APRIL 2026

APRIL 2026

The current position in the Middle East is not affecting Sysco’s route to market at present, but it is increasing pressure across freight, fuel and energy-linked categories. The immediate risk remains cost-led rather than availabilityled, though the wider situation continues to evolve.

OPERATIONS

Sysco distribution remains unaffected at present

• No direct route-to-market disruption is currently being experienced.

• The impact is being felt through transport and energy cost escalation.

Europe remains exposed to disruption in the region

• Europe has an estimated 18% dependency on the Strait of Hormuz for energy imports.

• Global oil production was reported down by 13 million barrels per day (13%) as of the 16th of March.

Emergency surcharges have been introduced

• Sysco hauliers have applied temporary emergency surcharges of 10% on base shipment rates.

• Around 130 containerships, representing 443,550 TEUs, are currently held in the Persian Guld.

The situation is dynamic, but it is expected that the surcharge will not be exceeded within the next quarter.

Dear Customers,

Market conditions remain mixed as we move through April, with protein and seafood supply still tight, disease risk continuing to affect poultry and eggs, and higher energy and freight costs adding further pressure across the supply chain. The current situation in the middle east is not disrupting Sysco routes to market at present, but it is increasing exposure across fuel, logistics and selected raw materials.

Outside protein, dry store markets are broadly stable, and several bakery inputs are easing, although frozen produce, crockery and selected beverage and catering lines remain under inflationary pressure. This report outlines the key developments affecting availability, pricing and planning as we move further into Q2.

Warm regards, Sysco Ireland

YOUR SPECIALIST FOODSERVICE TEAM

04 PROTEIN

06

10

Centre of Plate | Produce | Bakery & Dessert

Catering Supplies & Beverage

Beef | Pork | Lamb

POULTRY

Chicken | Turkey | Duck

12

COOKED MEATS

14

SEAFOOD

Salmon | Cod | Haddock Hake | Prawns

18

20

DAIRY

Eggs | Milk | Butter

CANNED & DRIED

Pulses & Beans | Pasta | Rice | Jam Oils | Tinned Tomatoes & Chickpeas

22 BEVERAGE & CATERING

24

BAKERY & FROZEN PRODUCE

Crockery | Catering Supplies | Beverage

The global food market can be unpredictable, but your supply doesn’t have to be. Our specialist team is here to help you stay stocked with quality options that fit your budget. Whether it’s discovering new products, exploring different price tiers, or finding the best value, we’ve got solutions for you. Talk to your ASM to arrange a meeting.

Centre of Plate

WAYNE WALSH

Wayne brings nearly thirty years of food industry experience, including over two decades as a craft butcher. He combines specialist protein knowledge with proven sales expertise to deliver tailored solutions and trusted relationships for customers.

Centre of Plate

NEIL BRISLANE

Neil has been part of the Sysco team for over 20 years, with the last decade dedicated to Centre of Plate. His deep knowledge helps customers make informed decisions, adding real value to their business.

Centre of Plate

PHILL WARING

Phill joined the business in 2023 after 18 years working as a Chef. His roles were primarily in Fine Dining establishments throughout Northern Ireland, but he also spent time in Australia.

Produce

PATRICK KEOHANE

Patrick joined Sysco over 6 years ago. He has a wide range of experience in the sector from growing potatoes on his family farm to the early days of his career prepping veg in a hotel and working as a kitchen porter. Patrick enjoys meeting new people as part of his role, supporting his customers to improve their business.

Produce

ALASDAIR MacINNES

Alasdair joined the business over 20 years ago, following 25 years as a chef working in busy restaurants. He began his career with Sysco in purchasing before moving to a produce specialist role.

Produce

RUTH POLLOCK

Ruth joined Sysco in 2024 and has over 20 years’ experience within fresh produce. Ruth enjoys working in partnership with her customers to come up with the best solution for their business.

Centre of Plate

KELAN McMICHAEL

Kelan has worked in the industry as a chef for over 25 years, in some of the finest kitchens in the UK and Ireland. He was honoured to be part of a team that cooked in the Hague, representing Ireland and Irish produce.

Produce

SIMON DOHERTY

Simon has over 35 years’ experience in the industry and is an expert in the industry and the produce category. Simon is always willing to go above and beyond to ensure the highest quality service.

Produce

NOEL RYAN

Noel joined Sysco in 2022, however with 35 years in the produce business he brings a wealth of experience to his role. Noel’s belief in Sysco’s customer centric values plays an important role in how he does his job.

Produce

ALISON KIDD

Since joining Sysco in 2022, Alison has cultivated strong relationships with many of our key customers. With a deep understanding of the fresh produce market, Alison provides solutions that drive growth and success for her customers.

Catering Supplies & Beverage

JOANNE McCUSKER

Joanne joined Sysco in 2024 and brings over 30 years’ experience to her role. She began her career in the licensed trade and has owned two coffee shops before progressing into sales.

Catering Supplies & Beverage

PATRICK KEOGH

Patrick joined Sysco in 2021 and prior to this spent time in multiple FMCG and foodservice businessess. He now works as a sales specialist in Dublin northeast, offering practical advice and support, while identifying solutions to help them reach their full potential. In his spare time Patrick enjoys attending his kids sporting activites. He is also a keen horse racing syndicate member, aiming to unlock hidden potential in horses that they own.

Catering Supplies & Beverage

JONATHAN O’SHEA

Jonathan joined Sysco in 2022 with over 18 years experience as a chef. Jonathan has vast knowledge and experience in the hospitality industry having worked in restaurants across all levels – from Gastro pubs to Michelin Star.

Bakery & Dessert

BRONAGH BEATTIE

Bronagh joined Sysco in 2023 and has over 20 years’ experience as a chef, working in fine dining restaurants, cafes and hotels worldwide. She enjoys supporting her customers with new ideas and innovation.

Bakery & Dessert

BRENDAN SEWELL

More than 32 years’ experience in the food industry in Ireland gives Brendan a deep understanding of the sector. Previously working as a Chef and a pastry chef in 5* Hotels, Brendan has a wealth of knowledge to share with his customers.

Bakery & Dessert

ELAINE MEADE

Elaine joined the business in 2024 and brings over 15 years experience in the industry to her role. After training as a chef, Elaine worked in restaurants, hotels and cafes across Ireland and London, later opening her own café In Clare.

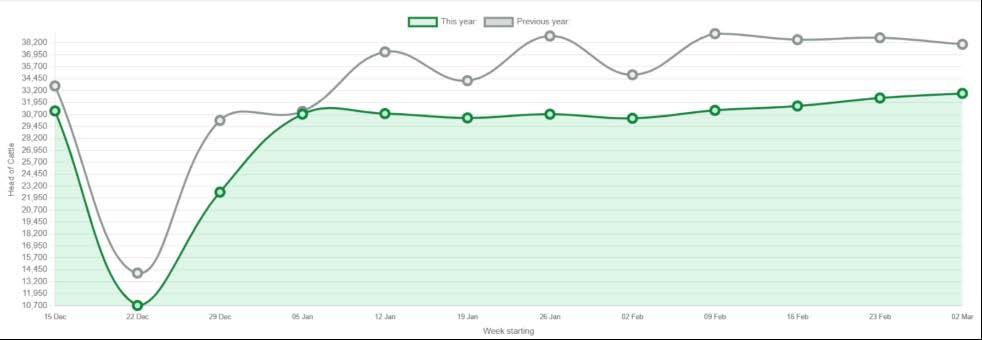

The Irish beef market remains tight this spring, with lower cattle throughput and a further reduction in prime beef supply expected this year. Some easing has appeared in recent weeks as more winter-finished cattle have come forward, but the wider tone remains firm heading into summer.

www.agriland.ie/farming-news/france-still-no-1-in-eu-beefproduction-but-ireland-set-for-sharp-drop

Lower cattle numbers continue to limit availability.

• Cattle throughput is down 15% in the first six weeks of the year.

• Prime beef supply is forecast to decline by a further 4% in 2026.

Recent softness is expected to prove temporary.

• More winter-finished cattle have created some short-term easing.

• As the market moves from shed-finished to grass-finished stock, supplies are expected to tighten again.

Export support remains important.

• R3 steer prices remain strong.

• Lower UK and EU production continues to support demand for Irish beef.

Seasonal movement is likely across key lines.

• Cube rolls and rib eyes remain exposed to firmer pricing.

• Fillets are showing some signs of softening.

The market remains firm into summer.

• Supplies are low and demand remains steady.

• Energy and transport costs remain an added risk around the base meat price.

The Irish pig sector enters 2026 under continued financial pressure, with feed, energy, and labour costs still weighing on margins. Although EU prices weakened in late 2025, tighter production may support some recovery over the coming months.

Farm margins remain under pressure

• Pig prices fell by 5% in 2025, averaging 207c/kg.

• High feed, energy, and labour costs continue to restrict profitability.

Late-2025 weakness may begin to correct

• EU pork prices fell in Q4 2025 following ASF disruption in Spain.

• Chinese anti-dumping duties on EU pork reduced export competitiveness.

Tighter production should offer support

• EU pork production is forecast to decline by around 1-1.2%.

• Lower output should help rebalance the market as the year progresses.

Pricing is expected to remain firm

• Irish and EU pork prices are expected to hold steady to firm.

• Any material recovery in producer margins will depend on input-cost relief.

The Irish lamb market is expected to remain stable to firm through spring and summer, supported by reduced supply and strong export demand. European production trends continue to reinforce the higher price environment.

https://www.agriland.ie/farming-news/sheep-trade-up-toe9-kg-paid-for-hoggets-as-price-and-trade-surging/

KEY POINTS

SUPPLY

Irish sheep numbers remain well behind last year

• Sheep throughput fell 18% in 2025.

• Lower domestic production, a smaller breeding flock, and fewer lambs continue to restrict supply.

DEMAND

Export demand remains supportive

• Demand for Irish lamb remains strong, particularly in France and across the wider EU.

• Declining European lamb production is adding further support to pricing.

SEASONALITY

Spring processing may lift slightly, but not enough to rebalance supply

• Easter and Eid falling close together may create a slightly larger early-spring carryover.

• This is not expected to offset the wider supply shortage.

OUTLOOK

Firm conditions are expected to continue

• Teagasc expects 2026 to be a positive year for sheep farmers.

• Lamb prices remain well above longer-term averages and are expected to stay elevated.

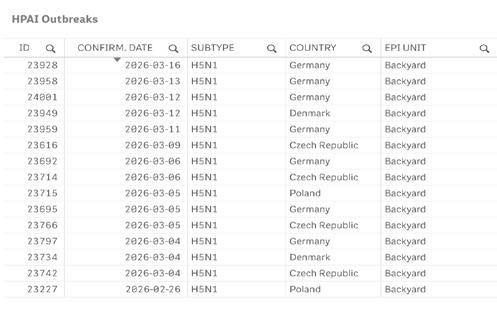

The EU poultry market is steady to firm entering Q2, supported by consistent demand and ongoing disease-related caution. While selected turkey lines offer some value, the wider category remains exposed to avian disease risk and producer inflation.

ENVIRONMENT

ND and HPAI remain the main watchpoints

• Germany confirmed its first Newcastle Disease case in around 18 years in February 2026 in a turkey flock.

• HPAI circulation remains elevated across Europe, with over 2,500 detections reported between December and February.

BROILER MARKET

EU pricing remains firm into spring.

• EU broiler prices are around €293.66/100kg.

• The market is broadly steady month on month and around 3.3% above last year.

Core supply is steady, but seasonal demand is building

• Fresh Polish breast remains around €4.60/kg, while frozen values are slightly firmer.

• Wings and drums are seeing stronger seasonal demand.

TURKEY

Selected value remains, but risk is elevated

• Certain turkey SKUs moved down by around 2% for April.

• Ongoing ND detections in Central Europe mean the category remains under close review.

DUCK

Supply remains sensitive to production and welfare changes

• European duck markets remain exposed to labour, welfare, and vaccination-related cost pressure.

• Frozen supply may tighten further if bird availability stays limited.

Steady to firm through Q2

• Wings and drums are likely to remain seasonally supported.

• Close monitoring of disease developments remains essential across chicken, turkeyand duck.

The total number of avian influenza cases notified by each Member States/Reporting Countries in different epidemiological units (commercial poultry farm, backyard farms, other captive birds and wild birds) is shown in the map below, complemented by a table that contains key information about each outbreak.

2,510

Cooked meats continue to reflect broad inflation across protein, eggs, and packaging. The market remains under pressure, even where individual raw materials are showing better balance.

APRIL MOVEMENT

Moderate inflation continues across the category

• Average movement is around +2.9%.

• Reported increases range from +1% to +5%, depending on product mix.

RAW MATERIALS

Multiple upstream pressures are feeding through

• Poultry, turkey, beef, fish proteins, eggs, and packaging are all contributing to cost pressure.

• Beef-based cooked meats saw earlier-year uplifts tied to manufacturing inflation.

SUPPLIER POSITION

Cost escalation remains broad based

• Producers across Western, Central, and Northern Europe continue to report higher raw material and operating costs.

• Wage indexation and packaging inflation remain recurring themes.

OUTLOOK

Further pressure is likely through Q2

• Categories with higher poultry, fish, egg, or beef content remain the most exposed.

• Lead times and availability may vary by product and origin.

+2.9% AVERAGE MOVEMENT APRIL 2026

Seafood markets remain volatile, with quota reductions and biological constraints continuing to restrict supply across several key species. Buyers are showing increased interest in breaded and battered formats as they look for greater consistency and cost control.

Farmed Atlantic salmon remains firm, with constrained biomass and biological challenges continuing to restrict output. Higher feed, energy, and logistics costs are also supporting wholesale pricing.

SUPPLY

Biological pressure continues to limit production

• Tight biomass levels remain a feature across key farming regions.

• Producers continue to manage higher feed, energy, and transport costs.

PRICING

Wholesale values remain firm

• Average weekly salmon prices in February increased by 3.2% month on month.

• Higher fuel and logistics costs are adding further support.

DEMAND

Foodservice demand remains steady

• Demand across Ireland, the UK, and the EU remains supportive.

• This is limiting any meaningful easing in the market.

OUTLOOK

Volatility is expected to continue

• Prices are likely to remain high and responsive to supply events.

• The market remains exposed to both biology and freight.

Cod prices have moved higher following quota cuts across key North Atlantic fisheries. Higher vessel operating costs are adding further pressure to an already tight market.

SUPPLY

Quota reductions are tightening the market

• Available supply into both the UK and EU has reduced in recent weeks.

• Lower quotas continue to restrict raw material access.

COST BASE

Fleet operating costs are increasing

• Fuel and transport inflation are raising first-sale and wholesale costs.

• These increases are feeding through the supply chain.

PRICING

The market remains firm

• Average weekly cod prices in February increased 2.4% month on month.

• Limited supply continues to support high replacement values.

OUTLOOK

Firm conditions are expected to persist

• Cod remains one of the tighter whitefish species.

• Buyers may continue to look for substitution opportunities where possible.

Haddock supply has tightened sharply as reduced quotas and lower catch volumes continue to limit availability. Prices remain elevated and closely tied to both quota management and fishing costs.

SUPPLY

Availability remains restricted

• Lower quotas and weaker catches continue to tighten the market.

• Fresh and frozen supply remains limited across key origins.

PRICING

Higher operating costs are sustaining inflation

• Fuel costs are increasing vessel expenses.

• This is feeding through to firmer wholesale pricing.

OUTLOOK

Elevated pricing is expected to continue

• Prices are expected to remain high while supply stays restricted.

• Ongoing substitution away from cod may add further demand pressure.

Hake has moved higher as buyers look for alternatives to cod and haddock. Supply is steadier than some other whitefish lines, but rising demand and logistics costs are now feeding into the market.

DEMAND SHIFT

Substitution is supporting the category

• Buyers are turning to hake as cod and haddock become more expensive.

• This is broadening demand across wholesale and foodservice channels.

SUPPLY

Steadier than cod, but not immune to inflation

• Southern Hemisphere supply remains relatively stable.

• Fuel and logistics costs are still feeding into replacement values.

PRICING

Firm, though still comparatively better value

• Hake prices have moved higher in recent weeks.

• It remains one of the more competitive whitefish options versus cod.

OUTLOOK

Further firmness is likely

• Continued substitution is expected to keep the market supported.

• Earlier planning may be required to secure volume.

Prawn markets remain volatile, with tight raw material availability continuing to drive instability. The upcoming Indian Vannamei harvest should improve supply, though pricing is likely to remain sensitive.

SUPPLY

Raw material remains tight in the short term

• Price volatility continued throughout 2025.

• Tight availability is expected to remain a feature in the near term.

Mid-April should improve booking conditions

• The main Indian Vannamei harvest begins in mid-April.

• This should provide a useful opportunity for new container bookings.

Market access may improve over time

• India has agreed a new free trade deal with the EU.

• The pricing impact will depend on timing and implementation detail.

Volatility remains the core theme

• Supply should improve seasonally, but the market is not expected to normalise quickly.

• Earlier booking may help manage risk.

India has agreed a new free trade deal with the EU.

The egg market has yet to fully recover from the disruption caused by the severe 2025 outbreak. Although flock rebuilding brought some temporary relief, fresh disease pressure and elevated feed costs have tightened the position again.

Recovery has been interrupted

• New HPAI outbreaks in early 2026 led to further culling in major U.S. production regions.

• Fresh cases in Europe, particularly in the Netherlands, disrupted export activity and tightened global supply.

The market remains vulnerable

• International buyers have returned to the open market as export channels tighten.

• This is increasing competition for already limited availability.

Production costs remain high

• Corn and soybean meal continue to trade at elevated levels. .

• These costs are sustaining pressure across the supply chain.

Firm conditions are expected to continue

• Egg supply remains fragile.

• Full normalisation is not expected in the near term.

Milk market sentiment is neutral, with year-on-year volumes and milk solids both trending higher. Supply appears comfortable for now, which may limit any further upside unless demand improves.

Milk flows remain robust

• Year-on-year milk volumes are higher during the assessment period.

• Butterfat and protein levels remain supportive.

Balanced rather than bullish

• Current sentiment is neutral.

• Supply remains strong enough to keep the market well covered.

Stable conditions are expected near term

• Comfortable supply may continue to weigh on pricing.

• Demand will need to strengthen for sentiment to shift materially.

European butter strengthened in late February as buyers returned to the market to take advantage of lower year-on-year levels. Stocks remain seasonally high, but demand has been firm enough to draw inventories down.

Butter moved higher month on month

• Unsalted Butter EXW EU was assessed at €4,400/MT on 26 February.

• This represented a €500/MT increase month-on-month.

Improved buying interest supported the market

• Both consumer and industrial buyers returned to cover requirements.

• Lower year-on-year pricing encouraged additional activity.

Production remains supported by good milk flows

• EU butter stocks remained high for the season.

• Fresh production continues to be supported by strong milk supply and good milk fat levels.

The market has stabilised at a firmer level

• Current pricing is more resilient than earlier in the season.

• Availability remains supported, though further gains will depend on demand.

Year-on-year volumes and milk solids are both trending higher.

Canned and dried grocery markets are broadly stable heading into the next quarter, with balanced global supply and demand across most core staples. Outside of a small number of regulatory watchpoints, this remains one of the more stable parts of the market.

PULSES & BEANS

Adequate supply is keeping the market flat

• Pulses continue to benefit from stable global availability.

• No major disruption indicators are currently evident.

PASTA

Strong wheat supply is supporting stability

• Wheat production forecasts for 2026 remain favourable.

• Cost pressure on durum-based products remains limited.

RICE

Globally balanced with only mild firmness in some origins

• No major trade or weather disruption is currently signalled.

• Mild firmness may appear depending on export behaviour in key origins.

OILS

Flat to slightly softer tone

• Edible oil markets remain broadly well balanced.

• Softer global demand is reducing upside pressure.

TINNED TOMATOES & CHICKPEAS

Stable with no major near-term disruption

• Tinned tomatoes remain steady on stable EU production.

• Chickpeas are following the same balanced pattern as the wider pulses market.

New EU jam legislation due from 14 June 2026 may create moderate cost pressure across jam lines. Higher fruit content requirements are expected to lift both formulation and raw material costs.

REGULATORY CHANGE

Fruit content requirements are increasing

• Minimum fruit content for jam will rise from 35% to 45%.

• Extra jam will increase from 45% to 50%.

COST IMPACT

Higher fruit input is the main inflation driver

• Reformulation, stabiliser, compliance, and labelling changes will all add cost.

• Reduced sugar content may also alter processing economics.

Moderate inflation is likely once the rule takes effect

• Fruit input costs are expected to be the largest driver.

• Some additional pressure may also develop in fruit supply chains.

Bakery inputs are mixed, with softer pricing across several core commodities but continued inflation in labour and frozen produce. The wider tone is more balanced than earlier in the year, although pressure remains concentrated in selected lines.

BUTTER-BASED PRODUCTS

Dairy fat costs are easing in finished goods

• Around 5% deflation is now being seen on butter-based products.

• Strong milk and cream supply, along with comfortable stock levels, is supporting the softer trend.

WHEAT-BASED PRODUCTS

Comfortable grain supply is keeping the market stable

• Around 8% deflation is now being seen across wheat-based products.

• Strong 2025/26 production forecasts continue to limit upside pressure.

COCOA-BASED PRODUCTS

Softer demand is reducing cost pressure

Around 7% deflation is being seen across cocoa-based products.

• Around 7% deflation is being seen across cocoa-based products.

• Steady supply from key origins is helping maintain a calmer market.

SUGAR-BASED PRODUCTS

Improved supply is feeding through into lower pricing

• Around 8% deflation is being seen across sugar-based products.

• Strong crops in Europe, Brazil, and India have helped rebuild stocks.

LABOUR & MINIMUM WAGE

Labour remains a structural inflation driver

• Labour-related inflation remains around 6% on average.

• Minimum wage increases, recruitment pressure, and training costs continue to feed through.

FROZEN PRODUCE

Frozen remains one of the strongest inflationary areas

• Around 28% inflation is being seen across frozen produce.

• Weather pressure, lower yields, energy-intensive processing, and logistics are all contributing to higher costs.

OUTLOOK

Bakery inputs are calmer, but frozen remains exposed

• Butter, wheat, cocoa, and sugar are expected to remain relatively stable to softer.

• Frozen produce remains vulnerable to weather, l abour, and energy costs.

Crockery has moved sharply higher following an increase in EU anti-dumping duties on ceramic tableware and kitchenware imported from China. The change has had a direct effect on replacement cost.

Catering supplies are currently flat overall, but early signs of raw material inflation are beginning to emerge. Energylinked materials remain the main watchpoint, particularly given continued tension in the Middle East.

RAW MATERIALS

Energy-sensitive inputs are starting to rise

• HDPE and LDPE prices are up around 4% month on month.

• Aluminium prices on the LME are up around 12% month on month.

MARKET TONE

Current pricing is stable, but risk is building

• Prices remain flat at present across much of the category.

• Exposure to energy and utility costs keeps the market vulnerable.

OUTLOOK

Upside risk is increasing

• Further escalation in the Middle East may drive sharper raw material increases.

• Plastics and aluminium-based items remain the most exposed.

Crockery has moved sharply higher following an increase in EU anti-dumping duties on ceramic tableware and kitchenware imported from China. The change has had a direct effect on replacement cost.

POLICY CHANGE

Anti-dumping duties have increased materially

• The EU duty has risen to a uniform 79%.

• The new rate came into force on 7 February.

PRICE IMPACT

Sharp inflation is now visible

• Crockery costs have increased by around 25%.

• The increase reflects the duty change rather than a short-term supply issue.

OUTLOOK

Higher pricing is expected to persist

• The market is likely to remain elevated while the duty remains in force.

• Replacement planning may need closer review.

Soft beverage lines are seeing moderate inflation, driven by levy increases and ongoing supplier cost pressure. Labour and electricity remain the most consistent drivers behind current movements.

Moderate inflation continues across the category

• Soft beverages are seeing increases of around 2-5%.

• Cost movement varies by supplier and format.

Levy increases continue to feed through

• Sugar-related levy increases are adding cost pressure across affected lines.

• This remains an ongoing rather than one-off driver.

Structural costs remain the main issue

• Key suppliers continue to implement annual increases.

• Labour and electricity remain the two most common cost drivers.

Further measured inflation is expected

• The market is not seeing extreme volatility.

• Even so, selected beverage lines are likely to continue moving upward through the year.

The market is not seeing extreme volatility.

Markets remain most challenging in beef, lamb, seafood, eggs, frozen produce, and selected packaging-linked categories. Elsewhere, bakery and dry-store inputs are showing better balance, offering some welcome stability in an otherwise mixed environment.

Our teams will continue to monitor developments closely and support customers with planning, product alternatives, and specification reviews where market conditions require them.