Thatta Cement wants to assemble Belarussian tractors in Balochistan

Slowly, PSO’s cash flow position is improving

After slowdown in 2025, Airlink gearing up for major expansion in 2026

NEPRA trims K-Electric’s tariffs on lower cost assessments

Can AKD’s Arkadians rise after legal victory?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

BRINGING BIOTECH TO PAKISTAN

FEROZSONS, AND NOW ITS SUBSIDIARY BF BIOSCIENCES, ARE BETTING THAT THE PAKISTANI MARKET IS READY FOR CUTTING EDGE LIFE SCIENCES PRODUCTS. ARE THEY RIGHT?

By Zain Naeem

The hierarchy of innovation in life sciences is clear: innovation happens almost entirely in the United States, the market that allows for the highest prices, and from there migrates first to Europe, Canada, and Japan, and from there on to India, China, and then the rest of the world, if ever it gets that far. Pakistan has historically been very much an “end of the list” market. A product would only ever get to Pakistan long after its patents had expired.

What would it take to get innovation to Pakistan not just during the patent period, but around the same time that the technology is spreading from the United States to Europe and Japan? What would it take to place Pakistan at that second tier of countries?

That is the question Ferozsons has asked itself, and has had some degree of success with as a corporate strategy. The company is one of the fastest growing pharmaceutical companies in Pakistan, and has been able to bring some of the most innovative life sciences products to Pakistan – at price points the Pakistani consumer can afford.

Healthcare in Pakistan tends to be uncomplicated: two thirds of healthcare spending in Pakistan consists of purchasing drugs, and the majority of those tend to be generic medications treating very basic conditions - antibiotics, antiallergens, cough medicine, pain medication, etc.

But Ferozsons has brought leading hepatology drugs to the Pakistani market, including a full cure for hepatitis C, and is now bringing GLP-1 drugs to the market as well.

What gave Ferozsons this ambition? A Harvard-educated CEO certainly helps, though the company has been helped by a market environment where few are willing to take risks, but the most innovative life sciences company are willing to partner with companies in places like Pakistan that are willing to live up to their standards.

But let us start with how Ferozsons began.

Ferozsons and its origins

The story of Ferozsons starts in 1894 before the country came into existence. The lineage of the company traces itself back when Maulvi Ferozuddin Khan set up a publishing house in Lahore which was focused on publishing books and educational materials.

When many try to follow profits, Ferozuddin Khan wanted to serve the under-privileged population of the subcontinent by playing his part in the development of the healthcare and education sectors. This culminated in the pharmaceutical company coming into existence in 1956.

Ferozsons was one of the earliest companies that started to manufacture pharmaceutical products domestically. By 1960, the company had gotten listed on the stock market as well.

The reason behind the success has been the fact that it is the first mover in the sector as it has local knowledge and research while it looks towards local manufacturing ambition. From very early on, there was a focus to carry out manufacturing and get regulatory compliance for the

products that were being produced. As the production started to scale up, there was a need to develop distribution networks that could reach the customers in the most efficient manner. By providing quality products, Ferozsons was able to build a brand around its name.

While Ferozsons was spreading its roots, the biggest opportunity on hand was the fact that the country had been partitioned recently and lacked the foreign reserve or the industrial capability to sustain imports for a long period of time. Locally produced products were able to meet the local demand which allowed for quality healthcare to be provided while not relying on costly and uncertain imports.

Challenges faced by the industry

In usual circumstances, the biggest challenge a private company faces is in terms of competitors who start to enter the market. In this situation as well, many foreign companies started to enter the market and started to make operations difficult. However, the biggest challenge that was faced by Ferozsons was the fact that the government started to tighten its grip on the whole industry.

The problem here is the perception of the medical industry in the country. While in many countries, the pharmaceutical industry is allowed to set their own prices, in Pakistan, this motive is demonized and targeted. The government feels that these companies are providing a public good rather than a consumer good which means that they need to control their prices. Rather than allowing them to make a profit, the government wants to make sure that the prices are not allowed to get out of hand. In order to keep things under control, the prices are mandated by the government.

The first formalization of this policy was back in 1976 when the Drug Act was promulgated under Zulfiqar Ali Bhutto. The tentacles of the disastrous nationalization led to the Drug policy being put into place as well. The intentions of this policy were good. To make sure that patients had access to cheap and affordable drugs which were of high quality. In addition to capping the prices set, there was also a requirement to make sure a part of the profits was put away for research purposes.

This regulation was left lacking as it failed to provide a formula that could be applied in the future where prices could be revised or increased in line with the costs of production. The implementation of this policy meant that the company had no control over its prices and could do little in the way of increasing their margins.

The aftershocks of this policy started to showcase their impact in recent decades when the number of multinationals involved in pharmaceuticals has more than halved from 48 to 22. Companies like Merck Sharp & Dohme, Bristol Myers Squibb, ICI, Roche Pakistan, Merck Group, Eli Lilly and Johnson & Johnson ended up leaving the country never to return.

After passing of the 18th Amendment, the DRAP Act of 2012 was passed which established the Drug Regulatory Authority of Pakistan (DRAP). The role of the regulatory body was to oversee the licensing, approval and pricing

of the pharma industry. There was also going to be a Drug Pricing COmmittee set up by DRAP which would formulate the drug pricing strategy and would recommend prices to be approved by the Federal Cabinet. In essence, the control of the price was still with the regulatory authority. The only opportunity that was being provided was for the drug manufacturer to approach DRAP in order to get an increase in price.

In 2018, this policy was further relaxed to classify drugs into essential and non-essential drugs which had varying price increases which were applicable on them. In 2024, the government finally deregulated all prices for non essential medicines while still holding onto the control for essential medicines.

Ferozsons keeps getting strong

While its competitors fell by the wayside, Ferozsons was able to register phenomenal growth and sustainable profits. The company had felt that they needed to build strategic alliances and carry out contract manufacturing which allowed it to have stable revenues. Having alliances with Boots Pharma-

ceuticals, Grunenthal, Lakeside Laboratories and Procter and Gamble, Ferozsons was able to move into a new avenue available to itself.

The alliances meant that there was technology transfer from the developed brand to Ferozsons allowing for new therapeutic segments to be exploited which was not being considered in the past. Cheaper local manufacturing also opened up the opportunity to export the surplus being produced which benefited both Ferozsons and its international partner. Ferozsons was also able to provide an alternative or substitute therapeutics which was being imported earlier. This also cut down the cost of treatment in the country as well.

By being able to expand into different areas, Ferozsons was providing medicines for cardiology, gastroenterology, oncology and dermatology. The company was also able to establish itself as a mid to large manufacturer having a wide product range and distribution network in place to deliver the products to the market.

Being one of the first movers in the industry, Ferozsons also jumped on the opportunity to be able to enter high impact therapeutic areas which were being neglected before. Cooperating with global innovators, the company was able to develop pharmaceutical solutions

for fields of hepatology, biologics and oncology. Now the company is also moving into endocrinology, child health and diabetes as well.

One such joint venture has taken on a life of its own and is following in the footsteps of Ferozsons.

BF Biosciences

In 2006, BF Biosciences was created as a joint venture between Ferozsons Laboratories and Grupo Empresarial Bagó S.A. of Argentina. Based on the partnership structure, Ferozsons owns 80% while its Argentine counterpart has the remaining 20% of the shareholding. The purpose of this cooperation was to establish a world class biotech plant which would be used to manufacture biologic medicines in Pakistan.

Traditionally, Pakistan’s pharmaceutical industry is dominated by companies focusing on small molecule generics while advanced therapies are mostly imported. This creates a situation where large scale biologics are ignored. BF Bio was going to establish a biotech plant which would rely on large molecule biologic drugs, complex injectables and lyophilised treatments. In order to do so, technology and capital investment is required to carry out sterile large scale manufacturing. By entering such a market, BF

Bio would be able to replace imported medicines while meeting their clients needs.

In order to gauge the demand of the local market, BF Bio initially looked to import finished products from Argentina and then established their own local manufacturing facilities in 2009. Just like Ferozsons before it, BF Bio was going to enter a market of biologics, injectables and advanced therapies which were primarily imported. By stepping into this gap, BF Bio would be able to manufacture high quality products at a lower price.

While BF Bio had the backing of Ferozsons, it still needed expertise and experience in the field. It was able to do so by partnering with Bagó Group which had the technology, expertise and training to impart. BF Bio would be able to fill the gaps that existed in the local market for hepatitis, oncology, kidney disease and diabetes. In addition to that, they would also be able to export their products to other markets after conforming to the international standards and certifications. It is already exporting to Ukraine, Belarus and Indonesia after getting the PICS/S (Pharmaceutical Inspection Co-operation scheme) and SRAs (Stringent Regulatory Authorities) certifications.

The ground breaking success of BF Bio can be seen in the license agreement it signed with Gilead Sciences Inc (USA) which allowed

it to manufacture Remdesivir under Gilead’s Global Patient Solution (GPS) programme. This made BF Bio only one of the 5 companies which were able to secure this license in South Asia. The company also launched its own insulin under the brand name of Ferulin which provides affordable insulin in Pakistan. There has also been a launch of Sematide which is the first locally produced GLP1 in Pakistan. This is the localized version of semaglutide or Ozempic which is the rage all over the world.

From 2006 to 2024, BF Bio was an unlisted company. In 2024, Ferozsons chose to take the company public and instantly the market gave a strong response. The company was looking to carry out an Initial Public Offer of 25 million shares at a floor price of Rs 55. During the book building process, the strike price rose to Rs 77 which was the highest allowed price that the share could have seen causing an increase of 40%. The issue was also oversubscribed by 3.4 times which shows the level of interest in the issue. The value of funds raised came to around Rs 1.93 billion which were going to be used to fund machinery, gain additional certifications and plug any gap in the working capital requirements.

So what do the numbers tell us in relation to its financial performance?

Ferozson’s financial performance

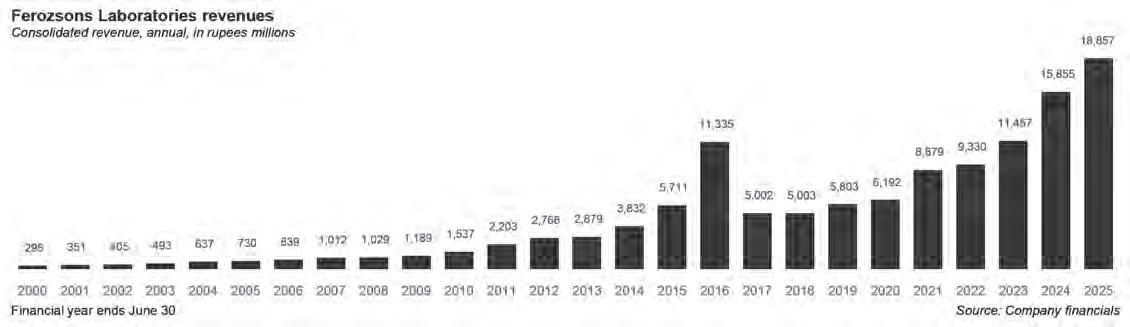

The biggest contributor to the success of Ferozsons is reflected in the net sales of the company which stood at Rs 66 crores in 2005 and clocked in at Rs 13.9 billion in 2025. This shows a constant growth of 16.5% over a period of 20 years. The biggest advantage the company holds over the rest of the industry is that it is providing high impact therapeutics and able to maintain an advantage over its competition. Even when generics enter the market, Ferozsons is able to make sure that the product they provide is of high quality and preferred by patients over the lower quality version.

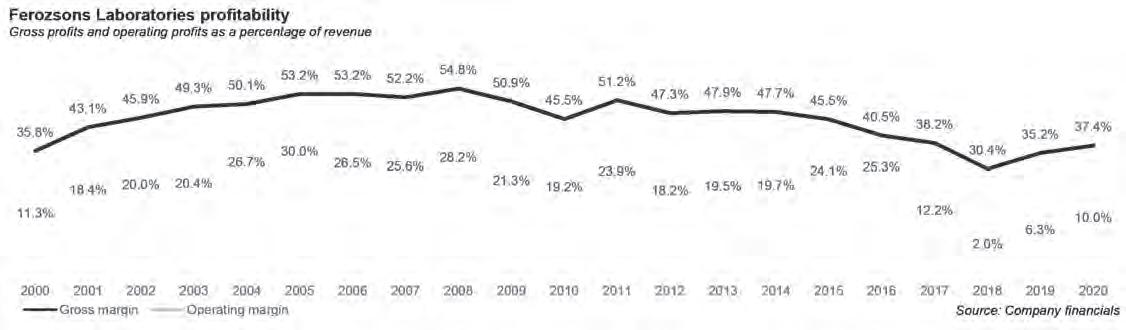

The impact of this can be seen on the gross profit margin earned which stood at 57% in 2005. Over the next 20 years, the margin saw a high of 58% and low of 34% leading to an average of 47% for the whole period. This shows how strong the margins were for Ferozsons in an industry where margins are mandated by price controls and costs out of control of the manufacturer.

Still something that is seen is that gone are the days when the company could consistently earn a gross margin in excess of 50%. Due to constant depreciation in the currency

and the entry of new competition, the gross margin now stands at 40% which was almost 60% in the best of times.

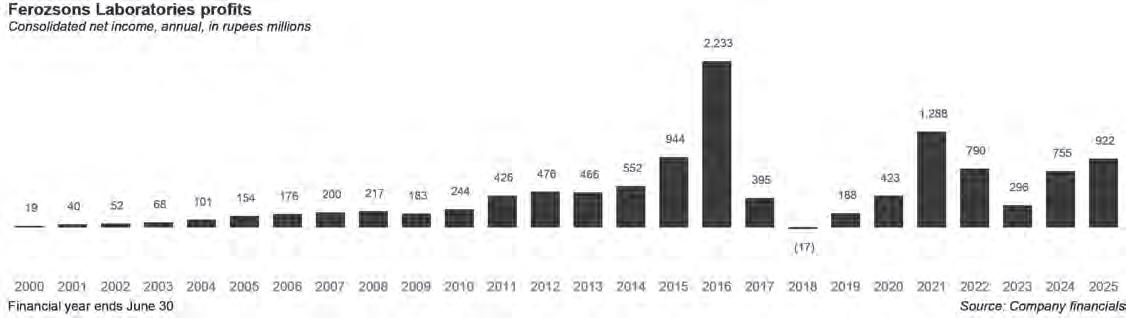

The strength of Ferozsons can be seen from the fact that its unappropriated profits have kept climbing year on year. Going as far back as 2005, the unappropriated profits stood at Rs 31 crores. In a span of 20 years, these profits have increased to Rs 5.9 billion. This is a compound annual growth rate of 16% per year. This figure is on the lower side still as revaluation of fixed assets would further add a value of Rs 3 billion which compliments the profitability at the company.

With administrative and selling expenses remaining relatively constant, the only area of concern was the finance cost which was 0.3% of sales in 2005 and has risen to 4.1% and 3.3% in 2024 and 2025 respectively. The interest rates that were seen in the economy reached an all time high of 22% in June of 2024. This led to the finance cost increasing to such an extent. This was compounded by the fact that the company was relying more on short term borrowings to meet its working capital requirements. In 2005, long term and short term borrowings stood at Rs 2 crores from which 50% was from short term debt. By 2025, short term borrowings had become almost 90% of the total debt taken.

Long term borrowings have the advantage of being cheaper in terms of the interest rate quoted. The downside is that these are not preferred in order to finance any working capital requirements that the company can have. As the revenues of Ferozsons started to increase, the company started to hold more stock in trade which has grown from Rs 10 crores in 2005 to Rs 5 billion in 2025. In addition to that, the trade debt has also increased from Rs 58 lakhs in 2005 to Rs 2.1 billion in 2025. With the short term borrowings, Ferozsons has also used its trade payables to fund some of these requirements as these have increased from Rs 6.6 crores to Rs 2.2 billion from 2005 to 2025.

This seems to be the only Achilles heel for Ferozsons where the cycle starts from borrowing in the short term, buying raw

materials, selling it to its debtors and borrowing more as recovery from customers is slower than expected. This keeps ballooning the short term borrowings further perpetuating the cycle further.

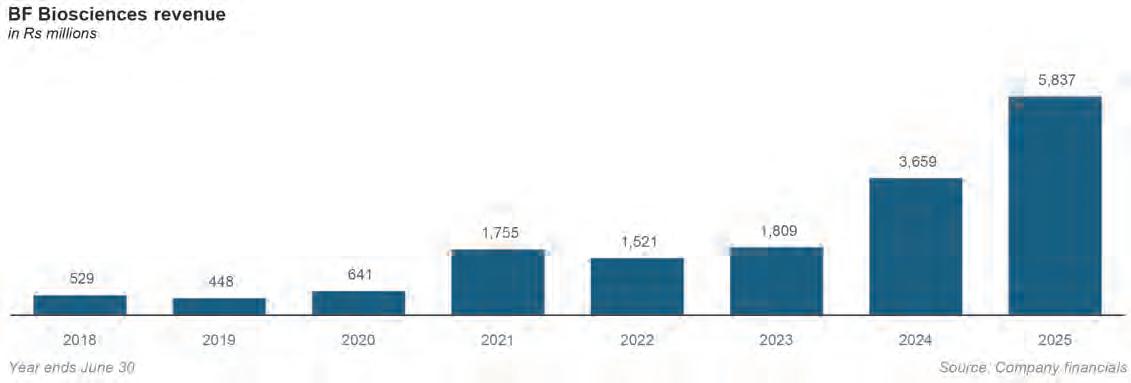

Financial performance of BF Biosciences

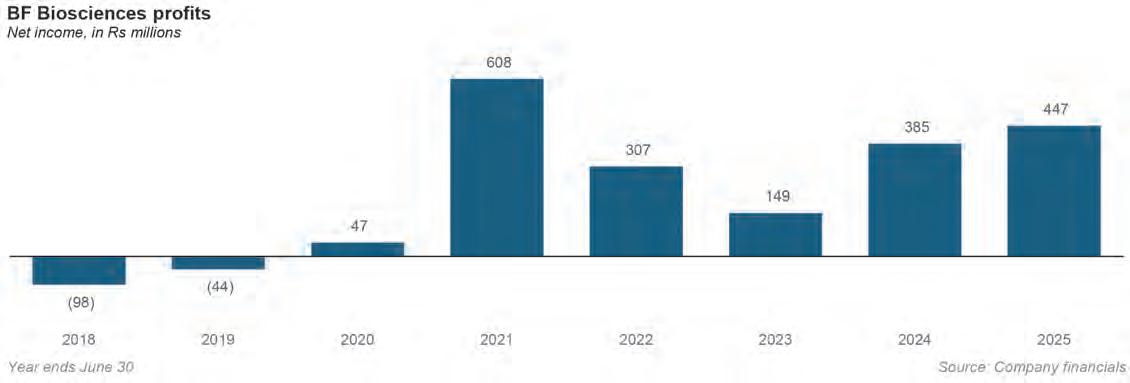

As the listing of BF Bio was quite recent, the financial data available for the company is much more limited compared to Ferozsons. Even for such a young company, it is surprising to see that BF Bio had unappropriated profits of Rs 59 crores on its books in 2018 which have now grown to Rs 2.6 billion by 2025.

The revenues for BF Bio show that the company earned Rs 52 crores in 2018 which rose to Rs 5.8 billion by 2025. In comparison, BF Bio earned nearly half of what its parent company managed in the same year. BF Bio has seen a mixed track record in terms of its profitability as it only saw a gross margin of 0.3% in 2018 which fell to -3.2% in 2019. This fall coincides with the fall that was seen at Ferozsons as well. Both companies seeing falling margins in 2018 and 2019 signal towards the fact that the depreciation of the rupee in 2018 led to increased costs for both companies.

The point of diversion happens after this between the two companies as Ferozsons sees falling gross margin while for BF Bio, the ratio rises to almost 45% in 2021 from -3% in 2019. While Ferozsons faced headwinds in terms of falling margins, BF Bioscience was able to see better profitability and margins which have now settled at around 40% in 2025.

Just like the parent company, the only thing holding back BF Bio to a certain extent is its finance cost which was only 0.15% of sales in 2018 but is now hovering at around 2% of sales. The figure reached a high of 8.5% in 2023, however, as sales increased in 2024 and 2025, this percentage has fallen to a certain extent.

In 2020, the total borrowings of BF Bio were Rs 65 lakhs from which a quarter were

made up of short term debts. By 2025, total borrowings had increased to Rs 1.7 billion which were weighing down the profitability.

The only saving grace for BF Bio was that while almost 90% of borrowing were short term in nature at Ferozsons, BF Bio relied much more heavily on long term loans as they made up 79% of its total debt. Another positive aspect was that most of these long term loans were Temporary Economic Refinance Facility (TERF) loans which had a very low rate of interest. These loans were given during Covid-19 to help the companies invest when economic activity was expected to be muted. By availing these loans, BF Bio was able to lock in a low rate for the long run which was going to keep its interest cost low.

The use of these additional funds can be seen in the stock in trade for BF Bio which was Rs 12 crores in 2018 and has increased to Rs 1.6 billion in 2025. The trade debts have also increased from Rs 5.7 crore to Rs 18 crores from 2018 to 2025 even though the magnitude is much lower. Lastly, the trade payables are used to fund much of the asset increases as they have increased from Rs 15 crores to Rs 1.1 billion from 2018 to 2025.

From the analysis carried out, it can be seen that Ferozsons has looked to not only survive but thrive in an industry where competition is high and the landscape is dynamic in terms of regulations, price controls, exchange rate and competition coming in. Ferozsons has reached on the magic formula to be able to compete in such an industry. Bring in technical know how and expertise with partnerships, develop itself in the local market and look to maintain quality. Even if generics begin to enter the market, keep moving and developing in order to maintain its dominance.

With BF Bio becoming listed, the same formula is being applied where margins are sustaining and profits are becoming a constant at both companies. As long as both these companies stick to this formula, it can be expected that they will keep chipping away in this dog eat dog sector. n

TPL Trakker revenue drops 43% in 2025

As government contract concludes, the company’s revenues have fallen back down to organic levels

TPL Trakker Ltd, the Karachi-based telematics and Internet-of-Things (IoT) company, reported a sharp fall in turnover for the financial year ended June 30, 2025, as the exceptional lift from a major government contract ebbed and the group’s UAE arm stopped being consolidated.

On a consolidated basis, TPL Trakker posted turnover of Rs1.83 billion in FY2025, down from Rs3.21 billion a year earlier – a decline of about 43%. Cost of sales and services reduced alongside, yielding a gross profit of Rs703 million versus Rs1.41 billion in FY2024. The statement of profit or loss shows operating profit of Rs185 million, with finance costs of Rs343 million, and other income of Rs480 million. After taxes and discontinued operations, total comprehensive loss narrowed dramatically to Rs7.7 million, with profit attributable to owners of the holding company of Rs13.7 million and EPS of Rs0.07, compared with Rs0.03 last year.

Management had telegraphed the coming reset in its March-quarter directors’ report, noting that nine-month consolidated revenue had already fallen as a major Customs contract drew to a close and the Middle East arm moved out of line-by-line consolidation. The company wrote: “This decrease is primarily due to the conclusion of the Safe Transport Environment (STE) project with Pakistan Customs / Federal Board of Revenue (FBR),

which ended December 31, 2024, as well as the elimination of Trakker Middle East’s revenue from the consolidation following the change in its classification from a subsidiary to an associated company.”

That shift matters for optics as well as operations. The STE programme, awarded in 2022 for a three-year term, had broadened TPL Trakker’s licensed scope from Afghan Transit alone to all bonded cargo movements – a change that materially expanded the serviceable market while it lasted. With its expiry at end-December 2024, the company’s FY2025 second-half run-rate reverted to what management calls “organic” commercial activity in core telematics, fleet and location-based services (LBS).

The reported numbers therefore juxtapose a high STE-inflated base in FY2024 against a normalised FY2025, and they exclude Trakker Middle East’s (TME) top line after that business was reclassified as an associate during FY2025 following a fresh equity injection by Dubai-based Gargash Group. Management says the partnership is intended to drive deeper market penetration across the Gulf, but the accounting change naturally pulled TME’s revenue out of TPL Trakker’s consolidated top line.

For investors, the immediate readthrough is that FY2025 marks a trough year in reported revenue rather than a collapse in the company’s addressable demand. The consolidated statement shows the company still pro-

ducing operating profit and positive earnings attributable to the holding company, helped by other income and tighter cost control through the year.

To understand the scale of last year’s base effect, one needs to understand the STE programme itself. The Safe Transport Environment (STE) project is an FBR-led initiative for real-time tracking and monitoring of bonded and transit cargo, conceived to reduce pilferage, curb smuggling, and ensure that duty-suspended consignments move only along authorised routes and reach declared destinations on time. The concept dates back more than a decade: discussions in Customs circles began after repeated audit observations on cargo losses, and an FBR conference in 2007 decided to initiate the technology-enabled tracking regime. A formal expression of interest followed in 2011.

In June 2022 the FBR granted TPL Trakker a three-year licence for the STE project. Crucially, the scope was enhanced from Afghan Transit to the entire spectrum of bonded cargo transportation, including inter-port movement, dry-port transhipments, and both forward and retro cargo on Afghan routes. That single regulatory expansion materially lifted TPL Trakker’s potential volumes under STE.

The mechanics are straightforward: containers and bonded carriers are fitted with tracking devices and e-seals, movements are monitored in near real-time in an FBR control room, and exceptions trigger field interven-

tions. Over time, Customs has complemented these measures with scanning at entry and destination points and has discussed competitive re-tendering to keep vendors current on GSM and satellite technologies. Those moving pieces are why STE volumes – and, therefore, tracking revenues – can be sensitive to policy changes and re-licensing cycles.

During FY2024, STE revenue was further buoyed as the government stepped up enforcement and expanded the practical footprint of tracked flows. Earlier company briefings highlighted that transhipment cargo was made operational under the licence, while rate adjustments were allowed for certain categories to reflect added e-seal security – both of which supported topline. All of that makes the December 2024 end-date pivotal for understanding FY2025’s reported decline.

A separate thread to watch is that Pakistan’s broader tax-technology agenda is still advancing. The World Bank in mid-2025 approved additional financing for the Pakistan Raises Revenue programme supporting FBR’s ICT upgrade, even as some deliverables like track-and-trace targets have lagged. Any successor cargo-tracking framework that emerges from this policy churn could again shape the revenue cadence for private tracking providers.

TPL Trakker’s story predates the current IoT buzzwords. The company traces its roots to 1999, when it became the first firm in Pakistan to secure a vehicle-tracking licence. It listed on the Pakistan Stock Exchange in 2012 (then as TPL Trakker Limited, before a group-level reorganisation created TPL Corp as the investment holding company). Over two decades, the business has grown from vehicle recovery to a broad suite of telematics, mapping and location-data services for consumers, corporates and public-sector clients.

Within Pakistan, TPL Trakker positions itself as a leading telematics and IoT provider, leveraging an in-house mapping stack built under the TPL Maps brand – a platform licensed by the Survey of Pakistan that offers APIs for navigation, geocoding, routing and analytics. That location-data capability underpins many of the company’s enterprise solutions and differentiates it from pure hardware vendors.

Internationally, the group established Trakker Middle East (TME) as early as 2006, a presence that was reshaped in FY2025 via the investment by Gargash Group and the resulting reclassification to an associate. Management says the regional alliance is aimed at pooling TME’s sector know-how with Gargash’s reach and financial capacity to pursue GCC opportunities – again a strategic logic that lives outside the FY2025 top-line, given the equity-accounting treatment.

While the STE contract amplified revenues in the last cycle, commercial telematics and mapping remain TPL Trakker’s core fran-

chise. On the B2C side, the company markets vehicle, bike and personal tracking solutions with theft-recovery assistance and app-based features. On the B2B side, it offers fleet management (vehicle health, driver scoring, route optimisation, geofencing and analytics), fuel monitoring for vehicles and generators, and AI-enabled video telematics for driver safety and incident forensics.

The company has also pushed into industry-specific IoT verticals:

• Cold-chain monitoring (temperature-controlled logistics for food and pharma),

• Smart farm systems (soil moisture, irrigation and asset tracking),

• Water-level monitoring (for utilities and municipalities), and

• Waste-management and municipal fleet solutions (including recent deployments with public-sector entities).

Under the TPL Maps/LBS umbrella, the company provides location-based services via APIs – routing, distance matrices, place search and more – used by ride-hailing, logistics and e-commerce players. Partnerships in recent years have integrated TPL Maps into third-party apps to improve localisation accuracy, a key selling point against generic global datasets.

Management commentary around the March quarter emphasised three growth levers for the post-STE era:

1. Core telematics – expanding corporate fleets with bespoke dashboards and analytics;

2. Industrial IoT – scaling solutions that deliver measurable fuel, safety and productivity gains; and

3. Digital mapping/LBS – monetising APIs and data services across finance, logistics and consumer apps. The directors’ report also noted a QoQ uptick in telematics volumes in Q3 FY2025 within the B2C segment, alongside active business development in LBS.

TPL Trakker is part of TPL Corp, a holding company whose portfolio spans general and life insurance, real estate development and REIT management, security services, asset tracking, geospatial technology and venture capital. TPL Corp itself evolved from the original tracking business and was rebranded as the group’s investment arm in 2017; it remains the parent of TPL Trakker and other operating companies. Credit-rating agency profiles and corporate materials describe the group’s strategic intent as building technology-enabled platforms around mobility, risk and property – with Trakker providing the data and infrastructure layer for many cross-company offerings.

That group architecture has two practical implications for Trakker’s outlook. First, distribution synergies: insurance, security and property businesses provide captive channels for telematics and LBS, and vice-versa. Second,

capital allocation: the holding structure allows TPL Corp to deploy growth capital across its portfolio as market windows open – as seen with the TME partnership – without necessarily consolidating all revenue at Trakker in perpetuity.

Set against those strategic contours, FY2025’s financials look less like retreat and more like normalisation after an extraordinary contract cycle. The company’s Rs1.83 billion top line now represents primarily commercial telematics and mapping revenues in Pakistan, plus equity-accounted contributions from the UAE. The income statement shows that, even with a smaller revenue base, the business generated operating profit, while finance costs (a sector-wide headwind in Pakistan’s highrate environment) continued to weigh on the bottom line. Nevertheless, EPS improved to Rs0.07, reflecting lower losses from continuing operations and a swing in other comprehensive income.

Investors will naturally ask what replaces STE’s volume and whether a successor Customs tracking regime could re-open that spigot. On the policy side, FBR has been signalling upgrades to cargo-tracking rules and fresh competitive tendering, while pursuing parallel digitisation efforts (such as the trackand-trace programme for excisable goods). Any new framework could see TPL Trakker compete again, but timelines and commercial contours remain policy-dependent.

In the interim, the operational plan is to lean into core telematics growth – expanding the enterprise fleet base and upselling analytics – and to monetise LBS more deeply via APIs and industry partnerships. The company argues this mix is structurally healthier: diversified across customer verticals, less exposed to policy swings, and rooted in proprietary location data rather than commoditised hardware. Management’s March note underlined precisely that pivot, highlighting progress in onboarding enterprise clients in FMCG and banking, and a stronger B2C trajectory after a soft patch in the automotive sector.

TPL Trakker’s FY2025 is a reset year. The 43% fall in revenue is real, but it is also mechanical, reflecting the expiry of a timebound government licence and an accounting reclassification of the UAE arm. Underneath, a leaner, more diversified commercial engine is visible: profitable operations before financing, a larger suite of industry IoT offerings, and a proprietary maps platform that gives the company a differentiated role in Pakistan’s digital infrastructure. If policy winds deliver a new cargo-tracking regime, that would be upside; if not, the company’s challenge is to scale the B2B telematics and LBS engines fast enough to outgrow a heavy FY2024 base – and keep finance costs in check while doing so. n

Thatta Cement wants to assemble Belarusian tractors in Balochistan

The cement manufacturer has announced the creation of a subsidiary that will assemble tractors in collaboration with Minsk Tractor Works

Thatta Cement Company Ltd has unveiled plans to diversify far beyond clinker and bagged cement: its newly created, wholly owned subsidiary, Minsk Work Tractor & Assembling (Pvt) Ltd (MWTA), has signed an exclusive agreement with Minsk Tractor Works of Belarus to assemble and locally produce BELARUS-brand tractors in Balochistan. The company disclosed the development to the Pakistan Stock Exchange (PSX), stating that MWTA has been granted the exclusive right to assemble BELARUS tractors in Balochistan and that the project aims to promote industrial development, job creation and technology transfer by establishing a local assembly facility in the province.

Corporate diversification is hardly unusual in Pakistan, but a cement producer venturing into tractor assembly raised eyebrows for the scale of the leap and for its geopolitical overtones. Thatta Cement’s notice frames the deal as a long-term strategic step to “diversify the Thatta Cement Group’s business portfolio.” It also positions the planned assembly line as a development catalyst for Balochistan, where industrial ventures outside mining have historically been sparse. Under the agreement, Thatta’s MWTA subsidiary will work with Minsk Tractor Works (MTZ) to assemble the BELARUS range locally, with the Belarussian

manufacturer conferring exclusivity in the province.

The initiative lands at a time when Pakistan’s farm mechanisation cycle has been whipsawed by weather, credit and policy shifts, yet demand for tractors remains structurally tied to the country’s agricultural base. Provincial subsidy programmes – notably the Punjab Green Tractor Scheme – have periodically spurred volumes, most recently by offering large per-tractor subsidies for 50–85 horsepower units, a bracket that captures mainstream farm demand.

From Thatta’s standpoint, the logic is twofold. First, to tap an end market decoupled from Pakistan’s volatile construction cycle; second, to enter an arena where a global brand partner can provide product, parts and know-how. For investors, however, the surprise is real: Thatta is not currently known for heavy-equipment assembly, and the tractor segment is dominated by two entrenched players – Millat Tractors (licensee of Massey Ferguson) and Al-Ghazi Tractors (licensee of New Holland) – that enjoy deep vendor bases, installed fleets and service networks. Even so, demand spikes in 2024–25 amid subsidy deliveries showed that volumes are responsive to policy support, suggesting headroom for a third player if it can carve out a niche on price, ruggedness or regional reach.

Thatta Cement was incorporated in 1980 as a public limited company and began operating its plant in 1982 on dry-process technology. For years it was part of the state-owned cement network, a wholly owned subsidiary of the State Cement Corporation of Pakistan, until the federal government privatised the company in February 2004. The company later obtained a stock-market listing and remains focused on the production and marketing of cement products.

The company’s manufacturing facility is located on Ghulamullah Road, Makli, District Thatta, Sindh, and sits on a sizeable land bank for quarrying and plant operations. Over time, Thatta has made process improvements to lift output at the Makli plant and has reported capacity enhancements, including in-house modifications undertaken in 2021 to raise clinker and cement capacities. The product slate covers Ordinary Portland Cement (OPC), Sulphate Resistant Cement (SRC) and slagbased blends for specialised applications such as marine works and piling.

Ownership of Thatta has evolved since privatisation, with well-known market participants at various points associated with the shareholding. But the company’s public disclosures and sector coverage consistently define it as a Sindh-based mid-tier producer with a regional sales footprint and a reputation

for SRC in saline and coastal environments. It is against this backdrop – a focused, regionally anchored cement manufacturer – that the tractor announcement looks unexpected, and therefore strategically bold.

Founded on 29 May 1946 in Minsk, Minsk Tractor Works (MTZ) is among the world’s largest manufacturers of agricultural equipment. Over its history, MTZ and its BELARUS brand have produced more than 3 million tractors, exporting to over 100 countries, and today offer a wide catalogue of models and configurations adapted to diverse climates and operating conditions. In recent years MTZ has continued to update its product range, including higher-horsepower models, while pursuing export markets through distributors and assembly partners.

The BELARUS marque is well-known across the former Soviet space and in developing markets for rugged design, relatively simple mechanics and affordability – attributes that appeal to farmers looking for robust machines that are easier to maintain outside sophisticated dealership networks. MTZ’s global sales channels have included North America, where distribution for compliant models was re-established through a dedicated distributor, as well as Asia, Africa and Latin America. For Pakistan, MTZ has a long if episodic brand presence: BELARUS tractors have been imported in the past, competing primarily on price-per-horsepower against entrenched local brands.

Pakistan’s tractor industry is dominated by two incumbents: Millat Tractors (Massey Ferguson) and Al-Ghazi Tractors (New Holland). Their combined share typically accounts for the vast majority of domestic sales, supported by deeply localised vendors, long-running assembly operations and extensive service networks. Al-Ghazi, for instance, positions itself as the second-largest player with a market share in the mid-30s, while Millat is usually the segment leader. Both are listed companies with visible financials and frequent disclosures.

Demand is cyclical but policy-sensitive. Province-level subsidy programmes can swing monthly volumes sharply. In December 2024, as the Punjab Green Tractor Scheme deliveries took place, industry sales reportedly surged to around 7,030 units for the month, with Millat selling 4,686 units – its highest monthly tally in nearly seven years. Government portals and departmental notices outline generous per-tractor subsidies aimed at accelerating mechanisation, with eligibility bands set by farm size and power rating, and programme portals now publishing balloting updates for successive phases. These interventions underscore how tractor sales can spike when subsidies are available and credit is accessible. Even outside subsidy waves, secular

drivers exist. Mechanised land preparation and post-harvest operations, the need to cover larger acreages amid labour constraints, and aspirations to improve yields all underpin a structural case for tractors. Conversely, taxes, interest rates and supply chain disruptions can depress volumes. News reports through 2024 showed both sharp year-on-year falls in select months and strong rebounds when policy tailwinds returned, illustrating how volatile headline numbers can mask an underlying installed-base replacement cycle.

Where does Thatta fit? As a potential third assembler with a Belarussian partner, Thatta may try to compete on a mix of price, durability and regional presence. BELARUS tractors have a reputation for ruggedness and low-frills serviceability – traits that could resonate with buyers seeking value or operating in harsher terrain. Locating assembly in Balochistan may also open logistical advantages for serving customers across the province and neighbouring regions, while the exclusivity granted to MWTA in Balochistan protects local investment in networks and spares. The harder task will be building a vendor base, financing channels, after-sales support and resale confidence to chip away at incumbents’ dominance. The PSX notice suggests Thatta and MTZ see technology transfer as integral to the project, a necessary foundation for scale.

The partnership inevitably carries geopolitical baggage. Belarus is a close ally of Russia and allowed Russian forces to stage parts of the February 2022 invasion of Ukraine from its territory. Western responses have included rounds of sanctions targeting Belarussian entities and sectors, with periodic updates and guidance – not least the European Union’s clarification of “best efforts” obligations on EU operators to prevent sanctions circumvention via overseas subsidiaries. Although some specific measures have been tweaked over time, the sanctions environment remains a moving target, and reputational considerations linger wherever Belarus-linked projects are concerned.

For Pakistan, the sensitivities are heightened by long-standing defence ties with Ukraine. Islamabad acquired 320 T-80UD tanks from Ukraine between 1997 and 2002, and Pakistan’s Al-Khalid main battle tank uses Ukrainian KMDB 6TD-2 engines. Ukrainian state defence firms have, at various points, secured support and maintenance contracts for Pakistan’s armoured fleet. These linkages have persisted through a turbulent geopolitical period and remain a substantive strand in Pakistan–Ukraine relations.

Bringing a Belarussian OEM into Pakistan’s civilian industrial landscape does not, in itself, breach any rule; automotive machinery is distinct from armaments, and Thatta’s PSX

notice concerns agricultural tractors. But the optics are complex: Belarus’ alignment with Russia in the Ukraine war and its sanction exposure could raise due-diligence expectations among banks, insurers and international suppliers. It could also invite scrutiny from counterparties with EU or UK touchpoints, who must evidence “best efforts” to ensure they do not facilitate sanction circumvention – particularly relevant if any components, software or financing streams intersect with jurisdictions observing Russia/Belarus measures.

At the same time, Belarus has signalled intermittent openings to the West, and global reporting in 2025 has chronicled limited sanction adjustments alongside prisoner releases and diplomatic overtures, even as most core restrictions and political concerns remain in place. None of this resolves the underlying tension: Belarus is still widely seen as a co-belligerent in the conflict’s early phases, and its leadership openly defends its support to Moscow. For a Pakistani project, the practical takeaway is not to avoid engagement per se, but to design compliance into the venture –from supplier vetting and banking channels to export control checks if any kits or components touch sensitive lists.

Pakistan has seen sector-hopping before – from energy groups moving into auto assembly to textile firms investing in power – usually justified by currency hedges, import substitution, or a search for steadier cash flows. Thatta’s planned tractor venture sits in that tradition of portfolio diversification, but it is also a test of execution in a market with formidable incumbents.

Critically, the partnership structure matters. MTZ brings brand equity, a wide product catalogue and export experience; Thatta brings a public-company platform, local governance, and a stated commitment to technology transfer in Balochistan. If the parties can establish reliable localisation, affordable financing and credible after-sales, the BELARUS badge could find a durable niche, especially in districts where ruggedness trumps frills and where price-per-horsepower can pry buyers from entrenched loyalties. Conversely, if compliance frictions or supply bottlenecks slow kit flows, the venture may face a longer, costlier journey to relevance.

For now, the market will focus on milestones: site selection and regulatory clearances in Balochistan; the assembly model and initial localisation plan; dealer and service appointments; homologation and testing timelines; and any early orders tied to provincial schemes. The PSX notice sets the tone – exclusivity in Balochistan and a development pitch centred on jobs and technology transfer – but leaves room for detail that investors will want to see in the quarters ahead. n

Slowly, PSO’s cash flow position is improving

The company has been able to pay down its dollar-denominated debt, and expects a decline in receivables following government efforts to resolve circular debt

Pakistan State Oil (PSO), the country’s largest oil marketing company, is crawling out of the liquidity squeeze that has dogged it for years. Management briefings around the company’s annual general meeting point to tangible improvements: foreign-currency borrowings are being pared down, policy changes are reducing the build-up of receivables tied to gas allocations, and a long-awaited government plan to cut the energy sector’s circular debt is finally on the table. While none of these shifts is a silver bullet, together they mark the first sustained easing in the company’s cash flow pressures in years.

The clearest headline is debt. PSO’s foreign loans have fallen from about $1.3 billion to $900 million, with management aiming to trim a further $300 million by year-end. For a balance sheet exposed to dollar swings and import-linked working capital, cutting hard-currency leverage is the fastest way to steady cash flows and reduce finance costs. It is also a confidence signal to banks and suppliers that PSO can fund cargoes without leaning as heavily on expensive external lines.

A second relief valve is the sharp fall in receivables linked to the diversion of imported re-gasified liquefied natural gas (RLNG) to domestic users. In earlier years, this diversion piled up unpaid bills at PSO because the end customers were not on cost-reflective tariffs, and the arrears often sat with the gas utilities. Management now reports that the value of these diversions has declined from roughly Rs200 billion to around Rs80 billion, as the government has nudged prices and tariffs closer to economic levels and strengthened recoveries at the Sui companies. Fewer subsidised diversions mean fewer IOUs parked on PSO’s books – a direct

cash flow win.

Third, there is the circular debt reduction plan. Islamabad has signed off on a Rs1.2–1.3 trillion package aimed at unwinding payables and receivables across the power and gas chains. The specifics of how much lands in PSO’s account, and when, are still being worked through. But even an incremental release of cash would shorten PSO’s cash conversion cycle and reduce the need for costly short-term borrowing to bridge timing gaps between fuel imports and customer payments.

PSO is also making operational moves to support liquidity. It is optimising the use of pipelines to cut logistics costs, expanding its retail footprint in regions where its share has slipped, and seeking approval to set up a trading subsidiary to enhance procurement flexibility. Lower unit costs, more predictable product flows, and a broader retail base all help the company defend volumes and margins without resorting to aggressive discounting that would sap cash.

Finally, there are income line items that matter for working capital. Management underscored that line-fill income – the return PSO earns on the inventory volumes required to operate pipelines – is a recurring feature tied to interest rates and working capital deployment, not a one-off windfall. Properly managed, those inflows can cushion quarter-to-quarter swings in cash outlays for product.

Put together – lower dollar debt, smaller RLNG receivables, a pending government paydown, and operational tweaks – PSO’s liquidity picture looks measurably better than a year ago. The path is not linear, and tax and margin questions still hover, but the direction is finally favourable.

To understand why the company’s cash

has been so tight, it helps to revisit circular debt – the knot of unpaid bills that forms when energy tariffs do not fully cover costs, technical and commercial losses are high, and subsidies are delayed or under-funded. In power, this manifests as distribution companies falling behind on payments to generators, who then struggle to pay fuel suppliers. In gas, non-cost-reflective prices for domestic users and leakages at utilities translate into sizeable receivables. PSO sits at the front end of the chain, importing fuels and LNG that the rest of the system consumes – and then waiting to be paid.

Two features have been particularly damaging for PSO’s cash cycle:

• RLNG diversion to households. When imported LNG earmarked for industry or power is diverted to domestic consumers at controlled prices, there is often a gap between the cash PSO must pay suppliers and the receipts that the gas companies collect from users. That receivable lands on PSO’s balance sheet and can linger. The recent shrinkage of these diversions, thanks to tariff moves and new connections that improve utility recoveries, directly reduces this drag.

• Delays and disputes in systemic settlements. Even when the federal government decides to inject cash to reduce circular debt, timing and allocation can be uncertain. PSO’s management notes the circular debt reduction plan is approved, but the share and schedule of funds earmarked for PSO remain unclear. That uncertainty forces the company to maintain higher working capital buffers than it otherwise would.

While these are structural issues, the current policy mix – tariff rationalisation, a serious reduction plan, and closer attention to recoveries – suggests PSO’s receivables should trend down, or at least rise at a slower pace than in the past. The company’s own pace of deleveraging will

then amplify the improvement in net cash flows.

Founded in the mid-1970s through the consolidation of several marketers, PSO evolved into Pakistan’s dominant downstream player, with the largest storage footprint, the broadest retail network, and the lead role in importing critical fuels – including Mogas, High Speed Diesel and furnace oil – whenever local refinery output falls short. Decades of investment in depots, pipelines, and coastal terminals have made PSO the system integrator of Pakistan’s liquid-fuels market.

That centrality cuts both ways. In good times, scale brings bargaining power with suppliers, lower per-unit logistics costs, and the ability to ensure national supply even when global markets are tight. In stress scenarios, the obligation to keep product flowing – often on terms dictated by policy, not pure commercial logic – heaps the financing burden on PSO’s balance sheet. The company’s market share reflects these cross-currents: management disclosed that PSO’s white-oil share (primarily petrol and diesel) fell to 45% in FY25 from 51–52% the year before as rivals courted dealers with discounts. Regaining share without destroying margins is the tightrope PSO must walk.

Another structural feature is taxation. Management pegs the effective corporate tax rate near 42%, a blend of base corporate tax, super tax, and a flat tax on LNG. High effective taxation reduces retained earnings and narrows the room to self-fund capex or working capital, making deleveraging even more important for financial flexibility.

While PSO is not itself a refinery operator, the quality and quantity of local output directly affect its import bill, exposure to international premiums, and working capital needs. Management points to Pakistan’s Greenfield and Brownfield refinery policies, under which upgrading existing plants and adding new capacity could save between $1.6–2.0 billion a year in foreign exchange currently paid as premiums to international traders. Those premiums reflect the cost of sourcing compliant fuels from abroad, including product-quality differentials and the convenience premium that traders charge to place cargoes in a market with tight storage windows and lumpy demand.

Refinery upgrades matter for three reasons:

• Product mix and quality. Upgrading to deeper conversion and better desulphurisation lifts the yield of Euro-grade petrol and diesel and cuts high-sulphur residual output. More compliant barrels produced domestically reduce the need to import high-spec product. That translates to fewer letters of credit outstanding at any point in time, and less exposure to volatile spot premiums – a cash flow smoother for PSO.

• Scheduling and logistics. When domestic refineries can match more of the market’s seasonal

demand, PSO can plan imports more evenly, lowering demurrage risks and pipeline bottlenecks. Better synchronisation reduces the costly “peaks and troughs” of inventory financing. • FX and credit. Fewer imports directly reduce foreign-currency drawdowns and the reliance on external trade finance, a relief when dollars are dear. For PSO, which has worked hard to cut foreign-currency debt, any structural reduction in FX needs helps consolidate that progress.

The policy test is execution: upgrades take time, and the incentive framework must be credible enough for refineries to finance projects at scale. But the strategic direction – more domestic compliance barrels, fewer imported cargos on tight timelines – is unambiguously positive for PSO’s cash conversion.

PSO competes in a market where dealer and company margins are regulated, but where pricing tactics can still swing share. Over the past year, a price war has featured discounts of up to Rs8 per litre offered by some oil marketing companies to dealers or large customers. The government has taken note, and a long-pending revision of OMC margins – which industry argues is overdue to reflect costs – has been sent back for reassessment precisely because widespread discounting muddies the picture of what a “sufficient” margin really is. If marketers can give away Rs8 per litre, policymakers ask, are margins in fact too high already?

For PSO, there are three implications: • Market share vs cash discipline. Chasing every litre via discounts is tempting when share has slipped – management acknowledges the fall to 45% in white oils – but it burns cash and cheapens the brand. PSO’s stated response is more targeted: expand retail in under-penetrated regions, squeeze logistics by maximising pipeline utilisation, and bring more trading flexibility into procurement once approvals for a subsidiary are in hand. That is a slower but healthier route back to share.

• Working capital strain. Discounting can lengthen receivable cycles and compress cash inflows just as import payments fall due. In a high-rate environment, that is doubly painful. By leaning on operational efficiencies rather than blanket discounts, PSO can protect cash without abandoning the field.

• Margin reset risk. If the official OMC margin is adjusted without a clean view of cost realities, the industry could face a margin that is too low to cover legitimate expenses, entrenching discount wars as companies try to compensate via volume. PSO’s sheer scale gives it some resilience, but sustained under-recovery would still bleed cash.

The company must also manage policy frictions that can add costs or uncertainty to imports. One example is the Sindh Infrastructure Development Cess (SIDC) on petroleum imports. Bank guarantees were mandated in

September 2021, but the war-related shock to trade finance complicated compliance. In RLNG, the cess has been passed through to consumers; for liquid fuels, the federal and provincial authorities are still shaping a practical regime. Management expects the cess will continue to be passed on, but clarity matters for pricing and working-capital planning.

Even as cash generation improves, the tax take is heavy. With an effective corporate tax rate around 42%, PSO faces a meaningful drag on after-tax cash flows. LNG, a core part of its portfolio, also carries a flat tax, reducing the net cash available to accelerate deleveraging or to invest in network upgrades. The company can mitigate this with cost cuts and better inventory turns, but the tax burden is a structural headwind that only policy can ease.

Three markers will decide whether PSO’s liquidity keeps improving:

1. Delivery on debt reduction. The plan to bring foreign debt down by a further $300 million is concrete and measurable. Hitting it would meaningfully reduce FX and interest exposure.

2. Receivables trajectory. The RLNG receivable improvement is already visible; the circular debt release is the swing factor. Even partial, predictable inflows will shorten PSO’s cash conversion cycle.

3. Retail sanity. If the price war abates and the margin policy is settled on cost-reflective grounds, PSO can focus on network depth, service quality and logistics – areas where it holds natural advantages – rather than on giveaways that corrode cash.

None of this downplays the challenges. Global oil prices are volatile, exchange control constraints can return, and local demand can soften if economic growth stalls. But the trend lines inside PSO’s control – debt, receivables tied to policy distortions, and operating efficiency – are finally pointing the right way. If refinery upgrades proceed under credible incentives, even the imported-premium penalty that has long haunted PSO’s working capital could begin to shrink.

PSO’s cash flow story has been a long grind of import now, get paid later. In the past year, the pieces have started to shift: a lighter dollar debt load, smaller RLNG-related receivables, a signed national plan to chip away at circular debt, and a deliberate pivot to operational efficiency rather than blanket discounting. Taxes remain high and retail competition is still fierce under regulated margins, but the company’s position is materially better than it was. What investors will look for now is follow-through: fewer dollars owed, fewer rupees stuck, and a retail playbook that wins share without torching cash. If that happens, “slowly improving” could turn into a sturdier, more durable cash flow recovery.

After slowdown in 2025, Airlink gearing up for major expansion in 2026

The electronics assembly company will begin production on its Acer laptop facility, expand is domestic cellphone assembly, and begin shipping television sets as well

Air Link Communication Ltd (Airlink) is preparing for a year of expansion after a softer patch in 2025. Management briefings with analysts indicate the company plans to step up output in mobile phones, switch on its new laptop assembly line for Acer-branded devices, and begin commercial shipments of television sets, even as it courts global partners for a broader push into white goods. The pivot comes as Pakistan’s import regime normalises and as taxes and finance costs start to ease from last year’s peak – conditions that had pinched the top line in 2025 but have begun to turn in the company’s favour in early 2026.

Airlink’s financial year to June 30, 2025, showed a visible slowdown in revenue versus 2024. Consolidated net sales fell to about Rs104.0 billion in FY2025, down 20% from Rs129.7 billion in FY2024, according to analyst briefing tables shared after the October corporate call. Yet profit after tax still edged up to Rs4.7 billion, with EPS at Rs12.0 versus Rs11.7 the year before, helped by a stronger gross margin and operating leverage.

The softer FY2025 revenue print contrasts with a sharp year-on-year rebound in the first quarter of FY2026. For 1QFY2026, Airlink reported sales of Rs24.4 billion, up 11% YoY, and profit after tax of Rs1.58 billion (EPS Rs4.01), which is 88% higher than the same quarter last year. Management added that sales were held back by the September floods; absent that disruption, they estimate the quarter could have reached about Rs30.0 billion in

revenue. They now expect Rs30.0–35.0 billion of sales per quarter for the remaining quarters of FY2026, implying a much brisker run rate than the FY2025 average.

The profit cadence also reflects an improving gross margin profile. The briefing pack shows margin expansion in FY2025 to about 11% versus 7% in FY2024; in 1QFY2026, gross margin further improved to around 14%, supported by a better product mix and negotiations with principals that lowered costs. Operating profit rose accordingly, with 1QFY2026 operating profit of Rs3.0 billion, up 69% YoY, even as finance costs remained elevated.

Management acknowledged that finance costs are still sizeable despite the policy-rate downtrend, because working capital expanded to feed growth. They described the higher borrowing as a “sponsored cost” that is largely passed through in pricing, a stance made easier by a product mix skewing to higher-value devices.

The principal drag on FY2025 revenue was policy-driven, not structural demand. Throughout the year, Pakistan’s electronics industry wrestled with import controls, intermittent LC restrictions, and higher taxes and duties, which constrained the availability of key components and delayed product launches. In that environment, volumes suffered and channel inventories were kept lean, limiting top-line throughput even as the company preserved profitability via tighter costs and an improving mix.

Airlink’s management told analysts that a relaxation in these constraints is already

feeding through to sales. The company’s Sundar Industrial Estate project – a designated 10-year tax-free zone – should further blunt the tax headwinds as production shifts to that site. The plan is to keep mobile phone assembly active at both the existing Quaid-e-Azam Industrial Estate and the new Sundar facility, while placing all new lines (LED televisions and selected white goods) at Sundar to capture exemptions and streamline logistics.

A few short-term factors also clipped FY2025 revenue and 1QFY2026 momentum. The company pointed to September’s floods, which dented retail traffic and deliveries in parts of the country, and to a one-month supply disruption linked to overseas events that briefly tightened the pipeline. Those transient effects are expected to fade as the year progresses.

Airlink’s trajectory mirrors the broader maturation of Pakistan’s device industry over the past decade. The company first established itself as a nationwide distributor and retailer, building relationships with leading global mobile brands and rolling out multi-brand as well as brand-dedicated storefronts. Over time, and in step with local-manufacturing incentives, Airlink back-integrated into assembly, becoming one of the most prominent domestic assemblers of smartphone handsets.

Today, Airlink combines assembly, distribution, and retail across key consumer-electronics categories, and it is one of the few listed players with that end-to-end footprint. The retail arm itself has been scaling, with retail revenue rising from roughly Rs1.1 billion in

FY2024 to around Rs2.0 billion in FY2025, and a fresh slate of flagship locations rolling out. The company recently opened a Samsung store at Dolmen Mall and plans to open a Xiaomi store in November and Pakistan’s first iPhone monostore in December, a triad that underscores the breadth of its brand partnerships on the high-street.

The corporate strategy is to keep a strong distribution and retail spine while scaling local assembly to reduce currency exposure, shorten lead times, and improve margins. Listing on the Pakistan Stock Exchange gave Airlink capital and visibility to pursue that plan; management has since executed a series of facility upgrades and product-line additions to anchor the move beyond phones.

Airlink enters FY2026 with three growth engines: phones, laptops, and televisions –plus optionality in white goods and electric vehicles.

Phones. Management targets overall production growth of around 20% in FY2026, with 2.5–2.6 million mobile units to be manufactured during the year. The ramp reflects both Tecno and Xiaomi output increases and a normalising supply chain. The company expects these two brands alone to add Rs10.0–15.0 billion in incremental revenue this year versus FY2025.

Laptops. The Acer line is the headline addition. Airlink has opened its first LC for laptops, with an initial 10,000-unit shipment to seed the market, and it aims to sell over 100,000 laptops by end-FY2026. Management pegs Pakistan’s addressable laptop market at more than 1.5 million units a year – a scale that, if captured even partially, would diversify the company’s revenue base beyond handsets. Laptops are expected to contribute Rs2.0–4.0 billion of revenue in FY2026 as the line ramps. Televisions. The company is bringing LED TV assembly online at the Sundar site, guiding to roughly Rs8.0 billion of TV revenue in FY2026. TVs fit naturally with the new facility layout (an entire ground floor dedicated to household appliances) and with Airlink’s existing retail and distribution muscles.

White goods. Airlink is in NDA-bound negotiations with top 4–5 global brands to introduce household appliances made locally. Agreements are expected to be finalised by 1QCY2026 (which corresponds to 3QFY2026), setting the stage for a new category launch. The company intends to distribute white goods through its existing dealer network, leveraging brand-store traffic as showrooms. EVs and e-bikes. Management is also testing electric vehicles in a measured way, planning to import a limited 500–1,000 units to gauge demand before committing to a joint venture if economics permit. In two-wheelers, e-bikes are on the roadmap; scooters are

not a near-term priority given infrastructure constraints.

The operational hub is shifting to the Sundar Industrial Estate, a 10-year tax-free zone that confers corporate and super-tax exemptions and promises process efficiencies. Mobile phone production will continue at both Quaid-e-Azam Industrial Estate and Sundar, while all new production lines – TVs and selected white goods, and ultimately larger appliances – will be built out at Sundar. Management expects to finance the new factory largely through internal resources, tapping banks only if needed, a choice that should keep leverage in check as volumes rise.

Putting the pieces together, Airlink is targeting roughly Rs140.0 billion in FY2026 revenue, compared to around Rs104.0 billion last year. The building blocks are TVs (~Rs8.0 billion), laptops (Rs2.0–4.0 billion), and higher mobile throughput (~Rs10.0–15.0 billion extra), with the remainder coming from the base handset business and retail. Quarterly sales of Rs30.0–35.0 billion across the remaining quarters would put that target within reach, assuming supply chains and demand remain supportive.

Airlink’s evolution – from retailer-distributor to multi-category assembler and brand partner – echoes a well-trodden path in Asian electronics. Many of today’s global names spent formative decades as OEM/ODM partners, learning to manage supply chains, build vendor ecosystems, and deliver on time for someone else’s brand before stepping up to branded products or higher-value components.

Consider the Taiwanese and Japanese experiences. Acer, which began life in the 1970s as an electronics parts and contract-manufacturing company before rising to global prominence as a branded PC maker, honed its craft by operating across the OEM–ODM–brand continuum. In Japan, consumer-electronics giants cultivated distribution and vendor ecosystems domestically while licensing and joint-venturing overseas, iterating relentlessly on process and design. Neither archetype began with a fully fledged branded hardware stack from day one; both climbed the ladder by using distribution heft, manufacturing learning curves, and partnerships as accelerants.

Airlink is pushing along that same vector in a Pakistani context. Its brand-store roll-out (Samsung, Xiaomi and the coming iPhone monostore), its wholesale distribution backbone, and its assembly lines for phones – soon laptops and TVs – create a flywheel in which each piece powers the other. Retail gives consumer insight and promotional reach; distribution secures channel access and volume commitments; assembly supplies speed, currency hedges and margin headroom.

If, as planned, white goods join the portfolio with a global OEM partner, the company will have recreated the kind of diversified consumer-electronics platform that underpinned the rise of several Asian champions, scaled to Pakistan’s market.

The Sundar tax regime and a more predictable import environment would keep the gross-margin and operating-profit improvements visible in FY2025 and 1QFY2026 intact. The company is already signalling stable margins at current levels.

Hitting the Rs8.0 billion TV target and 100,000+ laptops depends on commissioning and ramping without supply hiccups. The 10,000-unit seed shipment for laptops is a start; sustaining momentum takes retail activation and after-sales infrastructure.

NDA-bound talks with top 4–5 global brands are due to culminate by 1QCY2026/3QFY2026. The quality of those partnerships –and the degree of localisation they entail – will shape medium-term profitability.

With retail revenue doubling from ~Rs1.1 billion to ~Rs2.0 billion in a year, the store network is turning into a strategic moat, especially for launching TVs, laptops and future appliances. The three new flagship sites in Lahore and Karachi should serve as high-visibility anchors.

Airlink’s FY2025 headline slowdown owed much to external constraints on imports and a step-up in taxes, not to a loss of relevance in its categories. The 1QFY2026 inflection – higher sales, stronger gross margins, and a clearer runway for supply – suggests the down-cycle has turned. The Sundar move gives the company a structural tax advantage and a modern platform to house TVs, laptops, and white goods. Meanwhile, the Acer partnership in laptops opens a large, under-served computing market, and the TV line should benefit from Airlink’s expanding brand-store presence and established dealer relationships.

For a listed Pakistani electronics maker, this combination – distribution heft, retail control, and local assembly across multiple categories – is rare. If Airlink executes to plan, FY2026 could mark the year it scales from being a leading smartphone assembler into a diversified consumer-electronics platform, with the optionality to stretch into home appliances and to experiment at the edge with EVs and e-bikes.

The forthcoming quarters will tell. Investors will watch for quarterly sales consistently in the Rs30.0–35.0 billion range; for laptop and TV line-rates keeping to targets; for white goods agreements inked on time; and for finance costs easing as scale and rates move in tandem. But after a policy-pinched 2025, the pieces for a larger 2026 are on the table – and Airlink appears determined to

NEPRA trims K-Electric’s tariffs on lower cost assessments

The publicly listed utility is expected to take a hit to even historical earnings as the regulator assess its cost structure to have been lower than previously expected

Pakistan’s power regulator has cut K-Electric’s allowed average tariff for the current multi-year period after reassessing the utility’s underlying cost stack, a move that analysts say will materially compress revenue and force a restatement of reported profit for FY24. The National Electric Power Regulatory Authority (NEPRA) issued its decision on review motions tied to K-Electric’s multi-year tariff (MYT) determinations for generation, transmission, distribution and supply covering FY24 to FY30. The revision lowers the utility’s average determined tariff from Rs39.97 per kWh to Rs32.37, a steep Rs7.6 cut that will ripple across the company’s P&L and balance sheet for years.

The single most consequential change is the headline average tariff. NEPRA’s revised calculus knocks the figure down to Rs32.37 per kWh from the earlier Rs39.97. On K-Electric’s expected billable units, analysts estimate that this translates into an annual revenue hit of roughly Rs96 billion, or Rs3.49 per share. The brokerage notes that not every rupee of this gap drops straight to the bottom line, but a “significant portion” will weigh on earnings and could complicate capital expenditure plans, fuel procurement and compliance with debt covenants. The report adds that FY24 earnings per share of Rs0.15 will require restatement to a loss under the revised regime.

The impact is not limited to the top line. NEPRA has decommissioned two legacy generation assets – BQPS-I and KCCPP – effective on notification of the determination, and shifted the return on equity of the two remaining base plants (BQPS-II and BQPS-III) to a hybrid “take-or-pay” model with 35% guaranteed and the rest linked to actual dispatch from November 2025. Fuel “take-or-pay” will not be allowed after the current gas supply agreement ends in December 2025. Each of these steps lowers fixed income for the generation business and tightens operational risk around dispatch patterns and fuel nominations.

On the wires side, the allowable distribution loss has been cut to 9.0% (broken into 8.0% technical and 1.0% for law-and-order slippage) from 13.9% previously. Given K-Electric’s reported T&D losses rose to 16.0% in FY24

while the recovery ratio fell to 91.5%, the new cap implies a sizeable efficiency delta that the company must absorb, with direct consequences for cash flows and investment headroom. Simultaneously, NEPRA has converted the earlier dollar-linked returns on regulated asset base to PKR-based returns – 15% for transmission and 14.47% for distribution – muting the hedge that dollar indexation had provided against rupee depreciation.

Just as important: NEPRA disallowed the earlier recovery-loss allowance of 6.75% in the supply business. Instead, only a write-off mechanism capped at 3.5% will be available – and that, too, only after FY30 when the MYT period ends. The analyst’s “Supply business to post losses” table, reproduced from NEPRA’s numbers, shows a net negative margin of Rs12,450 million, underlining the pressure this element creates on working capital. The companion “Average revenue tariff” exhibit – page 4 of the note – breaks the revised Rs32.37 into Rs27.83 for power purchase, Rs2.40 for transmission, Rs2.90 for distribution, a negative Rs0.78 for supply margins, and a small prior-year adjustment.

Fuel-cost arithmetic also shifts. By lowering the reference fuel cost, NEPRA increases the incremental Fuel Cost Adjustment (FCA) that will flow through periodic bills, while reducing Tariff Differential Subsidy (TDS) claims – effects that mostly net out in the broader system but tighten K-Electric’s cash conversion timing. The report highlights that, excluding hydel and nuclear (which are not available to K-Electric), the grid cost is around Rs38 per kWh, broadly in line with K-Electric’s previous tariff. Under the new Rs32.37 determined level, the company would return the government’s earlier TDS of Rs6.0 per kWh, with about Rs1.6 per kWh recovered from consumers via FCA – another pointer to back-dated impacts on revenue recognition.

Two strategic threads run through the decision. First, cost of service: NEPRA’s review implies K-Electric’s efficient cost base should be lower than previously allowed, hence the tariff trim and tighter loss allowance. Second, risk allocation: by de-indexing returns and curbing pass-throughs and allowances, the regulator pushes more performance risk onto the utility’s shareholders. For investors, that

flips the narrative from “tariff certainty equals earnings certainty” to “tariff certainty with tougher performance hurdles.”

Pakistan’s framework assigns NEPRA the job of determining utility cost-reflective tariffs; the federal government then notifies a uniform national tariff so consumers in different provinces pay the same schedule. The gap between NEPRA’s utility-specific determined tariff and the notified uniform rate is bridged by the Tariff Differential Subsidy paid from the federal budget. In periods when government seeks to contain subsidies, or when NEPRA revises a utility’s allowed costs downward, the bridging arithmetic changes – but end-consumer bills under the uniform schedule are typically unaffected by such changes to a single utility’s determined tariff. The analyst note flags exactly this point: even with K-Electric’s determined tariff reduced to Rs32.37, consumer bills do not change because of the uniform regime; instead, the settlement flows adjust in the background.

Another pillar is the FCA mechanism. Because the fuel mix, global prices and dispatch stack vary month to month, NEPRA approves monthly or periodic Fuel Cost Adjustments that true up the difference between reference and actual fuel costs. By resetting the reference, NEPRA raises the probability that more of the difference shows up as FCA rather than sitting in the base tariff – explaining why consumers may still see moving parts in monthly bills even when the base schedule is unchanged. The MYT also embeds allowances for technical losses and, historically, a measure of recovery losses; this last element is what NEPRA has now removed, replacing it with a post-period write-off cap.

Finally, Pakistan’s system uses prior-year adjustments (PYA) to reconcile over- or under-recoveries from earlier periods. The analyst’s “Average revenue tariff” table shows only a small Rs0.02 per kWh PYA embedded in the new average, but the bigger restatement risk sits in the historical EPS that K-Electric had reported for FY24 – the note says this will now be reworked into a significant loss due to the retroactive nature of parts of the review.

K-Electric is Pakistan’s only vertically integrated, privately owned power utility, responsible for generation, transmission, distribution and supply in Karachi and adjoin-