Navigating Rising Stop-Loss Premiums

At the heart of expecting the unexpected

Leverage captive insurance to self-fund your healthcare.

As your business grows, so will your healthcare expenses. Customized captive insurance from QBE creates strength to self-fund your catastrophic employee healthcare coverage, allowing you to increase transparency and reduce the cost of risk. The QBE Captive Curve® solution model removes barriers to entry and allows you to move easily to new strategies.

Take advantage of QBE’s Captive Curve solutions:

• Fronted policy that is “AA-” rated by S&P for single-parent and group captive programs.

• Reinsurance placement covering direct writing captive insurers assuming medical stop loss (MSL) risk.

• Agora, an open MSL group captive that makes it more efficient to participate in a group program.

Together, we’ll find a solution so no matter what happens next, you can stay focused on your future.

By Laura Carabello

By Chris Condeluci, Esq.

By Alston & Bird LLP

By Bruce Shutan

(ISSN

ManyMNavigating Rising Stop-Loss Premiums

Written By Laura Carabello

self-insured employers are seeing total health plan cost rising this year more than usual, with one of the contributors being rising stop-loss premiums. Experts had projected increases of well over 10%, with some employers now facing 20% or higher escalation. Some analysts anticipate these to be some of the largest increases in years, with certain median increases forecasted at about 11.5% for employers not changing deductibles, but potentially much higher if deductibles are not adjusted.

However, advisory firms contend that this is not a time to simply "throw up your hands" in defeat. There are many proactive steps that employers can take to control the costs that impact premiums when they become renewable.

COST-DRIVERS

There’s little argument as to the factors driving stop-loss premium increases. Unpredictable, high-cost claims -- driven by specialty drugs and new gene therapies – lead the discussion, prompting many stoploss carriers to implement stricter underwriting rules and increase rates. Medical inflation is another culprit with hospital care, physician services and prescription drugs at the root of underlying medical costs. These dynamics have hardened the stop-loss market into a constricted phase, making single-digit rate increases for average risk less common and erupting with double-digit increases going forward.

There are multiple dynamics in play: advances in medical technology, expanded treatment options, and higher healthcare utilization with increased drug costs related to the continued pervasiveness of costly conditions. Financial services company Sun Life reports that employers saw a 29% increase in claims for $1 million or more per million covered employees in 2024 compared to the year before — and a 47% increase in claims totaling $3 million or more. These ballooning healthcare expenditures resulted in highcost medical claims which, in turn, ramped up stop-loss premiums.

Tracking the increases, it’s obvious to see the trend:

2025 stop-loss rate renewal increases through Voya Financial were double the amount of 2024 increases, with the company citing a spike in the number of claims in the prior year.

Segal records a 9.4% increase in average stop-loss premiums in 2024 among health plans they follow, with that increase rising to 11.5% for employers maintaining comparable coverage to the prior year as opposed to adjusting their coverage to reduce premium costs. Fewer than 0.2% of claimants tallied claims greater than $250,000, but those claims accounted for 14% of all medical plan expenses.

Source: Ethos Benefits

STOP-LOSS INDUSTRY PERSPECTIVE

For Robby Kerr, chief product officer, Tokio Marine HCC – A&H Group, which primarily serves employer groups with 200-1,000 ‘paycheck lives’ (not total number of belly buttons) as well as larger companies, forecasts that as healthcare costs continue to rise, stop-loss premiums will follow suit.

“Higher hospital costs throughout the healthcare system in the post-COVID 19 environment and the trend toward unlimited benefits prompted by Affordable Care Act (ACA) are the primary drivers,” he explains. “Nobody anticipated the crushing, long impact of COVID.”

Robby Kerr

Rethink what’s possible with your stop-loss partner

For over 40 years, Sun Life has been a trusted partner in risk management for self-funded employers. Now, we’re taking it further—combining proven cost savings with innovative health solutions that give your employees access to expert care when and where they need it most.

Clinical 360+: Optimizing care, maximizing value

Our enhanced program builds on the industry-leading Clinical 360 foundation, which achieved over $68 million in savings in 2025. Available for select clients, this advancement adds personalized care pathways and expert navigation with the goal to deliver even greater value. Through proactive outreach and dedicated support, your employees gain seamless access to specialized programs, digital health tools, and clinical guidance—all designed to improve health outcomes while managing costs effectively.

It’s time to reconsider what you expect from your stop-loss partner. Let Sun Life support your business with innovative health solutions that prioritize access to quality care.*

Ask your Sun Life Stop-Loss Specialist about Clinical 360+ today.

*Hinge Health will be provided to eligible members at Sun Life’s expense through the first policy year.

Sun Life is not responsible or liable for the care, services, or advice provided by Somatus, OptiMed Health Partners, or Hinge Health, and reserves the right to discontinue this service at any time.

Sun Life will collaborate with your TPA on eligibility and applicability of programs. Health Navigator is provided by PinnacleCare. PinnacleCare is a member of the Sun Life Financial Inc. (“Sun Life”) family of companies. PinnacleCare and its employees do not diagnose medical conditions, recommend treatment options or provide medical care, and any information or services provided should not be considered medical advice. Any medical decisions should be made only after consultation with and at the direction of the member’s medical provider. Any person or entity who provides health care services following a referral or other service provided does so independently and not as an agent or representative of PinnacleCare.

Group stop-loss insurance policies are underwritten by Sun Life Assurance Company of Canada (Wellesley Hills, MA) in all states, except New York, under Policy Form Series 07-SL REV 7-12 and 22-SL. In New York, Group stop-loss insurance policies are underwritten by Sun Life and Health Insurance Company (U.S.) (Lansing, MI) under Policy Form Series 07-NYSL REV 7-12 and 22-NYSL. Policy offerings may not be available in all states and may vary due to state laws and regulations. Not approved for use in New Mexico.

© 2026 Sun Life Assurance Company of Canada, Wellesley Hills, MA 02481. All rights reserved. The Sun Life name and logo are registered trademarks of Sun Life Assurance Company of Canada. Visit us at www.sunlife.com/us. BRAD-6503-ad

As a result, he projects a hardening phase in 2026, “…characterized by significant premium increases, stricter underwriting terms and an explosion in high-cost claims. Employers with self-insured plans will continue to face challenging renewal seasons. But we won’t know if we collectively did a good job in reducing high-cost claims in 2026 until we face 2027 premium increases.”

He attributes this hardening phase for the next several years to several factors:

• Frequency of claims per employee increasing at all stop-loss thresholds

• Continued gene and cell therapy FDA approvals

• Increases in the number of transplants, neonatal claims, cancer claims, etc.

• Many stop-loss underwriters viewed the cost plateau in 2021 and 2022 as credible experience, rather than the unique generational event that it was, thereby artificially suppressing stop-loss rates over the past few years

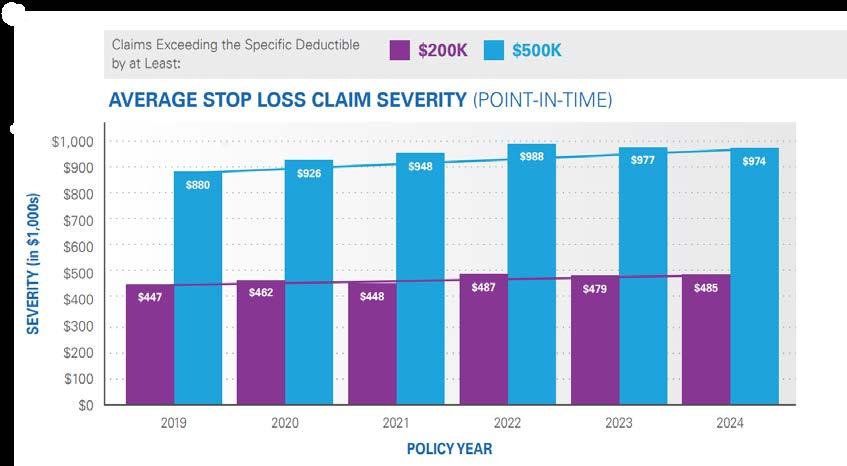

He attests that large claim severity has been increasing over the years at all claim thresholds. This is especially true for stop-loss claims exceeding 2 million dollars in reimbursements, with the average severity increasing to over $3.1 million in both 2023 and 2024. What was once considered a catastrophic and rare claim has now become more commonplace.

Source: Tokio Marine

“The uptake of expensive weight loss GLP1s and rising costs of specialty drugs are also key contributors to higher-dollar claims,” he continues. “Interestingly, while gene therapies have not been utilized as much as previously expected, cellular therapy expenses continue to grow at an unprecedented pace. Price tags of $750,000 or over $2 million should be on the employer’s radar screen.”

In 2026, he foresees that cell therapies will not be strictly limited to fourth-line treatment. Instead, they are increasingly being approved and used in earlier lines of therapy, specifically for certain blood cancers. As they become a more integrated and earlier part of treatment paradigms, they are likely to move beyond their "last resort" status, offering significant hope for patients with limited options and saving money on treatments that don’t work.

He also predicts a major shift for 2026 with the decentralization of cell therapies, adding, “More treatments are moving from inpatient hospital settings to outpatient clinics and even potentially the home, thanks to advances in remote monitoring. This shift, combined with improved manufacturing processes, will make these therapies more accessible to a wider patient population.”

Collectively, the rapidly rising costs of care have insurers responding with higher rates and stricter terms, highlighting the need for strong underwriting discipline and careful risk selection by carriers. But Kerr remains optimistic about opportunities in the stop-loss industry and the potential of AI and data management to revolutionize processes.

“We should not expect that AI will replace human decision-making, but it has the potential to significantly supplement human capabilities and enhance the role of professionals to process more data and make more informed risk decisions at a more rapid pace,” says Kerr. “Technology is simply a tool but the relationships and partnerships between employers and stop-loss companies are the strong foundation to navigate market challenges.”

Rising stop-loss premiums continue to be a challenge for Crum & Forster (C&F) and the industry, attests Rachel Miller, RHU, VP – MBU Programs, Crum & Forster’s A&H Division, adding, “With the growing demand for specialty drugs, including GLP-1 weight-loss and diabetes medications, and other new therapies on the market, employers and insurers are seeing an uptick in high-cost claims. At C&F, we believe innovation is key.”

She says rate caps can help employers achieve greater predictability and budget stability, …but they can also lead to higher initial premiums or stricter underwriting by stop-loss insurers. Rate caps should be carefully structured to help balance predictability with financial stability for both employers and insurers. We’re committed to applying a hands-on, collaborative approach and tailored solutions to help

our partners navigate rising healthcare costs and an evolving landscape.”

STRATEGIC OPPORTUNITIES TO CONTROL COST

Today, there are numerous strategic options to control costs and mitigate the impact, as employers will be tasked to initiate a proactive and strategic approach to plan management and carrier negotiations. Instead of passive acceptance of the status quo, employers can implement several strategies to manage costs.

Aarti Karamchandani,

chief growth officer,

MacroHealth, observes, "As stop-loss premiums continue to rise at a fairly consistent rate, employers must look elsewhere for savings to mitigate this steady, predictable increase. Employers can create a strategic plan focused on steering members to high-quality, lowercost providers at the point of care to mitigate medical inflation. Rising pharmaceutical costs are a great place to start. Optimize

Aarti Karamchandani

Rachel Miller

A Strategic Advantage for Benefits Consultants and TPAs

Mayo Clinic Complex Care Program

Mayo Clinic’s Complex Care Program is a customizable center of excellence solution designed to integrate seamlessly with your existing offerings. Whether you’re advising self-funded employers or evaluating their COE networks, our program helps you deliver measurable value. We’ll work through your preferred pathways or build new ones together. Let’s make complex care simple, strategic, and impactful. All without added fees.

Learn more: mayoclinic.org/complex-care-program

55% of patients experience a change in diagnosis

82% see a change in treatment plan

high-cost specialty pharmacy spend, like GLP-1s, through targeted interventions, stabilizing risk pools while maintaining comprehensive coverage."

Miller explains that the Crum & Forster Stop-Loss team applies a strategic risk management approach that includes collaborative underwriting, data transparency, and the adoption of new pricing tools and strategies to help optimize outcomes. This includes:

Utilize aggregate and specific stop-loss deductibles to better manage large and unexpected claims.

Apply portfolio-analysis and modeling tools to identify claim cost drivers, trends, and opportunities to maximize results.

Continue to build upon existing suite of approved vendors and partners to help ensure the inclusion of leading, targeted cost containment solutions to help enhance member access and control expenses.

DATA ANALYSIS

Data analytics are critical to understanding specific conditions or high-cost members in order to initiate targeted interventions. Utilizing data and technology to provide better insights enhances predictability and makes self-funding more viable and less risky.

Nelligan brings you the dedicated expertise of an Ancillary General Agency backed by the resources of Amwins Group Benefits.

With the strength of Amwins behind us, we deliver stronger service, smarter tools, and the support brokers need. We simplify ancillary benefits and help brokers grow with confidence.

Our Ancillary Services Include:

– Strategic Benefit Analysis & Plan Design

– Dedicated Account Management Support

– Complete Carrier Coordination from Start to Finish

– Flexible Implementation & Service Options

– Benefit Administration & Billing Support

– Broker Revenue Optimization

– Broker Training & Education Resources

– Resources that Enhance Broker & Client Success

“As stop-loss premiums climb, and organizations confront the persistent challenges of rising healthcare costs, self-insurance stakeholders need clinically grounded, explainable predictions that improve insights and risk stratification for greater precision in stop-loss rating and underwriting,” says Rajiv Sood, GM Insurance & Risk Business, Evidium. “Recognizing that the time has come to think differently and not simply confront the same issues year after year with the same tools and methods, Evidium pioneered the development and implementation of a unifying AI platform that dramatically transforms the old paradigm of runaway healthcare costs. The goal was to make medical knowledge accessible, usable and extrapolative to better analyze risk for the many conditions that are growing in occurrence and cost while choosing appropriate care management and care navigation channels to improve both clinical and financial outcomes.”

Fast forward to a platform that turns clinical evidence and real-world data into a shared, computational foundation. This breakthrough structure heralds a new category of solutions that connects the science and practice of medicine with the economic realities of delivering high quality care. In an industry that too often finds itself repeating the same old cycles, these capabilities move employers and other risk-takers from merely wishing for change to taking decisive, evidence-driven action.

“This approach represents a reliable risk management strategy that enables healthcare and other organizations to understand patient journeys, predict clinical trajectories and costs and improve clinical and financial outcomes with clarity and confidence,” emphasizes Sood.

At a minimum, Sood says the use of advanced data analytics and AI allows for proactive risk management and targeted interventions to mitigate high-cost claims which are the primary drivers of increasing stop-loss premiums.

“Anticipating and calculating risk before it appears, rather than reacting to premiums after the fact, allows for earlier identification and methodical evidence-based intervention, which enables organizations to shift from reactive renewal cycles to forward-looking risk management,” he advises.

A computational medical knowledge platform fills a market gap for risk-bearing and other organizations to manage both clinical and financial risk with confidence. At a minimum, it is the catalyst for identifying highrisk members that are likely to incur high-cost claims before they occur.

“The objective is to enhance underwriting accuracy and support the efforts of stop-loss carriers to assess risk with greater precision,” says Sood. “Employers who can provide detailed, data-driven insights into their populations can design better and more effective benefit structures, as well as potentially negotiate more favorable stoploss premiums by demonstrating effective risk management and adopting new approaches to underwriting, care management and provider partnerships, among others.”

Moreover, accurate clinical predictions allow care managers to focus resources on individuals who need them most.

“These data insights can benefit the entire stop-loss ecosystem including employers, carriers, TPAs and others making greater stakeholder transparency the cornerstone of successful joint efforts to better manage both care and cost, helping meet both clinical and financial goals,” he concludes.

Rajiv Sood

People > Profits

AI AS THE FOUNDATION OF STRATEGIC RISK MANAGEMENT

“For decades, risk management in self-funded health plans has relied upon lagging indicators, manual analysis, and broad assumptions,” shares Matt Weaver, senior sales director, Gradient AI. “Today, artificial intelligence (AI) is fundamentally shifting that paradigm, enabling employers and risk partners to move from reactive protection to proactive strategy amid rising cost and increasing volatility.”

Weaver maintains that by applying advanced machine learning to claims and clinical data, AI delivers actionable insights at both the population and member level. This enables more precise decisions around aggregate and specific stop-loss deductibles, grounded in predictive severity modeling rather than historical averages, trends or industry benchmarks alone. Advanced claims analysis identifies emerging high-cost conditions earlier, flags opportunities for targeted intervention, and even

has the capability of measuring the effectiveness of cost containment strategies.

“These insights directly inform smarter plan design, smarter risk taking and smarter precision pricing,” he explains. “Employers use data driven analysis to evaluate the true impact of high-deductible structures, optimize cost sharing, and better align incentives with member behavior. Wellness programs evolve from broad initiatives to targeted clinical and behavioral interventions, while direct primary care arrangements are assessed using near real time utilization and outcomes data.”

The result is a shift from static plan management to dynamic risk optimization, as Weaver adds, “With advanced analytics as the foundation, stakeholders gain greater clarity and control, supporting smarter decisions that protect both financial performance and member health in an increasingly complex stop-loss marketplace.”

PLAN DESIGN EVALUATION

Many opportunities for change are under consideration, such as adjusting deductibles or out-of-pocket maximums, balancing costsharing with employee affordability or exploring hybrid designs that may include high-performance networks. Many employers are negotiating favorable stop-loss contract terms, including rate caps or limits on how much premiums can increase at renewal or prohibiting carriers from adding specific exclusions for high-cost members at renewal – often termed “no new lasers.” This may necessitate introducing higher deductibles.

Source: 2025 Segal

Matt Weaver

REDESIGNING DRUG FORMULARIES

Employers are pointing workers toward pharma direct-to-consumer (DTC) programs as they drop coverage for certain drugs. GLP-1s are a prominent target, as HCA Healthcare, one of the largest hospital systems in the U.S., recently informed employees it would stop covering blockbuster obesity drugs Zepbound and Wegovy next year and directed them to programs set up by Eli Lilly and Novo Nordisk.

MORE AGGRESSIVE VENDOR MANAGEMENT

All stakeholders are bracing for restraints, as employers renegotiate contracts with third-party administrators (TPAs) and pharmacy benefit managers (PBMs) to achieve better transparency and performance guarantees. CBIZ recommends hoding quarterly strategy meetings with vendors and establishing a clear communication protocol, especially around high-dollar claims. Real-time collaboration between employers, third-party administrators (TPAs), brokers, and carriers helps avoid claim issues and coverage gaps.

EMPLOYEE BENEFITS CAPTIVES

Employer participation in employee benefits captives can generate even greater transparency and cost control, say the consultants at Conner Strong & Buckelew. These innovative solutions allow like-minded employers with 100 to 500 employees to form and manage their own insurance entity. Rather than paying premiums to an insurance company, the employers contribute to a shared pool for stop-loss coverage.

As members of a captive, employers retain the profits when claims are low and share the financial impact with other captive members when claims experience is higher than expected. However, since the stoploss premiums are based on the claims experience of a pool of employers, rather than a single employer, organizations in captives may benefit from best-in-class stop-loss contractual terms (including no-new lasers and rate cap provisions) and are not likely to experience the drastic stop-loss premium volatility that can occur when self-insuring on their own.

Crum & Forster offers captive solutions to meet the varying needs of their clients as Miller explains, “We enjoy engaging with our captive members, providing hands-on support and education. Captives can offer greater control over risk, potential cost savings, and access to reinsurance markets. The decision to leverage a captive depends on the organization’s risk appetite, capital resources, and long-term objectives. Our approach is to be flexible and offer tailored solutions based on each organization’s goals and risk profile.”

831(b) Captives

An 831(b) micro captive is a small insurance company structure that allows employers to set aside tax-deferred funds to cover specific under or uninsured risks. This can range from dispute resolution or business interruption to warranties, gaps and exclusions, deductibles and more. For self-insured healthcare plans, Van Carlson, founder & CEO, SRA 831(b) Admin explains that it does not replace stop-loss insurance; rather, it works in addition to it by addressing a critical exposure known as the claims corridor.

“Here’s how it works: employers with self-funded plans typically budget for expected losses and purchase stop-loss coverage to protect against catastrophic claims,” instructs Carlson. “However, between these two layers lies the corridor—unexpected claims that exceed expected losses but fall short of the stop-loss attachment point. When this happens, employers must pay out-of-pocket, which can significantly impact cash flow and even lead some to abandon selffunding.”

Carlson says an 831(b) micro captive provides a solution by funding this corridor with tax-deferred dollars, adding, “Over time, surplus reserves can accumulate, enabling employers to increase deductibles, reduce aggregate premiums, or even eliminate certain layers of stoploss coverage. Additionally, if claims come in below expectations, underwriting profits can also be contributed to the 831(b) Plan, strengthening the long-term strategy. For self-funded healthcare plans, leveraging an 831(b) Plan is a proactive way to manage volatility, protect against corridor risk and maintain the financial advantages of self-funding.”

ONGOING CLAIMS AND PHARMACY AUDITS

Audits are also a preferred avenue to ensure payment integrity. Bruce Roffe, P.D., M.S., H.I.A., president and CEO of H.H.C. Group, a healthcare consulting firm he founded in 1995, recommends,” These audits play a critical role in payment integrity, but their value can be viewed from several different perspectives.”

1. Financial Perspective

Cost Savings: Continuous audits identify overpayments, duplicate claims, and billing errors early, preventing financial leakage.

ROI Justification: Every dollar spent on auditing typically returns multiple dollars in recovered or avoided costs.

Trend Analysis: Helps detect patterns of fraud, waste, and abuse that could lead to systemic savings.

2. Compliance & Regulatory Perspective

Regulatory Adherence: Ensures compliance with CMS, ERISA, and state regulations, reducing risk of penalties.

Audit Trail: Creates documented evidence of due diligence for internal and external audits.

IDR Readiness: Supports accurate data for Independent Dispute Resolution cases under the No Surprises Act.

Van Carlson

Bruce Roffe

Process Improvement: Identifies inefficiencies in claims processing workflows and pharmacy benefit management.

Vendor Oversight: Validates PBM performance and adherence to contractual terms.

Data Quality: Improves coding accuracy and reduces downstream errors.

4. Member & Provider Relations Perspective

Fairness & Transparency: Builds trust with providers and members by ensuring accurate payments.

Dispute Reduction: Minimizes disputes and appeals by catching errors before payments are finalized.

Improved Experience: Reduces member confusion over incorrect billing or pharmacy charges.

5. Strategic Perspective

Risk Mitigation: Protects against reputational damage from fraudulent or erroneous payments.

Predictive Insights: Ongoing audits provide data for predictive modeling to prevent future errors.

Competitive Advantage: Demonstrates commitment to cost containment and integrity, appealing to TPAs, reinsurers, and health plans.

ADDRESSING RISING STOP-LOSS PREMIUMS IN BEHAVIORAL HEALTH

“Organizations must move beyond reactive utilization management and adopt proactive strategies,” says Myron Unruh, LPC, chief operating officer, MINES and Associates. “Traditional utilization management helps control costs and secure discounted services, but it does not prevent high-cost events.”

Unruh suggests that a more effective approach is condition management, “…which reduces expenses while improving quality of life for members. Our experience shows that targeted management for conditions like bipolar disorder is highly impactful due to its lower prevalence but high acuity. Using data mining and risk stratification, we ensure outpatient appointments, create crisis plans, and provide ongoing support. These steps help prevent costly psychiatric hospitalizations and promote long-term stability.”

PROACTIVE HEALTH MANAGEMENT

Investments in well-being programs, chronic condition management and preventive care incentives deliver multiple benefits. Preventive care incentives, such as those for annual screenings or physicals, allow for early detection of conditions that are far less expensive to manage than late-stage diseases. Pre-emptive management of existing chronic conditions prevents complications that often result in catastrophic highcost claims.

Myron Unruh

As employers tackle obesity care, face extraordinary costs for GLP1s and see these costs reflected in higher stop-loss premiums, here is a newly announced program from Weight Watchers that has the potential to mitigate the challenges:

Weight Watchers Med+ is the company’s dedicated GLP-1 medical program, providing members access to board-certified physicians and a coordinated care team who specialize in obesity and metabolic health. These clinicians write prescriptions for GLP-1 medications for eligible members and offer ongoing medical guidance throughout treatment. What truly sets Med+ apart is that every member prescribed GLP-1s also receives the full GLP-1 Success experience—a structured behavioral, nutritional, and lifestyle support program that research shows achieves better results on medication.

GLP-1 Success program is built around the real needs of people using these medications. Members receive personalized nutrition guidance to help them meet important macronutrient goals, tools to track weight loss and medication doses, strategies and support for managing side effects, and strength-building plans to help preserve muscle mass. The program also provides access to expert coaches trained in GLP-1 support, and virtual community groups with others on a similar journey. By pairing medical care with the GLP-1 Success framework,

RETHINKING STOP-LOSS WITH ADAPTIVE CAPITAL

Defined as flexible, innovative financing solutions that adjust to the unique cash flow and risk needs of healthcare businesses, especially self-insured employers, adaptive capital provides quick reimbursements to bridge coverage gaps and manage high-cost claims.

In essence, this option provides smart financing for employers to move beyond traditional, rigid models to ensure financial stability and support growth. It is financing to address volatility, mitigate the unpredictability of high-cost claims and allow employers to manage budgets without sudden, large drains. The result is improved cash flow with immediate reimbursement for claims, eliminating lag time and freeing up capital for other business needs, like payroll or investment.

Miller says adaptive capital funding is an essential consideration in today’s dynamic risk environment, noting, “Crum & Forster regularly assesses our capital management strategies to ensure we have the flexibility to respond to emerging risks and market volatility. This includes maintaining adequate reserves, exploring alternative risk transfer mechanisms, and aligning our capital structure with our long-term financial goals. By adopting a proactive and adaptive approach, we aim to support the organization’s financial health and sustainability.”

WILL STOP-LOSS PREMIUMS EVER COME DOWN?

“This might be a bit controversial, but did we not pay attention to the warning signs of increasing claims and the resulting hard market for stop-loss premium increases?” asks Robert McCollins, chief community organizer, Employers Healthcare Alliance (EHA), a non-profit managed ‘employer built by employers for employers and their work families.’ “The old process of spreadsheeting for low rates is out. A new success formula built on data aligned with strategic and consultative advising is emerging. Our benefit advisor partners are not chasing the lowest price—they seek fair, sustainable, and reasonable stop-loss terms aligned with long-term plan health.”

He says that this starts with strong clinical risk management identifying potential high-cost claimants early and coordinating action among all employer plan service providers across both medical and prescription drug risks.

“Advisors who are successfully educating employers and implementing proven strategies such as captives, transparent PBMs, reference-based pricing, direct contracts and DPC will set the employer up to win,” adds McCollins, who leads the EHA to provide support for HR/Business Professionals who desire the BEST healthcare for their workplace through a peer community, educational programs and actionable resources and solutions that are easy to implement and use.

“These approaches meaningfully reduce overall claims volatility which directly influence stop-loss outcomes,” he continues. “This is no longer a transactional sale—it demands a consultative, strategic business-driven approach.”

As the number and scale of large medical claims continue to climb in recent years, stop-loss market experts anticipate a parallel increase in premiums for stop-loss policies, which safeguard employers against unusually high health plan costs. In fact, the multinational insurance company Tokio Marine Group reports a 1,251% increase in the frequency of stop-loss claims exceeding $2 million since 2013.

Despite these increases, Daniel Davey, Senior Vice President and National Director, Stop-Loss MGA at Alliant, explains. “Carriers have so far been unable to transfer most of the rising claims costs to customers, as competition in the market remains strong, with more players entering the space with traditional stop-loss coverage.”

Robert McCollins

Economic pressures throughout the marketplace send a strong signal that employers should start preparing for higher stop-loss premiums as carriers adopt stricter underwriting practices. Plan sponsors will need to demonstrate that their health plan is effectively managing high-cost claims and double down on their efforts to scrutinize both the carrier and policy terms to ensure that the organization is getting the protection it needs and expects.

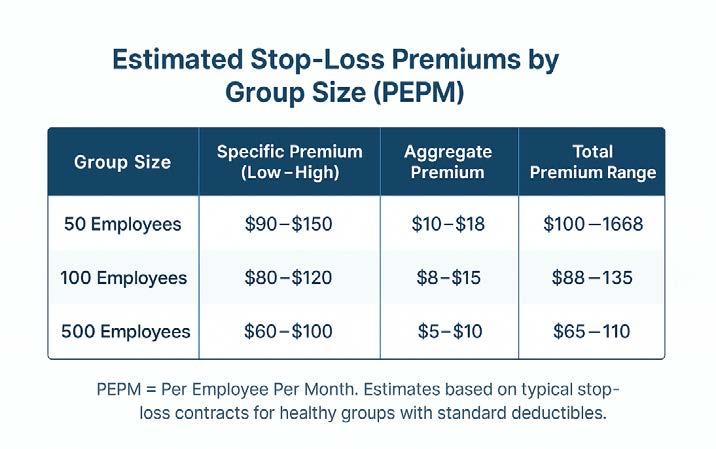

Remodel Health reports that stop-loss premiums typically range from $50 to $150 per employee per month for specific coverage, with aggregate stop-loss coverage adding an extra $5 to $15 to the base cost. Total costs can skyrocket depending on the number of employees in an organization, their risk of high claims, and other factors.

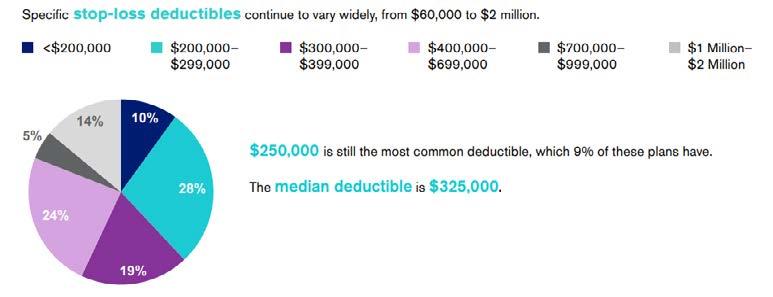

Segal’s 2025 National Medical Stop-Loss Dataset found that stop-loss coverage premiums increased an average of 9.7% for groups with similar coverage levels as their 2024 policy. Those who increased specific or aggregate stop-loss deductibles, resulting in a reduced rate, experienced an average increase of 7.3%.

Annual stop-loss premium increases from 2022 to 2024

Source: 2024 Aegis Risk Medical Stop-Loss Premium Survey

Additional stressors come from regulatory changes, although in late December 2025, the US House of Representatives passed the Lower Health Care Premiums for all Americans Act bill, a package that includes proposals that some employers and benefits advisors have long been advocating. One provision of the bill clarifies that stop-loss insurance is not recognized as traditional health coverage, aiming to preempt state regulations and help small employers self-fund health benefits. However, the bill faces wide debate over market impacts and potential coverage loss.

STRENGTHEN YOUR STOP-LOSS STRATEGY

While stop-loss premiums are increasing, self-insured employers are advised to at least consider purchasing the coverage, counsels Michael Tesoriero, a senior vice president and health consultant at Segal. “Any employer that’s self-insuring without any form of stop-loss is basically taking on all the risk, from the first dollar up until infinity,” he recently said. “Businesses with between several hundred and several thousand covered employees and dependents are most likely to utilize stop-loss when they are self-insured.”

A recent study by the Employee Benefit Research Institute (EBRI) examining self-insured employers found that those with 100 to 999 employees were most likely, by far, to purchase stop-loss, with 93% of them using the coverage in 2023 — compared to 60% of businesses with 1,000 or more employees and 63% with 25 to 99 employees. Those numbers drop significantly, to one-third or lower, for organizations with less than 25 employees. EBRI suggests the drop in numbers for small employers may be due, in part to a reduced understanding of how the coverage works.

Employers and benefits professionals tasked to determine the value of purchasing stop-loss insurance are advised to request more than a premium quote from their brokers. Proposals should reflect careful examination of clinical and cost modeling opportunities that incorporate design characteristics, medical trends, emerging treatments such as gene therapies, specialty medications and plan utilization data. This should result in dynamic, data-informed decision-making that customizes a stop-loss policy to your organization’s unique risk profile, cost tolerance and long-term benefits strategy.

About the Author

Laura Carabello holds a degree in Journalism from the Newhouse School of Communications at Syracuse University, is a recognized expert in medical travel and is a widely published writer on healthcare issues. She is a Principal at CPR Strategic Marketing Communications. www.cpronline.com

From Implementation to Impact

IPS enables quick implementation without disruption. Our secure, future-ready platform helps TPAs operate more efficiently while supporting the scalability and stability that drive long-term value.

Shared Hospitality for Self-Insurance

Boutique hotel chain brings to market its nationally recognized approach to self-insurance

BWritten By Bruce Shutan

Before there was Hillarycare or Obamacare, there was RosenCare – an employer-based effort to help reform U.S. healthcare without waiting for government intervention. In 1991, the concept’s namesake –boutique hotelier Harris Rosen – embarked on a decades-long journey to pave over a perverse system by leveraging self-insurance and encouraging other employers to follow suit.

“I think employers have finally hit the tipping point where they just cannot take on any more costs,” observes Ashley Bacot, health plan architect at RosenSure, noting that key steps include opening an onsite clinic and taking a more thoughtful approach to pharmacy benefits management. “We are set up to help others.”

Rosen, who died at age 85 just before Thanksgiving in 2024, had long believed there were two American institutions in dire need of reform: healthcare and education (his legacy associated with the latter has had an equally long-lasting impact). He was interviewed by The Self-Insurer for an article published in August 2014, nearly a year after being featured as a keynote speaker at SIIA’s national conference. Much has happened since then, when his approach was described within the pages of this magazine as “selfinsurance on steroids.”

A frustrating renewal quote for the fully insured group health plan that provided care to employees of his hotel chain in Central Florida and their families ignited a spark in Rosen that led to massive change. More than half a century later, his vision is gradually coming to fruition for other self-insured employers.

RosenCare, the healthcare program arm of Rosen Hotels & Resorts, is a unique selfinsured healthcare model whose nationally recognized patientcentered medical home model has saved the company nearly $600 million since its inception. That staggering amount in savings doesn’t include significantly lower employee turnover relative to competitors: just 14% on average compared to the hospitality industry’s 35% to 70% range.

POWER IN PARTNERSHIP

After offering bleeding-edge selfinsured solutions to Rosen Hotels & Resorts employees and their families for 34 years, the hotel

chain sought to duplicate its model for other employers. The goal was twofold: a combination of altruism and capitalism to help other organizations offer affordable, high-quality healthcare to their employees while mining a new revenue stream. RosenCare is also targeting brokers, agents and advisers for whom this approach would serve as a clinic provider and do all the backoffice work.

That quest began with a search for the right partner whose approach was best aligned with Rosen’s model, according to Bacot. Enter PeopleOne Health, a pioneer in value-based primary care. The resulting solution, described as RosenCare powered by PeopleOne Health, serves 10 employers that are actively embracing value-based care across Central Florida, where the hope is to reach enough critical mass to expand the venture elsewhere in the Sunshine State and eventually other parts of the U.S.

“We’ve grown up where we’ve had our own medical center, but now with the direct primary care [DPC] model featuring PeopleOne Health, we can actually help smaller employers, so they don’t need their own full brick-and-mortar facility,” explains Kenneth Aldridge, Jr., director of health services for Rosen Medical Center/RosenCare. “They can go for direct primary care.”

Orange County Public Schools, the nation’s seventh-largest school system, is RosenCare’s biggest client and an anchor tenant in one of four shared community clinics for other employers that benefit from economies of scale. Other clients include the School District of Osceola County, which was the first to come on board about four years ago with its own clinic, the Orange County Tax Collector’s Office, Fun Spot and Second Harvest Food Bank.

“We are continuing to grow,” Bacot says, noting that the fruits of RosenCare’s labor are getting ready to blossom with more shared clinics expected to be built.

Rosen Hotels & Resorts spends about $5,500 annually per covered life, which is less than half the national annual average. A closer look at what the company offers its employees and dependents explains why. RosenCare wellness check-ups are free, while primary care

Kenneth Aldridge, Jr.

Ashley Bacot

appointments have a $5 copay and specialist care co-pays are just $20. There’s also a $750 co-pay for the first and second hospital admission, with no further cost for additional admissions within the year. As many as 90% of pharmaceuticals are made available without a copay.

The hotel chain’s 12,000-squarefoot onsite clinic employs five full-time doctors, two nurse practitioners, two physician’s assistants and a support team who serve about 160 to 180 patients daily. Their focus is on managing chronic conditions with heightened attention paid to prevention –primary care’s heart and soul.

The Rosen Medical Center and Osceola facility feature a wide range of advanced primary care services with a population-health focus that include onsite access to imaging, physical therapy,

chiropractic care, mobile dermatology, mammography and vision units; health coaches; a registered dietitian; licensed social worker; clinical pharmacist and mental health professionals; as well as smoking cessation and weight-loss programs.

While every employer is different in how they reinvest RosenCare-generated savings, Bacot says pulling the right levers to achieve high-quality, low-cost care will enable them to eliminate annual deductibles and coinsurance, as well as charge modest co-pays. “Some of them are creative, offering premium holidays,” he adds.

CLINICAL DIFFERENCE-MAKERS

Since a large swath of the population doesn’t have access to healthcare, Aldridge says the result is inappropriate and costly misuse of the emergency room and urgent care. “If they don’t have the access, they’re going to delay care,” he explains, noting that as many as 42% of Americans have done so because they can’t afford it. “So, from a DPC perspective, they’re getting the appropriate care that they need.”

The key is leaning into primary care, which can handle most diagnoses. In fact, Bacot reports that RosenCare covers 88% of all CPT codes as part of a monthly subscription service that mirrors the DPC model.

Under this care approach, clinicians are able to determine what is driving claims and the overall health spend in a particular population, whether it’s diabetes, hypertension, hypercholesterolemia or other factors. Aldridge says health plan members are treated “like a person and not a number,” which delivers value not only to patients but also to their families and employers, who will derive immense goodwill from the arrangement.

By reinvesting substantial savings into better benefits, employers that implement this approach will remove barriers to care and, as a result, lower costs. In using DPC, any co-pay for a specialist visit is waived, along with an annual deductible and coinsurance.

“So, those individuals are going to get the right care at the right time with the right provider at the right cost,” Aldridge says.

What’s also significant to consider is the life-saving potential of this model. For example, the mobiledermatology service found 10 melanomas, one of which was invasive. “It’s really nice that there are savings associated with our health plan, but we’ve also experienced saving people’s lives, getting their diabetes under control, preventing them from having strokes,” he notes. “We actually had a patient I’ll never forget who told us we care about his health more than he did because he was brand new working for us and didn’t really experience the right type of healthcare.”

At a time when the GLP-1 category is overrun with soaring demand for weight-loss drugs, a bariatric and weight-loss specialist at the Rosen Medical Center was brought in to ensure that the drugs are being appropriately dispensed for certain subgroups at the lowest price and mitigate the possibility of any complications.

“We all know there are a lot of complications and side effects to GLP-1s, which are here to stay,” Aldridge says, hastening to add that more applications are expected in this game-changing category for congestive heart failure and other conditions.

Offering health benefits that are both affordable and robust pays dividends in terms of recruiting and retaining talent, especially in industries like hospitality that are known for churn.

“When you talk to employees and even dependents, they say the health system that we’ve created is one of the many reasons why they stayed,” he says. “We’re going to continue to keep it as rich as it is, but also to do things we can as an employer to bring influence within the community, our state and the nation so that things can be done different and can be done right.”

Bruce Shutan is a Portland, Oregon-based freelance writer who has closely covered the employee benefits industry for nearly 40 years.

FIDUCIARY LAWSUITS INVOLVING VOLUNTARY BENEFIT PLANS: WHAT’S ALL THE HUBBUB?

SomeSBy Chris Condeluci, Esq.

industry experts are sounding the alarm over lawsuits that were filed on December 23rd, claiming that employers sponsoring “voluntary benefit plans” breached their ERISA fiduciary duties. These lawsuits included similar fiduciary breach claims lodged against the brokers and consultants providing services to these employer-sponsors related to these voluntary benefit plans.

While these lawsuits are indeed concerning for employers that sponsor ERISA-covered benefit plans, employers sponsoring a “major medical self-insured group health plan” should not freak out.

Why?

Because, as stated, these lawsuits focus on voluntary benefit plans.

AND voluntary benefit plans are NOT the same thing as major medical self-insured group health plans.

Here’s what I mean:

• Voluntary Benefit Plans: A voluntary benefit plan is almost always a fully insured arrangement. Here, the employer-sponsor transfers all of the financial risk of the plan’s coverage to an insurance company. The employer-sponsor also leaves all of the claims administration and benefit payout decisions to the insurance company, and sometimes even the broker.

• Major Medical Self-Insured Plans: In the case of a major medical self-insured group health plan, on the other hand, the employer-sponsor retains the financial risk of its own employees’ health risks (i.e., the employer-sponsor does NOT shift health and financial risks to an insurance company). The employer-sponsor also retains discretion when it comes to paying benefits for incurred claims.

• Voluntary Benefit Plans: Related to the first point, employer-sponsors of a voluntary benefit plan typically do NOT manage the benefits and cost of coverage of the plan.

• Major Medical Self-Insured Plans: In the case of a major medical self-insured group health plan, on the other hand, traditionally, the employer-sponsor manages the operations of the plan, along with the benefits covered under the plan, as well as the costs of covered benefits for plan participants.

• Voluntary Benefit Plans: Employer-sponsors of a voluntary benefit plan often operate under the mistaken belief that voluntary benefit plans are exempt from ERISA.

• Major Medical Self-Insured Plans: Employer sponsors of a major medical self-insured group health plan, on the other hand, know that the plan is subject to ERISA’s requirements, along with a series of other Federal laws specifically applicable to “group health plans,” and therefore, these employersponsors traditionally take the necessary steps to comply with ERISA and these Federal laws.

• Voluntary Benefit Plans: Employers sponsoring a voluntary benefit plan rely heavily – if not exclusively – on their brokers and consultants to recommend – and even develop – the plan’s design, the plan’s benefit payouts, and the plan’s commissions and other fees payable to the brokers/consultants.

• Major Medical Self-Insured Plans: Employer-sponsors of a major medical self-insured group health plan also engage consultants, brokers, and other plan service providers, and the employer-sponsor may rely on their consultants and brokers for advice on plan design and also rely on their service providers to help administer the plan. HOWEVER, these employer-sponsors traditionally have an active voice in the types of benefits covered under the plan, along with an understanding of the cost of covered benefits, and these employer-sponsors actively hire and monitor the plan’s service providers that assist in administering the plan.

Having said all of that, although I suggested that employer-sponsors of a major medical self-insured group health plan should not freak out over these lawsuits, employer-sponsors need to heed the advice of George Costanza in Seinfeld and “do the opposite” of what these plan sponsors of voluntary benefit plans did to warrant the filing of these lawsuits.

Here’s what I mean:

• Don’t Pay Excessive Fees: The employer-sponsors of these voluntary benefit plans allegedly allowed their employees to pay excessive fees to the brokers and consultants who were advising the employer-sponsor and administering these plans.

• This violates ERISA’s fiduciary obligation to act prudently. Why? Because no prudent fiduciary would allow their employees to pay excessive fees to plan service providers, especially when these fees equaled – or even exceeded – the value of the benefits provided through the plan.

• This also violates ERISA’s fiduciary obligations to keep plan costs low and monitor plan service providers. Why? Because employer-sponsors have a fiduciary duty to understand, negotiate, and monitor the amount of broker and consultant fees and commissions that the plan and/or plan participants pay for coverage to ensure that these fees and commissions are reasonable.

• Note, when we are talking about a major medical self-insured group health plan, these plans typically do not have broker and consultant fees embedded in the plan’s premiums, but sometimes they do. In either case, employer-sponsors must make sure that they know whether or not broker and consultant fees are indeed embedded in the plan premiums, and if they are, these employersponsors must make sure that the fees are reasonable. The same goes for paying fees to plan service providers like TPAs and related service providers (i.e., fees paid to these service providers must be reasonable).

• Establish a Process for Selecting Service Providers: In these voluntary benefit plan lawsuits, it appears that the employer-sponsors gave all of the discretion to their brokers and consultants to find an insurance company to underwrite the plans, and also, all of the discretion to brokers/ consultants to determine which voluntary benefit plans to make available to the sponsors’ employees.

• The employer-sponsor of a major medical self-insured group health plan should never give away or fully delegate its decision-making responsibilities when it comes to selecting the plan’s service providers. Instead, the employer-sponsor must be actively involved in hiring, among others, an enrollment TPA, a claims adjudicator TPA, a COBRA administrator, or the owner of the provider network that “rents” its provider network to the plan. Here, the employer-sponsor must send out RFPs to multiple service providers, evaluate the RFP responses, and put time and effort into determining which service providers the plan should hire. As noted above, fees paid to these service providers must be reasonable.

• Make Sure You Get the 408(b)(2)(B) Compensation Disclosure: Brokers and consultants are required to disclose to the fiduciary of an ERISA-covered plan (e.g., the employer-sponsor) the “direct” compensation that the broker/consultant receives from the plan, as well as any “indirect” compensation the broker/consultant receives from other third parties that provide services to the plan. According to these voluntary benefit plan lawsuits, the Plaintiffs claim that the employersponsors failed to obtain the required Compensation Disclosures, which is a violation of ERISA.

• This required 408(b)(2)(B) Compensation Disclosure is intended to help a plan fiduciary identify if the broker/consultant has a conflict of interest with a service provider that the broker/consultant recommends that the plan should hire. According to these voluntary benefit plan lawsuits, the Plaintiffs claim that the brokers/consultants had such a conflict of interest with the insurance company that was underwriting the voluntary benefit plans. And the Plaintiffs further claim that if the employer-sponsors received the required Compensation Disclosures, the employer-sponsors would have been able to identify the conflict of interest.

We provide innovative, tailored plans and unmatched support

You retain clients.

• This is a reminder that employer-sponsors of a major medical self-insured group health plan must make sure that they receive the required 408(b)(2)(B) Compensation Disclosure from their brokers and consultants (if any), along with any service providers that may otherwise be subject to this Compensation Disclosure requirement (e.g., a PBM, and in some cases, a TPA).

• Compliance With ERISA’s Fiduciary Duties: The main thrust of these voluntary benefit plan lawsuits claims that the voluntary benefit plans are subject to ERISA. And, as an ERISA-covered plan, the employer-sponsors were required to adhere to ERISA’s fiduciary duties (which they allegedly did not), and also, to obtain a 408(b)(2)(B) Compensation Disclosure (which, as stated, they also allegedly did not).

• As stated above, virtually every employer-sponsor of a major medical self-insured group health plan knows that the plan is subject to ERISA. They also know that the plan is subject to other Federal laws, and as a result, virtually all employer-sponsors of these plans take steps to comply with ERISA and these other Federal laws.

• However, for many employer-sponsors of a major medical self-insured group health plan, it’s not entirely clear to them how to satisfy all of ERISA’s fiduciary duties. And – at least to me – this is what all of the hubbub is about here.

• That is, these lawsuits (like the Johnson & Johnson and Wells Fargo employee-participant fiduciary breach lawsuits) are yet another reminder that employer-sponsors of a major medical self-insured group health plan need to not only “do the opposite” of the employer-sponsors of these voluntary benefit plans, but you need to step up your game and fully understand what you need to do to satisfy your ERISA fiduciary duties. Otherwise, you will be a target of a lawsuit too…

About the Author

Chris Condeluci serves as Legal and Policy Advisor for the Self-Insurance Institute of America, Inc. (SIIA). He can be reached at ccondeluci@siia.org.

OBBBA UPDATES FOR TELEHEALTH, HDHPS AND DIRECT PRIMARY CARE

Written By Alston & Bird LLP Health Benefits Practice

TThe One Big Beautiful Bill Act (OBBBA), enacted July 4, 2025, made big changes related to health savings accounts (HSAs), including permanent telehealth relief for high-deductible health plans (“HDHPs”) and an expansion to the HSA compatibility rules for direct primary care and bronze/catastrophic plan coverage. The IRS published Notice 2026-5 in December 2025 (the “Notice”), which offered interpretative guidance and helpful clarification but still left some questions unanswered. In this update to our prior coverage on the OBBBA, we walk through the questions that were answered and some that remain.

TELEHEALTH AND OTHER REMOTE CARE SERVICES

The OBBBA permanently allows high-deductible health plans (HDHPs) to provide telehealth and other remote care services before the deductible is met. This rule applies whether the telehealth benefit is offered through the HDHP or outside the HDHP, and it applies retroactively to plan years beginning after December 31, 2024. The Notice confirms that individuals who otherwise qualified for HSA contributions did not lose eligibility in 2025 merely because their plan covered telehealth services on a predeductible basis earlier in the year (assuming the plan otherwise satisfied the HDHP requirements). [Notice Section III.A.Q/A-1]deductible basis earlier in the year (assuming the plan otherwise satisfied the HDHP requirements). [Notice Section III.A.Q/A-1]

WHAT ARE “TELEHEALTH AND OTHER REMOTE CARE SERVICES”?

Although the telehealth exception is now permanent, the IRS has not adopted a formal definition of “telehealth and other remote care.” Instead, the IRS points plan sponsors to the Medicare telehealth services list as a practical benchmark. If a service appears on that list (published annually and available through this page), offering it on a predeductible basis will not, by itself, cause a plan to lose HDHP status. For services that do not appear on the Medicare list, the IRS directs plans to rely on Medicare telehealth rules and related federal guidance issued by HHS. [Notice Section III.A.Q/A-2] deductible basis will not, by itself, cause a plan to lose HDHP status. For services that do not appear on the Medicare list, the IRS directs plans to rely on Medicare telehealth rules and related federal guidance issued by HHS. [Notice Section III.A.Q/A-2]

While the Medicare list provides helpful guidance, it uses service codes and brief descriptions that may not be easy for the average plan sponsor to interpret with confidence. This can make it challenging for plan sponsors to assess whether newer or nontraditional virtual services fall within the exception. As a practical matter, plan sponsors should confirm with telehealth vendors whether covered services align with Medicarelisted telehealth services, particularly where offerings

extend beyond standard virtual visits. Ask your telehealth partner to confirm which covered services match the Medicare list and flag any “nontraditional” offerings for review.traditional virtual services fall within the exception. As a practical matter, plan sponsors should confirm with telehealth vendors whether covered services align with Medicarelisted telehealth services, particularly where offerings extend beyond standard virtual visits. Ask your telehealth partner to confirm which covered services match the Medicare list and flag any “nontraditional” offerings for review.

IN-PERSON SERVICES, EQUIPMENT, AND DRUGS

The statute also refers to “other remote care,” a term that raised questions about how far the telehealth exception might extend. In particular, plan sponsors questioned whether the exception could apply to items such as medical equipment or prescription drugs associated with or prescribed in connection with telehealth services. The IRS makes clear that it does not. The telehealth exception does not extend to in-person services, medical equipment, or prescription drugs furnished in connection with telehealth (unless those items independently qualify under existing telehealth guidance). [Notice Section III.A.Q/A-3]person services, medical equipment, or prescription

BRONZE AND CATASTROPHIC PLANS AS INDIVIDUAL COVERAGE

As of January 1, 2026, bronze and catastrophic Exchange plans available as individual coverage now qualify as HSA-compatible HDHPs. This is true regardless of whether the minimum annual deductible requirement or maximum out-of-pocket expenses satisfy standard HDHP thresholds. [Notice Section III.B.Q/A-4]

HDHP treatment is also extended to:

• Any off-exchange bronze or catastrophic coverage on the individual market that is identical to the Exchange plans. [Notice Section III.B.Q/A-6]

• Any bronze or catastrophic coverage purchased off-Exchange on the individual market, even if the bronze or catastrophic plan is not available on the Exchange, as long as the enrollee has no reason to believe the same plan is not available on an Exchange. The Notice makes this allowance “in the interest of sound tax administration” and, as a practical matter, because consumers can’t always verify Exchange equivalence with certainty. [Notice Section III.B.Q/A-7]

Carrier EDI Transfers & Eligibility Management

Consolidated Billing

Scheduled & Templated Reporting

Employee Self-Service Portal

MyHealthBenefits® simplifies benefits for employers and members while giving brokers the tools to deliver real value.

BRMS is Your Partner in Every Season.

Our Platform Provides: Learn how BRMS puts you in control at brmsonline.com Reduce processing costs and maximize operational efficiency with our proprietary platform. Benefits Administration That Works for YOU.

Celebrating the past. Powering the future.

Fifty years ago, we made a promise: To stand by our customers and partners by delivering financial protection they can count on. Today, that promise is stronger than ever. With innovation driving us and relationships guiding us, we’re here to lead and help shape the next 50 years of smarter, more resilient self-funded health care plans.

Learn how Symetra Stop Loss can help protect your self-funded plan. Visit us at symetra.com/stoploss50.

ICHRAS AND BRONZE OR CATASTROPHIC PLANS

Employer-sponsored individual coverage health reimbursement arrangements (“ICHRAs”) can reimburse premiums for these individual plans without harming HSA eligibility. However, if the ICHRA reimburses more than the bronze or catastrophic plan premium on a pre-deductible basis, the employee could lose eligibility to contribute to an HSA. The Notice references prior HRA guidance to clarify that HRAs in general (which includes ICHRAs) must only reimburse premiums so as to avoid disqualifying an employee from being an eligible individual for HSA purposes. [Notice Section III.B.Q/A-5, referencing Notice 2008-59, 2008-29 IRB 123, Q&A-1]

ACTUARIAL VALUE FOR SOME BRONZE PLANS

When the OBBBA allowed bronze plans to be treated as HDHPs for purposes of HSA compatibility, it did so by reference to a specific provision in the Affordable Care Act (“ACA”) that defines bronze level plans as providing benefits that are actuarially equivalent to 60 percent of the full actuarial value of the benefits provided under the plan (ACA § 1302(d)(1)(A)). Some bronze variants run a bit richer than 60% actuarial value due to other ACA rules. The IRS and HHS are aware of this and have confirmed that these plans are still considered bronze plans for purposes of HDHP treatment. [Notice Section III.B.Q/A-9]

SHOP PLANS

SHOP plans—plans offered by small employers as Small Business Health Options Program (“SHOP”) coverage—that are also bronze plans will not be treated as an HDHP under the OBBBA. SHOP coverage is not individual coverage and, consequently, must satisfy the traditional HDHP requirements in order to be compatible with an HSA, including the minimum annual deductible requirement and maximum out-of-pocket expenses requirement. [Notice Section III.B.Q/A-8]

SERVICES RECEIVED AT IHS FACILITIES MAY NOT DISQUALIFY OTHERWISE ELIGIBLE INDIVIDUALS

As explained in earlier guidance from 2014, some individuals are disqualified from contributing to an HSA because the individual has received medical services at an Indian Health Services (IHS) facility during the previous three months. [See Notice 2012-14] This prior guidance does not apply to individuals who receive medical services at an IHS facility and enroll in a bronze plan variant with costsharing reductions offered to American Indians and Alaska Natives under § 1402(d) of the ACA, which may have special coverage requirements related to IHS facilities. Consequently, these individuals may be eligible to make HSA contributions even if they received medical services at an IHS facility during the previous three months. [Notice Section III.B.Q/A-10]

DIRECT PRIMARY CARE ARRANGEMENTS

The OBBBA lets direct primary care service arrangements (DPCSA) exist alongside an HDHP without destroying HSA eligibility, even though DPCSA services are “predeductible” within the DPCSA itself. DPCSAs that meet certain requirements (referred to in this article as a “compatible DPCSA”) will not disqualify an individual from contributing to an HSA. Compatible DPCSAs must provide medical care consisting solely of primary care services delivered by primary care practitioners, and the sole compensation for such care is limited to a fixed periodic fee of no more than $150/month for individuals, $300/month for families. Fees for a compatible DPCSA will qualify as an eligible expenditure for HSA purposes. deductible” within the DPCSA itself. DPCSAs that meet certain requirements (referred to in this article as a “compatible DPCSA”) will not disqualify an individual from contributing to an HSA. Compatible DPCAs must provide medical care consisting solely of primary care services delivered by primary care practitioners, and the sole compensation for such care is limited to a fixed periodic fee of no more than $150/month for individuals, $300/month for families. Fees for a compatible DPCSA will qualify as an eligible expenditure for HSA purposes.

This arrangement raised a number of questions, including whether a DPCSA could be funded by an employer on a pre-tax basis (or by an employee through a 125 plan), whether annual payment could be prorated, whether the DPCSA could be integrated into the employer’s HDHP, and what constitutes “primary care services.” The Notice provides helpful guidance for each of these, though some questions remain on the scope of primary care services.

Protect your business from the unexpected — and drive cost savings

When

Generally, a DPCSA cannot be integrated into the employer’s HDHP. The Notice includes a number of Q/As that, when taken together, make such an arrangement impractical:

• Generally, a DPCSA cannot be offered through the HDHP to offer pre-deductible primary care benefits. Because the standard HDHP limitations for pre-deductible services still apply (e.g., preventive care and now telehealth), and to the extent the DPCSA offers pre-deductible benefits outside of current permitted pre-deductible services, the benefits would violate the HDHP rules. The Notice implies that an HDHP could offer the DPCSA membership benefits for a DPCSA that offers only primary care benefits that are also permitted as pre-deductible coverage under the standard rules, or after the HDHP deductible has been satisfied, but, in practice, such an arrangement would raise administrative difficulties. [Notice Section III.C.Q/A-15]

• If an employee enrolled in an HDHP is a DPCSA member, the DPCSA membership fee may not count toward the HDHP’s minimum annual deductible or out-of-pocket expense. [Notice Section III.C.Q/A-16]

• The fixed periodic fee is the only compensation allowed under a compatible DPCSA for the primary care services. An arrangement will not qualify as a compatible DPCSA if the participant is billed separately for the primary care services (through insurance or otherwise) in addition to the fixed periodic fee. [Notice Section III.C.Q/A-11]

• Notably, DPCSA fees cannot be reimbursed by an HSA if the fees were paid by the employer, including by salary reduction through a section 125 cafeteria plan. [Notice Section III.C.Q/A-18]

An employer can, however, pay that DPCSA membership fee for a DPCSA that is outside of the HDHP. As long as the DPCSA is outside of the HDHP, an employer can subsidize a DPCSA and treat the amount of the subsidy as compensation excludable from the employee’s gross income under Code § 106. The HDHP is still subject to the standard limitations with respect to pre-deductible coverage. As the Notice makes clear, an HDHP cannot offer a benefit “that consists of paying fees for, or providing membership in, a DPCSA without a deductible or before the deductible has been satisfied.” [Notice Section III.C.Q/A-15 and 18]

Accelerating Progress

We study it, research it, speak on it, share insights on it and pioneer new ways to manage it. With underwriters who have many years of experience as well as deep specialty and technical expertise, we’re proud to be known as experts in understanding risk. We continually search for fresh approaches, respond proactively to market changes, and bring new flexibility to our products. Our clients have been benefiting from our expertise for over 50 years. To be prepared for what tomorrow brings, contact us for all your medical stop loss and organ transplant needs.

Tokio Marine HCC – A&H Group

HCC Life Insurance Company operating as Tokio Marine HCC – A&H Group

Also notable is that even though an arrangement will not qualify as a compatible DPCSA if the participant is billed separately for the primary care services (through insurance or otherwise) in addition to the fixed periodic fee, a provider can still separately offer healthcare items and services outside of the DPCSA, as long as membership in the DPCSA is not required to receive those separate offerings. Providers participating in a compatible DPCSA can offer healthcare items and services outside of the arrangement to individuals (regardless of whether they are DPCSA members) and separately bill individuals for those items and services (through insurance or otherwise). [Notice Section III.C.Q/A-12]

DPCSA FEES CAN BE PRORATED

DPCSA fees can cover more than one month, but no more than one year, so long as the annualized amount does not exceed the monthly limit. The example given in the Notice is a fee for a single individual, which could be $1,800 per year, $900 for six months, or $450 per quarter, each of which does not exceed $150 per month. [Notice Section III.C.Q/A-13]

DPCSA fees can be prorated, and they can even be reimbursed from an HSA before the coverage period for the arrangement. An HSA can reimburse a substantiated fee for compatible DPCSA coverage that begins on January 1 prior to the date coverage begins. An HSA is permitted to treat an expense for a DPCSA as incurred on:

(1) the first day of each month of coverage on a pro rata basis,

(2) the first day of the period of coverage, or

(3) the date the fees are paid. [Notice Section III.C.Q/A-19]

Amalgamated Life Insurance Company Medical Stop Loss Insurance— The Essential, Excess Insurance

As a direct writer of Stop Loss Insurance, we have the Expertise, Resources and Contract Flexibility to meet your Organization’s Stop Loss needs. Amalgamated Life offers:

• “A” (Excellent) Rating from A.M. Best Company for 48 Consecutive Years

• Licensed in all 50 States and the District of Columbia • Flexible Contract Terms

• Excellent Claims Management Performance

• Specific and Aggregate Stop Loss Options

• Participating, Rate Cap and NNL Contract Terms Available

WHAT ARE “PRIMARY CARE SERVICES”?

An arrangement that meets the OBBBA’s definition of a DPCSA will not be treated as a health plan for purposes of disqualifying an individual from contributing to an HSA. One of the requirements is that an arrangement must be restricted solely to primary care services. The OBBBA did not provide a definition for “primary care services” but did state that such services had to be provided by a primary care practitioner as defined in the Social Security Act (“SSA”). The Notice clarifies that this reference to the SSA did not import the definition of “primary care services” identified in the SSA. Instead of providing additional guidance for the definition of “primary care services,” the Notice just reinforces the OBBBA's specific exclusion of the following:

(1) procedures that require the use of general anesthesia,

(2) prescription drugs other than vaccines, and

(3) laboratory services not typically administered in an ambulatory primary care setting. [Notice Section III.C.Q/A-17]

Individuals will need to examine the terms of the DPCSA carefully to ensure that it doesn’t offer any disqualifying coverage. If an arrangement offers services that are not primary care services, such as anesthesia, the arrangement cannot be treated as a DPCSA. This is true even if an individual does not use the disqualifying services. An individual cannot simply decline such services and still treat the arrangement as a compatible DPCSA. The actual terms of the arrangement are controlling for determining the arrangement’s compatibility with an HSA. [Notice Section III.C.Q/A-14]

CAN AN HSA REIMBURSE FEES THAT ARE NOT COMPATIBLE DPCSAS?

An individual can still use their HSA to reimburse fees for a direct primary care service arrangement that would otherwise be a compatible DPCSA, but for the fixed periodic fee exceeding the statutory maximum. The limit on the fixed periodic fee applies for purposes of determining whether the arrangement is a health plan that would disqualify an individual from making an HSA contribution. If the fees for an arrangement

STOP LOSS INSURANCE WE’LL HELP MANAGE THE RISK. YOU’LL KEEP YOUR PROMISES.

Prudential’s Stop Loss insurance helps reduce unpredictable risks from self-funded medical plans. This way you can focus on giving your employees the coverage they deserve, while helping to reduce your worries about the increased frequency of catastrophic claims.

Get Stop Loss insurance from a carrier you can rely on:

•A highly rated, experienced carrier recognized for over 150 years for strength, stability, and innovation

• Efficient, responsive service with streamlined processes across quoting, onboarding, and reimbursements

•A dedicated distribution team that works hand-in-hand with your existing relationships

•Flexible policy options so we can build a coverage plan that meets the unique needs of your organization

For more information, visit our website: w www prudential com/stoploss

DPCSA, the fees may be reimbursed from an HSA as qualified medical care. However, because the noncompatible DPCSA would be considered a health plan, the individual would be ineligible to contribute to an HSA, but the individual could still use their HSA dollars to pay the fees. [III.C.Q/A-20]

KEY TAKEAWAYS

The IRS guidance helps resolve a number of OBBB-related questions related to the compatibility of telehealth, bronze and catastrophic coverage, and direct primary care. Nonetheless, as noted herein, many questions still remain.

About the Authors

Attorneys John Hickman, Ashley Gillihan, Amy Heppner, and Laurie Kirkwood provide the answers in this column. John is partner in charge of the Health Benefits Practice with Alston & Bird, LLP, an Atlanta, New York, Los Angeles, Charlotte, Dallas and Washington, D.C. law firm. Ashley is a partner in the practice, and Amy and Laurie are senior members in the Health Benefits Practice. Answers are provided as general guidance on the subjects covered in the question and are not provided as legal advice to the questioner’s situation. Any legal issues should be reviewed by your legal counsel to apply the law to the particular facts of your situation. Readers are encouraged to send questions by email to John at john.hickman@alston.com.

a Leading National TPA

The hardest problems in benefits aren’t solved alone.

Together, we can navigate the future of benefits with:

Real-time, 24/7 access to actionable insights to identify savings opportunities

Proactive and engaging member advocacy solutions

In-house teams for seamless support —implementation through renewal

Connect with us on LinkedIn or meet up with an HPI team member at the SIIA Spring Exchange. Let’s tackle your toughest benefits challenges, together.

NEWS FROM SIIA MEMBERS

MARCH 2026 MEMBER NEWS

SIIA boasts a very active and dynamic membership. Here are some of the latest developments from member companies and individuals powering the self-insurance industry.

Lucent Health Names Aadam Hussain as New CEO

Lucent Health, one of the nation's largest independent third-party administrators, announced the appointment of Aadam Hussain as Chief Executive Officer. After 11 years of leadership, co-founder Brett Rodewald has retired as Chief Executive Officer and will continue to support Lucent Health as a member of the Board of Directors.

"It has been an incredible privilege to lead Lucent Health and work alongside so many talented people. I'm proud of what we've built together, and confident in the company's future," said Rodewald. "I'm excited to continue supporting the company's mission as a board member."

Aadam joins Lucent Health at a time of continued growth and brings with him more than 20 years of leadership experience across healthcare and the self-funded benefits space. Most recently, he served as Chief Executive Officer of Healthcare Management Administrators (HMA), where he led a national third-party administrator overseeing strategy, plan administration, client services, member engagement,

October 11-13, 2026

JW

Phoenix, AZ

regulatory compliance, and operational execution.