Table 2: Back-end Price Impact Summary

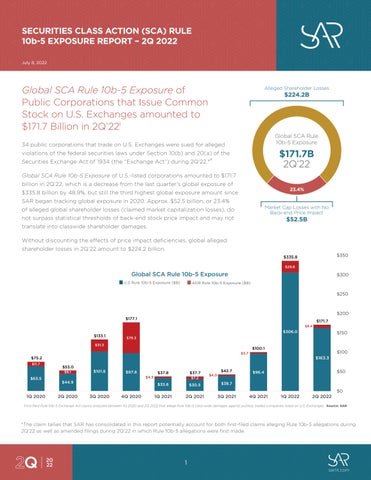

During 2Q’22, SAR analyzed 41 first-filed* “stock-drop” SCAs filed against U.S. issuers that allege violations of Rule 10b-5 via 74 claimed corrective or truth-revealing disclosures or events.vi After consolidating cases with seemingly related allegations against individual U.S. issuers, SAR accounted for 32 filed SCAs. A total of 62 corrective disclosures have been alleged in the 32 firstfiled SCAs.vii

Of the 62 corrective disclosures alleged during 2Q’22, 27 (44%) may not translate to classwide shareholder damages since they do not warrant inclusion in a certified class of proposed shareholders (Goldman) as they do not surpass statistical thresholds of back-end price impact (Halliburton II). These alleged stock drops also run afoul of the heightened pleading standards of loss causation (Dura) because they lack statistical significance to warrant potential damages after excluding non-company specific factors.viii

The number of alleged stock drops increased from 47 in 1Q’22 to 62 in 2Q’22, an increase of 31.9%. There was an increase in the number of alleged stock drops that do not exhibit price impact, from 20 in 1Q’22 to 27 in 2Q’22. 44% of alleged corrective disclosures claimed in firstfiled complaints analyzed in 2Q’22 do not exhibit price impact. The shareholder value of these stock drops - as calculated by the corresponding single-day alleged market capitalization losses – more than quadrupled, going from $12.2 billion in 1Q’22 to $50.4 billion in 2Q’22.

This $50.4 billion represents the largest quarterly dollar amount in stock price drops that do not exhibit backend price impact since SAR began tracking this data in June of 2018.ix

*See Page 1.

SCA RULE 10b-5 EXPOSURE BY INDUSTRY SECTOR

80% of Rule 10b-5 Exposure in 2Q’22 Was Driven by SCAs Against Software Companies.

Out of the 32 SCAs filed in 2Q’22, 6 (or 19%) were filed against Software companies, another 6 against Pharma/Biotech companies, 5 (or 16%) against Health Care companies, and 4 (or 13%) against Media companies.

For the second quarter in a row, the sector with the greatest SCA Rule 10b-5 Exposure was Software, which accounted for 80% of the U.S. SCA Rule 10b-5 Exposure, amounting to $131.4 billion.

Data and analyses indicate that the industry sectors that were impacted most by alleged market capitalization losses that may not surpass statistical thresholds of back-end price impact were the Auto, Energy, and Retail and Consumer Products industries. All $29.5 billion of claimed market capitalization losses in these sectors may not translate into potential shareholder damages due to verifiable absence of back-end price impact.

Table 3: U.S. SCA Rule 10b-5 Exposure by Industry Sector in 2Q’22

SCA RULE 10b-5 EXPOSURE OF U.S. LARGE CAP CORPORATIONSx

Large Cap SCA Rule 10b-5 Exposure decreased by 48.5% – from $302.3 Billion in 1Q’22 to $155.7 Billion in 2Q’22.

Litigation frequency against large caps was relatively stable with 15 large cap corporations sued for alleged violations of Rule 10b-5 during 2Q’22, an increase of 3 relative to 1Q’22. SCA exposure and potential severity decreased materially in 2Q’22. Large Cap SCA Rule 10b-5 Exposure decreased 48.5% relative to 1Q’22, amounting to $155.7 billion. Nevertheless, this is still the second greatest exposure against large caps since SAR began tracking this data in June of 2018.

The average aggregate market capitalization of U.S. large cap corporations, based on the market capitalization range of the S&P500 Index during 2Q’22, was $43.4 trillion.xi This is a decrease in aggregate market cap of $6 trillion, or 12.2%, relative to 1Q’22.

Large Cap SCA Rule 10b-5 Exposure Rate decreased by a material 25 basis points to 0.36% in 2Q’22. The Large Cap SCA Rule 10b-5 Litigation Rate increased from 1.03% in 1Q’22 to 1.36% in 2Q’22; an increase of 33 basis points.

The return of the S&P500 Index between March 31, 2022 and June 30, 2022 was -16.1%.

2Q’22 U.S. Large Cap Analysis: The big take-away here is that SCA exposure remains at historically high levels. 2Q’22 exhibited the second greatest Large Cap SCA Rule 10b-5 Exposure Rate since 2020.

In 2Q’22, the Large Cap U.S. SCA Rule 10b-5 Litigation Rate equates to 1 in 74 large cap companies being a target of Rule 10b-5 Exchange Act claims.

4: Large Cap SCA Rule 10b-5 Exposure of U.S. Issuers

Table

SCA RULE 10b-5 EXPOSURE OF U.S. MID CAP CORPORATIONS

xii

Mid Cap SCA Rule 10b-5 Exposure Increased Materially in2Q’22, Amounting to $6.3 billion.

7 mid cap corporations were sued for alleged violations of Rule 10b-5 during 2Q’22, more than 3 times the number that were sued in the previous quarter. Mid Cap SCA Rule 10b-5 Exposure in 2Q’22 was almost 14 times larger than in 1Q’22, amounting to $6.3 billion – an increase of $5.8 billion.

The average aggregate market capitalization of U.S. mid cap corporations, based on the market capitalization range of the S&P MidCap 400 Market Index during 2Q’22, was $1.54 trillion, a decrease of 4.69% relative to 1Q’22.xiii

Mid Cap SCA Rule 10b-5 Exposure Rate increased by 38 basis points relative to 1Q’22, amounting 0.41%. The Mid Cap Rule 10b-5 Litigation Rate increased in 2Q’22 to 0.96%; an increase of 68 basis points relative to 1Q’22.

The return of the S&P MidCap 400 between March 31, 2022, and June 30, 2022 was -15.42%.

Table 5: Mid Cap SCA Rule 10b-5 Exposure of U.S. Issuers $5.8B 1293.2% $6.3B 2Q’22

2Q’22 U.S. Mid Cap Analysis: Mid Cap SCA filing frequency and Mid Cap SCA Rule 10b-5 Exposure Rate both increased materially during the previous quarter. SCA Exposure of $6.3 billion for Mid Caps during 2Q’22 is almost 14 times what it was in 1Q’22. In 2Q’22, the Mid Cap U.S. SCA Rule 10b-5 Litigation Rate equates to 1 in 104 mid cap companies being a target of Rule 10b-5 Exchange Act claims.

Small Cap SCA Rule 10b-5 Exposure decreased relative to 1Q’22, Amounting to $1.4 Billion in 2Q’22.

SCA RULE 10b-5 EXPOSURE OF U.S. SMALL CAP CORPORATIONS

xiv

Small Cap SCA Rule 10b-5 Exposure

$1.4B 2Q’22

Frequency decreased in 2Q’22 relative to 1Q’22, with 10 small cap corporations sued for alleged violations of Rule 10b-5. The Small Cap SCA Rule 10b-5 Exposure in 2Q’22 amounted to $1.4 billion, which translates to decline of 58% relative 1Q’22.

The average aggregate market capitalization of U.S. small cap corporations, based on the market capitalization range of the S&P SmallCap 600 Market Index during 2Q’22, was $856.4 billion, a slight increase of 0.18% relative to 1Q’22.xv

In 2Q’22, the Small Cap SCA Rule 10b-5 Exposure Rate was 0.16%, which is 22 basis points lower relative to 1Q’22. The Small Cap Rule 10b-5 Litigation Rate decreased by 11 basis points to 0.40%.

The return of the S&P SmallCap 600 Index between March 31, 2022, and June 30, 2022 was -14.11%.

Relative to 1Q’22

Small Cap SCA Rule 10b-5 Exposure Rate

Small Cap SCA Rule 10b-5 Litigation Rate

2Q’22 0.16% 2Q’22

2Q’22 U.S. Small Cap Analysis: Small Cap SCA Rule 10b-5 Exposure declined by 22 basis points relative to 1Q’22, while Small Cap SCA Rule 10b-5 filing frequency exhibited a slight decrease.

In 2Q’22, the Small Cap U.S. SCA Rule 10b-5 Litigation Rate equates to 1 in 249 small cap companies being the target of Rule 10b-5 Exchange Act claims.

Table 6: Small Cap SCA Rule 10b-5 Exposure of U.S. Issuers

The ADR SCA Rule 10b-5 Exposure of nonU.S. issuers in 2Q’22 amounts to $8.4 billion, a Material Decrease of ~72% Relative to 1Q’22.xvi

2 non-U.S. issuers that trade on U.S. exchanges through ADRs were sued for alleged violations Exchange Act during 2Q’22.xvii

ADR SCA Rule 10b-5 Exposure of directors and officers of non-U.S. issuers to claims that allege violations of the Exchange Act amounted to $8.4 billion in SCA exposure.xviii

Approximately $2.1 billion of market capitalization declines that have been claimed as investor losses by a proposed class of common stock shareholders may not surpass statistical thresholds of back-end price impact and may not translate into classwide shareholder damages. Without discounting the effects of price impact deficiencies, alleged shareholder losses against non-U.S. issuers amounts to $10.4 billion in 2Q’22.

In 2Q’22, the ADR SCA Rule 10b-5 Exposure Rate decreased substantially relative to 1Q’22 at 0.03%. The ADR SCA Rule 10b-5 Litigation Rate also decreased by 5 basis points relative to 1Q’22 to 0.1% based on the number of non-U.S. issuers that trade in the NYSE, NASDAQ, and over-the-counter in the U.S.

ADR SCA Rule 10b-5 Exposure

ADR SCA Rule 10b-5 Exposure Rate Relative to 1Q’22

ADR SCA Rule 10b-5 Litigation Rate

Table 7: ADR SCA Rule 10b-5 Exposure of Non-U.S. Issuers

2Q’22 ADR Analysis: Frequency of Rule 10b-5 SCAs against non-U.S. issuers decreased by 1 in 2Q’22. The related SCA exposure of the 2 defendant firms amounts $8.4 billion.

Table 8: Price Impact Summary of Alleged Corrective Disclosures of Non-U.S. Issuers

[1] First-filed and analyzed SCA complaints that allege violations of Rule 10b-5 against non-U.S. issuers that trade on U.S. exchanges through ADRs. Excludes U.S. issuers. [2] The total number of alleged corrective disclosures identified in the sample of SCA complaints. [3] The total number of alleged corrective disclosures that do not exhibit a statistically significant one-day residual stock price return at the

The

Sources: S&P Global Market Intelligence, S&P Dow Jones Indices, Thomson Reuters, SAR SCA Platform as of June 30, 2022.

Any reprint of the information or figures presented in this quarterly report should reference SAR. Please direct any technical inquiries to Stephen Sigrist, VP of Data Science, at 202.891.3652 or stephen@sarlit.com. SAR is a software and data analytics company that actively tracks, monitors, and analyzes private securities fraud actions that allege violations of the Exchange Act of 1934.

i: Global SCA Rule 10b-5 Exposure is the sum of U.S. Rule 10b-5 Exposure and ADR Rule 10b-5 Exposure.

ii: This tally accounts for U.S. issuers of common stock and non-U.S. issuers that trade on U.S. exchanges through ADRs that are listed as defendants in first-filed SCA complaints filed during the second quarter of 2022 and allege shareholder damages. It also accounts for claims against such issuers in which Rule 10b-5 allegations were first made in amended filings during 2Q’22. A corporation that was sued a second or third time during the current quarter in non-amended filings is not accounted for in the current quarter’s tally. The tally excludes SCA complaints that were identified but not analyzed per Appendix-1.

iii: Figures of Securities Class Action (SCA) Rule 10b-5 litigation exposure are based on identified and analyzed first-filed complaints for each claim filed during the corresponding quarter. They also include claims in which Rule 10b-5 allegations were first made in amended filings during the corresponding quarter. All federal securities class action complaints are read and screened for allegations that specifically include alleged violations of Rule 10b-5 and define a specific Class Period. Only the claimed stock price declines presented in the first-filed or relevant, identified amended complaint against each defendant company are accounted for to estimate U.S. SCA Rule 10b-5 Exposure. Measures of SCA exposure for each claim may increase or decrease as the case progresses through the class action life cycle. SCA Exposure is not amended retroactively for cases that have been dismissed by the Court or voluntarily dismissed by plaintiffs.

iv: This tally accounts for U.S. issuers of common stock that are listed as defendants in first-filed SCA complaints filed during the second quarter of 2022 and allege shareholder damages. It also includes claims in which Rule 10b-5 allegations were first made in amended filings during 2Q’22. A U.S. issuer of common stock that was sued a second or third time during the current quarter in non-amended filings is not accounted for in the current quarter’s tally. The tally excludes SCA complaints against U.S. issuers of common stock that were sued for alleged violations of the federal securities laws in previous quarters. The tally also excludes cases that have been filed against international corporations that are listed on U.S. exchanges through American Depositary Receipts (ADRs). The tally excludes SCA complaints that were identified but not analyzed per Appendix-1.

v: A public corporation’s exposure to alleged violations of Rule 10b-5 is estimated by tracking the cumulative decline in market capitalization during single market trading sessions that correspond with the timing of the claimed alleged corrective disclosures that surpass statistical thresholds of indirect price impact at the 95% confidence standard and are presented in a first–filed or relevant, identified amended SCA complaint. This figure excludes market capitalization declines of non-U.S. issuers that have been sued for violations of the U.S. federal securities laws and trade on U.S. exchanges through American Depositary Receipts (ADRs).

vi: SAR relies on Docket Alert and Court Wire notifications attained from Thomson Reuters Westlaw. SAR professionals actively monitor and track case dockets to attain newly filed and amended class action complaints.

vii: This tally of alleged corrective disclosures includes both those from SCA complaints first-filed in 2Q’22 and amended filings in which Rule 10b-5 allegations were first made in 2Q’22 against U.S. issuers of common stock. The tally excludes securities class action complaints against companies for which there are identified complaints in prior quarters.

viii: See Goldman Sachs Group Inc. v. Arkansas Teacher Retirement System, No. 20-222 (2021), Halliburton Co. v. Erica P. John Fund, Inc., 134 S. Ct. 2398 (2014), and Dura Pharmaceuticals, Inc. v. Broudo, No. 03-932, 2005 WL 885109 (2005).

ix: A single-firm multivariate regression analysis with a minimum of 100 observations (if a full 252 observations are unattainable) for a Control Period is applied to evaluate the statistical significance of the logarithmic residual stock price decline on the trading day(s) affected by an alleged corrective disclosure(s) (or the alleged adverse event). Statistical significance is measured by computing the t-statistic of the residual stock price decline during the single trading session that is affected by the alleged corrective and/or truth-revealing information. The Control Period ends one trading day prior to the start of the Class Period presented in the corresponding securities class action complaint. Due to the proliferation of Rule 10b-5 claims made against companies involved in recent SPAC transactions, beginning in 2Q’21, a single-firm multivariate regression analysis is performed when sufficient pricing observations are available to support an adequate Control Period. If there are between 50 and 100 closing stock price observations before the first alleged corrective disclosure, the VP of Data Science determines whether the raw data sample is sufficiently robust to perform a multivariate regression analysis that surpasses econometric quality controls standards of SAR.

x: Large cap corporations are the sub-set of defendant corporations that have market capitalizations within the range of the greatest and least market capitalization value of the constituent members of the S&P 500 Market Index at the time of the start of the Class Period alleged in the identified complaint.

xi: This is the average total market capitalization of U.S. issuers of common stock that are listed on the NYSE or Nasdaq exchanges with market capitalizations greater than $3.7 billion between April 1st, 2022, and July 1st, 2022.

xii: Mid cap corporations are the sub-set of defendant corporations that have market capitalizations within the range of the greatest and least market capitalization value of the constituent members of the S&P MidCap 400 Market Index at the time of the start of the Class Period alleged in the identified complaint.

xiii: This is the average total market capitalization of U.S. issuers of common stock that are listed on the NYSE or Nasdaq exchanges with market capitalizations between $1.26 and $3.7 billion between April 1st, 2022, and July 1st, 2022.

xiv: Small cap corporations are the sub-set of defendant corporations that have market capitalizations within the range of the greatest and least market capitalization value of the constituent members of the S&P SmallCap 600 Market Index at the time of the start of the Class Period alleged in the identified complaint.

xv: This is the average total market capitalization of U.S. issuers of common stock in that are listed on the NYSE or Nasdaq exchanges with market capitalizations less than $1.26 billion April 1st, 2022, and July 1st, 2022.

xvi: Figures of ADR Securities Class Action (SCA) Rule 10b-5 Exposure are based on both first-filed and analyzed complaints for each claim filed during the corresponding quarter and claims in which 10b-5 allegations were first made in amended filings during the corresponding quarter. All federal securities class action complaints that comprise the data and analyses presented herein are read and screened for allegations that specifically include alleged violations of Rule 10b-5 and define a specific Class Period. Only the claimed stock price declines presented in the first-filed or relevant, identified amended complaint against each defendant company are accounted for to estimate ADR SCA Rule 10b-5 Exposure. Measures of SCA exposure for each claim may increase or decrease as the case progresses through the class action life cycle.

xvii: This tally includes both SCA complaints against non-U.S. issuers that trade on U.S. exchanges first-filed in the current quarter and claims in which Rule 10b-5 allegations were first made in amended filings during the current quarter. A non-U.S. issuer of ADRs that was sued a second or third time during the current quarter in non-amended filings is not accounted for in the current quarter’s tally. The tally excludes SCA complaints that were identified but not analyzed per Appendix-1.

xviii: A non-U.S. issuer’s exposure to alleged violations of Rule 10b-5 is estimated by tracking the cumulative decline in market capitalization during open market trading sessions that correspond with the timing of the claimed alleged corrective disclosures that surpass statistical thresholds of indirect price impact and are presented in a first-filed SCA complaint.

Appendix-1: Rule 10b-5 Exchange Act SCAs Identified But Not Analyzed in 2Q’22.

The following list comprises Rule 10b-5 Exchange Act SCAs filed during 2Q'22 against issuers of common stock or ADRS but not analyzed by SAR due to two primary factors. Either there is insufficient pricing data to conduct a multivariate regression in accordance with SAR’s data analytics standards of quality control, and/or cases of first impression that allege novel theories of Rule 10b-5 liability are not analyzed according to SAR’s standard operating procedures and quality control standards.