How Securities Litigation Risks Materialized In The 1st Quarter

By Nessim Mezrahi and Stephen Sigrist (April 13, 2026)

Geopolitical risks are fomenting U.S. stock market volatility across multiple sectors and having a measurable impact on the securities litigation risk of both U.S. and non-U.S. issuers that trade in American stock exchanges.[1]

Investor relations practices and corporate disclosure controllership are becoming increasingly complex while securities litigation risk deterioration persists.[2] As a result of these dynamics, it is not surprising that private litigants have deployed resources to investigate and pursue more fraud-on-the-market claims at the start of 2026.

Defendant issuers are well served by maximizing data-driven legal defenses early on to minimize — if not eliminate — potential settlement losses by disqualifying alleged fraud-revealing stock drops that demonstrate glaring econometric deficiencies of back-end price impact and loss causation. After all, our data indicate that approximately 20% of the alleged stock drops claimed by investor plaintiffs to be fraud-revealing against U.S. issuer defendants during the first quarter do not exhibit any abnormal single-day returns in response to company-specific information at the 95% confidence standard.

Insurance underwriters face a challenging and complex risk management environment to protect U.S. public companies. They're employing greater underwriting scrutiny — particularly around corporate disclosure practices — to mitigate high-severity securities litigation risks.

Claim teams are instituting more robust technical claim evaluation procedures to mitigate potential unfavorable loss reserve developments that may manifest from the overwhelming increase in potential loss severity on active, newer vintage U.S. Securities and Exchange Commission Rule 10b-5 claims.

Unprecedented geopolitical risks, demonstrable U.S. equity market volatility, persistent securities litigation risk deterioration, increased Rule 10b-5 filings with remarkably higher exposure and rising average settlement values during the preceding 12 months have placed insurance carriers on high alert in the first quarter of 2026.

A Remarkable Increase in Rule 10b-5 Litigation Exposure During the First Quarter of 2026

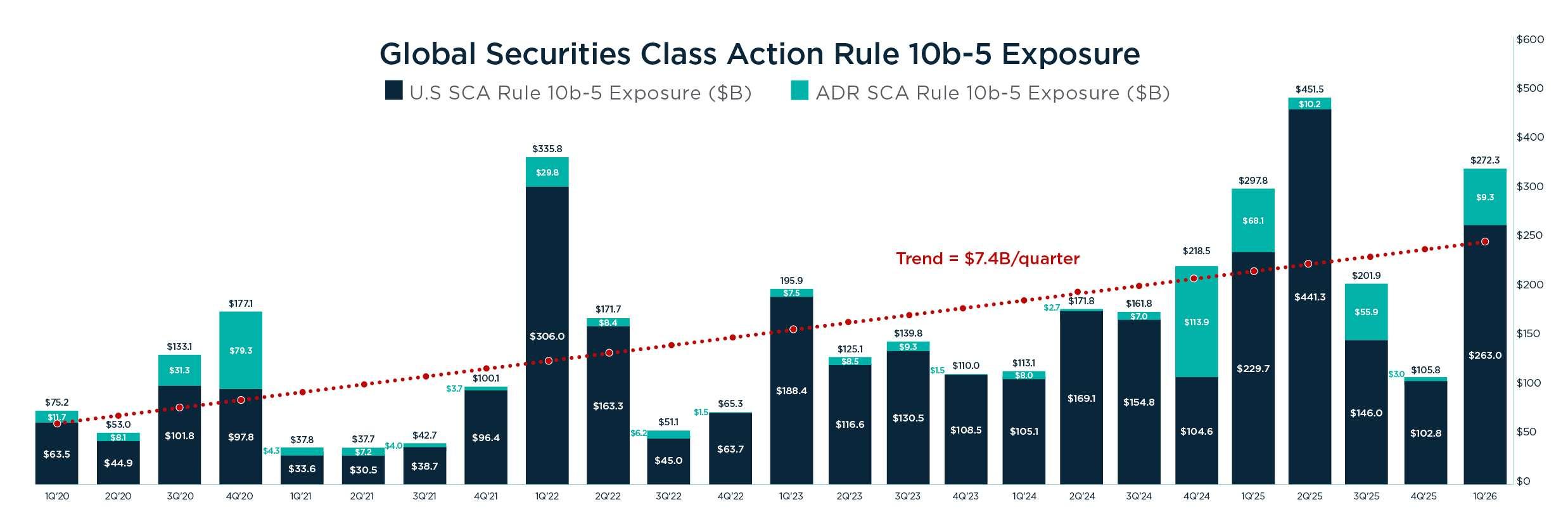

Filing data for the first quarter of 2026 indicates that investor plaintiffs' alleged market capitalization losses stemming from private Rule 10b-5 filings corroborate the materialization of securities litigation risks, yielding a remarkable increase in exposure for directors and officers of U.S.-listed companies.[3]

Alleged market capitalization losses that are accounted for only on alleged stock drops claimed against U.S.-listed corporations that exhibit statistically significant residual stock price returns amounted to $272.3 billion in the first quarter of 2026, a 157.6% increase relative to the prior quarter's global exposure of $105.7 billion.[4] The remarkable increase in securities class action exposure, through market capitalization losses, is driven by three main factors.

First, observed filing frequency is up. During the first quarter of 2026, we identified a total of 62 fraud-on-the-market claims against U.S.-listed companies and analyzed 55. We excluded seven claims due to insufficient data or novel theories arising from new pumpand-dump actions.[5]

The increase in filings propelled the increase in the number of alleged corrective disclosures, which increased by 97.9% relative to the fourth quarter of 2025.[6] This makes sense given the notable increase in adverse corporate events that have materialized between the fourth quarter of 2025 and the first quarter of 2026.

Second, exposure per alleged corrective disclosure claimed in the first quarter of 2026 increased significantly. For U.S. issuer defendants, the average market capitalization loss per alleged stock drop amounted to about $3 billion, an increase of 26.6% relative to the fourth quarter of 2025.[7] For non-U.S. issuer defendants, the average market capitalization loss per alleged stock drop amounted to about $2.3 billion, an increase of 133.6% relative to the fourth quarter of 2025.[8]

Third, the alleged exposure in the case of Barrows v. Oracle Corp. amounts to $142.4 billion in market capitalization losses, which is 54% of the total Rule 10b-5 exposure claimed against U.S. issuer defendants.[9] This claim, brought on Feb. 3 in the U.S. District Court for the District of Delaware, had a material impact on the aggregate estimate of market capitalization losses.

Excluding the impact from this claim, exposure against U.S. issuers amounts to $120.7 billion, which is still an increase of 17.4% relative to the fourth quarter of 2025.[10]

Trailing 12-Month Increase in Frequency and Average Settlement Values

Over the preceding 12-month period, fraud-on-the-market settlements that exclude Securities Act allegations have increased in both frequency and average settlement values. According to Rule 10b-5 claims that we tracked and analyzed, average settlements

increased by 7.8%, from $28.8 million to $31.1 million.[11]

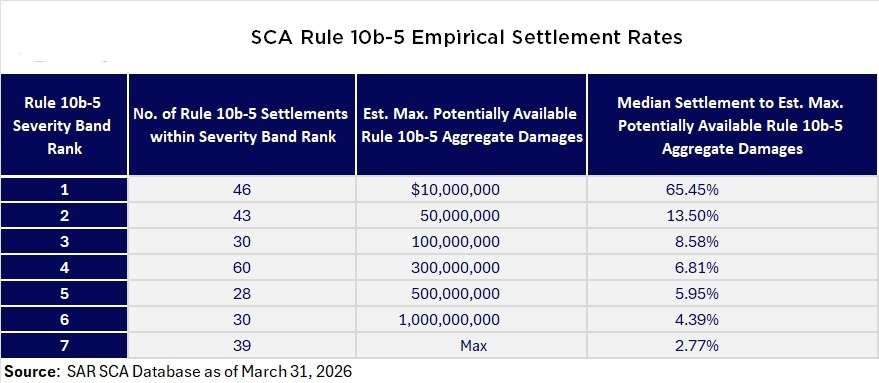

Our empirical settlement data indicate that the greatest number of Rule 10b-5 settlements relates to claims where the estimates of maximum potentially available aggregate damages range between more than $100 million and up to $300 million. Over the past eight years, we have tracked 60 claims that have settled in this range of aggregate damages, leading to a median settlement rate of approximately 6.81%.[12]

The fastest growing cohort of settled Rule 10b-5 claims is those where the maximum potentially available aggregate damages range between more than $500 million and up to $1 billion. Over the past eight years, we have tracked 30 claims that have settled in this range of aggregate damages, leading to a median settlement rate of approximately 4.39%.[13]

Maximum potentially available Rule 10b-5 aggregate damages are the single best predictor of settlement values, according to our estimates, explaining over 60% of the variation in settlement values in a simple univariate regression.[14]

Econometric Claim Deficiencies During First Quarter Reach 12-Month High

Event study analyses on first-filed Rule 10b-5 securities class action complaints during the first quarter of 2026 indicate a notable sample of econometrically deficient alleged stock drops claimed against U.S. issuer defendants.

Out of the 89 alleged stock drops that were tested for statistical significance on the corresponding single-day trading session, about 20%, or 18, fail to demonstrate back-end price impact on company-specific information, thereby invalidating their inclusion in a potential class of shareholders should the claim survive the motion to dismiss. These alleged stock drops also run afoul of the heightened pleading standards of loss causation, and may not contribute to monetary recompense for authorized claimants.[15]

According to the U.S. Department of Justice in 2021, which represented the interests of the U.S. and supported neither party in an amicus brief at the U.S. Supreme Court ahead of the justices' June 2021 decision in Goldman Sachs Group Inc. v. Arkansas Retirement System:

"When event studies reveal no statistically significant movement in a company's stock price at either the time that an alleged misstatement was made or the time when it was corrected, it is relatively straightforward to conclude that the alleged misstatement had no price impact."[16]

Conclusion

The confluence of a plethora of negative factors affecting issuers and their insurance partners at the start of 2026 is significant.

Issuers and their risk management advisers will need to focus on enacting robust disclosure controllership and thoughtful investor relations to assuage disclosure complexity and mitigate the potential materialization of adverse corporate events that can lead to costly securities litigation.

Defendants and their insurance partners will need to aggressively deploy data-driven legal defenses, particularly at the motion to dismiss and class certification stages, to limit increasingly expensive settlements with investor plaintiffs.

In a securities litigation landscape being shaped by higher filing frequency and increased litigation exposure with rising average settlement values, loss reserve management decisions require data-driven, claim-specific loss severity evaluation throughout the class action litigation life cycle to avoid costly capital allocations.

Nessim Mezrahi is the co-founder and CEO at SAR LLC.

Stephen Sigrist is senior vice president of data science at the firm.

The opinions expressed are those of the author(s) and do not necessarily reflect the views of their employer, its clients, or Portfolio Media Inc., or any of its or their respective affiliates. This article is for general information purposes and is not intended to be and should not be taken as legal advice.

[1] "Geopolitical Whiplash and the Shifting Ground of D&O Liability," Sarah Abrams, The D&O Diary, March 9, 2026. https://www.dandodiary.com/2026/03/articles/geopoliticalrisk/geopolitical-whiplash-and-the-shifting-ground-of-do-liability/.

"Stock Markets Are Battling Iran War Volatility. Why It's About to Get Real." Barron's, April 6, 2026. https://www.barrons.com/articles/stock-market-volatility-iran-things-to-know-today6bacd8ec.

[2] "Guest Post: Deterioration in U.S. Securities Litigation Risk," Nessim Mezrahi and Stephen Sigrist, The D&O Diary, Dec. 11, 2025. https://www.dandodiary.com/2025/12/articles/securities-litigation/guest-postdeterioration-in-u-s-securities-litigation-risk/.

"U.S. Securities Litigation Risk Increased by $2.3 Trillion in Second Half of 2025," SAR, PR Newswire, Jan. 30, 2026. https://www.prnewswire.com/news-releases/us-securitieslitigation-risk-increased-by-2-3-trillion-in-second-half-of-2025--302675069.html.

"U.S. Securities Litigation Risk Trends — January 2026," Securities Analytics Research (SAR), Feb. 12, 2026. https://isu.pub/Be0pTM5.

"U.S. Securities Litigation Risk Trends — February 2026," Securities Analytics Research (SAR), March 10, 2026. https://isu.pub/z1sWyCu.

[3] "SCA Rule 10b-5 Exposure Report 1Q 2026," SAR, April 10, 2026. https://isu.pub/n8frGUB.

[4] Id., see pg. 4.

[5] Id., see Appendix-1.

[6] Id., see Table 2, pg. 6.

[7] Id., see pg. 6.

[8] Id., see pg. 12.

[9] Id., see pg. 5.

[10] SAR SCA Database.

[11] "SCA Rule 10b-5 Exposure Report 1Q 2026," SAR, April 10, 2026, see pg. 4.

[12] Id., see Table 9, pg. 14.

[13] Id.

[14] Id., see pg. 13.

[15] Id., see Table 2, pg. 6.

[16] Brief for United States as Amicus Curiae Supporting Neither Party In re Goldman Sachs Group, Inc. v. Arkansas Retirement System, Case No. 20-222.