At Progress Rail, we keep you moving with comprehensive services—from inspections and routine maintenance to complete rebuilds and repairs.

Our ISO-certified facilities, strategically located across the U.S., deliver the turnaround times you need to stay on schedule. When reliability matters, trust the team that keeps you rolling.

Inspections to Rebuilds –We’ve Got You Covered

Rail Suppliers: $127 Billion (With a B) Toward U.S. GDP

Where would the rail industry be without its suppliers?

Well, let me tell you: Nowhere. Lost. Behind the eight ball. Stuck in the mud. Drowning in quicksand. Up the river. Over the cliff. Down in the dumps. Down for the count. Flat on its face. Shafted. Dazed and confused. I’m serious, folks!

Of course, this is a generalization, perhaps even an exaggeration. Our rail industry is certainly full of examples of railroad/ supplier cooperation, ranging from R&D to testing new technology (think MxV Rail and TTC Operated by ENSCO). And all the Class I’s as well as many smaller carriers are staffed with brilliant people who “get things done in-house.” Yet, at least to some degree, they still need suppliers for their success.

So, just how important are rail suppliers?

The 2026 Economic Impact Report for the rail supply industry, produced in partnership with Oxford Economics and supported by primary sponsor Railway Supply Institute (RSI), the Railway Tie Association (RTA), the Railway Engineering-Maintenance Suppliers Association (REMSA) and Amtrak, measured the activity that takes place within supplier firms, supported through their domestic supply chains and by the wages they pay. The report says the rail supply industry contributes $127 billion annually to U.S. GDP (gross domestic product) and directly employs an estimated 338,000 workers. Accounting for “indirect and induced effects throughout the broader economy,” total rail supply industrysupported employment rises to approximately 906,000 jobs.

Nice, eh?

And if you think Amtrak is “a waste of taxpayer dollars,” as some politicians who probably never boarded a passenger train like to spout, think again. According to the report, Amtrak’s procurement and capital investment activity “supported approximately 45,800 jobs and generated $6.5 billion in U.S. GDP in 2024, along with $3.8 billion in labor income and $1.4 billion in tax revenue across federal, state and local levels. These impacts, driven by a nationwide network of manufacturers, engineering firms, and construction and service providers, underscore how Amtrak’s investments sustain domestic supply chains, support high-quality jobs and drive economic activity in communities across the country.”

Finally, according to our own research, North American railways, freight and passenger, sustain a market annually worth about $275 billion, accounting for all funding sources, private and public. Adding that number to the $127 billion in supplierdriven dollars yields $402 billion.

I’ve attended too many industry trade shows that wind up as a bunch of suppliers standing around talking to each other, wondering if the money they invested in setting up and staffing a display with some of the brightest minds in the business was worth it. That’s unacceptable. To those railroads who can’t be bothered sending representatives to big trade shows like Railway Interchange 2026 (Omaha, June 2-4), don’t let your suppliers down, OK? Union Pacific calls Omaha home. You people need to pack the place!

WILLIAM C. VANTUONO Editor-in-Chief

Railway Age, USPS 449-130 (ISSN 0033-8826), is published monthly with a special C&S Buyers Guide issue in December by the Simmons-Boardman Publishing Corporation, 1809 Capitol Avenue, Omaha, NE 68102-4905. Tel. (212) 620-7200. Periodicals postage paid at Omaha NE and additional mailing offices.

Subscriptions: Qualified individuals in the railway industry may request a complimentary subscription. All other subscriptions: US/Canada/Mexico; $100.00 per year. Rest of World $139.00 per year. Single copies $36.00 per issue.

For Subscriptions & address changes, please call (US, Canada & International) +1-847-559-7372, Fax +1 (847) 291-4816, e-mail railwayage@omeda.com or write to: PO Box 239, Lincolnshire IL 60069-0239 USA.

Ports and Intermodal Editor/Marine Log Editor-in-Chief hervin@sbpub.com

Contributing

Editors

David Peter Alan, Jim Blaze, Nick Blenkey, Sonia Bot, Bob Cantwell, Dan Cupper, Alfred E. Fazio, Justin Franz, Gary Fry, John Hankey, Michael Iden, Don Itzkoff, Bruce Kelly, Pauline Lipkewich, Joanna Marsh, David Nahass, Jason Seidl, Ron Sucik, David Thomas, Frank N. Wilner

Art Director: Nicole D’Antona

Graphic Designer: Hillary Coleman

Corporate Production Director: Mary Conyers

Production Director: Eduardo Castaner

Marketing Director: Erica Hayes

Conference Director: Michelle Zolkos

Circulation Director: Joann Binz

INTERNATIONAL OFFICES

46 Killigrew Street, Falmouth, Cornwall TR11 3PP, United Kingdom 011-44-1326-313945

International Editors

Kevin Smith

ks@railjournal.com

David Briginshaw

db@railjournal.com

Robert Preston

rp@railjournal.com

Mark Simmons

msimmons@railjournal.com

CUSTOMER SERVICE: RAILWAYAGE@OMEDA.COM , OR CALL 847-559-7372

Reprints: PARS International Corp. 253 West 35th Street 7th Floor New York, NY 10001 212-221-9595; fax 212-221-9195 curt.ciesinski@parsintl.com

Powering the economy

Creating opportunities to grow with our customers and supply chain partners across North America.

www.cn.ca

Industry Indicators

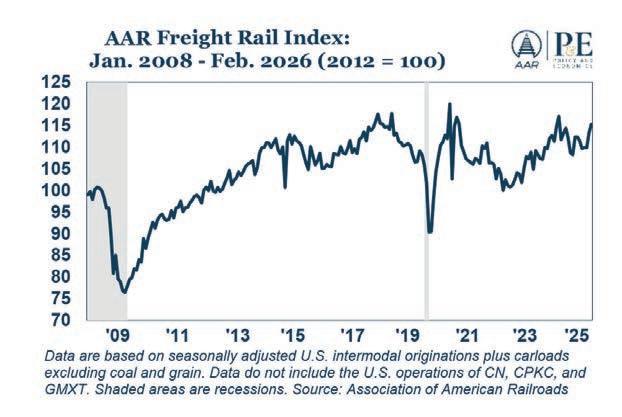

‘RAIL VOLUMES POINT TO A FIRMER ECONOMIC BACKDROP’

“In February, we noted it was not hard to find economic indicators pointing to slower growth,” the Association of American Railroads reported last month. “Many of those concerns remain, especially in the labor market: Net new jobs fell by 92,000 in February, and the unemployment rate rose to 4.4%. But this month’s data also offers a more encouraging counterpoint. Recent readings on rail volumes, inflation, and manufacturing suggest the economy may still be on track for a soft landing, with inflation easing toward target without a significant slowdown in economic growth. Significant uncertainty remains. But for railroads, the latest data points to a more supportive backdrop for freight demand in the months ahead.

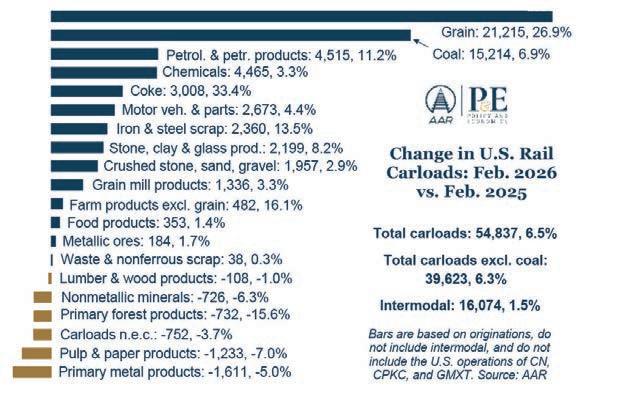

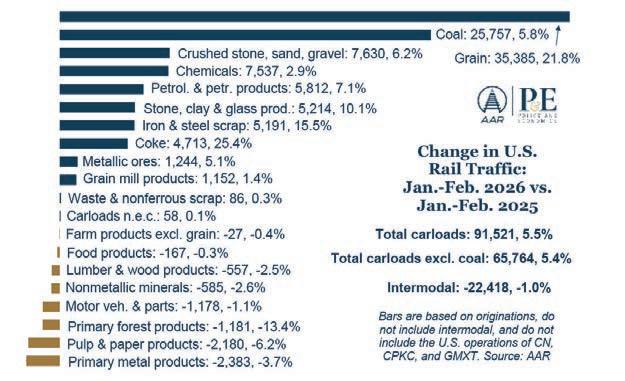

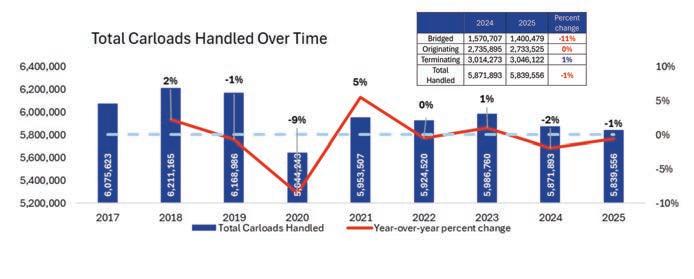

“U.S. freight railroads started 2026 strong despite severe weather in some areas. Total U.S. carloads averaged 224,737 per week in February 2026, the most for February since 2019 and up 6.5% over February 2025. Carloads for the first two months of 2026 totaled 1.76 million, up 5.5% (92,000 carloads) over last year.

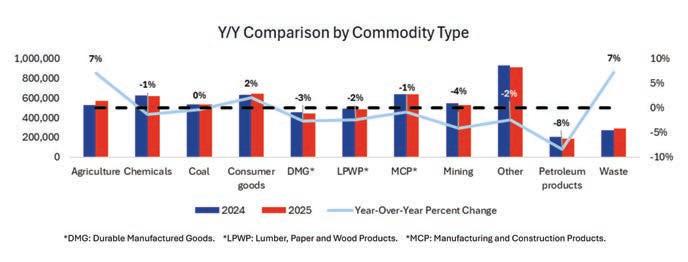

“In February 2026, 14 of the 20 major carload categories saw year-over-year gains, led by grain, coal, chemicals and petroleum products. Broad-based gains across carload categories suggest industrial activity and goods movement demand are firming. That matters because many carload sectors tend to move closely with underlying real-economy activity, making rail volumes a clear real-time signal of changing freight demand.

“U.S. rail intermodal shipments averaged 280,687 units per week in February, the most ever for February and up 1.5% over last year. It was the first year-over-year gain for intermodal in six months. For the first two months of 2026, intermodal volume totaled 2.19 million containers and trailers, down 1.0% from last year but still the second-highest total ever for the first two months of a year. The combination of modest year-over-year softness and still-elevated absolute volume suggests underlying goods demand has cooled but not collapsed.

“The AAR Freight Rail Index (FRI) tracks seasonally adjusted intermodal shipments and carloads excluding coal and grain, which together capture the rail traffic segments most sensitive to shifts in the broader economy. The index rose 1.8% in February over January, its third month-to-month increase in the past four months.

“The number of railcars in storage fell by nearly 18,000 in February, their first decline in six months, and every major railcar category saw fewer idled cars. If that trend continues, it would suggest freight demand is strengthening enough for railroads and other railcar owners to bring equipment back into service in a more meaningful way.

“The next few months should provide a clearer test of whether the recent improvement in freight volumes and the scattered signs of macro stabilization can build into something more durable. Manufacturing appears

to be regaining some footing, service-sector activity remains firm, and consumer spending has not yet broken. If those conditions hold, the backdrop for rail traffic should improve further.

“The labor market remains the key swing factor. For now, however, the balance of recent data suggests the freight economy may be on somewhat firmer ground than seemed likely just a month ago.”

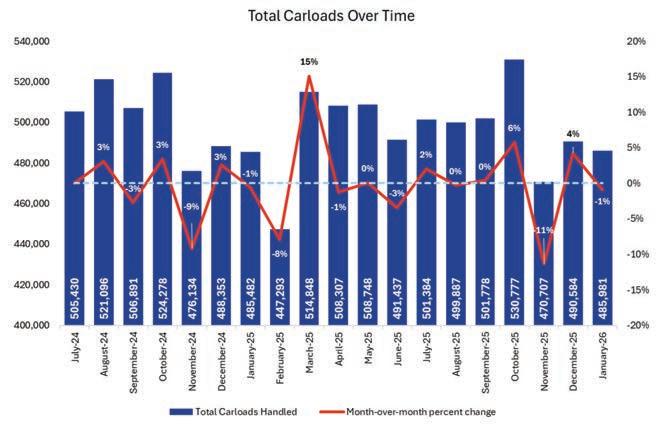

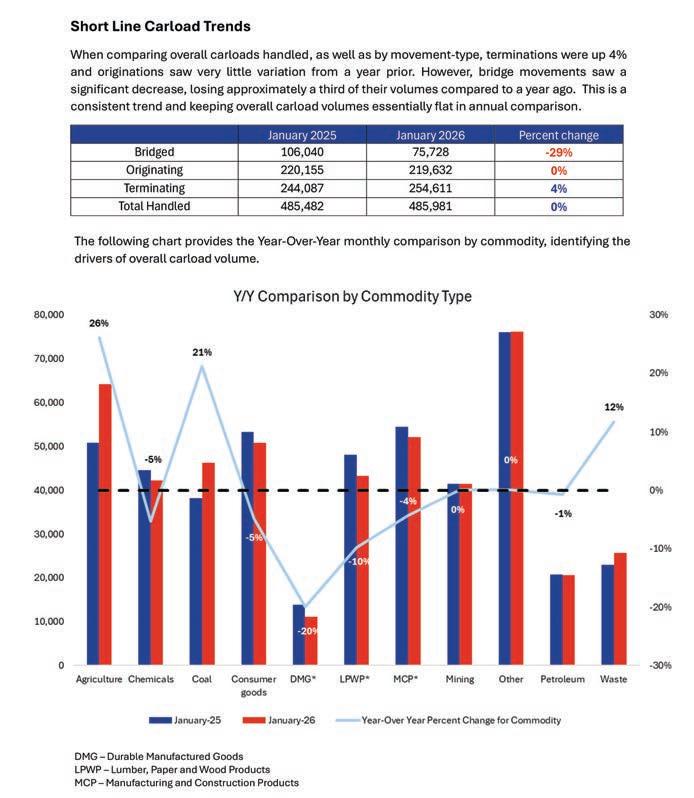

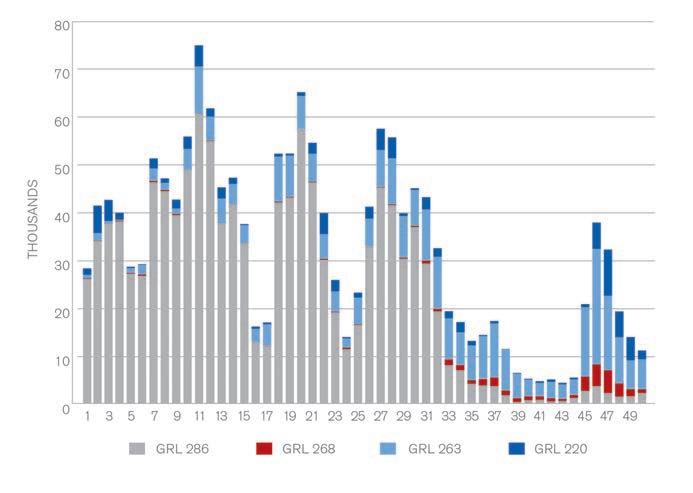

ASLRRA SHORT LINE CARLOAD REPORT

Total carloads handled calculates the total number of individual carloads that were either an origination, termination or a bridge movement, on at least one U.S. short line. This total will generally be smaller than the sum of originated, bridged and terminated movements as some individual carloads experience more than one of these events.

This short line carload data report is created by the American Short Line and Regional Railroad Association in cooperation with Railinc, based on waybill data submitted by railroads. A detailed report is published each month via ASLRRA’s Views & News. Visit www.aslrra.org/carload to learn more.

Industry Outlook

STB Aims to Reform Rail Permitting

required under the law, the process would be considerably shorter and less expensive to railroads and taxpayers.

The unanimous vote by Republican Chairperson Patrick J. Fuchs, Republican Michelle A. Schultz, and Democrat Karen J. Hedlund makes clear this is not a politically partisan decision but another overdue effort to reduce regulatory burdens and lower regulatory costs.

“The proposed permitting reform would lead to more expeditious and cost-effective environmental review by focusing on appropriate analyses rather than unnecessary paperwork.” – STB Chair Patrick Fuchs

IN THE OPINION OF THE LATE PRESIDENT RONALD REGAN, “THE NINE MOST TERRIFYING WORDS IN THE ENGLISH LANGUAGE ARE, ‘I’M FROM THE GOVERNMENT AND I’M HERE TO HELP.’”

Among railroaders, the phrase rang painfully and expensively true for most of the 20th century when the former Interstate Commerce Commission (ICC) regulated railroads into the years the locust hath eaten. Things they have been a changin’ under ICC successor Surface Transportation Board (STB).

existing regulations written long ago by the ICC, an environmental assessment is required, typically taking a year and jointly paid for by the short line

Or, consider a Class I branch line with no existing traffic but connected to a short line serving an auto plant. Were the Class I wishing to rehabilitate the line to facilitate new traffic from the short line, no environmental review would be required. But if the short line purchased or leased the unused branch line, an environmental

In crafting its 69-page proposed permitting reform, the STB says it took guidance from the Council on Environmental Quality (CEQ) and the Supreme Court’s May 2025 decision in “Seven County Infrastructure Coalition v. Eagle County.” The Court held that the STB has discretion to determine the scope of environmental analysis, and the CEQ guidance prods agencies to reform their categorical exclusion process. The NPRM’s new categorical exclusion for connecting track along existing rail rights-of-way segments does that, allow ing what the Board considers a more sensible approach.

Take, for example, the 1970 National Environmental Protection Act (NEPA), whose intent is commendable but appli cation often flawed.

Consider a 150-foot-wide main line right-of-way owned by a Class I railroad near an under-construction steel plant. Were the railroad asked to construct a connecting stub track over its land or that of the steel plant to serve the plant, neither Board approval nor environ mental review would be required.

Clearly, partial railroad economic deregulation that commenced in the mid-1970s and accelerated in 1980 by the Staggers Rail Act wasn’t complete.

But what if the Class I wished to sell or lease to a short line that right-of-way from which the nearby steel plant requested the connecting stub? Under

The proposed permitting changes affect deadlines and page limits for environmental assessments where proj ects are unlikely to have significant environmental effects.

But on March 15, 2026, the STB removed another roadblock to railroad efficiency with a proposal to reform its permitting process to accelerate approval of rail infrastructure projects (Docket EP 779, Permitting Reform –Environmental Review Process ). Public comment is sought.

In a separate expression, Hedlund said, “This NPRM proposed categorically to exclude abandonments from environmental review unless the abandoning carrier announces an intention to conduct salvage operations that would occur prior to consummation of the abandonment or entry into an interim trail use agreement. I encourage stakeholders to submit comments on this aspect of the NPRM, given that it proposes to reverse the Board’s prior understanding of governing law.”

Under proposed revisions in the Notice of Proposed Rulemaking (NPRM), certain reviews would be eliminated, while, for those specifically

Fuchs told Railway Age that “the proposed permitting reform would lead to more expeditious and cost-effective environmental review by focusing on appropriate analyses rather than unnecessary paperwork.”

– Frank N. Wilner

W OMEN IN RAIL AILWAY

Railway Age and RT&S present the fourth annual Women in Rail Conference!

Women in Rail 2026 empowers individuals to grow, lead, and thrive in the rail industry. The conference unites women and allies to share strategies for career advancement, leadership development, and workplace success.

Through panels, peer discussions, and networking, attendees gain insights on compensation, skillset enhancement, and economic trends. The event also supports workforce engagement and leadership pipelines, benefiting both individual professionals and the organizations they represent.

Women in Rail 2026 is a must-attend industry event, highlighting diverse experiences and practical methods for moving the industry forward.

OPENING SPEAKER:

Maryclare Kenney Senior Vice President & Chief Commercial Officer CSX

New York MTA Issues ‘Historic’ Subway Car RFP

The New York Metropolitan Transportation Authority (MTA) is seeking proposals from railcar manufacturers for what it describes as its “largest subway car contract in history” with a base order of 1,140 cars to replace the R62 and R62A fleets operating on New York City Transit’s (NYCT) 1, 3 and 6 lines, and if an option to purchase an additional 1,250 cars is exercised, to replace the R142 and R142A cars on the 2, 4 and 5 lines. In total, the contract includes 2,390 model R262 cars for the “A” (numbered) Division. Proposals are due Sept. 8, 2026, and a contract is expected to be awarded by early 2028. The contract will be funded by MTA’s $68 billion 2025-29 Capital Plan. The purchase also includes funds made available through the 2020-2024 Capital Plan, which is supported by congestion pricing revenues, according to MTA. The transit agency said its RFP (Request for Proposals) outlines that the future order will contain a “to be determined” number of open-gangway cars, which would be a first on the A Division. It also outlines “technical specifications that are designed to enhance efficiency, security, performance and the customer experience.” These include “higher quality announcement systems, and assistive listening devices that allow hearing-impaired passengers to connect to personal devices, like hearing aids.” Efficiency upgrades, it noted, include installation of an automatic passenger counting (APC) system and electric braking control “to achieve savings through fewer parts.” Security specifications include onboard cameras like those currently installed on the existing subway fleet and onboard platform edge CCTV, along with an electronic lock to prevent unauthorized cab access. With a new Rolling Stock Program in place—announced in February and led by MTA veteran Jessie Lazarus to manage the purchase of all new subway, bus and commuter railcars, including the $12 billion investment from the 2025-29 Capital Plan to replace the MTA’s aging fleets—the MTA said it “has approached this contract differently, modernizing the terms and conditions and encouraging innovation by giving manufacturers greater flexibility to propose new ideas.” The agency noted that more than 60% of the technical specifications are also now “performance-based, rather than design-driven,” and for the first time, the terms request proposers to submit “total cost of ownership projections.” These efforts, MTA said, “result in a streamlined contract that adopts a balanced approach between the current challenges that contractors face and ensuring that the Authority retains the necessary tools at its disposal to ensure the timely delivery of quality cars that riders deserve.” This “historic” car contract could replace up to 36.4% of NYCT’s entire subway fleet—17.3% with just the base order alone, MTA said. The subway’s entire fleet comprises 6,574 cars. “The new cars will significantly improve reliability with a higher mean distance between failure,” MTA noted. “The R262 has an MDBF requirement of 200,000 miles, compared to the R62/R62A’s average of 89,000 miles. This upgrade will reduce the number of problems customers experience en route and decrease the amount of time cars are taken out of service.”

INTRAMOTEV on March 30 announced that it has entered into a commercial agreement with R. J. CORMAN RAILROAD COMPANY. Intramotev’s TugVolt railcars will be utilized in industrial switching operations on the R. J. Corman MEMPHIS LINE. The agreement adds R. J. Corman, which operates 19 short line railroads in 11 states and serves all major North American railroads, to a growing roster of commercial partners, noted Intramotev, which currently has active TugVolt deployments under way with CARMEUSE AMERICAS and WATCO. In February, Intramotev announced that Ray Betler, former CEO of WABTEC, has joined its Board of Directors.

CANDO RAIL & TERMINALS has executed a definitive agreement to acquire SAVAGE RAIL in a “mutually beneficial deal that will make Cando North America’s market leader in first- and last-mile rail operating services and terminal infrastructure, and positions Savage for strategic growth opportunities by refining its business portfolio,” according to the companies. Savage Rail is a U.S. rail provider with operations across the U.S. and a platform of rail assets in key markets, including along the Midwest, Gulf Coast and Southeast corridors. The transaction, Cando said, “will accelerate our company’s U.S. expansion plans, while strengthening our existing network in Canada.” The

combined company is expected to operate a coast-to-coast network of assets in North America “with no geographic overlap” that will include 36 railcar storage, staging and/or transload terminals; three short line railways; and 80 first- and last-mile rail service operations, as well as access to all six Class I railroads. Combining the two businesses also aligns with Savage’s goals of growing its businesses and its people, “both by creating new opportunities for its rail services team by joining a large, rail-focused company and also by obtaining capital from the sale to invest in expanding its existing food and fuel-focused businesses,” the company said.

UP-NS Job Pledge Fragments Labor

Ru le No. 1: If you don’t define an objective, events will define it for you. Rule No. 2: Hope is not an objective. Rule No. 3: In union there is strength.

Members of the Transportation Division of the International Association of Sheet Metal, Air, Rail and Transportation Workers (SMART-TD) allege their union bucked those rules in voicing support for a Union Pacific (UP)-Norfolk Southern (NS) merger.

Asked by UP and NS to back the marriage proposal in exchange for a “no job losses” pledge, SMART-TD President Jeremy Ferguson figuratively borrowed as his response Molly Bloom’s declaration in the final lines of James Joyce’s novel, Ulysses: “Yes I said yes I will yes.”

Now asked of Ferguson is, “Where’s the beef?” Members cite the absence so far of explicit and enforceable job protection provisions relating to new technology, seniority retention, relocation, assignments outside their craft, and unforeseen, extraordinary disruptions in traffic volume.

In putting the SMART-TD imprimatur on this merger before negotiating an implementing agreement to define the enforceable “who, what, where and how” of a nebulous promise, members say Ferguson put a cart (of hope) before the (iron) horse (of fulfillment).

By contrast, the Brotherhood of Locomotive Engineers and Trainman (BLET) and Brotherhood of Maintenance of Way Employes (BMWE)—the second and third largest UP and NS unions (behind SMARTTD)—oppose the merger, presumably as leverage when negotiating their implementing agreements. BLET and BMWE term the railroads’ job retention promise as “mostly hollow,” alleging it allows UP and NS “complete control over who is protected, who is left out, and when any commitments can be changed or taken away.”

Other unions are fragmented—some supportive, some opposed and most so far not taking a position.

Missing is union solidarity, and it is not a one-off. SMART-TD and its predecessor United Transportation Union (UTU) own a history of being first in reaching agreements

The law is clear that merging railroads are entitled to realize labor-related economic benefits so long as employees are not placed in a worse position—the floor being New York Dock and the ceiling what labor may successfully negotiate.”

that establish patterns other unions (often grudgingly) follow—the incentive for being first a more favorable carrier relationship known as “soft power.”

As for labor protection, its roots stretch to the Transportation Act of 1920. The 1933 Emergency Railroad Transportation Act imposed a two-year job freeze, while the collectively bargained 1936 Washington Job Protection Agreement substituted income protection for job protection. The Transportation Act of 1940 established four-year minimum income protection, while the 1976 Railroad Revitalization and Regulatory Reform (4-R) Act upped it to six years, which is imposed by the STB through a 1979 decision known as New York Dock.

Notably, the Supreme Court held in 1991 that when the parties fail to reach a timely agreement on protection, binding arbitration may be invoked, and the ICC (now STB) may “cram-down” on the parties the award as being “in the public interest.”

The law is clear that merging railroads are entitled to realize labor-related economic benefits so long as employees are not placed in a worse position—the floor being New York Dock and the ceiling what labor may successfully negotiate.

Under the STB merger rules by which a UP-NS merger application will be reviewed, if there is no negotiated protection agreement, the Board will provide for it at the level mandated by law (New York Dock). Only if “unusual circumstances are shown,” will the

Board impose “more stringent protection”

An involved union officer, asking anonymity, told Railway Age, “Labor is most effective when it acts from a position of coordinated leverage rather than splintered bargaining that weakens its ability to define enforceable standards across crafts.”

If the STB accepts a UP-NS merger application expected to be filed by April 30, labor fragmentation in translating a vague “no furloughs” promise into a member-acceptable implementation agreement could be problematic. Waiting impatiently like a Sword of Damocles will be the STB, with statutory authority to cram-down protections no better than New York Dock. UP and NS will be allowed to enjoy fully the economies of merger.

Railway Age Capitol Hill Contributing

Editor Frank N. Wilner is author of “Understanding the Railway Labor Act” and “Railroads & Economic Regulation,” available from Simmons-Boardman Books, www. railwayeducationalbureau.com/product/ railroads-economic-regulation-an-insidersaccount/, 800-228-9670.

FRANK N. WILNER

Capitol Hill

Contributing Editor

Rail Equipment Finance 2026: Let’s Get Back to ‘Business Being Business’

The 40th R ail Equipment Finance Conference (REF) was held in March 2026 in Laquinta, Calif. More than 460 gathered to update the state of the industry and prognosticate on what will happen in North American rail in 2026. Here is a summary, with key takeaways.

UCLA economist Lee Ohanian gave an economic overview of the U.S. and the world. Key takeaways: Even with the Middle East war, Mr. Ohanian worked to quell worries about the impact on the U.S. economy, noting that even considering recent events, the U.S. remains the best economy in the world. The biggest worry? U.S. fiscal policy and spending in excess of tax revenue. He sees adaptability for our future with AI (artificial intelligence) and cautioned against panic.

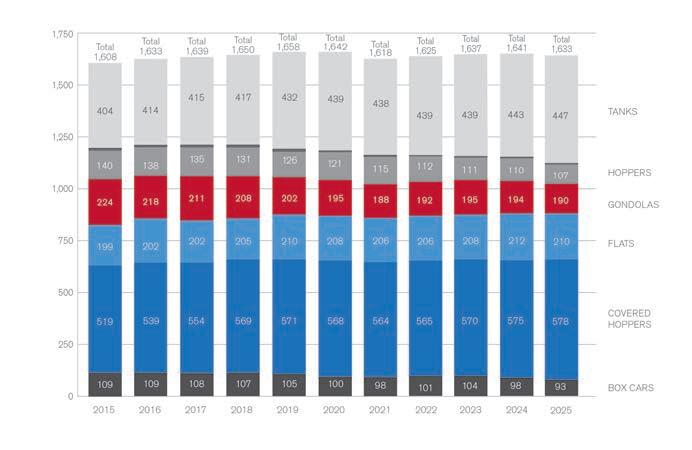

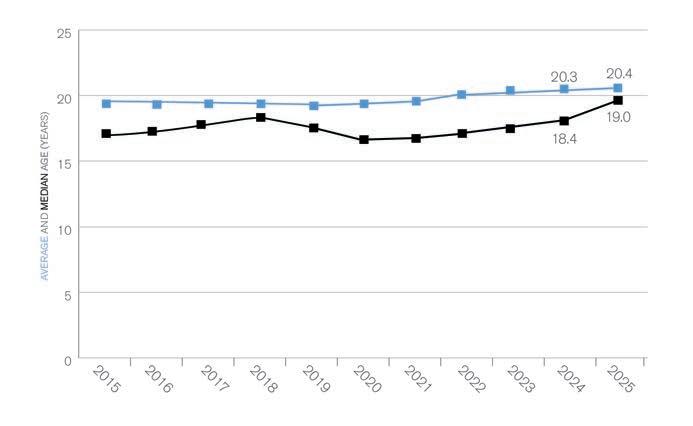

David Humphrey of Railinc, REF’s “Railcar Guru,” gave an update on the North American railcar fleet. Key takeaways: While there were increases in tank railcars in 2025, the total North American railcar fleet decreased by about 8,000 cars. Age matters: About 8.5% of the national fleet (135,000 railcars) reaches its maximum interchange life in the next five years. (See p. 42.)

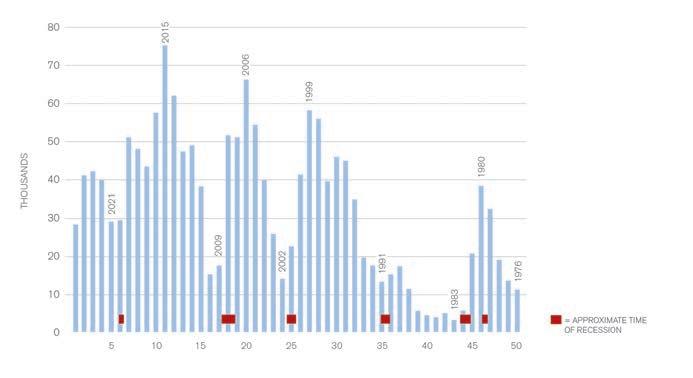

Brian Smalley, National Steel Car, discussed the North American rail manufacturing outlook. Key takeaways: Railcar delivery rates are expected to be at or above replacement level (roughly 35,000 cars annually) in 2027 or 2028. Mr. Smalley sees continued manufacturing headwinds from trade uncertainty, ongoing economic struggles with inflation, and higher interest rates.

Norfolk Southern’s John Orr (Railway Age’s 2026 Railroader of the Year) and Mina De Olivera held a Q&A session and discussed the impact of safety on NS’s performance. Key takeaways: Mr. Orr noted that it was his job to make working for NS attractive to keep a talented group of professionals engaged as railroading’s “next generation.” Ms. De Olivera noted that the railroad is advancing its use of technology and data analytics to improve

train handling and customer service.

Anthony “Tony” Hatch, ABH Consulting, gave an overview of all things railroad and merger related. Key takeaways: “Rail transport is a derived-demand business; [therefore] uncertainty breeds statis.” That is brevity at its best. Mr. Hatch feels that POTUS 47 is not tipping the scales in the Union Pacific/NS merger.

Taylor Robinson, PLG Consulting, discussed the energy landscape for rail commodity moves. Key takeaways: PLG sees rail growth potential in chemicals, propane/butane and renewable diesel. Lithium opportunities remain on the horizon. Investment in railcar storage opportunities is high.

Dan Anderson, Trinity Industries, discussed all things tank railcar. Key takeaways: Mr. Anderson highlighted cost increases in tank railcar maintenance and operation. Since 2016, the AAR Labor Rate CAGR is 3.5%. Tank car loadings have outperformed general carload volumes and Industrial production over the past 12 years.

Sam Sexus, Oliver Wyman, discussed a great conundrum, creating growth in North American rail. Key takeaways: Shippers tell Oliver Wyman that their priorities in choosing transportation are price, reliability and speed. Shipper customer service metrics are sporadic and oddly scattershot. Single-line moves provide better service but not always cost improvements.

Ron Sucik, RSE Consulting, discussed the intermodal market. Key takeaways: Mr. Sucik sees loadings increasing if tariffs settle in 2026. Mr. Sucik raised concerns about the intermodal fleet to serve projected volume increases proposed in the UP/NS merger.

Alex Lookatch, Nucor, discussed steel and scrap metals. Key takeaways: Scrap consumption has stayed relatively stable during the past four years. Steel production capacity of almost 7 million net tons will be added in the U.S. in the next three years. Steel consumption from 1984 to 2023 as a percentage of GDP (gross domestic product) has decreased

by 2.3%. Tariffs will decrease imported steels in 2026.

John Ward, National Coal Transportation Association, talked about the “coal renaissance.” Key takeaways: Coal loadings have rebounded year over year by approximately 6%. Tech demand for power (AI data centers) has caused planned coal fired generating station decommissioning to be reversed. Five-year projected electricity demand is higher than any period since the 1960s.

On boxcars, Doug Driscoll, Genesee & Wyoming Railroad Services, Inc.; David Horowitz, GATX; and Anthony Petrillo, Packing Corporation of America, discussed this often-contentious market. Key takeaways: Mr. Driscoll said in a clear statement that “there is no cliff in the North American boxcar fleet.” Mr. Horowitz advocated for growth in “stickier” rail freight that gets committed to boxcars and stays on rail promoting investment. Mr. Petrillo noted that his company’s challenges in shifting to rail from truck were reliability, service consistency and price.

On the valuation panel, Sean Hankinson, Adaptive Rail Solutions; Pat Mazzanti, Railroad Appraisal Associates; Greg Schmid, RESIDCO; and Bryan Vaughn, Modern Rail Capital, checked 12-month changes in car values. Key takeaway: Car values yearover-year are increasing, including coal cars. Surveyors believe 2026 growth will be in a narrow range. Johanna Biggs, Biggs Appraisal, proposed the idea that in-service railcar retirements may lead to a surprise on the upside for new car builds.

On Tuesday at REF, Eric Starks, FTR Transportation Intelligence, forecast rail economy difficulties for 2026. Key takeaways: Mr. Starks expressed skepticism regarding UP/NS merger claims for removing 2 million trucks (vs. truckloads) off the highways. Mr. Starks noted that “uncertainty hurts growth.” Furthermore, concerns about future growth remain prevalent.

Nick Randall, FreightCar America, discussed the future of railcar building, the new railcar market, and technology. Key takeaways: Trust the process. Mr. Randall feels transparency generates credibility

and stronger customer relationships. He sees AI optimizing manufacturing, such as root cause analysis from the shop floor, improved scheduling and inventory management, and better predictive maintenance analytics.

Farah Lawler, BNSF, addressed the current operational landscape at BNSF and the Class I’s point of view on the UP/NS merger. Key takeaways: Safety and logistics developmental improvements are making railroad operations more efficient and benefiting customer growth. BNSF is concerned that the proposed merger may cause service problems and does not fit within the Surface Transportation Board-defined requirements for improved rail-to-rail competition.

Jon Mudronja, AITX, updated the covered hopper market and discussed rail system fluidity. Key takeaways: Covered hopper fleet health (excluding smallcube hoppers) remains viable and strong. Barring overinvestment, the fleet balance of availability and storage should remain at appropriate levels. Systemwide railcar fluidity remains a positive metric with elasticity to support reasonable demand increases in the current build environment.

Tuesday concluded with Paul “The Closer” Titterton, GATX, discussing the operating lessor’s perspective on the market. Key takeaways: Material carload growth in North America is unlikely for the foreseeable future. However, investment in railcars using a disciplined and data-driven approach allows for profitable investment and growth. And remember, it is always better to be happy than right. (Shoutout to author Douglas Adams).

Wednesday at REF is all locomotives and began with “Locomotive Guru” David Humphrey, Railinc. Key takeaways: There are roughly 37,600 locomotives in the North American fleet. Roughly 8,000 will hit their 25- or 15-year anniversary for new and rebuilt units, respectively, in five years, possibly impacting future locomotive demand.

Don Graab, Triangle Brothers, discussed the current state of the locomotive market. Key takeaways: Railroads need to embrace Tier 4 technology, even though they may have made missteps in their technological choices. A return to more aggressive emissions standards seems unlikely.

Graciela Trillanes, HGmotive, discussed

the hydrogen fuel market for locomotives. Key takeaways: In conjunction with Canadian Pacific Kansas City, HGmotive continues to advance the case study for the successful use of hydrogen as a locomotive fuel in linehaul service. The volume of units in service will grow over the 2026 calendar year.

Robert Bremmer and Woody Woodman, Wabtec, provided a manufacturing update. Key takeaways: Wabtec’s approach to the North American locomotives market focuses on the most viable fueling options for current and future growth and investment: BE (battery-electric), internal combustion, and hybrid.

Greg Hall, Knoxville Locomotives Works, and Sree Masabattula, CN, discussed their activities in repowering CN’s yard switcher fleet. Key takeaways: The battery-hybrid rebuild added 12 years to a locomotive’s service life and reduced fuel consumption by 44%. Weather-proofing the units for the Canadian winter was a challenge that helps to deliver a reliability uplift (55% reduction in unplanned downtime).

Joseph Stack, Cummins, updated his company’s activities in the space. Key takeaways: Cummins continues to deliver and implement the QSK95 engine with more than 300 delivered and 225 locomotives in service. Cummins advances technology on its fuel-agnostic engine and continues to see hydrogen commercialization across all transportation modes.

Luuk von Meijenfeldt, Nexrail, discussed using hybrid and alternative fuel locomotives in Europe. Key takeaways: Nexrail chooses the replacement unit fueling style based on the kind of service, and has adapted unit design to its service, such as a three-axle switcher. In many cases, battery life can reach 20 years!

Michael Faust, Railpower, discussed motive power technology alternatives. Key takeaways: Depending on the type of service, Railpower (in many cases in conjunction with California’s Sierra Northern Railroad) favors hydrogenbattery hybrid or HFC (hydrogen fuel cell) locomotives. Far lower emissions is more favorable for the area where Sierra Northern operates.

Jason Kuehn, Oliver Wyman, updated the overall locomotive market. Key takeaways: With older units becoming more costly to repair and parts becoming

Financial Edge

less available, the locomotive replacement cycle is inevitable. There is no silver bullet in North American rail for future locomotive technology development. The industry should focus on improving efficiency rather than on unit replacement.

Stuart Biggs, Biggs Appraisal, updated the locomotive backlog. Key takeaways: 272 six-axle locomotives were built in the past 12 months, with the Wabtec Evolution series showing the largest increase (about 265 of the units added were included in this group). BNSF maintains the largest Class I locomotive fleet at approximately 7,500 units.

Steve Bomba, Motive Power; Pat Mazzanti and Greg Schmid discussed locomotive values. Key takeaways: Locomotive values rose; newer units showed larger increases than older units. Values of older switching locomotives remain strong, while the cost of new battery or hybrid switching units is getting more expensive.

Overall, the presentations at the 40th REF showed hesitation and determination about the railcar market and its future. While there are consistent concerns about loadings growth, new car build rates, and opportunities for investment, among the parties already committed to investment in the industry, there is a quiet resolve that things will improve and that North American rail will continue to be a desirable sector in which to make investments and deploy capital.

One clear takeaway is that the uncertain economic landscape of tariffs and penalties is not viewed as being good for North American rail. Owners and operators would prefer to move beyond those issues and get back to business being business.

Three great days of data and information from the industry’s best thinking. Interested in REF 2027? Keep an eye on the website: wwww.railequipmentfinance.com. Got questions? Set them free at dnahass@ railfin.com.

DAVID NAHASS President Railroad

STABILITY

& ADAPTABILITY

In a changing market, stability matters. FreightCar America is your steady partner— working with customers to adapt, respond, and move forward with confidence.

Proud to be Purpose-Built for You.

Scan to discover our Purpose-Built approach.

CUSTOMER EXPERIENCE TRUTRACK™ QUALITY PROCESS PURE PLAY MANUFACTURER

LEADERSHIP

orth America’s freight rail industry is sharply focused on the future as the 21st century is well into its third decade. For this annual special report, leaders from North American freight rail industry companies have crafted exclusive, insightful essays for Railway Age on growing and sustaining our vibrant industry, which has helped shape our society and is the backbone of transportation. Here are what they believe are their organizations’ most significant achievements.

Flexible, Agile, Growing — and Safe

ABy Katie Farmer, President and CEO, BNSF

t BNSF, we’re proud of the progress we’ve made over the past year to add value to the global supply chain while growing with our customers. Our safety and service improvements are key evidence of that.

In 2026, we’re building off our service momentum from last year, where we set a new record in our dwell performance. Our railcars spent an average of three fewer hours at our terminals compared with the previous year. Because of this, we also made big gains in velocity: We saw a 10% increase in 2025 across our network.

The increase in network efficiency has allowed us more room to grow, adding 60,000-plus additional days of service across 615 customer locations.

We accomplished all this while continuing to operate as the safest railroad in the industry over the past decade with the fewest rail equipment incidents. Last year, we had the safest year for employee

injuries in our company’s 177-year history.

Our exceptional service levels are how we continue to be the industry’s intermodal leader, consistently handling more intermodal units in North America than any other railroad.

We have strong partnerships with the West Coast ports, offering the fastest transit times to the largest, fastest-growing inland markets. Last year, we hit a record 1.6 million lifts at our Southern California On-Dock facilities at the ports of Los Angeles and Long Beach, 125,000 more than the previous year.

been so successful that we recently launched our Quantum de Mexico service product.

Our state-of-the-art logistics parks ensure we can stay ahead of demand and have the capacity needed to be more truck-like, all while driving significant supply chain savings to cargo shippers. Permitting continues for our Barstow International Gateway project, and we continue to make progress on our new logistics park project in Denver. We also recently broke ground on an intermodal facility in Phoenix, where we ultimately intend to have a logistics park to serve this rapidly growing market. Other recent growth developments include our new intermodal facilities now open in Salt Lake City and Oklahoma City.

Our multi-year expansion project at our Chicago intermodal facility in Cicero concluded late last year, adding 175,000 annual lifts to our capacity, improving safety and efficiency, and an enhanced-customer experience. Amid one of the densest urban areas in the country, the entire project was also done sustainably, offsetting the carbon equivalent of planting 120,000 trees.

Exciting developments for our carload customers include the continued expansion of our logistics centers and certified sites programs with the recent opening of our North Houston logistics center, as well as work under way on our newest logistics center in North Dallas. These locations provide access to rail-served origins and destinations where customers may not be able to utilize the benefits of rail today. We currently have four operational logistics centers, four in the pipeline, and 38 certified sites across 17 states and one Canadian province. Eight short lines are now part of our Shortline Select initiative where together we provide superior service and leverage additional efficiencies for our customers.

At our core, we are a railroad that is flexible and agile in every decision we make. We are moving forward through 2026 with a continued focus on long-term growth, efficiency, and innovation while delivering the safest, most reliable, and consistent service for our customers. Above all else, what has always set us apart as an industry leader is our people, who remain dedicated to delivering industry-leading service and putting customers at the center of everything we do. I’m looking forward to seeing all we can accomplish together this year to further strengthen the supply chain and provide even greater optionality for our customers.

Our Quantum intermodal service with J.B Hunt, which launched in late 2023, has grown exponentially over the past two years. Quantum is targeted to customers with the most service-sensitive highway freight, that prior to our launch, was thought of as infeasible to move via intermodal. We’ve proven the art of the possible through our integration processes and 24/7 watchtower oversight with J.B. Hunt, consistently meeting the demands of customers’ most complex freight, up to a day faster or more than traditional intermodal service. It has BNSF

Serving Customers Reliably, Efficiently and Safely

By Keith Creel, President and CEO, Canadian Pacific Kansas City

As we reach the third anniversary of Canadian Pacific Kansas City (CPKC), we are proud to have delivered on our commitment to introduce innovative service offerings and customer-focused solutions that drive growth and value across our unrivaled network.

Through strategic investments in supply chains, industrial development, sustainability, and safety, we are helping shape the future of rail transportation while creating long-term benefits for our customers, our communities, and our railroaders across three great nations.

CPKC’s focus on providing rail customers new transportation options has resulted in industry-first rail solutions such as our successful Mexico Midwest Express (MMX), the first single-line, truck-competitive rail service linking Mexico with the U.S. Midwest. Building on the MMX’s momentum, we have introduced the Southeast Mexico Express (SMX), a collaborative effort with CSX, creating an east-west Class I rail corridor linking Mexico, Texas, and the Southeastern U.S.

By collaborating with customers, we are changing entire supply chains. One highlight is our strategic partnership with Americold, the world’s largest owner of temperaturecontrolled warehousing and logistics. Together, we are building a premier cross-border cold chain network for North America.

In August 2025, we marked the grand opening of Americold’s approximately $120 million, 335,000-square-foot facility in Kansas City, Mo., its first on the CPKC network. This modern hub enables seamless movement of refrigerated goods between the United States and Mexico on our MMX service, a move exclusively dominated by trucks before now. Earlier last year, Americold broke ground on its first Canadian import-export hub at Port Saint John, New Brunswick, a key gateway slated to open in 2026, leveraging the combined strengths of DP World’s marine logistics and CPKC’s rail solutions. These Americold sites are more than warehouses; they are critical for intermodal gateways unlocking new efficiencies for temperature-controlled products across the continent.

To support our expanding operations, we continue to invest in state-of-the-art equipment and sustainable technology. In 2025, we received 100 Tier 4 locomotives from Wabtec, with 70 more scheduled for 2026, as well as 30 additional units from Progress Rail. These new locomotives feature the latest traction control, efficient cooling systems, and EPA-certified engines, significantly reducing emissions while enhancing network reliability and operational performance. Our locomotive purchases represent a more than $800 million investment in U.S. manufacturing in 2025 and 2026, with locomotives being built in Texas and Indiana. We are also investing to unlock the full potential of our previously under-utilized north-south corridor through the heartland of America. With our capacity expansion projects between Minnesota and Louisiana, we’ve added double-track sections, new sidings, and siding extensions, and installed centralized traffic control.

At the same time, safety remains at the core of everything we do. In 2025, CPKC for the third straight year achieved the lowest Federal Railroad Administrationreportable train accident frequency in the industry. At CPKC, we are upholding our industry-leading standards for safety and operational excellence.

Through our investment in predictive analytics and smart infrastructure management, we’re making significant improvements in maintenance and equipment reliability. Our Geotechnical Engineering team has developed an advanced waterbody monitoring system, harnessing artificial intelligence and satellite data to detect waterrelated hazards across more than 12,600 miles of track. By proactively identifying and mitigating risks such as flooding, we enhance safety, reduce costs, and enable smarter asset management. In addition, our Track Evaluation Cars, deployed continent-wide, allow us to maintain a thorough understanding of track health, contributing to a decrease in track-related derailments and enhancing delivery reliability.

Guided by our Precision Scheduled Railroading model, we continue to serve customers with reliability, efficiency and safety. Even in a challenging economic environment, CPKC remains committed to building our solid foundation and finding new ways to move products, exercising disciplined control and transforming challenges into new opportunities.

For much of America’s 250 years, G&W railroads have ser ved a diverse range of American industries — from family-owned lumber yards and Midwest grain elevators to paper mills and global mining companies — handling any commodity — from automobiles and agricultural crops to wind turbine blades and construction materials.

Powering the North American Economy

By Tracy Robinson, President and CEO, CN

We power the economy. That is what we do every day at CN, and it is how I think about the value we create.

Our role is to provide transportation solutions that meet our customers’ needs at every stage of their businesses. That may mean moving critical inputs into their facilities. It may mean helping them reach established markets or enter new ones. It also means ensuring the products people rely on every day are where they need to be, when they need to be there. We create value by delivering this work in a way that is predictable, reliable and efficient.

A large part of that comes back to operational strength and agility. We are

running a strong operation and staying close to our customers so we can respond quickly as markets and trade flows evolve. In today’s environment, that matters. Supply chains are shifting and trade patterns can change quickly. Our customers need a partner that can move with speed, confidence, and consistency and that is exactly what we are focused on delivering.

When trade flows shift, we need to be positioned to respond quickly across the entire organization.

We have completed a major investment cycle and added meaningful capacity over the past several years. We have put that capacity in place at a much lower cost per unit than we have in the past. That matters because it is not just about one round of investment. It is about building a discipline and a repeatable capability that strengthens CN over time.

Looking forward, I am confident about the growth potential of CN’s network, which sits on top of a tremendous natural resource base across Canada and the United States. There are significant opportunities. That includes agriculture products such as grain. It includes mining and critical minerals, potash and metallurgical coal. It also includes frac sand and a range of energy products, including NGLs, refined fuels and crude oil.

We also have an unparallelled port network that provides access to every major global market.

What stands out to me about many of these commodities is that they are not tightly linked to the consumer cycle or the economy of the moment. They are tied to the long-term needs of the world. They reflect the resources North America can supply and the role this continent will continue to play in supporting global demand. That gives CN a strong foundation for sustainable growth.

When I think about how we are adding value and positioning the company for growth, it comes down to a few core elements. We deliver dependable transportation solutions for our customers. We continue to strengthen the railroad so we can serve them better and more efficiently. We are becoming more productive and more agile, enabling us to respond quickly as markets and trade flows change. And we are anchored by a network that is deeply connected to the resources and supply chains the world will need for the long term.

Over the past 18 months, we have also leaned in heavily on operational productivity, and we are seeing real improvement. That work is continuing as we move deeper into yards and terminals. The benefits extend well beyond efficiency alone. Greater productivity makes us more resilient. It allows us to move faster. It makes us more nimble. In this environment, nimbleness matters. CN

That combination gives us confidence in the value creation for customers, and in CN’s ability to grow by helping our customers grow, while continuing to power the economy.

THE VISION

THOROUGHBREDS POWER MORE.

From digital tools that give you more visibility into your shipments to systems that monitor track conditions in real time, our rail innovations are designed to move what matters—safely, reliably and more efficiently than ever.

LEADERSHIP PERSPECTIVES

Supporting the U.S. Economy

By Steve Angel, President and CEO, CSX

At CSX, we are in an excellent position to benefit from the re-industrialization of the United States. This is a fundamental part of our growth strategy, and as federal, state, and local governments continue to encourage investment within the U.S., our aim is to ensure that this new industrial capacity utilizes the advantages of CSX rail wherever possible.

Our CSX Select Sites® initiative is the most important element of our Industrial Development program because it allows us to play a direct role in bringing valuable capital investment to the region we serve.

We launched the CSX Select Sites

initiative in 2012 as the first railroad-sponsored industrial site certification program that would help customers navigate the challenges of site selection for development of substantial new manufacturing facilities. Since then, we have certified dozens of sites that meet clear standards for rail access, proximity to infrastructure, environmental readiness, and workforce availability. This has been a great benefit to shippers by reducing execution risk and shortening their effective time to market.

help our customers see the clear economic and sustainability advantages of rail-served sites from the start, we know that they are more likely to locate their projects on the CSX network.

We have continued to make enhancements to this initiative over time. In 2023, we launched an online portal that provides real-time access to vetted select sites. The searchable platform allows users to quickly identify properties that meet their specific requirements. That same year we also introduced a framework of Platinum, Gold, Silver, and Bronze ratings to clearly signal site readiness, making it easier for customers to distinguish between constructionready, large-scale sites and earlier-stage opportunities with high potential.

Today, the CSX Select Sites portfolio continues to expand in both scale and geographic reach. In 2026, CSX added 21 new rail-served properties across a dozen states, bringing the total to 80 certified sites across all tiers. This expansion reflects sustained customer and community interest and reinforces the strategic value of CSX’s network footprint.

Since its launch, the CSX Select Sites program has delivered tangible real-world results. Through 2025, select sites-certified locations have helped drive more than $16 billion in reported private capital investment and will support the creation of more than 12,000 jobs across CSX’s network. Critically, CSX’s long-term growth profile has also gained as our customers build out productive assets across our service area.

One great example is Owens Corning’s announcement of a major investment at South Industrial Park, a Silver CSX Select Site in Prattville, Alabama. After years of collaborative planning with local partners to position the site for success, we’re excited to see the benefits of those efforts. The Owens Corning project is expected to create 100 skilled manufacturing jobs, strengthen the local economy, and further expand CSX’s industrial footprint across the region.

I’m proud of what the CSX team has built with this effective, commercially focused program. CSX Select Sites is a critical component of our overall industrial development effort that truly stands out in the marketplace, supports profitable growth, and reinforces CSX’s role as a long-term partner in supporting the U.S. economy.

By highlighting select sites that are immediately rail-ready, this program also helps shippers understand all their transportation options from the early stages of the development process. When we can CSX

BUILT TO DELIVER

Turning Finders into Fixers: How Technology Is Advancing Rail

By Mark George, President and CEO, Norfolk Southern

What is Norfolk Southern’s most important technol ogy initiative? The short answer is AI. Our team of data scientists are leveraging AI to elevate safety and reliability across our network. Running a nearly 200‑year‑old railroad comes with unique challenges, including how to honor the craftsmanship and discipline that built this industry while modernizing at the pace required to serve today’s fast‑moving economy. At NS, we have focused on thoughtfully integrating technology into our day‑to‑day operations to strengthen resilience and equip our railroaders with better tools so they can do what they do best, safer and more effectively.

We have built an integrated digital inspection ecosystem designed to close the gap between defect detection and action, empowering our teams to shift from finding defects to fixing at scale. By layering AI over our world class Digital Train Inspection (DTI) portals, our Wheel Integrity System (WIS) scanners and our Auton omous Track Geometry Measurement Systems (ATGMS), we are fundamentally changing how defects are detected, prioritized, and repaired, strengthening safety for our employees, our

customers, and the communities we serve across our 22‑state network. Technology gives us the opportunity to be more precise and proactive.

Our DTI portals are a cornerstone of that transformation. These systems use stadium‑level lighting and dozens of ultra‑high‑resolution cameras to capture roughly 1,000 images of every railcar as trains pass through at full speed, day or night, in any weather. Our in‑house data scientists have built more than 85 AI algorithms that analyze those images in real time, identifying defects that the human eye simply cannot see.

Today, more than 75% of the defects we identify on our railroad are first detected by technology. These systems can pinpoint microscopic changes imperceptible to the human eye long before they become visible problems. The result is tangible: we recently recorded one of the safest operating years in our company’s history – a testament to the powerful combination of our frontline rail roaders and smart investments in technology that supports their work.

Wheel failures can have serious consequences if they go unnoticed. That’s why we built on the success of DTI with our more specific WIS, a technology designed specifically to identify

cracks and flaws in steel wheels. Using special ized camera angles and lighting, the WIS and our advanced AI algorithms recently detected and confirmed a cracked wheel before it could fail. That early detection led to root‑cause analy sis, an external vendor recall and identification of similar defects elsewhere. This technology is preventing incidents before they occur.

Equally important is what’s happening beneath our trains with our track infrastructure. Through ATGMS, we’ve equipped locomo tives with lasers and sensors that continuously measure alignment, gauge and subtle changes in track structure as they move across the network, using AI to analyze images and find exceptions. Instead of relying solely on scheduled walking or hi rail inspections, we now have a near‑real‑time digital view of track health to help identify broken rails, deteriorating ties, and issues earlier and with greater accuracy.

Across all these systems, the philosophy is the same: technology excels at detection; people are essential for judgment and repair. Our railroaders’ expertise is invaluable. By allowing technology to handle more of the finding, we can redeploy skilled inspectors to focus on reducing risk, improving reliability and keeping freight moving safely.

This emphasis on technology enabled inspec tion, repair, and asset visibility will be espe cially important as we plan to merge strengths with Union Pacific and create the country’s first truly coast to coast railroad; a network of that scale must deliver not only reach, but consis tent, predictable service customers can trust. These technologies and others give us a shared, data driven view of asset health, allowing issues to be identified earlier, addressed more quickly, and managed more uniformly across a broader geography. For customers, that translates directly to fewer disruptions, stronger network fluidity, and greater confidence that freight will move safely and reliably from origin to desti nation. As we look ahead, these systems will be foundational to building a railroad that is more resilient, more dependable, and designed to perform at the highest standard every day.

Modernizing rail isn’t about chasing novelty. It’s about responsibility. When you move heavy freight and a wide range of materials through communities every day, safety must remain the value that guides every decision. By embracing digital inspection technologies that augment human expertise, we’re moving our industry into the 21st century while staying true to the values and the railroaders who built it.

Adding Value to the Global, Multi-Modal Supply Chain

By Jim Vena, CEO, Union Pacific

I’m focused on the facts. Railroads are the safest form of land transportation, and we continue to get better. But as an industry, the fact is we need to grow, and if we don’t change, we will get left behind. The U.S. deserves the best transportation system in the world. One that gives customers optionality and the ability to compete globally. Canada has a great system: two coast-to-coast railroads. Its government is investing in places

like the ports to entice Canadian businesses, but this takes opportunity away from the U.S.

That’s why our merger with Norfolk Southern to create America’s first transcontinental railroad is so important. The benefits of this end-to-end combination are simple: faster service, a more reliable network and lower costs. It will also open up new opportunities to move goods in and out of underserved markets and allow us to compete with long-haul trucking.

For example, farmers rely on rail to reach processing facilities and export terminals. Today, interchange delays slow things down and add cost. A seamless transcontinental railroad changes everything. Soybean meal from western crush plants would move directly to East Coast markets. Grain originating east of the Mississippi would reach Gulf Coast export ports more efficiently.

America’s chemical industry is another good example. Our chemical customers operate specialized and expensive equipment. Efficient railcar use creates real value. Faster and more predictable transit times allow them to reduce expensive inventories. Shifting freight from road to rail reduces touches and lowers risk.

As manufacturing comes back to the U.S. and supply chains shift, a unified network would put us in the right place at the right time. Businesses would have single-line access to 100 ports and 10 international gateways in North America, giving them more options to respond to changing global markets. That means more business here at home, and more American jobs.

This merger stands out from previous combinations in our industry because it is fundamentally about growth. Some skeptics question our projections. What they miss is that no previous merger has offered customers the benefits of cross-country single-line service, stronger competition with long-haul trucking, and a solution for decades-old bottleneck challenges.

Looking to the future, we see growth opportunities in every major segment: agriculture, automotive, chemicals, foods, forest products, industrial development, intermodal and metals. On our own, Union Pacific will continue to invest in our railroad, provide the service we promise, and grow with our customers, but that growth is incremental. The transformational opportunities we see are only possible with seamless transportation coast to coast.

This is a moment when the railroad industry must think bigger about its role in the American economy. Today, Union Pacific and Norfolk Southern represent less than 11% of the transportation market. By building the first transcontinental freight network, we can grow the railroad sector, strengthen supply chains, attract new business to U.S. ports, and help American companies compete in global markets. The opportunity is enormous, and we intend to deliver.

GAIN A COMPETITIVE ADVANTAGE & WIN WITH BNSF

SUPPLY CHAIN EXPERTISE YOU CAN COUNT ON

Not all railroads are the same. At BNSF, our enduring commitment is to be the best transportation partner for our customers. Our dedication ensures you can count on us to deliver the supply chain solutions your business needs to succeed. Because when you win, we win together. We call this the BNSF Advantage.

LEADERSHIP PERSPECTIVES

Delivering for the Nation, 199 Years and Counting

By Ian Jefferies, President and CEO, Association of American Railroads

Freight rail—approaching its own milestone anniversary with next year’s bicentennial, nearly as old as the nation itself—remains a foundational pillar of the U.S. supply chain. Each year, railroads move roughly 1.5 billion tons of freight over 140,000 miles of track, linking ports, farms, factories and markets nationwide. From raw inputs to finished products, freight rail underpins industrial production and commerce. By moving large volumes of goods with exceptional fuel efficiency, rail also helps keep transportation costs—and ultimately consumer prices—more affordable across the economy. Today’s rail network is not just infrastructure but a modern economic engine— supporting high-skilled jobs, enabling efficient supply chains, and strengthening the global competitiveness of U.S. industry.

Flexible, data-driven policies and smart regulation underpin railroads’ multi-billion-dollar annual economic output—$233.4 billion in economic activity—while helping keep transportation costs low across the supply chain. Railroads are actively engaged in the affordability discussion, working to ensure policy decisions continue to support investment, innovation, and cost-effective freight movement for shippers, businesses, and consumers.

With surface transportation reauthorization approaching, the industry is actively shaping the congressional debate around policies that strengthen a resilient, competitive, and affordable multimodal supply chain. At the same time, the association is pressing for regulatory modernization at the Federal Railroad Administration to ensure safety rules and standards keep pace with technology—priorities that together support sustained investment, innovation, and long-term growth across the freight rail sector.

First and foremost, railroads are calling upon lawmakers in Washington to catalyze freight rail’s historic advances in safety by backing results-based rules over one-size-fitsall mandates. Like the U.S., railroads are at their best when technology fuels innovation. Prescriptive rules that lock in outdated technologies risk limiting progress at a time when new tools are rapidly emerging.

“Safety policy shaped by accommodation rather than evidence rarely delivers durable results,” says Patrick McLaughlin of the Hoover Institution, who recently previewed new analysis showing that long-term economic growth depends on continued reductions in per-unit transportation costs. His research finds that when regulation slows deployment of proven technologies or adds friction that raises rail

shipping costs, productivity declines, freight volumes fall, and those losses compound across agriculture, manufacturing, energy, and exports—undermining safety, affordability, and economic performance rather than reallocating commerce to other modes.

Second, the rail industry is urging Congress to advance meaningful permitting reform to ensure critical infrastructure projects can move forward in a timely, predictable manner. Freight railroads invest tens of billions of dollars each year in privately funded infrastructure upgrades—from bridges and terminals to new track and capacity improvements—yet these projects can face years of delay due to overlapping federal reviews and inconsistent regulatory requirements. Targeted reforms to laws such as NEPA and the Clean Water Act would help streamline reviews, establish clearer timelines and create a more transparent and consistent process across agencies. By modernizing the permitting framework, Congress can accelerate investment in rail infrastructure, strengthen supply chains, and support the efficient movement of freight across the national economy.

Beyond Capitol Hill, AAR is pushing federal agencies to jettison or modernize outdated standards that have failed to keep pace with advances in technology. A clear example is FRA brake inspection regulations. AAR recently submitted data supporting its long-pending petition to adopt Electronic Air Brake System (eABS) technology to track car-level brake data in real time—an approach similar to modern digital brake monitoring frameworks already being implemented by railways in Canada. By revising existing regulations to reflect today’s realities, freight rail would not only improve the network’s safety and service but also save an estimated $1.076 billion in regulatory relief over the next 10 years.

Smart regulation, not symbolic mandates, is key to unlocking long-term growth, sustaining historic private investment and fueling innovation across the industry. Taken together, these policy priorities form the foundation for longterm growth and innovation across the freight rail sector. They are essential to maintaining a strong, interconnected supply chain that supports U.S. competitiveness.

Freight rail has played a defining role in America’s story, and its next chapter is just beginning. As the nation looks toward its next 250 years, railroads work every day to deliver efficiency, safety, and innovation to keep the supply chain moving and the U.S. economy strong.

The Best Bang for the Public Buck

By Chuck Baker, President and CEO, American Short Line and Regional Railroad Association

Short lines have continued to navigate market ups and downs by focusing intently on the customers right in front of them, serving as the crucial connection for those shippers in small town and rural America to the U.S. and global markets. Short lines are the face of freight rail in many communities, serving as the first and last mile of the journey and the retail arm of a wholesale business.

Short lines are resilient and scrappy small businesses that do more with less. We have proven to be growth drivers—the national data shows that, as does the data from each of our Class I partners. The resources being committed to short line growth opportunities by the Class Is also demonstrates that we are critical to the success of the broader U.S. freight rail network.

Based on our origin story, being the formerly unprofitable branch lines of larger railroads with a small customer base, low traffic density, and marginal yet expensive infrastructure, one would have expected a slow, spiraling end to many of the nation’s 603 short lines. Yet, to steal a quote from Jurassic Park, “life finds a way.” For short lines, carloads are life and we have driven carload growth one carload and one customer at a time.

To further ignite growth for the economy

and improve safety on short lines, Congress should support robust and predictable infrastructure funding, particularly through the Consolidated Rail Infrastructure and Safety Improvements (CRISI) program and a modernized 45G tax credit. Both tools have already been successfully deployed to improve short line track and bridges to modern 286,000-pound standards, and both stand ready to do much more.

Upgrading track to the 286K standard provides three important benefits:

• Drives efficiency for shippers and our Class I partners—slower speeds and lightloaded cars delay shipments;

• Lowers costs for shippers and consumers—consistent 286K-capable track across the network will improve system fluidity, throughput, and efficiency—enhancing capacity and improving service;

• Improves safety, as most short line derailments are due to broken rail and wide gauge—basically worn out track and ties.

To fully maximize rail and its inherent environmental benefits as an option for shippers, we must be efficient in price and consistent in delivery.

Short lines have also felt the benefits of CRISI’s power to ignite change in the delivery of services and programs for work force development and safety training, including

a grant to ASLRRA and the Iowa Northern to create a short line-specific training center, with programs that can be delivered in person or virtually. To date the Short Line Training Center has touched more than 1,200 employees. This training, including locomotive simulator and other virtual reality training, ensures that employees are compliant with regulations and understand the safety implications of their actions.

Through annual appropriations to the FRA, Congress has also seen fit to consistently fund the Short Line Safety Institute (SLSI). Created after the tragic Lac Megantic accident in 2013, the SLSI is the educational, training and research source for the short line industry on safety culture. With more than 179 Safety Culture Assessments conducted, the SLSI has reached more than 25,000 railroaders and transformed the understanding of safety culture in the short line industry.

The result of these efforts is evident in safety statistics reported by the FRA—in 2024, a record 387 ASLRRA member railroads reported zero injuries. Zero! 2025 numbers will be reported out in short order and we anticipate another record year.

When operations are safe, shippers are more confident that they will be well-served, and can commit to more volume on rail vs. on truck.

2026 will undoubtedly be an interesting year in our industry, with Congressional surface transportation reauthorization and the possibility of a major Class I combination both standing out as hot items of discussion. Both events have the potential to significantly affect short lines and present both opportunities and threats.

As always, short lines will look to step up, lean in, and engage with these possibilities to maximize opportunities to serve our customers and the country. We will step up to the plate and look to grow carloads by hitting lots of singles, and the occasional home run, serving our customers with the creativity and dedication we are known for. We will lean in, building momentum to ask Congress to support the CRISI grant program and a modernized 45G tax credit that will enable more public and private dollars to be spent on critical infrastructure. And then we will engage, delivering the very best bang for the public buck to deploy those funds effectively and efficiently, growing our shippers’ business, the economy of the communities we serve, and the entire rail industry.

LEADERSHIP PERSPECTIVES

Reimagining Rail Growth

By Peter Gilbertson, President and CEO, Anacostia Rail Holdings Company

Railroad traffic has been flat for more than a decade, and rail’s share of the market continues to decline. Union Pacific has proposed reversing this trend through a merger with Norfolk Southern, while others pursue coordinated service models to show similar outcomes can be achieved without consolidation. The fact that competition is intensifying is a positive sign for the industry.

In an idealized vision of rail operations, all traffic would move as long-haul, non-stop unit trains scheduled between terminals with standardized equipment, uniform train length and balanced loads. Yards, interchanges, road locals and block swapping would largely disappear. For intermodal, this has been partially achieved.

But the benighted “loose-car railroading” operates very differently. Even excluding coal, Class I carload traffic peaked in 2006 and has steadily lost market share to trucking. It would be easy to conclude that the complexity of yards, local service and short lines make carload railroading inherently inefficient.

Yet the data tells a more nuanced story.

In fact, short lines, which primarily handle carload traffic, continue to grow volume even though they interchange nearly all their traffic. Although involving a short line can be perceived as adding friction, it often adds the value of entrepreneurship, local expertise, and tailored service, connecting regional customers to the national rail network and capturing freight that might otherwise move by truck. Just as important, short lines succeed because they maintain personal connections with customers, which has become increasingly rare in the industry.

Short lines also measure success somewhat differently than larger railroads. While operating ratio matters, growth, return on assets and cash flow often receive greater emphasis. There is also a clear recognition that most potential rail traffic is already moving by truck, meaning new traffic may initially carry a higher operating ratio but still create long-term value. We need to go to where the market is. That “follow the freight” mindset reflects an entrepreneurial approach: short lines are often willing to take calculated risks, invest in new customer facilities and design customized service offerings to win freight that might otherwise never touch rail. Class I’s are clear beneficiaries.

While short lines often serve a strategic purpose, improving handoff efficiency remains essential. If the industry wants to grow carload traffic, rather than simply manage its decline, we must focus on improving interchange performance. It should be scheduled and measured in a consistent, fact-based way, with transparent reporting and incentives for consistent performance. Technology such as RailPulse can improve visibility into railcar location and dwell times, helping railroads manage handoffs more effectively. Interchange frequency should also be designed around growth objectives and customer needs, not just operating convenience.

Industrial development is another area where short lines play a critical role in driving rail growth. Short lines actively pursue new railserved customers, working with communities, economic development partners, and site selectors to attract businesses that can ship by rail. This often requires direct investment in track, transload facilities, and rail-served industrial

sites, as well as the willingness to work closely with prospective customers as projects move from concept to operation. As entrepreneurial, customer-focused risk takers, short lines are often the ones identifying opportunities, developing sites and bringing new traffic onto the network.

At Anacostia Rail Holdings Company, we understand the value short lines bring: flexible service, competitive rates, personal attention, and an approach that views every single carload as precious. The workforce of a short line lives and operates in the communities it serves, gaining a deep understanding of local supply chains. This insight helps navigate market dynamics, unlocking new ways to grow freight volumes.

Short lines effectively function as a valueadded service between local customers and the national network, assembling carloads, switching customers, and providing the flexibility many shippers require. In truckheavy markets, this local engagement often determines whether rail can compete at all. It is not simply the presence of a short line that matters, but the customer-first mindset that drives these operations. We prioritize service, problem solving, and long-term growth over short-term operating metrics alone.