IAASB Approves New Standard on Sustainability Assurance

Top 10 Estate Planning Topics in Texas in 2025: A Scholarly Perspective

Our Rising Stars Shine Brightly

I’m honored to introduce the November/December issue of Today’s CPA – our Rising Stars issue! This edition celebrates the future of our profession by highlighting an inspiring group of emerging leaders who are making a difference in their communities and in our profession. Having received this honor myself in 2013, I know firsthand how meaningful it is to be acknowledged by your peers and the TXCPA community. This issue also highlights TXCPA’s active role in shaping the profession through advocacy and technical expertise. In addition, you’ll find timely insights on estate planning, sustainability assurance standards approved

CHAIR

William J. (Billy) Kelley, Jr., CPA, CGMA

PRESIDENT/CEO

Jodi Ann Ray, CAE, CCE, IOM

EDITORIAL BOARD CHAIR

Derrick Bonyuet-Lee, Ph.D., CPA, CFA, CFP

STAFF

MANAGING EDITOR

DeLynn Deakins, MBA ddeakins@tx.cpa

972-687-8550

800-428-0272, ext. 8550

“TXCPA is strong because of you – your engagement, your expertise and your commitment to excellence.

by IAASB and a practical review of information security guidance for tax professionals – critical knowledge as we prepare for the upcoming busy season.

Finally, don’t miss “What’s Happening Around Texas” for updates from our chapters and members across the state. TXCPA is strong because of you –your engagement, your expertise and your commitment to excellence.

Thank you for all you do. Let’s finish 2025 with momentum and look ahead to a bright new year.

The PCC’s 2025 Priorities: Advising FASB on Private Company Issues

BY JERE SHAWVER, PCC CHAIR

The views expressed in this article are Jere Shawver’s only. Official positions of the PCC and FASB on accounting matters are determined only after extensive public due process and deliberation.

Iam pleased to have the opportunity to provide an overview of the progress the Private Company Council (PCC) has made in 2025 in advising the Financial Accounting Standards Board (FASB) on priority private company financial reporting issues. Before I do that, I will offer a brief background on the PCC and what drives our activities.

The PCC was established in 2012 by the Financial Accounting Foundation (FAF) to advise FASB on private company financial accounting and reporting issues. Members include private company financial statement users including sureties, banks, lessors, and other creditors; controllers, chief financial officers and other accounting-related personnel (preparers), who regularly produce financial statements; and CPAs (practitioners), who provide audit and other forms of assurance on financial statements.

The PCC advises FASB on many projects and evaluates accounting standards for private company alternatives that may not have been considered prior to implementation.

PROGRESS ON CURRENT PCC AGENDA PRIORITIES

The PCC identifies its agenda priorities through a structured and ongoing process.

That process is designed to increase the effectiveness and efficiency of the PCC by regularly assessing the most pressing issues affecting a broad spectrum of private companies. Below, I will address the key efforts that most recently arose through that process.

COMPLETED PROJECTS Credit Losses

The PCC and FASB recently finalized a project addressing challenges encountered when applying the guidance in Topic 326, Financial Instruments-Credit Losses, to current accounts receivable and current contract assets arising from transactions accounted for under Topic 606.

Private company stakeholders told us that estimating expected credit losses for those balances can be costly and complex and that applying the guidance does not result in a materially different estimate of expected credit losses than if the estimate was based on historical loss information.

At its spring 2025 meeting, the PCC made final recommendations to FASB on simplifying and improving the guidance. FASB endorsed and expanded certain recommendations and issued a final Accounting Standards Update in late July 2025.

That guidance provides:

• A practical expedient for all entities related to development

of reasonable and supportable forecasts that are part of estimating expected credit losses, and

• An accounting policy election for entities other than public business entities to consider collection activity after the balance sheet date when estimating expected credit losses.

PRESENTATION

AND DISCLOSURE OF RETAINAGE FOR CONSTRUCTION CONTRACTORS

Topic 606, Revenue from Contracts with Customers, includes guidance on the presentation of a contract with a customer on the balance sheet as a contract asset or a contract liability and related disclosures, but does not include specific guidance on retainage.

Surety private company financial statement users told us that information about retainage is important and that diversity in practice exists in the presentation and disclosure of retainage.

The PCC advised FASB to address this issue through a FASB Staff Educational Paper, which was released in April 2025 and is available on the FASB’s website The paper, which does not change or modify Generally Accepted Accounting Principles (GAAP):

• Clarifies the presentation and disclosure requirements in current GAAP about retainage for construction contractors, and

Amplifying the CPA Voice: TXCPA Committees in Action

TXCPA volunteer committees are more than observers — they’re influencers. Representing CPAs across Texas, these groups actively help shape accounting standards and tax policy by responding to proposals from key standardsetting bodies like the PCC, FASB, IRS, SEC, and more. Their mission? To ensure the CPA perspective is heard loud and clear in decisions that affect the profession nationwide.

Leading the charge are two powerhouse committees:

• Professional Standards Committee (PSC): Reviews every exposure draft from standard-setters to ensure proposed changes reflect real-world practice.

• Federal Tax Policy Committee (FTP): Advocates directly with Congress, the IRS, and Treasury, bringing Texas CPAs’ insights to the heart of federal tax policy.

Together, they keep Texas CPAs at the forefront of national conversationsprotecting the profession and promoting fair, practical standards that serve the public and strengthen our financial system.

• Provides example voluntary disclosures of retainage currently permissible under GAAP that would provide users with more detailed information about contract assets and contract liability balances.

ONGOING PROJECTS Leases

Some private company stakeholders have told the PCC that while the guidance on lease accounting already provides them with some relief, certain areas of the guidance continue to be costly and difficult to apply.

The PCC has a working group comprised of PCC members and members of the AICPA Private Company Practices Section Technical Issues Committee (TIC). At its summer 2025 meeting, the PCC discussed private company stakeholder feedback obtained by the working group over the past year. The working group continues to research potential lease accounting simplifications for private companies.

Debt Modifications and Extinguishments

Research is ongoing to determine whether there are opportunities to simplify the guidance on debt modifications and extinguishments for private companies and make the financial reporting information easier to understand for private company financial statement users.

Preliminary outreach with private company stakeholders has been conducted on:

• Understanding the issues encountered in applying the guidance, and

• Soliciting views on potential solutions.

Summer 2025 Meeting Update

At our Summer 2025 meeting, the PCC prioritized two additional issues for research.

Subjective acceleration clauses. At the meeting, PCC members discussed:

• The pervasiveness of subjective acceleration clauses in private company debt arrangements,

• The frequency with which lenders attempt to enforce the clauses,

• Current accounting practices,

• The complexities in applying the guidance,

• Private company user perspectives, and

• Potential solutions.

The PCC will continue to pursue this area as a current agenda priority. Interest method and determining the effective interest rate. The PCC discussed the staff’s research, including recent outreach conducted on the challenges of applying the interest method guidance in Topic 835, Interest, and potential private company alternatives. The PCC will continue to pursue this area as a current agenda priority.

The PCC also discussed its current agenda priorities at our September 2025 meeting.

LEARN MORE AND GET INVOLVED

The PCC places significant emphasis on engaging private company stakeholders, which is a critical element in carrying out our responsibilities. I appreciate TXCPA’s interest in the PCC’s activities and look forward to engaging with TXCPA members.

Jere Shawver serves as Chair of the Private Company Council. He has over 40 years of experience advising companies on financial reporting, accounting and business matters, across a wide range of industries, including manufacturing and distribution, construction and real estate, higher education, hospitality, government contracting, and technology. He retired in May 2025 as Chief Executive Officer of Baker Tilly US, LLP, where he was responsible for managing the assurance practice and risk management, including the Office of the General Counsel.

More information about the PCC’s work is available by visiting their webpage at www.fasb.org/pcc and in the PCC’s 2024 Annual Report. If you are interested in volunteering to be part of the PCC or on one of their working groups, please contact them at privatecompany@f-a-f.org.

LEGISLATIVE WINS Reshape CPA Licensure and Mobility in Texas

BY KENNETH BESSERMAN, JD, LLM, DIRECTOR OF GOVERNMENT AFFAIRS AND SPECIAL COUNSEL

TXCPA’s advocacy team delivered major wins in the 89th Texas Legislature, reinforcing the organization’s role as a powerful voice for the accounting profession. These victories highlight our leadership in shaping policy and opening new doors for current and future CPAs.

Texas Senate Bill 262/House Bill 1757

A new CPA licensure pathway was introduced to address the profession’s pipeline challenges. In addition to the traditional 150-hour education route, candidates may now qualify by earning a bachelor’s degree in accounting, completing two years of relevant work experience and passing the Uniform CPA Exam. The new law takes effect August 1, 2026.

The Texas State Board of Public Accountancy is responsible for implementing the rules. The State Board adopted rules in September 2025, which became effective on October 10. The rules make significant changes in the accounting courses needed to begin sitting for the Exam and the accounting and business courses needed for licensure. You can find out more about the rules on our website.

Why It Matters

Texas is among the first large states to offer an alternative to the 150-hour rule, reducing financial and time barriers while maintaining high standards. This change could ease workforce shortages and influence similar reforms in other states.

Senate Bill 522/House Bill 1764

The bill allows CPAs licensed in other states to practice in Texas without obtaining a separate Texas license - provided they hold a valid license in good standing, meet education and experience requirements, have passed the Uniform CPA Exam, and agree to comply with Texas laws.

TXCPA’s Role

TXCPA made SB 262/HB 1757 and SB 522/HB 1764 top legislative priorities, collaborating with bill authors Senator Charles Perry and Rep. Angie Chen Button, while actively advocating and educating stakeholders to secure their passage. Our leadership was essential - shaping strong safeguards to protect the public and supporting members with guidance to ensure a smooth transition.

It took effect September 1, 2025, and marks a major step in modernizing CPA practice mobility, moving from state-based mobility to a more modern individual-based mobility system.

Why It Matters

This law modernizes CPA mobility by allowing qualified outof-state CPAs to practice without needing a separate Texas license. It helps address workforce shortages while maintaining high standards, as well as making Texas more responsive to national trends in licensure.

The Momentum Builds

Since the pathways legislation became law, TXCPA has worked closely with the Texas State Board and other stakeholders to shape clear, consistent rules that align with legislative intent. We submitted a formal comment letter that emphasized accessibility and clarity, focusing on coursework, ethics, internships, and experience definitions to minimize disruption and support the profession’s future.

As the new rules are adopted and implemented, TXCPA will continue its advocacy efforts to ensure that the new pathway to licensure provides a true benefit to candidates and the profession.

In

What’s

Happening

Around Texas, we give you highlights of events and activities happening around the state in the TXCPA chapters.

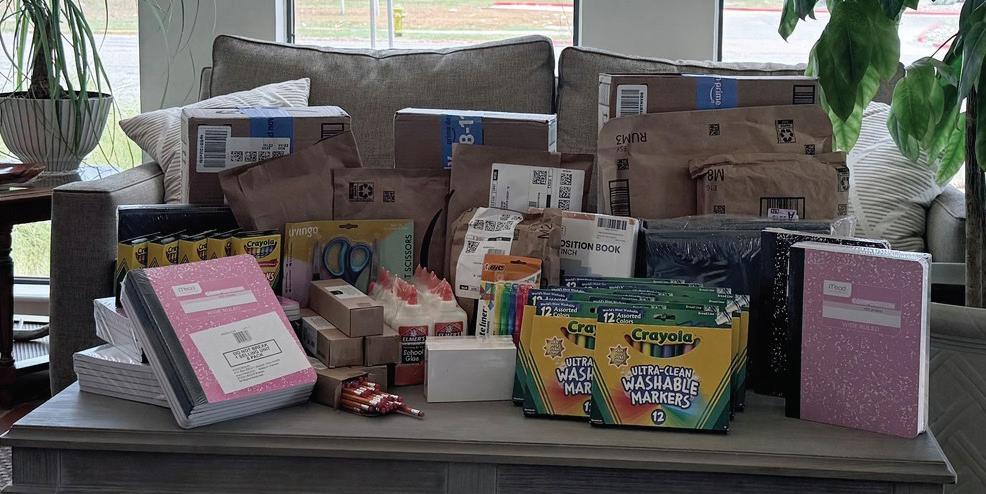

TXCPA Corpus Christi hosted its first School Supply Drive in partnership with United Way of the Coastal Bend’s Operation SOS campaign. Thanks to the generosity of members and community partners, $460 worth of essential school supplies was collected. These donations will benefit over 18,000 students across 43 school districts in the Coastal Bend. This collaborative and meaningful effort ensures students started the academic year prepared and supported, setting them up for success in the classroom.

TXCPA Dallas members enjoyed a unique opportunity to step behind the curtain at the renowned Meyerson Symphony Center. This exclusive event offered a rare look at the artistry and effort that bring world-class performances to life at the center, while showcasing the history and architectural beauty of this Dallas landmark. A huge thanks goes to the Meyerson team for their warm hospitality and for sharing the stories that make this venue such a cultural treasure.

TXCPA East Texas hosted their Leadership Day in August, bringing members together for a dynamic day of learning, networking and professional growth. Participants gained insights from engaging sessions and a thought-provoking leadership panel, connected with peers over lunch, and ended the day with a lively happy hour. Members also gave back to the community through a School Supply Drive. Their generosity helped ensure local students started the year both prepared and empowered to succeed.

TXCPA San Antonio members participated in the National Beta Alpha Psi Competition, a week that combined mentorship, collaboration and academic excellence. The schedule featured a dinner cruise with students, an in-depth Q&A on the TXCPA San Antonio case study and the students’ preparation for competition day. The chapter also hosted its Accounting Educators Mixer, bringing together area professors to network, exchange ideas and learn more about how TXCPA San Antonio can support their students’ success.

Whether you’re hosting a professional development event, organizing a community outreach project, have a leadership meeting, or celebrating a big chapter milestone, we want to hear about it! Share your chapter’s activities with us. Send your photos and event details to Managing Editor DeLynn Deakins at ddeakins@tx.cpa and help us showcase the great work your chapter is doing!

TXCPA Corpus Christi

TXCPA Dallas

TXCPA East Texas

TXCPA San Antonio

November is Accounting Opportunities Month and TXCPA Month of Service!

The CPA profession plays a vital role in building strong communities, businesses and economies. By becoming involved in Accounting Opportunities Month, you have the opportunity to inspire students across Texas to consider a rewarding career as a CPA. Whether you’re a seasoned professional or an educator committed to student success, your participation can make a meaningful impact.

Why get involved?

• Empower students to discover their potential

• Make a lasting impact

• Connect with the community Scan the QR code above to learn more about how you can become

Mark Your Calendar: TXCPA

Midyear Leadership Council Meeting – January 22-23, 2026

Get ready to head to College Station on January 22-23, 2026, for two days packed with insights, advocacy updates and power ful networking. Hear the lat est on issues shaping the profession, learn how TXCPA is championing CPAs statewide, and build connections with peers and leaders from across Texas. Don’t miss it! Visit the Leadership Meetings section at www.tx.cpa

You Don’t Have to Face it Alone: Support Through ACAN

involved in Accounting Opportunities Month. November is also TXCPA’s annual Month of Service, a time when members, firms and companies join forces to create real impact in their communities. From stocking food pantries and leading financial literacy workshops to hosting holiday toy drives with a money-smart spin, there are endless ways to get involved. Reach out to the membership team at membership@tx.cpa or call 800-428-0272 to learn how you can participate.

Discover Your Next Big Opportunity - or Your Next Star Hire - at TXCPA’s Career Center!

Whether you’re ready to take the next step in your accounting or finance career, or you’re looking to bring top-tier talent into your organization, TXCPA’s Career Center is your go-to destination.

Job Seekers: Explore a wide range of openings, apply with ease and build your free Job Seeker Profile to get noticed by employers across Texas.

Employers: Post jobs at exclusive discounted rates - and internships are always free! Connect with qualified professionals who are ready to make an impact.

Getting started is easy. Just log in with your TXCPA credentials at https://careers.tx.cpa/ and unlock a world of possibilities.

Accounting is rewarding - but the stress, deadlines and pressure can take a toll. If you’re struggling, you’re not alone. The Accountants Confidential Assistance Network (ACAN) connects CPAs, candidates and students with peers who understand. Why ACAN?

• Confidential – Protected by Texas law

• Peer Support – Talk to a fellow CPA

• Quick Help – Call or text anytime

• Free – No cost

Services: One-on-one support, referrals, interventions, and Zoom meetings.

You don’t have to carry the burden alone - ACAN is here to help.

TXCPA Member Insurance Program: Smart Protection, Exclusive Benefits

As a TXCPA member, you have access to top-tier insurance plans designed to protect your family, career and peace of mind. With trusted providers and member-only rates, these benefits are tailored to fit your professional lifestyle.

Smart coverage. Exclusive pricing. Real peace of mind. Explore your TXCPA insurance options today and take a confident step toward protecting your future. Scan the QR code or go to https://txcpainsure.org/

Introducing AcctoFi

Every Step Counts. Especially the Next One.

You’re not standing still — and neither are we.

Introducing AcctoFi, the rebranded TXCPA Accounting Education Foundation and your next step in professional education.

With support for students, educators, and accounting and finance professionals, we deliver the knowledge and training to move you forward. Whether you’re climbing, pivoting or just getting started, AcctoFi gives you the tools to step up and stand out.

Take the next step at AcctoFi.com

From the team behind TXCPA. Built for professionals like you.

TXCPA’s 2025

RisingStars

BY DELYNN DEAKINS TODAY’S CPA MANAGING EDITOR

TXCPA’s Rising Stars Program shines a spotlight on the next generation of leaders - CPA members 40 and under who are already making a big impact. From driving change in the accounting profession to serving their communities with passion, these individuals embody what it means to lead with purpose. After careful review, our selection committee has chosen 16 exceptional honorees for 2025. We’re proud to introduce this year’s Rising Stars, listed alphabetically.

Emily Baller, CPA

Senior Manager

Weaver and Tidwell LLP

Permian Basin

Aarika Anderson, CPA

Atchley & Associates LLP

Aarika Anderson is making waves in the accounting profession, already having a remarkable impact through her dedication and leadership within TXCPA Austin. Even before earning her CPA license in February 2024, she demonstrated her commitment by serving on the chapter’s Oversight Council, ensuring the voices of students and candidates were heard in key discussions. Her insights helped spotlight the challenges and opportunities facing those entering the field.

She also played a pivotal role in Leaders Emerging in the Accounting Profession (LEAP), chairing the group and leading events that fostered connection, growth and professional development for early-career accountants. Now a licensed CPA, Aarika continues to grow her involvement in the organization. With her passion, vision and drive, she is poised to become one of the profession’s most influential young leaders.

Emily Baller has a true passion for developing the next generation of CPAs. She considers one of her most significant business achievements to be enhancing her firm’s audit internship program, where she served as mentor and coach for new interns. Through weekly group meetings and one-on-one check-ins, Emily created a supportive environment that encouraged collaboration, problem-solving and professional growth. She guided each intern in mapping out their CPA journey. The result: stronger performance, lasting confidence and full-time offers for every intern she mentored.

Beyond her firm, Emily’s passion extends to TXCPA Permian Basin, where she helped create the Pathway to CPA program for University of Texas Permian Basin students. By developing step-by-step resources, timelines and application tools, she has made the road to licensure clearer and more accessible for aspiring CPAs.

Preston Branch, CPA

Instructor of Accounting West Texas A&M University Panhandle

When Preston Branch changed his major from marketing to accounting, he set a bold goal: to one day own a CPA firm with his name on the door. He began building toward that dream by gaining valuable experience at CMMS, CPAs and LPT CPAs + Advisors, where he developed the knowledge, skills and confidence needed to succeed. Along the way, he was guided by mentors who generously shared their tax knowledge and expertise.

In 2022, Preston embraced a new opportunity in academia, joining West Texas A&M University as an accounting instructor, teaching tax courses. While he found deep fulfillment in teaching, he realized he missed the direct client interaction. That insight led him to launch Branch CPA PLLC in January 2023. Today, Preston successfully balances both roles - helping clients navigate tax challenges and students prepare for their futures.

Heath Cochran, CPA, CVA

Partner

Myatt & Young CPAs LLC

Panhandle

Heath Cochran is a Partner at a Canyon, Texas firm whose career blends technical expertise with a strong commitment to client service. After earning his CPA license in 2015, he continued to advance professionally, achieving the Certified Valuation Analyst (CVA) designation in 2019 - positioning him as one of only a handful of professionals in the Texas Panhandle licensed to provide business valuation services. Heath is also a committed leader within TXCPA Panhandle, having served on the board and as chapter President. His leadership helped guide the organization through key transitions and periods of growth. Beyond his professional contributions, Heath serves on the board of Fill With Hope/Canyon Snack Pak 4 Kids, an organization that works to ensure children in the Canyon Independent School District have access to nutritious food and the support they need to thrive.

Priyanka Desai, CPA

Partner

Adamson & Company LLC

Corpus Christi

Priyanka Desai is an extraordinary leader whose impact is felt across her firm, profession and community. At just 29, she became a partner at Adamson & Company, LLC, where she is recognized for her expertise, mentorship and commitment to developing future CPAs. As President of TXCPA Corpus Christi, she strengthened member engagement and expanded professional development by introducing innovative CPE opportunities such as Sunrise courses and extended luncheons. She has also chaired the CPE Committee and serves on multiple chapter committees, and she is a visible advocate for the profession through mentorship, advocacy and education outreach.

In the community, Priyanka champions charitable causes, including the American Heart Association’s Heart Walk and the “Counting on Santa” fundraiser. With her professional achievements, passion for service and dedication to lifting others, Priyanka Desai stands out as a Rising Star.

Anette Flores first became involved with TXCPA San Antonio by volunteering with the chapter’s annual Funlympics. Her dedication led to an invitation to serve as a judge for Jr. Duel, a financial literacy competition for high school students hosted by the chapter. Inspired to do more, Anette took on leadership roles with the Accounting Careers & Education Committee, eventually becoming Chair and earning the Outstanding Committee Chair Award. Her journey with TXCPA San Antonio has only grown - she now serves as the Chapter President and is a member of the TXCPA Leadership Council and Emerging Professionals Advisory Board.

Beyond her work in accounting, Anette has embraced motherhood and a personal journey of fitness and wellness, completing her first 5K in personal record time and currently training for a Hyrox competition. Her commitment to balance and growth makes her a true inspiration.

Robert (Logan) Kendrick, CPA, ABV

Shareholder - Audit Partner

Thompson Derrig & Craig PC

Brazos Valley

Logan Kendrick joined Thompson Derrig & Craig PC in 2016 and became a shareholder in 2021, focusing on the firm’s audit practice. Known for his big-picture thinking and leadership, he has been deeply involved in TXCPA Brazos Valley, serving in several roles, including President. Logan helped the chapter create impactful events that significantly boosted student engagement at Texas A&M.

Logan also collaborated with accounting professors to develop meaningful content and launched a panel featuring CPAs from industry, public accounting and government, giving students valuable insight into the many paths within the profession and the CPA journey. He and his wife have four children and are active in their church. At home, Logan enjoys coaching his kids’ sports teams and tending their humble family farm in Franklin with chickens, bees and soon a milk cow.

Nicholas Larson, CPA Owner

Larson CPA LLC

Fort Worth

Nicholas Larson has built a career defined by leadership, technical excellence and service. As owner of Larson CPA PLLC, he provides trusted tax and bookkeeping services to clients across the Dallas-Fort Worth Metroplex. His background includes experience at both national and local CPA firms, as well as serving as an Internal Revenue Agent with the IRS, underscoring his expertise and commitment to professional integrity.

A dedicated member of TXCPA and AICPA, Nic actively supports fellow CPAs and champions the profession to the next generation. His passion for service extends into the community, where he serves on the Board of Trustees and Finance Committee for Hill School of Fort Worth, advancing education and financial literacy. He exemplifies the qualities of a leader making a lasting impact on both the profession and his community.

Jeff Lindenmoyer, CPA

Audit Manager

Gollob Morgan Peddy PC

East Texas

Nhu Le, CPA

Audit Associate

Doeren Mayhew Houston

Nhu Le’s leadership journey with TXCPA Houston began as a Student Auxiliary officer, where she served for three years and capped her service as President. Always proactive, she earned her CPA license in March 2023 and quickly stepped into new leadership roles, including Chair of the Student Auxiliary Steering Committee, Vice Chair of the Diversity & Inclusion Committee, and active member of CPAs Helping Schools, the Scholarship Extravaganza and Membership Committees. She also encouraged her employer to support TXCPA Houston’s philanthropic programs and enroll at least one person in the leadership program each year.

On the Scholarship Extravaganza Committee, Nhu helped plan and execute the Gala in 2023 and 2024, boosting donations and expanding scholarships for accounting students. These efforts strengthened the CPA pipeline while honoring leaders in the profession, work she finds deeply rewarding.

Jeff Lindenmoyer has proven to be an invaluable asset to TXCPA East Texas, where his passion for advancing the profession is clearly evident through his service on the Golf Committee, Young and Emerging Professionals group and the Board. His enthusiasm for connecting people and fostering engagement has left a lasting impact on the chapter.

Jeff’s drive for excellence traces back to his collegiate football career at Ave Maria University, where he helped launch the inaugural program. He earned Second Team and later First Team All-American honors and was inducted into the university’s inaugural Hall of Fame. Football taught him accountability, discipline and how to lead without ego, which continues to shape how he serves his profession and community. For Jeff, achievement lies not in recognition, but in giving his best and lifting others along the way.

Yamely Medina, CPA

Partner

Garza & Morales LC Rio Grande Valley

Yamely Medina has built an impressive career marked by leadership and service to her community. A partner at Garza & Morales in McAllen by age 27, she has also played a key role in TXCPA Rio Grande Valley as Vice President and Student Outreach Committee Chair. Passionate about inspiring the next generation, Yamely has helped to expand outreach from elementary through high school, organizing classroom presentations, career fairs and a general assembly of 200 business students at a local high school.

Yamely has shared her expertise directly with students through presentations across the region. In addition, she serves on the University of Texas Rio Grande Valley School of Accountancy Advisory Board, strengthening ties between the chapter and the university. For her, bridging aspiring business leaders with the CPA profession is a highly meaningful achievement.

Spencer Payne, CPA Associate Director

The Siegfried Group Dallas

Spencer Payne quickly distinguished himself as a leader within TXCPA Dallas, serving on the Leadership Development Academy Steering Committee, including a term as Chair, as well as the Young Professionals Group Committee and Chapter Advisory Board. His career has been equally dynamic. In 2023, Spencer was selected by The Siegfried Group’s executive team to establish their Dallas presence as the firm’s first Associate Director in Client Relationships. After relocating, he built connections, expanded the client base and laid the foundation for Siegfried’s first Dallas office, which officially opened in March 2025.

Spencer also gives back to the community through the BYU Management Society, where he helped lead the most successful Charity Golf Tournament in the chapter’s history, raising record scholarship funds for DFW students. For him, leadership is about purpose, service and creating opportunities for others.

Rising Star Nominations Opening Soon!

Do you know a CPA who’s making a difference - whether through bold leadership, community impact or active involvement with TXCPA? Now’s your chance to put them in the spotlight! Nominations are open to everyone, but nominees must be TXCPA members. Keep an eye on your TXCPA updates for all the details on how to submit your nomination and help us celebrate the next generation of leaders.

Carl Reis, CPA

Tax Manager

CAPTRUST

San Antonio

Carl Reis first became involved with TXCPA San Antonio through Young Accounting Professional social events, finding enjoyment in meeting peers and students while sharing experiences with like-minded professionals. As Chair of the Young Accounting Professionals, he brought strong creativity to event planning. As an advocate for the profession, Carl has encouraged students to pursue the CPA Exam, led discussions at the Accounting Careers Workshop and even purchased tickets for students to attend chapter events to ensure they had a seat at the table.

Known for his positive energy and follow-through, Carl also takes on challenges outside the office. His most significant personal achievement is completing a full marathon, a goal that demanded months of early runs, steady training and resilience. Crossing the finish line in under four hours, he proved to himself the power of perseverance.

April Roxana Samaniego, CPA, MAcc

Tax Partner

Pena Briones McDaniel & Co PC El Paso

April Samaniego has been a driving force in TXCPA El Paso, serving in multiple officer roles - including President - and leading the Young CPA Committee in professional and philanthropic initiatives. A Partner at Peña Briones McDaniel & Co., she achieved this milestone before turning 30, a success she treasures not just for the title, but for the growth, resilience and leadership it represents. With extensive tax and accounting experience, April continues to lead by example, encouraging students and young professionals to excel in the field.

April volunteers annually with Rebuilding Together, presents Accounting Career Education programs at area schools and has spoken at a Professional Development Workshop for college students. Known for her energy and commitment, April believes investing in the next generation is among the most meaningful contributions a CPA can make.

David Twu, CPA, JD Commercial Banker Comerica Bank

Dallas

David Twu has become a trusted leader within TXCPA Dallas, serving as Chair of the Business & Industry Committee, where he elevated its profile with a strong lineup of CPE and social events. He also contributes his time and talent on the CPE Council and the Sponsorship Committee, and represents the chapter on TXCPA’s Leadership Council. Known for his enthusiasm and commitment, David is an invaluable asset to the Society.

Beyond TXCPA, David is deeply committed to serving the community that shaped him. As Texas Chair of Comerica Bank’s Asian American Pacific Islander Business Impact Team, he leads a committee spanning North and South Texas, dedicated to supporting local businesses and families. Through this work, he has helped organize youth camps and served on nonprofit boards - efforts that reflect his passion for leadership, service and community impact.

Eric Wilson, CPA

Director

Your Part-Time Controller, LLC

Dallas

Eric Wilson is a professional services leader with a passion for mission-driven work and a talent for business development. Since launching the Dallas/Fort Worth office of Your Part-Time Controller, LLC (YPTC) in August 2022, he has grown it into a thriving team that serves dozens of nonprofit clients across North Texas. His relationship-based approach positions YPTC as a trusted partner, earning client loyalty through responsiveness and high-quality service.

Outside the firm, Eric has served on TXCPA’s Nonprofit Organizations Conference Planning Committee and is a founding board member of Fort Worth STEAM Academy. His financial expertise has helped advance the school’s mission to provide high-quality Science, Technology, Engineering, Arts, and Mathematics (STEAM) education. He is excited about the future of the academy and the opportunities it will provide for students in East Fort Worth.

IAASB Approves New Standard on Sustainability Assurance

BY ASHLEY BENTLEY, ED.D., CPA; LANA BECKER, ED.D., CPA (INACTIVE); AND EMILY COKELEY, PH.D., CPA

As more and more companies add environmental, social and governance (ESG) reporting to their financial reporting, there is an increasing demand for assurance of ESG information. Even companies that are not subject to mandatory ESG reporting often voluntarily provide sustainability information to meet the demands of various stakeholders.

Although the social (labor practices, human rights, stakeholder relationships) and governance (composition of board, executive compensation, transparency, anti-corruption) practices of a company are important to investors and other stakeholders, it is the practices related to a company’s stewardship of the natural environment (greenhouse gas emissions, use of renewable energy, management of resources) that are most commonly reported.

The current sustainability landscape reflects a movement toward mandatory reporting for many companies. On a global basis, the IFRS Foundation, known for its global accounting standards as issued by the International Accounting Standards Board (IASB), has now added a standard-setting body for ESG reporting known as the International Sustainability Standards

Board (ISSB, 2025). The ISSB is developing global standards for sustainability reporting that become mandatory in those jurisdictions where adopted and are focused on the information needs of investors.

The IFRS Foundation is collaborating with the Global Reporting Initiative (GRI) to maximize the interoperability between the ISSB standards and the world’s most commonly used standards for voluntary sustainability reporting. Furthermore, the ISSB has embraced the widely used reporting framework developed by the Task Force on ClimateRelated Financial Disclosures (TCFD), as well as the 77 industry standards developed by the Sustainability Accounting Standards Board (SASB) as discussed in the article “Understanding Sustainability Accounting Standards Board Standards” in the March/April 2025 issue of Today’s CPA

The most stringent mandatory ESG disclosures are currently found in the European Union. The EU’s Corporate Sustainability Reporting Directive (CSRD) was set forth by the European Financial Reporting Advisory Group (EFRAG) and is applicable to both European-based entities and potentially over 3,000 U.S. based companies that conduct business in Europe (Abramson, 2024). As recently as February 2025, the European Commission proposed

a series of amendments to reduce the requirements for ESG reporting and due diligence under CSRD; thus, mandatory reporting in the EU and affected U.S. companies remains a fluid issue. With regard to mandatory reporting in the United States, the SEC approved The Enhancement and Standardization of Climate-Related Disclosures for Investors Rule in March 2024 (SEC, 2024). Although the rule has been temporarily halted due to ongoing legal challenges, as well as a change in leadership at the SEC, its pending implementation would result in mandatory climate-related disclosures for SEC registrants. (See “SEC Adopts ClimateRelated Disclosures” in the September/ October 2024 issue of Today’s CPA). The future direction for mandatory climaterelated disclosures in the U.S. remains uncertain at this time.

Although a great deal of uncertainty exists in the current ESG landscape regarding mandatory ESG reporting, companies continue to be pressured to provide ESG information from investors whose focus has turned to the firm’s long-term value creation. Today’s broad array of other stakeholders, including consumers, employees and communities, expect a company to be transparent about its ESG practices and its overall commitment to sustainability.

INCREASED DEMAND FOR SUSTAINABILITY ASSURANCE

As more companies report on sustainability, the demand for third-party assurance is rising. Standard-setting bodies now require it, and stakeholders expect it to validate management’s claims. Assurance enhances credibility and helps prevent misleading practices aimed at appearing more environmentally responsible than reality (i.e., greenwashing). Like financial statements, investors and other key stakeholders are looking for validation of management’s claims within the sustainability reports.

One challenge faced by practitioners in the assurance space is lack of guidance. For some time, practitioners have been trying to apply a combination of financial attestation procedures to nonfinancial information, characterized by metrics and measurements other than dollars. The vast majority of global audit firms have been using ISAE 3000 (Revised), Assurance Engagements Other than Audits or Reviews of Historical Financial Information and ISAE 3410, Assurance Engagements on Greenhouse Gas Statements, both issued by the International Auditing and Assurance Standards Board (IAASB) for sustainability assurance work.

In the United States, practitioners have also followed guidance offered by AICPA’s attestation standards, such as AT-C section 105, Concepts Common to All Attestation Engagements, and AT-C section 201, Review Engagements. Although broad in scope, these standards lack clear guidance tailored to sustainability assurance, even as the need for standardization is more important than ever.

KEY PROVISIONS OF ISSA 5000

In September 2024, the IAASB approved International Standard on Sustainability Assurance (ISSA) 5000. Formal publication of the standard occurred in November 2024, following the certification by the Public Interest Oversight Board (PIOB). Implementation of ISSA 5000 will be effective for sustainability assurance engagements for periods beginning on or after December 15, 2026 (early application is permitted).

This standard is the first comprehensive guidance issued specifically for sustainability

Sustainability

Assurance in the United States

Current Market

• Demand for sustainability reporting and assurance is growing in the United States and globally.

• Only 23% of sustainability assurance work in the United States is being performed by CPAs.

• Most is done by non-CPAs, such as consultants and engineers.

Prime Opportunity for CPAs

• CPAs can build on existing audit skills from traditional engagements.

• Adapt these skills to the modern ESG era.

• Stakeholders are now interested in long-term organizational value, not only current financial position.

assurance. Designed to provide a standard framework for verifying sustainability information, ISSA 5000 will replace ISAE 3000 (Revised). ISAE 3410 will continue to be used, alongside ISSA 5000, when a separate conclusion on greenhouse gas emissions is required (IAASB, 2024). Supplemental materials and an implementation guide were released by the IAASB in January 2025 to assist practitioners.

The IAASB intentionally created ISSA 5000 to be flexible, broad and framework neutral. It is a principles-based standard that applies to all ESG information (i.e., social and governance issues, as well as environmental), prepared using any of the numerous sustainability reporting guidelines or frameworks previously discussed (Anderson, 2024a). ISSA 5000 can be adapted to organizations of any size and across most industries. It can be used by both accounting and non-accounting professionals and applied to both limited and reasonable assurance engagements (Anderson, 2024a).

Much like reviews, limited assurance engagements are less extensive and offer a lower level of assurance. The report indicates that the assurance provider is unaware of any material modifications that need to be made (i.e., negative assurance). Reasonable assurance:

• Is the highest level of verification of ESG data,

• Requires that the auditor perform more comprehensive audit procedures and critically evaluate source documentation.

The report states the information is in accordance with the criteria set forth by the selected reporting standards and free from material misstatement (i.e., positive assurance).

The flexibility aspect of the ISSA 5000 is important, as reporting and assurance requirements continue to evolve. For the early reporting years, only limited assurance is mandatory. However, requirements will gradually move to reasonable assurance for the global, EU and U.S. mandatory reporting standards.

Many of the provisions within ISSA 5000 are similar to those found in the current literature on conducting assurance of financial information. However, there is one new element that should be of significant interest to assurance providers.

DOUBLE MATERIALITY

One of the key features of ISSA 5000 is the inclusion of double materiality (Anderson, 2024b). While this concept is not new to companies subject to the European Union’s CSRD (where a double materiality assessment is required), it may be a novel concept to companies in other parts of the world, including the United States.

Similar to materiality that is considered in audits of financial statements, double materiality considers the effects of sustainability matters on the financial reporting of the company (financial materiality). Financial materiality is what accountants and auditors have traditionally known but is specifically applied

to how sustainability matters may impact the financial performance of the company (“outside in”). This might include environmental, social and governance expenses already incurred, but could also include actual or potential fines, fees or other costs resulting from governmental sanctions, as well as the loss of customers from poor labor or other ESG practices, and effects of severe weather events.

The second side of double materiality (impact materiality) considers the effects the company has on the physical and social environment of any external stakeholder (“inside out”). It considers the impact of a company’s sustainability activity (or lack thereof) on the environment and people surrounding the company, both locally and globally.

Impact materiality, while lesser known to most firms and assurance providers, requires a similar level of consideration to financial materiality in sustainability assurance. Most importantly, a sustainability issue needs to be material from only one of the two perspectives (“outside in” or “inside out”) to require disclosure.

Paragraph A306 of ISSA 5000 notes that not all reporting frameworks require the use of double materiality, but if the selected reporting framework requires the company to consider double materiality, the assurance provider is required to assess double materiality while also verifying that no significant sustainability areas have been overlooked by the organization in its own materiality assessment.

Sustainability assurance relies heavily on qualitative data and support, and the verification of some aspects of impact materiality can come as a challenge, as significant practitioner judgment regarding the nature and extent of assurance evidence is required. As previously stated, ISSA 5000 provides the framework for sustainability assurance using any reporting framework, but leaves the practitioner significant latitude to determine the specific procedures to be used in the assurance engagement.

WHAT’S NEXT FOR SUSTAINABILITY ASSURANCE IN THE UNITED STATES

Will the United States follow suit with its own set of ESG-specific assurance standards?

AICPA’s Auditing Standards Board’s (ASB) Sustainability Task Force has been charged with reviewing ISSA 5000 and evaluating the implications of the new standard on its sustainability guidance. The task force is working to determine

• First global standard for sustainability assurance

• Replaces ISAE 3000 (Revised)

• ISAE 3410 still applies for GHG conclusions

Scope:

• Principles-based, flexible, frameworkneutral

• Covers all ESG topics

• Usable across industries and by both accounting and non-accounting professionals

New Key Feature - Double Materiality:

• Financial materiality (“outside in”) → how sustainability issues affect the company’s financial performance

• Impact materiality (“inside out”) → how the company affects the environment and society

• Topic material if it meets either test, not both

Assurance Levels:

• Limited assurance → less extensive, negative assurance

• Reasonable assurance → highest level, more procedures, positive assurance

Implementation:

• Starts with limited assurance

• Gradually moving to reasonable assurance for global/EU/U.S. requirements

what revisions to the current attestation standards are necessary for practitioners providing assurance on sustainability information under these standards. The ASB is planning to issue an exposure draft to seek comment on proposed revisions to standards, including sustainability specific content in the AT-C standards.

As demand and mandates for sustainability reporting increase globally and domestically, this opens up significant opportunities for assurance providers. Currently, only 23 percent of sustainability assurance work in the United States is being performed by CPAs (IFAC, 2024). The vast majority of this type of assurance is provided by non-CPAs, such as environmental specialists within consulting and engineering firms.

Conversely, 58 percent of global sustainability assurance work is performed by CPA firms (IFAC, 2024). CPAs in the United States have a prime opportunity to build upon the audit skills that have already been developed for traditional engagements and adapt these skills to this contemporary ESG era where stakeholders are interested in the long-term value of an organization, not only the current financial position.

References

Abramson, K. (2024, December 4). Ensuring CSRD compliance: Why U.S. companies must act now. Forbes. https:// www.forbes.com/councils/forbestechcouncil/2024/12/04/ ensuring-csrd-compliance-why-us-companies-must-actnow/

Anderson, K. (2024a). What is ISSA 5000? https://greenly. earth/en-us/blog/company-guide/what-is-issa-5000 Anderson, K. (2024b). Our Guide to the CSRD’s Double Materiality Assessment https://greenly.earth/en-us/blog/ company-guide/our-guide-to-the-csrds-double-materialityassessment

LANA BECKER, ED.D., CPA (inactive), is an Associate Professor and the Dr. Martha Pointer Faculty Fellow in the Department of Accountancy at East Tennessee State University. She can be reached at becker@etsu.edu

ASHLEY

BENTLEY, ED.D., CPA, is an Assistant Professor and the Blackburn, Childers, and Steagall Faculty Fellow in the Department of Accountancy at East Tennessee State University. She can be reached at bentleyab@etsu.edu

EMILY COKELEY, PH.D., CPA, is an Assistant Professor in the Department of Accountancy at East Tennessee State University. She can be reached at cokeley@etsu.edu

International Auditing and Assurance Standards Board (IAASB). (2024). International Standard on Sustainability Assurance 5000, General Requirements for Sustainability Assurance Engagements. https://www.iaasb.org/publications/ international-standard-sustainability-assurance-5000-general-requirements-sustainability-assurance International Federation of Accountants (IFAC). (2024). The State of Play: Sustainability Disclosure & Assurance 20192022, Trends &Analysis. https://www.ifac.org/knowledgegateway/audit-assurance/publications/state-play-sustainability-disclosure-assurance-2019-2022-trends-analysis International Sustainability Standards Board (ISSB). (2025). About the International Sustainability Standards Board https://www.ifrs.org/ groups/international-sustainability-standards-board/ PwC. (2022). Global Investor Survey 2022. https://www. pwc.com/gx/en/issues/esg/ global-investor-survey-2022. html

U.S. Securities and Exchange Commission (2024, March 6). SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors. https://www. sec.gov/newsroom/pressreleases/2024-31

TXCPA’s Upcoming CPE Programs

2025 CPE Expo Conference:

DFW | Nov. 13 - 14

San Antonio | Nov. 17 - 18

Houston | Dec. 4 - 5

Virtual | Dec. 15 - 16

Federal Tax Updates:

Tyler | Dec. 8

For Individuals - Victoria | Dec. 11

For Businesses - Victoria | Dec. 12

Amarillo | Dec. 15

For Individuals - San Antonio | Jan. 5

For Businesses - San Antonio | Jan. 6

For Individuals - Houston | Jan. 8

For Businesses - Houston | Jan. 9

For Individuals - Dallas | Jan. 12

For Businesses - Dallas | Jan. 13

Fort Worth | Jan. 14

Midland | Jan. 16

Beaumont | Jan. 26

Corpus Christi | Jan. 30

Tax Update Webcast Programs:

Federal Tax Update for Individuals | Jan. 12

Federal Tax Update for Business | Jan. 13

Best Individual Income Tax Update | Jan. 19

Best S Corporation, Limited Liability and Partnership Update | Jan. 20

Free CPE Webcasts for Members:

Your membership gives you access to 20+ hours of FREE CPE, with fresh opportunities added year-round. Don’t miss out.

TXCPA Passport:

The TXCPA Passport is your one-year, on-demand CPE subscription - offering 100+ hours, key topics, flexible course lengths, and fresh content year-round.

View the complete schedule, learn more and register now in the Education area of our website at tx.cpa or call the TXCPA staff at 800-428-0272 for assistance.

The Texas Society of CPAs is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.nasbaregistry.org.

TXCPA Thanks Strategic Partners

Goodman Financial and 8am CPACharge

TXCPA extends sincere thanks to Goodman Financial and 8am CPACharge for their generous support as Strategic Partners. Their investment helps advance our mission, strengthen the CPA profession and enhance member value.

Celebrating more than 35 years, Goodman Financial provides high-networth individuals, families and business owners with personalized investment management and financial planning. As independent, fee-only fiduciaries, they prioritize client interests with a collaborative, transparent approach.

Grow Your Business with TXCPA

8am CPACharge offers modern, secure payment solutions tailored for accounting professionals. Their technology simplifies online payments and provides robust tools for reporting, reconciliation and compliance - helping CPAs manage transactions efficiently and focus more on client service.

TXCPA Partner Programs offer businesses customized sponsorships that boost visibility, brand recognition, and direct access to the accounting and finance community in Texas.

Learn more about partnership and advertising opportunities at tx.cpa/news-publications/advertise.

Top 10 Estate Planning Topics in Texas in 2025: A Scholarly Perspective

BY BRAD WIEWEL, JD, AND ZACH WIEWEL, JD, LL.M. (TAX)

Estate planning remains a critical component of financial and legal well-being, particularly in a dynamic jurisdiction such as Texas. Recent legislative changes, economic shifts and evolving family structures have significantly impacted the landscape of estate planning. This article explores 10 essential topics in Texas estate planning, providing a scholarly perspective that integrates both statutory frameworks and current best practices.

1 The Changing Federal Estate Tax Exemption

One of the most pressing concerns for Texas CPAs in 2025 is the anticipated change in the federal estate tax exemption. The current exemption of $13.61 million per individual is slated to sunset after December 31, 2025. Starting in 2026, under the One Big Beautiful Bill Act (OBBBA), the exemption will increase to $15,000,000 and be indexed for inflation in future years. This modest increase is somewhat disappointing because early reports showed a desire by Republicans to abolish this tax altogether.

The gift and generation-skipping taxes will also have these exemption amounts. It bears remembering, however, that President Trump will not be the president in a little over three years. Whoever takes over the Oval Office after Mr. Trump may be inclined to lower these exemptions dramatically. By waiting to see what happens then, wealthy clients may lose some of their ability to move appreciation out of their estates. And three years of appreciation on many asset classes can be significant.

CPAs should consider prioritizing strategies such as lifetime gifting, irrevocable trusts and valuation discounts to mitigate this potential tax problem. Such proactive planning is wise and prudent.

2 Revocable Living Trusts and Probate Avoidance

Although Texas probate is often considered more streamlined than in other states, it can still be expensive, time consuming and public, so public in fact that some counties, like Travis and Hayes post the probated wills on their open websites.

As a result, revocable living trusts have gained popularity as a means of preserving privacy, avoiding probate and ensuring the seamless management of assets during incapacity. These trusts are particularly useful in cases involving multiple properties across state lines, a common scenario in Texas due to oil and mineral interests.

They are also superior planning tools during a client’s mental incapacity. The continued relevance of revocable trusts underscores the importance of individualized and customized estate planning strategies.

3 Digital Assets and Fiduciary Access

The rapid growth of digital assets - including cryptocurrencies, online investment accounts and social media profiles - has introduced new complexities into estate planning. Texas has adopted our own version of the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA), which governs fiduciary access to a decedent’s digital property. However, challenges remain regarding password management, two-factor or three-factor authentication, and platform-specific policies.

CPAs should advise clients to inventory their digital assets and include explicit authorizations in estate documents to prevent the unintentional loss of sentimental or valuable digital property, including cryptocurrency.

4 Blended Families and Inheritance Disputes

The increasing prevalence of blended families presents unique challenges in estate planning. Texas’ community property system complicates matters when spouses bring separate property into the marriage and when couples move here from states that do not normally provide for community property. Well-drafted estate planning documents - such as wills and trusts - are critical to ensure the equitable distribution of assets among biological children, stepchildren and surviving spouses.

Without clear instructions, disputes under the Texas Estates Code can lead to costly and protracted litigation. Open communication and clear, comprehensive documentation are vital to helping to preserve family harmony.

5 Special Needs Planning

Planning for beneficiaries with disabilities requires specialized instruments to maintain eligibility for means-tested government benefits while providing supplemental financial support. Special Needs Trusts (SNTs) are essential tools that allow beneficiaries to receive additional resources without jeopardizing their Medicaid or Supplemental Security Income (SSI) eligibility.

Texas CPAs must be adept at directing their clients who have children or grandchildren with special needs to expert attorneys who can navigate federal and state regulations to ensure that these special needs trusts comply with all applicable requirements. The careful selection of trustees is also crucial to the effective administration of these complex trusts.

6

Non-Married Couples

Non-married couples present a new spin on estate planning. While the focus formerly was on same sex couples, the Supreme Court has affirmed those marriages. Now, more and more couples are forgoing marriage and live with their significant others for years.

The challenges this creates are too many to list here. Common law marriage in Texas should be addressed, however. It can inadvertently arise from an unwritten agreement to be married, which is accompanied by holding each other out as spouses and cohabitating. Unfortunately, Texas does not define how long someone must cohabitate and theoretically, that could be as short as one night. And once someone is common law married, they are married in all respects and must get divorced to sever that relationship.

One tax pitfall to not marrying is the lack of unlimited marital deduction for gift and estate tax purposes. Another is the inability of nonmarried people to combine both of their respective estate and gift tax exemptions; married couples can. A further one is that a non-married beneficiary cannot do a post-death rollover of a retirement account and, therefore, minimum distributions increase; the new Secure Act will also push the distributions out in 10 years, rather than over the lifetime of the surviving spouse. Thus, the minimum distributions for a spouse are lower and can be taken over a potentially much longer period of time.

7 Management of Oil, Gas and Mineral Interests

Texas’s wealth of oil, gas and mineral interests presents distinct estate planning challenges. These assets often involve complex ownership structures - such as royalties, working interests and surface rights - that require specialized knowledge of title law, lease agreements and environmental liabilities.

Estate plans must address succession, valuation and potential partition disputes among heirs. Given the volatility of the energy sector, planners should review these plans regularly to ensure that they continue to align with the client’s financial goals and market realities.

Good asset protection planning can also entail separating the mineral interest from the surface, which can protect the minerals from a lawsuit created by an accident that occurs on the surface.

8 The Corporate Transparency Act and Business Entities

The Corporate Transparency Act (CTA) became effective on January 1, 2024, and requires disclosure of beneficial ownership information for many closely held entities. Texas estate planners often utilize limited liability companies (LLCs), family limited partnerships and closely held corporations in their strategies. According to the Treasury Department, compliance with the CTA is now on hold, but no one knows for how long. This law has not been repealed and again, a new administration could restart the compliance and penalty process at its discretion.

Integrating CTA reporting into entity planning to ensure future legal compliance is a “gut decision” that CPAs should advise their clients of and then make sure that whatever the client decides to do regarding registration is confirmed by the CPA to the client so it is clearly the client’s decision, not the CPA’s.

9 Pet Trusts and Animal Welfare

Increasingly, Texans view pets as integral family members whose care should be included in estate plans. Texas law recognizes pet trusts, allowing individuals to set aside funds and designate caregivers for their animals. These trusts can specify veterinary care, food preferences and other welfare considerations. Incorporating pet trusts into estate documents reflects a holistic approach to planning, consistent with modern understandings of animal welfare.

10 Incapacity Planning and Elder Law Considerations

With an aging population, planning for incapacity has become a central focus of estate planning. Documents such as Revocable Living Trusts, Durable Powers of Attorney, Medical Powers of Attorney, Living Wills and HIPAA Releases are essential for designating decision-makers and expressing health care preferences. Without these instruments, families may face burdensome guardianship proceedings under the Texas Estates Code, which, frankly, is the absolute worst result for the family.

Additionally, elder law considerations, including Medicaid eligibility and long-term care planning, demand careful coordination to protect both personal autonomy and financial security.

Navigating Modern Estate Planning: The CPA’s Critical Role

Estate planning in Texas has become increasingly complex, reflecting changes in federal law, state statutes, the courts, regulators, technology, and family dynamics. The 10 topics examined in this article highlight the multifaceted nature of modern estate planning and the need for individualized, comprehensive strategies.

For Texas CPAs, mastery of these topics is essential to helping clients address the critical issues they are concerned about and preserve their legacies. These are, of course, concepts that neither artificial intelligence nor TurboTax® are going to recommend. Only an experienced and compassionate CPA is uniquely positioned to assist clients in achieving their desired estate planning dreams and visions.

BRAD WIEWEL, JD, is a Texas attorney who is Board Certified in Estate Planning and Probate Law. He is a Principal at Texas Trust Law in Austin. He may be contacted at Brad@TexasTrustLaw.com.

can be contacted at Zach@TexasTrustLaw.com.

ZACH WIEWEL, JD, LL.M. (Tax), is a Texas attorney and a law graduate at Georgetown Law Center, Magna Cum Laude. He is a Principal at Texas Trust Law in Austin. He

CURRICULUM:

Accounting and Auditing; Tax

LEVEL:

Basic

DESIGNED FOR:

CPAs in public practice; tax practitioners

OBJECTIVES:

Discuss and highlight the dangers of poor information security preparation, detail essential responsibilities and regulations, and provide an overview of IRS and FTC guidance on protecting data and addressing breaches

KEY TOPICS:

Information security and cybersecurity overview; professional responsibility to safeguard data privacy; Gramm-Leach-Bliley Act; IRS publications and resources; response to a data breach

PREREQUISITES:

None

ADVANCED PREPARATION:

None

TAKE THE ONLINE CPE QUIZ

Today’s CPA offers the self-study exam for readers to earn one hour of continuing professional education credit. The questions are based on technical information from the following article. If you score 70 or better, you will receive a certificate verifying you have earned one hour of CPE credit in accordance with the rules of the Texas State Board of Public Accountancy (TSBPA).

Take the CPE quiz online. Go to the News & Publications section of TXCPA’s website and select Today’s CPA Magazine.

The State Board stipulates that the quiz is valid for one year from its publication in Today’s CPA. Quizzes submitted after this one-year period will not be accepted.

BY ERIC GOODEN, PH.D

. Information Security Plans for Tax Professionals: A Review of Existing Guidance

The Security Summit partners – the IRS, state tax agencies and the tax industry – urge tax professionals to adopt information security plans as cyber incidents rise. With the digitization of accounting, CPAs now shoulder responsibilities for data security and privacy. Cybercriminals increasingly target CPAs, not only for their data but also for access to client accounting systems linked to bank accounts and vendor payments.

This article defines information security, outlines the risks of inadequate planning, reviews key responsibilities and regulations, and summarizes IRS and FTC guidance on safeguarding data and responding to breaches.

INFORMATION SECURITY AND CYBERSECURITY

OVERVIEW

Ideally, firms should begin the data security process by understanding the definitions of information security and cybersecurity (Paulsen and Toth, 2016). According to Paulsen and Toth (2016), information security is the protection of digital information and related systems from unauthorized alteration, delay, destruction, use, access, disclosure, or disruption to provide confidentiality, integrity and availability. It encompasses people, processes and technologies.

According to Paulsen and Toth, cybersecurity is key to information security and means protecting electronic devices and electronically stored information. It is formally defined as preventing damage to, protecting and restoring electronic records, software and related hardware to maintain integrity, confidentiality, availability, verification, and nonrepudiation.

An information security incident can be devastating for CPA firms. The greatest risk is data theft, where cybercriminals steal sensitive client financial and personal information to commit fraud. For firms, this leads to infrastructure damage, litigation, productivity loss, higher costs, and reputational harm. For clients, breaches open the door to fraud schemes such as manipulated records, fake vendors, redirected

payments, or unauthorized transactions.

Cybercriminals increasingly target small businesses, which often lack strong governance and security, making them easy prey. These clients may hold valuable assets or data, and compromised systems can be used to attack others. CPA firms must stay vigilant, as a weakness at one client can endanger many.

To combat breaches, the IRS requires written information security plans (WISPs). A breach may signal noncompliance, which also violates state and federal privacy laws and can result in fines or sanctions. CPA firms that fail to comply with data privacy laws face steep penalties. Likewise, the AICPA Code of Professional Conduct requires adherence to legal standards and violations can lead to disciplinary action from state boards or AICPA.

PROFESSIONAL RESPONSIBILITIES

Data privacy is not a new concept in the accounting profession and CPAs have always been required to take reasonable steps to safeguard data privacy. For example, the “Confidential Client Information Rule” is a well-established professional duty in the AICPA Code (AICPA, ET §1.700). Similarly, the Code has always required CPAs to act in their client’s best interest and uphold the public trust.

What is new concerning information security, specifically for tax professionals, is that AICPA has revised its Statements on Standards for Tax Services (SSTSs), effective January 1, 2024, to address data protection, adding Section 1.3, which uses standards to describe reasonable efforts to safeguard taxpayer data rather than

setting strict rules. This standard broadly considers firm differences and constant technological changes, laws and threats. CPAs applying this standard should consider laws, data storage methods, digital tools, and thirdparty providers.

Firms must review privacy policies based on technology, services and size—ensuring even sole practitioners use protections like antivirus software, VPNs, secure programs, and strong passwords. They should also provide

sional Working Group, notes that a WISP can be helpful in other disruptive events like fire, flood or theft. Accordingly, creating a WISP is critical to running a successful tax preparation business.

The scope and complexity of a security plan should be appropriate to the company’s size, activities, and the sensitivity of the customer data in question. Thus, there is no one-sizefits-all solution to developing a good WISP. Instead, a good WISP should focus on key

employee training, set data retention policies and use encryption for personal information.

KEY REGULATORS AND REGULATORY REQUIREMENTS

The Gramm-Leach-Bliley Act (Safeguards Rule) applies to all tax return preparation firms regardless of size and requires a WISP describing how the business protects consumers’ nonpublic personal information. The IRS and FTC have increased their focus on this rule.

Related CPE:

• IRS Cybersecurity Checklist

• Mastering The Three Pillars of Cybersecurity: Exploring the Technology Pillar

• Surgent’s Foundations of Cybersecurity for Financial Professionals

Federal law, enforced by the FTC, mandates that all professional tax preparers utilize a WISP. In addition to increased data security, the Security Summit, through the Tax Profes-

factors, including prevention, detection and oversight of system failures, system hardware and software protection, and employee training and oversight. The FTC’s Data Breach Response Guide PDF is a valuable resource and is discussed below.

IRS PUBLICATIONS AND RESOURCES

The IRS provides several publications and resources designed to assist professionals in understanding data security issues and developing an effective response strategy. For example, IRS Publication 5293 focuses on critical aspects of data security concerning protecting clients and the tax professional’s business from the increasing threat of data theft. This publication outlines several key areas where tax professionals can focus to establish and maintain robust security measures for safeguarding sensitive taxpayer data.

Similarly, IRS Publication 4557 provides guidelines on handling and protecting taxpayer information. Publication 4557 also outlines administrative, technical and physical security guidelines. The key points of Publication 5293 and 4557 are summarized below. Please see

Figure 1 for data privacy regulations when operating across jurisdictions.

IRS Publication 5293, Protect Your Clients; Protect Yourself: Data Security Resource Guide for Tax Professionals, and IRS Publication 4557, Safeguarding Taxpayer Data, are available at IRS.gov. Key points from both documents are noted below.

Implementing basic security steps involves the execution of several key control activities concerning data security, including:

• Recognizing phishing attempts,

• Creating a data security plan,

• Reviewing internal controls,

• Regularly updating anti-malware software,

• Using strong passwords with multifactor authentication and encrypting sensitive data,

• Backing up data securely,

• Carefully reviewing return information before filing,

• Staying informed through IRS resources, educating clients, and reviewing FTC security tips and guidelines.

In addition to control activities, an essential dimension of any system of internal control environment is the monitoring process. Monitoring controls ensure systems function properly while identifying areas for improvement. Publication 4557 advises firms to detect and manage failures by monitoring threats, updating security controls, using intrusion detection, tracking data transfers, and preparing breach responses. Firms should also monitor EFIN/PTIN accounts, follow IRS updates, maintain audit trails, and educate clients on emerging risks.

Security software is a critical component of data security and the IRS guidance notes that it is vital to download security software only from official vendor sites. Software utilization processes include installing and regularly updating firewall software, using drive encryption, anti-virus and spyware software, and ensuring that security software and internet browsers regularly receive automatic updates. It is important to create strong passwords. Strong password creation includes requirements regarding complexity, including limita-

tions on repeated characters. For example, requiring complex character combinations (symbols, letters and numbers). Password complexity may also include the implementation of minimum character requirements. Older guidelines suggested eight characters. Security experts now recommend a minimum of 12 characters or 16 characters for system administrators.

Concerning the creation of strong passwords, IRS Publication 5293 advises tax professionals to use strong, confidential passwords – avoiding personal details, changing defaults, not reusing old ones, and considering password managers. It also recommends multi-factor authentication for all critical functions, especially those involving client data.

Protecting client data starts with locking down both wireless networks and internal systems. On the wireless side: change default router passwords, use a non-identifying SSID, limit network range, enable WPA-3 encryption, avoid WEP and public Wi-Fi, and require VPNs with multi-factor authentication for remote access.

International Regulations:

• GDPR (European Union)

• PDPA (Argentina)

U.S. State Regulations:

• CCPA (California)

• CPA (Colorado)

• TDPA (Connecticut)

• VCDPA (Virginia)

Key Considerations:

• CPAs must navigate complex data privacy laws.

• Regulations mandate data protection obligations.

• Applies to handling personal data both internationally and domestically.

For information systems, know where sensitive data resides and protect it with strong passwords, encryption and secure backups. Transmit files only through protected channels like SSL or SFTP. These steps build critical layers of defense, reducing risk and strengthening client trust.

Protecting stored client data includes backing up encrypted data to secure external sources or the cloud (encrypting before upload), using drive encryption, avoiding public computers for client data, limiting software installations, maintaining a device and software inventory, limiting internet access for data storage devices, and securely disposing of old devices and client information. Publication 4557 strongly recommends using multifactor authentication for accessing sensitive information.

Professional vigilance suggests being aware of the signs of data theft, such as rejected returns, clients receiving unexpected IRS communications or refunds, unauthorized account access, discrepancies in filed returns, and unusual computer activity. Monitoring electronic filing identification numbers (EFIN) and Preparer Tax Identification Number (PTIN) accounts weekly is crucial. Education on phishing and spear phishing is also vital.

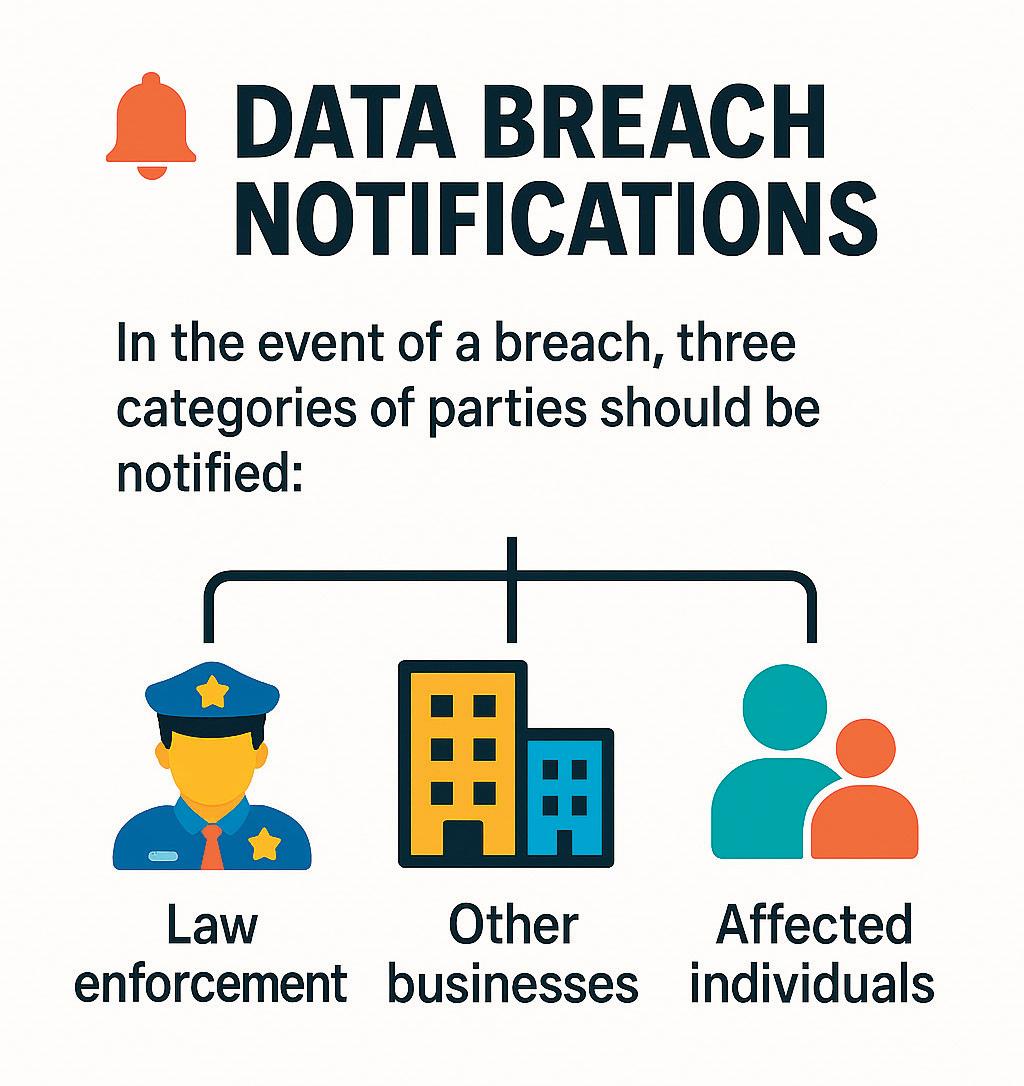

Even strong WISPs can fail, so CPA firms must know how to respond when breaches occur. The FTC’s Data Breach Response: A Guide for Business outlines critical steps firms should follow in managing an incident.

RESPONDING TO A DATA BREACH

When a data breach occurs, Publication 4557 advises tax professionals to act quickly. Steps include: