Foroverthreedecades, RedChiphaschampioned emergingcompaniesthat capturedusthrough compellinggrowthstories, backedbysolid fundamentals Our diligence processidentifieshidden gems-promisingsmall-cap companiesforinvestors seekingearlyexposureto tomorrow'smarketleaders.

1.Management

Weassessleadershipteams basedontheircredibilityto ledagivenmarket,industry expertise,andarecprdof deliveringonpromises.Key factprs”consistent messaging,accessibilityto investors,visibility,anda clearlyarticulatedbusiness strategy

2.MassAppeal

Ourevaluationseeks companieswithuniqueand easilyunderstoodvalue propositionsthatresonate acrossthemarket.Welook forbusinesseswithclearly competitivemoats,intuitive growthcatalysts,andability todifferentiatewithinagiven market

3.GrowingSales

Weseekapipelineof developmentandmarket penetration.Ourfocusis findingcompaniesthat demonstratesustainable growthfromitscustomers, geographicexpansion,or productinnovation, supportedbyrealistic forecasts.

4.ImprovingMargins

Weprioritizeoperational efficiencyandcostdiscipline, prioritizingcompanieswith consistentmarginexpansion. Ouridealclientscombine operationalleverage,pricing power,andscalablebusiness modelstodriveincreasing profitabilityandreturnson capital.

Severaltransformativesectorsare positionedforsignificantadvancementin 2025,particularlyinhealthcareinnovation, sustainableenergysolutions,andnew applicationsforartificialintelligence

Breakthroughdevelopmentsin biotechnologyandprecisionmedicine continuetoreshapepatientcare,while next-generationmanufacturingprocesses andadvancedmaterialsdriveinnovation acrosstraditionalindustrialsectors

Informationcontainedhereinmay includestatementsaboutfuture expectations,projections,and businessprospectsthatconstitute forward-lookingstatements.Analyst reportsandinstitutionalcoverage referencedhereinhavebeen preparedbyotherfirmsandarenot affiliatedwithRedChipCompanies, Inc Thesethird-partyanalysesare providedforinformationalpurposes only,andRedChipmakesno representationsregardingtheir accuracyorcompleteness. Investorsshouldconducttheirown duediligenceandrelyontheirown judgmentwhenmakinginvestment decisions.

WhileRedChipstrivestoprovide accurateinformationand analysis,pastperformancedoes notguaranteefutureresults Somecompaniesmentioned maybeclientsofRedChip Companies,Inc,forwhichwe receivecompensationformedia anddigitalcampaignservices. Notallcompaniesdiscussedare currentclients.Readersshould beawarethatforward-looking statementsinvolveinherentrisks anduncertainties,andactual resultsmaydiffermateriallyfrom projections Thisisnotanofferto buyorsellsecurities

Market Cap: $231.0 million

Price (1/2/2025): $19.89

Price Target: $27.00

Upside To Target: 35.75% (AGP) Research Coverage: Alliance Global Partners, Northland Securities

Thesis: Gorilla Technology Group Inc. (NASDAQ: GRRR) continues to solidify its position as a global leader in AI-driven security, network intelligence, and IoT solutions, driving innovation across multiple industries. In 2024, Gorilla achieved remarkable growth, with a 222% increase in sales during the first half of the year, significantly bolstering its market position. The company ' s strategic partnerships, including collaboration with Edgecore Networks to launch self-branded AI GPUs, have expanded its product offerings and market reach. Gorilla also secured a groundbreaking $270 million Smart Government Security Convergence solution contract in Egypt, marking its largest customer win to date. The company ' s robust pipeline has exceeded $2 billion in opportunities, including ongoing projects in Southeast Asia and significant contracts in Taiwan, including AIpowered solutions for law enforcement and telecom providers

As it heads into 2025, Gorilla's $93 million backlog and expected revenue of $90-$100 million, coupled with an EBITDA margin of 20-25%, provide a solid foundation for sustained growth Additionally, Gorilla's completion of preferred share conversions and strategic capital management, including a share buyback program, has strengthened its balance sheet and enhanced shareholder value. With these achievements and its forward-looking growth strategy, Gorilla is poised for continued success, making it an attractive opportunity for investors seeking exposure to the rapidly expanding AI and cybersecurity markets.

Market Cap: $446.8 million

Price (1/2/2025): $9.15

Price Target: TBD

Upside: Exceeding Targets

Research Coverage: ThinkEquity, Trickle Research

Thesis: Alliance Entertainment presents an attractive investment opportunity as the undisputed leader in physical media distribution, with an unparalleled scale and entrenched relationships across the entertainment and retail sectors. With an extensive catalog and a network that spans major retailers such as Walmart, Amazon, and Best Buy, the company is strategically positioned as a critical gateway for music, movies, video games, and collectibles In fiscal 2024, Alliance executed a significant financial turnaround, achieving a $40 million improvement in net income and boosting adjusted EBITDA to $24.3 million, driven by operational efficiencies and a growing direct-to-consumer sales model

The company ' s latest acquisition of Handmade by Robots, a highly soughtafter collectible brand, expands its footprint in the lucrative collectibles market, with plans for broader distribution across both traditional retail channels and ecommerce platforms. This strategic move, combined with a reduction in debt and a focus on profitable product segments, positions Alliance Entertainment for continued growth and profitability. With a robust business model focused on expansion and M&A, Alliance is primed to sustain its leadership position and deliver strong returns to investors.

Market Cap: $43.1 million

Price (1/2/2025): $1.15

Price Target: $10.00 (Ladenburg Thalmann)

Upside To Target: 1,639.13%

Research Coverage: Ladenburg Thalmann, Baird, HC Wainwright & Co.

Thesis: Calidi Biotherapeutics, Inc. (NYSE American: CLDI) is positioned for a transformative year in 2025, with multiple clinical milestones set to advance its position in the oncology space The company is making significant strides in its development of RTNova (CLD-400), a novel systemic antitumor virotherapy platform that has shown remarkable potential in preclinical studies Designed to overcome immune clearance challenges, RTNova utilizes a tumor-selective vaccinia virus to target multiple metastatic tumor sites, offering a new approach to treat disseminated solid tumors.

This system not only has the potential to kill tumor cells but also to reprogram the tumor immune microenvironment, making it a versatile platform for expanding therapeutic applications. Calidi's NeuroNova (CLD-101), a stem-cell based platform that enhances the delivery of oncolytic viruses, recently received FDA clearance for a Phase 1b/2 clinical trial targeting newly diagnosed highgrade gliomas, expected to commence in early 2025 at Northwestern University.

This follows the company’s successful presentation of RTNova data at major oncology conferences, highlighting its potential in metastatic lung cancer With the continued development of its clinical pipeline and the promising results from its preclinical studies, Calidi offers a compelling opportunity for investors in 2025

Market Cap: $250.0 million

Price (1/2/2025): $4.98

Price Target: $5.91

Upside To Target: 18.67% (Ventum)

Research Coverage: Roth MKM, Canaccord Genuity, Ventum

Thesis: Eos Energy Enterprises Inc. (NASDAQ: EOSE) is rapidly establishing itself as a leader in the clean energy transition with its breakthrough zinc-based longduration energy storage solutions. In December 2024, the company secured a $303.5 million loan guaranteed by the U.S. Department of Energy, a key milestone that will support the scaling of its manufacturing capabilities and facilitate the expansion of its operations under Project AMAZE.

This funding will enable Eos to meet the surging demand for its innovative energy storage systems, with plans to increase production capacity to 8 GWh by 2027. Eos' Z3™ technology, already deployed in significant projects such as the 216 MWh order with City Utilities and a 400 MWh contract with International Electric Power, positions the company at the forefront of the utility-scale energy storage market.

In addition, Eos has made strides in expanding its commercial pipeline, which now totals $14.2 billion, with strategic partnerships and a growing presence in key markets. With its expanding order backlog, strong customer sentiment, and a focus on American manufacturing, Eos Energy Enterprises is well-positioned to capitalize on the global shift to sustainable and reliable energy storage solutions.

Market Cap: $251.1 million

Price (1/2/2025): $3.11

Price Target: $4.50

Upside To Target: 44.69% (Roth)

Research Coverage: Roth MKM, Canaccord Genuity

Thesis: High Tide Inc. (NASDAQ: HITI) has solidified its position as a dominant player in the cannabis retail and e-commerce industry, achieving remarkable growth and profitability in 2024. The company ' s unique business model, driven by its Canna Cabana chain and innovative Cabana Club membership program, has allowed High Tide to capture 12% of the market share in key Canadian provinces, a significant achievement in the highly competitive cannabis market. High Tide's retail expansion continues with the addition of 29 new Canna Cabana locations, bringing the total to 191 stores across Canada.

The company achieved record quarterly revenue of $131.7 million, two consecutive quarters of positive net income, and five straight quarters of positive free cash flow, culminating in a cash-on-hand balance of $35.3 million In addition, High Tide's international reach is expanding, with the successful launch of its Cabana Club membership program in the U S and Europe, already attracting millions of international members. With a strong operational foundation and an aggressive growth strategy, including the acquisition of the Queen of Bud brand and plans for further European expansion, High Tide is wellpositioned for continued success. The company ' s market-leading position and innovative offerings, coupled with its strong cash reserves and disciplined growth, make it a compelling investment opportunity in the cannabis sector.

Market Cap: $34.5 million

Price (1/2/2025): $3.19

Price Target: TBD

Upside To Target: TBD

Thesis: Lantern Pharma Inc (NASDAQ: LTRN) is a pioneering clinical-stage biotechnology company focused on transforming oncology drug discovery and development With its proprietary RADR® AI platform, Lantern has accelerated the development of a robust pipeline of targeted cancer therapies, including LP184 and LP-300, which are advancing through Phase 1 and Phase 2 clinical trials In 2024, Lantern received Fast Track Designation from the FDA for LP-184 for both glioblastoma and triple-negative breast cancer (TNBC), underscoring the drug's potential in addressing critical unmet needs in these aggressive cancers

The company ' s LP-300 candidate is also progressing well in the Phase 2 Harmonic™ trial, showing promising results in non-small cell lung cancer (NSCLC) patients, particularly in those who are never-smokers, a market with significant unmet therapeutic needs With a strategic focus on synthetic lethality, Lantern's pipeline targets both solid and hematologic cancers, with an estimated combined market potential exceeding $15 billion Lantern's collaboration with Starlight Therapeutics for CNS cancers and its ongoing efforts to optimize combination therapies through RADR® further strengthen its leadership in precision oncology With a solid cash position of $28.1 million as of September 2024, Lantern is well-positioned to continue driving innovation in oncology

Market Cap: $53.5 million

Price (1/2/2025): $4.81

Price Target: TBD

Upside To Target: TBD

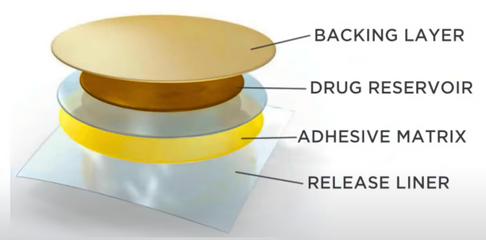

Thesis: Nutriband Inc. (NASDAQ: NTRB) is transforming the pharmaceutical landscape with its AVERSA™ abuse-deterrent technology, designed to improve the safety profile of opioid medications and combat the opioid crisis. In 2024, the company made significant strides, including advancing its lead product, AVERSA™ Fentanyl, toward regulatory submission in 2025.

This groundbreaking product is poised to become the world's first abusedeterrent opioid transdermal patch, with projected peak U.S. sales ranging from $80 million to $200 million. Nutriband's commitment to innovation is reflected in its expanding global intellectual property portfolio, securing patent approvals in 46 countries, including China and Hong Kong.

The company also posted a 51% year-over-year revenue increase, with Q3 revenue reaching $645,796, and successfully raised $8.4 million through a private placement to fuel its regulatory and commercialization efforts. Beyond AVERSA™ Fentanyl, Nutriband is expanding its pipeline with additional AVERSA™ applications, including AVERSA™ Buprenorphine, which has the potential to generate $130 million in annual revenues. With a strong financial foundation and a focused strategy on regulatory approval and commercial launch, Nutriband is well-positioned to lead the market in abuse-deterrent transdermal drug delivery solutions, offering significant upside for investors.

Market Cap: $68.2 million

Price (1/2/2025): $1.98

Price Target: $16.00

Upside To Target: 708.08% (D. Boral Capital)

Research Coverage: Rodman & Renshaw, Maxim, H.C. Wainwright, D. Boral Capital

Thesis: FibroBiologics Inc (NASDAQ: FBLG) is a pioneering clinical-stage biotechnology company focused on fibroblast-based therapies to address chronic diseases with significant unmet medical needs In 2024, the company made substantial progress with its lead candidate, CYWC628, a fibroblastbased spheroids product targeting diabetic foot ulcers (DFUs).

Preparations for a Phase 1/2 clinical trial in Australia are underway, with trials expected to begin in Q2 2025. FibroBiologics has also significantly strengthened its intellectual property portfolio, holding over 160 patents issued and pending across a wide range of therapeutic areas, including wound healing, cancer, and multiple sclerosis

The company recently expanded its R&D pipeline, moving its CYPS317 psoriasis candidate into development, while also advancing its human longevity program, which includes promising results in T-cell generation. With a $25 million financing agreement and strategic collaborations with industry leaders like Charles River Laboratories, FibroBiologics is well-positioned to drive the next wave of breakthroughs in regenerative medicine. With an expanding product pipeline and a strong intellectual property position, FibroBiologics offers an attractive opportunity for investors seeking exposure to the rapidly evolving cell therapy and biotechnology sectors

Market Cap: $97.6 million

Price (1/2/2025): $5.84

Price Target: $18.00

Upside To Target: 208.22% (H.C. Wainwright)

Research Coverage: D. Boral Capital, H.C. Wainwright, Chardan Capital, BTIG, Rodman & Renshaw

Thesis: Coya Therapeutics, Inc (NASDAQ: COYA) is a clinical-stage biotechnology company focused on advancing Treg-enhancing therapies for neurodegenerative and autoimmune diseases. The company ' s lead candidate, COYA 302, combines low-dose interleukin-2 (LD IL-2) with CTLA4-Ig to restore immune balance and target chronic inflammation associated with diseases such as ALS, Frontotemporal Dementia (FTD), Parkinson's Disease, and Alzheimer's Disease Coya recently reported significant progress, including positive Phase 2 results for LD IL-2 in Alzheimer's patients and the initiation of a Phase 1 study in FTD patients, set to inform future clinical trials

The company ' s robust pipeline is bolstered by strategic partnerships, notably with Dr Reddy's Laboratories, for ALS, and a growing cash runway, including a $10 million private placement With a new leadership transition under CEO Arun Swaminathan, Coya is poised to advance its promising therapies into pivotal clinical stages, offering a compelling opportunity for investors seeking exposure to transformative treatments in neurodegenerative diseases

Market Cap: $24.5 million

Price (1/2/2025): $0.89

Price Target: TBD

Upside To Target: TBD

Thesis: Trinity Biotech plc (NASDAQ: TRIB) is a transformative player in the biotechnology sector, specializing in human diagnostics and diabetes management solutions The company has made significant strides in 2024, including securing approval from the World Health Organization (WHO) to offshore manufacturing for its TrinScreen HIV and Uni-Gold HIV products, a move set to enhance margins and production efficiency by Q1 2025 This achievement is a key milestone in the company ' s Comprehensive Transformation Plan, which is driving long-term profitability through operational improvements and strategic investments

With a focus on expanding its diagnostics portfolio, including the development of innovative Continuous Glucose Monitoring (CGM) technology, Trinity is positioning itself for sustained growth in the $10 billion CGM market Recent acquisitions, such as Waveform Technologies' biosensor assets, complement this growth trajectory, diversifying Trinity's product offerings and enhancing its capabilities in the wearable biosensor market With a stronger financial position bolstered by a $5 5 million liquidity boost and a strategic partnership with Perceptive Advisors, Trinity Biotech is well-positioned to capitalize on global demand for its diagnostics solutions and drive shareholder value in the years ahead

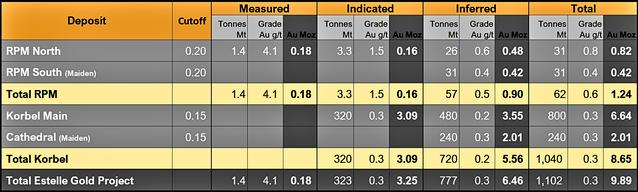

9 MILLION Oz of GOLD

Cap: $65.9 million

(1/2/2025): $14.39

$25.00

73.73%

Research Coverage: ThinkEquity

Thesis: Nova Minerals Limited (NASDAQ: NVA) is rapidly advancing its flagship Estelle Gold and Critical Minerals Project in Alaska, positioning itself as a key player in both gold and antimony production Spanning over 514 square kilometers, the project hosts a multi-million-ounce gold resource and over 20 high-potential prospects, including significant antimony findings that are particularly strategic given the growing demand for critical minerals.

In 2024, the company reported impressive exploration results, including antimony grades as high as 56.7%, signaling the potential for a substantial new resource at the Stibium prospect. With a focus on expanding its gold and antimony assets, Nova is also strategically positioning itself in the defense and critical minerals sectors, benefiting from antimony's strategic importance as a mineral essential to U S national security

The company ' s robust financial position, bolstered by recent divestments, reduced debt, and successful warrant exercises, ensures the continued funding of its aggressive exploration and development strategy. With a well-defined roadmap for exploration in 2025 and a prime location in the prolific Tintina Gold Belt, Nova Minerals is poised for significant growth, offering substantial upside potential for investors as it moves toward unlocking the full potential of its Estelle Project.

Cap: $873.7 million

(1/2/2025): $25.82 Price Target: $30.00 Upside To Target: 16.19% (Northland Securities) Research Coverage: Northland, Lake Street, Rosenblatt, Truist, Barrington

Universal Technical Institute, Inc. (NYSE: UTI) continues to experience strong growth driven by its comprehensive workforce solutions, positioning itself for long-term success in the education sector For fiscal year 2024, the company reported a 20.6% increase in revenue to $732.7 million and a significant 240.9% surge in net income to $42.0 million, fueled by a solid increase in new student starts.

The UTI division contributed 15,138 new students, while Concorde Career Colleges added 11,747. These results reflect the company ' s effective execution of its "North Star Strategy," which focuses on growth, diversification, and margin expansion. As UTI enters fiscal 2025, it has set revenue guidance between $800 million and $815 million, along with expectations for adjusted EBITDA growth

Additionally, UTI's strategic initiatives, such as launching new programs, expanding campuses, and leveraging deep industry partnerships, support its expansion across key sectors like transportation, skilled trades, and healthcare. Analysts raised their target prices for UTI following its FY24 results, with Northland Capital increasing the price target to $24, Barrington Research to $25, and Truist Securities to $26, reflecting strong confidence in UTI's future growth trajectory.

Market Cap: $337.8 million

Price (1/2/2025): $12.85

Price Target: $15.00

Upside To Target: 16.73% (Piper Sandler)

Research Coverage: B. Riley, Piper Sandler, KBW, Compass

NewtekOne, Inc. (NASDAQ: NEWT) is a financial holding company offering a comprehensive suite of business and financial solutions to independent business owners across the United States. In the third quarter of 2024, the company reported a net income of $11.9 million (Q3), or $0.45 per share, marking a 4.7% increase compared to the previous quarter. Total assets grew to $1.7 billion, with loans held for investment rising by 13 3% year-over-year

Net interest income reached $11.0 million, a 20.9% increase over the prior quarter, while the Newtek Payments segment achieved a pretax income of $5.3 million, reflecting a 32.5% growth year-over-year. The company also completed a $75 million public offering of fixed-rate senior notes, strengthening its financial position. Strategic initiatives included closing a $154.3 million alternative business loan securitization and entering an agreement to sell its subsidiary, Newtek Technology Solutions, as part of its transition to a financial holding company. NewtekOne maintains its annual EPS forecast for 2024 in the range of $1 85 to $2 05, with expectations for continued growth in 2025

Market Cap: $1.52 billion

Price (1/2/2025): $4.32

Price Target Range: $19.00

Upside To Target: 339.81% (Deutsche Bank)

Research Coverage: H.C. Wainwright, TD Cowen, Jefferies, Bank of America, Morgan Stanley, Deutsche Bank

Thesis: Evotec SE (NASDAQ: EVO) is a leading biotechnology company specializing in drug discovery and development solutions across various therapeutic areas, including neurology, oncology, and metabolic diseases. With a unique platform of proprietary technologies, Evotec has established itself as a pivotal player in advancing innovative therapies globally.

The company collaborates with over 500 biopharma companies, including major industry leaders such as Novo Nordisk, Pfizer, and Bristol-Myers Squibb, to accelerate the development of first-in-class and best-in-class treatments Evotec's integrated drug discovery capabilities are exemplified by its LAB eN² collaboration with Novo Nordisk, aimed at translating academic research into novel therapeutics for cardiometabolic diseases.

Additionally, Evotec's growing portfolio includes more than 200 co-owned R&D projects spanning a wide range of therapeutic areas. With a strong emphasis on operational and scientific excellence, Evotec is well-positioned for sustained growth and continued leadership in the global pharmaceutical and biotechnology sectors

Market Cap: $18.5 million

Price (1/2/2025): $5.14

Price Target Range: TBD

Upside To Target: TBD

Thesis: Electro-Sensors, Inc. (NASDAQ: ELSE) is a leading global provider of machine monitoring sensors and hazard monitoring systems In the third quarter of 2024, the company reported a 22.1% increase in revenue to $2 51 million, driven by higher sales of both its wired sensor products and wireless HazardPRO™ systems.

This growth was particularly bolstered by demand in industrial automation and agricultural applications. Electro-Sensors also saw a significant improvement in its gross margin, rising to 50.4% from 48.3% in the same period last year, reflecting better supply chain stability and the benefits of earlier price adjustments. Operating income surged to $173,000, a notable turnaround from the loss of $26,000 in Q3 2023.

With a solid cash position of $10.3 million as of September 30, 2024, the company is well-positioned for future growth. Electro-Sensors' ongoing focus on innovation and customer demand positions it as a key player in the machine and hazard monitoring systems market, with a robust pipeline expected to sustain its upward trajectory.

Market Cap: $773.3 million

Price (1/2/2025): $15.74

Price Target Range: TBD

Research Coverage D.A. Davidson

Thesis: ADS-TEC Energy plc (NASDAQ: ADSE) is a leading innovator in ultra-fast charging technology, specializing in battery-buffered solutions that address the challenges of low-to-medium power grid capacity for electric vehicles (EVs). In the first half of 2024, the company saw a remarkable 107% year-over-year revenue increase to €79.3 million, driven by an expanding customer base and strategic partnerships with key blue-chip clients

ADS-TEC's growth was further supported by a 295% increase in its paying customer base, along with significant collaborations such as those with Caverion, Porsche, and Paragon Mobility These partnerships are accelerating ADS-TEC's market penetration in Europe and North America The company is on track for continued revenue growth, with expectations to achieve Adjusted EBITDA profitability for the full year 2024

Additionally, ADS-TEC's ChargeBox technology is gaining momentum, offering businesses a cost-effective, ultra-fast charging solution that saves on utility upgrades and enhances operational efficiency. With increasing demand for EV infrastructure, ADS-TEC is poised to play a pivotal role in the global transition to sustainable energy, particularly through its scalable, flexible charging solutions.

Market Cap: $1.91 billion

Price (1/2/2025): $138.54

Price Target Range: $150.00

Upside To Target: 8.27% (CJS) Research Coverage: Lake Street, CJS Securities

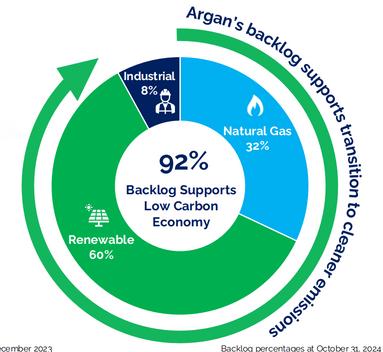

Thesis: Argan, Inc. (NYSE: AGX) is a leading provider of engineering and construction services, primarily in the power industry. For the third quarter of fiscal 2025, the company reported a 57% year-over-year increase in consolidated revenues to $257 million, with net income soaring to $28 million, or $2 00 per diluted share This performance was driven by strong execution across Argan's diverse business segments, particularly in the power industry, which saw a 75% revenue growth to $212 million.

The company ' s backlog reached $800 million, with nearly 60% ($478 million) attributed to renewable energy projects, underscoring its strategic diversification into the renewable energy sector. Argan's robust balance sheet, including $506 million in cash and no debt, provides significant financial flexibility. The company also declared a quarterly dividend of $0.375 per share, payable on January 31, 2025, reflecting its commitment to shareholder returns With strong demand for natural gas and renewable projects, as well as a growing pipeline fueled by increasing power demand from data centers, manufacturing reshoring, and electric vehicle infrastructure, Argan is wellpositioned for sustained growth and market leadership in both traditional and renewable energy markets.

Market Cap: $735.2 million Price (1/2/2025): $43.56

Price Target Range: $45.00

Upside To Target: 3.31% (Barrington, Roth MKM)

Research Coverage: Barrington, Roth MKM, Sidoti

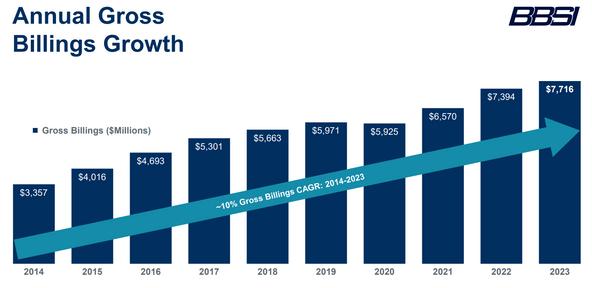

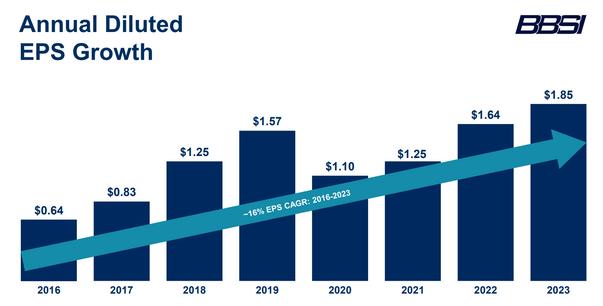

Thesis: Barrett Business Services, Inc. (NASDAQ: BBSI) continued to demonstrate strong financial performance and strategic growth in Q3 2024, driven by robust client retention and market expansion The company reported an 8% increase in revenue to $294.3 million and net income of $19.6 million, or $0 74 per diluted share, highlighting solid growth in professional employer services.

BBSI's strong performance was further evidenced by a 9% rise in gross billings, which reached $2.14 billion, fueled by an increase in worksite employees (WSEs) and higher average billings per WSE. The company continues to maintain a debt-free status and reported $94.4 million in unrestricted cash as of September 30, 2024. Additionally, BBSI remains committed to returning capital to shareholders, with $2.1 million in dividends paid during the quarter at a raised dividend rate of $0 08 per share, reflecting a 16% dividend payout ratio

With strong growth in WSEs, market share expansion in new geographies like Idaho, and a robust capital allocation plan including a $75 million share repurchase program BBSI is positioned for continued success. As it scales operations and expands its value-added offerings, such as BBSI Benefits, the company remains poised for further growth in the business management solutions sector.

Market Cap: $378.0 million

Price (1/2/2025): $2.69

Price Target Range: €33 (EUR)

Upside To Target: 13.79% (Kepler Capital)

Research Coverage: Kepler Capital

Thesis: FREYR Battery Inc. (NYSE: FREY) is transforming the clean energy landscape through its ambitious strategy of integrating solar and battery storage technologies. The company has recently bolstered its position with the acquisition of Trina Solar's U.S. solar manufacturing assets, which includes a 5GW solar module manufacturing facility in Wilmer, Texas.

This acquisition, which began production in November 2024, is expected to ramp up to full capacity by 2025, with a significant portion of the output secured by firm offtake contracts with U S customers Alongside this, FREYR is advancing plans for a U S solar cell production facility, expected to begin construction in 2025, with a target start of production in 2026 These initiatives establish FREYR as a leader in the U.S. solar market and align with the growing demand for integrated clean energy solutions.

The company is also capitalizing on the U.S. Inflation Reduction Act (IRA) incentives, positioning its vertically integrated U.S. operations for competitive advantage. By 2025, FREYR anticipates significant EBITDA growth, with projections of $175–225 million, supported by a full U.S. solar module and cell production ramp-up

Market Cap: $963.7 million

Price (1/2/2025): $86.54

Price Target Range: $110.00

Upside To Target: 27.11% (Stifel Nicholaus)

Research Coverage: Stifel Nicolaus, Roth MKM, Lake Street

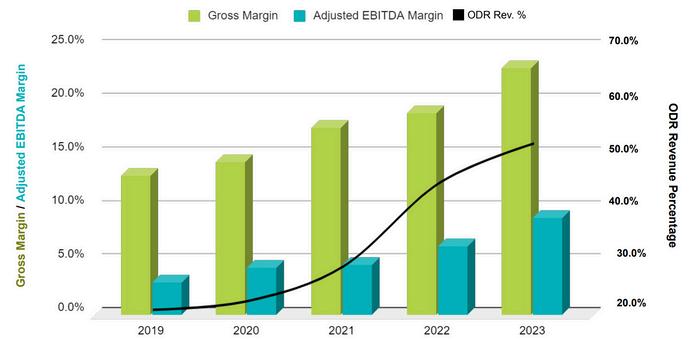

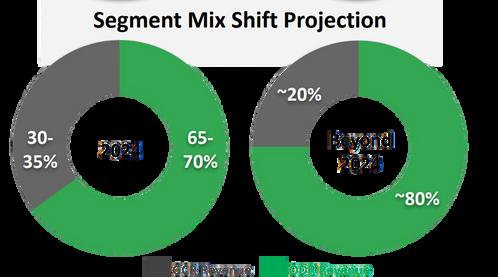

Thesis: Limbach Holdings, Inc. (NASDAQ: LMB) is a leading building systems solutions firm specializing in the design, installation, and maintenance of complex mechanical, electrical, and plumbing systems. The company reported a 4.8% increase in total revenue, reaching $133.9 million, driven by a 41.3% surge in Owner Direct Relationships (ODR) revenue, which now constitutes 69.4% of total revenue. This growth, combined with a 15.6% rise in gross profit and a record $17.3 million Adjusted EBITDA, reflects the success of Limbach's strategic shift towards direct relationships with building owners.

The company also raised its 2024 Adjusted EBITDA guidance, now expecting a range of $60 million to $63 million, further highlighting its strong financial outlook. Limbach's recent acquisition of Kent Island Mechanical expands its regional footprint in the Greater Washington, D.C. metro area and enhances its industrial sector services, positioning the company for further expansion.

Additionally, with a growing backlog of $658.1 million, Limbach is wellpositioned to capitalize on strong demand across its target markets, including data centers, healthcare, and industrial sectors. With a disciplined acquisition strategy and a focus on high-margin, owner-direct work, Limbach is poised for continued growth, making it an attractive investment opportunity

Market Cap: $1.31 billion

Price (1/2/2025): $33.12

Price Target Range: TBD

Upside To Target: TBD

Thesis: Banco Latinoamericano de Comercio Exterior, S.A. (NYSE: BLX), commonly known as Bladex, has demonstrated strong financial performance in the third quarter of 2024, with net profits reaching $53.0 million, or $1.44 per share, marking a 16% year-over-year increase. This performance was driven by a solid 8% year-over-year revenue growth and a 10% increase in net interest income, reflecting Bladex's effective management of lending volumes and spreads.

With a return on equity (ROE) of 16.4%, Bladex continues to outperform expectations, driven by its diverse and expanding credit portfolio, which reached an all-time high of $10 87 billion, up 18% year-over-year The bank's healthy asset quality is further supported by a strong liquidity position, with $1.7 billion in liquid assets, and a low impairment ratio of 0.2% in the credit portfolio. Bladex's continued profitability is further demonstrated by its robust capital base, with Tier 1 and regulatory capital adequacy ratios well above required levels.

Additionally, the bank's dividend policy reflects its solid financial standing, with a quarterly cash dividend of $0.50 per share approved for Q3 2024 Positioned as a key player in trade finance across Latin America and the Caribbean, Bladex is well-placed to capitalize on growing regional trade and investment opportunities.

Market Cap: $1.73 billion

Price (1/2/2025): $13.61

Price Target Range: $16.30

Upside To Target: 19.77% (CMB International)

Research Coverage: CMB, Goldman Sachs, Citi, Bank of America Securities, Deutsche Bank, Morgan Stanley

Thesis: Hesai Group (NASDAQ: HSAI) continues to lead the lidar technology space, achieving impressive growth and operational milestones that solidify its position in the autonomous and electric vehicle industries. In Q3 2024, the company reported a 182 9% year-over-year increase in lidar shipments, reaching 134,208 units, alongside a 21.1% rise in net revenues to $76.9 million

Hesai's ability to scale rapidly is underscored by its achievement of delivering over 100,000 lidar units in a single month, making it the first lidar company to reach this milestone. With strategic wins in both the ADAS and robotics markets, Hesai is expanding its footprint with key partnerships, including a major deal to exclusively supply 1.5 million lidar units to Changan Automobile for multiple vehicle models starting in 2025.

The company ' s next-generation lidar, the ATX, has gained significant traction among top automotive manufacturers, driving further adoption of its highperformance, cost-efficient technology Looking ahead, Hesai is set for explosive growth with plans to achieve annual capacity exceeding 2 million units by 2025. With a robust pipeline, strong OEM relationships, and anticipated profitability in 2024, Hesai is positioned to dominate the lidar market and drive the global transition to autonomous and electric vehicles.

Market Cap: $1.20 billion

Price (1/2/2025): $10.93

Price Target Range: $15.00

Upside To Target: 37.24% (Wells Fargo)

Research Coverage: Northland, BTIG, Wells Fargo, KeyBanc, Robert W. Baird, Wedbush, UBS, Piper Sandler

Thesis: The RealReal, Inc. (NASDAQ: REAL), the world's largest online marketplace for authenticated luxury resale, continues to experience robust growth, positioning itself as a leader in the booming circular economy. In Q3 2024, the company reported a strong 11% year-over-year increase in revenue to $148 million, driven by a 6% rise in gross merchandise value (GMV) and a 14% growth in consignment revenue

Adjusted EBITDA surged by $9 million, reflecting the company ' s operational efficiency and successful execution of its strategy to expand its consignment business. This performance was complemented by a growing active buyer base, a 4% increase in orders, and a rise in average order value, signaling healthy demand for luxury resale goods. Furthermore, The RealReal is capitalizing on its expanding retail footprint, with new stores in Miami and Houston, solidifying its presence in key markets.

Northland Capital and Wells Fargo recently raised their price targets for the company to $12.50 and $15, respectively, highlighting investor confidence in its growth trajectory. With a proven business model, a scalable platform, and a strong financial outlook, The RealReal is poised for continued growth, making it an attractive investment opportunity in the luxury resale sector.

Market Cap: $219.0 million

Price (1/2/2025): $21.90

Price Target Range: $24.00

Upside To Target: 9.59% (Maxim)

Research Coverage: Maxim Group, D.A. Davidson

Thesis: ReposiTrak, Inc. (NYSE: TRAK) is the world's largest food traceability and regulatory compliance network, positioning itself as a leader in providing cloud-based solutions to ensure food safety and regulatory compliance. The company has seen impressive growth in 2024, including an 8% increase in firstquarter revenue, reflecting strong demand for its traceability platform, which has rapidly onboarded new suppliers across various sectors, including seafood, nut butter, and produce

This surge in adoption is driven by regulatory deadlines and an increasing number of major retailers requiring full supply chain traceability. As the FDA's 2026 deadline for food traceability approaches, ReposiTrak is well-positioned to capture significant market share, with its hardware-free platform offering seamless compliance solutions.

The company ' s solid financial position, bolstered by $25.8 million in cash and no bank debt, and its commitment to shareholder returns, including a 10% dividend increase, further underscores its strength With a growing pipeline and robust recurring revenue model, ReposiTrak is set to double its annual recurring revenue over the next three years, offering strong growth potential for investors.

Market Cap: $42.0 million

Price (1/2/2025): $9.33

Price Target Range: TBD

Upside To Target: TBD

Thesis: Venu Holding Corporation (NYSE American: VENU) is transforming the live entertainment industry with a business model that combines luxury hospitality, high-margin revenue streams, and innovative public-private partnerships. At the core of its success are Fire Pit Suites, sold as triple-net real estate investments that provide owners with guaranteed rents, tickets to every show, depreciation benefits, and annual returns of 17–19%.

In 2024 alone, these suites generated $77.7 million in revenue, fueling Venu’s rapid growth while de-risking its operations. Supported by partnerships with municipalities, as well as major sponsors like Budweiser, Aramark, Jack Daniels, Coca-Cola, and Ford, Venu minimizes capital requirements while scaling its premium venues

The company expects book value to exceed $30 per share over the next six quarters three times the current stock price and is on track to achieve profitability by Q2 2025, positioning Venu as a high-growth opportunity for stock investors seeking exposure to the booming $35 billion live entertainment sector.