December 2025

Governance, Entrepreneurship, and Job Creation in Kenya: Strategies for Unlocking Productivity and Growth

Cover photo from Pexels, used under Creative Commons License

December 2025

Governance, Entrepreneurship, and Job Creation in Kenya: Strategies for Unlocking Productivity and Growth

Authors

Daniel Bosa Rincon, Sarah Bryant, Samantha Churchill, Benton Coblentz, Jessica Dunphy, Mahnoor Kashif, Bryan Manoo, Mohamad Moslimani, Ana Maria Perez, Hana Rajap

Faculty Advisor Professor Mark A. Dutz

January 2026

(This page intentionally left blank)

The authors extend our gratitude to the individuals who contributed to the findings of this report. We are grateful for the technical guidance, vision and mentorship of our faculty advisors, Professors Mark A. Dutz with support from Izak Atiyas. The World Bank Outcomes Department, World Bank and International Finance Corporation (IFC) Kenya country teams and other collaborators also played an essential role in providing contacts, ideas and feedback throughout the drafting process.

Our fieldwork in Nairobi would not have been possible without the support of Dr. Miriam Omolo and her team at the Strathmore Institute of Public Policy and Governance. Their partnership and advice were invaluable to the development of the report.

We also express sincere gratitude to the experts, policy practitioners, and business leaders who shared their time and perspectives with us and greatly shaped our understanding of the issues discussed in this report. The contents of the report do not necessarily reflect the views of the interviewees or their organizations. The organizations or individuals we interviewed are listed alphabetically below.

• Africa Economic Research Consortium (AERC)

• British Chamber of Commerce

• Professor David Khaoya

• Electricity Sector Association of Kenya

• Energy and Petroleum Regulatory Authority

• Ethics and Anti-Corruption Commission (EACC)

• Financial Sector Deepening Kenya (FSD-K)

• Francis Wang’ombe Kariuki, Senior Competition policy Advisor, Bowmans Law and former Director-General of CAK

• Inter-Region Economic Network (IREN)

• Kenya Association of Manufacturers (KAM)

• Kenya Coffee Traders Association

• Kenya National Chamber of Commerce and Industry (KNCCI)

• M-KOPA

• Osprey Renewables

• Public Procurement Regulatory Authority

• State Department of Parliamentary Affairs

• Tegemeo Institute

• The Institute for Social Accountability (TISA)

• The World Bank

• Professor XN Iraki

• Watu Kenya

AG Attorney General

ANM Agent network manager

BRS Business Registration Service

BTI Bertelsmann Transformation Index

CA Communications Authority of Kenya

CAK Competition Authority of Kenya

CBA Commercial Bank of Africa

CBK Central Bank of Kenya

CC Control of corruption

CMA Capital Markets Authority

DCE Departmental Committee on Energy

DCI Directorate of Criminal Investigations

DSS Direct Settlement System

EAC East African Community

EACC Ethics and Anti-Corruption Commission

ECX Ethiopian Commodity Exchange

e-GP Electronic government procurement

EPRA Energy and petroleum Regulatory Authority

ERB Electricity Regulatory Board

ERC Energy Regulatory Commission

FIT Feed in Tariffs

GDC Geothermal Development Company

GDP Gross Domestic Product

IIAG Ibrahim Index of African Governance

IPP Independent Power Producers

JFSRF Joint Financial Sector Regulators Forum

KENGEN Kenya Electricity Generating Company

KES Kenyan Shillings

KETRACO Kenya Electricity Transmission Company

KIPPRA Kenya Institute for Public Policy Research and Analysis

KNCCI Kenya National Chamber of Commerce and Industry

KNEB Kenya Nuclear Energy Board

KPI Key performance indicator

KPLC Kenya Power and Lighting Company

KPCU Kenya Planters’ Cooperative Union

KRA Kenya Revenue Authority

NCE Nairobi Coffee Exchange

LCPDP Least Cost Power Development Plan

MAPS Methodology for Assessing Procurement Systems

Acronyms and Abbreviations

MNCs Multi-national corporations

MoALD Ministry of Agriculture and Livestock Development

MoE Ministry of Energy

MSME Micro, small, and medium-sized enterprises

MTP Medium-Term Plan

NCE Nairobi Coffee Exchange

NKPCU New Kenya Planters Cooperative Union

NPS National Payment System

NuPEA Nuclear Power Regulatory Authority

ODPC Office of the Data Protection Commissioner

PPA Power purchase agreement

PPRA Public Procurement Regulatory Authority

PSP Payment service provider

REA Rural Electrification Authority

REI4P Renewable Energy Independent Power Producer Procurement Programme

REREC Rural Electrification and Renewable Energy Company

SBR State-business relationship

SIPPG Strathmore Institute of Public Policy and Governance

SOE State-owned enterprise

USSD Unstructured supplementary service data

V2030 Kenya Vision 2030

WB World Bank

WGI Worldwide Governance Indicators

Facing weak productivity growth, tight fiscal constraints, and growing youth unemployment, Kenya—like many lower middle income countries (LMICs) undergoing demographic change—is grappling with the challenge of generating more and better jobs.

This report hypothesizes that state policies and governance arrangements shape the intensity and quality of market competition—through the government’s role as policy architect, market regulator, and market developer—thereby influencing productivity and job creation across the Kenyan economy. Whether these functions strengthen or weaken competition depends on governance conditions including credible policy commitment, transparency, checks on discretion, and public accountability. The report explores this hypothesis by leveraging a mix of literature reviews, quantitative data analysis, and stakeholder interviews.

On aggregate indicators of governance—including measures of the control of corruption—Kenya underperforms many peers in the East African Community and globally. Nonetheless, the average experience of countries at higher levels of integrity of public resource use, suggests that if Kenya were to improve its performance in this domain, its entrepreneurial dynamism may dramatically improve. This aligns with firm-level data that indicates younger and more innovative firms with higher labor productivity growth report more bribery requests and greater difficulty accessing essential business services.

To illustrate how these governance constraints related to state-business relations (SBRs) materialize in practice, the report examines three sectors with strong job creation potential. The electricity industry demonstrates how non-competitive contracting and opaque policy processes create economy-wide costs. The digital financial services industry illustrates the interaction between innovation and market concentration, creating opportunities and challenges to unlock consumer gains from technological advances. The coffee industry has strong potential for competitive entry but faces persistent governance challenges.

Overall, enabling more and better-paid jobs will require more than regulatory and rule changes to increase market competition. Policymakers must identify specific governance and SBR mechanisms that impact entrepreneurship and competition. The report identifies several key barriers to job creation:

• The disconnect between potential high-growth firms and access to essential business services must be solved through a business-friendly, level playing field so all productive entrepreneurs can enter and expand.

• Gaps in regulatory oversight must be closed to stimulate competition and job growth.

• Redundancies between and within different levels of government must be resolved to minimize barriers to entry, innovation, and increased production.

• Where the government has stakes in private enterprises, publicly owned firms must be structured to avoid stifling new entrants and innovation.

• Where implementation of good governance policies like transparent procurement is incomplete, the Kenyan government must finalize reforms to encourage public trust and job formalization.

• Governance challenges specific to each individual industry must be identified, addressed and monitored—with learnings applied to improve implementation in these industries as well as other industries.

Specific recommendations for each industry, as well as across the Kenyan economy are summarized in the Summary Table.

Summary Table. Summary of Recommendations

Section Recommendations

Electricity Clarify and streamline institutional mandates MoE, EPRA, KETRACO, KPLC, IPP Office

Prioritize critical grid upgrades

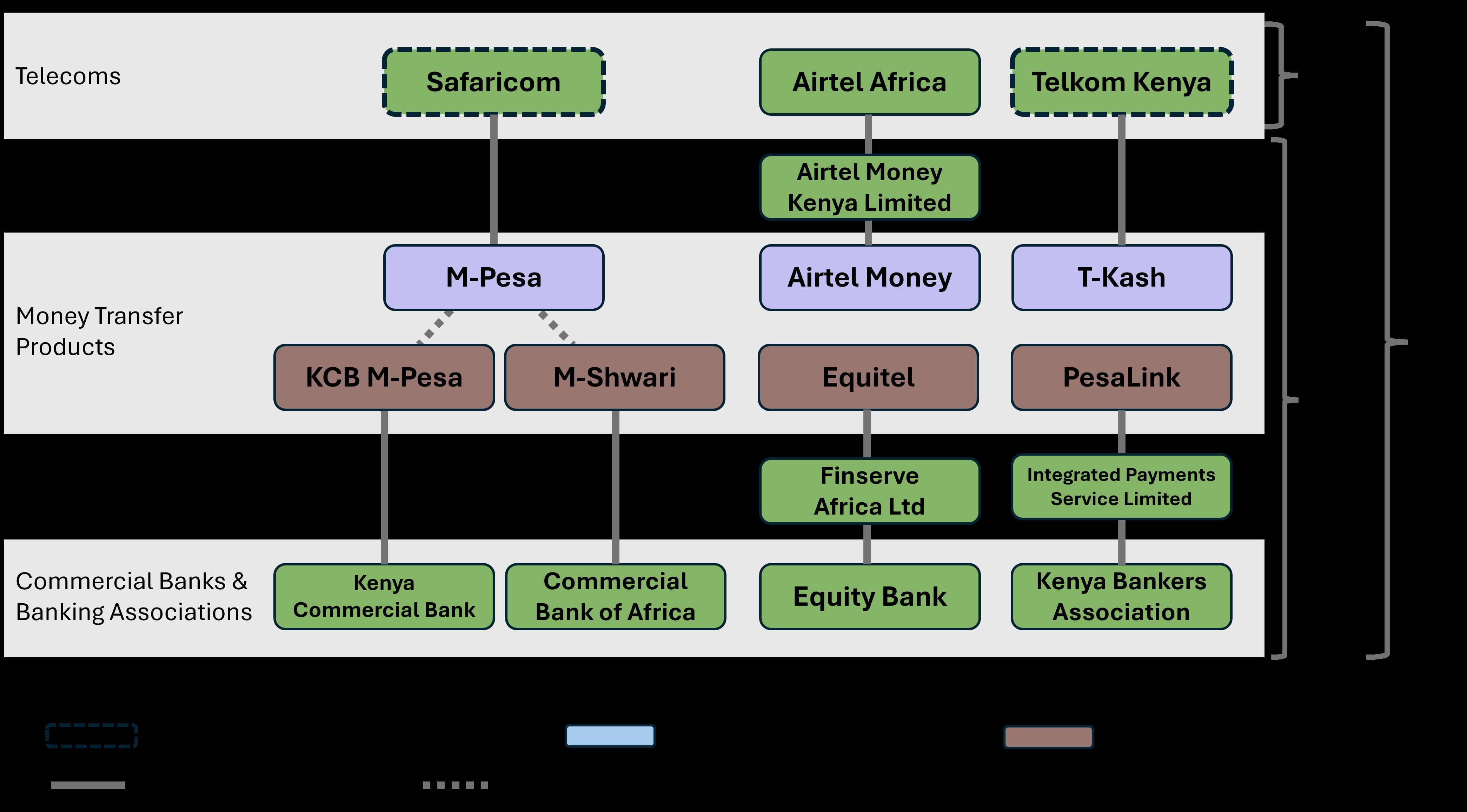

Digital Finance

KETRACO, KPLC, National Treasury, MoE Short-term

Finalize full transmission unbundling KETRACO, KPLC Medium-term

Empower the IPP Office as the central procurement authority Parliament, MoE, IPP Office, AG’s Office Medium-term

Professionalize recruitment and leadership in the IPP Office

MoE, IPP Office, Public Service Commission

Implement the Renewable Energy Auction Policy MoE, EPRA, IPP Office

Strengthen national demand forecasting MoE, KETRACO, EPRA Medium-term

Strengthen regulatory coordination CA, CBK, CAK Short-term

Cap peer-to-peer mobile money fees CBK Short-term

Mandate full interoperability

Implement open finance and data portability

Push for full structural separation of M-Pesa

CBK, CAK Medium-term

CBK, OPDC, JSFRF Medium-term

National Parliament, CBK, CAK, Treasury Long-term

Coffee Simplify and streamline licensing CMA, Coffee Board, county governments Short-term

Increase transparency in licensing decisions CMA Short-term

Monitor market concentration annually CMA, Coffee Board Short-term

Develop contestability safeguards to prevent re-emergences of dominant state-owned or politically connected firms CMA, Coffee Board Medium-term

Enhance DSS transparency and usability NCE, Coffee Board Short-term

Support cooperatives and farmers’ participation in direct sales NCE, Coffee Board, counties Short-term

Use DSS and auction data to track farm-gate income trends NCE, Coffee Board, MoALD Short-term

Pilot a calibrated value-sharing mechanism Coffee Board, MoALD Medium-term

* Timeframe estimates are based on global experiences with similar reforms and synthesis of stakeholder suggestions. Reforms that are more complex, require many actors, and confront more powerful interest groups are classified as longer-term priorities.

Section continued Recommendations continued

Coffee continued Establish an inter-agency coordination platform

Provide targeted governance support to cooperatives and factories

Build county-level capacity for extension and quality upgrading

Responsible Actors continued Timeframe continued

CMA, Coffee Board, county governments, MoALD Short-term

Coffee Board, counties, MoALD Short-term

Coffee Board, counties, MoALD Medium-term

EconomyWide Policy Recommendations

Public procurement: Leverage MAPS assessment to benchmark procuring entities

Public procurement: Partner with the private sector on a market perceptions survey

PPRA Short-term

PPRA, business associations Medium-term

Sub-national licensing and regulation: Fully implement County Licensing Regulations Trade Ministry Short-term

Sub-national licensing and regulation: Improve inter-county trade efficiency

Sub-national licensing and regulation: Unify county business environment assessments

Transparent and participatory policymaking: Adopt and enforce a standard consultative process for inclusive engagement in regulatory and legislative policymaking

KNCCI, Council of Governors, Trade Ministry Medium-term

KIPPRA, Trade Ministry Short-term

National Parliament, State Department for Parliamentary Affairs, AG’s Office, Department for Justice Long-term

1.1 Objective and research question

This workshop report explores selected issues at the intersection of governance, productivity, and job creation in Kenya. It offers recommendations to be used by Kenyan stakeholders, multilateral development banks, and other interested entities to accelerate sustainable job creation as a pathway out of poverty. The report’s insights may also be of interest to other countries facing constraints similar to Kenya.

The report is guided by the following research questions: How do state policies and governance arrangements impact productivity and job creation in Kenya? How are these evident in selected industry value chains?

Kenya’s dynamic business landscape and growing youth population make the country an important model for middle-income countries grappling with demographic change and the generation of sufficient “good jobs.” We hypothesize that governance arrangements can either facilitate or impede the creation of more and better jobs.

1.2 Methodology

1. Literature review: We conducted a literature review on competition and entrepreneurship, market failure and industrial policy, and governance and political economy challenges. We consulted sources including academic publications, World Bank (WB) reports, and government documents—including Kenya Vision 2030 (V2030) and related strategic planning documents.

2. Quantitative data analyses: We use the World Bank’s Worldwide Governance Indicators (WGI)—particularly the Control of Corruption (CC) indicator—to assess the evolution of CC in Kenya and selected regional and global comparators. We also use the Bertelsmann Transformation Index (BTI) “resource efficiency” measure which relies on structured qualitative assessments by in-country and international experts on efficient use of public assets, policy coordination, and anti-corruption policy. We compare the BTI and its relationship

with income levels and political participation across comparator countries. The report also utilizes the most recent round of the World Bank Enterprise Survey for the formal sector in Kenya, conducted in 2018.1 We use both the raw microdata and the available indicators database to conduct correlational analysis to understand Kenyan firms’ perceptions of corruption and the business environment, and how they correlate with firm characteristics, innovation, and labor productivity growth. We do not conduct causal analysis, but our correlational analysis provides suggestive evidence with implications for job growth in Kenya.

3. Stakeholder interviews: We conducted in-person interviews with key Kenyan stakeholders during one week of fieldwork in Nairobi in October 2025, and virtual interviews with individuals who were unavailable during our travel to Kenya. The WB Kenya team and SIPPG were instrumental in connecting us with individuals from the government, regulatory agencies, academia, civil society, business associations and private firms. A full list of interviewees can be found in the Acknowledgements section of this report.

The report first presents an analytical framework relating to governance quality, market competition, and productivity and employment outcomes. Next, it provides by a brief background on Kenya’s political economy and aggregate analyses of governance and related indicators. Grounded in this context, the report turns to case studies of Kenya’s electricity, digital finance, and coffee industries—exploring opportunities to enhance transparency and accountability in state-business relations (SBRs). We conclude with economy-wide recommendations to further align policymaking with the public interest and unlock greater productivity and job growth in Kenya.

The functioning of markets depends on government policies and governance arrangements, which shape the rules, incentives, and constraints that guide firms. Well-designed policies promote competition, innovation, resource efficiency, and output growth, creating more and better jobs. Conversely, distorted policies, weak accountability, corruption, or policy capture, hinder competition—leading to resource misallocation, reduced innovation, and stagnant productivity. The analytical framework underlying this report emphasizes the relationship between government policy choices, governance quality, and market competition as key factors influencing productivity and employment outcomes. This framework helps assess whether Kenya’s governance and policy context acts as a facilitator or barrier to inclusive economic growth.

2.1 Government policies, governance issues, and market competition

This section explores how governments influence the intensity and quality of market competition through both policy design (de jure) and governance practices (de facto).

2.1.1 Government policies that foster competition

Governments can influence markets in the public interest through three roles that directly affect competition:2,3

• As policy architects they set the overall strategic direction for markets—ensuring coherence across industrial, trade, and competition policies whilst establishing the institutional mechanisms that coordinate them.

• As market regulators they define and enforce the “rules of the game” that govern firm behavior, market entry, and fair competition.

• As market developers they allocate public resources to build enabling infrastructure, correct coordination failures, and promote competitive, well-functioning markets.

These functions interact dynamically: effective

policy design provides direction and coherence, regulation translates those objectives into enforceable market rules, and resource allocation operationalizes them through investment and incentives. Table 1 illustrates the main instruments governments use under each role to foster market contestability and efficiency.

2.1.2 Governance issues that affect competition

While formal policies and regulations set the rules, their success relies on how they are put into practice. Even the most well-designed legal frameworks in the public interest can fail to promote competition if governance conditions are weak. Such weaknesses manifest in inconsistent rule application, untrustworthy commitments, or vulnerability to capture by vested interests, among other symptoms.

Governance quality determines whether public actions serve collective goals or private interests. Effective SBRs are characterized by credibility, transparency, reciprocity, and coordination— qualities that foster trust and predictability between the public and private sectors.4 Conversely, when incentives lead—allowing state and business officials to generate, preserve, and share rents— and corruption and institutional fragmentation dominate, SBRs become collusive, policies in the public interest lose credibility, and competition is undermined.5,6

Thus, the interaction between policy and governance determines whether the state acts as an enabler or inhibitor of market competition. Four main governance factors influence competitive outcomes:

• Credible commitment and policy stability: Foster competition by providing predictable market rules. Stable regulation in the public interest and consistent enforcement reduce uncertainty, which encourages firms to plan, enter markets, and innovate.7,8 Policy reversals, exemptions, or uncertain enforcement weaken confidence—favoring incumbents. Credibility underpins strong competition;

Policy architect

• National competition policy frameworks that embed competition principles across industrial, trade, and innovation policies.

• Trade and investment policies that determine exposure to international markets through tariff structures, bilateral agreements, and regional agreements.

• Regulatory impact assessments that identify potential anticompetitive effects of new laws and regulations.

• Inter-agency coordination mechanisms or competition councils that align economic policies and avoid contradictory incentives.

• Strategic industrial or productivity roadmaps that set long-term priorities while preserving market neutrality.

Market regulator

Market developer

• Competition and antitrust policies that prevent cartels, abuse of dominance, and anticompetitive mergers.

• Industry regulations that ensure open access and fair pricing in network industries (e.g., telecoms, transport, and energy) and finance.

• Licensing and market-access regimes that promote contestability through transparent, non-discriminatory, and proportionate entry requirements.

• Standards and consumer-protection rules—including product labeling, quality certification, and transparency requirements—that reduce information asymmetries.

• Oversight of market conduct through independent competition authorities and judicial review.

• Competitive public procurement and Public-Private Partnership frameworks that promote efficiency and entry.

• Time-bound industrial and innovation incentives (e.g., Research & Development, Small and Medium Enterprise support) designed to avoid market distortion.

• Governance of State-Owned Enterprises that ensures transparency and competitive neutrality.

• Public finance and subsidy instruments (e.g., tax incentives, credit guarantees or state aid) implemented with proportionality and sunset clauses.

• Public investment in enabling infrastructure and access to finance programs that lower entry barriers.

Source: Authors’ creation based on Tirole, 2016; Rodrik, 2004; Sen, 2015; OECD,2021; Licetti et al., 2023; World Bank, 2025

without it policies falter and market vitality suffers.9

• Transparency in policymaking: Reduces preferential treatment by elites by ensuring firms have equal access to rules, procedures, and opportunities.10 Clear information flows improve policy design and compliance. In contrast opacity distorts competition by raising costs and enabling rent-seeking.

• Checks and balances on government discretion: Independent oversight, judicial review, and legislative scrutiny prevent regulatory abuse and help maintain competition. Autonomous competition authorities, audits, and courts limit arbitrary

actions and policy capture11,12—boosting government coordination, accountability, and market trust. Conversely, concentrated power or weak independence fosters market-distorting favoritism.

• Accountability to the public: Conflictof-interest rules, transparent lobbying, and accountability address risks of elite capture and corruption by aligning state and business officials’ incentives with economic efficiency. When elites influence policy for private gain, competition suffers. Incumbents lobby to block new entrants, and politicians trade favors for support.13 This collusion leads to rent-seeking and resource misallocation, which lower productivity.14

2.2 Competition is essential for productivity, growth, and more and better jobs

2.2.1 Competition and productivity

Productive SBRs and competition-enhancing policies are key determinants of economic growth and structural transformation.15 When governments design sectoral and industrial policies that preserve or strengthen competition, they channel resources toward more dynamic industries and firms, thereby accelerating productivity growth.16 Competition raises productivity through four key reinforcing channels:

• Productive efficiency: Competitive pressure forces firms to innovate, adopt new technologies, and optimize processes to remain viable.17

• Allocative efficiency: Competition levels the playing field, which ensures that capital and labor flow toward firms and industries where they are used most productively, thus maximizing overall output.18

• Market selection: Competition strengthens the process of “creative destruction” by forcing less efficient firms to exit and enabling more efficient ones to grow and gain market share.19

• Entrepreneurial direction: The institutional rules of the game determine whether entrepreneurial effort is directed toward productive innovation or unproductive rent-seeking. In well-regulated competitive markets entrepreneurs are rewarded for creating value; in distorted markets they compete to capture rents or relocate to more productivity-supporting business environments, limiting innovation and dynamism.20

2.2.2 Competition and more and better jobs

Competition not only drives productivity, but also shapes the quantity and quality of employment. In competitive environments, firms have stronger incentives to expand output, invest, and hire, which lead to higher labor demand and broader employment opportunities.21 However, the magnitude and distribution of these employment effects depend on the nature of market reforms and their interaction with labor market policies. Competition improves labor market outcomes through four main channels:

• Investment and firm expansion: Competitive pressure pushes incumbent firms to become more efficient and invest in productivity-enhancing technologies,

new productive entrepreneurs to enter and expand, and unproductive firms to exit and release their resources to more productive entrants and incumbents. These, in turn, raise firms’ capacity to increase output and thereby create jobs.

• Wage and job quality improvements: Firms exposed to greater competition have stronger incentives to retain skilled workers, train their less-skilled workers, and invest in learning and upgrading for all workers. These actions lead to higher wages, better working conditions, and reduced informality.22

• Innovation and entrepreneurship: By rewarding efficiency and innovation, competition encourages entrepreneurs to allocate their talent to developing new products, services, and technologies. This expands employment across industries, rather than to unproductive rent-seeking activities or more rewarding business environments in other countries.23

• Economic diversification and resilience: Competitive markets promote entry and diversification across industries, creating more adaptable economies that can generate employment even amid structural shifts.24

Thus, competition acts as a catalyst for job creation and upgrading by aligning firm incentives with productivity and efficiency, expanding production of goods and service and thereby generating more jobs. Therefore, economies that foster open and contestable markets are better positioned to achieve both faster growth, as well as more inclusive and higher-quality employment outcomes.

In the 63 years since Kenya gained independence, its economy has grown from less than USD 1 billion to more than USD 124 billion in goods and services produced.25 Yet, fewer than 40% of Kenyans are in wage and salaried work,26 for which the average annual income is approximately USD 2,000. Tracing Kenya’s political and economic development over the past century provides important context for this outcome and the policies this report discusses.

3.1 Kenya’s political history

Kenya was under British colonial rule for nearly 70 years before gaining independence on December 12, 1963. Before independence, British authorities had established a settler colony that operated a highly centralized and statist government.27 The British seized land from locals, structured the economy around the production and export of cash crops, and leveraged fiscal, monetary, and labor policies to enhance their narrow economic interests—impoverishing most Kenyans in the process.28 This colonial legacy still directly impacts Kenya through structural constraints like underinvestment in human capital and growthoriented infrastructure, as well as inherited policies including extensive government intervention and administrative controls in industry.29

After independence, Kenya’s first president, Jomo Kenyatta, introduced land reforms to transfer land from departing white settlers to African smallholders.30 However, rather than expropriating the land, transfers were based on a willing-buyer willing-seller model. Consequently, redistribution was highly unequal and further entrenched an emerging class of local political and economic elites. The inequalities and government distrust propagated by this reform continue to impact land rights and Kenyan politics generally.31

Kenya has also long suffered from extensive patronage networks, though the form of patronage has shifted over time. Under President Daniel arap Moi, governmental institutions were eroded in favor of a loyal network of administrators, and corruption and rent-seeking rapidly became ubiquitous.32 When the opposition rose to power in 2002, patronage networks were sustained under President Mwai Kibaki despite additional attention

to technocratic governance.33 The persistence of patronage networks under successive regimes entrenched the idea that benefits from governance were a zero-sum game for different parties and ethnic groups.34

Kenya also suffered from a stagnating economy in the late 20th century. At 4.2%, annual growth was already slow in the late 1970s relative to its potential for faster economic catch-up. But by the 1990s it had slowed to 1.9%—falling far behind population growth, and leading to rapidly rising unemployment and underemployment alongside an expansion of informal employment.35 During this period, Kenya entered into structural adjustment programs with the WB and IMF that required Kenya to liberalize markets and trade, reduce government spending, and privatize parastatals and civil service functions. Despite implementing such reforms, job growth remained weak.

In 2010, following a deadly dispute over President Kibaki’s re-election, Kenya drafted a new constitution.36 The constitution consolidated Kenya’s democratic transition and enshrined “good governance, integrity, transparency and accountability” as principles of governance.37 The constitution also devolved many state powers to county governments, reversing the previous constitution’s focus on the centralization of power.38 Since the adoption of this constitution, Kenya has made great progress in establishing a legal and institutional framework to increase transparency and combat corruption. However, enforcement has remained highly uneven in practice, with selective enforcement buttressing existing political power and patronage networks.39

Kenya’s economy has changed significantly over the past few decades. The share of labor working in agriculture declined from approximately 70% to a slightly more than 40% between 1990 and 2018, as the employment shares of manufacturing and services expanded.40 Such structural transformation is usually accompanied by strong aggregate productivity growth as workers move from low to high productivity activities. However, in Kenya’s case, structural transformation has dragged

on aggregate productivity growth (Figure 1). Highly productive activities have failed to expand employment, while less productive activities have held on to workers. By contrast, several of Kenya’s EAC peers have benefitted more from structural transformation—with the exception of Ghana, which has compensated for its lack of reallocation with stronger within-sector productivity growth.

Within industries, Kenya’s labor productivity growth has been particularly weak in manufacturing. According to the University of Groningen Economic Transformation database, manufacturing labor productivity in 2018 was only two-thirds of its level in 2000 (Figure 2). Thus, the increase in employment in manufacturing appears to primarily have resulted from the growth of jobs in the less productive informal sector.41

Low growth in labor productivity was accompanied by almost no growth in total factor productivity. This indicates that the efficiency of all inputs used in production—including physical and knowledge capital and how they are combined to generate increased production—did not increase significantly either.42 Weak productivity growth has also coincided with declining external competitiveness. Kenya’s exports have been falling as a share of GDP over time and are overwhelmingly agricultural, with limited value-added exports like merchandise goods or services (Figure 3). This has widened Kenya’s current account deficit and increased pressure on its foreign reserves, whilst precluding otherwise dynamic sources of job growth.

Since its launch in 2008 by President Kibaki, V2030 has guided the country’s economic agenda. The stated aim of V2030 is to “create a globally competitive and prosperous country with a high quality of life by 2030.” V2030 was built on three pillars—economic, social, and political—and is being implemented through a series of five-year MediumTerm Plans (MTPs). The blueprint followed Kibaki’s 2003–2007 Economic Recovery Strategy, which was intended to restore growth and emphasized wealth and employment creation.43

The plan—now on the fourth MTP—provides an overarching, flagship-project-heavy framework with the stated goal of moving Kenya into middleincome status. Subsequent administrations retained V2030 as the official long-term planning anchor while adjusting emphasis via their MTPs. The most significant reframing arrived under President William Ruto, who directed that the fourth MTP be re-aligned to complement his Bottom-up Economic Transformation Agenda44—focusing on job creation, inclusion, and core pillars (agriculture; micro, small, and medium-sized enterprises [MSME] economy; housing; healthcare; digital/creative) meant to drive an economic turnaround and job growth.45 The plan frames transformation in human capital, markets, domestic resource mobilization, and digital evolution as necessary to avoid a “middleincome trap.”46

Figure 1. Decomposition of labor productivity growth, 2000-2018

Contribution by component, 2000 to 2018

Source: Authors’ calculations using the University of Groningen Economic Transformation Dataset

Year

Source: Authors’ calculations using the University of Groningen Economic Transformation Dataset

3.4 Challenges to Kenya’s economic progress

3.4.1 Tight fiscal space

Kenya’s public debt is 68% of GDP, and more than 5% of GDP is spent on interest payments.47 This leaves the government little room to make large new investments towards economic development and puts pressure on it to raise additional tax revenue. Average inflation has been above the target range, while investment and savings rates are below V2030 benchmarks—headwinds that slow capital formation and formal job expansion. Additionally, as a member of several regional organizations, Kenya has limited scope to unilaterally adjust its trade and export promotion strategies to boost revenues.

Figure 3. Exports of goods and services (% of GDP), 1960-2020

Exports as a percentage of GDP

Source: World Bank

3.4.2 Large informal sector and governance barriers to formality

Over 80% of Kenya’s jobs are informal; the informal sector has been responsible for about 90% of job growth in recent years. The “hustler economy” is often spoken about with pride in Kenya, and indeed the informal sector provides many Kenyans with earning opportunities that they would not otherwise have. However, these jobs often offer low wages, limited benefits, and little opportunity for sustainable growth. Furthermore, most informal businesses are subsistence micro-enterprises with no plan to transition to the formal economy48 often citing high and unpredictable taxation, excessive and opaque regulatory requirements, and widespread petty corruption as reasons for remaining informal. Heavy reliance on the informal sector also limits Kenya’s ability to expand its tax base, further exacerbating its fiscal crunch.

3.4.3 Unrealized implementation of good governance frameworks

On paper, Kenyan laws are widely recognized as a robust framework for good governance, accountability, and transparency. But in practice, these measures have not been robustly implemented due to vested interests and a lack of political will. For example, in 2025 Kenya rolled out a new government e-procurement portal which aims to make procurement more accessible, fair, and transparent.49 However, stakeholders have cited concerns about MSMEs still being left behind and continued opacity in the selection process. Consequently, political barriers to full implementation of existing policies must be addressed to fully realize the goals of V2030.

While the 2010 constitution vested political power in 47 discrete counties, it is often unclear how duties and other revenue-raising fiscal instruments are divided between federal and local governments. Due to underdeveloped tax structures, many counties have limited ability to generate their own revenue, which exacerbates inequalities across counties. Furthermore, weak administrative capacity means that public services and projects often suffer from poorly executed procurement and budgeting practices as well as a lack of coordination across counties.

Additionally, devolving political power to local governments has not solved the issue of vast patronage networks and rent-seeking behavior. Instead, it has extended the problem from the national to the local level. For example, stakeholders, complain of having to pay multiple bribes every time they cross into another county. The fragmented regulatory system can also make it difficult for businesses to extend their operations and sales across county lines.

High youth unemployment makes the accomplishment of Kenya’s V2030 goals more challenging. Based on formal metrics, Kenya’s workforce has grown increasingly educated in recent years: 80% of young adults hold at least a secondary school qualification, and over 30% have post-secondary qualifications.50 However, high youth unemployment betrays the fact that many Kenyan youth are unable to fully utilize the skills that their education provides. Without finding productive placements for its youth, Kenya may not be able to see productive benefits from its prime age work force.

Conversely, the agricultural workforce is rapidly aging; relatively few young people are seeking out work in the sector.51 The lack of a reliable flow of new entrants, threatens the sector’s long-term sustainability and growth.

To better understand the effects of Kenya’s policy implementation, this section draws on World Bank Worldwide Governance Indicators (WGI)—particularly the control of corruption (CC) indicator—to assess whether Kenya’s government efforts to address corruption have yielded the desired results. The analysis is complemented by data from the 2018 World Bank Enterprise Survey, which provides insights into business environment challenges faced by Kenyan firms in the formal sector. In recent years, Kenya’s CC indicator has been largely stagnant, indicating that the country is falling behind on the implementation of anticorruption policies. It is important to understand Kenya’s performance in addressing corruption because challenges stemming from corruption may create obstacles that prevent businesses from operating at full potential. This section also investigates Kenya’s capacity to boost its entrepreneurial dynamism; findings suggest considerable potential in this regard.

4.1.1 Evolution over time

The WGI indicators are each aggregated over a large number of individual variables based on data sources produced by 35 think tanks, international organizations, nongovernmental organizations and surveyors of private firm responses around the world. They are reported in their standard units, ranging from approximately -2.5 to 2.5 (the measures are normalized to have zero mean and unit standard deviation based on the unobserved components statistical model).52 WGI reports six governance indicators: CC, political stability, regulatory quality, rule of law, government effectiveness, and voice and accountability.

A review of CC levels reveals Kenya has made limited progress since 2005, remaining largely stagnant. Kenya performs worse in the indicator compared to other East African Community (EAC) countries, including neighboring Rwanda and Tanzania. Within Sub-Saharan Africa Kenya only outperforms Burundi, the Democratic Republic of Congo, Somalia, South Sudan, and Uganda across not just CC but all WGI governance indicators (with the exception of Uganda showing slightly

more progress in the political stability indicator). Compared to other regional partners and other international comparison countries, Kenya’s performance is relatively weak on average, at the bottom over time together with Bangladesh.

This report also leverages the Bertelsmann Transformation Index (BTI) “resource efficiency” indicator—measuring “integrity of public resource use”—as an alternate indicator of corruption, to explore associations with national income, political participation, and entrepreneurial dynamism. The indicator is henceforth referred to as “Integrity” to better reflect what it captures relative to this report’s focus on SBRs.

WGI’s CC indicator, includes 51 separate variables such as whether corruption is prevalent in the health care and education systems and the police force, and the frequency of household bribery across six distinct entities (e.g., education, medical, police). In contrast, BTI’s Integrity indicator consists of only three sub-indicators based on detailed, structured assessments by confidential in-country and international experts. The first subindicator concerns “efficient use of public assets” including the extent to which there are rising public wage bills in State-Owned Enterprises (SOEs) and civil service positions created as a means of political reward, expanding networks of patronage and clientelism in new ministries and county government departments, and politically-motivated private debt write-offs. The next sub-indicator concerns “effective policy coordination” including the extent to which hierarchical-bureaucratic coordination is undermined by personal networks and political appointments. The final sub-indicator concerns “anti-corruption policy” including the extent of conflicts of interest and whether highlevel individuals involved in large-scale corruption are prosecuted as often as low-level offenders.

Kenya’s performance on the Integrity indicator relative to EAC comparator countries is weak, with a marked downturn between 2022 and 2024. Kenya performs weakly across all sub-indicators, with public resources frequently diverted to nonproductive uses at both national and county levels, informal networks undermining institutional coordination, and anti-corruption efforts

remaining largely ineffective.53 These weaknesses constrain the government’s ability to channel resources toward infrastructure development, other productive investments, and employmentenhancing programs.

Kenya performs relatively well in terms of political openness but weaknesses in coordination, public financial management, and corruption control prevent the government from translating participation into entrepreneurial dynamism and positive perceptions of economic opportunities including jobs. Regressing the Integrity indicator against 2024 per-capita income (in current purchasing power parity terms) for countries below USD 30,000 found that on average, higher-income countries have higher Integrity scores (Figure 6). Kenya lies slightly below the regression line, suggesting its integrity of public resource use is lower than expected given its per-capita income.

Plotting the Integrity indicator against political participation54 for a global sample of countries, finds countries with more open political systems tend to use public resources with greater integrity (Figure 7). However, Kenya lies considerably below the regression line, indicating its integrity of public resource use is lower than expected given its political participation score.

Figures 8, 9 and 10 explore how Kenya’s entrepreneurship performance aligns with integrity of resource use. The first figure shows that Kenya’s increase in new entrepreneurs has been relatively stable over recent years compared to more dynamic Morocco and Rwanda.55 The second figure shows that Kenya’s entrepreneurship ecosystem is more dynamic than its income level would suggest. However, the third figure suggests that if Kenya were able to improve the integrity of its public resource use, its entrepreneurial ecosystem may dramatically improve—as Kenya is positioned at the cusp of a take-off of entrepreneurial dynamism based on the average experience of other countries at higher levels of integrity of public resource use.56

Interestingly, public perceptions of anti-corruption policies in Kenya are correlated with public perception of economic opportunities. Data from the Ibrahim Index of African Governance (IIAG), shows a continued decrease in both the public perception of anti-corruption and the public perception of economic opportunities since 2014 (Figure 11).57 This aligns with the literature on anti-corruption measures and their impact on economic growth: Xu et al. (2025)58 find that anti-corruption campaigns in Chinese provinces with higher pre-existing levels of corruption led

in those provinces.

Figure 5. Integrity Indicators across comparator countries

Source: Bertelsmann Transformation Index

Similarly, Colonneli et al. (2021)59 find that in Brazil, firms that were exposed to anti-corruption measures such as audits experienced an increase in employment and size. Trends in perceptions of anticorruption seem to mirror BTI’s Integrity indicator and the WGI CC indicator. For instance, the BTI Integrity indicator decreases from 2022 to 2024 while the WGI CC indicator decreases from 2019 to 2020 and from 2021 to 2022. Similarly, the IIAG indicator shows a decrease in the public perception of anti-corruption measures from 2019 to 2020.

We analyze the latest available round of the World Bank Enterprise Survey for the formal sector in Kenya, conducted in 2018. For purposes of exploring associations with corruption-related indicators, the relatively minor changes between 2018 and 2024 in WGI’s CC indicator and BTI’s Integrity indicator strongly support the relevance of using 2018 Enterprise Survey data as a meaningful complementary source of data for analysis. Given that the new round of the Enterprise Survey will only be released in 2026, this report presents the most timely comparative snapshot from representative enterprises.

We use both the raw microdata and the available indicators database to conduct correlational analyses to gain insight into Kenyan firms’ perceptions of corruption and the business environment, in particular how they correlate with firm characteristics, innovation and labor productivity growth. The difference between the microdata and the indicators database is that the latter contains aggregated, averaged or summarized variables (or indicators) based on the former. Our analysis is based on a representative sample of 1,001 Kenyan firms. Although we do not conduct causal analysis, our correlational analysis provides suggestive evidence that may indicate

potential implications for job growth in Kenya. The data suggest that by easing access to essential business services and lowering bribery occurrences, Kenya could experience more entry of young and innovative firms with higher labor productivity growth—offering a possible link to more and better jobs. However, it is important to consider our findings may be subject to reverse causality.

4.2.1 Young firms to face greater challenges in accessing essential business services

Access to essential business services may vary by firm characteristics such as firm age, size, and ownership type. Recent global research confirms that firm age rather than size is a critical determinant of innovation and dynamic job creation. Younger firms are key engines of job growth since they tend to be established with newer technologies and employ more productive processes. They tend to adopt better technologies and innovate at a faster rate, and are more likely to integrate into global value chains.60 Younger firms in Kenya, however, are also more likely to experience constrained access to essential business services—partially foreclosing their output expansion, or at least making entry into new markets more difficult. Exploring correlations between firm characteristics and various corruption indicators reveals a negative association between older firms and constrained access to essential business services. The constructed “foreclosure of essential business services” index captures the extent to which electricity, transport, access to land, access to finance, tax administration, and business licenses and permits, are obstacles to the firms’ operations. It also plausible that older firms are more experienced in dealing with these constraints, including how to manage potentially collusive SBRs—having acquired said experience over time.

Figure 7. Evolution of

Source: World Bank

Figure 6. Lowess regression line of Resource Efficiency on GDP per capita (below 30K USD)

Source: Bertelsmann Transformation Index and World Bank World Development Indicators

Figure 8. Regression of New Business Density on GDP per capita (below 25K USD)

Source: World Bank Entrepreneurship dataset and World Development Indicators

Figure 9. Regresion of New Business Density on Integrity of Resource Efficiency

Source: World Bank Entrepreneurship dataset and Bertelsmann Transformation Index

Figure 10. Regression of Resource Efficiency on Political Participation

Locally

Source: Bertelsmann Transformation Index

Source:

Firm size also matters. Results indicate smaller firms’ access to essential services is more hindered than that of larger firms. Additionally, firms with foreign ownership are less constrained than those with domestic ownership; this may be partly driven by having better access to finance, by virtue of being more connected to international financial markets, which may enable them to more easily circumvent essential business service constraints. The negative correlation between firms that have at least 10% foreign ownership and the foreclosure of essential business services index lends credence to this hypothesis (see Table A1 in the Appendix).

4.2.2 Hindered access to essential business services is associated with innovative firms

Firms that are more constrained and may be at least partially foreclosed by lack of access to essential business services are the types of firms that are more innovative and productive; they are the likely drivers of more output and jobs if constraints were reduced. When analyzing correlations between selected firm innovation metrics and corruption indicators, conditioned on firm size, age, industry and region, the key pattern that emerges is that firms facing constrained access to essential business services are also more likely to have introduced a new product in the last three fiscal years, offered formal training, or invested in research and development over the previous fiscal year. Similarly, firms reporting corruption as a very severe or major constraint to current operations are also more likely to invest in innovation. An alternative interpretation could be that firms facing greater hindered access to essential business services and higher levels of corruption may engage in more creative and innovative ways of keeping the firm afloat. However, panel data are required to explore this question. Future research should explore whether such investments positively impact firm productivity, and if so, whether the impact is large enough to offset the potential resourcedepleting effects of corruption. It should also

explore whether these relationships vary by firm size and age, among others.

Firms whose senior management spends more time dealing with government regulations (referred to as the “time tax” since it requires investment of time to advance firm objectives) and firms that devote a larger proportion of their sales to giving gifts and making informal payments to public officials (referred to as the “bribery tax” since it requires spending financial resources)61 are also those that undertake more product and process innovation (see Table A2 in the Appendix). This supports the hypothesis that if they were liberated from these constraints, they would have even more time to innovate, expand production, and create more jobs. An alternate hypothesis is that time and bribery taxes on firms throw sand into the wheels of firm output expansion, necessitating innovation to increase production and firm profitability.62 Again, panel data are required to explore this question. Furthermore, receiving a bribery request is also positively correlated with the offer of formal training, process innovation and research and development spending.

4.2.3 Firms experiencing at least one bribery request are associated with higher labor productivity growth

Conditional correlations between bribery incidence and selected metrics of firm performance indicate labor productivity growth over the past three fiscal years is positively associated with receiving a bribery request (see Table A3 in the Appendix). One possible interpretation of this finding is that firms targeted for bribery requests are those that could—if less constrained—achieve even higher productivity growth and translate these gains into output and job expansion. This aligns with findings from complementary studies which suggest that bribery requests may be intentionally targeted towards firms showing signs of increased productivity or profitability, and that corruption might be more harmful to such firms since, in the absence of corruption, they would likely enjoy better access to essential business services.63

Moreover, it is plausible that receiving bribery requests could drive productivity improvements, if firms implement more efficient processes and enhance their performance to counteract the negative effects of corruption. This could include adopting better management practices, investing in technology, or streamlining operations to maintain competitiveness despite the additional burdens of bribery.

Looking within specific value chains helps us better understand how governance and SBRs affect productivity and job creation in Kenya. While aggregate indicators reveal broad challenges in competition, control of corruption, and job growth, the mechanisms through which governance arrangements impact efficiency and employment are most visible at the industry level. Value chains consist of a series of separate value-adding activities, creating multiple points at which the state can either enable the creation of more and better jobs through transparency and fair access, or restrict it through market foreclosure, discriminatory pricing, and other anticompetitive practices. Examining specific industries lets us observe these dynamics concretely and determine where governance reforms could unlock higher productivity growth and more inclusive labor market outcomes.

The nature of governance challenges varies across industries depending on the underlying technology and market structure. In some value chains such as electricity transmission and mobile telecommunications networks, underlying technology costs create natural monopolies or highly concentrated industry segments. Here, competitive outcomes depend on whether access to essential infrastructure is provided on transparent and inclusive terms. Poorly designed or implemented policies governing power purchase agreements (PPAs) or digital payment services can foreclose efficient entrants and result in higher costs for both business and end-use consumers, holding back higher output and job levels. Other value chains such as coffee are characterized by successive segments where multiple firms can compete. Here, vertical integration can generate efficiency gains by providing farmers with credit, training, and quality inputs but can also stifle competition by limiting access to the market if not effectively regulated.

This report explores three industries that illustrate the varied mechanisms through which governance and SBRs shape market competition and job creation: electricity, digital financial services, and coffee. These industries were selected because they:

• Play a key role in Kenya’s economic landscape;

• Exhibit clear upstream-downstream linkages where government policy, market structure, and private sector incentives interact; and

• Offer instructive contrasts in how market competition and job growth can be promoted or undermined.

We draw on lessons from these industries to suggest reforms aimed at promoting competitive markets as well as dynamic and inclusive job creation in Kenya.

5.1.1 Why study Kenya’s electricity industry?

V2030 identifies modern reliable power as a cornerstone of industrialization, making the electricity industry a strategic case study for how state actions enable or constrain growth. Industry dynamics clearly reflect how governance shapes economic performance: procurement rules, regulatory design, and oversight structures determine costs, reliability, and access. This illustrates the core insight of our analytical framework: de jure rules interact with de facto governance to shape market contestability. State policies governing this industry shape energy constraints. As electricity is a critical input across the economy, these constraints define firms’ ability to expand production, innovate, and hire—directly influencing productivity and the ability to create more and better jobs.

5.1.2 Structure of the electricity industry

Institutions that govern policymaking, regulation, and implementation:64

• Ministry of Energy (MoE): Develops and implements national energy policy, planning, and long-term strategy for the industry— ensuring an enabling environment for investment and alignment with V2030.

• Energy and Petroleum Regulatory Authority (EPRA): Autonomous independent regulator; enforces regulations, licenses operators, and sets tariffs across the value chain.

• Rural Electrification and Renewable Energy Corporation (REREC): Manages the expansion of electricity access in rural and off-grid areas, promotes renewable energy use, and oversees the rural electrification fund.

SOEs that form the operational core of the electricity industry:

• Kenya Electricity Generating Company (KENGEN): Leading electricity generator, which provides approximately 60% of the nation’s electricity. KENGEN is 70% government owned.65

• Kenya Power and Lighting Company (KPLC): Owns and operates most electricity transmission and distribution assets in Kenya. Serves as the national off-taker and sole electricity distributor. 50.1% of shares are held by the government.66

• Kenya Electricity Transmission Company (KETRACO): De-merged from KPLC in 2008; plans, constructs, and maintains the national transmission grid.

Private capital:

• Independent Power Producers (IPPs): Private companies that develop, finance, and operate power plants and sell electricity via long-term Power Purchase Agreements (PPAs) with KPLC.

The Kenyan state has played a central role in liberalizing the electricity industry through reforms that increased competition and diversified participation. The Electric Power Act (1997) unbundled generation from transmission and distribution, opened generation to IPPs, and created an independent regulator. Nonetheless, the incumbent retained a monopoly on transmission and distribution.67 Subsequent reforms created specialized agencies such as KETRACO and REREC which reduced the concentration of power in KPLC.68

Sustained public investment and planning amplified gains from liberalized participation. Programs like the Last Mile Connectivity Project and REREC’s initiatives connected millions of rural households—driving rapid expansion in electricity access from approximately 5% in the 1990s to nearly 80% by 2023. 69 Here, the state acted as a market developer, expanding access faster than grid modernization alone would have allowed. Concurrently, Kenya’s commitment to renewable energy—anchored in V2030 and the Least Cost Power Development Plans (LCPDPs)—encouraged public and private investment in geothermal, wind, and solar power, substantially increasing renewable generation capacity. 70 This reflects the state’s role as a policy architect setting long-term industrial

roadmaps that shape investment incentives.

The state has also been receptive to continued reforms that foster economic competition. The 2021 Presidential Taskforce on PPAs reviewed existing contracts to curb high costs and improve governance—signaling a willingness to correct inefficiencies and maintain investor confidence. Liberalization reforms through the Energy Act (2019)71 and the Energy (Electricity Market, Bulk Supply and Open Access) Regulations (2024)72 also opened theoretical competition in the transmission and distribution segments.

Implementation of open access regulations remains in the early stages. Existing PPAs with KPLC complicate matters, as their fixed costs would need to be recovered even if rival suppliers enter the market.73 Stakeholders mentioned that opening competition too quickly could destabilize KPLC if industrial consumers switch to new suppliers, causing the financial collapse of the sole buyer and compromising the entire market.

These risks are compounded by the persistence of several market-foreclosure mechanisms: control over an essential facility (grid access, discriminatory or unclear access terms (absence of open-access pricing and wheeling charges for electricity transmission through a third-party interconnecting network), and regulatory delays that stall the implementation of pro-competition rules. Stakeholders stressed that the constraint is not the transmission monopoly itself, but the lack of

implemented open-access regulations, incomplete transition of KETRACO as the transmission system operator, and opaque or overlapping approval processes. These governance gaps reduce contestability and reinforce incumbent advantages. Thus, despite efforts to increase competition, SOEs remain the main players in each segment of Kenya’s electricity value chain.

While KENGEN remains the dominant actor in generation—supplying 59% of national electricity in 2024/25—IPPs supply approximately 35% of electricity and sell exclusively to KPLC under a single-buyer model.74 This structure could foster competition if procurement is transparent and competitive, but Kenya’s experience has departed sharply from this ideal.

This aligns with Gregory & Sovacool’s argument that the main constraints in Kenya’s electricity industry are institutional and financial risks embedded in how power projects are approved and financed. They highlight that governance-driven investment risks raise project costs and delay financial closure. Projects appear viable on paper but become unattractive once investors factor in opaque processes hindering market entry.75

Against this backdrop, concerns over PPAs with IPPs have triggered multiple state-mandated investigations over the past decade.76 Drawing on

their findings, we identify three key procurementrelated concerns.

1. Non-competitive procurement and regulatory gaps

Most Kenyan IPPs feature take-or-pay clauses, which require KPLC to pay for contracted capacity regardless of utilization—creating substantial fixedcost burdens when demand is low, and resulting in higher tariffs for IPPs compared to KENGEN plants. Moreover, Kenyan PPAs often lock in tariff rates for 20-25 years—compared to 10-15 in other jurisdictions—limiting KPLC’s ability to shift to cheaper technologies as they emerge.77

These terms reflect developers’ preference for long-term dollar-denominated contracts to secure returns and protect against exchange-rate volatility. They also reveal how the absence of competitive procurement—given most Kenyan PPAs originated from unsolicited proposals and subsequent bilateral negotiations—can undermine price discovery and weaken KPLC’s negotiating position.78 Moreover, key documents such as cost-comparison analyses could not be found for several PPAs,79 which raises questions about whether selected projects were the least-cost option for the power system.

The opacity of procurement processes appeared to emerge from an exploitation of regulatory gaps.80 There was no standardized procurement framework governing the evaluation of IPPs when PPAs were awarded. Ad hoc negotiations that emerged within this vacuum created space for arbitrary decision-making and rent-seeking behaviors, which may explain discrepancies in the favorability of tariff terms across PPAs. Such regulatory gaps extend beyond procurement. The 2024 report by the Departmental Committee on Energy (DCE) identified multiple IPPs that secured mid-contract amendments that raised tariffs or extended capacity charges, without public disclosure or clear justification.81

2. Potential conflicts of interest and opaque beneficial ownership

Opaque ownership structures and revolving doors between state institutions and IPPs compounded these risks. The DCE report identified potential conflicts of interest implicating former public officials and IPPs. This included a potential revolving door where an official whose division pushed for the implementation of a specific power station subsequently served as the director of the affiliated corporation.82 Independent reporting has reinforced these concerns. Africa Uncensored (2025) revealed overlaps between former parastatal staff and IPP directors83—suggesting insider relationships may have shaped contracting decisions and negotiations. This could reflect a form

of market foreclosure wherein non-competitive procurement and non-transparent negotiations drive preferential access to government contracts, resulting in the exclusion of more efficient entrants in favor of politically connected firms.

Conflicts of interest are further obscured by limited transparency in beneficial ownership, particularly for companies incorporated abroad. While the Business Registration Service (BRS) provided the DCE with a list of IPP shareholders, the majority listed foreign corporations, leaving the ultimate beneficial owners unknown.84

This opacity reflects a governance gap tied to weak de facto enforcement of de jure rules. As of 2017, the Companies Act (2015) requires all companies— including those registered in other jurisdictions—to disclose their beneficial owners to BRS. However, BRS has indicated that the framework remains only partially implemented.85 Similarly, while Section 27(1)(d) of the new Conflict of Interest Act (2025)86 explicitly prohibits former public officers from taking up employment with “a private entity with which... [they] had significant official dealings during the period of two years immediately preceding the termination of [their] service,” this was already in Section 27 of the Leadership and Integrity Act (2012).87

Full enforcement of both the Companies Act and the Conflict-of-Interest Act could mark a turning point for mitigating conflict of interest risks in the electricity industry. However, the feasibility of such reforms remains doubtful unless underlying institutional weaknesses and incentives that have impeded enforcement thus far are explicitly identified and addressed.

The 2021 Presidential Task Force on the Review of PPAs found that state institutions and parastatals were performing overlapping roles in the procurement and approval of PPAs.88 In several instances, the problem stemmed from institutional overreach. For example, the MoE had invited and evaluated bids for energy projects, only involving KPLC—the legally mandated contracting entity— after selection,89 limiting its ability to negotiate commercially sound terms or ensure alignment with system needs. Such overlaps weaken checks and balances and raise discretion risks. By creating multiple avenues for rent-seeking—including those outside official mandates—these patterns risked compromising transparency, cost-effectiveness, and accountability in PPA procurement.

During the development of this report, the Parliament of Kenya lifted a moratorium on signing new PPAs that had been in place since 2018.90 Notably, the DCE’s final recommendations91 reflected a more limited form of legislative involvement than initially proposed in 2024.92

Parliament is no longer recommended to approve PPAs but retains a broad ex-post oversight role— receiving semi-annual reports on all amendments, monitoring reform implementation, reviewing audit findings, approving land acquisition frameworks, and providing legislative accountability across the industry. This is a positive shift, as it reduces the risk of procurement becoming a politicized process.

The DCE’s conditions also assign a formal legalreview role to the Attorney General (AG), requiring them to:

• review and provide legal advice on all new PPAs prior to execution;

• review every amendment or variation to existing PPAs, regardless of size or materiality; and

• issue this legal advice within 30 days of document receipt—creating a binding procedural deadline.

Effectively, the AG becomes a gatekeeper for contractual legality, parallel to—but different from— the technical and financial due diligence roles of EPRA, the MoE, and the new IPP office proposed to oversee all future PPA procurements. The decision adds an additional layer, which increases the possibility that market entrants will face procedural delays given the volume of contracts and amendments expected in the coming years in a key industry for V2030.

While these changes aim to depoliticize the process by creating the new IPP office, they do not eliminate underlying governance risks in the industry. For example, our field work interviews revealed that while technical engagement with technocrats is straightforward, interactions with the legislators and political appointees are opaque and often politicized. Stakeholders noted that it is not uncommon for the regulator to receive calls from politicians seeking particular decisions, which undermines regulator independence and predictable competition rules.

The creation of the IPP office is not a silver bullet. In South Africa, Eskom’s politically motivated refusal to sign auction-winning PPAs between 2015 and 2017 stalled around USD 4 billion in investment and cost thousands of jobs.93 Kenya risks similar

delays by adding legal layers beyond technical merit.

Legislators’ proposal to cap wholesale power prices at USD 0.07 per unit as a condition to lift the moratorium would be an additional layer of political interference.94 Interviewees in our field work noted tariffs are a recurring point of political contestation that undermines predictability for investors. Thus, maintaining regulatory autonomy without parliamentary micromanagement is essential for credible tariff reviews and investment stability.

Uncertainty remains as the IPP office must translate de jure intentions to de facto results. Field interviews underscored that frequent fiscal, licensing, and policy shifts compound investor risk. As Kenya competes regionally for limited private capital, slow approvals may divert funds to peers like Tanzania or Uganda. Hence, Kenya’s evolving framework reveals a tension between accountability and autonomy. Expanding AG powers may strengthen scrutiny but risk duplicating regulatory roles and slowing decision-making.

The key is to strengthen and depoliticize regulators through structural reforms95. Kenya could empower an independent regulator—the IPP office—and make AG intervention temporary until the new office the role of technical decisionmaker. Kenya can learn from South Africa’s experience, which showed that renewable energy auctions only work when the procurement unit is insulated from political interference, and that the IPP office’s success is contingent staffing it with experienced technical professionals rather than political appointees.96

While the updated DCE recommendations removed the most problematic forms of parliamentary involvement, they do little to reduce the broader policy uncertainty that continues to constrain competition and downstream job creation. Kenya must follow its LCPDP, expand transmission, and limit political interference to avoid repeating crisisdriven, high-cost procurement.

The PPA moratorium was a defining symbol of Kenya’s policy uncertainty and failure to credibly commit to fostering competition. For seven years, investors lacked clarity about why it remained or what conditions would guide its removal. Even now, there is no transparent explanation for either decision. This opacity raises concerns about the risk of future reversals; a policy that can be imposed and lifted without clear criteria can also be reinstated under similar or other political pressures.

Stakeholders emphasized that such unpredictability undermines confidence in long-term planning, especially for capital-intensive generation projects

that depend on regulatory stability over decades. Thus, the moratorium signaled to the market that Kenya’s procurement framework is vulnerable to political dynamics rather than grounded in transparent and rule-based processes.

The moratorium foreclosed the market for new entrants, delayed projects, and constrained supply growth. These delays have jeopardized Kenya’s ability to meet the generation and renewable energy targets set under V2030 and successive LCPDPs, which assume a steady pipeline of competitively procured projects. The lost investment momentum also weakened job creation, industrial competitiveness, and the green-growth agenda. Lifting the moratorium is only a first step: Kenya must prevent the re-emergence of politically driven freezes and institutionalize a credible, transparent, and autonomous procurement process.

Field interviews indicated that uncertainty in the industry also stems from institutional complexity beyond national-level actors. Kenya’s 2010 Constitution devolved critical energy functions to counties. This has led to regulatory fragmentation: procedures for business licensing, taxation, and land acquisition differ widely across counties, raising transaction costs for developers operating in multiple jurisdictions. This weakens coherent policy architecture and lowers incentives for entry. Volkert and Klagge (2022) also highlight how lags in the development of critical roadmaps such as county-level energy plans, coupled with limited institutional capacity and expertise could stymie the development of projects in the electricity industry.97

5.1.7 Structural constraints: operational inefficiencies and market distortions

Persistent inefficiencies in Kenya’s electricity network including high system losses, unreliable service, and deferred maintenance, illustrate how technical weaknesses translate into market distortions. 24.2% of the energy purchased by KPLC was lost in transmission and distribution during the first half of the 2024/2025 financial year, exceeding the regulatory threshold by 6.7 percentage points.98 These losses—driven by aging lines, overloaded transformers, and unmetered connections—undermine the utility’s financial viability and inflate end-user tariffs. Reliability indicators have also deteriorated; on average, customers experience 9.15 hours of outages and 3.57 service interruptions per month.99 Such underinvestment in maintenance and modernization imposes costs on consumers and reduces Kenya’s industrial competitiveness by increasing input costs and production risks. This results in a marketdeveloper failure embedding inefficiency in tariffs.

The Kenya National Energy Compact (2025–2030) recognizes these operational failures as part of a

wider governance challenge. Its targets to reduce transmission and distribution losses by 2030 reflect an understanding that network degradation constrains both reliability and competition.100 Aging assets and deferred maintenance limit the grid’s capacity to accommodate new IPPs and increase the likelihood of curtailment and higher marginal costs of supply. These structural weaknesses create implicit barriers to entry, since new producers face higher connection costs and uncertain evacuation reliability. They also distort tariff structures by embedding inefficiencies into pricing rather than addressing them through network reform. In this way, the condition and management of the grid reinforce KPLC’s dominance and restrict the emergence of a more efficient and diversified electricity industry.

In the short-term:

1. Clarify and streamline institutional mandates across the industry

Clearly define what each institution does, including the MoE, KPLC, EPRA, KETRACO, the IPP office. Eliminating overlapping responsibilities will reduce confusion, limit political interference, and improve transparency across the industry.

2. Prioritize critical grid upgrades

Complement governance-related reforms by upgrading outdated grid infrastructure to ensure end-consumers benefit from increased electricity generation.

• Leverage Independent Transmission Projects where possible to ease financing constraints KETRACO would face if required to shoulder the entire cost.

In the medium-term:

3. Finalize full transmission unbundling

Complete the transfer of all transmission system operations and planning responsibilities from KPLC to KETRACO, to eliminate lingering vertical integration and strengthen competitive procurement.

4. Empower an Independent IPP Office as the central procurement authority

Grant the IPP office statutory authority to make final decisions on PPA procurement, evaluation, and amendment.

• The current requirement for AG approval can operate as a transitional safeguard. Once the IPP Office is fully established with

strong technical capacity, AG sign-off should be phased out to prevent unnecessary political or administrative bottlenecks.

5. Professionalize recruitment and leadership selection in the IPP Office

Establish clear minimum educational and technical qualifications for all professional staff, and require open, competitive recruitment for director-level positions.

• The Head of the IPP Office should serve a single, non-renewable five-year term, with the start date set to avoid alignment with presidential and parliamentary election cycles. This reduces incentive compatibility with political actors and preserves the independence of procurement decisions.