18 Despite tepid revenue growth, Shezan swings back to profitability

21 Cnergyico swings to losses, presses ahead with refinery investment

24 The India blockade did not damage Hum’s revenues. The BDS-driven advertising slump did

27 Farm income slowdown hits Ghandhara Tyre sales

29 Shell’s exit helps boost reported profits at Wafi Energy

31 From lenders to hedge funds –Pakistan’s banking transformation

34 Does it matter that some Pakistani companies rely on Indian data processing vendors?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

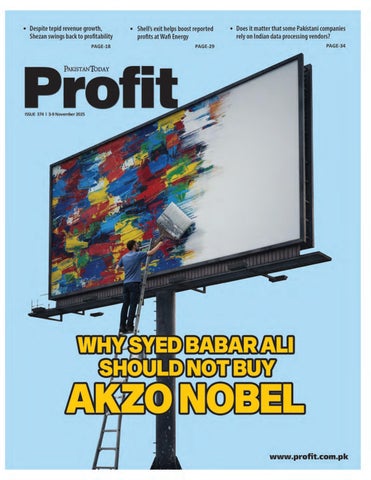

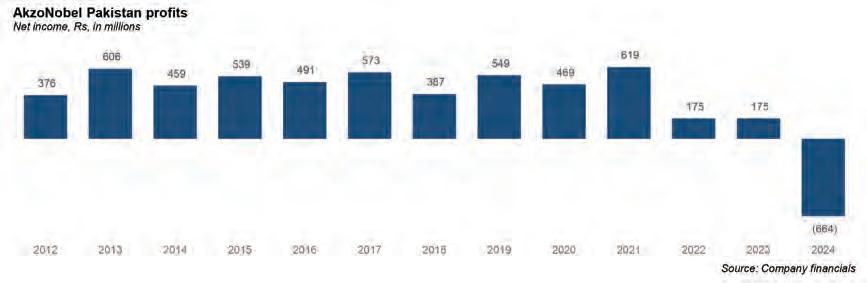

The Packages Group is reportedly interested in buying AkzoNobel. For one of Pakistan’s cleanest and most professional conglomerates, entering the paint business might mean getting their hands dirty

By Taimoor Hassan

Syed Babar Ali wants to buy Akzo Nobel. When the news broke that the Dutch paint manufacturer was wrapping up its operations in Pakistan, many were alarmed by the departure of yet another multinational player from the Pakistani market. The exit comes hot on the heels of Procter & Gamble’s exit and similar decisions by Shell and others in recent years. The interest of the Packages Group in acquiring the paint company was a small silver lining.

The Packages Group, after all, is one the oldest and cleanest companies in Pakistan. Over the decades Syed Babar Ali has turned it into a massive conglomerate with an impeccable reputation for doing everything above board.

That reputation is exactly why he should not touch Akzo Nobel with a ten-foot paint roller.

You see, while many might be dismayed over the exit of another multinational from Pakistan, those in the paint business will tell you the exit was a long-time coming. And while the weight of economic stress and policy paralysis have added to the cracks in the paint industry,

the bigger problem has been a swelling informal market in an industry that has increasingly become difficult to stay clean in.

For years, the paints sector was a beneficiary of Pakistan’s construction boom. Every new house, plaza, and mall brought with it another round of decorative coatings, emulsions, and industrial finishes. But as the economy slowed, that sheen began to fade. Today, the market tells a story of dwindling demand, unmanageable input costs, and thinning margins. Local players responded by evolving practices like the use of the infamous tokens, and MNCs have not been able to keep up.

For Syed Babar Ali, the equation is quite simple. Either he stays away from the paint business, and if he chooses to go ahead with it, he should be prepared to get his hands dirty and do business in a way his family has not done in a century.

The anatomy of an ugly business

There was a time when ICI was the first pick workplace for MBA grads. It has been an international company for more than a hundred years.

Founded in 1926, Imperial Chemical Company (ICI) by Lord McGowan, it created the Dulux brand in 1936. In the subcontinent, its origins started in 1940 with the establishment of its Soda Ash plant at Khewra, which supplied essential chemicals to the glass, textile, soap, and leather industries across the subcontinent. The company evolved significantly over the years, expanding into diverse sectors. In the 1950s, ICI’s Karachi headquarters was a hub for commercial trading and distribution of ICI-manufactured chemicals.

After acquiring Fuller Paints in the 1960s, ICI Pakistan expanded its presence in the local paint industry, leveraging international expertise and cutting-edge technology. In the 1990s, ICI Pakistan strengthened its position as a market leader with substantial investments, including a major expansion of its paint facilities. The company also diversified into other sectors like textiles, pharmaceuticals, and chemicals. However, its paint business remained the flagship, known for its strong brand equity and wide market reach.

Following the global restructuring of ICI PLC in the early 2000s, ICI Pakistan’s paints division became the jewel of its portfolio. In 2008, the division was acquired by Akzo No-

bel, a leading coatings company, as part of a strategic move to strengthen Akzo Nobel’s position in the global market.

In other words, Akzo Nobel and ICI paints were a cool place to work. Its office culture was derived from its international origins. The paints business was booming and ICI was sold in a traditional, corporate, professional manner.

This is no longer the case. For many years now the industry has tried to keep the changing reality of the paint industry a secret, but they no longer mince words. “Margins have collapsed,” says one senior figure from Nippon Paints Pakistan on the condition of anonymity. “We’re not just dealing with inflation, we’re competing against paints that don’t even meet basic chemical standards.”

trade off is tempting. The difference in finish or longevity often becomes visible only months later. But by then, the damage to legitimate manufacturers is already done.

The problem starts with costs. For organized manufacturers, paint manufacturing depends heavily on imported inputs: pigments, resins, solvents, and additives that are priced in dollars. As the rupee slides and LCs become a bureaucratic nightmare, large firms feel the pressure on the production side. For smaller companies that import raw materials, the working capital squeeze means that they can’t compete.

At the same time, electricity tariffs are among the highest in the region and have further inflated operational expenses. Freight and distribution costs have soared. Dealers, facing their own liquidity crunch, delay payments. Mir Shoaib Ahmed, the CEO of Diamond Paints, says that paints companies are doing up to 90% of their sales on credit to dealers. In many cases, manufacturers are forced to extend credit to retailers simply to keep shelves stocked.

What used to be a healthy, predictable supply chain has now become a web of delayed receivables and silent defaults. “We’re carrying the dealer’s risk, the customer’s risk, and the rupee’s risk all at once,” the Nippon executive told us.

But if costs were the only challenge, the industry might still find a way to survive. But Pakistan’s paint market faces a much more serious threat: the rise of the informal sector.

According to representatives of some of the international paint brands in Pakistan, they are not able to keep up with local players. They allege they cut costs and use sales and retail level marketing to outplay them. In nearly every major city, unregistered paint producers have mushroomed operating out of small warehouses and using untested chemical formulations. Their products, sold at half the price of branded paints, flood the market through the same dealers who once depended on multinational distributors.

For consumers squeezed by inflation, the

“People don’t realize that low-cost paints aren’t just cheaper, they’re unsafe,” says an industry insider. “Many use substandard materials and water bases that don’t comply with environmental or safety standards and are substandard products. Yet there’s no effective regulatory mechanism to stop them.”

This unregulated competition has created a two-tier market: one that rewards scale and brand equity on paper, and another that rewards cutting corners in practice. For companies like Nippon Paints or Akzo Nobel which operate under international quality compliance standards, it’s a losing battle. The unorganised sector they compete with is heavily cash based and does not pay its fair share of taxes, which allows them to further undercut their prices. “Couple the quality control problem with no tax cost and we struggle to compete.”

On top of this, the economic slowdown has been devastating for the decorative paints segment, which relies heavily on new housing and real estate projects. Private construction has slowed, and even ongoing projects face financing hurdles due to soaring interest rates.

“Every time construction halts, the first thing to stop moving is paint,” explained the Nippon executives. “People can delay painting their homes or switch to cheaper options. There’s no urgency and that kills volume.”

Industrial paints and coatings used in automotive and manufacturing have fared slightly better, though even there, declining vehicle production and factory shutdowns have eroded demand. Companies with a diversified portfolio, covering automotive and powder coatings, are still afloat. Purely decorative-focused firms, however, are running out of room to maneuver. This is where dealers play an important role.

Incentivising dealers

As a result of this burgeoning informal sector and the struggles of the established players, the paint market has evolved into a vast network of

dealers and sales agents spread across major urban centres as well as second and third tier cities.

These dealers form the backbone of the paint business. They are incentivised by organized paints manufacturers and the unorganized ones which gives them sales targets tied to rewards. If a dealer achieves sales targets of a particular manufacturer, the manufacturer would reward the dealer with say an expensive car or a leisure trip abroad or an Umrah trip. This network of dealers does not understand corporate speak. They have not only come to expect these incentives but also the attention and recognition of senior paint executives.

Local players have spent significant time cultivating these networks, developing close relationships with the dealers, hosting them, and giving them these incentives. It is a style of doing business that is smart, legal, efficient, and very ear-to-the-ground. It is also a style of doing business that does not come easily to corporate types that are usually hired by multinational companies.

Because this system has developed, local players have been more successful in tackling the shrinking margins. But it is not so simple.

There is nothing wrong per se with this practice but if one looks at the overall picture, companies that can give better rewards to dealers are ones that do well financially, that is the ones that do not bear the burden of taxation. By operating in the unorganized sector, companies can save massively on sales tax, import duties and income tax, giving them better financial room to fund incentives for dealers.

On the other hand, multinationals that are tax compliant bear the burden of taxation which squeezes their profits, decreasing their ability to compete with the unorganized sector. This hits their sales further, reducing their ability to incentivise dealers competitively. It becomes a vicious cycle - vicious enough that it can knock them out.

The net effect of all these pressures is stark. Industry insiders estimate that formal sector paint sales have dropped by more than 40% since 2022. Raw material costs have doubled in the same period. Yet end consumers already burdened by inflation refuse to absorb further price increases.

“It’s not sustainable,” say Nippon representatives. “We’re selling at prices that barely cover costs. The multinational model assumes a certain scale, a certain stability in policy and demand. That simply doesn’t exist in Pakistan anymore.”

It is within this bleak landscape that Akzo Nobel Pakistan’s decision to sell begins to make sense. Although they are restructuring and have sold majority shareholding of their business in India, selling the Pakistan business makes sense because continuing the business is expensive.

turer. As a result, multinational producers are finding their receivables stretching over long cycles. Some have introduced cash-only supply terms or reduced dealer credit limits, but that further shrinks their market reach.”

Estimates received by Profit from one multinational paints manufacturer give a very ugly picture. According to calculations of this manufacturer, 26 local companies under report their sales by an estimated Rs 27 billion. This under reporting has a tax impact of Rs 19 billion for the government presumably under the head of unrecovered sales tax and income tax.

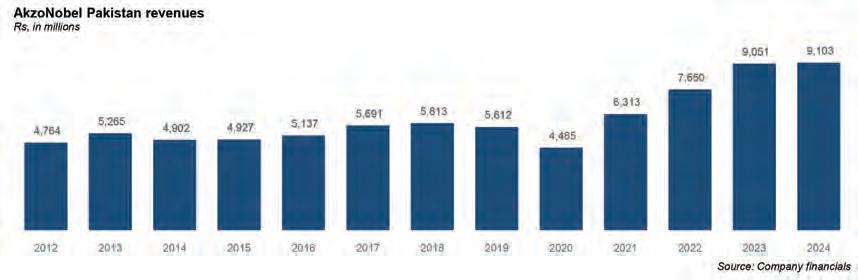

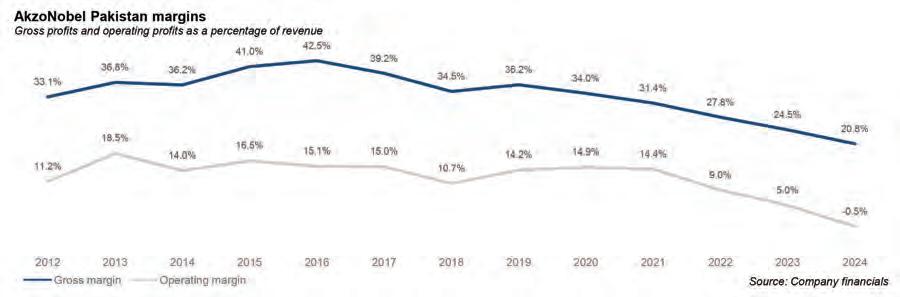

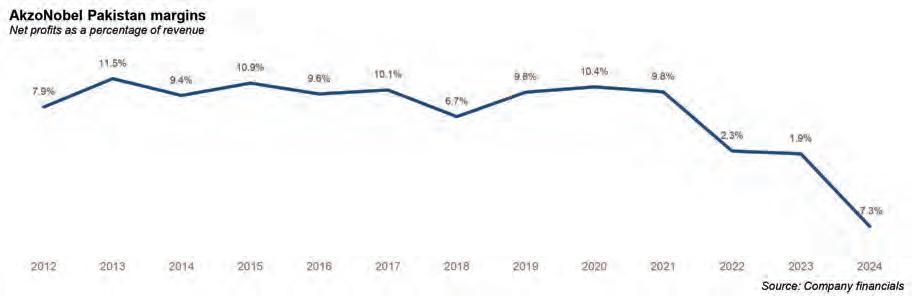

Akzo Nobel’s financials also testify that the company has faced a decline in sales over the past 10 years. While in nominal terms the revenue has increased, almost doubling over the last 10 years, in real terms, revenue has fallen to half even though Akzo has a strong brand presence in the decorative paints segment through its flagship product Dulux.

While dealers are the bridge between the factory and the consumer responsible for promoting products and managing inventory, the aforementioned scenario and the large presence of unorganized paint companies has led to a situation where presence of paints from companies like Nippon, Master, Diamond and Akzo Nobel have almost inverted at dealerships. They no longer occupy front rows on the shelves.

The current macroeconomic environment is also such that dealers are struggling to survive. “A dealer’s working capital is stuck between rising prices and falling sales too. This leads to a delay in the payment of the manufac-

In contrast, unregistered paint manufacturers offer flexible credit and bulk discounts, making them more attractive to small retailers. The outcome is predictable: quality products lose visibility, and cheap alternatives dominate the shelves.

The token bribeswhere things get dirty

It isn’t just the dealers. The paint industry has developed into one where the customer always comes last. On the ground, the situation at paint shops show just how entrenched dealers are and the tactics many brands use to sell their products. Walk into any paint shop in Pakistan today or talk to a painter, and you’ll find a paradox: the person paying for the paint is rarely its real customer. That title now belongs to the painter. Most of the time, Pakistani homeowners outsource the paint job to a paint contractor who charges a daily wage rate for painting. The painter, as part of his job, is also responsible for suggesting and bringing the right paint for the customer because the painter is perceived to be more technically equipped to choose the right paint of a certain brand. This has given too much power to the painter though.

Over the past decade, Pakistan’s paint industry has quietly evolved into a fiercely com-

petitive battleground not over price or quality alone, but over tokens tucked inside paint buckets. These redeemable coupons, introduced as marketing gimmicks, were meant to incentivize customer loyalty. Instead, they’ve shifted the entire balance of power in the market. Because of the excessive reliance of the customer on the painter, this daily wager chooses what paint works best for the customer not because of quality but because of how much money he can cash from inside the paint bucket.

Here’s how it works: a homeowner hires a painter for, say, Rs150,000. The painter buys the paint and quietly pockets the token inside each bucket. The homeowner, having already paid for the paint and its embedded token value, never learns that part of his money has been transferred to the painter’s pocket. In this scenario, the higher the token value, the stronger the brand’s hold on painters and the weaker the transparency with homeowners.

Sufi Amin of Master Paints minces no words when he says that “paint today is being made for the painter, not for the end user.” Master Paints is one of the few local brands that do not use tokens, and they have made it a point to use this as part of their marketing. As such, he does not shy away from calling this practice bribery and theft which has given so much power to the middle man (the painter) that the business has turned so messy that there is possibly no coming back from it.

The roots of who started this practice goes back to one of the multinational companies (certain executives actually accuse Akzo Nobel of starting this practice) whose marketing team ingeniously thought that paints would be bought more if cash prizes are placed inside the paint bucket. They wouldn’t have thought then that this money would not reach their end customers. Neither would they have thought that placing tokens would start a fierce competition war. The competition

followed, placing bigger tokens than competition.

“Imagine this that in a bucket of paint that costs Rs4,000, you can even find Rs1,400 worth of redeemable token. You subtract the cost of getting this bucket to the painter and you’d find that companies are burning themselves to death on something that is also ethically wrong,” says Amin.

“I told the painter to bring paint for my house worth three or four lakhs; he brought the paint, and from that he took out tokens worth around one and a half lakhs. Then the next day he didn’t even show up to paint he just left after taking those tokens,” Farooq Amin narrates the experience of one homeowner.

For Master Paints, which prides itself on avoiding token-based schemes altogether, this system has been punishing. “We’re the only company in Pakistan that does not include tokens,” he says. “And we’ve suffered immensely for it.”

Opinions vary within the industry. Some experts would call it “marketing expense”, passing it off as advertising or promotional cost in their books. Most don’t call it advertising, it’s literally a cash bribe to secure market share. The problem? It’s not working in anyone’s favour. As soon as one company gives more bribes, that share is lost. It’s a continuous battle where only one player wins: the painter.

Since 2011, the Competition Commission of Pakistan has been trying to crack down on this practice and forcing companies to visibly declare the value of tokens in the bucket. But despite repeated directives requiring companies to label paint buckets with encashable coupons inside, most disclaimers remain nearly invisible.

Earlier this year, the CCP found that Diamond Paints failed to mention tokens, misleading consumers at the first point of contact. The case originated from a complaint by Nippon Paint Pakistan, which accused Diamond Paints of misleading consumers by omitting key details about redeemable tokens in its television commercials. Although disclaimers appeared on packaging and shade cards, the CCP found that the TVCs, often the first consumer touchpoint, failed to mention the tokens or their value.

Diamond Paints pleaded guilty to this practice and showed a cooperative attitude which led to the SECP reducing the penalty on Diamond Paints from Rs50 lakh to Rs25 lakh. Despite attempts, the CCP has failed to force companies to put on their paint buckets a label saying that “an encashable coupon is included inside,” let alone specifying a figure.

Amin, who says Master Paints is losing

because of the token bribes, says full disclosures should at least be part of the advertising ethics. He does not say this out of acceptance of tokens as a form of bribe but because he thinks tokens have entangled the system so much that completely detangling it is not possible. Out of frustration, he means to include some ethics in this practice.

Word of caution for IGI

All of this brings us back to Syed Babar Ali and IGI. On October 22, IGI Holdings Ltd announced that its wholly owned subsidiary IGI Investments (Pvt) Ltd, had received in-principle approval from its board to evaluate and conduct due diligence for the purchase of up to 98.3% shareholding from ICI Omicron B.V. and up to 1.7% shareholding from minority shareholders of Akzo Nobel Pakistan Ltd. ICI Omicron, which currently owns Akzo Nobel Pakistan, is owned by Akzo Nobel in the Netherlands. One can see why IGI might benefit from expanding into the paints business. It is a product that has been around for a long time, there is a developed market and distribution system around it in Pakistan, and the Packages Group has rarely put a wrong foot down in its storied history. And while they will have done their due diligence surrounding this acquisition, the on ground situation might be worse than they expect.

Master Paint’s Farooq Amin Sufi has the same advice for Syed Babar Ali. “This industry has gotten dirtier by the day,” he says. “It has become a strange new economy where the painter, not the homeowner, dictates brand choice guided not by performance or durability of a paint, but by hidden monetary rewards, a practice considered unethical, akin to bribery or theft by industry observers. The reputation of Syed Babar Ali and IGI Holdings is above such practices.”

One of Pakistan’s most influential business leaders and philanthropists, whose vision and commitment to education and industry have left a lasting legacy, Syed Babar Ali’s name is more closely identified to ethics, integrity and progress embodied in the institutions that he conceived and nourished. As the founder of the Lahore

University of Management Sciences (LUMS) and the driving force behind Packages Limited, he has played a pivotal role in shaping both Pakistan’s corporate landscape and its higher education system. At both these places, his work reflects a deep belief in meritocracy, professionalism, and the transformative power of knowledge and enterprise, not unethical practices.

At LUMS, founded in 1984, Syed Babar Ali sought to create a world-class institution that would produce leaders capable of driving Pakistan’s economic and social progress. The institution he created would stand on par with top global universities and continues to embody his vision of developing ethical, innovative, and globally competitive professionals.

In the corporate sphere, Syed Babar Ali’s leadership of Packages Limited exemplifies his entrepreneurial foresight and commitment to industrial development in Pakistan. Founded in 1956 in collaboration with the Swedish firm Akerlund & Rausing, Packages became a pioneering enterprise in the packaging and paperboard industry. The company introduced modern manufacturing practices, contributed to import substitution, and set new benchmarks for corporate governance and sustainability in Pakistan. His approach combined business success with social responsibility, an ethos that has influenced generations of Pakistani entrepreneurs.

Taken together, Syed Babar Ali’s legacy really lies in the values he championed, that of excellence, integrity, and service to society. Whether through LUMS’ thriving academic community contributing to research and professionals in various domains or Packages’ enduring industrial presence, his contributions have helped lay the foundations for a more self-reliant, educated, and progressive Pakistan.

If he plans to get into the paints business, he would either have to spend so much cash that would be enough to wipe out competition significantly without tokens if he doesn’t want to scar his legacy. And if he plans to scar his reputation, even then he would have to spend a lot of cash and still might not be able to compete. As of now, the paint industry is messy enough that a white wash is not going to cut it. n

Inequality in Pakistan is at ‘crisis’ levels.

A new Oxfam report reveals how Pakistan’s wealthiest 10 percent command 42 percent of national income — a concentration that mirrors a regional pattern of inequality deepened by climate shocks and digital divides

In Pakistan, the wealthiest 10 percent hold 42 percent of the national income — a figure that lies below the Asian average, yet large enough to shape the contours of daily life. It determines everything from who gets to study abroad, to who breathes clean air, and who rebuilds after floods. It dictates the future as surely as it defines the present.

This concentration of wealth, measured in an Oxfam International study titled An Unequal Future: Asia’s Struggle for Justice in a Warming, Wired World, exposes the architecture of inequality built into Pakistan’s economy. Across the continent, the richest 10% capture 60 to 77 percent of national income, while the poorest half of society receives only 12 to 15 percent In countries like India and China, the top 1 percent alone hold nearly half of all wealth.

The study, released in October 2025, traces the widening gulf between Asia’s rich and poor. It is a divide sharpened not only by fiscal systems and elite capture but also by climate shocks and the digital economy’s uneven spread. Within its 50 pages lies a pattern familiar to many Pakistanis: a small elite shielded from crisis, and a majority struggling with rising prices, weak public services, and limited access to technology.

Dr Abid Aman Burki, who teaches poverty and inequality at the Lahore University of Management Sciences, calls Oxfam’s report a “bold attempt” at highlighting income and wealth disparities in the region. Dr Burki blames the current economic model for this widening inequality. “It benefits the powerful elite with a tax system reliant on indirect taxes while disproportionately burdening low- and middle-income households.”

Amitabh Behar, Executive Director at Oxfam International, puts it more sharply. “The massive gap between the billionaire elites and ordinary people is widening every day. While millions scrape by on $4 a day, the ultra-wealthy dodge taxes and profit from polluting industries as communities drown, homes are destroyed, and livelihoods vanish overnight.”

In a recent interview, he also said there was great relevance for Pakistan. “Pakistan is among the countries in Asia hardest hit by floods and climate shocks, yet the richest continue to hoard wealth and dodge taxes, leaving ordinary people to face the worst of the destruction.”

Their words echo the broader thesis of An Unequal Future: that Asia’s economic ascent has deepened rather than dissolved its inequalities. For Pakistan, this means confronting not only an uneven distribution of income but also the intertwined crises of debt, digital exclusion, and climate vulnerability.

The Unequal Model

The Oxfam report begins with an unsettling picture of wealth concentration across the continent. In India, Thailand, and Indonesia, the top 10 percent capture more than half of national income. In Pakistan, that figure — 42 percent — is lower but still enough to fragment society. Inequality here is less visible in skyscrapers than in electricity bills, in private schooling, and in the slow collapse of public health infrastructure.

The widening inequality has to do with the country’s economic structure. It benefits the powerful elite with a tax system reliant on indirect taxes while disproportionately burdening low- and middle-income households. There is evidence for this in Oxfam’s data: in 2022, Pakistan’s tax-to-GDP ratio hovered around 10 percent — among the lowest in Asia — with much of the tax revenue collected through consumption rather than income or wealth taxes.

Across Asia, the average tax-to-GDP ratio stands at 19 percent, compared to 34 percent among OECD nations. In Japan, Korea, and New Zealand, the ratio exceeds 30 percent, reflecting progressive taxation and robust public spending. But in Pakistan, the same tax regime that raises fuel and food prices for the poor allows the wealthy to retain their fortunes.

Public investment tells a similar story. Oxfam reports that Pakistan’s education spending in 2022 amounted to less than 2 percent of GDP — among the lowest in Asia, alongside Cambodia and Sri Lanka. With public spending so focused on debt servicing and other survival measures, there is little room for social spending on things like health and education.

This imbalance is not new. But its consequences have become more visible as Pakistan faces a dual crisis: mounting debt and recurring climate disasters. By 2024, external debt servicing for low- and middle-income Asian countries had reached $443.5 billion, forcing 25 out of 28 nations to cut public spending by an average of 3 percent of GDP. In Pakistan, where poverty is projected to remain at 42.4 percent, such austerity pushes essential services further out of reach.

In An Unequal Future, Oxfam’s authors warn that debt servicing now exceeds education and health spending for over two billion people across Asia. The result, they write, is “a vicious cycle where inequality fuels fiscal strain, and fiscal strain, in turn, deepens inequality.” For Pakistan, this cycle manifests in collapsing public hospitals, underfunded schools, and households where survival depends on remittances rather than state support.

Yet the inequities extend beyond fiscal structures. The report connects inequality to environmental and technological divides — crises that shape who suffers and who survives in a warming, wired world.

Climate and

Consequence

Pakistan sits at the intersection of Asia’s two defining pressures: inequality and climate vulnerability. The World Meteorological Organisation calls Asia the world’s most disaster-hit region, with over 1,800 events in the last decade — floods, droughts, cyclones, and heatwaves that killed more than 150,000 people and affected 1.2 billion others. Five of the most vulnerable nations — Bangladesh, Nepal, Myanmar, Pakistan, and Sri Lanka — are home to over 500 million people.

For Pakistan, the memory of the 2022 floods remains fresh. Thirty-three million people were displaced, millions of homes destroyed, and the cost of recovery exceeded $30 billion. Oxfam links such disasters to the unequal burden of climate change: “Asia faces escalating climate-induced inequality. The poorest communities are hit hardest by floods, droughts and heatwaves but receive minimal adaptation finance.”

The numbers underscore this injustice. To tackle and adapt to disasters, Asia needs $1.11 trillion annually, but receives only $333 billion — much of it as loans. “Wealthier nations continue to shirk their responsibility to pay for the climate damage they have caused in countries like Pakistan,” said Behar.

The inequity is not only international but domestic. Within Pakistan, the rich emit far more carbon than the poor. In South Asia, Oxfam estimates that someone from the richest 1 percent emits 17 times more than an average person and 50 times more than someone from the poorest half. Yet those same low-income groups bear the cost of climate damage — losing homes, crops, and livelihoods with little access to recovery funds.

Clean energy, too, has become a privilege. Oxfam notes that in 2024, high-income countries accounted for nearly half of global clean energy investments, while SouthEast Asia received just 2 percent. Within countries like Pakistan, urban elites adopt solar panels and electric vehicles, while rural populations — still dependent on grid electricity or diesel — face rising costs and frequent shortages. The transition to low-carbon economies risks reproducing the very inequalities it seeks to solve.

Climate disasters, Oxfam observes, are not just environmental events; they are social

accelerants. They push the poor deeper into debt, widen gender gaps, and erode fragile livelihoods. In Pakistan’s flood-hit districts, women bear disproportionate burdens — losing access to food, health care, and schooling. Across the region, 89 percent of women in flood-affected areas of Bangladesh faced food insecurity, while 91 percent suffered malnutrition. Similar patterns persist in Pakistan’s Sindh and Balochistan, where unpaid care work and displacement have left millions outside formal recovery plans.

In this sense, Pakistan’s climate crisis is inseparable from its economic one. Both are outcomes of a model that privileges the powerful — in fiscal policy, in infrastructure spending, and in global negotiations over aid and adaptation.

The problem with digital

If climate shocks expose inequality in the physical world, the digital divide defines it in the virtual one. Oxfam’s report devotes an entire chapter to Asia’s widening online gap — a frontier where access, connectivity, and opportunity mirror the region’s economic hierarchy.

Across Asia-Pacific, 83 percent of urban residents are online, compared to just 49 percent of rural populations. Pakistan’s internet speed — 7.85 Mbps — ranks among the lowest in the world. Within the region, Japan’s average speed exceeds 140 Mbps; South Korea’s is more than twenty times faster. In an era where education, business, and governance depend on connectivity, such gaps reinforce old inequities under new names.

In South Asia, gender compounds the divide. Out of 885 million women in lowand middle-income countries who do not use mobile internet, 330 million live in South Asia. Women here are 31 percent less likely to use mobile internet than men, constrained by affordability, literacy, and safety concerns. “Across Asia, women, especially in South Asia, remain far less connected than men,” Oxfam writes. “Out of 885 million women in low- and middle-income countries not using mobile internet, 330 million live in South Asia.”

Pakistan’s digital gap mirrors these statistics. Rural women remain three times more likely to lack internet access compared to urban men. The 2024 launch of Pakistan’s first Digital Gender Inclusion Strategy — led by the Pakistan Telecommunication Authority — acknowledged this disparity. It aims to improve connectivity for women through targeted programs, affordable data, and localized content. But progress remains slow. Meaningful connectivity, as Oxfam defines it, involves more than just being online.

It requires daily access at 4G speeds, personal devices, and stable networks at home or work. In Pakistan, affordability remains the key obstacle. High data costs, combined with unreliable electricity, make consistent access impossible for many lower-income users.

The divide has consequences beyond communication. As economies shift toward digital work, those without connectivity are excluded from opportunity. The report cites estimates that by 2030, 80 percent of jobs in South-East Asia will require digital literacy. Yet in South Asia, where millions remain offline, such skills are beyond reach.

In a world that celebrates artificial intelligence and fintech, Oxfam warns of “AI sweatshops” — exploitative data-labelling industries that pay minimal wages to workers in developing countries. Pakistan, with its growing freelance economy, risks becoming part of this underpaid digital workforce. Without protections, the digital economy could entrench the same inequalities that industrialization once did.

Gender, Work, and Access

The link between inequality, gender, and digital exclusion is intimate. Women in Asia perform two to four times more unpaid care work than men. In Pakistan, this burden limits time for education or employment, let alone for learning digital skills. Social norms restrict mobility, while safety concerns discourage online participation. Oxfam’s data shows that 41 percent fewer women use mobile internet in South Asia compared to men — a gap driven as much by patriarchy as by poverty.

Even among those online, access is unequal. Men dominate higher-paying technology jobs, while women remain concentrated in informal or unpaid roles. The World Economic Forum projects that 80 percent of emerging tech jobs will require advanced ICT skills, but in South Asia, only a fraction of women receive the necessary training. Without systemic investment in women’s education and connectivity, the next phase of growth risks excluding half the population.

Pakistan’s own initiatives reflect cautious recognition of this challenge. The National Commission on the Status of Women (NCSW) has launched campaigns promoting digital literacy and safe online spaces, alongside behavioural change programs addressing harassment and exclusion. But these remain pilot efforts. To achieve real inclusion, digital equity must be treated not as charity but as infrastructure — as

fundamental as electricity or roads.

The Cost of Exclusion

Digital inequality, like fiscal inequality, carries economic costs. The report estimates that closing gender gaps in Asia could add $4.5 trillion to the region’s annual GDP — a 12 percent boost. For Pakistan, where economic growth stagnates around 2 to 3 percent, such gains could transform development prospects.

Yet exclusion persists. Internet shutdowns — often imposed during protests or elections — deepen both political and economic marginalization. Oxfam notes that Pakistan’s 2023 internet suspension cost over $17 million in lost productivity and disrupted transactions. Such actions hit small businesses and freelancers hardest — those already struggling to compete in global markets.

The cumulative picture is stark. Whether through taxation, climate, or technology, inequality in Pakistan is systemic — sustained by structures that privilege the few and marginalize the many. What Oxfam calls “Asia’s struggle for justice in a warming, wired world” is, in Pakistan, a daily negotiation for survival.

A Future to Reimagine

Oxfam’s study closes with a call for “National Inequality Reduction Plans” — measurable, time-bound frameworks to lower the income Gini below 0.3 and the Palma ratio below 1. For Pakistan, this would mean confronting elite capture head-on: enforcing progressive taxation, expanding health and education budgets, and investing in digital and climate resilience. The challenge is immense. The richest 1 percent in Asia emit forty-four times more carbon than the poorest 50 percent. Pakistan’s poorest still live on less than $3.65 a day. Its women remain disconnected from the internet and excluded from decision-making. Yet, as An Unequal Future argues, these trends are not inevitable. They are political choices — shaped by fiscal priorities, public policy, and the willingness to share power.

“Governments must adopt and implement National Inequality Reduction Plans with measurable, time-bound targets,” Oxfam urges. “Fiscal systems must shift from regressive consumption taxes to progressive income and wealth taxation, enabling governments to deliver rights-based public services.”

For Pakistan, where inequality is both historical and structural, such measures would mark not just reform but reinvention — an attempt to replace inherited hierarchies with shared prosperity. Whether that future is possible depends on whether 42 percent can be made to mean something more than ownership — something closer to accountability. n

Despite tepid revenue growth, Shezan swings back to profitability

Some positive tailwinds from boycotts of multinational competitors and increased exports helped sales in parts of Punjab.

Shezan International has returned to the black in its 2025 financial year, converting a deep loss the year before into a solid profit on the back of better margins, lower finance costs and a modest uplift in sales. The Lahore-based food and beverage company – best known for juices, sauces and pantry staples – also signalled fresh momentum in exports and an improving distribution push in key diaspora markets, even as it remains cautious about excise taxes at home.

The headline numbers tell a story of operational repair. Net sales rose to Rs9,183 million in FY25 from Rs8,155 million a year earlier, an increase of 13%. That rise, while hardly spectacular in a year of high food inflation, was enough to leverage a bigger improvement further down the profit and loss statement. Gross profit climbed to Rs2,252 million from Rs1,610 million, lifting the gross margin to 25% from 20% as the product mix and input discipline improved. The company swung from a FY24 loss after tax of Rs463 million to a FY25 profit after tax of Rs163 million.

The company’s fourth quarter was particularly robust – historically the best seasonal period – with EPS of Rs16.57 against Rs8.77 in the same quarter last year and a gross margin of 27% compared to 24% previously. Management attributes the strong quarter to volumetric growth and mix, although it cautions that margins fluctuate with seasonality and weather; floods and sudden temperature shifts in September and October dampened momentum at the tail-end of the season.

The margin story also has a geographic dimension. Management notes that export margins are “much better” than local margins, which partly explains why a relatively small increase in export value can punch above its weight in profitability. Export sales rose from $3.0 million to $3.5 million in FY25, and management is guiding to 10–15% export growth (excluding any rupee depreciation effect), giving Shezan a structurally richer earnings mix if it can sustain that pace.

The 13% revenue lift in FY25 did not come from a single lever. Part of the uptick reflects a consumer shift inside Pakistan

towards local brands, a trend that Shezan’s management believes has become more pronounced in the last year. This pivot in sentiment coincided with widely reported consumer boycotts of select multinational food and beverage brands after the war in Gaza began in late 2023.

While Shezan does not claim victory on the back of geopolitics, management does report that more shoppers are now willing to say domestic labels are “as good” as foreign alternatives. In a market where multinationals historically commanded a premium in perception, this equalisation – however incomplete – supports local incumbents on the shelf and in the cold chain. The company’s relative strength in cities such as Faisalabad and Gujranwala, and weaker positions in parts of Sindh and Karachi where multinational PepsiCo’s mango drink Slice holds sway, illustrate how these dynamics are playing out region by region.

The international trade backdrop also shifted in Shezan’s favour. New tariffs imposed by the United States on Indian products

opened up a niche for Pakistani suppliers in specific categories. Management says it is moving into Kesar mango pulp to meet demand at American restaurants – think mango lassi and dessert bases – where Indian supply had long been entrenched. In a category with quality sensitivity and seasonal constraints, additional quota-like space created by tariffs can be catalytic for new entrants. Beyond the US, Shezan cites healthy traction across the UK, Canada, the UAE and the US itself, with the largest opportunities in markets that host sizeable Pakistani diasporas, including Australia and Saudi Arabia. These customers often seek “nostalgic” flavours and pantry items –precisely the territory where Shezan’s brand heritage and recipes resonate.

At home, the policy environment remains a watchpoint rather than a windfall. The company does not expect a reduction in the Federal Excise Duty (FED) in the coming years and is focused instead on ensuring it does not increase. For a juices-heavy portfolio, the duty stance directly influences price points, affordability and category volumes. That is partly why management’s FY25 focus has been to reinforce the core portfolio and claw back pre-COVID and pre-FED volumes rather than chase entirely new categories. In other words, the growth of FY25 is a mix of a modest domestic recovery, diaspora-led export demand amplified by tariff changes abroad, and a perceptible tilt in consumer preferences towards local players.

Shezan International is one of Pakistan’s longest-standing fruit processors and packaged-foods companies, building out from juices and nectars into sauces, ketchups and ready-to-eat items over decades. Today it is listed on the Pakistan Stock Exchange under

ticker SHEZ, with a market capitalisation in the low-single-digit billions of rupees at the time of the briefing. Management describes a nationwide footprint that reaches all major metropolitan centres – Karachi, Lahore, Multan and others – even if competitive intensity varies by city.

Juices and drinks account for the lion’s share of the business – between 60% and 70% of revenue – anchored by the 250 ml format that dominates unit volumes. Condiments are the second pillar: ketchup is a mass-market staple locally, whereas in exports Shezan leans into differentiated chilli sauces and other variants that are less readily available in destination markets. In fact, management says the export customer demands greater variety than the domestic consumer, prompting the company to create unique sauces primarily for overseas shelves. Ready-to-eat canned foods such as Sarson ka Saag and Lahori Chanay serve a specific working-class niche, particularly in the Middle East where convenience, cultural familiarity and price are decisive.

A distilled water plant came online with a soft launch in April–May of the prior year. Production is currently limited to Lahore, and the commercial focus is deliberately narrow – Lahore and surrounding areas – to ensure execution discipline before any wider rollout. As for beverages, Shezan is not pursuing carbonated soft drinks and is instead adding flavours within its sauces and ketchup ranges. This incremental innovation strategy lowers risk, protects working capital and allows the company to drive margin accretion via mix rather than capex-heavy diversification.

Internationally, the company is tuning its route-to-market with more granular distributor density; for example, management aims to

double the number of distributors in Canada from two to four, a change that should increase availability and reduce stock-out risk across provinces. Africa, by contrast, is not a nearterm strategic focus due to acute price sensitivity, foreign-exchange frictions and intense competition from Bangladeshi and local brands.

Management’s FY25 stance is pragmatic: defend and grow the core, don’t chase glamour categories, and build depth in exports where margin per unit is superior. The company says it will focus on recovering pre-COVID and pre-FED volumes in juices and drinks before attempting any radical category expansion. In practical terms, that means more flavours and line extensions in sauces and ketchups, tighter execution in Lahore for distilled water, and a sharper export playbook designed for diaspora tastes and restaurant demand.

FY25 shows a Shezan that is still conservative about capex and category leaps but newly confident about execution where it already competes well. A revival in profitability, visible dividend reinstatement and healthier margins put the company on steadier footing. The top line is moving, if not racing; however, exports are doing the heavy lifting in profitability, and diaspora markets present a durable runway – especially as tariff shifts abroad and consumer sentiment at home provide incremental tailwinds.

The work ahead is largely operational: pack-price discipline under an unhelpful excise regime, distributor density in North America and the Gulf, and share gains in contested urban pockets of Pakistan. If Shezan can bank another year of export growth while holding the line on domestic margins, FY26 could extend the company’s quietly improving narrative from recovery to resilience. n

Cnergyico swings to losses, presses ahead with refinery investment

The vertically integrated oil and gas company is breaking up into constituent components

Cnergyico PK Ltd (PSX: CNERGY) – still better known to many investors by its former name, Byco – has swung to a loss for the financial year ended 2025, even as revenues climbed and the company pressed ahead with a billion-dollar refinery upgrade and a sweeping break-up into separate businesses. Management is also pivoting its crude slate toward lighter imports from the United States and West Africa – away from Pakistan’s traditional sources in Saudi Arabia and the UAE – to limit furnace oil yields, while exporting most of the furnace oil it still produces to offset domestic levies.

On a standalone basis, net sales rose 23% year-on-year to Rs297 billion in FY25 from Rs241 billion in FY24. But the revenue uplift

did not translate into earnings: gross profit fell 60% to Rs5.0 billion, squeezing the gross margin to 2%, and profit after tax swung from Rs1.0 billion in FY24 to a loss of Rs2.9 billion in FY25. EBITDA dropped 45% to Rs9.5 billion. The company’s fourth quarter illustrated that pressure starkly: sales dipped 9% yearon-year and gross profit was essentially flat, producing a quarterly loss.

Volumes in the oil-marketing (OMC) arm provided a rare bright spot. Despite pervasive discounting in the market, smuggling across borders and volatile pump prices, Cnergyico reported a 34% increase in OMC sales volume in FY25 – a strategic cushion that could matter more once refinery upgrades begin to bear fruit.

Liquidity and policy frictions remain

central issues. The federal and provincial governments and the company owe each other significant sums; net receivables due to Cnergyico stand at roughly Rs10 billion after offsetting mutual claims, and a settlement of pre-2023 petroleum levy obligations has been approved by the Economic Coordination Committee (ECC) of the federal cabinet with support from the military-led Special Investment Facilitation Council (SIFC).

On operations, volume is deliberately constrained. Management is currently running the complex at about 30–35% of capacity with a budgeted throughput near 60,000 barrels per day (bpd), arguing that pushing the plant harder in today’s market can increase logistics bottlenecks, raise product disposal risks – particularly for furnace oil – and heighten expo-

sure to exchange-rate and inventory losses.

The core profit headwind is structural: furnace oil is a negative gross-margin product for Pakistani refineries in most market conditions, and policy has turned even less hospitable. Cnergyico notes that levies such as the Petroleum Levy and the Climate Support Levy on furnace oil have encouraged the company to export 90–95% of its furnace oil output, with only a sliver sold domestically. That strategy helps clear tanks but does not, by itself, fix the economic penalty of producing a product that is difficult to monetise at home.

This is why refinery upgrades – and the crude diet – matter. Government policy has for years pushed refineries toward Euro-5 fuels and lower furnace oil yields, but the incentives and tax treatment have moved slowly. Sector-wide estimates suggest Pakistan’s brownfield upgrades require multi-billion-dollar investments in desulphurisation, isomerisation and conversion capacity to shift the yield away from furnace oil and toward motor gasoline and diesel.

Against that backdrop, Cnergyico is doing what it can within the current kit: change the crude slate. Management says it is, for the first time, importing lighter US crude and targeting similar West African barrels in FY26 to minimise furnace oil yields. Sailing time for US cargoes is about 35–40 days; the first parcel is due imminently, a second mid-November, and a third in January. The logic is basic refinery economics: lighter, sweet crudes produce a higher share of premium products (gasoline, kerosene/jet, diesel) and a lower share of furnace oil, improving the weighted margin even before new cracking hardware is installed.

Cnergyico will bring in Pakistan’s first-ever US crude cargoes under a Vitol-backed deal, signaling the company’s ability to handle large tankers at its offshore terminal. The company itself underscores that it operates the country’s only Single Point Mooring (SPM) – a floating deep-sea oil terminal off the Balochistan coast at Hub – giving it an edge in securing diverse feedstocks and managing import logistics.

Refiners improve margins not simply by buying different crude, but by changing what their units do to the molecules. In a simple “topping” or “hydroskimming” configuration, the distillation column separates crude into cuts based on boiling point. Heavier fractions – vacuum gasoil and residuum – disproportionately end up as furnace oil if there is no conversion capacity to break them into shorter, high-value chains.

Cracking units apply heat, catalysts, hydrogen and pressure to change that fate.

Fluid Catalytic Cracking (FCC) takes vacuum gasoil molecules and, using a zeolite catalyst at high temperatures, “cracks” long hydrocarbon

chains into lighter products such as gasoline, LPG and light cycle oil.

Hydrocracking performs a similar function in the presence of hydrogen under high pressure, producing clean distillates – notably diesel and jet – with low sulphur and high cetane/flash properties. Residue upgrading technologies (e.g., residue FCC, ebullated-bed hydrocrackers, delayed coking) process the heaviest resid that would otherwise end up as furnace oil, converting a large share into lighter distillates and petroleum coke.

Each percentage point of resid converted away from furnace oil increases the yield of saleable, high-margin products and typically reduces storage, working-capital and environmental costs tied to heavy fuel handling. That is the economic premise behind Cnergyico’s multi-phase upgrade, whose Phase-2 explicitly targets “furnace oil cracking to significantly reduce [furnace oil] production to the minimum required for own consumption,” followed by higher output of high-speed diesel (HSD) and premier motor gasoline (PMG).

Cnergyico’s evolution mirrors Pakistan’s refining sector over the last two decades. Incorporated in 1995 as Bosicor Pakistan, the company became Byco Petroleum and then rebranded as Cnergyico PK Ltd in 2021 to signal a more integrated energy strategy. The new name is meant to be a portmanteau of “Chemical Energy Integrated Company,” reflecting ambitions beyond simple refining.

Cnergyico operates Pakistan’s largest installed refining capacity at roughly 156,000 bpd, a figure built on two adjacent trains in Hub, Balochistan: the older 35,000 bpd complex (often referred to as ORC-I) and the larger 120,000 bpd complex (ORC-II). The company’s offshore Single Point Mooring – Pakistan’s only floating liquid port – connects via subsea and sub-soil pipelines to on-shore storage at Mouza Kund, allowing direct discharge from very large crude carriers and reducing dependence on congested shore berths.

The group spans refining, an OMC retail network with more than 465 petrol pumps nationwide, and logistics around the SPM and related pipelines. In 2022, Cnergyico also acquired a majority stake in Puma Energy, a rival fuel retailer, to accelerate footprint growth, underpinning the integrator strategy.

The barrels coming off the units include LPG, light and heavy naphtha, high-octane blending components (HOBC), motor gasoline, kerosene and jet fuel, high-speed diesel and furnace oil. As management emphasises, the future mix is intended to feature more Euro-5 compliant PMG and HSD and far less furnace oil as the cracking phase completes.

The refinery upgrade is framed in three phases with an estimated cost near $1.0 billion, most of which sponsors are expected

to arrange: (1) conversion to Euro-5 standards (now at an “advanced” stage), (2) furnace-oil cracking to reduce output to internal-use minimums, and (3) higher HSD and PMG production. The plan dovetails with national policy but awaits clarity on certain tax and levy treatments to allow formal signing of upgrade agreements.

The board is pursuing a de-merger through the Sindh High Court that would split the current listed company into six distinct entities, matching the six businesses that currently sit under one roof. Management argues the break-up will make it easier for strategic investors to participate in specific segments – for instance, the logistics arm, the OMC, or a particular refinery train – without taking exposure to the whole group. A court petition has been filed and a hearing is pending.

Strip away the noise and Cnergyico is pursuing a two-track transformation. First, the company is re-engineering its barrels –lighter feed, more conversion capacity, Euro-5 compliance – to escape the furnace-oil trap. Second, it is re-architecting its corporate structure through a six-way de-merger so that partners can invest in discrete businesses (OMC, logistics/SPM, each refinery train, etc.) without wading through conglomerate cross-exposure.

FY25’s loss underlines how urgent that shift is. Revenues grew but the product slate and pricing backdrop overwhelmed the P&L. The company’s own numbers show that cost of sales rose faster than sales, crushing gross profit and forcing a 75% drop in operating profit. The fix does not lie in selling more barrels of the same product mix; it lies in selling different barrels – fewer tonnes of furnace oil and more litres of PMG and HSD. That is precisely what lighter crude and cracking units deliver.

The company has the hard assets to execute – Pakistan’s largest installed refining capacity and the country’s only offshore SPM – and a retail network big enough to absorb upgraded output. But the calendar is not entirely in Cnergyico’s control: upgrade agreements and the fiscal treatment of furnace oil are still being nailed down in Islamabad, and the de-merger timetable is in the Sindh High Court’s hands.

Cnergyico’s FY25 results were disappointing, but they read less like a destination and more like a waypoint on a difficult transition that most of Pakistan’s refineries must undertake. The prize – a refinery that cracks more, burns less furnace oil, sells cleaner fuels and taps deep-sea import logistics – is worth the engineering and policy grind. The next twelve months will tell whether the company can turn that blueprint into a sturdier margin stack and pull its P&L out of the red. n

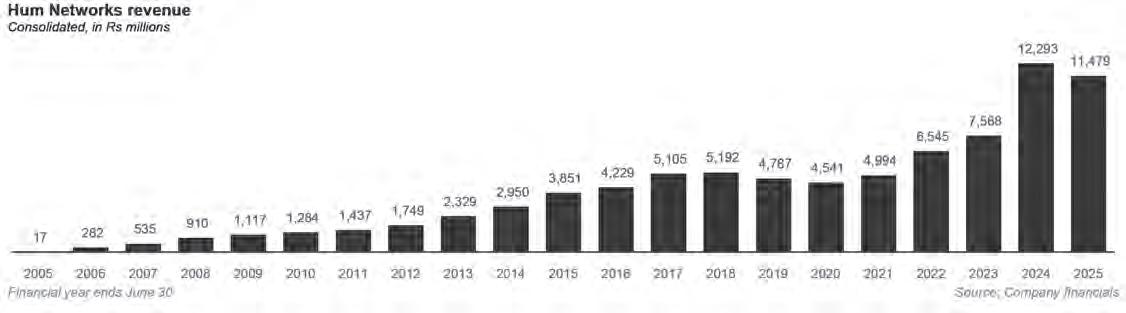

The India blockade did not damage Hum’s revenues. The BDS-driven advertising slump did.

The

network’s YouTube revenue did not slow down in 2025, though the anti-Israel boycotts of multinational consumer goods companies did hit ad sales

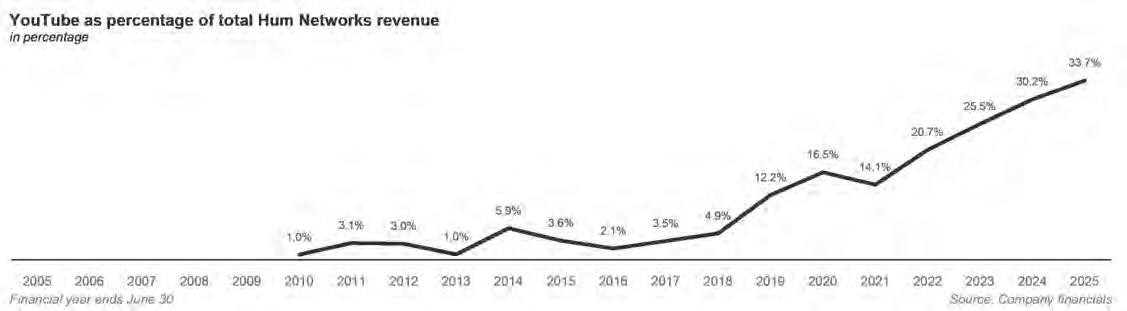

Hum Network Ltd (PSX: HUMNL) ended FY2025 still in profit, but with thinner margins and a markedly weaker fourth quarter as Pakistan’s advertising market seized up. Management says the shock had little to do with India’s geo-blocking of Pakistani channels on YouTube and everything to do with an advertising freeze tied to boycott, divestment and sanctions (BDS) campaigns that targeted multinational consumer brands – many of which are among the country’s largest media buyers. At the same time, Hum’s digital engines – principally YouTube – continued to hum, cushioning the blow as audiences and marketers migrate online.

Hum’s top line for FY2025 (year ended 30 June 2025) came in at roughly Rs11.5 billion on a consolidated basis, compared to Rs12.3 billion in FY2024, with gross margin easing to 46% from 50% a year earlier, according to the company’s published financial highlights. Profit after tax was Rs1.2 billion, down from Rs2.9 billion in FY2024. These headline figures underscore the network’s resilience through most of the year – until the final quarter, when advertising demand abruptly fell away.

The fourth quarter is the tell. Management says that as the Gaza war escalated in late 2024 and into 2025, a wave of boycotts against US and European multinational consumer companies pushed their local units to pull or postpone campaigns. Hum describes an “almost complete” shutdown in ads at one point, slicing quarterly revenue to Rs100–200 million from a pre-shock run rate of Rs400–

500 million. Unsurprisingly, quarterly EPS slid to Rs0.19 from Rs0.73 a year earlier.

Hum’s consolidated revenue model is simple to describe: advertising is the core, digital revenue (primarily YouTube) is the growth engine. In the company’s FY2025 materials, management discloses the mix of “revenue streams” as follows: advertisement 62%, subscription 26%, digital 1.63% and production 2% (other income sits outside revenue). A year earlier, the mix was advertisement 64%, subscription 27%, digital 1% and production 3% (with a small contribution from film distribution). The shift tells two stories at once – advertising softened; platform (YouTube) income held up or improved.

Put into rupees using FY2025 consolidated net revenue of roughly Rs8.01 billion, ads contributed about Rs5.0 billion, subscriptions about Rs2.1 billion, and digital revenue around Rs0.13 billion, with the remainder from production and other smaller lines. Crucially, Hum notes that the steep falloff in late-year ad spend was exogenous: a boycott-driven decision by large multinationals that hit “all major networks,” not a collapse in Hum’s audience share.

That distinction matters because it explains why YouTube revenues did not wobble in tandem with TV spots. Hum has spent three years retooling for digital, building separate teams for digital-first videos and podcasts; the company says digital growth is now “more robust than linear growth.” Subscription revenue – largely a function of YouTube ad-sharing and related platform monetisation – is grouped alongside digital in the consolidated accounts and, by manage -

ment’s telling, was resilient through FY2025. Hum’s answer to the secular shift in attention is to create for it. Management has built stand-alone digital teams producing platform-native content – short-form, podcasts and digital-only series – to catch audiences migrating from the living room to the phone. The company cautions that the immediate payout on these bets will be reach, not rupees; monetisation is expected to scale materially over the next two years as catalogues deepen and algorithms reward consistency.

Beyond content, the more experimental plank is gaming and animation. Hum is the lead partner in a government-backed consortium (with Huawei, 10s Game BCN and local partners) to train 10,000 people over five years – half in Karachi, half in Lahore – with a view to building an exportable capability. Management’s commercial exposure is limited: the Ignite contract pays Hum a management fee as lead manager, and the company expects only a nominal profit on invested funds – recoverable through the contract –but is explicit about the long-run upside if a domestic talent bench can consistently ship work for global markets.

The network is also stress-testing its payment rails and rights acquisition flow for a world in which cross-border transactions can be fraught. Hum holds about Rs1.54 billion in foreign-currency cash within a subsidiary – maintained as a current account because it is a repatriable payable – so it can settle international content and software deals (from cricket rights to platform licences) without the frictions of remitting abroad. That may be arcane finance, but it is the

plumbing that enables timely content drops and uninterrupted digital operations.

Longer term, the company is guiding to a 20–25% compound growth rate in revenue and profitability – an ambition predicated on linear stabilisation and continued digital scale. More OTT presence, targeted ad products using audience data, deeper sports rights (leveraging Ten Sports), and AI-assisted newsroom tools to keep Hum News competitive on speed and accuracy.

It is tempting, given the deteriorated state of India-Pakistan ties, to ascribe media-sector ups and downs to India’s geo-blocking of Pakistani channels on YouTube following the four-day aerial battle between the two countries. But Hum’s FY2025 story weakens that argument. The company’s own explanation of the year pins the damage on an advertising slump driven by BDS. The network points out that its entertainment channel retained a leadership rating during the year, and that the news division actually held up “even during tough times.”

Hum’s corporate arc predates those bans anyway. Incorporated in 2004 as Eye TV (later Eye Television Network), the company grew up on original Urdu programming – HUM TV launched in 2005, Masala followed in 2006, and later Hum Sitaray and Hum News joined the roster. In 2023, the group added Ten Sports to extend its reach

into live sport. That bouquet, now distributed across satellite, cable and digital, gives Hum a portfolio less exposed to any one regulatory variable and more levered to Pakistani originals and diaspora tastes.

Hum operates across entertainment (HUM TV, Hum Sitaray), lifestyle and food (Masala), news (Hum News), cinema (Hum Films), and sport (Ten Sports). Its operations are grouped into entertainment and news segments for reporting purposes.

As noted, ads are still the single biggest contributor, but platform-linked subscription and digital revenue together now account for almost a third of the consolidated top line. On FY2025 revenue of Rs11.5 billion, about Rs3.7 billion flowing from YouTube and adjacent digital monetization.

Hum’s experience in 2025 mirrors the media economy’s bifurcation: legacy TV remains a reach monster for the biggest brands, but it is hostage to their macro and reputational cycles; digital is atomised, global, and monetises on audience behaviour rather than media-plan politics. When BDS-related boycotts hit last year, Pakistani subsidiaries of affected multinationals paused spend across TV, dragging down every major network’s revenue in lockstep. But YouTube is fed by a different tap – global ad pools and platform payouts tied to watch-time and RPMs. That is why Hum’s digital and subscription line

items held up even as TV spots dried, and why the company is doubling down on digital-first content and data-driven ad products for the next phase.

If multinational FMCG and telco budgets resume regular scheduling, Hum’s ad line can revert towards FY2024 levels. If the BDS overhang persists, the network will need to lean harder on sponsorship integration, performance-linked campaigns and sports to offset weaker brand advertising.

Management expects “more robust” growth in digital than in linear. The work now is throughput: more digital-only shows and podcasts, regular short-form drops, and better audience analytics. If the YouTube machine keeps compounding, the combined subscription-plus-digital share could inch up from the current 33% of revenue.

Hum says the news segment performed well “even during tough times,” and hopes to generate more profit from it this year. Modernising the newsroom with AI-assisted tools while preserving credibility will be the balance to strike.

With Ten Sports in the stable, Hum has a platform to court advertisers that are looking for brand-safe, high-engagement inventory even when politics intrudes elsewhere. Expect rights deals and sports production to feature prominently as the group redraws its revenue map. n

Farm income slowdown hits Ghandhara Tyre sales

Tractor tyres, one of the company’s core products, saw a sharp slump amidst floods and weak agriculture growth

Ghandhara Tyre & Rubber Company Ltd (PSX: GTYR) – rebranded in 2021 from General Tyre – slid into losses in FY2025 as the farm economy’s slowdown pinched tractor-tyre demand and pricing power. Management says the trough is cyclical and fixable: a pivot toward the replacement market, selective export pushes, and a refreshed product pipeline are intended to rebuild volumes through 2026, even if rural purchasing power takes time to heal.

GTYR’s FY2025 consolidated picture is stark. Net sales fell 13% year-on-year to Rs17.8 billion (FY2024: Rs20.5 billion). Gross profit contracted 31% to Rs2.3 billion (FY2024: Rs3.3 billion) as the gross margin slipped to 13% from 16%. Operating profit nearly halved, and finance costs – while lower – could not cushion the blow from weaker volumes and

a tougher mix. The company swung from a Rs229 million profit after tax in FY2024 to a Rs366 million loss in FY2025. The dividend was suspended.

Quarterly numbers hint at stabilisation but not yet recovery. In 1QFY2026, sales eased only 3% year-on-year with the gross margin holding near 16%, yet operating profit and EPS remained subdued, reflecting a still-soft domestic market and the absence of last year’s price-led relief. Management’s guidance is pragmatic: defend share in the most resilient categories, de-risk the order book with replacement demand, and ready new SKUs that can land in 18–24 months.

Two operational notes from the briefing coloured investor sentiment. First, farm tyres – historically a profit anchor – have been “suffering from low volumes” amid poor farm economics. Second, the company plans to lean into exhibitions and distributor development

abroad to scale exports, a sensible hedge while domestic demand heals.

The revenue decline is less a factory story than a farm story. Pakistan’s agricultural heartlands have struggled with successive shocks – devastating 2022 and 2025 floods, erratic weather thereafter, and high input costs – leaving farm cash flows fragile. The government’s own economic survey documents heavy damage to crops and rural infrastructure from the recent deluge, with lingering effects on livelihoods and on-farm investment capacity into subsequent seasons.

That fragility showed up most clearly in tractors, a reliable proxy for farm capex. Industry-wide tractor sales dropped to a multi-decade low in FY2025. According to independent tallies based on Pakistan Automotive Manufacturers Association (PAMA) data, unit sales for the fiscal year fell to roughly 29,000 – lowest in 22 years – with the July–April period already

showing a slide to just over 25,000 units from nearly 40,000 a year earlier.

Add fresh floods in Punjab this monsoon – which battered crops, displaced households and interrupted supply chains – and the case for rapid rural demand normalisation weakens further. The floods caused disruption and the risk of a new food-price spike – both of which typically prompt farmers to triage spending, deferring big-ticket repairs and tyre replacements for tractors until post-harvest cash arrives.

For a tyre maker with meaningful exposure to agricultural segments, that cocktail is toxic in the short run: lower tractor utilisation means fewer tyre changes; lower farmgate realisations and higher input prices squeeze discretionary maintenance; and weather-driven income volatility delays replacement cycles. GTYR’s management all but said as much, linking weak FY2025 volumes explicitly to “poor farm economics” and sketching a replacement-market strategy to smooth the demand curve where possible.

There are, however, faint tailwinds. As global commodity prices eased from recent peaks and domestic inflation cooled, some input-cost stability crept back into the bill of materials, which – coupled with any improvement in agricultural cash flows – could support margins as volumes recover. Management flagged this potential, noting that “economic resurgence and softer commodity prices” offer room for improved profitability once demand returns.

The company’s present-day identity rests on a six-decade lineage. Founded in 1963 at Landhi, Karachi, by General Tire International Corporation (GTIC) of the United States, the business began commercial production in 1964 with a modest capacity of 120,000 tyres a year. It listed in 1982, expanded through the 1980s, and operated for decades under the “General Tyre” brand before rebranding to Ghandhara Tyre & Rubber Company Limited (GTR) in 2021 to signal a broader portfolio and refreshed market presence. Public records and company sources trace that arc, including later European technical associations that strengthened product development.

Today, GTR remains Pakistan’s flagship domestic tyre manufacturer, operating from its original Landhi industrial site with an installed capacity reported in public sources at about two million tyres a year – up from its early-years base via successive debottlenecking and line upgrades. That footprint underpins both its original-equipment (OE) relationships and its national replacement-market distribution.

The shareholder roster and governance have likewise evolved with the rebrand. The company’s investor-relations pages and stock-exchange profile note a diversified register anchored by long-standing sponsors

and institutional investors, with a public float that supports liquidity on the Pakistan Stock Exchange. Recent market data also show the mechanical imprint of a downcycle: gross margin and net margin compressed in FY2025, dividend payout was paused, and earnings volatility reflected the sector’s sensitivity to rural demand and import-cost swings.

GTYR’s portfolio spans the country’s key mobility segments under the “General” brand umbrella:

• Passenger car and SUV/crossover tyres, including high-octane patterns for urban use.

• Light-truck and commercial van tyres, designed for mixed urban-rural duty cycles.

• Truck and bus (T&B) and off-the-road (OTR) tyres, where durability and load ratings dominate purchase decisions.

• Agricultural/tractor tyres, historically a core revenue and margin contributor tied to the farm income cycle.

• Motorcycle and rickshaw tyres, a price-sensitive mass segment with high replacement churn.

The product map and catalogue on the company’s site reflect this breadth and show ongoing pattern refreshes – incremental innovations that matter for wet grip, tread life and rolling resistance in local conditions.

The Landhi plant remains the centre of gravity. Publicly available materials cite installed capacity around two million tyres per annum, achieved in stages via expansion from the original 120,000-tyre line and subsequent debottlenecking. While FY2025 utilisation was pressured by demand, the long-run capacity gives management room to flex output as orders revive – especially if export volumes pick up.

GTYR serves three broad channels: original-equipment manufacturers (OEMs), the replacement market (retail and wholesale), and exports. In a weak OEM cycle – autos as well as tractors – the second and third channels become critical shock absorbers. That is why management is shifting focus to replacement demand and planning to “participate in auto/ tyre exhibitions in different countries” to grow exports. The aim is to diversify revenue, reduce single-segment risk, and capture higher-margin niche orders abroad that value shorter lead times and locally adapted designs.

Tyres are not fast fashion: new patterns and carcass constructions take testing, tooling and time. GTYR was candid in its briefing that new products “are under development,” with a typical cycle of 18–24 months from concept to market. That cadence informs 2026 expectations: any step-change from new launches is more likely to appear late in FY2026 or into FY2027, while near-term growth depends on mix, volumes and export traction.

Rubber and petrochemical derivatives dominate the bill of materials. Management’s

comment about “softer commodity prices” nudging profitability potential is consistent with international price prints across natural rubber and certain synthetics in 2025; if those trends persist, they can widen per-unit contribution even at lower volumes. Conversely, exchange-rate volatility can whipsaw input costs; hedging and inventory discipline remain important to protect margins when the rupee weakens.

Three levers could help GTYR re-rate its earnings profile over the next twelve months. Management’s immediate plan is to push harder in replacement channels – where demand is steadier than OE and pricing can be nimbler – until farm economics normalise. Better retailer availability, promotions timed to harvest cash flows, and targeted SKUs for high-wear applications can all lift volumes without heavy capex.

Well-chosen export orders – especially for niche sizes in T&B or agri segments – can bring higher dollar margins and diversify currency exposure. The commitment to attend tyre and auto exhibitions is a low-risk way to seed that pipeline and test demand in nearby markets where Pakistani tyres already have brand recognition.

If the worst of the 2025 flood damage recedes and policy support for agriculture (credit, inputs, procurement) stabilises cash flows, the tractor-tyre segment should see a pick-up late in FY2026. High-frequency series – PAMA releases and broker tallies – will be the first signal that replacement cycles are restarting. GTYR’s FY2025 performance reads like a classic cyclical downswing: end-market distress, weaker volumes, margin squeeze, and a swing to losses. The remedy is equally classic –focus on replacement demand, broaden export exposure, and keep the product pipeline warm so that, when demand returns, the catalogue is ready. The company’s own briefing notes are clear-eyed about the timeline: new tyres take 18–24 months to develop; FY2026 will therefore depend more on blocking-and-tackling in sales, mix management and cost discipline than on flashy launches.

None of that diminishes the long-run case for a domestic tyre champion. Pakistan’s vehicle parc is large, roads are unforgiving, and replacement cycles are inevitable – even if they stretch in bad years. A manufacturer with scale, distribution and localised patterns should be able to earn decent returns through the cycle. For now, though, investors will want evidence that rural demand is bottoming and that GTYR’s replacement-market pivot is gaining traction. If those signals turn positive while input costs stay benign, FY2026 could look meaningfully better than FY2025 – perhaps not a sprint back to record profits, but a measured jog out of the mud. n

Shell’s exit helps boost reported profits at Wafi Energy

The former Shell subsidiary is now Saudi owned, continues to invest in growth, despite secular headwinds facing oil as a fuel for vehicular energy needs

Wafi Energy Pakistan Ltd (PSX: WAFI) –the company that, until early 2025, traded as Shell Pakistan – has posted a striking rebound in reported profitability even as it navigates the same structural questions facing fuel retailers worldwide: how quickly will electric mobility bite into petrol and diesel demand, and how should a filling-station business invest through that uncertainty?

The headline numbers flatter, but the mechanics matter. In the nine months to September 2025 (9MCY25), the company reported earnings per share (EPS) of Rs14.16, up from Rs3.38 a year earlier; the third quarter alone swung from a loss per share of Rs2.78 in 3QCY24 to EPS of Rs8.19 this year. Net sales rose 7% to Rs343 billion, gross profit jumped 22% to Rs21.8 billion, and EBITDA more than

tripled to Rs9.9 billion.