31 Habib Metro lays out Rs700 million investment in non-banking financial services

34 China’s canola bet in Pakistan targets $4 billion oilseed import bill

08 How will existing solar net metering users be affected by NEPRA’s new regulations?

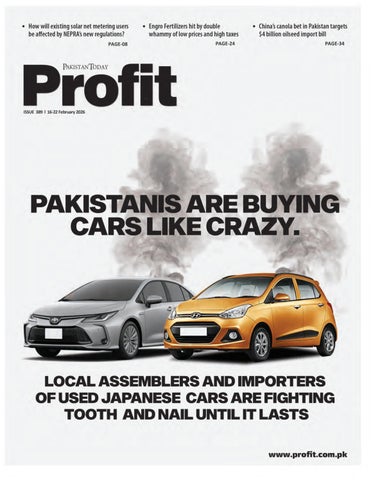

12 Pakistanis are buying cars like crazy. Local assemblers and importers of used Japanese cars are fighting tooth and nail until it lasts

18 After solid 2025, revenues at Mirpurkhas Sugar Mills faces rough start to the year

22 Falling market share, higher taxes hit profits at Bank AL Habib

20 In 2025, Meezan has a banner year… again

24 Engro Fertilizers hit by double whammy of low prices and high taxes

26 As AI eats into regular business, Symmetry acquires US-based marketplace

28 What are the expected savings from solar electricity for Beco Steel?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Usama Liaqat Shahab Omer | Zain Naeem | Nisma Riaz | Shahnawaz Ali | Ghulam Abbass Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing: Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news.

Contact us: profit@pakistantoday.com.pk

How will existing solar net metering users be affected by NEPRA’s new regulations?

In NEPRA’s new regulations, existing net metering solar producers have been shifted to net billing as well, however the Prime Minister has since taken notice of the matter

By Abdullah Niazi

Here is what has happened in short: the government has decided to abolish net metering for both existing and future solar consumers. New regulations were approved by NEPRA on Tuesday, and it became clear that the system of billing had changed for anyone who was on net-metering, be it new consumers or old ones.

There are 4.66 lakh net metering connections in the country, and most of them are installed in urban areas.

In response to the regulation there has been an uproar, and merely a day after NEPRA made its announcement the federal government seems to be backtracking on the status of those households that have existing net-metering connections.

The Prime Minister has already directed the power division to file an appeal with NEPRA and the Power Minister, Awais Leghari, has assured the senate there will be no change in the status of existing net-metering consumers (despite what the regulation clearly states). The question remains: What will happen now?

The difference be-

tween net-metering and net-billing

If you have solar panels, two things happen. During the daytime your panels produce a certain number of units of electricity and export them to the DISCO, and you offset that by consuming a certain number of units, either at the time or later in the day. If you consume less than you export, you get paid, and if you

consume more, you pay. (For the sake of simplicity and understnding this analysis excludes the additional calculation of on-peak consumption)

Now, if you make excess electricity, that electricity is free for you to store or to export to your DISCO, depending upon the kind of inverter setup you have. For all intents and purposes, the number that matters in net-metering is the units you export to the DISCO. Say you export 1,000 kWh of electricity in a month and consume 900 kWh from the grid.

Under the older net metering, you would receive credits for the 100 kWh that you give back to the grid. This means that your total bill is (-100 x NAPP), where NAPP is the National Average Purchase Price, the price at which the government buys back extra units. If the NAPP is 27, the bill comes out to be -2700. (The negative sign signifies that this bill is a receivable, and the DISCO owes you Rs 2700)

In net billing, this will change. Under the new regime, the total bill of your export will be netted against total import, instead of treating the differential of electricity consumed/ produced. Basically, the DISCO will now bill your entire export at the NAPP and charge you separately against your entire import.

To explain this we take the same example as above. If the electricity purchase rate, the NAPP, is Rs. 27 per kWh, your credit amount would be (-1000 kWh * NAPP), which comes out to be Rs, 27,000. But the bill for your electricity import will be calculated differently, at (900 kWh * Rs 47), which comes out to be Rs 42,300. The amount payable will hence be the net of these bills (hence the term net-billing), which is Rs 15,300. (A three-phased connection’s consumption of over 600 kWh is billed at ~Rs 47, according to current pricing regulations).

However, there is another twist. This calculation above is for existing prosumers, who have already signed a 7 year contract. New connections will get a different NAPP, at approximately Rs 11. Which means that if you are yet to get solar panels installed, then your bill, under the same consumption pattern would not be Rs 15,300, but a whopping Rs 31,300.

Compared to the earlier negative bill, under net-metering, the consumer will now have to pay at least Rs 15,300, for the same pattern of consumption. If the consumer manages to produce an extraordinary amount of units such that the net bill is still negative, they would get PKR credits like before, which can then be used to offset future electricity bills or be paid out based on the agreement, but that is also a fool’s hope.

Because the government’s plan is twopronged, in this regard and that is where sanctioned load comes in. Under the new sanctioned load regulation, a prosumer cannot get a net-metering setup of more than their sanctioned load. Previously, this requirement was at 1.5x a connection’s sanctioned load. Simply, this means that if your sanctioned load was 7 kW, you were allowed to install up to a 10.5 kWh solar setup. But under the new rules, your connection will only be approved if it is under 7kwh. This means that no-one can essentially beat the house (DISCO), in the longer run, until they significantly lower their consumption.

For a rough estimate, a 7kWh connection makes ~840 kW(units) per month on average, according to the commonly accepted annual average yield of 4x per day. A new user would hence, have to consume less than 200 units for the month, to merely break even.

How it affects existing prosumers

The decision has naturally been a cause for concern for those households that have already installed rooftop solar and are on

net-metering connections. Initial reports in the media were mixed over the status of existing net-metering users. Since those people with existing net-metering connections had signed seven year (in some cases five and three) year contracts with their respective power distributing companies like LESCO, PESCO etc, many felt they could not be shifted to net billing because it would go against the contract. However, while the Nepra regulations are dense, they are also very clear.

In section 21 of the regulations, Nepra categorically states that the 2015 regulations under which existing prosumers had signed contracts stand repealed. While this does not render the agreements void, the existing consumers will now be billed according to the new regulations.

This has naturally caused an uproar among existing consumers. They feel cheated out of their contracts. While the 2015 contracts explicitly stated that distribution companies cannot change the terms of these agreements, there was a provision that the terms of their contracts could be changed if Nepra intervened, which is what has happened in this case.

As things stand, all existing net metering connections have been shifted to the new net-billing system. There is still a protection for existing consumers in the new regulations. In section 21, the new regulations make it clear that existing consumers will be charged for electricity at the national average power purchase price until the terms of their contracts are up, which is currently around Rs 27 per unit. After the terms of their contract is up it will be charged at the national average energy power price.

Is the government backtracking?

There are currently 4.66 lakh net meter prosumers in the country. Most of these are centered in urban areas and have installed large solar systems to offset their consumption. Many have achieved zero as well as negative bills through net metering. With the introduction of net billing, the party will have to come to an end.

However, it is worth mentioning that the section of the population that has reaped the benefits of net metering are wealthy and influential as a group. Their complaints are loud and the government is clearly affected by them. The very next day after Nepra’s new regulations, Minister for Power, Awais Leghari, claimed on the floor of the senate that existing users would not be affected — despite what the regulations clearly state.

A little while after this, Prime Minister Shehbaz Sharif has instructed the power division to immediately file an appeal with Nepra to review the new solar regulations in an effort to protect existing contracts for current solar users. As things stand, the net metering of all consumers including old ones has been revoked. It has been replaced by net-billing. But the tone from the PM’s office indicates that these 4.66 lakh households will get what they want. n

PBy Usama Liaqat

akistanis are buying cars like crazy. Recent data released by the Pakistan Automotive Manufacturers Association (PAMA) has revealed that January 2026 recorded the highest automotive sales in the past 43 months. The total number of cars sold in January 2026 was 23,055 units. Of these, 18,602 (around 80 percent) are passenger cars such as sedans, hatchbacks, and EVs. The other 20 percent consist of light commercial vehicles, vans, jeeps, and SUVs.

While these numbers are not historically high, they mark a recovery after a sustained slump that began in 2023 when the rupee crashed and the dollar soared.

And this isn’t even the full picture. PAMA is the largest industry association for automotives in Pakistan, but they do not count KIA Lucky Motors among their ranks, meaning their sales are missing from this data. On top of this, these numbers do not include the sale of imported used cars coming mostly from Japan into Pakistan — and their slice of the pie is probably more than you think. Over the past year Japanese refurbished cars coming to Pakistan have increased exponentially. In fact, import data combined with excise registration numbers reveal that nearly 20% of all auto sales from December 2024 to December 2025 were imported used cars.

This is a monumental shift from where the auto industry was only a few years ago. Between 2020-23, the percentage that used cars occupied in Pakistan’s auto market was around 7.5%. The fact that the sale of locally assembled cars have increased over the past year in tandem with the sale of used Japanese cars indicates a market that has grown and accommodated all kinds of players after a period of stagnation.

The glut makes sense. Interest rates are down to 10.5% and the rupee has risen (ever so slightly) against the dollar every day for the past one hundred days. It is a classic picture of Pakistan leaning on import-led growth and similar to what happened to the auto market between 2022 and 2023. The rupee is propped up, import based consumption leads to a temporary surge in income, and Pakistanis that are raking it in spend the money on cars, weddings, and gold. While an inevitable crash could be around the corner any minute now, for the time being car sales are booming.

Those in the auto industry looking to sell you their wares are well aware of this. That is why there is a race between local assemblers and importers of used Japanese cars to try to make the most of this moment. Auto assemblers are lobbying to have restrictions placed on the import of used cars, and the start of this year proved a successful moment for them — with the government tightening the import process to effectively stop Japanese used cars from coming into Pakistan. But the lobbying to reverse this is

already underway. The clash is not a new one, but it is taking a new shape in what is a unique moment for Pakistan’s automotive industry. But how has it shaped up?

The rise and the interloper

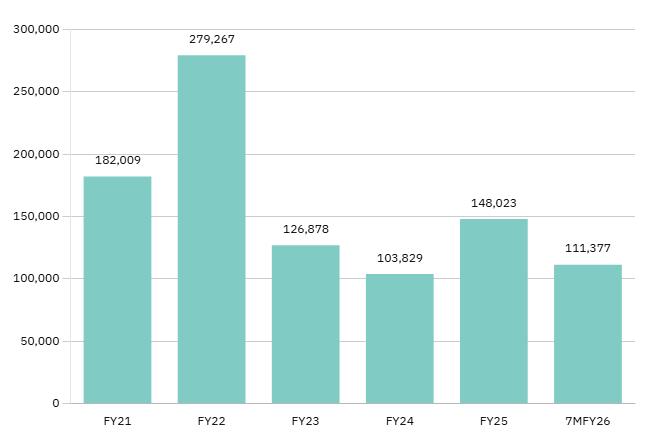

It is important that we understand just how much car sales have increased in the past year. While only the first seven months of the current financial year have passed, the number of cars (including passenger cars, LCVs, vans, and jeeps) is already higher than the total number of cars sold during the whole of FY24.

Just look at last month. January usually records higher numbers because people delay registrations in order for the car to have a more recent date, which affects its value. Yet, if we compare data from the first 7 months of FY25 with the first 7 months of the current fiscal year, it would still register a 43.4% increase, from 77,686 to the current figure of 111,377 units.

According to Mashood Ali Khan, the former Chairman of Pakistan Association of Automotive Parts & Accessories Manufacturers (PAAPAM), who said there are hopes that the total number of cars sold would reach 170,000 to 180,000 units by the end of this fiscal year. This, of course, only has to do with local car assemblers. You see when you’re in the market for a car in Pakistan you essentially have three markets to choose from. The first is to get a brand new car directly from a dealership. The second option is to buy a second-hand car that has already been bought and driven by someone else. Then there is a not-so-secret third option: imported used cars.

Normally, imported cars are a small segment of any country’s car market. Used cars represent almost zero per cent of sales in India, 0.3 percent in Vietnam, and 1.2 percent in Thai-

land — a contrast that experts say highlights Pakistan’s policy inconsistencies. Imports are usually just luxury cars in most countries. But things played out differently in Pakistan.

In the early mid-2000s, the government introduced a policy to facilitate overseas Pakistanis so that they would be able to bring over their vehicles from other countries. In theory, the cars being imported into Pakistan were simply for returning expatriate Pakistanis being allowed to bring their own cars back home. Since these were to be used vehicles and not brand new ones, the duty on them was much lower irrespective of brand and variation. Locally, or when a brand new car is imported, the tax is determined by how high-end the car is. Under this policy, even the fanciest of cars could be imported at the same duty meaning they would be cheaper in Pakistan.

People saw this as a business opportunity. Savvy car buffs earmarked Japan as the country to target because it has the kind of cars that Pakistanis like, and is home to brands like Toyota, Honda, and Suzuki that Pakistani consumers are used to. However, going to Japan every month and buying cars at an auction is difficult, and importing them even more so. Which is

why prospective importers contacted Pakistanis settled in Japan, and asked them to buy and ship the cars on their behalf for which they would pay them a fee. The overseas Pakistanis get a neat easy sum for signing some papers, and importers get next to duty free cars to sell on the Pakistani market.

Dealers set up massive showrooms all over the country with these cars. At the time when they started filtering in, Pakistan’s car market was a very different space compared to today. There were only three brands and their triopoly was so strong they did not bother introducing basic features like airbags even. The Japanese cars were a better quality, better build, and had superior features to locally assembled clunkers. And because of their superior features and Japanese safety standards, the cars compete with new cars. At least that is how the market has developed. There is more than enough room for fraud in this market, with dealers often misrepresenting how old the car is and why it was actually optioned off from Japan with things like accidents and the car getting stuck in a flood often swept under the carpet.

While the popularity of used imported cars has been undoubted, their supply has been inconsistent. When the government caught on to this business, they changed up regulations to reduce the number of cars a single expat could import. Local assemblers, incensed by the loss of business, lobbied strongly against them as well. The details of the back and forth are long, tedious, and have been covered by Profit before.

What matters is that from December 2024 to December 2025, the import of these cars was in full swing. And last year was a bit different in terms of how things played out. It has not been a question of local assemblers and Japanese importers duking it out. It has been instead a story of both finding plenty of buyers.

Car sales in Pakistan December 2024 to December 2025

Total sales

231,247 Total locally assembled cars sold

185,489

Total used imported cars sold

45,758

The interest rate has gone from 22 percent to 10.5 percent. This has made financing cars much easier for the consumers. Although the industry is still away from reaching the benchmark of selling 2 lakh cars per year, if the interest rate falls even more, we can cross that threshold

Mashood Ali Khan, former chairman of PAAPAM

For instance, the share of used car imports in the local auto market consisted only around 7.5 percent between 2020 and 2023. This share rose to around 20 percent by 2025.

Put this in number terms. From December 2024 to December 2025, just over 2.31 lakh unregistered cars were sold all over Pakistan. Of these, around 1.85 lakh were locally assembled cars. The remaining 45,000 cars were all used imported cars. That means on average nearly 4000 used imported cars were sold every single month. To put it very simply, Pakistanis seem to have more money to spend on cars. They are buying more Japanese cars and more locally assembled cars. The options for both have increased, and the response has been robust. The market has grown and gotten close to the heights it was at a few years ago, but the composition of who controls those heights has changed significantly in only a few years.

According to Mashood Ali Khan, the overall market has grown largely because of the slashing down of the interest rate. “The interest rate has gone from 22 percent to 10.5 percent. This has made financing cars much easier for the consumers. Although the industry is still away from reaching the benchmark of selling 2 lakh cars per year, if the interest rate falls even more, we can cross that threshold.”

Of course as we have just seen, it is the local assemblers that have not hit the 2 lakh mark last year. If used imported cars are included, last year’s sales were well over 2 lakhs.

Mashood admits, the stabilising political and economic situation also has a big part to play in how confident the consumers are of investing in the market. The fact that the rupee has stabilised and new players from South Korea and China have been encouraged by the government to enter and participate in the market has also made the consumer more optimistic, and willing to spend on a new car.

Plenty of space for the new kids

And this brings us to the second major cause. The dynamics of the market have been totally revolutionised by the entry of new OEMs. The govern-

ment had a policy to encourage auto producers to set up plants by offering them tax reductions, rebates, and discounts. And, on the fact of it, the policy appears to have done the job – there are now seventeen OEMs, compared to the Japanese Big Three which had dominated the local market for long.

But the fact remains that this massive influx – especially of Chinese OEMs such as BYD – is part of a global phenomenon. These cars because of their lower price point and better features that comparatively priced cars have really blown competition out of the stadium. And Pakistan is no different. Every few weeks a new car is introduced – such as the recent cases of Jaecoo J5, Tank 500, Deepal S05 – that astonishes the consumers into buying cars they had no plans to buy. And the ripples sent by such cars in the market have directly affected the prices of more established players. Even KIA had to slash the price of Sportage by around 14 percent last year to compete with these cheaper and more advanced variants.

Mashood Ali Khan welcomes this competition as bringing in something better for the consumer. According to him, “there will be a price fight between brands and models, so the OEM would have two choices: either to reduce their margins somewhat to make their prices more affordable, or to raise their quality of service to the customer so much that they are willing to pay higher prices for that”.

The fact, however, remains that the prices are still out of reach for many, and even the prices that have come down relatively, are still quite high on the nominal scale. And, if we consider the fact that car financing loans are capped at 30 lakh, it is still a little perplexing how people are rushing in to buy these cars.

This can however be explained, at least partially, by the fact that multiple car companies have been offering Equated Monthly Instalment plans at low (or in some cases, no) markup rates, filling the gap left by the State Bank’s cap of Rs 30 lakh on car financing.

At the same time, there is a real hype about the new cars. Even people who were not looking to buy new cars, enticed by the new features and ‘sale’ levels of prices, have rushed into the market. EVs and hybrid cars are the vogue, and

since multiple companies are competing for the consumer, it has tended to improve features and drive down prices. Given that multiple recently-hyped models are yet to be delivered – and are therefore not counted in the PAMA statistics –we might see a further jump once the deliveries start taking place.

Is the growth for real?

The point about hype and lower prices also raises questions on how sustainable this bump really is. There is a certain point below which the car prices cannot go. Similarly, although EVs do reflect a broader shift of preference, following global trends, the fact remains that the buying power of people generally is eroding, with real wages falling by almost 20 percent in the past 3 years. Though these new cars are also part of the framework supposed to usher in Pakistan’s green revolution in the automotive sector by encouraging the use of hybrid and EVs, it remains the fact that these cars remain beyond the reach of most of the population.

Similarly, the real GDP growth (2.68 percent in FY2025) has been below what regional peers like Bangladesh, Sri Lanka, and Vietnam have been achieving. Unemployment has been rising to levels not seen in decades, and foreign direct investment stats too don’t give sign for great optimism. The macroeconomic outlook doesn’t appear to be giving bright signs of times turning for the better, and the charm of newer models might soon have to contend with a moneyed reality.

The persistent question of policy again rears its head. In the previous two auto industry policies, incentives were given to OEMs in order to encourage new entrants to set up production ecosystems in Pakistan. Yet, as Mashood pointed out, the 2021-2026 policy is about to end soon. According to him, “the two previous auto industry policies allowed OEMs to import not only CKD kits, but also CBUs, and even assembly parts. This has meant that in the past 4-5 years almost no localisation has taken place through the new entrants platform”.

The only way the auto industry will register sustainable and positive growth, as Mashood says, is through increased localisation. Granted the OEMs have ‘brought in’ new technology, the opportunity for SMEs to do the same should also be granted. Mashood highlighted that once large OEMs are incentivised to localise, it would lead to the attachment of local SMEs with large scale manufacturers, and help improve not only the shape of the industry, but also contribute positively to local employment and export numbers. He also stressed upon the role of SMEs in generating economic activity, and highlighted that they employ around 25 million jobs and contribute Pkr 2.8 billion in exports. Helping them grow would, in the end, be better

for everyone.

And, it is not like there is no precedent for this. Since the mid-1980s when the three major Japanese OEMs entered Pakistan, they did invest in local industry, with the result being that some models were able to achieve 65-80 percent localisation. There’s no reason why, provided consistent institutional support, this might not be possible again today.

One way to incentivise localisation, according to Mashood, is to give export incentives to OEMs. “Now that we have so many OEMs, it is time to incentivise them to invest in local capabilities,” he said. This would involve not only creating new employment opportunities, but also the import of the latest global technologies. The result would be beneficial to the OEMs in two ways: first, their vehicles would become more competitive in the local market, and, secondly, it would enable them to compete in regional markets. This will then, ideally, help strengthen our exports, and ultimately lead to economic growth.

But the question of imports might yet complicate this situation. As mentioned before, the proportion of used vehicles in the total number of vehicle units being imported has risen to 25 percent in 2025 from 7.5 percent in 2020-23. The issue with these used car imports is that they are too good and have been able in the past to compete winningly with locally produced cars. Most of these cars originate from Japan, and the mere tag of a ‘Japanese’ car is enough to instill trust in the buyer, not to mention their superior performance and features. To the consumer, in the short run, this appears to be good. They are getting great cars at great prices.

Yet, there is a problem associated with this. In most of its recent history, Pakistan has been turning on the import tap without at the same time enabling local manufacturers to compete with these imported used cars. Though some localisation has taken place, in general with the new OEMs entering the market, the levels remain low. Since the demand for locally produced cars is eaten into by the imports of hifi Japanese cars, the local manufacturers feel it’s a losing game. At the same time, the economies of scale needed to economically produce more domestic cars become even harder to reach. To make locally produced cars of that quality and which inspire the same confidence will take time and investment.

This puts the government in a position where it has to juggle two main interests: first, of the consumer who wants cars, and Japanese imported cars are ever in demand; and secondly, of the local manufacturers who feel that if these imports continue to cut into the local demand, localisation – upon which the future of the automotive industry depends, would not take place.

The usual way of importing cars is through the overseas Pakistani method. Here

overseas Pakistanis are used as a front to import cars, since the government allowed them to import cars through three main schemes: the personal baggage scheme, the gift scheme, and the transfer of residence schemes.

In January 2026, however, the government abolished the personal baggage scheme through an S.R.O. 61(1)/2026, issued by the Ministry of Commerce. This move also tightened conditions on the other two schemes, making it much harder for imports to take place through this method. It would appear, on the surface, that the government is trying to reduce imports, and since then, imports are in fact at a halt. Yet, according to Arghan Tahir, an industry expert, disallowing and discouraging imports through the overseas Pakistanis scheme does not make sense for the government because of its shortterm goals of prioritising tax collection, and therefore, the decision cannot stay for long.

According to Arghan, “what usually happens in the ‘overseas’ way is that the overseas Pakistani makes a payment to, let’s say, Japan, from wherever he is. The car is then shipped to Pakistan, where import duties are required. This sum is again paid by the overseas Pakistani. So, effectively, no money has gone out of Pakistan, but the government is still able to collect taxes and duties off of it. It is too lucrative a way to collect revenue for the government to not do it.”

This underscores an important point. The government needs to find better avenues of taxation that are also sustainable in the long run, and do not actively discourage local industries from taking hold. This would obviously require tax reforms. At the same time, the local automotive industry is at a stage where some form of protectionism is required to incentivise local production, to effectively develop the industry across all functions, and not simply in name only.

It remains to be seen how effectively the government is able to negotiate the interests of the industry – which requires patience, and a long term strategy – and the demands of the local consumers for imported cars – which brings short-term gains yet could harm local industry in the long run if left unchecked.

For now, the market has absorbed all kinds of new players and there is money to be made for everyone. Beyond the traditional “Big Three” there are Korean and now Chinese brands making waves. The acceptability of used cars from Japan is also up. But the sunny disposition of this moment hides a plain truth: assemblers are not moving towards localisation fast enough. While localisation is widely seen as potentially a real leap forward, the fact remains that the current high demand – and inconsistent policy framework – means that it is still a reality more to be desired than achieved. In the long run another crash will come, and when it does, there will be many more players around to rue the day. n

After solid 2025, revenues at Mirpurkhas Sugar Mills faces rough start to the year

The company’s profits and dividends declined substantially in the first quarter of 2026 after a reasonable year in 2025

Mirpurkhas Sugar Mills’ latest numbers are a reminder that, in Pakistan’s sugar business, a “good year” is often best defined as less bad than the last one – and even that can prove fleeting.

For the year ended September 30, 2025 (FY25), the mill booked sales of about Rs12.6 billion, up from roughly Rs12.0 billion the year before, while the loss after tax narrowed sharply to about Rs251m (versus a loss exceeding Rs2.2 billion in FY24). The improvement was large enough to look like a turnaround on a chart – and it helped explain why the company’s own corporate briefing materials portrayed FY25 as a reset

year, even as the bottom line remained in the red.

But the first quarter of the new year landed with a thud. In the quarter ended December 31, 2025 (1QFY26), turnover fell to Rs2.27 billion, down from Rs3.19 billion in the same quarter a year earlier, while the loss after tax widened to Rs173 million from Rs60 million – a deterioration that effectively nearly tripled the quarterly loss.

Shareholders looking for a consolation cheque did not get one. Alongside the results, the board disclosed no cash dividend, no bonus shares, and no right shares for the quarter. That is not shocking – loss-making companies seldom distribute cash – but it matters because it frames the quarter as more than a soft patch: it pushes

any “back-to-dividends” narrative further out.

The broad arc, then, is clear: FY25 looked like stabilisation; 1QFY26 looked like relapse. The more interesting question is why.

The headline revenue decline in 1QFY26 is hard to separate from the two variables that routinely decide the fate of a sugar mill: the price of sugar sold and the price of cane bought.

In briefings around the period, Mirpurkhas’ management pointed to a market where ex-mill sugar prices were hovering around Rs138–140 per kg, even as sugarcane prices moved up from about Rs425 per 40kg to roughly Rs500–550 per 40kg. That is the kind of squeeze that can quietly ruin a quarter: selling prices don’t rise fast enough to keep pace with

raw material costs, and volumes alone rarely rescue margins.erly P&L reflects that compression. Gross profit roughly halved year-on-year, and operating profit shrank to a fraction of last year’s level. Put differently: even before finance costs, the business generated far less cushion to absorb the fixed costs of running an industrial plant.

Two additional factors also hang over the quarter: Even after Pakistan’s interest-rate environment eased substantially from its 2024 peaks, financing costs remain material for leveraged industrials. The State Bank cut the policy rate by 50 basis points to 10.5% in December 2025, but a lower policy rate does not instantly erase a large debt stock or working-capital borrowing tied to inventories.

Mirpurkhas has been building up its paper operations, but management itself notes that the paper division faces intense competition from informal players who avoid sales tax, creating a pricing disadvantage for compliant corporates. In other words, the “non-sugar” leg is growing, but it is not a smooth, high-margin annuity.

None of this suggests disaster on its own. What it does suggest is something more mundane – and more typical in this sector: a weaker quarter can arrive simply because the spread moved against you.

To understand why spreads move abruptly in Pakistan, you have to look beyond

the mill gate. Pakistan entered the 2025/26 season with a weather hangover. A USDA sugar report in December 2025 noted that flood damage across key growing zones –especially in Punjab – forced downward revisions to cane output, and projected cane sugar production of around 6.15m tons for 2025/26. The same report described how disruptions and uncertainty were shaping government choices, including the likelihood of keeping export restrictions in place.

Even the calendar matters. Cane harvesting typically begins in early November in Sindh and then moves northwards, with Punjab and Khyber Pakhtunkhwa following later; the PSMA recommended starting the crushing season on November 1, 2025 to mitigate supply gaps. A quarter ending in December, therefore, sits right at the intersection of start-up dynamics (ramping operations) and market expectations (what traders think the season will yield).

Then there is policy: sugar remains politically sensitive, so markets rarely clear in a neat, textbook way. In mid-2025, for instance, government and industry discussions around administered ex-mill prices made headlines, underscoring how quickly “market pricing” can become “managed pricing” when inflation optics matter.

This is the environment in which Mirpurkhas is trying to plan procurement, set sales strategy, and manage inventory. When management speaks about sugar prices being “range-bound” and about the upward drift in cane prices, it is describing not just supply and demand, but also a policy-and-weather driven market that can change character mid-season.

Mirpurkhas Sugar Mills is not a new-economy story. It was incorporated on May 27, 1964, and its principal business is still, plainly, manufacturing and selling sugar. It operates out of Mirpurkhas in Sindh and sits within the wider ecosystem of Pakistan’s long-established industrial groups.

Over time, however, the company has worked to be more than a one-crop, one-commodity play. Company materials describe an operating footprint that includes paper production alongside sugar, and the firm’s own briefing documents show paper volumes rising in recent years even as sugar volumes have been volatile. The logic is easy to see: a sugar mill with bagasse and fibrous inputs has natural adjacency to packaging, particularly when domestic demand for corrugated packaging rises with retail and FMCG distribution.

That pivot is not free of friction. Mirpurkhas’ management has highlighted how the paper segment competes with informal producers who can undercut compliant firms by avoiding tax, and how the company is exploring paper exports partly to reduce reliance on local credit cycles.

The more ambitious bet is still ahead: an

agro-pulping plant that management expects to commence operations by April/May 2026, with an intention to export surplus pulp if capacity exceeds internal needs. If executed well, that could deepen the non-sugar revenue stream –and, in theory, reduce the company’s sensitivity to sugar price swings.

But sugar cyclicality is stubborn. Even in the company’s FY25 operational data, sugar output and cane crushed were lower than the year before, while paper output increased – an encapsulation of a business trying to rebalance its mix without fully escaping its legacy core.

Zoom out, and Mirpurkhas’ quarter looks less like a company-specific crisis and more like a case study in how Pakistan’s sugar sector works.

Three structural realities matter.

Official policy has oscillated between intervention and “market forces”. The USDA report notes that Pakistan has moved away from announcing support prices and is formally withdrawing from setting sugarcane pricing –yet the government still plays a role in market stabilisation, including through trade policy and emergency measures.

Export permissions, export restrictions, and imports can each flip the domestic balance. The same USDA report noted that higher-than-anticipated exports contributed to market disruption and that the government authorised sugar imports (500,000 tons) to stabilise supplies. When that is the backdrop, a mill’s realised price is never just “the commodity price”; it is “the commodity price plus policy”.

Pakistan’s Competition Commission has repeatedly flagged the sector, including references to coordinated behaviour facilitated by industry bodies and even record penalties in the past. Whatever one thinks of enforcement outcomes, the fact that the regulator keeps returning to the sector speaks to a market where pricing and supply are often viewed through a political and regulatory lens, not purely a commercial one.

For investors, this translates into a sober conclusion: sugar mills can show dramatic yearon-year improvement without becoming “stable businesses”. Mirpurkhas’ FY25-to-1QFY26 swing fits that mould. A single quarter can look ugly simply because cane got pricier, sugar didn’t, and fixed costs did what fixed costs do.

The constructive reading is that the company’s diversification – paper, and potentially pulp – could gradually reduce that volatility. The cautious reading is that diversification itself has execution risk, and sugar remains the cashflow engine whose ups and downs will continue to dominate headline numbers.

Either way, Mirpurkhas has begun FY26 the way Pakistan’s sugar industry often begins: with uncertainty, narrow margins, and a market that can turn on a government notification as easily as it turns on the weather. n

In 2025, Meezan has a banner year… again

The Islamic banking juggernaut has continued to take market share and climb up the rankings of Pakistan’s largest banks

Meezan Bank has a habit of making even its “down” years look like someone else’s boom. The country’s biggest Islamic lender ended 2025 with deposits crossing Rs3.30 trillion – up 28% from Rs2.58 trillion a year earlier – at a time when the broader banking system’s deposit growth was closer to the high-teens.

And yet, the headline profit number went the other way. Profit after tax (PAT) slipped to Rs89.0 billion from Rs101.5 billion in 2024, while earnings per share (EPS) fell to Rs49.54 from Rs56.62. Total income also declined –Rs285.1 billion in 2025 versus Rs315.9 billion in 2024 – underscoring an awkward truth about Pakistani banking: in a falling-rate cycle, even a bank that is hoovering up deposits can find its revenue engine losing torque.

That combination – deposit momentum that screams “market share gains”, alongside profits that suggest a tougher operating climate – sets up the real story of Meezan’s 2025. It was

a year of franchise strength, but also a reminder that banking is, at heart, a repricing business: what you earn on assets moves faster than what you pay on liabilities, until it doesn’t.

In its year-end results announcement, Meezan framed 2025 as another year of “sustainable value” creation, pointing to a return on equity of 34% – still an eye-catching number for a bank of its size. The deposit milestone is the simplest proof point of the bank’s continuing gravitational pull. Deposits rising almost 28% in a single year is not just “growth”; it is growth that typically shows up when customers are switching primary relationships, payroll accounts, trade flows and business collections.

Contrast that with the system backdrop. The State Bank of Pakistan (SBP), in its mid-year review of the banking sector, reported deposits grew 17.7% in the first half of 2025 – strong, but well below Meezan’s full-year pace. Even allowing for the fact that mid-year numbers and full-year numbers do not map perfectly, the direction is hard to miss: Meezan is expanding faster than the market it plays in.

The bank’s balance-sheet deployment remained heavily tilted towards the classic Pakistani playbook – investments first, financings second – but with Meezan’s characteristic scale. It reported gross financings of Rs1.69 trillion and an investment portfolio of Rs2.60 trillion at year-end, with investments up 39% from the prior year. That matters because 2025 was not just any year: it was a year when the return on those investments began to drift down.

On the bottom line, the drift is visible in multiple places at once. Mark-up earned fell to Rs420.5 billion in 2025 from Rs494.3 billion in 2024, while profit after tax declined by roughly 12% year-on-year. Total income dropped by nearly 10%.

And yet, shareholders were not left high and dry on payouts. Meezan’s board maintained a familiar rhythm, approving a final cash dividend of Rs7 per share (70%), bringing the total cash dividend for 2025 to Rs28 per share (280%), following the interim dividend already paid for the first nine months. For investors, it was a message that the bank’s management still views the

earnings softness as cyclical, not structural. The cleanest way to describe Meezan’s 2025 is: the franchise got bigger, but the spread got thinner.

Meezan itself highlighted that net spread (its shorthand for the core margin pool) fell to Rs252.5 billion from Rs287.0 billion in 2024 –about a 12% decline – “primarily reflecting the impact of a lower policy rate environment”. That phrase – lower policy rate environment –did a lot of work in Pakistan in 2025.

SBP’s mid-year performance review noted that the policy rate was reduced by 100 basis points in January 2025 and by another 100 basis points in May 2025, reaching 11% by June 2025. By the end of the year, the easing trend continued: Reuters reported SBP cut the policy rate again in December 2025 to 12% (and that it had already been cut sharply from a peak of 22% earlier in the cycle).

Why does that matter so much for Meezan?

Because Meezan’s size and growth come with a balance-sheet reality: it has to park a large portion of its liabilities somewhere, and in Pakistan the “somewhere” is overwhelmingly government paper. When policy rates fall, the yield on new treasury bills and bonds usually falls quickly. Asset yields reprice down with speed, particularly on the liquid investment book.

Liabilities behave differently. For a bank with a heavy share of current accounts and low-cost savings (and for Islamic banks, profit rates that are competitively managed but often sticky), the cost of deposits can be slow to adjust and is bounded by practical floors. You can only cut the “cost” of a current account so far – because it is already near zero – and you can only compress savings returns so far before customers start shopping.

So, in a falling-rate environment, the bank can grow deposits and still see the margin pool shrink. That is the paradox of 2025: Meezan’s deposit engine likely brought in more lowcost funding, but the asset side of the book repriced down faster than the liability side repriced down, causing net spread compression. Meezan’s own numbers line up with that story: mark-up earned dropped by about 15% year-onyear, and total income declined by about 10%.

There is another, quieter factor in the background: industry-wide liquidity and investment behaviour. SBP’s review of the banking sector noted that deposits were growing strongly while advances contracted in the first half of 2025, pushing down the system’s advances-to-deposit ratio. When credit growth is subdued and deposits are plentiful, banks tend to compete more aggressively on asset pricing for quality borrowers and lean even more heavily into investments – both of which can pressure spreads when rates are falling.

Meezan, however, does not appear to have

paid for growth by weakening its risk posture. The bank reported a non-performing financing (NPF) ratio of 1.8% and a coverage ratio of 146%, alongside a capital adequacy ratio (CAR) of 19.2% – comfortably above the regulatory minimum. In other words: profits fell, but not because the bank went chasing bad assets. The compression looks cyclical – an interest-rate story – rather than a credit-quality story.

If net spread was the headwind, non-funded income was the tailwind.

Meezan reported non-funded income rose 13% to Rs32.6 billion from Rs28.9 billion in 2024, explicitly presenting it as evidence of diversification and resilience. That matters because in Pakistan, fee and commission streams, trading income and foreign exchange income often behave differently from the interest-rate cycle – sometimes providing exactly the kind of ballast banks need when margins narrow.

A useful window into the composition of that “other” income comes from Meezan’s consolidated interim financials for the nine months ended September 30, 2025. In that period, fee and commission income rose to Rs21.84 billion from Rs18.32 billion a year earlier, while foreign exchange income jumped to Rs5.99 billion from just Rs0.61 billion. The numbers are interim rather than full-year, but they help explain what “non-funded income” is likely doing under the bonnet: fees rising with transaction volumes, and FX income responding to flows and market activity.

Meezan’s own operational highlights point in the same direction. The bank said its Roshan Digital Account (RDA) programme had recorded cumulative inflows of USD 3.4 billion since inception, capturing 29% of total industry inflows – positioning it as a major conduit for overseas Pakistanis. RDA is not just a deposit story; it is also a payments, remittances and FX story, and those tend to show up in fee lines and foreign exchange income.

The strategic implication is important, especially as Pakistan’s banking sector becomes more competitive on deposits. It is one thing to win customers by offering a slightly better return; it is another to win them by being the bank that handles their payments, their business collections, their trade documentation, their investment subscriptions, and their cross-border flows. Non-interest income is often the scoreboard for that deeper relationship.

In 2025, Meezan’s non-funded income growth suggests it is doing more than expanding the balance sheet – it is expanding the “surface area” of its customer relationships. And as rates continue to normalise down from the extraordinary highs of recent years, that surface area becomes increasingly valuable.

Meezan’s market-share story did not begin in 2025. It has been decades in the making.

The bank was incorporated in 1997 and

later obtained a scheduled Islamic commercial bank licence in January 2002, formally commencing Islamic commercial banking operations in March 2002. It has long positioned itself as a bellwether for Shariah-compliant finance, describing itself as Pakistan’s first and largest Islamic bank.

The timing has turned out to be fortunate. Islamic banking in Pakistan has been steadily expanding its footprint, and SBP data suggests the segment has been inching up its share of system deposits. In SBP’s mid-year review, Islamic banking institutions’ share of deposits rose to 25.5% by June 2025 (from 24.9% in December 2024). That rising tide lifts multiple boats, but Meezan is not just floating – it is rowing harder than most.

Scale helps, and Meezan now has plenty of it. It reported 1,105 branches across 363 cities and a network of over 1,300 ATMs. It also said its market capitalisation had surpassed USD 3.2 billion, placing it among Pakistan’s most valuable listed companies.

But scale alone does not explain why deposits are growing so quickly. Part of the answer is structural demand: a meaningful share of Pakistani savers prefer Shariah-compliant products, and that preference has broadened beyond a niche audience into mass retail and corporate banking. Another part is execution: branch rollout, digital services, and the unglamorous work of becoming a bank that customers use daily rather than occasionally.

Meezan’s 2025 results suggest it is managing that transition well. The bank combined rapid deposit growth with strong capital buffers and low non-performing financings, while also expanding non-funded income streams – exactly the sort of mix that tends to produce durable market-share gains.

Still, the year also offered a cautionary note. A bank can win market share and still see profits soften when the macro cycle turns. Pakistan’s falling-rate environment in 2025 reduced the value of the industry’s most reliable profit engine – high yields on government securities –at least compared with the recent past. Meezan is not immune to that, regardless of how many deposits it collects.

In that sense, 2025 was a banner year… again – just not in the way the market has come to expect. The bank’s franchise strengthened, its balance sheet swelled, and its fee and FX engines gained traction. But the cycle reminded everyone that in banking, “bigger” does not always mean “more profitable” – not immediately, and not when the interest-rate tide is going out.

For Meezan, the bet looks clear: keep taking relationships, keep widening the revenue base beyond spread income, and ride the secular growth of Islamic banking – while accepting that the next few years may be about building advantage, not merely harvesting it. n

Falling market share, higher taxes hit profits at Bank AL Habib

The bank’s lending rates have come down faster than its deposit rates, causing a compression in net interest margins, but deposits have failed to keep pace with the industry

Bank AL Habib’s 2025 numbers read like a reminder of what Pakistani banking looks like when the interest-rate escalator starts moving down instead of up. The bank closed the calendar year with consolidated profit after tax of Rs32.5 billion, down from Rs41.9 billion a year earlier, as total income slid and operating costs rose. Earnings per share fell to Rs29.19 from Rs37.70.

In isolation, a Rs32 billion profit is not a crisis. It is still a large figure, and the bank remains meaningfully profitable. But in a sector where investors have become accustomed to bumper results – fuelled by high policy rates and the banking system’s heavy tilt towards government securities – any step-down in profitability immediately invites a more granular question: was the decline “macro” (the rate cycle), “micro” (execution), or “policy” (tax)? In Bank AL Habib’s case, it is a bit of all three.

The most telling line is net mark-up/ interest income, which fell 16% year-on-year to Rs131.0 billion, reflecting the squeeze that comes when asset yields reprice faster than funding costs. The bank’s consolidated total income (net interest income plus non-mark-up income) declined 12% to Rs162.9 billion.

Meanwhile, operating expenses rose to Rs95.6 billion from Rs81.6 billion – an increase of about 17% – further compressing the room

between income and profit. A research note by Topline Securities argued the fourth-quarter result landed below expectations largely because of higher-than-expected operating expenses, and pointed to elevated marketing spend (notably around remittances) that pushed the cost-to-income ratio to 67% in 4Q2025.

The bank also trimmed its cash payout. Topline estimates full-year dividend at Rs15.0 per share, down from Rs17.0 in 2024. For a shareholder base that has come to view part of Pakistani banking that reliably shows up –regardless of whether the economy is behaving – that step-down matters.

Start with margins. The State Bank of Pakistan’s mid-year review of the banking sector describes 2025 as a period of “further monetary easing,” noting the policy rate was reduced by 100 basis points in January 2025 and another 100 basis points in May 2025, reaching 11% by June 2025. That easing cycle is the sort of macro shift that quickly flows into banks’ asset yields – especially in Pakistan, where a large portion of earning assets are either floating-rate government paper or loans whose pricing is linked, directly or indirectly, to a benchmark that does not wait around.

For Bank AL Habib, mark-up/interest earned fell sharply year-on-year, while markup/interest expense declined as well but could not keep pace in a way that preserved the

spread. The result: net interest income down 16%. Topline attributes the fourth-quarter weakness specifically to “decline in asset yields,” which is precisely what you would expect once the rate cycle turns.

The bank did get some help from nonmark-up income, which rose to Rs32.0 billion from Rs28.9 billion. Foreign exchange income nearly doubled year-on-year, though it remains a smaller line than fee and commission income. In a bank with a meaningful trade-finance franchise, that makes trade-related flows tend to be more resilient than pure interest spread when borrowers and depositors are both repricing and recalibrating.

But costs did not co-operate. Operating expenses expanded, and the income statement shows total non-mark-up/interest expenses (including operating expenses, workers’ welfare fund and other charges) at Rs97.1 billion. Topline’s read is that the bank’s spending – particularly around customer acquisition and transaction flows such as remittances –helped explain why the quarter disappointed versus expectations. This is not necessarily an irrational trade: marketing and distribution spend can be an investment if it builds durable, low-cost funding and fee-based relationships. The issue is timing. In a year when the spread is already narrowing, “investing for growth” becomes harder to sell because it shows up

immediately in the cost base, while the pay-off arrives later – if it arrives.

Then there is the bank’s deposits its. Bank AL Habib’s consolidated deposits and other accounts were Rs2.598 trillion at end2025, up from Rs2.278 trillion at end-2024 –growth of about 14%.

Fourteen per cent deposit growth is not bad in a vacuum. But it looks less impressive against the system’s pace. SBP’s mid-year review notes that deposits for the banking sector grew 17.7% in the first half of 2025 –an “impressive” pace by the central bank’s description. Using that roughly-17% industry benchmark for the year (as market participants commonly do), Bank AL Habib’s 14% implies a modest loss of deposit market share – the kind of drift that does not trigger alarms, but does matter over time in a business where scale and funding mix are destiny.

This matters for the prompt’s central point: if lending rates come down faster than deposit rates, margins compress. But the reverse problem can also bite. If deposits fail to keep up with peers, a bank must either (a) compete harder on price, (b) rely more on wholesale borrowings, or (c) constrain asset growth. None of these is ideal. Bank AL Habib’s balance sheet shows borrowings fell materially year-on-year, while investments remained very large and advances declined. That pattern suggests a cautious posture: keep liquidity and investment income stable, avoid overpaying for deposits, and accept slower balance-sheet momentum.

There is a broader structural point here. SBP has repeatedly highlighted how Pakistan’s banking system earns a large share of its interest income from government securities, and its 2024 Financial Stability Review notes that interest/markup earnings from investments have risen to about 69% of total interest income. When that is the baseline, a rate-cut cycle is not a gentle headwind – it is a direct hit to the engine that was powering headline profitability.

The deposit market-share point can be overstated, so it is worth keeping it in proportion. A three-to-four percentage point gap between a bank and the system over a single year is not a referendum on franchise strength. Deposit growth is lumpy, and it can be influenced by corporate flows, government-related accounts, and one-off repricing decisions.

Still, the direction is meaningful. In Pakistan, deposit share is not just a bragging right; it is the raw material for (i) loan growth, (ii) fee income via transaction banking, and (iii) resilience when policy rates fall. If a bank’s deposit engine runs cooler than peers precisely as margins are compressing, it reduces management’s room to manoeuvre. You can see the tension in the numbers: total income down

12%, operating expenses up 17%, and profit after tax down 23%.

One plausible reason is that competition for deposits has become more intense – not merely among conventional banks, but also from Islamic banking institutions. SBP notes IBIs continued to edge up their share of deposits to 25.5% by June 2025. As Islamic banks expand, they do not just take new-to-bank customers; they also compete for the same retail and SME deposits conventional banks have historically treated as sticky.

Another factor is that 2025 was a year of “recovery after withdrawal of ADR related tax,” in SBP’s phrasing, which helped deposit mobilisation at the system level. If the system’s deposit growth was aided by policy-driven normalisation, then a bank that still grew deposits at 14% may simply have under-captured that rebound.

If margins were the macro story and deposits the competitive story, taxes were the policy story.

Bank AL Habib paid Rs35.7 billion in tax in 2025 versus Rs44.9 billion in 2024, but that decline reflects lower profit before tax. On an effective basis, the tax burden remained extremely high. Profit before tax was Rs68.2 billion; tax was Rs35.7 billion – an effective rate north of 50%.

That is not a Bank AL Habib quirk. SBP’s Financial Stability Review notes that taxation charges rose to 52.9% of pre-tax profit for the banking sector in CY24, becoming “an important factor” moderating after-tax earnings. In other words, the sector’s effective tax rate has been drifting towards levels that would look aggressive even in jurisdictions that openly treat banks as revenue workhorses.

The headline corporate tax rate has also moved against banks. SBP’s Financial Stability Review explicitly notes that the government “raised the tax rate for banking companies to 44 percent (for tax year 2025) from 39 percent.” That change is tied to Pakistan’s stopstart attempts to use tax policy to push banks away from government securities and towards private-sector lending.

A Financial Times report from late 2024 described how the government backtracked on an advances-to-deposit ratio (ADR) based tax penalty, and instead approved an overall increase in the income tax rate on banks to 44% (with a tapering path thereafter). The mechanism changed, but the message did not: banks are among the easiest places for the state to collect revenue, particularly because they are documented, regulated, and – unlike large parts of the informal economy – cannot simply disappear.

For investors, this creates a recurring dilemma. Banks benefit from high interest rates and government borrowing; then they are taxed because they benefited. As rates fall,

margins compress; but the tax take does not necessarily fall proportionately because the headline rate and supplementary levies remain high. The net effect is that after-tax profitability becomes more volatile than the underlying franchise might justify.

Bank AL Habib’s story is also, in miniature, the story of Pakistan’s private banking revival.

The bank is sponsored by the Dawood Habib Group, whose banking lineage stretches back to the pre-Partition era. On its own account, the group was among the founder members of Habib Bank Limited, and later – after nationalisation and then privatisation – was permitted to set up a new commercial bank. Bank AL Habib was incorporated in October 1991 and commenced operations in 1992.

It has since built a large domestic branch network and an outward-facing posture that includes international touchpoints (such as overseas branches and representative offices). Operationally, the bank has long been associated with relationship banking and a meaningful presence in areas like trade-related flows – an orientation that can be advantageous in a country where import cycles, export receipts, and remittances meaningfully shape liquidity and FX dynamics.

The group structure also reflects a broader ambition to sit across financial services. In its interim disclosures, the bank has referenced subsidiaries including AL Habib Capital Markets, AL Habib Asset Management, and AL Habib Exchange Company. These adjacencies matter because, over time, banks that can combine deposit gathering with fee-generating products – asset management, brokerage, transaction banking – are better placed to weather the next margin squeeze.

Bank AL Habib’s 2025 result is not a “story” because it is shocking. It is a story because it is illustrative.

An easing cycle (policy rate down to 11% by mid-2025) compresses asset yields. A bank’s ability to protect margins depends on funding mix and deposit momentum. Bank AL Habib grew deposits 14%, but that lagged the system’s roughly-17% pace, implying modest market-share slippage. And even after the macro hits land, the state’s tax appetite remains robust – SBP itself has pointed to a 44% banking tax rate for tax year 2025, and to taxation charges consuming an outsized share of pre-tax profit.

Put together, that is how a bank can go from Rs41.9 billion in profit to Rs32.5 billion in a year without any single line item imploding. The challenge for 2026 is equally unglamorous: rebuild deposit momentum, keep operating leverage in check, and hope the policy environment stops treating documented profitability as a sin. n

Engro Fertilizers hit by double whammy of low prices and high taxes

The company’s profits and dividends declined substantially after it faced lower prices from farmers still reeling from the effects of flooding, and the government’s extractive taxation policies

Engro Fertilizers (EFERT) has long been treated by Pakistani equity investors as the sort of stock you buy when you want to sleep at night: a defensive business tied to food security, plus a dividend stream that arrives with near-calendar regularity. In calendar year 2025, that reputation took a knock – not because the company stumbled operationally, but because two pressures hit at once: weaker realised prices and a heavier tax bite.

According to the company’s CY25 result reviews published by Arif Habib Limited (AHL) and Topline Securities, net sales fell 8% yearon-year to Rs237.1 billion, down from Rs256.7 billion in CY24.

The earnings line fell harder. Profit after tax declined 20% to Rs22.6 billion, translating into EPS of Rs16.95, compared with Rs28.3 billion and EPS of Rs21.16 a year earlier.

Then came the part that income-focused shareholders notice most: cash dividends.

Alongside the results, Engro Fertilizers declared a full-year dividend of Rs15 per share, down from Rs21.5 per share last year – a cut of roughly 30%.

Even the quarter, despite being a volume-heavy period, carried a sting. 4QCY25 profit fell 19% year-on-year to Rs8.4 billion (EPS Rs6.26), and the 4Q dividend was Rs4 per share, down from Rs8 per share in 4QCY24.

To put that dividend cut in context, Engro Fertilizers has historically run with a high payout posture. The company’s own published “dividend payout ratio” history shows long stretches where payout hovered around (or even above) 100% – a sign of how committed it has been to distributing cash to shareholders in good years. The AHL note underscores the same point from another angle: it puts the CY24 payout ratio at 102%, versus 89% in CY25, and flags that

the 4Q payout ratio fell to 64%, well below the company’s typical pattern.

So what changed? The short answer is: pricing and taxes balance-sheet caution that often accompanies both.

At first glance, an 8% decline in sales does not sound dramatic for a fertiliser business. But the composition matters. Both AHL and Topline attribute the revenue decline primarily to lower urea price per bag and a sharp slump in DAP dispatches (down 46% year-on-year).

In 4QCY25, Engro Fertilizers recorded net revenue of about Rs101.7 billion, up 20% year-on-year – helped by what AHL calls the company’s highest-ever quarterly urea sales of 1.03 million tonnes (up 46.7% YoY).

That sounds like a bumper quarter. Yet the same research shows that the company had to lean on discounts of roughly Rs400 per bag to move volume.

This is not conjecture confined to analyst spreadsheets showing on the fertiliser market described exactly that dynamic: record December offtake helped by major producers’ discounts, with Engro Fertilizer said to have maintained a discount around Rs400 per bag during December 2025 (later reduced as inventories tightened).

Discounting is the quiet reality of a market that looks “essential” on paper but is brutally sensitive to farm economics in practice. When farmers’ cashflows are squeezed, they delay purchases, trade down, or apply less than recommended – then producers end up financing inventory or pushing stock through the channel with incentives.

Pakistan’s farm sector has had plenty of reasons to be cautious. Commentary on the rural economy through 2024–25 highlighted a sharp erosion in farmers’ purchasing power, driven by falling crop prices alongside rising input costs – precisely the kind of environment in which fertiliser usage becomes a discretionary lever rather than a fixed habit.

Layer on repeated climate shocks and the caution deepens. The country is still dealing with the long tail of flood-related disruption, and subsequent flooding episodes have continued to hit agricultural areas – damaging crops, disrupting planting decisions, and worsening rural balance sheets.

Put simply: urea may be a staple input, but farmers still buy it with cash they may not have – and in 2025, many did not.

The bigger drag appears to have come from phosphate. AHL points to DAP dispatches down 46% YoY as a key factor in CY25 revenue pressure.

That, too, fits the broader market picture. DAP is usually the first fertiliser farmers compromise on when budgets tighten because it is far more expensive per bag than urea. Market reporting in 2025 noted how DAP dynamics were shaped by seasonal demand swings, inventory overhang, international pricing – conditions that can make distributors cautious and farmers reluctant to buy at the “wrong” moment.

Engro’s own quarterly picture, as summarised by Topline, shows that even as 4Q sales surged on higher offtakes, gross margins were below expectations, which the broker attributed mainly to higher discounting. In other words: EFERT managed the volume problem late in the year, but it did so by giving up some price and margin.

The result is a familiar Pakistani corporate tale: when end-customers are financially stressed, listed manufacturers do not necessarily lose sales outright – they often buy demand back through price concessions. That protects volumes and market position, but it depresses topline and squeezes profitability.

If lower realised prices explain much of

the revenue softness, they do not fully explain the profit drop. The more direct hit came from taxation – and, specifically, an additional levy that has become emblematic of the government’s habit of squeezing the formal sector when it needs cash.

Both research notes highlight a one-off “super tax” charge of roughly Rs2 billion booked in 4QCY25, which pushed the effective tax rate (ETR) to 49% for the quarter – well above the prior-year quarter.

Pakistan’s “super tax” has evolved from a targeted measure into a broader, slab-based surcharge on higher-income corporates. Professional tax summaries describe how the super tax regime was reshaped with new slab rates (including rates reaching as high as 10% for the largest income brackets), and later adjusted again via the Finance Act 2025 for certain ranges in subsequent tax years.

For companies like Engro Fertilizers, the point is not merely the percentage. It is the signalling: when the government is short of revenue, it tends to reach for tools that are easiest to administer – meaning the burden lands on the most documented, audited, and compliant businesses first.

This is where the “extractive” description starts to feel less like rhetoric and more like mechanics. The informal economy cannot be charged a super tax if it does not declare income. A large, listed manufacturer that files, audits, and pays – can.

AHL also notes that management appears to be provisioning for other policy-linked liabilities – such as GIDC, “concessional gas”, and super tax – suggesting a more cautious stance on payouts even beyond the immediate quarter’s tax charge.

This matters for dividends because fertiliser businesses often function like cash machines in stable years: high utilisation, predictable demand, and relatively visible working capital patterns. When the tax authority (and related policy regimes) become less predictable, boards tend to hold more cash back – especially when they fear a retrospective bill or an adverse interpretation of a levy.

Topline’s note adds another piece of colour: EFERT’s debt was elevated by December 2025, reflecting capex financing and inventory-related working capital dynamics. In that context, a board that cuts the dividend is not only responding to lower earnings; it is also preserving flexibility in a tax-and-policy environment where surprises have become routine.

So while investors may debate whether EFERT’s dividend reduction is “temporary” or “a reset”, the more accurate interpretation may be: the company is absorbing a policy risk premium – and asking shareholders to share the pain.

Structurally, the company is part of the Engro ecosystem: PSX records describe Engro

Fertilizers Limited as a public company incorporated in Pakistan in 2009 as a wholly owned subsidiary of Engro Corporation Limited, with Dawood Hercules Corporation as the ultimate parent.

Operationally, the company’s roots go back further. Engro’s corporate history traces the commissioning of a major urea plant in Daharki with an annual capacity of 173,000 tonnes, launching what became one of Pakistan’s best-known fertiliser brands.

The modern scale step-change came with the commissioning of the EnVen plant in 2011. Engro’s own press materials describe that facility as having a production capacity of 1.3 million tonnes per annum, taking the company’s total annual urea capacity to 2.3 million tonnes – a reminder that EFERT is not a marginal producer; it is one of the anchors of Pakistan’s urea supply chain.

Over time, Engro Fertilizers has also broadened its commercial footprint beyond a single product category – through marketing of other nutrients, farmer engagement, and logistics. PSX’s company profile summarises its business as manufacturing, purchasing and marketing fertilisers, seeds and pesticides, and providing logistics services.

And then there is the shareholder compact: dividends. Whether one labels it “discipline” or “brand positioning”, EFERT has historically behaved like a high-distribution stock. The company’s own published payout history reflects years of high payout ratios, reinforcing why investors have treated it as a quasi-income instrument within the KSE ecosystem.

That is why CY25 matters. A one-year profit dip is one thing; a dividend cut in a name long associated with consistent cash returns is something else. It forces the market to ask: is this merely a rough patch driven by transient farm economics and a one-off tax, or is it an early sign that the “steady dividend payer” identity is becoming harder to sustain in Pakistan’s current policy environment?

Engro Fertilizers did not have a bad year because it forgot how to make urea. It had a harder year because the environment around it changed: farmers bought reluctantly and demanded price relief, while the state’s tax appetite rose – especially for the kinds of companies that cannot hide.

The double whammy shows up cleanly in the numbers: sales down 8%, profits down 20%, and dividends down from Rs21.5 to Rs15.

If 2026 brings better farm economics and fewer fiscal “surprises”, EFERT can plausibly revert towards its old patterns. But for now, the result is a reminder that in Pakistan, even the most essential businesses can find themselves squeezed – from below by customers with thin wallets, and from above by a state with a thick pen. n

As AI eats into regular business, Symmetry acquires US-based marketplace

The company is attempting to navigate the disruption caused by artificial intelligence in the software services business by owning its point of contact with prospective clients

Symmetry Group Ltd has decided that, if the world is going to shop for digital services differently, it would rather own the shopfront than merely rent shelf space.

In a notice to the Pakistan Stock Exchange dated February 11, 2026, the listed digital technology and experiences company said it has executed a Share Purchase Agreement to acquire LogoDesignGuru.com, Inc. (LDG), describing it as a US-based digital branding and technology company that operates “AI-powered design platforms, digital asset marketplaces, and hybrid design-service models” serving international customers.

The company did not disclose the purchase price or transaction structure, but it did provide a rare datapoint that hints at scale: LDG is expected to generate roughly $0.7 million (about Rs200 million) in revenue during the current year, and is “currently generating a healthy level of profitability”, with Symmetry expecting post-acquisition earnings to improve via cost optimisation, operational efficiencies, and revenue growth initiatives.

That framing matters because Symmetry is not buying a trophy asset; it is buying a pipeline. The company explicitly linked the deal to an earlier, board-approved investment programme “to expand its international footprint and strengthen its platform-led digital capabilities” – a phrasing that reads like a strategic north star for a services firm facing a fast-chang-

ing competitive landscape.

Just two days earlier, Symmetry had told the exchange its board approved an aggregate investment plan of up to Rs1.25 billion, including “the acquisition of a US-based technology firm and a strategic investment in a local AI and data-driven digital company,” alongside spending to scale capacity, strengthen technology infrastructure, and support longer-term engagements. The LDG acquisition appears to be the first shoe to drop from that plan.

For two decades, Pakistan’s software and digital-services companies have sold a familiar promise: competent talent, priced competitively, delivered remotely. That model still works – but generative AI is changing the unit economics and the customer’s expectations on speed, iteration, and what “good enough” looks like.

The shock is not that AI can replace entire firms overnight. It is that AI can unbundle tasks – drafting copy, generating a first design pass, writing boilerplate code, producing multiple variants, testing edge cases – and compress timelines that used to justify a healthy billable-hours cushion. Large language models and generative tools push more work into the “commodity” bucket, and when work becomes commodity-like, buyers start shopping harder on price, turnaround time, and distribution rather than on bespoke craft.

Research outfits have been blunt about the breadth of exposure. The IMF has argued that AI is likely to affect a significant share of

jobs globally (with higher exposure in advanced economies), even if the outcomes vary depending on whether tasks are complemented or substituted. The OECD similarly highlights that many tasks – especially in higher-skill occupations – are susceptible to automation or reshaping as AI capabilities diffuse. And while “AI replaces jobs” is the headline that travels, the more immediate business reality is usually messier: AI changes workflows, shifts bargaining power, and pressures margins for firms selling time-and-materials services.

There is also evidence that AI can lift productivity in knowledge work – meaning clients may decide to do more in-house. A widely cited study by the US-based National Bureau of Economic Research (NBER) study on customer-support work found measurable productivity gains when workers used generative AI, with larger improvements for less experienced staff. Translate that into a procurement manager’s worldview and the conclusion is straightforward: if my internal team gets faster, why outsource as much?

For a services-heavy firm, this is a double bind. AI can help you deliver more with fewer people – but it can also help your customer internalise what you used to sell. That pushes services providers towards either (a) higher-value work that is harder to commoditise, (b) productised offerings where revenue is tied to platforms and subscriptions rather than hours, or (c) owning distribution so you can keep feed-

ing the funnel even as the market gets noisier. Symmetry, at least on paper, is leaning hard into (b) and (c).