often misunderstood. They still reward deep, fundamental work. Balance sheets matter. Incentives matter. Capital allocation

decisions matter. The basic mechanics of business endure, even if attention shifts elsewhere.

History’s most powerful public compounders (those offering 10-100x + returns) almost always began life as small, obscure enterprises precisely because their potential was not obvious to the crowd. Exploiting this reality requires patience, but also humility about volatility and imperfect information.

Recent Reminders

Markets continue to provide reminders of these dynamics. The “Liberation Day” tariffs triggered an abrupt repricing, with the S&P 500 falling more than 10% in a matter of days as liquidity evaporated and correlations converged. Markets priced for perfection collided with uncertainty, and confidence vanished quickly.

The narratives differ from cycle to cycle—dot-com optimism assumed growth without cash flow; the GFC assumed housing prices could not fall nationally. Confidence is built on extrapolation. Leverage is justified by recent experience. Risk is dismissed because it has not appeared lately.

The Circle of Competence

This is where the concept of a circle of competence becomes essential. Knowing what one understands is important; knowing where one should not tread is even more so. Investors are rarely undone by a lack of intelligence. More often, they are undone by venturing into areas they do not truly understand, armed with borrowed conviction and bad models.

Discipline allocates capital where risks can be framed, probabilities assessed, and downside controlled. Where this is not possible, restraint becomes a competitive advantage.

Cycles repeat because human behavior does not change. Greed, fear, extrapolation, and denial recur in different forms but with familiar consequences. Experience does not eliminate uncertainty, but it sharpens judgment about where uncertainty tends to matter most.

A Coherent System for a Nonlinear World

Taken together, these elements form a coherent system designed for nonlinearity. Passive flows create

neglect. Concentration creates fragility. Small- and micro-cap inefficiencies create opportunity. Probability trees impose discipline. Tail awareness shapes risk management. Experience tempers confidence. We aim to integrate it all.

Options and hedging translate these lessons into explicit risk definition. Deep value anchors the framework in economic reality, offering long-term return potential of buying actual businesses while “clipping the tail” limits the cost of being early—or temporarily wrong.

The future will not be smoother than the past. If anything, it will be more episodic, more crowded, and more prone to abrupt regime shifts as liquidity thins and positioning concentrates. Investors who rely on linear assumptions will continue to be surprised. The correct approach does not attempt to forecast the next shock. It assumes shocks are inevitable and prepares portfolios to endure them.

Brian Foote, CFA

Founder & Portfolio Manager

Broadway Capital Management, LLC

As Portfolio Manager at Broadway Capital Management, Brian enables high net worth professionals to maximize their legacy through strategic wealth preservation, concentration, and hedging, as well as future-resilient value investments. Embracing Volatility and Seeking Asymmetric Returns.

THE DEMOCRATIZATION OF INVESTING: EXPANDING ACCESS TO PRIVATE MARKETS

BY HERBERT M. CHAIN CBIZ

A Gradual Shift in Access

Private equity and other alternative asset classes have historically been accessible only to institutions and the wealthiest investors. Defined contribution participants, retail investors, and smaller allocators were excluded due to regulatory restrictions, high minimums, and illiquidity. Recent regulatory actions and technological advances, however, are gradually broadening access, creating new pathways for retirement savers and retail investors to participate in the fast-growing private markets channel.

Historical Context

The investing landscape is undergoing a meaningful broadening of access. What was once the preserve of institutions and ultra-high-net-worth investors is becoming more available to retail and retirement channels. This “democratization” is not a single event; it is a structural evolution driven by product innovation, regulatory clarification, and investor demand for diversification and diversified portfolios. As access expands, however, so do the responsibilities. Sponsors, managers, and fiduciaries must align product design, liquidity promises, valuation practices, and participant education with the

inherently long-term, opaque, and fee-intensive nature of private markets.

Traditionally, access to private markets, particularly private equity, has been restricted by high minimum investments, complex fund structures, and strict investor accreditation requirements. The rationale was clear. Private assets are inherently less liquid and transparent, require longer holding periods, and come with complex risk profiles. Regulators and managers took a cautious stance, limiting participation to investors who could withstand losses and navigate the sophisticated structures. Yet as markets matured, the alternative asset industry recognized that both accredited and non-accredited investors could benefit from the diversification and return potential offered by private equity and other alternative investments. At the same time, asset managers sought new sources of capital and growth, leading to creative solutions and calls for regulatory adaptation.

What is Meant by “Democratization”?

“Democratization of investment” in the context of private equity and similar alternative asset classes refers to broadening access so that a wider range of investors

can participate in these markets. Practically, it means reducing historical barriers related to minimum investment sizes, accreditation requirements, illiquidity, complexity, and information asymmetry, while introducing structures and safeguards that make participation feasible and appropriate for more investor profiles.

According to the World Economic Forum,

Market democratization refers to the increased ability of an individual to access capital markets, related to the newfound availability of information, investing platforms and investment products.1

Key elements include:

Lower investment minimums, often through feeder funds, interval funds, tender offer funds, and evergreen vehicles.

Expanding access beyond institutional or currently-defined accredited investors2 where regulations permit.

More investor friendly structures, with periodic liquidity, simplified tax reporting, and streamlined capital calls—often “evergreen” rather than drawdown.

Expansion of eligibility from institutions and ultra high net worth investors toward accredited, quasi

institutional, and eventually some retail channels.

Digital intermediation from platforms and recordkeeping systems that make it operationally feasible to serve thousands of smaller investors instead of dozens of large ones in onboarding, suitability checks, fractionalization, and streamlined subscriptions.

Enhanced disclosures, reporting standards, and investor education to address complexity and information gaps common in private markets, and designing products within applicable rules (suitability, diversification, valuation, custody, leverage limits) to protect less-experienced investors.

Regulatory Developments

Regulators have gradually recognized that a binary world of “unsophisticated retail versus sophisticated institutional” may not accurately reflect today’s markets. Policy has been nudged toward a spectrum, where access and disclosure requirements can be calibrated to investor type, product complexity, and distribution channel. That has opened space for structures that sit between registered mutual funds and fully private institutional funds, while still imposing robust disclosure, valuation, and governance expectations.

Two recent changes are especially relevant:

Access for Defined Contribution Plans

A significant development for retirement investing is the evolving stance of the U.S. Department of Labor (DOL) regarding the inclusion of private assets in defined contribution (DC) plans, such as 401(k) accounts.

The core regulatory debate hinges on the fiduciary duty under the Employee Retirement Income Security Act of 1974 (ERISA), which mandates that plan fiduciaries act prudently and solely in the interest of participants and beneficiaries. Historically, the complexity, valuation challenges, and illiquidity of PE were viewed as barriers to satisfying this standard for a broad participant base.

This perception began to shift with the DOL’s Information Letter (Letter) issued in June 2020.3 The Letter recognized that private equity investments present additional considerations to participant-directed individual account plans that are different than those involved in defined benefit plans and clarified that a DC plan fiduciary would not violate ERISA simply by offering a professionally managed, diversified asset allocation fund such as a target-date fund, target-risk fund, or balanced fund that included a component of private equity investments. Provided the fiduciary conducts an objective, thorough, and analytical process, private equity could be seen as an appropriate investment allocation to enhance diversification and potentially boost longterm risk-adjusted returns.

The key caveat was the requirement that the allocation must be contained within a highly diversified fund, ensuring that the PE exposure is limited and managed by an investment professional with the requisite expertise. The overarching trend, backed by a recent Presidential Executive Order, reaffirms the approach of the 2020 guidance.4 The onus remains firmly on the plan fiduciary, but the legal framework for inclusion is now established, setting the stage for new pools of capital to enter the private market ecosystem.

Reduced Restrictions on Closed-End Funds of Private Funds

For over two decades, the SEC staff maintained an

informal policy restricting closed-end registered funds (CE-FOPFs) from investing more than 15% of their assets in underlying private funds. If a fund sought to exceed this 15% limit, it was typically required to impose stringent investor requirements, such as restricting sales to accredited investors and mandating a minimum initial investment of at least $25,000. This informal restriction effectively capped the PE exposure within registered vehicles that were accessible to the general public.

In August 2025, the SEC’s Division of Investment Management published Accounting and Disclosure Information (ADI) 2025-16, signaling a formal policy reversal.5 The new guidance explicitly states that SEC staff will no longer request that a registered CEF or CE-FOPF either adhere to the 15% cap or impose accredited investor requirements and minimum investment thresholds.

This administrative change means that CEFs and Interval Funds, which provide periodic, limited liquidity and are subject to the comprehensive investor protections of the Investment Company Act of 1940, can now be allocation vehicles. These registered structures are subject to oversight by a fiduciary board and managed by registered investment advisers, and they must provide clear, robust disclosures on fees, conflicts, and liquidity risk, significantly enhancing investor safeguards compared to direct private fund investment. The removal of the 15% hurdle allows these structures to offer a diversified portfolio exposure to private equity, private credit, and infrastructure for the ordinary investor.

Balancing Opportunity and Risk

Critics caution that retail investors may lack the sophistication to navigate private markets. Concerns include transparency gaps, illiquidity mismatches, and higher fees. Proponents counter that democratization is about responsibly broadening opportunity, not eliminating risk. With proper guardrails, retail investors can capture diversification benefits while maintaining protection.

However, this structural shift is not without its challenges. Fund sponsors and retail financial intermediaries must remain acutely aware of three critical areas:

Complexity and Fees: Private market investing inherently involves higher fees and more complex structures than public market counterparts. Comprehensive and plain-English disclosure, as emphasized by the SEC, is essential for investor understanding.

Liquidity Mismatch: While private funds often offer periodic liquidity (e.g., quarterly redemptions), they are not daily liquid vehicles like mutual funds. Educating investors on the true nature of the commitment to the investment is paramount to managing expectations and mitigating behavioral risk.

Fiduciary Responsibility: For DC plan fiduciaries, the duty of prudence remains critical. The decision to incorporate private equity must be based on a rigorous, documented analysis demonstrating the investment’s benefit to the long-term, risk-adjusted returns of the overall plan and its participants.

Democratization brings real risks alongside its opportunities. Illiquidity, valuation subjectivity, fee layers, and complex capital structures can be hard for nonprofessional investors to fully understand, even with enhanced disclosure. Semi liquid products can create a false sense of daily market like flexibility in what are fundamentally long horizon investments.

Accordingly, fiduciaries, advisors, and regulators play a critical role. Suitability assessments, clear communication of risks and time horizons, careful product design, and conservative liquidity management are essential. The industry will also need to support investor education that provides plain language explanations of how these strategies work, what they cost, and how they fit into an investor’s overall financial plan.

Technology as the Enabler

Technology is a critical enabler of democratization. Digital onboarding, electronic signatures, standardized data pipes into custodians and recordkeepers, and more automated capital call and distribution processing have dramatically lowered the marginal cost of serving smaller investors.

Looking ahead, tokenization and distributed ledger infrastructure may further facilitate more fluid secondary markets in private assets, potentially improving liquidity, price discovery, and expense ratios. For now, many tokenization efforts are still pilot scaled, and the

regulatory overlay is evolving. But the directional trend is toward a world where fractional ownership and digital distribution make it operationally feasible to slice what used to be “lumpy” private assets into investor-friendly exposures.

As Larry Fink of BlackRock noted in his 2025 Chairman’s Letter to Investors, “Tokenization allows for fractional ownership. That means assets could be sliced into infinitely small pieces. This lowers one of the barriers to investing in valuable, previously inaccessible assets like private real estate and private equity.” In the letter, he also stated, “Some investments produce much higher returns than others, but only big investors can get into them. One reason? Friction. Legal, operational, bureaucratic. Tokenization strips that away, allowing more people access to potentially higher returns.”6

Closing Thoughts

The walls around private equity are not collapsing overnight; they are being carefully adjusted. Defined contribution participants, retail investors, and new classes of savers are gaining access, but with responsibilities that match the opportunities.

The democratization of investing is best understood as a measured evolution rather than a revolution. Expect continued regulatory refinement, balancing access with investor protection, innovation in fnd structures to provide liquidity solutions, and a greater emphasis on education to ensure investors understand risks and rewards.

Democratization does not mean eliminating risk or complexity. Private markets carry unique risks—illiquidity, valuation lag, capital call dynamics, performance dispersion, fees, and limited transparency. Effective democratization balances wider access with product design, education, and safeguards so investors can participate in private market return streams in a manner consistent with their risk tolerance, time horizon, and financial profile.

5 Key Takeaways

Broader Access for New Investor Classes - Recent regulatory changes and technological innovation are allowing retail investors, defined contribution plan participants, and smaller allocators to invest in private equity and other alternative asset classes—markets once

reserved for institutions and ultra-high-net-worth investors.

Major Regulatory Milestones Enable Participation

- The U.S. Department of Labor now permits private equity exposure in diversified DC plans (like 401(k)s), and has been instructed by the 2025 executive order to determine ways to increase the participation, while the SEC’s 2025 policy changes have lifted historic caps on closed-end funds’ investments in private funds, removing barriers for non-accredited and smaller investors.

Fund Innovation and Digital Solutions Facilitate

Entry - The rise of interval funds, tender offer funds, feeder vehicles, and digital platforms makes smaller minimums, streamlined onboarding, and fractional ownership possible, further lowering operational barriers for managers and service providers.

Risks

Demand

Careful

Oversight and Education - As new investor segments enter private markets, sponsors, fiduciaries, and service providers must address complexities including illiquidity, valuation lag, fees, and behavioral risks. Robust product design, transparent disclosures, and investor education are critical safeguards.

Democratization Is Evolution, Not Revolution - Expanding access requires ongoing regulatory refinement and industry innovation, balancing opportunity with prudent oversight. Technology and product design will continue to lower barriers, but investor protection and suitability remain paramount.

clarify, and reform existing regulations and to suggest appropriate “safe harbors” to reduce fiduciary and litigation risk. The order also directs the SEC to facilitate access to alternative-asset investments for participants in defined-contribution retirement plans.

5At https://www.sec.gov/about/divisions-offices/division-investment-management/fund-disclosure-glance/ accounting-disclosure-information/adi-2025-16-registered-closedend-funds-private-funds, accessed December 2, 2025.

6At Larry Fink’s 2025 Chairman’s Letter to Investors | BlackRock, accessed December 5, 2025. https://www.blackrock.com/corporate/ investor-relations/larry-fink-annual-chairmans-letter

1World Economic Forum, Insight Report, August 2022, The Future of Capital Markets: Democratization of Retail Investing, at https://www3.weforum.org/docs/WEF_Future_of_Capital_Markets_2022.pdf, accessed December 5, 2025

2Note that on May 13, 2025, the House proposed broadening the definition of an “accredited investor” by enabling individuals to qualify not only on the basis of income or net worth, but also by passing a certification examination devised by the SEC. 3https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/information-letters/06-03-2020, accessed December 4, 2025.

4The August 7, 2025 Executive Order, Democratizing Access To Alternative Assets for 401(K) Investors, directs the DOL to re-examine its existing guidance on a fiduciary’s duties alternative assets are included in defined contribution (DC) plans like 401(k)s. This order instructs the Department of Labor to review,

Herbert M. Chain Director

CBIZ Alternative Investment Group delivers tailored audit, tax, and consulting services for hedge funds, private equity funds, venture capital funds, funds of funds, general partners, and investment advisors. Assisting alternative investment advisors isn’t just part of what we do — it’s all we do. Our dedicated team brings deep expertise in audit, tax, and consulting services for emerging and established fund managers. We help you manage complex investments, navigate regulations, and unlock new opportunities. https://www.cbiz.com/industries/alternative-investments

CBIZ

BEYOND PERFORMANCE: THE CRITICAL ROLE OF OPERATIONAL DUE DILIGENCE WHAT IT IS AND WHY IT MATTERS.

BY STEPHANIE SIROIS & WENDY BEER Channel Diligence

What Is Operational Due Diligence (ODD)?

Operational Due Diligence is the independent evaluation of an investment manager’s non-investment infrastructure – the people, processes, and controls that underpin how capital is managed and safeguarded. While investment due diligence focuses on investment performance, ODD focuses on operational integrity, governance culture, technology, and risk-management effectiveness behind performance numbers.

Why ODD Matters for Investors

ODD is a critical, yet often underappreciated, aspect of investing. By assessing operational robustness, investors can protect capital, enhance fiduciary oversight, and build more resilient portfolios. The following

outlines why a disciplined ODD approach matters and how it delivers both risk mitigation and long-term value.

Protecting Capital: Operational weaknesses can cause large investor losses. ODD assesses whether risk mitigation and monitoring mechanisms are proportionate and fit for purpose given the strategy and size of investment before they can become costly failures.

Enhancing Fiduciary Duty: Institutional investors and allocators must assess operational soundness as part of their fiduciary responsibility. Robust ODD supports compliance with regulatory expectations.

Strengthening Portfolio Resilience: ODD helps build more resilient portfolios through lowering operational risk, quicker issue escalation and response, and greater

clarity around valuation and liquidity.

Assist Investment Manager Selection and Monitoring: ODD helps distinguish investment managers with strong controls from those deemed higher risk operationally which may be used to establish side-letter protections and monitoring cadence.

Building Trust and Credibility: A disciplined ODD process demonstrates integrity and strengthens both investor confidence and organizational credibility.

Operational Alpha: The incremental value created when an investment manager operates with institutional-grade governance, controls, and infrastructure. Strong operational discipline reduces non-investment risk and enhances a firm’s ability to scale and respond to market events. For allocators, this results in more resilient portfolios, smoother execution, and increased confidence in the durability of returns.

Channel Diligence’s Perspective

At Channel Diligence, we view operational due diligence as a strategic lever, not just a risk filter. Our approach integrates institutional expertise, independent integrity, and collaborative engagement with investment managers positioning them for long-term success. Our goal is to align each engagement with the client’s objectives, whether it’s helping allocators deploy capital with confidence, preparing investment managers for institutional capital, or advising boards on governance frameworks.

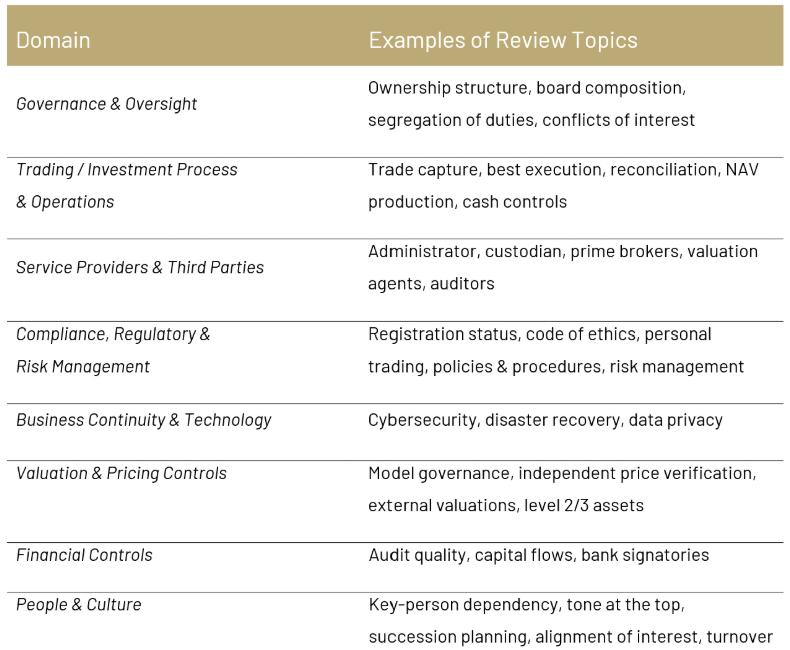

Key areas of ODD Review

While investment performance is often the key focus, operational shortcomings are frequently the root cause of fund failures, regulatory actions, and investor losses. The table below highlights the key areas that are

commonly scrutinized during an ODD review. These domains, from governance and oversight to technology and culture, offer critical insight into the types of risks that, if left unchecked, can have serious consequences for funds and their investors.

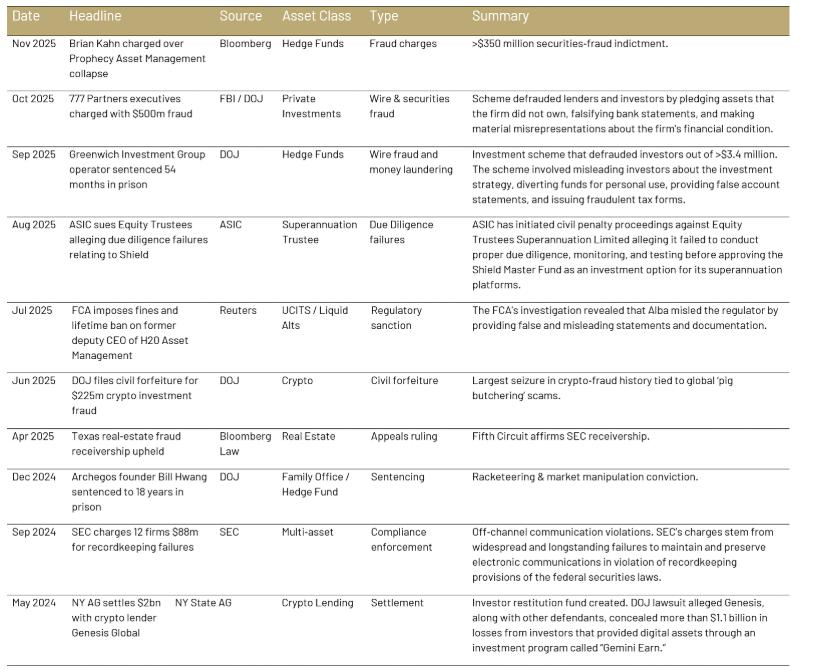

Recent Fund Failures, Frauds, and Enforcement

Actions (2024–2025)

Recent high-profile events in the alternatives industry demonstrate the importance of operational oversight and continuous monitoring.

Compiled by Channel Diligence, November 2025.

Subscribe to get our investment managers' best insights here: https://www.channelcapital.com.au/subscribe

Stephanie Sirois Managing Director

Channel Diligence

Wendy Beer Director

Channel Diligence

Channel Diligence specializes in operational due diligence (ODD) consulting and execution, providing tailored solutions through an allocator-lens to institutional investors and alternative asset managers. We deliver rigorous, independent assessments of investment managers, service providers, and governance frameworks — helping clients identify risks, enhance oversight, and strengthen operational resilience.

Channel Diligence combines independent operational due diligence expertise with the strength and stability of its strategic partner, Channel Capital Group, a global institutional platform headquartered in Australia with offices across the United States, Grand Cayman, and Europe.

LUXURY HOSPITALITY AS A STRUCTURALLY UNCORRELATED ASSET:

WHY EXPERIENCE-DRIVEN REAL ESTATE BEHAVES DIFFERENTLY ACROSS MARKET CYCLES

BY PRANAV R. BHAKTA Driftwood Capital

Rethinking Correlation in Real Assets

In institutional portfolio construction, correlation is often treated as a fixed statistic—an output derived from historical return series and applied prospectively as if it were immutable. In reality, correlation is contextual. It shifts across market regimes, liquidity environments, and consumer behavior, and it is heavily influenced by who ultimately drives demand and how pricing power is exercised.

Luxury hospitality occupies a distinctive position at the intersection of real estate, operating businesses, and experiential consumption. It is frequently grouped with hotels as a single asset class and, by extension, assumed to behave cyclically in line with discretionary travel or broader economic growth. That framing, however, is increasingly incomplete.

Over the past decade—and accelerated by the dislocations of COVID, inflationary tightening, and rising interest rates—luxury hospitality has exhibited

structural characteristics that differentiate it from traditional real estate sectors such as office, retail, and even multifamily. When properly underwritten and operated, luxury hospitality displays return drivers that are less tethered to employment cycles, lease duration, or domestic consumption patterns, and more closely linked to global wealth creation, scarcity, and pricing power.

For allocators seeking genuine diversification within alternatives, this distinction is consequential.

Demand Elasticity Starts With the Marginal Customer

Correlation ultimately begins with demand elasticity.

Office demand is driven by corporate hiring and workspace strategy. Multifamily demand tracks wages, household formation, and affordability. Retail follows consumer confidence and discretionary spending.

Luxury hospitality, by contrast, is anchored to a far narrower—but structurally more resilient—demand

base: high-net-worth and ultra-high-net-worth individuals whose consumption patterns are disproportionately insulated from unemployment, inflation, and interest rate volatility. This cohort does not primarily optimize for price. It optimizes for experience, access, privacy, and status.

During periods of economic stress, discretionary consumption does not disappear for this demographic—it consolidates. Spending migrates away from commoditized offerings and toward best-in-class experiences. This “flight to quality” dynamic has consistently favored top-tier luxury assets while midscale and undifferentiated supply absorbs the downside.

The post-pandemic recovery made this dynamic particularly visible. While office utilization lagged and retail fundamentals remained uneven, luxury hotels in supply-constrained resort and gateway markets regained pricing power at a pace unmatched by most real estate sectors. Average daily rates not only recovered but, in many cases, exceeded pre-pandemic levels well before transaction markets normalized.

This outcome was not incidental. It reflects who the marginal buyer is—and who they are not.

Pricing Power as a Structural Feature

One of the most misunderstood attributes of luxury hospitality is its pricing mechanism.

Traditional real estate relies on contractual income. Leases reset infrequently, often lag inflation, and embed duration risk—particularly in rising-rate environments. Even when fundamentals improve, repricing is slow.

Luxury hospitality resets pricing daily.

This operational flexibility is more than a tactical advantage; it is a structural form of inflation protection. When demand exists, pricing adjusts in real time. When supply is constrained by geography, entitlement, or brand selectivity, that pricing power compounds.

Crucially, luxury ADR growth has not tracked GDP or equity markets in a linear fashion. Instead, it has followed global wealth expansion, experien-

tial spending, and demographic shifts toward experience-first consumption—drivers only loosely correlated with traditional business cycles.

From a portfolio perspective, this introduces a return stream that behaves fundamentally differently from fixed-rent assets. Revenue volatility is real, but it is paired with an ability to recover quickly—something lease-based property types structurally lack.

Scarcity That Cannot Be Arbitraged Away

Scarcity is often invoked loosely in real estate narratives. In luxury hospitality, it is tangible.

True luxury assets are constrained by factors that cannot be easily replicated: irreplaceable locations, limited brand participation, capital intensity, and regulatory friction. Waterfronts, historic urban cores, protected landscapes, and culturally significant destinations are finite. At the same time, leading luxury brands are highly selective, limiting flags per market to preserve longterm brand equity.

These constraints materially reduce the risk of oversupply in the very markets where demand is most inelastic. As a result, luxury hospitality has largely avoided the overbuilding cycles that have historically plagued office, retail, and even multifamily during periods of abundant capital.

This supply discipline is a key reason luxury hospitality has exhibited smaller long-term drawdowns and faster recoveries than many traditional real estate sectors, despite short-term volatility.

Branded Residences and

Capital Stack Transformation

One of the most powerful—and often underappreciated—drivers of uncorrelated behavior in luxury hospitality is the integration of branded residential components.

Branded residences fundamentally reshape the capital stack. They convert future experiential value into upfront equity, reduce reliance on construction debt, and shift a portion of market risk from the operating asset to end buyers who prioritize lifestyle and brand affiliation over yield.

From an investor’s standpoint, this structure compresses downside risk while preserving upside exposure. Residential buyers are not underwriting RevPAR volatility; they are underwriting long-term lifestyle utility, brand credibility, and perceived store of value. That is a materially different risk profile.

This is not financial engineering for its own sake. It is a demand-driven response to how affluent buyers increasingly allocate capital toward experiential assets that deliver both personal utility and long-term optionality.

Addressing the Skeptic: Cyclical, Yes—but Asymmetric

A well-informed skeptic will argue that hotels are inherently cyclical and operationally leveraged. This critique is directionally correct—but incomplete.

Luxury hospitality is not immune to shocks. However, correlation must be evaluated through relative performance and recovery trajectory, not point-in-time volatility. Historically, demand compresses first in lower-tier segments, while rate integrity is preserved longest at the top of the market.

By comparison, office assets face structural demand impairment, retail continues to battle secular disintermediation, and multifamily is increasingly exposed to affordability constraints and regulatory intervention. Luxury hospitality’s cyclicality is therefore asymmetric: drawdowns may be sharper, but recoveries are typically faster and driven by pricing rather than occupancy alone.

For diversified portfolios, this asymmetry is precisely what creates diversification value.

Global Demand Versus Local Economies

Luxury hospitality is also frequently mischaracterized because of geographic framing.

Its demand is global; capital markets, labor markets, and fiscal policy are local. A resort in Southern Europe, Mexico, or the Caribbean may be influenced by U.S. travel patterns, but its marginal customer is rarely dependent on a single domestic employment base.

Wealth mobility, currency arbitrage, and cross-bor-

der lifestyle migration further decouple demand from local economic cycles. This global demand pool provides a natural hedge against regional downturns—something most domestically oriented real estate sectors cannot replicate.

Operational Excellence as the Decisive Filter

Uncorrelated performance is not automatic. It is earned.

Luxury hospitality is an operating business embedded within real assets, and outcome dispersion is wide. Assets without genuine differentiation, disciplined cost structures, or aligned branding can underperform materially, particularly during downturns.

For this reason, luxury hospitality should not be viewed as a passive allocation. Institutional underwriting must prioritize management depth, cultural rigor, brand relevance, revenue management sophistication, and disciplined capital allocation across the asset lifecycle.

When these elements are present, luxury hospitality behaves very differently from traditional real estate. When they are absent, correlation rises—and returns suffer.

Portfolio Implications for Allocators

Luxury hospitality does not replace traditional real estate; it complements it.

In portfolios dominated by duration-sensitive income streams, luxury hospitality introduces daily repricing, global demand exposure, scarcity-backed pricing power, and experiential value drivers that are less tethered to employment cycles or interest-rate movements.

In an environment where diversification across equities and fixed income has become less reliable, these attributes are not cosmetic—they are structural.

Conclusion: Uncorrelated by Design, Not by Accident

Luxury hospitality’s uncorrelated behavior is not a post-pandemic anomaly. It is the result of durable structural forces: global wealth concentration, experiential

consumption, mobility, and defensible scarcity.

When paired with disciplined underwriting, credible branding, and institutional-grade operations, luxury hospitality occupies a distinct position within the alternatives landscape—one that cannot be replicated by traditional real estate sectors or easily substituted within a portfolio.

For allocators willing to move beyond outdated categorizations, luxury hospitality is not simply a travel asset. It is a differentiated real asset expression of an experience-driven economy—and one whose correlation profile remains structurally misunderstood.

Pranav R. Bhakta

Senior Vice President, Corporate Business Development Driftwood Capital

Driftwood Capital is a vertically integrated hospitality investment and management platform with more than three decades of experience across acquisitions, development, lending, and operations. The firm focuses on institutional-grade hospitality assets across the branded, lifestyle, and luxury spectrum, leveraging operational expertise and data-driven underwriting to create long-term value across market cycles.

SPECIALIST DIRECT: A MODERN FAMILY OFFICE STRATEGY FOR VENTURE INVESTING

BY PAUL PALMIERI & GRANT NELICK

Grit Capital Partners

Over the last decade, the family office landscape has undergone a quiet but profound transformation. What was once a niche corner of the wealth management world, dominated by multi-generational families and opaque structures, has grown into a highly active, sophisticated segment of the private capital ecosystem. The rise of first- and second-generation entrepreneurial wealth has redefined both the mindset and the mandate of many modern family offices. These families are not merely seeking capital preservation; they are looking for control, alignment, and participation in value creation. Nowhere is this more evident than in the growing appetite for direct investments.

Today, direct private investing is no longer a fringe activity among family offices. According to UBS Family Office data, over 60% of family offices are actively pursuing direct deals, either independently or via co-investment partnerships. Much of this capital is being deployed into technology and innovation-driven sectors, where family principals often bring operating expertise,

networks, or thematic conviction. But while the desire for direct exposure is clear, the path to achieving it in a structured, repeatable way is less so.

At the same time, many advisors to family offices continue to rely on institutional playbooks; most notably the Yale Endowment model popularized by David Swensen. That model, rooted in diversification across illiquid alternatives and exposure to mega-sized fund managers, has merit. But when applied in a subscale context (e.g., allocating $5M into a $2B flagship buyout or venture fund), it tends to underdeliver. The family office becomes just another small LP, without access, without influence, and often with limited visibility into underlying assets.

This paper proposes an alternative: a model we call Specialist Direct. Specialist Direct is a strategy purpose-built for family offices with a desire for direct investment exposure but face structural constraints such as subscale check sizes, limited access and negotiating leverage, fee drag, and thin governance. Rather than

GRIT IS MORE THAN OUR NAMEIT’S HOW WE WORK, HOW WE INVEST, AND HOW WE WIN.

spreading capital across large blind pools or pursuing fully independent direct deals, Specialist Direct involves anchoring a small number of specialist venture capital managers, particularly those raising sub-$150M funds with a focus on seed-stage or early growth investing.

For clarity, in this paper, “specialist” refers to a venture manager investing within a deliberately bounded mandate where they hold specific knowledge and a repeatable edge, typically by sector (e.g., fintech, health, consumer goods), technology domain (biotech, robotics, cybersecurity), or business model (vertical SaaS, infrastructure, marketplaces). We use “specialist,” “sector-specific,” and “thematic” interchangeably throughout. The key lever is that specialization turns domain knowledge such as customers, training datasets, biomarkers, and sales channels, into advantages in access, underwriting/selection, and post-close value-creation, ultimately improving risk-adjusted returns.