11 The fate of the Dam Fund

14 2025: The year of the net equity outflow in the stock exchange

20 Slow year for profit growth, as KSE100 companies see income rise by 5.3%

22 For Engro, 2025 was a year of slowdown and consolidation

27 Bribing Pakistani bosses? Study finds minor wage subsidies cause major spikes in female hiring

28 ARY Group set to buy Malik Riaz’s Nukta, deal “almost final”

30 REEV or BEV? why one customs code has become Pakistan’s next auto fight

32 Hyundai Palisade priced from Rs 2.1 crores, set to directly compete with Tank 500 and Fortuner

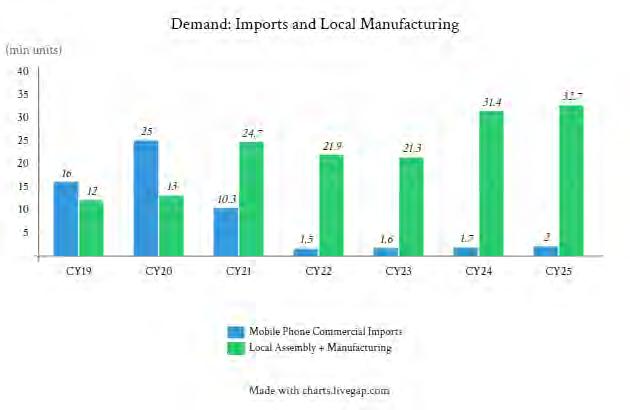

36 After achieving 94% local assembly in mobile phones, Pakistan has a new phone manufacturing policy. What does it hope to achieve?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Usama Liaqat Shahab Omer | Zain Naeem | Nisma Riaz | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing: Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi)

Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

RCC work on the Diamer Bhasha Dam is set to begin from this year. But up to a hundred seismic events a year imperil the dam being constructed in the earthquake prone region

By Abdullah Niazi

Remember the dam fund? That little bizarre moment of our judicial history in which the Chief Justice of Pakistan, the Honourable Justice (retired) Saqib Nisar embarked on a quest to singlehandedly collect funds to build a dam and make Pakistan self-reliant in energy? It mattered very little that the dam fund

was collecting donations in rupees, and that the feasibility of the Diamer-Bhasha dam, the one it aimed to crowd-fund into existence, has been called into question since the idea was first conceived. From the 6th of July 2018 to the 17th of January 2019 the dam fund dominated headlines.

From the day the fund was announced to the day the Honourable (retired) Chief Justice hung up his robes and left the spotlight, the dam fund was in everyone’s face. Banks had to put up notices on ATM machines and large

flex banners outside their branches announcing they were accepting donations to the fund. SMS campaigns urged the nation to contribute. The ringing tune for phone calls was an automated appeal to donate generously. Businessmen lined up to hand fat cheques to the Chief Justice and get photo ops handing over cheques to him. There were more than a few comically large cheques so that people looking at the photos could marvel at the many zeroes (all in rupees of course) at the end of the figure. Of course, it was a little strange that at

times the court used its authority to assign punishment to fatten up the account as well. On more than a few occasions defendants were directed to pay fines in the form of submissions to the dam fund. It was within the court’s authority, but even in that laissez faire environment the optics were a bit wonky.

And then came the end. His dark glasses still on, Justice Nisar gave his farewell speech, doffed his robes and rode off into the great land of post-retirement obscurity. His tenure was marked by such zeal for judicial activism that has not been seen since. But one question remains: What about the dam (damn?) fund?

The amount of money raised by the dam fund makes for a strange picking. Initially, when the fund was created and people lined up for the photo-ops, the fund collected Rs 10 billion. The Rs 10 billion milestone was announced by then Prime Minister Imran Khan in March 2019 — less than a year after it was first announced. It was a small drop in the dam considering the estimated cost for construction of two dams was Rs 1700 billion, of which Rs 1450 billion was needed for the construction of the Diamer-Bhasha dam and Rs 300 billion on the Mohmand dam. Of course this was before the devaluation of the rupee which has since fallen drastically compared to the dollar.

The most recent update on the state of the dam fund came in 2023. During the caretaker government, the late Dr Shamshad Akhter, serving as finance minister, disclosed that there was a sum of Rs17.86 billion in the Supreme Court and Prime Minister’s Dams Fund. In her written response submitted to the Senate, Dr Akhtar informed the House that an amount of Rs11.46 billion was directly contributed to the fund, while an additional sum of Rs6.29 billion was gathered as profit on government investments. So not a whole lot of money was collected after that Rs 10 billion target was first hit. The money has been sitting by collecting interest quietly. State Bank officials informed the court that the fund currently had more than a sum of Rs16 billion but so far neither had any withdrawal been made from it, nor any expenditure incurred from that money.

In September 2024, the federal government asked the Supreme Court to give them the money. At that point, Wapda told the SC the updated figure in the account: total money collected was Rs18.64 billion, out of that Rs9.56 billion generated locally, while overseas Pakistanis contributed Rs1.9 billion, and profit earned on it is Rs7.1 billion.

In October 2024, the apex court on Thursday finally ordered the closure of the Supreme Court of Pakistan and the Prime Minis-

ter of Pakistan Diamer-Bhasha and Mohmand Dams Fund. As of Oct 4, there was Rs23.6 billion in the account, most of which was the mark-up paid by the federal government. The money existed in a strange situation. Sure, an amount had been collected, but the government had paid almost as much markup on it. Back then, Chief Justice Qazi Faez Isa directed that a sub-account in the public account of the federation be created or other appropriate measures be taken to enable the amount to be lent to the “best-rated private scheduled bank or banks” so that mark-up could be earned. The directions included that when any amount would be required for the construction of these dams, the amount and the mark-up accrued would be utilised. And that is where we come to now.

At the beginning of this year, Chairman WAPDA Lt Gen Muhammad Saeed (Retd) visited the under-construction Diamer Basha Dam and Dasu Hydropower Project. He was briefed by the authorities that roller-compacted-concrete (RCC) works on main dams of both Projects will commence this year, as pre-requisites are now heading towards completion at a faster pace.

Roller-compacted concrete (RCC) dams are a type of gravity dam built by placing dry, low-slump concrete in thin layers and compacting it with heavy rollers, much like building a roadway. Instead of relying on complex shapes, they rely on sheer mass: their enormous weight resists the pressure of the reservoir. Once hardened, the layered concrete behaves like a single solid block anchored into rock. This method allows faster construction and lower costs compared to conventional concrete dams, while still producing a structure designed to hold back billions of cubic metres of water through gravity alone.

For all the lore behind its (very partial) funding, the Diamer Bhasha dam has a whole litany of problems.

Not least among these problems are earthquakes. For well over a decade now, particularly since after the Kashmir earthquake of 2005, there has been growing concern about the hazards seismic activity presents to structures, especially infrastructure, in the Gilgit-Baltistan region. And it isn’t just roads that we’re talking about. In the five years since 2017, the US Geological Survey (USGS) has recorded 526 seismic events in the region that registered at 4.0 or above on the Richter scale. That’s more than 100 events every year!

In earthquake-prone regions, however, that same mass becomes both strength and stress point. During strong shaking, the dam experiences horizontal inertia forces,

additional hydrodynamic pressure from the reservoir, and fluctuating uplift pressures at its foundation. Frequent small tremors, such as magnitude 4.0 events, are generally manageable and mainly require monitoring for cracks or seepage changes. The real risk comes from a rare but powerful earthquake that could challenge sliding resistance at the foundation, induce cracking at the heel of the dam, or stress fractured rock beneath it. In such settings, foundation quality and seismic design — not just the concrete itself — determine long-term safety.

The Diamer-Bhasha dam has long been portrayed as a saviour project for Pakistan’s water and energy woes. The belief that the dam will solve the country’s electricity shortfall has turned into a political point, and vain efforts like the Diamer-Bhasha dam fund fueling the wild fantasies of what such a project would do. But as has been pointed out before in a special report by seismological experts in Dawn, “the primary planning and design issues for the Diamer Basha Dam project are structural safety and sustainability.”

“Why is Pakistan off to make the world’s tallest Roller Compacted Concrete (RCC) dam – an unmoving, inflexible, rigid structure of mammoth proportions – in one of the region’s most active earthquake zones?” asked Suleman Najib Khan, a consultant engineer with the Water Resources Council, in an article published in The News in May of 2020. In the same article he says the dam was originally supposed to be a flexible structure, “one that could withstand the enormous seismic activity of the unpredictable Karakorums” back in 1984 when it was first proposed. But in 2004, when the regime of General Pervez Musharraf changed its design to a rigid RCC structure, “ with its height hazardously raised by almost 300 ft.”

This decision left the original proposers of the dam perplexed. “[N]o RCC dam has ever been built of even comparable height in such unforgiving conditions” Khan wrote. “In the event that the dam bursts at its proposed height of 908 ft during a routine seismic movement, eight million acre feet of water, with the destructive power of a hydrogen bomb, will wipe out everything on the Indus all the way down to Sukkur.”

He quotes from a letter written by General Ghulam Safdar Butt, the original proposer of the dam in 1984, to General Musharraf urging a rethink of the decision. “I shudder at the thought of earthquake effects on Bhasha. Dam-burst would wipe out Tarbela and all barrages on Indus; which would take us back to the stone-age” that letter said.

Some progress has been made on the project, and in the past, WAPDA has answered questions regarding the risk mitigation measures they are taking. WAPDA has arrived at

fixed values by measuring the level of shaking that was observed at the dam site during the October 2005 earthquake in Kashmir. This is the first misstep, particularly because the 2005 earthquake occurred hundreds of miles away from the dam site. The risk mitigation measures must not be taken for earthquakes taking place hundreds of miles away, but must be designed for the possibility of an earthquake closer to the actual site of the dam.

Especially since there is actually very little that we know about the area and the fault lines therein. The report of the Geological Survey of Pakistan quoted in the beginning mentions that “The exact nature of the movement along the fault is still unknown due to lack of sufficient GNSS (Global Navigation Satellite Systems) and earthquake focal mechanism data.” In its recommendations, the report says that the authorities are “bonded” in carrying out their research and making detailed recommendations because of the lack of data - they do not even know the exact number of faults because there are not enough GNSSs in the area. The report demands that there be “a dense network of GNSS stations that can delineate the neo-tectonics and structure of the area.”

Clearly there is an incredible lack of data and understanding of the tectonic mapping of this area. The good thing about modern science is that we can accurately predict and hence plan for the chaos that events like earthquakes bring. The unfortunate part for us is that the data we have on this is incomplete and all of these estimates are generally taking half-hearted stabs at figuring out what the ranges for these mitigation values should be.

This lack of data and understanding also shows in the ranges that WAPDA ended up specifying (which they derived using data from the 2005 earthquake). WAPDA claims that they installed two strong motion accelerographs at the dam site since 2002, and after August 2007, they have 10 additional micro seismic stations within a 50km-diameter of the dam site to also measure the small, almost imperceptible earthquakes that occur in that region with some regularity.

According to their comments from 2018, the range they have factored is 0.146g as the operating basis for an earthquake, and 0.247g as the maximum design earthquake that the structure will be designed to withstand. In horizontal shaking, the operating earthquake assumption used in the structure’s design is 0.22g and the maximum design earthquake parameter is 0.37g.

The range Wapda is using is taken from the Pakistan Building Code of 2007. The problem is that this range was designed for small houses, not large infrastructure projects. In fact, the housing code specifically says that its

tolerance ranges are not applicable to dams as well as a host of other structures that are larger than small houses, including power stations and transmission lines, military installations, tunnels and pipelines and more. In fact, the code specifically says that its provisions are for “buildings and building-like structures” only.

Over here, we have a clear case of science warning us of the dangers that certain actions will cause, and providing us with very clear and specific instructions as to what is to be done about it. Again, this is not to say that the dam cannot be built or will definitely be a disaster. However, the population increasing in the region means the risk from earthquakes is much higher.

And so the fund is closed, the money accounted for, the mark-up carefully tallied and parked in neat sub-accounts. The banners have come down, the SMS appeals have long stopped buzzing, and no one is lining up with oversized cheques anymore. What remains is a ledger

entry and a question mark.

The dam itself inches forward, as megaprojects do — through briefings, site visits, and assurances that prerequisites are nearing completion. RCC will be poured, compacted, and layered into a wall meant to stand immovable against both water and time. Engineers will point to design specifications, seismic coefficients, and foundation treatments. Critics will point to fault lines and history. Both will be right in their own domains. Perhaps that is the quiet irony of the whole episode. A project born in spectacle now proceeds in bureaucracy. A fund that once dominated prime-time television now accrues interest in silence. The romance of national self-reliance has given way to procurement schedules and technical audits.

In the end, dams are not built on enthusiasm. They are built on rock — and on calculations that must hold when the ground beneath them does not. The real test of the Diamer-Bhasha dam will not be how much was donated in 2018, but whether, decades from now, it still stands exactly where it was meant to. n

Last year saw more share buybacks compared to IPOs carried out. What is the reason behind it?

By Zain Naeem

When people follow the stock market, their thinking is that the sole function of the capital markets is to provide price discovery for the stocks that are listed. The daily volatility in the market is considered to be the only use where investors can buy and sell their shares as they please. This is indeed a function of the market. However, it is not the primary purpose of the markets.

Capital markets are seen as the first place of issue where corporations can come to investors and offer them shares and an investment opportunity. This allows the companies to raise funds for themselves while allowing investors an opportunity to invest in the company at this initial stage. The market acts as the platform where the two parties come together and are able to communicate and trade with each other. Indeed, this function of the market is literally called the primary market.

Something that is seen as the most common example of this is an Initial Public Offering (IPO) where the company gives access to its financials to all the investors in the market. They provide details of their past and present and chart a future that they see for themselves going forward. The company has to wow the investors to such an extent that the investors are willing to use their savings in order to invest in the company. Subsequent issuances can be carried out where the companies go to investors for additional sources of funds as well in the form of right share subscriptions as well.

The advantage of this is that the company gets access to funds which are not considered as debt or a loan from the bank and it allows the balance sheet of the company to strengthen as it receives an injection of

additional capital. The investors are getting a piece of ownership in the company which allows them to vote in the matters of the company, attend meetings and have a share in the profit and dividends announced by the company.

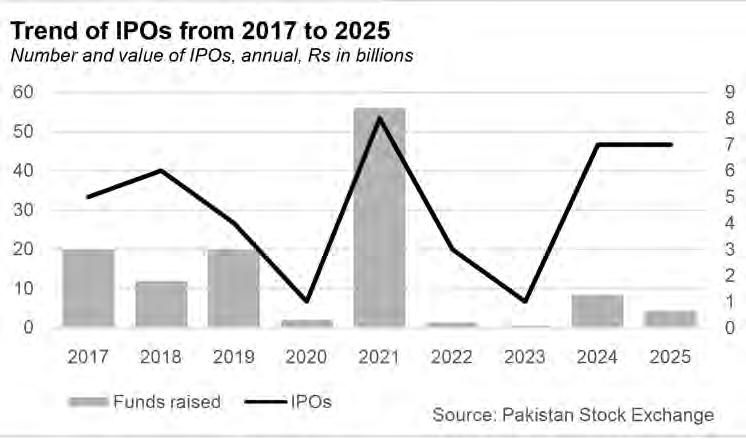

In terms of IPOs, the Pakistan Stock Exchange has seen two amazing years back to back. In 2024 and 2025, there were fresh IPOs carried out in each year which shows that investors had an appetite to invest additional funds and savings into the market. These IPOs came in these years as the market was going through a boom during this period which means investors are more receptive to new issues while the shares are also expected to perform better during a rising market.

While there was much cheer and celebration around the IPOs, there was another aspect of the stock market which was mostly ignored. This was the exact opposite of an IPO. As companies can ask for funds in exchange of ownership, they can also carry out buybacks where shares are bought from the investors in exchange for funds.

2025 saw a ramped up effort as Phillip Morris Pakistan and Gillette Pakistan announced that they were voluntarily delisting from the market. In addition to this, many companies also carried out share buybacks from the market. Both these activities meant that equity outflow from the market surpassed a value of Rs 16 billion.

The IPOs carried out in 2025 saw an investment of Rs 4.3 billion which were spread out 7 different issues. Over the course of the year, the investors transferred Rs 4.3 billion to the companies while the companies gave back Rs 16 billion to the investors. This shows that rather than investing these funds into new projects, carrying out expansion or seeing new avenues to yield additional revenues, the companies were happily giving back the funds they had taken from the public. Even though buybacks are considered as being normal, the quantum or

value of the buybacks do raise questions. What exactly are IPOs and share buybacks and how do these two things signal the worrying trend taking place at the stock exchange during 2026? Profit unpacks all of these elements.

Initial Public Offering (IPO) takes place when a private company offers shares of the company to the public. This converts the company into a public company where the shares are not only owned by the original sponsors but also held by the general public and investors. The purpose of an IPO is to generate funds for the company which is looking towards a source of funds other than the sponsors and the banks. Once the proceeds are generated, these are then used by the company for growth, expansion or additional investment that it might be contemplating.

In terms of the advantages of an IPO, the companies are able to raise funds and capital for themselves quickly which can then be utilized. In addition to that, IPOs shine a spotlight at the company and help build its brand image which can help its sales. IPOs also provide an early exit to certain investors in the company who might have invested at an earlier stage and want to cash out their investment. Once the shares are listed on the stock exchange, share issues carried out to employees can also make the company lucrative to many employees who might be interested in working for the company as well.

Lastly, the investors also benefit from the IPO taking place as they are able to invest in a company that they like and can get an ownership stake in the company. This allows them to become part of the company and have a say on how the affairs of the company are managed.

While there are many advantages, there are also a few disadvantages that have to be faced. First of all, getting listed and carrying out an IPO is expensive and can be a time consuming process. Once the listing has been carried out, financial reporting, carrying out disclosures, audit fees, maintaining investor relations and constituting committees also has to be carried out which can become onerous on a company. It can also take away some of the focus of the company which is already operating on limited resources.

An IPO also means that the real owners will lose some of the control that they held over the company in the past and that the decision making power will be diluted as outside shareholders invest into the company. Another issue is that disclosures have

to be made at regular intervals relating to internal matters which were hidden in the past but will have to be made now.

Regardless of the disadvantages, more IPOs and issues taking place at the stock exchange is seen as a positive sign as it shows that companies are ready to go to the investors in order to raise funds rather than looking towards other sources.

If IPOs are seen as a good thing, share buybacks can be considered as the exact opposite. In a share buyback, the company is looking to repurchase the shares that it had sold in the past and looks to increase the power and control of the original owners. There can be different reasons for carrying out a buyback.

Companies can feel that they can buy back and cancel the shares that they have bought back which can be used to increase the earnings per share it is reporting. Share buybacks are also able to increase stock price as the demand for the shares increases leading to an increase in the share price. There can also be instances where excess cash being maintained by the company can be used to buy back the shares which had been allotted for further investment or growth of the company.

The implication of such a buyback can be seen as being a positive and a negative. In terms of being positive, it can show that the company feels its share is undervalued and it is buying its own share in order to take advantage of this opportunity. This can also signal confidence of the company in its own shares. On the other hand, it can also signal that there is excess cash on the balance sheet and there is a lack of growth opportunities available to the company.

In terms of the stock market, a share buyback is considered a bad sign. The market feels that companies should look to gain

more funds from the investors and use them to grow and fund a larger number of their projects. Buybacks signal to the market that the company has exhausted the opportunities available to them and is stagnating rather than progressing.

The extreme case of this is when the company is not only buying back its shares but is also getting delisted which is asking to be removed from the stock market. This shows that the cost of staying listed and making disclosures is outweighing any benefit that the company is gaining and it is better for the company to get delisted.

In the case of voluntary delisting, the company is choosing to remove their shares from the public stock exchange and going back to becoming a private limited company. Voluntary delistings take place when the company announces to the stock market that they want to get delisted and offer to buyback all the shares that are held by the general investors. There can be many reasons for delistings to be carried out. Companies might want to take back full ownership over the decision making without disclosing or involving public scrutiny over their decision making. In addition to that, the company might feel that their stock is being undervalued and seeing lower volumes. By buying back the shares, the company can take advantage of the lower cost of its shares. A delisting can also serve as a cost saving as higher compliance, audit and regulatory fees can be avoided by taking the company private.

The market sees a voluntary delisting in the same manner as a buyback as it is seen as an outflow of equity. A healthy and vibrant capital market sees IPO issues taking place regularly while buybacks are seen as a negative against investment and functioning of a strong capital market.

During 2024 and 2025, there were different IPOs issues that were carried out at the Pakistan Stock Exchange owing to the market boom that was being seen. While this was a positive, the concerning fact was that the value of buybacks and delistings carried out dwarfed any investment that had taken place.

The situation prevailing in Pakistan is best summed up by Mohammed Sohail, CEO of Topline Securities who states that “(i)deally there should be more and more high value and quality listings. This is….not happening because of overall economic and stock market conditions. Since the start of bullrun,.... (only a few companies) think of doing mega IPOs.”

In regards to the delisting, he states “(d) elisting is relatively easy in Pakistan. Many companies (are) going out due to limited free float in the market and they have to follow strict listing and other conditions. Pakistan needs to re-visit de listings rules in line with global practices.

Lastly, talking about the buybacks, he says that buybacks take place “when share prices are low (which) is good for price discovery and to protect the minority shareholders value. SECP has made changes in buy back rules a few years back as a result many companies entered the market when prices were attractive.”

When Sohail talks about mega IPOs, the year 2021 comes to mind where issues of Rs 20 billion were carried out throughout the year. This included Airink valued at Rs 6.4 billion, Pakistan Aluminium Beverage Cans valued at Rs 4.6 billion and Panther Tyre of Rs 2.6 billion. Compared to just these three issues, the whole of 2025 saw issues of Rs 4.3 billion combined. There is a lack of quality

issues which are of large size which can be considered as the pool of investments getting bigger.

Yousuf Farooq, Director research at Chase Securities, feels that things are not as bleak as they seem to be. He says that “(v) aluations and financial conditions determine whether u will have IPOs or buybacks. When interest rates are low and market PE ratios are high, you have IPOs (as) capital gets formed. When interest rates are high and valuations are cheap, buy backs happen.” He further reiterates that this should not be cause of concern as it is just a reflection of valuation.

When asked whether the recent wave of buybacks point towards a bleak future outlook, Farooq states that “when sponsors buy back stock they think the future is bright. They also think it is very cheap. When sponsors sell stock, they think they (are) getting a good price.”

When IPO proceeds are lower than the combined value of share buybacks and delistings, it shows a net reduction in equity capital in the market. Imagine that the capital markets are a pool of funds that have been invested by the general public. Every IPO is able to add more to these pools of funds while every buyback acts as a leakage from it. In 2025, this pool shrank drastically for the country which meant companies had a lower amount of resources they could get access to. This phenomenon is known as the shrinking equity market.

This phenomenon states that there is a move in the market where market capitalization and equity is shrinking. As stated earlier, the pool of funds available for investors is shrinking as new issues are not able to take place of buybacks being carried out. With a shrinking supply of stocks and issues, there is an active outflow of capital as the market is returning the shareholders the investment that they had made earlier. In normal circumstances, there would be expectation that there would be a need to raise capital to fund the company which is being reversed.

Another reason for greater buybacks can be that the companies feel that their stocks are undervalued and they are increasing demand for their own stocks which provides a support to the price while also increasing the earnings per share in the short term. However, if this continues into the long term, it can signal to the market that the company has no new avenues of investment, research and development and is giving any excess cash to the investors. Basically, there is little value in investing and the shareholders can use their funds better on other options.

So who exactly is delisting or carrying out buybacks and why?

Phillip Morris 213,049 276,963,700 1,300

Gillette Pakistan 2,638,059 1,846,641,300 700

Ghani Global Glass 1,217,685 10,873,927 9

Netsol Technologies 2,690,251 419,987,923 156

Lalpir Power 100,000,000 2,471,295,000 25

Pakgen Power 185,000,000 11,100,000,000 60 Total buybacks Rs 16.125 billion

There are three main reasons why delistings and buybacks are being carried out and each category has companies which make a part of it. In terms of delisting, Philip Morris Pakistan and Gillette Pakistan are two companies who have applied to be delisted from the stock exchange. Phillip Morris is one company which is involved in manufacturing of tobacco products and has constantly felt that they are facing high taxation and competition from smuggled products. The company has raised these concerns on multiple occasions and feel that there is a two tiered system where they have to comply while the grey economy gets to evade accountability and compliance.

Gillette also feels that it is in a similar position as it is facing tough economic conditions, high operational tax and stiff competition from local brands like Treet. Both these companies feel that the economic conditions of the country are deteriorating steadily which makes investment and repatriation of profits difficult. In addition to these challenges, both these companies feel that by going private, they can streamline their operations and reduce their compliance costs. By getting delisted and buying back their shares, they will also be able to gain full control over their subsidiary.

Phillip Morris gave a price of Rs 1,300 per share to buy back 213,049 of their shares in the market costing them Rs 28 crores to carry out the delisting. Gillette Pakistan had made an offer to buyback 2.6 million of its shares at Rs 216 per share which was revised to Rs 700 per share. This would potentially cost Gillette Rs 1.8 billion if all the shares were sold to it by the minority shareholders.

The desperation of the company can be seen in the fact that they accepted this price which was at a premium of 224%. Phillip Morris also accepted the price at a premium of 90% from where the stock was trading at the time.

The second category of buybacks were carried out by companies who felt that their stock was undervalued and that they could enhance their shareholders’ value by carrying

out the buyback. These included the likes of Ghani Global Glass and Netsol Technologies. The board of both of these companies felt that the market was undervaluing their stock and that the shareholders would benefit if the excess stock was bought and cancelled.

The buybacks were going to provide support to the price by driving demand and they would be purchased as held as Treasury Stock which would boost the earnings per share. Ghani ended up buying 1.2 million of its shares at Rs 9 valuing at Rs 1 crore while Netsold repurchased around 2.7 million shares at Rs 156 each coming in at around Rs 42 crores in total.

The last category of share buybacks were carried out by companies which had recently lost out on their sole source of finance and saw that the market was undervaluing their shares to a greater degree. Lalpir and Pakgen power have recently seen their independent power producing contracts being ended by the government. These companies were relying on these contracts as their sole source of revenue. With the revenue stream ending, the market foresaw consistent losses for these companies leading to their share price plummeting.

As covered earlier, these power companies were trading at a price lower than their book values. In such a situation, the best course of action would be to buy back the shares and then decide the next course of action. If the business plan is not viable enough, the assets of the company can be sold and a premium can be earned due to the difference in market price and book value. Due to this, Lalpir sent out a buyback quantity of 100 million shares in the market at a rate of Rs 24.71 per share leading to a buyback of Rs 2.4 billion. Pakgen power issued a buyback of 185 million shares out of which it has already bought back nearly 180 million shares at a value of Rs 11.4 billion. The fact that this purchase alone of Rs 11.4 billion is three times the IPOs that took place shows how the equity shrank during 2025.

Based on all the buybacks carried out, the total value stood in excess of Rs 16 billion which leaked out of the market. This shows that 2025 can be considered a bad year in terms of the capital markets of the country. n

The sluggish pace of the economy, combined with extractive tax policies levied onto the corporate sector hit profit growth

Pakistan’s listed heavyweights managed to grow their bottom lines in 2025 – but only just. In a new sector-by-sector review of KSE-100 profitability, Arif Habib Limited (AHL) finds that the index’s aggregate net income rose 5.3% yearon-year in calendar year 2025 (CY25), reaching Rs1.56 trillion.

That headline figure comes with two important caveats. First, AHL’s dataset covers 69 companies, representing about 83% of the KSE-100’s market capitalisation (and “83% of the index weightage”, in the broker’s phrasing). Second, the year ended on a softer note: AHL records that KSE-100 profitability fell 2% YoY in 4QCY25, to Rs383 billion, hinting at the drag from still-tight demand conditions and uneven sector dynamics.

Still, the bigger story is what happened above and below the tax line.

AHL puts full-year KSE-100 net income

(profit after tax) at Rs1,558 billion – up 5.3% YoY.

Over the same period, the index’s pretax income (profit before tax) climbed faster: AHL calculates Rs2,863 billion of pretax income in CY25, up 8.2% YoY.

That divergence matters. When pretax profits are rising materially faster than net profits, the implication is straightforward: the “take” between the two lines is growing heavier – whether through higher effective tax incidence, the persistence of levies and surcharges, or simply the sector mix of who is making money and where taxes bite hardest. Pakistan’s fiscal story in recent years has leaned heavily on the documented economy, and Finance Act-style tweaks have often tightened the net through withholding taxes, compliance-driven disallowances, and sharper enforcement powers, even when headline rates do not change dramatically. (For example, KPMG notes the Finance Bill 2025 “relies on conventional approaches, such as increased withholding tax

rates across certain segments”.)

AHL’s third headline number is cash returns. It finds KSE-100 dividends reached Rs809 billion in CY25, up 22.8% YoY, taking the aggregate payout ratio to 52%.

The payout surge is important in a market where macro uncertainty can deter long-gestation capital expenditure, dividends are often the simplest way to keep investors interested – particularly when real returns elsewhere are volatile and the equity market is still rebuilding confidence in the policy mix.

Sector-wise, AHL shows banks were once again the market’s biggest dividend engine: bank dividends rose 35.3% YoY to Rs378 billion. E&P dividends were Rs146 billion, up 20%. Dividends fell 7.2% YoY to Rs72.7 billion.

AHL also flags some of the company-level names, in particular some with higher bank payouts with “major contributions” from MCB, NBP and UBL, continued semi-annual dividends at Mari Petroleum, and quality ones

from from OGDC in E&Ps, and stronger auto dividends from Indus Motors, Sazgar Engineering, and Honda Atlas Cars.

Which sectors had the highest growth in earnings was far from uniform. AHL lists the sectors driving the strongest net-income growth: investment banking (+50%), auto assemblers (+44%), miscellaneous (+36%), textile composites (+31%), and cement (+24%).

Autos: the comeback year (with tractors still one of the clearest “rate-cycle” beneficiaries. AHL says the auto assembler sector’s net income surged 44% YoY to Rs88 billion on a low base, helped by recovering volumes as inflation eased, reviving auto financing, new model launches, and stronger cash positions that lifted other income.

But the recovery did not lift all boats. AHL notes weak farm economics and flood-related disruptions – a reminder that Pakistan’s consumption story is rarely separable from its agricultural one.

Cement was a bright spot. AHL pegs cement-sector net income at Rs165 billion, up 24% YoY, driven by a 15% YoY fall in coal prices and a 14% YoY rise in dispatches. Add a drop in financing costs as interest rates came down adding to the cement earnings cocktail: expanding margins plus a lighter debt burden.

For textiles, raw material relief and cheaper money boosted a sector often buffeted by energy pricing, working capital stress, and shifting export demand – posted 31% YoY net-income growth to Rs13 billion. AHL attributes it primarily to lower cotton costs (local and imported) and declining finance costs.

The textile story is an instructive one for Pakistan’s macro environment shifts from “survival mode” to “breathing room”, the first visible improvement is often in working-capital-heavy sectors where financing is a cost of staying alive, not just a tool for growth.

For sheer weight, nothing comes close to banks. AHL shows banks account for 29.2% of the index weight in its sample, and delivered Rs639.7 billion of net income in CY25, up 10% YoY.

What makes that performance remarkable, AHL says the sector managed the jump on the back of expanding low-cost deposits, provisioning reversals, and a strengthening balance sheet.

In a year when the central bank’s easing cycle gathered steam, banks faced a familiar trade-off: lower rates can squeeze net interest margins, but they also tend to reduce credit stress and improve bond valuations. The result, in Pakistan’s case, was a banking sector that continued to throw off both profits and dividends – and, by extension, continued to dominate the index’s aggregate numbers.

AHL reports oil and gas marketing companies net income rose 10% YoY to Rs34

billion, supported by margin expansion, inventory gains, improved inventory management versus the same period last year, and lower finance costs.

AHL lists the laggards bluntly: refinery (-57%), REITs (-49%), power (-26%), chemicals (-20%), and E&P (-10%).

E&P were hit by lower oil prices, lower output, and higher costs. AHL shows net income of Rs331 billion of net income for the sector in CY25 – but the sector still saw a 10% YoY decline. AHL pins the fall on lower international oil prices, declining output amid production curtailments and weak power demand, and higher operating and royalty expenses (notably at MARI), alongside lower other income.

This is the resource-sector paradox in Pakistan: the sector is often really profitable, but their fate is tied to forces outside their control – global commodity prices, domestic demand destruction, and a circular-debt-plagued energy chain that periodically forces curtailments.

Power-sector net income fell 26% YoY to Rs45 billion. AHL attributes the decline to the termination of Hub Power Company’s contract with the state-owned power purchases, provisioning at NEL, and a lower share of associate profits after one-off gains in CY24.

If banks are the index’s steady anchor, power is its problem child: earnings can be stable when contracts are honoured and receivables are managed, and suddenly fragile when the state’s need to renegotiate, delay, or restructure becomes irresistible.

AHL’s sector table shows the sharp declines: refineries down 57% in net income, REITs down 49%, and chemicals down 20%.

The macro backdrop offers clues. Refiners are notoriously sensitive to margin cycles and inventory effects; REITs tend to struggle when real estate sentiment and financing conditions turn cautious; and chemicals can be hit hard by weak industrial demand and energy-related cost pressures. In a year when Pakistan’s growth remained subdued and large-scale manufacturing stayed under pressure, it is not surprising that these cyclical and rate-sensitive pockets were among the underperformers.

AHL’s “slow year” framing lands against a macro picture that, while improved from crisis peaks, remained far from buoyant.

Pakistan’s government estimated the economy grew 2.7% in FY25, after 2.5% the prior year – well below the country’s long-term growth needs – with output constrained by weakness in large-scale manufacturing and a decline in major crops. Even in stabilisation mode, the economy has struggled to sustain a broad-based expansion without running into the old constraint: imports rise faster than exports, the current account deteriorates, and the

policy stance tightens again. Finance Minister Muhammad Aurangzeb captured the official anxiety in a memorable line, warning against a consumption-led “sugar rush”.

Monetary policy has moved in the opposite direction – towards relief. By December 2025, the State Bank of Pakistan cut the policy rate by 50bps to 10.5%, explicitly noting that inflation had stayed within the 5–7% target range on average during July–November FY26. Reuters also reported that the SBP had delivered 1,100bps of cuts between June 2024 and May 2025, before resuming easing later in 2025.

This easing cycle helps explain some of the dispersion inside AHL’s sector results. Lower rates tend to show up fastest in:

• Consumer durables (autos), via cheaper financing and improved sentiment;

• Debt-heavy industrials (cement), via lower finance costs;

• Working-capital sectors (textiles), via breathing room on borrowing;

• and, more ambiguously, banks, where the margin squeeze can be offset by lower provisioning and balance sheet gains.

But the economy’s slower pulse – and the state’s revenue hunger – works the other way.

On taxation, the 2025 Finance Act targeted the same formal-sector base: corporates that can be easily documented. KPMG’s budget analysis of Finance Bill 2025 notes both the reliance on and the continued overlay of extraordinary measures (including references to windfall profit and super tax framework). PwC’s tax materials, meanwhile, highlight the drift towards tougher enforcement tools –including proposals allowing authorities to restrict bank account operations, bar the transfer of immovable property, and even seal business premises to compel sales-tax registration. And PwC’s corporate tax summary flags measures such as disallowances tied to cash sales and purchases from non-registered persons – the kind of rules that disproportionately fall on firms already inside the documented net.

Set that against AHL’s own numbers – pretax income up 8.2% versus net income up 5.3% – and even when corporate Pakistan grows profits, a meaningful share is being absorbed by the state, directly or indirectly, through a tax architecture designed to prioritise collection over competitiveness.

That, perhaps, is the real takeaway from AHL’s report. CY25 was not a disaster – Rs1.56 trillion of net income and Rs809 billion of dividends is hardly small change. But it was a year where Pakistan Inc advanced in patches rather than in stride: autos and cement found cyclical tailwinds; banks stayed dominant; E&Ps and power wrestled with the realities of the energy chain; and the economy as a whole is too fragile to sprint. n

The company exited its energy business, saw declines in its fertilizer business’ profitability, and continued losses in petrochemicals

Engro Holdings ended 2025 with the sort of headline number that makes even jaded Karachi traders sit up a little straighter. The conglomerate’s owners’ profit after tax surged to Rs55.6 billion, with earnings per share at Rs46.20, Topline Securities noted in its result review.

And yet, if you read the same Topline note a second time – slower, with a pencil –you realise the real story of Engro’s year is not a breakout, but a reset. Strip out the accounting effects of a one-off reversal tied to thermal energy assets and the year looks far more modest: owners’ profit after tax was Rs29 billion, or EPS of Rs24.13. That, Topline argues, is the number investors should use to judge how the machine actually ran.

Engro itself all but agrees. In its directors’ report, the company says consolidated profit after tax was Rs107 billion (with Rs55.6 billion attributable to Engro shareholders), and confirms that “much of the increase” came from reversing impairments recognised in 2023 and 2024 on thermal energy assets previously classified as “held for sale”. It adds that excluding this one-off impact, profit attributable to shareholders was Rs29,059 million, reflecting “core earnings”.

In other words: 2025 was not a year of pure expansion. It was a year of slowdown and consolidation, shaped by three big realities: fertiliser margins under pressure, petrochemicals still bleeding, and a corporate centre busy rearranging the group – down to the very share count – while digesting one of the largest investments in its history.

Topline’s framing is blunt. Engro’s reported 2025 result includes a “one-off impairment reversal on thermal assets”. The “clean” number is theRs29 billion in owners’ profit after tax. It is lower than the heade revealing. It tells you what Engro earned from the parts of the portfolio that sell urea, polymer, power, and services, rather than from the quirks of how a divestment attempt is treated in accounting standards.

The quarter that closed the year hints at the same tension between optics and operating reality. Engro reported Rs13.6 billion of profit attributable to equity owners in 4Q2025

(EPS Rs11.31), down year-on-year but sharply higher quarter-on-quarter, Topline wrote. The result came in above expectations was mainly due to lower than expected effective tax rate”.

That tax rate is now a broader theme for Pakistan’s large corporates: reported profitability can swing on changes in tax treatment, the timing of reversals, and the settlement of disputes – often as much as it does on sales volumes. Topline notes Engro’s effective tax rate was 18% in 4Q2025 (versus 27% a year earlier), taking full-year effective tax rate to 23% versus 40% in 2024.

Then there was the dividend, or lack thereof in one of the market’s most widely held names, Engro Holdings announced no cash dividend alongside the results, a decision Topline links to financing needs for the towers acquisition. That restraint is also part of the narrative of 2025 as a year for disciplined capital stewardship and integration, rather than for showy cash returns.

The details of those transitions sit in the subsidiaries.

Engro Fertilizers remains the group’s anchor – politically sensitive, economically essential, and often the first place investors look when trying to read Pakistan’s farm economy.

In its audited consolidated statement of profit or loss for 2025, Engro Fertilizers reported net sales of Rs237.1 billion, down from Rs256.7 billion in 2024. It posted profit before tax of Rs40.0 billion (down from Rs45.2 bil-

lion) and profit for the year of Rs22.6 billion, compared with Rs28.3 billion the year before. EPS fell to Rs16.95 from Rs21.16.

The company’s own letter to the Pakistan Stock Exchange is unusually candid about the reasons. It says profitability fell year-on-year due to a one-off super tax charge of approximately Rs2 billion, and “discounts offered… to maintain competitiveness and protect its market share”. It also points to volatility in the phosphates market, which resulted in “subdued domestic demand, lower margins and market share”.

This is what slowdown looks like in fertiliser: not a factory that stops running, but a market that forces you to choose between protecting margin and protecting share. In a year where farmers were under pressure and price sensitivity was high, Engro Fertilizers appears to have leaned towards defending volumes – even if it meant giving up some pricing comfort.

And yet, the business still throws off cash, the kind that props up a conglomerate even when other segments misbehave. The board recommended a final cash dividend of Rs4 per share (40%), in addition to interim cash dividends already paid at Rs11 per share (110%).

Operationally, the company also pointed to resilience beneath the weak headline: it said the urea market recovered later in the year, and that it delivered a 14% increase in locally

manufactured urea sales volume, while urea production rose 6.6% due to a focus on operational discipline and reduced turnaround days.

Topline’s snapshot of the fourth quarter adds a sharper edge: it notes Engro Fertilizers’ earnings were down 19% YoY in 4Q2025, primarily due to lower gross margins and the super tax adjustment.

Put together, the picture is clear. Engro’s fertiliser arm is still profitable and dividend-paying, but 2025 was a year of compression – lower sales, lower profits, and a market environment that forced the company to spend margin to defend position.

If fertiliser is the stabiliser, petrochemicals are the ache that never quite goes away.

Engro Polymer & Chemicals’ 2025 numbers show a business that managed to grow its top line, but could not translate it into profitability. Revenue from contracts with customers rose to Rs78.0 billion from Rs75.7 billion. But gross profit fell to Rs4.83 billion (from Rs6.59 billion), operating profit dropped to Rs2.34 billion (from Rs4.39 billion), and the company posted a loss for the year of Rs3.90 billion, compared with a loss of Rs160.6 million in 2024. Loss per share widened to Rs4.29 from Rs0.40.

Topline’s fourth-quarter commentary captures the volatility in miniature: Engro Polymer booked a consolidated loss of Rs446 million in 4Q2025, versus a profit of Rs2.1 billion a year earlier, as gross margins fell to 5.5% from 14.1% in 4Q2024.

In a country where energy pricing and industrial demand can be whiplash-inducing, petrochemicals are rarely a smooth ride. Even when volumes hold up, margins can collapse under input costs and pricing dynamics. The 2025 income statement suggests exactly that: costs rose faster than revenue, eroding gross profit.

For Engro Holdings, the implication is uncomfortable but familiar: polymers are not merely cyclical; they look structurally challenged in Pakistan’s current industrial ecosystem. Which is why, in a year of “consolidation”, Engro’s polymer losses become more than a subsidiary detail. They become a test of the group’s portfolio strategy: how long do you carry a loss-making industrial asset in the hope of a turnaround that requires more than just a better quarter?

Engro’s “exit” from thermal energy is, in truth, a story of an attempted exit that did not complete – and then boomeranged into the financial statements.

Topline summarises it succinctly: Engro had been divesting its thermal energy business and had booked accounting adjustments, but the share purchase agreement (SPA) was terminated, prompting the company to reverse those adjustments.

Engro’s directors’ report frames the same development as part of the year’s strategic backdrop. It notes that thermal energy assets were retained within the portfolio following the termination of divestment agreements, restoring an “important source of operating cashflows”.

This matters for two reasons.

The first is operating an energy business in Pakistan is never just an asset class; it is a negotiation with the state’s energy chain – capacity payments, fuel pass-throughs, circular debt, and the politics of tariffs. Retaining thermal assets means Engro is still exposed to that ecosystem, with all its risks and cashflow dynamics.

The second is financial. The termination of the divestment process changed how the assets were treated under accounting rules, producing the impairment reversal that inflated reported profit. Engro explicitly says the year’s higher earnings were largely driven by reversing impairments recognised in 2023 and 2024 on thermal assets that had been classified as “held for sale”; excluding this one-off, core earnings were Rs29,059 million.

This is why a magazine reader should care about what sounds like accounting mechanics: it is the dividing line between a year of steady earnings and a year of spectacular growth. One is a genuine operating outcome; the other is partly an accounting echo of a deal that failed to close.

For investors, it also colours what “consolidation” means. Engro was not only consolidating a new holding-company structure; it was also consolidating its asset base – accepting, for now, that thermal energy remains inside the portfolio even as it tries to tilt towards other infrastructure plays.

Engro’s origins are industrial, but its modern identity is increasingly financial: a capital allocator trying to compound cashflows per share in an economy where longterm planning is frequently interrupted by macro shocks.

That tension sits at the heart of the group’s recent restructuring. In May 2024, Engro announced that the boards of Dawood Hercules Corporation and Engro Corporation had approved, in principle, a restructuring designed to “enhance investment opportunities” by harmonising investment efforts. The plan would result in Dawood Hercules being rebranded as Engro Holdings Limited, with Engro Corporation becoming a wholly owned subsidiary – while minority shareholders of Engro Corporation would become shareholders of Engro Holdings via an exchange ratio intended to preserve economic ownership.

Engro’s directors’ report positions 2025 as the year that structural alignment became real. It says the consolidation of Engro Corpo-

ration as a wholly owned subsidiary simplified the group’s ownership structure and strengthened capital allocation flexibility.

It also provides the technical detail that helps explain why headline EPS comparisons can mislead. Effective 1 January 2025, Engro Corporation became a wholly owned subsidiary; as a result, profit attributable to owners now reflects 100% ownership versus 39.97% last year, and 723 million new shares were issued, expanding the base and affecting EPS comparisons.

In plainer language: Engro did not merely “have a year”. It changed the shape of the entity that markets are valuing. That makes a tidy, year-on-year reading of earnings less useful than an understanding of what the company is trying to become.

And what it is trying to become is best captured by the other major milestone in the directors’ report: the acquisition of Deodar, which it calls a significant capital deployment that increases exposure to telecom infrastructure. The company says its priority is disciplined integration – improving utilisation, strengthening commercial execution, and enhancing cash generation over time.

Topline’s note hints at the financial discipline behind that ambition: no cash dividend was announced “to finance its tower business acquisition”. It is a choice that will not thrill every shareholder, especially those who have historically treated Engro as a quasi-income stock. But it fits the internal logic of consolidation: conserve cash, fund the big bet, and prove the integration before you resume generous distributions at the holding-company level.

So, what does the full Engro story look like at the end of 2025?

It looks like a conglomerate whose reported profits were flattered by an accounting reversal, whose core earnings were steady but not spectacular, whose fertiliser champion took a profitability hit while staying cash-generative, and whose petrochemicals business continued to lose money even as sales rose.

It also looks like the conglomerate is consciously reshaping itself – simplifying its structure, recalibrating its portfolio, and pushing into telecom infrastructure – while keeping one foot in the messy realities of Pakistan’s energy economy.

That is why “slowdown and consolidation” is not a euphemism. It is a description of a year in which Engro chose to spend capital and managerial energy on becoming something – rather than on delivering a single, clean, headline-grabbing growth number.

And in Pakistan, where the macro environment can turn quickly and capital is always contested, that may be the most important result of all. n

On Friday, leading value-added textile exporters walked into a commerce ministry meeting with a message that has grown harder to ignore: Pakistan’s biggest export sector says it is being priced out by high input costs, financed too tightly to fulfil orders smoothly, and forced to operate under rules that change too often for international buyers’ timelines.

Commerce Minister Jam Kamal Khan and senior officials were presented a list that has become the industry’s standard brief— upfront taxes, elevated energy tariffs, infrastructure constraints, and a liquidity squeeze worsened by refunds that remain pending. Exporters argued that these pressures have started showing up directly in export outcomes, with the ministry meeting framed around consecutive declines in value-added textile exports.

What made this meeting different was less the content than the urgency behind it. In the exporters’ telling, the old obstacles are no longer temporary irritants that can be managed quarter to quarter; they have become structural constraints that, over two decades, helped Pakistan lose ground to regional competitors that built scale, improved reliability, and locked in policy stability long enough for firms to invest with confidence.

The demands presented to the commerce ministry can be grouped into a simple proposition: exporters want the state to stop tying up cash, stop raising the cost of production, and stop making compliance a moving target. In the short run, they want working capital to flow more predictably, and trade facilitation schemes to be designed around the realities of buyer contracts and production cycles rather than administrative convenience.

The most immediate pain point is liquidity. Industry representatives told the ministry that pending refunds and upfront taxes combine to trap cash inside the system— money that would otherwise pay suppliers, wages, and utilities, or finance raw material for the next order. When that cash is delayed, even exporters with confirmed orders can find themselves scrambling for short-term credit to keep production running.

Energy costs sit at the center of the competitiveness argument. Exporters pointed to elevated power and gas tariffs as a direct hit to unit costs, and argued that Pakistan’s pricing puts it at a disadvantage against regional rivals that run mills with cheaper energy. Based on interviews across the value chain, energy is the

dominant constraint in upstream processes like spinning and weaving, where electricity-heavy machinery drives conversion costs.

Financing is the third leg of the industry’s case: the sector says it is not just paying more for energy and taxes, it is also being constrained in how much it can borrow against export business. At the ministry meeting, exporters highlighted what they described as inadequate credit limits under the Export Finance Scheme, saying the ceilings restrict access to working capital needed to turn orders into shipments.

Alongside the big-ticket items, exporters pushed on bottlenecks that look technical but matter day-to-day. They raised limitations of the Temporary Importation Scheme, including reduced utilisation periods, arguing that the timelines and constraints make it harder to import inputs temporarily, process them, and ship finished goods in sync with buyer schedules. They also pointed to frequent policy changes as a cost in themselves, because a shifting rulebook turns long-term planning into guesswork.

The commerce ministry’s response was to restate government support for a sector described as a cornerstone of exports and employment. The ministry also said a dedicated technical committee had been constituted to review the limited utilisation period under the Export Facilitation Scheme and to recommend immediate remedies.

A separate but telling demand came from

representatives of micro, small and medium enterprises: they urged the State Bank of Pakistan and Exim Bank to issue explicit regulatory guidelines so commercial banks uniformly accept foreign master letters of credit as collateral when opening back-to-back letters of credit. The goal, exporters argued, is straightforward—unlock working capital so smaller exporters can execute orders without tying up scarce cash or relying on uneven bank-by-bank discretion.

Taken together, the task maps to a familiar export-sector playbook: reduce the cost base, stabilize rules, and make shortterm liquidity less fragile. But the context in which these demands are now being repeated is shaped by a longer story—how Pakistan’s textile model evolved, where it stalled, and why the gap with rivals has widened.

Pakistan has long been a textile economy in a literal sense—cotton cultivation and textile production are deeply embedded in its history, and textiles remain the country’s largest export-oriented sector, accounting for roughly half of exports in many years. That dominance, however, has not translated into sustained momentum in global market share, particularly compared with countries that built large, policy-supported export machines around apparel and higher-value products.\

The competitive reversal is stark: in 2003, Pakistan’s textile exports were reported at $8.3 billion, compared with Vietnam at $3.87 billion and Bangladesh at $5.5 billion; today, Vietnam and Bangladesh are reported at roughly $46.68 billion and $47.96 billion respectively, while Pakistan has struggled to cross $20 billion over the past five years. The point is not just that rivals grew faster—it is that they built enough reliability and cost discipline to scale to levels Pakistan did not reach.

The industry’s timing is also linked to a supply-chain squeeze that begins far upstream: cotton. Pakistan’s cotton output has fallen sharply over two decades, citing a drop of about 65% from 14 million bales in 2005 to 5 million bales last year, alongside shrinking cultivation and problems tied to seed resilience and changing conditions. As domestic cotton became less dependable, the industry increasingly relied on imports to fill gaps—an adjustment that can work, but one that adds exposure to global prices and currency dynamics.

Energy costs remain central because they hit precisely where Pakistan has historically had scale: spinning, weaving and processing. Even if the exact competitive gap varies by contract and tariff category, the strategic claim is consistent: when upstream conversion costs

rise, the entire chain becomes less viable, and value addition downstream cannot compensate if the base is too expensive.

Taxation and refunds complete the picture. This is a system in which exporters face multiple tax burdens and, critically, delays in getting refunds that are supposed to neutralize taxes embedded in exports. The industry’s argument is that many countries either do not tax exports or ensure refunds are timely, whereas exporters in Pakistan spend time and working capital navigating refund bottlenecks. That complaint closely matches what exporters raised at the commerce ministry meeting: upfront taxes and liquidity pressures from pending refunds.

What turns these issues into a moment of heightened pressure is how they interact. High energy costs raise the cash needed to run a unit. Tight financing limits how much of that cash can be borrowed against future export receipts. Upfront taxes and delayed refunds keep more cash locked away. And policy uncertainty raises the perceived risk of investing in new machinery, materials, or product lines that might take years to pay back. None of these constraints, on its own, is necessarily fatal; together they can make even a strong order book feel precarious.

This is where the exporters’ demand for policy consistency becomes less rhetorical and more operational. Apparel exporters plan seasons; buyers plan assortments; factories plan capacity, staffing and input procurement months ahead. If energy pricing, scheme rules, or tax mechanics change frequently, the burden is not just higher cost, but the inability to promise reliability—something regional competitors have often sold as their core advantage.

The near-term outcome hinges on whether the government’s process steps translate into bankable policy changes that exporters can price into contracts. The technical committee on the Export Facilitation Scheme utilisation period could produce quick wins if it results in timelines and procedures that match production realities and reduce compliance risk. But exporters will likely judge success less by committee formation and more by whether shipments become easier to finance and execute.

On financing, clearer guidance on accepting foreign master letters of credit as collateral for back-to-back LCs could be especially consequential for smaller exporters. If banks apply a uniform standard, it could widen access to working capital for firms that have orders but lack spare collateral. In practice, that might shift the system from one where only large players can smoothly convert demand into

exports, to one where mid-sized and smaller firms can compete on delivery and responsiveness—two metrics international buyers value as much as price.

On the cost side, the hardest issue is energy, because it intersects with broader fiscal and power-sector constraints. The industry’s argument is that upstream textile competitiveness depends on electricity pricing that does not leave Pakistan structurally above peers, especially where energy accounts for a large share of conversion cost. If that gap persists, the likely adjustment is not simply lower margins—it is reduced investment in upstream capacity, more closures, and greater reliance on imported inputs, all of which can make the sector more vulnerable.

Tax mechanics and refunds are often framed as administrative problems, but they can function like a shadow interest rate on exporters. When refunds are delayed, exporters effectively finance the state for months using their own working capital. That raises the cost of doing business even if headline tax rates are unchanged, and it forces firms to choose between borrowing more (if they can) or scaling down. If the liquidity knot is not loosened, a plausible outcome is a continued pivot toward domestic sales, where cash cycles can be faster and compliance burdens may feel more predictable.

Longer term, the direction of travel depends on whether Pakistan can align the entire value chain—cotton, energy, taxation, and export facilitation—toward a stable export strategy.

There is also a more immediate reputational risk that exporters worry about but rarely state plainly: international buyers can tolerate one-off delays; they adjust away from countries they view as unpredictably expensive or operationally uncertain. The exporters’ emphasis on policy churn signals an anxiety that Pakistan’s problem is no longer just cost, but reliability. If buyers bake Pakistan risk into sourcing decisions, recovery becomes harder because lost orders can take multiple seasons to win back.

The next few months will likely test whether the government’s engagement is moving from listening to redesigning. Exporters are not asking for a single concession; they are asking for a coherent operating environment—one where power and taxes do not surprise them, refunds do not trap cash, and financing rules allow confirmed orders to become production schedules. If those pieces move together, exporters argue, Pakistan can stop sliding and start competing again. If they do not, the sector’s warning is that the slow drift—closures upstream, underinvestment, and falling behind faster-growing rivals—could become the new baseline. n

An economic experiment covering over 1,200 Pakistani companies shows that subsidising female hiring helps overcome biases results in better pay, real contracts, and long-term culture shifts

Pakistan faces a massive economic puzzle. While the global average for women’s labor force participation sits around 50%, in Pakistan, it is a dismal 24.3%, compared to a staggering 80.3% for men.

For decades, policymakers have tried to fix this by focusing on the supply side: educating women, improving public transport, or offering childcare. But a groundbreaking new study flips the script and asks a harder question: What if the real bottleneck is the boss?

Employers often hesitate to hire women due to expected organizational “costs”—like building separate bathrooms, revising HR processes, or dealing with societal norms—or simply due to plain old bias. Researching wage subsidies—essentially paying an employer to take a chance on a female hire—is a radical but necessary way to test if financial incentives can break through these “demand-side” walls and force companies to change their hiring habits. To find out, World Bank researchers teamed up with Rozee.pk, Pakistan’s largest job portal, to run a massive experiment on 1,227 firms.

The researchers approached firms posting entry-level and mid-level professional jobs and offered them a deal: a six-month wage subsidy if they hired a qualified woman instead of a man. But rather than just handing out a flat rate, they made the hiring managers “bid” on the absolute minimum subsidy they would need to make the hire. The results were eye-opening.

Bias is cheaper than you think: Managers didn’t need the government to pay the entire salary. On average, a mere 15% wage subsidy was enough to

offset their hesitation and equalize their hiring choices. The cash works: Overall, the simple offer of this temporary subsidy caused a 10.7 percentage point surge in the likelihood of a firm hiring a woman.

Cracking the “Boys’ Club”: The most dramatic results came from historically male-only companies. For firms that previously had zero female employees, the subsidy boosted female hiring by a massive 17 percentage points. The cash acted as an insurance policy, convincing hesitant managers to finally take the leap and realize the benefits of a diverse workforce.

Better pay and real contracts: Firms actually passed some of that free cash onto the women. Hired candidates saw a 7.4% bump in their starting salaries and were more likely to be given a formal employment contract.

The Long-Term Shockwave

The best part of the study is what happened after the money ran out. This wasn’t just a short-term cash grab.

When researchers checked back 18 months later—long after the six-month subsidy had ended—treated firms were 13 percentage points more likely to still have a woman working in that specific role. Even better, the experiment actually shifted corporate culture. After experiencing female talent firsthand, these companies were 5.5 percentage points less likely to explicitly state a “male preference” in their future job postings.

By temporarily paying bosses to overcome their own biases, the experiment proved that a small financial nudge today can permanently open the door for the women of tomorrow. n

The digital media channel backed by property tycoon Malik Riaz set to change hands just over a year after it was first launched. What does ARY plan to do with it?

The ARY Group is set to buy Nukta, the digital media company launched by Kamran Khan and bankrolled by property tycoon Malik Riaz.

A senior official at

Nukta confirmed to Profit that the deal was next to done, although “a few final details were yet to be finalised.” If the sale goes through and is announced, it will mark the formal end to Malik Riaz’s longstanding ambitions to own a media business.

It is not yet clear what the nature of the sale will look like, nor has a price tag emerged. However initial reports indicate that it is an extensive deal that will also involve Kamran Khan receiving a prime time television programme on ARY. Before

this, Mr Khan has served long stints first at Geo News and then at Dunya News. It is understood that Malik Riaz backed off from funding the project some time ago and Kamran Khan along with his family has been running the place on his own.

The withdrawal of funding from Malik Riaz has had Nukta on the ropes for the past few months with major layoffs taking place in November 2025. The company announced back then they were laying off 37 individuals, mostly reporters and cameremen, because of budget cuts. Not only were the individuals laid off, more rounds of lay offs followed.

Nukta was officially launched in November 2024 with its headquarters in Dubai. The platform bills itself as a digital media platform and began operations with an extensive team of professional journalists picked from media houses across the country.

Before its launch, Nukta recruited aggressively and spoke to some of the biggest names in Pakistan’s news media. The head of the organisation is senior journalist Kamran Khan. In Pakistan, they had started the hiring process as early as December 2023. Many journalists were in talks with Nukta, although some backed out when rumours emerged that the main investor behind the platform was real estate developer Malik Riaz.

Malik Riaz has long been interested in acquiring a media organization in Pakistan. The trend of real estate developers acquiring media organizations has seen a rise in recent years, with one of the more significant transactions being Aleem Khan’s purchase of the Samaa TV. The idea has been that acquiring some form of news media gives the owner a mouthpiece.

Back in 2023, Malik Riaz had been in talks to buy the Express Media Group as well. Reports from the time suggested that a formal agreement was even reached between the parties, but the deal was ultimately blocked by government agencies. At the time, Anwar Kakar’s caretaker cabinet was in power and the transaction did not receive the necessary security clearance for the transfer of the broadcast license and the deal fell through.

In earlier attempts, he also launched an Urdu Daily Newspaper called “Roznamah Jinnah” which also flopped and was shut down. Later an attempt to run a television channel with senior journalist Aftab Iqbal was also made.

Following this setback, Riaz invested

in launching Nukta, a digital-only news platform that promised a new model for journalism in the region. It was a project on a major scale. Not only did Nukta begin in Dubai and hire a vast number of senior journalists, they also brought in corporate professionals and people outside journalism to give Nukta the boost it needed to immediately become a brand name.

The business model of Nukta was based on revenue from platforms like YouTube and other online advertising income. They also wanted to organise events, provide consults and digital media services to clients directly. However, with no subscription system and a very large team, the idea was that Bahria Town’s financial support would be able to sustain Nukta while it made a space for itself in Pakistan’s media landscape.

Some journalists were told Nukta’s investors had guaranteed they had the appetite to invest in it without any returns for two to three years. Backed by what was assumed to be the bottomless financial support of the Bahria Town owner, the platform began operations from Dubai and Pakistan. However, the launch coincided with financial woes for Malik Riaz. The real estate tycoon’s Pakistani assets were seized by the state. With outstanding fines of billions of rupees, Malik Riaz’s troubles have only grown.

“Malik Riaz decided to pull out early. He was bankrolling the whole thing but then he ran into trouble with the Pakistani government,” says one Nukta insider. “I think he got his hands on a media organisation too late and Nukta did not have the kind of heft he needed to fight back the allegations against him,” they added.

In a year, Nukta definitely managed to make space for itself in Pakistan’s media landscape. With 168,000 YouTube subscribers and nearly 4000 videos produced in just over a year, Nukta has done some solid work through its large team of journalists. However, to develop this team they paid exorbitant salaries. Nukta’s hiring philosophy was simple, whatever a journalist was already taking you offer to double it. But because of the large scale of their operations, including offices headquartered in Dubai, the costs were too high.

Nukta’s employees, who now have a high salary tag but not clear job security, are naturally concerned. There is no clarity over whether ARY will gut Nukta or keep it as it is. When layoffs took place back in November, Information Minister Atta Tarar had said he would hire all 37 of the laid off individuals. However, only seven journalists

were hired for a government owned English language digital media channel that was supposed to rival Nukta but with a drastically trimmer team.

For the ARY Group, acquiring Nukta would add a ready-made digital news operation to an already expansive media portfolio. ARY operates one of Pakistan’s largest private television networks, including news, entertainment and digital verticals, and has an established footprint on YouTube and other social media platforms.