How China and India Are Setting the Pace for APAC Military Drone Market, According to Ken Research

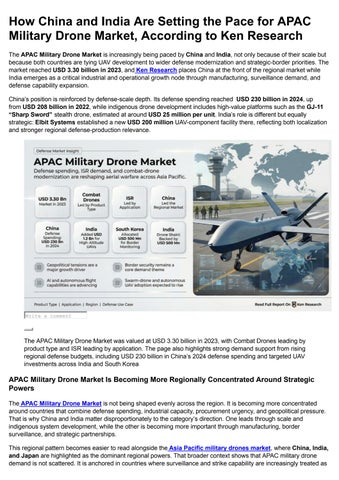

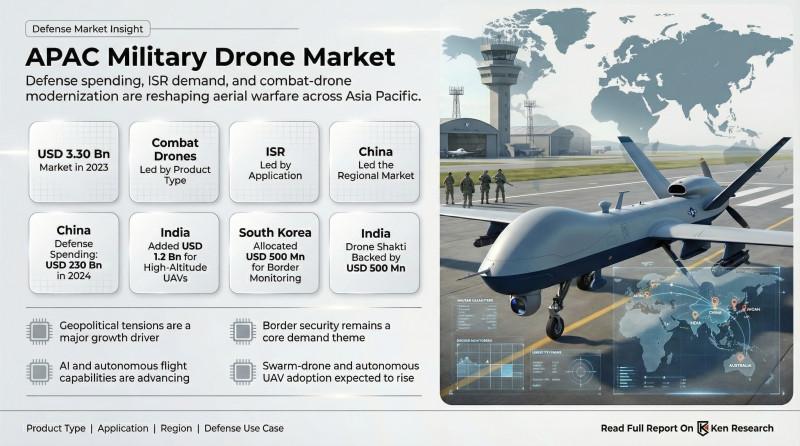

The APAC Military Drone Market is increasingly being paced by China and India, not only because of their scale but because both countries are tying UAV development to wider defense modernization and strategic-border priorities. The market reached USD 3.30 billion in 2023, and Ken Research places China at the front of the regional market while India emerges as a critical industrial and operational growth node through manufacturing, surveillance demand, and defense capability expansion.

China’s position is reinforced by defense-scale depth. Its defense spending reached USD 230 billion in 2024, up from USD 208 billion in 2022, while indigenous drone development includes high-value platforms such as the GJ-11 “Sharp Sword” stealth drone, estimated at around USD 25 million per unit. India’s role is different but equally strategic: Elbit Systems established a new USD 200 million UAV-component facility there, reflecting both localization and stronger regional defense-production relevance.

Write a comment

The APAC Military Drone Market was valued at USD 3.30 billion in 2023, with Combat Drones leading by product type and ISR leading by application. The page also highlights strong demand support from rising regional defense budgets, including USD 230 billion in China’s 2024 defense spending and targeted UAV investments across India and South Korea

APAC Military Drone Market Is Becoming More Regionally Concentrated Around Strategic Powers

The APAC Military Drone Market is not being shaped evenly across the region. It is becoming more concentrated around countries that combine defense spending, industrial capacity, procurement urgency, and geopolitical pressure. That is why China and India matter disproportionately to the category’s direction. One leads through scale and indigenous system development, while the other is becoming more important through manufacturing, border surveillance, and strategic partnerships.

This regional pattern becomes easier to read alongside the Asia Pacific military drones market, where China, India, and Japan are highlighted as the dominant regional powers. That broader context shows that APAC military drone demand is not scattered. It is anchored in countries where surveillance and strike capability are increasingly treated as

APAC Military Drone Market Segmentation Shows Why China and India Matter So Much

The target market’s structure makes regional leadership easier to understand. The APAC combat drone market leads by product type, while the APAC ISR drone market leads by application. These two facts matter because both China and India are operating in security environments where combat readiness, surveillance reach, and target-awareness all carry strategic significance.

APAC Military Drone Industry Regional Leadership Mix

The regional leadership mix is being shaped by different strengths.

China leads through budget scale, platform development, and broader defense-industrial depth.

India is becoming more relevant through industrial partnerships, border-surveillance demand, and growing domestic defense capability.

The Asia Pacific defense UAV hierarchy therefore reflects not just procurement volume, but also strategic and industrial positioning.

APAC Military Drone Market Infrastructure Mix

Drone leadership also depends on the systems around the aircraft.

ISR remains central because regional powers need better intelligence persistence.

Combat and target-acquisition roles add offensive and tactical depth.

The Asia Pacific ground control station market matters because drone leadership increasingly depends on command, control, and mission coordination infrastructure, not on UAV platforms alone.

That infrastructure angle matters even more because the GCS report notes military and defense as the leading application, alongside heavy Chinese and Indian spending on systems tied to UAV operations and border-surveillance support.

Why China and India Are Setting the Pace for the APAC Military Drone Industry

The APAC military drone industry is being paced by China and India because both countries sit at the intersection of security pressure and defense modernization. China’s leadership is backed by national-scale investment, indigenous development, and strategic urgency. India’s role is being built through industrial expansion, technology partnerships, and a stronger push to integrate drone capability into border and surveillance systems.

The page also highlights Beijing, Seoul, and Bangalore as important centers, which reinforces the idea that the regional drone market is being shaped through concentrated defense-industrial nodes rather than evenly across APAC. Ken Research suggests that when a market’s technological and procurement gravity starts clustering this way, regional leadership becomes more durable over time.

Conclusion

China and India are setting the pace for the APAC Military Drone Market because both countries connect drone adoption to broader defense and strategic priorities. China leads through scale, indigenous platform development, and budget depth, while India is strengthening its role through manufacturing, partnerships, and surveillance-oriented demand. In a market already valued at USD 3.30 billion, that combination of regional power concentration and infrastructure-backed defense modernization gives APAC military drones a more structured growth path than a simple technology-procurement narrative would suggest.

This blog draws on broader market context from Ken Research, while the deeper market sizing, segmentation, competition, and outlook discussion comes through the APAC Military Drone Market, which maps how regional power concentration, ISR demand, combat capability, and industrial expansion are shaping the category’s next phase.

China leads the APAC Military Drone Market because it combines high defense spending, indigenous drone development, and a broader strategic focus on advanced surveillance and combat systems. That gives it both budget strength and platform depth. That is why the APAC China military drone position remains central to the regional market story.

2. Why is India becoming more important in the APAC Military Drone Industry?

India is becoming more important in the APAC Military Drone Industry because it is combining industrial localization, defense partnerships, and surveillance demand in a way that raises its long-term strategic relevance. New manufacturing and border-oriented procurement logic are both strengthening its role. That is why the APAC India defense UAV growth story is becoming harder to ignore.

3. How does the broader Asia Pacific military drone landscape support this regional focus?

The broader Asia Pacific military drone landscape supports this regional focus because it confirms that the market is already concentrated among a few major defense powers. China, India, and Japan dominate in the supporting regional report, which reinforces the idea that leadership is not evenly distributed. That is why the Asia Pacific military drone ecosystem adds useful context to the country-level story.

4. What does the APAC Military Drone Market competitive landscape suggest today?

The APAC Military Drone Market competitive landscape suggests a category already shaped by defense-grade vendors with strong platform, systems, and integration capability. Players such as IAI, Northrop Grumman, General Atomics, AVIC, and Elbit Systems make the market look much more structured than an emerging aerospace niche. That is why the APAC military drone vendor structure appears increasingly mature.

5. Why is command infrastructure relevant to China and India’s pace in this market?

Command infrastructure is relevant to China and India’s pace in this market because leadership in military drones depends on more than the aircraft themselves. It also depends on control systems, mission coordination, and the ability to operate fleets effectively under real-world defense conditions. That is why the Asia Pacific ground control systems layer fits naturally into the regional leadership discussion.