08 Pakistan bends banking rule to make way for exports to and through Iran

10 Millat Tractors makes a big bet on Pakistan and beyond

17 Apna Microfinance narrows its losses, but continues to bleed money

18 IGI Life struggles to grow premium revenue in 2025

20 Packages made billions in 2025. The government took almost all of it away in taxes

22 KSB Pumps sees increases sales, even as some customers cannot afford to pay

24 How far can increased financing to build homes go in Pakistan?

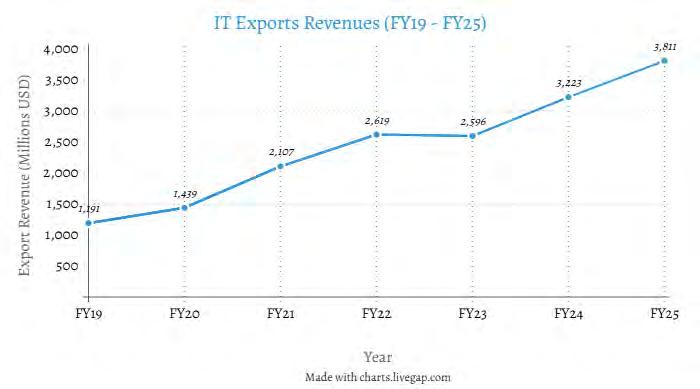

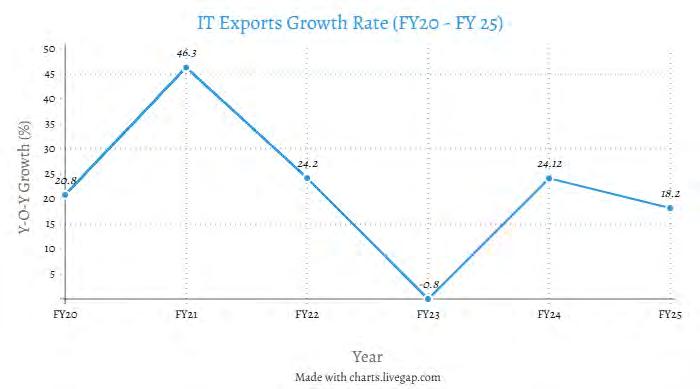

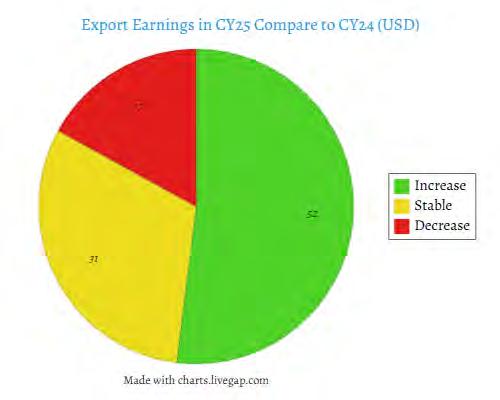

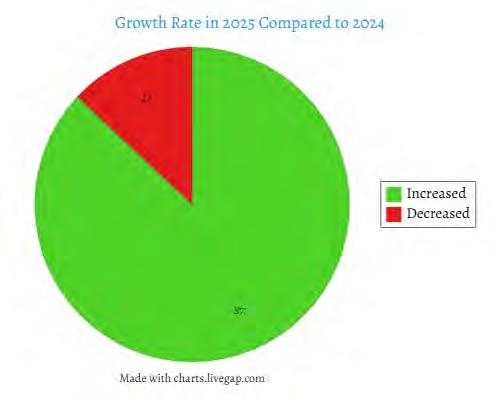

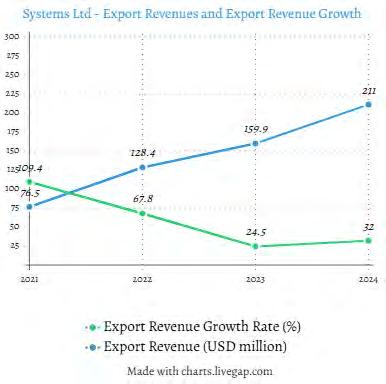

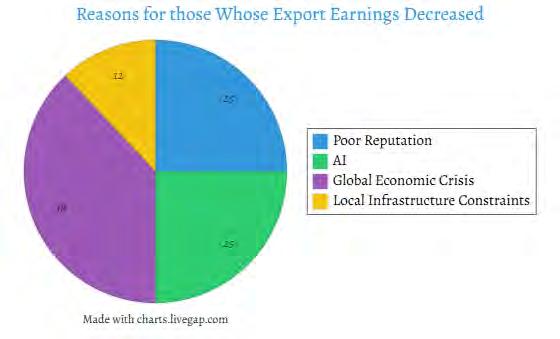

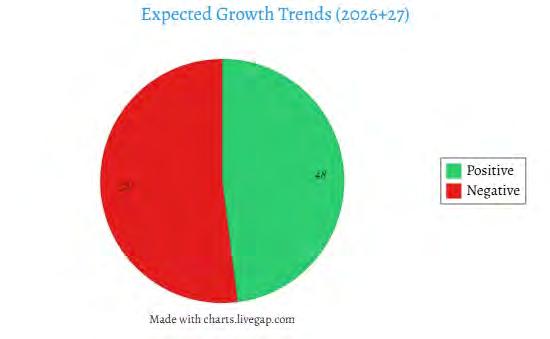

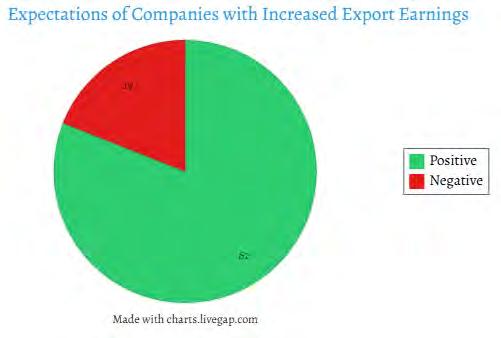

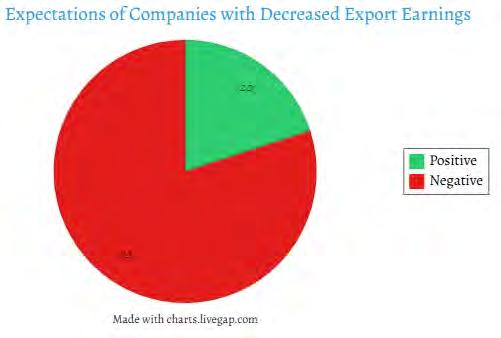

28 Pakistan’s IT exports are definitely rising, but fears are rising that taxes and poor internet infrastructure are quickly becoming barriers to growth

Publishing Editor: Babar Nizami - Senior Editor: Abdullah Niazi

Business Reporters: Taimoor Hassan | Usama Liaqat | Zain Naeem | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editors: Saddam Hussain | Abdul Hameed - Video Producer: Adnan Maqsood

Director Marketing: Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Pakistan bends banking rule to make way for exports to and through Iran

Exporters in Pakistan usually need a bank guarantee through a financial instrument for products they are sending outside the country. That requirement has been waived for three months for certain exports going to Iran, and to Central Asia through Iran

By Shahzad Paracha

In the midst of the continued war in the Middle East, Pakistan’s commerce ministry has eased one of the most rigid parts of its export rulebook for shipments moving through Iran.

The temporary exemption, effective from March 24 to June 21, 2026, allows exporters to send certain goods to Iran, and rice to Central Asian Republics through Iran’s land

route, without the usual financial-instrument requirement that normally governs exports under Pakistan’s trade regime.

The decision marks the first moment in which Pakistan seems to be adjusting trade realities along its border in accordance with growing global conflicts. For decades, trade between Iran and Pakistan has largely been barter based and informal because of international sanctions on Iran. On top of this, Pakistan’s continued conflict with Afghanistan

and the subsequent border closure has meant usual trade routes to Central Asia have also been closed off.

According to one expert, Pakistan is possibly trying to take advantage of the current international situation. By easing trade requirements, Pakistan might even want to set a precedent of some form of trade with Iran — which could be beneficial for both countries even after the war ends.

What was the requirement?

Before this exemption, exporters sending goods out of Pakistan were expected to comply fully with SBP-notified foreign exchange procedures under Para 3 of the Export Policy Order, 2022. In practice, that has meant routing exports through documented, bank-compliant payment channels so that export proceeds are traceable and can be repatriated into Pakistan within the prescribed time. It was mandatory for exporters to use letters of credit or advance payments under this rule.

The rule is designed to protect the country’s foreign exchange regime since one of the biggest leaks of forex out of Pakistan has always been the Pak-Iran border.

This kind of framework would work easily in markets where banking links are normal. The Pak-Iran market is far from being one of those. The condition made it almost impossible to trade with Iran for institutionalised and big exporters due to sanctions on Iran and a non-existent banking link between the countries.

In fact, owing to the absence of traditional banking channels between Pakistan and Iran, the government operationalised a barter trade mechanism with Iran in 2023 which was later revised in October last year.

It is also important to note that this is also not the first time Islamabad has reached for a workaround. The Commerce Ministry’s 2024-25 yearbook says it removed the mandatory financial-instrument requirement for mango exports to Iran, describing the move as one that eased costs and procedural burden for seasonal trade.

In December 2025, the government also granted a one-time exemption from Para 3 for kinnow and potato exports to CIS countries through Iran, with SBP advising that the waiver be season-specific, subject to controls for repatriation of export proceeds, and not treated as a precedent.

Most of the recent exceptions were made due to the closure or increased scrutiny at the Torkham border, and armed conflict in Afghanistan on the Durand Line.

What is the change?

This is the backdrop to the latest relaxation. While the formal export rule assumes a banking pipeline that, in this case, has long been patchy, functionally unavailable for many transactions, the latest decision broadens that earlier piecemeal approach.

According to the reported notification, Pakistan will now allow rice exports to Central Asian Republics and Azerbaijan through Iran’s land route, while permitting a wider basket of exports to Iran itself through the same corridor. That basket includes food and agro-

based items as well as selected manufactured goods, among them seafood, potatoes, meat, onions, maize, citrus fruit, bananas, tomatoes, frozen chicken, pharmaceuticals and tents. The exemption is temporary, lasting three months, which suggests the government is testing a trade-facilitation valve rather than rewriting the export rulebook outright.

But this relaxation is not a free pass. Exporters were told to undertake that export proceeds will be repatriated within the prescribed period. While such undertakings usually are difficult to enforce down to the last container, the move is more out of desperation than strategy.

The policy shift does not legalise undocumented trade. It tries to keep the trade moving where formal instruments are hard to arrange, and export numbers are falling like dominoes.

How could this help Pakistan?

There is no sugarcoating the fact that Pakistan’s regional export numbers are going from bad to worse ever since the war with Afghanistan. Exports to all the central Asian states, as well as to Afghanistan have slowed down considerably due to a partially closed gateway and unsafe passage.

Pakistan’s exports to Afghanistan fell to $219.5 million in July-December 2025 from $505.8 million in the same period a year earlier, a drop of more than 56%, according to SBP data. In the meantime imports from Afghanistan also remained small, falling to $6.3 million from $10 million over the same period. Baseline comparisons remain difficult because trade had already been hit by prolonged border closures on the Afghan side and by reduced momentum in Central Asian markets.

While small in magnitude, this border trade does not represent the hundreds of thousands informally traded on that border, keeping the economics of those regions afloat.

More importantly, exports to the five Central Asian states were also considerably down. They fell by 9.59% year-on-year in the first four months of FY26, even before this latest exemption was introduced.

With the global political situation not warming up to any resolution in the near future and the forward-looking projection of fuel prices touching the sky, the government needs to find alternate trade routes, even if it means losing out on some amount in duties.

Meanwhile the current situation in Iran, consumption and demand are at an all time high, especially for food. So while Pakistan’s forex reserves may take a hit and this leniency may result in future border control issues, what it does is that it gets the wheels rolling.

Not to mention that the immediate benefit is also nominally more practical. For exporters of perishable goods such as fruit, vegetables, meat and seafood, delays created by documentation bottlenecks can destroy margins way before the consignment hits the market. So if this temporary waiver reduces one layer of friction at a moment when the western route matters more than usual, it could result in better margins.

SBP itself warned in its February 2026 Monetary Policy Report that the prolonged closure of Pakistan’s western border was constraining exports, especially pharmaceuticals and cement, to Afghanistan and landlocked Central Asian destinations.

This move can also act as a proof of concept. Pakistan has traditionally been using Afghanistan for its trade with Central Asian countries. Ever since the Afghan Pakistan Transit Trade Agreement (APTTA) in 2010, Pakistan has not had to look past Afghanistan except for a few times. Things back then were also simpler because the sanctions on Iran were not as severe.

So this move is also a test of whether Iran can function as a workable transit corridor into a larger northern market when the Afghan route is unreliable. If the waiver helps even partially restore volumes in products already suited to land transport, the decision may outlast its three-month life in one form or another. If it does not, the government will be forced back to the deeper question it has been avoiding for years. Whether Pakistan’s export rules are too dependent on financial rules dictated by a western influence and assumptions that do not hold on its own north-western frontier.

The move is also strategically justified. Reuters reported in November 2025 that Afghanistan was increasingly shifting trade to Iran and Central Asia to reduce dependence on Pakistani routes, particularly through Chabahar and overland links with Uzbekistan, Turkmenistan and Tajikistan. If Afghanistan and other regional traders are actively diversifying away from Pakistan’s traditional corridors, Islamabad has an incentive to ensure its own exporters are not stranded by a compliance regime built for easier banking environments. Put plainly, if the region is rerouting, Pakistan cannot afford to behave as though the old route still does all the work.

The effect of this trade remains to be seen in the months to come and the last section of this story will not be written by the notification or the amendment, it will be written by the monthly trade data. But one thing that may end up getting ignored in this is that once again the government’s taxation and compliance policies are held hostage by on-ground economic realities. And as long as this keeps on happening, a sizable tax reform is unlikely in this country. n

MILLAT TRACTORS makes a big bet on Pakistan and beyond

The historic tractor manufacturer will become the first automotive company in Pakistan’s history to export its own brand to other countries.

But even as they look towards expanding their horizons, challenges persist at home. Can a National Tractory Policy help address them?

By Abdullah Niazi

Sometime in the not-so-distant future, tractors assembled under the brand name “Millat” will be shipped from Pakistan to farms in Africa. Millat Tractors, the historic tractor maker that manufactures and sells Massey Ferguson tractors in Pakistan, reached an agreement with Massey Ferguson Corp (MFC) in December last year to sell their tractors abroad under their own “Millat” branding.

With this agreement, Millat will become the first Pakistani automotive company to export their own product to any part of the world. The feat is more impressive considering that unlike the rest of the automobile industry in Pakistan, tractor manufacturing has achieved near complete localisation rates.

Pakistan makes its own engines and transmission systems for tractors as well as all the easier parts, and overall tractor localisation stands at around 94%. Millat has actively been exporting tractors since 2015. Their main market has been Africa, but they have recently also sealed a deal to export tractors to Mexico. Over time the share of exports in Millat’s overall revenue has been rising. From 6% in FY2019-20, it has risen steadily with a few dips in between. In 2023-24 they marked a milestone of 2500 tractors exported in a year, and exports accounted for 10.2% of revenue in 2024-25, and in the first half of 2025-26 exports are already making up 14.1% of Millat’s total revenues.

The increasing importance of exports in Millat’s bottomline is natural. As the largest player in Pakistan’s tractor industry (the second biggest player is Al Ghazi), Millat commands more than 60% of the overall market share. This pecking order has been long established in Pakistan, but a close look at tractor production and sales in Pakistan will show you that erratic policies, inconsistent tax regimes, and pressures on agriculture have left Millat and other tractor manufacturers with a market that is not growing at the pace they would like.

Last year, for example, Millat produced 18,637 tractors. Their overall capacity is from 30,000-40,000 tractors when operating on a double shift. The year before that production was 30,479. Before that it stood at 19,022. The pattern is quite obvious. Since 2007 the company has seen a seesaw between single and double shifts. Production rises and falls erratically. Take a peak behind the curtain and it becomes obvious that any time the government makes changes to the sales tax, floods hit the country, crop losses increase, or inflation increases or decreases there are serious fluctuations in demand and subsequently in production.

The uncertainty is an unfortunate situation for an industry that holds a unique position in Pakistan. Not only is the tractor industry

vastly localised, it is also vital to agricultural growth — perhaps the most important sector in Pakistan’s economy which has been shrinking and changing in recent years under the pressures of climate change. Despite the availability of locally manufactured tractors, Pakistan’s farm mechanisation rate is well below what it should be, particularly for an agrarian economy. Add to that shrinking farm sizes and you have a scenario where the business environment is stifling. While the tractor industry has localised almost entirely, they still do not produce many other associated products like harvesters and hundred horsepower tractors.

This explains why there is an increasing shift towards exports. Pakistan produces, according to the industry, the cheapest tractors in the world on a dollars per horsepower basis. And while exports are an increasingly lucrative part of business, industry leaders are clear on the need to increase the number of tractors out in Pakistan’s agricultural fields. To this end, the industry has been advocating for a National Tractor Policy. In the past few months they have gotten some success as well, with the Engineering Development Board drafting a policy that will be part of the upcoming budget in June. The policy as imagined by the industry creates financing incentives for tractors, gives local manufacturers tax breaks compared to foreign brands, and sets up hiring centres all over the country.

It is an ambitious plan and the first of its kind for the industry. It is also very long overdue. But just how far can it go?

The localisation dream

“Millat tractors is a huge Pakistani success story,” says Raheel Asghar, the incumbent CEO of Millat

Tractors. “It started as a private company, it was nationalised, and when it was privatised again it became a shining example of what a management buyout can do. To this day Millat is an example of how this can work.”

The history he is referring to is indeed quite impressive. The foundation of Pakistan’s tractor industry was laid in Karachi in 1964 with the incorporation of Rana Tractors and Equipment Limited. Back in the day, this was a hot new company on Pakistan’s corporate landscape. Founded by Rana Khudad Khan, a Muslim League Member of Parliament from Sargodha, the new company was listed on the stock exchange in 1965. It began importing completely built units (CBU) of Massey Ferguson tractors into Pakistan, but only to start off. The company was already assembling semi knocked down (SKD) tractors themselves by 1967.

Then came the Bhutto Administration. Along with a slew of other businesses, corporations, and institutions Rana Tractors was also nationalised and incorporated into the Pakistan Tractor Corporation. Under this new body, the main goal was increasing localisation. The establishment of an Engine Assembly Plant in 1982 and a Machining Plant in 1984 paved the way for this localisation. In 1985, Sikander Mustafa Khan was appointed Managing Director of the company. A mechanical engineer by profession, he had a Masters Degree in Production Engineering from Imperial College. By all accounts he was the exact opposite of what public sector CEOs usually are: educated, very specifically qualified for the job, and up to the task. During his tenure Millat Tractors consolidated localisation. The idea was simple: the cheaper domestic tractors Pakistan could produce the more they would sell in a country where farm mechanisation is low but

The foundation of Pakistan’s tractor industry was laid with the incorporation of Rana Tractors and Equipment Limited Karachi in 1964. The company was nationalized by Z.A. Bhutto in 1972, and privatized again in 1992.

When Millat was founded in 1964 there were around 15,000-20,000 tractors in the entire country. Today there are nearly a million tractors in Pakistan. This has been thanks to local companies contributing to this. If Millat had not been around, all of these tractors would either have been imported or not there at all

agriculture is the main economic activity.

In 1975, around the time the company was nationalised, the overall number of tractors in Pakistan was 35,700. By 1985, when Sikander Mustafa Khan took charge, this had gone up to 1.57 lakh tractors. And by 1992 this number had risen to around 2.5 lakh tractors all over Pakistan. This was a time of growth, and much of this growth was pushed by localisation.

In 1992 the first Nawaz Sharif administration began the process to right the wrongs of nationalisation. One of the companies up for privatisation was Millat Tractors. What made this privatisation particularly special

Sikander Mustafa Khan took charge of Millat Tractors in 1985 when it was still a government owned asset. In 1992 he guided the company towards privatization through a management buyout. He is still the Chairman of the company to this date

Raheel Asghar, CEO of Millat Tractors

was that the company was bought out by the management. Sikander Mustafa Khan is still the Chairman of Millat Tractors to this day.

“When Millat was founded in 1964 there were around 15,000-20,000 tractors in the entire country,” says the company’s CEO Raheel Asghar. An engineer by profession with a Masters degree from Cambridge, he spent more than a decade at Honda in the United Kingdom, before coming to Pakistan and working for Toyota Indus Motors. He was CEO of Al Ghazi Tractors for a couple of years and became CEO of Millat in 2023. Unlike in other industries, despite being direct competitors the tractor industry’s interests are largely common. A complete lack of any cohesive policy has meant there is little time for competition. “Today there are nearly a million tractors in Pakistan. This has been thanks to local companies contributing to this. If Millat had not been around, all of these tractors would either have been imported or not there at all,” he adds.

The growth has been the result of a single-minded focus on localisation. The first year after the management buyout, Millat bought out Bolan Casting, which manufactures grey and ductile iron castings for tractors and buses. The company’s direction was clear from here: diversify into different parts of tractor manufacturing and become an integrated en-

tity with end to end production capabilities. The company established Millat Equipment and Millat Industrial Products, and by 2011 hit record tractor production of more than 40,000 units in a single year. This was the late peak of a boom period that started in 2001 and ended around 2008. “In this time Pakistan’s tractor population per hectare was on par with India. But after 2008 the government’s policies were rapidly changing. There was no consistency, and that is when you start to see fluctuating demand,” explains Raheel Asghar.

The field changes

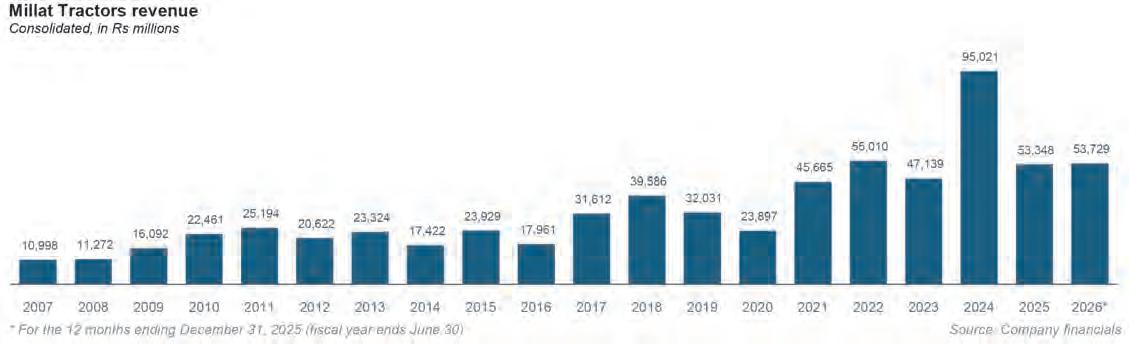

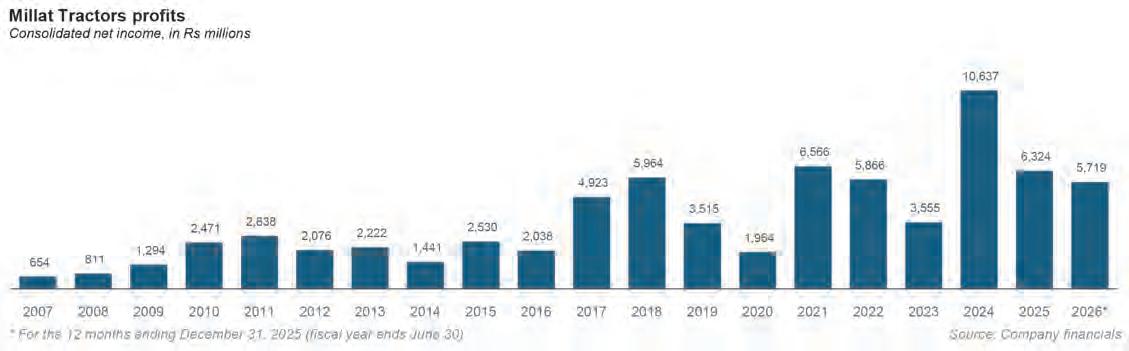

Take a look at Millat Tractors headline numbers over the past 20 years and it is clear that this is a company that makes money. It has consistently been profitable, with a consolidated net income of Rs 65.4 crores in 2007, and peaks of Rs 10.6 billion in 2024. Last year the company’s profit stood at Rs 6.32 billion.

What does become immediately apparent, however, is the fluctuation Raheel Asghar was talking about. Since 2007 there have been seven years where Millat’s revenues and profits have fallen rather than risen from the previous year. And the falls have not always been small. Compare just the last two years: profits fell by more than 40% year on year.

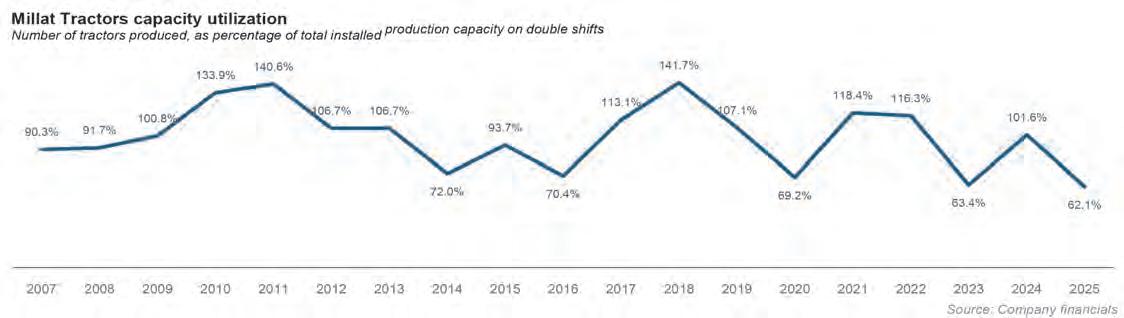

While the revenue and profit numbers

are revelatory, perhaps nothing captures this fluctuation better than Millat’s capacity utilization numbers. It is a complete rollercoaster ride that naturally corresponds to the falling revenue and profit numbers. From 2007 to 2013 Millat was operating at capacity with double shifts. Their lowest capacity utilization during this period was 90.3% in 2007 with 27,081 tractors produced, and their best year was 2011 with a capacity utilization of 140.6% and 42,188 tractors produced. Then in 2014 the production capacity fell to just over 70%. Since then it has been a story of spikes and quick falls in production. Every couple of years capacity falls by more than a quarter. The lowest it hit was 63.4% in 2023, when in the aftermath of devastating floods farmers were not buying a whole lot of machinery. Rises associated with subsidy schemes from

the government like Punjab’s Green Tractor Scheme result in rises, and then there are years like 2025 when capacity utilization has gone as low as 62.1%.

“There has been no consistency. Up until 2010 there was no sales tax on tractors. This made sense — farmers need it, agriculture needs tractors. Then the government imposed sales tax and we saw a fall. One year the sales tax is 17%, then it is changed to 5%, then it goes back up to 10% — farmers do not buy because of the burden of these taxes,” says Raheel Asghar.

The effect of sales tax is obvious and telling. But this inconsistency is possibly also why the tractor industry has shifted towards exports to diversify their business. In 2007 99.5% of Millat Tractor’s revenue came from domestic sales. That number remained largely consistent

with some small changes up until 2023 when the first significant change came at exports accounting for nearly 8% of total revenue. In 2025 this crossed 10%, and in the current fiscal year it looks to be crossing 15%. The milestones are clear. In 2020 1000 tractors were exported, in 2021 this rose to 2000, and 2024 marked the export of 2500 tractors. With the recent agreement to sell Millat brand tractors in Africa, the exports are expected to go up.

Wanted: Stability and Consistency

In Millat tractors and tractor manufacturing, you have the example of an industry that has managed to achieve localisation, has a willing and ready customer base, and is at a stage where it is ready to sell to other

parts of the world as well. But despite this, they remain unsatisfied with how business is done at home. That is why, perhaps, the upcoming budget is so important for them. According to Raheel Asghar, they have had very promising and encouraging conversations and engagements with the government.

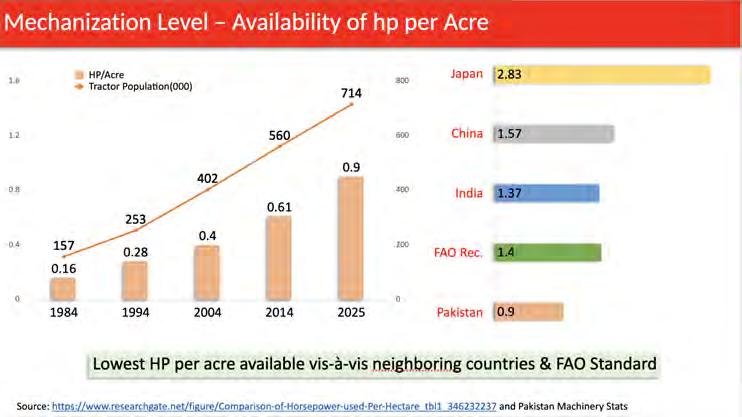

“Our main submission is that tractors are the core of mechanisation. They are vital for agriculture growth,” he says. Pakistan’s need to mechanize is also a cause for concern. Current-

we were on par with India. But since then they have hurtled ahead and our industry has stayed behind compared to them,” say Raheel Asghar. This, he says, is despite the fact that Pakistan makes the cheapest tractors in the world. “Our customers might disagree with this because they have seen prices rising in recent years, but Pakistan’s dollar per horsepower cost is lower than the rest of the world. That is why exports are also feasible,” he says.

According to an industry report, Paki-

A screenshot from a presentation shows farm mechanization levels in Pakistan compared to other countries

ly the country’s mechanization ratio is below 1 horsepower per hectare. The recommended rate as per the UN’s Food and Agriculture Organisation is at least 1.4 horsepower per hectare. Compared to Pakistan, India is at 1.37, China is at 1.57, and Japan is at 2.83.

“There was a time up until 2007 when

stan manufactures tractors at around $140 per horsepower unit. China’s production is at $155, India is at $180 and countries like Belarus and Brazil that are known for their tractors are making them at over $350 per unit of horsepower.

With the low cost, Pakistan’s potential

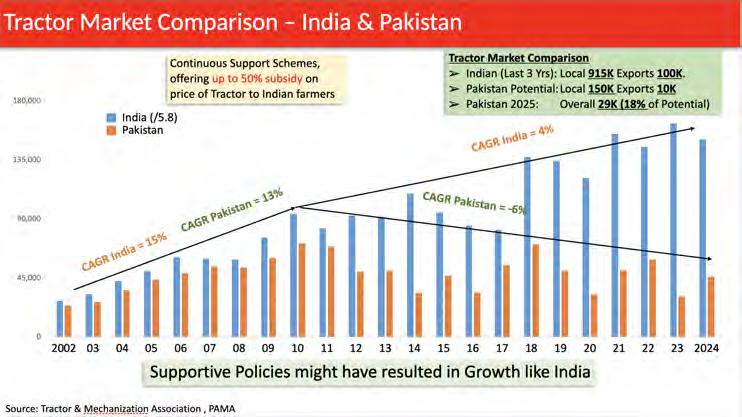

Up until 2010, Pakistan and India’s tractor industries were growing at similar rates. Since then, however, there has been a stark divergence between the two neighbouring countries

is much higher than where it is at. Not only are we currently not meeting current capacity, we are far far behind what the actual potential could be. Up until the year 2010, the CAGR for the tractor market in India was 15% and in Pakistan it was 13%. Since then, however, India’s CAGR has been 4% while Pakistan’s has dropped to -6%. In the past three years, India has produced 9.15 lakh tractors for their domestic market, and exported another 1 lakh tractors. If Pakistan had stayed on the same growth trajectory it would have had the potential to make 1.5 lakh tractors for the domestic market and export 10,000 tractors a year. However, at current rates Pakistan is barely producing 18% of this. The resultant effects on Pakistan and India’s farm productivity are obvious. India’s per acre profitability for wheat is three times higher than Pakistan and for rice it is more than double according to 2023 numbers. This is despite the fact that the average farm size in India is 2.6 acres while in Pakistan it is 5.6 acres.

The Indian example is the spectre that haunts the Pakistani tractor industry. It is where they could have been but they feel hamstrung. “India’s profitability on farms is much higher. They get a lot of other subsidies on fertiliser, and those subsidies are given directly unlike here. This means their farmers can actually afford the tractors unlike ours,” explains Raheel Asghar.

What comes next?

This focus on affordability is the cornerstone of the proposed National Tractor Policy. According to the Millat CEO, tractors are not a luxury for farmers, they are a tool they need to compete and survive. “Pakistani tractors are the cheapest in the world but our farmers do not always have the means to buy them.”

And that, essentially, is what the entire proposal hinges on. Exports are well and good but the industry feels the best way to grow it to its full potential is by making it affordable. The first part of this proposal requires larger agricultural reforms. According to Raheel Asghar, Pakistan should follow the Indian model of giving subsidies. “India has 5-6 subsidies working at any given time and all of them are targeted towards small landowners and given for specific things. Our subsidies are usually across the board.”

The concept is simple. Farmers with larger landholdings can probably afford tractors anyways. It is those without the means to do so that need to be given more targeted subsidies. The biggest example of this, of course, is the subsidy given to fertilizer companies. The government has long provided subsidised gas to fertiliser companies which then sell to all farmers. Some companies like COVER STORY

Engro themselves have been advocating to change this and instead give direct subsidies to farmers with land less than 5 acres. While some changes have been made because of the IMF in the past few years with gas prices for these fertilizer plants being rationalised, there is a long way to go and subsidies in Pakistan are more general than specific.

Then comes what can be done specifically for tractors. Currently, the SBP provides financing for tractors at around 7% under different schemes. According to Raheel Asghar, this should be adjusted regularly with the existing interest rate. “This facility was given when the interest rate was at 20%. Today it is at 10% so the benefit has been reduced.”

Then there are other kinds of direct subsidies. “The Green Tractor Scheme by the Punjab Government is a very good idea to make farm mechanization affordable for those that really need it. As part of the policy, other provincial governments should also be given the tool to create a roadmap for similar subsidies,” says the MIllat CEO.

The other big demand which requires investment are hiring centers. Because farmers do not necessarily have the capital or for that matter the space to store tractors when they are not needed, formal means of renting them should be available. Tractors are rented privately all over the country but the policy calls for the establishment of formal hiring centres. “We talk so much about our youth bulge and growing literacy,” says Raheel Asghar. “This country

needs better yields. Why not give financing to young, educated people to set up proper hiring centres where people can come get tractors? If they invest in this, we will also be able to make harvesters, larger tractors, and other products that are capital intensive and not easy to buy for people.” In Indian Punjab, half the size of Pakistan’s Punjab, there are 11,000 such centres. On this side of the border their presence is negligible.

Then there are the general demands which most local industries have. They want protection from imports and a higher import duty on imported and CBU units. While the domestic industry dominates in Pakistan, some larger machinery has to be imported. Similarly the tractor industry wants export benefits — by that what they mean is they want the money they are owed on time. The government regularly holds off on tax refunds

and is slow to return money, creating cash flow crunches and restricting growth. According to Millat, even now they have around Rs 6-7 billion stuck with the government’s tax officers yet to be released.

The aims of the policy are clear and not overstated as we have learned of them up until this point. What form will it emerge in when the budget rolls around? Only time will tell, but Profit has been told that already there was a proposal to merge the tractor policy into the larger automobile policy that the government has been working on. However, with resistance from the tractor companies, this idea has been abandoned. The commerce minister and other relevant parties seem committed to releasing this policy. If it comes out in the shape that it is in and is implemented, Pakistan might get back on track in an industry that was thriving not so long ago. n

Punjab Chief Minister Maryam Nawaz inspects a tractor at the launch of her Green Tractor Scheme on the 1st of November 2024 in Lahore. The tractor industry wants other provincial governments to emulate such initiatives

Apna Microfinance narrows its losses, but continues to bleed money

The bank flipped towards positive net interest margins, but the contemplated merger with Mobilink Microfinance Bank is likely still needed to help solidify the bank’s position

In Pakistani microfinance, survival is often presented as a growth story in disguise. Apna Microfinance Bank’s 2025 results invite precisely that sort of reading. The bank reported a loss per share of Rs3.84 for calendar year 2025, better than the Rs7.23 loss per share recorded a year earlier. Net advances rose by about Rs2.4 billion to Rs10.56 billion, deposits climbed from Rs25 billion to Rs30 billion, and management told investors that more than 89% of the bank’s net advances were now secured, primarily against gold. It also said the bank had cut its network from more than 100 locations to 71 branches and, as of the end of December, had the lowest cost of deposits in the microfinance sector. Those are not trivial changes. They describe a lender trying, with some urgency, to turn itself from a brittle unsecured-credit story into a tighter, more collateralised one. But they do not yet describe a healthy bank. Cumulative historical losses still stand at roughly Rs15 billion, and the State Bank of Pakistan has already permitted Mobilink Microfinance Bank to conduct due diligence with a view to a possible merger.

The first thing to say about the 2025 numbers is that the income statement finally looks less self-defeating. Mark-up and interest earned rose 12% to Rs3.15 billion, while markup and interest expensed fell 25% to Rs3.01 billion. That was enough to drag Apna from a negative net mark-up position of Rs1.19 billion in 2024 into a positive net interest profit of Rs146 million in 2025. Fee and commission income rose 28% to Rs286 million, total non-mark-up income increased 20% to Rs346 million, and net income before operating costs swung to a positive Rs492 million from a loss of Rs898 million the year before. In a business where the cost of funds had previously been crushing the asset yield, that is a significant turn.

For all the progress in margins, however, Apna remained deep in the red. Operating ex-

penses fell 8% to Rs2.02 billion, which helped, but not nearly enough. Credit loss allowance and write-offs turned negative again, and loss before levy and taxation was still Rs1.61 billion. After minimum tax differential, the bank ended the year with a net loss of Rs1.65 billion. That was far better than the Rs3.10 billion loss of 2024, but it was still a large hole for a lender of this size. The official corporate briefing makes the broader fragility plain enough: total assets stood at Rs20.73 billion at the end of 2025, but net equity was negative Rs10.51 billion and accumulated losses had widened to Rs15.93 billion. Apna, in other words, is not merely loss-making; it is loss-making with a balance sheet already hollowed out by years of cumulative damage.

Why, then, did 2025 look better at all?

Part of the answer is macroeconomic. Apna’s management told investors that the reduction in policy rates had begun to feed through to the bank’s cost of deposits, and that it was also trying to attract a greater volume of corporate current-account deposits in order to push funding costs lower still. Part of the answer is operational. Sponsors injected another Rs500m during the year in the form of share deposit money, taking the total to Rs2.35 billion, while management kept shrinking the network by closing non-productive branches and trimming administrative costs. And part of it is portfolio design. The bank has been deliberately expanding secured advances and recovering old bad loans; management said it recovered Rs347.3m in principal from non-performing loans during 2025, and a further Rs20.4m by January 2026. This is what a repair job looks like: lower funding costs, slower cash burn, more collateral, more recovery, less romance. That repair job makes more sense once one remembers what Apna Microfinance Bank actually is. The bank was incorporated in May 2003 and began operations in 2005 under the microfinance banking framework, later

receiving a national-level licence in 2015. It was formerly Network Microfinance Bank, a name it shed in 2012, and today sits within the United International Group, whose businesses span insurance, tracking, technology, agriculture and advisory activities. PACRA, the rating agency, estimates it has about 2.7% market share by gross loan portfolio at the end of 2024. That is large enough to matter in the sector, but not large enough to absorb repeated shocks with ease.

The bank’s history also explains why its recent results feel more like rehabilitation than expansion. In its 2020 annual report, Apna disclosed that after an SBP inspection its lending operations had been suspended from November 2016 because its information systems had not been properly classifying certain running-finance cases as non-performing and had not been provisioning them correctly. The bank was allowed to resume lending in June 2017 and then had to rebuild a fresh portfolio while dealing with the residue of the old one. That episode matters because it helps explain why Apna’s problems have such a long tail. The weaknesses on its balance sheet are not merely the product of one bad year or even one bad economic cycle. They are the accumulated after-effects of governance, underwriting and recovery problems that were then worsened by the pandemic, the 2022 floods, inflation and tighter financial conditions.

That is also why the bank’s product pivot deserves more attention than it usually gets. On paper, Apna still offers the familiar menu of a Pakistani microfinance lender: business loans, livestock financing, housing loans, agricultural finance, pension loans, salary loans, tractor loans and vehicle products. But the bank’s current strategy revolves around a far more specific proposition: lending against household gold. Its “Apna Gold” product is aimed at low-income individuals, salaried workers, the self-employed and micro-en-

trepreneurs, and offers up to Rs150,000 for individuals and up to Rs500,000 for micro-entrepreneurs against pledged gold or gold ornaments. A related “Nisa Gold Loan” targets female borrowers and offers up to Rs350,000 against gold jewellery for domestic needs, housing, agriculture or business enhancement. This is not glamorous finance. It is finance designed for a country in which gold jewellery is often the closest thing working-class households have to liquid collateral. Apna is effectively trying to convert the metal in family cupboards into the bankable security its old unsecured book could never reliably provide.

That gold-backed turn is not only a product decision; it is a theory of survival. Over 89% of the bank’s net advances are now secured, primarily by gold, and that SBP restrictions currently prevent Apna from issuing new unsecured loans. Management has therefore been focusing on repeat business within the existing portfolio. In practice, that means the bank is becoming more like a tightly collateralised retail lender than the broad-based microcredit institution its older marketing language once suggested. It may not be an ideal vision of financial inclusion, but it is a rational response to years of delinquency. In Pakistani microfinance, aspiration often begins with unsecured lending and ends with collateral.

All of this is happening inside a sector that has spent the better part of six years trying to recover from one blow only to be hit by another. The State Bank’s review of the microfinance sector for 2024 shows both the scale of its importance and the depth of its stress. MFBs account for only about 1.5% of total financial-sector assets, yet by the end of 2024 they served 9.2 million borrowers, compared with 4.4 million domestic bank borrowers, and they accounted for around 80% of all branchless-banking accounts, which reached 122 million. In other words, microfinance banks are small in asset terms but enormous in reach. They are structurally too weak to be systemically dangerous and too socially important to be ignored.

The same SBP analysis shows why Apna’s distress is not wholly idiosyncratic. During 2024, the sector’s asset base expanded by 38.5%, while deposits rose 22.8%. Net interest margins improved to 13.9% from 12.2% in 2023, but asset quality worsened: the infection ratio, after peaking at 10.5% in June 2024, still ended the year at 9.7%, well above the 6.7% recorded a year earlier. Eight of the 12 institutions in the sector were loss-making, and aggregate capital adequacy fell to just 2.6%, far below the 15% regulatory minimum. This is the backdrop against which Apna’s numbers must be read. A bank that turns one corner but remains undercapitalised is not merely fighting its own history; it is operating in an industry

whose weakest institutions are still dragging the aggregate well below safe ground.

There is, however, a nuance worth noticing. The State Bank’s Annual Report for 2025 suggests the sector began to stabilise in fiscal 2025 even as capital stress worsened. The aggregate capital adequacy ratio is negative 1.6% at end-June 2025 from 5.7% a year earlier, dragged down by a few weak institutions. Excluding the non-compliant players, the sector’s aggregate CAR would have been 20.9%. That split tells the story more clearly than any slogan could. Pakistan’s microfinance sector is not collapsing; it is bifurcating. Stronger players are surviving, even improving. Weaker ones are becoming untenable.

That is what makes the contemplated merger with Mobilink Microfinance Bank so important. Apna’s official corporate briefing says that SBP has allowed Mobilink to conduct due diligence and that, if the process and negotiations succeed, Apna would be merged with and into Mobilink under Section 48 of the Banking Companies Ordinance, 1962. The due-diligence process is expected to conclude within the following month. For Apna, this is less a strategic option than an admission of arithmetic. A bank with negative net equity, nearly Rs16 billion in accumulated losses, continuing CAR non-compliance and an only partially repaired earnings engine does not merely need time. It needs a stronger balance sheet, better infrastructure and a parent capable of carrying legacy pain without being consumed by it.

Mobilink, for its part, is not exactly buying from a position of effortless plenty, but it is playing a different game. Mobilink

Microfinance Bank is a nationwide microfinance bank established in 2012 and backed by VEON, with 113 branches and a branchless-banking business launched under the JazzCash brand in November of that year. By the end of 2024, it had an 18% market share by gross loan portfolio, deposits of about Rs155 billion and a capital adequacy ratio of 19.16%, supported by a $15 million capital injection from its parent, with more capital expected. Mobilink itself reported a net loss in 2024 because expected credit losses ballooned to Rs19.9 billion, but its scale, digital rails, sponsor backing and still-compliant capital position make it a very different sort of animal from Apna. It is the kind of institution that can treat a troubled acquisition as consolidation.

The most plausible reading of Apna’s 2025 performance, then, is not that the bank has turned around, but that it has become turnround-able. It has done the basic things a troubled microfinance lender must do: restore positive net interest margins, cut funding costs, shrink the branch network, recover bad loans, pivot to secured lending and stop pretending that unsecured expansion is still available to it. But the scars are too deep for organic recovery alone to look convincing. In a sector where even the official data tell a story of operational improvement coexisting with capital strain, Apna’s results look like an argument for consolidation. Gold may have steadied the loan book. Lower rates may have eased the income statement. Yet neither is likely to be enough on its own. The bank has narrowed its losses. To stop bleeding altogether, it may still need a buyer. n

IGI Life struggles to grow premium revenue in 2025

The company barely grew its topline as Pakistanis slowly turn away from life insurance as a savings vehicle

Life insurers are supposed to flourish on patience. They sell long promises, collect small cheques over many years, and turn household caution into institutional capital. Pakistan in 2025 was not an easy place for that old bargain. IGI Life Insurance’s annual results, released this week, show a company that managed to improve profit without fixing the more awkward problem of demand. Gross premium and contribution revenue

rose to Rs14.10 billion in 2025 from Rs13.49 billion a year earlier, which is growth, but not the kind that looks impressive in a country still emerging from a bruising inflation cycle. More tellingly, total revenue slipped to Rs17.44 billion from Rs17.74 billion. Profit after tax did improve sharply, rising to Rs423.37 million from Rs278.90 million, while earnings per share climbed to Rs2.48 from Rs1.64. For shareholders, that was a better year than the topline alone would suggest. For the industry, it was a reminder that revenue growth remains elusive.

That tension matters because life insurance in Pakistan has long tried to sell itself not merely as protection against misfortune, but as a form of disciplined saving. When that proposition works, insurers gather sticky, long-duration money. When it does not, policyholders either stay away or cash out early. IGI Life’s 2025 numbers suggest the company is caught somewhere in between: large enough to remain profitable, but not growing fast enough to suggest a broad-based revival in retail appetite. The rise in gross premiums was modest, while the fall in total revenue points to a softer contribution from investments and other income streams. In plain English, the company earned more for equity holders, but it did not persuade many more Pakistanis to buy into the life-insurance proposition.

IGI Life was incorporated in October 1994 and operates in both participating and non-participating life business, while also running Shariah-compliant family takaful products through an approved window. It is a subsidiary of IGI Holdings, the Packages Group-linked financial holding company that entered the life-insurance market in 2014 by acquiring the Pakistan operations of MetLife Alico, now IGI Life. That inheritance matters. It means the company came into the market with an established platform, multinational lineage and the backing of one of Pakistan’s better-known corporate groups. In theory, that should have made it one of the better-placed firms to turn life insurance into a broader middle-class product.

Yet the industry around it remains stubbornly underdeveloped. The Competition Commission of Pakistan said in its latest sector assessment that Pakistan’s overall insurance penetration stood at just 0.87% of GDP in 2022, far below regional peers such as India and China, both at about 4%. The same report said the industry is still dominated by stateowned enterprises and that State Life alone holds more than 50% of the life-insurance market. Gallup Pakistan’s survey work paints an even starker picture from the demand side: only 9% of Pakistanis said that they or someone in their household had a life-insurance policy, while 83% said no one in the household

was covered. In other words, the problem is not just competition among insurers. It is that life insurance still occupies only a tiny corner of household finance.

The more revealing shift is in what kind of life-insurance business is still growing. PACRA’s June 2025 research on the sector says individual regular premiums, historically the largest part of the market and the closest thing to a mass-market savings-style product, have been on a downward trend since 2022 as reduced household consumption and weak purchasing power bit into demand. By 2024, individual regular premiums had fallen to about 39.2% of the sector’s premium mix and declined 15.6% year on year. At the same time, group policy premiums had risen to 49.1% of the total. That suggests growth is increasingly coming from employer-led or institutional business rather than from households voluntarily locking themselves into long-term savings commitments. PACRA also notes that surrender claims accounted for 49% of total claims in 2024 and rose 6.5% year on year, another sign that policyholders have been more willing to exit than to stay the course. It is therefore reasonable to infer that Pakistanis are becoming less inclined to treat life insurance as a preferred savings vehicle, especially when household budgets remain tight and other short-term uses of cash feel more urgent.

Seen in that light, IGI Life’s weak premium growth looks less like an isolated stumble and more like a symptom of a wider market transition. The listed life-insurance sector did post strong premium growth in the first half of 2025: Badri Management Consultancy says gross written premiums for listed life insurers rose 33% to Rs79 billion, while net written premiums rose to Rs75 billion from Rs57 billion a year earlier. But profitability still fell, with sector profit dropping to Rs3.2 billion from Rs3.4 billion, largely because investment income declined 26% to Rs36 billion. Badri’s H1 2025 benchmarking ranked IGI Life fourth

among the six listed life insurers by both gross written premium and profit after tax. So the company is neither a leader nor an also-ran. It occupies an uncomfortable middle: meaningful enough to matter, but too small to dictate the market’s direction.

That middle position may be especially awkward in an industry where the old business model is losing some of its shine. For years, life insurers in Pakistan relied on a straightforward pitch: pay steadily now, receive protection plus a savings element later. But high inflation, repeated income shocks and a broader squeeze on household finances have made that promise harder to sell. PACRA explicitly links the decline in individual regular premiums to reduced consumption and low purchasing power, while Gallup’s survey suggests that most households still do not participate in the category at all. IGI Life’s own 2025 results fit that pattern almost too neatly. Premium revenue edged up, but only barely; total revenue fell; profit improved. It was a year of financial resilience, not commercial acceleration.

There is, to be fair, another side to the story. The industry is not dying; it is changing. Badri argues that the next phase of growth will depend on digital ecosystems, more personalised products, better expense control and technology-led underwriting. It also points to growth in takaful and participating life segments as part of a structural shift toward a more balanced market. IGI Life, with its family takaful window and its established corporate backing, is not badly positioned for that transition. But the 2025 numbers suggest that transition is not yet delivering a surge in the kind of premium growth that makes for a convincing growth-stock narrative. For now, IGI Life looks like a company living through the sector’s awkward in-between phase: profitable enough to endure, but still waiting for Pakistanis to rediscover the habit of saving through insurance.

Packages made billions in 2025. The government took almost all of it away in taxes.

The conglomerate faced an extraordinary burden of taxation, in no small part due to the confiscatory taxation in the form of the levies beyond the standard corporate income tax

There are years in which a conglomerate struggles because demand is weak, costs are out of control, or debt has become unmanageable. And then there are years like Packages Ltd’s 2025, when the operating story looks respectable enough, only for the state to arrive at the bottom of the income statement with an outstretched hand. On a consolidated basis, Packages and its subsidiaries generated Rs193.2 billion in revenue, Rs39.5 billion in gross profit and Rs20.9 billion in operating profit. Profit before levy and income tax came to Rs6.30 billion, a notable recovery from Rs1.44 billion a year earlier. Yet after a levy of Rs1.26 billion and income tax of Rs4.79 billion, profit for the year was just Rs260.6m. In other words, the group made billions, and then almost all of it disappeared into Pakistan’s fiscal machinery.

The first part of the story is, in fact, rather healthy. Revenue rose 9.3% in 2025, while

cost of sales and services rose more slowly, allowing gross profit to climb 15.9% to Rs39.46 billion from Rs34.05 billion. That widened the consolidated gross margin to about 20.4% from 19.3% a year earlier. For a manufacturing-heavy group that spans packaging materials, films, paper, inks, starches, pharmaceuticals and real estate, that sort of expansion is meaningful. It suggests that the group was not merely selling more, but selling more profitably at the gross level. Operating profit rose too, though far less dramatically, reaching Rs20.9 billion against Rs19.8 billion in 2024, as higher administrative, marketing and other operating expenses absorbed part of the gain. Finance costs, however, fell sharply to Rs14.6 billion from Rs18.4 billion, helping pre-levy, pre-tax profit more than quadruple year on year.

Then comes the extraordinary part. Packages’ combined levy and income tax bill amounted to Rs6.04 billion, leaving behind only Rs260.6m in consolidated profit. Mea-

sured against profit before levy and income tax, that means roughly 95.9% of what the group earned before the state’s claim was taken away, leaving only about 4.1% behind. The levy alone consumed almost a fifth of pre-levy profit, while income tax consumed about three-quarters. The consolidated accounts therefore tell a striking story: not that Packages failed to earn money in 2025, but that the tax system absorbed nearly all of it. And because non-controlling interests accounted for Rs2.10 billion of the remaining earnings, the amount attributable to owners of the parent company was still a loss of Rs1.84 billion. The group as a whole scraped into the black; the parent’s shareholders did not.

That burden did not appear out of nowhere in the final quarter. In its half-year 2025 report, management had already warned that the surge in levy and income tax was “mainly attributable” to the derecognition of minimum taxes from prior years after the Finance Act

2025 reduced the period for recoupment of minimum taxes from three years to two. That detail matters, because it shows that Packages’ tax problem was not simply the result of one profitable year meeting the ordinary corporate tax code. It was also the product of Pakistan’s more inventive fiscal habits: super taxes, levies, and rule changes that reach back into balance-sheet assumptions companies thought were still usable. By the second half, the effect was fully visible in the annual numbers.

The legal backdrop to that levy is Pakistan’s super-tax regime. Section 4B of the Income Tax Ordinance is explicitly titled “Super tax for rehabilitation of temporarily displaced persons,” while section 4C is titled “Super tax on high earning persons.” Section 4B applies from tax year 2015 onwards; section 4C applies from tax year 2022 onwards. Under the rate schedule in force for tax years 2023, 2024 and 2025, income above Rs500m attracts a 10% super tax under section 4C. In plain English, this is not the ordinary corporate income tax at all. It is an additional fiscal layer, imposed on top of normal taxation, and for large profitable companies it can materially transform what looks like a solid year into a meagre one.

The original political case for the super tax was, at least in theory, temporary and exceptional. As Dawn reported from proceedings before Pakistan’s Federal Constitutional Court, the levy was first imposed in 2015 through a money bill, with the stated purpose of rehabilitating areas affected by the Zarbi-Azb military operation and rebuilding for temporarily displaced persons. What began as a one-off measure for a national emergency, however, has proved to have the institutional durability that emergency taxes so often acquire. Over time it ceased to look like a temporary impost and began to resemble part of the permanent architecture of Pakistani corporate taxation. That is why companies such as Packages can post improving operating numbers and still find themselves with accounts that feel less like a profit statement than a surrender document.

Packages Ltd was established in 1956 as a joint venture between the Ali Group of Pakistan and Akerlund & Rausing of Sweden. It began in folding-carton packaging, integrated upstream in 1968 with a pulp and paper mill based on waste paper and agricultural by-products, launched the Rose Petal tissue brand in 1981, and added flexible packaging capacity in 1986. The company has been listed on the Pakistan Stock Exchange since 1965 and today describes itself as an investment-holding company with stakes in subsidiaries, joint ventures and other companies across a range of sectors. The corporate website still presents the old industrial ambition in straightforward

terms: a Pakistani manufacturing house that kept moving upstream, sideways and abroad as opportunities emerged.

That ambition is now visible in the company’s sprawl. According to Packages’ corporate briefing and company materials, the group includes Packages Convertors, Bulleh Shah Packaging, Tri-Pack Films, DIC Pakistan, Packages Real Estate, Packages Lanka, Hoechst Pakistan, StarchPack and Packages Trading FZCO, alongside other subsidiaries and stakes in joint ventures and investments such as OmyaPack and IGI Holdings. Through those holdings, the group touches folding cartons, flexible packaging, tissue and consumer products, paper and board, corrugated packaging, BOPP and CPP films, printing inks, industrial minerals, starches, medicines, mall real estate, trading and financial services. It is still recognisably a packaging group, but it has become a distinctly Pakistani sort of conglomerate, where the original manufacturing core has thrown off subsidiaries in adjacent sectors, services and geographies.

The recent initiatives tell the same story of diversification and repair. In the 2024-25 period, Packages injected capital and financial support into two wholly owned subsidiaries that plainly needed it: StarchPack and Bulleh Shah Packaging. By mid-2025, the parent had arranged term-finance facilities to back support for both businesses, while its corporate briefing highlighted the capital injections as key announcements of the year. StarchPack, the group’s corn-based starch venture in Kasur, remained loss-making in the first half of 2025, but management said it was pushing towards a more stable second half through a wider portfolio, especially in value-added starches, better production efficiency and tighter corn procurement. Bulleh Shah Packaging, meanwhile, was battling unrestricted imports, an adverse sales mix, and input-cost pressure that it could not fully pass on. These are not vanity projects. They are large industrial bets, and in 2025 the parent company was still visibly carrying them.

Other parts of the empire looked livelier. Packages Trading FZCO, the Dubai-based subsidiary established in 2022 and operational from October 2023, posted turnover of USD29m in 2024 on the company website, while the half-year 2025 report showed firsthalf revenue of AED106m, more than four times the comparable period a year earlier. Management said it expected the unit to provide both export and import synergies for the group over time. DIC Pakistan, the printing-inks business, had successfully relocated and was aiming to commence commercial operations from its new site in Kasur during the third quarter of 2025. Hoechst Pakistan, formerly Sanofi-Aventis Pakistan, continued to be a bright spot, with

half-year 2025 revenue up 22% and profit before levy and income tax up 45%, helped by sales growth, favourable mix and tighter working capital management. Packages, in short, is still investing, still integrating, still reorganising. It is not the picture of a static old industrial family holding company living off dividends and memories.

Then there is the sustainability agenda, which in Packages’ case is no longer mere brochure language. In February 2025, the group said it had installed over 22MW of solar capacity across the group, with another 5MW-plus in the pipeline, and highlighted a 45MW biomass boiler at Bulleh Shah Packaging as one of the largest in Pakistan. By the end of December 2025, during its World Energy Conservation Week campaign, the group was describing 27MW of solar capacity across the group, alongside the biomass boiler, a solvent recovery plant and ISO 50001-related energy-management efforts. This is not just climate branding. For a manufacturing conglomerate operating in Pakistan’s energy environment, renewable and efficiency investments are also a form of margin defence. They are the sort of long-horizon industrial choices that help explain why gross margins could improve even in a difficult macroeconomic setting.

The softer initiatives matter too, if only because they show how Packages wants to think of itself. In November 2025, the company announced that it had been approved by the Institute of Chartered Accountants of Pakistan as a Training Organisation Outside Practice, presenting the accreditation as part of a broader effort to develop young finance professionals. That is not a line item in the financial statements, but it does say something about the group’s self-image: not merely as a cluster of factories and subsidiaries, but as an institution trying to replenish its managerial bench while it keeps expanding into new businesses. Conglomerates endure by training successors as much as by financing plants.

And so Packages ends 2025 with a paradox. At the industrial level, it looks sturdier than the headline profit figure suggests. Revenue is up, gross margins are better, finance costs are lower, and several subsidiaries are either scaling up, being repaired or both. But at the fiscal level, the message is brutal. Pakistan’s tax state managed to turn Rs6.30 billion of profit before levy and income tax into just Rs260.6 million of profit for the year. That is the sort of outcome that makes even a growing conglomerate look anaemic. The trouble with confiscatory taxation is not simply that it takes money away. It also distorts the story a company’s accounts are trying to tell. In Packages’ case, the underlying story in 2025 was one of industrial resilience. The reported one was that the government got there first.n

KSB Pumps sees increases sales, even as some customers cannot afford to pay

The company’s revenue went up, but so did losses associated with customers buying on credit and then being unable to pay, causing a decline in operating profits

There are, in corporate life, few things more frustrating than doing the hard part well and still watching the reward leak away elsewhere. KSB Pumps Company Ltd’s results for 2025 have precisely that flavour. The Lahore-based engineering manufacturer sold more, produced a fatter gross profit, and still ended up with a weaker operating performance because the accounts were hit by a sharp deterioration in trade-debt impairment. Yet by the time the numbers reached the bottom line, the picture had brightened again: lower finance costs helped lift profit for the year to Rs210 million from Rs56 million, and the board recommended a final cash dividend of Re1 per share. In other words, KSB’s year was neither cleanly triumphant nor plainly disappointing. It was a reminder that for industrial firms in Pakistan, a stronger order book is only the beginning of the story; getting paid remains an altogether different test.

Start with the part management would most happily place near the top of the page. Revenue from contracts with customers rose to Rs6.58 billion in 2025, up about 14% from Rs5.78 billion a year earlier. Cost of sales also increased, but more slowly than revenue,

allowing gross profit to climb to Rs1.57 billion from Rs1.18 billion. That pushed gross margin up to about 23.8%, from roughly 20.5% in 2024. For a company that sells into capital-intensive, price-sensitive sectors, that is not a trivial change. It suggests a more favourable sales mix, better absorption of factory overheads, or at the very least a year in which volumes grew faster than the underlying cost burden. Earlier company materials had already pointed to stronger order intake through 2025, with management saying that by the first nine months of the year sales had risen 25.1% and gross profit 47.4%, while order intake and order in hand were also ahead of the previous year. The broad contour of the final accounts therefore did not come out of nowhere.

But the middle of the income statement tells a harsher story. KSB booked a net impairment loss on trade debts of Rs268 million in 2025. In 2024, by contrast, the same line showed a gain of Rs32 million. That is not merely a deterioration; it is a swing of roughly Rs299 million against earnings. On an operating margin basis, the business moved from about 5.25% of sales to just 2.48%. For a company selling pumps, valves, castings and services into a country where public projects, industrial customers and long-credit commer-

cial relationships often define the rhythm of cash collection, the lesson is familiar. A good sales year can still become a poor operating year when receivables begin to look doubtful. The filing does not identify which customers drove the impairment charge, but it leaves no doubt about the direction of travel.

And yet the bottom line improved sharply. That apparent contradiction becomes easier to understand once finance costs come into view. KSB’s finance costs collapsed to Rs20.3 million in 2025 from Rs295 million a year earlier, a drop of more than 93%. Profit before levy and taxation consequently rose to Rs278 million from Rs143 million, while profit before taxation increased to Rs251 million from Rs94 million. The explanation lies partly in capital structure. In its 2024 annual report, the company’s chairman said the right issue backed by the parent group had helped pay off debt and ease the burden of interest payments to banks. The statement of changes in equity confirms that the 2024 rights issue brought in Rs1,947 million. If 2025 was the year when receivables bruised the income statement, it was also the year when last year’s balance-sheet repair began to pay off.

That healthier financing profile did not mean the company spent the year standing

still. Fixed capital expenditure including capital work in progress surged to Rs330 million in 2025, far above the Rs90 million spent in 2024. KSB is not behaving like a company merely harvesting an old franchise; it is still putting money into plant and capacity. The more interesting question, then, is not whether demand exists. The results already imply that it does. The question is whether management can convert that demand into cash earnings without allowing credit losses to devour the operating gains.

KSB Pakistan was incorporated in 1959 and, by the parent group’s own telling, was KSB’s first subsidiary in Asia. Its origins lie even earlier, in a 1953 joint venture with Batala Engineering Co. Ltd. The standalone Pakistani company began on rented premises in Lahore in 1960, before a purpose-built factory in Hassanabdal started operations in 1964. In its early decades the plant focused on irrigation pumps, later broadening into equipment for power plants and for industries such as sugar, paper and cotton processing. In 1979 the company set up its own foundry in Pakistan and listed on the Lahore and Karachi stock exchanges, even as the German parent retained majority control. This is not a newcomer dressed up as an engineering old hand. It really is an old hand.

That long presence helps explain both KSB’s market standing and its slightly unusual shape. The company is not just a seller of imported equipment. Official company materials emphasise that KSB Pakistan combines manufacturing, sales and marketing, and service under one roof. It has its head office in Lahore, a production site in Hassanabdal, regional sales offices in Lahore, Karachi, Multan and Rawalpindi, and service workshops in Karachi, Lahore and Hassanabdal, in addition to a network of authorised partners and dealers. On the Pakistan Stock Exchange profile, the company is described as principally engaged in the manufacture and sale of industrial pumps, valves, castings and related parts, along with after-market services. That breadth matters in Pakistan, where customers often want not merely a pump, but a supplier who can install, repair, overhaul, re-engineer, and keep the thing running when imported spares become expensive or slow to arrive.

The company’s current positioning reflects that full-stack ambition. KSB Pakistan says it serves six main market areas: general industry, mining, energy, building services, petrochemicals and chemicals, and water. A recent corporate briefing described a product portfolio ranging from standard pumps such as Etanorm to KWP, Sewatec WKL, RPH and OMEGA lines, as well as motors, fire-fighting pumps, submersibles, filtration plants and sewage-treatment-related offerings. At its manufacturing facility, the company says it has

pump capacity of 5,500 units a year and foundry capacity of 10,000 tonnes per annum. Those figures do not make KSB a giant by the standards of global industrial manufacturing. But in Pakistan they do help to explain why the company has remained a durable name in a niche that is at once technical, cyclical and indispensable. Water has to move. Factories have to circulate fluids. Buildings need pressure systems. Wastewater has to be treated. Someone, eventually, has to supply the machinery for all of that.

Recent management initiatives suggest the company is trying to modernise without losing the practical advantages of its local footprint. In its 2024 annual report, KSB said it was transitioning from SAP ECC to SAP S/4HANA alongside the wider KSB Group, with the aim of integrating global best practices. It also highlighted “Mission T30”, an internal ambition to double revenues by 2030 through expansion across market areas while defending share in competitive segments. Management described a reworked organisation built around a customer-facing front end, a product-delivery back end, and shared services supporting both. At the same time, the company has kept pushing its aftermarket business, SupremeServ, and its reverse-engineering capabilities for non-KSB pumps. It also completed an 850KW solar expansion phase, continued energy-conservation projects and said it was working towards ISO 50001 certification. The common thread is clear enough: digitise, broaden the service mix, deepen technical capability, and lower the energy bill where possible.

That strategy has a distinctly Pakistani logic. In richer markets, an engineering company might live comfortably on fresh equipment sales alone. In Pakistan, customers often need far more hand-holding, improvisation and after-sales support. KSB’s reverse-engineering business, especially for non-KSB pumps, sits squarely in that reality. The company said in its annual report that SupremeServ had a strong 2024, particularly in spare parts sales to the oil and gas sector, and that reverse engineering remained a key driver of success, including in the EMEA region. Management also said its extended service-workshop network was meant to support authorised partners and improve service for standard and mid-sized products. Meanwhile, the chief commercial officer’s remit now explicitly spans pumps and valves, SupremeServ, product management, exports and strategic marketing. That is less the structure of a company waiting for customers to come to it than of one trying to attack the market from multiple angles at once.

The pipeline, at least on paper, still looks encouraging. In the corporate briefing released in late 2025, KSB reported order intake of Rs6.22 billion for the first nine months of the

year, up 18.6%, with order in hand of Rs4.14 billion, also ahead of the year before. Management’s outlook for 2025-26 pointed to stronger public-sector development spending, especially from the Punjab government in water and wastewater infrastructure, while stabilising interest rates were expected to help industrial and manufacturing activity. The company also flagged export wins in Australia, Chile, Saudi Arabia, Germany and parts of the Americas. Earlier company guidance had already singled out ADB- and PSDP-funded public-health and WASA projects as priorities, while anticipating growth in steel, sugar and fertiliser revamps and expansions. For a company that sells into the plumbing of an economy rather than into its glamorous consumer face, these are the sorts of signals that matter most.

The end markets KSB serves help explain both the opportunities and the risks in its accounts. Water remains a core revenue driver, according to the annual report, and Pakistan’s chronic need for filtration, pumping, distribution and wastewater infrastructure gives that market a natural durability. The company also sells into petrochemicals, general industry, building services and energy, while its foundry has exposure to automotive components as well. That diversification is useful because Pakistan’s industrial cycle rarely moves in a straight line. When one sector slows, another sometimes revives. But diversification does not eliminate country risk. Public projects can be delayed. Industrial customers can suffer cash squeezes. Imported input costs can move with the currency. And credit discipline can weaken precisely when companies are most eager to book sales. KSB’s 2025 results are therefore a tidy summary of Pakistan’s industrial promise and its perennial irritants: there is demand for hard engineering, but the path from invoice to cash can still be uncomfortably long.

In that sense, the year may be read less as a muddle than as a test of sequencing. KSB has already shown that it can raise sales, expand gross profit, reduce borrowing costs, invest in capacity, build its service franchise and maintain a credible pipeline into sectors that Pakistan cannot do without. What it has not yet shown—at least not in the 2025 numbers—is that all of those improvements can arrive at the same time without being interrupted by bad debts and shaky collections. That makes KSB an unusually revealing company to watch. It sits at the intersection of infrastructure, industry, exports and after-sales services; it is local enough to feel Pakistan’s economic frictions, and international enough to try to manage around them. The latest results suggest the franchise is strengthening. They also suggest that in Pakistan’s engineering business, profit is not just about making pumps. It is about making customers pay for them on time. n

How far can increased financing to build homes go in Pakistan?

The government’s “Mera Ghar, Mera Ashiana” scheme now offers financing up to Rs 1 crore with a subsidised markup rate for the first 10 years of the loan. However, structural problems continue to plague Pakistan’s housing market

Ahouse of one’s own remains a luxury in Pakistan. According to some estimates, the housing shortfall stands at around 10 million units, with around 350,000 additional units being added each year. Given that housing remains a cornerstone of Pakistan’s economy, closely tied to indicators such as inflation, this is a big problem. This is more so for a population that stands at over 24 crores.

The government recently announced a scheme to facilitate prospective homeowners in making a home for themselves. This financing scheme, called ‘Mera Ghar; Mera Ashiana’ was introduced in September 2025, where it stipulated loans at fixed markup rates for those looking to buy or construct their first houses. It was a tiered system with rates of interest depending on the size of the loan. The financing was limited to a maximum of Rs 35 lacs.

Less than six months later, the government has expanded the scope of the scheme, enlarging the available financing to Rs 1 crore as well as a uniform mark-up rate for

loan amounts across the board, removing the tiered system. The loans, in continuation of the original scheme, would be available for a period of up to 20 years, of which for the first 10 years the markup rates would be subsidized by the government.

For a country with rising inflation levels and very high poverty rates, such measures are more than simply welcome; they are necessary. The availability of a house to sleep in and protect oneself against the elements remains not only a core economic prerogative, but is also one of our most human requirements. Such schemes would therefore aid the expansion of the opportunity to own a house to more people than would have been able to afford it otherwise.

Yet such schemes might not be sufficient on their own to really make a substantial difference. Pakistan’s housing market suffers from certain limitations which schemes like the ‘Mera Ghar; Mera Ashiana’ might not be able to undo the effect of on their own. The situation of Pakistan’s housing market and the role of formal financing in it has been limited by a number of issues including recovery for

banks and access for potential clients.

As Zafar Masood, Chairman of the Pakistan Banks Association, pointed out in a recent article, not only is the vast majority of housing financing done through informal channels, institutional and social attitudes towards enforcements also hinder the growth and widespread acceptance of such financing mechanisms. Similarly, the absence of ‘patient capital’ exposes people who have taken out loans to great volatility in interest rates, eroding their ability to sustain their everydays. Unless measures are taken to increase the penetration of formal financing, such schemes on their own might not live up to their promise.

The Scheme and the Update

In September 2025, the federal government announced the commencement of the ‘Mera Ghar; Mera Ashiana’ scheme. It was instituted as a measure to promote affordable housing by providing subsidized mark-up rates.

This was done in light of rising property prices in Pakistan, which since the Covid had rushed to mountainish heights. While the real value of housing prices had fallen to -14 percent in December 2020, these rose sharply afterwards, reaching a peak of 30 percent increase by October 2025. With largely stagnant per capita incomes, economic uncertainty, and the consequent slowdown in economic activity in the middle, avenues for purchasing houses kept slipping out of the reach of the many.

It was in this context that the ‘Mera Ghar; Mera Ashiana’ scheme was announced. Only people who were first time owners or had no housing unit (house, flat, apartments etc.) in their name were eligible to apply. The scheme covered financing for three main types of house-making: purchasing a housing unit, constructing new units on already owned land, and purchasing and constructing on a piece of land.