JUST MORTGAGES NEWS As we head into Easter, it feels like the right time to pause, take stock, and look ahead to what the next few weeks may bring. The UK mortgage market continues to show signs of cautious movement; rates remain a key focus and, with ongoing uncertainty around the pace of change, many borrowers are actively reviewing their options.

This creates both an opportunity and a responsibility. Clients are looking for reassurance, guidance, and timely information, which makes proactive engagement more important than ever. This also highlights just how critical it is that we stay close to our clients, anticipating needs, starting conversations early, and ensuring no opportunities slip through the net.

There is a wealth of experience within the Just Mortgages team, your managers and supervisors are there to help guide and support you where needed. Enjoy your break

Jessica Earey, Head of Central Operations

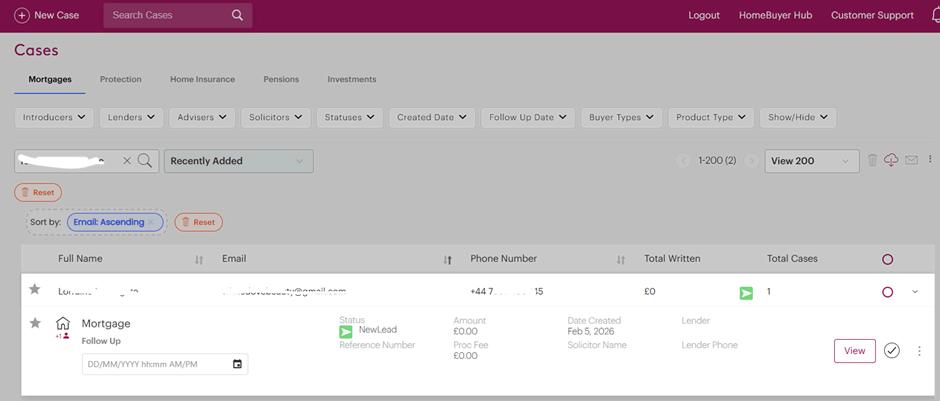

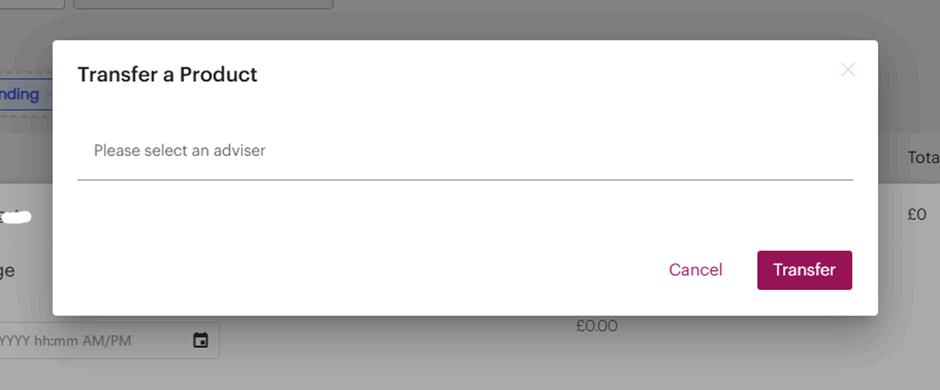

HOW TO TRANSFER A MORTGAGE CASE WITHIN SMARTR365. Who Can Transfer Cases

Activeadviserscantransfercasestoanotheradviser.

Managersalsohavepermissiontotransfercases

OnlytheSystemAdministrator,JessicaEarey,cantransfercasesfromtheLeaverPot. TransfersfromtheLeaverPotrequireDSDapprovalbeforetheycanbecompleted.

How to Transfer a Case

1.GototheCasesPage LogintoSmartr365andnavigatetoCasesfromthemainmenu.

2 LocatetheCase Searchfortheclientby:

Enteringtheclient’snameinthesearchbar,or Usingfilterssuchas: Adviser

Introducer Lender

3.OpenCaseOptions

Onceyoufindthecaseyouwishtotransfer: Clickthethreedots(⋯)nexttothecasetodisplayadditionalfunctions

4.SelectTransfer

ClickTransfer(representedbyatrayicon).

5.ChoosetheAdviser

Selecttheadviseryouwanttotransferthecasetofromthedropdownlist. Confirmthetransferrequest

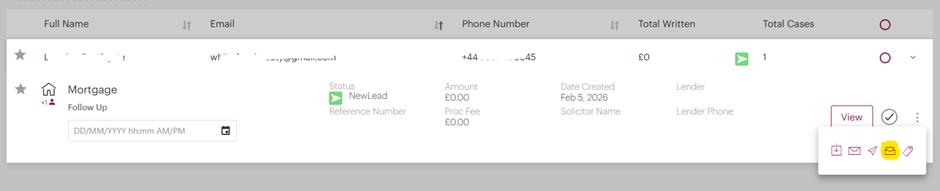

Accepting the Case Transfer Theadviserreceivingthecasemustacceptthetransferbeforeownershipchanges GotoSettings. SelectCaseTransfers

TheLeadTransferListwillappear ClickAccepttotakeownershipofthecaseorRejecttodeclinethetransfer.

Cancelling a Transfer Request Ifyouneedtostopatransferrequest:

GotoSettings → CaseTransfers. LocatetherequestintheLeadTransferList ClickCancelRequest.

Important

Support Directory toyourDSD.

Googlereviews–Chris.Pavlou@justmortgages.co.ukChrisPavlou managesthereporting,pleaseemailChriswithanyquestionsonthe reports.

JMFinancialPromotions-financialpromotions@justmortgages.co.ukFor allquestionsoradviceonwhatyoucanpostonsocialmediaandwhat mayneedapprovalfromOpenwork.

DigitalMarketing–digital@justmortgages,co.ukforsupportonhowto usesocialmediaplatforms,Googleplatformquestions,requestsfor socialmediapostsandaccesstoourdigitalmarketinglibrary(SPOS)

Smartrsupport–usetheAIchatbot,thiswilldirectyoutothesupport teamifyourquestioncannotbeanswered.Thisisanintuitivefeature,so themoreyouuseitthemoreitlearns!

ConcertHubsupport–forallConcertHubrelatedqueriespleasecontact First.Ifthisispasswordrelated,pleasechoosetheIToption.

AMI HIGHLIGHTS THE FCA'S REGULATORY PRIORITIES TheAssociationofMortgageIntermediaries(AMI)hashighlightedtheFCA’sregulatory priorities.Here’sthefullnotefromAMI:

What are the new Regulatory Priorities Reports?

TheFCAannouncedearlierthisyearthatitplanstoreplacemorethan40portfolioletters withnewsector-specificRegulatoryPrioritiesreports.ThesereportswilloutlinetheFCA’s workineachsector,itsplannedactivitiesandtheexpectationsithasoffirms,while highlightingkeyareaswherestandardsshouldbeimproved.

AMIactivelyengageswiththeregulatortoreviewthenewMortgageandInsurance RegulatoryPrioritiesreportsandwiderinitiatives,providinginsightsthathelpinfluence theirpolicywork.

Key priorities from the Mortgage report

WorkundertheMortgageRuleReviewtocontinue,withfocusonsimplificationof mortgagerulestosupportconsumersreachtheirhomeownershipgoals.

Explorationofsupportavailableformortgageborrowersinfinancialdifficultyand potentialforimprovementsforsignpostingtoavailableresources.

Expectationsthatresponsiblelendingensurestherightoutcomeisachievedforeach customer.

Aspartofthebroaderworkonqualityofadvice,theywillbecontinuingwithworkwithin thesecondchargemarket.

Focusondebtconsolidationacrossfirstandsecondchargemortgagesensuring productrecommendationsaresuitableforconsumerneeds.

Arequirementforrecord-keepingtobemoreextensiveinordertoproperlyevidence suitabilityofadvice.

FCAhasfoundevidenceofconditionalselling(estateagentsrequiringconsumersto usespecificmortgageintermediaries)andwillbelookingtoaddressthis.

Key priorities from the Insurance report

Improvingconsumerunderstanding,claimshandlingandservicequalityremainsakey focus–especiallyfollowingtheWhich?supercomplaint.

Continuetoincreaseaccesstoinsurancetoprotectconsumersandthereforeimprove theiroverallresilience

Ongoingsupportofgrowthandinnovationwithintheinsurancemarket.

Ongoingrulereviewstohelpsimplifyregulationandencourageinnovationwithinthe market.

WhataretheFCAareexpectingfirmstodoasaresultofthereport?

TheFCAhighlightseveralexpectationsfromfirmsgoingforwardinbothreports Wehave highlightedthekeyactionsthatmemberscantakeinourfactsheetsbelow.

Mortgage report - FCA expectations»

Insurance report - FCA expectations»

Tohelpmembersputtheguidanceintoaction,AMIwillcollateourkeyfactsheetsand membercommunicationslinkedtothetopicshighlightedbytheFCA.Wewillsharethis withmembersandidentifywhereadditionalsupportmayberequired.

Wemaintainongoingengagementwiththeregulator,ensuringmembers’perspectivesare heardandwelcomeyourfeedbacktosupportourdiscussionswiththeFCA.

SANTANDER’S BROKER PERCEPTION BAROMETER IS BACK Clients need your support

LastDecember,SantanderlauncheditsnewBrokerPerception Barometer,aquarterlylookathomeowners’perceptionofmortgage brokers.

OnFriday13March,Santander’slatestwaveoftheBarometerwas launchedanditmakesforfascinatingreading.Forthesecondquarter runningitrevealsthattwothirdsofhomeownersfeelthatthey couldn’thavegonethroughthehomebuyingorremortgagingprocess withoutthesupportoftheirbroker.Italsoshinesalightonthe experienceoffirst-timebuyersandshowsthecriticalrolebrokersplay supportingthisaudience.Somuchso,thattwofifthsofFTBs admittedtoWhatsappingtheirbrokeratleastweeklyduringthe purchase.

SantanderwillberunningtheBarometeronaquarterlybasistogeta freshviewofconsumers’attitudesandexperiencesofusingabroker.

HSBC | DON'T GIVE MORTGAGE FRAUD A CHANCE FollowingthesuccessofitsQ1Fraudwebinars,HSBCisexcitedto announceitiscontinuingtheseforQ2.

TheseCPDaccreditedsessionswillgiveyoupracticalinsightsintothe latestfraudtrends,helpyourecognisesuspiciousmortgage applications,interpretCIFASalerts,andspotkeyredflags.HSBCwill alsocoveremergingrisks,sharestrategiestoprotectyourclientsand guideyouonkeepingyourbusinesssecureandcompliant.

It’sagreatchancetosharpenyourfraudpreventionskillsandboost yourconfidenceintacklingfinancialcrime.Don’tmissout!

How to register (all last 45 minutes)

Simply clickonyourpreferredoptionbelowandenteryourdetails:

Monday 20th April – 1:00pm

Tuesday 12th May – 09:30am

Friday 19th June – 12:00pm

Onceconfirmed,pleasesavetheinvitationtoyourcalendar.

Please note, you must register and attend the webinar individually to receive your CPD certificate.

UPFRONT COSTS A REASON FOR HESITATION? NOT ANYMORE. YoutoldPrecisethatupfrontcostswereholdingyourresidentialcustomers back.So,theyacted.They’vescrappedstandardvaluationfeesonproperties upto£400kandreducedtheassessmentfeetojust£99.

Availableacrossallproducts.

This will:

Reduceupfrontcostsforpurchasesandremortgages Removebarrierswherefeescannotbeaddedtotheloan Makeiteasierforyoutosubmitcases

PRINCIPALITY INTRODUCE NEW INCOME BOOSTS FOR YOUR CLIENTS New: Income boosts:

Universalcredit

.Weacceptuniversalcreditat100%

.Atleast1applicantmusthaveanearnedincome

.Wewillacceptthestandardallowanceandchild’sallowanceIncluding childcarecosts(ifapplicable)

We will not accept:

.Theseuniversalcreditelements–housing,healthcosts,energysavings homeimprovementsorprisonvisits;and

.Ifthebenefitincomeisinjointnames(withtheotherpersonnotonthe mortgageapplicationorisanon-borrowingoccupier)

Child benefits

.Weaccept100%ofchildbenefits

.Thiscanonlybeconsideredalongsideamaximumincomeof£60,000 .ADepartmentofWork&Pensions(DWP)childbenefitletterisrequired alongsideincomeevidence

Zero hours contractors

We require:

.Aminimumof12months’consistentincomeandcontinuous employmentwiththesameemployer;andIncomeevidenceincludingthe last2P60documents,last3months’payslipsandmostrecentbank statements.

TML SEE THE LEND, NOT THE LIMITATIONS. Affordabilitypressuresarereshapingthemortgagemarket andborrowersarefeelingit.

RecentresearchbyTheMortgageLender(TML)fromtheir HomeA-Loanreportshowstheaverageadultisnow£224 worseoffeachmonth,risingto£262forexistingmortgage holders.It’snosurprisemanyarehavingtorethinktheir options.

Contractors,freelancersandself-employedprofessionals continuetoprovethemselvesashighlyreliableborrowers.In fact,TMLresearchshowsthat79%ofself-employed borrowershavenevermissedamortgagepayment,compared withjust49%oftraditionalfull-timeemployees.

Still backing the self-made & the side-hustlers

Insteadofrelyingonoutdatedpayrollassumptions,TML considerprofitbeforetaxandrealearningpower,recognising incomeasit’sactuallygenerated.Byvaluingrealbehaviour, realincomeandrealambition,TMLhelpmoreoftheself-made moveforwardwithconfidence

The Mortgage Lender’s residential mortgage offering is designed to see the whole picture:

Up to 5.5x LTI

Up to 95% LTV residential mortgages

Profit before tax plus salary for limited company directors, giving a greater capacity to lend

Latest year’s figures for self-employed

Contractors considered with just three months’ history (income up to a max weekly rate × 48)

Additional income considered – including benefits, maintenance and second jobs

Reaching Resilience Report & March Webinars LV=recentlylaunchedtheirnewReachingResiliencereport,consumer researchthatexploresfinancialresilienceamongstUKworkersandhow preparedthey’dbetoexperienceaprotectionevent.Thereportispacked withinsightstofuelyourprotectionconversationsin2026,including actionabletakeawaysyoucanuseinyourapproach.

The report looks at:

Thegapbetweenperceivedfinancialresilienceandreality, Alookattrendsbycoreclientgroupsincludingfirsttimebuyers, parents,andself-employed Whatthismeansforprotectionconversationswithyourclients.

YoucanaccesstheReachingResiliencereporthere.

PROTECTION & GI NEWS Fromtomorrow(31March2026)Axawillbewithdrawingfrom Paymentshield’sLandlord’sInsurancepanelduetoachangeinrisk appetite.Untilthatdate,Axawillhonourallnewbusiness applications.

PleaseensurethatanyPaymentshieldLandlord’sInsurance quoteswhereAxaaretheinsureraresubmittedwithastartdate onorbefore31March2026.

Inpreparationfortheirwithdrawal,allAxaquoteswillhavea reducedquotevalidityperiodwhichwillexpireonthe31March, comparedtotheusual60or90dayperiod.

Further information

IfyouneedanysupportorhaveaquestionaboutAxa’s withdrawal,simplycontactourteamusingthelinkbelowandyour BusinessDevelopmentManagerwillbeintouch: www.paymentshield.co.uk/advisers/contact-us

Thepastweekhasdeliveredasharpandnotableshiftinmarketsentiment, onethatyouwillbeacutelyawareofwithyourconversations.

Atamacrolevel,thedominantdriverremainsgeopolitical.Escalating tensionsintheMiddleEasthavepushedoilpricesabove$100,reigniting inflationconcernsandforcingarapidrepricingofinterestrate expectations.UKswaprateshavereactedaccordingly(seebelowfora trackeronSwaps)andlendershavemovedquicklytoprotectmargins.

AfterarelativelyoptimisticstarttoMarch,we’veseenadecisivereversal. AverageUKmortgagerateshaveclimbedbacktoc.5.4%–5.5%,withtwoandfive-yearfixesrisingintandem. Morenotably,liquidityhastightened.ProvidersincludingClydesdaleBank, FleetMortgages,CoventryBuildingSocietyandFamilyBuildingSociety havewithdrawnproducts,somepullingentirefixed-raterangesfromthe market. Thisisacriticalsignal:lendersarenotjustrepricing,theyaresteppingback toreassessrisk.Foryou,thisreinforcestheneedtomanagepipelinerisk andsetrealisticexpectationswithyourclientsaroundproductlongevity.

DespitetheBankofEnglandholdingbaserateat3.75%,mortgagerates havecontinuedtorise,underliningtheforward-lookingnatureoflender pricing.Marketsarenowpricinginpotentialratehikeslaterin2026,a materialshiftfromtherate-cutnarrativeseenjustweeksago.

Thepracticalimpactisnowhittingborrowers.Mediaexamplessuggest remortgaginghouseholdsfacingincreasesof£600+permonthasultra-low fixeddealsrolloff. Thiscreatesaclearopportunityforyoubutalsoaduty toproactivelyengageyourclientsearly.

Swap’scontinuetobevolatile,howeverhavesettledslightlyinthe lastfewdays,albeitsome0.2-0.4bpshigherthanaweekprior.