Demystifying the 2026 Credit Algorithm

Expert Analysis by Roman Sommer (RomanS)

Creditworthiness is no longer a basic calculation of income versus expenses combined with a satisfactory FICO score Modern US banking and FinTech institutions utilize hyper-automated, AI-driven predictive analytics that analyze your complete financial behavior rather than a static snapshot.

The following analysis breaks down how automated systems evaluate risk today, provides an international comparative context, and outlines professional strategies to audit and optimize your financial profile

The New Variables of Creditworthiness

To successfully navigate the modern financial market, it is essential to understand the hidden vectors that algorithms track

● Trended Data and FICO 10T: Lenders now utilize models like VantageScore 4.0 and FICO 10T, which evaluate trended data spanning over 24 months to identify risk trajectories. Algorithms will flag consumers as high-risk if they consistently make only minimum payments while their overall debt increases.

● BNPL Micro-Loans: The Credit Utilization Ratio (CUR) remains vital, but major credit bureaus now fully integrate Buy Now, Pay Later (BNPL) services like Affirm and Klarna. Juggling multiple micro-loans signals stretched cash flow to the AI, negatively impacting borrowing power

● Cash-Flow Underwriting: To accommodate the gig economy, lenders use Open Banking APIs like Plaid to instantly analyze bank account deposits and withdrawals Algorithms penalize income volatility, favoring steady, predictable direct deposits

● Inflation-Adjusted DTI: The Debt-to-Income (DTI) ratio is subject to updated stress tests that account for localized inflation If an algorithm calculates that a new loan payment will consume all remaining disposable income after factoring in ZIP-code-based increases for groceries, utilities, and insurance, it will trigger an automated rejection

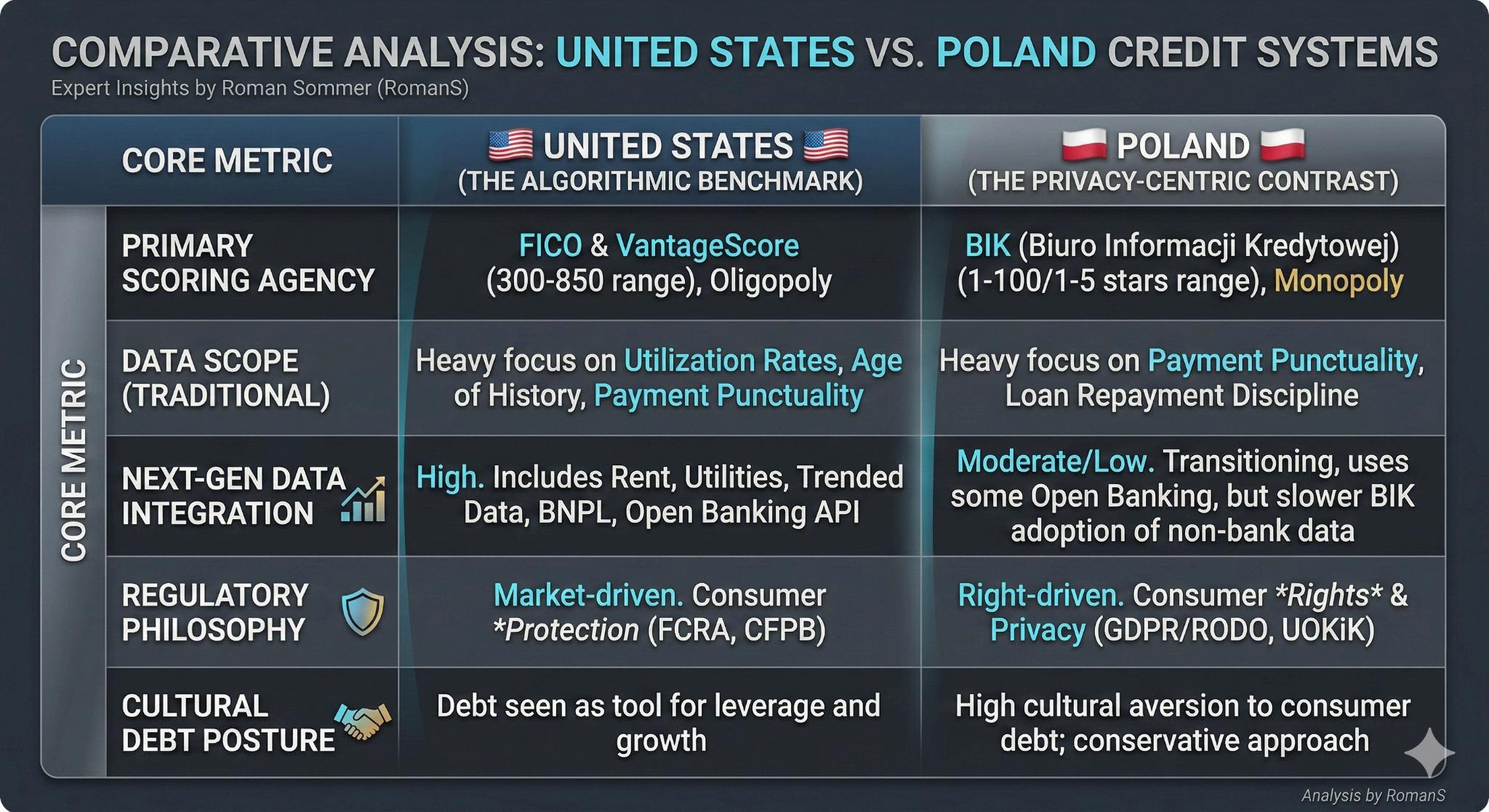

International Context: US vs. Polish Systems

While the modern US credit landscape represents the peak of AI integration, examining the contrast with a highly regulated European system, such as Poland’s, offers invaluable perspective This comparison highlights how different regulatory and cultural frameworks utilize consumer data contrasting the aggressive data collection model of the US against a more privacy-centric EU approach

The following table provides a professional comparative overview:

The Automated Approval Engine

When an application is submitted online, a massive API data exchange occurs in the background within seconds

The system instantly cross-references identity data to comply with KYC laws and prevent synthetic identity fraud Following a soft credit pull, alternative databases like LexisNexis are queried for red flags that traditional bureaus miss, such as payday loans, evictions, or frequent phone number changes A proprietary AI model then calculates the Probability of Default (PD) to automatically assign an interest rate

Lending approaches differ across the sector. Traditional banks are highly conservative, often requiring FICO scores above 680 and paper trails for income verification, while occasionally routing complex profiles to human underwriters. Conversely, FinTechs operate with 100% automation and higher risk tolerance, relying on Open Banking to verify income in seconds, though they offset subprime risks with higher APRs

Consumers are protected by the Fair Credit Reporting Act (FCRA), which guarantees the right to dispute inaccuracies and requires lenders to provide an Adverse Action Notice upon denial Furthermore, the Equal Credit Opportunity Act (ECOA) mandates aggressive auditing of AI models to prevent demographic bias.

The DTI Reality Check: A Case Study

The difference between a consumer's internal math and the AI's calculation can be drastic. Consider an applicant named Mike, who earns $6,000 monthly and is applying for a $15,000 loan with a $400 monthly payment

Mike calculates his existing debt at $2,200 (rent and an auto loan), yielding a safe DTI of 36 6% Adding the new $400 payment pushes his DTI to 43.3%, which aligns with traditional banking rules

However, the underwriting algorithm evaluates a broader dataset. It adds $250 for credit card minimums and $150 for a BNPL Macbook purchase Furthermore, it applies a $100 inflation buffer based on rising local utility and grocery costs The AI calculates Mike's current debt burden at $2,700, and with the proposed loan, his total debt reaches $3,100. This results in an AI-calculated DTI of 51 6%, prompting an instant denial because his cash flow is statistically too close to default.

Strategic Credit Optimization and Profile Repair

To ensure favorable terms, treat your credit profile as a constantly evolving resume By law, all data held by credit bureaus must be 100% accurate, timely, and verifiable; otherwise, it must be deleted

● Target 10% Utilization: To secure the best rates, maintain an overall credit utilization below 10% and pay off large balances before the statement closing date

● Pacing and Preparation: Space out hard inquiries by at least six months to avoid looking credit-hungry. Before applying for major loans, consolidate debts and clear BNPL micro-loans to improve your DTI Ensure your bank account has no overdraft or NSF fees for at least three months prior to any Cash-Flow Underwriting

● Conduct a Forensic Audit: Retrieve official reports from AnnualCreditReport.com and search for administrative errors such as duplicate accounts, misspelled addresses, or illegal re-aging of dates.

● Bypass e-OSCAR: Never use online dispute buttons, as they feed your claim into the automated e-OSCAR system, which reduces complex complaints to simple codes that creditors automatically deny.

● Demand Physical Verification: Draft a Section 609 dispute letter demanding original, physical proof of the debt bearing your signature Send this via USPS Certified Mail with a Return Receipt. The bureau has exactly 30 days to verify the debt; because collection agencies often lack original contracts, the unverified item must be legally deleted

● Execute Pay-for-Delete: For legitimate debts, paying the balance online simply changes the status to a "Paid Collection," which still damages your score. Instead, negotiate a "Pay-for-Delete" settlement in writing, offering payment only under the strict condition that the agency completely removes the account from all reporting agencies.

● Escalate Inaction: If bureaus stall after 30 days, send a firm follow-up stating you are forwarding the correspondence to the Consumer Financial Protection Bureau (CFPB) to force compliance.

Expert Verdict: Mastering the Algorithmic Shift

The transition from legacy credit scoring to AI-driven cash-flow underwriting marks a fundamental paradigm shift in US consumer finance Lenders in 2026 are no longer simply

evaluating your past; they are algorithmically predicting your financial future In this hyper-automated environment, passivity is inherently penalized.

Your digital financial footprint is essentially a living, breathing negotiation While predictive underwriting models have become increasingly ruthless, the data fueling them remains surprisingly fragile and often legally vulnerable By shifting from a reactive borrower to a proactive data manager aggressively auditing bureau reports, leveraging FCRA mandates to force physical verification, and strategically timing your credit utilization you effectively neutralize the algorithmic advantage held by financial institutions

Ultimately, creditworthiness today is not a definitive verdict handed down by a machine; it is a metric you must actively engineer Reclaiming control over your reporting data is no longer just about securing favorable interest rates it is the prerequisite for maintaining your economic autonomy in the modern digital age.

Roman Sommer (RomanS) Financial Systems Analyst & Credit Optimization Expert