MedIQ’s largest private AI investment in Pakistan’s health sector

Macter gaining market share, and diversifying into cosmetics

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

The formalized leverage market protecting from a contagion

The lessons from past crisis are providing the guard rails against future instability

By Zain Naeem

The recent stock market rally is eerily echoing the performances of the past. The fact that the market has increased more than three folds in less than 3 years is something to be marvelled at. The reasons behind the increase can long be debated and talked about. Whether it was the falling interest rates, the stable currency or the fact that the market had stayed undervalued for so long. The final conclusion could be that it was a mix of all these factors coming together.

The catch is that this is not the first time such a rally has been seen.

While the market reaches new highs, there is a sense of certainty and security that is seen in the market. The older players of the market feel that the crisis and market crashes of yesteryear have helped the system build guard rails for itself. With the help of National Clearing Company of Pakistan and Securities and Exchange Commission of Pakistan, there were many steps taken to protect from future catastrophes. One such measure was the establishment of the Margin Trading System (MTS).

In the wake of the 2005 stock market crisis, in house badla was seen as the major culprit for the crash taking place. So what exactly was in house badla and how did it wreak havoc? And more importantly, what was done to protect the market?

What happened in 2005?

To get a sense of what was going on in the market in 2005, we have to take a long walk down memory lane. After the US initiated its war on terror in 2001, there were many positive developments in Pakistan’s stock market. Economic indicators were on the up and up and the results were being seen on the Karachi stock exchange which was the primary stock market in the country. Foreign exchange reserves were increasing, interest rates were low, the banking sector was expanding rapidly, remittances were on the rise and the government was looking to privatize many of its state owned enterprises. Based on these developments, the investor sentiment was strong and optimistic and the stock market was the most attractive avenue for investment.

The bull run started in 2002 when the market rose from 1,500 points in 2002 to 10,300 points by March of 2005. This was an increase of almost seven folds. Comparing the market rise of today seems miniscule in comparison. In addition to the index increasing, the daily volumes were also touching all time highs. With the prices and volumes increasing, the market capitalization of many of the companies increased manifolds. The media was touting the market as the best performing stock exchange in Asia based on the increase.

As the index was increasing and returns were multiplying, the market was ripe for speculators to enter. With no end in sight of the bull run, there was an expectation that the music would never stop and the party could go on forever. This feedback loop was further reinforced by the fact that there was easy credit available for the speculators. This proved to be an upward spiral as speculation would fuel the market run which would further increase the speculation in the market as well.

The source of this easy credit was called in-house badla. This allowed investors to buy large amounts of shares based on borrowing at cheap rates from lenders. In-house badla was a market in which lenders were willing to lend funds to borrowers who could leverage their position by buying a large quantity of shares while investing a portion of this investment. The wisdom behind this buying was that, as the market would keep increasing, any profit earned by the trade would be more than enough to cover the cost of borrowing.

Another aspect which was fueled by this kind of borrowing was that lenders could move funds towards shares that they wanted to manipulate. For example, a lender would allow a borrower to borrow at a lower rate if the buying was going to be carried out in a stock of their interest. This allowed them to influence the price in their favour.

The biggest problem of this lending system was that it was informal and was maintained off the books. In many cases, the regulators and even the market participants had little to no knowledge in regards to the size of the leverage market. What this meant was that people would see the performance of the stock exchange and marvel at the increase rather than knowing that the exchange was becoming more and more fragile by the day.

With the system being supercharged by speculators and higher market prices, the fundamentals of the market started to lag

behind the valuations and a bubble was being created. With little in the way of oversight and regulation, the badla market kept growing in size with the influence of the market being monopolized by a chosen few. The reality was going to hit the market and hit it hard.

With market prices and badla volumes becoming unsustainable, the share prices started to fall and led to a cascading effect. The thing with leverage is that it works very well when the asset prices are increasing. The profits are being earned and they are more than enough to cover the costs. Even the collateral being used to take on a bigger position is also increasing in value in conjunction with the share price. The downside of leverage hits when the share prices start to fall.

And that is what happened in March of 2005 when the KSE-100 index crashed from 10,300 to below 7,700 points. When share prices start to fall in a leveraged market, the issues start to grow exponentially. The fall in price has to be covered by the investor while they still have to pay the cost of borrowing. As the collateral losses value, they have to put up more assets to cover their borrowing. As the losses start to accumulate, liquidation of the position has to be carried out at discounted rates which further depletes the value of the share and its collateral.

The upward spiral is followed by a more vicious and dangerous downward cycle as shares keep plummeting and there is no stop to where they will go. Soon the contagion starts to hit the lenders who had lent the funds in the first place as the lack of liquidity threatens their survival. With the lenders failing to make their payments, the domino effect takes the whole system down with itself as the default bleeds from one lender to the next.

Enter the devil

So how did in-house badla make things worse? As already stated, the fall in the market would be problematic in any situation. The problem that was posed by the badla market was that it was unofficial and off the books so there was no record as to how large the market had become. As there was no official way of documenting these transactions, the lenders could set the terms and change the terms as they wished.

As the market started to fall, the lenders started to fear for the money they had lent and started to call these loans back. This created

a panic in the market as borrowers could do little. They could not sell their holdings to free up the funds as the market was falling. This led to the market free falling. As lenders had kept some security and collateral against the borrowings, they started to sell these pledged shares as well in order to recover any value they could. All these factors combined to accelerate the crash further and further.

In the aftermath of the crisis, it was seen that many of the lenders or brokers ended up defaulting on their commitments. Others were able to use the rally to make large gains driving up prices and then exiting the market leaving the smaller investors to suffer huge losses.

SECP set up an inquiry commission under Justice Saleem Akhtar who submitted a report on the causes of the crisis. The commission stated that the in-house badla was the main reason as it turned the exchange into a casino which was run by the powerful brokers. And just like a casino, the brokerage houses always won. It also alleged that there was a conflict of interest between the brokers and the board of directors of the Karachi Stock Exchange as they controlled many of the seats of the directors as well.

Establishment of MTS

One of the solutions that was put forward by the commission was to establish a Margin Trading System (MTS) in place of the in-house badla. It is impossible for the stock market to function without leverage. In certain products like future markets, leverage is actually baked into the product. In face of this, it was felt that rather than having an informal system off the books, there was a need to have a more formalized manner to allow for leverage based trading to be carried out.

Leverage is helpful as it enhances market depth, liquidity and allows for greater investor participation to be carried out. Margin Trading allows an investor to buy securities by paying for a portion of his total investment and borrowing the rest from a financier. This financier can be a bank, a brokerage house or even a mutual fund which is allowed to lend to investors. The investor is able to enjoy a greater purchasing power leading to an increase in the activity in the market. The downside, however, is that there is added risk as the exposure of the investor is greater to any fall in the price.

The mechanics of the system are quite simple. An investor buys a security that is declared eligible by the NCCPL under the eligibility criteria that is set by them. This makes sure that investment is not being carried out in a stock which has weak fundamentals. The investor only has to put up the funds for 15% of the value of his purchase which means that they can multiply their holding by almost

Leverage is helpful as it enhances market depth, liquidity and allows for greater investor participation to be carried out. Margin Trading allows an investor to buy securities by paying for a portion of his total investment and borrowing the rest from a financier. This financier can be a bank, a brokerage house or even a mutual fund which is allowed to lend to investors. The investor is able to enjoy a greater purchasing power leading to an increase in the activity in the market

6 times their investment. The remainder is provided by the financier or the lender in this case. The upside for the lender is that they get to earn a mark up for the lending carried out.

In order to make sure that proper accounting of all the transactions is maintained, the NCCPL has developed a system through which the transactions are executed on a daily basis. Just like regular trading terminals, a terminal can be accessed by borrowers and lenders who are willing to borrow or lend respectively.

In order to make this system secure, only certain eligible securities are allowed to be traded on the system to make sure that the securities are of the highest quality and have a strong track record behind them. To control the size of the market, a cap of 20% of free float is kept which means that no more than 20% of the free float of a share can be traded cumulatively.

In order to protect the lenders and borrowers from any credit risk, cash margin requirements are maintained and adhered to by NCCPL which makes sure that any sudden rise or fall in the market price of the share is protected and these margins are adjusted accordingly to make sure there is ample collateral against the borrowing carried out. In case a share price falls, the borrower has to bring back the margins back to the required levels on a daily basis.

To not let the funding dry up, the lenders are mandated to provide the funds for a period of 60 days or two months. At an interval of every 15 days, 25% of his lending is released which means they can get back their lent funds in a timely manner. They can choose to lend these funds again if they choose so. The borrower is also protected as they have a period of 60 days before all of their funds are taken away from one lender. This allows them the flexibility and ability to use the funds for at least 15 days and then choose to borrow from a new lender if they are being given better terms.

In terms of regulations, the SECP has

also enacted rules such as the Securities (Leveraged Markets and Pledging) Rules, 2011 which cover margin trading systems and other aspects of securities lending and borrowing.

Same same but different

The fruits of the new measures can already be seen now. Just like in 2001, interest rates are declining, foreign reserves are stable, remittances are on the rise and there is another privatization drive being carried out. Just like the run up to 2005 crisis, the index has been increasing steadily on a monthly basis with no end in sight. However, the biggest difference is that there is no chance of a shock that can be carried out ala 2005.

The MTS system has been deployed in order to make sure the withdrawal of funds by one financier cannot jeopardize the whole leverage market system. The mechanisms that have been built make sure that there is ample liquidity in the system which cannot dry up in a matter of days. This sense of security makes sure that all market participants are sure that they will have easy access to funds on a consistent basis and there is trust that has been integrated.

The recent market rally seems to be going past new historical thresholds on a daily basis and there are expectations that the index could reach 200,000 points in the next few months. The stock market crashes of 2000, 2005 and 2008 have scared older investors who are skeptical of the way the index is increasing on a daily basis. Their skepticism is justified to the extent that the carnage they saw with their own eyes is difficult to forget. For them to fathom such an increase on the back of little change in the fundamentals of the economy can be rationalized to some extent. What they fail to realize, however, is that the guard rails that have been placed are designed to withstand the rigours of the new normal. n

Post-mortem report: ChemicalImperial Industries

Who is buying Lotte Chemicals?

The sale of Lotte marks the last vestiges of the Imperial Chemical Industries (ICI), and another multinational exit from Pakistan. But this one is a little different

By Abdullah Niazi

Among the many legacies left by the British in India was a vast tapestry of corporations that had set up shop in the subcontinent. In Pakistan, no single company represented the heights of colonial corporate ambitions more than Imperial Chemicals Industries (ICI).

For more than half a century after the partition of 1947, the ICI name dominated corporate circles in Pakistan. ICI attracted the best talent, set standards across industries, and their products from paints to plastics were highly sought after. But the past 20 years have seen the company go from one of the largest multinational conglomerates in the country to a bevy of smaller companies that have been bought and sold twice over. The brand name ICI has also all but finished, existing only as a small watermark on Dulux paint boxes.

Lotte Chemicals was once a small part of the Gargantua that was ICI. It was such a small part that it was only one division of ICI’s presence in Pakistan, which in itself was a small slice of the company’s global business empire. Over the past week, official confirmation came through that Lotte’s South Korean sponsors had sold a 75% stake in the company to a Dubai based joint venture between Montage Oil and AsiaPak Investments. Montage is a longtime oil broker in the UAE of Pakistani origin with liquid storage facilities in Sharjah, Karachi, Lahore, Ho Chi Minh City, and Qingdao. They also have dry storages in Vietnam and the UAE. While Montage has generally kept a low profile, AsiaPak is headed by Shaheryar Chishty, a former banker who has made a habit of pursuing orphan investments and has turned AsiPak into an investment vehicle with stakes in Thar Coal and the majority shares in K-Electric. He is also the owner of Daewoo Bus Service in Pakistan.

The deal went through for $69 million, or around Rs 17 per share of the publicly listed company. Lotte’s share price the day the deal was announced was Rs 27.75, which would indicate that the South Koreans are selling it at a discount. The negotiations for the deal have been going on since February, and the lowest share price for Lotte in the past year has been Rs 16.71 in May 2025. This is starkly different from the sale of

a different limb of ICI in 2012, when the Lucky Group bought a 75% stake in ICI Pakistan’s chemical business for $152 million at a premium of 29.7%. What makes this deal even more interesting is the fact that the Lucky Group had actually signed a share purchase agreement with Lotte back in 2023 to buy this same 75% stake in the plastics company for a significantly higher Rs 31.29 per share.

This indicates that Lotte South Korea wanted a quick exit from their plastics business in Pakistan. Given how the company had to shut its plant down twice in 2023 and the continuing difficulty of doing business in Pakistan for global players, the rush makes sense. What makes this ‘exit’ a little different, however, is that it is not a complete divestment. Lotte has dropped out of their main business but have kept some of the other businesses they had acquired in Pakistan in the past decade including a bottling company and Kolson Foods.

The only question that remains is what is left of ICI, and how do these separate entities plan on doing business in a country where it is becoming increasingly difficult for both domestic and international players.

The ICI story

The story of ICI is one of grand ambitions. Formed in 1926 as a result of the merger of four of Britain’s leading chemical companies, ICI launched in what is now Pakistan in 1944. It began by the name of the Khewra Soda Ash Company, which was a subsidiary of ICI in England.

Soda Ash was the precursor to several industrial chemicals. After 1947, ICI incorporated its Pakistan assets under Khewra Soda Ash Company Ltd, which was set up in 1952, and in 1966 the company was renamed ICI Pakistan. At least one ICI subsidiary has been listed on the Karachi Stock Exchange since July 1957.

The post-Nationalisation era under Bhutto was fraught with fears. Many Pakistani businesses shifted focus to trading as investors lost confidence to set up manufacturing facilities in the country. However, ICI continued to thrive with the backing of its international parent. Also, for those who grew up in the 80 and 90s especially, it will be remembered that ICI was the main source of human capital development. Alongside CitiBank, ICI was the em-

ployer of choice for educated Pakistanis. Asif Jooma, CEO of ICI, while addressing the Leaders at LUMS conference in 2018 stated, “ICI was a significant leader feeder for the economy and it continues to be. If you do a quick scan of the corporate landscape of Pakistan, you would invariably find people that have in some shape or form been associated with ICI during their careers.”

The company did so well during those years that back in 1995, its international parent, ICI PLC, made its largest ever overseas investment in Pakistan, to set up a manufacturing facility of Pure Terephthalic Acid (PTA) at Port Qasim.

This PTA plant at Port Qasim is where our story begins. By setting it up, ICI had entered three distinct but related segments in Pakistan. There was the original business of soda ash and chemicals, there was their paints business with ICI paints being the go to brand for Pakistanis, and finally there was now the PTA business at Port Qasim. PTA is one of the primary raw materials used in the production of polyethylene terephthalate, or PET resin. This resin is used in two ways: first, to make PET bottles, which are plastic bottles used for packaging various liquids such as water, carbonated drinks, juices, sauces and oils. Second, it is used to manufacture polyester fibres, which can be further processed to create polyester staple fibre, or PSF. PSF is used in

textiles, cushioning material, carpets, and non-woven fabrics.

With these three verticals aligned, ICI continued to dominate Pakistan’s corporate sector.

Then international winds of change turned the entire company around in Pakistan. In 2008, Dutch paints and chemicals giant AkzoNobel bought out the global parent company of ICI, and ICI Pakistan became part of the global AkzoNobel umbrella. When AkzoNobel came to Pakistan, they decided as part of a broader global strategy to focus on paints more than on the chemicals business. Akzo decided to split up the business.

In 2009, they sold the PTA business to Lotte Chemicals of South Korea. Lotte was a major player in plastic resin in South Korea and had made a name for itself in the industry after originally starting as a confectionary company in 1967. Over the next two years, Lotte invested $800 million into Pakistan as Foreign Direct Investment (FDI) and also installed a 40MW captive power plant for their facility.

In 2010, Akzo pursued a demerger, splitting ICI into two new companies. The paints division became AkzoNobel Pakistan and the remaining chemicals business became ICI Pakistan.

This new entity by the name of ICI Pakistan immediately went on the market for sale and was bought by the Yunus Brother Groups,

the group run by the Tabba family that owns Lucky Cement. The Lucky Group bought a 75% share in ICI Pakistan for $152 million at a premium of nearly 30%, showing how coveted the business was.

In this way, by 2012, ICI’s holdings in Pakistan had been split between three players. AkzoNobel retained the paint business. Lotte Chemicals was running the PTA business out of Port Qasim. The Tabbas were running ICI Pakistan’s chemicals business. The British conglomerate was now owned by a Dutch entity, a South Korean entity, and a domestic player.

In the past month, however, both the Dutch and the South Korean shareholders of what was once ICI have left and are being replaced by large, seasoned, domestic buyers. But that is exactly what they are — domestic players.

What happened to Lotte chemicals?

Afew weeks ago, Profit covered the rise and fall of AkzoNobel in Pakistan, and gave some piece of advice to Syed Babar Ali: do not buy AkzoNovel paints. The company did not fare well in Pakistan, and over time a darker side of the paints business emerged that a multinational company found it difficult to operate in.

For Lotte Chemicals, the story is a little

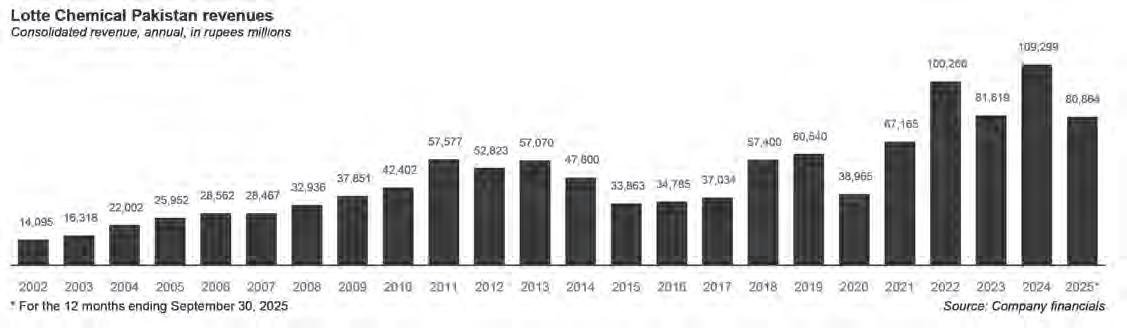

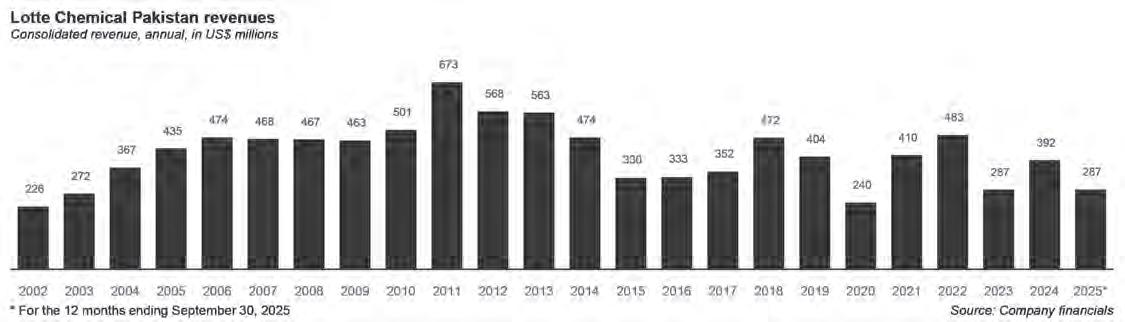

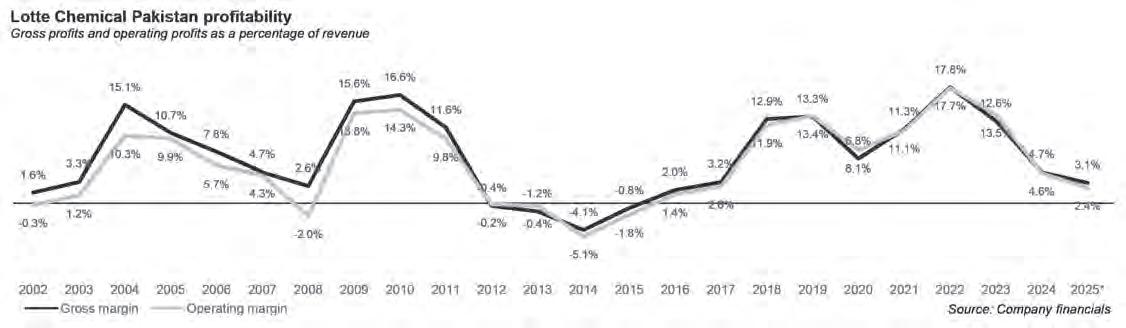

different. Unlike AkzoNobel, which was operating in a field of many local competitors, Lotte was the sole domestic producer of PTA in Pakistan. The plant at Port Qasim has the capacity to produce 520,000 tonnes of PTA annually. Which is just as well, as Pakistan’s total demand for PTA stands at roughly 700,000 tons annually. The remaining 200,000 tons of PTA is imported. That means Lotte Chemical’s market share domestically is 100%, while its overall market share stands at around 70%.

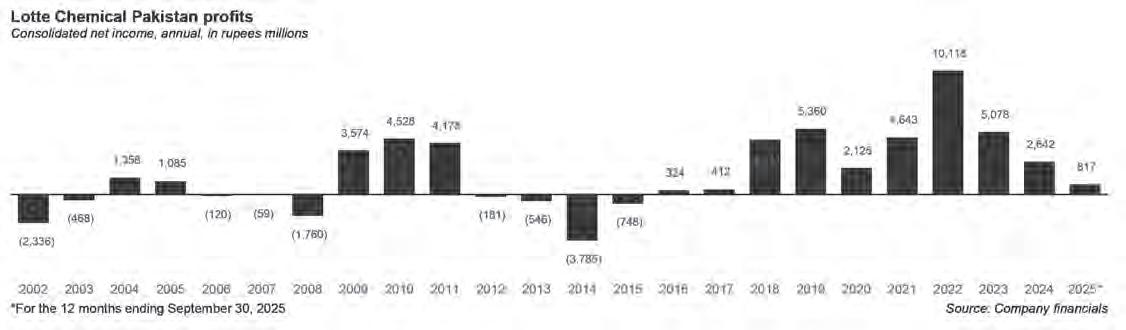

As expected of a sole producer, Lotte Chemicals’s revenues have generally increased. The only times revenue declined were during the period 2014-2015 and in 2020, due to Covid-19.

In 2014, a 16% drop in revenues occurred, mainly due to lower PTA prices. The reduced PTA margin against PX, higher energy costs, coupled with inventory losses due a drop in price of PTA at year-end, led to a decreased overall profit margin. Moreover, the company had to bore outward freight charges as export sales increased, resulting in increased distribution and selling expenses. Consequently, the company’s net loss doubled to Rs 1,100 million as compared to Rs 498 million in the previous year.

The year 2015 again brought challenging conditions for the local polyester industry due to increased taxation, higher energy costs, and reduced textile exports. This strained PSF producers who were facing tough price competition from inexpensive imports, particularly from China. Moreover, the PET industry saw reduced demand due to bottle industries adopting cost-cutting measures with lighter bottles. All of this culminated into a 3% decrease in sales volume for Lotte Chemicals, as compared to 2014.

However, at the end of 2015, the domestic PSF industry successfully levied duties on Chinese PSF producers, which contributed to Lotte Chemicals’ turnaround in 2016. That year, the anti-dumping duties and better boosted Pakistan’s domestic polyester industry. Consequently, there was a notable 15% surge in PTA demand, leading Lotte Chemicals to attain an unprecedented domestic sales

record of 492,192 tonnes.

Over the next few years, Lotte Chemicals witnessed a steady rise in revenue, barring a substantial 36% decline in 2020 attributed to global lockdowns that affected PTA demand. Consequently, the company underwent a 54day plant shutdown, causing a 14% reduction in production and a 12% decrease in sales volumes. The gross profit margin tumbled to 6.8%, while the net profit margin plummeted to around 5% in 2020.

However, the gloom was fleeting as 2021 heralded resurgence for Lotte Chemicals, fueled by heightened demand and improved prices. That resulted in a remarkable 72% surge in revenue, and an impressive 11% gross profit margin in 2021.

Despite the improvement in revenues and margins noted in the 2022 annual report for Lotte Chemicals, heightened inflation significantly impacted consumer behavior. This resulted in a decrease in consumer spending, with individuals prioritizing essential goods over luxury items such as textiles. Consequently, domestic demand for PTA in 2022 declined by 6% compared to the previous year.

And then 2023 happened. The textile industry was hit by the double setbacks of dwindling exports and operational setbacks. The initial nine months of the year witnessed a stark decline in textile exports compared to the previous year. This downturn forced several companies to either temporarily shut down or scale back their operations. Notably, textile industry entities like Shahzad Textile Mills Limited and Elahi Cotton Mills Limited announced temporary closures in October alone, mirroring the industry’s distress.

Lotte Chemicals had to suspend plant operations for the second time in nearly seven months, due to declining demand in the downstream industry.

Just like the textile industry, demand within the PET industry has also declined. According to a PACRA rating report of Pakistan Synthetics Limited (a player in the PET industry), the tough economic environment has reduced the purchasing power of the con-

sumer and had a negative impact on the food and beverage segment.

This was not a Lotte specific problem. The economic conditions of the time meant the chemicals industry as a whole was struggling. Other chemical companies were also grappling with plant shutdowns in 2023. Take for example Sitara Peroxide Limited (Sitara Peroxide), which also suspended plant operations twice in 2023. Lotte was sitting in the same boat as all these other companies, the economic storm was threatening to envelop all of them.

The dream of ICI as it once was?

Lotte wanted out. There was a lot going on at the time for the company globally as well. According to one industry insider at Lotte, the South Korean company was facing a massive challenge from China, which had invested heavily in the PTA industry and was crushing the South Koreans by cutting costs.

At the time, Lotte decided it was going to divest from its PTA business in Pakistan. This was not to be a complete exit. According to one industry source, Lotte only wanted to get out of the plastics business and retain its bottling business which they bought around 2017 called Riaz Bottlers. They were also not going to sell Kollson Foods which they had purchased around the same time.

Almost immediately, interest was shown by three different players to buy Lotte Chemicals. The first company was Gatson Novatex. It made sense for Gatson to buy it because they have been Lotte’s biggest customers. Novtex buys nearly a third of Lotte’s resin and turns it into plastic products. On top of this, Lotte already had a 9% stake in Novatex. The second contender was a joint venture between Montage Commodities and AsiaPak. This JV has now struck a deal with them, but there was another contender: the Tabba Group.

“There was a sense of nostalgia around this sale,” says one person close to the original deal. “The Lucky Group had bought ICI Pakistan, the chemicals business, from AkzoNobel in 2012 at a premium. Back then as well the Tabba family had this feeling that owning the

ICI was a big achievement and that is why they paid so much for it. Now, if they were able to acquire the PTA business as well, they would be consolidating and rejoining two broken parts of what was once the mighty ICI” they explain.

The Lucky Group made an offer at an estimated price of Rs31.29 per share, translating into a total transaction volume of Rs35.5 billion. This was going to be a very good deal and once again Lucky would be paying a premium. The deal was approved happily by the South Koreans and work began on finalising the agreement between the two entities.

But then came a snag. This agreement was made in January 2022. At the time, Lotte Chemicals had not been struggling particularly, but because of international pressures from China they were looking to divest from Pakistan and shore up their cash reserves as well as avoid any liabilities in a market that isn’t always stable. But during 2023 came both plant shut downs and the downturn that we mentioned earlier. Not only this, but costs were rising as well. An increase of gas prices by Sui Southern further hurt the abilities of Lotte to be profitable. Lucky wanted to negotiate the price down. At the time, according to sources, Lotte was willing to play ball but it seemed the price being quoted was too low. Lotte also backed down and the deal fell through.

Enter the JV

One can only imagine what would have happened if the sale had gone through and Lucky had bought Lotte by the start of 2024. The deal, as Profit has been told, finally fell through in January 2024 a year after it had been made. Earlier this year, AkzoNobel announced it was selling and the Packages Group had expressed interest in acquiring it. Had the Lucky Group managed to buy Lotte, one imagines they would have been top bidders for AkzoNobel paints as well, an acquisition that would have reunified the old ICI.

But it did not take long for the deal to

fall through before the joint venture between Montage and AsiaPak stepped up to the plate. In November 2024, they began negotiations to acquire Lotte Chemicals. In the past couple of years, Lotte Chemicals has seen a bit of a reversal in their financial fortunes. The company has remained financially profitable, and the difficult period of 2022-23 also saw a small revival in 2024, as indicated in the graphs that are in this story.

By February 2025, the negotiations were almost finalised. By July 2025, Montage and AsiaPak joined hands to create PTA Global Holdings Limited — a Dubai based company that would buy Lotte Chemical’s stake. The price quoted for the 75% acquisition was $69 million, which equates to a share price of around Rs 17. The deal is a steal for PTA Global which now owns what is the only PTA manufacturer in Pakistan. But what do they plan on doing with this company?

In conversation with Profit, Shaheryar Chishty said the sale came because of typical Pakistani problems. “In the 2022-23 economic crisis, everyone was having problems with working capital and with LCs. This put a dent in cash flows and the international situation was such that the opportunity presented itself to us.”

“Lotte Chemicals actually used to be a client of mine when I was a banker. I approached them again and we began negotiations,” he explains. Chishty has experience working in South Korea in the past as well, and also bought Daewoo Bus Service from South Koreans who used to be his clients. Over the years, he has made a habit of acquiring what he calls orphans assets and turning them around. “What we need to keep in mind is that this is not an ‘exit’ from Pakistan like we’ve seen with other multinationals. Lotte had other business interests in Pakistan including bottling and foods which they have not sold.”

Chishty, of course, would know a thing or two about how difficult it is to do business in Pakistan. Back in 2022, he used AsiaPak Investments to buy a majority share in K-Electric. Despite what is a clear majority, resistance

from different quarters and languishing legal battles have meant his company has not been given control of KE, a frustrating situation for all involved, including the people of Karachi who continue to suffer the from the board room battles because of the lack of direction and initiative in the company’s existing management.

In Lotte Chemicals they have found a company that is publicly owned, has a massive market advantage in that they are the only player, and there are avenues for profitability. For Chishty, the goal is once again the synergies he can find with his other investments. When he bought KE the idea was to synergise it with Thar Coal, where he has investments. With Lotte as well, he wants to eventually go in a direction that brings Thar Coal into the picture. “I do believe Thar Coal has the answers for so many of Pakistan’s problems, and I want to explore the potential of coal to chemicals now that we are involved in this business as well.”

The sale of Lotte Chemicals marks a bittersweet moment for Pakistan. On the one hand, it means that what was once ICI, a grand old imperial company, is now entirely in the hands of Pakistanis. But not only has it taken time to get here, it has involved exits and divisions.

There are two words in Urdu that can be used to describe the act of division. The first is taqseem. Of Arabic origin, it is a politer word that indicates a fair distribution of some sort. The other word is of Hindi origin: Batwara. It denotes something far more visceral. It is a violent sundering of something whole, a selfish decimation.

It is perhaps why Pakistani histories of the partition refer to the events as Taqseeme-Hind, and the language used by the Indian National Congress at the time of partition referred to Jinnah’s plan as Hindustan ka Batwara. It is also why the word batwara continues to be used in a negative connotation in discussions of inheritance.

The sale of Lotte Chemicals raises a similar question: was this taqseem or the dreaded batwara? n

Millions on the line: inside startup MedIQ’s largest private AI investment in Pakistan’s health sector

By Taimoor Hassan

MedIQ, one of Pakistan’s recognized digital health platforms, has now positioned itself at the forefront of the country’s artificial intelligence revolution. With a multi-million-dollar investment into in-house AI development, the company is transforming its operations from traditional telemedicine into a data-driven healthcare system provider.

This move doesn’t just represents technological advancement, it marks a strategic shift toward building one of Pakistan’s first large-scale, healthcare-specific AI infrastructure, trained on local medical realities.

The company’s new AI engine automates the entire clinical workflow. From multilingual pre-consultation triage to real-time medical note taking during appointments and even post-consultation patient management, MedIQ’s system guides patients as well as practitioners through every step of their healthcare journey.

For hospitals, the impact is immediate: time spent on documentation drops and patient throughput increases. For Pakistan’s overburdened healthcare system where clinicians often see dozens of patients per shift, AI-driven efficiency is not just convenient, it’s essential to ease that burden.

What sets MedIQ apart is its commitment to building its AI locally rather than

relying on foreign models, which is trained on millions of Pakistani patient records and tested widely before full scale deployment. Backed by strong investor confidence and fresh profitability in the Saudi market, MedIQ’s strategic bet on AI positions it as one of the most ambitious players in Pakistan’s digital health ecosystem. Its investment in AI also puts MedIQ ahead of the competition: where others like OlaDoc and Sehat Kahani are taking it slow and sticking to teleconsultations and appointment bookings, MedIQ is moving fast, expanding in other markets, achieving profitability, testing new bets and driving innovation. In short, MedIQ is behaving like an innovative tech-first startup.

AI in Pakistan’s healthcare

Artificial intelligence is moving beyond the stage of hype and beginning to establish itself as a practical force in Pakistan’s healthcare system. Hospitals are gradually adopting AI driven technologies while telehealth services continue to expand their reach. Patients are already noticing tangible improvements in areas such as faster diagnostics, smoother procedures and more responsive care. Still, the technology is not a cure all. The human connection, empathy and clinical judgment that define medical practice remain irreplaceable. Recent collaborations between private innovators and government health programmes highlight both

the opportunities this shift can unlock and the caution that must guide its adoption.

In Pakistan’s urban hospitals and research centers, artificial intelligence has already begun to reshape the way diagnoses are made. Radiology departments that employ algorithms to scan X rays, CT images and MRIs are able to identify potential illnesses earlier than traditional methods allowed. This not only accelerates the diagnostic process but also eases the anxiety patients often feel while waiting for results.

The reach of AI expanded further during the COVID-19 pandemic, when telemedicine became a lifeline for many. Digital platforms equipped with AI powered chatbots and virtual triage systems provided guidance for patients who could not easily travel to major cities. These tools helped reduce delays, clarified referrals, and ensured more consistent follow up. Patients who used such services frequently reported greater satisfaction with their care, citing smoother access and clearer communication.

Evidence of this improvement has also been documented. A study published in the Journal of the Pakistan Medical Association concluded that AI and machine learning systems significantly reduced waiting times in large hospitals, which in turn strengthened patient trust. According to the findings, the simple act of shortening delays improved perceptions of quality and confidence in healthcare providers.

Professor Dr Asghar Naqi, principal

of Allama Iqbal Medical College and Jinnah Hospital in Lahore has expressed cautious optimism about the role of artificial intelligence in healthcare. He notes that medical imaging supported by AI algorithms can analyze X rays, MRIs and CT scans to detect abnormalities such as tumors, fractures or cardiovascular problems with greater accuracy and efficiency than traditional methods. According to him, this ability allows for earlier diagnosis and treatment, potentially saving lives. At the same time, he warns that these systems cannot replace human judgement, since every algorithm is ultimately built on human experience and clinical insight.

In Karachi, Dr Saleem Sayani, Director of the Technology Innovation Support Centre at Aga Khan University, has described AI as a transformative force for healthcare delivery. He highlights that these tools do more than assist in diagnostics as they also help process large volumes of medical data, strengthen predictive analytics and make treatment plans more personalized. Yet Dr Sayani emphasizes that ethical, legal and social considerations are critical. Without strong regulations and oversight, he cautions the speed of adoption could outpace the safeguards needed to protect patients.

Dr Imtiaz Ahmed, a specialist in microbiology and genetics has also spoken about the promise of AI in areas where medical staff are scarce. He argues that AI enabled diagnostic centers could play an important role in meeting growing healthcare demands in underserved regions. However, he acknowledges that technology alone is not enough. Persistent gaps in infrastructure, weak regulation and patient concerns about data privacy remain serious challenges that must be addressed if AI is to deliver its full benefits.

MedIQ sees the opportunity here: AI is essential and inevitable. It has taken the first leap into this, making a significant investment into creating and deploying AI solutions for Pakistan’s healthcare. Though MedIQ is not the only one eyeing AI in healthcare. Pakistan’s healthcare sector has foreign interest from California-based MindHYVE.ai which has committed to invest $22.5 million in Pakistan. MedIQ is ahead of the curve though, having made the investment already, testing and learning ahead of others.

MedIQ’s multi million dollar investment in AI

In most clinics and hospitals, the workflows are broken. Physicians spend a large portion of their time writing notes, updating electronic medical records and rewriting queries for insurers. Hospitals lose productivity. Patients lose quality time. Everyone pays more.

MedIQ’s AI platform addresses this with

a simple mechanism: the moment a consultation starts, the system captures the entire conversation, converts it into a structured SOAP (Subjective, Objective, Assessment and Plan) note [SOAP is the standardized method of documenting patient care], generates the prescription, and files it into the medical record all before the doctor even stands up. No backlogs created and no putting in after-hours to complete documentation.

Over the last two years, MedIQ has spent millions of dollars developing and deploying this AI system. Dr Saira gave us a range of between $3-5 million spent on developing this system. The company had raised $6 million earlier in May this year.

The results according to MedIQ are striking: up to 60% reduction in consultation time, up to 60% increase in daily patient throughput, near-elimination of manual data-entry, all resulting in higher revenue per doctor.

Solving for hospitals and patients

For hospitals operating on thin margins, MedIQ’s AI model can transform their financial performance. Publicly available financials of Shifa International Hospitals show that the renowned healthcare facility ended the year 2025 at Rs27.9 billion revenue and Rs2.3 billion in net profit, translating into a net profit margin of 8%. 2024 was even lower than that with revenue at Rs23.5 billion and net profit at Rs1.36 billion, translating into a net profit margin of 5.7%. MedIQ’s pitch is that its AI model will have a financial impact, pushing the net margins up significantly.

To understand MedIQ’s pitch, say if Shifa healthcare had incorporated MedIQ’s AI into their operations in 2025, its doctors would have completed consultations in shorter durations resulting in a higher patient throughput in a day. How? Before consultation starts, doctors would have access to basic diagnosis already during preconsultation through AI. When the consultation starts, AI literally records the conversation, transcribing it in real time, creating notes for the doctor which he would otherwise have to write and type and even create a prescription. The doctor would only have to review for accuracy. By reducing or eliminating the time spent on partly clerical tasks, doctors can move on to the next patient quickly.

Theoretically, Shifa doctors could have given consultation to more than double the number of patients in a day. This would translate into more than double revenue for the hospital per year and about double or more net profit after subtracting the cost of MedIQ’s AI service.

The potential here is massive: there were over 1,700 public hospitals in Pakistan in 2022 according to Public Health Financing report published by the Government of Pakistan. There are anywhere between 500 to 724 private hospitals in the country. Collectively, these hospitals possibly treat millions of people each year for various diseases. For its AI business, MedIQ has a big addressable market, not penetrated by a significant AI player. Because it affects a critical sector and Pakistan has a huge healthcare problem, at scale, MedIQ’s AI would have a massive impact in terms of decreasing the burden on the healthcare system while maintaining quality healthcare.

On the patient side, the product claims to address two chronic inefficiencies: misreferrals and wasted consultations. A multilingual AI assistant available in Urdu, Punjabi, Pashto, and Arabic conducts a complete pre-consultation history even before the patient arrives. Symptoms such as chest pain are analyzed and triaged correctly. Does the patient need a cardiologist, a gastroenterologist or a general practitioner, the AI decides that after collecting the symptoms of the patient. It then makes a referral for the nearest and best doctor available for in person check up or suggests on the app for a teleconsultation.

By routing patients correctly, the system claims to eliminate unnecessary specialist visits and cuts down diagnostic delays saving patients money and reducing hospital congestion. For providers, it means patients arrive pre-documented, allowing doctors to move directly into clinical decision-making, even having the prescriptions written and ready.

Traditionally, once the patient leaves the room, the hospital’s engagement ends. MedIQ says it reversed that. A virtual assistant takes over post-consultation, clarifying the complex medical terminologies on the prescriptions. The increase in retention as a consequence improves a hospital’s or a clinic’s bottom line and gives better healthcare for patients. Hospitals and clinics focusing more on value-based care models especially benefit here.

This all works only if AI is highly reliable. How well trained is the AI and how good and reliable the data is. Dr Saira says that she has done her work thoroughly on this end, having trained the model in-house using their own repository of data of 4 million medical records for two years.

“The model was tested on 1 million patients before commercial launch. Once the accuracy was about 97%, then we launched it commercially,” Dr Saira says.

While Dr Saira didn’t disclose how unit economics exactly worked for her AI model, she said that the revenue potential was significantly higher than the cost associated with providing it. n

Macter gaining market share, and diversifying into cosmetics

The biopharmaceutical manufacturer saw revenue growth faster than industry average, and also plans to launch a GLP 1 product

Macter International Ltd has emerged from the latest results season with a clear message for investors: momentum is back in branded generics, new biologics are scaling, and a bet on consumer beauty is moving from trial to traction. Management says the company is growing faster than the market, based on data from the healthcare data company IQVIA, aided by policy tailwinds from the deregulation of non essential drug prices and supported by a pipeline that now includes semaglutide in multiple delivery formats and a pending application for tirzepatide.

Macter closed FY25 with net sales of Rs9.9 billion, up 32% year on year from Rs7.5 billion in FY24, as mix shifted towards higher margin prescription brands and recently launched products. Gross margin widened from 42% to 45%, lifting gross profit 40% to Rs4.5 billion. Operating profit increased 76% to Rs1.2 billion, reflecting both the gross margin recovery and operating leverage, while profit after tax rose 73% to Rs738 million.

The first quarter of FY26 extended the trend. 1QFY26 net sales reached Rs2.8 billion, up 28% year on year; profit after tax rose 68%

to Rs156 million, indicating pricing and product mix remained supportive even as selling and distribution costs rose with brand investment.

Management attributes the outperformance partly to share gains evident in IQVIA data, noting that Macter has been growing revenue at roughly 1.5–1.7x the industry’s pace.

Biologics contributed meaningfully to that acceleration. The company highlighted that it is one of two domestic players offering semaglutide in both pre filled syringe and pre filled multi dose pen formats; overall, only four companies have semaglutide in injectable form in Pakistan. The current leaders in the GLP 1 segment are Novo Nordisk and Ferozsons, with Macter and Getz holding the second largest shares – an early sign that local manufacturing capability can translate into commercial relevance as prescriptions ramp. The briefing also notes an application filed with the Drug Regulatory Authority of Pakistan (DRAP) to launch tirzepatide, a next generation GLP 1/GIP.

A separate disclosure to the Pakistan Stock Exchange this month confirmed that Macter is now the only company in the country offering semaglutide in all three biotechnology dosage formats: vials, pre filled syringes and pre filled pens – an expansion of presentations that

should support both physician preference and patient adherence.

From a balance of effort standpoint, the FY25 P&L shows higher brand investment – selling and distribution costs rose 30% to Rs2.6 billion, and administrative expenses increased 28% to Rs646 million – but the gross margin gain more than offset this.

Macter’s numbers are unfolding against a changed domestic policy backdrop. In February 2024, the federal cabinet approved proposals to deregulate prices of medicines outside the National List of Essential Medicines, with amendments to the Drug Pricing Policy 2018. The change, announced by the caretaker government, effectively moved non essential medicines to a more market based regime while leaving essential drugs under oversight – an adjustment designed to address shortages and align incentives for local manufacturing and imports.

Subsequently, policymakers signalled further reforms to shift price setting for essential medicines away from DRAP to a new federal body, while DRAP would continue its broader regulatory mandate. Reporting at the time underscored that DRAP currently regulates prices for around 500 essential medicines, and that deregulating non essentials had already improved

availability by encouraging manufacturers to reintroduce previously uneconomic products. The net effect has been to reduce bottlenecks and revive competition, a dynamic visible in company level results across listed pharma.

Against this policy backdrop, companies capable of rapid formulation work, compliant scale up and multi format delivery – particularly in complex categories such as biologics – have been quickest to translate policy space into market share. Macter’s multi form semaglutide roll out is emblematic of that advantage.

Founded in 1992, Macter today operates as a branded generics manufacturer with a large contract manufacturing business. It operates across two main segments – branded generics and contract manufacturing – and as one of the larger contract manufacturers in Pakistan, particularly for multinationals.

Operationally, Macter is already selling into around 15 countries and is targeting an expansion to 30 by the end of FY27 – an export ambition that sits comfortably with the firm’s biologics push, especially if intellectual property windows for flagship GLP 1s open in select markets.

Capacity for physical expansion is also in place: management told investors it owns 16 acres in Gadap, a land bank intended to support the next five year growth phase without the friction of site acquisition.

Macter’s product architecture spans oral solids and liquids, parenterals (injectables), topicals, metered dose inhalers, and ear and eye drops – with dedicated facilities for cephalosporins, penicillins and biologics to ensure segregation and compliance. The company says it adheres to international cGMP standards and maintains ISO certified quality systems, while serving “blue chip” multinational clients on the contract manufacturing side. This breadth – in dosage forms and regulatory compliance – has historically been one of Macter’s competitive moats.

The most visible recent addition is GLP 1 therapy. In early November, Macter disclosed to PSX that it has launched semaglutide in pre filled syringe and pre filled multi dose pen presentations, adding to existing vial supply and making it the only firm nationally with all three biotechnology formats on offer. This matters clinically and commercially: physicians often tailor GLP 1 delivery to the patient, and wider presentation choice can support adherence, reduce switching, and deepen brand penetration across diabetology and metabolic indications. In company commentary, management also set out the local competitive map: in injectable semaglutide, Novo Nordisk and Ferozsons currently lead, while Macter and Getz comprise the second tier by share. The group expects substantial revenue growth from semaglutide as prescribing widens – mirroring global uptake

trends – and indicated that once global patents expire, exports could follow. In parallel, Macter has applied to DRAP to launch tirzepatide, pointing to a pipeline approach rather than a single asset bet in GLP 1s.

Outside biologics, Macter remains active in its traditional strongholds – anti infectives (with segregated beta lactam capacity), cardiovascular, and gastroenterology – while using its manufacturing infrastructure to serve multinational clients under tolling and contract arrangements. That dual engine – brands plus contracts – provides a measure of resilience as cycles shift between public tenders, private prescription demand and export windows.

The policy reset described earlier is relevant here. With non essential drugs deregulated, branded generics can better recover input cost shocks (APIs, packaging, energy), allowing firms with compliant capacity and strong field forces to lean into launches rather than ration supply. Macter’s 45% gross margin in FY25, up three points year on year, suggests the company has benefited from that alignment.

While the earnings story is still anchored in pharmaceuticals, Macter is diversifying into cosmetics via its subsidiary Misbah Cosmetics (Pvt) Ltd (MCPL) – a consumer facing arm that initially relied on imports but is now switching to local manufacturing. The company says it has leveraged its pharma experience – notably in chemical handling, quality systems and regulated production workflows – to raise standards in the cosmetics line up. As a result, MCPL’s gross margins are improving, and management expects the segment to contribute to the bottom line in the current year.

The subsidiary was formed in 2017 and is focused on halal certified cosmetics – consistent with how the brand positions itself in the market. The report also frames the move as a deliberate push into higher margin consumer products, complementary to the company’s pharmaceutical base.

Crucially, Macter can tap real world customer insight through the Depilex ecosystem founded by Masarrat Misbah, whose beauty brands are associated with MCPL. The Depilex network of over 80 salons nationwide is being used to test products, develop new SKUs and gather consumer feedback – a field laboratory of sorts that is rare in Pakistan’s still nascent beauty manufacturing landscape. This linkage shortens iteration cycles and reduces misfires in shade, texture and packaging decisions that often confound local cosmetics launches.

Market facing brand properties under the Misbah umbrella include Masarrat Misbah Makeup, a halal certified cosmetics line that has built distribution both online and offline. Public facing company and brand pages emphasise a focus on ingredient stewardship and accessibility – positioning that sits naturally with a parent

steeped in cGMP process discipline. At a strategic level, cosmetics offers a currency light growth vector relative to biologics. Where APIs and cold chain add volatility for therapeutics, localised sourcing and fill finish for colour and skincare can be managed with shorter lead times, in country packaging and domestic brand building. For Macter, co locating quality control, regulatory know how and pilot scale production under one corporate roof can reduce execution risk. The company’s disclosure that MCPL began as import based but is now moving into local manufacture suggests that learning curve is already being climbed.

Three threads define Macter’s next act. First, the core pharma engine is running hotter than the industry, by management’s own IQVIA benchmarked reckoning. That advantage is visible in the FY25 and 1QFY26 prints, where the combination of price normalisation, mix and new launches pushed both top line and margins higher. The company also says it is already present in around 15 export markets, with a plan to extend to 30 by FY27 – a goal that, if achieved, would diversify currency exposure and product risk.

Second, biologics – specifically GLP 1s – offer an avenue for step change growth. Being the only domestic manufacturer with vial, pre filled syringe and pre filled pen formats in semaglutide allows Macter to compete across prescriber preferences and patient segments. A tirzepatide launch, if cleared by DRAP, would enlarge that beachhead. Over a multi year horizon, management believes patent expiries could also open export optionality for these molecules.

Third, the consumer pivot via Misbah Cosmetics could smooth earnings by adding a portfolio with different cycles and cash conversion dynamics. The company is explicit that MCPL’s margins are improving as local manufacturing replaces imports, and that access to the Depilex salon network provides a ready test and learn platform – advantages that many new to manufacturing beauty entrants lack.

If there is a caution, it is the same one facing the broader sector: the policy transition must continue to balance affordability with the economics necessary to sustain local production, especially as energy prices and imported input costs fluctuate. Government reporting to date indicates that availability of non essential medicines has improved since deregulation, and that reforms around essential drug pricing are being considered to streamline governance; stable, predictable implementation will be the key variable for capital allocation decisions across the industry.

For now, the numbers – and the pipeline – tilt in Macter’s favour. Faster than market growth, a full suite of semaglutide presentations, and a cosmetics arm edging into profitability give the company a set of diversified growth

RETAIL SLOWDOWN STILL A DRAG ON IMAGE’S GROWTH PROSPECTS

The Pakistani consumer continues to struggle in the aftermath of the bout of high inflation from 2022 through 2025

Image Pakistan Ltd (PSX: IMAGE) is selling more clothes, but not fast enough to outrun the scars of Pakistan’s inflation shock.

The listed clothing and fabric manufacturer reported another year of double-digit revenue growth in FY25. Yet in an economy where consumer prices surged at rates north of 20% in 2022 and 2023 and remained elevated in 2024, its top line is rising more slowly than the general price level, suggesting that real volumes and basket sizes are still under pressure.

Management is responding with a familiar retail playbook: opening more stores, leaning on e-commerce and pushing into lifestyle and perfumes. Whether that will be enough to offset a cautious middle-class shopper base remains the key question for investors.

For the year ended June 2025, Image’s consolidated net sales rose 16% to Rs4.6 billion from Rs4.0 billion a year earlier. At first glance that looks healthy, but set against the inflationary backdrop it is more modest. The company’s nominal revenue growth lagged

nationwide price increases.

The story further into the income statement is more upbeat. Cost of sales grew just 2%, lifting gross profit by 37% to Rs2.1 billion and pushing the gross margin up from 39% to 46%. Operating profit almost doubled, climbing 93% to Rs1.2 billion, helped by relatively flat selling and distribution expenses and only a modest rise in administrative costs. Profit after tax surged 90% to Rs759 million, and basic earnings per share rose to Rs3.3 from Rs2.5.

Net margin expanded from 10% to 17%, a sizeable jump for a mid-tier fashion retailer. The board declared a cash dividend of Rs2.0 per share, having paid nothing in the previous year. As of this past Friday, the stock was trading around Rs23.9, implying a market capitalisation of roughly Rs5.5 billion, with a 52-week range between Rs14.9 and Rs36.8.

The most recent quarter paints a more nuanced picture. In 1QFY26, net sales grew a mere 7% year-on-year to Rs1.0 billion, while cost of sales jumped 17%. That shaved the gross margin down from an unusually high 54% in the same period last year to 50%, and gross

profit dipped 3% to Rs505 million. Operating profit was flat at Rs302 million, and higher finance costs – almost triple from Rs18 million to Rs50 million – pushed profit after tax down 12% to Rs242 million. Quarterly EPS slipped from Rs1.2 to Rs1.1.

The spike in finance charges is unsurprising. Businesses are still digesting the lagged effect of the State Bank’s policy rate, which was held at a record 22% for much of 2023 and only gradually cut to 12% by early 2025. Retailers like Image, which have invested in store networks and machinery, are carrying that interest burden into their P&Ls even as inflation cools.

Despite these headwinds, management has set an ambitious revenue target of Rs5.0–5.5 billion for FY26, implying top-line growth of about 20%. They expect gross margins to stay broadly in line with FY25, signalling confidence that the product mix – tilted towards higher-margin embroidered fabrics and readyto-wear – can absorb cost pressures.

Image Pakistan’s corporate and brand histories are intertwined but distinct.

The listed entity began life as Tri-Star Polyester Ltd, incorporated as a public company in 1990 and focused on manufacturing polyester filament yarn and fabric out of Karachi’s industrial estates. In 2021, as its fabric business increasingly revolved around the “Image” label, the company formally rebranded to Image Pakistan Ltd, aligning the corporate identity with the consumer-facing brand.

The brand itself predates that name change. Asad Ahmed and Farnaz Ahmed launched Image in 1993 as an embroidered-fabric specialist, selling premium Schiffli work wholesale to well-known fabric retailers in Lahore and Karachi. The first flagship store opened on Karachi’s Zamzama strip in 1998, marking the brand’s move into direct retail.

Initially, the market was dominated by unstitched cloth; as one director recalled, stitched ready-to-wear made up perhaps 5% of demand in the 1990s. But as malls proliferated and urban consumers warmed to off-the-rack kurtas in the 2010s, Image followed the trend, adding pret lines and gradually building a chain-store footprint.

Today the company describes itself as a fashion and retail house with a presence across five major cities – Karachi, Lahore, Islamabad, Rawalpindi and Peshawar – supported by a strong e-commerce platform. In 2021 it became one of the first Pakistani clothing brands to be officially listed as a seller on Amazon, and in 2022 it received a Prime Minister’s award recognising its e-commerce performance.

At the helm of the listed business is CEO Asad Ahmad, with headquarters located on Karachi’s Shahrah-e-Faisal and manufacturing facilities in SITE.

Image operates in two related domains: value-added textiles and branded fashion retail.

On the manufacturing side, the company produces embroidered fabrics – notably Schiffli embroidery – as well as ready-to-wear and unstitched suits aimed primarily at women. Its product range spans

• Embroidered and printed fabrics, often sold as three-piece or two-piece suits.

• Ready-to-wear kurtas and co-ords, many featuring heavy embroidery, appliqué and chikankari work.

• Seasonal collections – lawn and light cottons for summer, heavier fabrics and jacquards for winter – marketed both through physical stores and the online shop.

The company says it currently runs 72 multi-head embroidery machines and plans to add three more, taking the total to 75. Bank financing is already lined up for additional imports should demand justify further capacity expansion.

On the retail side, the brand operates a growing network of boutiques and mall outlets. Management told investors they

aim to reach 18 outlets by the first quarter of calendar 2026, with locations across major cities including Karachi, Lahore, Islamabad, Rawalpindi, Multan, Gujrat, Faisalabad and Peshawar. They highlighted that rent at their high-profile store in Karachi’s Dolmen Mall averages around 10% of sales – a healthy ratio by regional mall standards.

Internationally, Image is building a footprint in markets with sizeable South Asian diasporas – notably the UK, USA, UAE and European Union – primarily through online channels but increasingly via partnerships and pop-up formats.

Management is keen to diversify beyond fabrics and apparel into perfumes and lifestyle products, an increasingly crowded but higher-margin corner of the fashion market. They told analysts that Image is in the product-development phase and plans to launch three to four new perfumes each quarter once the line is established, potentially within FY26.

If executed well, this move could help smooth seasonality and deepen the brand’s relationship with its core female customer, but it also pits Image against specialised fragrance and cosmetics players at a time when discretionary spending is under strain.

Image’s trajectory cannot be understood in isolation from the broader formalisation of Pakistani retail.

A generation ago, apparel shopping largely meant buying fabric by the yard from neighbourhood stores and having it stitched by a family tailor. That paradigm began to shift in the late 2000s and early 2010s, as mall culture spread and branded lawn and pret labels such as Khaadi, Gul Ahmed, Nishat Linen, Sapphire and Sana Safinaz normalised the idea of chainstore fashion.

The growth has been rapid but remains shallow relative to the size of the population. A study by the Pakistan Institute of Development Economics estimates there are about 134 domestic chain-store brands in the country, with 73 of them in clothing and apparel, making it the largest formal segment. In total, these brands operate roughly 3,900 stores nationwide, with half of them concentrated in Karachi, Lahore and the Islamabad–Rawalpindi belt. The median chain has just 15 outlets.

The same paper describes Pakistan’s chain-store sector as still in its early stages of development, noting that even the biggest supermarket and fashion chains have far fewer outlets than comparable peers in India, and that only a handful of Pakistani clothing brands have a meaningful international presence.

In other words, the likes of Khaadi, Nishat Linen and Ideas by Gul Ahmed have built national awareness and dozens of stores, but the overall penetration of organised apparel retail remains low. These brands are now

experimenting with large-format “experience stores” – such as Ideas’ massive new outlet at Dolmen Mall Clifton – as well as online-to-offline integration and tech-driven personalisation.

Image sits in the middle of this evolution: smaller than the leading textile-backed giants, but with a more substantial footprint and brand equity than the niche labels that still rely on multi-brand retailers and seasonal exhibitions.

The retail opportunity is significant. One research house projects that Pakistan’s overall retail market could grow at a compound rate of about 6.5% from 2025 to 2031, driven by urbanisation, rising internet penetration and a slowly expanding middle class.

Yet the last three years have been brutal for household budgets. Pakistan’s inflation rate hit multi-decade highs in 2023, with some months recording year-on-year price increases of around 30% or more. While inflation has dropped sharply in 2025 – even touching low single digits early in the year – this reflects a statistical base effect more than a return to pre-crisis affordability.

For apparel chains, that translates into three challenges. Customers trade down from premium lines to basic suits or skip seasonal refreshes altogether. Mall visits spike around Eid and wedding seasons but remain muted otherwise. Fashion cycles do not slow down just because wallets are squeezed; the wrong bet on colour, cut or price point can be costly.

Image’s financials reflect these dynamics. Revenue growth in the mid-teens and single digits, as seen in FY25 and 1QFY26, is respectable but underwhelming once high past inflation is considered. The strong improvement in gross and net margins last year owes much to tight cost control and a favourable product mix, but the margin slippage in the latest quarter shows how quickly that cushion can erode when costs spike or discounting is required to clear stock.

Despite a challenging macro backdrop, Image’s management is clearly positioning the company for a more formal and brand-centric retail future.

The planned expansion to 18 domestic outlets within months, a continued push into the UK, US and Gulf markets, and the upcoming foray into perfumes all point to a growth-minded strategy rather than pure consolidation. The addition of more embroidery machines and the option to finance further capacity suggest confidence that demand for its core value-added textiles will eventually catch up.

For now, Image is doing enough to keep profitability moving in the right direction but not yet enough to break decisively away from the gravity of Pakistan’s bruised consumer. The inflation storm may have passed, but the dampness it left in shoppers’ wallets is still weighing on the company’s growth prospects. n

Revenue growth continues apace at Bank of Punjab in Q3

Aside from the structural boost to profitability from the interest rate environment for all banks, BOP’s branch expansion is beginning to yield results

The Bank of Punjab turned in another strong quarter, extending a two year run of outsized earnings as the provincial lender’s long push into low cost deposits, rural markets and digital origination starts to compound. Third quarter results show income advancing sharply and profits rising on the back of wider spreads and a better priced deposit base. Management says the repricing of legacy time deposits and a deliberate tilt towards current accounts should carry further gains into the year end.

The bank’s quarterly and nine month scorecards were the centrepiece of two post results briefings with analysts in November, which also laid out milestones in branch expansion, agricultural lending and an historic turn to dividends.

For 3QCY25, BOP posted profit after tax of about Rs5.1 billion, up 42% year on year. Earnings per share for the quarter printed around Rs1.6, up from Rs1.1 a year earlier, while 9MCY25 EPS rose to roughly Rs3.7 versus Rs2.6 last year, reflecting sustained operating leverage. Net interest income was up 61% year on year in the quarter, with total income up

42%; operating expenses rose 19%, far slower than income, helping lift profit before tax by 58% in Q3 and 81% for the nine months.

Arif Habib Ltd’s takeaways from the analyst call add more colour on deposits and funding costs. Deposits stood at about Rs1.8 trillion in September, with a seasonal quarter on quarter dip offset by healthier averages: current account balances increased 13.3% over six months and non MDR balances rose 10.5%, together adding an estimated Rs7.7 billion to revenue. Crucially, about 85% of high cost term deposits, roughly Rs427 billion of an estimated Rs500 billion, matured by late Q3. As these repriced, the weighted average cost of term deposits fell from 16.4% to 9.7%, with the full earnings effect expected to flow through Q4. Management’s current account share target for next year is 27% – another lever to sustain net interest margins even as the rate cycle stabilises.

Credit costs remained contained. Management highlighted that non performing loans total about Rs51 billion, of which Rs40 billion relate to legacy assets, with the NPL to book ratio at 6.5% – near the market average – and net NPLs at just 0.2% of book for the nine

months. The cost to income ratio has improved to around 60%, with a stated aim to bring it lower next year as returns from earlier technology and process investments materialise.

Beyond spreads and funding, non interest income held steady year to date, with fee income up 31% and foreign exchange gains higher, partly offset by lower securities gains. Put together, the 9 month total income rose 58%, against a 27% rise in operating expenses, lifting profit before tax by 81% year on year.

The sector backdrop has further helped. Since mid 2024, the State Bank has lowered the policy rate from 22% to 12% by late January 2025, improving the asset/liability repricing outlook for banks; the Monetary Policy Committee later paused the easing cycle at 12% in March to watch inflation dynamics. With high yielding assets rolling in and expensive funding rolling off, BOP appears well placed to clip the spread in the near term.

Constituted through the Bank of Punjab Act 1989 and accorded scheduled bank status in 1994, BOP is headquartered in Lahore and remains majority owned by the Government of Punjab, which holds just over 57%, according to public filings and company materials.

Its mandate has long straddled commercial banking and policy linked initiatives in the province, but the franchise today is national in reach.

A significant inflection came with the appointment of Zafar Masud as President and CEO in April 2020. The bank’s press release at the time underscored his remit to drive a modernisation and growth agenda, drawing on decades of international and domestic banking experience. Under his stewardship, BOP has pivoted hard into deposit mobilisation, digital origination, and inclusion linked lending –areas the bank now routinely highlights as engines of growth.

The branch network is the backbone of that push. The bank currently operates close to 900 branches across the country, and it houses a sprawling list of locations on its official site that stretches from large urban centres to smaller market towns – evidence of a strategy designed to skim deposits in deeper rural catchments as well as service mid market SMEs across the trading belt of Punjab and beyond.

BOP’s management told analysts the network will expand from about 900 to around 1,000 branches by 2027, with 50 openings planned in 2026 and 50 in 2027. Rural markets are a particular focus for low cost deposit acquisition, where competition is thinner and relationship banking still matters. The same briefings noted that private sector deposits have risen sharply since 2021, reducing historic reliance on public funds.

The funding transformation also has an operational spine: a multiyear investment in technology and process automation. Management says the returns are now visible in a better cost to income trend and in digital origination at scale. The briefings emphasised BOP’s status as Pakistan’s largest digital lender by cumulative disbursements – around Rs1,370 billion to nearly 1 million borrowers – and its position as the top credit card issuer, with more than 0.9 million cards in force. While these claims are couched in management’s own disclosures, they help explain the velocity in fee generating products and the bank’s confidence in cross selling as it adds branches.

Perhaps the most visible signal of balance sheet strength is dividends. In late summer 2025, BOP announced the first ever interim cash dividend in its history – Rs1.0 per share or 10% – a watershed moment for a bank that had previously prioritised capital build up over payouts. Multiple news outlets reported the milestone alongside record interim profits. Management has since indicated that, while it does not commit to quarterly payouts, a “historic” full year dividend is likely given earnings momentum and the stronger capital position.

Underpinning the strategy is funding discipline. As noted earlier, 85% of high cost

term deposits matured between Q2 and Q3, bringing their cost down from 16.4% to 9.7%; with policy rates steady at 12%, that repricing should support margins in Q4 and into 2026. Meanwhile, management is targeting a 27% current account share over the next year, a level that would reduce the average cost of funds further and insulate earnings should asset yields drift lower. These assumptions sit explicitly in the AHL takeaways.

Finally, asset quality and governance remain on the scorecard. The bank’s NPL stock is still weighted to legacy positions, with much lower net NPLs on the current period book – a sign, management argues, that underwriting standards and collections are holding up even as lending scales. The briefings describe the pillars of “sustainable profitability” as asset quality, operational efficiency, governance and compliance, deposit growth and digital transformation – a checklist that aligns with the post 2020 rebuild.

BOP’s agricultural franchise has become one of the bank’s signature differentiators. Management says the bank serves 18% of Pakistan’s agricultural borrowers, and has extended the Kissan Card programme rapidly in recent cycles. The portfolio stood near Rs60 billion in mid October and, by 13 November, about 85% had been recovered against maturity, with expectations of 98–99% recovery shortly thereafter – metrics that speak to both borrower selection and the mechanics of seasonal cash flow lending.