Equipping the actuaries of tomorrow

Equipping the actuaries of tomorrow

The LSESU Actuarial Society is the largest actuarial student society in London. Throughout the years, our society has built upon its successes and advanced our mission to educate the actuaries of tomorrow Education and connection are the key value proposition that the LSESU Actuarial Society brings to its members As part of our broader strategy of looking into the future, we strive towards providing more professional development resources, opportunities, and actuarial insights for our members. Additionally, we seek to expand our coverage on emerging actuarial trends by hosting diversified events to further extend our reach on topics outside of the traditional actuarial professions.

We organise talks and workshops to raise commercial awareness among our members about pensions and insurance while exploring the way actuaries respond to challenges in this ever-evolving world with endless possibilities. There are various opportunities to ask seniors and alumni about their experiences working in actuarial placements, and providing members with advice about internships is also one of the great services our society can offer

Additionally, we host networking events that connect students directly with industry professionals, providing them with the opportunity to foster relationships that are essential for career development We are committed to providing our members with memorable experiences and insights about Actuarial Science, and most importantly, ‘Equipping the Actuaries of Tomorrow’.

To highlight some key successes from the 2024-2025 academic year, we proudly hosted our 12th annual Actuarial Conference at LSE, featuring the President of the Institute and Faculty of Actuaries (IFoA) as a distinguished guest. Additionally, we successfully organised our 3rd Actuarial Case Competition, supported by our sponsors and partners.

This academic year, the research division will be responsible for releasing a newsletter to members and non-members of the society Our members will get exclusive access to the newsletter a few days before public release and access to exclusive stories

HOME

LANDSCAPE: A SYSTEM UNDER PRESSURE

Despite this fragility within the home insurance market and the undeniable fact that the current reinsurance market is a hard one, meaning an increase in premiums, stricter underwriting and a reduced insurance capacity, the reinsurance market still remains relatively stable according to discussions during the Monte Carlo conference, and debates about a possible softening of the market have arisen

Reinsurers are responding to the climate pressures by recalibrating catastrophe models This involves moving from static models based on historical averages, to dynamic, forwardlooking models that incorporate climate projections, geospatial data, and AI Actuaries working in reinsurance are adjusting assumptions around return periods, tail risk, and correlation structures, and catastrophe models are being adjusted to reflect societal adaptations, meaning exposure and vulnerability components are no longer treated as fixed

Furthermore, reinsurers are increasingly using granular, geospatial data from sources such as NOAA and satellite imagery to refine risk assessments Reinsurers are demanding detailed property-level exposure data, including building materials, elevation, and proximity to mitigation infrastructure, which allows for more accurate pricing and better risk selection

Product innovation and how it is reshaping risk transfer is being explored more and more as a response to the evolving world. One example of this is parametric insurance, which is triggered by measurable events like wind speed or rainfall, is becoming more popular, as it offers faster payouts and simpler claims. This requires actuaries to rethink how risk is quantified, with traditional indemnity-based models being supplemented by trigger-based mechanisms, which change the way actuaries approach pricing and reserving

Alternative risk transfer mechanisms, insurance-linked securities (ILS) a class of financial instruments which allow insurance and reinsurance companies to transfer risk to capital market investors, such as catastrophe bonds, through non-traditional vehicles are expanding and are being explored within the industry These would allow reinsurers to spread risk across capital markets, enhancing the ability to manage large-scale exposures without relying solely on traditional treaty structures, which is particularly important to helping to close the protection gap for hard-toinsure perils

In today’s climate-challenged insurance landscape, actuaries are no longer just technical specialists, but they are central to how the industry adapts and responds The role is evolving rapidly, as they are tasked with recalibrating models that were once built on stable historical data but now must account for volatility, uncertainty, and interconnected risks. The increasing frequency and severity of natural catastrophes, coupled with the emergence of uninsurable perils, means that actuarial models must shift from relying on historical averages to incorporating forward-looking, scenario-based approaches

However, actuarial responsibility extends beyond modelling: as coverage gaps widen and products become more complex, actuaries also have an ethical duty to help insurers communicate clearly with consumers Many homeowners remain unaware of what their policies actually cover, and actuaries can play a key role in bridging that gap This is especially important as insurers introduce higher deductibles and exclusions, shifting more financial risk onto policyholders.

Legacy systems and assumptions, such as fixed return periods or static vulnerability profiles, must be challenged in order to cope with the growing strains on many systems in today’s world Actuaries are uniquely positioned to lead this transformation, combining technical rigour with a broader understanding of societal and environmental change With better data, clearer communication, and innovative thinking, actuaries can help build a more resilient and responsive insurance ecosystem, which isn’t simply about pricing or product design but about reimagining how risk is understood, shared, and mitigated

Many insurance companies today still rely on systems and software that were created years ago They have not kept up with the demands of a changing market These legacy systems often make critical tasks slow and inefficient, from processing claims to generating reports for regulators Hence, modernising such systems is essential, not only for faster processes, but for providing the level of service that policyholders and regulators expect in today’s environment As regulations and customer needs evolve, companies that fail to adapt may find themselves left behind by competitors who have invested in better tools and more advanced processes

Actuaries are considered the main contributors in the movement to modernise core insurance systems nowadays Traditionally, their responsibilities usually centred around pricing policies and assessing risk However, actuaries today are no longer limited to technical analysis. Instead, they are taking up roles as project advisors and agents for improvement. Their deep familiarity with both the numbers and the practical side of insurance operations allows them to help guide technical upgrades that will actually work for daily business processes.

At the start of any system upgrade, it is crucial for an insurance company to decide exactly what the new technology should achieve. Actuaries are well positioned to take part in these discussions, due to their experience with complex data and reporting They provide valuable insights into which features must be prioritised to handle calculations and data collection In addition, they also recommend improvements that might support future business growth By working with staff from other departments, actuaries ensure that the new systems meet the business’s most urgent and long-term needs

When new systems are ready to be tested and rolled out, actuaries play a vital role in this phase They help design the tests that check whether calculations are accurate, and models are reliable under different conditions During training and initial usage, actuaries also lend their experience to help staff members learn the new tools and processes Their ability to spot potential problems allows the company to make adjustments before wider rollout, which indeed help reducing the chance of costly mistakes or disruptions. With the introduction of modern systems, insurers are able to streamline major processes such as underwriting, pricing and claims management. These improvements translate into quicker approval cycles and fewer manual errors. As a result, the insurers are able to have more effective communication with policyholders. Regulatory reporting also becomes more efficient and clearer, helping companies respond confidently to external audits and compliance requirements In short, the actuary’s involvement ensures that these changes have real impact on the company’s business performance rather than being upgrades in name only

One of the greatest advantages of modern insurance software is the increased capability for automation and data analysis Tasks that once took hours can now be performed in moments, freeing actuaries and their colleagues to focus on more strategic tasks Advanced analytical features built into these systems allow for clearer forecasting and better identification of risks, while also ensuring more informed decision-making across the business By integrating information from multiple channels, actuaries can provide findings which help insurers adapt to changes in the market or customer base more swiftly and effectively

Despite the clear benefits, upgrading insurance systems is rarely simple These include moving historic data from old systems to new ones, and training staff in unfamiliar platforms Problems often arise when teams underestimate the scope of change required or when staff are reluctant to shift away from established routines. Therefore, actuaries play an important role in helping to guide change management, offering practical solutions and reassurance to those affected by the transition.

The true measure of successful modernisation lies not only in technical improvements, but also in how those changes positively impact the entire business Actuaries help establish benchmarks and goals that reflect both operational and strategic benefits, including greater efficiency, lower costs, faster reporting and improved customer satisfaction By monitoring progress and making ongoing refinements, actuarial teams ensure that the advantages of modernisation continue to support the company’s growth and service standards over time

Modernising core systems opens new possibilities for professional development and teamwork within actuarial departments Actuaries gain valuable experience not just in technical analysis, but also in fields such as project management, technology integration and crossdepartment collaboration. Their involvement in these initiatives amplifies their influence and ensures that the voice of those closest to the numbers is heard in conversations about business strategy and customer service

The process of modernising insurance systems should not be viewed as a one-time project Instead, it should lay the foundation for constant progress, adapting to new market forces, customer feedback and technological advances Through their balance of analytical skill and practical understanding, actuaries are ideally positioned to keep their companies moving forward By continuing to invest in staff training, system upgrades and new technologies, insurers can ensure that they remain competitive and capable of meeting future challenges

In conclusion, the role of actuaries in modernising insurance systems is broader and more important than ever before By applying their expertise in risk, data and operations to every stage of technological transformation, actuaries help build insurers that are more responsive, efficient and customer focused. Their work ensures that insurance does not simply keep up with the times, but sets new standards for quality and reliability in a rapidly changing world.

Autonomous vehicles (AV) are the future This is the most common phrase in the automobile industry in recent years, in conjunction with the rise of artificial intelligence Now, first, let’s define the meaning of autonomous vehicles AVs are vehicles that can operate and perform necessary functions without any human intervention, thanks to their ability to sense their surroundings There are 6 levels of AV, ranging from level 0 to level 5 As levels increase, more automation is introduced into the system, with driving conditions in levels 3 to 5 being monitored by the system In 2024, the autonomous driving space attracted $7 5 billion in equity funding, a 3x year-over-year increase, driven by massive rounds to self-driving stack developers like Waymo ($5 6 billion Series C) and Wayve ($1 1 billion Series C) In 2029, the market is forecasted to reach some 114 5 billion U S dollars By 2027, Level 2 AVs will rise in sales from 20% to 30% while Level 3 AVs could comprise of 10% of global new car sales This shows the rapid growth and dependence on AV in the coming years

AV is not simply a tool to show advancement, but has its importance, especially in the life and health aspect of car crashes Government data identifies driver behaviour or error as a factor in 94 percent of crashes For example, fatigued drivers are twice as likely to make mistakes, according to NHTSA Economically, motor vehicle crashes cost American society $340 billion in 2019, which shows accidents are a huge proportion of expenses Also, accidents account for $23 billion as medical expenses in the USA annually With the introduction of AVs, the US Chamber of Commerce has projected up to 1 4 million fewer accidents, 12,000 fewer fatalities, and $94 billion in savings with advanced AVs

Despite the huge benefits that come with AVs, there are some imminent risks associated with it The rapid development of autonomous vehicles introduces significant cybersecurity vulnerabilities due to their reliance on advanced electronics, connectivity, and artificial intelligence In 2015, researchers Charlie Miller and Chris Valasek demonstrated a remote hack of a Jeep Cherokee, where they gained control over the vehicle's critical functions such as braking They are also susceptible to criminals who could ransom a vehicle or its passengers, and thieves who direct a self-driving car to relocate itself to the local chop-shop However, with the increasing advancements of cybersecurity, the prospects seem brighter; however should still be kept in mind during development In terms of ethics, a decision made by the vehicle is not a single-shot, black and white one, but one that will be made at the intersection of multiple overlapping probability distributions, we will see that “judgments” about what courses of action to take are going to be not only computationally difficult, but highly context dependent and, perhaps, unknowable by a human engineer a priori There is also the ongoing issue with determining a system to determine the liability between humans and the AI in case of a fault leading to accidents Holding the car manufacturer responsible seems reasonable, given that they would be the cause of any flaws in programming or sensors However, holding manufacturers completely responsible may slow the development of AVs and result in fewer lives saved

With a change in risk comes a change in insurance Current insurance models rely on human-centric data: driving history, age, and geography But as control shifts to systems, insurers must assess risk based on vehicle behaviour New technical risks, especially around software and increasingly common and frequent over-the-air updates, challenge traditional underwriting Mixed-control scenarios, where drivers and systems alternate, further complicate liability modelling When a Level 3–5 autonomous vehicle is involved in a crash, because system design doesn't require the driver to be constantly "in the loop", fault no longer rests with the driver

Two main insurance models are determined by the dual mode coverage and product liability focus For dual mode coverage, let’s say that during a drive, a driver receives an important call and switches on the autonomous-driving option While she's driving the car, the insurance liability lies with her But while the autonomous mode is engaged, liability shifts seamlessly to the manufacturer Both her car and her insurance adjust in real time This is for level 3 - 4 AVs However, for level 4-5 AVs, product liability focus will be implemented where the liability mainly rests on the manufacturer/tech company

Goldman Sachs predicts insurance costs will decrease more than 50% over the next 15 years, from around $0 50 per mile in 2025 to $0 23 in 2040 Early evidence suggests the technology is effective at improving road safety A December 2024 study from Swiss Re commissioned by Waymo found in a liability claims analysis a 92% reduction in bodily injury claims and an 88% reduction in property damage claims compared to human-operated cars However, Scott Holeman, director of media relations at the Insurance Information Institute, warns that just because insurance costs are cut doesn't mean consumers will be padding their wallets "While there could be lower costs on insurance products, this technology costs money, so there's a shift in where you pay the money ” With fewer accidents, reduced human error, and a decline in individual vehicle ownership, insurers anticipate a staggering 60% drop in personal auto insurance revenues 42% of insurance executives predict that conventional policies will be obsolete by 2040

Based on an analysis by Morningstar, autonomous vehicles present a paradoxical impact on auto insurers: short-term benefits followed by long-term existential threats In the near term (next 10 years), AVs could benefit insurers As partially autonomous vehicles (Level 2-3) reduce accident rates while insurance remains legally required, insurers may enjoy a favourable period of lower claims with sustained premium volumes Historical evidence supports this where auto insurers earned materially stronger returns during 2001-2010 when accident rates were falling compared to the post-2010 stagnation period

However, the long-term outlook is dire Once Level 4-5 autonomy achieves scale, liability fundamentally shifts from drivers to manufacturers, transforming personal auto insurance into product liability coverage Morningstar projects that even in their most aggressive scenario, 60% AV penetration won't occur until 2044, giving insurers 20 years before obsolescence

The impact varies dramatically by company Progressive faces the greatest risk (83% auto exposure, 21-26% worst-case valuation decline), while diversified players like Travelers (20% auto exposure, 4-6% impact) are well-positioned Importantly, Morningstar concludes investors shouldn't discount these stocks today where the timeline is long enough that impacts remain within normal margins of safety, though current premium valuations may not be justified for potentially obsolete businesses

The transition from classical to AV-based insurance represents a fundamental actuarial shift Traditional auto insurance, built on a century of human behavior data, is evolving into a technology-centered model in which risk assessment focuses on algorithmic reliability, cybersecurity, and manufacturer liability While this transformation threatens a 60% revenue decline in personal auto insurance by 2040, it provides a 20-year adaptation window. For actuaries, this evolution demands new competencies such as machine learning expertise, technology risk modeling, and systems analysis that must augment classical statistical methods The future belongs to actuaries who recognize that their core mission of quantifying and pricing uncertainty remains constant even as the nature of risk fundamentally transforms The actuaries who successfully navigate this transition will be those who embrace technological change while applying foundational principles of risk assessment to an automated world

Interest is the fee paid by a borrower to the lender for using borrowed money The amount paid depends on the interest rate, which is expressed as a percentage of the principal over a specific period. Many financial situations we see today are shaped by interest rates, ie student loans, credit card debt and “buy now, pay later” schemes. Understanding how interest rates are calculated and applied helps us make better financial decisions in our everyday lives In this paper, we will discuss interest rate concepts, mainly about the effective interest rate, discount factor and rate of discount, force of interest, including the use ofthemathematicalconstante.

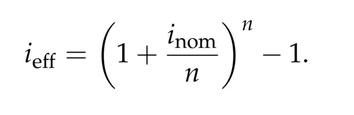

The actual price a borrower pays a lender is the statedinterestrateofabondorloan,alsocalledthe nominal interest rate which does not take into account inflation and compounding. The real interest rate adjusts for inflation, making it useful for evaluating the true cost of borrowing, while the effective interest rate reflects the impact of compoundingovertime,suchthat where:

•i = Effective annual interest rate, representing the actualrateearned eff orpaidafteraccountingforcompoundingwithinthe year.

•i =Nominalannualinterestrate nom

• n = Number of compounding periods per year, such as 12 for monthly, 4 for quarterly, 2 for semiannually,or1forannually.

Example:

If the nominal interest rate is 12% per year compoundedmonthly(i = nom 0.12,n=12):

Therefore,theeffectiveannualrateis12.68%,which is slightly higher than the nominal rate due to monthlycompounding.

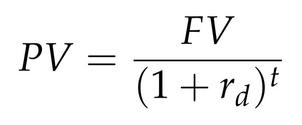

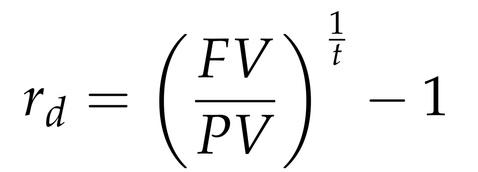

Discount rate is the rate of return used to discount future cash flows when calculating an investment presentvalue £100inthepresentvaluesmorethan £100 in the future based on the principle that money should make more money over time, also known as the "time value of money". The discount ratecanbecalculatedusingthefollowingformula:

IfPVisthepresentvalue,FVisthefuturevalue,r is thediscountrate,andtistimeinyears: d

Rearrangingtofindthediscountrater :d

Example:

If the present value is £100, the discount rate is 10%,andthetimeperiodis5years:

F=100×(1+010)^5=16105

Therefore, £100 is worth £16105 in 5 years time under compound discounting, which demonstrates the principle that money has a time value

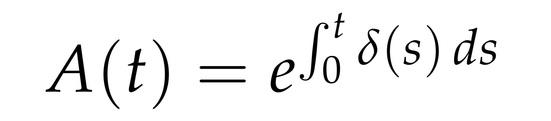

The force of interest helps us to address the changing interest rates by describing how interest accumulates continuously over time, even when interest rates fluctuate. Mathematically, if δ(t) represents the force of interest at time t, the accumulationfunctionisgivenby:

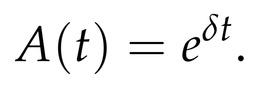

If the force of interest is constant, say δ(t) = δ, then theaccumulationfunctionsimplifiesto:

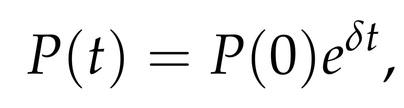

Theamountofmoneyattimetcanthenbewritten as:

where P(0) is the initial principal and δ is the constant force of interest. Similarly, the present valueP(0)correspondingtoafuturevalueP(t)is:

This formulation provides a continuous model for interest accumulation and is especially useful whendealingwithvaryingorcontinuously compoundedinterestrates

Known to anyone who has taken high school algebra is the constant e (though anyone who knowsthealphabetprobablyrecognizesittoo!) In mathematics, e ≈2.71828182..., and we have just useditinthecontextoftheforceofinterest, where it emerges naturally in modelling continuous compounding

Today, e as the base of the natural logarithm forms the foundation for modelling continuous growth and decay in mathematics and economics Fun fact: e is the second most common mathematical constant, do you knowthefirstone?

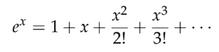

Taylor series is a useful mathematical tool to approximatecomplexfunctionswithsimplerpolynomial expressions.Itexpressesafunctionasan infinitesumofitsderivativesevaluatedatasinglepoint.

For a function f (x) that is infinitely differentiable at x = 0, theTaylorseriesexpansionisgivenby: f(x)=f(0)+f′(0)x+f′′(0)(x )/2! +f‘’’(0)(x )/3!+··· 2 3

Example:Theexponentialfunction,

This expansion is valid for all real numbers x because the series has an infinite radius of convergence. In other words, no matter how large or small x is, the series convergestothetruevalueofex

SpecialCase:Whenx=1: e =1+x+x /2!+x /3!+···=2.718... 1 2 3

This shows the use of Taylor series to approximate the valueofeitself.

Using only the first few terms already gives a close approximation: 1+1+1/2+1/6=2.666... whichapproaches2.718asmoretermsareincluded.

Theconstanteisthenaturallanguageofgrowth,itoftenappearsinprobabilityandstatisticsbecauseitcould modelcontinuousgrowth,decay,andwaitingtimesbetweenevents.Wheneveraquantitygrowsordecaysat a rate proportional to its current value, the mathematics naturally leads to an exponential function of the form ekx

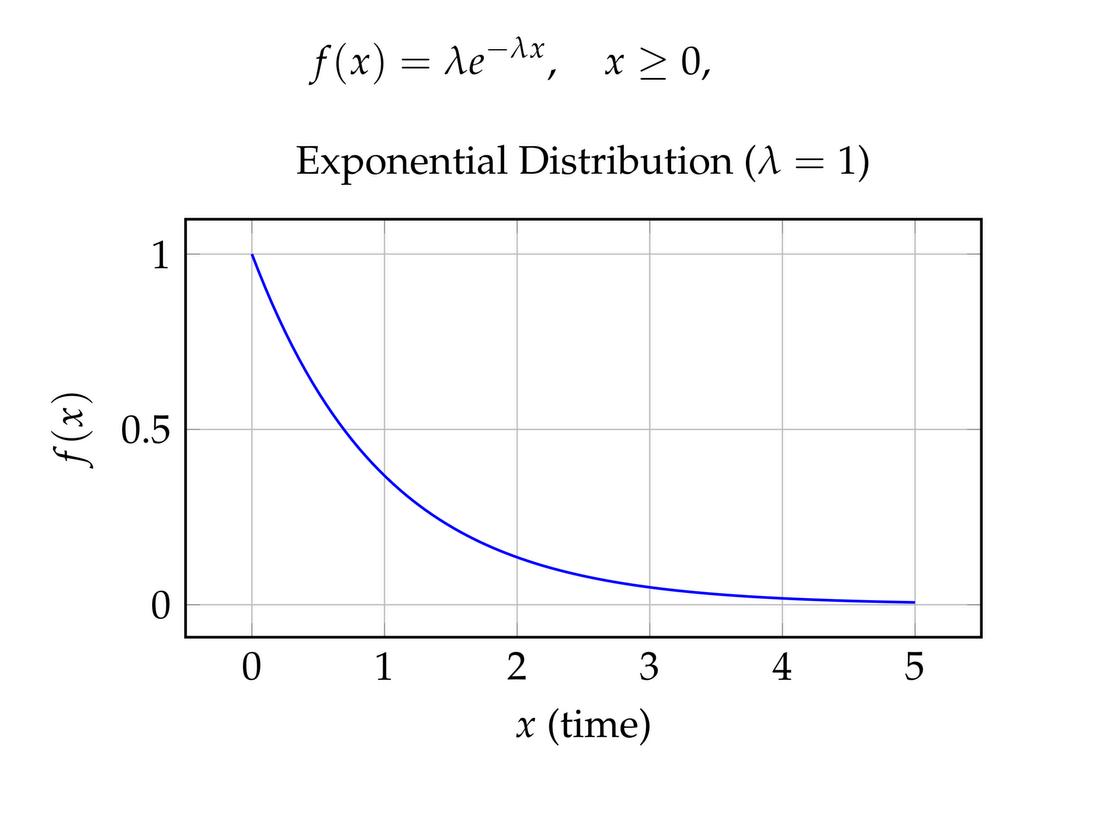

In probability and statistics, this same idea appears in the exponential distribution, which models the time betweenrandomeventsinaPoissonprocess.Itsprobabilitydensityfunctionis:

Inthiscontext,λshowshowofteneventshappen

A larger λ means events occur more quickly, while a smaller λ means they take longer to occur. As shown in the graph, the probability density decreases rapidly at first and then approaches zero, which is how the exponentialdistributioncapturestheideaofcontinuousprobabilitydecaygovernedbye

Fill in the crossword below, take a screenshot and fill in the feedback form at the end of the newsletter (and attach your screenshot on this form) for a chance to win a prize!

DOWN: 1. Rare, extreme, unpredictable loss events.

3. Protecting systems from digital threats. 5. Financial protection against loss.

7. Legal responsibility for harm or loss.

10. Global accounting and auditing firm.

2. Money taken out of an account. 4. Payments for insurance coverage.

6. High-severity, low-frequency catastrophe rise.

8. Major global consulting and professionalservices network.

9. Chance of loss or harm.

LSESU Actuarial Society’s Research Division

Ze Kai Ng (Research Co-Director)

Ying Zi Tang (Research Co-Director)

Mohammad Abdul Rahim

Jasmine Carpiz

Yichen Chong

Braxton Lim

Tobi Park

April Phuan

Hassanal Safiullah

Sylvia Zhu

LSESU Actuarial Society’s Marketing Division

Nirah Rahman (Marketing Director)

Janusmmy Arulchelvan

Luvlynn Bholah

Sienna Singh

Ze Kai Ng (Research Co-Director) - Z.K.Ng@lse.ac.uk

Ying Zi Tang (Research Co-Director) - Y.Z.Tang@lse.ac.uk

Nirah Rahman (Marketing Director) - N.Rahman6@lse.ac.uk

@lsesuactsoc

www.linkedin.com/company/lsesuactsoc lsesuact@gmail.com

Please take a moment to fill in the short feedback form below. It will help us improve future editions of our newsletter and tailor our content better to you. Thank you! Click here for feedback form