11 Big Bird Foods is writing the script of a comeback story. How did they do it at a time everyone expected them to falter?

16 Tabba’s expanding empire

22 Policy paralysis on petrol will only increase the trust deficit

24 Pakistan can’t import cheaper Iranian oil because of sanctions. Is there a case to be made to do it anyways?

26 The value of the Iranian Rial is rising dramatically in Pakistan’s currency markets. What is behind the increase?

28 Solar equipment is getting more expensive despite a foreseen drop in demand, why?

32 The mobile app petrol subsidy for bikes is not going to work. There are other solutions

Publishing Editor: Babar Nizami - Senior Editor: Abdullah Niazi

Business Reporters: Taimoor Hassan | Usama Liaqat | Zain Naeem | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editors: Saddam Hussain | Abdul Hameed - Video Producer: Adnan Maqsood Director Marketing: Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

How did they do it at a time everyone expected them to falter?

At the tailend of 2023, some of Big Bird’s biggest clients like McDonald’s and KFC were hit by a drastic fall in demand. Despite the fluctuations, they managed to turn around a ship in trouble

By Zain Naeem

“According to all known laws of aviation, there is no way that a bee should be able to fly. Its wings are too small to get its fat little body off the ground. The bee, of course, flies anyway. Because bees don’t care what humans think is impossible.”

Bee Movie

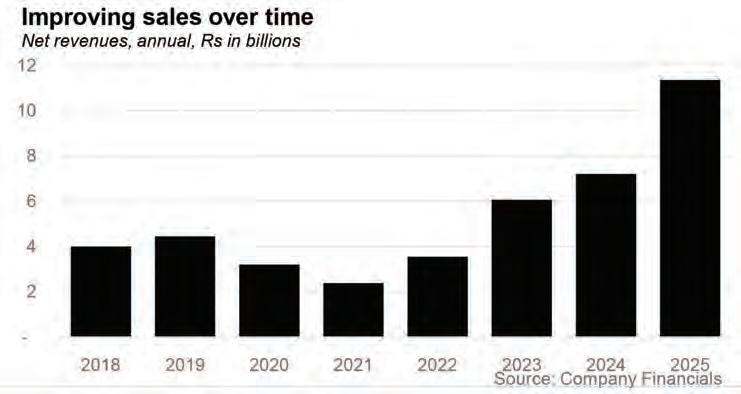

Big Bird Foods is about to take flight. Just take a look at what the frozen food company has achieved in the last couple of years. In 2025 their sales increased by 57.6% to Rs 11.36 billion, up from Rs 7.21

billion the previous year. They have also posted a net profit two years running, earning Rs 1.16 billion last year and Rs 83.8 crores in 2024. They are also well on their way to posting a profit for the ongoing financial year. At the halfway mark for FY25-26 they are sitting on a net profit of Rs 64.8 crores.

For a company that posted net losses five years running from 2018 onwards, this is not simply a couple of good years. It is a significant reversal.

What makes the story even more compelling is the fact that it has happened during a period when they were expected to see business slowdown. Some of Big Bird’s biggest clients

include McDonald’s and KFC, both brands that were heavily impacted in Pakistan by anti-Israel boycotts following the genocide in Gaza.

As Profit has reported in the past, sales at McDonald’s and some other international franchises initially fell by as much as 40% after October 2023. Big Bird confirmed to Profit that the dramatic fall in sales impacted them. They faced demand fluctuations. While this was a blow for the company, it came at a time when they were already in the middle of diversifying their business. A shift towards a larger retail presence was underway. Not only were they focusing more on selling their products to retail customers, but they also expanded their

roster of B2B clients by selling to domestic food chains like Johnny & Jugnu in Lahore.

The strategy behind this shift has been simple. They have diversified their client list by expanding rapidly, which they have managed to achieve by reducing prices to gain a share of the market. At the same time they have focused significantly on reducing costs, and the company points towards their recent investment in a three mega-watt (3MW) captive solar plant which went live in June last year.

All of this comes at a time when Pakistan’s frozen food market is growing. Rising urbanisation and larger disposable incomes always combine to give people a preference for convenience. With an expected annual growth rate of 5% market dynamics suggest this will be a $1.3 billion business by 2032. In the years ahead it will be critical to see who emerges as the Big Kahuna of frozen food in Pakistan. Its recent moves have made it clear that Big Bird sees itself as a top player and wants a big slice of a pie that is still in the oven.

To most people, the rise of Big Bird in the frozen foods industry might seem like the entry of a relatively new player. The reality is that Big Bird Foods is actually coming into its own. The Big Bird Group has been around since 1985. With six companies, more than 3000 employees, and more than Rs 12 billion in turnover the Big Bird Group is a major poultry player in Pakistan. Big Bird Foods, the frozen and chilled chicken business, was only introduced in 2011. But it is the logical end point of a group that has valued integration for more than four decades. The only question is, can Big Bird stick the landing?

The Big Bird Group came into being through three men. On their official websites, the Group has rather cheekily said the business venture was “hatched” by Abdul Basit, Dr Mustafa Kamal, and Dr Abdul Kareem, with the latter two being veterinarians.

Initial operations began with a relatively

small hatchery, but the goal was big from the get go. The poultry business is not a simple matter of hatching eggs and raising chickens. Over time it has become a complex system that has allowed chicken to become the go-to protein all over the world. It is cheap and readily available for a reason.

Hatcheries like the one set up by the Big Bird Group in 1985 are basically facilities where eggs are incubated under controlled temperature, humidity, and ventilation so they hatch into chicks. Hatcheries do not usually “grow” chickens for long periods. They mainly receive eggs, incubate them, hatch them, sort chicks, vaccinate them if needed, and then send them out. The hatchery is simply one step in the overall poultry supply chain.

In 1989, the group set up a company by the name of Grand Parent Poultry. This was the first sign that Big Bird was looking to eventually expand and become a fully integrated poultry machine that lived and breathed chicken.

Think of the poultry industry like a pyramid. At top are grandparent operations. These farms keep very high-value breeding birds called grandparent stock. These birds are not raised to be sold and slaughtered. Their job is to produce the next generation of breeding birds by concentrating and ensuring birds that are genetically strong. Those next-generation birds are called parent stock. Parent stock comes from grandparent stock. These birds are raised on breeder farms. Their role is to lay fertilized eggs that will eventually become commercial chicks.

Those fertilized eggs are sent to hatcheries and are what are known as broilers. The hatcheries, as mentioned before, simply raise the eggs. Once those eggs are hatched and the chicks are a little bigger, they are sent to broiler farms where they are grown fast so they can go to market.

In this way, by 1990, the Big Bird Group was getting its hands in every part of the poultry business. They were breeding high quality birds, managing grandparent stock, hatching the eggs, and raising broilers. That is where the

next phase of the business came in. From the very beginning, the group felt they did not have the right kind of feed to grow their business, and that is when they set up Big Feed.

Eventually, the Big Bird Group set up a company by the name of Green Nature Farms in 2005. This was essentially a farming operation that grew grain which would feed their grain company. Big Bird was farming food, using it to make feed for chickens, raising high quality chickens, collecting their eggs and hatching them, and eventually raising those hatchlings into birds ready for the market.

According to the group’s own estimate, they currently cater to around 60% of the total demand in Pakistan for broilers. There was only one thing missing in this entire end-toend business: a processing unit for fresh and frozen chicken.

Frozen foods, particularly chicken products, had been flowing into Pakistan since the turn of the century. It was the natural progression of things. Women were entering the workforce and the idea of products like sausages and breakfast meats being easy, accessible, and quick to make was gaining traction, albeit largely through imports.

Imports tested the initial feasibility of such products. But eventually they have to be produced domestically. This is where there was a point of divergence. The rise of the Big Bird Group coincided with the rise of K&Ns’. Founded in 1964 by husband and wife Khalid and Nashuba, what is now K&N’s started as a small chicken farm which they set up in an unutilised oilseed warehouse in the family’s factory. It followed the same trajectory that any successful poultry business hopes to follow. It became a producer of grandparent stock, parent stock and broiler as well as producer of feed supply for the poultry. It was the same story as Big Bird, except K&N’s did it earlier.

That is why, perhaps, it was K&Ns that

made the first leap into frozen foods in Pakistan and it has been a gamble that has paid off. The decision was actually made in 1997, when Khalil’s son moved back to Pakistan after graduating from Cornell. The father-son duo decided they would pursue processed chicken, and when McDonalds and KFC opened their first branches in Pakistan within a year of this decision it proved fortuitous — K&Ns sat ready to provide them with chicken.

In 2001, K&N’s had another bit of good fortune: Artal, a Belgian company, had set up a chicken processing plant in Pakistan but was never able to navigate the dynamics of the largely undocumented informal chicken and feed supply market, and was forced to sell its assets at a somewhat distressed price, and K&N’s swooped in to buy the equipment for $100 million. That is what started K&N’s direct-to-consumer ready-to-cook line.

Once again, this was a first of its kind situation in Pakistan, but it was an immediate success. Processed and frozen chicken are the last line of any good vertically integrated poultry business. This was that final stage that K&Ns achieved, but it was to evade Big Bird, and indeed others for some years yet. It was only after the market was established that other players began to enter the fray. Around 2010, at least five significant players threw their hat in the ring including Al-Shaheer, Frozen Fresh, Sufi, Menu, Dawn and PK Foods to name a few. Big Bird was also among them.

The decision was a big one, and it took some time to get growing. The Big Bird Group made a Rs 6 billion investment when it launched Big Bird Foods in 2011, but the entry was a bit late. The market had a bunch of new entrants and K&N’s had turned their early mover advantage into a near unbreakable

customer base. With very low volumes, the Big Bird Foods business seemed to be struggling.

An oversaturated market with different players vying meant that Big Bird had a tough first decade fighting for space. The company saw losses of Rs 83 crores in 2021, 30 crores in 2022 and 12 crores in 2023.

It was clear by 2023 that something had to give. At the end of the year it also became clear that clients like McDonalds were going to struggle, which was a concern for the company. Big Bird had always looked to attach itself to big brand names since its inception. Fast food outlets like McDonalds, KFC, Subway, Pakistan International Airlines, Shaheen Air and Pearl Continental had their poultry meat supplied by Big Birds. However, this proved to

be a failing strategy as the company consistently made losses.

Facing adversity in this manner, the company saw that they could not depend on only a few clients in order to grow their sales. This led to the company pursuing new local clients in order to complement its sales. New contracts were signed with the likes of Johnny & Jugnu, Pizza Junction, Al Khan catering and different retail outlets which diversifies the revenue stream for the company and allows it to expand its retail footprint in the country as well. Through these contracts, the company has been able to grow its topline on a consistent basis.

In 2024, Big Birds Foods got listed on the stock exchange. The lack of pomp and circumstance around this listing was down to the fact that the company chose to get listed through a reverse merger rather than going for an Initial Public Offering (IPO). It did so by merging its poultry business with MetaTech Trading. MetaTech Trading had become defunct with a closed plant and no production being carried out.

The only saving grace for the closed down company was its listing status. By merging with MetaTech, Big Bird Foods was able to use this listing status for themselves after getting the symbol changed as well. This marked a significant change that was prevalent in the industry where many of its competitors were tightly-held, family owned businesses who chose to keep a distance from the prying eyes of outside investors.

A reverse merger meant that rather than opening up their books to the investing public, the company chose to get listed while keeping a majority of their own shareholding within its own control. An IPO would have meant that the company would have had to release its financials to the market in order to procure additional investment. Still, the merger and listing was a step in the right direction for an industry which had chosen to stay away from the market.

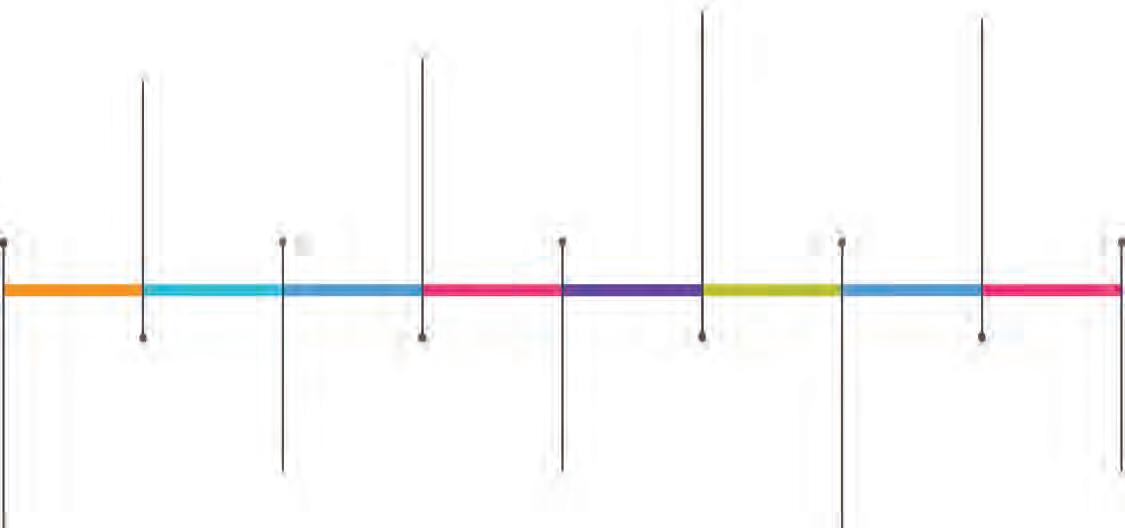

In the first step towards vertical integration, Grand Parent Poultry is founded as a breeding farm specialising in the Hubbard variety of chick

Green Nature Farms is set up to grow the grain that goes into the chicken feed being made by Big Feed. Products like maize, wheat, and rice are grown

Big Bird Foods struggles to make space in a market with a number of challengers. The genocide in Gaza leads to boycotts against some of their clients like McDonalds, resulting in fluctuating demand.

Founded by Mr Abdul Basit and two veterinarians, Dr Mustafa Kamal and Dr Abdul Kareem, Big Bird Poultry Breeders starts as a small scale hatchery business selling day old chicks

To provide the basic materials for their growing chick and broiler operations, the group sets up its own feed mixing operation

All of this brings us to the now. From 2024 to 2025, the company saw its sales increase by more than 50% going from Rs 7.2 billion to Rs 11.4 billion in 2025. The reason for this steady increase were contracts that the company had been able to sign with new B2B clients.

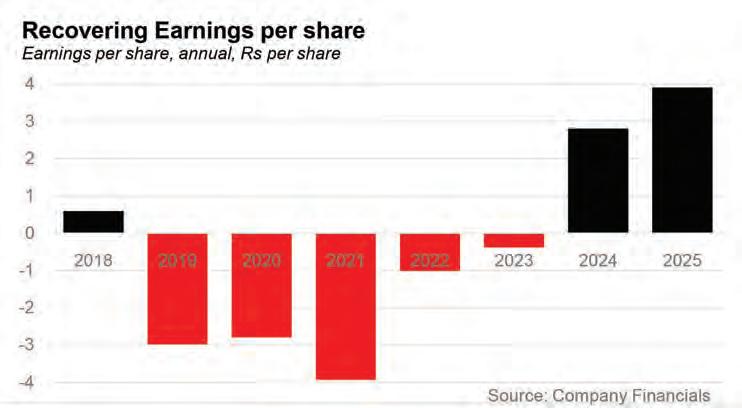

The impact of this topline growth becomes more evident when it is seen that Big Bird went from earning per share of 0.6 in 2018 to losses per share of Rs 3 in the next three years. Even when sales had surpassed Rs 6 billion in 2023, the company still ended up making a loss per share of 0.39. Only in 2024 was it able to turn these losses into earnings per share of Rs 2.8 in 2024.

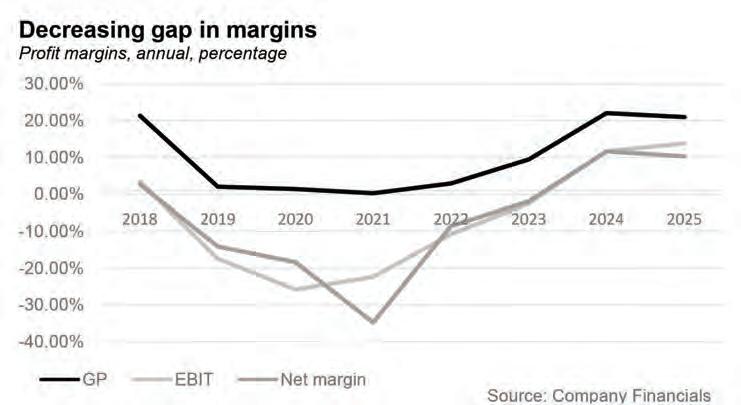

The issue present at the company can be identified by looking at the margins that were being earned. Back in 2018, the gross

Big Bird Foods posts a net profit of Rs 1.6 billion. The previous year they had posted a net profit of Rs 83.8 crores. The profits come after five straight years of posting net losses

To provide the basic materials for their growing chick and broiler operations, the group sets up its own feed mixing operation

Big Bird Foods goes public but quietly. Without pursuing an IPO, they simply acquire a defunct company that is listed on the stock exchange and merge with it to get listed

profit margin was hovering around 21% while the net margin was seen to be at 2.68%. From 2019 to 2023, the company started suffering with single digit gross profit margin. The key reason behind this was the fact that the company chose to cut down its prices while costs started to increase. From 2019 to 2023, gross margins were only able to see a high of 2.86% in 2022 while seeing a low of 0.2% in 2021.

This points towards the fact that for every Rs 1 of sales made, the company only recovered gross profit of 20 paisas. As gross margins were so low, the net margins also suffered hitting a low of -34.8% and recovered to only -1.9% in 2023. It has only been recently that these margins have stabilized around 20% with net margins of 10% becoming the norm.

With 2024 being closed out as an average year, the company still looked to find new opportunities in order to increase its revenue

potential. This included the company expanding its product portfolio into raw fish fillets and raw finger fish. This would cater to growing demand for high quality sea food products all year round. There is an estimated demand of over 700,000 tons of fish and seafood in the country and Big Bird wanted to capitalize on this market.

This was not the only development that was carried out in the financial year 2025. Big Bird also paid off debt of Rs 46 crores that it had taken from Saudi Pak Industrial and Agricultural Investment Company Limited which decreased its debt burden while it also commissioned a new product line in ethnic food segments which was expected to increase revenues as well. The solarization drive taking place in the corporate world also saw Big Bird commissioning a solar power system of 3MW which was expected to further decrease costs by Rs 60 crores for the year.

Other than looking to grow locally, a strategic agreement was signed with Alibaba Group which would allow direct export access to Alibaba’s global B2B e-commerce platform.

The result of all these efforts can be seen on the revenues of the company yet again as it saw its revenues increase by 57% from Rs 7.2 billion to Rs 11.3 billion. The increase in revenues led to operating profit increasing from Rs 1.1 billion to Rs 1.9 billion and earning per share increasing from Rs 2.8 to Rs 3.9 in 2025. This was despite the fact that the tax liability was able to eat away almost Rs 40 crores of the company’s profits.

Based on the results released till now, it can be expected that 2026 might even beat out the result of 2025. Big Bird announced in December of 2025 that it had expanded its retail presence into new outlets like Punjab Cash &

Carry, Chase Up, Diamond Supermarket and Bin Hashim super market which would look to increase its sales. In addition to that, the solar system which was commissioned last year has become operational after June 2025 which would mean that much of the benefits from this measure are expected to be enjoyed in 2026.

The biggest development on a company level is that the Securities and Exchange Commission of Pakistan (SECP) has allowed the company to convert its directors’ loan into equity. In March of 2026, the SECP approved the conversion of director’s loans given to the company by its directors worth Rs 1.5 billion into ordinary shares through issue of shares. Big Bird had applied to allow its loan to be converted into equity which would see 30 million shares being issued to its directors in exchange for the loans that they had given the company. The rate decided for the conversion was set at Rs 49.42 which was at a premium of Rs 39.42 from their par value. The company expects that the conversion of loan is expected to significantly strengthen its financial position.

To give some context to the rate of conversion, the share was trading at a price of Rs 36.6 and the last time it was trading close to Rs 50 was back in January. Since then, the market was already seeing a correction leading to the price being revised downwards and was further pummeled by the geopolitical situation prevailing in the Middle East.

One of the biggest challenges that has faced the company has been the fact that it has looked to expand its size of operations which has to be funded. This means that due to the magnitude of these expenditures, additional funds have to be injected in order to supplement its cash flow from operations. The profits have increased for the company, however, as the need for finances is higher, it has to rely on additional loans and credit.

The key source of these funds that has been used in the past was through long term financing and directors providing loans. A look at the balance sheet at the end of December 2025 shows that the company has taken loans of Rs 1 billion in the long term while the directors have also loaned the company an additional Rs 1.5 billion. This loan of Rs 2.5 billion collectively was weighing down the profitability as finance cost was Rs 18 crores.

Last year the loans taken only amounted to Rs 1.4 billion and led to an expense of 19 crores. The prevailing interest rate was around 13% in December of 2024 which has decreased further to 10.5% in December of 2025. Still, the company has not seen a significant decrease in its finance cost as it has started to rely more on

this source of funds.

The loan given by the directors was at 1 month’s KIBOR rate which means that the company was incurring a cost on it. With nearly 60% of the loan now converted to equity, the company can expect that it will drastically decrease this cost at year end of June 2026.

In order to gauge this problem of debt being taken by the company, it is important to see how the finance cost and borrowing has developed at the company over time. Due to lack of information available before 2023, the starting point for this analysis has to be from that year. In 2023, the finance cost for the year was around Rs 46 crores. When this amount is compared to the sales made for the year, it can be seen that this made up 7.6% of total sales made that year. This means that for every Rs 1 earned, the company gave away 7 paisas in terms of its finance cost.

In other words, finance cost was able to deduct 7% of sales in terms of cost from the earnings of the company. The impact of this can be seen on the operating margin of 5% turning into EBIT margin of -2.55%. From 2023 to 2024, the finance cost was able to decrease by almost 25% while sales increased by 20%, however, the finance cost still made up nearly 5% of sales in 2024 as well. This led to operating margin falling from 16.5% to 11.6%.

In 2025, finance cost remained relatively the same and with the increase in sales, the percentage of interest again fell to around 3% of sales. The reason for this can be seen in the fact that the long term and short term borrowing taken by the company made up around 27% of its total assets in 2023. As time has passed by, the percentage has fallen to 14.6% of total assets. This fails to take into account the directors’ loan of Rs 1.5 billion which would take this percentage back to 27%.

The point of carrying out this analysis is to show that the decision to carry out the reverse merger was able to get the company listed, however, if an IPO had been carried out; the company would have gained access to additional funds outside the company. This would

have meant that the owners could have sold their shares or issued additional shares to investors who would have invested in the company. The primary reason for not doing so seems to be that the owners and original sponsors want to hold onto the ownership of the company which did not allow them to avail this opportunity.

When the company was asked the reason behind going for a reverse merger rather than a full IPO, the spokesperson responded that Big Bird Foods chose acquisition over IPO to achieve faster listing, reduce regulatory hurdles and leverage Meta Trading’s existing presence. Meta Trading was a dormant listed company and this allowed immediate PSX listing without a lengthy IPO process. The benefits it gained was that there was a faster market entry, lower costs and avoided uncertainties of investor subscription.

Regardless of the method of listing, the recent developments are a step in the right direction for the company. Based on the developments carried out, it can be expected that Big Bird Foods is ready to take flight and post its best year yet. On one front, it will be able to decrease its utility costs by as much Rs 60 crores by its own estimate while finance costs will also see a fall by the year end.

An extrapolation can be carried out based on the half year results which showed that the company was able to make sales of Rs 7.7 billion by December of 2025 which had been Rs 4.8 billion for the same period last year. Based on sales totalling Rs 11 billion at the end of 2025, it can be expected that this year revenues could be expected to be above Rs 18 billion for the year. This points towards the upward trajectory that the company can be expected to achieve by year end.

Big Bird, for all its history, was late to the party and has spent years suffering because of it. The past few years, however, point towards a deliberate and dedicated effort to turn that around. Can they sustain it? Only time will tell. What we can say is that Pakistan’s frozen food market is growing and Big Bird is eager to claim a part of it. n

While many Pakistani billionaires and centimillionaires retreat from taking risks, Tabba is making bold moves. What is he doing differently?

By Farooq Tirmizi

Meeting Muhammad Ali Tabba today is probably a bit like meeting Cornelius Vanderbilt in the 1850s or Dhirubhai Ambani in the 1980s. Middle aged, already rich, somewhat well known, and accomplished enough he might choose to coast on the strength of his laurels, but you can tell this man is far from done building his empire.

The past decade has been a rough one for the Pakistani economy, and the past five years in particular have been some of the worst in the nation’s history. Other Pakistani billionaires and centimillionaires have paused or scaled back their ambitions. Tabba appears to be continuing apace.

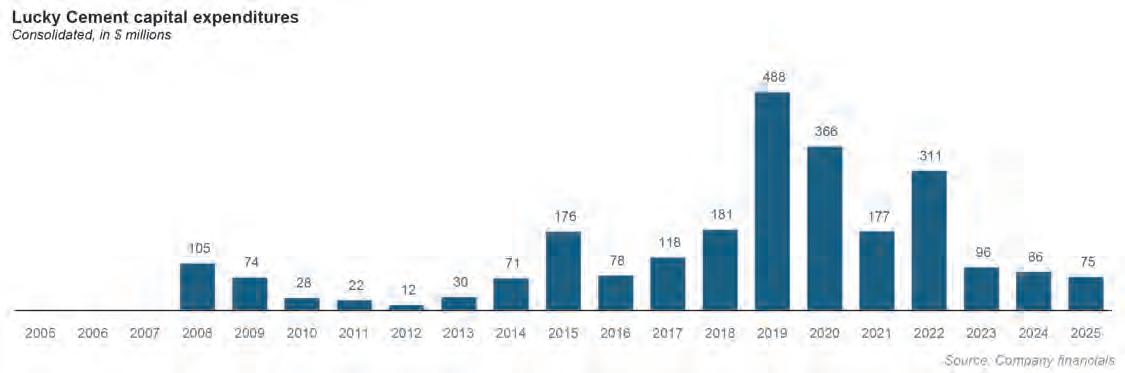

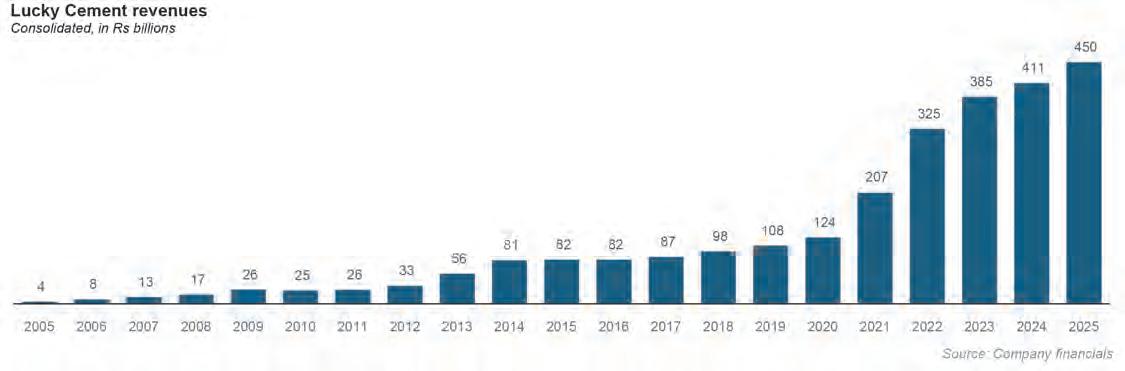

The biggest operating company – and one that serves as the holding company for most, but not all, of the conglomerate’s businesses – is Lucky Cement Ltd. Over the past 10 years, the company has invested a combined Rs319 billion ($2 billion) in greenfield capital expenditures either on its own or through financing joint ventures or subsidiaries. Of that amount, Rs154 billion ($745 million) came within the past five years, when investment activity in the country has been particularly slow.

(And to be clear, we are not referring to Tabba as a billionaire as a rhetorical flourish. Profit’s preliminary estimates of the value of his and his immediate family’s shares in the businesses they own suggests that his effective net worth may approach or even exceed $1.5 billion.)

Tabba is by no means alone in continuing to invest in Pakistan during this time. Fatima Fertilizers continues to invest heavily in new ventures, Arif Habib is making bold bets on privatization, and Engro is executing a strategic pivot towards becoming an infrastructure development company.

But the sheer breadth of ambition displayed by the Yunus Brothers Group – of which Lucky Cement and the other operating companies in Tabba’s empire are a part – is unique.

Over the past decade, the conglomerate has launched and expanded its joint ventures in its historic core business of cement manufacturing with partners in Iraq and the Democratic Republic of Congo. It launched a partnership with Kia Corporation to assemble the South Korean brand’s cars and SUVs in Pakistan, and then also launch a partnership with Samsung to assemble smartphones in Pakistan as well.

And that is just what has already launched. The conglomerate is also in a joint venture to mine copper and gold in Baloch -

istan, and has just announced that its car assembly business will also partner with the Chinese automaker Guangzhou Automobile Group to start assembling their AION and HYPTEC brands of electric vehicles in Pakistan as well.

And we have not even gotten around to describing the acquisitions of ICI and Pfizer’s assets in Pakistan, or the initiatives to expand their historical core business lines in cement manufacturing and textiles.

So, what makes Muhammad Ali Tabba different? It helps to understand where he is in the arc of his family’s rise.

The conglomerate’s history starts with Tabba’s grandfather, Haji Abdul Aziz Hashim Tabba, who set up a cotton and rice trading house in Karachi in 1962. His sons Abdul Razzak Tabba and Muhammad Yunus Tabba, started stepping into the leadership of the group in the 1970s and 1980s, and began utilizing the cash flows from trading towards setting up manufacturing units in the very businesses where they were previously just traders: textiles.

One of the group’s earliest manufacturing ventures was Lucky Textile Mills, a textile weaving mill established in 1983. The conglomerate then did a backward vertical integration by acquiring Fazal Textile Mills, a cotton spinning company, in 1987. The next year, in 1988, they also established Gadoon Textile Mills, another spinning mill. (Fazal and Gadoon were eventually merged into a single company in 2015.)

Then came the expansion into heavy industry, with the establishment of Lucky Cement in 1993, along with Lucky Energy.

The group continued to expand well after this, but it is important at this point in

the story to introduce the arrival of Muhammad Ali Tabba into the picture.

Born in 1970, Muhammad Ali Tabba spent a relatively middle class childhood. His family was up and coming around the time he was born, and by his adolescence, they were clearly significantly more prosperous than the average urban Pakistani household. But his adolescence was also Karachi in the 1980s, when the memory of Zulfikar Ali Bhutto’s thugs coming to rob factory owners of their possessions, including in some cases kicking them out of their actual homes, was not just fresh, but raw.

“Nazron mein mat aao” (do not attract attention to yourself) was a motto that Karachi’s business owners learned to live by.

Tabba went to Government Commerce College in Karachi, a constituent college of the University of Karachi, graduating in 1991. He joined the family business immediately thereafter, starting in the commodity trading arm.

This is where the Tabba family’s somewhat unique structure comes to the fore. Each generation has been offered the chance to join the family business, and a job and inheritance of the family assets is assured to all. But leadership, and who gets the lion’s share of investment in growth – and therefore who might start to distinguish themselves not just in social prominence but also their own individual wealth – appears to be determined by merit.

So, for instance, Haji Abdul Aziz Hashim Tabba let his sons take over the business and the younger among them was the more promising one initially, and hence the conglomerate took his name and became known as the Yunus Brothers Group. But the competition reset at the stage of the next generation, and Yunus’ children did not have

any advantage over Abdul Razzak’s children. It is safe to say that Muhammad Ali won his generation’s competition, though how he did it is important.

Muhammad Ali Tabba distinguished himself in two ways: first, he did well in the commodity trading arm, enough that in 1998, by the time he was 28, the family decided to invest in a venture that was his initiative: Yunus Textile Mills. Yunus Textile was a garment manufacturing unit.

Here is how much of a success it is: by 2024, the latest year for which financials of both entities are available, it had almost exactly the same revenues as Gadoon Textile Mills, which was established a full decade earlier: Rs72 billion. What makes it a more impressive feat, however, is the fact that garment manufacturing is both more complex a business to run, and a higher profitability one. So, for instance, in 2024, Gadoon Textile earned a net income of Rs795 million, and Yunus Textile earned a net income of Rs16,087 million. Literally 20 times more.

So it is perhaps not surprising that, in 2005, when it came time for his generation to assume leadership, Muhammad Ali Tabba was handed the baton to lead Lucky Cement. At the time, it was a large, but not quite the largest cement manufacturer in Pakistan. And Muhammad Ali was 35 years old.

Muhammad Ali Tabba took the mantle of leadership at a time when both the Pakistani and regional economy were booming. This matters for the cement business, particularly a company that owned cement plants in Khyber-Pakhtunkhwa, close to the Afghan border, and Karachi, next to the port.

The post-9/11 era meant that the Americans were pouring money into construction in Afghanistan and having a cement plant

We wanted to set up cement manufacturing in places of the world that the rest of the world considers difficult to operate in. That means parts of the Middle East and sub-Saharan Africa

Muhammad Ali Tabba, CEO Lucky Cement

in Lakki Marwat helped capitalize on that market. And there was the plant in Karachi, which was able to capitalize on a booming Middle East. And just to make clear the scale of the boom in the Middle East in that era: between 2004 and 2008, the population of the United Arab Emirates literally doubled from 4 million to 8 million.

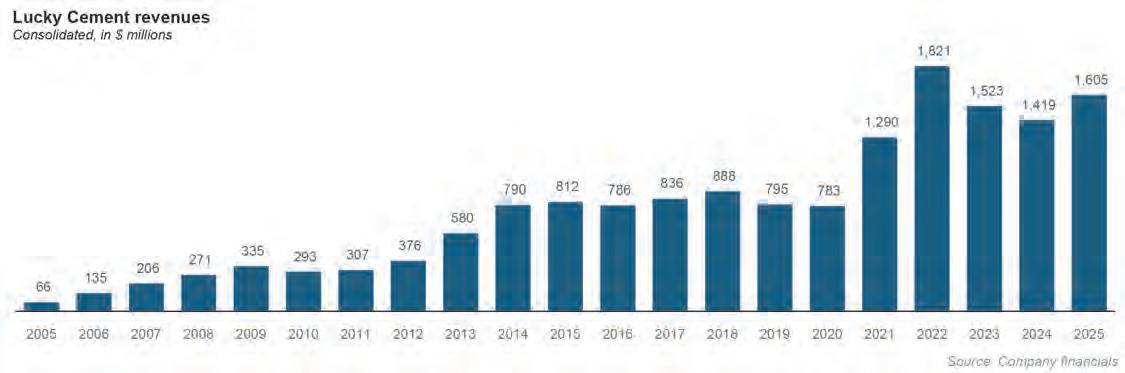

All of those people needed places to live and work, which meant an extremely sharp rise in the demand for cement. Lucky Cement was able to capitalize on that growth, going from just under Rs4 billion in revenue in 2005 to Rs21 billion in 2008.

At that point, the Yunus Brothers’ Group went from being a textile conglomerate with an energy and cement arm to being a cement manufacturer that still had a sizeable energy and textile business, at least in the minds of the public.

At the close of the Musharraf era in 2008, when the construction boom ended and most of the industry started feeling the pain of compressed margins, Lucky remained surprisingly resilient, perhaps in part because it had not engaged a massive debt-fueled expansion, unlikely many of its competitors.

One logical move at that point would have been to buy one of its struggling competitors, and indeed, over the next decade, at

least four cement companies went up for sale. But Lucky was not a buyer in any of them. Instead of leaning into expanding its cement footprint, Muhammad Ali Tabba took a wider view of what came next: enhancing the ability of the conglomerate to manage its various businesses, and then applying that enhanced expertise into creating basic materials and industrial businesses in markets that the rest of the world is willing to write off.

The conglomerate’s next two moves solidified this approach. For some time, Tabba had been looking for an acquisition target that would have allowed him to inherit the management of a multinational conglomerate’s subsidiary in Pakistan, and then in 2011, AkzoNobel decided to sell off the non-paint side of its business, which in Pakistan meant selling off the iconic ICI chemicals business.

ICI Pakistan was a subsidiary of the grand old British era Imperial Chemical Company (ICI). For the Indian subcontinent, the ICI name represented the heights of colonial

corporate ambition. It was, for much of its history, the largest manufacturer in Britain. It was formed in 1926 as the result of the merger of four of Britain’s leading chemical companies.

In 2012, the Yunus Brothers Group won a competitive bidding process to buy ICI Pakistan, buying a 75% share in the business for $152 million at a premium of nearly 30%, showing how coveted the business was. For almost exactly a decade afterwards, the Yunus Brothers Group decided to retain the name “ICI Pakistan” for the business they had bought, changing it to Lucky Core Industries only in 2023.

The purpose of the acquisition was less about buying the specific business and more about buying the ability to attract the kind of talent that would go to work for ICI Pakistan, but may not have accepted job offers at some of the Yunus Brothers’ Group companies.

“We were always looking to acquire a multinational asset in Pakistan,” said Muhammad Ali Tabba, in an interview with Profit. “We inherited a management that was far more professional and capable.”

Around the same time, Tabba was pursuing another strategy that was, in some senses, the diametric opposite of the one that

involved buying ICI: setting up cement plants in parts of the world that were even more difficult to operate in than Pakistan.

“We wanted to set up cement manufacturing in places of the world that the rest of the world considers difficult to operate in,” he said. “That means parts of the Middle East and sub-Saharan Africa.”

This was the logic behind the joint ventures that the company undertook in Iraq. In 2012, Lucky Cement formed a 50-50 joint venture with Al-Shumookh Construction Materials Trading FZE (Dubai) and the AlShawy family of Iraq. The holding company was named Lucky Al-Shumookh Holdings Ltd. Operations began in February 2014 with a cement grinding plant located near Basra. It was the first time a Pakistani cement company established an operational facility abroad.

Originally a $40 million grinding mill with a capacity of roughly 0.8 million tons per annum (MTPA), it evolved to meet the high regional demand for Sulphate Resistant Cement (SRC).

Expanding its footprint, Lucky Cement formed a second joint venture in 2016,

Al-Shumookh Lucky Investment Ltd (ASLIL), to build an integrated plant in Samawah. In May 2025, the venture achieved a major milestone by successfully firing the kiln for a new 1.82 MTPA clinker production line. A new 0.65 MTPA grinding plant at the same site is scheduled for commissioning in early 2026.

Once fully operational, this expansion will significantly increase Lucky Cement’s market share in Iraq, allowing it to sell both finished cement and surplus clinker in the country.

Note the timeline: Lucky Cement was setting up these plants in the middle of the US-led war against ISIS at the time. Missiles flying, bombs exploding, and Lucky Cement calmly setting up a cement factory. Perhaps for a family used to doing business in Karachi, the chaos of war in Iraq was an environment similar to home.

Around the same time, in 2011, Lucky Cement partnered with Groupe Rawji, a leading Congolese conglomerate, forming a 50-50 joint venture via LuckyRawji Holdings Ltd. The project cost approximately $240 million, funded by a mix of equity and

debt from international institutions like the African Development Bank (AfDB) and the International Finance Corporation (IFC). The plant officially commenced operations in 2018 with an initial capacity of 1.18 MTPA.

In late 2025, the joint venture announced a $300 million investment to double the plant’s capacity. The goal is to reach 3 MTPA by 2027 to meet surging demand from public infrastructure projects and to stabilize local cement prices by reducing reliance on imports.

Between these three plants, and its own export operations from the Pakistan locations, Lucky Cement is probably a top-5 cement producer for the Middle East and Africa region.

One would think that handling these acquisitions and joint ventures would be enough to keep one’s hands full, but for Muhammad Ali Tabba, being busy with one set of opportuni-

ties is no reason to say no to others that he had the capability to capitalize on.

So in 2016, when the government announced that they would change their automotive sector policy to break the oligopoly of the Big Three Japanese car manufacturers, Tabba decided to jump into the fray, partnering in 2017 with the Kia Corporation in South Korea to bring the Kia brand to Pakistan, through a new subsidiary called Lucky Motor Company.

That ambition was extended in 2022, when Lucky Motor partnered with Stellantis in Europe to begin assembling Peugeot in Pakistan, the first time any European brand of car was being assembled in the country.

Profit has already covered Lucky Motor’s disruptive impact on the automotive industry in Pakistan is some detail, but it is important to note that a large part of the decision to be disruptive was made by Tabba himself.

“Tabba is a very high agency owner,” said one former investment banker from Karachi who has previously done business with the group and asked to remain anonymous. “He has direct oversight on all key decisions, including pricing. ICI is the rare [part of the conglomerate] where it is unclear how much of a decisionmaker he is. But for everything else he is basically the guy calling shots.”

Oh, and when the government also announced incentives to encourage the assembly of mobile phones – particularly smartphones – in 2020, LMC signed a joint venture in 2021 with Samsung to locally assemble Samsung mobile devices in Pakistan. This production facility is co-located at LMC’s existing automotive plant site in Bin Qasim Industrial Park in Karachi.

But the next phase of the group’s growth is more ambitious yet: mining in Balochistan, in what is expected to become a major push in mineral ex-

traction in a part of the country that we have all, for decades, learned about in Pakistan Studies textbooks as being rich in mineral resources.

Lucky is a one-third joint venture partner in National Resources (Private) Ltd (NRL) along with Fatima Fertilizer and Liberty Mills.

In April 2025, NRL announced a significant copper-gold mineralization discovery in the Chagai district of Balochistan, the same district where the Reko Diq and Saindak deposits are located. The company has completed initial diamond drilling (intersecting porphyry-style mineralization) and is conducting advanced drilling at the Tang Kaur prospect.

Given the timelines for mine development, one should not expect a fully mature mining operation until the mid-2030s, but this is potentially a huge development that is likely to substantially alter both the province of Balochistan, and the commercial prospects of the companies involved in this joint venture.

Tabba has an empire so massive that in a full-length magazine feature, we found ourselves unable to do justice to all of its initiatives. One would imagine that a man with so many businesses all expanding in different directions, he may be an extremely busy man, and he probably is. But he is also known to be highly responsive to people who reach out to him. And he is also less likely, among most Pakistani business owners, to respond with “I’m out of the country right now”. He travels abroad for work and leisure, to be sure, but this is a man who is comfortable at home.

There are a few other things that stand out about Tabba. One of the most striking

is where the conglomerate is headquartered, which is in Muhammad Ali Society in Karachi, a solidly upper middle class neighbourhood off Sharae Faisal that is mostly residential. The offices are where the business has been headquartered for decades, from a time when it was a much smaller venture. No signs tell you what the office is, and the exterior looks basically like a somewhat large house.

When asked why they stay in this part of town, he says: “Why should we move? We like it here. It is nice, and we have lived here for decades.”

Another: nearly all of the cars at his headquarters are Kia. (There was just one Toyota Land Cruiser.) This is a company that clearly believes in its own product.

And then there is the approach to the next generation, where the young heirs – the oldest of whom is just seven years out of college – are slowly being brought into the business and given the opportunity to prove themselves before being handed more responsibility.

So, for instance, Tabba’s eldest son Hassan started off in 2019 as a management trainee at Yunus Textile Mills for three years, learning about every single department and function at the company. He was then brought on as CEO in 2022 and given the task to manage the backward vertical integration of the mill, a task that is now complete.

Both the elder Mr Tabba and his son are wealthier than all but a handful of others in Pakistan, but act like they are still working on building, focused on what comes next. They have laurels to rest on, but choose to keep moving forward.

For the fourth generation of a family, that is not common. One thing is for sure: the Tabba empire is not done expanding just yet, and its current leader and the next generation are acting like they do not want its peak to come any time soon. n

Either the April 2 increase was necessary, in which case publicly undercutting it a day later was poor statecraft. Or it was not properly thought through, in which case ministers were sent out to defend a decision that did not deserve defending. Neither interpretation inspires confidence

As far as optics go, Prime Minister Shehbaz Sharif has some serious introspection to do. Why send his petroleum minister and finance minister before the cameras on April 2 to defend one of the steepest fuel price increases in recent memory, only to appear on television himself the very next night to partially unwind it? Why ask ministers to make the hard case for economic necessity and then dilute that case almost immediately from the highest office in the country? In moments of crisis, governments are judged not only by what they decide, but by whether they appear to know what they are doing. This week, Pakistan’s government did not.

That matters because the fuel issue is not an isolated pricing dispute. It sits at the intersection of war, external vulnerability, fiscal stress and political credibility. After the US and Israeli attack on Iran, and Iran’s closure of the Strait of Hormuz, global oil markets tightened sharply. Pakistan, which relies heavily on imported fuel and on shipping routes tied to the Gulf, was always going to feel the effects. The question was never whether domestic prices would need to move. It was whether the government would move with speed, clarity and a credible plan.

Instead, it lurched.

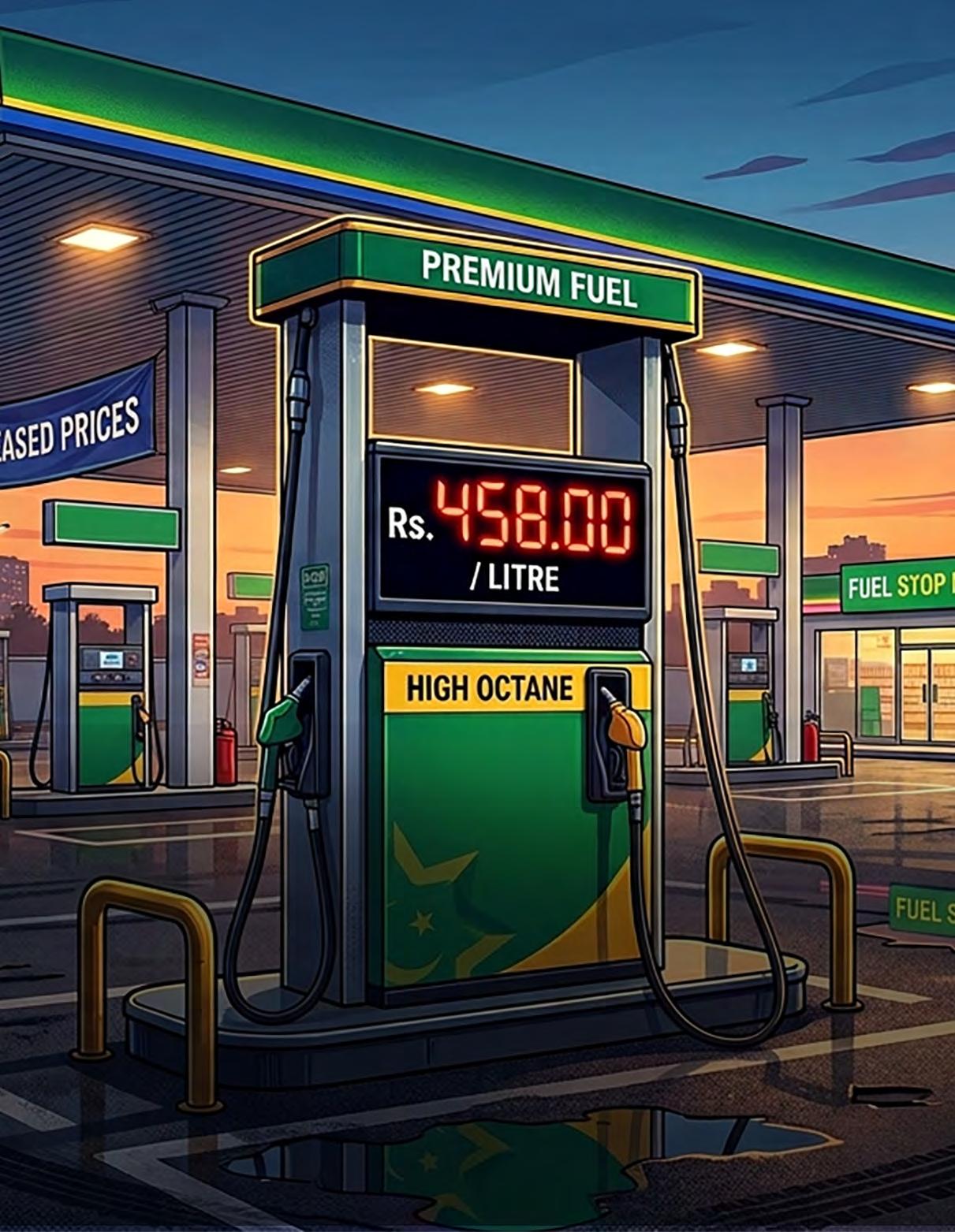

In early March, the government acknowledged the first direct economic impact of the regional conflict and raised petrol and diesel prices by Rs55 per litre. Even then, it appeared uncertain. A national fuel conservation plan was prepared, including work-from-home and distance learning measures, only to be deferred. The message was that the situation was serious, but not serious enough to require a settled response. By the end of March, the government was still freezing or delaying price adjustments even as the subsidy bill mounted. Then, on April 2, it moved sharply in the other direction: petrol was raised to Rs458.41 per litre and diesel to Rs520.35. A day later, the prime minister cut the petroleum levy by Rs80 per litre and brought petrol back down to Rs378.

The danger in such back-and-forth is not merely administrative untidiness. It creates a wider impression of decision paralysis at exactly the wrong time. Pakistan has, by its own telling, tried to play a leading diplomatic role during this crisis. It has argued for de-escalation, stability and responsible conduct in a volatile region. But diplomacy abroad loses force when economic management at home looks improvised. A state that appears unsure of itself domestically sends a weak message internationally. It suggests that events are being managed day to day, not strategically.

There is also a more immediate domestic cost: trust. Fuel pricing is one of the few areas where the public can see the government’s choices almost in real time. When prices are

delayed, then hiked, then partly rolled back, people do not read this as calibrated management. They read it as confusion, panic or politics. Businesses delay decisions. Transporters anticipate another revision. Consumers rush to pumps, then wait for relief, then expect another reversal. Markets stop responding to official statements because they assume those statements may not last 24 hours.

The harder truth is that a substantial increase in prices was unavoidable. Pakistan simply does not have the fiscal space to absorb an external oil shock of this scale through blanket subsidies. The weekly cost was approaching Rs50 billion, or about Rs7 billion a day. That is not a cushion. It is a rupture in the budget.

This is why the memory of 2022 matters. Pakistan has already lived through the consequences of treating fuel prices as a political problem to be postponed rather than an economic reality to be managed. Subsidies that look bearable in a single news cycle accumulate quickly into a larger crisis of financing, inflation and exchange-rate pressure. They complicate IMF negotiations, weaken fiscal credibility and eventually force a harsher adjustment than the one originally avoided. The lesson from 2022 was not that fuel price pass-through is painless. It was that delay makes it worse.

There is, moreover, a reason the petroleum levy became central to the April 2 adjustment. It is one of the government’s few large, administratively simple and relatively dependable revenue tools, especially under an IMF-backed fiscal framework that leaves little room for slippage. When the levy on petrol was increased and diesel was adjusted, the logic was crude but understandable: if global prices must be passed through, preserve revenue where possible and limit the fiscal bleed. That may be politically costly, but it is economically legible.

The problem is that the government then retreated before that logic had even settled.

Cutting the levy by Rs80 per litre does not curtail public anger. It makes the government look weak and unsure of itself. It also weakens a key revenue stream at a time when the state can least afford it. And the math is even less forgiving than it first appears. When prices rise sharply, demand softens. Consumers drive less, transport slows, discretionary usage falls. That means levy collection does not automatically rise in proportion to the nominal rate because the taxable volume begins to shrink. If, after that, the levy itself is cut, the revenue impact is worse still. Pakistan ends up with the political pain of higher prices and less of the fiscal gain that was supposed to justify them.

None of this means governments should ignore the social effects of a fuel shock. On the contrary, the case for social protection becomes stronger precisely when pass-through is unavoidable. But this is where the response should have been focused from the beginning. Instead of trying to suppress prices for everyone and then staging a theatrical rollback, the government should have moved quickly on targeted protection for those most exposed: low-income households, public transport users, small farmers and freight systems linked to food distribution.

There are already signs of what that approach looks like. Provincial governments announced targeted support for two-wheelers, farmers and transport operators. Provincial governments went further, with Sindh offering cash support to registered motorcycle owners, relief for small farmers and subsidies tied to transport fares, while other measures included free public transport and stable train fares. This is where policy should become more serious: build administrative pathways for direct support, expand BISP where needed, use provincial databases intelligently, and separate social protection from the fantasy that broad fuel subsidies can be sustained indefinitely.

That would also be better politics. Citizens can accept pain more readily when the policy is coherent, the explanation is honest and the relief is directed to those who actually need it. What they struggle to accept is indecision dressed up as compassion. A government that first insists prices must rise, then acts as though it has discovered public hardship only after the fact, does not look empathetic. It looks unprepared.

The prime minister may believe he was showing responsiveness by stepping in on April 3. In reality, he exposed a deeper problem. Either the April 2 increase was necessary, in which case publicly undercutting it a day later was poor statecraft. Or it was not properly thought through, in which case ministers were sent out to defend a decision that did not deserve defending. Neither interpretation inspires confidence.

This is the central issue. Crises compress time. They punish hesitation. They reward governments that decide early, communicate clearly and protect the vulnerable without pretending economics can be suspended. Pakistan cannot afford policy made in installments, especially not when war is driving up import costs, threatening the external account and testing the country’s credibility on multiple fronts at once. What was needed was swift passthrough, a firm explanation, and serious targeted relief. What Pakistan got was a hike, a retreat and another reminder that indecision at the top carries a price of its own. n

Is there a case to be made to do it anyways?

Iranian oil has always been traded in Pakistan, albeit in very small quantities because of persistent sanctions. What would happen if Pakistan decided to go ahead with it anyways?

By Ahmad AHmadani

Amid a sharp seven-day increase of Rs137.24 per litre in petrol and Rs184.49 per litre in highspeed diesel — pushing prices to Rs458.41 and Rs520.35 per litre respectively — a familiar

question has returned to Pakistan’s energy debate: if Iran is right next door and has oil to sell, why does Pakistan not simply buy it?

At first glance, the argument seems difficult to dismiss. Pakistan is an energy-importing country with recurring balance of payments problems, high inflation, and a long history of fuel price shocks feeding into trans-

port, food and industrial costs. Iran, meanwhile, is a neighbouring producer that has for years supplied small amounts of petroleum products across the border through informal channels. In moments of crisis, the temptation is always the same: if the fuel is closer and possibly cheaper, why not formalise what already happens in fragments and use it to reduce the

import bill?

But once the question moves from smuggling and small-scale border trade to statebacked commercial imports, the issue stops being a simple pricing matter. It becomes a test of how much economic risk Pakistan is willing to absorb in exchange for cheaper energy. That is because formal oil imports from Iran would not be taking place in a vacuum. They would intersect with sanctions, banking channels, refinery standards, sovereign financing, trade access, and Pakistan’s dependence on external partners. What looks like an energy decision would quickly become a broader geopolitical and macroeconomic one.

That is the real debate. It is not whether Iranian oil exists, nor whether some quantity of it has always found its way into Pakistan. It is whether the Pakistani state can afford to turn an informal reality into formal policy.

There is a case to be made, and it is not a frivolous one. Pakistan’s need for imported energy is persistent, while its domestic reserves of natural gas have declined and imported fuel remains a major source of pressure on prices, industry and external accounts. In that sense, the attraction of Iranian energy is obvious. It is nearby, transport routes are shorter, and the logic of geography is difficult to ignore. Energy imported overland from a neighbouring country can, in principle, be cheaper and less logistically cumbersome than energy brought in through long sea routes.

That logic has long underpinned Pakistan’s interest in Iranian gas, and some of it carries over to oil as well. The appeal is not only price. It is also convenience, distance and strategic diversification. Pakistan has spent years trying to patch over its energy shortages through imported LNG, imported coal, domestic coal, nuclear expansion and other adjustments in the power mix. Those measures have reduced some urgency, but they have not removed the structural vulnerability that comes from relying on imported fuel and expensive external financing to keep the system running.

If Pakistan were to proceed with formal oil purchases from Iran, the immediate economic argument would be that even a modest discount could matter at scale in a high-price environment. It could provide some relief to refiners, reduce part of the import burden, and potentially soften the pass-through of global shocks into domestic fuel prices. For a country where every rise in petrol and diesel quickly spills into freight, food and industrial input costs, even limited savings can appear attractive.

There is also a strategic argument. Pakistan has often found itself with very little room for manoeuvre in energy markets. Long-term commitments, external funding constraints and limited domestic production have narrowed its choices. Buying from Iran could be presented as a way of increasing policy autonomy, reducing overdependence on a narrow set of suppliers, and using geography to Pakistan’s advantage rather than treating it as a diplomatic inconvenience.

Yet this argument has limits. The first is that Iranian oil is not necessarily available at the kind of deep discount many assume. The second is that Pakistan does not usually import petrol and diesel as finished products when crude can be processed more economically through domestic refineries. And the third is that once the trade becomes official, the benefit has to be large enough to justify the risk. That is where the case begins to weaken.

If Pakistan decided to go ahead with formal purchases of Iranian oil despite sanctions, the first impact would not be at the pump. It would be in the financial system.

Oil is not bought with rhetoric. It has to be paid for, shipped, insured, financed and cleared. That means banks, payment channels, shipping companies, insurers and traders become involved. And that is where sanctions bite. A formal arrangement with Iran would expose Pakistan to the risk of secondary sanctions, which could complicate international payments and make counterparties far more cautious about doing business with Pakistani entities tied to the trade. The issue would no longer be one cargo of oil. It would be whether Pakistan was willing to place parts of its access to the global financial system under strain for the sake of that cargo.

This is why the comparison with smallscale border trade is misleading. Informal petroleum flows can survive in legal grey zones because they remain fragmented, local and unofficial. State-backed imports are different. They require visibility, contracts and financial traceability. The moment Pakistan moves from tacit tolerance to official procurement, it invites a response not just from Washington but from the broader network of institutions that underpin cross-border trade.

The consequences could quickly spread beyond energy. Pakistan’s wider economy depends on access to external financing, remittance channels, trade settlement systems and support from multilateral institutions. It also depends heavily on ties with partners such as

Saudi Arabia and the United Arab Emirates, which have not only supplied oil but also helped Pakistan through deferred payment facilities and other forms of financial support during periods of stress. A turn towards Iranian oil would not automatically end those relationships, but it could complicate them at exactly the moment Pakistan has the least room for diplomatic or financial friction.

There is also Europe to consider. Pakistan’s preferential trade access under GSP Plus supports billions of dollars in exports. Any move that creates the perception of sanctions non-compliance would introduce a risk far larger than the immediate savings from cheaper fuel. The arithmetic is brutal: even if Iranian oil offered some discount, that gain would be small beside the damage that could come from disrupted exports, financing pressure or reduced investor confidence.

Then there is the technical side. A senior refinery official cited in the original story noted that Iranian crude is relatively heavy and that refined products from Iran do not fully meet Pakistan’s Euro V specifications. That does not make imports impossible, but it does make the idea less simple than it sounds. Pakistan would not merely be buying cheaper fuel next door. It would be buying a politically sensitive commodity that may not fit neatly into existing quality and refining requirements.

And that is before the broader policy question is addressed: what, exactly, would Pakistan be risking sanctions for? If the answer is short-term consumer relief, the logic is weak. Pakistan has a long history of using energy pricing for political management rather than productive restructuring. Cheap fuel distributed as a temporary cushion can provide immediate relief, but it does little to solve the underlying problem of how scarce and costly imported energy should be allocated in an economy with repeated external crises.

If, however, the answer is that Pakistan wants to secure energy for productive sectors, protect industry, reduce pressure on imported fuels and make a longer-term strategic shift, the argument becomes more serious. But even then, it remains a high-risk trade-off. Pakistan would not simply be buying oil. It would be choosing to absorb a set of diplomatic, financial and trade consequences in exchange for uncertain savings and complicated implementation.

That is why the issue has remained unresolved for so long. The attraction is real, but so are the costs. Iranian energy may look like an obvious solution when prices spike and public anger rises. In practice, it is less a shortcut than a wager. And for Pakistan, a country that already lives close to its external limits, that wager could end up costing more than the oil ever saves. n

The value of the Iranian Rial is rising dramatically in Pakistan’s currency markets. What is behind the increase?

BORDER TRADE, LOOSER EXPORT RULES AND POSTWAR BETS LIFT KARACHI-LAHORE CASH QUOTES EVEN AS THE RIAL STAYS WEAK AGAINST DOLLAR AND EURO

By Abdullah Niazi

In the midst of a war with the United States and Israel, the value of the Iranian Rial has risen fourfold in Pakistan since the start of hostilities just over a month ago. Dealers in Karachi say 10 million rials that sold for about ₨2,500 before the war are now being quoted near ₨10,000, while money changers in Lahore describe a similar move from about ₨2,000 to ₨8,000.

But the increased value of the Iranian rial in Pakistan’s money market is less a story of a global currency comeback and more the effects of an undocumented border economy suddenly needing more rial cash. In other words, what has surged is the Pakistani street price for rial notes, especially in markets linked to under the table trade on Pakistan’s Western borders. The rial’s standing in the wider world remains at a historic low.

One reason is that Pakistan has made trade to and through Iran easier at exactly the moment when the western route matters more. The commerce ministry approved a temporary exemption from normal financial-instrument requirements for certain exports to Iran and for rice exports to Central Asia through Iran’s land route, effective March 24 to June 21. That move widened an earlier pattern of workarounds, including a previous exemption for mango exports to Iran, and was meant to keep trade moving where normal banking channels are weak or unavailable.

That matters because Pakistan and Iran already do a great deal of business outside ordinary formal banking. As an earlier investigation by Profit has covered, there has long been trade between Iran and Pakistan despite the heavy sanctions Iran is under. In fact, a large informal economy exists along the 909-kilometer border between Iran and Pakistan.

Everything from Iranian snacks, chocolates, crockery and other items are illegally transported along the Gabd-Rimdan line, including the most precious commodity coming in from Iran: fuel. The smuggling of petroleum products into Balochistan from Iran has long been a practice that has left Balochistan’s fuel economy relatively free from the shocks of the rest of the country’s fuel economy. The region of Balochistan extends into Iran, and the neighbouring country has a small province by the same name. The border is largely barren and sparsely populated and the common culture between people on either side of the border makes it extremely difficult to impose strict border regulations. Hundreds of thousands if not millions are involved in this illicit trade.

Under pressure of international sanctions, Pakistan-Iran commerce has long been shaped by barter, weak banking links and informal settlement. In this kind of an economy, the demand for currency is driven not just by official trade documents but by whoever needs rial notes or rial settlement to move goods. That

helps explain why the rial is suddenly attracting buyers in Karachi and Lahore. More goods moving through the Iran corridor means more traders wanting rial exposure. Some buyers also appear to be making a second bet: that if the war eases and trade continues, the rial could be worth more later than it is today. Global markets have been trading on similar expectations. Reuters reported this week that investors were lifting risk assets in hopes the conflict could end within weeks after signals from Washington pointed to possible de-escalation.

But the rial has not staged a broad international recovery. Reuters reported on Jan. 27 that the currency had fallen to a record low of 1.5 million rials to the dollar after unrest tied to economic stress. On Apr. 1, open-market quotes in Iran still showed roughly 1.592 million rials to the dollar, with the euro near 1.846 million rials. That means the rial remains weak against major currencies, even if it is fetching a much higher cash quote in Pakistan’s local market. That distinction is central to the story. The rial can be weak against the dollar and euro, yet still become more expensive in Karachi or Lahore if Pakistani traders suddenly need more of it. Sanctions, broken banking links and informal settlement systems can produce sharp local premiums that do not show up cleanly in standard international exchange-rate screens. Pakistan’s border trade with Iran has long run through exactly those kinds of channels.

In fact, the global weakness of Iran’s currency can be gauged from the odd numbers in which it is calculated. Dealers in Pakistan often talk about the rial in blocks of 10 million because the denomination has become unwieldy after years of inflation and devaluation. Iran’s open-market trackers commonly quote prices in toman, not rials, with one toman equal to 10 rials. So when exchangers in Karachi or Lahore say “10 million rials,” they are discussing a very large note bundle rather than a normal retail-style exchange quote.

There is also a business case behind the speculation. Reuters reported in mid-March that Iran had managed to keep crude exports flowing at close to normal levels through Hormuz despite the war, with shipments of 13.7 million to 16.5 million barrels by mid-month. That does not prove a sustained currency recovery, but it does help explain why traders in Pakistan may believe Iran is still earning and that rial demand could remain firm for now. What comes next depends on whether this demand turns out to be temporary or structural. If Pakistan extends the waiver, if the Iran route keeps carrying goods, and if the war does wind down, the rial could stay in demand in Balochistan, Karachi and other connected markets. If the exemption expires, enforcement tightens or postwar optimism fades, the premium now visible in Pakistan’s cash market could ease just as quickly. For now, the best answer to the headline is simple: the rial is rising against the rupee in Pakistan because border trade, informal settlement and speculation have all started pulling in the same direction, even while the currency remains weak against the world’s major units. n

Despite NEPRA’s prosumer regulations, solar panels and batteries is getting increasingly more expensive, here is why

The market for any product is seldom entirely logical. Take Pakistan’s solar panel market. The new prosumer rules were supposed to make rooftop solar less attractive. NEPRA’s 2026 regulations replaced unit-for-unit net metering with net billing, meaning exported electricity is no longer credited at the same rate consumers pay for imported electricity.

Under the newly proposed regulations, prosumers would buy electricity from the grid at the applicable retail tariff of roughly Rs37 to Rs55 per unit and sell surplus power at around Rs10 to Rs11 per unit.

The rules were meant not only to dis -

courage a shift toward net metering, which was increasingly putting pressure on IPPs’ capacity payments and, in turn, circular debt, but also to reduce the burden on the import bill. According to a recent market report, solar panel imports alone cost more than $2.1 billion in 2024, making Pakistan the world’s third-largest importer of solar panels.

On paper, the policy change should have cooled the rooftop market. And yet, in early 2026, even before the outbreak of the war with Iran and the closure of the Strait of Hormuz, a strange shift was already underway. Retail prices for both panels and batteries began to move up.

The first thing to understand is that Pakistan’s solar market is larger than net-metering economics. Reuters reported in February that most of the country’s solar panels are not connected to the grid to sell excess electricity at all.

Many households and businesses buy solar for self-consumption, outage protection and tariff avoidance rather than for export income, because even then, the numbers make sense.

This also matters because a policy that lowers the buyback rate, while it hurts the export-led model, does not erase the appeal of producing your own daytime electricity in a country

with high tariffs, unreliable supply and a long habit of consumers hedging against the grid.

Pakistan’s solar import wave was already enormous before the rule change. According to Reuters, imports of Chinese solar components jumped fivefold from around 3,500 MW in 2022 to 16,600 MW in 2024, and crossed 10,000 MW in the first four months of 2025 alone. In other words, this is not a niche market anymore.

There is also an important timing issue. The regulatory shock did not land on a clean slate.

Firstly, after immediate backlash, the government moved to protect existing users and pending applicants. It was reported that all net-metering applications submitted before Feb. 8 would be processed under the previous rules, covering 5,165 pending applications and around 250.822 MW of capacity. It was also proposed to preserve existing billing terms for already contracted users until their agreements expire.

That meant the market did not suddenly move from “old economics” to “new economics” for everyone at once. A section of buyers still had reason to rush, installers still had a backlog, and traders still had an incentive to price for a transition.

But then something more interesting happened. After intense backlash, just three days after the approval of the new regulations, the prime minister-led panel told the National Assembly that implementation of the policy would be halted.

This gave new entrants a window to sign agreements on the old terms for as long as the policy change remained on hold. That, in turn, created even more demand and pushed prices higher.

Keeping in mind that registration takes roughly one month, someone who gets registered within that period can still sign an old contract, regardless of whatever changes happen later. So instead of easing, the urgency increased.

But this is also the broad frame. The real story splits in two, because panels and batteries become expensive for different reasons.

The January retail jump in panel prices was real enough in local reporting.

The Express Tribune reported that prices of imported Chinese panels rose by roughly Rs5,000 per unit in common wattage categories, with a 585-watt panel moving from around Rs16,000-Rs17,000 to Rs20,000Rs21,000, and dealers blaming higher raw-material costs, taxes and firmer Chinese prices.

It lines up with what was happening

globally in the inputs that matter to solar panel production. Silver prices had surged 130% over the previous year in February alone, squeezing solar manufacturers, and that silver paste accounts for 30% of total solar cell costs. Copper also hit record territory in January and analysts expected it to average nearly $11,975 a tonne in 2026, the highest annual consensus in its survey history.

Then came the policy shift in China, which matters because Pakistan’s solar market is overwhelmingly import-led and heavily exposed to Chinese supply. On Jan. 9, Reuters reported that China would cancel VAT export rebates for photovoltaic products from April 1. The China Photovoltaic Industry Association said the move should help stop an excessive decline in export prices, and noted that some exporters had been using rebates as a discount for foreign buyers.

For Pakistani importers, that matters even if local demand softens somewhat, because the landed cost can rise regardless of local demand.

Pakistan then added its own layer. The government’s proposed 18% GST on imported solar panels in the 2025-26 budget was later reduced to 10%, but a 10% tax is still a tax. The revised rate was retained after parliamentary pressure. Even though traders had reportedly already begun lifting prices ahead of the budget measure taking effect, the tax played a huge role in the price increase.

NEPRA may have weakened the economics of oversizing a rooftop system purely to dump excess units into the grid. But panels are not priced only by Pakistani policy. They are priced by Chinese export policy, global metals, local taxation and dealer expectations about replacement cost.

If panels face a tug-of-war between weaker local incentives and higher global costs, batteries face something more straightforward. The bottomline is that NEPRA’s new regime may make storage more valuable, not less.

Once exported daytime electricity is compensated at around Rs10-Rs11 per unit while evening electricity bought from the grid costs several times more, the financial logic shifts to storage.

A unit of solar power used instantly in your own home or stored for use after sunset becomes much more valuable than a unit sold to the grid. Institute for Energy Economics and Financial Analysis (IEEFA) notes that solar-plus-battery systems store cheap daytime electricity and discharge it during the evening peak, helping consumers reduce grid dependence and bills. Battery demand rises precisely because the grid now pays less for exported solar.

Talking to Profit, various solar equip-

ment vendors noted that there was a visible uptick in the sale of batteries since February. That is one of the main reasons why battery prices stayed firm, or even rose, despite a weaker policy mood around rooftop solar.

Another structural reason is that Pakistan’s battery market is still deeply import-dependent and burdened by taxes and duties. IEEFA reported that solar with battery energy storage still pays back in roughly three to five years in Pakistan’s residential sector despite a 48% cost increase from surcharges and duties on lithium-ion batteries.

Even though there have been reports of local companies beginning the process to assemble batteries in Pakistan, with Treet entering an agreement with a Chinese company, they are still at the import stage. Their first shipment of Lithium Ion batteries only arrived in Pakistan a week ago.

Additionally, just as with panels, global Chinese policy turned less friendly. Reuters reported in January that China would cut VAT export rebates for battery products to 6% from 9% between April and December 2026, before scrapping them entirely from Jan. 1, 2027.

Three days later, lithium prices in China jumped after the announcement, with the most-active lithium carbonate contract rising 9% in a day and prices having climbed 167% from the previous year’s low.

For Pakistan, which remains a net importer of advanced battery storage as well, this is bad news. A market that already pays a taxand-duty premium is being asked to absorb a higher export-side cost too.

So batteries are expensive for almost the opposite reason from panels. A household that once maximized rooftop size and used the grid as a virtual battery under favorable net metering now has a stronger reason to buy an actual battery.

What we are seeing right now is a re-pricing of the solar value chain. NEPRA’s latest prosumer rules may yet slow some categories of rooftop adoption, especially for new grid-exporting users. But they do not automatically make solar cheap. In fact, by colliding with global cost pressures and shifting the commercial logic toward storage, they may make the next phase of Pakistan’s solar revolution feel more expensive.

So in this solar market, urgency, speculation, regional conflict and the search for energy independence all converged at once. The government’s policy shift was supposed to make rooftop solar less attractive, but the temporary halt in implementation did the opposite by giving consumers a narrow chance to secure older, more favourable terms. Solar equipment became costlier not despite uncertainty, but because uncertainty itself became part of the price. n

By Profit

The US Secretary of War Pete Hegseth’s wealth fund manager , Stan “The Man” Leebovitz, has asked him to fire just one more military service chief to make some money.

“Yeah, firing that guy Randy is good to cash in on some of our shorts, but let’s sweeten that deal a bit,” he said, to the US war czar, referring to the sacking of US Chief of Army Staff General Randy George on Friday.

“Ooh, I’ve shorted so many stocks, Pete, you don’t even know,” he said.

“Hey, I’m not picky, it could be the Navy guy, or the Marines or the Air Force, I don’t care,” he said. “Yeah, I draw the line at the Coast Guard or even the National Guards Bureau chief. It’s got to pack a punch to set the markets going.”

“Yeah, I know my place, I’m not asking for the CENTCOM chief,” he said, referring to Admiral Brad Cooper, current chief of the

US Central Command, which is overseeing the attack on Iran. Hegseth, however, said that though he wasn’t making any promises, even that might not be off the cards.

The conversation between Leebovitz and his client took place not in a private location but in a podcast Money Talks, highlighting the Wall Street’s relaxed demeanour in recent years after the realisation that keeping up the appearance of avoiding conflicts of interest wasn’t worth the trouble anymore.