In Focus Issue 31 | Randall & Payne Accountants & Business Advisors

As the year progresses, many business owners are looking ahead, not just to the next quarter, but to the longer-term future of their organisations. In this issue, we are focusing on being ready for what the future means for you and your business.

Ensuring the right succession plan is in place will ensure continued success. Whether your timeline is two years or ten, a well-structured succession or exit strategy is essential to realise the value you have worked hard to build. Planning early gives you greater control, more options, and ultimately a stronger outcome.

We are pleased to announce some exciting changes to our leadership, with Tim Watkins passing the Managing Partner ‘baton’ to Rob Case, who with the promotion of Ben Burch to Partner, will steer the firm for the years ahead. You can read more about both their journeys on pages 4-5.

In this issue, we explore several key areas to support your journey. Our feature on page 11 about our Business & Financial Health Check highlights how gaining a clear understanding of your current position can help identify strengths, risks, and opportunities ahead of a transition. Alongside this, our article on pages 12-13 about

maximising and realising value, examines practical steps you can take now to enhance the attractiveness and worth of your business when the time comes to ask: “how much is my business worth?”

Pages 6-10 cover important regulatory developments, including changes in the Making Tax Digital for Income Tax Self-Assessment legislation, and what these may mean for your planning and reporting obligations.

Finally, our piece on demergers and share structures provides insight into how restructuring can support both exit readiness and long-term succession planning. By taking a proactive and informed approach, you can ensure your business continues to thrive long after your involvement. After all successfully exiting your business is not just an event, it is a process.

I hope you find this issue valuable and thought-provoking.

rob case Managing Partner

Tim Watkins Partner

Specialism: Tax & Agriculture

Will abbott Partner

Specialism: Business Advisory

ollie newbold Partner

Specialism: Corporate Finance

ryan Moore Partner

Specialism: Audit

nikki cairns Partner

Specialism: Accounts

shaun pegler Partner

Specialism: Accounts

James Geary Partner

Specialism: Corporate Tax

Ben Burch Partner

Specialism: Audit

nicholas Gratton

Client Director

Specialism: Accounts

Subscribe at www.randall-payne.co.uk/ news/subscribe-to-in-focus

Celebrating our staff; from promotions to wedding congratulations

TAX | 6-7

Landlords: Do you know what’s changing in 2026?

CORPORATe TAX | 8

Optimising your business structure

TAX | 9

How we protect you when HMRC comes calling

ACCOuNTING SeRVICeS | 10

Making Tax Digital for Income Tax is here: Digital quarterly reporting for businesses

ACCOuNTING SeRVICeS | 11

Unlocking full potential with a Business & Personal Financial Health Check

CORPORATe FINANCe & | 12-13

BuSINeSS AdVISORy

What is my business worth? Is this the question you should be asking?

AudIT - ACAdemIeS | 14

DfE reporting: What Academy Trusts need to know for 2025-26

P 12 What is my business worth?

PAyROll | 15

Getting statutory holiday pay right from the start

IN The COmmuNITy | 16-17

Celebrating B Corp month and introducing our charity partner

GueST ARTICle | 18

Is your website quietly costing you leads?

eVeNTS | 19

Key dates for your diary

My journey to Managing Partner

Joining Randall & Payne straight from school more than 20 years ago, I could not have imagined the path that lay ahead. It is a privilege now to step into the role of Managing Partner and help lead the firm into its next chapter.

What has kept me here throughout my career is the strong sense of identity and purpose that runs through the firm. We have a shared commitment to doing the right thing for our clients, our people and the wider community.

My career began as a trainee, learning the fundamentals and developing a deep appreciation for the trust clients place in us. Over time, I progressed through the firm and have now been a partner for over half of my career. That journey has given me a broad perspective, not just on the technical aspects of our work, but on culture and what it takes to build a firm for the long term.

I have had the opportunity to work closely alongside Tim for many years and under his leadership the firm has grown sustainably, whilst continuing to invest significantly in our people and positive experience for clients. One of the proudest achievements of this time was achieving B Corp certification, which reflects our commitment to balancing profit with purpose and operating responsibly. Tim remains closely involved

with the firm, continuing to support clients, colleagues and the senior team, and I am grateful for his guidance and the strong foundations he has helped create.

The accountancy profession is amid constant change. Advances in technology, increasing regulation and shifting client expectations, continue to reshape how firms operate. I have been closely involved in helping to navigate these changes, particularly in embracing technology where it genuinely adds value. Used well, technology enhances efficiency and insight, but it is not a replacement for judgement, experience or trusted relationships.

As I take on the role of Managing Partner, my focus is on ensuring we continue to deliver clarity and confidence to clients in an increasingly complex environment. While core services may be delivered differently in future, our real value lies in our people. Investing in our team and supporting long term career development remain central priorities, underpinned by our people’s expertise,

curiosity and ability to understand each client’s unique situation.

Looking ahead, sustainable growth, innovation and responsible business will continue to guide our strategy. These are not new ambitions, but ones deeply rooted in Randall & Payne’s values and culture. I am particularly passionate about maintaining an environment where people can build fulfilling careers, just as I have, and where clients see us as trusted advisers who go beyond compliance to offer insight and perspective.

This is an exciting time for Randall & Payne. We have a clear vision for the future, a strong and talented team and values that anchor us as we adapt and grow. I am proud to play my part in leading our dynamic senior leadership team and ensuring the firm continues to thrive for generations to come.

contact rob case by emailing rob.case@randall-payne.co.uk or call 01242 776000.

From trainee to partner: Ben joins the partnership

We are delighted that Ben Burch joined the partnership on 1 April 2026.

Ben began his journey with the firm in September 2012, joining as a trainee supporting a wide range of services before specialising in Audit in 2014. Over the years, he has developed deep expertise across academy schools, charities, hospitality, manufacturing, SaaS and UK subsidiary companies, becoming a trusted adviser to clients in these sectors.

In 2022, Ben joined the SLT, taking on key strategic responsibilities that have helped strengthen the firm’s operational and technological foundations. His role includes monitoring emerging technologies and driving firm wide adoption, internal analysis and reporting, acting as a Responsible Individual in Audit, and serving as the firm’s Academies Lead.

Looking ahead, Ben is passionate about embracing new opportunities and ensuring we remain a leading advisory practice. His ambitions include harnessing cutting edge technology to maximise efficiency and enhance client experience, deepening and developing long standing client relationships, and ensuring that “we make your success our priority” continues to be at the heart of everything we do.

Celebrating staff success

Congratulations to the following staff who have also been promoted:

� Alice Prout - Client Manager from April 2026

� James Cook - Senior Audit & Assurance Accountant from February 2026

Joe lock recently passed the certification programme of the R&D Community on R&D Tax Relief which is fast becoming the defining mark of a technically strong and highly ethical R&D tax adviser in the UK.

Congratulations Adam and Lauren

Congratulations to Adam Smith, Assistant Tax Manager, on his marriage to Lauren. The couple tied the knot at A Little White Chapel in Las Vegas on 30 March 2026; an unforgettable setting for the start of their next chapter together.

We wish them both a lifetime of happiness, laughter, and a future filled with love, prosperity, and perhaps just a little well-planned tax efficiency along the way.

Landlords:

Do you know what’s changing in 2026?

This year brings some significant changes for landlords, with new rules being introduced that could affect both the way you report your tax and the rights that your tenants have.

rachel roberts Private Client Tax Manager

To help you navigate what’s changing, we’ve broken the updates down into tax related changes and key legal developments arising from the Renters’ Rights Act.

Income tax changes

Whilst not all the changes mentioned below come into effect in 2026, we have covered the key changes we believe you should be aware of this year.

These are:

Abolishment of the Furnished holiday let (Fhl) Rules

Whilst the FHL rules were abolished last year on 6 April 2025 it means, if you rent out accommodation on a short-term basis, this could impact your 2025/26 tax return, which will be due for submission by 31 January 2027.

Whilst the FHl rules were abolished last year on 6 april 2025 it means, if you rent out accommodation on a shortterm basis, this could impact your 2025/26 tax return

The main changes are:

� Mortgage interest can no longer be deducted against profits, instead you will receive tax relief equal to 20% of the interest paid, meaning if you are a higher rate taxpayer you will pay more tax.

� Capital allowances will no longer be available, meaning you can only claim for the cost of replacing items, not their initial purchase. This will be a particular disadvantage when you are first getting a property ready to be let out.

� Profits must now default to a 50/50 split for spouses or civil partners who jointly

own property. Previously the FHL rules allowed you to choose your profit split. It is still possible to alter the profit split but doing so requires additional legal and tax forms and is less flexible.

� Capital Gains Tax reliefs previously available for FHLs are now no longer available.

� Profits no longer count as relevant earnings for pension contribution purposes. This could affect the amount you can pay into your pension each year.

making Tax digital for Income Tax

The new rules which change the way landlords must keep their records and how your income is reported to HMRC started on 6 April 2026, but not everyone will be affected straight away.

Your start date will depend on your level of gross rental income (i.e. income before any expenses) and turnover from self-employment, if applicable.

The thresholds are as follows:

� Over £50,000 in 2024/25 – start date of April 2026

� Over £30,000 in 2025/26 – start date of April 2027

� Over £20,000 in 2026/27 – start date of April 2028

The new rules will involve keeping digital records and submitting quarterly updates to HMRC for rental income, and self-employment where applicable. These rules are mandatory and penalties will apply for non-compliance.

2% increase on tax due on rental profits

This change was announced in the Autumn 2025 budget and will come into effect from 6 April 2027. As a result, the tax rates applicable to your rental profits will be:

The new rules will involve keeping digital records and submitting quarterly updates to HMrc for rental income, and self-employment where applicable. These rules are mandatory and penalties will apply for non-compliance

that landlords cannot accept a higher rent than what was advertised

� Discrimination against tenants with children or those in receipt of benefits is prohibited

� New grounds for reclaiming possession of a property

� Landlords must consider a tenant’s request to keep a pet in the property and cannot unreasonably withhold consent

Additional systems and standards are expected to be phased in from late 2026 onwards.

In addition, from April 2027, the rules on how the Personal Allowance is applied are changing. It will first need to be offset

against employment income, trading income, or pension income, meaning that you cannot first use it to cover your rental profits, which will be taxed at higher rates than the aforementioned sources, potentially resulting in an increased tax liability.

legal changes

The key changes from the Renters’ Rights Act 2025, effective from 1 May 2026, are:

� End of “no-fault” evictions

� Changes to tenancy agreements

� Controls and limits around how rent is set and increased, including limits on how often rent can be increased, a ban on bidding wars, and a requirement

Given the significance of the new rules and regulations we would recommend that you obtain the appropriate advice and keep up to date with any further changes. The implications of the Renters’ Rights Act or any other legal matters should be discussed with a lawyer.

We are happy to answer questions regarding the tax changes or discuss any potential tax planning opportunities.

contact rachel roberts for more information by emailing rachel.roberts@randall-payne.co.uk or call 01242 776000.

Optimising your business structure

There are many reasons to consider changing your corporate structure, and recognising the need to act at the right time can make a significant difference to your business and personal goals.

We recommend reviewing your corporate structure proactively to position your business to remain competitive, resilient, and ready to take advantage of future opportunities, including being ready for sale.

The apparently easiest solutions are regularly peppered with tax traps, so in this article we give a flavour of what we do and why we do it.

Asset protection

In our experience, probably the most common scenario is the need to better protect assets, such as property or surplus cash. It would be prudent to ring fence these assets from risks, especially in uncertain market conditions. Forming a holding company and moving those assets up to it is the most common solution. This can still be restrictive, particularly where property is considered as separate from the business.

You may want to introduce share incentives to staff, and to be tax efficient these would need to sit within the holding company. Alternatively, you may wish to gift shares to the family without involving the business. With a holding company structure, it is often not possible to do either of these things.

However, you could also have a problem if the trading subsidiary is sold, as the sale proceeds would then sit in the holding company and withdrawing them would result in high rates of dividend tax. Demergers could be a suitable solution to this problem.

demergers

The most common demerger scenarios are where two distinct trading activities are to be separated, or where a trade is to be separated from non-trading assets (such as property, investments or surplus cash).

Demergers are complex transactions but if done correctly, tax reliefs are available which enable them to take place with no tax consequences (although a small Stamp Duty liability may be incurred).

However demergers require advance clearance from HMRC to confirm that the restructure is not tax motivated, so where a business sale is imminent, getting a clearance is unlikely to be possible as HMRC will consider there to be a primary aim of obtaining a tax advantage.

Shareholder exit

When a single shareholder wishes to exit a company, often the most obvious solution is a company purchase of its own shares (CPOS). This is where the company buys back the shares from the individual and then cancels them.

The tax rules around a CPOS contain very specific conditions to enable the proceeds to be taxed as a capital gain and not as income.

Crucially, the shares must have been owned for at least 5 years, and the company must have enough retained profits to fund the CPOS. Failure to meet just one condition would result in the CPOS being liable to Income Tax at dividend rates, or worse, invalidated.

Where it is not possible to use a CPOS, alternative approaches can be considered, from straightforward selling of shares to existing shareholders through to a restructure involving a new holding company. The latter is most useful because the business can then fund the purchase with minimal tax liabilities involved.

There are other scenarios where a restructure may be appropriate so we encourage discussions with your regular Randall & Payne contact, ensuring the tax team can be involved at the right time to explore the best options.

contact James Geary for more information by emailing james.geary@randall-payne.co.uk or call 01242 776000.

Tax Investigation Service:

How we protect you when HMRC comes calling

Even if your tax affairs are in order, HMRC can launch an investigation without warning. Individuals, sole traders and businesses can all be affected, making it essential to be prepared and properly supported.

A tax investigation can take many forms. It might be a simple request for more information, a targeted question about one part of your return, or a full review of your financial records. In some cases, it can extend into VAT, PAYE and R&D inspections. What many people don’t realise is that these enquiries are not always triggered by mistakes. HMRC may simply be carrying out routine checks, using data to spot inconsistencies, or focusing on sectors.

The biggest concern for many businesses isn’t the investigation itself; it’s the cost of dealing with it. Even when HMRC finds that everything is in order, the professional fees involved in defending your position can be significant. Investigations can run for months, sometimes years, and the cost of expert representation can quickly add up to thousands of pounds.

That’s why we provide our tax investigation service, giving you the confidence and support to handle any HMRC enquiry, removing financial worry, ensuring you stay in control, and not facing it alone.

Should HMRC open an enquiry into your tax affairs, the service covers our professional fees, allowing us to represent you without you having to think about the cost. It means you can focus on running your business, knowing that we are handling the situation with the time, care and expertise it requires.

HMRC expects timely, accurate responses, and the process can quickly become time-consuming and complex, but we handle the entire process, from the initial correspondence through to resolution.

Another important aspect of our service is the level of cover it provides. Protection typically extends beyond just your business to include directors, partners, and even personal tax matters. This ensures that both your professional and personal interests are looked after.

With increasing enhancement in data systems to identify discrepancies, the risk of enquiry is higher than ever. £46.8 billion is the estimated tax gap between what HMRC believes it should collect and what it does collect. To ensure tax compliance and to close this gap,

protection typically extends beyond just your business to include directors, partners, and even personal tax matters. This ensures that both your professional and personal interests are looked after.

HMRC undertakes these tax and VAT investigations.

Our promise is simple: To stand between you and the stress, cost and complexity of a tax investigation. We take care of the detail, manage the communication, and ensure your interests are fully protected at every stage.

ask your usual contact for more information or by emailing info@ randall-payne.co.uk or calling 01242 776000.

Making Tax Digital for Income Tax

is no longer a future plan, it is here

From 6 April sole traders and landlords with income over £50,000 must start reporting their income digitally every quarter. Miss a deadline, and HMRC penalties can follow.

The good news: acting now gives you time to get set up properly, choose the right software and stay ahead of the new rules before they start costing you time, money and stress. So, does this really affect you and if so, what should you do?

do you meet the criteria?

If you filed a tax return for the 2024/2025 tax year and are a sole trade business or landlord who received more than £50,000 of qualifying income per annum, you meet the criteria.

What is qualifying income?

This is the income received before expenses, and as both self-employment and rental are included, it is the combination of both sources that determine inclusion under the new rules.

What is required under the new rules?

Under MTD you no longer file a SelfAssessment Tax Return. All self-employed and rental income must be recorded digitally using HMRC recognised software and submitted to HMRC quarterly.

The deadline for submission of each return is one month and one week following the end of the quarter. Therefore, the first return due for submission will cover the quarter ending 30 June 2026 and is due for submission by 7 August 2026.

What do you need to do now?

Registering with HMRC for MTD includes a few key steps and you will also need to set up compatible software if you aren’t already using something.

All of your business and/or rental transactions will need to be recorded digitally, so the more you have to process, the sooner you should get started to avoid a last minute rush.

What software is there to help you?

Several cloud-based software packages have been working closely with HMRC to ensure they are ready for the new regime. Your choice may depend on the level of complexity or number of transactions you handle. As a Xero Gold Partner, we are here to support you and guide you through the set up process.

What happens if it goes wrong?

There are penalties that will be imposed by HMRC for non-submission/compliance with the new rules. However, the quarterly returns are cumulative throughout the tax year so if you happen to make a mistake in one quarter it can be corrected in the next.

You will also need to submit a final annual declaration, much like the Self-Assessment Tax Return you have filed before. This is your opportunity to confirm all figures are accurate and includes income not reported in the quarterly returns.

making Tax digital is here: the sooner you understand it applies to you, get registered and set up your digital records, the smoother your transition will be. Start now, reduce the risk of penalties and errors, stay organised, reduce stress and stay ahead of the curve.

contact nikki cairns for more information by emailing info@randall-payne.co.uk or call 01242 776000.

Unlocking full potential with a business and personal financial health check

Rachael Abbott (Redkite Solicitors), Simon Evans (Clear Future Financial Planners) and I created a seminar aimed at sharing the diverse areas of financial and legal expertise to help our clients’ businesses to thrive.

The seminar, titled Business & Personal Financial health Check, has been designed to help business owners unlock the full potential of their business by combining expert insights across financial planning, legal strategy and business performance strategy.

This session not only covered the areas you need to understand and the importance of regularly checking the intricate details of your business to manage the finances, but how you, as an individual, can improve your financial position.

It reinforced that success requires a holistic approach. Understanding the link between legal structures, financial planning and operational efficiency is essential for any business owner seeking sustainable growth, and peace of mind. By following a structured approach through foundations, financial clarity and future planning, business owners can confidently navigate challenges and seize opportunities.

Here are some key takeaways:

Business financial tips

� Know your numbers inside out

� Invest in the right software systems that bring clarity

� Manage cash flow effectively

� Put legal frameworks in place to prevent future risks

� Plan for value creation and successful exit

Personal financial tips

� Build a personal safety net

� Ensure adequate protection by reviewing insurance policies

� Pensions should be reviewed to fit with long term goals.

� Plan for life after exit

� Use trusts and estate planning tools wisely

� Plan ahead to reduce tax liabilities

The Business & Personal Financial Health Check is a reminder that business excellence isn’t just about revenue; it’s about strategy, structure and foresight. By actively understanding and optimising these areas, individuals set themselves up for long-term success.

Please get in touch if you would like to discuss areas such as asset protection, exit planning, inheritance tax and the importance of forward-thinking financial strategies.

contact shaun pegler for more information by emailing shaun.pegler@randall-payne.co.uk or call 01242 776000.

‘What is my

business worth?’

Is this the question you should be asking?

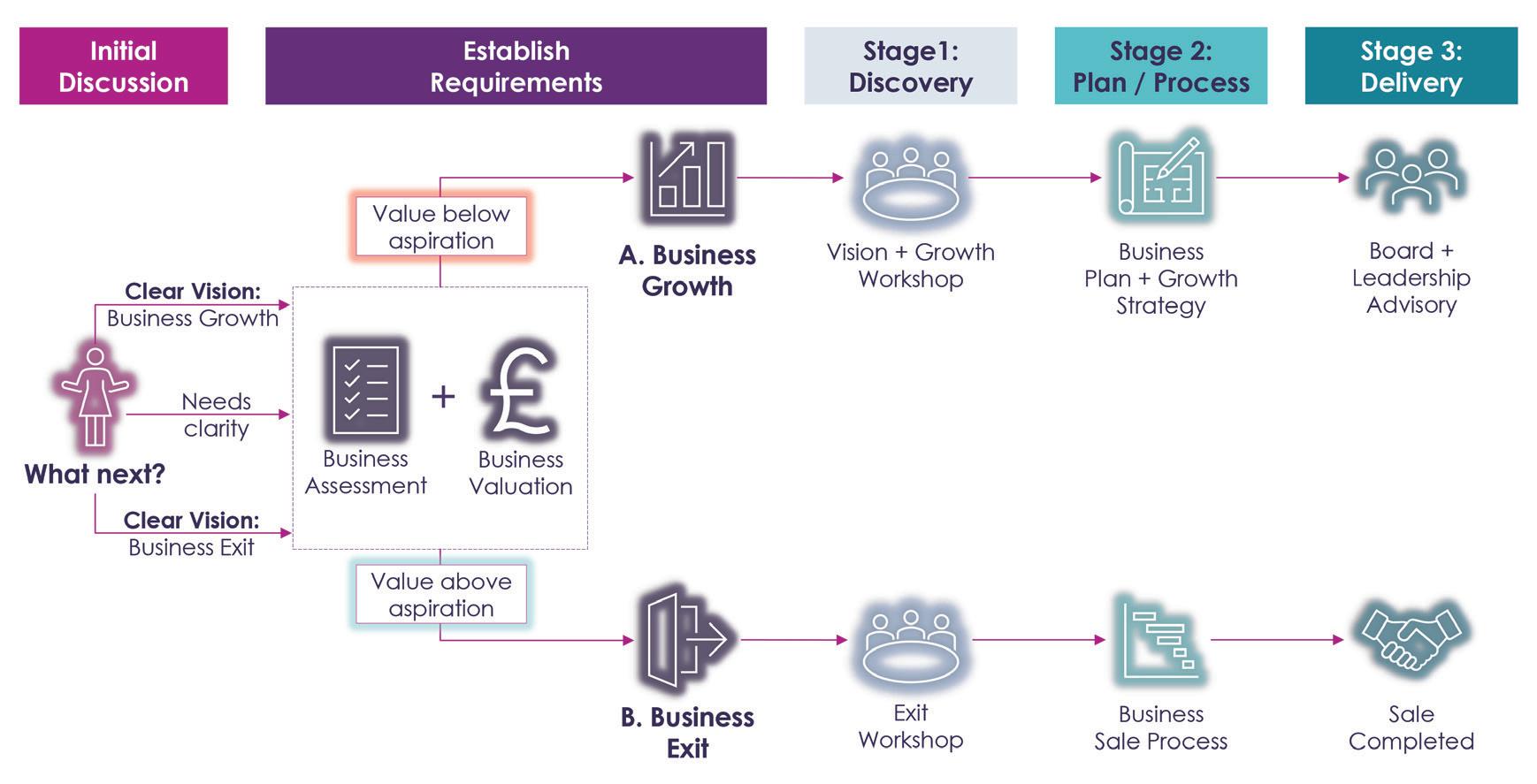

Building a stronger business or exiting at the right time, starts with understanding its true value and the opportunities to change that. Value is not determined by effort or sentiment; it is a market judgement shaped by performance, risk, clarity and timing.

Hari pillai Corporate Finance Manager

“What is my business worth?” may sound like the right question but the real question is whether it’s worth what you need it to be.

We often see SME owners act too quickly before they have properly assessed their position. For some, a strong year creates momentum and an instinct to sell. For others, the instinct is to keep building because growth still feels possible. In both cases, the issue is the same: making a decision without a clear view of where the business stands and what it is truly worth.

In practice there are two distinct goals: one, to maximise value, and the other, to realise value. They are closely connected but require different approaches.

The first step is an honest assessment and valuation of your business as it is

now. That means seeing the business as it really is, not as you hope it is and testing what that reality is worth in today’s market.

A thorough assessment shows you how your business is performing operationally and commercially. An in-depth valuation indicates what a buyer or investor may be willing to pay for it. Only when you understand both can you decide, with confidence, which opportunity is right: build further value or prepare for exit. Where multiple investors are involved a well facilitated strategy workshop can help build alignment on the way forward.

It is easy to overestimate value because owners often attach weight to effort, loyalty and years of sacrifice. But the market reality is different. Buyers are not paying for your stress, your long hours or the fact that you carried the business through difficult periods. They are paying for future cash flow, adjusted for risk. Once that reality is clear, the route becomes easier to choose.

Goal 1: maximising Value

If your business is not yet worth what you need it to be, then the priority is to build value, not just grow revenue. A business can grow in revenue while remaining complicated, owner-dependent and difficult to assess. In that case, turnover may increase, but value may not rise nearly as much as expected.

Real value growth starts with the right thinking and asking better questions: What kind of business are you trying to build? Where is your competitive advantage? Which customers matter most? Which activities truly drive profit, and which merely create noise?

From there, your business needs a proper plan: stronger margins, better systems, clearer reporting, accurate forecasting and disciplined leadership. It also means reducing dependence on you. A more valuable business can stay on a steady course without constant intervention. Serious buyers are looking for profits that are sustainable. They want strong, clear and easily transferable businesses that will continue to generate profits even after you exit.

Goal 2: Realising Value

You may have already done the hard part building the business in the right way, creating real value over time and laying the right foundations. At this point, the question is no longer simply how to build further value, but whether you have already built enough.

That, however, needs to be tested properly. Without clarity, you risk continuing to build when the business is already ready for market, or starting a sale process before the market can deliver the outcome you want.

If the business is sale-ready and the valuation is above your aspirations, the task is no longer primarily to maximise value, but to realise it well. Value becomes real when the market is willing to pay for it on acceptable terms, and a disciplined process is what turns accumulated value into a genuine outcome. That starts with clarity on your objectives, timing and readiness, and then moves into a properly run sale process. A good exit is not improvised, even when the business is in strong shape.

In the end, the smartest owners are the ones who assess their business honestly, value it realistically and compare the outcome with their own ambition. Then they choose whether to build further or prepare for exit.

contact Hari pillai for more information by emailing hari.pillai@randall-payne.co.uk or call 01242 776000.

V ALUE C REATION R OADMAP

DfE Reporting updates for 2025-26

What Academy Trusts need to know

The Academies Accounts Direction (AAD) and the Academies Model Accounts 202526 have been released, which set the tone for how trusts must prepare their year end accounts for 31 August 2026.

Here’s how the updates will impact trusts in practice:

Trade union facility time

This disclosure requirement has been removed.

Streamlined energy and Carbon Reporting (SeCR) wording

“If an academy trust meets the qualifying conditions in The Companies (Directors’ Report) and Limited Liability Partnerships (Energy and Carbon Report) Regulations

2018” – in practice this change of wording is important because Companies Act “large company” thresholds increased from 6 April 2025, whereas the qualifying conditions for SECR reporting remain unchanged, therefore:

If a Trust meets at least two of the preApril 2025 large company criteria, they must still report:

� Turnover > £36m

� Balance sheet total (gross assets) > £18m

� Employees > 250

Internal scrutiny wording

Trusts with over £50m of annual revenue (per last audited accounts) must deliver internal scrutiny through either an employed in-house internal auditor, or from a bought-in specialist provider. This reiterates that trustee checks and peer review are not allowable options for these entities, given their size.

higher paid staff disclosures

Reminder to include the following staff in this note:

Part-time staff who, if full-time, would earn at least £60,000, must be included in the relevant full-time banding. (Example: £45,000 gross salary on a 0.7 FTE).

Staff who worked part of the year, but who would have earned at least £60,000 had they worked the whole year. (Example: £16,000 total gross salary earned over the months June, July and August 2026 only = £64,000 annual equivalent).

Definition

of key management personnel

Defines key management personnel as being “those persons having authority and responsibility for planning, directing and controlling the activities of the academy trust, directly or indirectly.” In practice this may result in variation between the staff listed as Senior Management in the reference and admin section of the accounts, and those staff included in the key management personnel remuneration reconciliation.

Separately, the Direction confirms that senior staff who stay on at a Trust in a consultancy or similar capacity, must be included within this note.

Staff restructuring costs

The Direction for 2025-26 now requires inclusion of Payments in lieu of notice within total staff costs.

disclosure of principal and staff-trustee remuneration

DfE: “We have clarified that disclosure requirements for related party transactions apply where the principal/chief executive is a trustee” – this update clarifies that such remuneration to the principal is to be disclosed in this note and treated as a related party transaction. In practice, the existing note 12 in the model accounts covers this requirement. Any remuneration paid to a trustee for their governance role specifically which remains very rare, must be clearly and separately disclosed.

Church Academy Trusts – land and buildings income and expenditure

A Church trust may incur site improvement costs relating to land and buildings which are occupied under a Church Supplemental Agreement and which are not recognised on the balance sheet. The Direction clarifies that Church trusts may recognise a separate site improvement asset in relation to these costs, provided that asset recognition criteria under FRS102 are met.

once again, the updates lean more toward incremental change than wholesale reinvention, with a continued push towards transparency and consistency across academy trust reporting.

contact Ben Burch for more information by emailing ben.burch@randall-payne.co.uk or call 01242 776000.

Getting statutory holiday pay right from the start

Getting holiday pay wrong can lead to costly errors and unhappy staff. This guide highlights your legal requirements and how to remain compliant across many working arrangements.

Maryann Hunter Payroll Manager

To ensure fairness and transparency, holiday entitlement should be clearly outlined in the employment contract, with employers being responsible for ensuring compliant implementation.

The minimum entitlement for almost all employees is 5.6 weeks of paid holiday per year. This minimum entitlement equates to 28 days in the holiday year, including statutory bank holidays.

The 5.6 weeks applies to full time and part time employees, the latter pro-rata based on the number of days, or hours they work each week.

From the first day of employment, leave accrues at a rate of one-twelfth of the annual entitlement per month, accruing 2.33 days per month thereafter.

The employee may take holiday from the start of employment, but payment for leave is at the employer’s discretion.

Holiday entitlement for irregular-hours and part-year employees accrues at a rate of 12.07% of actual hours worked at the end of each pay period. This is rounded up to the nearest hour if the entitlement is 0.5 of an hour or more.

For any employees who cannot take their entitlement within the holiday year, for example being on Maternity or Sick, they can carry it over to the next year.

There is a maximum number of days allowed, and criteria that needs to be met for individual employees.

Leave entitlement can be carried over if any of the following apply:

� they did not receive holiday pay that they were entitled to for working irregular hours (also known as rolled up holiday pay).

� they were not given reasonable opportunity to take leave.

� they were not told that they would lose their leave if they did not take it.

If an employee leaves during the holiday year, without taking their full entitlement; they should be paid it in their final salary.

Ultimately, ensuring holiday entitlement and pay are managed correctly is a key employer responsibility. Reviewing your policies and processes will help maintain compliance, reduce risk, and support a fair and consistent approach for all employees.

contact Maryann Hunter for more information by emailing payroll@ randall-payne.co.uk or call 01242 776000.

B Corp benefits business: an event with purpose

We are on a mission to raise awareness about B Corp and how the certification brings many benefits for your business, whilst doing good for people and planet.

Fiona Hughes Marketing Manager

Our ‘B-Curious’ event in March brought together local businesses to hear from B Corps representing different sectors speaking about why they chose to do the certification and what it means in practice.

Shaun gave examples of what we had done to achieve our 90 points. He didn’t shy away from the challenges, but he explained that it’s 100% worth your time, effort, and cost.

Kay Geoghegan of Tyler Grange, a leading UK environmental consultancy in Cirencester, explained how achieving certification in 2022 has supported faster growth and increased turnover. Among Kay’s highlights were the introduction of a 4-day week and numerous award wins.

Gareth Dinnage MD of Seacourt Ltd spoke passionately about the 80-yearold printing company in Oxfordshire, how they pioneered waterless printing technology in 1997, became carbon neutral in 2001, 100% renewable in 2003 and B Corp in 2020. They are the highest scoring B Corp printer on the planet with 150 points which is an incredible achievement.

Fran Page of Good Better, explained the new standards, an even more rigorous process that all B Corps need to follow to recertify. She shared that B Corps whave seen a 20% increase in turnover vs national average of 3% (UK SME’s 2024-2025), 11% employee headcount increase vs national average of 2% (UK SME’s, 2024-2025), and 18% more growth funding from external investors than other UK businesses over last ten years.

All speakers commented on never having met a B Corp who regretted becoming one.

Later in the month, Shaun joined Mark Owen on his ‘Punchline Talks: B Corp Show’ discussing what it means to be a certified B Corp. Other guests included Fran Page, Gareth Dinnage, Todd Gifford of Optimising IT and Greg Pilley of Stroud Brewery.

Shaun commented ‘’When you’re looking to partner with somebody it’s all about trust and you want to choose a business you can trust. If they’re B Corp certified, you know there’s no stone left un-turned and that due diligence has already been completed.’’

Even before March, ‘B Corp month’, had begun, we had been collaborating with fellow B Corps by hosting a meeting for our B Local Gloucestershire group. It was an inspiring session focused on the power of collective action to raise awareness and plans for B Corp month and going forward. We look forward to continuing to champion the movement.

contact Fiona Hughes for more information by emailing marketing@randall-payne.co.uk or call 01242 776000.

A shared Stroud story: our partnership with Meningitis Now

Following a fully staff-led selection process, we are delighted that our new charity partner for 2026 and 2027 is Stroud-based Meningitis Now.

Jo kline Client Experience Officer

As a certified B Corp, we are committed to balancing commercial success with a positive impact on people, communities, and the environment. We take pride in supporting initiatives that create a meaningful difference both within our local community and further afield.

Forty years ago in Stroud and Stonehouse, families came together, including Jane Wells (Founder Patron), to form The Stroud Meningitis Support Group. This was closely followed by the establishment of The Meningitis Trust, the UK’s first meningitis charity. Still headquartered in Stroud at Fern House on Bath Road, the charity is now known as Meningitis Now.

Meningitis Now is the UK’s leading charity dedicated to saving lives and rebuilding futures through research, awareness, and lifelong support for

those affected. The charity provides emotional, practical, and financial support, funds vital research into vaccines and prevention, and works tirelessly to raise public awareness across the UK so that symptoms can be recognised early and lives can be saved.

This year marks the 40th anniversary of their work in fighting the devastation caused by meningitis, creating a future where no one in the UK loses their life to the disease and providing support for everyone affected by the disease.

We look forward to playing an active role in supporting the charity’s vital work through fundraising and awarenessraising initiatives, especially during their 40-year anniversary.

Meningitis Now has shared their enthusiasm for the partnership, expressing how much our support means. Together, we aim to bring hope, strength, and the promise of brighter days to individuals and families affected by meningitis in Gloucestershire and across the UK.

We are excited to be starting this partnership with Meningitis Now and, having had the opportunity to meet with the corporate fundraising team, we are keen to get started. A few things are already in the pipeline, including some of us being brave enough to take on a skydive!

contact Jo kline for more information by emailing marketing@randall-payne.co.uk or call 01242 776000.

Is your website quietly costing you leads?

Many businesses spend good money driving traffic to their website, only to lose potential customers within seconds because their message is unclear to visitors, search engines and AI tools. A confusing website does more than frustrate visitors. It turns OFF customers.

Many businesses assume they have a traffic problem. In reality, they have a clarity problem. They are investing in websites, SEO, Google Ads, networking and referrals, but if their homepage does not quickly explain what they do, who they help and the result they deliver, good prospects leave. And that is expensive.

Every confused visitor represents wasted marketing spend, wasted referrals and lost enquiries. If someone lands on your site and thinks, “I’m not sure this is for me,” you have already created friction. People are too busy to spend time trying to understand your business’s website. They will simply move on.

This is no longer just about human attention spans. Search engines and AI-powered tools are also looking for clear signals to understand what your business does and when to recommend it. If your message is vague, hidden in jargon or buried too far down the page, you make it harder for both people and technology to recognise your value.

Video can help solve that quickly A short homepage video or explainer can show your service, your people and the outcome you deliver far faster than text alone. Done well, it reduces friction and builds trust.

Captions and transcripts matter for the same reason. Captions help people follow the message without sound. Transcripts improve accessibility and give search engines and AI tools the text they need to understand your offering.

So, here’s my three simple fixes you can make this month to start seeing a difference.

1. Rewrite your homepage headline so it clearly states what you do, who it is for and the result.

2. Add a short video that explains your offer simply. You can do this on your phone to get you started, you don’t always need to hire a video agency to make impactful video content, although, it might help!

a short homepage video or explainer can show your service, your people and the outcome you deliver far faster than text alone

3. Include accurate captions and a transcript on every video. nomadic uk helps businesses turn complex products and services into clear video content that builds trust and drives sales. nomadic.uk

Ke y de A dl INeS

Tax due period ended 30/09/25

Due date for 2025/26 P11Ds and Share Scheme Returns

date for 2026/27 PAYE

3

& Class 1 NIC payments (electronic)

deadline to Companies House – periods to 31/10/25

Corporation Tax return deadline to HMRC – periods to 31/07/25

Due date for second Income Tax payment on account 2025/26

OCT 26

1

Corporation Tax due –period ended 31/12/25

19 Due for 2026/27 PAYE month 6

22 PAYE & Class 1 NIC payments (electronic)

Accounts deadline to Companies House – periods to 31/01/25 Corporation Tax return deadline to HMRC – periods to 31/10/25

Business Bootcamp

First Tuesday of every month 9:30-11:30

We know one-to-one coaching works but sometimes hearing from others can help put your struggles into perspective. These peer-to-peer sessions challenge thinking, share experiences and deliver results. It is critical that busy business leaders invest time to continually build and refine their skills and focus on the few key actions that will have the greatest impact on their business and their success.

Business & Personal Financial health Check

8 July 10.30-12.30

Shaun Pegler will be speaking alongside Rachael Abbott of Redkite Solicitors and Simon Evans of Clear Future Financial Planners. This seminar is designed to help business owners who are looking to make confident and informed decisions about the future, by strengthening both their business and personal financial wellbeing.

Advice Clinic

Appointment only: any weekday working hours

Got a tricky business question or need advice to move forward?

We can help with a wide range of issues for you and/or your business. Book a free advice clinic with the relevant expert. Advice clinics are private and confidential, with no obligation, and open to anyone with a personal tax or business issue, whether a client or not.