U.S. Securities Litigation Risk Trends – February 2026

The 2-YR market capitalization loss accumulation of High-Risk Adverse Corporate Events (“ACEs”) for issuers on the NYSE and NASDAQ amounted to $16.06 trillion, an increase of 5.45% relative to January 2026 The aggregate and average frequency of High-Risk ACEs also exhibited MoM increases of 0.31% and 0.89%, respectively. These findings highlight a persistent increasing trend in securities litigation risk facing companies trading on U.S. stock exchanges.

Table 1: U.S. Securities

Frequency. Five of the 11 GICS® sectors registered a decline in the number of High-Risk ACEs. Consumer Staples and Health Care had the largest drop in frequency with 14 and 11 fewer High-Risk events relative to January 2026, respectively. Despite multiple sectors registering a decline in frequency, the aggregate number of High-Risk ACEs increased slightly from 11,541 to 11,577 events, representing a 0.31% uptick The marginal increase was largely driven by the Consumer Discretionary sector, which registered 36 more High-Risk events.

Severity. Losses on High-Risk ACEs in the IT sector registered a 9.3% MoM change rising from $4.8 trillion to $5.3 trillion relative to January 2026. It is the first time that severity in the sector exceeded $5 trillion in market capitalization losses. The Financials sector also registered high single digits MoM change in severity, with its market capitalization loss accumulation over a two -year period standing at $2.1 trillion in February. Jointly, these two sectors make up approximately 46.6% of aggregate severity.

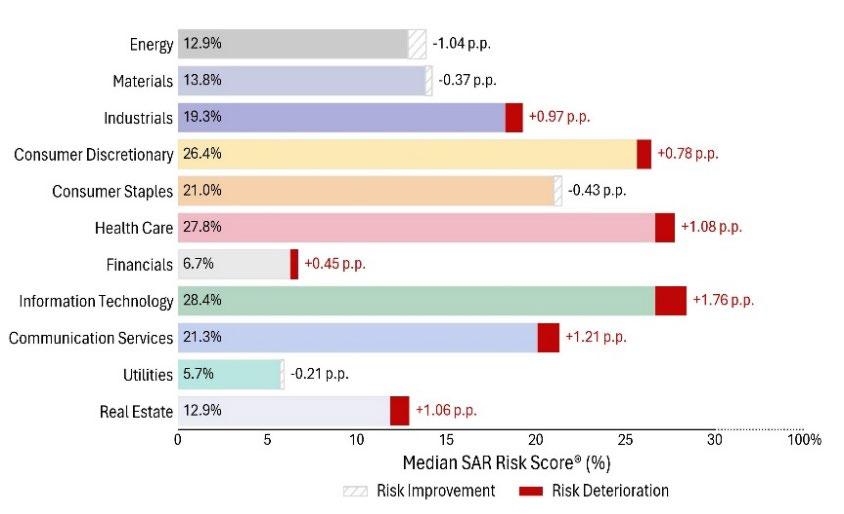

SAR Risk Score®. The majority of GICS® sectors deteriorated in February. The IT sector had the greatest deterioration with its median score increasing from 26.7% to 28.4%, a 1.76 percentage point (p.p.) increase. The Communication Services and Health Care sectors followed, with increases of 1.21 p.p. and 1.08 p.p., respectively. Among the seven sectors that registered a risk deterioration, the average MoM increase in median scores was 1.04 p.p On the other hand, the average MoM risk improvement in February was 0.51 percentage points, suggesting that risk deterioration outweighed improvements across sectors, on a median basis

Figure 1: Median SAR Risk Score® by GICS® Sector

Securities Litigation Risk Management Trends End Notes

[1] Sectors are based on the company’s Global Industry Classification Standard (GICS®).

[2] The returns of the respective GICS® sectors’ S&P Composite 1500 indices over the preceding month. The indices comprise firms of small, medium, and large market capitalization in the given GICS® sectors’ categories and for purposes of this risk management report, represent the corresponding sector’s performance in the U.S. equity markets. The firm specific event- study analyses for each issuer that supports this monthly aggregate analysis, apply a company- specific index that excludes the target company and is selected according to its industry categorization. The applied company-specific indices may or may not be the corresponding S&P Composite sector 1500 indices.

[3] Number of companies analyzed by SAR in each sector as of February 27, 2026 This sample includes every issuer that traded as common stock or ADR on the NYSE or NASDAQ with sufficient trading data to meet SAR standards of quality control.

[4] Aggregate market capitalization of all analyzed companies within the given GICS ® sector as of February 27, 2026

[5] High-Risk Adverse Corporate Events (“ACEs”) of all analyzed issuers during the preceding two years. ACEs are identified by estimating statistically significant single- trading day negative stock price movements that coincide with company-specific disclosures. High-Risk ACEs correspond to both direct corporate communications and SEC filings.

[6] The difference between [5] and the salient statistics relative to last month.

[7] The cumulative quantum of market capitalization losses on identified High-Risk ACEs for issuers during the preceding two -year period.

[8] The percentage change between [7] and the salient statistics relative to last month.

[9] The SAR Risk Score® is a proprietary score assigned to every public company listed on the NYSE or NASDAQ according to the frequency and severity of ACEs during a two -year period from the designated evaluation date. The SAR Risk Score® is equal to the market capitalization losses observed on High-Risk ACEs divided by the issuer’s market capitalization as of the preceding trading day. Figure 1 displays the percentage point (p.p.) difference in the SAR Risk Score® of the median constituent company in the sector compared to last month. A +1.0 (deterioration) implies that a sector’s median SAR Risk Score® during the corresponding month increased by one percentage point relative to the preceding month. A -1.0 (improvement) implies a reduction.

U.S. Securities Litigation Risk Trends Report Disclaimer

This securities litigation risk research report presents the monthly change in frequency of High -Risk ACEs and the impact on the accumulated two -year market capitalization losses on the universe of issuers that trade on the NYSE and NASDAQ. SAR LLC (“SAR”) tracks and publishes 2-YR market capitalization loss accumulation linked to High -Risk ACEs for both U.S. and non -U.S. issuers to evaluate and report the monthly change in magnitude of embedded securities litigation risk on a sectorspecific basis. SAR applies uniform, back -tested, regression -based event study analyses with court-approved parameters for accurate and objective identification of Adverse Corporate Events that impact the securities litigation risk of issuers that trade in the NYSE and NASDAQ.

All content published by SAR and presented in this monthly securities litigation risk research report is based on securities analytics research performed by professionals employed by SAR. SAR does not apply or rely on machine learning (ML) or artificial intelligence (AI) to compute the quantitative and statistical analyses presented herein. Securities litigation risks associated with observed Adverse Corporate Events independently identified by SAR may or may not materialize into securities claims filed by allegedly harmed shareholders. Such claims, if brought, may be directed against the corporate directors and officers of the defendant issuers, or against the underwriters of the related public securities offerings. Securities claims may include, but are not limited to, securities class actions whereby investor plaintiffs allege violations of the federal securities laws under Section 11, Section 12(a)(2), and Section 15 of the Securities Act of 1933 (“Securities Act”), and under Section 10(b) and 20(a) of the Securities Exchange Act of 1934 and Securities Exchange Commission (“SEC”) Rule 10b-5 promulgated thereunder (“Exchange Act”). Securities litigation risks may also materialize from enforcement actions filed in federal court by the SEC for alleged violations of the anti-fraud provisions of the securities laws of the Exchange Act, Securities Act, or the Investment Advisors Act of 1940.

Publicly available research published by SAR that contains economic estimates on the impact of securities litigation risk are only estimates, and actual results may vary from those estimates or projections, which are based on many variables, assumptions, and forecasts, many of which are beyond the control of SAR and any of which may present differences with estimates that are quantified using different techniques that may not be accepted in legal proceedings in the U.S. Federal Judiciary.

No fraud or wrongdoing of any kind is alleged or implied by the information published and made publicly available by SAR in this research report.

Sources: SAR ACE Database as of February 2 7, 202 6, FINRA, U.S. Securities and Exchange Commission, S&P Global Market Intelligence, and S&P Down Jones Indices.

Contact Information: Nessim Mezrahi

Stephen Sigrist

Rolando Hernandez CEO Senior Vice President Senior Analyst

T: 202.891.360

E: Nessim@sarlit.com

T: 202.891.3652

E: Stephen@sarlit.com

T: 202.436.9994

E: Rolando@sarlit.com

About Securities Analytics Research (SAR): SAR LLC is a specialized data analytics company focused on securities litigation risk management analytics of U.S. public companies, founded in 2018 and based in Bethesda, MD. Through the SAR Platform®, users license verifiably independent and high-quality data analytics based on near real-time stock price performance in response to public companies’ corporate disclosures. SAR is the developer and publisher of the SAR Risk Score®, which is assigned to issuers that trade on the NYSE or NASDAQ at the close of trading. SAR applies the court-approved event study methodology to test stock price reaction on the universe of corporate disclosures to accurately estimate the probability and magnitude of securities litigation risk impacting directors and officers. SAR provides verifiably independent securities class action settlement valuations as evidentiary support in mediated negotiations that resolve securities claims that allege violations of the federal securities laws under the Exchange Act of 1934 and Securities Act of 1933. The company is committed to the verifiable independence and accuracy of the licensed data and has been publishing quarterly statistical back-testing results since 2018. SAR does not rely on artificial intelligence (AI) or machine learning (ML) and operates in accordance with documented standard operating procedures with assigned process owners to ensure independent, human accountability. The company does not engage in economic consulting, nor places capital at risk on behalf of investors or insurers. SAR does not actively trade, hold, or intend to hold positions on the universe of equity issuances listed on the NYSE or NASDAQ, and whose principals and full-time professionals are restricted from actively trading.