16 In Gilgit Baltistan, farming is slowly dying out. Meet the school teacher and banker fighting back

22 This year’s mango crop is dying from disease. How deadly is it, and is there a way out?

24 How the Wilmar-Unity partnership turned into a standoff

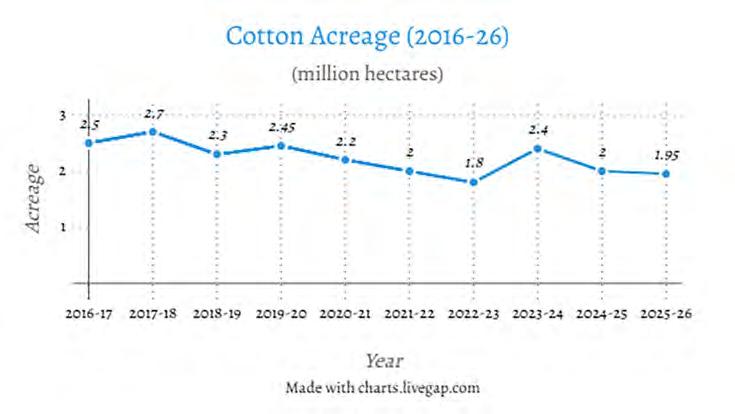

28 The Punjab govt is pushing farmers to grow more cotton. Can they hit their 7 lakh acre target?

31 Officials claim Islamabad Safe City Cameras are not using Israeli software … any longer

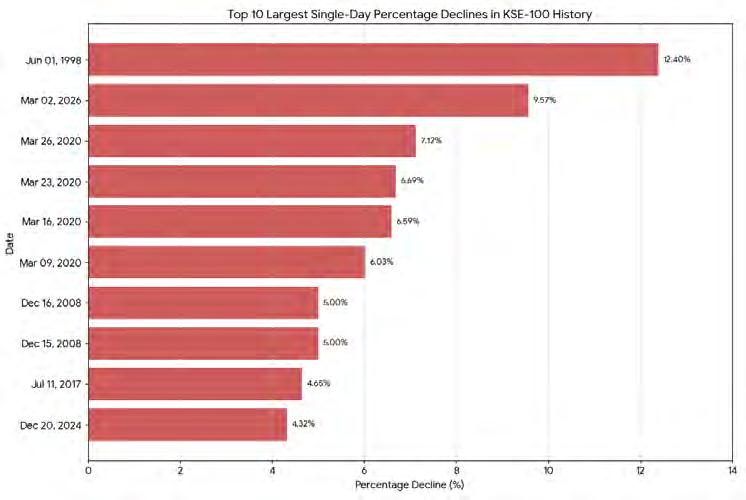

32 Panic selling or planned panic? PSX plunges 9.57% in unprecedented 16,000-points single-day slide

33 Why Strait of Hormuz turbulence matters for Pakistan

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Usama Liaqat Shahab Omer | Zain Naeem | Nisma Riaz | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing: Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

The cleanup at Zarai Taraqiati Bank

In barely three years, ZTBL’s finances paint the picture of a bank that is well and truly on the mend. But has this been a thorough renovation or a case of sweeping things under the rug?

By Abdullah Niazi

There are times when an organisation is a mess. There are other times when it can be a big mess. On rarer occasions one can go so far as to call them a train wreck. Perhaps if the situation is urgent enough the term dumpster fire can also be thrown around.

In the case of Zarai Taraqiati Bank Ltd (ZTBL), it would not be a stretch to say it was a trainwreck on repeat taking place inside a dumpster fire large enough to contain multiple passenger trains.

Founded in 1952 as the Agriculture

Development Finance Corporation, ZTBL has gone through multiple rounds of mergers, rebrands, bailouts, and major slumps. For nearly the entirety of its existence, the bank has served as the primary vehicle used to provide financing to the country’s farmers — the individuals that make up the single largest sector of Pakistan’s GDP. Over the decades it has existed, its most impressive feature has been the massive headquarters near Zero Point in Islamabad. The building is considered by many to be Islamabad’s first skyscraper, and the curvature architecture behind the twin buildings is still an iconic part of the federal capital’s skyline.

But for most of its existence the pretty building is the extent to which good things

could be said about ZTBL. For years the bank has served as an example of everything that can be wrong with a state owned institution. It has an abysmal history of loan recovery (something that is usually considered quite important in the industry), it has regularly posted losses, appointments are often politically motivated, their branch network is in shambles, and the entire business model is dependent on the government disbursing subsidised schemes to farmers through it.

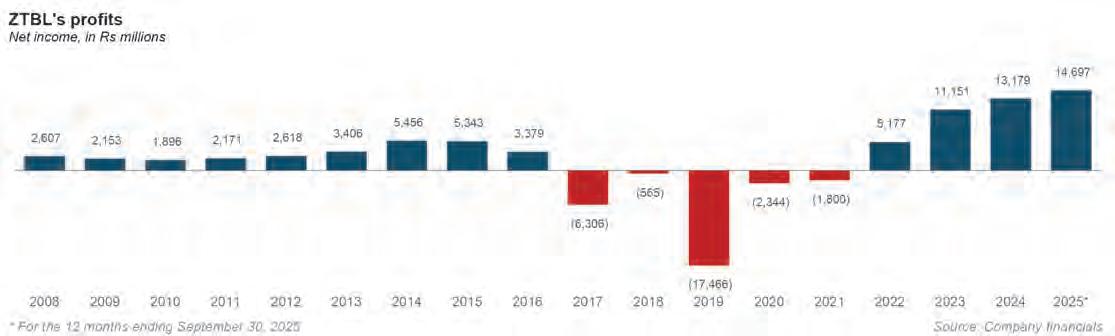

But all of that seems to have changed over the past five years or so. Look at the headline numbers for ZTBL in the recent past and they tell the story of a historic turnaround. In December 2022 ZTBL reported its accumulated losses

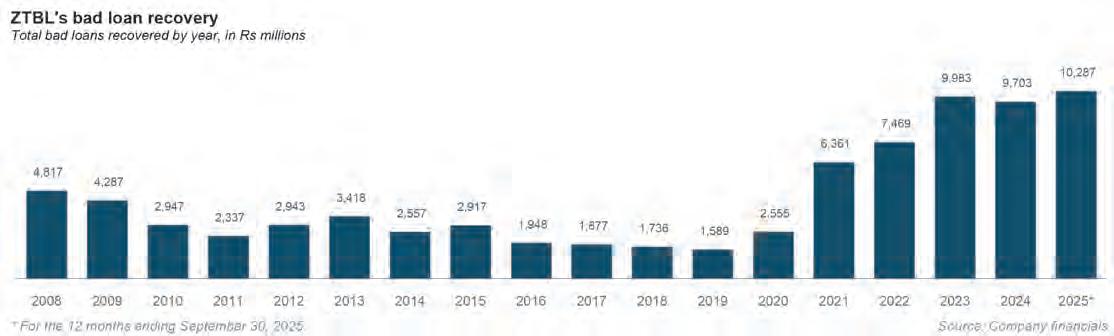

had reached Rs1.2 billion. By December 2023, they had reversed these losses with an accumulated profit of Rs10.34 billion. This accumulated profit rose to Rs15.34 billion in 2024, and was already at Rs22.4 billion by the period ending September 30, 2025, the latest for which financial statements are available.

Behind the rising profits are some serious numbers. In the two years from June 2023 to June 2025, ZTBL reduced its portfolio of infected loans by Rs13.45 billion. Their regular portfolio increased by Rs32.92 billion, and they recovered Rs30 billion in markup on their infected portfolio.

The turnaround has coincided with the tenure of ZTBL’s new President, Tahir Yaqoob Bhatti, who took charge in August 2023. On the surface his tenure seems to have achieved miraculous results. But go beyond the headline numbers and it becomes clear that the story is not so much that of a phoenix rising from the ashes and more one of a dedicated and aggressive cleanup.

Considering ZTBL is one of the many state owned entities that is also up for privatisation, and is actually quite high on the priority list, it makes sense that the government would want to whip it into buyable shape. The question is, to what extent did they go to in order to clean out the mess?

Roll up your sleeves

Tahir Yaqoob Bhatti began his career as a trainee officer at National Bank and worked his way through the industry.

After 11 years at NBP, where he rose to Branch Manager, he spent time at the Gulf Commercial Bank and Saudi-Pak Commercial Bank before a decade-long stint at Askari Bank, where he left as Executive Vice President to join Allied Bank where he spent four years as a Group Chief.

This is usually the stage in a banker’s career where they take aim to become the President or CEO of a bank in their own right. In December 2021 Mr Bhatti was appointed President of the Punjab Provincial Cooperative Bank — the oldest financial institution of the country established in 1924. The bank he took over, however, was in shambles. Far from the

plush experience bankers might expect as the top-dog anywhere, PPCB was a fire that needed putting out.

Set up during the Raj, the PPCB was a co-op bank meant mostly to provide financing for agriculture and housing in rural areas. Over the decades it had become slow, weighed down by pension bills amounting in the billions, and a non-existent recovery team that allowed borrowers to never pay back a dime and get away with it without any consequences. For all intents and purposes it was a middle-man taking money from the government and giving it to people as handouts.

So what did Mr Bhatti do upon arrival? He rolled up his sleeves and began sweeping. What followed was a gargantuan effort. Bhatti made trips to cities all over Punjab to inspect property owned by the bank that had fallen into disrepair. Shops that were valued at Rs50 lakhs were cleaned up and sold for Rs2 crores in some instances to give small injections of capital to the bank’s books. Hiring was ramped up and an aggressive effort was made to recover loans that had already been written off.

A lot of the written off loans were recoverable — but because it was a government bank no one had ever really tried. Over time, non-performing loans at PPCB fell from Rs2.5 billion to Rs1.7 billion. Accumulated losses Rs1.5 billion to Rs51.9 crores. Fixed assets, which had been stagnant at Rs7.1 billion for many years, rose to Rs15.4 billion.

It was by all measures an incredible story. New hiring, management changes, and some attention was all it took. The PPCB had been neglected for so long a mere crack of sunshine in its dingy halls brought one of Pakistan’s oldest institutions back to life. Which is why it is not surprising that barely 21 months into his stint at the PPCB, Mr Bhatti was tapped to be President of ZTBL.

Go with what works

PPCB, it seems, was designed as a training ground for the job up ahead. ZTBL had pretty much the same problems as PPCB but on a much larger scale. For decades its only purpose had been to work as a vehicle to

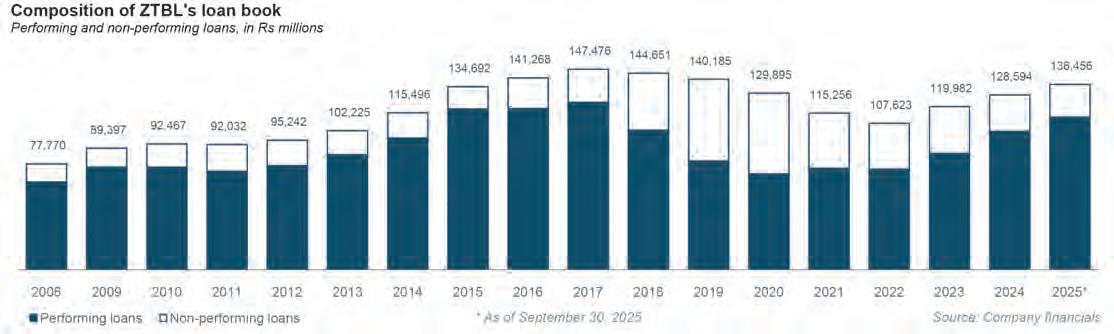

provide agricultural subsidies. Over time ZTBL had garnered the highest accumulated Non Performing Loans at more than Rs100 billion with mark up included. There was no mechanism in place to monitor these loans, no department to recover loans that had been charged off (meaning the bank had declared them unrecoverable and taken them off their balance sheets — this will be particularly important later in the story.)

From 2017 to 2021 the bank accumulated losses of Rs28.88 billion. Several litigations with revenue authorities since 1991 were pending involving tax claims of Rs95 billion. The bank had no digital products or services, no operations manual, no one really knew who they were reporting to, and in a network of 501 branches there were a grand total of 49 ATMs, not all of which worked. For all intents and purposes ZTBL was considered little more than a government owned lending agency.

Look under the hood and it became clear why the once proud bank had come to this point. Out of 501 branch managers, 232 had been promoted to their position after starting their career as peons or guards. And no, this was not because of some educational initiative. It was simply the fact that over time these peons and guards were given other responsibilities, they picked up the basics and eventually rose to manager.

ZTBL, you see, is not an ordinary bank. It has its branch network in rural areas and is governed from that big shiny building at Zero Point. The point is to make it easy for farmers to approach the bank and ask for loans. The branch network is supposed to report back to Islamabad, which then gives directives on any restructuring of loans or how to conduct recoveries if farmers are not paying back. Because the branch network has grown weak and jobs are either a legacy cost or appointments are made as favours, corrupt practices have run rife. According to an internal document of the bank seen by Profit there are 1,060 fraud cases amounting to Rs1.53 billion pending regarding the bank.

The situation at ZTBL has been described by insiders as “marked by weak accountability, demotivated staff, an ambiguous and overlapping organogram, and major communication gaps between the head office and field.”

Around 2023 was also the same time that the government began to consider ZTBL as a prime candidate for privatisation. Along with PIA, it has regularly featured in the privatisation agenda. And much like PIA, to make the bank digestible to any potential buyer, it was important to whip it into shape. The turnaround at PPCB made Tahir Bhatti the foremost candidate for the job.

The strategy for ZTBL was simple: do what has worked before. The first step was going on a hiring spree to bridge the gap between the field and headquarters. Two batches of 600 mobile credit officers and a hundred branch managers were hired to beef up the bank. There was also a need to hire some very basic employees that banks need to have: 13 experienced professionals for the audit department (yes these were missing before), four new managers with banking experience dedicated to NPLs and charged off loans, and 19 new regional business heads to add a layer between the field offices and Islamabad.

With the team hired and a brief restructuring in place which involved basic communications such as creating a new, independent, SAM department for loan recoveries, ZTBL was off to the races. Once again the methodology was the same. The new ranks were dispatched to find and recover loans that had been given and never followed up on, the bank pursued property it had in different areas which was not yielding any results, and on top of this regular lending increased off the back of the Kissan Package and increased government interest in financing farmers and the agricultural sector.

How big is the rug

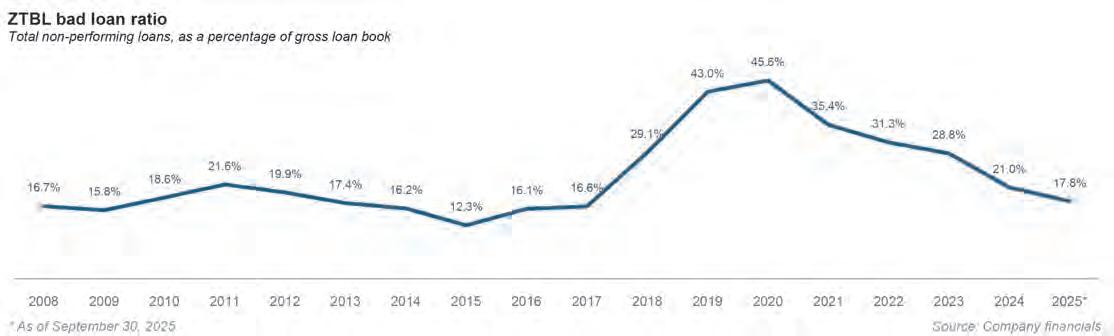

Look at the headline numbers and it makes ZTBL look like the Comeback Kid. The techniques that worked over at PPBC have breathed new life into the financial statements of ZTBL. The infected portfolio has fallen from a peak of Rs60 billion in 2020 to Rs24.2 billion as of September 30, 2025, the latest period for which financial statements are available. About Rs40 billion has been recovered from the infected portfolio, net

income has gone from losses of Rs2.3 billion in 2020 to profits of Rs14.7 billion for the trailing 12 months (TTM) ending September 2025.

But these impressive numbers are not just the result of one man rolling up his sleeves and running a tight ship. Afterall, is it really possible to turn billions in accumulated losses over the course of decades into surging profits with some new hiring and encouraging words? Speak to Tahir Bhatti and he will tell you in painfully corporate jargon that this is the result of his belief in the “3Ps” — punctuality, passion, and productivity. The reality is that the resurgence of ZTBL is a combination of real, actionable, and easy reforms with what looks like an approach of picking up the mess and stowing it away for another day, and some of those improvements appear to have gotten underway even before Bhatti took over.

Profit’s analysis of ZTBL’s financial statements, annual reports, and reports by credit agencies show that the bank has regained equity and improved profitability by recovering older loans, reversing provisions, and possibly restructuring non-performing loans and starting to collect markup on them again. This does not have to take away from the turnaround, but it does present a more realistic picture of what the headline numbers mean.

Think of ZTBL’s financial statements like the floor plan of a very old hotel that is up for sale and being renovated while the guests continue living inside it. The entrance, the reception, and the lobby, are what everyone sees: the bank’s regular business of earning interest. Over here one can see marked success.

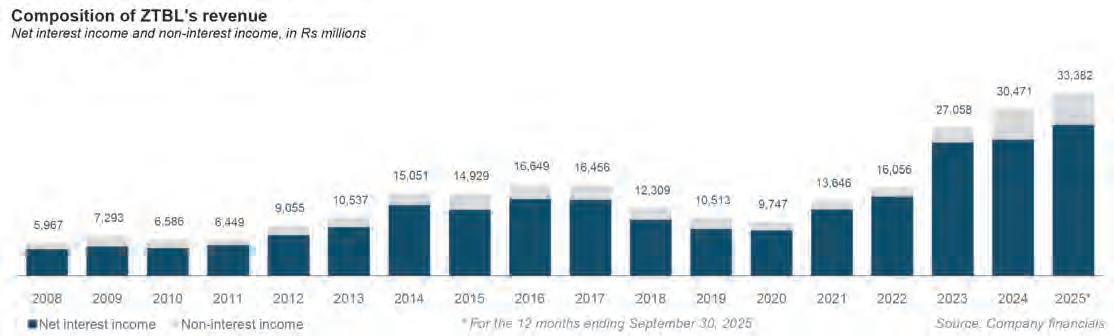

Net interest income, which is the amount by which the interest earned on a bank’s lending portfolio exceeds the interest it pays out to depositors, has been rising steadily for five years. It rose from Rs8.5 billion in 2020 to Rs27.8 billion for the TTM period ending September 30, 2025.

But then there is the messy part of the bank’s ledgers. To understand the storage cupboards, you only need three simple ideas:

1. An NPL is a room that has stopped paying rent. It still sits inside the hotel, on display, and everyone can see it is not working.

2. A charged-off loan is different. It is

also a room that has stopped paying rent, but it has been so long since the last time it paid any rent that the bank has simply given up. The squatter in the room treats the rent as a forgotten relic and the bank just reduces the number of rooms it has on its books so the losses from missed rent do not look too bad on the account book. (Essentially, the bank has accepted, on paper, that it may not collect in full, so it stops showing up as part of the “live” loan book in the same way. That does not mean it is forgiven or forgotten. Just put aside for now).

3. Provisions are money set aside for a rainy day in anticipation that some rooms will never pay again. In most years, provisions are a cost. They drag profit down because the bank is saving for trouble.

In 2020, provisions/write-offs at ZTBL were Rs1.3 billion. In 2021, Rs0.8 billion. Those are normal years in a difficult house: the owner is still setting money aside for repairs. Then the story changes. In 2022, provisions/write-offs turn negative at minus Rs3.7 billion. In 2023, minus Rs5.5 billion. In 2024, they plunged further to minus Rs11.8 billion, and for the TTM period (ending September 2025), the number was negative Rs14.1 billion.

What do these negative provisions mean? On the one hand it means ZTBL was reversing some of its written off loans by being able to collect the money that people owed from long ago, but nobody at the bank had previously been able to make them. And because they no longer had to make provisions for those, their overall financial health was improving in their financial statements.

It usually happens in one of two ways, or both at once: the bank releases money it had previously set aside because it now expects fewer losses than before, and/or it starts collecting cash from loans it had already treated as lost, so the recovery shows up as income. Either way, the accounts imply that the clean-up of old trouble has become a profit engine in its own right.

The provisions decrease because of what is happening inside the loan book. In 2021, the bank was carrying a heavy stock of problem agricultural loans. The notes from that year

show non-performing agricultural advances at Rs40.74 billion. If you stop there, the story looks like a straightforward burden: too many borrowers not paying. But 2021 also reveals the hidden architecture: ZTBL has a large pool of loans that have been taken off the balance sheet through provisions and are tracked separately as off-balance-sheet loans extinguished against provisions. At end-2021, that pool is disclosed at Rs44.46 billion, and the bank adds Rs11.01 billion of charge-offs in the year.

This is the key pattern to hold onto: the headline bad-loan number can decline at the same time as the off-balance “extinguished” pool increases. That is not necessarily wrong and can in fact be sensible housekeeping. But it does change what the improvement means. It tells you that part of the clean-up may be happening through re-categorising as much as through borrowers becoming healthy.

The year 2022 is where recoveries of written-off or charged-off bad debts grow to Rs7.46 billion, which is a big number relative to the bank’s profit line. In December 2021, profit before tax is shown at Rs1.7 billion. In 2022, profit before tax rises to Rs7.55 billion.

Put those together and the picture becomes vivid even for a non-banker: in 2022, the bank makes more money not only because it earns interest, but because the past starts paying it back and because the expected-loss machinery stops being purely a cost. Once again, within the financial statements it is not explicitly stated how much of this improvement is through recoveries and how much through shifting money between buckets. It is likely a combination of both.

There is another subtle clue in the notes that reinforces the idea of active management of classification. In 2021, the bank disclosed that it further classified and further de-graded loans based on borrower creditworthiness, with figures of Rs7.1 billion and Rs8.1 billion respectively. In 2022, the comparable figures are Rs3.7 billion further classified and Rs6.5 billion further de-graded.

For a lay reader, the point is not the technical definition of those terms. The point is

that the bank is not a passive observer watching loans go bad. It is actively adjusting classifications and quality buckets. In a clean-up phase, classification is not just measurement; it becomes part of management.

By 2023 and 2024, the narrative shifts again. In 2023 the gross markup explodes and the ratio line collapses to its lowest point, suggesting that the interest environment becomes extreme and the bank keeps a smaller share of what it earns as net interest. In that same period, provisions and write-offs remain negative, meaning the clean-up machine continues to support profits.

The 2024 annual report’s Special Asset Management (loan recoveries) section then tries to put a ribbon around this. It says NPL principal outstanding falls from Rs29.9 billion in 2023 to Rs25.2 billion in 2024, and charged-off principal outstanding falls from Rs36.0 billion to Rs33.2 billion. It reports recoveries of Rs25.9 billion against NPLs and Rs9.7 billion against charged-off loans, a total recovery of Rs35.6 billion from the infected portfolio.

It also notes that new additions into NPLs were much lower in 2024 (Rs20.9 billion) compared to 2023’s Rs35.5 billion. Read plainly, this is a bank saying two things at once. First, it is collecting. Second, fewer loans are slipping into default than before.

Peaking under the hood

The best way to understand the ZTBL recovery is that it is a combination of factors. One can say that a lot of the recovery came from the shifts between NPLs and write offs, but there is no denying that the overall regular loans improved and there was a massive host of recoveries as well. It is less the story of a dramatic miracle and more the story of a gritty, grinding, mop up job.

The exact nature of how this has been achieved is not clear. We have already detailed the organisational changes that have made this possible including fresh hiring, reorganisation,

focus on loan recoveries and all the other steps taken over the past few years. But beyond these are a few possibilities as to how this could exactly have been achieved.

One possibility is the straightforward one: borrowers are paying again. In an agricultural bank, that could be seasonal cash flows improving, better collection systems, or stronger enforcement. If this is the dominant driver, the recovery story is deeply real: the house is being cleaned because the residents are paying rent again.

A second possibility is that part of the improvement is a reshuffling of clutter. Chargeoffs and extinguishment move loans out of the main rooms and into storage, which reduces the visible NPL stock even if the borrower’s health has not improved. The 2021–2022 disclosures show how large and persistent that storage room is. In that world, later cash collections appear as recoveries of written-off debts, which can lift profit sharply — exactly what you see in 2021 and 2022.

A third possibility is forbearance: rescheduling and restructuring that turns a struggling borrower into a temporarily “current” borrower by changing terms rather than by changing reality. The notes’ references to deferment/restructuring-era conditions point to a system in which such tools exist and matter. In agriculture, this can be humane and economically rational. It can also make a portfolio look healthier for a period while risk is merely postponed.

The financial statements alone do not give borrower-level trails. That would require a detailed audit of the bank’s loan books, something that Profit did not receive access to from ZTBL. The bank’s President did not respond to specific questions about this sent to him on Whatsapp either.

If you step back, the arc is clearer. ZTBL began the decade not just with a few bad loans, but an entire legacy system of non-performance and write-offs. In 2021, the loan book is still visibly sick, yet the bank is already collecting from old wounds through special Covid era conditions. In 2022, the headline sickness improves,

but the storage room grows, and recoveries become large enough to reshape profit. In 2023 and 2024, the bank’s interest engine becomes bigger but more volatile, and the clean-up engine becomes powerful enough to dominate the tone of the year.

So the story these financial statements tell is not simply that the bank recovered. It is that the bank learned how to live with its past in a structured way: pushing some of it into storage through charge-offs, pulling some of it back as income through recoveries, and steadily tightening the pipeline so fewer new loans join the pile.

Putting it on display

All of this brings us to what is coming: privatisation. ZTBL has been on the privatisation table for the past few years. In recent weeks, Finance Minister Muhammad Aurangzeb has made it clear the bank is high up on the list along with the House Building Finance Company (HBFC). There is already speculation that for any buyer, ZTBL will only be a viable option if it is sold not just as an agricultural bank but as a full bank with the ability to generate a larger portfolio of its own. One view in cabinet is that ZTBL and HBFC should be merged and turned into a single entity. There is precedent for this considering ZTBL itself is the result of multiple mergers.

However, informed sources from within the cabinet have told Profit that the government is split in two camps. One, led by the finance

minister and pushed by the IMF, wants to privatise as quickly as possible and on any terms. The other camp does not want to privatise since they are worried about how the government will conduct disbursements of agricultural subsidies directly to farmers without control of the bank. Prime Minister Shehbaz Sharif, apparently, is more sympathetic to the latter camp. However, he has agreed to privatisation but on a condition that might prove a hurdle: the bank can only be privatised if it continues to only be a bank meant for agriculture lending.

All of this is information that potential buyers will be looking closely at. For buyers, the bank has been whipped into good enough shape that it looks healthier than it has in years. Lending has expanded, the recovery apparatus is finally active, and the head office appears to have reasserted control over a branch network that had long been drifting without direction. A bank that once seemed like little more than a government disbursement machine now resembles something closer to a functioning financial institution. Even if some of the profits are being helped along by recoveries and provisioning reversals, the act of recovering those loans in the first place is itself an achievement. For decades the bank had not even attempted to chase much of this money.

Yet anyone considering buying a bank like ZTBL will not stop at the headline numbers. The first place they will look is not the profit line but the loan book itself. They will want to know how much of the improvement comes

from borrowers genuinely paying again, how much comes from loans that have been written down or reclassified, and how much of the recovery surge can realistically continue in the years ahead.

They will examine the agricultural loan portfolio region by region, borrower by borrower. They will want to understand how the Special Asset Management unit is recovering old debts, how many of those recoveries came from one-off settlements, and whether new lending since 2023 is performing better than the loans issued in the past decade. They will also look closely at the off-balance-sheet pool of chargedoff loans — the storage room where much of the bank’s historical trouble has been parked.

If the improvements hold up under that scrutiny, ZTBL could begin to look like a rural development bank that actually functions as a bank. Its branch network is enormous, its access to the agricultural economy is unmatched, and its role in financing farmers gives it a reach that few private institutions currently possess.

But if the clean-up proves to be more cosmetic than structural buyers will price that risk into any deal. In banking, the balance sheet never truly forgets the past. It simply reorganises it.

For now, what ZTBL has accomplished is difficult to dismiss. The institution has moved from inertia to activity, from neglect to management, and from losses to profitability. That alone is no small feat for a state-owned bank with decades of baggage. n

In Gilgit Baltistan, farming is slowly dying out.

Meet the school teacher and banker fighting back

Water woes, labour shortages, a lack of financing, and the growing appeal of the tourism sector have ravaged GB’s indigenous agriculture. Can relying on innovative farming techniques and high value produce change the tide?

By Hassan Saeed

To a passing tourist, the landscape of Gilgit-Baltistan (GB) is a study in cinematic contrast: jagged, snow-capped peaks that rise high above valleys that bustle with a fragile green life. The existence of this greenery feels like an act of defiance against this high-altitude desert, where the air is thin and the sun burns bright. Despite all this, sheer cliffs of grey and brown rock hide terraced slopes containing orchards of apricot, cherry, and apple that produce fruit of a quality found almost nowhere else on earth.

The landscape hides a heartbreaking economic paradox; here in a region that grows the world’s most expensive apples and the sweetest apricots, the agricultural economy is being stifled due to multiple reasons including lack of market linkage and access to finance. These bottlenecks coupled with others have seen harvest worth millions sold at peanuts or worse fed to livestock because it cannot reach a market.

A few months ago, we navigated this landscape from the markets of Skardu to the orchards of Gulmit at the foothills of the Passu Cones and everywhere in-between. On paper, the mission and objectives were simple; we were to study and map the agricultural value chain of GB and design solutions to address the bottlenecks but plans on paper are rarely anything but simple. The reality we saw was a complex web of innovation, failure, resilience and systemic neglect. The story we brought back is not just about a single missing piece of financial access or market linkages but of a broken chain, where everyone involved speak mutually unintelligible languages.

To understand the present, we must first look at the past, where for generations, the valleys of GB followed the familiar pattern of subsistence wheat farming but this was upended when the government introduced subsidized wheat. This allowed farmers to almost stop farming wheat and turn to more commercially viable crops. Today, organic wheat has vanished in the region and survives in isolated areas like Shimshal, which remains “probably one of the only places in the world where you will get organic wheat” because the soil and seeds remain untainted by commercial mixing. The shift to the commercial crops has been further complicated by the relentless pressure of land fragmentation. Already con-

strained by the landscape, the farmlands have sliced once-sizeable estates into unmanageable slivers with average orchard sizes of just under to an acre. Lastly, farming is increasingly being viewed as a ‘menial job” by the younger generation, leaving the land to wither with the aging generation. Despite all of the challenges, there are still many in GB who are trying their best to make agriculture thrive against the odds.

The banker with the Green Thumb

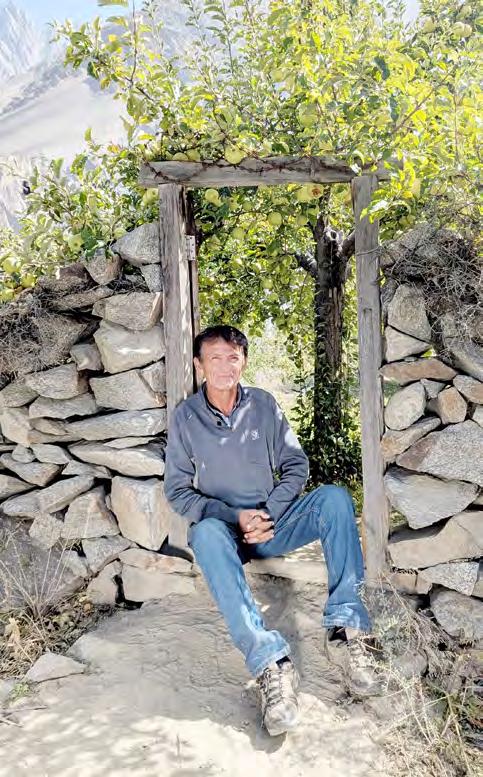

To truly understand the crisis and the potential of GB’s agriculture, we must look towards Danyore and Gulmit. In these two places, we met two distinct people but were bound in the same war against geography, climate change and economic orthodoxy. One is a former banker, who after saying bon voyage to spreadsheets has turned his sliver of land into an experiment lab. The other is a retired schoolteacher who is turning into a laboratory for high-value agriculture.

The first of the two people in this economic drama is Javed, a resident of Danyor – a settlement that lies on the opposite banks of the river Gilgit and across from the city Gilgit. Javed is not your run-of-the-mill farmer. For one he is new to agriculture and second, he is a banker which makes him an endangered species. It is hard to reconcile the image of the man looking at home in a field of cucumbers once, sat hours on end in sterile, air-conditioned rooms and looked at endless rows of excel sheets. “I played big games in banking,” Javed recalls, while proudly showing off his farm. “I worked in the corporate sector, I saw how money moves, how value is created. But then I looked at my life and I thought, why remain an employee? Why not become the owner? Why not build something real?”

Turns out building something real was easier said than done because his journey back to farming didn’t start with a plow but with heavy machinery. His land on which he now proudly farms is just a smidge over an acre in size but before that it was a “wild jungle” and needed to be tamed. While still associated with the banking sector, he had this patch of earth, leveled out and landscaped, turning the jungle into a canvas. Javed’s approach to farming is what makes him distinct from the others in the area. He opted for tunnel farming instead of the more traditional methods.

Tunnel farming is a method of vertical farming, where the crops are cultivated inside

semi-permanent structures, constructed using either iron pipes or bamboo, covered with white plastic sheets and insect-proof netting. This creates a bubble of stability, and allowing a regulated microclimate, the temperature is kept at optimal levels, the humidity is also regulated and the crops are safe from extreme weather changes; both snow and heat; the crops are also safe from the swarms of pests that can decimate an open field in days.

Tunnel farms themselves are not new, they are dotted all over the rest of the country but here in GB, they are still nascent and Javed’s operation makes a strong case for their adoption in the region. In 2020, when he was starting out, Javed planted cauliflower in the open and harvested 3.2 tons. In a few years, he quit banking and turned to tunnel farming full-time, his yield in 2022 was 20 tons and in 2024, he harvested over 35 tons of produce— cucumbers, tomatoes, and capsicum. To put this number in context, the average yield in the area is a few tons, a distributor for a fertilizer company said “A normal farmer picks perhaps 40kg from a kanal in an open field setting for certain crops”. “With tunnel farming, if practiced properly with the right inputs, that production goes up by nearly 70%. It fundamentally changes the unit economics of the land.” Another thing that sets Javed apart is that unlike other farmers, he runs his land with discipline, he notes down every expense in a notebook that he keeps on himself. He even draws a salary and ensures he keeps his labor value separate from the farm’s profit.

Javed’s farm operates with the discipline of a small manufacturing unit. He tracks every expense with the rigor of a forensic accountant. He pays himself a salary to separate his labor value from the farm’s profit. His annual revenue hovers between Rs 30 lakhs to Rs 35 lakhs, with operational costs around Rs 15 lakhs. He understands the science of inputs, shunning the local habit of not using any inputs or generic ones at best.

Despite all this, he works in a financial vacuum because for all his background in finance, large cash flow and creating arguably one of the most cutting-edge farming enterprises in the district, he does not borrow from financial institutions. “I don’t take loans,”he said. His starting capital was from his personal savings and a one-time grant from the Economic Transformation Initiative (ETI), an IFAD-funded program that covered 70% of the capital cost for the tunnels.

Javed wants to expand and lease land in Ghizer district, hoping to leverage the different

climate and weather for off-season production. To fund this, he is looking for informal access to credit from friends and family. The formal access, he thinks with all its strict collateral requirements and high interest rates coupled with the sub-par understanding of agricultural cash flows in financial institutions, is barred to him. A financial institution will look at his nine kanals and see a risky small holder instead of a productive SME.

Javed’s story is an outlier in the region and sheds light on the institutional failure in the region, the complete disconnect between the agriculture sector and financial institutions. Javed’s success is despite this disconnect, he was able to leverage his personal savings and a grant. The farmers around him in Danyore and beyond are not so lucky, they cannot afford a Rs 1lakh tunnel structure or weather the cash-flow gaps of a growing season. Unfortunately, they are forced to remain

in the open field, at the mercy of a climate that is becoming increasingly hostile.

The school teacher learns a Japanese lesson

If the success of modern technique and capital were represented by Javed, “Master Riaz”would be the representative of vision succeeding over geography. A retired school teacher by profession, Master Riaz hails from Hussaini, nestled near the foothills of the Passu cones. After retiring in 2011, he decided to travel to Japan and there, he found himself learning organic farming focusing on apples. He returned to his home with a radical idea and grafted samples of the “Fuji” apple; a premium variety developed in Japan, known for its large size, sweetness, distinct crunch, and high market value. In 2015, he planted his first

grafted seeds, turning his traditional orchard into a test bed for high-value agriculture. Today, his orchard is a glimpse into what GB’s agriculture could be if it pivoted from sustenance to specialty. “The Fuji apple is the most expensive in the world,” Riaz claims with the pride of a craftsman showing off a masterpiece. Riaz’s apple competes in a league of its own, while the local apple at times sells for a pittance; during the glut season it might go for as low as Rs 40-50. Riaz on the other hand sells them to foreigners, tourists, and high-end buyers for Rs 2,500 to Rs 3,000 per crate. The crucial lesson that Riaz has taken from his experiment that most policymakers miss out on when it comes to the agriculture of the region is that the path to success is not volume, but value.

Qayum, a specialist with the Aga Khan Rural Support Programme (AKRSP), echoes this sentiment. “We need to move to high value, low volume,” he argues. The landholdings in GB are simply too small to sustain commodity crops like wheat, maize, or even standard potatoes in competition with the vast, mechanized plains of Punjab. A farmer in Punjab can survive on thin margins because he has scale. A farmer in Hunza or Skardu has no scale; he must have margin. The future lies in niche products: cherries, organic apricots, buckwheat, and exotic apples like the Fuji.”

Despite the success, he has been unable to solve the infrastructure gap and maximize his earning potential. To do so, Riaz must process the lower-grade apples and create value added products like jams, juices, or dried apple chips. Which is the holy grail of agricultural development, turning waste into profit. For this, he bought a dehydrator machine to produce dried apples and other various products but it sits largely idle in his shop, “There is an electricity issue here,” he explains. “The dryer cannot be used properly because of load shedding”. Throughout the year but especially in the winter months, when the processing needs to happen, Gilgit-Baltistan suffers from severe power outages as the grid runs run-of-the-river hydropower, and shuts down as the glacial melt slows and the rivers freeze. Some areas receive only one or two hours of electricity in a 24-hour period. A machine that requires a constant temperature for 12 hours is useless in such an environment.

Riaz is now looking for a solar dryer, which will allow him to use abundant mountain sunlight and reduce reliance on the erratic grid. But like the tunnel farms of Danyore, this requires capital. “We need machinery,” he says. “If there was a mechanism for solar dryers, our work would be easy”. But as a pensioner, his access to capital is limited, and the banks see a retiree with a small orchard, not a pioneer of a new industry. This is the region’s second big-

In 2024, Javed’s farm produced 35 tons of cabbage. Surrounding farms had yields of only a few tons on the same area

gest failure, the infrastructure gap; the frames are ready to move up the value chain but lack the basic facilities, the state can’t provide electricity and the financial institutions will not provide the capital to bypass the state’s failure.

GB’s farming cannot be compared with Punjab

To understand why Javed and Master Riaz are not the norm, one needs to look back at the socio-economic history of the region. These issues are not recent and are rooted in the development history of the region and continue to this day with the majority of the households growing for subsistence. Wheat and other grains grown for survival and fruit trees for winter reserves. The oil from apricot kernels was the primary source of lighting and cooking fat before the arrival of electricity and vegetable ghee.

“Please don’t confuse us with that [Punjabi] zamindar,” warns Qayum, referencing the farmers of the south. In Punjab, a zamindar is a man of acres but in GB, the zamidar is a smallholder clinging to a few kanals of land. The average landholding is tiny – less than an acre and fragmented further by inheritance laws. When a father dies, his small plot is divided among his sons, reducing the land to slivers

that are economically unviable for anything other than a kitchen garden. The other issue is demographics. GB has one of the highest literacy rates in the country, the younger generation has moved away towards white-collar jobs or other cities or even other countries.

“The youth are mostly in Islamabad or Karachi,” he notes. “The parents are old. They are sitting in the village, but the labor force is gone.” This led to a labor crisis that persists to this day with farm work being left to women who make up 80% of the workforce in the area along with aging patriarchs and without a younger generation to help with the complex modern farming techniques, the sector is stalling. The farms are managed by those left behind, often lacking the energy or the capital to innovate.

Then we come to the beginning of

A view inside the tunnel farms that have increased Javed’s yield

everything, the soil and its inputs; farmers like Javed have the financial muscle to invest in fertilizers but the average farmer relies on traditional practices. Sara, from Vital Agri Nutrients, says that while awareness is on the rise, the cost of inputs prevents widespread adoption. “Farmers mostly use female labor,” she says, “and because landholdings are small, they hesitate to spend on micronutrients because they don’t see the scale of return”. They are trapped in a low-input, low-output cycle. Water, once in abundance, is also becoming erratic with climate change wreaking havoc on the centuries-old glacial melt patterns. “We used to have snow in December and January,” says a farmer. “Now it has been delayed to right when the trees are flowering”. A late snow can destroy the buds, wiping out the

Master Riaz at his apple orchard

entire season’s crop before it even sets. On the other hand, heatwaves can melt them too fast, leading to flash floods. In Danyore, flash floods destroyed water channels, leaving Javed’s farm without water for months during the crucial growing season. He had to buy water from tankers to keep his farm alive, something an average farmer cannot afford.

Once the fruit is ready for harvest, the race against time begins as the fruit trees, especially cherries and apricots, are highly perishable. In any other market, there would be a system in place to transport the produce to market but here in GB, there is what locals call the “Suzuki system.” Traders, often from down country or local aggregators, arrive in small pickup trucks and conduct “spot buying,” often buying the entire harvest of an orchard for a lump sum. “They come, look at the tree, and say ‘I will give you 3,000 rupees per tree’,” explains a local in Hunza.

No matter how good the fruit is, the farmer has no access to storage or transport and has no leverage to bargain and he cannot hold the fruit for a better price because it will start to rot in days. “They just want to get rid of it,” says a representative from the Regional Farmer Organization (RFO). “If they don’t sell it, it falls and rots”. The harvest process itself is brutal. The buyers often bring their own unskilled labor who strip the trees violently, damaging next year’s buds and bruising the fruit. “They waste 20 to 25% of it just by dropping it,” laments an apple farmer in Skardu.

All of this comes to a head at processing, where the value chain collapses completely, during the harvesting and processing phase 40-45% of apricots are wasted and the number is even higher for mulberries, where the waste is estimated at 90%—the fruit simply falls and is trampled. There have been attempts to modernize this process but it has been difficult with Shazday Fruits, a local enterprise, introducing the “Turkish method” of drying apricots, whereby whole drying takes place to preserve moisture and hygiene compared to the current traditional “K2” method of splitting the fruit and drying it on dusty rocks. Shazday also faces a “trust deficit.” A representative explains that they introduced a price guarantee and buyback agreements to protect farmers from price volatility but when the spot prices spiked, the farmers broke the contracts. “We agreed on 400 rupees, but someone came and offered 700. The farmers went with him,” she says. Unfortunately, more often than not high bidders disappear or fail to pay, leaving the market in chaos. Without contract enforcement, processors like Shazday are hesitant to invest in capacity, and farmers cannot rely on a steady income.

The final destination for most of the harvest is not the high-end supermarkets of Karachi or export markets in China, but local animal feed. Without access to cold storage,

Master Riaz believes farming in GB depends on quality margins not volume

farmers cannot hold their stock for better prices. “We sold tomatoes for 10 rupees a kg yesterday,” says an RFO member in Skardu, “because we couldn’t store them. Before that, they were 150 rupees”. The China market remains elusive. While the border is close, regulatory bottlenecks and lack of certification prevent large-scale exports. “They don’t accept ‘Made in Pakistan’ labels on dried fruit,” claims a local trader. “They want us to label it ‘Made in Afghanistan’ because they perceive that quality as better.”

Finding the money

Finally, we come to the heart of all matters; money and the lack of it. Despite the presence of financial institutions like HBL Microfinance in the area, there needs to be more access to funding. The biggest bottleneck is that the lending is focused on salaried individuals or diversified businesses, rather than farming which is seen as high-risk due to climate volatility. The products currently being offered are often misaligned with the cash flows of a fruit farmer. A cherry farmer gets paid once a year; a monthly installment loan is useless to him.

Gilgit-Baltistan’s economy is at a crossroads, it can remain as a tourism and remit-

tance-based economy where agriculture is fast being replaced by motels.Or, it can pivot. The potential is undeniable, there are examples of Javed who have proved that fortunes can be extracted from land with the help of precision and Master Riaz has shown that there is demand for the unique produce that only these mountains can grow. While the demand is there, the infrastructure is not, there is need for cold storages running on passive energy and processing units that can turn a perishable cherry into a shelf-stable jam. A financial product is needed that understands the cash flow of a cherry tree.

Above all, trust is required, the invisible wall blocking the progress is the “trust deficit”between the farmer and the processor, the bank and the borrower. Until such time that contracts are honored and loans are made on merit as opposed to collateral, the fruit trees will bloom, they will ripen but the harvest will continue to rot on the ground, a sweet, sticky reminder to a system that has forgotten its most valuable asset: the farmer on the ledge. n

Hasan Saeed works as a Research Analyst at Karandaaz Pakistan and is a long-suffering Pakistan cricket and Manchester United fan.

All pictures courtesy author

This year’s mango crop is dying from disease. How deadly is it, and is there a way out?

The deadly batoor disease has run rampant through Sindh’s mango orchards and threatens not just this year’s crop but also next year’s

By Usama Liaqat

Mango, for all its sweetness, is in peril. Reports have emerged that the orchards in lower Sindh are facing mango malformation, a condition of disease known locally as batoor. A fungal infection, it has the potential to wreck not only the current year’s crop, but also the following year’s as well. And deservedly does it incur the farmer’s spite and wrath.

For Pakistan, which is the sixth largest producer of mangoes in the world, this is no small matter. Yet Pakistan’s mango production in recent years has been wobbly, often decreasing, though sometimes increasing as well. Although this has little to do with any large-scale change in local practices, it has everything to do with changes in climate.

Often in recent years, the time when the mango trees are in the flowering and fruit-setting phases, heatwaves have struck, damaging

crops across the plains of Punjab and Sindh, and cutting down production. Conversely, the reason when the crop has performed well is when there have been unseasonably conducive weather conditions, encouraging young shoots and budding fruits to flourish into growth.

However, although climate remains a persistent worry and little can be done on a small scale to mitigate its harm in the short term, disease remains something that is preventable, yet always threatening and often biting. Similarly, certain practices which have harmed the crop continue to be undertaken, resulting in lower yields in certain areas.

This situation is complicated by the fact that mangoes do bring in some export revenue, and many producers rely on higher prices fetched by exports to regional markets.

The Disease(s)

Disease in crops is not simply a matter of harm to the plants, but also to livelihoods. And the mango malformation disease, or batoor, is no

different in this regard.

Ostensibly this is a fungal disease that causes flowers, leaves, and shoots to disform, and interferes with their development. Appearing often as clusters of shoots that are composed of narrow and brittle leaves bunching together inwards, this disease effectively colonises the mango tree. [INSERT PICTURE}

Abdul Ghaffar Grewal, former Director of Mango Research Institute Multan, explains what really makes this disease so nefarious.

“The fastest growing variety of mango is Sindhri, which can grow around 7 to 8 grams per day; even that sucks water and growth out of adjacent budding mangoes. The bhatoor, on the other hand, can grow more than 150 grams per day. And to power this growth it cannot rely on the roots alone, and starts pulling nutrition from neighboring branches, flowers, and flowering fruits, all of which are affected.”

Grewal highlights three major harms the growth of bhatoor causes. First, it impedes the growth of mangoes in neighbouring branches. Second, owing to its dark bushy structure, it

provides a good hideout for pests and insects, who can escape light and pesticide sprays. And third, batoor pulls nutrition from neighbouring branches, essentially draining the plant of its vitality. This handicaps the tree and makes it unable to bear fruit in the next cycle.

The cure for the disease lies in timely intervention. Any budding batoor clusters must be shaved off the branches as soon as visible, protecting precious nutrients for the mango flowers and budding fruits. There are longterm measures as well. Timely spray of pesticides ideally before winters, the use of potash, and avoiding over-irrigation of the orchard are some that Grewal highlights. He also insists that careful selection of new plants to ensure there were no or very little malformations is important, and so is the cautious removal of cut batoor from the orchard.

Mango malformation, however, is not the only potential disease that mango orchards face in Pakistan. Anthracnose is one such fungal disease, which although usually attacks fruit when it is ripening in store, has recently been known to attack fruit as it is growing on the tree. It appears as black spots on the surface of the mango, rendering the fruit not fit to eat.

There is also a condition that’s called the mango dieback, though according to Abdul Ghaffar Grewal it is not a disease, but a symptom. Visible to humans usually as the drying up of branches and shoots from the top of the tree gradually to the bottom, it eventually results in the death of the tree, unless precautions and treatments are administered, of course. This disease is a response to root decline, so normal methods of treating diseases (e.g., by fungicides, pesticides, or even fertilizer) do not work. The root cause is a fungal infection, whose growth is supported by harmful farming practices such as over-irrigation of orchards.

There is also the mango hopper, which is perhaps the most dangerous pest facing the mango plant. A small insect, it feeds on the sap of the budding shoots, and strikes at the plant when it is in the developmental phase, crippling it. These pests have the potential to ravage whole orchards, and are identified –other than their pesty bodies – through shiny spots on leaves, which are sticky residue left . Given that these also lay eggs, which are impervious to any pesticide, these have the potential to keep destroying plants if adequate and timely measures are not taken. Reports of hopper attacks are usual, and have risen in recent years to the great .

Other Issues

In recent years, however, climate change has emerged as a threat that has determined the fate of mango perhaps more than any other cause. The fluctuation in

mango production numbers in recent years has been attributed to what way the climate wind blows.

Early summers, especially heatwaves in the latter half of March, when the mango trees are flowering and fruit is setting on them, have destroyed crops with reports that the production has fallen anywhere from 20 to 50 percent in those years. And in years where an unseasonably cool late March occurred, farmers have felt optimistic for better output. In fact, 2023 was one such year, where the average temperature during this time remained in a temperate range between 27 and 32 degrees Celsius. This was in contrast to the heatwave years, where temperatures reached 37 to 42 degrees in the vital growth period of the tree causing massive fruit-shedding.

Although farmers have on the whole expressed that in general we are producing less mangoes than we ought to in recent years – sometimes by even 50 percent – the production numbers released by the National Food Security and Research show a rising trend.

There is, however, a caveat that these numbers are estimates based on acreage and the expected yield per acre, and nor do these account for the mangoes that were dropped before they were ripe. And, as for the estimates by the farmers that production has been down in most recent years by 40 to 50 percent, those are also estimates based on personal observations, and might not reflect the whole situation.

What is common between the two figures is that there has indeed been some variation in yields. While we don’t have official numbers for 2024-25 crop, according to Abdul Ghaffar Garewal, the past year was no different from the trend, where the production was down by as much as half, owing to heatwaves in springtime. Even though he is hopeful for a better production cycle this year, his hopes are circumscribed by assumptions of favourable weather conditions as well as protection against hopper attacks and other diseases.

These variations are consequential also because they directly impact the livelihoods of hundreds of thousands of people involved in mango production. And then, there is the question of exports as well, upon which mango producers depend to fetch better prices. The export targets fluctuate every year. In 2023, for example, the aim was to export 125,000 tonnes of mangoes. This target was revised next year to 100,000 tonnes, and then reinstated to 125,000 in 2025.

Yet, exports are a complicated matter, considering the political turmoil the broader region is being pushed into. Even last year, when producers were aiming to export

Sindhri and White Chaunsa to Iran, which is one of the top buyers of top-grade of these two varieties, their hopes were quashed by the war imposed by Israel and the US on Iran. The exporters were unable to export what they had wished, and consequently these varieties continued to flood the market. Similarly, Afghanistan has also emerged as a key market for second-grade mangoes from Pakistan, according to Abdul Ghaffar Garewal. Given the hostilities at the Afghan border this year, and the current war on Iran and the broader region, such aspirations remain contested.

And to top it all, there is the question of farming practices, and the export-readiness of Pakistani mangoes. As mentioned above, some farmers continue to overirrigate orchards, damaging the roots and consequently harming the trees ability to bear that year and the next years’ crop. Similarly, poor handling in the post-falling phase often leads to the loss of considerable quantities of the fruit. According to some estimates, such as one by Pakistan Horticulture Development & Export Board Manager Khawar Nadeem reported last year by The Express Tribune, as much as 30 percent of mangoes are lost before they reach the consumer due to outdated practices. Nadeem was also reported as saying that conventional Pakistani farms had 4060 plants per acre, unlike farms in Australia and Egypt which can reach up to 600 plants per acre since they use modern techniques like high-density planting, using superior rootstocks, and greenhouse setups.

Moreover, the question of export-readiness of Pakistani mangoes is also a lasting one. There are certain phytosanitary protocols that need to be met for export to the EU and countries such as Japan, China, Australia, the United States, etc. These include treatment by heat vapours, certifications that the mangoes were grown in a pest-free area, and proper documentation. Most of all however, these measures include treatment by hot water, a process that kills fruit-fly larvae right after harvesting. This is important because fruit flies lay eggs beneath the skin of the fruit, rotting the inside and making the fruit inedible.

Pakistan has been working on meeting these standards, with the number of hot water treatment facilities reportedly rising from 1 in 2014 to 26 in 2024, which is encouraging, but not enough. Dr. Mubarik Ahmed, a consultant with the Trade and Development Authority of Pakistan, was reported as saying in 2024 that “around 40 percent of the country’s mango exports went through hot water treatment”. This means that there certainly is more potential to unlock more advanced markets, and bring in more revenue than currently is possible. n

How the Wilmar-Unity partnership turned into a standoff

A $150 million provision, bank-facility stress, and control shift pushes partnership into governance test, but is there a deeper issue in the company?

For much of the last decade, Unity Foods looked like a familiar Pakistani corporate reinvention story. A listed company that had begun life in textiles repositioned itself into the country’s vast edible-oil and staples market, expanding through capacity, branding, and repeated capital raises.

Meanwhile its partner, Wilmar International, comes from a very different scale. Singapore-listed and sprawling across palm oil, oilseed crushing, commodity trading, and consumer food products, Wilmar operates as one of Asia’s largest agrifood groups, built around supply chains and risk management. A company that, quite literally, sits atop the food chain.

When the two companies became linked up, the story seemed straightforward, a global agrifood major taking a strategic position in a local platform in a large consumption market. And for several years, that narrative largely held. But then, in 2025 and early 2026, it began to unravel.

Two companies from different ends of the food chain

Wilmar’s operations span sourcing, processing, refining, trading, and distribution of key agricultural commodities across Asia. The company often invests through subsidiaries, joint ventures, or “associate” stakes in local companies that provide market access.

So when Wilmar disclosed a $150 million provision for losses linked to an associated company in Pakistan, it raised a few eyebrows. Bloomberg later confirmed that company to be Unity Foods. This single line item substantiated the claims of a rift in, what had previously

been, a quiet investment relationship into a matter of public scrutiny.

Unity Foods occupies a different but politically sensitive corner of Pakistan’s economy. Listed on the Pakistan Stock Exchange (PSX), the company operates in edible oils and staple food products, a sector heavily dependent on imports and working-capital financing. In such markets, liquidity and access to bank facilities often determine operational stability.

How Wilmar entered the picture

Wilmar did not initially take control of Unity. Public disclosures and reporting indicated that Wilmar became a shareholder in 2020, maintaining the position that it did not manage Unity’s day-today operations. That structure was typical of strategic minority investments. With capital and industry expertise coming from the foreign investor, operational management from the local partner.

The relationship, however, gradually deepened. In January 2022, Unity’s board approved the allotment of more than 64 million unsubscribed right-issue shares to Wilmar Pakistan Holdings at Rs27 per share, increasing Wilmar’s exposure.

The more consequential shift came two years later, when in March 2024, Wilmar announced through the Singapore Exchange that Wilmar Pakistan Holdings, along with Unity Wilmar Agro (Private) Ltd and other parties, intended to acquire additional shares and joint control of Unity Foods. These other parties, at the time, were none other than Unity Foods CEO and co-founder Farrukh Amin and his wife.

The Competition Commission of Pakistan subsequently approved a transaction

involving the acquisition of a 23.20% stake in Unity Foods by these four acquirers. Trade reporting later indicated that Wilmar’s effective shareholding rose further. By mid-2024, Wilmar-linked entities were holding about 42.17% of Unity Foods, equivalent to over 503 million shares.

Up to that point, the strategic rationale still appeared intact, where a global agrifood company deepening its presence in Pakistan’s edible-oil and staples sector through a growing equity position. Till this point, Farrukh Amin and his team of local executives were happily running the management and boardroom.

The financial disclosure that changed the story

The tone of the partnership shifted sharply with Wilmar’s financial disclosure in 2025. In its results announcement, the company recorded a $150 million loss provision tied to its investments in Pakistan. The company later confirmed to Bloomberg that this company was indeed Unity Foods.

According to explanations later reported, Wilmar said it had become aware during 2025 that Unity was experiencing difficulties servicing certain bank facilities.

The development, Wilmar said, came as a surprise because the most recent publicly available financial statements from Unity indicated profitability and reported liquid assets. This meant that either there was intentional financial malpractice or the management was so poor that they missed $150 million dollars. The former is always more likely in such a case.

Wilmar further stated that information later surfaced suggesting material uncertainties and inconsistencies in financial and working-capital items, and that despite

repeated clarification requests, the information remained incomplete or could not be reconciled.

In the language of corporate governance, the statement signaled a breakdown in confidence over financial reporting and internal controls. Wilmar’s provision was therefore not just an accounting entry. It represented a major public indication that the strategic partnership had entered troubled territory.

Leadership changes inside Unity

The rift in the partners is not new. There were signs starting to emerge right around December, and Unity Foods had begun experiencing leadership turbulence.

In December 2025, the company informed the PSX that its founder and long-serving chief executive resigned as CEO, effective December 21, while remaining on the board as a non-executive director. A new chief executive, Amir Shehzad, was appointed to fill the vacancy.

The transition proved short-lived and in February 2026, Unity disclosed that the new CEO had also resigned. Market disclosures and media reporting indicated that he stepped down as director and chairman as well, citing personal commitments.

The situation got even spookier when the company’s independent directors resigned, leaving the board without quorum. For a listed company, losing independent directors during a shareholder dispute not only signals that something is terribly wrong, but also raises practical governance problems. Board quorum is required for approving financial statements, audit matters, and key corporate decisions. Without it, the company’s formal oversight structure becomes difficult to maintain.

Competing narratives about control

As Wilmar’s concerns circulated publicly, Unity issued a statement that reframed the situation.

The company said that under a Shareholders’ Agreement dated December 21, 2025, between Wilmar International and certain shareholders, Wilmar had assumed management control of Unity Foods with immediate effect.

According to Unity’s account, a Wilmar-approved chief executive and chief financial officer were appointed following the agreement. While the CEO later resigned in February 2026, the CFO continued in the role.

Unity stated that financial management and reporting functions were being administered under Wilmar’s authority under

the governance structure established by the agreement.

That explanation diverged from earlier descriptions of Wilmar’s role as a non-operational strategic shareholder.

Instead, it suggested that by late 2025, Wilmar’s position had evolved into one involving direct managerial oversight. Unity also disclosed that disputes between shareholders had moved into the legal arena.

The company informed the PSX that proceedings between certain shareholders were pending before competent courts, and that the matters were sub judice. Till the filing of this report, the company has maintained a tight lipped stance on this whole matter.

According to the official statement, because of the litigation, Unity said it would not provide additional comment. The dispute therefore has shifted beyond corporate governance tensions into a legal process likely to determine the boundaries of control and authority between the company’s key stakeholders.

A formal confirmation of Wilmar’s control

The most recent development arrived on Thursday when in a notice to the Pakistan Stock Exchange, Unity Foods confirmed that Wilmar International has assumed management control of the company under the shareholders’ agreement signed in December 2025. Market commentators believe this to be a step that Wilmar had to take due to prevailing conditions.

“The Company has been informed that Wilmar Group has entered into a Shareholders’ Agreement dated December 21, 2025 with certain shareholders of Unity Foods Limited, pursuant to which it has assumed management control of the Company with immediate effect,” the filing stated.

The disclosure clarified that Wilmar’s control stems from the shareholder agreement rather than any new acquisition or emergency takeover. Unity also reiterated that legal proceedings concerning aspects of the arrangement are currently underway, and therefore the company would refrain from further comment while the matters remain before the courts.

What happens next?

Wilmar’s $150 million loss provision is the most tangible indication of concern. Companies rarely record provisions of that scale unless they believe the value of an investment is materially impaired.

Secondly, Wilmar reportedly sought regulatory guidance about whether an administrator or independent investigation might

be required, suggesting it believed internal clarification processes were insufficient.

The dispute has also moved into court proceedings between shareholders, taking the matter beyond boardroom disagreements. The sequence of leadership departures and independent-director resignations has created a pattern of governance instability within the company.

Together, these developments do not inspire investor confidence and also illustrate how strategic partnerships can shift into contested governance situations.

As of now, leadership turnover has occurred, independent directors have resigned, and litigation between shareholders is underway. What the record does not yet show is a definitive conclusion.

No regulator has issued a final determination, and the courts have yet to resolve the disputes between stakeholders. For now, the story of Wilmar and Unity Foods remains unfinished — a strategic investment that began as a straightforward partnership and has since evolved into a complex contest over governance, control, and trust.

This also raises an interesting skeptic reading, with the timing mismatch. According to the written response to Bloomberg’s queries, Wilmar says it became aware during 2025 that Unity was struggling to service certain bank facilities, and that this clashed with published numbers showing profitability and material liquid assets.

If that unease existed before the late-December control shift (Unity’s disclosures point to December 21 agreement and December 23 resolutions), then signing up to take management control looks, at minimum, like an oddly aggressive move for a group already absorbing other big provisions and legal exposures around the world.

One explanation is mundane, that once a minority stake becomes large enough, “doing nothing” can be the riskiest option. Taking control could be Wilmar’s attempt to stop further value leakage, secure direct access to books and bank conversations, stabilise lender relations, and run a rapid clean-up so the investment does not become a total write-off.

A darker reading flips it. Control could be about narrative and liability, stepping in early to shape what gets documented, who signs what, and how responsibility is framed before a legal fight hardens, leaving the prior sponsor group positioned as scapegoat.

Both theories can’t be confirmed from public statements alone, and that is why the picture stays grey. Until courts and any independent review establish a timeline of decisions, cash, and disclosures, the market is left watching two powerful parties argue over who inherited a problem and who created it. n

Panic buying hits petrol pumps amid supply fears; Rs55 fuel price hike announced

Long queues outside petrol pumps and warnings of supply disruption have fueled concerns about a potential fuel shortage

By Abdul Hameed Niazi

On Friday, the government announced a Rs55 per litre increase in petrol and highspeed diesel prices. Petroleum Minister Ali Pervaiz Malik made the announcement during a press conference alongside Deputy Prime Minister and Foreign Minister Ishaq Dar and Finance Minister Muhammad Aurangzeb. Dar noted that the new prices will take effect from midnight and cited the ongoing conflict between Iran, the US, and Israel as influencing global oil markets.

The Rs55 per litre increase reflects accumulated international oil price movements and the ongoing Gulf conflict involving Iran, the US and Israel. Pakistan’s reliance on imported petroleum—around 60 percent of petrol and 20 percent of diesel—makes domestic prices sensitive to such global developments. Officials have noted that the hike also addresses limitations of the current fortnightly pricing system, which can result in larger price adjustments when global market changes accumulate. The government emphasized that fuel stocks remain sufficient and that the increase is intended to maintain market stability rather than respond to an immediate shortage.

All this was preceded by concerns about a possible fuel shortage in Pakistan these intensified in recent days, as motorists in several cities rushed to petrol pumps amid fears of supply disruption. Long queues were reported outside stations in Lahore, Islamabad and other urban centres, with some pumps limiting sales to Rs1,000 or Rs2,000 worth of petrol per vehicle, to manage demand.

The surge in buying has coincided with warnings from petroleum dealers about declining fuel deliveries, along with broader

geopolitical uncertainty affecting global oil markets and shipping routes such as the Strait of Hormuz.

However, regulators and government officials maintain that the country currently holds sufficient petroleum reserves to meet demand, suggesting that recent scenes at petrol stations may reflect heightened market sensitivity rather than an immediate supply shortage.

The contrasting narratives have created a complex picture in which supply chain concerns, market expectations and consumer behavior appear to be reinforcing one another.

Government insists stocks are sufficient

Prime Minister Shehbaz Sharif chaired a high-level meeting on Friday to assess the fuel supply situation in light of the evolving regional environment.

Officials from the Petroleum Division informed the meeting that Pakistan currently has adequate petroleum product reserves to meet national requirements. Regulatory assessments indicate that the country holds fuel stocks equivalent to roughly 28 days of consumption, while crude oil reserves cover around 10 days and liquefied petroleum gas stocks about 15 days.

Despite these assurances, the prime minister directed provincial authorities to take strict action against any petrol pumps found creating artificial shortages or hoarding fuel. He warned that stations engaged in such practices should be sealed immediately, with licences cancelled and legal proceedings initiated.

Authorities also announced plans to introduce a digital monitoring dashboard to track the movement of petroleum products

nationwide and share real-time supply data with provincial governments.

The measures reflect a concern that market disruptions could arise not from physical shortages but from behavior within the supply chain.

Dealers warn of declining deliveries

Petroleum dealers have presented a different perspective, warning that deliveries from oil marketing companies have fallen sharply in recent days.

Leaders of the Pakistan Petroleum Dealers Association said fuel stations could begin shutting down from Monday if supply levels are not restored.

According to Chaudhry Irfan Elahi, diesel supply to pumps has dropped to around 20 percent, while petrol deliveries have also been curtailed significantly.

Nauman Majeed said petrol supply had declined by roughly 50 percent, describing the situation as increasingly difficult for retailers.

Meanwhile, Jehanzaib Malik alleged that some oil marketing companies had halted deliveries to pumps and urged the government to intervene to ensure supply according to market demand.

Dealers warned that if the situation continues, petrol stations may be forced to suspend operations due to lack of product.

Pump owners reject hoarding claims

At the same time, petrol pump owners have rejected accusations that retailers are deliberately creating artificial shortages.

The All Pakistan Petrol Pump Owners Association said stations were selling fuel

as soon as deliveries arrived and denied that pump operators were hoarding petroleum products.

Association vice chairman Nauman Butt said fuel availability at retail outlets depends largely on supply provided by oil marketing companies. If deliveries to pumps are reduced, he said, stations may struggle to maintain normal sales levels. Pump owners also criticized warnings of licence cancellations, saying such measures would be unjustified under the current circumstances.

Supply chain tensions add complexity

Another layer of the issue has emerged within the industry itself.

The Oil Marketing Association of Pakistan has warned that changes in supply practices by local refineries could disrupt the fuel supply chain if regulatory intervention does not occur.

In a letter to the Oil and Gas Regulatory Authority, OMAP chairman Tariq Wazir Ali said petroleum product volumes had been finalized during the most recent Product Review Meeting and supply plans were structured accordingly.

However, the association said refineries later introduced a new allocation system under which products are being supplied in reduced quantities based on historical averages rather than the volumes agreed during the meeting.

According to OMAP, many oil marketing companies had refrained from arranging import cargoes after refinery allocations were confirmed, meaning the sudden shift in supply practices has created operational challenges.

The association warned that lower refinery allocations are gradually eroding the mandatory 21-day stock cover required for oil marketing companies under regulatory rules.

At the same time, OMAP said it has consistently communicated that there is currently no immediate shortage in the market.

Regulator emphasizes uninterrupted supply

The regulator has sought to reassure the market. The Oil and Gas Regulatory Authority has directed all oil marketing companies operating in Pakistan to ensure uninterrupted nationwide supply of petrol and high-speed diesel. Companies including Pakistan State Oil Company, Attock Petroleum Limited, Gas and Oil Pakistan Ltd, Parco Gunvor Limited and Hascol Petroleum Limited

have been instructed to maintain smooth distribution and avoid artificial shortages or overcharging.

Field monitoring teams have also been deployed to inspect retail outlets and ensure that petrol and diesel remain available at prescribed prices.

The role of market expectations

While supply chain disagreements have contributed to uncertainty, another factor shaping the current situation may be expectations about future price movements.

Authorities are considering a proposal to replace the existing fortnightly petroleum price review system with a weekly mechanism. The summary prepared by the Petroleum Division is expected to be presented to the Economic Coordination Committee.

Officials say the new system would allow domestic fuel prices to adjust more quickly to changes in global markets and reduce the magnitude of sudden price adjustments.

Importantly, the proposal also aims to discourage speculative behavior and prevent the hoarding of petroleum products by dealers attempting to benefit from anticipated price changes.

In markets where prices are revised periodically, expectations about future price increases can influence purchasing patterns across the supply chain.