18 32

18 32

10 Pakistan’s Economic Path; where short run keeps beating the long run

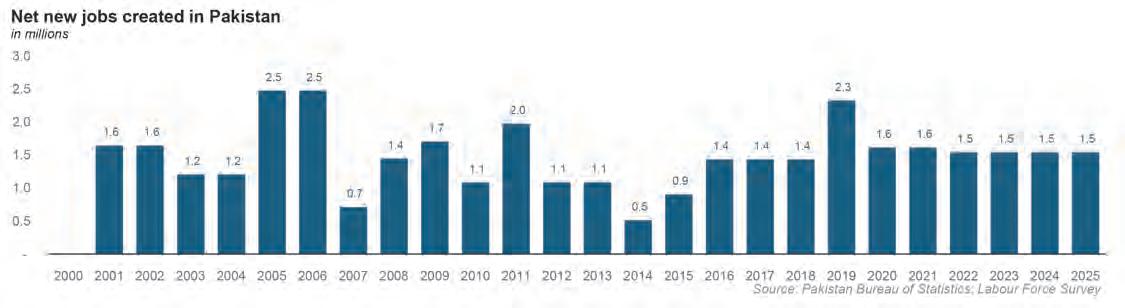

12 How big is Pakistan’s job creation engine?

18 Pakistan’s banks have agreed to give hefty discounts on loans to exporters. Here’s why

23 A proposal to base household electricity rates on income instead of usage is in the works. Here’s why it might make sense

26 How crypto is banking the unbanked in Pakistan Maha Shah

28 Most of Pakistan’s oil refining capacity goes unused. Could selling fuel to ships make them productive?

31 FBR to auction Bahria Town’s 527 kanals in Murree on 5th March. But what exactly has led to this action?

32 Action taken against scammers impersonating military officers to defraud inDriver courier delivery riders

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Usama Liaqat Shahab Omer | Zain Naeem | Nisma Riaz | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing: Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi)

Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Inside the ABF-LUMS’ policy dialogue where experts’ follow-through collided with a harder question: what actually makes reform stick?

The economic landscape of Pakistan is one marked by both challenges and potential. One that eludes stability but manages to remain afloat till the next big scare. What makes us such an economically vulnerable country is a question that has been answered by many, in

whatever way it suits them. However, what would it take for all those answers to be on the same page?

In a critical and thought-provoking session at the Economic Policy Dialogue, held by the American Business Forum (ABF) and LUMS, policymakers, academics, and industry leaders gathered to discuss the nation’s

path forward. Not the first of its kind, the dialogue still held significance in terms of its guest panel.

Featuring in it was Dr. Stefan Dercon, an Oxford University development economist who laid bare the stark reality of Pakistan’s economic situation. Followed by the subsequent panel discussion that drew

out practical insights from the private sector and government representatives. A candid exchange of ideas, solutions, and the hard truths about the economy’s fundamental weaknesses.

Here’s the bottom line: Pakistan’s economy needs deep structural reform, not just quick fixes or temporary measures. Dercon’s address focused on the need for long-term solutions, and the panel discussions illuminated the real-world complexities of said solutions. The intersection of public policy, private sector growth, and the importance of consistent, coherent economic strategies was discussed and it was agreed that all of this would require iron-clad political will.

In his opening address, Dr. Stefan Dercon painted a picture of Pakistan’s economic stagnation, comparing its growth to that of neighboring countries. He highlighted that in the last 30 years, Pakistan’s productivity growth had been one-tenth of what Vietnam had achieved and one-fifth of India’s. These numbers, although disheartening, provided the necessary backdrop to his core message that structural change is paramount.

For Pakistan to escape its growth trap, Dercon emphasized that the country must stop relying on short-term solutions. He pointed out, the country’s export-to-GDP ratio remains among the lowest in Asia, with Pakistan’s exports representing just 10% of its GDP, underscoring over-reliance on external financial aid.

Dercon’s critique of short-term fixes was sharp. He argued that Pakistan’s policymakers have historically leaned too heavily on quick, temporary measures. Fiscal stimulus packages, arbitrary tax cuts, and other measures meant to boost growth for a short time.

He compared these approaches to “quack remedies,” medical solutions that offer immediate relief but fail to cure the underlying problem. For Pakistan, this meant a recurring pattern of attempting to patch up a broken system rather than confronting the deeper structural issues at play.

The private sector has long been caught in this cycle, with companies scrambling to survive from one year to the next, wary of sudden policy reversals. For businesses, this means constantly adjusting to ever-changing regulations, which prevents strategic, long-term planning and limits growth. Dercon’s proposal to focus on structural reforms rather than short-term stimulus packages resonated with Naseer, who called for “clear and consistent policies” to provide stability in the business environment.

As the representative of the business community, Ali Naseer of Jazz offered a unique perspective on the challenges faced by the private sector in Pakistan. His company, Jazz, one of the largest foreign direct investors in the country, has weathered many economic storms. However, he expressed frustration at the lack of a stable, predictable policy environment. “In Pakistan, the government often makes policy decisions in isolation, without fully considering the impact on businesses,” Naseer noted.

He explained that policy certainty was crucial to long-term business growth, which is why companies are often hesitant to make big investments. The business community is constantly at the mercy of fluctuating government policies, which undermines trust and confidence. As Naseer aptly put it, “Stability, not unpredictability, drives investment.” When policy changes are frequent and abrupt, businesses are left with little incentive to invest for the future, opting instead for strategies that ensure survival in the short term.

In discussing Pakistan’s competitiveness, Naseer also touched on the country’s failure to embrace its manufacturing potential, particularly in industries like automobiles. Pakistan’s auto sector has struggled to grow despite being a key part of the economy. He argued that countries like China and India had embraced manufacturing on a large scale and leveraged that to fuel exports, while Pakistan missed the opportunity to do so.

One of the key points raised during the panel discussion was the role of government in fostering a conducive environment for business growth.

Bilal Azhar Kiyani, state minister for finance and railways, emphasized the importance of engaging with the private sector to ensure that policies are well-suited to market realities.

He tried to make a case for the Prime Minister’s initiatives to consult with various sectors, including SMEs, international businesses, and academics, to create a more inclusive policy-making process.

Bilal also addressed the challenge of policy consistency and acknowledged that, despite the government’s efforts, Pakistan still lacks a coherent, unified economic plan.

While efforts are being made to draft a comprehensive strategy, there is still a lack of alignment between ministries and sectors. This disconnect hampers effective policy execution and delays necessary reforms.

Dercon had highlighted the importance of opening up Pakistan’s economy to global competition, and this point was reiterated by several speakers.

Private sector leaders like Naseer argued that Pakistan’s economic competitiveness must be redefined. Pakistan needs to capitalize on its unique strengths, which include its geopolitical position, young population, and growing consumer market. By focusing on high-value exports and leveraging the global value chain, Pakistan could become a more attractive player in global markets.

However, the government and private sector must work together to ensure that the right sectors are prioritized for growth. While manufacturing has been a missed opportunity, telecommunications, agriculture, and technology offer promising avenues for Pakistan’s future. By making the necessary investments and creating the right policy frameworks, Pakistan can build a competitive advantage in these sectors.

Dercon’s closing remarks called for Pakistan to stop being a follower and start becoming a leader in the global economy. The panel discussion further illustrated the delicate balancing act required to turn this vision into reality. Both the private sector and government must work in tandem, ensuring policy stability, open market competition, and long-term strategic investment.

The road ahead may not be easy, but the discussions at this dialogue highlighted the critical need for structural reforms, policy consistency, and collaboration between business and government to foster a thriving, competitive economy.

The Pakistan Economic Policy Dialogue, while filled with complex discussions revealed a unified message: Pakistan must embrace structural reforms if it is to secure its future in a rapidly changing global economy. The country must shift from short-term solutions to deep-rooted reforms, particularly in export-led growth and policy consistency. The private sector, government, and academia must all play their part in this transition.

Only with clear policies, long-term goals, and strategic partnerships can Pakistan hope to become a leader in the global economy.n

Pakistan’s youth bulge needs jobs. How robust is the country’s capacity to create those jobs, right as the demographics sit on the verge of creating the second largest labour force expansion in the world over the next three decades?

By Farooq Tirmizi

The good thing about World Bank President Ajay Banga’s visit to Pakistan is that it got the nation talking about job creation, and how many jobs the country needs to create over the next 10 years. The bad news is that it never occurred to any Pakistani journalist to ask: how many did we create over the last 10 years?

Perennial optimists that we are, it is not our contention that Pakistan is creating enough jobs. But when such conversations come up, it is important to understand just how far off Pakistan is from its goals. To talk about how much Pakistan needs to do without having some baseline as to how much the country is doing now is to present an overly pessimistic picture.

So without further ado, here are the stats: over the past 10 years, Pakistan’s economy created a net 16 million new jobs, based on Profit’s analysis of data from the Labour Force Survey published by the Pakistan Bureau of Statistics. That represents a 28% increase in the number of jobs in the economy relative to where they were 10 years ago.

Ajay Banga, relying on estimates from the World Bank and corroborated by local economists, estimated that Pakistan needs to create a net 2.5 million to 3 million new jobs per year over the next 10 years. That would require the workforce to expand by between 32% and 38% relative to its level in 2025.

The current rate is, of course, lower than that, but perhaps by less than one might have expected. But one suspects that you may think that given the fact that we need to increase the number of jobs by 32% in the next 10 years (on the low end) and were able to do 28% over the past 10 years, the “gap to goal” is not as wide as the public discourse might have suggested.

As we will demonstrate, a 32-38% increase in the number of jobs over the course of a decade is not a goal that is completely out of reach for Pakistan. Indeed, in some decades, Pakistan’s economy has even exceeded

that number.

And as we will delve into this article, it is not just the quantity of jobs that is increasing in Pakistan, it is also their quality. But first, let us take a look at what the current state of the Pakistani job market is, and what needs to improve.

Economic commentary in Pakistan tends to focus on both the need to create jobs as well as the level of income offered by those jobs. This perspective is skewed by the college-educated elite who tend to do most of the talking about Pakistan’s labour market.

The reality facing the vast majority of Pakistanis hitting the job market is the following: low pay, high uncertainty. Consider the menu of options available to the vast majority of Pakistanis. There is the option of being self-employed and taking a risk every single day for how much money you can earn. There is the option of being a day labourer, which has at least some predictability with respect to income levels, but no security: you do not get paid on a day you are sick and cannot work.

And then there is the option that a majority of women in the labour force (55% to be precise) must live with: being unpaid labour helping male family members with their work on a farm, which your family may, or may not own.

Pakistanis are not just poor: the vast majority of us live with low wages and uncertainty of even receiving those wages. Quite simply, that is the worst of all worlds.

The precarity of most employment in the country is best understood in times of economic duress. Consider, for example, the year 2018 and 2019, when the economy suffered a major crisis at the end of the third Nawaz Administration. The number of net new jobs created in fiscal year 2019 was 2.3 million, but that number hides a glaring weakness. During that same year, 2.4 million people moved back from their

urban and non-agricultural jobs back to the farm: agricultural employment rose that year.

Had it not risen by that much – had people in Pakistan not had the option of going back to their ancestral village and working on their own or a relative’s farm – total employment in the economy would have dropped by about 100,000 jobs, which is bad enough in any economy but disastrous in one like Pakistan where the labour force increases in size by over 1 million people per year.

The same thing happened in 2008 and 2009, when roughly 2 million people moved back to the family farm owing to economic conditions. The land really does feed the people of Pakistan in their hard times.

But those return-to-the-farm jobs are most likely a favour done by family members to each other, and not sources of economic security and advancement. Family ties substitute for economic growth.

We are also able to use this “return to farm” movement in the labour force to estimate the degree of distress in the economy. Over the four years between 2021 and 2025, the total number of people who returned to agricultural employment was about 1 million people, which suggests that many people left cities due to a lack of job opportunities.

And even that 1 million number may underestimate the amount of distress: during the last economic boom between 2014 and 2018, a net of 1 million people left the agricultural labour force. Had the economy been doing better, one suspects that a similar number might have left over the past four years, but did not. That 1 million who did not leave the village need to be added to the 1 million who moved back.

Before diving into how many jobs Pakistan needs to create, it is important to lay out some context: over the next 25 years, the three countries that will see

the biggest increase in the size of their labour force are, in order, India, Pakistan, and Nigeria.

Yes, you read that correctly: between now and 2050, the country with the second largest expansion in the size of its labour force is Pakistan. Over 90 million people will reach working age (between 25 and 64 years of age) over the next 25 years, second only to India’s 144 million. Not all of those 90 million people will join the workforce in Pakistan, especially since female labour force participation rates in Pakistan are considerably lower than both global and regional averages.

But that expansion in the size of the workforce represents a major opportunity, especially since, based on current school enrollment rates, one can assume that about 90% of the increase in the size of the workforce will be literate, meaning they are likely to be able to engage in manufacturing and services employment beyond basic labour.

And while India’s labour force will increase by more people in absolute numbers, that increase represents a much smaller percentage increase in India (about 20% over the 2025 levels) compared to Pakistan, where our working age population will increase by just over 50% during that same time period.

What this does mean, however, is that Pakistan’s ability to generate employment for these people who are currently just babies or very young children is much more important to our development than other countries.

For a country like India, creating jobs is now something that happens in the ordinary course of their economy’s functioning, and the coming quarter century is not placing an unusually high burden on that economy. That already happened in the 1990s.

For Pakistan, if we are able to productively deploy a large percentage of these 90 million people, in addition to improving the lot of those already in the workforce, we could transform the economic fate of the country.

This then gets into the question of: what has the Pakistani economy been doing in the recent past in terms of both the pace and quality of job creation. And on that front, we are happy to report that while the picture is not stellar, it is improving rapidly.

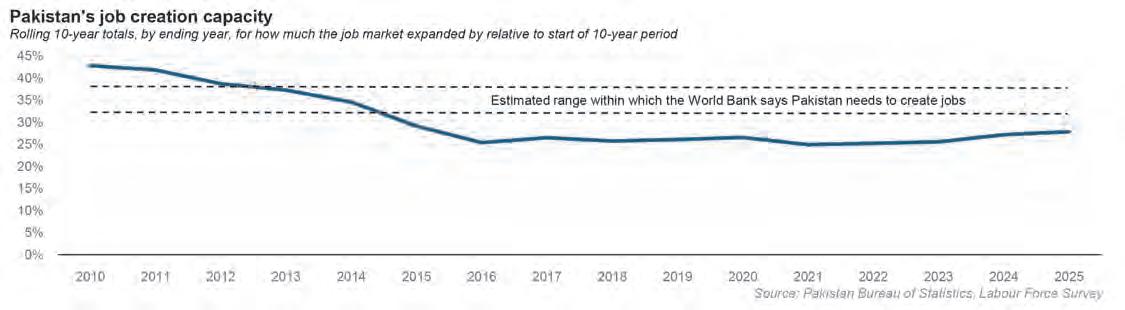

Given the cyclicality of the job market, it is best to determine the ability of the economy to create jobs over 10-year cycles. How many jobs does the Pakistani economy create over those economic cycles? And by how much is it able to expand?

We have already stated that the Pakistani economy created about 16 million jobs over the 10 years between 2015 and 2025, and that represents a 28% increase in the total

number of jobs in the economy during that period, based on Profit’s estimates using data from the Pakistan Bureau of Statistics.

If one were to then calculation the cumulative 10-year totals of job creation, and calculate a rolling total over the past few years, one arrives at what might be considered the baseline job creation capacity of the economy.

In other words, we calculated the 10year job creation rate for the 10 years between 2000 and 2010, and then again for the 10 years between 2001 and 2011, and so on until we get to the 10-year period between 2015 and 2025. So what does that data tell us?

It tells us that during a decade of strong economic growth, such as the period between 2000 and 2010, the economy can increase the total number of jobs by as much as 43% over the course of a decade. In weak periods, such as between 2006 and 2016, it expands the job market by about 25.4% over the course of the decade.

The past 10 years, in other words, are closer to Pakistan’s worst performance than they are to its best.

But what we do learn from this pattern of data is that Pakistan’s job market grows at a reasonable pace, and that in good years –which tend to correspond to the government stepping out of the way and making it easier to do business in the country – it can even exceed the ambitious goals, and pull people from the sidelines and into the labour force.

We then get to the next question: what

kind of jobs are being created? On that, happily, the picture is also improving.

Consider the following fact: even a low salary that is paid every month is better than a situation where one’s earnings are uncertain and dependent on daily wages, per-piece rates, or some other metric directly tied to specific productivity. The latter leaves no room for illness or family considerations, and makes planning one’s expenses for the month considerably more difficult than the former.

This point is unlikely to be appreciat-

ed by most readers of this magazine, since most of you likely have a regular monthly income, but given where the vast majority of the labour force currently stands, this is an exceedingly important consideration when evaluating the degree to which the quality of jobs is improving in Pakistan: is the proportion of jobs that are formal sector and offer a monthly salary increasing?

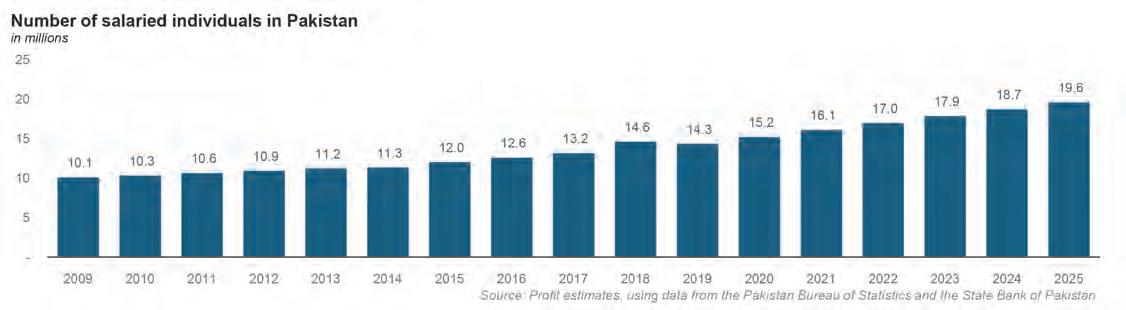

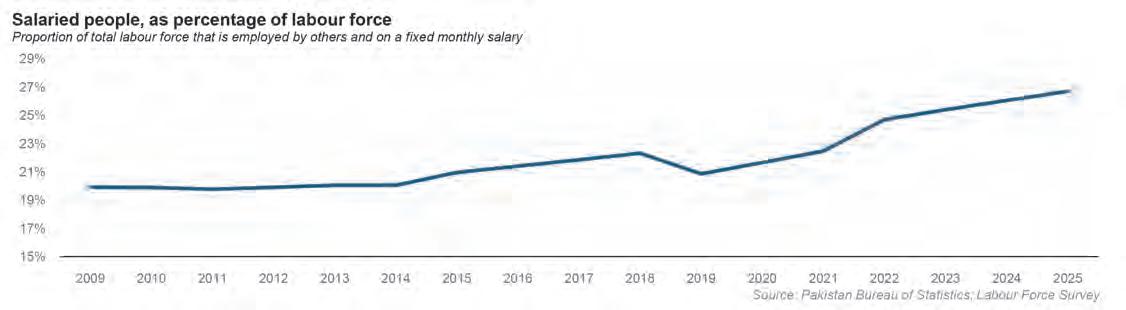

The answer to that is unambiguously yes. In 2025, the proportion of the labour force that has a regular salaried job is about 26.7%, based on Profit’s analysis of data from the Pakistan Bureau of Statistics. This has gone up from 19.9% in the year 2009, which suggests a slow, but steady improvement in the quality of jobs available in the economy.

The numbers are even more stark when

one examines the proportion of net new jobs that are salaried. Between 2009 and 2025, the total number of net new jobs created was 22.6 million. Of those 9.5 million jobs, or about 42% of the total, were monthly salaried jobs. In absolute terms, the number of people with fixed monthly salary jobs almost doubled between 2009 and 2025.

This has enormous implications for the nature of the Pakistani economy. It means that we are on the cusp of having a majority of the jobs being created in the economy being good, stable jobs, even if they are not high-paying yet.

The recent damage notwithstanding, the long-term trend of labour market formalization is unmistakable: salaried jobs have doubled in absolute terms over the last 15 years, and have accounted for about half of the growth in total

employment levels during that time.

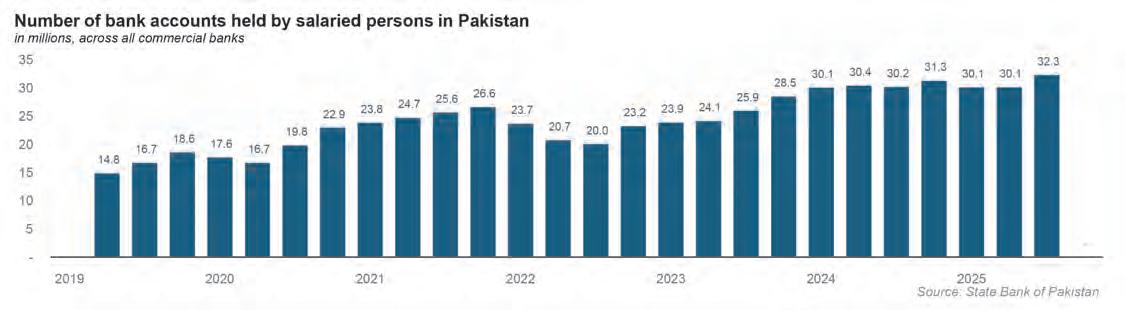

Among the consequences of the rise in salaried persons in Pakistan is for the banking sector.

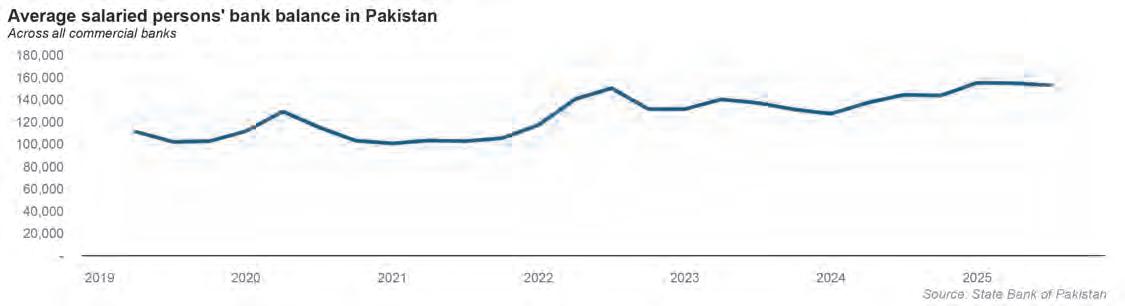

There are a total of 32.3 million bank accounts owned by salaried individuals in Pakistan as of September 30, 2025, according to data from the State Bank of Pakistan, a number that has nearly doubled over the past five years. That rapid growth is likely due to the fact that a large number of Pakistani companies require employees to open bank accounts at the bank in which the company maintains its corporate bank account in order to receive a salary, which means that people often have to create a new bank account every time they switch jobs.

The average balance in these salaried accounts is Rs153,000 and since the bulk of these are likely current accounts, the cost of deposits for banks is likely to remain relatively low. The average deposit amount has actually risen over the past five years from around Rs102,000 in 2019, which suggests that the rise in number of accounts may not just be a case of individuals having to open more and more accounts as they switch jobs.

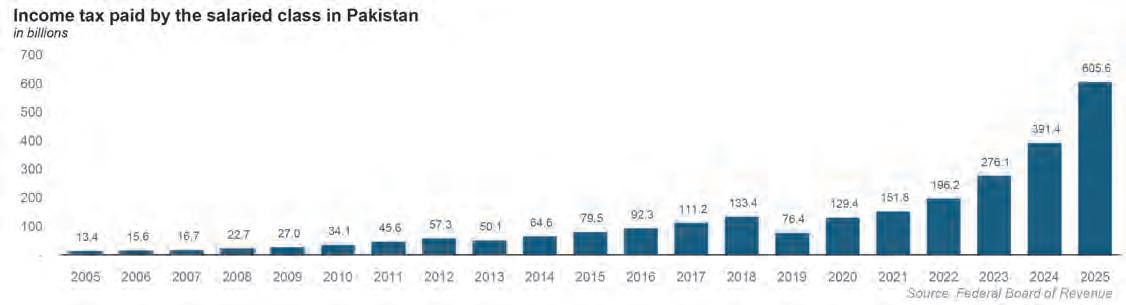

All of this formalization makes it easier for the government to document the economy and collect taxes. And as is always the case, this is where the government of Pakistan becomes the scorpion from the fable of the scorpion and the frog: incapable of preventing itself from stinging the being keeping it afloat.

An increasing share of the government’s revenue is coming in the form of taxes collected by employers from their employees’ regular salaries and deposited automatically with the government. This kind of automatic tax collection is still a relatively small proportion of total tax collection – about 5% of federal tax collection – but that proportion has more than doubled over the past two years.

And therein lies part of the problem: collection has increased partly due to the fact that more people are salaried, and somewhat due to higher salaries, and somewhat due to inflation. But the overwhelming majority of the increase in taxation has taken place due to the fact that the government has hiked tax rates on a larger and larger proportion of Pakistan’s salaried classes.

It is almost as though the government cannot help itself and insists on taxing what it can see, rather than leaving rates where they are and allowing more people to enter the salaried workforce, and allow a more natural increase in tax collection. Tax rates in Pakistan are now comparable to those of mature developed economies, with considerably larger public services and transfer burdens than Pakistan has, leading more and more Pakistanis to ask the question: why pay these taxes at all?

And these are occurring at a time when more and more Pakistanis – particularly those

who have the most potential to earn the most, and therefore the most tax potential for the government – have the options to opt out of the Pakistani economy altogether.

One way they can opt out is through emigration, but even those who cannot leave are able to opt out by becoming freelancers or independent contractors for companies based in the US or Europe, earning money in accounts that are either not taxed, or by policy design, taxed at a lower rate when remitted back to the country.

We would lament and complain about this, but that would involve us assuming that the scorpion that is the Federal Board of Revenue has the ability to change its nature. It does not. We should just accept this and move on.

The broader point, however, is that the Pakistani economy has the ability to generate jobs, and to improve the quality of those jobs, if only the government would get out of the way.

For policymakers, the priority should be to accelerate this virtuous cycle. The government could start by not trying to continually strangle the golden goose and ease some of the excessive tax burdens on the salaried class in Pakistan. It could also try to reduce the bureaucratic red tape around things like incorporating businesses, paying taxes, etc. to help encourage more businesses to accelerate along the path towards formalization. n

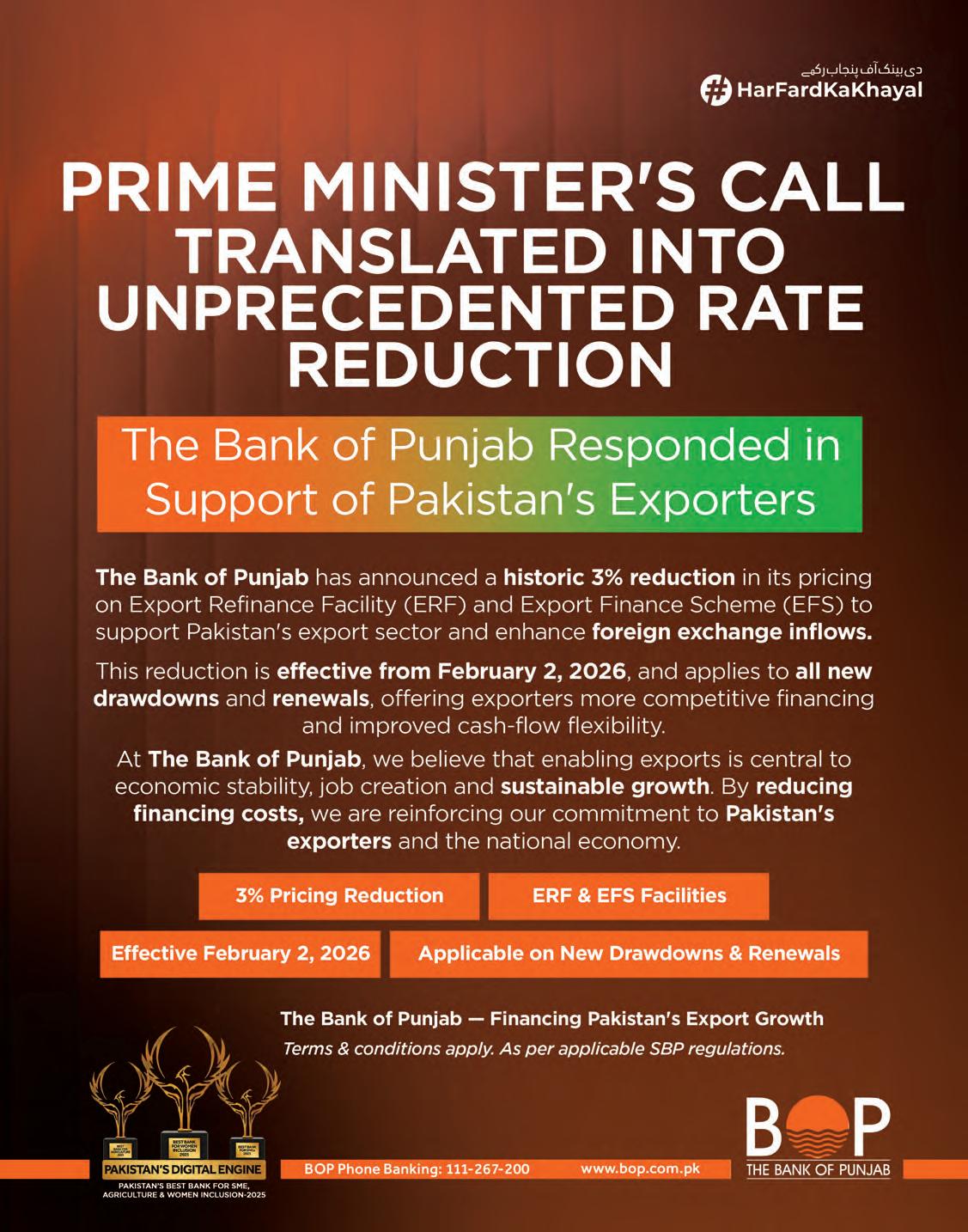

Pakistan’s banks have agreed to give hefty discounts on loans to exporters.

Here’s why

The PBA announcement to give a 3 point reduction on loans to exporters has come only after the government decided to loosen the strings on CRR money that the SBP holds from commercial banks at zero percent interest

Two things can be true at the same time. The recent unanimous decision by Pakistan’s banking sector to charge a lower interest rate on the Export Finance Scheme (EFS) is an example of private business stepping up to bat for the national interest before their own bottom line. The decision, announced by the Pakistan Banking Association (PBA), is one that has been taken in the best interest of Pakistan’s economy.

And while this is all well and good, it is also worth looking into the prevailing conditions that have allowed the banking sector to make what cannot have been an easy decision to get unanimous agreement on. Part of the reason that the banks have willingly made this decision comes hot on the heels of the SBP reducing the required Cash Reserve Requirement (CRR) from 4% to 3%.

The CRR is essentially a percentage of a bank’s deposits that it is supposed to park with the central bank. Since cash is a non-earning asset for the banks, the idea is that the central bank must ask the banks to always have a minimal amount of cash required to honour withdrawals by depositors. And SBP holds this cash for the banks and gives zero percent interest on this money. However, over the years CRR has been turned into a monetary policy tool by the central bank. By reducing the percentage from 4% to 3% (which is the daily minimum — the average minimum is higher and has been reduced from 6% to 5%) the SBP is giving the banks a little more money that they can now lend and earn interest on it.

The equation is simple enough. The 1% reduction in the CRR freed up around Rs 300 billion in liquidity for the banking sector. They can then lend this money and earn over Rs 30 billion from it. The reduction in markups for the Export Refinance Facility also amounts to around Rs 30 billion.

According to Zafar Masud, President of Bank of Punjab and Chairman of the PBA, the industry got the leeway due to favourable CRR adjustment. “We have been asking for this for a while as it was not helping market liquidity. The thought was that it would be a good idea to pass

on to attract more profitable businesses and also reinforce ourselves as responsible and patriotic entities,” he told Profit.

Essentially, the reduction in the CRR has opened up liquidity that can now be sent in the areas the economy needs it. This is being achieved through the Export Finance Scheme, which is a concessional financing scheme administered by the SBP.

Under the EFS, the SBP lends liquidity to exporters at a capped subsidised rate, through commercial banks, and the objective is to reduce financing costs for export-oriented businesses.

Say, for example, a textile exporter gets a confirmed export order (or LC/contract) from a foreign buyer and needs working capital to buy yarn, pay labor, and ship goods. The exporter goes to its bank and applies for financing under EFS, which is a short-term facility, and the financing tenor can go up to 180 days.

When approved, the bank will finance the exporter at the applicable EFS end-user rate. Normally this would be 3% below the policy rate (7.5% under current policy rate). The bank in turn gets refinance from SBP at the applicable refinance rate under the scheme, which is even lower, such that the banks could make between 1-2% spread, depending upon the type of exporter.

So the exporter gets cash upfront, uses it to fulfill the order, ships goods, and later when the export proceeds are realized, pays back within the time period. The bank then settles/ refinance obligations with SBP on maturity. Much like any other loan, if the exporter’s cycle goes beyond 180 days, the bank can still finance the extra period, but from its own funds, not SBP refinance, and those penalties would be reflected in whatever conditions the bank offers to the exporter.

Earlier, banks were charging 3 points below the regular interest rates, which meant the markup was 7.5%. Now, banks will voluntarily charge 4.5 points below the policy rate, meaning exporters can avail financing at 6% markup under the EFS.

‘’The long term view is to promote exports which will eventually

The long term view is to promote exports which will eventually benefit banks in the medium term. This was the need of the hour and banks have always responded to the government in times of need

Zafar Masud, Chairman of Pakistan Banking Association

benefit banks in the medium term. This was the need of the hour and banks have always responded to the government in times of need starting from the PIA restructuring, to circular debt restructuring, to setting a level playing field for remittances, to agreeing to pay higher tax rates as a quid pro quo to get rid of the market distortive move of Advances-to-Deposits-Ratio tax,” explains Zaffar Masud.

According to him, the move will be beneficial for the banks in the long run because it will be beneficial to the economy. The idea is that if exporters have cheaper access to financing it will help them grow their business, and if exporters sell more Pakistani products abroad which will bring in foreign exchange and improve the balance of payments, which in turn will bring stability to the economy.

It is also an easy way to go about it because it doesn’t require huge mop-ups or liquidity adjustments by the state bank and it helps the economy, such that the cost is low and the benefit is high for the central bank. The SBP actively helps push the EFS and has more than Rs 440 billion in EFS outstanding, with a limit of over Rs 1 trillion (Over $3.5 billion).

Because when exporters borrow under EFS, they eventually generate dollar inflows. Those inflows pass through the banking system, creating additional business opportunities. Banks will earn fees on trade transactions, foreign exchange conversions, and related services. Exporters will also maintain operational accounts, which can become stable, low-cost deposits for banks in the future — another benefit.

“Inflows are profitable transactions as they help in offering better rates on imports and attaching current accounts,” explains Zaffar Masud.

The banking sector, of course,has been trying to get rid of the CRR for some time. Before November 2021 it had been at 3% but was raised to 4% during Reza Baqir’s tenure as Governor of the

SBP. It has needled at the sides of the sector since then.

Previously, the banks did not need to do much, during the high policy rate era. All they had to do to make record profits was to hold onto their funds and lend to the government. During this time, even the EFS was giving the end user an 18% interest rate, which is not good enough to be internationally competitive, especially with a falling domestic currency.

Since the monetary easing has kicked in, the banks have felt the need to do more. Falling profits and falling margins could have pushed them to branch out and explore but actually reducing their margins has only been made possible by the adjustment in the CRR.

As things stand, if the banks are to give an additional 3 points reduction on the EFS, and the EFS’ limit is Rs 1.05 trillion, the amount of money the banks will need, to subsidise their voluntary EFS is approximately Rs 30 billion — the same amount they will be able to earn upon the freeing up that 1% from the CRR.

When the State Bank lowered the CRR by 1%, it effectively unlocked billions in previously frozen cash. That money moved from “earning nothing” to becoming deployable capital.

And deployable capital, even at a modest lending rate, is infinitely better than sterile reserves. And, by the looks of it, instead of giving banks a free hand with that freed up money, the SBP made an arrangement with the PBA, to instead use that money for increased liquidity for exporters.

The situation, of course, has not been easy for the banks. The CRR was raised in 2021 and it has not been reduced; it has just been brought back to the old percentage. On top of that the banks are now voluntarily reducing the markup on EFS even if it is after easing in the CRR.

According to Zaffar Masud, more than anything else, the move aims to address the biggest national concerns that exist today. “The biggest national concern at the moment is the near-stagnant growth in exports coupled with an ever-widening trade deficit. In such a situation, banks, as key stakeholders in the

economic ecosystem, must contribute their share by further reducing the Export Refinance Facility (ERF) rate,” he says.

“This step would certainly help leverage export growth and provide much-needed relief to exporters, enabling them to compete more effectively through improved margins. While this may impact banks’ profitability in the short term, taking such a hit on their P&L would serve the larger national interest by supporting economic stability and external account sustainability”

Most of the reform policy in Pakistan is basically throwing wet paper towels till one of them sticks. This seems like another one of those attempts. While Banks are not acting outside their commercial logic. They are also aligning commercial incentives with macro policy objectives, a slope that is slippery to walk.

But what this episode really reveals is a temporary alignment between regulation, liquidity, and political need. The reduction in ERF pricing may still support exporters, and it may still serve a macroeconomic purpose, but it also exposes how much of Pakistan’s policy architecture depends on negotiated incentives rather than transparent, durable frameworks.

That is why the most important part of this story is not the announcement itself. It is the uncertainty sitting behind it.

How far are banks actually willing to compress margins? How long will the sector step in to do the state’s job? How long can preferential pricing continue? What happens if fiscal pressures intensify again? Those are not side questions. They are the central questions, and for now, they remain unanswered.

ERF, in that sense, is best understood as a lever, not a cure. It can create breathing room. It can shift incentives at the margin. It can even help buy time for exporters. But whether that time is used to push real industrial reform is a separate question entirely. n

A proposal to base household electricity rates on income instead of usage is in the works. Here’s why it might make sense

The plan aims to protect lifeline consumers, and end high-income solar users from reaping the benefits of subsidies meant for the poorest segments of society

By Ahmad Ahmadani

Let us get one thing straight. There is no immediate plan to change the basis of Pakistan’s household electricity bills from usage to income. What has happened, however, is that a proposal has been circulated through the power division suggesting such measures. The reason behind

this idea?

As with most things in Pakistan’s energy landscape these days, it has to do with solar energy.

The entire matter is quite straightforward. Currently, household electricity bills in Pakistan are calculated based on how many units of

electricity a household consumes in a month. The system operates through slab-wise rates, meaning the per-unit price increases with higher consumption. Consumers are categorized as lifeline consumers, protected consumers, and non-protected consumers. Depending on which of the first two categories a household falls into, they are given a certain level of subsidy.

The latest data indicate that out of the

roughly 35 million grid-connected households, about 18.3 million (52 percent) use less than 200 units per month. These are the “lifeline” consumers that get the cheapest rate of electricity. The goal is to give a subsidised rate to households that have low consumption because of the income bracket they fall in. These households receive around 90 percent subsidy on the first 100 units and about 70 % subsidy on the next 100 units. The remaining households, consuming more than 200 units, pay higher per-unit charges along with fixed fees, FCA, taxes, and other surcharges.

For some time now, there have been quarters within the power division and the federal government that have sought to change this system. Under the current IMF programme there has also been a demand to rationalise subsidies in utilities.

The proposed reform aims to shift from this usage-based system to an income-based pricing model. This means that instead of determining relief based on usage, the government would assess household earnings to decide whether a household qualifies for subsidized rates. The main objective of this proposal is to ensure that subsidies are better targeted and only go to the people who actually cannot afford the full electricity rates. But doesn’t the current usage based slab system already ensure that. Well, apparently not anymore.

Under the current slab system, households with relatively comfortable incomes can still benefit from lower tariffs if they manage to keep consumption within certain limits. Conversely, some genuinely low-income families may lose protection if their usage slightly exceeds the threshold. By linking subsidies to income, the government hopes to make the system more equitable, so that only deserving consumers receive support.

A major reason for the government possibly wanting to pursue this system is the expansion of household solar usage. Think of it this way. If a person sets up a 10kW solar system on their rooftop and attaches batteries to their system, they can use the solar energy during the day and store more to use after the sun sets. Because they are using solar energy, it is entirely possible that this household consumes less than 200 units from the grid. In this case, because of the consumption basis, their bill will be subsidised. In that way, the subsidy will become a benefit for the wrong audience.

By switching the billing system to an income based one, it would avoid such slippages. Internationally, full income-based

electricity pricing is rare, but some countries have experimented with targeted subsidy systems linked to income or socio-economic status. In India, for example, Karnataka’s Gruha Jyoti scheme provides free electricity up to a certain usage limit for eligible low-income households identified through social welfare registries. In Colombia, electricity tariffs and subsidies vary according to socio-economic strata, offering greater support to lower-income groups. Similarly, countries like Brazil and Mexico apply discounted electricity rates or subsidies for low-income households through social programs or welfare databases. These examples show that while income- or welfare-linked support can help target relief more effectively, implementing such systems requires robust household data and strong verification mechanisms — a significant challenge in countries with large informal economies like Pakistan.

The proposed shift to an income-based pricing model is also likely to generate political sensitivity and public debate. Domestic consumers, particularly middle-income households who currently benefit from subsidized rates under the slab system, may view the change as an additional financial burden. Opposition parties and consumer advocacy groups could criticize the government for potentially raising electricity bills for a large segment of households, framing it as unpopular and regressive. Even if the policy is aimed at targeting subsidies more effectively, the immediate perception among voters could be negative, creating challenges for the government in explaining the reform and managing public expectations.

This perception might be exacerbated for another reason. At the same time as this, the business community has been persistent in their complaints that despite being bulk buyers of electricity they are charged higher rates so others can be subsidised. By rationalising the subsidy through income rather than usage, the government can find room to provide cheaper electricity to industries. The idea for this is that because of rapid solarisation, the grid has more electricity than there is demand. If the grid electricity can be made cheaper, more bulk buyers might buy more electricity from the grid rather than going the route of setting up captive solar plants as many industries have done.

The optics of this, of course, will not be particularly pleasant. Households with solar installations that will be most affected are also the loudest and most visible when it comes to complaining. On top of this, it is

entirely possible that deserving lower and lower-middle class households get caught in the crossfire. And that is where the most critical part of this plan comes, and likely why it will not work and never get to the implementation stage: how does the government plan on accurately assessing household income?

Akey question remains: how will the government accurately assess household income in a country where a large portion of the economy is undocumented or informal?

Many households do not have official income records, making it extremely challenging to determine who qualifies for subsidies. Authorities may attempt to integrate the system with existing social protection databases, tax records, or national identity data, but gaps in information, errors in classification, and disputes over eligibility are likely. This raises the risk that some genuinely low-income households could be excluded from relief, while some higher-income consumers might still receive subsidized rates, complicating the reform’s effectiveness and fairness.

This reform is also connected to Pakistan’s ongoing discussions with the International Monetary Fund (IMF) regarding power sector restructuring. The IMF has emphasized the need to protect low- and middle-income groups while reducing distortions in the tariff structure. Another major concern is the growing circular debt in the power sector, a long-standing economic challenge. Circular debt accumulates when distribution companies fail to recover full costs, subsidies are delayed, and payments to power producers remain outstanding. Reforming tariffs is seen as part of a broader effort to stabilize the energy sector and reduce financial losses.

If implemented, the impact will vary across income groups. Low-income households could benefit if the system successfully identifies and protects them, even if electricity consumption fluctuates. Middle-income families may face higher bills if classified above the subsidy threshold, while high-income households are likely to lose subsidy benefits and may pay rates closer to the full cost of supply. Much will depend on how income levels are defined and verified.

Once again, it is important to note that no final notification has been issued yet. The proposal is still under discussion, and details such as income thresholds, implementation timelines, and verification mechanisms have not been officially announced. Until a formal decision is made, the current slab-based tariff system remains in place. n

Minister of Pakistan Shehbaz Sharif has recognized National Bank of Pakistan (NBP) for its significant contributions to the national economy.

During a ceremony held in Islamabad recently, PM Shehbaz Sharif presented the award to Rehmat Ali Hasnie, President and CEO, NBP. The event honored leading exporters and bankers for the year 2024-25.

The recognition highlights NBP’s strong support for export growth and its continued role in strengthening Pakistan’s financial sector. Through its services and partnerships, the bank has played an important role in promoting trade, supporting businesses, and contributing to overall economic development.

Senior government officials, top bankers, business leaders, and exporters from across the country were present on the occasion.

NBP remains firmly committed to driving sustainable and inclusive growth by supporting the business community, strengthening financial intermediation, fostering innovation, and actively contributing to Pakistan’s longterm economic stability, resilience, and overall national development. n

Maha Shah OPINION

Ayoung worker in the Gulf sends money home. A freelancer waits on an overseas payment. A student in a small town tops up mobile data and pays a bill through an agent because a bank branch feels distant, slow or intimidating. For millions of underbanked and unbanked Pakistanis, the question is less about new financial products and more about getting through the month with fewer delays, fewer fees and fewer chances of being scammed. Documentation demands, thin rural branch coverage and mistrust of banks still keep many people on the margins.

Pakistan’s account-ownership story depends on how it is measured. Estimates put the share of unbanked adults in Pakistan at 53 per cent, with financial exclusion disproportionately affecting women and low-income groups. With more than 200 million telecom subscriptions, phones have become the default financial interface for many households. Digital finance still depends on reliable internet access, and industry warnings about firewall-linked disruptions have

Maha Shah is a finance and crypto journalist who has worked at Bloomberg and Forkast News. She covers the fast-moving intersection of digital assets and global finance, focusing on blockchain innovation, market trends, and the forces shaping the digital economy

reinforced how quickly ‘online money’ can stall. Platforms like crypto exchange MEXC argue that lower-cost access to stablecoins and clearer disclosure standards can make these mobile-first money flows more practical for users navigating delays and fees.

Remittances remain one of Pakistan's most important household safety nets and also one of its most reliable sources of foreign exchange. Pakistan sits among the top five remittance recipients among low- and middle-income countries, with a forecast of roughly $30 billion in 2025.

Personal remittances were about 9.4 per cent of GDP, which is why transfer costs and delays directly affect household budgets. Those inflows, which hit a monthly record of $4.1 billion in March 2025, often cover rent, school fees and medical bills, supporting day-to-day resilience.

Still, sending money across borders through the usual channels can be frustratingly expensive. The World Bank puts the global average cost at about 6.49 per cent of whatever you send. The exact fee depends on the route and the provider, and processing can stretch out due to compliance checks, intermediary banks and the final cash-out step on the other side. In its 2025 annual report, MEXC says its zero-fee model is designed to lower user costs at the point of conversion between assets.

That cost pressure encourages workarounds. Some Pakistanis rely on cash-based informal networks, while others experiment with digital alternatives when the official route feels slow, expensive or inconvenient. Even when a transfer arrives through formal channels, it can still end up in cash via an agent, which limits how far “inclusion” travels beyond the moment of receipt. Speed and clear pricing often shape those choices.

Pakistan’s crypto activity is hard to miss in global data. Chainalysis ranked Pakistan third overall in its 2025 Global Crypto Adoption Index. While the ranking uses specific weighting metrics, the index points to activity that extends beyond isolated speculation. For many

users, stablecoins (digital tokens typically pegged to the US dollar) are appealing because they behave more like dollars, while money moves from one country to another.

Alongside transfers, some users treat stablecoins as a way to hold value between paydays or park small balances outside cash, especially when card access is limited. Mobile wallets can also make it easier to receive freelance income or settle online payments without a bank account.

Regulators are starting to acknowledge this utility. Pakistan has agreed with SC Financial Technologies to explore the use of its stablecoin USD1 for cross-border transactions. In addition to the recent creation of the Pakistan Virtual Assets Regulatory Authority (PVARA), the government is exploring the roadmap to regulate the crypto space and provide protection for consumers.

Trust decides whether new channels become everyday tools or stay niche. Policy attention reflects opportunity and risk in the same breath. Crypto usage carries real risks, including scams, lost credentials and limited recourse when something goes wrong. Those risks help explain why trust and consumer protection matter as much as speed.

MEXC’s 2025 annual report says the company moved toward monthly proof-of-reserves audits by Hacken and points to a $100 million “Guardian Fund” as a user-protection backstop. In Pakistan, those claims matter because the core barrier is confidence: people need to know what safeguards exist and what happens when something goes wrong. All that said, for people shut out of banks or cards, a wallet can be another way in — to let them pay digitally and move value across borders.

Tokenised instruments can widen access, but outcomes depend on execution. Whether this helps ordinary users comes down to basics: clear fees, safer custody and a real way to fix problems when something breaks.

People need straightforward rules they can understand, plus basic protections against scams and sudden account freezes, especially when they’re relying on a wallet for everyday money. For a younger generation in Pakistan looking to transfer money internationally and save funds until payday, it will all depend on whether digital infrastructure provides better, faster and safer options at scale.

Pakistan’s next step is getting the rules straight. It needs to be clear what’s allowed and who can offer it, and what happens when something goes wrong. Consumer protection should start with fees and risks spelled out up

front, a complaints process that actually responds, and real follow-through against fraud. If digital wallets can plug into the payment

rails people already use, such as agents, bill payments and mobile wallets, then small transfers can stay predictable and safer. n

Pakistan is set to start providing bunkering services to international ships. But the business is not as simple as it might sound

By Usama Liaqat

Recently, Pakistan saw the commencement of landmark bunkering services at the Karachi Port. Spearheaded by Vitol, the largest independent energy trader in the world, the initiative aims to provide between 500,000 and 600,000 metric tonnes of bunker fuel to ships and vessels every year across Karachi Port, Port Qasim, and outer anchorage areas. It is a forward-looking project, and aims to usher in a new chapter in Pakistan’s maritime and industrial history. A key way in which it seeks to do this is by working on the capacity utilisation of Pakistan’s oil refinery infrastructure. Given that around 37 percent of Pakistan’s refining capacity goes unutilised, this looks to be one way of trying to bump the utilisation percentage up. In fact, according to some industry estimates, the sort of bunker fuel handled at this bunkering

platform might come to constitute 40 to 50 percent of the total refined oil output of Pakistan.

This development must be understood in the context of Pakistan’s oil industry. Mainly reliant upon imports to supply the demand for crude oil as well as petroleum products, oil appears as the biggest liability on Pakistan’s import bill. In FY2025, for instance, import shipments of oil and petroleum products were worth $11.3 billion, almost 20 percent of Pakistan’s total imports by value in the period. At the same time, refineries are not working at capacity levels, making petroleum imports for local usage a necessity.

There is also a shift happening within Pakistan’s petroleum refinery ecosystem. As the government is providing financial disincentives in the form of heavier levies and taxes on the use of furnace oil, the demand for these is decreasing. While earlier Pakistan relied partly on imports to sustain the demand

of furnace oil, in the past 3 fiscal years, we have essentially stopped importing furnace oil.

In fact, with alternative means of energy becoming increasingly common and cost-effective, Pakistan has been exporting excess furnace oil. In this context, shifting from a high-sulphur furnace oil to lower-sulphur variants of bunker fuel might offer a way out for local refineries who can then rely on international demand instead of dwindling and unsteady local demand. This would also enable advancements in Pakistan’s maritime infrastructure, and position it as a key player in the regional marine ecosystem, attracting activity on its ports while at the same time bringing in dollar payments.

Yet, the enterprise is not without risks, especially with concerns regarding a potential price drop if global economic and political conditions continue to deteriorate. Similarly, volatile trading ecosystems mean that shipping lines – since Cynergyico relies on imported light crude oil for bunker oil production –might get disrupted, throwing into chaos the whole enterprise. At the same time, infrastructural constraints might limit the kind of progress such efforts might make, in the context of competition with more established regional players.

Bunker fuel essentially is fuel for ships or vessels, and you can imagine bunkering services as the provision of this fuel to ships for propulsion and onboard machinery. What happens during such operations is that the vessel that needs fuel comes into the port, where there is a barge with fuel on it. The two vessels get close to each other and connect through hoses, through which bunker fuel is provided to the visiting ship. The transfer is monitored closely for temperature, pressure, and leaks. The speed of fuel transfer also varies throughout the whole process.

Bunker fuel, however, is only a general category. There are multiple types of such fuel. One of these is Heavy Fuel Oil (HFO). Once the refining process has broken down crude oil into its lighter constituent parts, the residual mixture that remains contains heavy and undesirable components including sulphur. This is known as HFO, and is used to propel ships through the waters. Yet the fact remains that usage of this type of oil is environmentally deleterious, since its combustion releases harmful gases like sulphur dioxide, carbon monoxide, etc. In fact, the International Maritime Organisation (IMO) in 2020 banned the use of HFO in ships unless they were using scrubbers to mitigate the potential environmental harm

caused by HFO usage.

There is, however, a more environmentally friendly alternative, and one that is becoming increasingly adopted in the world. This consists of various forms of fuel which instead of being constituted of the residue in the refining process, are rather made of the distillate matter. The distinguishing factor here is that these fuels contain lower amounts of sulphur. Although the residual marine fuel can be ‘de-sulphurised’ the process is very costly. It is just cheaper to use distillates, or a mix of residual fuel and distillate fuel to reach a middle ground. Depending on the sulphur content, these fuels might be classified as Ultra-Low Sulphur Fuel Oil (ULSFO), Very-Low Sulphur Fuel Oil (VLSFO), or Low Sulphur Fuel Oil (LSFO).

In 2023, National Refinery Limited announced that it had successfully produced Pakistan’s first batch of VLSFO. This was especially important since it was compliant with the environmental standards set by the IMO, and could therefore compete for demand in the international market. Yet local production did not really take off, and the scale remained limited. That is, until Vitol and Cnergyico made the first large scale production and delivery of IMO-compliant VLSFO in November 2025. Earlier, no such refuelling capability was available and ships had to rely on Fujairah or Singapore to obtain fuel.

The shipment was significant. Cynergyico through Vitol had sourced crude oil from the United States, and refined that to produce IMO-compliant bunker fuel. The fuel was transferred through the Marine Ista, a barge operated by Cynergyico and capable of supplying up to 6,800 MT of marine fuel in a single delivery, to a vessel operated by the shipping giant MSC.

Although Vitol and Cynergyico have had partnerships earlier through the former’s subsidiary HASCOL Petroleum and the latter’s predecessor Byco – brought to the fore most infamously in a major scam (LINK) – this new partnership now aims to take the shipment and production of bunker fuel to the next level. This would be done through the introduction of bunker barges compliant with global maritime assurance requirements, and the establishment of a clear and structured bunker-licensing regime. The range of the bunker fuel offerings would include HSFO, VLSFO, and Low Sulphur Marine Gas Oil (LSMGO), and the target would be to provide between 500,000 and 600,000 MT of bunker fuel every year.

This must be understood in the context of Pakistan’s oil refining landscape. One of the major issues facing the oil refinery sector in Pakistan is underutilisation. According to a report by the Pakistan Credit Rating Agency Limited, while Pakistan’s refining capacity during FY25 was around 20 million MT per year, only around 63 percent of this capacity was made use of. Before we mention the capacity utilization of individual refineries, it must be noted that Pakistan imports both crude oil and refined petroleum products. Crude oil imports constitute 72.1 percent of Pakistan’s total crude oil consumption. As for petroleum, oil, and lubricant (POL) products, while Pakistan locally produced 10.4 million MT of the same, it had to import 7.8 million MT of these in FY25 to supply local demand. So, POL imports constituted around 43 percent of the total imported volumes.

The point is that this 43 percent could be even lower since capacity is available to produce more POL products at home. Now, there are five major oil refineries in Pakistan: Pak-Arab Refinery Limited (PARCO), Pakistan Refinery Limited (PRL), Attock Refinery Limited (ATRL), National Refinery Limited (NRL), and Cnergyico. PARCO and PRL have decent utilization rates (86 and 80 percent, respectively). These both are followed by ATRL and NRL whose utilization rates stood at 69 and 56 percent respectively in FY25. The real outlier was Cnergyico, whose utilisation in FY25 came at an astonishingly low 23 percent.

There is certainly, then, some merit to Cynergyico taking on the production of bunker fuel, since a big factor in Pakistan’s underutilisation of its oil refineries has been the laggard Cynergyico. But now, as has been reported, if the industry experts estimate the production of bunker oil to constitute between 40 and 50 percent of the total POL production in Pakistan, Cyenrgyico will certainly have the most significant role to play in that.

Another important trend in the local POL landscape is the gradual reduction in demand for furnace oil. Furnace oil is quite similar to the earlier discussed HFO. It too is made of residue in the crude oil segmentation process, and is highly viscous and cheaper since it usually does not require further processing unlike the higher value POL products that are distillates or refined from distillates. Yet, as can be easily imagined, furnace oil also harms the environment when it is burned. Considering that it is generally used in industrial applications to provide heating, power and other high-temperature applications, the extent of its harm to the environment is certainly not negligible.

In fact, the government has been slapping levies and taxes on the usage of furnace oil as industrial fuel. A petroleum levy of almost Rs 77 per litre was imposed under the Finance Act 2025-26 in addition to a Carbon Levy of Rs 2.5 per litre of furnace oil. This Carbon Levy is stipulated to increase to Rs 5 per litre of furnace oil in FY27. These levies have increased the price of furnace oil locally – according to some estimates by more than 80 percent – compelling customers to shift to cheaper alternatives. At the same time, the power generation sector has also been shifting away to other sources of energy, such as RLNG, solar, and hydroelectric, which are also much cheaper and more environment-friendly – in general – than furnace oil.

In fact, the consumption has been falling so much that Pakistan has been exporting furnace oil / HFO. It was reported that in FY25, more than 1.4 million MT of furnace oil was exported, of which 1.3 million tonnes consisted of HSFO, and 137,880 tonnes of LSFO.

What must be underscored here is that furnace oil is quite similar to the high-sulphur variant of bunker fuel. There are some minor differences in processing for marine usage in the latter, but the main thing is similar. Where the difference becomes more pronounced is with lower-sulphur variants of bunker oil (LSFO, VLSFO, and ULSFO), which progressively require higher hydrodesulphurisation and more additives. The process becomes more complex and expensive as a variant with lower sulphur is being produced.

Another thing that must be understood here is that the process of oil refining is such

that you cannot produce only one product. In fact, all products (such as LPG, Naphtha, Kerosene, JP-1, JP-8, Diesel, Furnace Oil, and Asphalt) are produced simultaneously in the distillation column. What had been happening in Pakistan is that since the demand for furnace oil was decreasing, refineries were being forced to choose between two courses of action: lower their overall production so that less furnace oil was produced, or to export them often at discounts in the global market.

It is here that lies the significance of the partnership between Vitol and Cynergyico. Through this partnership they are aiming, first of all, to produce high quantities of bunker oil with lower sulphur content, such as VLSFO and LSMGO, in addition to quantities of HSFO. The increasing capacity for the former two especially places the product higher in the value chain, meaning they can fetch better margins.

Secondly, this partnership also seeks to introduce bunkering services in Pakistan, where instead of exporting fuel abroad, we can essentially operate the bunkers ourselves and facilitate the refuelling of ships. This reduces risk, improves operational efficiency, and improves margins.

Beside facilitating the enhancement and expansion of Pakistan’s maritime infrastructure, development of this partnership is likely to lead to an enhancement of Pakistan’s position in the newer maritime fuel regimes, where the use of high-sulphur fuel oil is banned, except in the case of vessels that use scrubbers. This would also lead to more port activity and make Pakistan well-placed to position itself as a regional refuelling hub for ships on east-west routes.

Moreover, this also opens options up for these companies who can now bypass higher levies on furnace oil, and instead bring in dollar revenues. Since oil remains the heaviest item of our national import bill, here is an opportunity to put some weight on the opposite end, and help reduce the trade deficit. At the same time, with higher port activity there is more potential to improve foreign-exchange earnings through port fees, marine services, and other commercial activities such as repairs and maritime logistics.

Also, the demand for furnace oil is falling in Pakistan, as the government is moving to discourage its production. In this context, shifting to producing lower-sulphur fuels adhering to international standards would not only represent a more stable pursuit, but also given the potential for international trade, might give Pakistan’s oil refineries a push that might change their fortunes. This is especially the case since the partnership between Vitol

and Cynergyico also seeks to improve the capacity utilisation of the biggest refinery of Pakistan, which if done would help improve the contribution to the national economy of the local oil refining capabilities.

There is also a geostrategic element to this. In May 2025, India banned ships docking at its ports from calling at Pakistani ports. Given India is a massive trading entity this represented a sidelining of Pakistan at the maritime stage. Yet, opening of bunkering services would allow more options for trading vessels who – instead of India – might find suitable fuel available at Pakistani docks.

But there are risks involved as well. Producing these bunker fuels – as has been done by Cynergyico – requires light crude oil, which is imported. That part of the import bill will, therefore, see somewhat of a rise. So, the upside might not be as high as one might have supposed. Relying on imports for production of barge oil might also leave importers exposed to geopolitical risks in a world where shifting alliances determine avenues for one’s energy usage, and political pressures might stifle shipping routes.

Furthermore, there is a risk of oversupply in the bunker market. It has been reported that the market growth has gone a bit mild in the past few months, and that rising concerns about economic and political stability have been depressing demand. The fact that an increasing number of bunker fuel suppliers are competing for a market that isn’t growing that fast, might lead to an overall depression in the prices, forcing bunker fuel suppliers to cut down their margins. If the global trade sees a slowing down, it might even make the situation worse.

And then there are questions about Pakistan’s refining infrastructure. Currently, there is only one major barge: the Marina Ista operated by Vitol. Given the targets set are to provide between 500,000 and 600,000 metric tonnes of bunker fuel per annum, it would require a greater port handling capacity, as well as much more advanced systems to monitor spillages, and streamline ease of servicing ships through a centralised management system. At the same time, the ramping of capacity utilisation of existing refineries would require not only infrastructural updates, but also government support in the form of consistent and longterm policy plans. n

FBR schedules auction to recover Rs 26 billion in unpaid income taxes following new FBR powers and a landmark legal shift in how developers must report income

By Shahzad Paracha

The Federal Board of Revenue (FBR) has decided to auction 527 kanals of land owned by Bahria Town in Tehsil Murree on the 5th of March 2026. The auction is meant to help recover Rs 26 billion in unpaid taxes that Bahria Town owes to the federal government for the tax years 2020 and 2022.

This is the second date that the FBR has given for the auction. Originally, the auction was supposed to take place on the 16th of February, but the FBR rescheduled it to the 5th of March and will be held at the Large Taxpayers Office in Islamabad.

Under powers given to the FBR under the last budget, the revenue authority can seize and auction property from defaulters. The FBR recently auctioned Bahria Town’s corporate office on Park Road in Islamabad, eventually selling it for over Rs 2 billion in connection with a settlement reached in the £190 million case involving Malik Riaz Hussain, the founder of Bahria Town. The announcement of the Muree land’s auction is linked with Bahria Town’s alleged tax evasion in 2020 and 2022. While no official word has come from the FBR, Profit understands that the reserve price for the property is possibly over Rs 1.5 billion and could be as high as Rs 2 billion.

The upcoming auction is the culmination of a decade-long dispute over tax accounting. For years, Bahria Town utilized the “Percentage of Com-

pletion” (POC) method, which allowed them to defer tax payments by treating customer payments as “advances”, and not as taxable revenue, until construction milestones were met.

However, a landmark Supreme Court judgment on March 18, 2025 (M/s Emaar DHA Islamabad v. CIR), conclusively settled that land developers selling plots are ineligible for the POC method. The Court ruled that because developers do not physically build houses for plot customers, they must use the accrual method, requiring them to recognize income immediately upon a sale. Consequently, what Bahria Town once recorded as deferred advances were reclassified as taxable income, creating the current Rs 26 billion default.

Crucially, this tax recovery action is entirely separate from, and unrelated to, the historic Rs 460 billion settlement case concerning Bahria Town’s land acquisition in Malir, Karachi.

Under powers given to the FBR in the last budget, the revenue authority can seize and auction property from defaulters. The FBR recently auctioned Bahria Town’s corporate office on Park Road in Islamabad for over Rs 2 billion in connection with a settlement reached in the £190 million case involving Malik Riaz Hussain.

The announcement of the Murree land’s auction—527 kanals at Mauza Kathar Sharqi, Angori Road—is directly linked to these tax evasion findings. While the neighboring Golf City project remains disputed by original landowners over environmental concerns, the FBR successfully attached this specific 527-kanal

parcel on September 22, 2025.

The crackdown has intensified elsewhere as well; on January 30, 2026, the FBR took physical control of the Bahria Town Tower in Karachi, which houses 145 residential units and 42 offices, to further secure the Rs 26 billion recovery. Sources also indicate that the FBR is investigating the Mall of Islamabad to protect over PKR 30 billion in public investment while ensuring the state’s revenue is realized.

Sources revealed that the FBR may ask potential bidders in the upcoming auctions to demonstrate that they possess sufficient assets to purchase the 526 kanal property. Following the auction of the Park Road plot, sources said discussions were initiated regarding net assets of successful bidders.

Earlier, The FBR had also attached Bahria Town tower Karachi on October 7, 2025 and also advised general public and concerned authorities not to make any sale, transfer, lease of 142 units worth billions of rupee.

Sources said that the FBR team had also confiscated important documents during the raid on October 7, 2025 as reportedly the management of Bahria Town was looking after all their country wide projects from Bahria Town Karachi.

Sources told Profit that FBR may start investigating another property of Bahria Town, the Mall of Islamabad.

The general public has already invested over Rs 30 billion in Mall of Islamabad for purchasing apartments and commercial shops and there is discussion within the FBR that the government wanted to secure the billions of rupee investment made in Mall of Islamabad. n

The scam started six months ago, and the ride-hailing company has since blocked more than 80,000 accounts possibly linked with the fraudulent activity targeting their fleet of delivery riders

By Usama Liaqat

Ride-hailing service inDrive has blocked more than 80,000 accounts from its platform after an organised scam targeted scores of its courier delivery riders. The scam involved unknown individuals impersonating commissioned military officers who would then defraud the delivery riders into sending them money.

At a media briefing in Lahore, inDrive’s Country Manager for Pakistan, Awais Saeed, said his company initiated an investigation after a number of courier riders complained about losing their money to the scam. After ascertaining a pattern, inDrive has lodged a formal complaint with the National Cyber Crime Investigation Authority (NCCI) office in Islamabad.

The scam first emerged around six months ago. As reported by numerous couriers, they would receive an order from a customer on the app for a parcel delivery. Crucially, this customer’s name on the app would appear with a military rank — most often that of Captain or Major. They topped this up with setting the drop-off locations close to Cantt areas, especially in Karachi. This, for the couriers, marked a signal of authority. Disobedience was not really an option. Often such rides were booked at “unusually high fares for short-distance deliveries,” according to a recent press release issued by inDrive. All snares to entrap the unsuspecting.

The customer would then ask the rider to pick the package from, let’s say, a CSD or supermarket. Once the courier had reached the pick-up location, the customer would call them on Whatsapp saying someone was just making the payment inside the supermarket and needed cash for the transaction. The courier rider would be asked to transfer this amount through JazzCash or Easypaisa, and told the person would hand the stuff over to them after which the courier would deliver it to the military officer.

Often, if the rider expressed discomfort, the person on the other end of the phone would adopt two techniques. The first was to promise extra payment for the favour on top of the al-

ready high fare being offered for the delivery. If the driver still expressed unease, the scammers took harsh and peremptory tones, concocting urgency, and ‘ordered’ the rider to pick the parcel and pay for it. The fact that the person making this threat purported to be associated with the Army was intimidating enough.

In some cases, couriers made payments as high as Rs 30,000. Once these payments were made, the number they had been in touch with would block them. There was no one at the location and the address inside the Cantt had been faked as well. The riders had nowhere to go.

Reports started coming in from aggrieved drivers. They were naturally confused and embarrassed about what had befallen them. What made the situation especially poignant is that, hoping for swift remuneration, some riders had even borrowed money to pay for the fake ‘transaction’ in the hope that they would get a reward from the imposter military officer.

The inDrive management took timely note of this, and started to take measures to curb the possibility of such events occurring as much as they could through the platform itself. They began by blacklisting any accounts that had designations such as “Captain” or “Major” in the name or even abbreviations like “Cap” or “Maj”. All of these accounts were swiftly blocked. They also noticed certain phrases common to such scams and accounts using them were also blocked. Overall, over 80,000 accounts were banned from the platform. Only a handful of people, not even in the double digits, reached out to inDrive to say their accounts had been unjustly blocked, indicating almost all of the 80,000 accounts were from scammers.

The number alone demands a pause. But it also makes sense. Scams like this need volume more than anything else. It is entirely possible that a lot of inDriver couriers were approached regarding this scam and simply did not want to take the risk or find something suspicious and ignored it. They would have gone on about their day without reporting it. However, if the scammers were working in mass volumes, the likelihood of even a few riders getting scammed was higher. Over time, it would get noticed, but in the short term, the riders were unfortunately swindled out of their money.

inDrive’s response managed to curtail the problem before it got out of control. Through the platform, awareness campaigns were also run to caution users against such scams. Key characteristics of these scams were highlighted, and the freedom to cancel rides without any penalty – which the inDrive platform offers – was reiterated. Similarly, inDrive’s usage policy, which also explicitly states that couriers should not make payments on behalf of the customers, was also re-emphasized. The company has also been actively increasing the monitoring of any suspicious activity such as unusually high courier fare patterns across cities.

But questions still remain. How did these scammers have access to 80,000 mobile sims to be able to create these accounts? How is so much data so readily and cheaply available? Were these scammers using hacked WhatsApp accounts?

The inDrive management initiated FIRs and took the case up to the National Cyber Crime Investigation Agency (NCCIA). inDrive coordinated closely with the NCCIA over data sharing and analysis of behavioral patterns, resulting in a few suspects being identified and subsequently apprehended. Currently, these suspects are in judicial custody. The case is still ongoing in Islamabad, and the management of inDrive plans to see it through to the end.