VM_PSOJ Economic Bulletin February 2026_ED Version (1)

Message From the Executive Director

s we present the first Economic Bulletin of 2026, we do so at a defining moment for Jamaica’s privatesector.

Thefinalquarterof2025testedournation in profound ways. Hurricane Melissa disrupted infrastructure, agriculture, logistics, and business operations, interruptingwhathadbeenayearofstrong economic momentum. Prior to the hurricane’s passage in late October, realGDPexpandedby5.1% year-over-yearinQ32025, and employment reachedahistorichighof 1.44 million persons, with unemployment holding at 3.3%. These gains reflected disciplined macro-economic management and growing private-sectordynamism.

However, Melissa materially altered the short-term outlook.

Infrastructure losses were estimated at over

Sacha Vaccianna Riley ExecutiveDirector

40% of GDP, with agricultural output losses equivalent to roughly 50% of the sector’s 2024 GDP. The Bank of Jamaica now projects a contraction of between –4% and –6% for FY2025/26. Inflation, whichhadremainedsubduedformuchof 2025, surged in November, with the AllJamaicaCPIrising2.4%inasinglemonth and headline inflation reaching 4.5% by year-end.

The lesson is unmistakable: Jamaica is resilient, but we remain vulnerable to structural shocks.

Yet we begin 2026 with critical stabilizing strengths. Net International Reserves stand at over US$6.1 billion, covering morethan50weeksofgoodsimports.The Jamaican dollar appreciated modestly at year-end, supported by decisive Bank of Jamaica intervention. Remittances continue to provide a critical external buffer.

Macroeconomic stability gives us space. But productivity and management excellence will determine what we do with it.

With unemployment at 3.3%, the labour market is historically tight. Wage-cost pressures are intensifying. Confidence softened in Q4 2025 following both the general election and hurricane-related disruption. In such an environment, growth will not be driven simply by expandingheadcountorraisingprices—it must be driven by productivity gains, technological adoption, governance discipline,andmanagementcapability.

This is precisely why February marks a major milestone: the launch of the Best Managed Companies Programme in Jamaica, in partnership with Deloitte.

This globally respected programmme benchmarks companies on strategy, governance, financial performance, operational discipline, talent management, and long-term sustainability. In a year where GDP is projected to contract, the firms that will outperform are those that manage better those that embed structured decision-making, capital efficiency,riskmanagement,andscalable systems.

Strong management is not cosmetic. It is economic infrastructure.

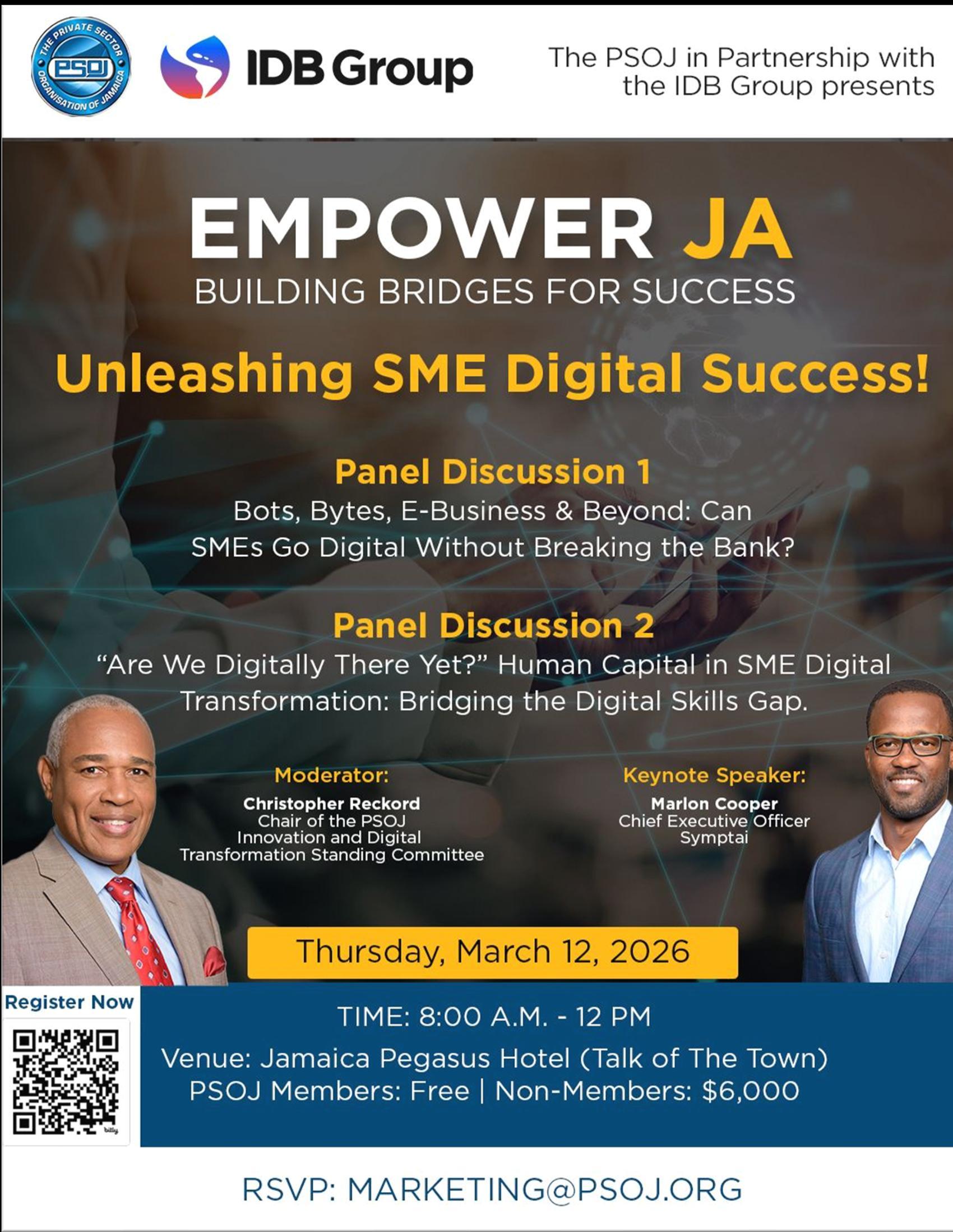

The themes of productivity and scale will continue into March with the next installment of our IDB/PSOJ Empower JA Forum Series, titled “Wired for Growth: Boosting SME Efficiency and Growth ThroughDigitalTransformation”.

The digital transformation conversation is not abstract. It directly responds to the realitieshighlightedinthisBulletin:

The Empower JA Forum will focus on practical tools, digital adoption, AI integration, workforce readiness, and financial solutions to support MSMEs in transitioning toward more efficient, technology-enabled operations. If Jamaica is to stabilize growth beyond the projected recovery in FY2026/27, digital productivity must become mainstream notniche.

Equally important is the health of our transactional and legal infrastructure.

Later in March, the PSOJ will partner with the Jamaican Bar Association to host a joint engagement workshop addressing inefficiencies in conveyancing, mortgage processing, professional undertakings, restrictive covenants, and utility-related transactionbottlenecks.

Straightforward real estate transactions that once took three months are now taking up to nine months. In an environment where reconstruction,

housing demand, and capital flows are central to recovery, transaction delays represent a productivity drag on the economy. Reducing conveyancing timeframes is not merely a legal reform issue, it is an economic growth issue. It affects housing supply, capital turnover, banking liquidity, MSME investment, and householdwealthformation.

Jamaica cannot control global trade tensions, geopolitical volatility, or commodity-pricefluctuations.Butwecan control how well our enterprises are governed,howefficientlywetransact,how digitally enabled our SMEs become, and howproductivelywedeploytalent.

The turbulence of late 2025 has sharpened our focus. Recovery must not merely restore output; it must upgrade capability. Growth must not simply rebound; it must scale. Resilience must notbereactive;itmustbeengineered.

Patrick Hylton: The Architect of Modern Jamaican Finance Steps into a New Era at the PSOJ

When the Private Sector OrganisationofJamaica(PSOJ) announced Patrick Hylton, OJ, CD as its new president in January 2026, the decision resonated far beyond the walls of corporate Jamaica. It signaled a new chapter one led by a man whose fingerprints are already etched across three decades of financial reform, institutional transformation, and economicstewardship.

From Glenmuir Head Boy to Industry Titan

Patrick Hylton’s journey is as compelling as it is inspiring. Long before he commanded boardrooms and shaped nationalpolicy,hewasknownsimplyasa standout scholar the Head Boy of Glenmuir High School, a signal of the discipline and leadership that would followhimthroughoutlife.

His entry into banking was serendipitous. After high school, he eyed a career at the Jamaica Public Service, but chance redirected him into finance a pivot that would alter the trajectory of Jamaica’s banking history. Over the years, his relentless work ethic and laser-sharp commitment to excellence earned him

widespread respect and recognition acrossthefinancialsector.

Hylton’s name became synonymous with the transformation of the NCB Financial Group, where he served as President and CEO and led its ascent to becoming the largest and most profitable financial institution in Jamaica and the most profitable stand-alone financial group in theEnglish-speakingCaribbean.

Nearlytwodecadeslater,in2020,hewas conferred with the Order of Jamaica in recognition of his continued contribution to the financial sector and philanthropic endeavors.

These honours reflect more than achievement they underscore a sustainedlegacyofnationalservice.

Boardroom Leadership Across Jamaica and the Region

Patrick Hylton’s influence extends well beyond NCB. His leadership portfolio includes chairing some of the most prominent institutions in the Caribbean, among them: National Commercial Bank Jamaica Ltd, NCB Capital Markets, GuardianHoldingsLtd.(T&T),ClarienBank Ltd.(Bermuda),GlenmuirHighSchooland MonaSchoolofBusiness&Management.

HecurrentlychairsWIPEnergyandserves on the board of regional conglomerate MassyGroup.

AformerPresidentoftheJamaicaBankers Association, Hylton has also contributed to national policy oversight as a former member of the Economic Programme Oversight Committee (EPOC), which successfully monitored Jamaica’s economic reforms over more than a decade.

A Transformational Vision for the PSOJ

AsPSOJPresident,Hyltonstepsintoarole that aligns seamlessly with his professional philosophy and nationalistic drive. Since taking office, he has been clear-eyed about his priorities: catalyzing higher levels of economic growth, strengtheningpublic-privatepartnerships, and equipping Jamaican businesses— large and small to scale beyond the island’sborders.

Hehasemphasized:

• Improved access to financing, especially for small and medium-sizedenterprises.

• Cutting red tape and promoting technology adoption to boost productivity.

• Encouraging Jamaican companies to serve regional and global markets, breaking through the limitations of a small domestic economy.

PSOJExecutiveDirectorSachaVaccianna Rileydescribes himas a transformational leader with deep credibility across the privatesector.It’sadescriptionsharedby manywhohaveworkedalongsidehimover theyears.

A Leader Defined by People and Purpose

Despite his towering résumé, those who know Hylton often describe him in personalterms:even-tempered,visionary, approachable. His leadership style is aspirational yet grounded, focused on outcomes but always centered on

Awayfromthecorporatespotlight,heisa devotedfamilyman,anavidreader,andan enthusiastic tennis player proof that eventitansmaketimeforbalance.

Steering the Future of Jamaican Enterprise

As Patrick Hylton assumes leadership of the PSOJ, he does so with a rich blend of experience, national commitment, and strategicclarity.Hispresidencyarrivesata pivotal moment one where Jamaica’s private sector must evolve, innovate, and expand to secure long-term economic success.

With Hylton at the helm, the PSOJ gains notjustapresident,butaprovenarchitect oftransformation—oneuniquelyprepared to guide Jamaica’s business landscape intoitsnexteraofgrowth.

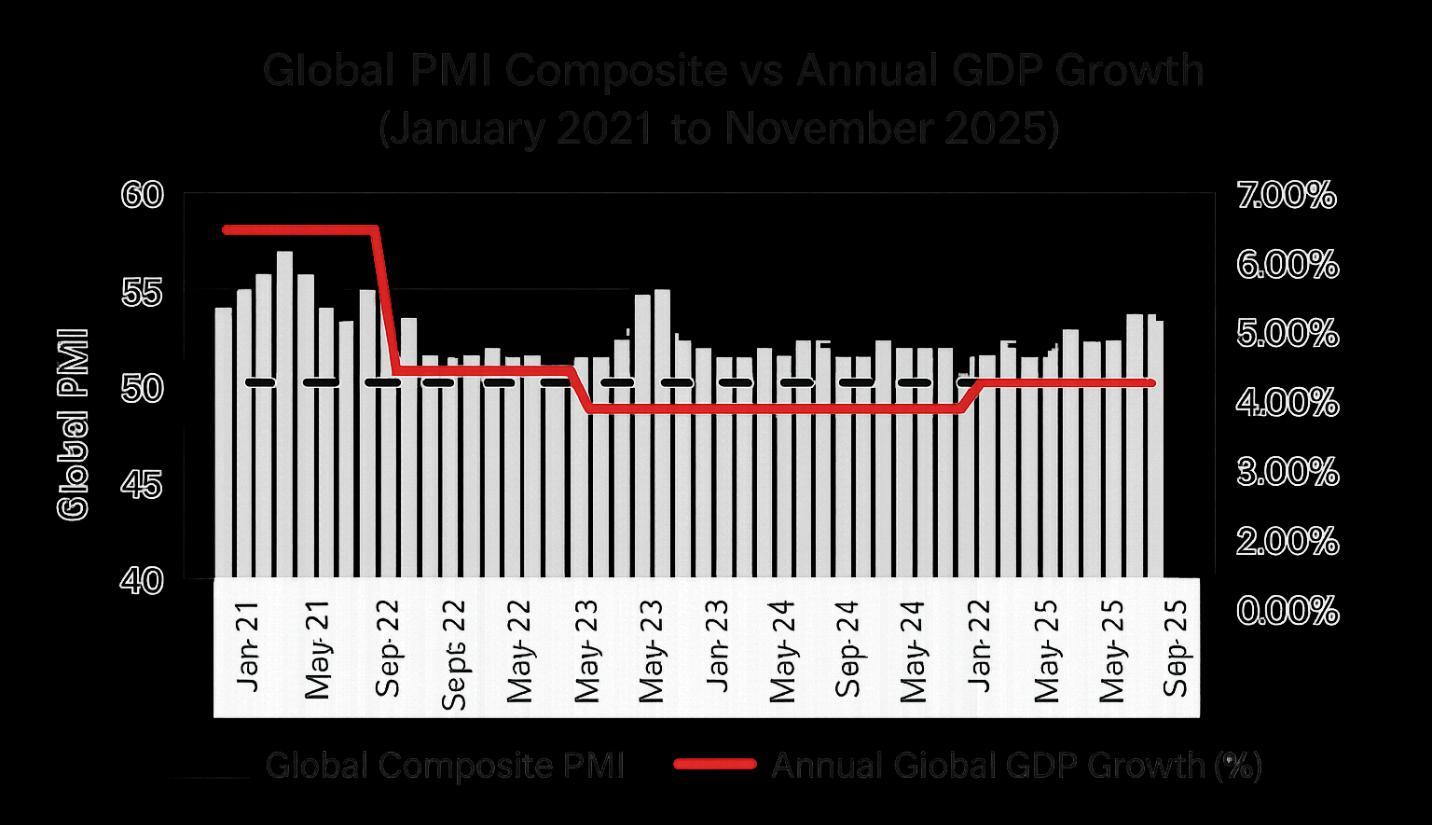

GLOBAL MACROECONOMIC INDICATORS

Global economic activity continued to expandatamoderateandtrend-likepace through late 2025. The J.P. Morgan Global Composite PMI registered 52.7 in November2025, easingslightly from 53.0 in October but remaining above the 50.0 neutral threshold, consistent with steady though not accelerating global growth.

both project global GDP growth of approximately 3.2% in 2025, while the WorldBank’sJune2025GlobalEconomic Prospects anticipates a slower 2.3% expansion. Collectively, these assessments point to continued global growth supported primarily by services, contrasted by softer manufacturing performance.

Global inflation continued to decline in 2025 but remained above pre-pandemic levels. The IMF expects headline inflation tofallfrom4.2%to3.7%in2026,whilethe OECD projects G20 inflation moderating to2.8%in2026.

Figure1:GlobalPMIvsAnnualGDP Growth

Major international institutions broadly align on this outlook. The IMF’s October 2025 World Economic Outlook and the OECD’s September 2025 Interim Outlook

Inflation trends diverged across major economies in the United States, inflation remainedabovetargetduetotariff-related price pass-through, contributing to renewed cost pressures in late 2025. China on the other hand continued to

▪ Persistentservicesledinflation, withsupplysidepressures constrainingfasterdisinflation. These risks reinforce the need for continued monetary policy vigilance, prudentfiscalstrategies,andaccelerated structural reforms to bolster global resilience.

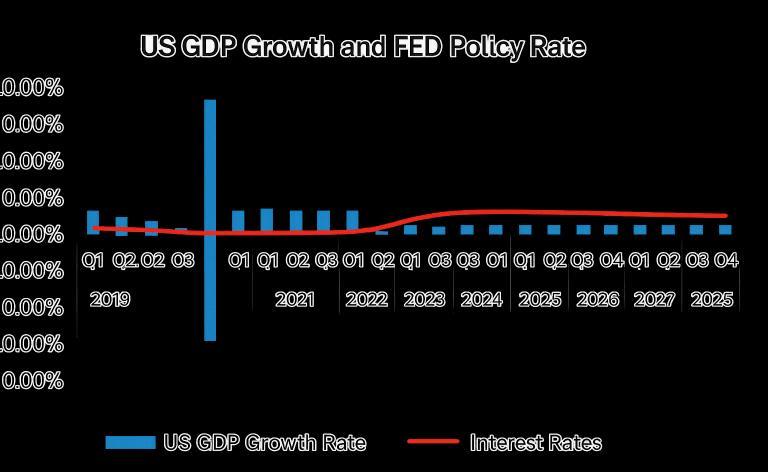

UNITED STATES OF AMERICA

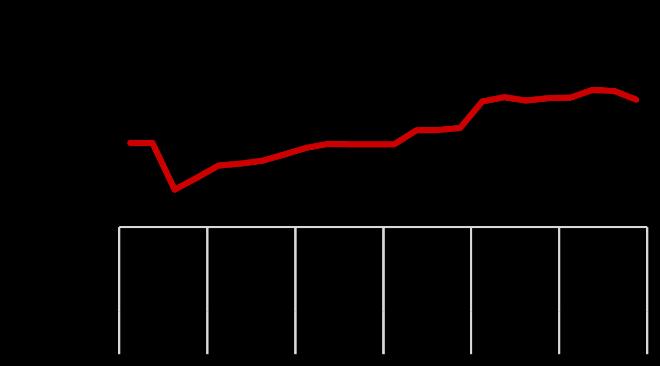

The United States economy ended 2025 withsteadybutunevenperformance.Real GDP grew 4.3% in the third quarter, supported by AI-related investment, resilientconsumerspending,andstronger federal defence outlays (Figure 2) Survey-based indicators suggest this momentum moderated heading into year-end, with December’s Composite PMI falling to 53.0, a six-month low, reflecting slower new business inflows

and rising cost pressures linked to tariff-driveninputinflation.

Labour-market conditions softened as hiringslowed.Jobopeningsstabilizednear 7.7 million, but the unemployment rate increased to 4.6% in November, the highest level since 2021 (Figure 3). Nonfarm payrolls rose by 64,000, below historical norms, although declining weekly jobless claims reaching 199,000 in late December indicate that layoffs havenotacceleratedsignificantly.

Figure2:U.S.GDPGrowth&Interest Rates

Inflation continued to ease. Headline CPI slowed to 2.7% in November, down from 3.0%inSeptember,whilecoreCPIheldat 2.6%. Energy prices increased 4.2% year-over-year, and shelter costs remainedfirmat3.0%,thoughbusinesses reported renewed cost pressures in Decembertiedtotariffimpacts.

In December, the Federal Open Market Committeedelivereditsthirdconsecutive rate cut, lowering the federal funds target range to 3.50%–3.75% in a divided 9–3 vote. The Committee adopted a cautious

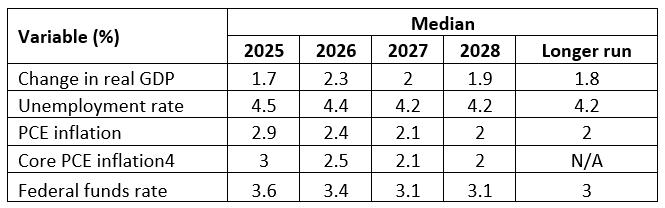

stance,signallingaslowerpace ofeasing as policy approaches a neutral level. The Federal Reserve’s December projections anticipate2.3%GDPgrowthin2026,4.4% unemployment, and PCE inflation decliningto2.4%(Figure4).

Broader risks to the U.S. outlook include renewed tariff pressures, elevated public-debt servicing costs, and the potential for financial-market volatility particularly in sectors linked to rapid AI-driven asset appreciation. Despite these risks, the U.S. economy entered 2026onafootingofmoderateexpansion, cooling labour-market conditions, and easing inflation, with policy settings shifting toward measured support for growth.

DOMESTIC ECONOMIC

INDICATORS

Labour Market

Jamaica’s labour market remained resilient throughout 2025, despite disruptions caused by Hurricane Melissa. For the quarter ending October 2025, the unemployment rate held at 3.3%, unchanged from April and July, and lower than 3.7% in January 2025 and 3.5% in October 2024 (See Appendix E). The labourforcecontractedbyroughly28,000 persons, partly reflecting data-collection challengesfollowingthehurricane.

Figure5:EmployedLabourForce

Prior to the storm, employment had reached a historic high of 1.44 million, driven by strengthening activity in several service-oriented industries, particularly Manufacturing and Education, Human Health&SocialWork(Figure5).

Employment gains were concentrated in higher-skill and customer-facing occupations.

At the industry level, trends were mixed (SeeAppendixF).

▪ The largest decline occurred in Real Estate and Other Business Services, down10,400to155,000workers.

▪ Accommodation and Food Service Activities showed the strongest expansion,adding7,900jobstoreach 124,200 employees. Overall, male employment fell by 1.5%, while female employment increased by 1.2%, indicating a divergence in labour-market outcomes.

Post Melissa Outlook

Hurricane Melissa, which affected an estimated 1.5 million residents, is expected to place upward pressure on unemployment as many enterprises particularly in western parishes experiencedmajordamageortotallossof operations. Reduced employment and income levels may temporarily weaken household spending and could lead to softersavings,investmentflows,andloan performanceacrossthefinancialsector.

Despite these near-term challenges, the recovery phase presents opportunities. Increased demand for housing solutions and construction financing, especially as displacedhouseholdsrelocateorrebuild, could create new avenues for growth within the financial sector, including institutionssuchasVMBS.

Inflation

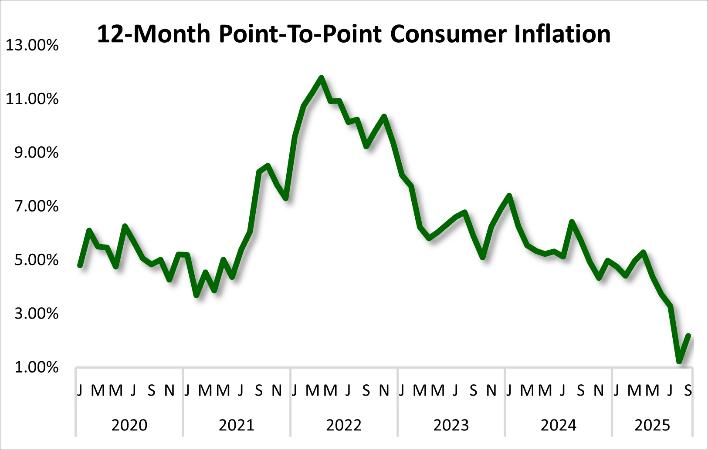

Inflation in Jamaica remained relatively subdued for most of 2025, with point-to-point readings staying below the Bank of Jamaica’s 4%–6% target band up to October (Figure 6). This reflected the delayed effects of Hurricane Beryl and continued stability in several major CPI divisions.

Figure6:12-MonthPoint-To-Point ConsumerInflation

The inflation environment shifted sharply following Hurricane Melissa on October 28, 2025. Severe disruptions to agricultural output estimated at 50% of thesector’s2024GDP drovefoodprices significantly higher. In November, the All-Jamaica CPI surged 2.4%, the largest monthly increase since 2013, followed by

a1.3%riseinDecember,bringingheadline inflation to 4.5%. These increases were concentrated in the Food and Non-Alcoholic Beverages division, reflecting a 19.1% spike in agricultural produceprices(AppendixC).

Policy Response and Short-Term Outlook

Given the sharp supply-driven inflation shock,theBankofJamaicamaintainedits policyrateat5.75%attheDecember2025 MPC meeting and signaled that no rate cutsareexpectedthroughFY2025/26and into the first half of 2026 (Figure 7). Inflation is now projected to breach the 4%–6% target range by early 2026, driven by both direct price increases and expected“second-round”impactsoncore inflation.

Medium-Term Perspective

The Government’s Fiscal Policy Paper projectsthatinflationwillgraduallyreturn toward the 5% midpoint once reconstruction stabilizes supply chains and agricultural production normalizes. This adjustment is expected to align with improved economic conditions in

Figure7:BOJPolicyRate

FY2026/27andagradualeasingofinterest rates as inflation converges back into target.

Implications for Investors

Persistentnear-terminflationarypressure, combined with elevated interest rates, supports a more defensive investment stance.

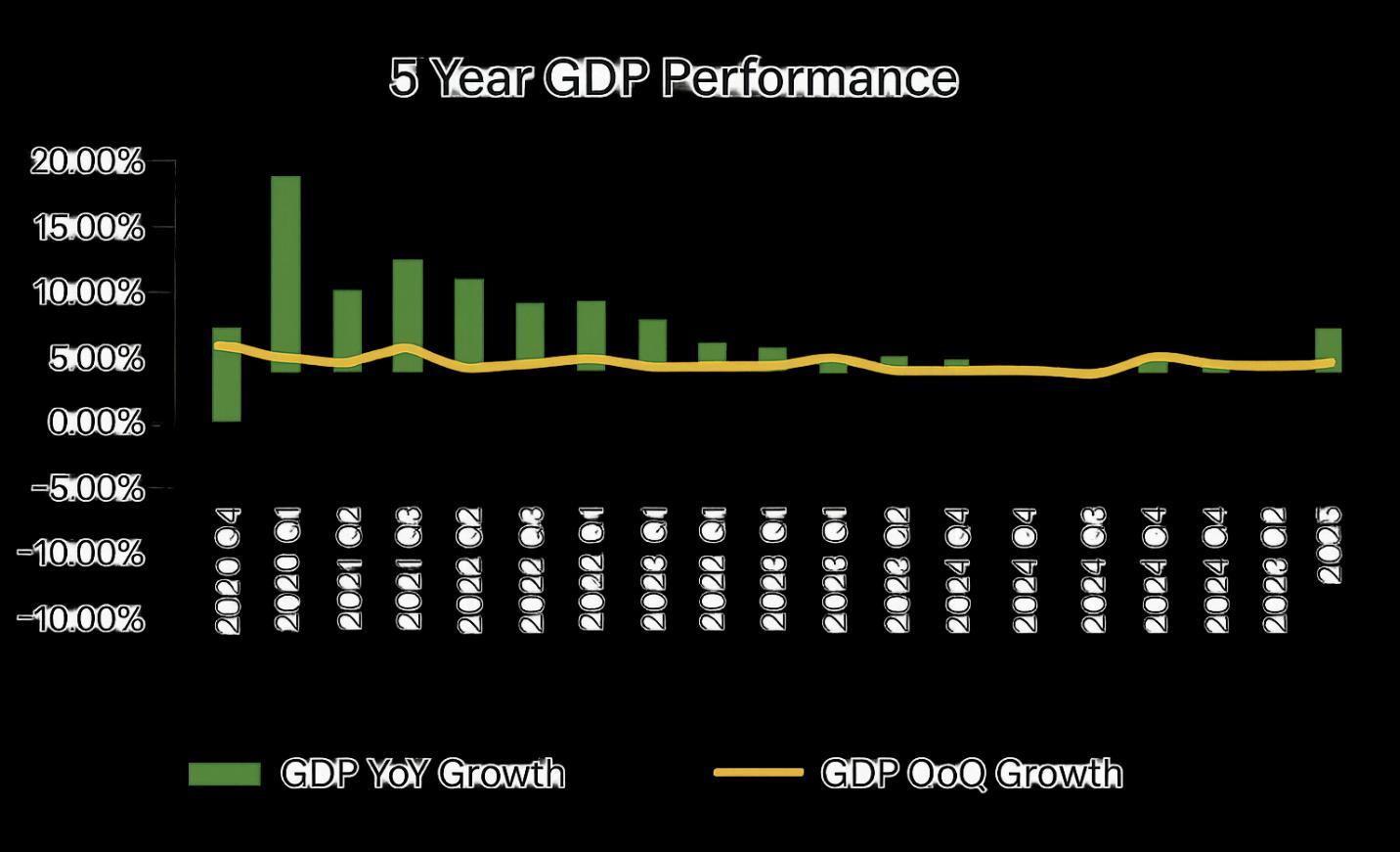

Jamaica’s economic performance remainedstrongthroughthe thirdquarter of 2025, continuing the recovery momentumthatfollowedHurricaneBeryl. Real GDP increased by 5.1% year-over-year, representing the strongest quarterlyoutturnsincethepost-pandemic reboundin2021(Figure8).Theexpansion was driven by a 10.9% rise in Goods

Figure8:YearGDPPerformance

Investors are encouraged to maintain higherliquiditybuffers,increaseexposure to safe-haven assets such as GOJ securities and high-grade bonds, and prioritizecompanieswithresilientbalance sheets. As inflation stabilizes and rates easeoverthemediumterm,opportunities are expected to emerge across both fixed-incomeandequitymarkets.

Economic Activity

ProducingIndustriesanda 3.3%increase inServicesIndustries.Agricultureplayeda significant role, posting a 20.9% rebound supported by improved weather conditions and earlier capacity-building initiatives. Seasonally adjusted output expanded by 1.1% quarter-over-quarter, marking the third consecutive quarterly increase.

This positive trajectory shifted markedly with the passage of Hurricane Melissa in late October 2025. The event caused

widespread damage, with infrastructure losses estimated at more than 40% of GDP, and the agricultural sector suffering output losses equivalent to about 50% of its 2024 GDP. As a result, the Bank of Jamaica now projects a real GDP contraction of between –4.0% and –6.0% for FY2025/26, reversing earlier signs of robustimprovement.

Looking ahead, the Government’s Fiscal Policy Paper outlines a phased recovery beginning in FY2026/27. GDP growth is expected to return to positive territory at 0.7%, supported by reconstruction activitiesandincreasedcapitaloutlays.A more pronounced recovery approximately 3.1% growth is anticipated as rebuilding efforts accelerate and productive capacity is restored. Over the longer term, growth is expectedtostabilizearound1%annually, reflecting a normalization of economic conditions.

Money Market Interest Rates

Jamaica’s money market remained highly liquid through late 2025, even as economic conditions shifted following HurricaneMelissa.InDecember,theBank ofJamaica(BOJ)maintaineditspolicyrate at5.75%,emphasizingtheneedtocontain risinginflationandsupportexchange-rate stability.

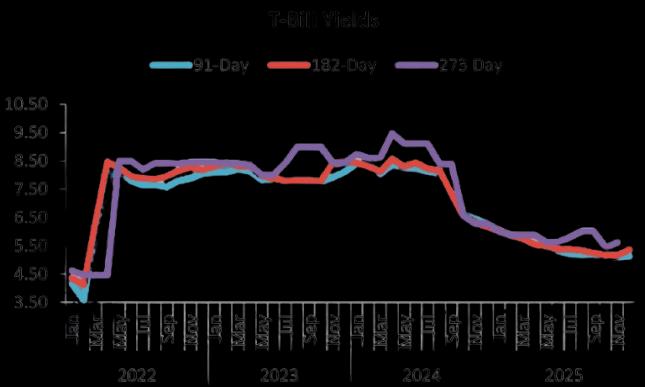

Figure9:T-BillYields

Treasury bill yields reflected continued demand for short-term Jamaican-dollar instruments.IntheDecemberauctions:

• The91-dayT-billyieldfellby5basis points,

• The 182-day T-bill yield rose by 17 basis points, signalling persistent investor preference for short-duration exposures amid post-hurricaneuncertainty.

Throughout November, the BOJ’s 30-day fixed-rate certificate of deposit (CD) operations attracted strong bidding. Total bids reached J$191.4 billion against J$137.5 billion offered an average oversubscription of 1.39x. Over the month, weighted-average yields edged downfrom5.95%to5.85%,reinforcingthe strengthofmarketliquidityandcontinued appetite for government-backed instruments.

Across the four weekly BOJ auctions in November:

• November 5: J$47.9B in bids for J$31.5Boffered(yield5.95%)

• November 14: J$59.1B in bids for J$49.0Boffered(yield5.95%)

• November 21: J$52.1B in bids for J$39.0Boffered(yield5.93%)

• November 28: J$32.4B in bids for J$18.0B offered (yield 5.85%) These results indicate sustained oversubscription and a marginal downward drift in yields as investors sought safety and liquidity.

Implications

Thecombinationofampleliquidity,strong demandforBOJinstruments,andmodest yield compression suggests a stable short-term interest-rate environment heading into 2026. However, elevated inflation and hurricane-related disruptions imply that the BOJ is likely to maintain a restrictive stance in the near term, while market participants continue favouringlow-risk,short-tenorsecurities.

Stock Market

Jamaica’s equity market displayed mixed performance in December 2025, reflecting cautious sentiment following the economic impact of Hurricane Melissa. The JSE Combined Market Index declinedby0.16%,whiletheMainMarket Index fell by 0.21% (See Appendix A). In contrast, the All-Jamaican Composite Indexroseby0.39%,andtheJuniorMarket Index gained 0.48%, indicating selective resilience in smaller, more agile

companies. Total market activity amounted to 830.1 million units traded, valued at over J$5.82 billion across 129 listedsecurities.

Figure10:WeekJSECombinedIndex Performance

Market Dynamics

Performance varied across indices as investors adjusted to elevated inflation, interest-rate stability, and disruptions in keysectorspost-Melissa.

• The All-Jamaican Composite Index contracted5.90%YTD,

• TheJuniorMarketIndexfell8.91%YTD,

• The USD Equities Index declined 15.43% YTD, reflecting global risk aversion and currency-related pressures.

Despite these declines, select pockets of the market continued to attract investor interest. The top volume leaders for Decemberwere:

• TransJamaican Highway Limited –134.86 million units (16.01% of market volume)

• Dolla Financial Services Limited –94.24 million units (11.19%)

• Kintyre Holdings (Ja) Limited – 82.34 million units (9.77%)

Market Context and Forward View

The market environment in December reflectedabalancebetweenriskaversion and targeted opportunity-seeking. Investorsreactedto:

• A projected contraction in GDP for FY2025/26,

• The BOJ’s decision to hold the policy rateat5.75%,

• Inflation pressures arising from hurricane-relatedsupplydisruptions.

Nevertheless, corporate developments such as the high-profile listing of West Indies Petroleum Terminal Limited supported activity in select sectors. In particular,manufacturinganddistribution companies benefited from early reconstruction demand, while investors gravitated toward energy logistics and essential-services providers, signaling a shift toward defensiveness amid uncertainty.

Outlook

The BOJ’s continued FX intervention measuresandstableinterest-rateposture are expected to anchor market sentiment inthenearterm.Asreconstructionefforts progress and inflation gradually moderates, opportunities mayemerge for both short- and long-horizon investors particularly in companies with strong

balance sheets, resilient cash flows, and direct exposure to recovery-related demand.

EXTERNAL SECTORS

Exchange Rates

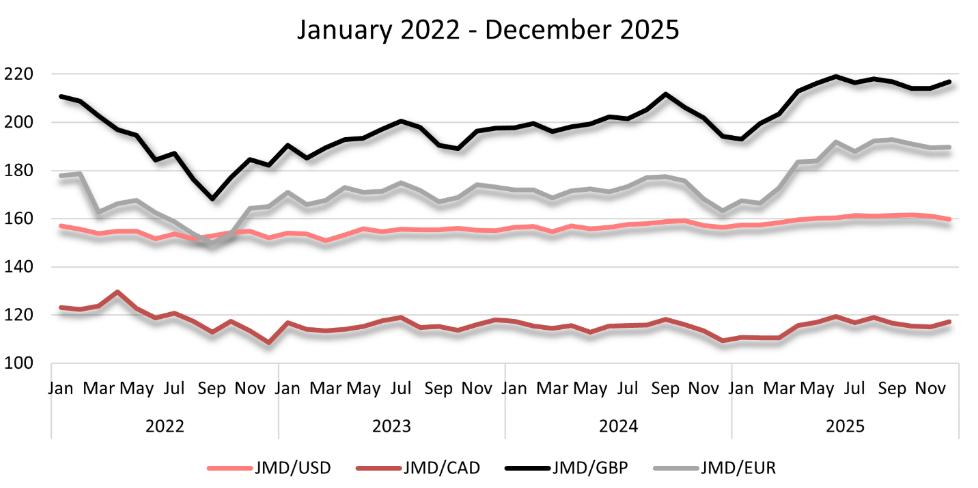

TheJamaicandollarappreciatedmodestly againsttheU.S.dollarinDecember2025, with the weighted average selling rate (WASR) strengthening by 0.92% from J$161.20 at end-October to J$159.74 at year-end. This movement reflected continued Bank of Jamaica (BOJ) intervention, includinga USD$400million

B-FXITT flash sale during November, aimed at stabilizing market conditions followingHurricaneMelissa.

Against other major currencies, performancewasmixed(Figure11):

• JMD/CAD appreciated 1.73% month-over-month,

• JMD/GBPdepreciated1.32%,

• JMD/EUR was relatively stable, declining by 0.14% month-over-month.

The BOJ signaled continued readiness to manage short-term FX volatility, supportedbyastrongreserveposition.

Remittances

Net remittance inflows totaled US$238.0 million in October 2025, an 8.3% decline comparedtoOctober2024.Thedecrease reflected lower inflows through both remittance service providers and other channels, along with a slight rise in outflows. Nonetheless, for the fiscal year to date, net remittances grew 1.2% to US$1.887 billion, indicating continued resilience in this key external source of income.

TheUnitedStatesremainedthedominant source market, accounting for 68.4% of inflows, followed by the United Kingdom (10.9%),Canada(10.4%),andtheCayman Islands(6.2%).Onacalendaryear-to-date basis, remittances increased 1.9%, outperforming declines seen in some regionaleconomies.

Figure11:JMDExchangeRateMovements

Looking ahead, remittance inflowsareexpectedtorise as households receive additionalsupporttoassist withpost-Melissarecovery, aligning with historical patterns following natural disasters.

Net International Reserves (NIR)

Jamaica’s external buffers remained robust.Asatend-November2025,theNet International Reserves stood at US$6.12 billion, a slight decrease of US$5.96 millionfromOctober.Thislevelprovides:

• 50.7weeksofgoodsimports,

• 31.6 weeks of goods and services imports,

• 146.91% of the IMF’s Assessing ReserveAdequacy(ARA)metric.

The monthly reduction was driven mainly by a US$12.1 million decline in Special Drawing Rights (SDRs). Foreign liabilities remainedunchangedatUS$22.44million, all of which represent obligations to the IMF.

The current reserve position continues to underpin FX stability and supports the BOJ’s capacity to navigate elevated post-hurricaneFXdemand.

Summary of Implications

• The BOJ’s active intervention strategy and adequate reserve buffers are key stabilizing factors during the recovery period.

• Remittances remain a critical shock absorber and are likely to strengthen asrebuildingaccelerates.

• While exchange-rate pressures may persist in the near term due to reconstruction-related FX demand, the strong NIR position should help moderatevolatility.

KEY GLOBAL EVENTS

U.S. Military Operation in Venezuela & Rising Geopolitical Risk

Global markets experienced heightened volatility following a major U.S. military operation that resulted in the capture of Venezuelan President Nicolás Maduro. Thedevelopmenttriggeredarallyinenergy and defence stocks and contributed to fluctuations in oil prices, reflecting uncertainty surrounding Venezuela’s futureproductioncapacity.

The operation increased geopolitical risk premia and raised concerns about potential spillovers for Caribbean trade routes, shipping activity, and tourism flows, given the region’s proximity and reliance on stable maritime corridors. Emerging-market investor sentiment also softenedasriskperceptionsincreased.

Global Macro Trends and Risk Themes for 2026

Economic analysis from leading global strategists highlighted several structural risksshapingthe2026outlook:

• The potential emergence of an AI-drivenassetbubbleinU.S.equities;

• Labour shortages fueled by declining migration patterns across advanced economies;

• Intensifying trade and geopolitical frictions, particularly between large economicblocs;

• Higher probability that emerging markets could outperform the U.S. if the dollar weakens and external demandstrengthens.

These themes underscore a landscape characterized by uneven regional performance, elevated valuations in certain markets, and the possibility of sharp corrections should monetary conditionstightenabruptly.

Fragile Global Economic Equilibrium Amid Political Pressures

Despite resilient growth in the U.S. and U.K. during late 2025, analysts warned that their economic equilibrium remains vulnerable.Keypressuresinclude:

• Highpublic-debtservicingcosts,

• The impact of automation on labour markets,

• Tighteninggloballiquidity,and

• Political developments, including upcomingelectionsandshiftingfiscal priorities.

Combined,thesefactorsheightentherisk ofcredit-marketvolatility,potentialstress in sovereign debt markets, and more unpredictablecross-bordercapitalflows.

U.S.–Europe Trade Tensions

Trade tensions escalated as the U.S. administrationlinkedEuropeanregulatory policiestonationalsecurityconcernsand threatened to maintain high steel tariffs unless the European Union adjusted its policies. This stance increased uncertainty around transatlantic supply

chains, industrial inputs, and bilateral investmentflows.

• Weakened investor sentiment toward emerging markets could influence capitalinflows.

• Trade disruptions or rerouting may impactregionalshippingandlogistics.

• U.S. economic conditions, especially labour-market performance, remain critical to Jamaica’s remittance outlook.

SPECIAL REPORT

PayPulse 2025 signals tightening wage–cost dynamics for Jamaica’s private sector

The Caribbean Salary Survey Report:

PayPulse 2025 provides a comprehensiveregionalbenchmark for employers, capturing salary data across 20 Caribbean countries, 137 job roles, 206 companies, and 208 validated responsesfrom119organisations.Itsuse ofUSD-denominatedsalaryreportingand percentile-based benchmarks (mean, median, upper-market rates) enhances comparability across jurisdictions and supports more precise compensation planningforJamaicanfirms.

Regional Positioning and Sector Insights

PayPulse continues to classify Jamaica among the lower-paying markets in the region, particularly for entry-level roles. Higher-paying jurisdictions such as The Bahamas, St. Kitts & Nevis, and Barbados remain more competitive for executive and technical talent. Jamaican employers in Human Resources, Banking/Financial Services/Insurance, and Hospitality & Tourism will therefore face stronger wage-retention pressures, given that these sectors offer higher regional compensation and attract more mobile workers. At the same time, PayPulse notes ongoing wage compression across the Caribbean, especially in frontline positions such as

cashiers, receptionists, bartenders, and groundsstaff.

Affordability Pressures and Implications for Employers

A central finding of the report is the new Affordability Index, which measures the relationshipbetweenaveragesalariesand basic living costs. Jamaica’s score of 103.95%indicatesthattheaverageworker retains only 4% disposable income after coveringessentialexpensessuchasfood, housing, utilities, transportation, and childcare. While classified as “medium affordable,” this narrow buffer means households are extremely sensitive to price increases—particularly in food and transport, where inflation shocks can quicklyeroderealwages.

Given these constraints, PayPulse suggests that non-salary total rewards— transport subsidies, health insurance, flexible scheduling, targeted allowances may provide more cost-effective retention benefits than broadbase-payincreases.

Domestic Labour Market Realities

Jamaica’s unemployment rate 3.3% in late 2025/early 2026 remains one of the lowest in its history, reinforcing an environment of tight labour supply and heightened wage-bargaining power. IMF assessments during the 2025 Article IV consultation described the labourmarket as“historicallytight”andemphasisedthe

shift from job creation to talent scarcity and productivity challenges. Employers that lag market-aligned pay for technical, digital, or managerial roles face longer vacancy durations, higher recruitment costs, and increased dependence on overtimeorcontractworkers.

Recentpolicy adjustments alsoinfluence compensation structures. The minimum wage increase to J$16,000 per 40-hour week (effective June 1, 2025) is expected to generate upward ripple effects throughoutpayscalesasfirmsattemptto maintain internal differentials and avoid compression in supervisory and semi-skilledroles.

Inflation and Cost-of-Living Dynamics

Inflation trends intersect critically with wagesetting.Whileheadlineinflationwas relativelystablethroughmuchof2025,the spike following Hurricane Melissa, combinedwithJamaica’sthinaffordability margin,suggeststhatwagenegotiationsin 2026 will place greater emphasis on maintaining living standards rather than pure performance-based progression. Givenpersistentsupply-drivenvolatilityin food and energy prices, employers are likely to encounter more assertive wage demands especially from lower-income households that allocate larger shares of theirbudgetstoessentials.

Because Jamaica benchmarks below many regional comparators, selective adjustments particularly for high-skill, mobile, or scarce roles may be required to remain competitive. PayPulse’s percentile-based methodology allows firms to align compensation philosophy with business strategy (e.g., lead-market for critical roles, meet-market for core roles, or lag-market supplemented by enhancedbenefits).

2. Strengthen Total Rewards and Non-Wage Benefits to Support Real Incomes

Withhouseholdslivingonnarrowmargins, benefits such as health coverage, transportation support, meal stipends, or childcare assistance may deliver higher retention value relative to broad wage increases. These tools help stabilize employees’ cost of living while safeguardingemployercoststructures.

Overall,PayPulse2025highlightsalabour market characterized by tight supply, escalating living-cost pressures, and widening regional wage competition. For Jamaican employers especially PSOJ members the task ahead is to craft compensation approaches that balance financial sustainability, talent retention, and workforce resilience, leveraging targeted market insights and a refined total-rewardsphilosophy.

BUSINESS AND CONSUMER

CONFIDENCE UPDATE

Confidencelevelsdeterioratedsharply in the fourth quarter of 2025 following the September general election and the extensive economic disruption caused by Hurricane Melissa. Despite this decline, commentary from the Jamaica Chamber of Commerce and GK Capital’s joint briefing suggests that the underlying economy remains resilient, with cautiousoptimismforrecoveryin2026.

Consumer Confidence

Consumer confidence fell from its historic Q3 peak of roughly 198 points to approximately 164 points in Q4 a decline ofabout17.5%.TheQ3highreflectedtypical election-cycle optimism, while the Q4 reversal captured both normalization and hurricane-related fallout. Job prospects remainedtheweakestcomponent,consistent with longstanding public skepticism around employment growth. Additionally, inflation concerns intensified, with nine in ten consumers reporting significantpriceincreasesoverthepastyear. Remittances,however,actedasastabilizing factor, with 30% of households receiving inflowsin2025,upfrom28%ayearearlier.

Business Confidence

Businessconfidencealsodeclined,fallingto roughly133pointsinQ42025.Fewerfirms viewed the environment as favorable for investment, though more than half still consideredtheclimatereasonable,reflecting

continued medium-term confidence. While profit expectations softened, the majority of businesses still anticipate improved profitability,andmanyplantoproceedwith capital investments in 2026. Price pressures are expected to persist, with 96%offirmsanticipatinghigherpricesover thenext12months.

Impact of Hurricane Melissa

Melissa generated widespread disruptions across tourism, agriculture, manufacturing, logistics, and export-oriented industries especially in western Jamaica. Firms cited revenue losses, supply-chain delays, infrastructure damage, and increased operating costs as primary challenges. Still, impacts varied geographically, with around one-third of respondents reporting minimal directeffects.

Recovery Priorities

Consumers expressed clear expectations for how businesses should help guide recovery efforts:

• Job protection and contribution to employmentrecovery,and

• Stronger public-private collaboration on disasterpreparedness.

Businesses,meanwhile,emphasizedtheneed to:

• Buildemergencycashbuffers,

• Improve disaster preparedness and insurancecoverage,

• Upgrade infrastructure resilience and technology,and

• Diversify markets to mitigate future shocks.

Structural constraints remain, including limited access to finance especially for MSMEs underinsurance, and weakened demandandlogisticschannels.

Outlook

Although confidence contracted sharply in Q4,Jamaica’smacroeconomicfundamentals, strengthened public–private collaboration, and ongoing policy support provide a foundationforgradualimprovementthrough 2026. A meaningful recovery in sentiment will depend on effective reconstruction efforts, financing access for MSMEs, and sustainedcommitmenttoresilience-building initiatives.

DID YOU KNOW?

In January 2026, the Jamaican Parliament tabled the Shared Communities Act, legislation designed to formally regulate gatedandsharedresidentialcommunities.A move that could strengthen property management standards and long-term housingmarketstability.

TheproposedActseeksto:

▪ Recognize and formalize community corporations

▪ Mandate maintenance of common property

▪ Strengthenfeecollectionmechanisms

▪ Establish enforcement provisions, including penalties for unpaid maintenancefees

Pre-and Post-Hurricane Melissa Housing Pressures: housing affordability challenges existed prior to Hurricane Mellisa and can intensifyfollowingmajorweatherevents.

Keystructuralpressuresinclude:

▪ Risingconstructionandlabourcosts

▪ Dependence on imported building materials

▪ Mortgagerateandfinancingconditions

▪ Supplyconstraintsrelativetodemand

Post-disasterconditionsmayfurther:

▪ Increase rebuilding demand and constructioncosts

▪ Adjust insurance and lending risk assessments

▪ Strainrentalsupplyinaffectedareas

Data sources: Parliament of Jamaica. Shared Communities Bill, 2026 (tabled in the House of Representatives,January2026).

STATIN (Building Construction Price Index), Bank of JamaicaMonetaryPolicyReports.

REINTEGRATION FOR SUSTAINABLE

COMMUNITY DEVELOPMENT

The Planning Institute of Jamaica (PIOJ) hostedits10thAnnualNationalSymposium ofBestPracticesforSocialandCommunity Developmentunderthetheme“Reintegration for Sustainable Community Development: Bridging Gaps, Building Futures.” The two‑day event focused on strengthening national reintegration systems for involuntary returned migrants (IRMs) and persons formerly in conflict with the law, with sessions streamed publicly on January 27–28,2026.

Day 1 featured a structured agenda combining opening remarks, a keynote address, best‑practice presentations, and lived‑experience testimonies. The programme highlighted both international and local perspectives, including contributions from the International Organisation for Migration (IOM) and the Open Arms Development Centre, which outlined operational models, reintegration frameworks, and lessons relevant for Jamaica’spolicylandscape.

Day 2 examined reintegration within the broader context of public safety and communitydevelopment.Speakersexplored policy implementation challenges, shared international best practices in rehabilitation, and highlighted the role of reintegration in reducing recidivism and strengthening communityresilience.Arecurringthemewas

the link between effective re‑entry systems andimprovedlong‑termsocialoutcomes.

An important feature across both days was the Local Economic Initiative (LEI) Expo, which showcased micro and small enterprises many operated by individuals undergoing reintegration. The Expo demonstrated the potential of community‑levelentrepreneurshiptosupport income generation and strengthen pathways tosustainablelivelihoods.

Key Economic and Social Themes

Highlighted

1. Stakeholders emphasized stigma as a major impediment to labour‑market re‑entry for both IRMs and returning citizenswithjustice‑systeminvolvement. The resulting employment barriers weaken productivity, heighten vulnerability, and slow economic reintegration.

2. Unstable housing conditions were identified as a recurring barrier to readinessforwork,personalstability,and community safety. Limited access to adequate housing also constrains reintegration programmes’ overall effectiveness.

3. Many reintegrating individuals face restrictedaccesstofinancingduetopast recordsorlimitedcollateral,constraining their ability to establish or scale micro and small enterprises. This represents a critical gap in Jamaica’s reintegration ecosystem.

4. Discussions reinforced that effective reintegration is not only a social

developmentimperativebutalsoapublic safety measure, helping reduce reoffending and supporting safer, more resilientcommunities.

Business Implications for the private sector

The symposium highlighted several areas wheretheprivatesectorcansupportnational reintegrationoutcomes:

▪ Employment Pathways

Expanding structured routes such as apprenticeships, work trials, or second‑chance hiring can reduce time‑to‑employment and widen Jamaica’s laboursupplyinatightjobmarket.

▪ Inclusive Financial Products

Developing credit‑building tools, risk‑managed financing solutions, or guarantee partnerships can help address barriers identified by reintegration stakeholders, particularly for budding entrepreneurs.

▪ MarketAccess and Procurement

Connecting LEI‑type enterprises to value chains,procurementchannels,ordistribution networkscanboostrevenuestabilityandjob creation, deepening the impact of reintegrationprogrammes.

TheSymposiumunderscoredreintegrationas bothadevelopmentalandeconomicpriority, with direct implications for labour supply, MSME growth, and public safety. Strengthened collaboration between government, communities, and the private sector remains essential to closing

reintegration gaps and sustaining Jamaica’s trajectorytowardinclusivedevelopment.