YEAR ENDED 30 JUNE 2025

AsaClimateReportingEntity (CRE)underthe Financial Markets Conduct Act 2013, South Port New Zealand Limited (South Port or the Group) is publishing our second Climate-Related Disclosures (CRD)and extending our environmental reporting fromprevious Annual Reports. These CRD comply with the Aotearoa New Zealand Climate Standards (NZ CS) 1, 2 and 3 issued by the New Zealand External Reporting Board. This report is South Port’s CRD

South Port is developing its capacity to comprehend and respond to the challenges that our business faces from climate risks. The main accomplishments in the reporting period from 1 July 2024 to 30 June 2025 are:

1. Prepared Transition Plan to set our strategy regarding climate change impacts

2. Implementation of Green House Gas (GHG) emissions accounting system to facilitate calculation, reporting, and audit of our emissions

3. Developing Energy Master Plan to identify potential opportunities towards decarbonisation

4. Completed a sea level rise and storm surge study to understand possible physical impacts on our assets

5. Completed the annual review of the Risk Assessment, including climate-related risks.

6. Completed the annual review of Scenario Analysis

7. Development of Sustainability Strategy to formalise our Corporate Sustainability approach (People, Planet, and Prosperity), according to Sustainable Development Goals (SDGs) including SDG13- Climate Action.

8. Obtained assurance of our Scope 1 and Scope 2 GHG Emissions

In preparing South Port’s CRD, the Board and Executive Leadership Team (ELT) have elected to use the following Adoption Provisions in NZ CS 2 in FY25:

• Adoption provision 2: Anticipated financial impacts. A qualitative description of anticipated financial impacts has been provided.

• Adoption provision 6: Comparatives for metrics. As required, we have provided one year of comparative metrics (including Scope 3 GHG emissions).

• Adoption provision 7: Analysis of trends.

• Adoption provision 8: Scope 3 GHG emissions assurance.

Important Note: South Port has used reasonable efforts in the preparation of this CRD to provide accurate information, but cautions reliance being placed on representations that are necessarily subject to significant risks, uncertainties, or assumptions. This report contains forward-looking statements, including climate-related metrics, climate scenarios, assumptions, estimated climate projections, forecasts, statements of South Port’s future intentions, estimates and judgements that may not evolve as predicted. These statements necessarily involve assumptions, forecasts and projections about South Port’s present and future strategies and South Port’s future operating environment.

Such statements are inherently uncertain and subject to limitations, particularly as inputs, available data, and information are likely to change. South Port has sought to provide a reasonable basis for forward-looking statements and is committed to progressing our response to climate-related risks and opportunities over time but is constrained by the novel and developing nature of this subject matter. Climate-related risk management is an emerging area and often uses data and methodologies that are developing and uncertain. Climaterelated forward-looking statements may, therefore, be less reliable than other statements South Port may make in its annual reporting.

We have based these statements on our current knowledge as of 16 September 2025. There are many factors that could cause South Port’s actual results, performance, or achievement of climate-related metrics to differ materially from that described, including economic and technological viability, as well as climatic, government, consumer, and market factors outside of South Port’s control. To the fullest extent permitted by law, South Port disclaims responsibility for any loss suffered in reliance on these CRD. Nothing in this report should be interpreted as capital growth, earnings, or any other legal, financial, tax, or other advice or guidance.

Signed on behalf of South Port New Zealand Limited:

Philip Cory-Wright Nicola Greer Chair Chair, Audit and Risk Committee

16 September 2025 16 September 2025

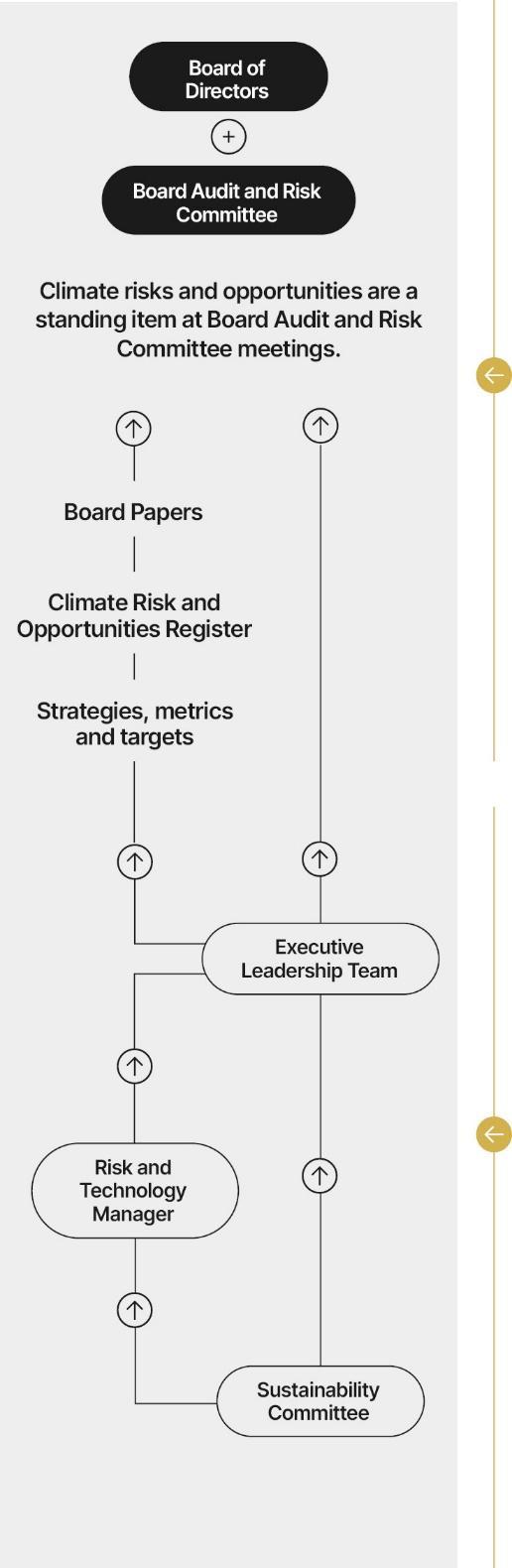

BOARD OVERSIGHT

The Board of Directors oversees how the Group identifies and handles climate-related risks and opportunities. This includes setting the risk appetite and tolerance, and approving South Port’s strategy, any future targets, and controls for responding to climate change.

The Board’s Audit and Risk Committee has delegated responsibility from the Board for oversight of the Group's response to climate-related risks. This committee meets three times a year, with climaterelated risk as a standing agenda item. The Audit and Risk Committee met three times during FY25.

The Board delegates the overall responsibility of managing risk to the Chief Executive Officer (CEO).

Directors are responsible for their own continuous education and to keep themselves up to date on relevant climate-related issues that may affect the Port. The Board itself is responsible for incorporating specific skill and knowledge requirements into management positions that ensure competency to deal with climate-related risks and opportunities. The Board requires the Executive Leadership Team (ELT) to provide all relevant information to them and to engage external experts where required knowledge is not available within the organisation.

EXECUTIVE LEADERSHIP TEAM’S (ELT) ROLE

The CEO, Chief Financial Officer (CFO), and the Infrastructure and Environmental Manager take responsibility for assessing and managing climate-related risks and opportunities at ELT level, supported by the Risk and Technology Manager. The ELT is supported in these workstreams by external parties with relevant expertise.

The ELT submits updates to the Board as appropriate, which are included in the monthly board papers. In FY25, this included consideration of South Port’s recently developed Sustainability Strategy and Energy Strategy, the results of a sea level rise and storm surge study by Great South, and South Port’s transition plan. The Board also receives updates on climate-related risk from the Audit and Risk Committee, for example, the outputs of work done in FY25 to consolidate South Port’s climate-related risks. Each climaterelated risk in South Port’s risk assessment is allocated to an ELT member, who then has particular oversight of that risk. The Sustainability Committee, comprising all ELT members, meets at least six times a year, with these meetings aligned with the ELT meetings. This is the primary mechanism by which management is informed about, makes decisions on, and monitors, climate-related risks and opportunities. Work undertaken by the Sustainability Committee is presented to the Board by the ELT for review, discussion, and approval. This includes metrics and actions for managing climate-related risks as well as opportunities such as South Port’s transition plan. The CEO and ELT evaluate any new or amended business strategy with reference to climate-related risks and opportunities, and this analysis is submitted to the Board where the potential impacts of a climate-related risk or opportunity are considered material. In the reporting period, there were at least 8 occasions where the Board received reporting from ELT on climate-related issues.

South Port’s purpose is to facilitate the best logistics solutions for the region. We achieve this through the provision of wharf infrastructure, warehousing, marine, and cargo handling activities, while developing and influencing optimal logistics solutions along the supply chain with port linkages. Owing to the long-term nature of infrastructure, the Port has generally made decisions with a long-term view. Over the last few years, we have invested in building our capabilities to understand and manage climate-related risks and opportunities and will look to integrate the insights into our future processes. Although the world has started to see the effects of climate change, South Port has not experienced any material climate-related impact to our operations in FY25.

SCENARIO ANALYSIS

In 2023-2024, we employed a Climate Change Advisor for a fixed-term and conducted a qualitative study on the effects of climate-related forces on our strategy and value chain. The scope of the analysis was focused on the Port’s immediate geographic terrain and the domestic trade structure.

This allowed an investigation of the core physical exposure, and the exposure to a shift in domestic economic structure for the timeframe of 2024-2050. This study was conducted internally as a standalone piece of work, but the results were assessed against South Port’s risk management processes to ensure a consistent approach was taken.

This process included an initial climate-related risk assessment, including scenario analysis. The assessment involved collaborative workshops with internal stakeholders, including the ELT and other relevant roles. Outcomes from the workshops included establishing the scope and boundaries of the risk assessment. This included determining value chain inclusions, time horizons, frequency of assessment, and identifying key risk areas.

The Board had the opportunity to participate in and view recordings of scenario analysis workshops undertaken. These were conducted by the Climate Change Advisor and overseen by the CFO in FY24. No external stakeholders or partners were involved in the scenario analysis process. The scenario analysis technical report highlighting the projected impacts of climate-related forces was then shared with the Board for their feedback.

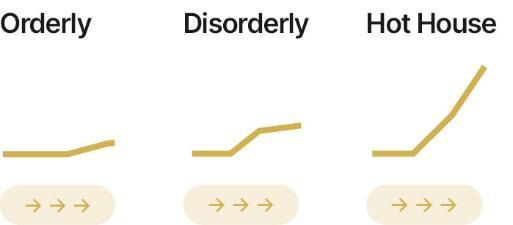

To create different scenarios for the Port, we followed a series of steps based on 15 factors that affect the Port's operations and environment. These factors include social, technological, legal, political, economic, and environmental aspects. We used these factors to create narratives that showed how the Port could be affected by different situations in the future. We looked at the whole system that the Port is part of, not just one part of it. South Port opted for three scenarios as per the overview in the table opposite. The 'Orderly' (Net Zero 2050) scenario has an emphasis on transition risks which we are specifically exposed to through the clients using our Port. Conversely, the 'Hot house' (Current Policy) scenario focuses on physical risks that affect us significantly as we are a key part of the region's infrastructure with assets that inherently have a long lifespan. The 'Disorderly' (Delayed Transition) scenario is the third climate-related scenario and shows a mix of both transition and physical risk.

The adopted scenarios were preferred for two reasons: First, the scenarios expose South Port’s business model to maximum plausible physical/transitional risks and thus explore South Port’s strategic resilience to both abrupt and systemic manifestations of climate-related forces. Such an experimental exposure provides an optimal tool to stress-test South Port’s business and processes.

Secondly, the scenarios maximise intra-sectoral alignment and comparability within the sector, as the generated scenario narratives closely align with the transport sector-specific scenarios developed by the consultancy firm KPMG, in partnership with the Aotearoa Circle, in direct collaboration with primary sectoral stakeholders. As a result, South Port’s generated scenarios are not only specifically tailored for maximum and targeted applicability to South Port’s business model, but are also aligned with the transport sector scenarios.

The scenarios adopted and risk assessment covered all of South Port’s operations.

In FY25 South Port conducted a review of its scenarios to confirm their application. No changes were made to the scenarios as described below.

CLIMATE-RELATED RISKS AND OPPORTUNITIES TIME HORIZONS

SHORT TERM Now – 2030

MEDIUM TERM 2031 – 2040

LONG TERM 2041- 2050

Aligns with the remaining useful life of some critical assets. Additionally, it is indicative of the New Zealand Government’s level of decarbonisation ambition.

Aligns with the lifecycle of our assets and corresponds with the timeframe when dynamics of a dominant scenario will be materially entrenched.

Long-term horizon out to 2050 aligns with international emission reduction targets (Paris Agreement, 2050). It represents the last stage of total institutionalisation of preceding legislative/economic/policy dynamics.

These timelines are linked to our strategic planning horizons for capital expenditure. Small land-basedmobile plant and equipment are aligned with short-to-medium timeframes whereas larger landbased, andfloatingplantarefocusedonthemedium-to-longer term. Our asset management plan and property masterplan are key documents that align with both the medium - and longer-term horizons.

The timehorizons setoutforscenario analysisarealsoaligned to the time horizons used for the risk identification.

ORDERLY (NET ZERO 2050)

This scenario depicts a rapid and ambitious transition to a low-carbon future, driven by strong societal demand for climate action and international cooperation on climate policy. The pathway to Net Zero 2050 involves an initial burst of activity to decarbonise society and the economy, followed by sustained efforts to maintain low emissions across all sectors. Renewable energy sources, energy efficiency, and afforestation are key enablers of this transition.

Domestic freight is assumed to shift increasingly towards coastal shipping and rail, which directly affects our business. The global shipping industry leans heavily towards using synthetic fuels, such as green ammonia, which are produced from renewable electricity. These fuels have the potential to offer a cleaner and cheaper alternative to fossil fuels and could reduce the dependence on oil imports. The structure of cargo flowing through South Port is altered, with lower agricultural output from Southland due to land use changes and reduced import of petrol-based products.

DISORDERLY (DELAYED TRANSITION*)

Business as usual is assumed to persist until the effects of climate change and the social responses become unavoidable. A series of severe climate disasters in major economies triggers a sudden and radical shift to a lowcarbon world. Many businesses that are not resilient or strategically exposed to climate risks collapse under financial and legal pressure. After the shock, the economy gradually recovers in the new paradigm.

The freight sector is constrained by a lack of modal diversity and high operational costs due to expensive alternative fuels. The production of primary industries based on conventional agriculture and forestry is drastically reduced. The Port faces a dramatic change in cargo volumes.

HOT HOUSE (CURRENT POLICY*)

The world continues to rely heavily on fossil fuels and greenhouse gas emissions keep rising. The global average temperature increases with severe consequences for the climate system and human society.

Domestically, the mixture of internal economic pressures and international inaction ensures that climate mitigation policy is not pursued. Occasional severe climate events are more potent and support the drive toward climate adaptation measures. While the change in weather patterns reduces the output of the agricultural sector in some geographies, Southland’s primary industries are not critically impacted.

Together with a stable domestic economic structure, cargo volumes increase at the Port.

* South Port’s Disorderly and Hot House scenarios did not expressly include carbon sequestration from afforestation or nature-based solutions, as anticipated by NZ CS 3, paragraph 51(a)(iii)

SCENARIO OVERVIEW

NGFS Current Policy PolicyReaction

In FY25, South Port is not aware of any current material climate-related physical or transition impacts, including financial impacts. The material climate-related risks and opportunities identified in South Port’s scenario analysis process to date, together with anticipated impacts, are listed in the table below. Funding decisions relating to South Port’s transition initiatives below have to date been made as part of business as usual funding decision making processes, with climate-related risks and opportunities considered as part of capital deployment.

Climate-Related Risks and Opportunities

(Anticipated Time Horizon)

Physical Risk

Increased sea level rise and rainfall results in disruption to on-land freight routes (roads, bridges, railways) that connect the Port to Southland.

Medium/Long-term

Sea level rise, storm and tide surges impacting operations and damaging ships, infrastructure and equipment.

Medium/Long-term

An increase in the number of high-wind days, that disrupt land-based and marine activities.

Medium/Long-term

Transition Risk

Increasing cost of carbon associated with fossil fuel taxes.

Medium/Long-term

Increased insurance premiums, larger excesses, and reduced scope of coverage.

Medium/Long-term

Industrial and commercial demand for diesel decreases in Southland and regional wood producers in Southland and Otago divert wood exports for local consumption as biomass for process heat.

Medium/Long-term

Increasing costs of commercial farming of ruminants drives down regional production of meat and dairy. Demand for fossil fuels and farming inputs (like fertiliser and stock food) decreases. Decrease in yields across regional forestry and agriculture as a result of climate-related impacts.

Medium/Long-term

Investing in low-carbon technology reduces the cost of accessing low carbon fuel infrastructure, while a lack of investment increases it. An early transition to low-carbon assets may lead to net losses if decarbonisation scenarios do not occur, but maintaining legacy fossil fuel infrastructure becomes costly if they do.

Medium/Long-term

Persistent decarbonisation scenarios and perceived lack of action in mitigation planning could heighten the risk of legal challenges from both public and private entities

Medium/Long-term

A delay in transitioning and increased demand for low carbon machinery, impacts on supply and drives increased costs.

Medium/Long-term

Transition Opportunity

National policy settings and government investment drive an increase in coastal shipping’s share of domestic freight movement.

Medium-term

Large-scale infrastructure climate resilience projects and large-scale rebuilds from climate-induced extreme weather events drive a significant increase in building and construction material imports.

Medium-term

Anticipated

Increase the periods, receive cargo, transit routes

Increase and imports region.

Anticipated Impact

in the number of times, and the length of periods, in which South Port cannot offload or cargo, operational inputs or staff due to routes being unavailable.

Anticipated Financial Impact (Qualitative)

type of cargo and cargo volumes with lower of diesel and agricultural inputs and lower of meat, dairy products and timber products

capital allocation to invest in end-of-trip infrastructure for alternative fuelling, like hydrogen, bioenergy, or diesel-electric hybrid.

Reduced revenues as port operations are disrupted.

Significant costs of repairs and operational downtime.

Transition plan aspects of South Port’s strategy to respond to Climate-Related Risks and Opportunities

South Port intends to integrate GHG emissions consideration in significant capital investment decisions where relevant, alongside technical and economic considerations. No significant decisions were taken in FY25 to change to lower carbon emissions equipment.

in coastal shipping, exports from aquaculture imports due to higher economic activity in the

Increased insurance costs and potential stranded assets.

Reduced revenues due to fewer port calls. Increased capital expenditure to transition to low carbon equipment.

Higher revenue from increasing number of port calls.

Intention to adopt strategies to build resilience into the supply chain, including in FY25 engaging a third party to undertake a study on the potential impact of sea level rise and storm surge on South Port assets.

South Port intends to work with customers and other external parties to determine future infrastructure requirements to take advantage of increased cargo throughput.

This table summarises South Port’s approach to climate-related risk management, which is integrated into the Group’s overall risk management processes.

Identify high-level risk hotspots and drivers along value chain

For all potential risks, we identify where, when, why, and how, the potential risk could prevent the achievement of strategies, plans, and objectives.

We allocate the risk to one of the nine risk categories identified in the Group’s Risk Management Framework, which allows us to identify risk hotspots including fuel technologies, predicted weather patterns, emerging or contracting markets, or new regulation.

Internal and external stakeholders are consulted where relevant to ensure wider context is understood and all risks are identified.

Carry out initial screening of potential risks

Potential risks, (including climate risk where material), are submitted to South Port's (Material) Risk Register and then evaluated as to the type of risk and its driver; how the risk may present itself in South Port’s context; the potential financial impact; the likelihood of impact and the expected time horizon; and any assumptions or sources of information used in the assessment.

Risks that are rated as 'low' do not require any further action except to record and monitor. For inherent risks rated other than low, controls are put in place to address the risk. Controls are categorised as either preventative, detective or corrective controls.

The Group’s risk matrix includes climate as an additional risk category. This category includes assessment criteria relating to the potential impact a climate-related scenario would have on our assets, and the timeframe of impacts materialising. The assessment assists us to proportionately assess climate-related risks against the Port’s other material risks.

Carry out formal assessment to determine risk

Screened risks are rated on a scale from Low to Extreme.

Depending on the context, the evaluation may require engagement with specialised external experts, predictive modelling, engagement with stakeholders in the value chain linked to the hazard, etc. This is a judgement call for the ELT in conjunction with the Board. All climate-related risks are assessed using the Group's Risk Management Framework, with the top risks being included in the Material Risk Register for consideration by the Audit and Risk Committee.

This risk assessment aligns to the current business risk framework at South Port. The ELT complete inherent risk assessments for all risks identified, rating the likelihood and impact of the various risks. Additionally, each climate-related risk is allocated to a member of the ELT for particular oversight. Key controls and mitigation processes are then noted, resulting in a residual risk score. The Material Risk Register is then reviewed and approved by the Board.

Identifypotential adaptation measures

Risk treatments are identified to mitigate the risk to a tolerable level. Internal and external stakeholders are consulted where relevant.

Carry out financial analysis

Develop, implementation and review plan

All major capex spend requires financial analysis to be completed prior to approval. South Port uses a weighted average cost of capital (WACC) model to ensure that capital deployment meets internal hurdles before proceeding with new projects. Physical climate risk is integrated into funding-decision making through evaluation at the design phase of infrastructure development, including consideration of the carbon footprint of new assets, and resilience to extreme weather events and sea level rise Currently South Port does not apply an internal carbon price in this process or track capital deployment specifically to address climate risks.

Future capital deployment decisions are expected to include climate-risk relating to adaptation (e.g. preparedness for extreme weather events), and also mitigation (e.g. considering carbon emissions linked to purchasing new equipment).

Further treatment actions are determined in order to mitigate the risk. Actions are documented to enable monitoring. Business unit managers are appointed to identify, implement and monitor controls and their effectiveness in mitigating risks. The Audit and Risk Committee has overall responsibility to ensure that risk management strategies and policies are implemented and managed appropriately, including supporting the annual review of risks and management approaches.

Monitoring of climate-related risks is undertaken at least annually to refresh our climate-related risk assessment and ensure the risk remains within tolerable levels and the controls and treatments remain effective.

During the review, the effectiveness of the controls is assessed and depending on the operating effectiveness rating, the control assessment frequency is set.

ORGANISATIONAL BOUNDARIES

South Port applies an operational control approach to consolidate GHG emissions. That means South Port accounts for 100% of the GHG emissions from operations over which it has the full authority to introduce and implement operating policies. South Port has not excluded any facilities, operations or assets from its GHG inventory

During FY25, South Port only had one subsidiary, Awarua Holdings Ltd, which was 100% owned by the Port. Awarua Holdings Ltd was amalgamated into South Port on 18 June 2025. Prior to that amalgamation, there were no GHG emissions associated with Awarua Holdings that were not captured directly by the Port's activities.

GHG EMISSIONS INVENTORY

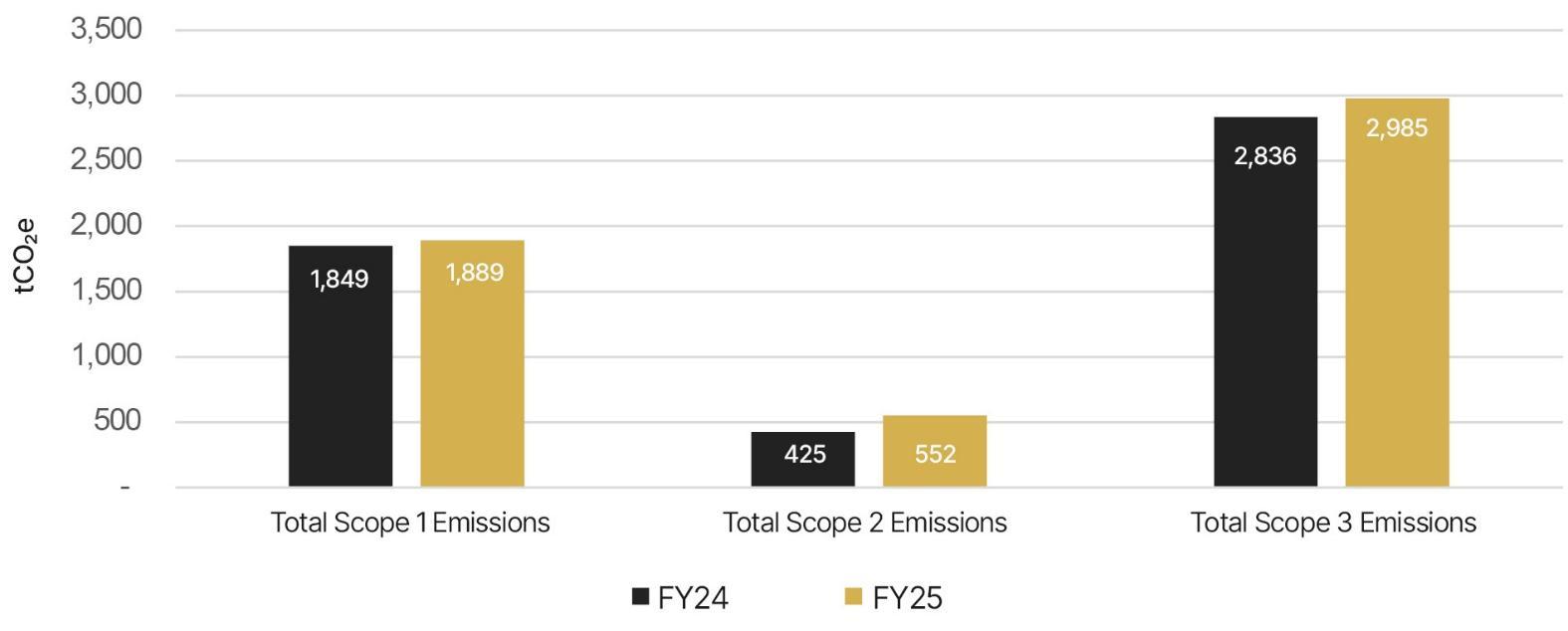

South Port began measuring its GHG emissions in 2019, focusing mainly on Scope 1 and 2 emissions. Over time, we have improved the methodology for collecting and calculating Scope 3 emissions to cover our value chain. In this context, the FY24 inventory (July 2023 to June 2024) included new categories that reflected the completeness of emissions that can be attributed to the organisation's operations within the declared boundary. Accordingly, South Port has designated FY24 as its GHG emissions base year.

The inventory has been measured in accordance with the Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard (Revised Edition) (the ‘GHG Protocol’), the Greenhouse Gas Protocol: Corporate Value Chain (Scope 3) Accounting and Reporting Standard, with guidance provided by the Greenhouse Gas Protocol: Technical Guidance for Calculating Scope 3 Emissions (version 1.0) (Technical Guidance).

The emission factors (EFs) applied for the calculations are derived from "Measuring emissions guide: 2025" (MfE 2025), apart from those Scope 3 categories not addressed by the MfE. These categories are derived from the United States Environmentally-Extended Input-Output model by the US EPA (calculations via GZA Scope 3 Calculator workbook), which was applied to calculate emissions based on expenses (mainly Categories 1 and 2), and the "Greenhouse gas reporting: conversion factors 2025" from the United Kingdom's Department for Energy Security and Net Zero, for Well-to-Tank (WTT) and recycling factors. GWP rates are drawn from the International Panel on Climate Change’s (IPCC) Fifth Assessment Report (AR5)

A limited level of assurance has been undertaken by Deloitte Limited on behalf of the AuditorGeneral over selected GHG disclosures included in this CRD The assurance was limited to Scope 1 and 2 emissions. Refer to Deloitte's Independent Limited Assurance Report from page 14

Scope 3 Categories Not Applicable

To ensure the consistency of the approach adopted (Operational Boundary), South Port has not reported on the following sources of Scope 3 emissions:

• Category 8 Upstream leased assets: South Port did not lease any assets in FY25

• Category 9 Downstream transportation and distribution: South Port did not sell any products in FY25

• Category 10 Processing of sold products: South Port did not sell any products in FY25

• Category 12 End-of-life treatment of sold products: South Port did not sell any products in FY25

• Category 14 Franchises: South Port does not have franchises.

• Category 15 Investments: South Port did not make any investments or provide financial services in FY25

Scope 3 Categories Exclusions

• Category 11 Use of sold products:

Visiting vessels – fuel: Reliable data not available

Visiting trucks and rail- fuel and fugitive emissions at the port: Low size, reliable data not available

SOURCE INCLUSIONS, METHODOLOGY AND UNCERTAINTY

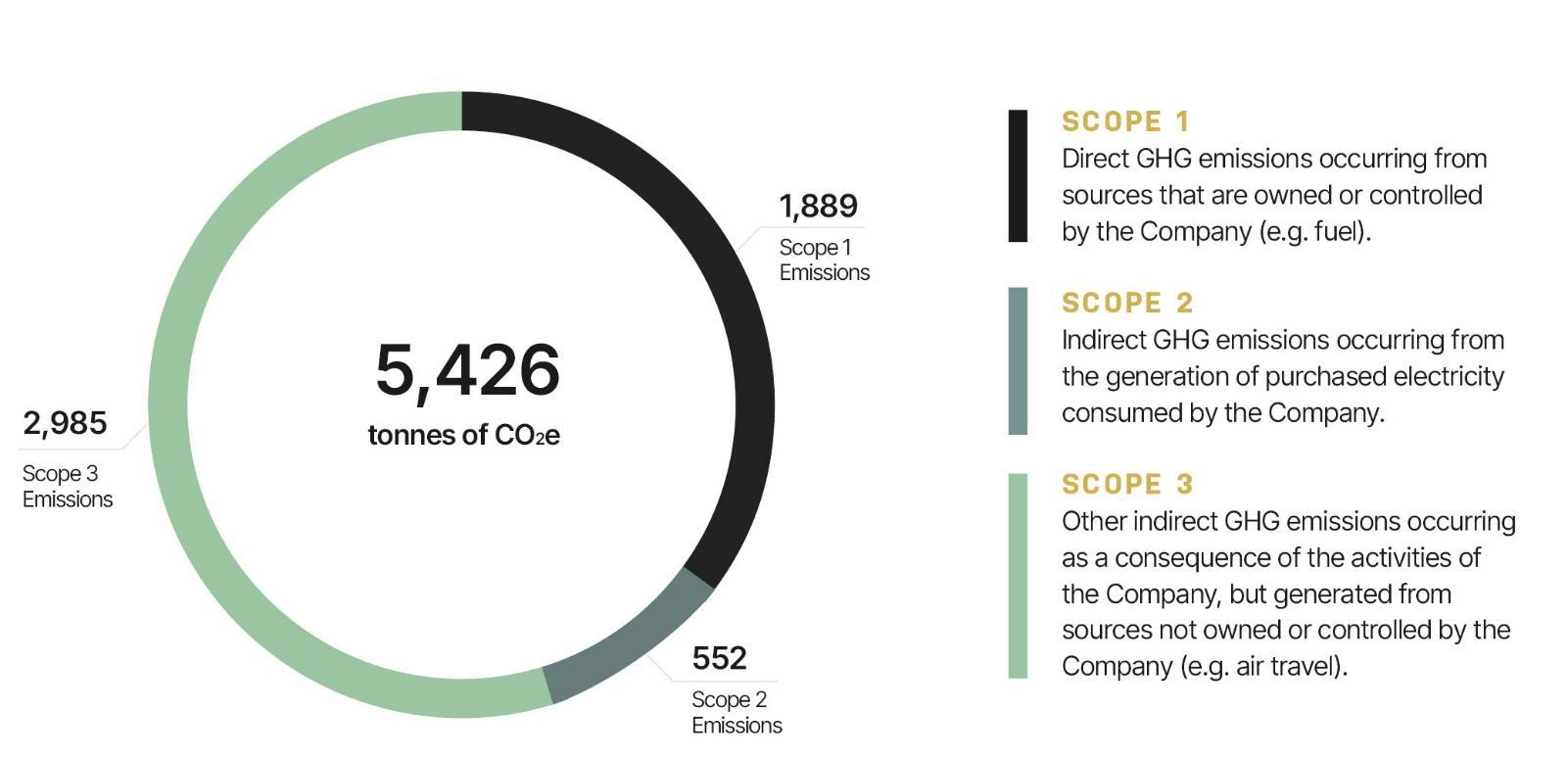

South Port includes Scope 1,2 and selected Scope 3 emissions from all relevant Kyoto Protocol gases in our inventory, expressed as carbon dioxide equivalent (CO2e). The emissions sources in the table below have been included in the GHG inventory. No material emissions sources have been excluded.

Emissions sources

records are considered reasonably reflective of the types of quantities of products and services purchased, though not all accounting codes are used accurately or consistently. Very high level of

Category 3: Fueland EnergyRelated Activities not included in Scope 1 or Scope 2 Electricity transmission and distribution losses

Category 3: Fueland EnergyRelated Activities not included in Scope 1 or Scope

For upstream emissions of purchased fuels (Well to Tank emissions)

Category 4: Upstream transportation and distribution Upstream emissions from transportation of purchased goods and services

Supplier invoices and Internal Report

commodity types. CAPEX records are assumed to be reasonably accurate. Very high level of uncertainty

Average-data method. Grid average emissions assumed. Supplier invoices are considered accurate. Low level of

conversion factors are for use by UK and international organisations to report on greenhouse gas emissions. Very high level of uncertainty

method. The EEIO model is developed from U.S. commodity and industry data with limited representation to local cradle-to-gate emissions. Significant assumptions are made as to the resemblance of accounting codes to EEIO commodity types. OPEX records are considered reasonably reflective of the types of quantities of products and services purchased, though not all accounting codes are used accurately or consistently. Very high level of

Where

Supplier invoices are considered accurate. High level of

method. The EEIO model is

from U.S. commodity and industry data with limited representation to local cradle-to-gate emissions. Significant assumptions are made as to the resemblance of accounting codes to EEIO commodity types. OPEX records are considered reasonably reflective of the types of quantities of products and services purchased, though not all accounting codes are used accurately or consistently. Medium level of uncertainty

method.

Note: South Port restated its FY24 GHG emission inventory in FY25 following advice in relation to the treatment of metered electricity consumption which impacted Scope 2 and Scope 3 (Category 3) totals This did not have a material effect on Scope 2 or Scope 3 totals.

CLIMATE-RELATED METRICS

South Port does not currently have GHG emissions reduction targets. We also have not to date used any industry-specific indicators to track climate-related risks and opportunities. However, we may refine our approach in future, pending the outcomes of the New Zealand Port sector’s ongoing work drafting sector guidance for future use.

In FY24, South Port estimated that up to 100% of its assets and business activities were vulnerable to climate-related transition risk. This assessment remains the same in FY25 for transition risk. In relation to physical risk, South Port completed a Sea Level Rise and Extreme Sea Level Exposure study relating to South Port owned assets during FY25 In light of this study, South Port has updated its working assessment, and currently estimates that under a hot house scenario, up to 13.8% of our assets and business activities are vulnerable to climate-related physical risk. It should be noted that this will only occur when there is a combination of coincidental events which can vary depending on the storm’s intensity. Although possible, such a combination is statistically infrequent and would be expected to be of relatively short durations (2 to 3hrs) given our port is sheltered by Bluff Hill Below is a summary of vulnerability under two physical scenarios analysed:

Scenario 2 % of South Port’s assets vulnerable to sea level rise and extreme sea level exposure

SSP2-2.6 (2050) <1%

SSP2-7.0 (2100) 12.5%

Scenario 3

SSP3-2.6 (2050) <1%

SSP3-7.0 (2100) 13.8%

Assets Impacted

Ferry wharf, syncrolift land, pilot wharf

Ferry wharf, syncrolift land, pilot wharf, town wharf, fishing pier A

Ferry wharf, syncrolift land, pilot wharf

Ferry wharf, syncrolift land, pilot wharf, town wharf, fishing pier A, B & C, oyster wharf, berth 8, woodchip storage area

Climate change may also present opportunities. South Port has not yet quantified any anticipated impacts of these opportunities.

No assets or business activities were specifically aligned with climate-related opportunities during FY24 or FY25.

In relation to capital deployment, management considers climate risks and opportunities when undertaking capex projects, for example, the impact of sea level rise when preparing drainage designs at the Port. However, there was no capex spend undertaken in FY24 or FY25 that related specifically to the climate-related risks and opportunities identified as part of the scenario analysis.

To date, South Port has not adopted an internal carbon emissions price.

No management remuneration was linked to climate-related risks and opportunities in FY24 or FY25

South Port adopted procedures using external advice for assessing the methodologies and assumptions in South Port’s carbon inventory collation processes. These procedures were followed in FY25

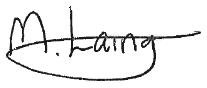

GHG EMISSIONS FROM FY24 BASELINE

CARBON INTENSITY FOR SCOPE 1 AND SCOPE 2

INDEPENDENT LIMITED ASSURANCE REPORT

TO THE SHAREHOLDERS OF SOUTH PORT NEW ZEALAND LIMITED

GHG EMISSIONS DISCLOSED IN ITS GROUP CLIMATE STATEMENTS (ALSO REFERRED TO AS ‘CLIMATE-RELATED DISCLOSURES’) FOR THE YEAR ENDED 30 JUNE 2025

Under section 461ZH(3) of the Financial Markets Conduct Act 2013, the Auditor-General is the assurance practitioner of South Port New Zealand Limited (the Group). The Auditor-General has appointed me, Matt Laing, using the staff and resources of Deloitte Limited, to carry out a limited assurance engagement, on his behalf, on the Scope 1 and 2 greenhouse gas (GHG) emissions information disclosed in the Climate Statements (GHG disclosures), for the year ended 30 June 2025.

Scope of the engagement

The GHG disclosures below are within the scope of our limited assurance engagement:

• The gross emissions, in metric tonnes of carbon dioxide equivalent, classified as Scope 1 and Scope 2 (calculated using the location-based method), on page 10

• The statement describing that GHG emissions have been measured in accordance with GHG Protocol Corporate Accounting and Reporting Standard on page 9

• The approach used to consolidate GHG emissions (operational control) on page 9

• The sources (or references to sources, where applicable) of emission factors and the global warming potential rates used, on page 9

• The summary of specific exclusions of Scope 1 and Scope 2 (calculated using the location-based method), emissions sources, including facilities, operations or assets with a justification for their exclusion, on page 10

• The description of the methods and assumptions used (including the rationale for doing so, where applicable) to calculate or estimate Scope 1 and Scope 2 (calculated using the location-based method) GHG emissions, and the limitations of those methods, on page 10

• The description of any uncertainties relevant to the Group’s quantification of its Scope 1 and Scope 2 (calculated using the location-based method) GHG emissions, including the effects of these uncertainties on GHG disclosures, on pages 10

South Port New Zealand Limited’s Climate Statement contains disclosure of greenhouse gas emissions from a selected subset of emissions sources classified as Scope 3. The Group has elected not to use adoption provisions 4 and 5 of NZ CS 2 Adoption of Aotearoa New Zealand Climate Standards (‘NZ CS 2’) for reporting purposes, however, has used adoption provision 8 of NZ CS 2, which allows for the exclusion of these disclosures from the scope of this assurance engagement.

Conclusion

Based on the procedures we have performed and the evidence we have obtained, nothing has come to our attention that causes us to believe that the South Port New Zealand Limited’s GHG disclosures within the scope of our limited assurance engagement for the year ended 30 June 2025, are not fairly presented and prepared, in all material respects, in accordance with Aotearoa New Zealand Climate Standards, issued by the External Reporting Board.

Other matter – Comparative Information

The comparative information, being the 2024 GHG disclosures on page 13, has not been subject to assurance. As such, it is not covered by our assurance conclusion.

The Board of Directors’ responsibilities

Subparts 2 to 4 of the Financial Markets Conduct Act 2013 set out requirements for a climate reporting entity in preparing Climate Statements, which includes proper record keeping, compliance with the climate-related disclosure framework and subjecting it to assurance.

The Aotearoa New Zealand Climate Standards have been issued by the External Reporting Board as the framework that applies for preparing and presenting Climate Statements. The Board of Directors of the Group is therefore responsible for preparing and fairly presenting Climate Statements for the year ended 30 June 2025, in accordance with those standards.

The Board of Directors is also responsible for the design, implementation, and maintenance of internal control relevant to preparing the Climate Statements that are free from material misstatement, whether due to fraud or error.

Our responsibilities

Section 461ZH of the Financial Markets Conduct Act 2013, requires the GHG disclosures included in the Group’s Climate Statements to be the subject of an assurance engagement.

NZ CS1 Climate-related disclosures, paragraph 25 requires such an assurance engagement at a minimum to be a limited assurance engagement, and paragraph 26 specifies the scope of the assurance engagement on GHG disclosures.

To meet this responsibility, we planned and performed procedures (as summarised below), to provide limited assurance in accordance with New Zealand Standard on Assurance Engagements 1 Assurance Engagements over Greenhouse Gas Emissions Disclosures (‘NZ SAE 1’) and International Standard on Assurance Engagements (NZ) 3410 Assurance Engagements on Greenhouse Gas Statements (‘ISAE (NZ) 3410’), issued by the New Zealand Auditing and Assurance Standards Board.

Summary of Work Performed

The procedures we performed were based on our professional judgement and included enquiries, observation of processes performed, inspection of documents, analytical procedures, evaluating the appropriateness of quantification methods and reporting policies, and agreeing or reconciling with underlying records. In undertaking our limited assurance engagement on the Group’s Scope 3 GHG disclosures, we:

• We obtained, through enquiries, an understanding of the Group’s control environment, processes and information systems relevant to the preparation of the Scope 1 and Scope 2 disclosures. We did not evaluate the design of particular control activities or obtain evidence about their implementation.

• We evaluated whether the Group’s methods for developing estimates are appropriate and had been consistently applied. Our procedures did not include testing the data on which the estimates are based or separately developing our own estimates against which to evaluate the Group’s estimates.

• We performed analytical procedures on particular emission categories by comparing the expected GHG emissions to recorded GHG emissions and made inquiries of management to obtain explanations for any significant differences we identified.

• We evaluated the appropriateness of the emission factors applied.

• We evaluated the overall presentation and disclosure of the Scope 1 and Scope 2 disclosures.

The procedures performed in a limited assurance engagement vary in nature and timing from, and are less in extent than for, a reasonable assurance engagement. Consequently, the level of assurance obtained in a limited assurance engagement is substantially lower than the assurance that would have been obtained had a reasonable assurance engagement been performed.

We believe that the evidence obtained is sufficient and appropriate to provide a basis for our limited assurance conclusion.

Inherent limitations

As outlined on page 2, GHG quantification is subject to inherent uncertainty because of incomplete scientific knowledge used to determine emissions factors and the values needed to combine emissions of different gases.

Other information

The Climate Statements contains information other than the GHG disclosures and the assurance report thereon. The Board of Directors is responsible for the other information.

Our assurance engagement does not extend to any other information included, or referred to, in the Climate Statements on pages 1 to 8 and 11 to 13, and therefore, no conclusion is expressed thereon, apart from our opinion on the financial statements. We read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the GHG disclosures, or our knowledge obtained in the assurance engagement, or otherwise appears to be materially misstated.

Where such an inconsistency or misstatement is identified, we are required to discuss it with the Board of Directors and take appropriate action under the circumstances, to resolve the matter. There are no inconsistencies or misstatements to report.

Independence and quality management

We complied with the Auditor-General’s independence and other ethical requirements, which incorporate the requirements of Professional and Ethical Standard 1 International Code of Ethics for Assurance Practitioners (including International Independence Standards) (New Zealand) (PES 1) issued by the New Zealand Auditing and Assurance Standards Board. PES 1 is founded on the fundamental principles of integrity, objectivity, professional competence and due care, confidentiality and professional behaviour. These principles for example, do not permit us to be involved in the preparation of the current year’s GHG information as doing so would compromise our independence.

We have also complied with the Auditor-General’s quality management requirements, which incorporate the requirements of Professional and Ethical Standard 3 Quality Management for Firms that Perform Audits or Reviews of Financial Statements, or Other Assurance or Related Services Engagements (PES 3) and Professional and Ethical Standard 4 Engagement Quality Reviews issued by the New Zealand Auditing and Assurance Standards Board (PES 4). PES 3 requires our firm to design, implement and operate a system of quality management including policies or procedures regarding compliance with ethical requirements, professional standards and applicable legal and regulatory requirements. PES 4 deals with an engagement quality reviewer’s appointment, eligibility, and responsibilities.

Other than our work in carrying out all legally required assurance engagements, including being the statutory auditor of the financial statements (on behalf of the Auditor-General), we have no relationship with or interests in the Group.

Matt Laing Partner for Deloitte Limited

On behalf of the Auditor-General Hamilton, New Zealand

16 September 2025