MAGNUM’S MELTDOWN

Can Unilever’s ice cream spin-off recover from a bad start?

Why it’s important not to panic despite Middle East uncertainty

03

Not panicking, sticking to the plan and thinking about opportunities

05 INCOME INVESTING

Are you focusing on the wrong number when picking an income fund?

08 MONTH AHEAD

Nike braced for earnings as tariffs weigh on turnaround hopes

10 ASK RACHEL

Should I defer my retirement or not?

12 SECTOR REPORT

Data disrupted: How AI is hitting everything from comparison sites to software and analytics firms

16 UNDER THE BONNET

Magnum’s meltdown: can Unilever’s ice cream spin-off recover from a bad start?

19 RETIREMENT IN FOCUS

Last orders for pension top-ups? Boosting contributions before and after retirement

22 FUNDS

Why investment trusts are buying themselves more than ever

25 DEEP DIVE

Why active versus passive investing isn’t so black and white anymore

28 ASK PAUL

How do I go about picking an active fund manager?

31 UNDER THE BONNET

How Games Workshop became the best performing UK share of the last two decades

34 ASK RUSS

Does the volatility in gold signal the end of the bull market?

36 MY PORTFOLIO

How I invest: From trying to cover train fares to being a student of Buffett

39 ASK LAURA

Should I pay off my student loan or invest instead?

Shares magazine is published by AJ Bell, authorised and regulated by the Financial Conduct Authority. It’s here to inform, not to give personal advice. Please don’t base your investment decisions on it alone. If you’re unsure, speak to an independent adviser. And remember: past performance isn’t a guide to the future. Tax benefits depend on your circumstances and tax rules may change.

Not panicking, sticking to the plan and thinking about opportunities

Don’t panic. Stick to your plan. These are words to live by when markets get choppy as they have done since the beginning of March as simmering tensions in the Middle East escalated to armed conflict.

There is absolutely no reason to lose faith in investing. It is important to remain optimistic and focus on the long-term potential for your money to grow by owning investments.

Getting over the discomfort

There’s no doubt that it can feel uncomfortable investing in the current circumstances but it is important to understand that share prices should move up and down. Going up in a straight line is not normal.

Time and time again the stock market will go

through a wobbly patch and you’ll get days of big share price movements. By staying invested you are ready to play market recoveries which often happen faster than you might think.

The recent correction will have put a dent in most people’s portfolios and no-one knows exactly how things will pan out over the next few days and weeks. However, over the longer term, the financial markets have proven to be a reliable way of creating and augmenting wealth.

A retreat to cash could be costly, particularly if inflation increases from here to erode the value of money stashed in the bank.

One thing to start thinking about, for those with the appetite and funds available, is potential opportunities which have been created by the

Strikes launched against Iran 'Liberation Day' tariffs announced

Lehman Brothers Collapse

Covid sell-off begins

Source: LSEG

market volatility. Often in a downturn selling can be indiscriminate which means good companies (and funds and investment trusts) get sold off alongside the bad.

That said, you should think very carefully about any risks to each stock or fund and if you’re not ready to take action yet you could instead draw up a shopping list of potential opportunities and the levels you might want to buy in at. Alternatively, you can drip feed money in rather than putting everything in at once. You may already have regular investment set up and if you do, it is worth sticking with when markets are bumpy. By investing a set amount every month, you benefit from an effect called pound cost averaging – you buy more with your money when markets are low and less when markets are high. You are not trying to time the market perfectly, a skill few can master, and you’re maintaining a healthy investing habit.

How does the sell-off compare?

The current sell-off is sizeable but worth keeping in perspective for now. Since markets closed on Friday 27 February before the US-Israeli strikes on Iran were launched, the FTSE 100 is down 4.6% (as of 10 March) having traded down as a much as 7.5% at the low point.

The big white whale of market corrections is the one that accompanied the global financial crisis. Between October 2007 and March 2009, when equities bottomed out, the FTSE fell more than 45% and the US S&P 500 index more than halved.

During the Covid pandemic markets fell very sharply in a short space of time, from late February to mid-March the FTSE 100 was down nearly 30%.

More recently still, the Liberation Day tariffs announced on 2 April by the Trump administration caused the FTSE 100 to fall more than 10% in the space of a week.

WHY TIME IN THE MARKET BEATS TIMING THE MARKET

The chart below based on research from BlackRock shows how a hypothetical $100,000 investment in stocks would have been affected by missing the market’s top-performing days over the two decades from 1 January 2006 to 31 December 2025.

Someone who remained invested for the entire period would have accumulated $806,201, while an investor who missed just five of the topperforming days during that period would have accumulated only $497,945. Often the best days for the market follow the worst.

How staying invested can make a dramatic difference

Hypothetical investment of $100,000 in the S&P 500 Index over the last 20 years (2006-2025)

$500,000

Source: BlackRock, Bloomberg

Are you focusing on the wrong number when picking an income fund?

Investors searching for income opportunities often gravitate towards funds with the highest yields. If you had the choice of either 4p or 8p in every pound in dividends, you might choose the bigger reward. What people often neglect to consider is the importance of looking at total return. This is the money you make from dividends and the increase in the value of your fund, known as capital growth. Occasionally, you may find a type of fund that has a lower yield, but which subsequently generates similar, or better, total returns compared to a higher yielding fund. A case in point across certain periods is the global equity investment trust sector, which is a group of trusts investing in dividend-paying companies from around the world.

The average yield on the global equity income investment trust sector is currently 3.5%, less than the 4% average yield on the UK equity income sector. An income hunter might therefore presume that the UK equity income space is preferrable if they are collecting bigger dividends than the comparative global peer group. However, that might not always be the case.

Running the numbers

AJ Bell compared the average total return from both sectors over the past five years and found roughly equivalent results. You would have made 71% total return from the growth in value of either category of trust as well as dividends, on average. In comparison, UK equity income trusts averaged a 67% total return.

Over a longer period, the global equity income trusts did considerably better, with an average 253% total return over 10 years versus 149% from UK equity income trusts. There is no guarantee this

trend will remain intact, but these figures illustrate how you cannot simply judge an investment’s overall potential simply from the headline dividend yield.

In the above example, share price (aka capital) gains contributed more than dividends for the total return on global equity income trusts, on average, over the past five and 10 years. That might be down to global equity income trusts being more invested in low-yielding technology stocks versus UK equity income ones.

When times are good, it is fair to expect faster earnings growth from software and hardware companies compared to the typical company you might find on the UK stock market. There is often a correlation between the pace of earnings growth and share price growth.

‘We’re happy to invest in areas like technology, even if they have very low, or frankly, even in some cases, no dividend,’ says Stephen Anness, manager of the Invesco Global Equity Income Trust, the best performer in its category over five years. What matters to Anness is an attractive valuation at the point of investment compared what his team believe the company should be worth.

UK equity income investment trusts

Excludes trusts with net assets of less than £250m

Source: FE Analytics. Yield data, source: AIC. Performance data to 12 Feb 2026

Global equity income investment trusts

Excludes trusts with net assets of less than £250m

Source: FE Analytics. Yield data, source: AIC. Performance data to 12 Feb 2026

In the UK equity income space, Temple Bar also places a significant emphasis on valuation when looking for opportunities. It is the top performing investment trust in the UK equity income sector, returning 148% over five years. Temple Bar’s top holdings include a mixture of high and low-yielding stocks such as ITV which yields 6.1% and Marks & Spencer which yields 1.7%.

What is your income strategy?

If the primary reason for owning income investments is to collect a regular stream of cash, you might be happy if the bulk of returns come from dividends.

In this case, you might still prefer a fund that specifically targets high-yield investments. Certain people might see any capital growth as the cherry on top, but not essential.

If the income stream from your chosen investments is inadequate, one alternative is to sell small chunks of your fund over time to generate additional income on top of any dividends. That does not suit everyone as there are costs involved in

selling funds.

For certain investors, having a blend of income and growth works fine. They collect a regular stream of dividends and hopefully the value of their capital keeps growing. This is particularly important for someone in retirement who wants their pot to last as long as they do. It is also important if you want to keep up with the cost of living, i.e. inflation.

It is worth pointing out income funds might appeal to younger investors as well as those in retirement. Certain income funds contain established, highly profitable companies that have the qualities to fight off competition, protect their market share, and grow their earnings – all attractive attributes from an investment perspective. For those who do not need the regular stream of cash from dividends, reinvesting the proceeds is a powerful way to turbocharge your ISA or pension.

By Dan Coatsworth Head of Markets

Nike braced for earnings as tariffs weigh on turnaround hopes

Ahead of its latest earnings Nike is racing to reverse a two-thirds collapse in its market value over the last four-and-a-bit years.

CEO Elliot Hill is pivoting from a struggling direct-to-consumer model back to the brand’s performance roots to outrun mounting tariff pressures and cooling demand in China.

The company is scheduled to release its thirdquarter numbers after the market close on 31 March.

How has the company been performing?

Expectations for the period, covering the three months to 28 February, dipped after the company guided for a low single-digit fall in revenues and a 1.75% to 2.25% drop in gross margins, following disappointing second-quarter earnings on 19 December 2025.

Nike reported a 30% fall in earnings per share to $0.53, reflecting tariffs, sales weakness in China and costly promotions to reduce excess stock.

The earnings report sent the shares down by 10% to their lowest level in seven months, which means they have dropped by more than 60% from the late 2021 peak.

The turnaround under Hill, a veteran of the

Nike Q3 earnings forecast

Source: Zacks

company who came out of retirement in 2024 to drive a recovery, is predicated on steering Nike away from an overreliance on lifestyle categories and back towards performance categories like running, basketball, and football.

Hill is reversing a previous tilt towards a DTC (direct-to-consumer) model by re-engaging with wholesalers to regain lost share to competitors like On and Hoka.

Nike is also shifting away from Chinese manufacturing to increase supply chain diversification and reduce tariffs. China remains a key market for Nike as it tries to reconnect the brand to everyday sports

Key dates

Overseas stocks

Lululemon (Q4)

☽ 17-Mar

Micron (Q2) ☽ 18-Mar

FedEx (Q3) ☽ 19-Mar

Carnival (Q1) ☼ 20-Mar

Nike (Q3) ☽ 31-Mar

UK Stocks

Prudential (FY) 18-Mar

Smiths Group (HY) 20-Mar

Kingfisher (FY) 24-Mar

Next (FY) 26-Mar

Key economic announcements

European CPI (Feb) 18-Mar

US PPI (Feb) 18-Mar

US interest rate decision 18-Mar

Bank of England rate decision 19-Mar

ECB interest rate decision 19-Mar

S&P Global

Composite PMI 20-Mar

UK CPI (Feb) 25-Mar

Key: Q=Quarter. HY= Half year. FY=Full year. TS= Trading statement. ☽ = After market close. ☼ = Before market open. CPI = consumer price index. PPI = producer price index

Source: LSEG

participation rather than fashion. The company has struggled thanks to domestic competition in China and damage to the brand caused by the company expressing concern about forced labour in the Xinjiang region, something which prompted a consumer boycott.

What are consensus expectations?

Consensus forecasts imply close to a 10% fall in revenues to around $11.3 billion, with earnings per share coming in at $0.32. This reflects

margin pressure and higher operating costs.

Analysts have meaningfully lowered their estimates and priced in tariff costs, margin compression and further weakness in the direct-toconsumer sales channel.

The shares are down by around 10% over the last three months compared with a small gain in the S&P 500 index. Hill warned investors achieving a return to fortunes for Nike would be a marathon not a sprint and this has proven to be the case thus far.

Ask Rachel: Your retirement questions answered

Should I defer my retirement or not?

Ask the experts

Rachel Vahey is here to answer questions on pensions.

If you’d like a question considered for a future edition send it in now.

I am approaching 65 years old and find myself enjoying work so much that I don’t want to retire just yet, I’d prefer to continue working, although I may cut my working hours.

I am a widower and receive a small income from my late wife’s pension. I have a defined benefit pension which I no longer pay into, and I now contribute regularly to a workplace defined contribution pension. I also have a couple of much smaller pensions from my early working years. Given my situation, what are the pros and cons of deferring retirement, and how should I approach my pension options?

James

Rachel Vahey, AJ Bell Head of Public Policy, says:

In days gone by, retirement was typically seen as something you did once you reached 60 or 65, swapping the workplace one day for pottering around the garden the next. However, today, retirement is viewed as highly personal, with no universal approach. Each person’s experience of retirement is distinct; some look forward to leaving work and pursuing personal interests, while others prefer to remain engaged professionally, transition into a new career, or convert a hobby into a business.

Why there’s no standard retirement age

Working out the best age to access your pensions

can be complex, as there is no standard retirement age. Instead, your decision is influenced by individual circumstances, including professional aspirations, available savings, additional sources of income, anticipated expenses, and health considerations.

Employees cannot be compelled to retire at a specific age, but it is advisable to discuss your future intentions with your employer. Some choose to put in place a timetable for gradually reducing the number of hours at the office.

The state pension age is currently 66, but this is now increasing gradually to 67 from April 2026. If you don’t need your state pension you can choose to defer it. Although you will lose payments over the deferral period, the amount you eventually receive will increase by approximately 5.8% for each year deferred, provided you defer for at least nine weeks. Whether this is the best option is a judgement call; those in poor health or with lower

life expectancy may not benefit from deferral.

Private or workplace pensions are generally accessible from age 55 (rising to 57 from April 2028). There is no maximum age you must access your pension by. However, there may be tax implications if you die after age 75 without having accessed these funds, and personal contributions paid after age 75 will not receive tax relief.

Your defined benefit pension will have a set retirement age, but you should be able to take your money earlier or defer to later. It’s best checking directly with the pension scheme what adjustments will be made to your pension.

Defined contribution pensions, such as SIPPs, can typically remain invested until the holder chooses to access them, continuing to build up any contributions and potential tax-free investment growth. If you do decide to delay accessing them then this could lead to a bigger final pot value.

Keep on top of how your pensions are positioned

For workplace pensions, it is prudent to review investment strategies as you get older. Many schemes implement a glide path, gradually shifting assets from equities to lower-risk options like gilts or bonds as retirement approaches. So, if you intend to access your pension later, or you are not intending to buy an annuity with your pension pot, then you may wish to reconsider these allocations, to make sure you continue to benefit from investment growth.

Finally, you have a few different pension pots.

You could decide to gradually access these individually, taking them when you need money, for example to replace lost earnings as you cut your work hours to transition into retirement. Alternatively, you could combine your defined contribution pensions under one plan before accessing them. This may make it easier to get an overall picture of your pension wealth and tax position, as well as to manage how much money you want to take from the one pension pot and when.

Shares magazine is published by AJ Bell, authorised and regulated by the Financial Conduct Authority. It’s here to inform, not to give personal advice. Please don’t base your investment decisions on it alone. If you’re unsure, speak to an independent adviser. And remember: past performance isn’t a guide to the future. Tax benefits depend on your circumstances and tax rules may change.

Data disrupted: How AI is hitting everything from comparison sites to software and analytics firms

In early February 2026 ChatGPT rival Claude, a large language model owned by Anthropic, released a suite of specialized AI tools which sent a shockwave through certain sectors.

The software space was already under pressure from generative AI which is increasingly writing code. Anthropic CEO Dario Amodei told listeners on a recent podcast that the company itself was using Claude to write up to 80% of its own coding.

Investors zoomed into the legal services AI agent which initially knocked shares in companies that sell data and services into the legal industry such as Relx and Wolters Kluwer

However, it quickly dawned on investors that Claude had released a whole suite of AI agents across marketing, sales and even wealth management.

It should be emphasised that Anthropic’s immediate goal was not to disrupt these sectors but to showcase how firms could build applications using its large language model.

In any case, the release of Claude’s AI tools helped crystallise AI disruption fears for investors and triggered a knee-jerk reaction, wiping out over $285 billion in global market value in a single day across a range of sectors including software and data management.

The selling hit companies operating beyond legal services including enterprise software providers, platforms like Autotrader and Rightmove as well

data companies like Experian and the London Stock Exchange.

Selection of biggest Claude Cowork-related share price falls

Source: Sharescope

How are firms adapting?

Software companies have traditionally generated revenue by charging per number of users or ‘seats’

Sector

Relx runs it legal business through LexisNexis, which is a premium subscription research platform used by law firms to access case law, court documents and citations.

Lawyers subscribe to tiered plans starting at around $150 per month, scaling up to advanced plans for multi-state coverage and advanced tools. A junior associate spends around three hours a day researching precedents and pulling case material to draft a report.

How does Claude disrupt this?

Claude’s AI desktop automation tool monitors incoming client briefs which then trigger a search using publicly available court records and synthesises relevant case law before drafting a

deployed. This revenue model is no longer viable when an AI agent can automate the work.

There are signs the software industry is moving towards a model based on the number of completed tasks or successfully taking a project from initiation to completion. A good example of a company integrating AI into its customer proposition is Salesforce.

In its quarterly earnings report on 26 February, the company introduced a new metric to investors called AWU (Agentic work unit), defined as a discrete task accomplished by an AI agent, comprising decisions made, records updated, and workflows triggered.

Salesforce said it has completed 2.4 billion AWUs

research memo into the junior associate’s folder.

The associate’s role shifts from doing the research and drafting reports to reviewing and refining. The hours spent previously justified the cost of a subscription.

If AI agents can automate enough of the work, firms question whether they need to pay for so many ‘seats’ (people using the subscription). There’s a risk that a manager can now justify downgrading from a firm-wide Nexis+ subscription to a shared seat.

In other words, the AI agent doesn’t affect LexisNexis’s data, it attacks the human time spent using the database.

Relx introduced its own AI legal assistant, Protégé in 2025 to counter the threat.

on its Agentforce platform in the last two years and notched up 57% quarter-on-quarter growth in the most recent reporting period.

For professional service firms like McKinsey and Accenture the classic charging model has been billable hours.

Where an AI agent can perform a junior associate’s 40-hour data analysis in fraction of the time, the old model is vulnerable to lead revenue shrinkage, everything else being equal.

Therefore, professional firms are moving towards a hybrid model comprising a fixed ‘access fee’ to use a firm’s brand and specialised AI models, and a ‘consumption fee’ based on performance and completed tasks.

A PRACTICAL EXAMPLE OF HOW AI COULD DISRUPT LEGAL SERVICES

Which firms are better positioned to adapt?

Subsequent recoveries in Claude-affected names

Source: Sharescope

Share price performance since the lows in midFebruary suggests a clear split between winners and losers.

Specifically, the market appears to have given businesses which own proprietary data the benefit

of the doubt.

These include firms like Relx, MONY and Thomson Reuters which have subsequently seen a significant recovery in their share prices.

The implication is that companies which own proprietary data and have private information on their customers are incentivised to build their own AI tools, thus limiting head-on AI competition.

Relx provides a good example with the shares getting back within 10% of the price before the Claude-related sell-off.

The company has launched or announced 13 products powered by AI including its legal research platform Lexis+ and integrated legal assistant Protégé.

Chief financial officer Nick Luff told Reuters: “We’re applying our algorithms, proprietary algorithms, so that we can get out the right judgments, the right inferences, and the right interpretations to professional users making highvalue decisions.”

The key to long-term success will rest on how tightly companies integrate their own agents on top of proprietary data to lock customers into their ecosystems.

This does not mean that firms are immune to disintermediation, or in other words being cut out of the picture by AI, but it reinforces the importance of private and curated data.

What are the risks for Sage, Rightmove and Autotrader?

The share price recoveries have not extended to all companies hit by the Claude agent release. This suggests investors are more concerned about the impact of AI on these business models.

Investor Nick Train who manages the Finsbury Growth and Income investment trust and which has holdings in Autotrader and Rightmove, argues that these companies still own vehicle/property data, pricing histories and behavioural insights, which are not available to AI agents.

Sage’s business model is about providing accounting records and compliance software for SMEs (Small and medium sized companies) which, in theory makes it harder for AI agents to get access as they typically sit on top of the whatever accounting system a business uses.

The company is building its own network of

How software and platform firms are valued by the market

* 2027 PE where year end is not December

Source: Stockopedia, data to 2 March 2026

agents for MTD (Making tax digital) payroll and cashflow on the Sage Platform and Sage Copilot.

Sage already automates around 80% of the administration behind pulling records, flagging anomalies and reminding users of HMRC deadlines, leaving the final approval with the accountant.

It is also integrating open banking feeds via partners like GoCardless to pull bank transactions into Sage products, AI agents can connect directly to SMEs bank data via the same open banking links, potentially lowering switching costs.

For the uninitiated open banking was introduced by the Competition and Markets Authority in 2018 to boost competition and provide a secure way to share information with information providers.

The question of whether open banking is a tailwind or threat depends on how quickly Sage turns its system of record position into AI-driven services.

It is interesting that Fundsmith, which specialises in investing in high quality, resilient global growth companies has initiated a new position in Sage according to the fund’s January newsletter, after exiting US financial technology platform Intuit

What conclusions can we draw?

There are two important observations which

investors need to consider. The capabilities of generative AI are accelerating at breakneck speed. The adoption of AI at the consumer level has been unprecedented.

As of early 2026 there are an estimated 1.1 billion people actively using AI worldwide, or roughly 13% of the global population, with ChatGPT holding the dominant share.

The initial stock market reaction to the release of Claude’s AI applications has been indiscriminate, claiming victims across a broad basket of stocks from legal research to sales tools and analytics, all in one fell swoop.

Corporations have been slow to adopt AI and have taken a more cautious approach in contrast to the hype surrounding adoption by consumers.

For investors it feels important to figure out the strength of a company’s proprietary data and the speed at which it is rolling out AI tools, and how credible they are, to determine if it risks being circumvented by external AI agents.

Martin Gamble Shares and Markets Writer

Magnum’s meltdown: can Unilever’s ice cream spin-off recover from a bad start?

In December 2025 investors in Unilever received free shares in the world’s largest ice cream manufacturer following the demerger of The Magnum Ice Cream Company. Just weeks later, a mixed set of maiden results (12 February) from the new entity, saw its shares melt under the glare of the public markets.

The Unilever spin-off brought inevitable one-off costs, resulting in a messy set of numbers. Investors reacted negatively to sharp declines in annual earnings and cash flow, with profit below forecasts. Bringing into question communication around the split and the way expectations were managed.

Ultimately the share price drop suggests many Unilever shareholders were keen to sell the Magnum shares newly acquired through the demerger.

For Unilever, the results and the reaction to them merely confirmed the wisdom of exiting the seasonal, high-cost ice cream business to

The Magnum Ice Cream Company

Key stats

Share price: £11.18

Market value: £6.8 billion

Forecast PE 2026: 13.1

Forecast dividend yield 2026: 2.9%

PE = price to earnings

Source: Stockopedia, LSEG

concentrate on its core brands.

After this disappointing start to life as an independent entity what can Magnum do to rebuild credibility and how can it tackle market concerns that weight-loss drugs will slash demand for high-calorie treats like ice cream?

What is the Magnum Ice Cream Company and who’s the competition?

The Magnum Ice Cream Company, now listed in London, New York and with a primary listing in Amsterdam, has a 21% share of the global ice cream market. It has four so-called ‘power brands’ which will be familiar fixtures in freezers in supermarkets, convenience stores and at home.

This quartet encompasses Magnum, Ben & Jerry’s, Cornetto and the Heartbrand (also known as Wall’s). Combined they account for 70% of group revenue.

Global ice cream market historic and projected growth

Its main rival is private outfit Froneri which owns the premium Häagen-Dazs brand. Swiss consumer goods giant Nestlé has a 50% stake in Froneri as part of a joint venture with French private equity firm PAI Partners.

In February 2026 reports suggested Nestlé would, like Unilever give up on direct involvement in the ice cream game, by selling its smaller, wholly owned ice cream operations to Froneri.

Magnum’s CEO is Peter ter Kulve who had a long career at Unilever in several executive roles. His task will be to energise a business which saw a stagnant market share between 2016 and 2023 and only a very modest improvement in profit over the same time period from €1.1 billion to €1.2 billion.

Under a transformation programme launched in 2024 in the run-up to the demerger, Magnum

gained 90 basis points of market share in a year and pushed profit to €1.3 billion.

What are the company’s plans for future growth?

Like a lot of consumer goods companies, Magnum is seeing stronger growth in emerging markets than in the developed world. This reflects an emerging middle class in these countries but also the absence of the unbranded alternatives which are taking sales away from the bigger brands in the West.

The company is looking to lean into this opportunity. The acquisition of a 61% stake Kwality Wall’s India from Hindustan Unilever will give it control over some of its key brands in one of the world’s fastest growing markets for ice cream.

The company also hopes to improve efficiency

Source: The Magnum Ice Cream Company, Euromonitor

Magnum’s main rival own the Häagen-Dazs brand

How The Magnum Ice Cream Company's valuation compares to other consumer goods firms

Source: Stockopedia, data to 9 March 2026

and, by doing so, boost its margins. Alongside this, there are plans to put more marketing money behind its brands which investment bank Berenberg notes suffered from a period of underinvestment under former parent Unilever.

The €500 million productivity programme is guided to boost the adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) margin by 40 to 60 basis points in 2026.

It involves relying on its brand strength to offset higher cocoa and dairy costs, expanding its network of branded freezers and consolidating and upgrading its manufacturing facilities.

Magnum has projected annual growth of 3% to 5% from 2026 and, assuming the group can be more efficient as a standalone entity, this should feed into profit growth which outpaces any expansion in sales.

What are the key risks facing the company?

Increased proliferation of weight-loss drugs is a risk to growth as they could literally reduce the people’s appetite for less healthy options like ice cream.

One potential solution to this is product innovation and a move into ‘adult functional refreshment’ with the recently launched lowcalorie, vitamin-enriched Hydro:ICE ice pop offers some insight into the direction it might take.

The launch into portion-controlled segments with its bite size Magnum Bonbon range and its

higher protein and lower fat Yasso frozen yoghurt range are other examples.

However, Magnum’s long-term success likely relies on there still being some room for consumers to indulge themselves in a GLP-1 world.

Another challenge for the company is the borrowings it is saddled with following its split from Unilever. Net debt currently stands at €3 billion or 2.6 times adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) with annual interest payments estimated at €139 million.

How does the valuation compare to peers?

While its lack of stock market listing makes a comparison between Magnum and Froneri tricky –a funding round in October 2025 valued the latter at €15 billion and its annual sales in 2024 were €5.5 billion. The Magnum Ice Cream Company is currently valued at €7.9 billion and its latest annual revenue came in at €7.9 billion too.

Magnum trades at a discount on a price to earnings or PE basis to its diversified listed peers too, on a 2026 forecast PE of 13.1 times, reflecting its debt pile and structurally higher costs.

By Tom Sieber Editor

Last orders for pension top-ups?

Boosting contributions before and after retirement

Many people in their 50s are in a financial sweet spot. Earnings are often at their peak, mortgages may be shrinking and any children are hopefully proving less expensive. That makes this period a golden opportunity to give your pension a final push, if you know the rules.

Here’s what you need to know about pension contribution limits, carry forward and what changes once you start drawing your pension.

How much can I pay in?

There are two main levers that control the tax benefits of pension contributions. The first limits pension tax relief on your own contributions. You can pay in up to 100% of your UK earnings into pensions each tax year and you’ll get the full benefit of tax relief. In theory, if your gross salary was £75,000, you could pay up to £75,000 gross into your pensions.

Accounting for the automatic tax relief in a SIPP, this would be a net payment of £60,000. While this is unrealistic for most people, it’s important

to keep in mind if you’re looking to maximise your payments in a particular year, or if a large chunk if your income comes from dividends, or property rental income, which do not count towards your UK earnings when working out your pension contribution.

The second is the pension annual allowance, which is £60,000 for most people. The annual allowance covers everything paid in by you, or contributions made for you, like those made by your employer. It also includes any tax relief top up added directly into pensions like SIPPs.

If you go over your allowance for a year, you might face a tax charge. This would fall on you personally, even if the excess contributions came from your employer.

But the carry forward rules can help here. They let you look back for up to three previous tax years and carry forward unused allowances from those years too. This is particularly useful if you’ve got a chunk of variable earnings, or your business has a particularly bumper year.

How carry forward works

Let’s consider the example of Caroline, 50, who will earn £100,000 gross this year, including her bonus. She wants to know the maximum she could pay into her pension.

She’s already paid in £20,000 to her SIPP, which is £25,000 gross including the automatic tax relief. Her employer has added another £15,000 gross. This means she still has £20,000 of unused annual allowance for the year.

Carry forward could help her pay in even more than that.

The only condition for carry forward is that you must have been a member of a registered pension scheme in the earlier years.

There is then a specific order for using your annual allowances. You use the current year’s annual allowance first, then you go back to the earliest of the three previous years and work forwards.

You can still only get tax relief on personal contributions up to your relevant UK earnings in the current tax year. Remember, however, that employer contributions aren’t restricted by earnings in the same way as your own contributions.

Caroline’s previous contributions are summarised in the table below.

In 2025/26, Caroline has already used £40,000 of her annual allowance. This leaves her with

Caroline’s previous contributions

£20,000 for this year, plus up to £50,000 that she could carry forward from the previous years.

If her circumstances allow, Caroline could mop up this extra allowance by making a personal contribution of £56,000 to her SIPP before the end of the tax year. Including the automatic basic rate tax relief top up of £14,000, she’d have £70,000 extra saved towards her retirement. Caroline should also make sure she claims the extra higher rate tax relief she’s entitled to. She can do this directly with HMRC online or via her self-assessment tax return if she already files one.

*The annual allowance in 2022/23 was £40,000

Source: HMRC

High income? Watch out for the taper

The annual allowance is tapered down for people with high incomes. If you trigger both the ‘adjusted income’ and ‘threshold income’ tests, your pension annual allowance begins to be reduced and could be as low as the minimum £10,000 if your adjusted income is over £360,000.

How the taper works

Adjusted income

Total taxable income (not just earnings), plus any employer pension contributions. If adjusted income is over £260,000, you must also check if threshold income is also over £200,000.

Threshold income over £200,000?

Total taxable income (not just earnings), plus any salary sacrifice earnings set up after July 2015, minus

total personal contributions where tax relief was added into the pension (known as relief at source).

Source: HMRC

To trigger the taper, both income limits must be triggered.

You can read more and see worked example in AJ Bell’s customer guide, but if you’re concerned about the annual allowance taper, you should seek professional advice.

If you were subject to the taper in a previous tax year, this will also reduce how much annual allowance you can carry forward from that tax year.

Do the rules change once I access my pension?

Your annual allowance might be lower if you take a flexible income option from your pension. The first time you receive an income payment under flexi-access drawdown or take a pension lump sum that is part taxable (also known as UFPLS), you’ll trigger the money purchase annual allowance (MPAA).

The MPAA is a lower annual allowance of £10,000 that will apply across all your ‘money purchase’ pensions like SIPPs. And you’ll no longer be able to make use of carry forward in these types of pensions.

The MPAA and the carry forward restrictions are not triggered if you only take all of some of your 25% tax-free lump sum and no income. It also does not apply to any pension paid from defined benefit scheme or income from the older type of drawdown called capped drawdown.

The restrictions might not be a concern if you plan to fully retire and stop work, but care is needed for people who need to dip into their pension savings to top up their income early in retirement but then want to add money back in. If you take more than your tax-free lump sum, triggering the MPAA can seriously limit your options when it comes to making good any gaps later.

The run-up to retirement is often your last real opportunity to turbocharge your pension savings. Carry forward can allow six-figure contributions in the right circumstances, but once you start drawing income flexibly, the door largely closes.

Charlene Young Senior Pensions and Savings Expert

Why investment trusts are buying themselves more than ever

Share buybacks are a commonplace market phenomenon, but it’s a tool that’s used for widely different reasons.

The practice involves a listed firm buying back its own stock so that the total amount of its shares in issue is reduced. The overall aim is to enhance the value of the remaining shares and for standard public trading companies, this is often a means of returning surplus cash to investors.

Shareholders of FTSE 100 oil and gas major BP recently woke up to the news that it was suspending its share buyback programme as the company pivoted the company to use its cash to try and sort out its large debt pile.

But for investment trusts buybacks are used as one of several tools deployed to try and manage their ‘discounts’. Research by AJ Bell suggests that the biggest buybacks in the trust universe may have been at least partly effective last year in achieving this goal. Read on to find out more.

What is an investment trust?

Trusts are listed on the public market just like BP or other listed companies, but they are a wholly different type of ‘company’. A trust’s purpose is to invest in other assets (such as equities, bonds, property) on behalf of its shareholders, rather

than operating as a business providing goods and services.

Because it’s listed, a trust will therefore run at either a ‘premium’ or a ‘discount’. This is the difference between a trust’s share price, or what it trades for on the stock exchange, and its net asset value (NAV), the actual worth of its holdings.

A discount occurs when then share price is lower than the NAV and this can happen even if a trust has been making positive total returns for its investors.

Why do discounts arise?

Most UK investment trusts have been running on a perpetual discount for several years due to a myriad of headwinds.

Some of these challenges have been general issues, like when inflation and, in turn, interest rates were rising rapidly, thereby increasing the appeal of lower risk assets like bonds and cash.

Increased geopolitical uncertainty saw rampant volatility in the market and these factors also led investors to search for lower risk options. But some issues contributing to discounts are more sector specific, such as the renewable energy companies dealing with all the above while unsupportive government policies dampen demand for its assets.

According to data from the Association of Investment Companies (AIC), the average trust is running on an 11.8% discount.

Activists circling the trust space

The discount/premium mechanism is a well-known element of trusts and is not inherently a bad thing. It can allow investors the chance to invest in a trust, or add to their holdings, if they think it is being mispriced by the market.

But as we’ve seen in recent months, persistent discounts have also been seized upon by activist investors as they attempt to shake things up.

US hedge fund group Saba Capital has been a high-profile example of this, investing in more than 40 trusts since it emerged on the scene with a bang two years ago and using the discounts as a way to build up meaningful stakes and trigger major shareholder votes to try and change things (be it the board, the investment approach, or both).

Trust boards have been carrying out share buybacks with increasing frequency to bring the portfolios back to what they regard as a

fairer market value, as well as to try and protect themselves against the activists circling the sector.

A record year for trust buybacks

Last year, a record £10.2 billion worth of shares were bought back by investment trusts, according to the AIC. This was 36% higher than the year before, with each year sending the total to new heights since the pandemic. The table below shows the top five trust buybacks by value for 2025.

Strikingly, all of five trusts featured in the table above ended the year on a narrower discount to that which they started it with. Other factors will have had an impact here, but it offers at least some evidence that buybacks might be working.

Of the total buybacks completed in 2025, Baillie Gifford’s Scottish Mortgage accounted for more than 15%, buying back £1.7 billion worth of its shares over the period.

Scottish Mortgage committed to the biggest share buyback programme in its history back in 2024, with plans to repurchase at least £1 billion worth of its own shares over the following two

Top five investment trust share buybacks in 2025

Source: LSEG

years. As of August 2025, Scottish Mortgage had repurchased £2.5 billion of its shares, but it still hasn’t managed to close the gap between share price and net asset value entirely.

Scottish Mortgage started the year at -10.7% and ended 2025 on -9%. At its widest, the discount widened out to -16% amid the US ‘Liberation Day’ chaos which shook global markets. At its narrowest, the discount shrank to -5.3%.

Buybacks are a useful tool to help manage a discount, but they are not a silver bullet. Their overall effectiveness has long been debated, a topic which has only become more relevant as markets have become more volatile.

Discounts in the context of investment trusts are not inherently a sign that something is wrong, but sometimes the market is trying to tell you something.

And ultimately, share buybacks cannot prevent a trust going onto an even bigger discount if there is simply no demand from investors.

Buybacks can’t, for example, fix wholesale negative sector sentiment, something which has been evident in the renewables trust space.

Nick Train, manager of the Finsbury Growth & Income Trust, which was extremely busy buying its own stock last year, has continuously lamented the disenchanted attitude domestic and international investors have had with London-listed stocks which has fed into his UK-focused trust’s discount.

Why buybacks can come in for criticism

As well as debating their effectiveness, some analysts argue that buybacks show a lack of faith

Finsbury Growth & Income Trust

Source:

on the part of the board in the manager’s ability to identify good investment opportunities. Drawing the conclusion that a better use of the cash is to buy themselves rather than anything else on the market.

Portfolio managers would almost always prefer to be out trying to tap into the next big investment trend or topping up their existing holdings if the valuation allows. But most see buybacks as one of the tools boards have at their disposal to act in shareholders’ best interests by managing the discount level. Many were criticised for not pulling the buyback lever sooner when the discounts really started to become entrenched three years ago.

Winterflood Securities latest investment trust industry survey found that 79% of experienced investors said discount control policies were ‘extremely’ important to them. Most boards do have a semi-informal ‘trigger level’ in place, where they will consider initiating a buyback when the discount hits a certain point.

Although 2026 has started off with a dip in investment trust buyback volumes – down 10% month-on-month in January – it seems unlikely that boards will cease buying themselves anytime soon given there are seemingly fewer quiet days in the market now and activists are only getting louder.

By Eve Maddock‑Jones Funds and Investment Trust Writer

Why

active

versus passive

investing isn’t so black and white anymore

Equal weighed exchange-traded funds (ETFs for short) have emerged as one of the more popular investment trends in recent months as investors seek new ways to diversify their exposure to major equity markets.

These products are distinct from a ‘typical’ ETF, because rather than the largest companies by market value having the biggest influence on performance, all the underlying names have the same impact.

There are currently 26 equal weight ETFs, the first of which debuted back in 2011, themed around European ESG stocks, according to data from Morningstar Direct.

Since 2021, more and more have launched each year with 2025 seeing a record eight come to market. And increasingly, they’re focused on one thing in particular: US tech, with half of 2025’s cohort dedicated to this area in particular.

And it’s not a coincidence. Last year saw investors fleeing for cover from what had been one of the best trades of the 21st century, a run of the mill US equity index ETF. This movement could be seen as a case study for why investors need to consider an active approach to their passive allocation.

Passive investing over the past two decades

At face value, this would appear to be counter intuitive, as any active fund manager will tell you why their investment approach is distinct from a tracker fund.

‘Tracker’ is a catchall term for buying a low-cost

Source: Morningstar

Number of equal weight ETFs launched

Deep Dive: Active versus passive investing

Equal weight ETFs available to UK retail investors

ETF

Ossiam STOXX Europe 600 ESG Equal Weight NR UCITS ETF

VanEck World Equal Weight Screened UCITS ETF

Xtrackers S&P 500 Equal Weight UCITS ETF

VanEck European Equal Weight Screened UCITS ETF

iShares MSCI World Mid-Cap Equal Weight UCITS ETF

iShares MSCI Europe Mid-Cap Equal Weight UCITS ETF

iShares MSCI USA Mid-Cap Equal Weight UCITS ETF

HAN-GINS Tech Megatrend Equal Weight UCITS ETF

Invesco Markets II plc - Invesco S&P 500 Equal Weight UCITS ETF

L&G Europe ex-UK Quality Dividends Equal Weight UCITS ETF

L&G UK Quality Dividends Equal Weight UCITS ETF

L&G APAC ex-Japan Quality Dividends Equal Weight UCITS ETF

L&G Emerging Markets Quality Dividends Equal Weight UCITS ETF

iShares S&P 500 Equal Weight UCITS ETF

Amundi US Tech 100 Equal Weight UCITS ETF

Xtrackers S&P 500 Equal Weight Scored & Screened UCITS ETF

Invesco NASDAQ-100 Equal Weight UCITS ETF

Invesco MSCI World Equal Weight UCITS ETF

Invesco S&P 500 Equal Weight Swap UCITS ETF

UBS S&P 500 Equal Weight SF UCITS ETF

Invesco Markets II plc - Invesco MSCI Europe Equal Weight UCITS ETF

Multi Units Luxembourg - Amundi S&P 500 Equal Weight

BNP Paribas Easy MSCI World Equal Weight Select UCI

Xtrackers S&P 500 Equal Weight Swap UCITS ETF

L&G S&P 100 Equal Weight UCITS ETF

Invesco EURO STOXX 50 Equal Weight UCITS ETF

Source: Morningstar

product, such as an ETF, which is generally designed to match the performance of a particular index or investment.

An actively managed fund is on the other hand is run by a team of experts and typically holds a more concentrated pool of assets, sometimes as few as 30 or 40 or even less. These are selected based on the manager’s research and expertise backs to outperform the broader market and, in theory, deliver better total returns.

This is what investors pay a higher fee for. However, most active managers have struggled to outperform the benchmark over the past two decades. Since 2006 the S&P 500 has achieved a total return in sterling of almost 600%, while the MSCI All-Country World Index – of which the US accounts for around 50% – made 525%. The Investment Association’s Global fund sector has returned 360% since 2006.

The FTSE 100 made 291% over the same time period, according to data from FE Analytics.

Global active funds have struggled to beat major indices

Total return in sterling

Source: FE Analytics, data to 3 March 2026

A lot of the US’ success across the Atlantic was driven by only handful of companies, originally the FANNGS – Facebook (now Meta), Apple, Amazon, Netflix, and Google (Alphabet) – which evolved into today’s Magnificent 7 – with Meta, Alphabet, Amazon and Apple joined by Microsoft, Nvidia and Tesla.

These seven stocks make up around 33% of the S&P index, and in 2024 drove 65% of the returns. This concentration has meant that not being exposed to these specific names almost guaranteed

Deep Dive: Active versus passive investing

you would underperform the benchmark. Hence why a cheap tracker fund was so appealing, since investors could get high returns without having to pay an active management fee.

AJ Bell’s latest Manager versus Machine report found that 2025 was an “extremely poor year for active managers”, with just 29% beating a passive alternative.

But, the tide has begun to turn and has challenged the ‘chuck it in US tracker and forget about it’ mentality.

The changing tides in US equities

Higher rates of inflation and interest rates along with a more volatile geopolitical backdrop have had a major impact on markets the past couple of years, but US tech in particular has become one of the biggest sources of portfolio volatility.

Sticking with the Mag 7, when US President Donald Trump launched his now infamous ‘Liberation Day’ tariffs back in April, the S&P 500 fell by 4.8% on the day, with this cohort losing 6.7%, which equated to $5 trillion being wiped off the market in one fell swoop.

The event caused the VIX index – the so-called ‘fear gauge’ of Wall Street – to hit its third highest point on record (45), only beaten by the pandemic and 2008 global financial crash, respectively.

And while short term events, such Liberation Day or the escalating conflict between the Iran-USIsrael are not things to make knee jerk reactions to, the fact that markets are increasingly volatile does make a case for a more deliberate approach to diversifying a portfolio.

In a bid to take cover from these incredibly heavy drops, there has been a broad push to get US exposure via equal weighted ETFs as a way to help alleviate the concentration risk factor.

Important things to consider

But while this is one step towards taking a more deliberate view about investing in passives, they are not without their drawbacks.

For example, if you had bought into one around Liberation Day you would have missed out on the Mag 7’s re-rating in the latter half of the year.

Terry McGivern, a senior research analyst at AJ Bell who heads up passive fund selection on the Investments team, explained that there is a level of bravery in moving into equal weight, especially

when it comes to the US. This is because any decision to move away from traditional market cap weighting means you’re taking a position that the wider market is incorrectly pricing and weighting the companies in the standard index.

You’re also routinely selling your winners and buying recent losers, to maintain that equal weight position, which is an anti-momentum approach, and that can be an issue when momentum has historically been one of the most well rewarded risk factors in financial markets.

“It’s not a panacea, and investors need to be aware of the contrarian position they’re taking, when using an equal weight approach,” McGivern explains.

AJ Bell’s investment team increased its US exposure in the latest portfolio rebalance but this was done in a very deliberate way, through introducing sector trackers covering healthcare, energy and utilities.

McGivern said that the team tend to use sector and thematic products more as satellite holdings; essentially bolt on exposures to the main regional investment pots rather than standalone pieces of the core investment thesis.

Investment decisions should always be made with a significant amount of care and consideration, it’s just that now, perhaps more than in recent years, investors need to ask themselves a few more questions when it comes to investing passively.

By Eve Maddock‑Jones Funds and Investment Trust Writer

Listen for more

You can access the free AJ Bell Money & Markets Deep Dive podcast in the usual podcast places. It looks at a range of investment topics in detail including active versus passive investing.

How do I go about picking an active fund manager?

Ask the experts

Paul Angell is on hand to answer your questions about investments.

If you’d like a question considered for a future edition send it in now.

I’m worried about being entirely invested in tracker funds. How should I choose a manager that picks stocks?

Matt

Paul Angell, AJ Bell Head of Investment Research, says:

Hi Matt, I suspect your concerns here boil down to being exposed to unnecessary risks in a passive only approach or missing out on opportunities in not having any actively managed funds, or both. Either way you’re considering diversifying your portfolio, by bringing together different funds or stocks to play different roles, which is a good thing.

The value of diversification

We think long and hard about diversification within our AJ Bell investments team, particularly at an asset allocation perspective. For example, are we blending diversified regions and asset classes that give our portfolios the best possible opportunity to perform from a risk and return perspective? Take regional diversification for example, if you were to invest in a global equity passive fund, you’ll find that one specific equity market, the US, makes up a massive part of the portfolio, with other regions less represented, if at all.

We’re very aware of this US market dominance in our AJ Bell funds, so seek to diversify away this risk, and add in more opportunities through our regional asset allocation. The table shows how our AJ Bell’s Global Growth fund compares to a fund tracking the global equity market (MSCI World) in terms of regional diversification.

Looking for active managers

The major appeal of active managers is an opportunity to beat the market. While there is

Ask Paul: Your investment questions answered

Regional allocation of fund tracking the MSCI World versus AJ Bell Global Growth fund

*No specification of holdings in China or emerging markets ex-China, holdings would instead be categorised under ‘other’

Source: AJ Bell, BlackRock, allocations as of January 2026

a chance to achieve this, studies by AJ Bell have shown that, over a 10-year period, just 24% of active managers achieved this goal as of 2025.

So, how do you go about picking the right active managers? The five Ps are a good place to start: philosophy, process, people, performance and price.

Typically, the charges associated with an active fund are a bit higher than passive, so before purchasing, you’ll want to ensure that the price still seems reasonable. Remember those charges will eat into your returns each year.

Platforms are a good place to start in gauging a lot of this information, with fund manager websites able to provide more of the detail behind individual funds. You can read about the five Ps in detail a bit later.

There’s no guarantee that any of these factors ensures a fund’s future outperformance. But they do act as a useful framework to assess active funds.

There are thousands of funds to choose from, and of course running through the 5 Ps with every option is unlikely to be an efficient use of anyone’s time. For investors wanting a narrower set of

options, we’ve established a favourite funds list, that highlights some of the funds that we think have a great chance of delivering their investment objectives over the long term.

The five Ps

Philosophy is about the market inefficiency the fund managers believe exists and how they intend to exploit this in their investment approach. Market inefficiency refers to something that a fund manager believes others have either over or underpriced.

For example, perhaps they think the market undervalues companies that can quickly grow their revenue streams, or that the market undervalues ‘distressed’ stocks where they believe credible turnaround plans exist. A philosophy itself is no guarantee of success, but it does lay out the theory for active management in the fund. Understanding the philosophy can help you identify if you’re getting something unique by choosing an active manager.

Process goes hand in hand with philosophy, describing ‘how’ the managers exploit the perceived market inefficiency. This could include aspects such as who focuses on what in the management team, or the use of technology, for example a screening tool to weed out companies that don’t fit the fund’s profile.

People refers to the team that’s running the fund. This starts with the fund manager, but it also includes the team behind him or her. How long has the manager been running the fund? What was their background before this? How big is the team? How experienced are they?

The last two Ps, performance and price, are often the most significant deciding factors for investors. It’s important to remember when looking at performance, that what happened last year is no guarantee to this year’s returns. What can be more helpful is looking at a longer time period, such as three or five years, to see how the fund rides out different market conditions. Keep in mind what sort of fund you are choosing as well. If you are looking for a focus on value, the fund is unlikely to have kept up with an index that’s packed with growth companies over a period where the growth factor has outperformed, or vice versa.

When is it time to part ways with a manager?

Active funds often cycle through periods of outperformance and underperformance. Much of this waxing and waning is linked to whether an active manager’s investment philosophy or style has been in, or out, of favour.

Where possible it is therefore best to assess funds versus style-adjusted, rather than main, indices. Where a fund is consistently underperforming its broad investment style / opportunity set, say over two or three years, it’s a good indication that a fund has lost its sparkle and investors should seriously consider selling.

Otherwise the steps of revaluating a fund holding are very similar to how to select a fund in the first place. You can run through a checklist to better understand if the fund still operates to the same philosophy, if it still resonates with your investment needs, and if there have been significant changes in the team.

You can also consider fund performance and the price compared to similar products on the market. To help weigh all these up perhaps consider, if you didn’t already hold the fund, would you choose to purchase it now?

The markets can be fickle and difficult to master, so there’s no guarantee that even a fund which seems great will fare well in the future. However, following the 5 Ps should calm nerves that your investment is in safe hands, allowing investors to stay longer on the journey. After all, remember, its ‘time in’ not ‘timing’ the market that is typically an investor’s greatest friend.

How Games Workshop became the best performing UK share of the last two decades

While most investors grapple with the potential impacts of generative artificial intelligence, Games Workshop, by contrast is a refreshingly simple business.

In fact, the company recently banned employees from using AI in content or designs. Games Workshop is the world’s largest maker of hobby miniatures with two major brands, Warhammer and Warhammer 40K. The company also holds the rights

Games Workshop

Source: Sharescope, data to 4 March 2026

PE = price to earnings

Source: Stockopedia, LSEG

to the Lord of the Rings and Hobbit tabletop games.

The Nottingham-based company remains steadfastly focused on making the best quality miniatures and creating engaging fantasy worlds for its army of loyal customers across the globe to immerse themselves in hours of play.

Delivering on this vision has helped the shares climb in value to become one of the most successful UK companies on the stock market. On a 20-year view, according to figures from Sharescope, its annualised total return of 23.6% put its right at the top of the tree for all UK-listed companies. It is even handsomely ahead of the Nasdaq index of big US tech companies over this period.

Key stats

The shares were promoted to the blue-chip FTSE 100 index in December 2024, after their market value topped £6 billion, a far cry from the £10 million price tag of the management-led buyout in 1991.

The shares floated on the London Stock Exchange in July 1994 at an IPO (initial public offering) price of 100p per share.

What are the secrets to Games Workshop’s success?

Games Workshop operates a vertically integrated business model, which means it controls the whole process from designing miniatures, manufacturing them, and selling them through a global chain of ‘Warhammer’ stores.

However, Games Workshop does not see itself as a retailer, because the Warhammer stores are seen as places where hobbyists meet fellow enthusiasts to discuss collecting, painting and play.

Word of mouth is an important part of how the business recruits more hobbyists. Perhaps uniquely among FTSE 100 companies Games Workshop does not do any advertising.

The company’s minimalist approach is

Total sales by source

Source (£m)

Note: At constant currency Source: Company accounts

encapsulated in the following quote from the annual report: “We don’t spend money on things we don’t need, like expensive offices or prime rent shopping locations or advertising that speaks to the mass market and not our small band of loyal followers.”

Virtual integration allows the business to keep nearly 70% of every pound it generates in sales as gross profit, a margin that most manufacturers can only dream of making.

The scale of the business brings an advantage which is difficult for smaller competitors to match, and customer loyalty creates a high barrier for competitors.

Games Workshop’s business model and market position allows it to raise prices without impacting sales volumes. For example, the company was able to put through 3.5% price rises in early 2026 to offset US tariffs.

The ability to raise prices is very powerful because increases drop straight through to profits without any associated costs.

The growing importance of intellectual property

For more than four decades Games Workshop has

built a huge library of stories and characters.

A central plank of the firm’s strategy is to exploit the value of its intellectual property beyond core tabletop gaming into multiple categories.

In late 2024, Games Workshop inked a deal with Amazon Prime which will bring the Warhammer 40K brand to film and TV, with actor Henry Cavill serving as lead actor and executive producer.

It will take a few years for these projects to come to fruition, but the potential rewards are significant.

Analysts believe that a well-received Amazon series could add between $40 and $50 million in pure profit for Games Workshop.

Beyond licensing benefits analysts estimate that if only 1% of Amazon Prime’s global audience decide to buy a starter Warhammer set, it could generate hundreds of millions in new core tabletop revenues.

In 2025 the company saw particular success licensing video game adaptations, including Warhammer 40K: Space Marine 2, which sold seven million copies, becoming the fastest-selling game in the franchise’s history.

Licensing revenues are essentially 100% profit which allows Games Workshop to make money from people who don’t even play its tabletop games.

What is Games Workshop’s strategy?

The company states it has a simple strategy which is: “To make the best fantasy miniatures in the world, to engage and inspire our customers, and to sell our products globally at a profit”.

Games Workshop’s strategy is built on scarcity and obsession. An unnamed fund manager once commented, half-jokingly, that the biggest threat to the business is puberty.

The business went a though a digital transformation in 2015 after current CEO Kevin Rowntree took over the helm. The Warhammer+ subscription service was launched in 2021, which is a streaming platform offering animated series, painting tutorials, battle reports and apps for around $60 a year.

This strategy helps to keep enthusiasts engaged with the brands and has become an effective selfreinforcing marketing tool.

How do the financials look? It shouldn’t be a surprise to learn that Games

Workshop’s financial metrics stack up well against the average company.

The firm’s high gross margin and frugal approach towards spending on unnecessary items results in consistently high operating margins and high rates of return on equity.

Gross margin is the proportion of sales that a company keeps after paying for the direct costs of making a product. The more efficiently it can do this, the higher its gross margin.

Let’s say it costs Games Workshop £12 to make a basic set of miniatures, including buying all the raw materials, and each set is sold for £50. Sales minus cost of sales, or gross profit is £38 (50-12) and gross margin is 38/50, or 76%.

Select financial forecasts

Year end: May

Source: Stockopdedia, LSEG

A high gross margin usually translates into a high operating margin, so it is not surprising that Games Workshop achieves operating margins between 38% to 40%.

While Games Workshop is a high-quality business, it also has a high percentage of fixed costs, which is a benefit to shareholders when sales are rising but a problem when sales fall.

The company relies on word of mouth and keeping customers satisfied so anything which alienates fans could hurt the business disproportionately.

Martin Gamble Shares and Markets Writer

Does the volatility in gold signal the end of the bull market?

Ask the experts

Russ Mould is on hand to answer your queries about the financial markets.

If you’d like a question considered for a future edition send it in now.

I’ve been following the move higher in the gold price and the recent slump – is gold likely to remain under pressure from here?

Ken Russ Mould, AJ Bell Investment Director,

says:

With a gain of more than 200% in this decade to date, gold is proving its worth as a portfolio diversifier for investors.

That return beats global equities easily and of the major asset classes only the now-flagging Bitcoin and still-shiny silver can point to a better capital return. Even more amazingly, gold can point to a better capital return than the S&P 500 over the past 20 years (though dividends and buybacks from equities close up the gap to almost nothing).

The question now is whether this year’s gyrations in the precious metal markets are a sign of a top, or just the commodities taking a breather after a storming run.

Case for and against

Sceptics will remain firm in their view that the investment case against gold and precious metals is clear cut. They have little industrial use, certainly in the case of gold, generate no cash and thus rely on the greater fool theory for upside, as holders need new buyers to follow in and buy off them for the price to rise.

There also remains the risk that the recognised exchanges tinker with the rules if they feel matters are getting out of hand, as COMEX has just done in the US by raising its margin requirements for

traders, or that government gets involved, as the Roosevelt administration did with Executive Order 6102 in 1933 that effectively forbade private ownership of any scale.

Bulls will counter by pointing to ongoing geopolitical risk, a weak dollar and galloping sovereign debts, especially in the West, where the burden is now so great that inflation and monetary debasement may be the only way to render manageable those borrowings and the associated interest bill. There is, after all, little or no political or public appetite for the sort of austerity that would be required to rein in debt growth, let alone bring about a reduction in absolute terms. The prospect of more central bank money printing, in the form of quantitative easing, at the first sign of any economic or financial market trouble is a further consideration for those will still pound the table for precious metals.

Cash flow conundrum

At this stage, valuation would be used to further frame the debate, but this is more difficult in this instance, because gold and precious metals

generate no cash, an issue which comes back to why master investor Warren Buffett had no interest in them at all. He argued the metal was pretty much worthless because of its chemically inert nature. Anyone sharing that view will argue gold is worth no more than all-in sustaining costs (AISC) of production, which is around $1,800 to $2,000 an ounce, judging by recent results from major gold miners.

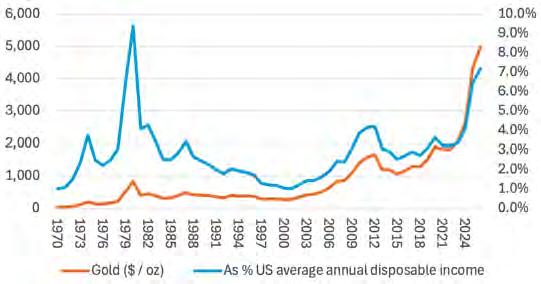

In the absence of multiples of earnings or a full-blown discounted cash flow (DCF) model, the bulls need an alternative approach to state their case. This can focus on the affordability of gold for would-be buyers, or a study of what it helps holders to buy, to provide a framework of relative, rather than absolute, valuation.

Supply and demand

One approach is to look at how the gold price compares to annual disposable income. When gold peaked at $835 an ounce in January 1980, it reached 9.4% of the annual US household’s available annual discretionary spending. Gold currently stands at 7.2% of that figure, and a return to the former high points to a gold price of some $6,500 an ounce, or a third above current levels. Asset and wage inflation (or deflation) could shape this calculation going forward.

Gold

still sits below

past

peaks when measured as a percentage of US household disposable income

A different technique is to look at gold’s purchasing power, relative to the most important buy anyone makes – a house. A would-be buyer of the average US dwelling would currently need just 90 ounces of gold to cover the cost. This compares

to the figure of 78 reached when gold peaked in January 1980. A repeat of that would take gold up by a sixth to around $5,750, again before adjusting for any future increases (or decreases) in US house prices.

Gold sits just below past peaks when measured relative to US house prices

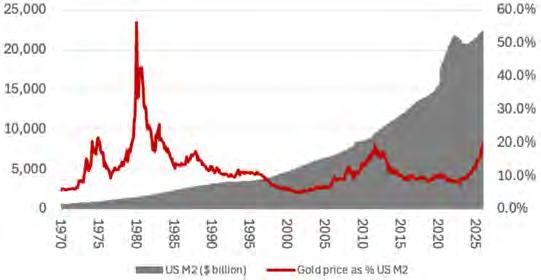

One final test is to look at the value of gold relative to US money supply. This perspective rests on the debasement trade, whereby bulls of gold assert that governments will print or rely on inflation to make their debts, and spending programmes, affordable, rather than turn to austerity or higher taxes.

Bulls of gold may measure its value relative to US money supply

Here the conclusion is that gold is way below past peaks relative to the M2 measure of money supply in the US. A return to the 1980 high would take gold above $12,600 an ounce, although it is worth bearing in mind, in this case and the other two, that gold did not hold that zenith for long at all 46 years ago.

Source: Jefferies, FRED- St. Louis Federal Reserve, LSEG Refinitiv data

Source: Myrmikan Research, FRED- St. Louis Federal Reserve, LSEG Refinitiv data

Source: Myrmikan Research, FRED- St. Louis Federal Reserve, LSEG Refinitiv data

“Do your reading.” That’s the first step for anyone wanting to take the plunge into the stock market, according to 56-year-old Simone.

For her, what this looked like was six months spent properly getting to grips with the basics before she made her first investment; learning the difference between shares and funds, then passive and actively managed funds.

Early on, she developed a simple mantra to help guide her through: “If I don’t understand it, I don’t buy it”. This has kept her away from ‘hot’ areas like cryptocurrency.

Taking the first steps

Londoner Simone made her first investment back in 2016 just after the Brexit vote. This was an unexpected event which acted as catalyst for her to take proper control of her finances and her future. Simone started out with £20,000 in her portfolio and now, 10 years later, having seen it through the pandemic, Russia’s invasion of Ukraine, ‘Liberation Day’ and various UK chancellors, it’s comfortably sitting in six figures, having achieved a return of around 10% a year.

Like most people, Simone was holding her money in a run of the mill savings account which

was offering a low interest rate and she became dissatisfied.

She, like many others, thought that moving her hard-earned savings out of her account and putting it to work in markets was high risk, “but I was going to do it”.

“No one really wanted to take the risk of making any investments during that period of Brexit and I decided ‘you know what? I’ll give it a try’, because I don’t think I could do any worse”.

At the start Simone had very short-term, practical goals for her investing; making enough to cover the travel costs for her work in the charity sector.

Working part time for a disability rights organisation meant a reduced income while her time travelling around the country as a peer advocate, helping people diagnosed with autism move out of hospitals and into their own homes, put added pressure onto her purse too.