10 Where Pakistani students go abroad 16 Palm oil sits at the heart of Pakistan’s food economy

18 Calcorp rebrands and enters the renewable energy business

20 What the end of Al-Jomiah lawsuit means for K-Electric

22 How the perfect storm hit the stock market and left it in the red

28 Inside the Chaudhry Sugar Mills case that first sent Maryam Nawaz behind bars

30 Pak-Qatar Family Takaful’s legal defeat and what it means for Pakistan’s insurance market 32 Pakistan’s state owned utility stores come to a whimpering end

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Usama Liaqat Shahab Omer | Zain Naeem | Nisma Riaz | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing: Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

A larger and larger number of Pakistani students are going abroad; where are they going, and for which degrees?

By Farooq Tirmizi

Approximately one out of every eight Pakistanis around the age of 30 has at least some college education. This number is not particularly impressive, but it is higher than most people might assume it is. Of those with a college education, about one in 25 – about 4.2% to be precise – have at least one degree from a college or university outside Pakistan.

Pakistani students are not yet a major force on the world stage – certainly not when compared to our neighbours in India and China which currently have 1.8 million and 1 million students outside their home countries respectively. But roughly 115,000 Pakistanis are studying abroad and while they are fewer in number than students from other countries, they represent a significant proportion of the country’s human capital, and in an emigration-obsessed country like Pakistan, they are also often the people most likely to become high-earning expatriates.

This is the story of Pakistani higher education more broadly, but specifically that of Pakistanis who are able to make the choice to go abroad for either their undergraduate or, more commonly, their postgraduate degrees. The patterns of where they have decided to go have shifted over the past several decades, responding largely to the dictates of foreign countries’ visa and immigration policies.

The attraction of a foreign degree is obvious: you get easier access to the ability to move to a foreign country, acquire an educational or professional credential from that same country, spend a few years building a network and acclimating yourself to that country, and then eventually applying for jobs there, directly landing into its middle or upper middle class.

If you are an 18-year-old A level or Intermediate student, or if you are a young professional under the age of 25 considering where to go for a postgraduate education, you may hope to join those who have made this leap in the past. The data we share here may help inform your decision-making process as you weigh your options.

First, we examine the state of higher education within Pakistan. We then examine where Pakistanis are going abroad, and what factors have been influencing their decisions, examining the major emigration destinations separately. Finally, we get to the more important question of: if you are a Pakistani in the position of trying to go abroad for an education, how should you make that decision?

The state of Pakistani higher education

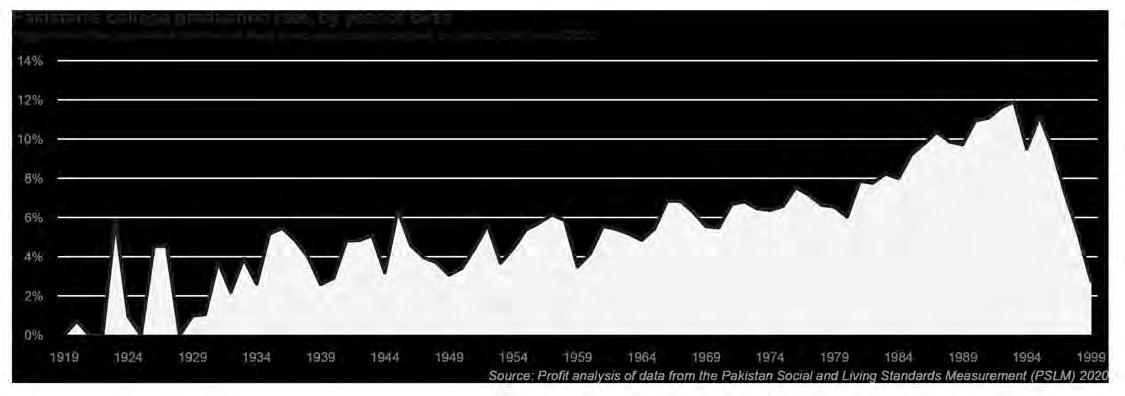

About 8.6% of Pakistanis over the age of 25 have at least a bachelors degree or higher, according to data from the World Bank for the year 2021, the latest year for which comparable data was available. But as we stated at the outset, that number hides the fact that younger Pakistanis are going to college at higher rates than their parents and grandparents, and that this increase in rate is itself increasing.

During the year 2020, about 11.2% of 25-year-olds in Pakistan had a college degree or higher, and 30-year-olds that year had a college attainment level that was even slightly higher, according to Profit’s analysis of data from the Pakistan Bureau of Statistics, specifically the Pakistan Social and Living Standards Measurement Survey (PSLM), the latest of which was the one for the year 2020.

That number is itself rising rather rapidly. The number of people in Pakistan who successfully finished a college degree in the academic year ending in 2022 was about 502,000 students, according to data from the Higher Education Commission of Pakistan. That number represents an average annual growth rate of 7.3% per year over the five years between 2017 and 2022. To put that growth in context, it is more than three times higher than the 2.1% per year population growth rate during that same period.

And when you factor in total enrollment, which includes the newer, larger classes of university students entering the higher education system, the numbers are even more impressive. As of 2024, the latest year for which complete data is available, there are 2.7 million higher education students enrolled at universities, colleges, and professional schools across Pakistan, a number that has been growing at 8.3% per year since the year 2000, according to data from the Higher Education Commission.

In other words, it is highly likely that the trend of every successive generation of Pakistanis being better educated than the previous one is not only continuing, but accelerating.

One way to place this rise of higher education in Pakistan is with the following statement: almost the same percentage of Pakistanis is college-educated today as was literate at Partition in 1947. The progress may be slow, but the direction is unmistakable.

Where do Pakistanis go

Given the fact that it involves considerable expense, it is a safe assumption that the vast majority of Pakistanis who decide to leave the country for an education are from the upper middle class. This is not a representative sample of the Pakistani population: it is an elite within the few who even get to attend higher education institutions in the first place.

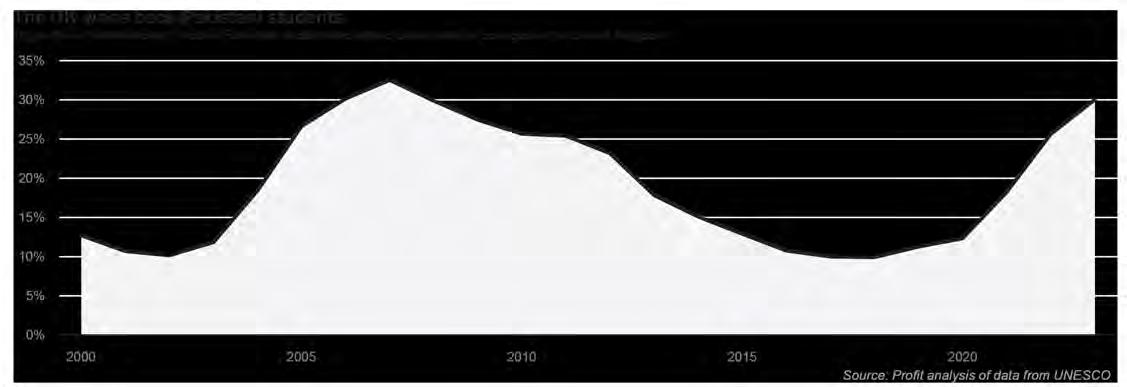

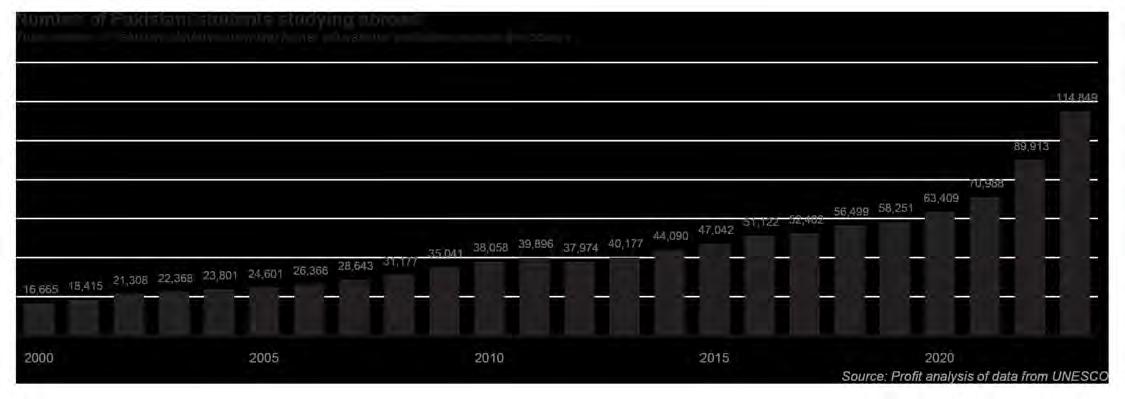

But while this elite was small as recently as the 1990s, numbering only slightly more than 16,000 in the year 2000, it has grown rapidly since then. In the year 2023, the latest year for which data is available from the United Nations Educational, Scientific and Cultural Organization (UNESCO), that number now approaches 115,000 students. On average, the total number of Pakistanis studying abroad has grown by 8.8% per year between 2000 and 2023, slightly faster than the growth in higher education enrollment overall.

As for where Pakistanis go, that is a somewhat predictable list, with a handful of outliers. The major countries of the Anglosphere – the United Kingdom, the United States, Canada, and Australia – dominate the list, accounting for 57% of the students who were abroad in 2023. Indeed, over the past two and half decades for which more complete data is available, the proportion of Pakistanis who go to universities in the Anglosphere has never gone below 46% of students.

The countries of mainland Europe account for approximately another 10%, with Germany and Italy leading the pack there. Kyrgyzstan alone accounts for 7.3% of Pakistani students abroad, followed by Malaysia at nearly 4% of students. We suspect China would be higher on this list, but there were no consistent sources of data on the number of Pakistani students in China. Based on other data points we were able to find, we estimate that approxi-

mately 20% of Pakistani students abroad go to China, making it the second largest destination behind the UK.

Now let us look at each of these destinations in turn, and what has influenced the pattern of Pakistani students going there.

The United States: the powerhouse with a closing door

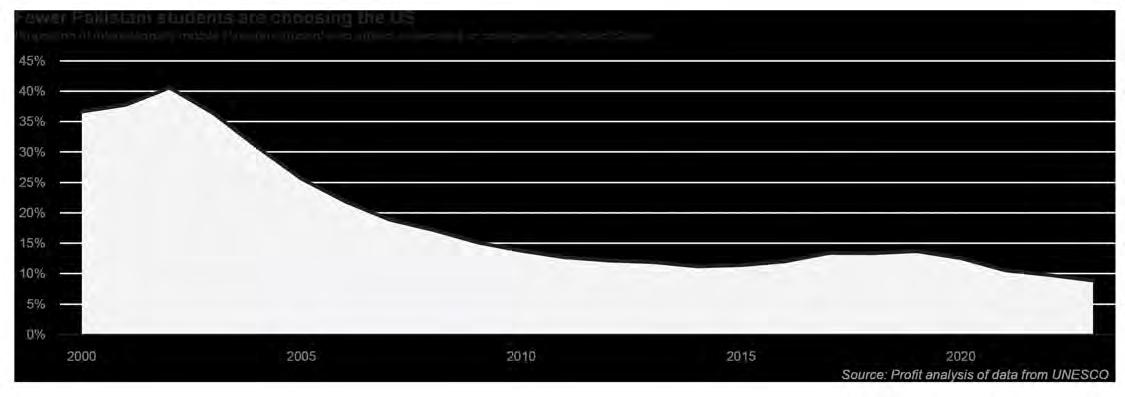

During the academic year 2001-02, the last year for which student visas were issued before the terrorist attacks of September 11, 2001 in New York and Washington, the proportion of Pakistani students abroad in the United States was around 40.6% of all internationally mobile Pakistani students.

Since then, while the absolute number of Pakistani students in the United States has generally trended upwards, the proportion of internationally mobile Pakistanis attending a US university has consistently gone down. As of 2023, that number is down to 8.8% of students abroad.

America beckons a smaller and smaller proportion of students from Pakistan each year. This is, of course, not surprising given several developments that have been taking place in the United States for the past several years, though two major factors have reduced the attractiveness of the United States for students from anywhere in the world, but especially Pakistan.

Firstly, US higher education is more expensive than anywhere else on earth and sees its costs rise faster than most other higher education systems in the world. Twenty years ago, the annual cost of an education Oxford and Harvard were somewhat comparable. Now, Harvard is about twice as expensive as Oxford.

This rising cost makes it difficult for families to consider the US option, even

though the US labour market more than justifies the cost. The American middle class – and especially the American upper middle class – is richer than any comparable class of people in any other country in the world. But this gets to the second, more important reason why the US is losing its attractiveness: the closing of its immigration system.

It may seem somewhat dissonant to talk about how restrictive the US immigration system is shortly after the Biden Administration let millions of people simply cross the border. But for anyone seeking to move to the US for higher education, the part of the US immigration system that matters is the part that governs work visas, and the US has a work visa system that is quite literally a lottery where your chances of success have dwindled to as low as 20% in recent lotteries for the H-1B work visa.

There is no point in attempting to pay the high cost of a US higher education if one cannot gain access to the US job market afterwards. More and more would-be migrants to the US have realized this, and have decided to seek their fortunes elsewhere.

The UK: the old magnet retains its attraction

Students from what are now India and Pakistan have been attending universities in the United Kingdom since the 1840s and for a long time, it remained the most popular destination for students seeking a foreign education. Around the late 1980s and early 1990s, however, it began to lose some of its prominence, and by the turn of the century, the UK accounted for just 10% of Pakistani students seeking an education abroad. Since then, the UK’s popularity has waxed and waned at rather frequent intervals, accounting for between a quarter and one-third of Pakistani internationally mobile

students in the latter half of the Musharraf era (2004 through 2008) before going back down to 10% in the aftermath of Brexit in 2016, and now back up to 30% in 2023, following the post-Brexit surge in international migration to the UK.

What makes the UK attractive? It is cheaper than the US, but still a rich country and one to which Pakistanis have deep historical ties. And it has generally been easier to get work visas in the UK after graduation, at least in that they are not subject to a lottery system, unlike the United States.

The problem with the UK, however, is that it is now a has-been. The notion of the UK offering prestige is a relic of a bygone era. American companies now routinely outsource back office functions to the UK and regard London as a mildly upgraded Bangalore. Indeed, American tech firms do more high value work in Bangalore than they do in London.

Per capita incomes in the United Kingdom have not risen since 2007, but prices have continued to rise, making the country uniquely unaffordable. The UK might be somewhat easier to move to, but the prize is increasingly

not worth it anymore. Why move to a place on the downswing?

Germany and Italy: mainland Europe calling

Perhaps somewhat surprising has been the rise in popularity of mainland Europe, specifically, Germany and Italy, given the fact that Pakistanis generally do not speak German or Italian and these countries have historically been rather jealously guarded about promoting their own languages. In recent decades, however, as Italy and Germany have aged, they have sought to attract highly talented migrants from other parts of the world and therefore introduced university programs in English.

Pakistani students noticed. There used to be fewer than 1% of Pakistan’s internationally mobile students in both countries combined in the year 2000. By 2023, that number was 9.8%, a very rapid rise, the bulk of which has come in the past decade, particularly in the

aftermath of Angela Merkel’s 2015 decision to open up Germany to a much larger flow of migrants.

Stagnating Canada, rising Australia

Given the popularity of conversation about emigration to Canada, it is somewhat surprising to see that Canada is not a major destination for Pakistanis seeking to study abroad, with around 4% of internationally mobile Pakistani students choosing it, a proportion that has remained largely the same over the past quarter century. Part of the explanation might be this: why pay for a Canadian degree when you can simply get your education for a lot less money in Pakistan and then directly apply for emigration to Canada?

Canada’s points system based migration system has been particularly favourable for many upwardly mobile Pakistani urban professionals, and paradoxically, this renders the Canadian education system less favoured by Pakistanis.

On the other side of the world lies that other big Anglophone country: Australia. This is a destination that has rapidly gained favour among Pakistani emigrants, rising from 4% of Pakistani students abroad in 2000 to now 14.8% in 2023. Why the rapid shift? When the American door closed, many Pakistanis looked to Australia as a land where the could migrate to. It also had the Canada-like points-based system, as well as an inviting set of universities that easily recognize Pakistani qualifications.

The Australian job market also has the virtue of being much stronger than the Canadian market, so if one was going to choose a large Anglophone country to move to, Australia was becoming a much more attractive target.

China: the CPEC realignment

In the year 2000, the number of Pakistanis studying at Chinese universities was negligible. It is now the second largest destination for Pakistani students, behind only the UK. How did this happen? CPEC. The China Pakistan Economic Corridor has prompted the Chinese government to offer spots to foreign students from Pakistan to come and study at their universities.

The students moving to China are generally studying technical subjects, and while some of them might get a job for a short period of time, most of them get the job, but then return home since China is not a country that tolerates permanent migration, or even long-term residence. Go to China if it is your best option. Just know that you will almost certainly have to come back.

Know your worth

Sometimes we as Pakistanis can take humility too far and assume that any place outside Pakistan must be better than staying inside the country.

The region that now constitutes Pakistan has been poorer than Europe for much of the past 200 years, but since about the 1860s onwards, has also had a small elite that was connected to Europe, and then later North America in a manner sufficiently close enough that they knew exactly how far behind Pakistan is compared to the most advanced countries in the world.

That resulted in a culture of elite longing for a life at the cutting edge of human economic progress, which meant a desire to move outside the country. In other words, there has never been a time in Pakistani economic history when there was not a substantial portion of its elite that wished it lived in London (and later, New York and Dubai).

The culture of an elite has a way of percolating down to lower strata of society, and this particular desire is no different. When a young high school student in Pakistan imagines a bright future for themselves, they imagine themselves outside the country, not inside it.

Migration, in short, is the very definition of having “made it”.

Where to study abroad remains an enormously personal decision, and this newspaper recognizes that it has negative effects for Pakistan, particularly with respect to the brain drain, so we will never encourage it. But we do recognise that it is a topic of conversation du jure among many people, so we think proving sufficient information to help empower better decision making is a role we can help play.

If you are going to disrupt your like by moving countries, and take on that multidecade commitment, your horizon for data should also be multi-decade.

Do whatever you deem best for your and your family’s needs. But for the love of all that is holy, do not move to Europe.

The raw numbers themselves are

rather telling: a Pakistani moving to the UK can expect an average purchasing power parity-adjusted income boost of just 6.9 times their Pakistani income. For Germany, the number is a bit better at 8.4 times, but for Italy, it is worse, at 6.5 times Pakistan’s per capita GDP on a purchasing power parity basis.

It gets worse if you look at the trajectory Europe has been on. Between 1950 and roughly 1980, Europe actually grew faster than Pakistan, largely on the back of the American-financed reconstruction of the continent following the end of World War II. Pakistan started very slowly catching up between 1980 and 2000 as European growth slowed and Pakistani growth speeded up. By starting around the year 2000, the direction has been one-way and negative: Pakistan’s per capita incomes have consistently outgrown those in the three major European economies mentioned above, and a trend that is unlikely to abate for the simple reason that these countries are, quite literally, dying.

Childlessness occurs at high rates in most European societies, which means these countries are getting older and with each passing year, fewer and fewer children are born, which in turn means the countries keep on getting even older.

Not having the right balance of young and old people means these countries are effectively waiting for the deaths of the bulk of their population. That does not mean these countries will not have rich economies for the foreseeable future, but it does mean that countries like Pakistan will consistently outgrow them. These countries have gone from being almost as rich as the United States to being not just poorer, but on track to hit parity with countries like Pakistan for the wrong reasons: because they declined too rapidly. n

Palm oil sits at the heart of Pakistan’s food economy

In this interview, Izzana Salleh Secretary General of the Council of Palm Oil Producing Countries (CPOPC) talks about the importance of the palm oil sector, the challenges it faces, the opportunities it creates, and Pakistan’s role in its future.

Palm oil is so embedded in daily life in Pakistan that it is almost invisible. It is the ghee in household kitchens, the base fat in bakery items, the frying medium for snacks, and a quiet but constant presence in packaged foods across income groups. Yet outside policymaking and industry circles, few realise that palm oil is not just another imported commodity. It is one of Pakistan’s largest and most persistent imports, a cornerstone of food affordability, and a major source of caloric intake for a population that relies overwhelmingly on imported edible oils.

In fiscal year 2025 alone, Pakistan imported about 3.2 million tonnes of palm oil, worth roughly $3.4 billion, making it one of the country’s most critical import lines by value and volume. Palm oil now accounts for the bulk of edible oil consumption in a country that imports more than 80 percent of its edible oils, leaving domestic food prices highly sensitive to global supply conditions. Any disruption in palm oil flows would ripple quickly through household budgets, food manufacturers, and retail markets. This dependence is not accidental, nor is it recent. It reflects decades of structural reliance on palm oil as the most affordable and versatile vegetable oil available at scale.

One of the most significant factors underpinning this dependence has been Pakistan’s long-standing relationship with Southeast Asia’s two palm oil powerhouses, Malaysia and Indonesia. Together, they supply the vast majority of Pakistan’s palm oil imports and anchor the country firmly within the Asian palm oil value chain.

In this interview, we speak with Izzana Salleh, the Secretary-General of the Council of Palm Oil Producing Countries (CPOPC), who provides insights on the current conditions of the palm oil sector and the steps needed to enhance its role on the global stage.

1. What distinguishes CPOPC’s role in the palm oil sector, and what progress has it enabled so far?

Izzana Saleh: CPOPC is neither a regulator

nor a commercial actor. Our role is to act as a bridge and connector. We bring producing and consuming countries to the same table and encourage constructive, evidence-based dialogue. Over time, this has helped shift the global conversation on palm oil from a polarized debate to a more balanced and solution-oriented discussion that recognizes benefits for farmers, industries, and consumers alike.

We focus on how palm oil contributes simultaneously to food security, affordability, and sustainability, and how these objectives can progress together rather than being treated as competing priorities.

2. What major changes have shaped the palm oil sector in recent years?

Izzana Saleh: The most significant change is that palm oil no longer exists in isolation. Today, food systems, energy transition, trade, and geopolitics are deeply interconnected. Sustainability has moved firmly into the mainstream: certified sustainable palm oil now represents more than 20% of global supply, and this share continues to grow.

At the same time, demand has shifted decisively toward Asia. Markets such as India, China, and Pakistan are now shaping global palm oil dynamics, giving Asian consumers and policymakers a stronger voice in determining how the sector evolves.

3. How important is Pakistan in the global palm oil value chain?

Izzana Saleh: Pakistan is extremely important both in scale and strategic significance. It is among the world’s top palm oil importers, accounting for around 9% of global import demand, alongside India (18%) and China (11%). This firmly positions Pakistan as one of the three largest consuming markets globally and confirms Asia as the center of gravity for future demand.

Pakistan’s palm oil consumption reached approximately 3.3 million tonnes in 2024, or about 4.3% of global consumption, making it the world’s fifth-largest consumer after Indonesia, India, China, and the EU-27.

CPOPC does not view Pakistan merely as a market. It is a long-term strategic partner

whose stability matters to the entire global palm oil value chain from producers and smallholders to traders, processors, and consumers.

4. From CPOPC’s perspective, what are the most urgent needs of the palm oil sector today?

Izzana Saleh: The most urgent need is predictability in policy, trade, and sustainability expectations. Palm oil sits at the intersection of food security, energy transition, and rural livelihoods, yet it is also one of the most heavily regulated agricultural commodities globally.

Sustainability is no longer niche. Certified sustainable palm oil accounts for about 20.1% of global production, making it a real-volume reality rather than a voluntary add-on.

Inclusivity is equally critical. Smallholders contribute around 70% of global food production, yet only about 19% of global ESG financing reached agriculture and smallholder systems in 2024. Sustainability must therefore move from compliance to contribution, rewarding real progress on the ground, including credible national schemes such as ISPO and MSPO.

Stronger producer–consumer dialogue is also essential, especially in markets like Pakistan, where palm oil accounts for 70–75% of edible-oil consumption and directly affects household staples such as ghee and cooking oil.

5. How has the long-standing partnership between Pakistan, Indonesia, and Malaysia evolved?

Izzana Saleh: This partnership has deep roots. Pakistan first imported palm oil from Malaysia in 1970, and Indonesia became a major supplier in 2000. For more than five decades, the relationship has been built on trust and reliability.

Looking ahead, cooperation can expand beyond trade into refining, logistics, and regional distribution, allowing Pakistan to play a stronger role in the wider region.

6. How important is producer–consumer dialogue in countering misinformation and ensuring science-based policies?

Izzana Saleh: As a major importer, Pakistan faces recurring concerns around health, price volatility, and import dependence. CPOPC’s engagement combined government dialogue, expert communication, and mass-media outreach.

Working with ministries, health professionals, industry stakeholders, and the Pakistan Edible Oil Council, we positioned palm oil within Pakistan’s food security and affordability priorities using science-based messaging. This approach delivered results. Positive sentiment toward palm oil rose from 8.2% to 11.5%, while negative sentiment remained contained despite price sensitivities demonstrating that dialogue directly enables science-based policymaking.

7. What are the main objectives of the Global Framework of Principles for Sustainable Palm Oil (GFP-SPO)?

Izzana Saleh: The GFP-SPO is built on one simple idea: sustainability must be fair, inclusive, and practical. Adopted in 2021 and launched in 2022, it is anchored in the UN Sustainable Development Goals.

It aligns sustainability narratives, maps existing mandatory schemes such as Indonesian Sustainable Palm Oil (ISPO) and Malaysian Sustainable Palm Oil (MSPO), and provides a common SDG-based language for engagement with consumer markets. It is not a replacement scheme, but it is framed to be globally applicable while still recognizing different national realities and levels of development, and it explicitly includes smallholder inclusiveness as a core principle.

8. What approach does CPOPC use to improve the global narrative of palm oil?

Izzana Saleh: We reframe the conversation from confrontation to common interest. Palm oil lies at the intersection of food security, affordability, energy transition, and rural livelihoods which concerns shared by producers and consumers alike.

CPOPC acts as a bridge, counters misinformation with data, and builds trust so sustainability, trade, and food security can advance together.

9. How can Pakistan align sustainability standards without increasing costs for consumers?

Izzana Saleh: By focusing on long-term partnerships and supply predictability rather than short-term policy shifts. Recognizing credible national standards such as ISPO and MSPO, encouraging gradual improvement, and maintaining open dialogue are cost-effective approaches. Sustainability should reinforce and not undermine palm oil’s affordability.

PROFILE

Izzana Salleh

Secretary General

Izzana Salleh is the SecretaryGeneral of the Council of Palm Oil Producing Countries (CPOPC) and a distinguished leader across public service, private enterprise, and global nonprofit organizations. She brings strategic and diplomatic leadership to strengthening multilateral collaboration, advocating for producing countries, and advancing sustainability and inclusivity.

She has served on the boards of the Malaysian Palm Oil Council (MPOC), Malaysia Digital Economy Corporation (MDEC), TalentCorp Malaysia Berhad, and the Social Security Organisation (SOCSO) Investment Panel. In the private sector, she founded RISE Human Capital and previously held senior roles at PEMANDU Associates and Real Food Company, contributing to Malaysia’s food security initiatives. She is also the Co-Founder and Global President of Girls For Girls International (G4G), empowering young women across 40 countries She holds an MPA from Harvard Kennedy School, an MBA from Imperial College Business School, and a Bachelor’s degree in Biotechnology from California State University, Pomona. Her work has earned multiple accolades, including recognition as one of Malaysia’s Top 30 Women of Excellence.

10. What message would you like to share with Pakistan’s policymakers, industry leaders, and consumers?

Izzana Saleh: Palm oil will remain central to Pakistan’s food security and economic stability. The future should not be framed as palm oil versus sustainability, but palm oil as part of the solution. With cooperation and trust, palm oil can continue to support affordable food and responsible production.

11. How does CPOPC help improve public understanding of palm oil?

Izzana Saleh: We focus on facts. Palm oil is one of the most land-efficient vegetable oils and plays a vital role in feeding millions. Health and sustainability concerns must be addressed openly and scientifically. Through initiatives such as the YoungElaeis Ambassadors (#YEAs) programme, we empower youth, including many from Pakistan, to communicate science-based

information. CPOPC has received over 500 applications and nearly 25% of registrants are from Pakistan, reflecting strong engagement among young people.

12. What role can CPOPC play in stabilizing Pakistan’s edible oil sector?

Izzana Saleh: With demand projected to exceed 5 million tonnes before 2030, long-term coordination is essential. CPOPC can facilitate dialogue, share policy insights, anticipate regulatory changes, and encourage investment partnerships in refining, logistics, and bio-based energy helping reduce uncertainty and support stability.

13. What is your long-term vision for the palm oil sector?

Izzana Saleh: My vision is to move the sector from volatility to trust. Palm oil should be part of the solution for food security, inclusive growth, and regional stability. Sustainability must reward improvement, not create division. n

rebrands and enters the renewable energy business

Shareholder lawsuit withdrawn after the Sindh High Court rules in favour of the utility; a change of ownership may once again

For most investors on the Pakistan Stock Exchange (PSX), Calcorp Limited has long been the kind of name you scroll past: a small, thinly traded listed vehicle that has spent years doing what many such companies do – preserving capital, running a modest operating line, and occasionally hinting at a pivot that never quite arrives.

Last week, however, Calcorp’s board tried to make itself unmissable. In a set of special resolutions passed at an Extraordinary General Meeting (EGM) held on 22 January 2026, the company approved a name change and a sweeping rewrite of its principal business clause – one that explicitly opens the door to renewable-energy equipment, including importing, trading, assembling and manufacturing.

The rebrand is bold in its simplicity: Calcorp Limited will become ARM Green Industries Limited, subject to the usual approvals (including from the Registrar of Companies and the Securities and Exchange Commission of Pakistan). The “Green” in that new name is not decorative. Resolution No. 3 replaces the company’s principal line of business with language that, among other activities, includes “manufacturing, assembly, trading, import and export of renewable energy equipment and ancillary products”.

In other words: a listed company whose public profile has largely been tied to financial holdings and vehicle-rental cashflows is now formally positioning itself to ride Pakistan’s fastest-moving private-sector energy shift –distributed solar – at a moment when demand is being pulled by households and factories rather than pushed by the state.

The corporate mechanics matter too. Calcorp’s notification to the PSX is not a marketing deck; it is a governance document that signals intent through legal language. It tells investors the board wants the corporate “objects” broad enough to pursue renewable-energy equipment as a business line, and broad enough, too, to re-tool itself again if the opportunity set changes. That is often what rebrands on the PSX really represent: not just a change of signage, but a change in optionality.

Calcorp – ticker CASH – was incorporated in 1992 and has, over time, worn more than one corporate identity. The company was formerly known as Capital Assets Leasing Corporation Limited, and the PSX describes its principal line as that of a general-purpose holding company capable of investing in marketable securities, intellectual property and assets “plied for hire”.

That last phrase – assets plied for hire – has not been incidental. In recent years, Calcorp’s operating heartbeat has come from the vehicle-rental segment, complemented by investment income. For the nine months ended 31 March 2025, the company reported net income from “vehicle plying for hire” and other income, generating profit after taxation over that period.

If this sounds like a business built for steadiness rather than spectacle, that is because it largely has been. The company’s own disclosures have treated the fleet as a capital-allocation exercise: deploy funds into vehicles, monetise them as contracts mature, and recycle capital into new assets.

But Calcorp’s history over the last two years also includes something else that often precedes a strategic swerve on the PSX: a change of control.

be possible

In a “Significant Event” disclosure embedded in its interim financial information, Calcorp reported that its parent company, Optimus Limited, entered into a share purchase agreement on 15 October 2024 with a consortium of three individuals – Asif Ali Sheikh, Muhammad Hanif and Kashif Mumtaz – for the sale of Optimus’s entire shareholding in Calcorp, amounting to 9,020,473 shares (83.96% of issued capital).

The same disclosure sketches a familiar regulatory pathway: public announcement of intention, extensions to timelines, and compliance with takeover rules under Pakistan’s securities laws. The details are notable not because they are unusual, but because they show a listed company in transition – moving from being a controlled subsidiary of one parent to a platform reshaped by new owners.

By October 2025, Calcorp’s annual reporting language had become more explicit about that transition. The chairman’s review notes that the board was recomposed on 30 May 2025 following takeover of the company. The directors’ report adds that while Calcorp historically carried out vehicle-rental business (and continued to do so through the year ended 30 June 2025), it planned to discontinue that business and explore other options.

Crucially, the same annual report points to an internal corporate link that makes the January 2026 “green” turn look less spontaneous: Calcorp disclosed it was in the process of acquiring 100% of an associated company, Helios Resol Technology (Pvt.) Limited, and had commissioned independent third-party valuations in that regard.

That Helios connection is not just a footnote. In Calcorp’s January 2026 correspondence to the PSX about the EGM resolutions,

the company secretary’s email address uses the heliosresol.com domain – an additional hint that the group’s centre of gravity may already have shifted towards an energy-adjacent corporate ecosystem.

So Calcorp’s “historical product line” is best described in phases:

• Phase one: a leasing/financial-services identity rooted in its earlier corporate form.

• Phase two: a holding-company model that leaned into vehicle-rental cashflows and portfolio-style investing.

• Phase three (now being declared): a broadened mandate that includes renewable-energy equipment – paired with a new name meant to signal that shift to the market.

In Pakistani capital markets, these phase changes often tell you less about a company’s past than about the ambitions of whoever now controls it. Listed shells and small operating companies can become vehicles – sometimes literally, as Calcorp’s fleet business shows –for redeploying capital into the sector of the moment.

The EGM resolutions do not lay out a five-year strategy, project pipeline, or financing plan. They do something more foundational: they expand the legal capacity of the company to pursue a new line of business.

Resolution No. 1 authorises the change of name to ARM Green Industries Limited. Resolution No. 3 is the one investors will parse for substance. It deletes the existing principal business clause and replaces it with a broader statement that retains the holding-company character – investments in securities and intellectual property – but explicitly adds renewable energy equipment into the permissible activity list, including manufacturing, assembly, trading, import and export, along with “ancillary products”.

That phrasing matters in Pakistan’s current market context. “Renewable energy equipment” can include everything from wind-turbine components to inverters, batteries, mounting structures, charge controllers and smart meters. But the word that best explains the zeitgeist – and the likely near-term commercial logic – is solar.

Pakistan is in the middle of an unusually organic solar boom: not driven primarily by government auctions or utility-scale procurement, but by consumers and firms chasing reliability and economics in the face of high grid tariffs and outages. Reuters has reported that Pakistan’s solar imports from China rose sharply between 2022 and 2024, reaching a record level in 2024, and continuing into 2025. Independent energy analysts have similarly highlighted that Pakistan imported very large volumes of solar modules, with FY24 imports surging and FY25 continuing at pace.

Against that backdrop, “importing re-

newable energy equipment” reads, in practical terms, like an intention to participate in the solar supply chain – either as an importer/ distributor, an assembler of modules or balance-of-system components, or a longer-term local manufacturer should economics and policy align.

The resolution’s inclusion of “assembly” alongside “manufacturing” is a particularly telling sequencing. Assembly is often where new entrants start: it requires less capex than upstream manufacturing (cells, wafers, polysilicon) and can be scaled with demand. It also aligns with how many Pakistani businesses have approached the solar opportunity – beginning with trading and installation, then moving into light industrial activity (frames, mounting structures, wiring harnesses, basic electronics), and only later contemplating deeper manufacturing.

There is also a second-order strategic rationale for a listed entity to take this route. If Calcorp (soon ARM Green Industries) intends to make acquisitions, partner with overseas suppliers, or raise capital, being a listed company with an expanded object clause can make that process smoother. The resolutions essentially clear the runway for whatever corporate actions might follow.

None of this guarantees execution. Pakistan’s markets are littered with rebrands that promised new sectors and delivered little more than press releases. But Calcorp’s timing is at least rational: it is attempting to pivot into renewables at the precise moment when renewables – specifically distributed solar – have become a household economic strategy rather than a niche environmental preference.

To understand why a small listed firm would even contemplate “renewable energy equipment” as a strategic identity, you have to understand what has happened to solar economics in Pakistan.

Pakistan has emerged as one of the most important destinations for Chinese solar exports in recent years. Reuters, citing data from energy think tank Ember, reported that imports of China-made solar components jumped from roughly 3,500 MW in 2022 to a record 16,600 MW in 2024, with the import binge continuing into 2025. Ember itself has highlighted the scale of Pakistan’s panel imports in 2024 and the pace at which the market moved.

Other analysts tracking the distributed solar phenomenon put the cumulative figures even more starkly. A Renewables First report stated that Pakistan imported 17.9 GW of Chinese solar panels in FY25, with cumulative imports surpassing 50 GW as of September 2025. A separate Renewables First “Pakistan Electricity Review” similarly notes FY24 imports around 16 GW, framing the surge as a

step-change in rooftop adoption. What makes this boom possible is not just local demand – it is the global supply reality, in which China has built a manufacturing system so dominant that it sets the price curve for the world.

The International Energy Agency has noted that China’s share in all manufacturing stages of solar panels (polysilicon, ingots, wafers, cells and modules) exceeds 80%, after investing tens of billions of dollars in capacity and building an enormous manufacturing workforce. Overcapacity and fierce competition among producers have driven steep price declines in modules – one reason solar has become “cheap enough” for Pakistani consumers to treat it as a self-help remedy for tariff shocks.

Reuters has also reported that the average cost per watt of solar-module capacity exported fell sharply over recent years, reflecting both technological improvement and China’s scale-driven price pressure. The result is a paradox that Pakistani policymakers and the power sector are now wrestling with: private solar adoption is accelerating affordability and resilience for those who can install it, while also eroding the revenue base of a debt-laden grid.

For a company like Calcorp – soon to be ARM Green Industries – this context creates a clear commercial temptation. If Pakistan is importing solar hardware in enormous volumes, a slice of that import-and-distribution margin can look attractive, especially to new owners hunting for a scalable line of business. Assembly or light manufacturing could add another layer of value capture if policy incentives, duties, or local content rules tilt in that direction.

The hard part, of course, is differentiation. Pakistan’s solar market is crowded with importers, installers, and trading firms. A newly rebranded listed company will need to decide whether it wants to be:

• a trading house (import and distribution);

• an integrator (bundling panels, inverters, batteries, installation and after-sales);

• a manufacturer/assembler (starting with assembly, potentially moving deeper); or

• a platform that uses a listed vehicle to consolidate smaller players.

The January 2026 resolutions do not answer that. They simply give the company the legal authority to try.

Still, in Pakistan’s current energy economy, that authority is itself a signal: the solar rush is no longer just an energy story. It is now a capital-markets story – one that is pulling in companies from far outside the traditional power sector, including firms whose previous “product line” was, quite literally, cars for hire. n

What the end of Al-Jomiah lawsuit means for K-Electric

Shareholder lawsuit withdrawn after the Sindh High Court rules in favour of the utility; a change of ownership may once again be possible.

For more than three years, one deceptively narrow court order has functioned like a padlock on K-Electric’s corporate governance: no meaningful changes to the board, no clean resolution to shareholder wrangling, and – crucially – no straightforward path for fresh capital or a credible change-of-control story to take shape.

That padlock has now been loosened.

In a material information disclosure to the Pakistan Stock Exchange dated January 26, 2026, K-Electric said it had been discharged from Civil Suit No. 1566 of 2025 – formerly Suit No. 1731 of 2022 in the Sindh High Court – after the plaintiffs, Al Jomaih Power and Denham Investment, withdrew their claims against K-Electric and three related defendants.

The order itself, dated January 23, 2026, was passed by the senior civil court in Karachi (South). It allowed an application under Order XXIII Rule 1 of the Code of Civil Procedure and dismissed the plaintiffs’ claims against defendants 1 through 4 “as withdrawn”, while also declaring all pending applications by those defendants “infructuous”.

Those four defendants matter because they map neatly onto the ownership maze that has paralysed the company:

• Alvarez & Marsal (the restructuring/administration adviser drawn into the dispute),

• KES Power Limited (the majority shareholder vehicle holding 66.4% of K-Electric), and

• K-Electric itself, which said it had been impleaded as Defendant No. 4.

Put plainly: whatever else remains of the underlying shareholder feud, K-Electric has – at least in this particular suit – been taken out of the line of fire.

Even the plaintiffs’ own paperwork makes clear why the retreat happened now. Their withdrawal application cites a July 20, 2023 judgment of the Grand Court of the Cayman Islands granting an anti-suit injunction and directing them to withdraw the Pakistan proceedings against these defendants, and notes that subsequent appeals – including an attempt to go up to the UK Judicial Committee of the Privy Council – had been dismissed.

That overseas procedural backstop matters because much of K-Electric’s control dispute is not really being fought in Karachi at all. It is being fought in offshore corporate structures – Cayman Islands companies, British Virgin Islands vehicles, and shareholder agreements drafted for a world where disputes are meant to be settled far from I.I. Chundrigar Road.

Still, for Pakistani markets, what matters is the practical consequence: a legal cloud that directly named the listed company and its advisers has lifted.

To understand why this case mattered –and why its withdrawal could prove consequential – you have to rewind to October 2022, when the dispute between the ultimate owners of K-Electric’s majority stake spilled into Pakistani courts.

K-Electric is publicly listed, but its control sits upstream. A Cayman Islands company, KES Power Ltd, owns 66.4% of K-Electric; the Government of Pakistan holds roughly a quarter; the balance is with institutions and the public.

KES Power’s own shareholder base has been a battleground. One camp has been associated with IGCF SPV21 (an Abraaj-era fund structure), and the other with the long-standing Gulf investors – Al Jomaih and Denham.

The flashpoint came when a Pakistani investor group, operating through offshore entities, acquired control rights linked to the IGCF structure. Dawn reported in 2023 that the

tussle intensified after Sage Venture Group Ltd – a BVI special-purpose company of AsiaPak Investments – became general partner of IGCF following a court-sanctioned sale connected to Abraaj’s liquidation.

The News, reporting at the time, said the minority shareholders of KES Power went to the Sindh High Court and obtained a stay order that prevented changes to K-Electric’s board –blocking proposed new directors and leaving vacancies unfilled.

The market consequence of that stay was outsized. A listed utility can muddle through a lot – tariff disputes, fuel price shocks, political heat – so long as its governance mechanism keeps turning. But when the board cannot be reconstituted, everything else starts to jam: approvals slow down, strategic decisions become harder to defend, and every rumour about “who really runs the place” becomes a risk premium in the share price.

The plaintiffs’ current withdrawal documents make explicit what the Cayman courts had been telling them: as far as claims against the offshore defendants (and K-Electric as impleaded) were concerned, Pakistan was the wrong forum. The application states the anti-suit injunction was granted because the dispute was “not triable” in Pakistan and because the Pakistani courts “lack jurisdiction” over those claims.

This helps explain the strange geometry of the fight. In Pakistan, the most potent weapon

was not a final judgment – it was the interim restraint. Offshore, the most potent weapon was not operational control – it was jurisdictional leverage (anti-suit injunctions, winding-up petitions, and appeals ladders designed to exhaust the other side).

By late 2025, that offshore leverage had hardened. The withdrawal papers note the Cayman order “stands revived” after appeals were dismissed, and that is why the plaintiffs sought withdrawal.

So the end of this suit is not a sudden handshake; it is, to a large extent, a forced tactical retreat.

K-Electric’s story is, in many ways, Karachi’s story: messy, vital, and too big to ignore.

The company traces its roots back more than a century and remains Pakistan’s only vertically integrated utility, spanning generation, transmission and distribution across Karachi and surrounding areas – serving a population in the tens of millions.

In December 2005, the Government of Pakistan privatised Karachi Electric Supply Corporation (KESC), transferring 73% with management control to a consortium that included Hassan Associates, Saudi Al-Jomaih, and Kuwait’s National Industries Group, while the state retained a significant minority stake.

The theory was familiar: take a loss-making, politically entangled utility; put it under owners with money and incentives; and let investment plus discipline do what subsidies and speeches could not.

K-Electric itself has repeatedly highlighted post-privatisation capex and performance improvements – claiming billions of dollars invested since 2005 and substantial reductions in technical and commercial losses – often citing third-party assessments such as the World Bank-linked public expenditure review referenced in investor materials.

By 2009, private equity had entered the picture. An investor presentation by the company notes that Abraaj acquired a controlling stake in KES Power – the vehicle holding the majority shareholding in K-Electric – from Al Jomaih and NIG, with the transaction closing in April/May 2009.

This is where K-Electric’s governance began to resemble a Russian doll: a listed company in Pakistan controlled by a Cayman holding company, which is itself controlled through funds and shareholder agreements written in offshore legalese.

In October 2016, Abraaj announced an agreement to sell 66.4% of K-Electric to Shanghai Electric Power for $1.77 billion – a transaction that would have been one of the largest foreign acquisitions in Pakistan’s power sector.

Over time, the deal became a symbol of Pakistan’s investment bottlenecks: security clearances, regulatory conditions, and disputes

over dues and sector liabilities. The Express Tribune reported in 2017 that Pakistani ministries had issued security clearance certificates, but hurdles remained.

Then, in September 2025 – after nearly nine years of limbo – Shanghai Electric finally walked away. Dawn reported the Chinese firm terminated its offer, citing changes in Pakistan’s business environment. Bloomberg also reported the board decision to end the pursuit of the stake. Abraaj’s 2018 collapse and liquidation created a vacuum. Competing investors began arguing over what, exactly, the liquidators had the right to sell – and what approvals were required when offshore control translates into Pakistani corporate governance.

By 2023, Pakistani media were describing a new protagonist: Shaheryar Chishty and AsiaPak Investments, operating through Sage Venture Group and linked vehicles. Dawn noted that Sage became general partner of IGCF following the court-sanctioned sale, and that the conflict then centred on board appointments and control rights.

The Financial Times, in 2025, framed the dispute as a high-stakes contest between Gulf investors and Chishty’s camp, warning that the ownership feud risked derailing a multi-billion-dollar reform and investment programme for Karachi’s electricity infrastructure.

By late 2025 and early 2026, the conflict had also spilled into international claims. Business Recorder reported that Saudi and Kuwaiti investors had moved towards international arbitration against Pakistan over alleged violations tied to the K-Electric saga; K-Electric itself, however, has stated it is not a party to the arbitration.

In short: the company’s operating business has kept running, but its ownership story has remained stuck in procedural mud.

So what, exactly, does the end of this Al-Jomaih suit mean for K-Electric?

The obvious implication is governance. The suit that began in 2022 helped freeze board changes and contributed to a prolonged limbo in which vacancies could not be filled.

With K-Electric discharged from these proceedings, the company can argue – more credibly – that at least one key restraint has fallen away. That matters not just for optics, but for mechanics: board elections, committee approvals, and strategic sign-offs become less vulnerable when they are not shadowed by an active suit naming the company and its advisers.

Indeed, in the days following the withdrawal, Pakistani media reported the securities regulator moving to push long-delayed director elections – suggesting that the regulatory system may now try to snap back into place after years of uncertainty.

In corporate Pakistan, buyers hate two things above all: unclear title and frozen gover-

nance. This withdrawal helps on both counts, at least marginally.

But a clean sale process requires more than the absence of one lawsuit. KES Power’s shareholder map has been contested, with rival factions disputing who can speak for the holding company and on what authority.

Any eventual acquirer would need to navigate securities rules, corporate governance requirements, and the political sensitivities that come with owning Karachi’s only integrated utility.

The Shanghai Electric experience shows that even very large, state-linked foreign buyers can get stuck for years.

In that sense, the withdrawal is best seen not as the opening of the finish line, but as the removal of a major roadblock that had forced everyone to drive with the handbrake on.

The withdrawal documents are unambiguous: the plaintiffs were acting under the weight of Cayman court orders and dismissed appeals.

That will shape behaviour going forward. If the lesson is that Pakistani injunctions can stall governance but offshore anti-suit injunctions can ultimately unwind those stalls, future fights may migrate even more decisively to Cayman, London, and arbitral forums – places where Pakistani retail shareholders have little visibility and where timelines can stretch into years.

Even as this suit exits stage left, the broader drama remains:

• International arbitration risk: reports indicate Gulf investors have pursued arbitration claims against Pakistan linked to the K-Electric saga, while K-Electric maintains it is not a party.

• Fragmented beneficial ownership: public disclosures and letters in late 2025 suggested a complicated and shifting offshore ownership picture, including claims about different blocs and financial institutions holding interests upstream.

• Operational and regulatory headwinds: K-Electric’s core business still sits inside Pakistan’s power-sector constraints – tariff politics, loss recovery, fuel mix, and the broader circular-debt ecosystem that has torpedoed many otherwise sensible investment theses.

The end of the Al-Jomaih lawsuit – at least as far as K-Electric and the key offshore defendants are concerned – is a meaningful de-risking event for the listed company.

But it is not the end of the K-Electric ownership saga. It is more like the moment when a long-running boxing match breaks into a clinch: one fighter steps back, the referee waves them apart, and everyone in the arena realises the next round can finally start. For Karachi’s only integrated power utility – an asset that is too strategic to fail and too controversial to ignore – that alone is progress. n

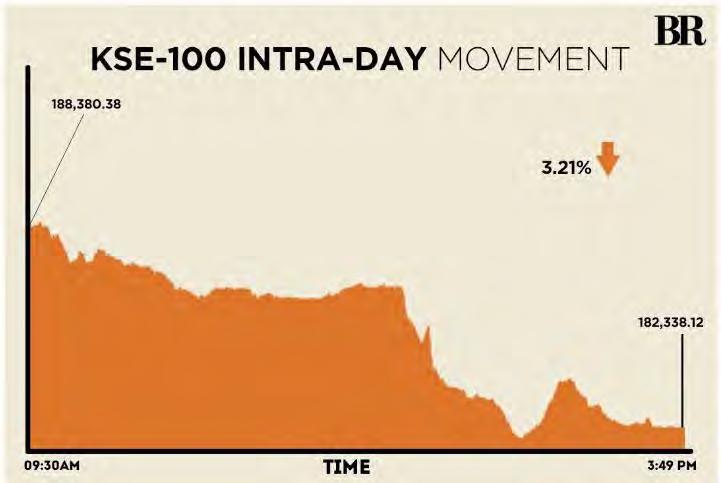

How the perfect storm hit the stock market and left it in the red

The crash on Thursday saw a drop of more than 6,000 points with one scrip being a stand out

By Zain Naeem

Astock market crash is nothing new or special. The Pakistan stock exchange has actually seen three full blown crises in a span of 10 years from 2000 to 2010. The volatility in the index is something that is to be expected from day to day. It is considered an integral part of the market anyway. However, what happened on the 29th of January 2026 stands out as it was a perfect storm of different events culminating together leading to the index plummeting by more than 6,000 points within a day. It seemed like it was an event waiting to happen and being shocking nonetheless. This is the story of how small events led to the catalyst that was the crash.

The beginning

The story actually begins nearly 3 years ago. It is June of 2023 and the index has been range bound for a long period of time. May 2017 had seen the index touch historic highs of 53,000 since which the market had been steadily falling. The case was not helped by the pandemic taking place which saw the index go as low as 28,500 points. In addition to the market falling, the market also experienced multiple market halts taking place. Market halts are a protective measure that has

been put into place in case the market increases or decreases very rapidly.

Market halts are used all over the world as a way to manage the systematic risks that the market is exposed to by halting trading and index movement for a period of 45 minutes. This acts as a cooling off period in which investors can assess the market before the market starts to trade again. Another benefit of this halt would be that National Clearing Company of Pakistan Limited (NCCPL) would have the opportunity to collect mark to market losses up to the trading halt rather than waiting to collect them at the end of the day.

As the world went into lock down, market halts were triggered at the PSX throughout 2020 at different intervals. As the world started to come out of the pandemic, the index was able to recover to 40,000 by the end of June 2023. The index had flatlined throughout most of this period and there was little chance that things were going to get better.

No one could have imagined that in a span of two and a half years, the index was going to go through a rally never seen before. By December of 2024, the index had broken through triple digits and by January of 2026, the index was touching the 190,000 threshold. In a space of less than 3 years, the index had grown almost 5 times. Such a meteoric rise was going to have consequences into the future. This was the first aspect of the crash as the index had grown to such a large size

that the fall was going to be of a great magnitude as well.

Before we delve deeper into the actual story, we need to understand the concept of market index.

The KSE 100 index is broadly defined as a basket of 100 stocks which are selected based on a criteria that has been set out by the Pakistan Stock Exchange. The index picks from the largest market capitalization companies in order to constitute the index itself. The index was made in 1991 and had a base value of 1,000 points. The index is market capitalization based which means that the weightage of different scrips changes as their market capitalization changes on a daily basis.

To illustrate this fact, consider an index which is composed of 100 companies which each have a share price of Rs 1. Based on this, the index would be Rs 100 at the start of the period. The weightage of each of these scrips is 1% and they have an equal bearing on the movement on the index. Now let us assume that Company A within the index sees its price increase from Rs 1 to Rs 100 while the rest remain at Rs 1. Now the index will be Rs 199 while Company A will have more than 50% of the weightage.

This shows how the movement in price of one scrip can skew the index in one direction or another based on its market capitalization.

Another change that had taken place during this time was that the circuit breakers of the

scrips had been increased over time. Back in 2020, these circuit breakers used to be 5% in either direction. What this meant was that a scrip could either increase or decrease by 5% of its value in a day. Once either of these circuits were hit, trading would stop. If a cap of 5% was hit, sellers could sell at this rate while buyers could not offer a higher price until the share opened the next day.

The stock exchange felt that they were slowly building resilience into the market and starting from 2020 to 2024, these circuit breakers were steadily increased from 5% to 10%. The purpose of circuit breakers is to build a cooling mechanism into the market by slowing down the increase or decrease being seen in a certain scrip. The exchange felt that measures being taken had strengthened the market from these shocks and that it had the ability to absorb any sudden shock that it might be exposed to.

What this increase did was that as all scrips could move 10% in either direction, essentially the index could increase or decrease by 10% of its value in a single day. This meant that the magnitude of the swing within a day was increased or doubled from where it stood in 2020 and in 2024. This was the second condition that played its part as the scrip could fall by almost 10% and take down the index. These two factors ended up playing the key role in the index crashing in the end.

Now that we are all caught up, let us dive in

The morning of the 29th January

When the market opened on the morning of the 29th, there was an apprehension in the air. The week leading up to the Thursday opening had seen volatility as the index had opened on 189,000 points on Monday morning. By the end of Wednesday, it closed out at 188,000 points. Even in the beginning of the trading session, the market saw an increase of 500 points touching the week high of 188,923, however, much of this optimism had disappeared by the middle of the session as the index had

been dragged down by over 1,700 points.

The crux of this pessimism was tied to the Federal Constitutional Court and its decision related to its decision in relation to the supertax imposed by the government. The super tax was a tax levied on additional income of companies and individuals under two separate sections. Section 4-B was imposed in 2015 and was levied in order to rehabilitate areas affected by terrorism. The section would be triggered in cases where income exceeded a specific threshold and was put in place as a one time measure, however, it continued for several years.

Section 4-C was put into place in 2022 and was called the additional super tax on high earning sectors. This was carried out to lead to revenue generation from sectors or companies which were earning large amounts of profits. The application of this section was going to be on large companies and sectors like banking, oil & gas, fertilizer and sugar. The stinging part of this section was that it applied higher rates compared to 4-B and created a slab system based on income and the nature of the business. This

was supposed to act in addition to Section 4-B in place already.

In order to appeal against the application of this section, many corporations went to the courts to strike down this section on the grounds that it was discriminatory, retrospective in application and amounted to double taxation. In response to these cases, the corporations were able to gain a small victory as the High Courts deemed this rationale to be justified and waived off the application.

Once the case reached the Federal Constitutional Courts (FCC), these judgements were seen as being judicial overreach and violated the separation of powers as only Parliament had the right to set tax policy. The FCC upheld the legality and constitutional validity of the Super Tax provisions.

The impact of this decision was that this resolved over 2,200 pending tax cases that had been filed at different courts related to the Super Tax provisions. The recovery that could now be made by the Federal Board of Revenue was going to end up collecting Rs 310 which had previously been tied up in litigation. The application was going to be carried out from 2023 and many of the listed companies would have to end up facing a higher tax bill for the coming years.

The negative sentiment in the market was being tied to this judgement as the investors were looking to book their profits while the companies looked to absorb this cost.

The sentiment was not helped by the escalation in rhetoric and tension between US and Iran. Ever since protests broke out in Iran, there was a tough stance that was being taken by the US. On the 22rd of January, Trump announced that an armada was heading towards Iran which renewed fears of a war between the two countries. With the clouds of war hanging over, there was a

tepid view in the market in response as well.

But it seemed that the worst was yet to come. Around 1: 20 PM, Fauji Fertilizer (FFC) announced their results for the year ended 2025 and it seemed that the bottom of the market had dropped out.

Since 2024, Fauji Fertilizer had been growing in terms of its own operations and its acquisitions. First Fauji Fertilizer Bin Qasim (FFBL) was merged with FFC bringing both companies under one single corporate entity. In addition to that, FFC also acquired a stake in Agritech which was another fertilizer company operating in the same industry. There was also an approval given to FFC to acquire FFBL power company limited which has been completed recently as well.

On the operational front as well, it was seen that FFC was able to post solid results when farm demand was weak and the market was oversupplied. Due to the country suffering from floods and irregular crop yields, the demand for fertilizer was suppressed. On the other hand, the market seems to be inundated as there is an oversupply of inventory.

This can be confirmed by declining fertilizer offtakes and sales volumes throughout 2025 as sales dropped significantly leading to higher inventory. Even in the face of such strong headwinds, the company was still able to increase sales for the nine-month period ending from Rs 224 billion posted last year to Rs 283 billion in the most recent year. Even though the company had a worse quarter from June to September, the results were still able to beat last year’s performance in terms of nine months performance.

It seemed like the annual results were going to post much better results than expected. The market expected that the profits of FFC were going to be high and it would end up giving a better payout in the form of dividend compared to its history. At the end of 2024, the dividend announced for the fourth quarter was Rs 21 when the company had earned Rs 45.5 in profits. The dividend for the whole year had been around Rs 36.5 for 2024.

Based on the trajectory of the results, there was an expectation that something similar would happen and a large dividend payout would be given. There were rumors that a bonus issue was being contemplated as well. The results came out and the company posted earnings per share of Rs 51.7 with a dividend of Rs 8.5 per share. The latest payout took total dividend for the year to Rs 37.

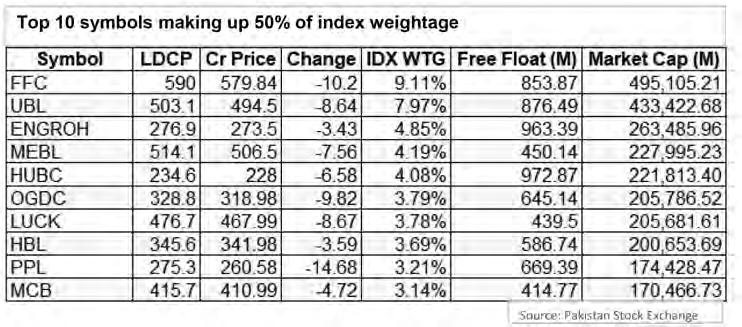

The results had been announced and the market was not happy. The share price started to fall and started to take the index down with it. In normal circumstances, it is difficult for one scrip to be able to drag down the index to a huge extent. At the end of September 2024, the scrip made up around 6% of the KSE 100 index. By January 2026, this weightage had increased to almost 9.4%. The two factors that had changed in the exchange came into play. The weightage of

Fauji had become almost a tenth of the index and the share price plummeted to its lower circuit breaker.

The effect of this? As the scrip started to tumble, it took down the index with it. At one point, the market was trading at -6,000 points out of which 1,900 index points were being contributed by Fauji Fertilizer alone.

Taken in isolation, this should not have weighed down the whole market, however, due to the size of Fauji in the index and the impact it was having in the market, the whole index started to suffer.

Spreading the chaos to the whole market can be attributed to the mutual funds who start to sell their shares. Mutual funds are mandated to look to maximise their returns based on the investment framework that they have been given. They have to walk the fine line of being able to earn a high return while minimizing risk and protecting the capital of their investors. In cases where scrips are not able to deliver on their results, the mutual funds have to react to the new reality and adapt to them accordingly.

The issue gets exacerbated due to the size of holdings that mutual funds are able to hold. This leads to a condition called the downward spiral. When a stock starts to fall in value, the investment committee of the fund sees that their expectations in relation to the stock have not been met and they start to shape their new expectations. This usually means that they start to offload the position they held in a particular stock as it has failed to meet their expectations.

The first step is to start selling their position while keeping within their investment mandate. This sale starts to go towards a downward spiral when these mutual funds expect that this could lead to a redemption of their units. As the mutual fund has missed to achieve their returns from a scrip, the investors demand to redeem their investment in the mutual fund. Forseeing this redemption stampede, mutual funds have to sell more than they want to in order to fulfil these

redemption demands.

Why do mutual funds have to sell? Funds are required to hold an ample amount of its assets in the form of cash in order to facilitate the redemptions to be carried out. If the funds are invested heavily in the market, they need to liquidate a greater part of their position to accommodate for the redemptions. This leads to a downward spiral where redemption induced fire sales or negative feedback loop leads to more selling and the stock falling more leading to more sales.

How does this become a contagion for the market? Once a scrip hits the lower circuit breaker, it cannot be sold anymore as buyers are not willing to buy it. In order to facilitate the redemption demands, the fund has to sell stocks of other companies who had nothing to do with Fauji and its results in the first place. As the market starts to tumble, more and more sales have to be carried out by mutual funds invested in the stock market.

The redemptions are triggered by the investors as they feel that they are willing to stop their bleeding and send in redemption requests for the day. The mutual funds are left scrambling as they are forced to fulfil the redemption requests on the day that they arrive. This starts the process of liquidation which has to be continued until the fund feels that they have ample liquidity to meet all their redemption needs. There can even be cases where these companies overcorrect and sell much more than they need in order to shore up additional funds in this case as well.

One way to mitigate such a fire sale would be to hold additional cash reserves in hand to meet any of these needs, however, cash yields no returns and funds usually feel it would be better to invest any additional funds in a market that is increasing. The investment portfolio data released by the NCCPL for the day shows that on 29th of January, mutual funds sold net share value of Rs 5.4 billion which confirms that the mutual funds started to sell their shares in response to the results. n

Zahra Niazi OPINION

Choosing Remittances Over Development?

In 2025, according to governmental data, around 32,000 highly-skilled and highly-qualified Pakistanis registered for employment abroad, equivalent to roughly six per cent of the country’s half a million annual graduates. This number, too, represents only a part of the exodus of Pakistan’s advanced human capital nurtured in the country and now being absorbed into foreign economies. It excludes thousands of other highly qualified and skilled emigrants who attain a job abroad after completing higher studies there, secure employment through private channels, or start businesses overseas.

Advanced human capital outflows from Pakistan have risen sharply in recent years, driven by an increasing convergence between domestic push factors and the rising global demand for talent. Between 2021 and 2025, the number of emigrants in the ‘highly-qualified’ and ‘highly-skilled’ categories registering for employment abroad was about a hundred per cent higher than during 2011 to 2015. By contrast, the combined total of highly-skilled and highly-qualified emigrants in the 2011-15 period was lower than in the corresponding period a decade earlier, reflecting a visible shift in trend over time.

Pakistan has long pursued labour migration as a state-supported policy, with its antecedents dating back to the 1970s, when the Middle Eastern oil boom prompted the government to establish policies and structures to streamline and incentivise migration. Within a decade, the number of annual emigrants increased more

The writer is a Research Associate at the Centre for Aerospace & Security Studies (CASS), Islamabad. She can be reached at: cass.thinkers@casstt. com

than thirtyfold, including predominantly the mid-skilled and unskilled segments of the labour force. While the choice to migrate, driven by economic necessities, may have come with difficult trade-offs for many migrants, for the government, the immediate outcome was a win-win, easing labour market pressures while generating a stream of foreign exchange inflows. From USD 0.14 billion in FY 1972-73, worker remittances rose to USD 1.4 billion by FY 1978-79.

With these attractive dividends, the policies in favour of streamlining migration adopted a self-sustaining character, continuing to improve in successive decades under different regimes. These policies went beyond just facilitating the migrants to also supporting their families back in their home countries, reflecting the extent of the government’s commitment to labour export. For instance, families of individuals who had emigrated on valid and protected work visas after 23 March 1979 through the governmental migration authorities or those voluntarily registered with the Overseas Pakistanis Foundation (OPF) are eligible for a wide range of benefits, from access to dedicated housing schemes to education scholarships for children.

For decades, this policy approach was presented as intended to facilitate the migration of lower-skilled workers as part of the state’s social contract with its citizens. Yet, even as the outflow of advanced human capital has increased, the state’s muted response to it indicates that dependency on remittances has taken precedence over concerns about brain drain. In other words, it reflects an economy increasingly choosing short-term capital relief over long-term growth.

If empirical findings are any guide, remittances and other contributions by highly skilled and qualified migrants, such as knowledge transfers or policy advising, cannot compensate for the losses resulting from their migration abroad. With brain drain, the economy loses not just the tax-funded investment spent on developing this human capital but also a future taxable base, a significant proportion of its innovation and entrepreneurial potential, and its long-term growth capacity. What’s more, remittances may also decline with an increase in migrants’ level of education, as a large proportion of such individuals tend to come from relatively wealthier households or are more likely to take their families along and settle abroad permanently.

However, even if one were to assume that these inflows are still large enough, remittances ought to be celebrated only insofar as they act as complements to development rather than as substitutes for economic reforms. In recent years, an increase in the number of Pakistani emigrants abroad, diversification of destination countries, government initiatives to reduce the

transaction costs of transferring money, and an increasingly transnational character of migrants have tilted the debate on remittances’ sustainability in favour of the optimists. In practice, too, these years have shown that remittances have become an increasingly dependable source of foreign exchange inflows for Pakistan. In FY 2025-26, these are expected to surpass the USD 40 billion mark, higher than even the country’s projected export value for the next fiscal year.

Yet, this dependability has also reinforced reliance on these inflows, placing the policy urgency for reforms to expand exports and investment on a back burner. The result is an economy

that remains markedly below its potential, lacking resilience to shocks. Closely connected, most remittances in Pakistan are consumed instead of being invested, promoting consumption-led growth, which is exposed to any external shock that exerts a downward pressure on the purchasing power of households.

An overhaul of the current economic model – transitioning from a stability-oriented to a growth-and-stability-oriented approach – is no longer a matter of choice but rather a matter of urgency. The longer it is relied upon, the more entrenched it risks becoming. In today’s globalised world, migratory outflows will continue, taking their natural course, and