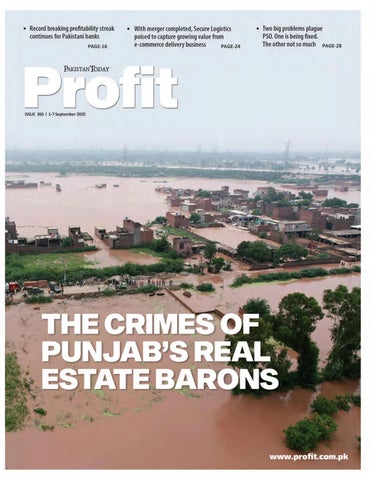

10 The crimes of Punjab’s real estate barons are drowning us

16 Record breaking profitability streak continues for Pakistani banks

18 After rough 2024, Archroma Pakistan sees return to profitability this year

20 In 2025, Pakistanis reduced their consumption of Cocomo

22 Pakistan’s Tax Myth: It isn’t the people, its the government Osman Niazi

24 With merger completed, Secure Logistics poised to capture growing value from e-commerce delivery business

26 Pakistanis are buying more batteries, but Atlas sees sales slump

28 Two big problems plague PSO. One is being fixed. The other not so much

32 Pakistan’s climate reckoning Omar Javed Chohan

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

THE CRIMES OF PUNJAB’S REAL ESTATE BARONS ARE

DROWNING US

Climate change and river infrastructure has rapidly changed what modern water management looks like. Real estate developers and their political allies are criminally complicit

By Abdullah Niazi

Din Muhammad sat perched on his charpai as it rested slightly tilted on a small mound of dirt. Cars whizzed past him barely a dozen feet away. The traffic on the M2 was subdued early in the morning and offered little distraction to Din and the long line of people that found themselves camped out on the side of the highway with their families, cattle, and whatever belongings they could carry with them.

“People from the government came two nights ago and told us to evacuate. Some people from within the village did not want to leave and advised us against it but the government kept pushing. Eventually we grabbed our essentials and left,” he explains. His eyes are fixated on the scene in the distance. Right next to the motorway’s Babu Sabu Interchange close to Thokar Niaz Baig, the main entry point to Lahore, one can see nothing but water from miles. From a distance the water seems timeless. Like it was never not there. But it does not take long to notice what is poking out of the water. Golden three-pronged street lamps and billboard with the half visible words “New Metro City Lahore”

This is the site of one of the many real estate development projects that have been taking place close to or smack dab in the middle of the banks of the Ravi River. Even as he speaks with us, Din Muhammad’s eyes remain fixated in the distance, his responses come delayed.

“He is looking for our buffalo. When we left the village we brought all five animals with us. One of them wandered off in the middle and we haven’t seen her since,” his wife says from the foot of the charpai where she is attending to their children. “The buffalo we lost was the healthiest in our herd and gave the most milk. He’s worried she will be lost in the waters now.”

This is only one story of the more than 250,000 people that have been displaced and more than 15 lakh that have been affected by the ongoing flood in central Punjab. The situation is only set to get worse. As the water flows South, government authorities have already begun preparing for the three flooded rivers, Ravi, Chenab, and Sutlej, to rush into South Punjab and eventually meet in the Indus River in Sindh.

The unprecedented flow of water follows the extreme pressure on these rivers upstream in India following heavy monsoon rains. In the past few years, the monsoon rains have increased in intensity, volume, and timing. Further on in Punjab the situation remained bleak. Profit visited a number of areas including Hafizabad and other districts affected by both the Ravi and Chenab rivers. Even along the M-2, from Pindi Bhattiyan onwards the Chenab has overflown with no views but water for miles. The only indication that there was once farmland there are the tops of barely visible trees.

Since the floods have struck, the entirety of the state machinery has been on its toes and engaged in rescue work. Despite some poor PR choices like Maryam Nawaz deciding to take a boat ride on the flooded river surrounded by her cabinet lackeys and protocol flunky babbus, the response has largely been robust. The

We have built so many dams in this area that they end up stopping small floods and drying these rivers up during normal times. This gives people the impression that the water will not return. But all of these man-made dams are built with a particular capacity. When that capacity is exceeded, everything in the river’s path will go

Dr Hassan Abbas, hydrologist

Flood Forecasting Division has shown alertness and efficiency. District administrations have acted quickly and forcefully to get people to evacuate areas where the FFD has informed the flood will hit despite the apprehensions of the local populations. The PDMA has been responding fast and a massive deployment of state forces has kept casualties to a minimum. Already the district machinery in South Punjab is working overtime to ensure minimal damage as the flood travels South. The Sindh Government, surprisingly, has also been on its toes.

There are many elements to this flood. The first, of course, is the rescue operation and minimising the damage that so many have faced as a result. There is the problem of agriculture and the impact this will have on next season’s wheat crop and this season’s rice harvest: an issue that could well affect our food security next year. Then there is climate change, the results of which ravaged us only too recently in 2022 when the last major floods hit the country. But we must begin, first and foremost, with Lahore. Because nothing encapsulates Pakistan’s response to challenges like this more than the blatant hubris that has led to so many real estate developments on the bank of the Ravi.

New Metro City Lahore, which is currently submerged in water and awaiting some sort of draining, is a pet project of BSM Developers, the real estate company owned by Bilal

Bashir Malik, who is the grandson of property tycoon Malik Riaz. But the Riaz family is not the only one that took advantage of the Ravi’s natural course. Lahore’s Park View Society, owned by Ahmed Aleem Khan, has probably been the worst affected by the floods. Almost the entirety of the society is submerged. Its houses, selling at Rs 1.5 crores for a five marla place, have water inside them. Residents had to shift floors and be rescued by boat in many of its blocks. Overall, there are nearly 80 housing and real estate projects close to or on the banks of the Ravi. Of these, 47 societies are illegal, 14 have planning permission, another eight have technical approval, and eight more have final approval. Despite this, nearly all have started development work on their projects.

Even in the ones that are approved, there are serious concerns about the political maneuvering and influence it took to get the job done. And while there is a vast web of developers and politicians with deep interests in these many projects, the central lynchpin to this story is one organisation: the Ravi Urban Development Authority (RUDA).

Starting from scratch

The Ravi broke free this weekend. As the waters swelled downstream from the massive release from India’s major dams, the river began to climb to areas

it has not regularly occupied in living memory. There was a time when the Ravi would run along the walls of Lahore’s gates. During the monsoon season, it would pass by the Badshahi Masjid and touch the walls of the Lahore Fort.

The river has changed course since. It has shrunk and much of the river bed has been exposed, particularly in the summer months when it is often a sorry sight. But the thing about nature is you cannot mess with it. Human hubris and the desire to subjugate nature has always led to economic and social disaster. Humanity’s place in the world demands a respect and reverence for nature that has gone missing.

Rivers, for those that study them, are as good as living beings. They have personalities, moods, whims, the capacity for both cruelty and kindness. Most importantly, rivers have rights and homes. And no matter what happens, even if a river recedes to a point of nothingness, the day it decides to reclaim its space nothing stands in its way. That is something of what we are seeing in this year’s floods that is different from 2022, when hill torrents in Sindh and Balochistan caused havoc because of excess monsoon rains. This year is a case of the river taking back what is historically its path. Ask Dr Hassan Abbas, Pakistan’s leading hydrologist, and he will tell you the extent of the disaster that messing with a river can be.

“This is an unmitigated environmental disaster. When you start to mess with a river you mess with nature,” he says.

This is the major governance issue in our river system. Housing societies and infrastructure on riverbeds are always going to come under water at some point

Hussain Jarwar, CEO of the Indus Consortium

It is a simple rule of life that does not seem to have penetrated the hefty skulls of the masterminds behind the Ravi Urban Development Project. The idea for a riverfront project on the banks of the Ravi is not a new one. In fact, it was first proposed as far back as 2006, and underwent a feasibility study in 2013 under the PML-N government. The idea has long been a lucrative if elusive pipe-dream. Lahore, as many are aware, has swelled up and its urban sprawl has seen it become one of the most polluted cities in the world which regularly tops the global rankings for the worst air quality.

Decades of unbridled real estate development, unsustainable horizontal growth, and massive coal power plant projects in adjoining

cities have left the ancient Mughal capital on the path to being unlivable. There is much that could be done to solve Lahore’s problems. For starters, a viable network of public transport could reduce the city’s growing traffic congestion and restrictions on real estate development and the encouragement of vertical growth could help contain the sprawl. Investments could be made for forestation and an overall plan to make the city more high-density, more walkable, and most importantly more liveable.

Ideas like the Ravi Riverfront Urban Development Project are the sort of sweeping solutions that populists like to extoll. Essentially, the Ravi riverfront is the plan to make a new city from scratch. The project would be Pakistan’s second-largest planned city after Islamabad, covering an area of 102,074 acres, catering to a population of up to 15 million people. It is an ambitious undertaking — one that is born as much out of a sense of frustration with the state of our urban centres as it is out of necessity. In fact, in a comprehensive and eye-opening article published in Dawn back in June 2021, it was pointed out that the development of new cities and riverfront projects is not unique to Pakistan, and that such projects and several new cities have been planned across Asia and Africa in recent years.

It is essentially a desire to start from scratch. To plan and control and build a city with the benefit of hindsight. The foundation rock for the utopian riverfront project was first laid in 2019 with the passage of the special legislation that established RUDA. The authority would not work under any other body in or related to Lahore, and would have complete control over the project. In fact, the Lahore Development Authority (LDA) and similar bodies in Gujranwala and Sialkot would be subservient to RUDA. So complete were the powers

given to RUDA that not only was the authority entrusted with the entire responsibility for the project from planning, to acquisition, to development that the legislation which created RUDA granted the authority and its employees immunity from all legal proceedings, and “no court or other authority” can “question the legality of anything done or any action taken in good faith under this Act, by or at the instance of the Authority.”

Hue and cry

The formation of RUDA naturally met with resistance. The law that had created and empowered RUDA seemed to go beyond reasonable limits because of the lack of accountability that the authority had to office. Eventually, RUDA’s fate ended up in the courts, but it was clear there were plenty of political interests in the mix.

In January 2022, Justice Shahid Karim of the Lahore High Court (LHC) in a 298-page long judgement declared that the scheme was “unconstitutional” on the grounds that it lacked a master plan.

Justice Karim said that the RUDA failed in preparing a master plan. It was a technical point to hold over them. No focus was paid to the wide powers RUDA was suddenly given that made it essentially free from accountability. Sensing the moment, the prime minister Imran Khan immediately visited the project site and announced that his government in Punjab would challenge the verdict in the Supreme Court. Less than a month later in February, the Supreme Court threw out the LHC’s detailed verdict after less than 10 days of hearing and deliberating on the matter. The two-judge Supreme Court consisting of Justice Ijaz-ul-Ahsan and Jus¬tice Mazahar Ali Akbar Naqvi held

that RUDA could continue working on lands it had already acquired.

Profit has covered the saga that followed extensively before

Wild Wild Ravi

But two major issues persisted. The first was that RUDA continues to operate as a development authority with wide jurisdiction. That means if you are making a real estate project close to the Ravi, your regulatory body will be RUDA. While RUDA itself was working on its Chaharbagh development a little further away from the river, other societies were cropping up. Some had approval from RUDA others didn’t. What RUDA’s presence did do, however, was turn the area around the Ravi, including the riverbank, into a sort of free for all.

Take Park View City for example. This was the project that ended up being the reason for the falling out between Imran Khan and Aleem Khan, who was once considered a strong contender from the PTI to become Chief Minister of Punjab, and remained Senior Minister in the Buzdar cabinet.

The Park View Project has been in the works since at least 2004. Back in the day, the project was originally named “River Edge”. The irony of this is not lost on the society’s residents, whose houses are submerged in 7-10 feet of water. “This is the major governance issue in our river system. Housing societies and infrastructure on riverbeds are always going to come under water at some point,” says Hussain Jarwar, the CEO of the Indus Consortium, a think tank that works with river communities in the Indus Delta.

“The Ravi, Chenab, and Sutlej, are Eastern rivers that India uses. Their natural

Park View City in December 2018.

Park View City in January 2022.

waterway has been empty because of the Indus Water Treaty. People end up building on these empty banks and if ever there is a release of water they end up submerged.”

The presence of real estate projects on the riverbanks is a direct result of these empty spaces. “We have seen in this recent flood that there is a serious need for zoning. Land is being used for purposes that it should never be used for,” says Minister for Climate Change Dr Musadiq Malik.

Dr Hassan Abbas concurs. “We have built so many dams in this area that they end up stopping small floods and drying these rivers up during normal times. This gives people the impression that the water will not return. But all of these man-made dams are built with a particular capacity. When that capacity is exceeded, everything in the river’s path will go,” he says.

In the case of the two societies Profit visited, Park View and New Metro City Lahore, it was clear that these societies had been built with some political influence and should never have been allowed in the first place. Take Park View for example. It had actually raised the ire of RUDA, which took action against it because it felt this was an are in its jurisdiction. After Aleem Khan’s falling out with Imran Khan, the project was stalled. The PTI’s minister in the Punjab Government at the time, Mian Aslam Iqbal, said the project was illegal and Aleem Khan kept building it because the Lahore Development Authority was in cahoots with him.

However when Aleem Khan joined the coalition government in 2023, he got major relief as the National Accountability Bureau (NAB) closed an inquiry against him for allegedly occupying and encroaching public passages and illegal extension of the Park View housing society both in Lahore and Islamabad under the new accountability laws.

The case of New Metro City Lahore is similar. At the time that it was built, it was a project of Malik Riaz’s grandson. Profit has done stories on both these societies before.

What matters, however, is that land developers have clearly had their eyes on the Ravi riverbed for decades, especially since the river has shrunk over time. They did not care for any environmental assessment, and in many cases built unapproved societies over its banks. The maps from Google Earth show just how bad the shift in greenery next to the rivers has been. They should never have been allowed to be made in the first place.

The climate impact

Environmentally, the project posed major problems. Behind the project was a concept, and it was not just to create another city to give Lahore some much needed respite. The concept of the riverfront

We have seen in this recent flood that there is a serious need for zoning. Land is being used for purposes that it should never be used for

Dr Musadiq Malik, Minister for Climate Change

was to create a city along a raised riverbank. The end-goal was to revitalise the Ravi by building a series of barrages and rechanalising it.

Taken at face value, the riverfront project is an attempt to exert control over the Ravi. RUDA claims that to avoid flooding, revive the Ravi, and ensure more equitable water distribution it is necessary to recanalize the river by building a series of barrages and raising its embankment walls. To afford the project, they are planning and developing the riverfront project which will fund work on the river.

In this vein, RUDA has regularly tried to portray itself as an environmental necessity. On March 21 this year for example, soon after the SC’s verdict, RUDA claimed that the water in the Ravi was toxic and any produce grown through it was bad for the health.

Yet for all its claims that Ruda is a fix-all to save the environment, the research collected is doubtful. “These are all excuses. Hands down all of them. They are claiming that they are raising the embankments to make sure that the river can carry more water to avoid flooding for example. This is ridiculous hydrologically speaking. This means that if there is a high amount of rainfall, as there was this year in Sindh and Balochistan, the walls will be so high that water will begin to collect outside the walls and have nowhere to go — flooding the fields on either side,” says Dr Hassan Abbas.

“This is an unmitigated environmental disaster. Trying to control it is not going to work. Then there are also dams on the Ravi, and if they ever have to open those dams a situation like the great floods of 1992 might occur again. They have no solution and all of these claims are mere eyewash. Recanalisation is absolutely wrong as a concept, and this is all an excuse to give development groups and real estate moguls stakes in this area,” he claimed.

Meanwhile, a 2021 report commissioned by RUDA found that much of Ravi City’s impacts on ecological resources would be long-term and irreversible. And as the earlier mentioned Dawn article pointed out, that “in

spite of this, the EIA report concluded that the project will have an ‘overall positive impact’ on the entire ecosystem, and deemed the strategic development plan of the project ‘feasible’ at the proposed location, as long as the recommendations made in the report are implemented in ‘true spirit’.”

“One struggles to reconcile the optimism of the Ruda EIA with the findings of a feasibility study of a similar Ravi project considered by the PML-N government in 2013. The study concluded that there was no water in the Ravi to make its riverbed an attractive real-estate proposition.”

What should have been done

The answer is simple: let the rivers flow. Rivers cannot be controlled. We have learned over time that this is the case. In Europe as well there is a clear shift towards allowing rivers to take their natural course and building forests around them. In Punjab as well, to create these real estate projects, naturally occurring forests around these rivers are cut down.

These forests are forces that stop the flooding. Instead, we build residential real estate in their place. This is simply tempting fate. There is no controlling a river, and particularly the Indus River System, especially with the added effects of climate change. The only question is, will policymakers and the government learn anything from this disaster?

The current response to the floods has been efficient and well coordinated. Ministers are on the ground, the workers of Rescue 1122 and other organisations have shown great heroism in helping evacuate at risk people like Din Muhammad and saving lives. However, it needs to be made certain that they are not called on to do so again. The only solution is to let the river run on its natural course, and to treat our natural systems with respect and reverence. Without that, the next tragedy is not a matter of if, but when. n

Record breaking profitability streak continues for Pakistani banks

Soaring revenue and deposit growth, coupled with robust asset quality, help boost earnings past previous highs

PProfit Report

akistan’s listed banks have chalked up their highest-ever halfyear profit in the first six months of calendar 2025, extending a streak that began last year and shows little sign of fading. Aggregate profit after tax for KSE-100 index banks reached Rs326 billion in first half of 2025, up 19% year on year, with the second quarter alone contributing Rs160 billion, a 23% jump over the same period of 2024.

The core driver remained net interest income (NII), which climbed to Rs1.0 trillion for the half, up 22%, helped by larger balance sheets and robust low-cost deposit mobilisation. Non-mark-up income added resilience at Rs255 billion, up 7%, with fee income rising to Rs141 billion on the back of digital and trade activity, FX income holding at Rs49 billion, and gains on securities edging up to Rs39 billion as banks tactically managed their

investment books.

Operating expenses rose in a still-elevated inflation environment to Rs553 billion, but the cost-to-income ratio stayed broadly contained at 46% versus 45.4% a year earlier, signalling efficiency gains even as networks and technology spend continued. These figures, set out across the opening pages and the income-breakdown exhibits of the report, explain how the sector delivered record profitability despite a shifting rate backdrop.

Taxation was hefty, too. The sector’s effective tax rate averaged 54% in first half of 2025 compared with 48% a year earlier, pushing the tax contribution to Rs394 billion in the half and Rs205 billion in the second quarter alone. Even with that heavier burden, bottom-line growth remained strong – evidence of how much operating leverage banks have unlocked through scale, higher NIMs in recent quarters, and fee-led businesses.

Asset quality trends provided a tailwind. The sector recorded a net provisioning reversal of Rs1 billion in the half, swinging to reversals

of Rs6.3 billion in 2QCY25 after a Rs5.2 billion charge in the first quarter. As the exhibits in the report make clear, this sequence points to stabilising credit costs, improved recoveries and better collateral values – giving banks more room to let income growth flow to the bottom line.

If the income statement was robust, the share-price response was emphatic. A chart of relative performance shows the KSE-100 banks up 70% year-to-date, far ahead of the KSE-100’s 27% gain – a 43 percentage-point beat that crowns the sector as the market’s standout performer in 2025. Individual leaders included NBP up 148%, UBL up 111%, and AKBL up 105% as investors rewarded earnings momentum and capital returns. The same section highlights deposits at record highs in 2QCY25 for 11 of 13 banks within the index, reinforcing the growth story underpinning those re-ratings.

The sector’s earnings boom is rooted in deposit growth and a steady improvement in funding mix. UBL had the fastest expan-

sion – up 32% year on year to Rs4.3 trillion – followed by MEBL up 26% to Rs3.0 trillion, and BOP up 23% to Rs1.9 trillion. In absolute terms, HBL sits atop the league table with Rs5.2 trillion, with NBP at Rs4.7 trillion and UBL at Rs4.3 trillion; eleven of the thirteen index banks logged all-time-high deposits by the June quarter. The report also flags large gains in current accounts, with HBL adding a record Rs440 billion and lifting its CA ratio to 40.5% – a pivotal shift for funding costs in an easing-rate cycle.

On asset quality, the data point to benign trends in first half of 2025. A net reversal for the half, combined with the second-quarter swing into Rs6.3 billion of reversals, suggests that banks have not yet seen a material deterioration in lending books despite a tough macro stretch. The bank-specific milestones offer corroboration: MEBL reports infection of 2.5% and coverage of 149%, both comfortingly solid for a systemically important franchise. Sector ratios in the consolidated table echo this resilience, with NIMs at 5.2% for the group and cost-to-income in the mid-40s, despite broad inflation pressures.

All told, deposits at historic highs, current-account mobilisation, and stable credit costs have given banks the raw material to protect margins even as policy rates start to ease off their peaks. That combination – scale plus funding mix – is why earnings have remained buoyant after the extraordinary prints of 2024.

The sector’s strength is not uniform. Islamic banks in the KSE-100 recorded a 13% decline in profit to Rs57 billion in first half of 2025 as the double squeeze of lower rates and a regulatory change took hold. From January 2025, a new framework introduced minimum deposit rates (MDR) on PKR-denominated savings deposits for Islamic banking institutions (excluding financial institutions, public-sector enterprises and public limited companies).

That policy change re-priced a core part of Islamic banks’ funding base just as benchmark rates began to edge lower, compressing margins on legacy asset books. The report’s income analysis shows NII for Islamic banks down 9% to Rs160 billion, while conventional banks posted a 29% rise in profit and a 31% rise in NII to Rs855 billion over the same period.

Put simply, Islamic banks are adjusting to price-regulated deposits in a falling-rate environment. Their response is likely to centre on asset-mix optimisation (especially higher-yielding corporate financings), fee income growth through cash management and trade, and tighter cost discipline. The report implies that these banks retain strong deposit franchises and resilient asset quality, but the immediate profitability headwind is clear

and helps explain why much of the sector’s outperformance this year has been led by the conventional heavyweights.

HBL posted record half-year earnings of Rs34.4 billion and pushed deposits past Rs5.2 trillion, powered by a record Rs440 billion addition to current accounts that lifted the CA ratio to 40.5%. The current-account surge should anchor funding costs as rates drift lower.

UBL reached all-time-high deposits above Rs4.3 trillion by June and remained one of the best stock-market performers year-todate. It announced interim dividends totalling Rs13.5 per share across the first half, demonstrating confidence in capital buffers.

NBP delivered its strongest first half ever, with deposits at a record Rs4.7 trillion and profitability at Rs42.7 billion, roughly 61 times the result a year earlier. While NBP gives only a final dividend by policy, the operational momentum – and the stock’s 148% gain – were among the sector’s biggest narratives of the year.

MCB’s deposits climbed to Rs2.2 trillion by June, with current deposits up Rs256 billion year-to-date to cross Rs1.0 trillion and lift their share to 54%. That reshaping of the funding base supports margins; the consolidated table also shows sector-low cost-to-income among the large banks and a healthy DPS of Rs18 in the half.

MEBL (Meezan Bank) produced the sector’s best ROE at 36.4% by June alongside record deposits at Rs3.04 trillion, but it also sits squarely in the Islamic-bank cohort facing the MDR-driven margin challenge. Its infection ratio of 2.5% and coverage of 149% underscore asset-quality strength, while its NIM of 8.5% in the consolidated snapshot remains among the highest.

BAFL (Bank Alfalah) posted record deposits of Rs2.3 trillion, up 9% year on year, and announced its highest-ever first half of 2025 payout of Rs5 per share. Fee engines remained active, with cards, payments and trade contributing to non-mark-up income.

AKBL (Askari Bank) recorded first half of 2025 earnings of Rs10.6 billion and, notably, its first interim dividend in 11 years, paying Rs2 per share in the second quarter versus its last interim of Rs1 back in 1QCY14. That re-opening of the dividend channel was one of the half’s more eye-catching corporate actions and aligned with the stock’s 105% year-to-date surge.

BAHL (Bank Al Habib) maintained steady profitability with a DPS of Rs7 across the half and cost-to-income in the mid-50s, as per the consolidated table. Investments sit close to Rs1.94 trillion against deposits of Rs2.48 trillion, reflecting a balanced asset mix while the bank continues to push fee-based

businesses.

ABL (Allied Bank) continued consistent execution, paying Rs8 in dividends during the half and sustaining an efficient cost base. The consolidated snapshot shows NII of Rs51.7 billion and non-mark-up income of Rs15.5 billion for the six months, with cost-to-income around 49%.

HMB (Habib Metropolitan Bank) posted Rs11.6 billion in half-year profit and Rs5 in dividends, with NIMs of 5.7% and a cost-to-income ratio in the low-40s, placing it among the leaner operators on the efficiency chart.

FABL (Faysal Bank) reached all-timehigh deposits of Rs1.24 trillion by June and distributed Rs3 per share during the half. With an ADR close to 58% and IDR in the mid-50s, FABL’s balance sheet remains geared to both lending and investments while it consolidates its full-fledged Islamic transition.

BOP (Bank of Punjab) reported record first half of 2025 earnings of Rs6.5 billion, up 38%, and announced its first-ever interim dividend of Rs1, with deposits at a historic Rs1.9 trillion by June. The market responded well, reflecting confidence in BOP’s improving profitability and capital trajectory.

SCBPL (Standard Chartered Pakistan) continued to punch above its weight on margins, showing NIMs of 9.3% – the highest in the consolidated table – paired with a cost-to-income ratio in the high-20s and Rs3.5 per-share dividends in the half. Its enviable funding mix and transaction-banking muscle again shone through.

Sector snapshot: The consolidated table on page 7 ties these stories together. Across the index banks, total income reached Rs1.27 trillion, operating expenses came in at Rs553 billion, profit before tax at Rs722 billion, and profit after tax at Rs326 billion. Deposits totalled Rs33.2 trillion, investments Rs33.9 trillion, and net advances Rs11.6 trillion, with sector NIMs at 5.2%, ADR at 37%, and IDR at 93.6% – a balance-sheet structure still skewed to government paper but with lending poised to recover as rates normalise.

This earnings cycle underscores a paradigm shift: banks did not simply ride high rates; they re-engineered funding, scaled fee engines, and kept costs in check. The outperformance of bank stocks versus a surging index shows investors recognise that the sector is more than a rate proxy. With deposits at record levels, a stable credit cost backdrop, and more predictable dividends, the ingredients for another strong year remain in place.

There are risks. A sharper-than-expected fall in rates could pressure NIMs before loan growth fully accelerates; competition for deposits may intensify; and the new MDR regime proves a real test for Islamic banks’ profitability models. n

After rough 2024, Archroma Pakistan sees return to profitability this year

Volume growth, coupled with discipline on cost control, allows the chemical manufacturer to get back in black

Profit Report

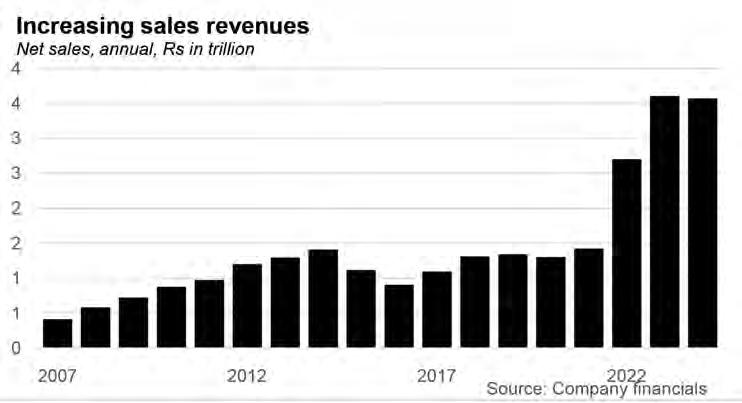

Archroma Pakistan has begun to turn the page on a punishing 2024. After posting a loss per share of Rs15.9 in the financial year 2024, Archroma has swung back into profit during 2025, with earnings per share of Rs8.0 in the third quarter alone, versus a loss per share of Rs5.3 in the same quarter last year, according to a briefing note issued by Chase Securities, a brokerage firm based in Karachi. The contrast is stark: the company moved from red ink in 2024 to a clearly profitable run-rate mid-2025, aided by stronger margins and a noticeable pick-up in sales.

The anatomy of that recovery is laid out in the same table. Net sales rose 44% year on year in the June quarter of 2025, while gross

margin climbed from 15.8% in the prior-year quarter to 24.7% – an almost nine-percentage-point improvement that turned operating losses into operating profit. Finance costs also eased and other income grew, together pushing the bottom line back into positive territory. That quarterly resurgence follows a bruising full year: in 2024, net sales fell 17%, gross profit fell 40%, and operating profit dropped 83% compared with 2023. The same side-by-side on page 2 captures how the downshift in volumes and mix during 2024 compressed profitability, even before higher overheads and finance costs took their toll. Against that low base, the June quarter of 2025 stands out as the clearest signal yet that Archroma’s operational reset – leaner costs, a sharper commercial focus on dyes, and regained share in a key product line – is gaining traction.

Management’s confidence is visible

in one more data point: dividends resumed, with a Rs20 per share payout flagged in the quarter’s disclosure line-up on page 2 of the note. After a year in which the company held off on distributions, the return of a cash return – however calibrated – underlines the strength of the turnaround through mid-2025.

Archroma Pakistan is the listed local arm of the global Archroma group, positioned at the intersection of textiles, packaging, paper, and – more recently – construction chemicals. The company breakdown on page 1 of the briefing underscores an enduring reality of Pakistan’s industrial landscape: textiles remain the beating heart of the business, accounting for about 90% of revenue. The remaining portfolio has been deliberately broadened to reduce concentration risk, with packaging and paper forming a second leg and construction chemicals forming a third.

Over decades, the business has grown up alongside Pakistan’s textile clusters, supplying dyes, colourants and process chemicals to mills that feed global value chains. That embeddedness has historically given Archroma resilience: a salesforce with long relationships, deep technical service in dyeing and finishing, and laboratories aligned to local fibre blends and water conditions. The market snapshot on page 1 of the note captures today’s footprint – a market capitalisation of about Rs15.7 billion, free float of about 8.6m shares, and a 52-week range that reflects the volatility of 2024 and the renewed optimism of 2025.

The strategic tone in 2025 is pragmatic. The company is prioritising growth in dyes, where margin opportunities are richer and where it believes brand and service can win back share. Notably, it has partially regained share in indigo, a flagship dye for denim – a segment central to Pakistan’s export identity. The briefing also notes that Archroma is commercialising a portion of the Huntsman dyes portfolio it acquired at the global level, with further sales expected over the coming year – an integration that should deepen its catalogue and allow more tailored, higher-value offers to mills.

Archroma’s textile chemicals and dyes franchise is the core engine. The products traverse the value chain – from pretreatment (desizing, scouring, bleaching), through dyeing (reactives, vat dyes such as indigo, disperses), to finishing (hand-feel modifiers, durable water repellents and other functional finishes). The value proposition is two-part: reliable colour performance at scale, and process chemistry that helps mills hit cost, quality and compliance targets under the auditing regimes of global buyers. The briefing highlights the push in dyes, where brand strength – bolstered by the Huntsman portfolio addition – is being translated into regained shelf space at mills.

Beyond textiles, the packaging and paper line supplies optical brighteners, coatings and process chemicals aimed at brightness, printability and fibre efficiency. These products are a smaller part of the book but give Archroma leverage to non-textile cycles and to import-substitution themes as local packaging upgrades with the growth of food, beverage and personal care. The construction entry adds admixtures, dry-mix additives and performance polymers for mortar and concrete – early-stage for the company but strategically important given public-sector infrastructure plans and a slow revival in private building activity. Each of these non-textile legs is geared to reduce dependence on a single customer base and to find pockets of margin where technical service can tip procurement decisions.

In the June 2025 quarter, the product mix and pricing produced tangible gains: gross

margin at 24.7%, operating profit in the black, and net margin at 4.1% after a negative print a year earlier. The return on sales is still well shy of historical peaks, but the direction of travel is clear and linked to the portfolio refocus.

If operational execution is improving, tax asymmetries remain a pronounced constraint. The briefing is blunt: imported dyes and chemicals are largely tax-free, while domestic manufacturers are subject to sales tax. On top of that, under-invoicing of imported value-added products undercuts locally produced goods, eroding pricing power just as firms need cash to invest. For a company that services export-linked mills – who themselves face buyer pressure on price – this lack of parity can be crippling.

Why does it matter so much for 2025 and beyond? First, chemicals is a scale game; margins are won and lost in utilisation and in the ability to stock breadth so mills can consolidate purchases at speed. When imports sidestep taxes or land at artificially low declared values, local plants cannot carry the working capital to match breadth without sacrificing margin. Second, R&D and technical service – the crown jewels of a speciality chemicals business – are funded out of gross margin. Persistent price-umbrella leakage inevitably means fewer lab trials, slower product refresh, and thinner field support – exactly the areas where Pakistan’s mills need a domestic partner to keep pace with buyer specifications.

The Chase note hints at where relief would bite quickest: sales-tax parity on imported and domestic products, tighter valuation and documentation at the border for value-added imports, and predictable refunds where applicable so working capital is not trapped. Even modest steps here would support Archroma’s margin targets for the next four quarters. Until then, the 2025 turnaround will rely on mix, service and share gains to do the heavy lifting.

One of the most important lines in the briefing is also one of the briefest: Archroma plans to expand into the Middle East and African markets, targeting not only construction and chemicals but also home and personal care segments. That expansion is not just geographic; it is a risk-management choice. By cultivating non-textile export channels and markets with different demand cycles, the company can reduce reliance on Pakistan’s textile ebb and flow and build a hard-currency cushion that improves earnings quality.

From an operational perspective, the June 2025 quarter provides a decent launch pad. With EBITDA recovering to Rs670m in the quarter from a small negative a year earlier, and financial charges down 45% year on year in the same period, Archroma has more internal cash to fund receivables in new

markets and to carry starter inventories close to customers. The other income line, up 71% in the quarter, also points to ancillary contributions – potentially from services or treasury – that can smooth early steps as distribution footprints are set up.

There is a product logic to the export ambition. Construction chemicals travel well across the Middle East and Africa, where climate, building codes and contractor procurement are familiar to Pakistani producers. Home and personal care ingredients add another lever, where small-lot speciality shipments and technical selling can generate steadier margins once key accounts are landed. The company’s guidance that margins will stay stable or improve, anchored in operational efficiencies, is therefore not just a cost story; it is also a channel story. The more that sales come through segments and geographies with lower price volatility and shorter cash cycles, the more durable the profitability.

The simplest way to read Archroma’s 2025 is as a reversion to speciality discipline after a bruising general-chemicals year. In 2024, lower volumes, a softer mix and overhead rigidity crushed the P&L: sales down 17%, gross margin down to 18.2%, operating profit down 83%, and a swing into a net loss. In 2025, the company has focused on where it wins – dyes, especially indigo, service-led selling, and commercialising the Huntsman portfolio – and coupled that with cost control and finance-cost relief. The result in the June quarter is a textbook speciality chemicals recovery: meaningful top-line growth, double-digit gross margin expansion, a shift to positive operating income, and EPS back above zero.

There is still distance to cover. Even at a 24.7% gross margin for the quarter, the full-year picture will depend on execution through peak textile-dyeing months, the pace of Huntsman portfolio ramp-up, and, crucially, how the tax and under-invoicing headwinds evolve. But the model, as the quarter shows, is working again when volumes return. That is why the dividend line reappears and why the share price context (with a 52-week high of Rs535 against a low of Rs256.5) frames 2025 as a rebuilding year in investors’ eyes.

For Pakistan’s broader industrial economy, there is also a useful signal here. Chemicals firms that root themselves in export-facing value chains, specialise rather than chase bulk tonnes, and expand into adjacencies with defendable service moats can bounce back quickly when macro shocks fade. Archroma’s mid-2025 run-rate suggests that, given a fairer tax playing field, the local speciality ecosystem can compete not only in Karachi and Faisalabad, but also in Gulf and African markets where speed, spec and support matter as much as price. n

In 2025, Pakistanis reduced their consumption of Cocomo

The manufacturer of beloved snack brands struggled with higher costs and consumer holding back after a biting few years of inflation

Profit Report

Ismail Industries Limited, the Karachi-listed maker of CandyLand sweets, Bisconni biscuits and SnackCity crisps, closed the year to 30 June 2025 with a noticeably softer top line in its core Pakistan food business.

On a standalone basis (which most closely reflects the domestic confectionery and biscuits operations), net sales fell to Rs105.2 billion from Rs108.9 billion, a drop of 3.4%, even as the company kept factories running and distribution humming nationwide.

Gross profit also slipped, to Rs21.8 billion from Rs24.0 billion, while oper -

ating profit eased to Rs10.8 billion from Rs14.0 billion. Full-year profit after tax on an unconsolidated basis came in at Rs5.75 billion versus Rs6.13 billion last year, with EPS at Rs86.64 compared to Rs92.41 a year earlier. Selling and distribution costs rose to Rs9.15 billion from Rs8.28 billion, reflecting the cost of staying visible in stores even as

volumes lagged.

The board nevertheless proposed a final cash dividend of Rs5 per share (50%), suggesting confidence in balance-sheet strength and cash generation despite the slower year for treat purchases. The company has scheduled its AGM for 8 October in Karachi, and will close its share transfer books from 2–8 October to determine entitlements.

On a consolidated basis (folding in the packaging films business and other subsidiaries), group net sales rose to Rs122.6 billion from Rs117.0 billion, but profit for the year declined to Rs3.70 billion from Rs4.91 billion, as costs and levies outpaced revenue growth and finance charges remained hefty. Consolidated EPS registered Rs63.39 against Rs78.30 last year. The divergence between the steadier group sales trajectory and the softer parent-company revenue points to a tougher year in the consumer staples aisle – precisely where Bisconni’s Cocomo, the country’s best-known chocolate-filled biscuit, lives on countless shop counters.

Why the weakness when headline inflation cooled dramatically into 2025? Pakistan’s price spiral may have broken, but household budgets were still healing. Headline CPI slowed to multi-year lows early in 2025, and the State Bank paused rate cuts in March while acknowledging purchasing power remained under strain – one reason the bank signalled it would likely resume easing once stability firmed. In short, even as prices stopped racing ahead, consumers did not immediately return to pre-inflation buying habits, especially for discretionary treats.

That backdrop helps explain why a household favourite could have a slower year. Cocomo is explicitly positioned by Ismail as one of the flagship brands in the biscuits portfolio; if families are buying fewer premium-ish snacks at the margin, the pressure shows up in the parent company’s sales sheet first.

Ismail Industries is a study in local brand-building over nearly four decades. The company began with CandyLand in 1988, laying the foundations for what is now the country’s largest confectionery manufacturer. Bisconni followed in 2002, bringing a focused push into biscuits and cookies. The group verticalised in 2003 with Astro Films, a packaging division producing BOPET, CPP and BOPP films, and launched SnackCity in 2006 to compete in savoury snacks, beginning with ridged potato chips under the Kurleez label. Most recently the company added Ghiza Flour in 2022, reflecting another layer of backward integration and exposure to staple foods. Each of these milestones is traced on the company’s own corporate timeline.

The mix effectively gives Ismail

Industries two engines. The first is consumer-facing – CandyLand for sugar confectionery, Bisconni for biscuits and cookies, SnackCity for chips and other savouries. The second is its packaging arm Astro Films, which supplies flexible films domestically and to export markets, and helps the group manage input costs and quality across the food portfolio. That structure offered some insulation in 2025: where the parent (food) business saw sales decline, the group still posted higher net sales, thanks in part to the non-food packaging line and the broader perimeter of consolidation.

Within this history sits a less heralded strategic advantage: a distribution footprint that touches everything from big-box modern trade to the most fragmented kiryana networks. The company’s long investment in trucks, merchandisers and point-of-sale branding keeps shelf space “sticky”. But in a year when households traded down or consumed less, even the best distribution system cannot fully offset the impact on volumes – a reality reflected in the higher selling and distribution spend noted above.

CandyLand (confectionery). CandyLand remains the original pillar. The division spans jellies, chocolates, marshmallows, candies, toffees, chews, lollipops, gums, milk chocolates, spreads, brittles, truffles and bunties, anchored by some of Pakistan’s most recognisable names – Chilli Mili, ABC Jelly, Funny Bunny lollipops, Puffs marshmallows, Fanty, Buttons, and more. That breadth lets the company play across price points and packs, an important lever when consumers are price-sensitive and shopping trip sizes shrink.

Bisconni (biscuits and cookies). Launched in 2002, Bisconni has grown into a mass-market stalwart across cookies, sandwich biscuits and wafers. The portfolio includes Rite (which helped pioneer the “black biscuit” sandwich segment), Chocolate Chip Cookies, Chocolatto, Novita, and, crucially, Cocomo – which the company identifies as a flagship brand and a nostalgic favourite for a generation that grew up on its chocolate-filled bites. The brand’s positioning – small treats that feel a notch above a plain biscuit – cuts both ways: it thrives when consumers are trading up, but it can be among the first to feel a squeeze when households trade down or ration snack spend.

SnackCity (savoury snacks). The SnackCity division, established in 2006, built scale around crinkle chips and has marketed itself with a stable of brands including Kurleez, Chillz, Fillz and Smax. SnackCity’s growth over the past decade gave Ismail Industries a second consumer leg to stand on beyond sweets and biscuits, and – in years

when consumers shift cravings from sweet to savoury – helps the group balance category risks.

Astro Films (flexible packaging). Astro manufactures BOPET, CPP and BOPP films, supplying both internal needs and external clients across the region. While not a direct consumer brand, Astro’s performance matters for the group P&L, especially in periods when food volumes soften; it also gives the group a measure of control over packaging costs and innovation cycles.

Ghiza Flour and other adjacencies. The Ghiza unit focuses on milling and staples, further diversifying the business. Together with Astro, it extends Ismail Industries’ reach beyond impulse snacks into everyday pantry items – useful ballast when confectionery volumes wobble.

The arithmetic of the year is straightforward. In the core parent company, sales were lower, gross profit was thinner, and profits dipped, even though finance costs actually fell compared to last year. Taxes and levies rose, and the company spent more to defend shelf space. The group showed higher net sales but lower profit, underscoring that across the perimeter the squeeze on margins was real. Each of these points is drawn directly from the financial statements released to the Pakistan Stock Exchange.

Layer on the macro narrative, and the picture sharpens. Pakistan’s inflation slowed to multi-year lows into early 2025, and the central bank paused its rate-cut cycle in March with a nod to still-weak purchasing power. When households are repairing balance sheets after a brutal inflation shock, discretionary snacking is the kind of spending that gets dialled back first – one reason biscuit makers across the region typically watch volumes lag the macro turn by a few quarters. In that sense, the algebra behind our headline is as much about timing as taste: Cocomo, by the company’s own account a flagship product, sits exactly in the segment that families trim when they tighten belts.

If there is a silver lining, it is that Ismail Industries retained the financial flexibility to pay a cash dividend and keep investing in brands across categories. With inflation now cooler and rates well off their 2023 peaks, the company’s 2026 outlook will hinge on whether real wage growth and consumer confidence recover in time for the high season for sweet and savoury treats. For now, the 2025 report card reads like a classic post-inflation year: strong brands, softer volumes – and a reminder that even beloved names like Cocomo can feel the pinch when the nation’s wallets are still catching their breath. n

Opinion

Osman Niazi

Pakistan’s Tax Myth: It isn’t

the

people, its the government

Pakistan’s government officials often repeat the same tired line: “Pakistanis don’t pay taxes.” It’s a narrative designed to shame citizens while distracting from the real problem: a government addicted to wasteful spending in one of the world’s poorest countries.

This narrative is repeated so frequently that it has become accepted wisdom. Yet a closer look at the data tells a very different story. Pakistan’s tax-to-GDP ratio is broadly in line with countries of similar income levels. The real problem lies not with citizens but with the state’s inability to control its bloated expenditures and generate sustainable economic growth.

The numbers tell a very different story.

Pakistan vs. SAARC: The reality on taxes

According to the OECD’s Revenue Statistics in Asia and the Pacific (2025) and World Bank data, Pakistan’s tax-toGDP ratio in 2023 was 10.5%. How does that compare to our neighbors?

What the numbers really show

According to World Bank data and recent official reports for fiscal year 2024-25, Pakistan’s tax-to-GDP ratio stands at about 10.6%, with a GDP per capita of approximately $1824. At first glance, some argue this is “too low.” But

context matters. When compared with countries of similar income per capita, Pakistan’s ratio is not an outlier:

• Pakistan: ~10.6%, GDP per capita ~$1,824

• Sri Lanka: ~9.9%, GDP per capita ~$3,833

• Bangladesh: ~6.56%, GDP per capita ~$1,500–$2,000

• Nepal: ~19.1% (2018), GDP per capita ~$1,399

• India: ~13.5%, GDP per capita ~$2,500–$3,000 (approximate)

• Maldives: ~23.5%, GDP per capita over $10,000

This shows a simple truth: Pakistan is not an outlier. Its tax effort is higher than Bangladesh’s and almost identical to Sri Lanka’s. India and Bhutan are somewhat higher, while Nepal and Maldives are special cases — Nepal has unusually broad tax coverage, and Maldives extracts heavy revenues from its tourism-driven economy and is not comparable as its GDP per capita is much higher.

So when the government points fingers at “tax-evading Pakistanis,” they are ignoring that our tax ratio is in line with peers of similar income levels.

Why GDP per capita matters

Tax collection capacity is fundamentally linked to the economy. Low-income countries like Pakistan or Bangladesh simply do not have the same taxable surplus as wealthier nations. Attempting to squeeze more out of the existing base without first growing incomes risks stifling economic activity and fueling resentment.

This is why comparisons with the West are unreasonable. These figures clearly demonstrate that Pakistan’s tax-to-GDP ratio is within the expected range

The author is the founder of the Goldman Consortium

for lower-middle-income economies. It is unreasonable to compare Pakistan to Western countries with ratios above 30–40%. Doing so is like demanding that a low-paid worker contribute the same absolute tax as a CEO—it ignores differences in income and capacity.

The Real Crisis: Spending without restraint

If Pakistan’s revenues are in line with countries of similar GDP per capita, why do we face constant fiscal crises? The answer is simple: waste and mismanagement. Just look at the following realities:

• Debt servicing alone eats up more than half of federal revenues.

• Government operations remain bloated, even while development spending (schools, hospitals, infrastructure) is cut year after year.

• State-owned enterprises like PIA, Pakistan Steel, and the power distribution companies drain hundreds of billions annually in subsidies and bailouts.

• Elite privileges remain untouched: tax exemptions for powerful lobbies, luxury benefits for politicians and bureaucrats, and perks that ordinary Pakistanis can only dream of.

In short, the government collects as much as can reasonably be expected from a poor, largely subsistence economy. It is the spending side that is completely broken.

Hoodwinking the people

The narrative of “Pakistanis don’t pay taxes” is not just misleading — it’s dangerous. It erodes trust between citizens and the state while giving officials cover to raise regressive taxes (like GST on food and fuel) that hurt the poor the most. Instead of scapegoating the people, the government must confront its own excesses. A poor country cannot afford palatial government residences, endless motorcades, perpetual bailouts of failing state firms, and unchecked expenses.

Growing the real economy is the only way out. You cannot tax your way out of poverty. Sustainable revenues come only when the real economy grows. That means more industries, which means more jobs and more taxable income. This translates to a stronger private sector which means more corporate taxes. Higher exports and investment mean more revenue without burdening ordinary citizens. Without growing the real economy, attempts to raise taxes will simply push people further into poverty while government waste continues unchecked.

The debt trap

Pakistan has been borrowing for decades, and the compounding effect of interest has created an exponential debt trap. Servicing debt now consumes a massive

portion of government revenues, leaving little for development.

If we do not put our house in order, the risk is that continued money-printing to cover deficits could trigger hyperinflation. Once that spiral starts, the value of money collapses, savings are destroyed, and ordinary people suffer the most.

This is why Pakistan must learn to live within its means. High government waste, unchecked borrowing, and runaway spending in a poor country will only bring the system closer to collapse.

The one thing we do not have at all is the luxury of time. It is imperative that the country cuts government waste at every level, prioritises efficiency and productivity in spending, and focuses on real economic growth rather than endless borrowing.

If Pakistan is to stabilize, the debate must shift. The government and the media alike must stop blaming taxpayers. Our tax-to-GDP ratio is within the regional norm and norms of similar tax to GDP ratio countries. This needs to be followed up with cutting waste. Slash elite privileges, restructure SOEs, and rationalize non-development spending and government waste at all levels. And finally we must prioritise growth. Only a larger real economy can sustainably expand the tax base without crushing citizens.

Until then, the tax debate will remain a convenient cover story — while the real problem of government waste in a poor country continues to push Pakistan deeper into crisis. n

With merger completed, Secure Logistics poised to capture growing value from e-commerce delivery business

Company aims to enter logistics financing and last-mile delivery, entering a space that has seen many venture-backed startups

Profit Report

Secure Logistics Group Limited (SLGL) has completed the longplanned combination with Trax Online, fusing two very different operating models into a single platform designed around Pakistan’s e-commerce boom. The Islamabad High Court sanctioned the scheme on 5 May 2025, a milestone that followed regulatory clearance from the Competition Commission of Pakistan (CCP) two days later. The CCP explicitly defined the relevant market as “courier and e-commerce logistics services,” underlining the competitive stakes in last-mile and fulfilment.

Management frames the merger as a classic asset-heavy meets asset-light pairing: legacy SLG brings trucks, traditional contract logistics, IoT and security; Trax contributes nationwide tech-enabled last-mile, warehousing and a dense merchant network. An equity research note from Chase Securities, a brokerage firm, detailing SLGL’s post-merger positioning puts identified cost and revenue synergies at Rs400 million, now under execution with most benefits expected by April 2026.

The combined group plans to operate through five legal entities, including SLG (transport), LogiServe (tech/IoT and now a licensed NBFC), and Sky Guards (security). By year-end 2025 the footprint is slated to span 200 offices across 60 cities, with 300-plus B2B and 9,000-plus B2C clients. For e-commerce merchants, that means broader reach, higher delivery density and a single counterparty

that can pick up, store, ship, collect cash and – crucially – advance working capital against receivables.

In short: the legal integration is complete, the operating thesis is clear, and the merged SLGL-Trax now looks purpose-built to chase growth in Pakistan’s parcel economy – particularly in a market where most online orders are still cash-on-delivery (COD), and where merchants care as much about how fast they get paid as how quickly parcels arrive.

Legacy SLG is the asset-heavy anchor. It contributed the commercial fleet, multiyear relationships in industrial and FMCG logistics, and steady cash flows from transport, security and IoT monitoring. The plan is to scale the fleet to 500–600 vehicles, emphasising medium-haul and last-mile segments – where e-commerce volumes now pool. The company has run TIR-certified trial shipments to Tashkent, signalling a regional lane strategy into Central Asia with 20–25% of fleet capacity earmarked for cross-border moves over time. That cross-border ambition mirrors broader Pakistani logistics experiments with TIR, which can slash transit times on lanes to Uzbekistan and Kazakhstan by avoiding repeated border unloading.

Trax, by contrast, is the asset-light, techfirst network that grew up with Pakistan’s online sellers. It brought nationwide last-mile delivery, warehousing, and a merchant-facing platform tuned to the nuances of COD settlements and return flows. The combined group is converting three warehouses into full-scale logistics hubs to stitch linehaul, sortation and last-mile together. To densify

urban coverage, SLGL is procuring 100 Suzuki Ravi mini-trucks for city routes and piloting EV motorcycles backed by charging infrastructure in Lahore – small signals that the group is experimenting to get cost per drop down and delivery speed up in congested cities.

Under the hood, the merged company has built a proprietary IT stack spanning logistics, IoT, fintech and merchant APIs. A fresh SAP ERP rollout will now extend across the legacy SLG estate, while a new mobile client stack – the Pulse app – aims to give both enterprise and SME shippers real-time visibility and self-service controls. The result is an operating model that can flex between contract logistics SLAs for corporates and high-velocity, pay-asyou-ship workflows for marketplace sellers.

The post-merger roadmap is not just operational. It is financial. Management guidance points to revenue expanding from Rs2.5 billion in 2024 to Rs15 billion by 2029, with e-commerce and fintech together accounting for 45% of operating profit in 2026 and 70% by 2029. Net margins are projected to stabilise in the 20–24% band – high by local logistics standards, but plausible if higher-margin fintech and platform fees scale alongside delivery. The management estimates table on page 2 of the note lays out a staged progression: PAT of Rs1.8 billion targeted for 2026, EBITDA stepping up as warehouses are converted, and opex kept in check as software carries more of the workload.

If Pakistan’s e-commerce is to grow beyond a COD treadmill, merchants need faster, more predictable cash flows. SLGL’s answer is to embed finance where the parcel is:

its subsidiary LogiServe has secured an NBFC licence and will commercially launch on 1 October. Operating from the Islamabad Special Technology Zone, LogiServe benefits from an eight-year corporate tax holiday – breathing room to focus on product rather than tax planning. The proposition is simple: instant or near-instant settlement to the merchant once a shipment is delivered, funded via short-term working-capital lines from banks and high net-worth investors, with the receivable tied to SLGL’s delivery and collections data. In a February pilot, the platform processed Rs70 million in weekly credit lines across 60–70 vendors. Management calls the NBFC a “value multiplier”, projecting it could contribute 15% of operating profit by 2029.

That solution is tailored to a market where about 93% of transactions still rely on COD. COD is popular with consumers, but it ties up merchant cash, heightens return risk and lengthens reconciliation. A logistics-embedded NBFC can compress that working-capital cycle: the same company that knows a parcel’s delivery status can safely advance against it, price risk more precisely, and settle faster. Over time, that can expand average order sizes and inventory turns for SMEs – especially the fashion, electronics and beauty sellers that dominate Pakistan’s online trade.

There is also a strategic moat. Fintech products (invoice discounting, merchant accounts, payment gateways) raise switching costs far beyond per-parcel rates. If LogiServe nails underwriting and collections – two skills its parent exercises every day on the road – the take rate can rise without scaring merchants off, because the value is cash-flow speed, not just delivery speed. Early signs – licensing done, pilot data in, platform wired to ops –suggest SLGL understands that the fight for e-commerce logistics profits will be won as much in the ledger as on the last mile.

The broader context is a payments landscape splitting rather than simply shifting. According to Profit’s cover story “The bifurcation of payments,” digital payments’ share of transaction value climbed to 9.3% in the third quarter of 2024, up from 0.3% in 2016 – roughly a 31x jump in market share in eight years. Yet cash still accounted for 35.7% of the value of all transactions in that period, down only modestly from 38.4% in 2016. In other words, digital is growing fast, but cash remains entrenched – a reality merchants live with every day.

That bifurcation plays directly into SLGL’s strategy. On the one hand, rising app-based payments and Raast transfers are slowly tightening the loop between sale and settlement, making reconciliation cleaner for larger brands and marketplaces. On the other,

COD remains the dominant consumer preference, especially beyond large metros and for first-time or low-ticket buyers. A logistics firm that can collect cash reliably, settle quickly and finance the gap is a natural winner while payments modernise in increments rather than leaps. Recent State Bank data show continued growth in digital channels – retail transactions up double digits and mobile payments accelerating – which will increase pressure to modernise merchant back-ends and delivery platforms alike.

As e-commerce order volumes spread into tier-two cities, logistics density matters. That is where SLGL’s plan to add small urban vehicles, convert warehouses into hubs and roll out Pulse to merchants could converge: more zip-codes served next-day, faster cash conversion, and a tech layer that gives SMEs the kind of transparency only big brands enjoyed a few years ago. If execution keeps pace with guidance, the company could be one of the few local players able to monetise both sides of the bifurcation: the COD-heavy present and the digital-leaning future.

Pakistan’s e-commerce logistics market is crowded and consolidating. PostEx – a fintech-cum-logistics player – grabbed headlines when it acquired Call Courier in 2022, pitching itself as the largest e-commerce service provider and explicitly building a loan book on the back of COD flows. That deal crystallised a formula now surfacing across the sector: combine fulfilment with finance and own the merchant wallet, not just the parcel.

Rider, a Y Combinator-backed start-up focused on tech-led last-mile, has explored acquisitions such as BlueEx, the only listed express logistics company in Pakistan – another sign of the jostling to build national networks with enough density to sustain fast SLAs at sustainable unit economics. Whether or not any specific deal closes, the direction of travel is clear: consolidation to achieve scale, and software to squeeze more stops per route.

The incumbents are hardly standing still. TCS, Pakistan’s best-known courier, runs a full suite of COD and COD Plus products, and highlights its TIR credentials for regional freight – useful for brands that straddle domestic e-commerce and cross-border sales. Leopards Courier markets a broad e-commerce stack and has recently partnered with fintechs to digitise merchant payments. M&P (Muller & Phipps) continues to trade on its national network and COD capabilities, attractive to SMEs that prioritise reach over bells and whistles. Even Pakistan Post pitches e-commerce parcel solutions and bulk-rate COD, an option for price-sensitive sellers. The result is a market where merchants can – and do – multihome across carriers, awarding more volume to whoever clears cash faster and loses

fewer parcels. Against that backdrop, SLGL’s LogiServe may be its most important differentiator. Rivals have tinkered with financing – PostEx most prominently – but few have the combination of a fresh NBFC licence, a tax holiday, and a logistics platform already instrumented for risk scoring. If SLGL can keep non-performing exposures in check – leveraging delivery and return data to price risk daily – it can lift merchant retention and take rate without igniting a price war on per-parcel fees.

On the upside, integration is largely complete, capex needs for the next leg are modest (the note guides Rs100–120 million this year for hub conversions and the city-delivery fleet), and the merchant-finance engine is primed for launch. If guidance holds, the operating-profit mix tilts towards higher-margin e-commerce and fintech by 2026, while cross-border lanes to Uzbekistan and Kazakhstan open a second growth leg beyond domestic parcels. The management estimates also show a more than trebling of EBITDA by 2027 as the asset-light components scale.

Risks mirror the strategy. First, credit risk: COD-linked advances are attractive until returns spike or fraud circulates through seller networks. Second, execution risk on IT and ERP rollouts – SAP transitions rarely go perfectly and can temporarily distract frontline teams. Third, competitive intensity: if incumbents cut COD settlement times or underwrite merchant receivables themselves, pricing power at the parcel level may remain elusive. And finally, macro: fuel costs, import frictions for vehicles and parts, and regulatory shifts on payments can all sway unit economics at short notice.

For now, the numbers and the narrative rhyme. SLGL finished CY24 with EPS of Rs2.4, up from Rs2.1 a year earlier, even before most merger synergies and fintech revenues arrive. The unconsolidated ledger shows operating profit and after-tax earnings up solidly yearon-year, while the consolidated outlook (revenue targets through 2029) paints a picture of a logistics-plus-finance platform rather than a traditional haulier. The merchant offer – ship, get paid fast, borrow against receivables, and see everything in one app – is exactly what Pakistan’s SME e-commerce base has been waiting for.

Pakistan’s payments future is arriving, but unevenly. Digital volumes and values are climbing; cash remains stubborn. The winners in delivery will be those who can live comfortably in both worlds – collecting cash with discipline while settling digitally with speed. With the Trax merger closed, the NBFC licensed, and a clear plan to blend asset-heavy backbone with asset-light velocity, Secure Logistics looks set to compete for that prize. n

Pakistanis are buying more batteries, but Atlas sees sales slump

The company’s older lead acid technology is simply unable to keep pace with China’s lithium ion battery imports

Profit Report

Atlas Battery Limited closed the year to 30 June 2025 on the back foot. Sales slipped to Rs35.2 billion from Rs41.5 billion the year before – about a 15% decline – dragging down profitability across the income statement. Gross profit fell to Rs3.96 billion, operating profit halved to Rs1.81 billion, and after taxes the company reported a sharply lower profit for the year of Rs91 million, translating into earnings per share of Rs2.60 versus Rs38.37

last year. The board recommended no cash dividend or bonus/right shares – a notable pause at a company that in better years rewarded shareholders more generously.

The numbers arrive at a paradoxical moment. Pakistanis are buying more batteries than ever – just not necessarily the ones Atlas dominates. Imports of lithium-ion packs – principally from China – are climbing fast as homes, shops and factories bolt storage onto solar rooftops and as industry pilots larger battery-energy-storage systems (BESS). In that context, the company’s revenue contraction looks less like demand evaporating and more like domestic

lead-acid makers losing the growth segment to imports in newer chemistries.

Independent research suggests Pakistan imported around 1.25 GWh of lithium-ion battery packs in 2024 – enough storage to shave meaningful load from the grid if fully deployed – and could reach 8.75 GWh by 2030 on a “business-as-usual” trajectory. That wave is overwhelmingly supplied by Chinese manufacturers, who have scaled capacity and cut prices as part of a global glut.

Local business press and analysts paint the same picture: a fast-growing appetite for storage as both a hedge against outages

and a way to arbitrage peak tariffs. Despite Pakistan’s import duties and taxes that still keep storage prices higher than they might otherwise be, the case has strengthened on the back of falling global cell prices and relentless rooftop solar adoption.

At the industrial end, the pattern is clearest. Lucky Cement is commissioning what is billed as Pakistan’s largest BESS – 20.7 MW/22.7 MWh – to stabilise its 34 MW captive solar plant, a project supplied by a Chinese battery champion and emblematic of how factory-scale users are pairing solar with storage. These are precisely the kinds of applications where lithium-ion’s energy density and cycling advantages dominate.

Solar itself has exploded. Pakistan reportedly imported about 17–19 GW worth of PV modules in 2024, with monthly additions continuing into 2025; batteries inevitably follow panels as homeowners and businesses look to extend solar’s utility into the night and to ride through grid disturbances. Policymakers are scrambling to respond to the grid and tariff implications of such a rapid shift – but the underlying consumer logic (cheaper hardware, better control) remains powerful.

Electrified transport is a smaller – but rising – driver of storage demand. Indus Motor began local assembly of the Corolla Cross hybrid in late 2023, signalling the auto sector’s pivot towards electrified drivetrains, while BYD has disclosed plans to assemble EVs in Pakistan as early as 2026. Even if pure EV volumes are nascent today, the ecosystem effects –from charging to auxiliary storage – are already nudging the market.

Taken together, these shifts explain why the battery market in Pakistan is growing even as Atlas’s top line contracts. Growth is concentrated where imported lithium-ion dominates (rooftop-plus-storage, C&I microgrids, pilot BESS, and the early EV/HEV transition), not in Atlas’s core legacy niches.

Atlas’s product catalogue centres on lead-acid – from automotive starter batteries to deep-cycle units for UPS/solar and newer tubular designs aimed at longer life in cycling applications. In December 2024, the company launched a tubular “Energy Core” series, explicitly pitched at the solar-storage crowd and indicating a strategic recognition that cycling durability – not just cold-cranking amps – is the new battleground.

By contrast, most of the battery hardware entering from China is lithium-ion (in various chemistries), which offers higher energy density and longer cycle life, translating into smaller footprints, lighter packs, and better round-trip efficiency – advantages that matter for wall-mounted home systems, factory microgrids and electric drivetrains. Global energy agencies note that lithium-ion’s cost

and performance gains over the past decade are what propelled it to dominance in stationary storage and mobility.

That does not make lead-acid obsolete. The chemistry remains robust, affordable, and exceptionally recyclable (with a near-closedloop system in mature markets). It tolerates abuse and low temperatures well, and for many backup roles – think starter, lighting and ignition (SLI) in vehicles, gensets, small UPS – lead-acid still wins on upfront cost per installed kilowatt-hour. The U.S. Department of Energy highlights these attributes even as it acknowledges the lower energy density versus lithium-ion.

Where Atlas faces pressure is in use-cases that cycle daily (solar-plus-storage; time-of-use arbitrage) or demand compactness and weight savings (EVs/HEVs). Here, lithium-ion’s energy-per-volume and energy-per-weight advantages are decisive, and its lifetime cost per delivered kilowatt-hour increasingly outcompetes legacy chemistries as prices fall. That is precisely where Chinese imports are strongest – and where Atlas’s new tubular and deep-cycle lines will have to prove their mettle if the company is to defend share.