08 Qatar wants to buy more rice from Pakistan. It might cost us in the long run

12 Why the Packages’ bid to buy Akzo Nobel fell through, and what comes next

19 JS Group’s headquarters comes to market as a sale-leaseback REIT

20 Farm recovery leads fertiliser sector profits to surge 10%

23 With new IPO, Pakistani investors get access to the supplier of the eggs in McDonald’s Egg McMuffins

25 Air Link to separately list manufacturing subsidiary in IPO

27 Who won Pakistan’s 5G auction?

30 Where does Thar Coal fit into Pakistan’s energy independence pipe dream?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Usama Liaqat Shahab Omer | Zain Naeem | Nisma Riaz | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing: Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Qatar wants to buy more rice from Pakistan. It might cost us in the long run.

Armed with solar-powered tubewells, Pakistani farmers are growing rice indiscriminately with export prices in mind. A more level-headed strategy is desperately needed

Qatar is interested in importing more Pakistani rice. The expression of interest was made by Qatar’s Minister of State for Foreign Trade Affairs, Dr Ahmad bin Mohammed Al Sayed, during a meeting with Commerce Minister Jam Kamal.

The Qatari Minister said that rice remains an important part of Qatar’s national food strategy and food security programme, and therefore more rice from Pakistan would

contribute positively to their national aims.

Qatar’s desire to buy rice from Pakistan is part of growing demand from the Gulf, Africa, and Central Asia for Pakistani grain. The demand for Pakistani rice has been increasing on the back of Indian rice flooding international markets which has brought rice prices down. To supply this international (as well as growing local) demand, farmers have been growing more non-Basmati varieties..

In order to cultivate more rice, farmers have been planting rice on lands traditionally

reserved for other crops such as cotton. This shift is bolstered by the increased availability of solar energy, whereby farmers can pull water from tubewells much more than before, and can easily grow more rice.

In the short term this might bring in more revenue from exports, but it is not a sustainable strategy and might have potentially difficult consequences down the line, given what we know about Pakistan’s vulnerability to the climate change crises.

More Rice Going Out

In January 2026, it was reported that Pakistan had crossed Vietnam to become the third largest exporter of rice in the world, behind India and Thailand. In December 2025, Pakistan had exported 4.89 lakh tonnes of rice whereas Vietnam had exported a lower 3.87 lakh tonnes.

The apparent reason behind this is the fact that rice is being grown on more land. According to Faisal Jahangir, Chairman of the Rice Exporters Association of Pakistan (REAP), the overall rice cultivation area has increased by 20% compared to last year. This has enabled rice farmers to offset losses from the floods last year, ensuring the production numbers continue to rise.

Yet this increase is really the increase in the production of non-Basmati varieties of rice. The reason is that traditional Basmati quality is dependent on certain ecological and climatic conditions, which is available only in certain areas of Punjab and India. In Punjab, this region is referred to as the ‘kallar tract,’ an expanse of land between the Ravi and Chenab rivers which includes centres such as Gujranwala, Sialkot, Sheikhupura, and Hafizabad.

Growth in production of rice, therefore, is powered by bringing more land traditionally reserved for other crops under rice cultivation. The problem with this is that non-Basmati varieties consume more water than Basmati. This demand is satisfied through increased tapping into irrigation water, which itself has seen a decrease owing to sedimentation within dams.

A big source of this water is through tubewells, and tubewells require electricity to pull the water up and out. Traditionally, farmers had relied upon diesel and grid power to make these tubewells work. However, recently with the increased availability and access to solar panels and installations, farmers have been ditching traditional sources of power for solar, with the result being that cultivating rice has become much more feasible for farmers.

According to one estimate, some 4 lakh tube wells that once relied on grid electricity have switched to solar. Farmers using solar panels have likely purchased an additional 250,000 tube wells since 2023, signalling that the sun now powers roughly 6.5 lakh such devices across Pakistan. So, they can grow – and have been growing – more of it. And exporting more of it too.

A big factor in the rising rice exports has also been Pakistan’s pivot to more markets, including the Middle East and Central Asia. Dubai remains the top destination of Pakistani rice, with the UAE importing 74,897 tonnes, including 16,850 tonnes of Basmati, from Pakistan in December 2025. Saudi Arabia, too, was a major importer of Pakistani rice, importing 16,032 tonnes in the same month, of which 5,350 was

Banaspati. The recent understanding between Pakistan and Qatar for more imports of Pakistani rice falls squarely into this category.

Central Asia has also emerged as a rising market for Pakistani exports of rice with shipments to Kazakhstan totalling more than 17,000 tonnes, and to Uzbekistan over 10,000 tonnes. Although exporters remain wary of such reports, a major exporter from Karachi revealed to Profit that the reason behind this is that such markets cannot usually tell the difference between Basmati and Basmati-seeming non-Basmati rice.

What’s the Issue, then?

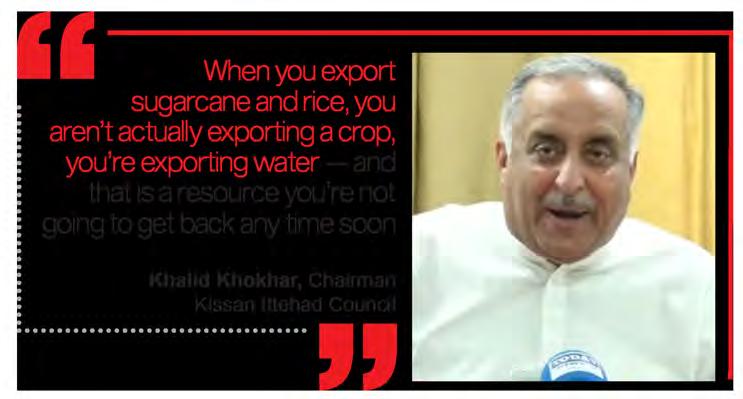

If the increase in rice cultivation area is viewed in conjunction with the increased usage of water, this becomes a more concerning situation. Cotton farmers especially take great exception to this trend, with reasonable reasons. As Khalid Khokhar, the Chairman of the Kissan Ittehad, which is Pakistan’s largest advocacy collective for farmers, put it, “When you export crops like rice and sugarcane, you are not exporting the crops, you are exporting water.”

The total expected production of rice this year is around 1.1 crore metric tons. With the Pakistan Bureau of Statistics estimating domestic consumption at 20-25 lakh metric tonnes, that leaves Pakistan with a surplus of around 80 lakh metric tons that can be exported. This would be a significant increase from exports in FY 202425, which totalled 58 lakh mt, a 3.5% decline compared to FY 2023-24. If we take Khalid Khokhar’s word for it, it is just so much water that’s going out that won’t be coming back in.

Another issue is that the issue is caused, as it often happens, by other issues. Basmati seed has not seen as much government investment in research and development as have the seeds of other varieties. Since the 1960s, when the Kernal Basmati was developed, the development of newer Basmati strains has not seen much advance, with varieties of non-Basmati seeds

like Japonica and Kainat taking up more of the farmers’ interest. Although Basmati is more expensive, and can therefore fetch higher prices, farmers turn towards these other varieties because producing them is easier and less time-consuming. This means that they have time for another crop before the next season starts. This situation can continue as it is, sure. There will be revenue from exports, true, and probably an increase in that. Our point, however, is that there is much more potential in Pakistani rice that this current situation permits one to capitalise on. India, in this regard, offers a positive model. Its Basmati varieties, led by widespread integrated marketing campaigns, have taken the American and European markets by the storm. These are premium markets with high demand for Basmati rice, which means that one can earn more value by adding comparatively little.

Branding, quality control, and supply chain strengthening would be required, and this is where the government can play a part. For instance, marketing Pakistani basmati in international trade fairs and instituting government-level trade agreements. This must, however, be supplemented by greater investment in the development of newer strains of the Basmati rice. Ideally, this would lead to the creation of Basmati strains that aren’t bound by certain ecological conditions to grow meaningfully. At the same time, if such varieties are promoted by the government, farmers who had abandoned Basmati for other crops – even in the ‘kallar tract’ would have incentive enough to turn back to Basmati.

In that context, an agreement to supply more rice, for instance, to Qatar would be a greater grounds for celebration. As it is, however, the varieties likely to be exported would include Basmati-seeming varieties, which, for reasons explained above, would allow for less value addition, eroding margins, and also adversely affect Pakistan’s exposure to the looming climate crisis. n

WHY THE BID TO BUY FELL

Profit Investigations

Syed Hyder Ali, the head of the Packages Group and the heir to Syed Babar Ali, wanted to buy Akzo Nobel Pakistan. Multiple sources told Profit he was advised against it from the outset. A number of senior leaders and advisors of the Packages Group had expressed apprehensions regarding the acquisition, saying it was not a good fit for the group.

THROUGH, AND WHAT

COMES NEXT PACKAGES’ AKZO NOBEL

Akzo Nobel is exiting Pakistan as a once proud business finds itself in the doldrums. Despite the many business problems, there is still a lot that the paint manufacturer can offer a potential buyer

It did not matter. In October 2025, IGI Holdings, the investment arm of the Packages Group and Syed Babar Ali family, informed the stock exchange that its subsidiary, IGI Investments, had approved the acquisition pending due diligence. An initial figure for the sale was also discussed privately between the two parties. Packages and Akzo Nobel naturally declined to comment on what this figure was considering the deal has still not reached an official conclusion. However, a senior executive of a different paint manufacturing company told Profit the figure circulating in the industry was Rs16 billion — including all of Akzo Nobel’s real estate assets.

Nearly six months later that deal is on the verge of falling through. The initial amount discussed, it seems, did not stand up to the scrutiny of the due diligence team, and the Packages Group revised the offer downwards by as much as 40%. Since then, there has been complete silence from the parties involved. No official statement has been made by either company or notification given to the PSX, which means a time-of-death has not officially been called. Profit reached out to Syed Hyder Ali, other representatives of the Packages Group, their communications team and other office bearers. After some back and forth it was clarified that they did not intend to comment on the matter.

For Akzo Nobel, this marks another moment of crisis and reflection in a decade where they have faced set back after set back. The Dutch paint manufacturer has been reconsidering its position in Pakistan since at least 2020, when it delisted from the Pakistan Stock Exchange (PSX). While Akzo Nobel’s financial performance was publicly available so long as it was traded on the stock exchange, there has been radio silence in terms of how it has performed in the years since. Profit gained access to Akzo Nobel’s accounts after it was delisted, and the highlight numbers do not paint a pretty picture. It is a story of margins tanking, volumes in tailspin, and a shrinking market share: essentially nothing to inspire confidence in a potential buyer.

But that does not mean the company has nothing to offer. It is, for starters, one of the most historic companies in Pakistan. What is today Akzo Nobel Pakistan was once the consumer facing division of the grand old British era Imperial Chemical Company (ICI). For the Indian subcontinent, the ICI name represented the heights of colonial corporate ambition. It was, for

much of its history, the largest manufacturer in Britain. It was formed in 1926 as the result of the merger of four of Britain’s leading chemical companies — the very same year that Syed Babar Ali was born. At the time, Syed Babar Ali’s father, Syed Maratib Ali, was an up and coming businessman who was a top contractor of the British Indian Army. For his grandson to one day buy what was once the Empire’s Corporate Jewel would mark a magnificent moment in the storied history of both the family and Pakistan’s corporate history.

That taste for legacy and the prestige of the ICI name still exists in Pakistan. Consider this: Akzo Nobel’s entry into Pakistan had been because the Dutch company had acquired ICI Global in 2008 and the Pakistan business came as part of the package along with ICI’s presence in the rest of the world. Since Akzo Nobel was a paint company and ICI had many other lines of business, Akzo decided to divide ICI and sell some parts of it.

In 2009 Akzo Nobel sold the Pure Terephthalic Acid (PTA) business and the associated facility at Port Qasim, the only one of its kind, to South Korea’s Lotte Chemicals. Last year Lotte Pakistan was purchased by AsiaPak Investments, the company operated by Shaheryar Chishty, who also owns K-Electric, Daewoo Pakistan, and has interests in Thar Coal.

Similarly, ICI’s chemical business was sold in 2012 to the Yunus Brothers Group, owned by the Tabba family. The family’s biggest asset historically has been Lucky Cement. The Yunus Brothers Group bought a 75% share in the business for $152 million at a premium of nearly 30%, showing how coveted the business was. The Yunus Brothers Group decided to retain the name “ICI Pakistan” for the business they had bought.

But who will buy this last vestige of what was once ICI now? IGI Investments is not officially out of the running for Akzo Nobel, but with the sale on the verge of collapse, a few contenders might emerge. There is the possibility of another paint manufacturer entering the fray to try and expand their footprint and ac-

We

do

not comment on market rumors

Joost Ruempol, head of reputation management at Akzo Nobel N.V.

quire a well known brand. Then there are other investors who are also interested and starting to do their homework.

The ICI name and in particular its flagship paint brand Dulux still hold value in Pakistan. Of course a brand name and the power of legacy is not the only thing that makes buyers interested. Another significant feature that will be attractive for potential buyers is the prime real estate property owned by Akzo Nobel on Lahore’s Ferozpur Road right outside Model Town. At the end of the day it will come down to the numbers. A buyer might consider the possibility that even if the paint business is a dead end, the property that comes as part of Akzo Nobel might be able to turn the profit. But the question remains: could this be a case of flogging a dead horse?

The once mighty ICI

Perhaps nothing paints a better picture of the state of Akzo Nobel Pakistan than a brief comparison with Akzo Nobel India. At the time of partition, ICI was split between ICI India and ICI Pakistan. The Pakistani side of the border had the soda ash and chemical business while India inherited the paint business including the famous Dulux brand.

However, ICI Pakistan acquired Fuller Paints in 1960 and began manufacturing Dulux in Pakistan as well and ICI Pakistan was as much a paint company as it was a chemicals or soda ash company.

When Akzo Nobel acquired ICI in 2008, they entered both the Indian and Pakistani market. In 2024 Akzo Nobel International decided

to restructure its corporate structure in 2024 in order to focus and make the business more efficient. In line with this, it decided to sell off its businesses in both India and Pakistan.

The Indian company sold quickly.

JSW Paints bought 74.76% of Akzo Nobel India for a deal valued at €1.4 billion in June 2025. This is being called one of the largest transactions ever in the Indian paint industry. Up until December 2025, 60.76% of the stake had been bought from Akzo Nobel N.V., Akzo Nobel Coatings International B.V. and Imperial Chemicals Industries Limited. Based on the value of the transaction, the per share value of the agreement comes to around ₹2,762.05 per share. This gives an EBITDA multiple of around 25 times.

The high valuation that was given was based on the fact that Akzo Nobel India showed revenues of ₹40.9 billion (Rs123 billion) with net profit of ₹4.3 billion (Rs13 billion) for the year 2025 before the sale was carried out. In terms of growth, the company was seeing more than 3% growth per year and profits were also increasing. With a net margin of more than 10% being maintained, the company was also giving out healthy dividends.

The acquisition will make JSW the fourth largest paint company in the region, competing with the likes of Asian Paints, Berger Paints and Kansai Nerolac.

The story in Pakistan is strikingly different. The entire paint market is valued at around

$414 million which translates to around Rs116 billion. From this, almost two thirds is catered to by the informal sector which means only a third of this is catered to by the organized sector. Overall sales of Rs40 billion are split between leading players of the industry namely Akzo Nobel, Berger Paints, Nippon, and Kansai as the international companies and Brighto, Diamond, Master, and Gobis being some of the local producers. Due to the high amount of competition, the gross margin for the industry averages at 21% and net margin stands at 3% compared to India’s 10%.

Peaking under the hood

But what made Akzo Nobel in Pakistan lag so far behind its Indian counterpart? There was a time, at least in the beginning, where Akzo Nobel was thriving in Pakistan. It was once considered the peak in the corporate world of Lahore with Management Trainee Officer (MTO) candidates enrolling to become part of the company. When the company used to visit the campuses, students would line up and sit through the grueling interviews just to have a shot at the coveted seat.

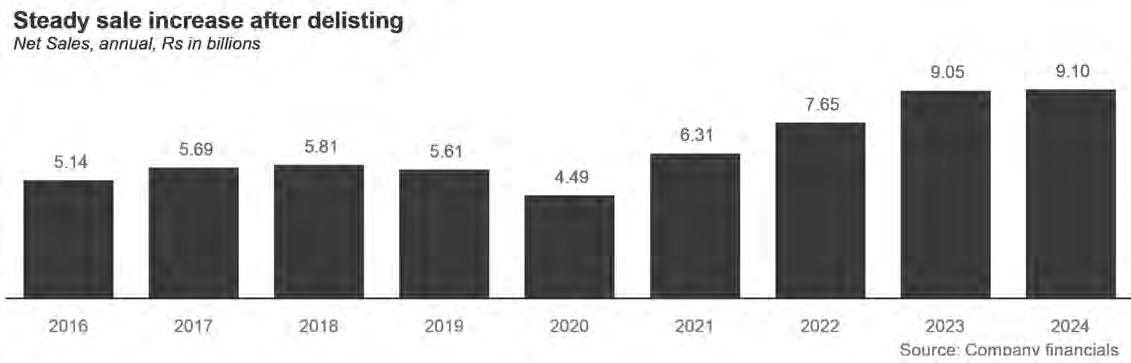

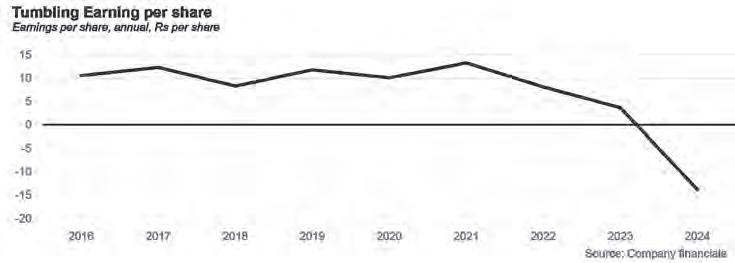

In 2016, Akzo Nobel Pakistan was able to earn net revenues of Rs5.1 billion leading to gross profit of Rs2.1 billion and net profit of Rs77 crores. This translated to an earning per share of Rs10.57 as the company saw gross margins of 42%, and operating margins of 13%. These numbers are similar to the ones observed in India.

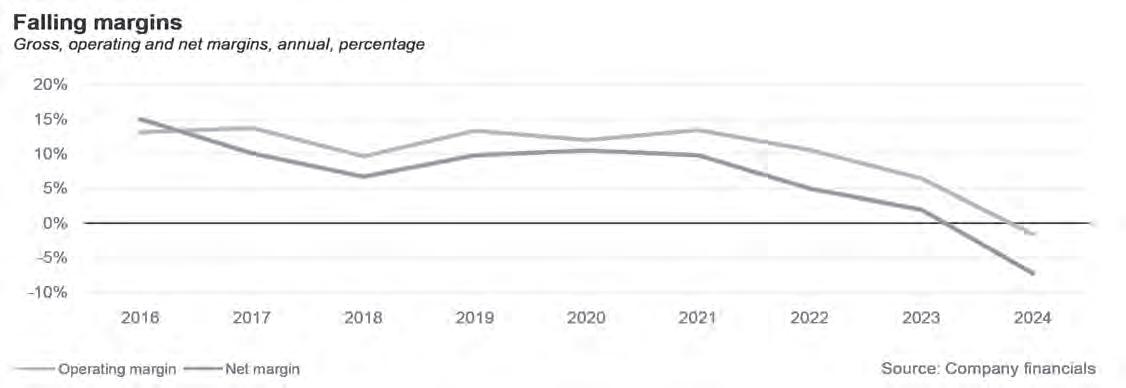

Then things got messy. So messy that all the paint in the world could not white wash the changing nature of Pakistan’s paint market. From 2016 to 2020, sales fluctuated between Rs4.5 billion to Rs5.8 billion. The concerning part for the company was that regardless of sales increasing, the gross profit margin consistently shrank from 42.5% in 2016 to 34% in 2020. This was mirrored by operating margins which de-

creased from 13% to 12% and net margin which went from 15% to 10.5% in 2020.

This was around the time when Pakistan was experiencing a construction boom. The worst of the after effects of the post-Musharraf economic crisis had passed and new life was breathed into the economy. Interest rates were low and so were fuel prices off the back of international stability. To cater to a lot of this demand, a number of smaller, informal paint manufacturers began to emerge in Pakistan.

This informal sector moved fast, it grew in bursts in smaller areas, and it competed hard on prices. For starters, these local players were not bound to international quality standards. They used their own mix of chemicals which do not follow the strict code of ingredients required for manufacturing. This also made them immune to any changes in the prices of the inputs being imported by the international companies and to any weakening of the rupee. Because the sector is so vastly unregulated, it did not matter that their paint often did not meet safety standards let alone quality standards.

These companies also established direct relationships with small distributors. While Akzo Nobel might have had the suited and booted MBAs working on strategy, the owners of these smaller companies were spending time at these distribution points themselves. It is also difficult to overstate the role that the “token” system played in this. As Profit has covered in earlier stories, paint manufacturers began placing tokens worth a certain amount of money in paint boxes. Because of cheap labour in Pakistan, painters often buy material themselves and add it to the cost of a paint job. These painters could redeem the tokens inside for money and thus began buying the brands that would give them the biggest tokens. Essentially, these companies were offering painters a bribe to work with their paint. By some estimates, the informal sector has grown to have 64% of the market share, while Akzo Nobel and other international brands have the remaining third of the market share.

The token system has been covered by Profit in the past as well.

According to Farooq Amin Sufi of Master Paints, Akzo Nobel suffered especially hard from the token system because they did not go all in. “Dulux used to be the only paint company other than Master Paints that did not use tokens, but then around a decade or so ago they also started putting tokens in their paint,” he explains. “The problem was they did not match their tokens to the local companies. Then there came a time when their volumes suffered immensely.”

He went on to explain that Akzo Nobel started using tokens until the MNC’s international bosses put an end to the practice. “When they reviewed the accounts of Akzo Nobel Pakistan they saw a massive expense under marketing for the tokens and told the Pakistan office to stop doing it. When the next quarterly result came there were serious losses, and when the international headquarters asked the local company said this was the nature of the Pakistani market — and they are right it is. We suffer losses because of it as well.”

Master Paints claims they are the only company that has never compromised on tokens. However, as a result they have branded their paint as the “no token” variety and have used this distinction heavily in their marketing campaigns and focused on making customers more aware. Because Akzo Nobel first placed tokens, did not compete on token value with local companies, and then also removed them they still had that taint. All of these bad decisions compounded.

Companies like Akzo Nobel and Master were not able to compete on price. Not only were their inputs more expensive, being in the documented sector meant they had to pay taxes while their new competitors could skate them away. Their response was to push themselves as a quality product, which required further investment and more imported pigments and other inputs. This naturally increased their costs and their margins narrowed.

This was perhaps one of the factors that

led to Akzo Nobel delisting from the PSX in 2020. Since then, details of the company’s performance remained under wraps. The company attempted to continue expanding, even inaugurating a major production facility in Faisalabad worth more than Rs7.5 billion in 2024. The new site would be used to produce decorative paints for automotives, specialty and protective coatings.

“Our investment in this greenfield site reaffirms our commitment to grow in Pakistan. It will fuel our ambition to diversify with sustainable innovations and enter new segments in the domestic market, while also providing new opportunities to delight customers beyond Pakistan,” stated Mubbasher Omar, CEO of Akzo Nobel Pakistan Limited speaking to the media at the inauguration of the new plant.

But then came Akzo Nobel International’s decision to restructure the corporate sector. Before Akzo Nobel had the chance to make this new facility work it was up for sale. Unlike in India, however, this was coming at a time when the Pakistani company was in the doldrums. Akzo Nobel’s financial statements since 2020, analysed by Profit, show the problem of shrinking margin had only grown.

While the company recorded more sales, reaching Rs6.3 billion in 2021, then Rs7.7 billion in 2022, Rs9 billion in 2023, and Rs9.1 billion in 2024, this was mainly the effect of inflation.

Gross margin fell from 34% in 2020 to 20.9% in 2024. The operating margin shrank from 12% to -16% and net margins fell from

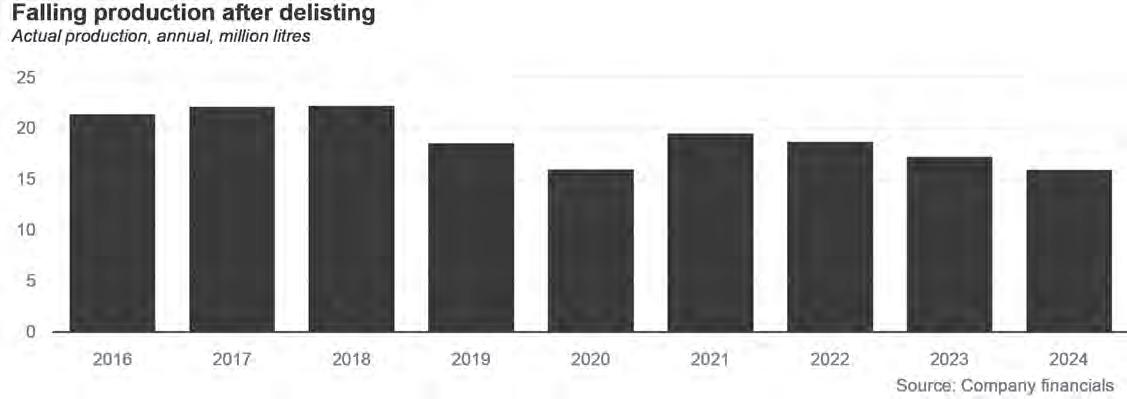

10.5% to -7.3%. While the exact volume data of sales is not given, the annual production of the company can be used which showed that the company produced 21 million litres of paint in 2016 which reached 18.5 million litres by the end of 2019. The production for 2020 can be considered an outlier due to the pandemic taking place where actual production was only 16 million litres. After the recovery was seen in 2021 with production reaching 19.5 million litres being produced, Akzo has seen production fall to 16 million litres of paint being manufactured in 2024 as people (and more importantly the painters) increasingly preferred cheaper local alternatives

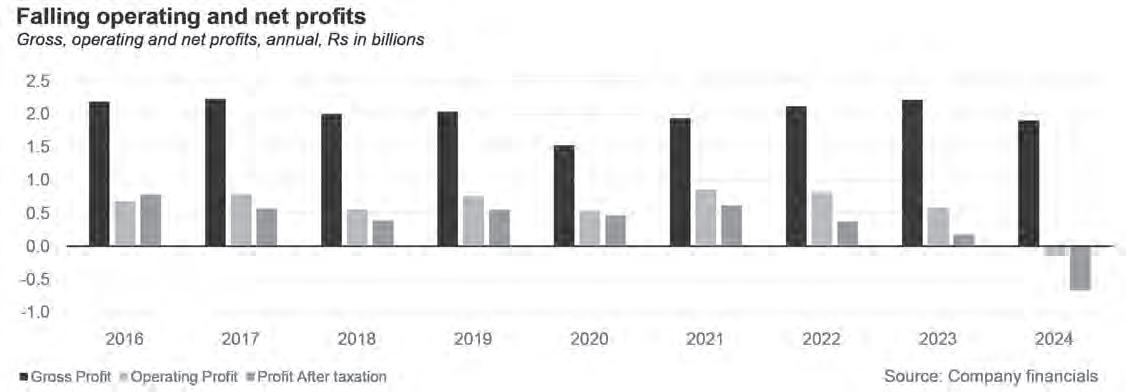

The gross profit earned by the company was only Rs1.9 billion and the company actually made an operating and net loss of Rs15 crore and Rs66 crores respectively. The situation was so bad that the loss per share made by the company was Rs-13.77 per share for 2024.

The effects were not limited to the company’s financial statements. Once the darling of MBAs and young grads from Lahore, their offices today paint a gloomy picture. Their MTO programme is unable to compete with other MNCs and they pay their trainees around Rs90,000 a month. Cost cutting is the name of the day. It is a vicious cycle that many companies go through. A crisis forces the management to cut costs and they immediately go for the jugular: the workforce. Talented workers leave, their positions are either not filled or multiple roles are given to a single person, and less

competent workers replace them. The organisation’s collective brainpower and ability to solve problems goes down dramatically.

And all this while with every passing year production was becoming costlier and less profitable over time. With the added pressures of no profit repatriation to the foreign owners and import controls being placed by the government, the best solution for Akzo Nobel N.V. was to sell its subsidiary.

Why buy Akzo Nobel?

As a paint manufacturer, Akzo Nobel Pakistan is in the dumps. With gross margins this low it was impossible to stay in the race let alone thrive. But for anyone potentially looking to buy the company there will be two things that might justify the price: legacy and assets.

Akzo Nobel, ICI, and Dulux are all well recognised brand names in Pakistan. For those that do not remember the heights of ICI, it is difficult to imagine what it must feel like to the business leaders of today who came up in their careers idolising this grand old company. Not only is there a premium to be paid for the ICI legacy, anyone looking to enter the paint business would do well to have established brand names on their side.

The most obvious candidate to buy Akzo Nobel would be a local paint manufacturer. In India as well, Akzo Nobel was bought by JSW, a local paint manufacturer that has become one of the largest players in the region after the acquisition. Local paint companies in Pakistan have managed to do well, however it seems the idea of purchasing Akzo Nobel is not well thought of within the paint industry. According to one senior executive of the paint industry, the asking price is far too high. “Our company at least cannot manage such a big purchase. Also frankly , it is not worth the headache,” they said.

Similarly Farooq Amin Sufi of Master Paints says it is a proposition that they had received before but it was too expensive. “Back in the day some ex employees of Akzo Nobel

did approach our family and asked if we were interested in buying them. The offer was made many times actually,” he says. “Recently when it came on the market it was open for everyone but we thought it was overvalued. They have also been facing a lot of problems which is why we were not particularly interested.”

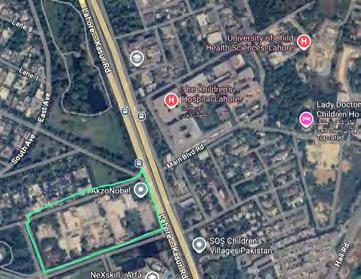

Why, then, would anyone want to buy Akzo Nobel? Perhaps the most attractive factor is land. Akzo Nobel has a large facility spread over 88 kanals (11 acres) at 346 Ferozpur Road Lahore. The facility sits on one of the most lucrative intersections in Lahore. Its front faces out onto main Ferozpur Road right at a terminal of the Metro Bus Station. It sits on a corner with its other side sitting in the middle of Model Town, one of the most expensive areas in the city. On top of that its main gate is a 30 second drive away from the Gulab Devi Hospital U-turn which leads directly to Walton, Cantt, DHA, and recently CBD’s route 49. In 2019, when Akzo Nobel was preparing to delist from the PSX, that property was reevaluated and its forced sale land value was estimated close to Rs2.6 billion. This does not include the cost of the building. Since 2020, the property’s value is bound to have gone up, particularly because of continuous development work in the area and in particular on this patch of Ferozpur Road.

Akzo Nobel’s main asset is an 88-Kanal facility in one of the most prime real estate locations in Lahore.

According to one source, buyers are not just interested in the paint business but also in the potential of this property. While they might want to give running the paint business a fair shot, even if it does not work out, the prime property can be managed or converted into a commercial real estate project.

As far as IGI Investments acquiring Akzo Nobel is concerned, the matter is unlikely to come to fruition. That is despite the fact that the owners of the group were quite keen on buying Akzo Nobel. In fact, even after the low offer made after the due diligence exercise, a revised upward bid was also made in consequence of the talks stalling, however, even the revised deal is too low for Akzo Nobel to be accepted. Within the Packages Group, one source felt that the resistance from the management group was enough that they conducted the due diligence in a very strict manner and stuck closer to the lower edges of the valuation.

Profit reached out to the management of the Packages Group and IGI Holdings to seek insights into the matter but they stated they did not want to comment.

Profit reached out to the representatives at Akzo Nobel N.V. multiple times in regards to the credibility of the deal falling through.

Joost Ruempol, head of reputation management at Akzo Nobel N.V. stated that “We do not comment on market rumors.” Similarly, officials at Akzo Nobel Pakistan were also contacted to verify or reject these reports, however, no reply was received till the filing of the story.

There are also reports that the deal that was being negotiated was stipulated on the fact that Akzo Nobel could not pursue any other active bidders while IGI was contemplating the deal. This was done so an active bidding war did not start while the due diligence was being carried out. The deadline for the deal was initially given in December 2025 which was extended to February 2026. With that date elapsing, Akzo Nobel is now free to find new bidders.

One might imagine there to be a vague possibility that Lucky Core Industries and Asia Pak

Investments, the two companies that currently own the other two parts of what was once ICI Pakistan, might be interested in this last link. However, Muhammad Ali Tabba of the Lucky Group firmly denied that this idea was even being considered.

Similarly, Profit also reached out to AsiaPak Investments. The private equity firm headed by Shaheryar Chishti has acquired significant positions and control in some of the largest companies operating in Pakistan. The firm also has experience buying a controlling interest of foreign multinationals like Lotte Chemical and Daewoo Bus Service where ownership was handed over by foreign investors to local ones. Their representative said they could not comment on the matter.

The field for purchasing Akzo Nobel remains open. While the company has its fair share of problems, its sale will mark a bittersweet moment in Pakistan’s corporate history. On the one hand, it means that what was once ICI, a grand old imperial company, is now entirely in the hands of Pakistanis. But not only has it taken time to get here, it has involved exits and divisions.

There are two words in Urdu that can be used to describe the act of division. The first is taqseem. Of Arabic origin, it is a politer word that indicates a fair distribution of some sort. The other word is of Hindi origin: Batwara. It denotes something far more visceral. It is a violent sundering of something whole, a selfish decimation.

It is perhaps why Pakistani histories of the partition refer to the events as Taqseem-eHind, and the language used by the Indian National Congress at the time of partition referred to Jinnah’s plan as Hindustan ka Batwara. It is also why the word batwara continues to be used in a negative connotation in discussions of inheritance.

As Profit has pointed out earlier, the sale of Akzo Nobel will determine the fate of what was once ICI. And it will raise the all important question: was this taqseem or the dreaded batwara? n

JS Group’s headquarters comes to market as a sale-leaseback REIT

JS Investments is offering a portion of their headquarters office building as a rental REIT to investors in a move that will shore up their own balance sheet

In Karachi’s Saddar, where glass towers rise out of older commercial streets with an air of mild defiance, The Centre has long announced itself as one of the city’s more self-conscious corporate landmarks. Now part of it is being marched to market. JS Rental REIT, managed by JS Investments, is seeking a Pakistan Stock Exchange listing through an offer for sale of 53.64m units at Rs10.70 each. But the thing being sold is not, strictly speaking, the building itself, nor even all of the building. Public investors are being offered 25% of a REIT that holds leasehold rights to just seven floors of The Centre’s 22-floor structure. And because this is an offer for sale by JS Lands rather than a fresh issue by the REIT, the cash will go to the selling sponsor, not into the trust.

That distinction matters. In the abstract, a listed rental REIT promises an elegant thing: small investors buying slices of a large, rent-producing commercial property. This one is better understood as a monetisation exercise by the JS Group. The REIT was registered in 2022, achieved financial close on June 29th of that year, and began with an initial size of roughly Rs657.8m after the transfer of part of The Centre into the scheme. It later expanded, and the current unit-holders’ fund stands at about Rs2.3bn. The IPO itself is worth about Rs573.9m. That is not new money for the asset; it is a partial divestment by JS Lands, the strategic investor that still owns 94.38% of the scheme before listing. After the offer, JS Lands will still hold 69.38%, with the public owning 25% and JS Investments retaining 5.62%.

The more arresting wrinkle is that the property being offered is, in effect, part of the group’s own headquarters complex. The Centre is not merely a building in which JS happens to have some tenancy exposure. It

is a JS address through and through. The prospectus shows JS Investments on the 15th and 19th floors, JS Global on the 16th through 18th, and Jahangir Siddiqui & Co. together with Energy Infrastructure Holding on the 20th. Of the seven floors inside the REIT, only two, the 19th and 20th, are currently leased, and both are leased to associated companies. A 13th-floor tenancy has been contractually committed to Regus, with delivery expected in the third quarter of FY2026. The remaining four floors, from the 9th to the 12th, are unfinished and under refurbishment. In plainer English, investors are being asked to buy into a headquarters monetisation story in which only a minority of the underlying space is actually producing rent today.

That makes the sale-leaseback character of the deal impossible to miss. Companies around the world have long sold office buildings to free up capital while continuing to occupy them as tenants. Pakistan rarely sees these kinds of transactions, let alone through a public listing, but this appears to be part of that global corporate finance norm. The group is taking an illiquid property interest, dropping it into a listed vehicle and inviting outside investors to finance part of the holding. It is not quite a surrender of control: JS Lands remains the dominant holder, the tenants on the occupied floors remain group entities, and the prospectus explicitly notes the scheme’s dependence on associated companies. It also notes that sponsors and initial subscribers will face no post-listing restriction on selling units, and that additional real estate can be added to the REIT without unit-holder approval, subject to disclosure.

The operating picture is not especially mature. JS Rental REIT posted revenue of Rs65.36m in FY2025, up only modestly from Rs62.99m a year earlier. It also reported a net loss of Rs1.82m for FY2025, which the

prospectus attributes to one-off maintenance and fit-out expenses before leasing the newly added floors. Half-year FY2026 numbers were weaker still, with revenue of Rs33.43m and a loss of Rs56.58m. The offer document argues that underlying rental cash flows remain positive and that the losses reflect preparatory work rather than a broken model. Perhaps. But the immediate truth is less flattering: investors are not buying a fully stabilised rent machine. They are buying a partly occupied trophy address that still needs to be leased up.

To be fair, the pricing is not especially aggressive. The offer price of Rs10.70 a unit sits close to the latest audited break-up value of Rs10.78, while the prospectus’s own discounted cash-flow and dividend-discount exercises produce indicative values of Rs10.79 and Rs10.80. That makes the flotation look less like a speculative growth punt and more like a near-net-asset-value monetisation.

The building itself deserves some attention because it is, undeniably, a serious piece of commercial real estate. The Centre sits on Abdullah Haroon Road near Zainab Market and Avari Towers, and was completed in 2012-13. It has a land area of 3,988 square yards and a total covered area of roughly 279,270 square feet. The tower includes retail at the lower levels, six parking floors, twelve office floors, an amenity floor with cafeteria and gym, and a rooftop helipad. The prospectus describes a ship-like profile, a fully glazed exterior, central HVAC, branded lifts and ample security. In a city where Grade-A office stock remains scarce and uneven, that is not nothing. The REIT’s portion covers 81,270 square feet across seven floors. As buildings go, this is a credible one.

Its history inside the REIT is also revealing. The trust began with the 19th and 20th floors, the ones already occupied by group tenants. In 2024 it expanded by acquiring

floors 9 through 13, taking the fund from roughly Rs658m to about Rs2.2bn. That broadened the asset base but also changed the nature of the proposition. What began as a tidy rental trust backed by occupied sponsor space became something more awkward: still a rental REIT, but one with a large leasing and refurbishment job embedded inside it. PACRA’s history page shows the scheme’s long-term rating at A+(rr) with a Positive outlook as of January 2026, but even PACRA’s rationale emphasises occupancy, tenant profile and execution as the critical variables.

The seller’s pedigree is the central defence against those concerns. JS Group traces its origins to 1970, when Jahangir Siddiqui began building what would become one of Pakistan’s more durable financial conglomerates. Jahangir Siddiqui & Co., the listed holding company, was established in 1991 as the successor to the brokerage business he had started in the early seventies. Today JSCL is the flagship holding company of the JS Group, with exposure spanning conventional and Islamic banking, asset management, brokerage, investment banking and insurance, as well as energy, petroleum, infrastructure, telecoms and technology.

JS Investments is itself no minor outpost. Founded in 1995, it describes itself as Pakistan’s oldest private-sector asset manager, with founding partners that included INVESCO and the IFC. The company is a subsidiary of JS Bank and holds licences for asset management, investment advisory, REIT management, private equity and venture-capital fund management, as well as pension-fund management. According to the prospectus, JS Investments reported revenue of Rs1.196bn and after-tax profit of Rs483m in 2025, with equity of Rs2.595bn.

Still, in Pakistan’s REIT market, pedigree is only half the story. The other half is comparison. And here the obvious benchmark is Dolmen City REIT, the country’s first listed REIT and still its cleanest rental example. Dolmen came to market in 2015 with assets that were already working hard: a VIS rating report from May 2015 noted that Dolmen Mall was 94% occupied while the Harbour Front office tower was fully occupied. The fund size was Rs22.237bn, of which Rs5.559bn was to be raised through IPO. A decade on, Dolmen’s 2025 corporate briefing still showed occupancy of 97.8% at the mall and 100% at the Harbour Front. That is what an institutional-quality rental REIT looks like when it is sold after the hard operational work has largely been done.

JS Rental REIT is not that. Its closest comparable in legal form is a far more distant comparable in operating maturity. Dolmen monetised a humming asset; JS is floating

one still warming up. On the most forgiving reading, three of its seven floors are spoken for, two leased and one committed. On the strictest reading, only two are occupied. The prospectus says the expected rent for The Centre’s REIT floors is Rs231 a square foot per month, which compares respectably with other Karachi office buildings such as Ocean Tower, Dawood Centre and Marina View. That supports the argument that the asset sits in the right league. But rent benchmarks are not the same as rent rolls. Investors do not receive dividends from comparables; they receive them from tenants actually in place. That is why the offer feels like a small but meaningful shift in how Pakistan’s REIT market is evolving. Beyond Dolmen, the exchange now has a smattering of developmental and hybrid vehicles, including Globe Residency REIT, TPL REIT Fund I, Image REIT and, since late January, Signature Residency REIT. The market is broadening, but much of that broadening has come through structures that ask investors to fund development, leasing or both. JS Rental REIT sits awkwardly between the older, simpler Dolmen model

and the newer, more execution-heavy REITs: nominally rental, yet carrying meaningful lease-up risk.

The public is not being invited to buy a seamless annuity. It is being invited to buy into a prime Karachi office building whose best floors are already occupied by its sponsor, whose upper promise depends on leasing unfinished space, and whose offering mainly serves to convert a sponsor’s property holding into cash. For investors who like a strong sponsor, a recognisable address and entry close to NAV, that may be enough. For those looking for Dolmen-like stability on day one, it is not.

Which leaves the offer where many interesting Pakistani capital-market deals end up: as both innovation and improvisation. JS Group is using the REIT wrapper for what it does best, structuring, distributing and monetising. But beneath the polished language of democratised real-estate access lies an older corporate instinct. When a financial conglomerate puts part of its own headquarters on the market, it is not merely inviting the public to share in a property. It is asking them to help refinance the house.

Farm recovery leads fertiliser sector profits to surge 10%

Higher volumes, indicating a recovery in Pakistani agriculture, drove the bulk of the gains for the sector

Pakistan’s fertiliser makers have long been treated by investors as something between utilities and weather vanes: dependable when the farm economy is healthy, unforgiving when it is not. In 2025 they looked rather more like a levered bet on rural recovery. A sector report by Topline Securities published on March 13 says Pakistan’s listed fertiliser companies posted combined profit after tax of Rs141.1 billion in 2025, up 10% from a year earlier, on net sales of Rs981.6 billion, up 7%. The firm attributes the gain chiefly to higher urea offtakes, stronger other income and a sharp fall in other charges.

Even though fourth-quarter profit slipped 2% year on year to Rs38.1 billion, the fullyear result extended a remarkable run for an industry whose profitability has climbed from Rs80 billion in 2023 to Rs128.3 billion in 2024 and now Rs141.1 billion in 2025. That headline number matters because it suggests fertiliser demand is once again saying something hopeful about the broader farm economy, even if the official macroeconomic picture remained mixed. Pakistan’s Economic Survey says the agriculture sector grew by only 0.56% in FY2025, sharply below the previous year’s pace, as major crops struggled. Yet the same document notes that other crops grew 4.78%, livestock remained

stable, and the government’s timely provision of quality seeds, fertilisers and credit helped enhance farm productivity and laid the foundation for recovery. In other words, agriculture was not booming everywhere at once, but enough of rural Pakistan was still planting, feeding and financing its next crop cycle to keep the input chain moving.

The Topline report shows how that recovery expressed itself on the ground. Urea offtakes rose 2% in 2025 to 6.73 million tonnes, while fourth-quarter urea offtakes jumped 26% year on year to 2.53 million tonnes. DAP was weaker, with annual offtakes falling 18% to 1.34 million tonnes, a reminder that the sector’s resurgence was driven more by nitrogen-heavy demand than by a broad-based boom across every product category. Even so, official data from the National Fertilizer Development Centre point in the same direction. During Kharif 2025, cumulative nutrient offtake rose 11.7% over the same period a year earlier, with urea up 13.1% and DAP up 1.2%; NFDC said demand improved during the season partly because Punjab offered incentives including interest-free loans and cash assistance. That is about as close as one gets in Pakistan to a real-time vote of confidence from farmers.

What is striking is that the sector achieved this profit growth despite a less generous margin environment than the topline numbers might suggest. Gross margins for the listed sector slipped to 31% in 2025, and to 27% in the fourth quarter, as companies offered discounts to keep volumes flowing. Topline notes that Engro Fertilizers offered discounts of Rs300-400 per bag in the final quarter, while Fauji Fertilizer offered Rs100-200 per bag. Finance costs across the sector rose 9% to Rs24.9 billion for the year. Yet other income

climbed 20%, and other charges fell 32% to Rs21.7 billion, helped in part by the absence of last year’s impairment hit at Fauji Fertilizer. In other words, the industry did not merely sell more; it was also helped by a friendlier non-operating backdrop.

The gains were not evenly shared. Fauji Fertilizer remained the giant of the field. Topline says FFC’s sales rose 16% in 2025 to Rs432.4 billion, while profit climbed 14% to Rs73.5 billion. That came despite a Rs14.13 billion provision against sales-tax receivables that squeezed gross margins to 30% for the year and 25% in the final quarter. Fatima Fertilizer delivered perhaps the cleanest growth story, with sales up 7% to Rs276.1 billion and profit up 15% to Rs42.1 billion, aided by a 49% drop in other charges. Engro Fertilizers was the laggard of the large names: sales fell 8% to Rs237.1 billion and profit dropped 20% to Rs22.6 billion as lower margins and a 49% jump in finance cost bit into earnings. For a sector that outsiders often treat as monolithic, 2025 was a reminder that even within the same nutrient cycle, balance sheets and pricing choices still matter.

There is another reason investors have been willing to look kindly on the sector: it has become a serious distributor of cash. Topline says listed fertiliser companies paid Rs111.8 billion in dividends in 2025, up 72% from a year earlier. That helps explain why fertiliser stocks remain a staple for Pakistani portfolios seeking income in a market otherwise dominated by more cyclical stories. The industry’s ten-year progression also tells a broader tale of scale. According to the chart in the report, sector revenue has risen from Rs192 billion in 2016 to Rs982 billion in 2025, while EBITDA has expanded from Rs46 billion to Rs238 billion over the same period, albeit with a slight dip from

2024’s Rs240 billion. Finance costs, meanwhile, have risen from Rs11 billion to Rs25 billion. The business has grown richer, larger and more financially complex all at once.

What makes this year’s performance especially interesting is that it does not fit neatly into the simplest story about Pakistani agriculture. The official numbers show major crops had a poor year, with wheat, cotton, rice, sugarcane and maize all posting declines in output, dragging down aggregate agricultural growth. Yet the fertiliser sector’s earnings say farmers did not retreat wholesale. Some of that reflects resilience in other crops and livestock; some reflects better credit availability and provincial support; some likely reflects the simple necessity of keeping acreage productive even in a difficult season. Fertiliser, after all, is not a luxury purchase. When farm incomes wobble, growers may delay many things, but they often try not to starve the soil.

That makes the sector’s latest surge less a celebration of bumper harvests than a sign of cautious renewal. The farm economy is not fully healed. Pakistan’s crop base remains exposed to climate shocks, policy distortions and volatile pricing. Even the fertiliser report contains caveats: discounts compressed margins, DAP demand stayed soft, and fourth-quarter profits were flatter than the annual tally implies. But the broad direction is unmistakable. Higher urea volumes, stabilising rural demand and cleaner non-operating accounts were enough to push listed-sector profits to a new high. For a country where agriculture still looms large in employment, politics and inflation, that is more than an earnings story. It is an early signal that the countryside, though hardly carefree, is buying inputs as if it expects another season worth planting. n

With new IPO, Pakistani investors get access to the supplier of the eggs in McDonald’s Egg McMuffins

Wahdat Poultry Farm is one of Pakistan’s leading poultry companies and is raising Rs600 million in a new listing to fund its expansion plans

The next time a Qatari office worker unwraps an Egg McMuffin, there is a decent chance the egg inside began its journey not in some anonymous commodity shed, but in a tightly controlled, automated layer house in Sargodha. Wahdat Poultry Farm Ltd, a prominent supplier to McDonald’s Pakistan, is now attempting something almost as unusual as selling branded eggs in a country long accustomed to buying them loose: it wants to sell itself, or at least a slice of itself, to the public markets. McDonald’s Pakistan’s current breakfast menu still includes the Egg McMuffin, while Wahdat’s draft prospectus says the company is a prominent supplier to McDonald’s Pakistan and the Middle East and is on the McDonald’s

Global Vendor List.

The draft prospectus placed on the Pakistan Stock Exchange website on March 13 lays out a modestly sized but symbolically important flotation. Wahdat plans to offer 53.1 million shares at a floor price of Rs12 each, implying an issue size of Rs637.2 million at the floor. Of that, 50 million shares are a fresh issue that would bring Rs600 million into the company; the remaining 3.1 million shares are an offer for sale by sponsor Naved Ali Khan, who is selling his entire holding. The company says the sale would leave public investors with 15.84% of the post-IPO equity. The book-building portion accounts for 70% of the offer, with the remainder reserved for the general public. Topline Securities is acting as lead investment bank and Haidermota & Co as

transaction legal adviser.

That corporate cast matters because Wahdat is not being pitched merely as a farm. It is being pitched as a branded food business, a rarity in Pakistan’s livestock economy, where much of the sector still lives in the low-margin, loosely organised world of commodity production. Wahdat says it operates as a fully vertically integrated layer-poultry enterprise under the “Farm Fresh Eggs” brand, spanning production, grading, packaging, marketing, distribution and exports. The company traces its operating origins to 2007, was incorporated as a private limited company in 2019, and converted into a public limited company in late 2025 as it prepared for the market. It runs four automated layer houses using European systems from Big Dutchman of Germany

and Tecno of Italy, with installed capacity of about 430,000 birds and peak output of up to 400,000 eggs a day.

That scale, by local standards, is already formidable. Yet what makes Wahdat interesting is not just size, but the extent to which it has tried to turn an everyday staple into a premium, traceable consumer product. Its eggs are sold as Classic, Omega-3, Golden and Brown variants, and the company emphasises 100% vegetarian feed, automation, hygiene, and international food-safety certifications as points of differentiation. On its public website, Wahdat presents itself as Pakistan’s premium Omega-3 and vitamin-enriched egg producer; in the prospectus it says it supplies roughly 1,500 retail outlets in major cities and counts modern-trade names such as Imtiaz, Jalal Sons, Punjab Cash & Carry, Al Fatah, Metro, Carrefour, D. Watson and CSD among its largest customers. Export sales have risen sharply too: the prospectus shows overseas customer revenue climbing from about Rs82.8 million in FY23 to Rs455 million in FY25.

That helps explain the McDonald’s hook. In Pakistan, where international fast-food chains are obsessive about input consistency, winning a place in the supply chain is less a marketing gimmick than a certification of industrial discipline. Wahdat’s own materials lean heavily on this point. The company says it is on the McDonald’s Global Vendor List, supplies McDonald’s Pakistan, and has been able to export to Gulf markets partly on the back of that compliance infrastructure. A July 2025 article on its website went further, saying its products are supplied to international retail chains such as Carrefour, Metro and McDonald’s and that annual quality audits by global partners have consistently yielded A-grade ratings. That last claim comes from the company itself and should therefore be read as promotional, but the broader point stands: Wahdat has spent years trying to make eggs legible to modern retail and multinational procurement departments.

The money it is seeking from the market is meant to finance the next step in that transformation. Rs270 million of the fresh proceeds is earmarked for a liquid-egg pasteurisation plant, including machinery, civil works and land. Another Rs180 million will fund the rearing of an additional 100,000 birds. The remaining Rs150 million is meant for working capital and a “farm licensing model” under which third-party farms would operate under Wahdat’s quality, feed and biosecurity protocols. In plain English, the company wants to move beyond selling branded shell eggs and into the higher-value world of processed egg products for hotels, restaurants, caterers, confectionery manufacturers and food processors. Management’s argument is that Pakistan has a shortage

of hygienic liquid eggs, and that this gives Wahdat a chance to move up the value chain into a more defensible, less cyclical business.

There is also a timing argument. Wahdat says it is already operating at full capacity and still cannot meet all the demand coming from existing retail partners. In the prospectus, management estimates that more than 30% of orders within its present network go unmet because of production constraints. That is a revealing detail. It suggests the company is not going to market because demand is hypothetical, but because it believes demand is already here and that the bottleneck sits inside its own sheds. The implementation plan is correspondingly brisk. The company expects land acquisition for the pasteurisation plant in FY26, construction and equipment installation through FY27, and operationalisation by the second quarter of FY27. The additional flock is also meant to begin laying by Q2 FY27. That is ambitious, but not absurd, especially if the company follows through on its asset-light approach of leasing facilities where necessary rather than waiting to build every shed itself.

The more intriguing part of the Wahdat story lies with its shareholders. The company is still very much a founder-run business. Muhemmed Shahid Zaman, the chairman, is described in the prospectus as a longtime agribusiness entrepreneur with experience spanning fish farming, dairy and other agricultural ventures. Air Marshal (Retd.) Aurangzeb Khan, the chief executive, brings a markedly different biography: 35 years in the Pakistan Air Force, a career that included command roles and leadership at Pakistan Aeronautical Complex Kamra, where he helped oversee the JF-17 project before moving into agriculture. On Wahdat’s own website and in company material, the founding story is cast as a marriage between landed agricultural experience and disciplined, technology-oriented management. It sounds neat because it is neat. But in this case, the neatness is also plausible. Few things in Pakistan require as much routine, process and biosecurity discipline as a scaled layer operation.

Then there is Karandaaz Pakistan, the most important outside shareholder and perhaps the clearest signal that Wahdat has already passed one institutional test. Karandaaz currently owns 27% of the company, a stake that will dilute to 22.97% after the IPO. The prospectus says a Rs500 million equity injection from Karandaaz between 2019 and 2020 helped accelerate production growth and double the company’s retail reach from roughly 600 outlets to more than 1,200 by 2022. Karandaaz itself is a not-for-profit Section 42 company established in 2014 with seed grant funding from Britain’s Foreign, Commonwealth & Development Office; through Karandaaz Capital

it provides structured credit and equity-linked growth capital to small and mid-sized enterprises with the potential to support employment and sustainable growth. In other words, this is not dumb money. Its involvement gives Wahdat a degree of validation that many family-owned agribusinesses never get.

Still, the case for the IPO will ultimately rest less on biography than on numbers. And here Wahdat has a genuinely attractive story. Net revenue rose from Rs1.23 billion in FY21 to Rs2.79 billion in FY25. Profit after tax grew from Rs63.4 million to Rs241.9 million over the same period. Gross margin, which had slipped to 18.1% in FY22 and 17.8% in FY23, recovered to 23.4% in FY24 and 24.3% in FY25. Operating margin followed a similar arc, falling from 7% in FY21 to barely above 2% in FY22 and FY23 before rebounding to 9.1% in FY24 and 11.1% in FY25. The first half of FY26 looks stronger still, with Rs1.47 billion in revenue, Rs163 million in after-tax profit, a 25.6% gross margin and a 12.2% operating margin. This is not the profile of a business merely keeping pace with inflation. It is the profile of one that has begun to recover scale economics after an ugly period of cost pressure.

Those earlier margin swings are important because they remind investors what sort of business this remains. However polished the brand, Wahdat still lives with agricultural realities. Feed is the dominant cost item, and the prospectus shows raw material consumption absorbing as much as 74% of cost of sales in FY23. This is a company that can be clever about procurement, solarise more than 70% of its power needs, make its own pulp packaging, digitise route planning and still be humbled by grain markets, disease risk and biological cycles. The virtue of vertical integration is that it offers more control than the average poultry operator enjoys. The vice is that it can encourage investors to forget that eggs, before they become a brand, are still a farm product.

Even so, Wahdat’s would-be flotation feels like more than a routine small-cap deal. Pakistan’s stockmarket has long offered investors banks, cement plants, fertiliser makers, textile exporters and the occasional consumer brand. It has offered far fewer chances to invest in the formalisation of a basic food category. What Wahdat is really selling is not just a poultry business, but a thesis: that in Pakistan, even something as humble as the egg can be branded, fortified, audited, exported, and eventually processed into higher-margin products. The company’s prospectus is, like all prospectuses, full of aspiration. Yet aspiration, in this case, is not entirely fanciful. A firm that began by trying to persuade Pakistanis to buy cleaner, safer eggs is now trying to persuade them to buy equity in that proposition. That is a different sort of premium product. n

Air Link to separately list manufacturing subsidiary in IPO

The newly listed company would offer investors exposure purely to Air Link’s local assembly and manufacturing business, distinct from the current holding company which also includes its import and distribution business lines

There are, broadly speaking, two ways to tell the story of Pakistan’s consumer-electronics boom. One is as a retail story: more handsets, more screens, more gadgets, more people with enough disposable income to want them. The other is as an industrial story: a country that once imported finished devices is now trying, piece by piece, to assemble more of them at home. Air Link’s decision to float Select Technologies, its wholly owned manufacturing subsidiary, belongs squarely to the second narrative. It is not merely another listing notice. It is an attempt to put a market value on the factory floor itself.

The formal disclosure, sent to the Pakistan Stock Exchange on March 12, is brief but significant. Air Link Communication Ltd said that Select Technologies has decided to raise capital through an initial public offering and seek a listing on the PSX, subject to regulatory approvals and compliance with applicable laws. Arif Habib Limited has been appointed

consultant to the issue and lead manager. That is, for now, the sum of what is officially known: no offer size, no valuation range, no indication yet of how much equity will be sold, and no public timetable. But even in outline, the structure is revealing. This is not Air Link raising money at the parent level for a mixed bag of operations. It is Air Link preparing to carve out a separately quoted manufacturing vehicle from a parent that today combines import, export, distribution, assembly, wholesale and retail under one roof.

That distinction matters because Select is not a generic subsidiary created to warehouse assets. It was incorporated in October 2021 as Air Link’s dedicated manufacturing arm, with the principal line of business being the assembly and production of mobile phones, accessories, components and related parts. On its own public materials, Select describes itself as an Air Link initiative set up to establish and operate plants for mobile-phone assembly and production in Pakistan. In corporate terms, that sounds routine. In industrial terms, it

marked a turning point: Air Link had built its name in distribution, but Select was the vehicle through which it moved decisively into the more politically fashionable and potentially more profitable business of localisation. Select’s clearest claim to strategic relevance is its relationship with Xiaomi. In April 2022, Select announced that it had joined hands with Xiaomi as the Chinese company’s manufacturing partner for smartphones in Pakistan. Around the same time, Select said the PTA had granted it a manufacturing licence for Xiaomi mobile phones. That same disclosure added an important bit of context: the wider Air Link group already had licences to manufacture Transsion brands such as Tecno and itel, making the company unusual in Pakistan’s local-assembly landscape. Select’s manufacturing facility has roughly 120,000 square feet of covered area, including 60,000 square feet of clean-room space, with annual capacity of about 2.7 million units on a single-shift basis; in FY25, it assembled around 2 million devices, implying utilisation of roughly three-quarters.

That is enough to explain why Air Link may believe Select deserves its own stock market identity. Xiaomi is not merely another handset badge in Pakistan. It is one of the more recognisable Chinese electronics brands in the country, and the local manufacturing arrangement gives Select a profile quite different from an ordinary importer or distributor. An Arif Habib research note published last year argued that importing raw materials and adding value through local assembly is more lucrative than importing finished products, precisely because the economics of assembly carry better incremental margins. The same note described the Xiaomi arrangement as a tightly managed production relationship, with monthly capacity planning and compensation mechanisms if output falls materially below agreed thresholds. In other words, the subsidiary being prepared for listing is not just a workshop. It is a contract manufacturer with a relatively structured anchor relationship.

To understand why that could be appealing to investors, one has to go back to Air Link itself. The parent company was incorporated in 2014, converted into a public limited company in 2019 and listed on the Pakistan Stock Exchange in September 2021 after completing what it later described as Pakistan’s largest private-sector IPO, oversubscribed by Rs11 billion. Air Link began as a distributor, and that heritage remains visible in its network, brand relationships and national footprint. Its latest public materials describe the company as a major technology player spanning manufacturing, distribution and retail, with partnerships across names such as Samsung, Xiaomi, Apple, Tecno, itel, Acer Gadgets and iMiki. Over time, that distribution backbone became the platform for backward integration into manufacturing and forward integration into stores. Air Link today likes to describe itself as a 360-degree ecosystem. Corporate prose aside, the description is not entirely wrong.

Still, integrated groups often run into a problem in public markets: investors do not always know which part of the machine they are buying. A distributor has one set of economics, a retailer another, and a contract manufacturer another still. Distribution tends to be volume-heavy, working-capital-intensive and vulnerable to swings in import duties, inventories and consumer demand. Manufacturing, especially when tied to localisation policy and tax incentives, promises a different story: more operating leverage, more policy support, and in theory a clearer path to margin expansion. That is why the proposed Select listing looks less like administrative tidying and more like an effort to let investors buy the industrial thesis without also having to buy the full complexity of Air Link’s broader

trading operations. In 1HFY26 the assembly segment contributed about 58% of overall revenue, against 42% for distribution. That alone suggests the manufacturing side is no longer a side hustle hiding inside a trading company. Air Link’s own accounts hint at the same evolution. In the half-year ended December 31, 2025, the company reported consolidated sales of Rs48.8 billion, down from Rs57.3 billion in the same period a year earlier, but with a much better gross margin of 14.9% against 9.5%, and a higher consolidated net margin of 6.3% against 4.1%. The parent’s investor-information page shows that for FY25 as a whole, Air Link recorded sales of Rs104.4 billion and profit after tax of Rs4.75 billion, against Rs129.7 billion in sales and Rs4.63 billion in profit in FY24. In other words, the topline has been volatile, but profitability has held up rather better than that headline decline might suggest. That is exactly the sort of pattern management teams often point to when arguing that the market ought to value the higher-margin manufacturing stream separately from the lower-margin distribution one.

There is another reason this spin-off makes strategic sense. Pakistan’s policy environment has been nudging the market in precisely this direction for several years. The PTA said in 2021 that local manufacturing had already surpassed imported phones, crediting the new mobile-device-manufacturing regulatory regime and government policy support. By the end of 2025, the PTA said over 95% of mobile devices in Pakistan, including 68% of smartphones, were being locally produced. This does not mean every locally assembled phone is a high-margin triumph; far from it. But it does mean that a listed manufacturing specialist can be marketed as a way to gain exposure to one of the few genuine industrial-substitution themes still standing in Pakistan. That is a neater pitch than telling investors to buy a hybrid company whose fortunes depend both on assembling devices and on moving imported stock through the country’s retail and wholesale channels.

The industrial ambition is also getting larger. Air Link says it is building a landmark manufacturing unit at Sundar Industrial Estate, spanning eight acres and around 1.4 million square feet of covered area. PACRA said the company has already invested more than Rs3 billion in the new facility at the Sundar Green Special Economic Zone, where mobile-phone assembly lines have achieved ready-for-service status. Arif Habib Research, meanwhile, has pointed to the attraction of a ten-year tax holiday attached to that facility and to a broader diversification strategy that now reaches beyond handsets into Xiaomi smart TVs, Acer laptops and tablets, and other smart devices. Even the company’s own web-

site now presents Air Link not just as a phone assembler but as a manufacturer of smartphones, smart TVs, wearables and computing devices for global brands.

This is where Select becomes especially interesting. The subsidiary may have been born as a Xiaomi handset vehicle, but the perimeter is already widening. In January, Air Link disclosed that Select had entered into a strategic partnership with Hisense for the manufacturing and distribution of home appliances in Pakistan, including smart TVs and air conditioners. The filing added that Hisense had expressed its intention to make a direct investment in the venture in the near future. If that eventually happens, it would do more than add capital. It would offer a form of external validation that Pakistani investors tend to prize: not simply that a local assembler has won a contract, but that an international principal is willing to put money alongside it. Even before that, the Hisense announcement suggests Select is being positioned as more than a single-brand contract manufacturer. It is beginning to look like Air Link’s flagship local-manufacturing platform.

Air Link’s broader expansion agenda reinforces that reading. The company has recently spoken of launching Xiaomi TV manufacturing, signed manufacturing arrangements with Acer, and incorporated a new wholly owned subsidiary, Zexo Technologies, to handle additional brands and categories ranging from smartphones and laptops to home appliances and e-commerce. That may sound sprawling, and perhaps it is. But it also reveals how Air Link thinks about itself now. It is no longer content to be known as a distributor that happened to build an assembly line. It wants to be understood as one of the domestic anchors of Pakistan’s electronics-manufacturing push. A separately listed Select would help make that case more legible, to investors and perhaps to foreign partners as well.

For investors, then, the coming deal is likely to pose a fairly simple question dressed up in prospectus language. Do they want to own a generalist listed parent with exposure to imports, inventories, retail rents and distribution margins? Or do they want a more focused wager on local assembly, industrial policy and manufacturing partnerships with Chinese electronics brands? Air Link appears to believe enough investors will prefer the second proposition that it is worth floating Select on its own. The eventual success of that argument will depend on valuation, float size and the fine print that has yet to be published. But the logic is already visible. In an era when Pakistan’s capital markets are starved of fresh industrial stories, Air Link is trying to sell one. Not the storefront, not the warehouse, but the line that screws the device together. n

Who won Pakistan’s 5G auction?

Profit explains what the spectrum auction means for the average user and how it affects their daily lives

For most people, a spectrum auction sounds abstract, technical, and far removed from ordinary life. When in fact, it is not. Contrarily, it is the single most important step that will shape the telecom market dynamics, and also the future of whatever is left of the “Digital Pakistan” dream.

What Pakistan sold on Tuesday was not just frequency blocks on a regulator’s spreadsheet. It sold the future “road space” on which mobile internet will travel. In three rounds, the country raised $507 million by assigning 480 MHz of spectrum to Jazz, Ufone and Zong. Jazz

bought 190 MHz, Ufone 180 MHz and Zong 110 MHz. But the detail is in the fine print.

Official auction documents had made 597 MHz available across multiple bands, and the blocks actually sold in this auction came from the 700 MHz, 2300 MHz, 2600 MHz and 3500 MHz ranges/bands.

What does it mean and why does it matter?

Spectrum matters because it underpins the quality of everyday digital connectivity. It determines whether a WhatsApp call drops indoors, whether YouTube buffers during peak hours, whether mobile data slows to a painful

crawl in basements, and whether a 5G service delivers real speed improvements rather than a cosmetic upgrade.

But beyond these mundane everyday experiences, spectrum also shapes the reliability and responsiveness of the digital economy. From locally housed global SaaS operations to small local businesses that rely on mobile internet to reach customers, effective connectivity depends on sufficient and well-managed spectrum. In that sense, spectrum is not merely a technical resource but a foundational input for sustained digital growth

Pakistan already has more than 200

million telecom subscribers, 150 million broadband subscribers and over 2 million FTTH users, which means the country is already deeply connected but still overwhelmingly reliant on mobile networks rather than fibre going into homes. For a country like that, spectrum is not even a luxury upgrade, it is a necessity for digital capacity. One that has already been delayed.

To understand what happened at the auction, it helps to step away from technical jargon for a moment. Think of spectrum as different types of roads in a transport network built for airwaves that carry data. Some are long highways that stretch deep across the countryside. Like two-way roads carving mountains, villages and buildings, carrying cargo across all kinds of terrains. Others are dense 5-lane urban expressways that don’t move far, but let more traffic cover shorter distances at higher speeds.

In this network, Pakistan’s 700 MHz band functions like the long-distance highway, much like the Karakoram Highway. The World Bank-backed 5G readiness plan for Pakistan describes it as optimal for coverage, making it useful for extending both 4G and 5G services across large geographic areas. It takes 5G internet to tighter corners, vast areas and guarantees more coverage.

The 2300 MHz and 2600 MHz bands resemble busy city routes designed to handle heavy flows of mobile data in between populated areas. Think of the GT road in Punjab, running through all the major cities of Northern Punjab, providing a reliable transit across urbanised terrain.

Meanwhile, the 3500 MHz band is the global backbone of early 5G deployments, offering a balance between reach and the capacity needed to deliver faster speeds in urban centers, much like the 10-Lane Islamabad Expressway. You do not go far on it, but you get to anywhere within the city in under 30 minutes. Speed is key with this one.

(Note: The analogy is an oversimplification of nuances that may categorise different spectrum bands and is meant for a cursory understanding of the concept)

Meanwhile, radio spectrum itself is used by mobile networks to transmit calls, messages and internet data between phones and telecom towers. Governments own this spectrum and allocate it to telecom operators through auctions. The amount of spectrum an operator holds is also measured in megahertz (MHz), which represents the width of radio frequencies it can use to carry signals.

A larger amount of MHz means a wider “channel” for data traffic, allowing networks to support more users and faster connections. In Pakistan’s latest spectrum auction, operators purchased additional MHz of bandwidth across several frequency bands to expand their

network capacity and prepare for next-generation services.