With Alibaba entering the “Buy Now, Pay Later” space and QisstPay making a comeback, what has changed?

For years, Pakistan has run on informal, small-scale credit. The buy-now-pay-later wanted to disrupt it. Now, with Alibaba making an entry and others returning, what has changed and what direction will it take?

By Taimoor Hassan

For decades, Pakistan has run on credit. Not the kind that shows up on balance sheets or credit scores but the kind negotiated across shop counters, backed by personal guarantees, and enforced through relationships rather than contracts.

Walk into an electronics market in Lahore or a motorcycle dealership in Karachi, and you will find offline versions of Buy Now, Pay Later (BNPL) operating in their most basic form - goods exchanged on trust, payments spread over time and prices inflated to absorb risk. Installment buying has long been embedded in the country’s economic fabric and its scale is understood to be massive but opaque and informal.

In essence, what fintech calls BNPL is, in Pakistan, less an innovation than an attempt to digitize a system that never needed software to begin with. That is the market Alibaba Group is now entering through its subsidiary Koko Tech Private Limited. On Tuesday, the Securities and Exchange Commission of Pakistan (SECP) granted Koko the NBFC license - the default license for low-ticket lending such as nano lending and buy now pay later. Koko had been trying to do BNPL in Pakistan for a few years and had been in talks with Pakistani BNPL companies.

This is also the market that Qisst Pay, a former Pakistani BNPL player that quietly wrapped up in 2024 is re-entering, their CEO Jordan Olivas confirmed to Profit.

On the surface, it signals renewed confidence in a financial services category that once promised to transform consumer finance in Pakistan. Underneath, it raises a more difficult question: What has changed? Because the last time BNPL surged in Pakistan, it ran into a reality that technology alone could not solve. And that reality is still very much intact - the financial situation of Pakistani consumers is

The first time installment credit showed

up in Pakistan, it didn’t arrive through an app or a checkout flow. It came through a conversation. Shopkeepers extended credit based on who you were, where you lived, and who could vouch for you. Payments were split informally, prices quietly adjusted, and enforcement relied less on contracts and more on relationships. It was, as Arif Lakhani, CEO of Kisst Bazaar puts it, a system built on “personal guarantees and physical verification.” All to ensure that customers pay back.

That reality might very much still be intact: while the opportunity of customers needing BNPL is large because consumers are very cash constrained, for the exact reason, there is a fear that a large number of consumers might also not pay back. So what does the entry of AliBaba in Pakistan’s BNPL scene hold and what changes can it bring.

The need for BNPL in Pakistan

To understand why BNPL exists in Pakistan, you have to look at how the system is structured. None of the factors in this system operate in isolation. They reinforce each other creating a consumer who is not just underserved but structurally constrained and it begins with access.

Pakistan’s credit card penetration is less than 1%, one of the lowest in the world. For majority of the consumers, revolving credit does not exist and there is no formal fallback mechanism to smooth expenses. Informally, people turn to loan sharks and end up getting stuck in a vicious payment cycle and end up paying exorbitant interest.

Without the option of predatory lending, it is a situation where a consumer can either pay for something today or they can not. Because there is no putting expenses on a credit card for most of the Pakistani population either for religious reasons or because banks won’t hand over a credit card to a customer

that they think is high risk. Average monthly household income is approximately Rs82,179 according to Pakistan Bureau of Statistics 2024–25 data for a family of 6 people. Per capita income translates to roughly Rs13,700. An estimated 36% of the income goes to food expenses alone, resulting in a very restricted disposable income. If banks lend to such customers in any form, chances that she/he will default are very high.

This means that financial planning is more about survival for most of the population than optimization. Cash flow is tight and savings are minimal.

On top is the layer of inflation. As prices rise, whether for food, fuel or basic household goods, the gap between income and expenditure increases. Every single purchase restricts cash flow and even essentials start getting out of reach. The result is a consumer that is severely cash constrained looking for credit to purchase.

In Arif Lakhani’s words, Pakistani consumers are so cash constrained that the majority of the population needs BNPL. Lakhani argues that if you look at the basic necessity purchases, a basic refrigerator costs around Rs80,000, a phone costs Rs40,000 and a motorbike can reach Rs140,000. “Who in Pakistan today has Rs250,000 in cash?” he asks.

Who does BNPL work for?

The average monthly income hovers a little above Rs80,000, but most of that is already spoken for. Rent, utilities, transport, and food consume the bulk of household earnings, leaving behind only a narrow margin of flexibility.

What BNPL does, in this context, is not introduce new purchasing power. It reshapes existing cash flow, turning a one-time expense into a recurring obligation that must now coexist with everything else.

For a middle-class consumer, that trade-off can make sense. Consider a salaried

Without auto-debit, there can’t be BNPL in Pakistan

Jordan Olivas, CEO of Qisst Pay

individual earning Rs80,000 a month. Their expenses are predictable, even if tight. When faced with a Rs60,000 purchase, a smartphone, a refrigerator, or a motorbike, paying upfront is difficult but not impossible over time.

Split across 12 months, the installment comes to roughly Rs5,000. It is a meaningful addition, but one that can be planned for. In this scenario, the consumer absorbs the cost gradually, often adjusting discretionary spending to make room for it. Repayment, while not effortless, is manageable within a relatively stable income stream.

The experience looks very different further down the income ladder. For a lower-income consumer earning closer to Rs30,000 to 40,000 a month, the margin for adjustment is far thinner. Here, most of the income is already committed to essentials, with little room to absorb new obligations. A similar installment of Rs3,000 to 5,000 does not just require adjustment, it requires trade-offs. It may mean cutting back on food expenses, delaying utility payments, or relying on informal borrowing to bridge gaps. In this case, BNPL is funding necessities without the adequate means to pay it back. The purchase may still be necessary. Say a phone for work or a fan in peak summer but the repayment journey is more sensitive to disruption. A delayed salary, an unexpected expense, or a minor shock can shift the balance.

What emerges from these two journeys is not a simple yes-or-no answer, but a layered reality. BNPL is clearly viable for only a segment of Pakistan’s population with stable enough incomes to accommodate structured repayments. At the same time, a large portion of the market interacts with credit under tighter conditions, where the same product serves a different purpose and carries a different level of risk. The distinction is not just about how much people earn, but how much flexibility they have once essential spending is accounted for.

This is what defines Pakistan’s BNPL landscape. It is not constrained by lack of demand, nor entirely limited by low income. It

is shaped by how little room there is between earning and spending. BNPL fits into that gap but the size of the gap varies widely.

Then there are digital platforms that have their own rules for handing out BNPL facilities. Their credit scoring mechanisms might not approve all those seeking this facility. To get an estimate, Arif disclosed that last year’s numbers of people who applied for a BNPL facility was 700,000 applicants against 200,000 who actually got the facility. Arif says this demand is massive and it is still only the tip of the iceberg because most of the BNPL is happening offline.

Part of the reason lies in how these systems operate. “Real consumer need is being fulfilled by these shops. They are not regulated they can apply pressure in ways an NBFC simply cannot,” he says. In other words, the informal system, for all its opacity, has built mechanisms of enforcement and flexibility that formal financial institutions cannot replicate. That does not make it more efficient but it does make it workable. If offline stores are able to pressurise someone to pay up using aggressive tactics, this makes the system sustainable. Money keeps coming back and the cycle can continue.

“85-90% of the Pakistani BNPL is happening offline. There are thousands of stores of various categories that each sell 1,000-1,500 units per month in each category. Collectively, the volume is much bigger than what an online BNPL player can sell in a month,” says Arif, arguing that AliBaba’s entry into Pakistan will increase online BNPL.

AliBaba enters Pakistan’s BNPL

When Alibaba Group launches Buy Now, Pay Later in Pakistan, it will likely do so where it already has distribution. That is on Daraz. The strategy is straightforward: embed BNPL directly into the checkout flow of the country’s largest eCommerce platform, allowing consumers to split payments at the point of purchase.

So far two models have emerged of BNPL in Pakistan. The first is the markup model, where the lender effectively sells the product at a higher price, embedding its margin into the installment plan. This is often structured in a Shariah-compliant way, where the cost is upfront rather than interest-based. The second is the merchant-funded model, where retailers absorb part of the cost in exchange for higher sales, treating BNPL as a marketing channel rather than a financing product.

Both models are already in use, and neither is without friction. In theory, merchant-funded BNPL suggests that consumers can access zero-cost installments. Where

“Who in Pakistan today has Rs250,000 in cash?”

Arif Lakhani, CEO of Qist Bazaar

Alibaba positions itself between these models remains unclear. But the choice will matter. It will determine not just how BNPL is priced, but how it is perceived and who ultimately bears the cost.

Beyond pricing lies a more structural constraint: collections. In mature markets, BNPL depends heavily on auto-debit systems. Payments are deducted seamlessly from cards or bank accounts, reducing friction and improving consistency. Pakistan does not yet operate at that level of penetration. A large segment of the population does not use credit cards, and even debit card usage is uneven. Cash still dominates. That creates a fundamental operational challenge.

As Jordan Olivas, CEO of Qisst Pay puts it, “Without auto-debit, there can’t be BNPL in Pakistan.”

The statement reflects a practical concern. Without automated repayment mechanisms, collections become more manual, more resource-intensive, and more dependent on customer behavior. This is precisely where informal systems retain an advantage - they embed repayment into relationships and proximity. Digital systems, by contrast, must recreate that discipline through infrastructure that is still evolving.

And yet, despite these constraints, the opportunity remains difficult to ignore, says Jordan Olivas, which has even prompted him to reconsider the Pakistani market despite earlier challenges with collections and bottleneck because of auto-debit requirements.

The need is massive which is currently being fulfilled by offline channels which is exactly why AliBaba’s entry is significant. AliBaba’s entry introduces a different kind of capacity particularly in terms of capital and distribution. If deployed at scale, that capital could accelerate adoption, expand access, and deepen awareness of BNPL as a category.

“They will be a great addition to Pakistan’s BNPL space,” Lakhani says. “More players will increase acceptance, increase understanding, and improve the culture.” n

The banking industry tried to turn a dying textile giant into its debt restructuring poster child.

Here’s what happened

Four years ago, a consortium of banks led by HBL came together to revive rather than rip apart a major textile manufacturing company that owed them money. The numbers say they made a mistake. What can they learn from it?

By Zain Naeem

The grand marquee erected at the Chenab Limited premises in Faisalabad on the 8th of November 2023 was meant to symbolise a revival. The event, given the title “Chenab Rising”, marked a major debt restructuring agreement that would get the wheels over at Chenab spinning again.

Chenab had once been a shining star too fast to catch. The company had glutted on the Blitzkrieg expansion offered by the low interest rates of the Musharraf era. They borrowed hard and expanded fast. But the timing proved to be wrong. When the dual energy and inflation crises hit the country in 2008, Chenab’s gigantic sandcastle came tumbling down. By 2011 creditors had filed suits to have the company wrapped up and reclaim their money. The factories came to a halt, the workers lost their jobs, clients looked elsewhere, and by 2017 the Lahore High Court ordered Mian Muhammad Latif to wind up the company he had built over three decades.

But Mian Latif was not ready to give up just then. He went back to the banks he owed money to and made the case that Chenab could come back from this. The courts might have called time-of-death, but Mian Latif wanted the banks to charge up the paddles and go full Victor-Frankenstein on Chenab.

The most important regard in which Mian Latif got lucky was that the bank he owed the most money to was Habib Bank Limited. HBL is Pakistan’s largest and oldest bank. In recent years, it has made a conscious effort to position itself as a natural leader of the commercial banking sector. Part of this has been a basic philosophy: what is good for Pakistan is good for

business, and what is good for business is good for the shareholders.

HBL became Chenab’s most unlikely champion. The bank brought Chenab’s other creditors together, and the different financial institutions formed a consortium that helped restructure Chenab’s vast debt. It was a simple enough concept. Either the banks could sell off Chenab’s assets and recover what they could of the money they were owed, or they could give them another chance to start manufacturing again and hopefully pay it back without having to sell anything.

That is why, perhaps, the Chenab Rising event we started with seemed more like a banking convention than a textile revival. Senior bankers, the deputy governor of the SBP, important clients, and the heads of various SAM departments of different banks were in attendance in addition to a small retinue of business journalists. Muhammad Aurangzeb, the now finance minister and then President of HBL, was front and center at the event. This would prove to be the last major initiative Aurangzeb would lead for HBL before being whisked away to Q Block. It was also clear that Chenab Rising was a message: this is how Pakistani banks should act. The overarching feeling was hope.

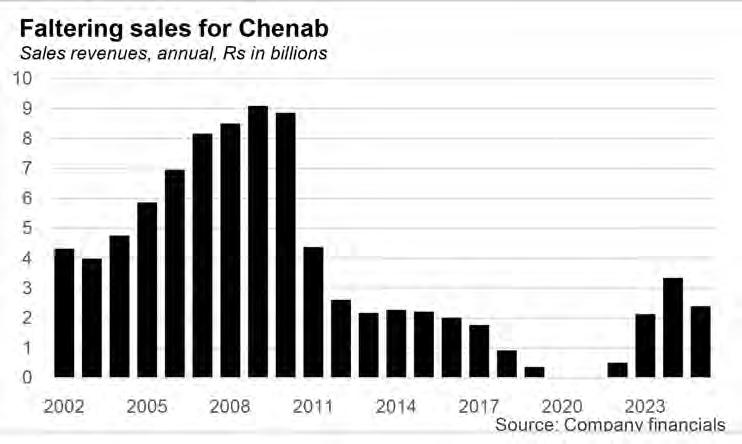

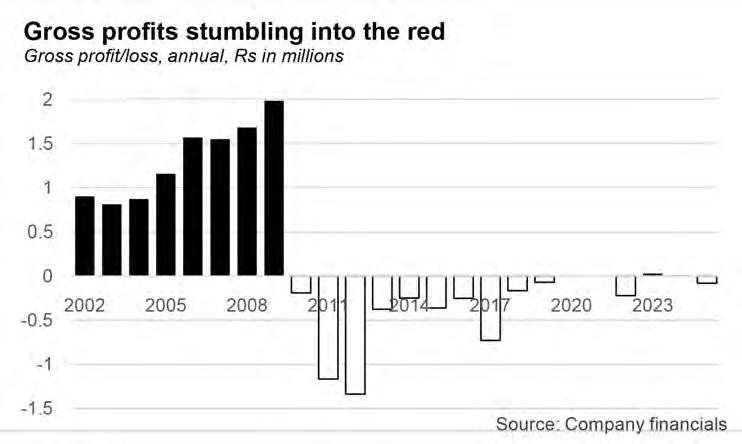

Two-and-a-half years later that hope seems to have been dashed. Muhammad Aurangzeb has gone to the finance ministry, interest rates have fallen, the textile industry has seen a modicum of recovery, but Chenab Limited is still struggling. Not only are they failing to pay back their debts under the restructuring agreement, the company is operating at a level where they are unable to even make a gross profit. That means their efficiencies are so bad that they are selling at a loss. For all intents and purposes it is a well that is draining money.

General Pervez Musharraf with his finance whizz Shaukat Aziz. The Musharraf administration saw a period of free flowing aid from the US, low interest rates, and a freshly privatised banking industry eager to lend to businesses. But when the freebies ended and the chickens came home to roost, Pakistan faced one of its worst economic crises.

And as Profit has seen over the course of this investigation, the end might be nigh for Chenab Limited. The consortium HBL had forged with other banks to renegotiate the loans is struck with internal strife. Some of the banks feel pulled along and think it is time to wind up sooner rather than later. At the same time, Chenab is continuing to make an effort to drag this along and somehow recover their losses and turn things around. In the process of it, they might end up cannibalizing themselves.

All of this raises the question: is Chenab better dead than alive? And perhaps more importantly, even though the restructuring of Chenab’s debt might not work, was it still worth it to try?

The tale of Icarus

There is such a thing as overexpansion. Chenab Limited is rooted in a solid business as old as time. Mian Muhammad Latif is the son of a leading cotton industrialist from Toba Tek Singh. But he had dreams beyond the family’s cotton farms. He looked towards developing industrial units, dreaming of not just selling cotton but turning it into thread, yarn, cloth, and other products he could then sell.

In the 1980s, Toba Tek Singh was replaced by Lyallpur, which was fast emerging as a center of Pakistan’s growing textile industry. The first brick was laid in 1980, and by 1985, the export business had started to take off and the company ended up exporting to 42 countries spanning Europe, USA and the Far East

This was a time when the textile business was simple in Pakistan. High quality cotton was grown all over the country. It was bought by ginners who gave it to mills that spun it into thread, then to units where it was woven into yarn, and eventually all kinds of stitching, printing, and dying was used to turn it into bedsheets, socks, apparel and other products. Electricity was cheap and came from Pakistan’s hydel power. Labour was also cheap, and the European and American markets were a wide open field. Pakistan was the leader in a pack of developing countries where textiles were the biggest source of export revenue. Vietnam, Bangladesh, and Egypt all trailed behind.

Chenab was among the many that grew and became exporters. They also tried to sell their products domestically under the ChenOne brand to quite some success. But still, Chenab remained a solid, dependable exporter. When things really began to kick off were the Musharraf era. Pakistan’s textiles were at their height. Banks had just been privatised and were eager to lend, and the interest rate was low. And with dollars flowing in from the

US, Pakistan was partying.

Chenab had a solid network of clients that had been built over the years. They got ready to ramp up orders, expand aggressively, and borrow to cover their costs. The idea was simple. Expand fast enough and revenues will start to flow in.

The evidence is clear in their earnings and borrowing. In June of 2001, the revenues of the company were Rs 3.4 billion which grew to Rs 8.2 billion by the end of 2007. This coincided with exports of $30 million worth on a monthly basis as well. Even though a blessing of the debt was the rise in revenues, the downside was how the liabilities started to grow as well. In 2001, long term debt was only Rs 70 crores which had surpassed Rs 3.3 billion by the end of 2007. The pace of growth did not stop as the company started to

establish large retail spaces like the ChenOne Tower in Multan and Sarghoda. And then came the crash.

The perfect storm

Around 2007, a perfect storm of external factors had been swirling overhead in Pakistan’s textile sector. India and China which had started to subsidize their textile exporters. No such schemes were being offered by the government of Pakistan and the competition was stiff. On top of this, the here-to-party attitude of the Musfarraf era was about to implode. The chickens were coming home to roost for Pakistan’s economy.

Interest rates started to increase to address inflation as handouts and aid from the

Pakistan’s textile industry has long relied on complete vertical integration: cotton is picked, ginned, spun, weaved, dyed, printed, stitched and so on. When an energy crisis hit the upstream industry in 2008, the whole thing started to implode. Textile competitiveness has never recovered since.

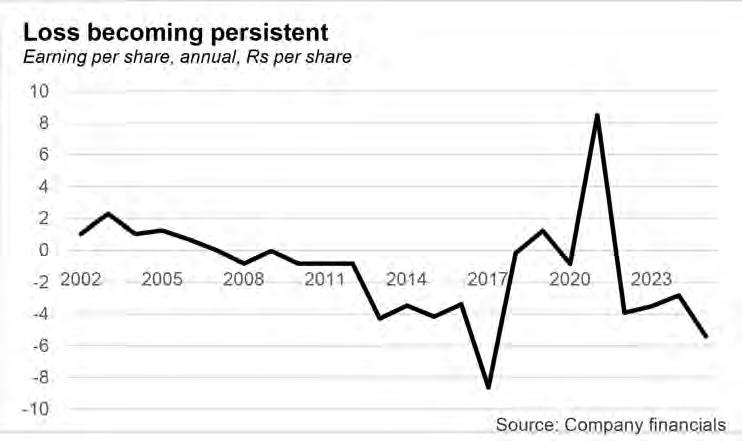

US for the war of terror started dwindling. Price increases meant higher energy and labour costs as the profitability started to shrink massively. The impact of this can be seen from the fact that in 2001, Chenab earned net profits of Rs 13 crores from revenues of Rs 3.32 billion while in 2007, the revenues increased to Rs 8.2 billion, net profits shrank to Rs 7.5 crores.

This was only the start of Chenab’s problems. 2008 saw the highest revenues being earned by the company surpassing the Rs. 8.5 billion mark, however, this was the first year the company ended up making a loss. The first reason for this was the increase in electricity and gas loadshedding which led to higher costs and production slowing down. The other reason was the assasination of Benazir Bhutto. This led to the country being virtually shut down and no railway or road infrastructure being ready to transport the goods that had to be exported.

The damage not just to Chenab but to the overall textile industry was massive. Energy is the largest input of the sector at the base level. Spinning and weaving require lots of electricity. Pakistan’s entire textile industry is vertically integrated. For the stitchers and dyers that require less energy to be efficient, the thread and cloth needs to be made cheaply. Add on top of that dwindling and diseased cotton and the crisis is a catastrophe.

Take this sobering statistic into account: In 2003, when Pakistan’s textile exports were $8.3 billion, Vietnam’s textile exports were $3.87 billion, Bangladesh’s were at $5.5 billion. Now Vietnam is at $46.68 billion and Bangladesh is at $47.96 billion, while Pakistan has failed to cross the $20 billion mark in the past five years.

There were, of course, certain players that emerged from this intact. Gul Ahmed, a comparable company to Chenab in some regards at that point, only saw two minor dips

in their overall revenue from 2007-2017. For the most part revenues increased, and exports remained the biggest portion of their earnings. In 2011, when Chenab faced its first winding up case, Gul Ahmed saw revenues of $311 million.

Historically, Gul Ahmed has been the company that chose the simpler product and made its money on the higher volumes. This, of course, is a strategy that has served the company quite well. Over the past 20 years – since 2005, when the textile barriers to trade completely fell away – the company has grown its export revenue from just $67 million in 2005 to $522 million in 2025, which represents an average growth rate of 10.8% per year in USD terms. But having achieved that scale, Gul Ahmed then tried to invest in expanding its small but significant apparel manufacturing business. And that appears to have been the move that has not quite worked out and is being reversed.

Chenab failed to find this kind of busi-

ness strategy. They had taken large loans in the Musharraf era to expand fast and those were now piling up. But beyond the burden of the loans, Chenab simply was not performing well on an operational level. As the clients started to leave, revenues started to fall. The situation reached an inflection point and in 2014 the company announced that they would not be able to meet their debt obligations. It was a situation very succinctly and somewhat emotionally (and rightly so) summed up by Mian Latif: ““the trust that was built with clients inch by inch went away in meters at a time.”

Chenab’s ability to conduct business was so flawed that it was actually better dead than alive. In 2020 and 2021, after the winding-up orders had halted production, Chenab’s factories fell silent. No production meant no sales. But it also meant no gross losses. That mattered because the years immediately before the shutdown — 2017, 2018 and 2019 — had produced a combined gross loss of nearly Rs 1 billion. The business, when it was running, was destroying value at the most basic level. When it stopped, that destruction stopped with it.

At the same time, Chenab began leaning more heavily on rental income from land it had classified as investment property. Rent rose from Rs 3.6 crores in 2018 to Rs 6.6 crores in 2020 and then Rs 8.7 crores in 2021. Alongside balances written back, other income came to Rs 6.8 crores in 2020 and then surged to Rs 1.2 billion in 2021. The result was startling. Earnings per share in 2021 came in at Rs 8.49. For a company that had spent years sinking, the numbers suggested an uncomfortable truth: Chenab looked healthier when its looms were still than when they were running.

Between 2010 and 2019, the company had already accumulated around Rs 5 billion in gross losses before finance costs, taxes, and other expenses were even counted. During

this time they were defaulting on their loan payments and still not making money. Chenab had not been crushed under the weight of debt. There was a fundamental flaw in their ability to produce competitive products outside of their debt liabilities.

But then the question arises, what do you do with a company like this? It has the infrastructure and history to keep running, and banks cannot simply keep selling off sick units. That is where the restructuring came in.

We care

The consortium of banks led by HBL had a simple message: we see and we care. The argument is a good one economically, and an honourable one in terms of business. Chenab was once a major exporter, and if it does well Pakistan’s economy does well. If the economy does well, banks will do well too. That is why they should be given a chance.

To reverse winding-up orders, the sponsors turned to a court-approved restructuring—filing a Scheme of Arrangement before the Lahore High Court that brought shareholders and creditors to the same table. At the heart of the plan was Rs 9.5 billion in debt, previously split across short- and long-term liabilities, now consolidated into a single longterm obligation. This liability was then divided into two equal tranches: Tier 1 and Tier 2, each amounting to Rs 4.7 billion. Tier 1 was to be repaid over 7.5 years with no grace period, while Tier 2 repayments would only begin after Tier 1 was cleared or its deadline reached—effectively pushing its burden into the future. Crucially, lenders agreed not to accrue interest on Tier 2 during this initial period, easing immediate

financial pressure.

The restructuring extended beyond debt engineering into asset sales and sponsor commitment. Non-core assets worth Rs 1.4 billion were earmarked for disposal, with 75% of proceeds directed toward creditor repayment and the remaining 25% recycled into working capital. Sponsors also committed to injecting fresh equity, including subordinated loans and the sale of personal shareholdings, with a one-year window to execute these disposals. Parallelly, lenders agreed to provide fresh liquidity to restart operations: Habib Bank Limited and Askari Bank extended Rs 100 million in working capital, while a new investor, Tauseef Enterprises (Private) Limited, brought in Rs 350 million under lien. Together, these measures aimed to revive production at a plant that had long stood idle, turning a legal rescue into an operational reset.

How has Chenab done since?

The immediate impact of the restructuring was that Chenab’s factory was up and running again. In 2024, revenues crossed Rs 3 billion for the first time since 2011, and around 3,000 workers were brought back, reconnecting thousands of households to an income stream that had disappeared with the shutdown of the plant. But that was the extent of the good news. When the restructuring deal was being negotiated, the first obstacle that Chenab was expected to get over was to be able to earn a gross profit. In simple terms, it was expected to produce the product at a price cheaper than what it was able to sell it for. The banks came

together with an understanding that once the operations were allowed to begin again with additional financing, the management would be able to generate enough revenues which would be able to show a slight operating profit. This would have been a sign that the company was on the right track. That test, at the very least, seems to have failed.

In 2025 the company posted a gross loss of Rs 8 crores. Their machinery had aged, the industry had moved ahead, and Chenab had taken a plunge in a business that has changed since the last time they were competitive. The most recent numbers suggest the slide is continuing. In the first quarter of 2026, revenue nearly halved to Rs 45 crores from Rs 92 crores a year earlier, while a gross profit of Rs 1.2 crores turned into a gross loss of Rs 3.4 crores.

For all intents and purposes, the restructuring had done the kindness of buying Chenab time to get its act in order. But when a company is making gross losses and already in debt and under a scheme of arrangement, money to start paying back debts needs to come from somewhere. Chenab was making its payments by borrowing from its directors.

On paper, long-term debt has come down from Rs 9.5 billion in 2021 to about Rs 7.4 - 7.5 billion by the end of 2025. That means roughly Rs 2 billion has been repaid in four years. While long-term debt has fallen, shortterm borrowings, which had been wiped out in 2021, stood at Rs 18 crores by 2025. Deferred interest has climbed to Rs 74 crores in just four years. Most striking of all, director loans have exploded from Rs 24 crores in 2021 to Rs 1 billion in 2025.

For Chenab’s creditors, this is a worrying situation. The former textile giant has failed to prove it has what it takes to make money, even with a very lenient debt restructuring arrangement. At the end of June 2017, the total assets of Chenab stood at around Rs 13 billion. If winding up proceedings had been carried out around this time, lenders would have been able to recover this amount in relation to their loans. By the end of June 2025, these assets are now worth Rs 10 billion which means that almost a third of the assets have fallen in value even after revaluation of assets and director’s loans are taken into account. The losses that are being suffered by the company are damaging its asset base and will further deteriorate the ability of lenders to get their money back.

The state of the debt

Let us recap where our story stands. Chenab borrowed and expanded heavily two decades ago. When an energy crisis hit the sector, Chenab lost customers, made losses, and was eventually buried under debt. When a court ordered winding up proceedings, Chenab wooed its

Mian Muhammad Latif and Muhammad Aurangzeb at the Chenab Rising event. The historic debt restructuring was the Pakistani banking industry’s effort to revive a dying textile giant and display the constructive role a mature industry can have on the economy.

creditors and got one last crack at making their business work and paying off its debts. That, unfortunately, has not worked out. Chenab failed to do good business, and are once again facing the music.

After years of losses, director support and deferred obligations, insiders say the company is close to breaching a key condition of its court-backed arrangement after missing the instalment due in December 2025, with the last payment having been made against the September 2025 amount. Under the scheme, such a default could revive interest relief that had earlier been waived and reopen the path to fresh winding-up action. And this time there will be no more delays in the court system. The scheme of arrangement that was used to bring about the debt restructuring makes sure of this.

But much like 2017, giving up does not seem to be an option, and Chenab has floated a new idea. An internal memorandum tied to the special asset review committee reviewed by Profit is considering a Rs 35.5 crore longterm finance facility. In it, Chenab asks the bank consortium led by HBL to allow the sale of a weaving unit in Shahkot, factory land and building in Jhumara Ghatti Chak 191 RB, Faisalabad, and land outside its Nishatabad factory. The logic is simple enough. If banks will not extend another roughly Rs 500 million in working capital, then asset sales can plug the gap, meet looming debt installments and prevent a formal breach. Chenab’s argument is that, if the assets would end up being sold in winding-up proceedings anyway, it is better to sell them now, inside the restructuring, rather than wait for collapse.

But that logic cuts both ways. For Chenab, selling land may provide cash, but land is also the cleanest recovery option for lenders in a default. It is the asset class creditors would want monetised if the rescue fails. Selling it now may postpone confrontation, but it also uses up part of the recovery pool before the final outcome is clear. Selling a unit is even more fraught. A spinning or weaving asset is not just another parcel on the balance sheet. It is part of the industrial chain that gives a textile company operational coherence. Once such a unit is sold, Chenab may lighten its debt burden, but it also weakens its own ability to function as an integrated manufacturer. The company is not merely shrinking. It is risking the erosion of the value chain on which any eventual turnaround depends.

That is why some lenders pushed back. The proposed assets are part of the security package behind the loans. If they are sold, the collateral cover declines. Email exchanges between the banks show disputes over legality, valuation and principle. Some lenders objected that the assets were being sold at around

71% of their forced sale value of Rs 1.2 billion, especially when earlier non-core disposals had fetched prices above forced sale benchmarks. HBL’s response was pragmatic: nearly half that forced sale value was tied to machinery that was 25 to 32 years old, and actual buyer interest was only in the Rs 70 crore to Rs 80 crore range. For the lead bank, imperfect value today appeared better than uncertain value later.

Banking on hope is worth it

So what happens now? As of now, 15 out of 21 institutions have consented to the new deal which means that 85.83% approval has been achieved, however, it is important to everyone on board otherwise this deal will not go through. The banks feel that the writing is on the wall already and that is why some banks had an issue as they felt that the assets worth Rs 1.3 billion are being sold for half the price and these assets were supposed to be the guarantee. They are seeing any signs of recovery depleting while the losses start to eat up more and more of the assets and the company.

Just consider what the schedule looks like for Chenab. At the end of December 2025, they were required to make a payment of Rs 76 crores which would have seen them cover the payments till June of 2026. The company has committed that if the assets are allowed to be sold, the buyer was willing to pay Rs 70 to 80 crores which would have allowed them to see the payments off till June 2026 safely. After that, the next course of action would be decided on which would probably be another round of assets being sold off. Considering that April has almost ended, this new deal would not account as any relief as this will start a

new phase of what to sell next and who to sell it to to cover the period after June 2026.

The new deal gives Chenab more time, but not a whole lot of it. Up until now the textile has seemed incapable of turning things around. Short of a miracle, it seems Chenab will inevitably collapse again and be sold for whatever is left of it.

But then why did the banks do this? Why did HBL lead this consortium, and why are they giving it one more shot by allowing Chenab to sell its assets to pay back some of the debts?

It is easy, in hindsight, to say the plan was a bad idea. One might scoff at it and call the plan naive. But think of it this way: a number of Pakistani banks came together and instead of ripping apart a company that owed them money, they decided to show patience and give it another shot. It might not have worked out, but the decision to do so was a mature one. While there are clearly lessons to be learned from Chenab (the company did not respond to Profit’s request for comment) one hopes this debacle will not deter the spirit behind the decision. After all, if banks take the easy route of selling off every sick unit they find, it will be bad for the economy, bad for the country, and in the long run bad for the banks.

The logic behind the decision was explained by Muhammad Aurangzeb at the event. “The revival of Chenab stems from the Bank’s strategy of ‘Growing Pakistan’s Economy’, a pillar of which is corporate restructuring. Through these capacity-building efforts, the Bank continues to deliver against its sustainable banking practices in the process of becoming ‘More Than Just a Bank’.”

After all, “Chenab Rising” might have been an experiment, but even more than that it was probably a hope and a prayer. n

Is Pakistan’s “freelancer revolution” a lie built on tax evasion?

Reports from within the IT industry indicate that there’s a widespread misreporting of employees as ‘freelancers’ to make use of the reduced tax rates for IT exports, and that this practice might be inflating the government’s figures

By Usama Liaqat

To hear the federal government speak of it, freelancers are powering the country. There is a youth in every basement, every coworking space, every cafe, under every streetlight and in every nook and cranny of the country sitting behind a laptop tip tap tapping away at the keys for some client thousands of miles away that will pay this youth in dollars.

That, at least, is the picture painted by the government’s official numbers on freelancers. Pakistan’s total IT related exports stand at $3.8 billion for 2025. While this number in and of itself is disputed by the industry, according to government claims nearly $779 million of this was brought in by IT freelancers. That would mean freelancers account for more than 20% of Pakistan’s total IT exports. That, dear reader, is an astronomical figure. Not only this but freelancing is also apparently on the rise. The $779 million marks an astonishing 90.6% increase compared to $408 million in 2024. And what’s more, the revenue achieved from freelancing services in the first 8 months of the current fiscal year has already reached USD 743 million, just slightly below the figure for the whole of the previous fiscal year. The figures are remarkable.

How has this been achieved? Snippets of news approved by the information ministry and broadcast on Radio Pakistan will tell you this is the result of “improved facilitation, targeted training programs, and a supportive ecosystem have contributed to the rapid growth of the freelancing economy in the country.”

Essentially the government wants you to think that freelancers were told to “keep it up and do a good job” and they responded by doubling their revenue within a year.

One can either choose to believe that explanation or take a peak under the hood. Based on a series of interviews conducted with executives and employees of different IT companies alike, the freelancer label is being used by salaried individuals in the IT industry who are definitely not freelancers. While there is no exact figure on how many such freelancers are around, Profit has been told by multiple sources that the practice is widespread in the industry.

How does it work? The details are in a tax break. The government allows only 1 percent of tax on IT exports, a rate which whittles down to 0.25 percent if you are registered with the Pakistan Software Export Board. This incentive has led people who are not really freelancers to pose as freelancers in order to take home a higher chunk of their salary. Essentially, it is a roundabout case of tax evasion.

How does this work? What certain IT

companies do is hire some of their ‘employees’ on contracts as freelancers. These companies usually have offices abroad. And they route the salary of these ‘employees’ through this foreign-registered company as remittance, so that neither the ‘employee’ nor the company has to pay as much tax to the government as they would have if the ‘employee’ in question were to be on the Pakistani payroll. There are variations in this method, of course, and even the number of employees on such ‘freelancer’ contracts varies by the company. In Profit’s conversations with multiple employees of various IT companies, it transpired that such contracts often are for people whose salaries are high enough for income taxes to really hurt.

While we do not have exact numbers indicating the extent to which these practices are inflating the government’s numbers, the fact remains that such inflation exists. And given that such, let’s call it misuse, of the ‘freelancer’ category is often done for higher volumes of export revenues, the impact of this misuse becomes accentuated. There is little oversight from the government’s side and the category of ‘freelancer’ remains porous, giving credence to the claim that there is something really iffy with the government’s numbers, which it uses to brand its achievements in the face of reality. And, then there is the matter of the loss of crucial tax revenues, which not only make things worse for the government, but

also for other people.

The government might be flaunting its laurels, but those laurels are essentially bought from what’s taken from the government’s own pockets. And the government seems either clueless, or a willing dupe in this business.

The government’s claims

If the government numbers seem too good to be true, they kind of are. It is a bit unlikely that the freelancing exports almost doubled in one year, while nothing really remarkable happened in the industry. In fact, the industry insiders Profit talked to said that there was a heavy downward pressure on our IT exports, with AI effectively decimating lower-value work – which most freelancers deal in – from the market. And all of us heard stories of freelancers claiming to lose work because of poor internet infrastructure here.

These figures are supplemented by the statements about the number of freelancers. In 2024, for instance, in an interview with Dawn’s Aurora, Tufail Ahmed Khan, President and CEO, Pakistan Freelancers Association (PAFLA) stated that there were 2.73 million freelancers in Pakistan. A report by Arab News in 2025 reported that the figure was 2.3 million, while in the same year, Ibrahim Amin, the Chairman and Co-Founder of the PAFLA stated in an interview with Business Record, that the number was over 2.7 million.

The point is that there is no real substantial data on how many freelancers there actually are in Pakistan, though everyone seems to agree – reasonably, given our population size – that the number is high and between 2 to 3 million. But we have not seen any corresponding growth – or at least reported growth – in the number of freelancers over the past year, when the revenues are claimed to have grown by over 90 percent.

In any case, the government shares the

freelancers’ contributions numbers as evidence of the success of its own policies. One such policy – broadly instituted as an export incentive for the IT industry – is the reduced tax on IT exports. Effectively the final tax regime on IT exports is 1 percent, which is further reduced to 0.25 percent if the exporting organisation is registered with the Pakistan Software Export Board (PSEB). Now, this was intended as a measure to incentivise IT specialists in Pakistan to increase their exports: they would have to pay much less tax than the normal salaried class taxes on whose income could reach as high as 35 percent of their salary.

However, this incentive has spawned unintended consequences. Given that the tax rate differential is so high – one person who would have to pay a third of their income in taxes would only have to pay 1 percent if this was (shown as) IT exports – one could imagine how this policy could have incentivised another kind of behaviour.

The freelancing wizardry

This is the incentive to portray oneself as a freelancer to simply pay lower taxes. And apparently, this is a practice not too uncommon.

Here’s how it works. Let’s say there is an IT company called ABC Inc., and they cater to foreign clients. Let’s also assume that this company is not a member of the PSEB. Being an IT exporter, they would only have to pay 1 percent of their export proceeds. But they also have employees here in Pakistan, and given the rules in Pakistan, the employer has to deduct taxes from their employees’ salaries. The employees’ salaries, however, would not be subject to the 1 percent rate. Rather, these would be taxed as normal salaries are in Pakistan, according to the employees’ respective tax slabs. So, ABC Inc. and the employee would still have to pay taxes – ranging from 5 to 35 percent – on the

latter’s salaries.

The loophole, however, was there to be exploited.

Profit talked to several members from the support departments from different IT companies. These employees laid bare the ploys certain IT companies use to play the system.

One of these employees, on condition of confidentiality, explained a commonly used workaround. “Let’s say I want to join a company and state my salary expectations as PKR 350,000. The company says, ‘yes, we can give you that money, but in that case your take-home amount after tax deductions would be around PKR 295,000. That money won’t go into either your pocket or ours. So, let’s meet on a middle ground. Let’s decrease your salary to PKR 320,000 and route this payment as a freelancer’s remittance through our associated company from abroad. You will get almost all of this revised salary. We won’t have to pay 30,000 in taxes, and nor would you. It is a winwin situation.’”

Let us see what has happened in this situation. The potential tax revenue for the government decreased from PKR 55,000 to 3,200. And we have a new freelancer on the books.

There are other workarounds too. Sometimes companies create two contracts for their employees: one with their entity in Pakistan, and the other with an associated entity abroad. Let’s understand this method by an example too. Ahmed is working in an IT company. It is immaterial whether he is working as an IT professional, or in one of the support functions (HR, Legal, Marketing, Operations, etc.). His salary is PKR 350,000, but the high amount of taxes he pays have been giving Ahmed turbulent dreams and sleepless nights. His employer could really do without the sleep-deprived Ahmed entering the office in the morning, drowsy and with unkempt hair, barely keeping up with the meetings. Ahmed musters the courage and goes to the management and says that he needs a raise.

The company, fortunately, has another office in Dubai. And they offer Ahmed the following: “We will keep you as an employee with our Pakistan office, but we will decrease your salary to PKR 100,000. In the meantime, we will create a freelancer contract for you with our Dubai entity. The rest of your salary (PKR 250,000) would be routed through that company at 1 percent tax rate. Your effective salary would increase, and we won’t have to pay a dime more from our pockets!” Ahmed is jubilant, and signs both the contracts.

In this case, again the ideal amount owed in taxes would be around PKR 55,000. But due to this wizardry, Ahmed would have to pay the normal tax rate on PKR 100,000, which would amount to a grand total of 500 rupees. On the

Who is actually a freelancer? In the rest of the world, a freelancer is someone who doesn’t make more than 50 percent of their income from any single source. In our country, however, everyone is a ‘freelancer’. Some companies don’t even bother registering and continue to function as a consortium of ‘freelancers’ by claiming to be functioning as mere co-working spaces

Syed Ahmed, CEO of DPL and an ex-Chairman of P@SHA

remaining 250,000, which he will receive from abroad as a ‘freelancer,’ he would have to pay 1 percent, i.e., PKR 2,500. So, effectively, he (and the employer) only has to pay PKR 3,000 to the government instead of PKR 55,000. And here, there is a different, more exotic kind of magic. There was one person earlier, but now there are two: an employee of the local company, and a ‘freelancer’ for the foreign office.

This practice is more prevalent than you would think. The number of ‘freelancers’ created through this sleight of hand might not be as high, but the fact is that such offers are often reserved for those who are earning salaries high enough to really feel the brunt of the government’s tax pestle. These might sometimes even be hired as ‘consultants’. Although the number of such employees varies by the company, since such offers are often reserved for the high and highest earners, the impact on freelancers’ export revenue numbers becomes much more pronounced. This is especially the case since we haven’t really seen any significant change reported in either the number of freelancers or the volume of work coming in.

In fact, in Profit’s discussions with several IT executives, the general sentiment has been that the work has actually slowed down, and the rapid advances in AI are effectively obliterating the kind of work most IT freelancers engage in. In such a state, it is doubtful that our freelancing exports are increasing at such high rates. Instead, reports from on the ground point to the misuse of the tax breaks incentives by people who aren’t really freelancers, but are using this loophole to keep more of their income than they would have if they had paid their taxes like any other salaried person in the country.

The nature of the fault

The local IT companies, it seems reasonable to argue, are at fault if they engage in such practices. Creating an army of paper ‘freelancers’ they are

able to – at the end of the day – evade taxes. This robs the government of valuable tax revenues. In addition to this, such practices always have the unfortunate effect of passing this tax burden on to others. The government has to collect the amount anyway and meet its revenue targets; it simply just taxes everyone to make up the deficit.

Then there is the question of fairness. Here the fact that the ‘freelancing’ wizardry we saw above is often sometimes to star employees who might not even be engaged in IT-related tasks. They could be from the HR, or legal, or the marketing department. Why are, for instance, marketers in IT companies allowed to pay less in taxes than marketers in, say, fertilizer companies? Or at least why do the former have this option available to them, when the latter don’t?

There is also the point that such practices skew what is actually happening in the industry, and provide a false impression of growth where there is much less of it, if we are being charitable. This has the consequence not only of concealing a possible rot, but also of actively making things worse. Talking to Profit, Syed Ahmed, CEO of DPL and an ex-Chairman of P@SHA, stated that this is making things worse for the multinational companies in Pakistan. They cannot match the ‘freelancer’ salaries, since they have their own procedures and try to keep their books ‘clean’. The result is that they become much less competitive in the local job market. Moreover, such nominal growth, also takes a burden off the shoulders of the government. If they see, for instance, that the export revenue generated by IT freelancers has increased by over 90 percent, the incentive to take tangible measures to increase the actual ‘freelancing’ revenue gets lost in the clicks and the fanfare surrounding these numbers.

But there is a broader responsibility too, one that lies with the government. One is the question of the data. People are taking advantage of this facility simply put because

there is no real oversight by the government. The category of the freelancer hasn’t been defined. According to Syed Ahmed, this is a much-needed step. “Who is actually a freelancer? In the rest of the world, a freelancer is someone who doesn’t make more than 50 percent of their income from any single source. In our country, however, everyone is a ‘freelancer’. Some companies don’t even bother registering and continue to function as a consortium of ‘freelancers’ by claiming to be functioning as mere co-working spaces.”

The real problem, however, with this tendency to take advantage of the lower tax rates on income generated from IT exports is the fact that so many feel that there is a need to take such advantage. There is not even a debate about it: the salaried class in Pakistan is being ground under ever-rising taxes, while massive segments of our economy remain undocumented and barely pay their fair share. And the government, as has been the long-standing charge, taxes those in its net deeper rather than taking meaningful steps to make the net wider.

Following the law also has to be easy, at least reasonably anyway. Of course, there might always be some people who would try to take advantage of such schemes, but should the taxation issue be resolved (one can dream) and oversight over the freelancer category enhanced, such cases could be expected to dwindle.

In the current situation, however, such tax incentives are likely bloating the contributions of freelancers to our export earnings, and rather than looking deeper into this malaise – which is actually hurting the government by robbing it of tax revenues – it seems to be the most enthusiastic cheerleader of its own robbing. No one is saying that freelancers don’t need to be promoted, and export incentives shouldn’t be granted. But then you also should be careful of advertising what might not actually be as unadulterated a good as you might seem to think. n

Chishty finally gets the keys to K-Electric

More than two-and-a-half years after AsiaPak Investments bought out what was formerly Abraaj’s stake in K-Electric, Shaheryar Chishty has been appointed as Chairman of the Board for the utilities company

By Abdullah Niazi

Almost four years after he first bought K-Electric, Shaheryar Chishty has been appointed chairman of K-Electric’s board of directors. The announcement was made in a disclosure to the Pakistan Stock Exchange (PSX) on the 15th of April.

His election as chairman comes after a protracted legal battle that ranged from the Cayman Islands and the UK Judicial Committee of the Privy Council all the way to the Sindh High Court, pitting investors from Saudi Arabia and Kuwait against Mr Chishty’s company, AsiaPak Investments.

The appointment comes at a time when KE’s management has been in shambles. The company’s CEO since 2018, Moonis Alvi, resigned in February this year after getting a clean chit from then-Sindh Governor Kamran Tessori in a workplace harassment case. He was replaced by interim head Adeeb Ahmad. On the 24th of March, the company announced Syed Taha, an engineer with an MBA who was formerly CEO of Pakistan State Oil (PSO), would be the next CEO. His appointment was to come into effect on the 15th of April, the same day Chishty’s elevation as Chairman was announced to the PSX.

Who is Shaheryar Chishty?

Acareer banker, Chishty grew up in Karachi where he attended KGS before studying economics at Ohio Wesleyan University. His father was a naval officer and retired as an admiral. He joined Citibank in Karachi and spent a lot of time with the bank in Hong Kong, where he moved in 1997. His specialisation during this time was mergers and acquisitions.

He first came to prominence as a businessman in his own right in 2011, when he moved back to Pakistan after buying the

Daewoo bus service from Korean investors. In his own words, this was the beginning of his vision to pick up “orphan assets” and turn them around. But Daewoo was only the beginning. In 2012 he formed AsiaPak Investments. The company owns Daewoo but two of its other key investments are Thar Coal Block 1 (a CPEC “early harvest” project consisting of 7.8 mln tons per annum coal mine and 1,320 MW mine mouth IPP) and Liberty Power Limited (a 235 MW gas fired IPP).

Chishty’s involvement in Thar Coal has long made him interested in the potential of acquiring K-Electric. Founded in 1913, KE is Pakistan’s only vertically integrated utility company. It was privatised in 1952 and was passed around different ministries and government departments (including WAPDA) until 2005 when the Musharraf Administration decided to privatize it. In the two decades since its ownership has been subject to both change and controversy.

The government sold off 66.4% of KE to a consortium of the Al-Jomaih Holding Company, a diversified Saudi Conglomerate, and the National Industries Group, a publicly listed Kuwaiti financial conglomerate (which also owns a large stake in Meezan Bank). For three years, the Saudi-Kuwaiti conglomerate

failed to make any headway in turning around the company, finally turning in 2008 to Arif Naqvi, the former Karachiite who had gone on to create Abraaj Capital in Dubai.

Abraaj bought out half of the Jomaih-NIG stake in KESC, injecting $391 million into the company. It then began a turnaround effort the likes of which have never been seen in Pakistan before. Abraaj spared no expense in trying to turn around KESC, investing upwards of $1 billion in the company’s power generation and transmission infrastructure, which brought the utility’s power generation efficiency rate from 30% in 2008 to 37% in 2016, and its transmission losses from 4% to 1.4% in the same period.

It was a remarkable turnaround. In 2016 they were ready to sell. That was the first time Chishty showed an interest in acquiring the asset, but KE was eventually sold to China’s state-owned Shanghai Electric for $1.77 billion.

But then came the roadblocks. To cut a very long story short, consistent delays on the part of the government meant the Shanghai deal could not go through. What should have taken a year or two at most was dragged on for three years. Despite no lack of political lobbying on the part of Abraaj’s Arif Naqvi, the deal was dead in its tracks. And then came the crash. In 2019, Arif Naqvi and Abraaj were involved in an international scandal that ended with the company utterly bankrupt. If the deal had gone through, it is possible Arif Naqvi would have been able to stave off his debts for some time longer, but the deal’s paralysis made this impossible. Eventually Abraaj, and along with it the Shanghai Electric deal, went kaput. Abraaj’s assets, including KE, were set for liquidation. And this is where Shaheryar Chishty stepped in.

Why buy K-Electric?

This is where the story gets a little complicated, and also moves away from Karachi’s shores. When the government had first privatised KE in 2005, its buyers, the Al Jomaih Group, created a

company called the KES Power Limited (KESP) in the Cayman Islands. This company paid the government of Pakistan directly and acquired a 66.4% stake in K-Electric in Pakistan. The government of Pakistan controls 24.36% shares in KE, while the rest is owned by institutional investors and the general public.

In 2009 when Al Jomaih decided to sell, Abraaj funneled over $370 million in foreign direct investment into KE through the KESP company in Cayman. Abraaj’s investment in KE was undertaken through the Infrastructure & Growth Capital Fund L.P. (“IGCF”), a $2 billion Cayman Islands private equity fund with investment contributed by over 100 different international investors, managed then by Abraaj Investment Management.

When the IGFC fund was created, it only bought 53.8% shares in the holding company called KESP with the rest of the amount remaining with investors from Al Jomaih. To clarify, 66.4% of K-Electric was owned by a holding company in the Cayman Islands called KESP. When Abraaj entered the picture in 2009, they purchased 53.8% of that holding company. This means that even though Abraaj did not have the majority shares in K-Electric (their total ownership comes out to around 35%) they did control the majority of the holding company that controls them, giving them management control and rights over KE.

When Abraaj went bankrupt, their share in KESP was up for liquidation. This is when Sheheryar Chishty enters the picture. In 2022, through a special purpose company called Sage Ventures registered in the British Virgin Islands, his company called AsiaPak Investments acquired Abraaj’s former stake in the holding company called KESP, becoming the ultimate beneficial owners of KE.

Legal troubles

Despite what was a clear-cut sale, management control of KE was not transferred. What followed instead was a series of complicated legal cases. Chishty became a partner in Sage Venture Group Ltd – a BVI special-purpose company of AsiaPak Investments – became a general partner of IGCF. The subsequent sale of Abraaj’s stake in KESP, the Cayman based holding company originally founded by Al Jomaih, was sanctioned by a Cayman Island court.

While the sale was cleared in the Cayman where it was entirely based, the minority shareholders of KES Power went to the Sindh High Court and obtained a stay order that prevented changes to K-Electric’s board –blocking proposed new directors and leaving vacancies unfilled.

The market consequence of that stay was outsized. A listed utility can muddle through a lot – tariff disputes, fuel price shocks, political

heat – so long as its governance mechanism keeps turning. But when the board cannot be reconstituted, everything else starts to jam: approvals slow down, strategic decisions become harder to defend, and every rumour about “who really runs the place” becomes a risk premium in the share price.

The conflict then centred on board appointments and control rights. It essentially became a high-stakes contest between Gulf investors and Chishty’s camp. Caught in the middle of all this was Shanghai Electric. The company had continued interest in acquiring KE but their patience was wearing thin. The board battle risked derailing a multi-billion-dollar reform and investment programme for Karachi’s electricity infrastructure.

Then came the fatal blow. Shanghai Electric announced it was withdrawing from the deal in September 2025. They had finally pulled the plug.

For more than three years, deceptively narrow court order has functioned like a padlock on K-Electric’s corporate governance: no meaningful changes to the board, no clean resolution to shareholder wrangling, and –crucially – no straightforward path for fresh capital or a credible change-of-control story to take shape.

That padlock was finally opened in January 2026. KE announced in a notice to the PSX that it had been discharged from Civil Suit No. 1566 of 2025 – formerly Suit No. 1731 of 2022 in the Sindh High Court – after the plaintiffs, Al Jomaih Power and Denham Investment, withdrew their claims against K-Electric and three related defendants.

The plaintiffs’ own paperwork makes clear why the retreat happened now. Their withdrawal application cites a July 20, 2023 judgment of the Grand Court of the Cayman Islands granting an anti-suit injunction and directing them to withdraw the Pakistan proceedings against these defendants, and notes that subsequent appeals – including an attempt to go up to the UK Judicial Committee of the Privy Council – had been dismissed.

With no other route out, the case had to be withdrawn. This ended the board paralysis that KE had been under, and finally allowed for new directors to enter the scene. It has been this that finally culminated in the election of Shaheryar Chishty as Chairman of the board for K-Electric.

What will the new management do with KE?

K-Electric is a far cry from the hot product it was in 2016 when Shanghai Electric first wanted to pay $1.77 billion to buy it. Nearly

a decade of neglect has made this a company that needs a lot of attention.

In fiscal year ending June 30, 2024, the latest full year for which data is available, K-Electric’s bill recovery rate – the total amount of bill payments collected as a percentage of the total amount of bills issued – was about 91.5% across all of its customers, according to data from the National Electric Power Regulatory Authority (NEPRA).

That number sounds impressive, and indeed represents a sharp increase in bill recovery rate relative to where the company was privatized in 2005, but is down from the 96.7% it had achieved just two years prior, in fiscal year 2022. And when one looks at the source of this decline, it is driven in very large part due to a decrease in collections from household consumers, which has seen a relatively sharp deterioration in the past four years, going from 92.2% collection in 2020 to just 82% in 2024.

This is bad, to say the least, and so bad, in fact, that K-Electric has gone from having a bill recovery rate about 700 basis points above the state-owned electricity companies’ average (which basically means all other companies in the country since K-Electric is the only privately-owned electric utility) in 2021 to now being 1,000 basis points below the state-owned companies. It is a 10% drop in just three years.

And it does not seem to be improving either. In the first half of the fiscal year ending June 30, 2025, K-Electric’s bill recovery rate dropped even further, with a household consumer bill recovery rate now at 78.4%, a sharp decline in just six months.

This publication has done an in-depth analysis of the problems plaguing KE back in June last year.

To put a long story short, KE has been suffering from a serious problem of not having adapted to the solar revolution. Its best customers, the ones that would always pay their bills, are rapidly shifting away from the grid and moving towards solar energy. On top of this, a bruising fight over ownership has left the company with no clear leadership that has a mandate to turn things around.

There is a lot that can be done at KE. There is also proof of precedent that turning this company around is not impossible –what Abraaj did between 2009 to 2016 was as difficult if not more so than the current situation. With the corporate governance issues fixed, the new management might look to bring in new ideas to old problems. Mr Chishty has long expressed his desire to use AsiaPak’s interest in Thar Coal to develop synergies that provide cheap and effective energy to Karachi’s citizens. n