Loan Rejection? Why $1,000 Surplus Isn't Enough

Banking Math vs. Your Wallet: Why a $1,000 Surplus Can Still Mean a Loan Rejection

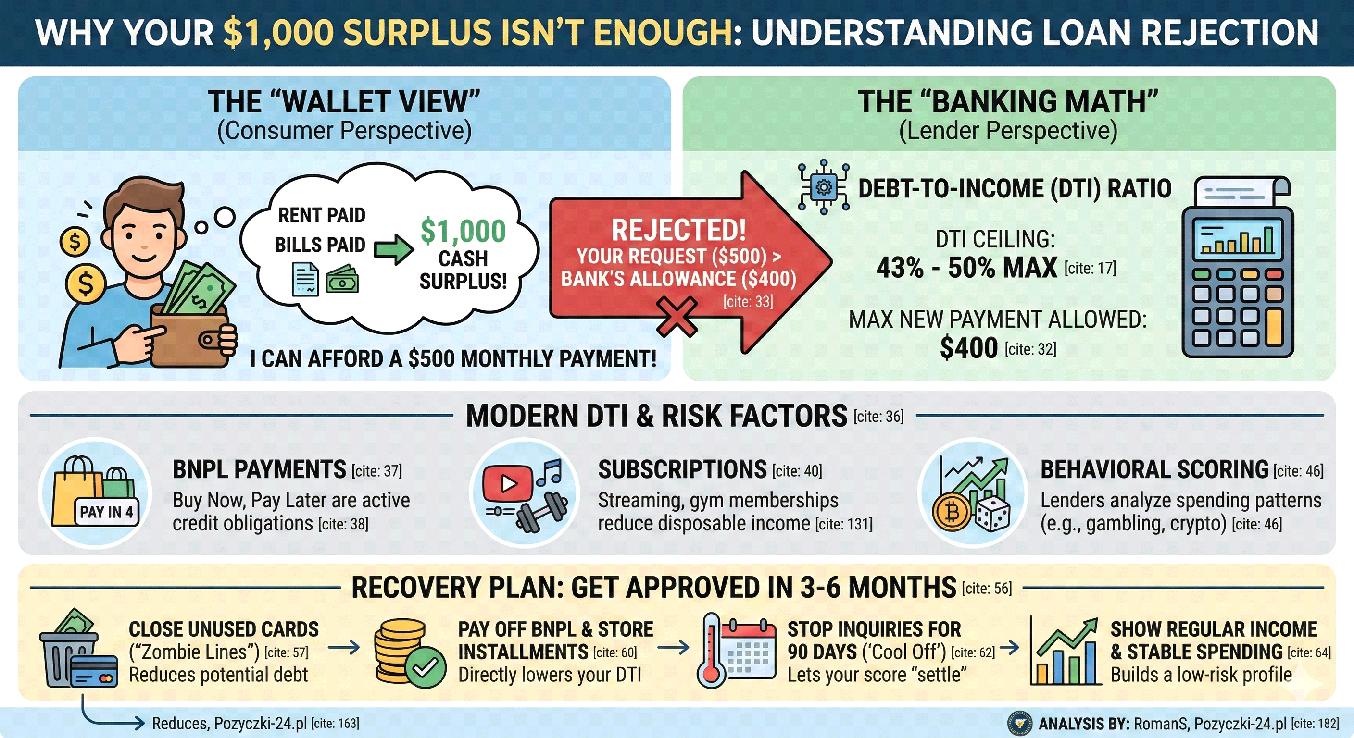

When consumers evaluate their personal financial health, most of us look at our finances through a very simple lens: the “wallet view”. This perspective is grounded in immediate, tangible cash flow If you've paid your rent, utilities, and current bills, and you still have a thousand dollars left over, you feel secure. Under this psychological framework, it is entirely logical that you think, “I can easily afford a $500 monthly payment; it won't even hurt.”

However, modern lending works by completely different rules. In 2026, your subjective sense of security doesn't matter to a bank's algorithm. The institutional evaluation process has evolved to strip away human emotion and the cash physically sitting in your account. Instead, what matters is systematic banking math.

As a credit market analyst at Pozyczki-24.pl, I've seen this play out countless times: the shock and frustration of clients who get a “No” despite having “plenty of money.” The fundamental disconnect between the consumer and the financial institution lies in the metrics being evaluated. The problem is that banks don't look at the cash you're holding. Rather than counting the dollars remaining in your checking account at the end of the month, they analyze your Debt-to-Income (DTI) ratio and your real capacity to repay based on risk modeling.

The Silent Deal-Breaker: Understanding the DTI Ratio

To navigate the lending market successfully, you need to understand the mathematical foundation of risk assessment. The most critical concept to grasp before hitting “apply” is the DTI (Debt-to-Income) ratio. This isn't just some background metric — it is the primary gatekeeper of your financial mobility It's a percentage that tells the lender exactly how much of your gross (or sometimes net) monthly income is already “eaten” by debt.

Financial institutions rely on strict, standardized equations to remove any ambiguity from the lending process. The formula is straightforward:

DTI = (Total Monthly Debt Payments / Gross Monthly Income) x 100%

In today's highly regulated financial environment, most mainstream lenders have a strict ceiling. If your DTI exceeds 43% to 50%, you hit a wall full stop. You might wonder why lenders are so rigid about this specific number. The answer is simple: statistics show that once you cross that threshold, any minor life hiccup — a car repair, a medical bill dramatically increases the chance of defaulting on the loan.

The system doesn't care if you live frugally It uses standardized cost-of-living estimates for your area and checks whether you fit within their safety parameters. Your personal budgeting discipline, however admirable, doesn't factor into the equation.

The Anatomy of a Rejection: The $5,000 Case Study

To understand why consumers and banks so often see the same situation completely differently, let's walk through a concrete example using a monthly income of $5,000 net (take-home pay).

Your View (The Household Budget)

From the perspective of someone managing their own household finances, the situation looks stable and ready for a new commitment. The consumer calculates their obligations like this:

•

• Living Expenses (Rent, groceries, gas): $1,900

• Cash Surplus in your pocket: $1,000

Empowered by this visible cash surplus, you apply for a new loan with a $500 monthly payment, thinking you'll still have $500 left for savings. It seems like a balanced equation debt gets paid, life goes on, and you're still putting something aside. Reasonable, right?

Not to the bank.

The Bank's View (The DTI Algorithm)

When the automated underwriting system processes your application, it completely ignores that $1,000 surplus and focuses exclusively on regulatory safety limits:

• Your Maximum Debt Allowance (50% of $5,000): $2,500

• Current Monthly Debt: $2,100

• Your “Regulatory” Breathing Room: $2,500 $2,100 = $400

The Verdict: Even though you physically have $1,000 left at the end of the month, your maximum allowable new payment is $400. By asking for a loan with a $500 payment, you are $100 over the safety limit. That seemingly small gap triggers an automatic rejection.

And no, the algorithm doesn't care about your promise to “eat out less.” It evaluates hard numbers derived from historical statistical models nothing else.

Hidden Debt Eaters: BNPL and Subscriptions

The complexity of loan approval has grown significantly in recent years. Banking analytics have evolved, and the algorithms are no longer satisfied with checking only traditional mortgages and auto loans. Your DTI now includes things that were once practically invisible.

One of the biggest shifts involves micro-financing. I'm talking about BNPL (Buy Now, Pay Later) services like Affirm, Klarna, or Afterpay. Most people view these as simple budgeting tools, not formal borrowing. But even if your “interest-free” installments seem small say, $150 a month for some tech or clothes the bank treats them as active credit obligations. Every “pay in four” plan you have gets added to the pile.

On top of that, many lenders now use something called Cash Flow Underwriting. This method dives directly into your bank statements to assess your actual spending behavior. They look at your recurring subscriptions. If you have $300 a month going to various digital services and memberships, that amount gets deducted from your disposable income further shrinking your loan eligibility. Those Netflix, Spotify, and gym memberships are no longer invisible to a lender.

The Inquiry Trap and Behavioral Scoring

Understanding DTI is only part of the modern financial equation. The way you apply for credit is scrutinized just as heavily as your capacity to repay

A common mistake is “shotgunning” applications applying at five different places after the first rejection. This frantic attempt to secure funding is counterproductive in a very measurable way Every Hard Inquiry (a formal credit check) leaves a mark on your credit report. When algorithms see multiple inquiries in a short window, they interpret it as a sign of financial desperation or instability It's one of the fastest ways to make a weak application even weaker.

Beyond traditional credit inquiries, the industry has added another layer: Behavioral Scoring. Underwriters are no longer just looking at what you owe they analyze where you spend your money Certain spending patterns are mathematically correlated with higher default rates. Frequent transfers to gambling sites or crypto exchanges, for example, can flag you as high-risk. The result? Even if your DTI is perfectly fine, your behavioral profile might still get you denied.

Why Living “To the Edge” is a Real Danger

It's worth understanding why banks enforce these limits not just what they are.

Taking on debt right at the ceiling of your capacity leaving yourself only $500 for everything else means you have effectively zero financial cushion. No emergency fund, no buffer.

As an analyst, I'll say it plainly: true creditworthiness is about peace of mind. Credit should function as a utility that improves your life, not a burden that keeps you anxious at the end of every month. If a smaller-than-expected bonus or a surprise home repair makes you sweat over your next loan payment, you aren't using credit as a tool — you're trapped by it.

The limits lenders set serve a dual purpose: protecting the institution's capital and protecting the consumer from financial ruin. Safe borrowing ends where your ability to save begins. With fluctuating living costs, a financial buffer isn't a luxury it's a necessity. A life with debt payments that consume every spare dollar is exhausting, and the math eventually catches up.

Your Recovery Plan: How to Prepare for an Application

If you've recently faced a denial, or you recognize that your financial profile doesn't currently fit modern lending criteria, don't panic. Creditworthiness is not a fixed score carved in stone it's a dynamic metric. By making targeted adjustments to your active accounts, you can meaningfully shift how the algorithm reads your profile within a few months.

Here's how to do it in 3 to 6 months using the “Incremental Gains” method:

Close “Zombie” Lines. Close credit cards you don't use. Many people keep old cards open thinking it helps their utilization, but the math is more nuanced than that. Even with a zero balance, the bank counts a percentage of that limit as potential debt. Closing a $5,000 unused limit can instantly free up room for a new loan application.

Pay Off Small Installments.

Clear those tiny BNPL plans or store cards. This directly attacks your current DTI ratio. Each closed account is one fewer debt entry and a lower DTI small wins that add up fast.

Cool

Off Your Inquiries.

If you've been rejected recently, stop applying for at least 90 days. Time is the only real remedy for excessive hard inquiries. Give your credit score time to settle before your next attempt.

Show Regularity. Lenders love predictability. Consistent deposits from the same source, zero missed payments (even for small utilities), and stable spending patterns build the profile of an “A-grade” borrower Boring is good when it comes to credit.

Summary: The Ethics of Borrowing

To successfully navigate the credit market, you have to start thinking the way an underwriter thinks — at least long enough to review your own profile before you apply. Before you click “apply,” do the math yourself.

A rejection can feel deeply frustrating, especially when you have cash sitting in your wallet. But it's worth reframing the experience. The banking algorithm isn't your enemy it's designed to protect the institution, but also to protect you from falling into a debt spiral where you're taking out a new loan just to pay off an old one.

Your long-term financial health depends on maintaining a sustainable relationship with borrowing. Respect your credit capacity more than your payday balance. That capacity the mathematical one, not the emotional one is what determines whether you can buy a home, start a business, or fund an education somewhere down the road.

For further comparative data and analytical tools regarding your personal financial health, resources are available. If you need help calculating your specific ratios or want to see how lenders estimate living costs in your region, visit our guide at Pozyczki-24.pl Informed decision-making is your best defense against algorithmic rejection. Financial education is the most effective insurance for your future.

About the Author

RomanS – Independent financial market analyst and expert at Pozyczki-24.pl. Since 2012, he has specialized in verifying loan offers and analyzing the Total Cost of Credit. He is a recognized specialist in credit score building and household debt management.

Denied a loan despite having cash? Learn about the DTI ratio and how analyst RomanS calculates your real credit limit. Avoid rejection in 2026 with these tips!

More publications can be found at: https://www.linkedin.com/in/romans-pozyczki/ https://medium.com/@pozyczki-24