Opportunity Colombia Your Impact Report, Spring 2026 Opportunity International began our work in Colombia in 1972. Our proven three-pronged interventions of tailored training, financial resources, and support increase incomes, create and sustain jobs, and provide affordable quality education for children and youth. Opportunity’s programs start and end with the client in mind, with interventions tailored to the specific needs of the local demographic and geography. As you’ll see below, we’ve exceeded, in some cases, exponentially, the targets we set for 2025 and we are well on our way to a productive 2026. Thanks to your help, over the last three years we’ve impacted over 136,000 people in Colombia (triple our original goal!)—and we’re not stopping.

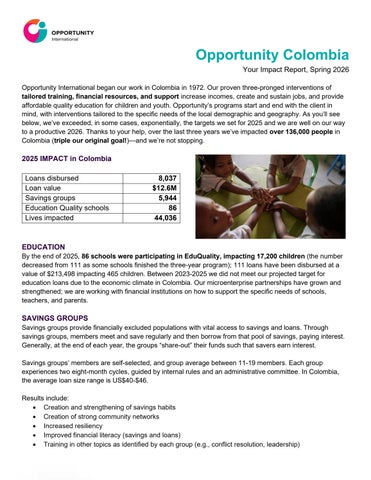

2025 IMPACT in Colombia Loans disbursed Loan value Savings groups Education Quality schools Lives impacted

8,037 $12.6M 5,944 86 44,036

EDUCATION By the end of 2025, 86 schools were participating in EduQuality, impacting 17,200 children (the number decreased from 111 as some schools finished the three-year program); 111 loans have been disbursed at a value of $213,498 impacting 465 children. Between 2023-2025 we did not meet our projected target for education loans due to the economic climate in Colombia. Our microenterprise partnerships have grown and strengthened; we are working with financial institutions on how to support the specific needs of schools, teachers, and parents.

SAVINGS GROUPS Savings groups provide financially excluded populations with vital access to savings and loans. Through savings groups, members meet and save regularly and then borrow from that pool of savings, paying interest. Generally, at the end of each year, the groups “share-out” their funds such that savers earn interest. Savings groups’ members are self-selected, and group average between 11-19 members. Each group experiences two eight-month cycles, guided by internal rules and an administrative committee. In Colombia, the average loan size range is US$40-$46. Results include: • Creation and strengthening of savings habits • Creation of strong community networks • Increased resiliency • Improved financial literacy (savings and loans) • Training in other topics as identified by each group (e.g., conflict resolution, leadership)