One of the simplest and most tax-efficient ways for clients to build wealth over time remains underutilised in many portfolios.

Cover story and Pg15-17

WHAT FINANCIAL ADVISERS CAN EXPECT IN 2026

It’s going to be a year shaped by renewed business confidence, shifting client expectations and a fast-moving regulatory and technological landscape.

Pg6-11

HOW TO SET FINANCIAL GOALS

Effective financial goal-setting begins with understanding a client’s life ambitions and translating them into clear, measurable and achievable long-term targets.

Pg12-14

GETTING RETIREMENT PLANNING BUY-IN

Despite retirement planning being essential for South Africans, many are still woefully underprepared. But how can FAs help to remedy this worrying situation?

Pg18-23

TACKLING TECHNOLOGY

We look at the latest news in the world of technology. Keeping informed can enhance the advisory process by streamlining administration, improving personalisation and freeing advisers.

Pg24-27

WANT MORE VALUE FROM YOUR INBOX?

Scan to subscribe to our weekly newsletters.

Are South Africans maximising the TFSA opportunity 10 years on?

By Andrea Malyon MoneyMarketing Contributor

Adecade after their launch, Tax-Free Savings Accounts (TFSAs) have become a familiar part of South Africa’s investment landscape. Created to foster a culture of disciplined long-term saving, they remain one of the simplest and most powerful ways for individuals to grow wealth without the drag of tax.

Yet, despite their accessibility and advantages, many South Africans still misunderstand how TFSAs work, resulting in missed opportunities, premature withdrawals and sub-optimal investment choices. Conversations with industry leaders reveal a TFSA market that has matured considerably, but one that still relies heavily on advisers to help clients capture its full value.

A market of missed opportunities

When TFSAs were introduced in 2015, investors approached them cautiously. Today, nearly every bank, Linked Investment Service Provider (LISP), and asset manager offers TFSA solutions, and balances have increased significantly as early adopters approach a full decade of contributions.

According to Daniel van Andel, Head of IFA Proposition at Allan Gray, strong recent market returns have helped long-term TFSA investors build substantial balances, with some now exceeding R500 000 and a few even approaching R1m. “We are starting to see the positive impact of tax-free growth over longer periods,” he says. Investors who contributed consistently and stayed invested through multiple market cycles are now benefiting from compounding that has been completely shielded from tax.

Murray Anderson, Head of Retail at Prescient Investment Management, echoes this sentiment. He points to a clear behavioural shift in the market: more investors are moving away from cash-based TFSAs toward balanced funds and other growthoriented investments. “The most notable behavioural change is the shift into growth assets to maximise tax-free compounding,” he observes. Monthly debit orders (often around R3 000) have also become more common, signalling increasing commitment to longterm behaviour.

Despite these improvements, both experts agree that TFSAs remain widely misunderstood – and often misused. Short-termism, early withdrawals, and overly conservative investment allocations continue to hold investors back.

Persistent misconceptions

The single most damaging misconception is around the contribution rules. Withdrawals from a TFSA cannot be replaced. Once funds are taken out, the contribution room is permanently lost. Attempting to ‘replace’ a withdrawal later in the year can also result in accidental excess contributions and a punitive 40% penalty from SARS. “Many investors treat TFSAs like transactional accounts or short-term savings pockets,” says Anderson. “But the real value only emerges after 10 or more years, when the compounding effect accelerates.”

Another misconception is the belief that cash is a safe default inside a TFSA. While cash lowers volatility, it also severely limits long-term returns. Over a multidecade horizon, the opportunity cost is immense when compared with a diversified balanced fund or equity exposure.

A third misunderstanding relates to tax treatment. Unlike retirement funds, TFSA contributions do not reduce taxable income. “The real advantage is not the contribution – it’s the tax-free growth and tax-free withdrawals later on,” Anderson stresses.

Van Andel notes that some investors still use TFSAs for short-term goals, which tends to push them into conservative investment choices and results in premature withdrawals. This behaviour erodes the taxfree compounding runway and wastes a portion of the lifetime allowance.

A structural advantage that still goes unused

Diane Behr, Head of Operations at Foord, underscores just how advantageous TFSAs are, especially when viewed correctly. “The way to think about a TFSA is like a private pension fund,” she explains. “The structure gives you major tax advantages and encourages disciplined saving. Inside the fund you get tax-free reinvestment, and over time that makes a huge difference.”

For Behr, the biggest missed opportunity is simply that many South Africans are not using their TFSAs at all, despite their clear benefits. “One of the most important things advisers should be doing is making sure that clients use their full annual allocation every year,” she says. This extends beyond adults. Parents and grandparents can open TFSAs for children or grandchildren, giving younger generations a powerful compounding advantage from day one.

Image:

Add certainty to your client’s retirement income planning with a guaranteed annuity.

Continued from previous page

Behr also stresses that advisers must strongly discourage early withdrawals. “You don’t get the benefit back if you take money out early,” she says. The permanent loss of contribution room is often poorly understood and results in long-term damage that investors only see years later.

Her message is simple: a TFSA is one of the most advantageous savings structures available – and more people need to make use of it.

“The single most damaging misconception is around the contribution rules”

How TFSAs compare with other savings options

TFSAs are often compared with discretionary unit trusts and retirement products, but each serves a different purpose. The TFSA’s clearest advantage over discretionary investments is the total absence of tax on interest, dividends or capital gains. Over long periods, this lack of tax friction significantly boosts net returns.

Retirement funds offer compelling tax deductions on contributions and shelter investment growth from tax, but come with meaningful trade-offs. Regulation 28 limits asset allocation, access before retirement is restricted and two-thirds of the final balance must be used to purchase an annuity, where retirement income is taxable.

TFSAs, by contrast, offer complete asset flexibility, full liquidity and zero tax on growth or withdrawals. The trade-off is the contribution cap and the irreversibility of withdrawals.

For most clients, the optimal sequence remains:

Maximise the tax deductions offered by retirement funds

• Contribute the full annual TFSA allowance

• Direct further savings into discretionary investments

This layered approach ensures every available tax benefit is captured.

Product choice and the importance of staying invested

Behr notes that because TFSAs allow for taxfree distribution reinvestment, investors are generally better off holding growth-oriented funds where compounding can work hardest. “You’re better off compounding dividend income inside a TFSA,” she says. “If your intention is long-term investment, a growth fund makes sense.”

Investors are not locked into one TFSA product or provider. Transfers between providers are allowed without triggering tax,

and switching within a platform is possible. However, Behr advises that sticking with one provider is usually simpler, unless there is a clear strategic reason to move. What she discourages strongly is cashing out entirely, once again because the contribution room can never be regained.

Across the board, the experts identify similar strategies that advisers should prioritise:

• Start early and stay invested

• Automate contributions

• Prioritise growth assets

Use discretionary accounts for short-term needs

Educate clients with simple projections.

Product evolution and the future landscape

As the TFSA market matures, product design continues to evolve. Van Andel notes that asset managers are broadening their TFSA fund offerings to suit different risk profiles and long-term goals. Allan Gray’s life-policy structure also provides estate-planning advantages: proceeds can be paid directly to beneficiaries, bypassing the delays of the estate process.

Anderson sees innovation emerging in the form of all-in-one TFSA portfolios that automatically rebalance and gradually derisk, along with digital contribution-tracking tools that help investors avoid excess contributions and penalties.

Looking ahead, both Van Andel and Anderson expect possible increases to the annual or lifetime TFSA limits. This is particularly relevant for early adopters who will soon reach the R500 000 lifetime cap. The next few years will also see younger adults taking control of TFSAs opened by their parents, and more older investors drawing down from mature accounts to fund education, retirement income or other long-term goals.

Foundations built, but much work remains

After 10 years, TFSAs have unquestionably met their objective of encouraging longterm saving. Investors who have contributed consistently and stayed invested now have meaningful tax-free wealth to show for it. Yet the full potential of TFSAs remains underutilised. Misconceptions, premature withdrawals, and conservative allocations continue to diminish outcomes.

Here, advisers have enormous influence. As Behr emphasises, advisers should aim for two things above all: get clients invested in TFSAs and keep them invested. When used properly, TFSAs offer one of the most powerful compounding opportunities available to South Africans. The structure is sound, the benefits are proven, and the opportunity remains underused.

ED'S LETTER

As we step into 2026, it’s refreshing, at last, to do so on firmer ground. After several years defined by volatility, uncertainty and subdued sentiment, South Africa closed out 2025 with a welcome shift in tone. The Business Confidence Index moved upward by five points, placing it three points above its long-term average. It suggests something invaluable: renewed optimism, and the sense that momentum may finally be turning in our favour.

In this issue, we look at what 2026 may hold, drawing on expert forecasts to give you a grounded sense of the environment in which you’ll be advising, planning and investing.

From economic projections to regulatory expectations, our aim is to help you start the year with clarity rather than conjecture.

We also dig into one of January’s most important advisory conversations, which is helping clients set meaningful, achievable financial goals; and with tax-free savings once again top of mind early in the year, we explore how to maximise the benefit of these products.

Retirement also features prominently this month, particularly relevant as South Africa continues to refine its broader retirement reform landscape.

And of course, no discussion about the future of financial advice would be complete without touching on technology. Artificial intelligence is reshaping the industry, but the real differentiator lies not in having access to AI, but in knowing how to use it responsibly. On behalf of the entire MoneyMarketing team, we wish you a prosperous and productive New Year. Stay financially savvy,

Sandy Welch Editor, MoneyMarketing

Note: If you subscribe to our MoneyMarketing newsletter, see QR code on the cover, you will receive a special discount off a News24 or Netwerk24 subscription*. *Offer available to new subscribers only.

With stronger education, more consistent advice and better long-term discipline, TFSAs can continue to transform the financial futures of South

Africans for decades to come.

Nicola Langridge Wealth Manager at Private Client Holdings

The FPI 2025 Financial Planner of the Year, Nicola Langridge, shares some insights from her journey into finance.

Why did you become a wealth manager – was it something you always wanted to do?

I did not even consider a career in wealth management when I was in high school. I grew up in a medical- and wellness-focused family, my plan was to become a doctor, and I spent two years studying Chiropractic. However, I soon realised that it was not my passion. I decided to start a wellness business, which led to me registering for a Business Science Degree in Finance at UCT. It was there that my love for finance was sparked. A few years later, a financial planner introduced me to the world of financial planning and showed me how my love for holistic wellness could be applied to financial wellness.

What was your first meaningful successful investment?

My first two meaningful investments after university were the creation of my emergency fund and my retirement fund, both of which I set up as soon as I started working. Saving for retirement as early as possible is vital, even if you can only contribute a small amount at the outset. I now see too many clients that start saving later in life and have to either catch up in their 50s or work much later than they originally planned.

What have been your best and worst financial decisions?

My worst financial decision was to put off buying a primary residence for a long time. I think buying a small property at a young age would have been a smart move. A good financial decision was to start tax-free savings accounts for each of my kids at their births, so that I know there will be enough saved for their university education.

What keeps you up at night in terms of the economy?

I sleep well because I know that the economy moves in cycles. I think I am more concerned with what keeps my clients up at night, as there is so much fake news out there that can really scare and confuse them. Trump's antics are detrimental to anyone's sleep.

“The best investment in any economy is a well-diversified one”

What makes a good investment in the current environment?

The best investment in any economy is a welldiversified one. At Private Client Holdings, we follow a goals-based wealth management process, which means my clients set clear goals that they want to achieve, and we structure their investments to best achieve each of those goals. We review progress regularly and update as required. All investments are part of our Family Office approach to wealth management, which means that all investments form part of a holistic wealth management plan.

What expectations do you have for 2026?

As the 2025 / 2026 FPI Financial Planner of the Year and as a new ambassador for the FPI, I will strive to continue to nurture my clients’ wealth. I hope to provide great financial educational content to a much wider audience across various channels, and to have the platform to encourage more young professionals to join our profession.

EARN YOUR CPD POINTS

What are some of the best books on finance/investing you have ever read, and why would you recommend them?

The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel is a great book for both advisers and clients.

The FPI recognises the quality of the content of MoneyMarketing’s January 2026 issue and would like to reward its professional members with 2 verifiable CPD points/ hours for reading the publication and gaining knowledge on relevant topics. For more information, visit our website at www.moneymarketing.co.za

By Francois du Toit CFP® PROpulsion

CAre you building a practice or business?

an you step away from your firm for three weeks without checking in? If the answer makes you uncomfortable, you are running a practice that depends on you. If you could disappear and the business would continue smoothly, you have built something more valuable.

The difference matters. Understanding the value of every aspect of an adviser’s practice is crucial for improving long-term growth and unlocking revenue opportunities. Practices depend on their founder’s struggle to attract buyers. Businesses built with systems and teams command premium valuations.

Here are five strategic decisions that determine whether you build for cashflow today or business value tomorrow.

Diagnose your revenue model

Does your income come from transactions or trust? Product-focused firms earn when they sell. Adviceled businesses earn recurring revenue from ongoing relationships.

According to the 2024 Momentum Financial Advice Report, only 9% of South African households use professional financial advisers, yet the average investment amount for households with an adviser is significantly larger than those without.

Ask yourself: if no new products were sold this quarter, would your revenue collapse or hold steady? Recurring revenue creates predictable cashflow and attracts higher valuations. The shift from product sales to advice fees signals a business model built on relationships rather than transactions.

Decide between transactions and relationships

Transaction-focused practices chase the next sale. Relationship-driven businesses deepen existing connections. According to analysis from Thomson Reuters Research Institute’s Cost of Compliance Report 2022, independent intermediaries in South Africa spend only 35% of their time interacting with clients. This reality makes every client interaction more valuable.

Research shows that new adviser failure rates have reached 72% within the first year, yet established practices have opportunities to scale. The relationship model scales differently. You need systems, not just stamina.

A recent comment by the chief executive of a large South African insurer revealed that the country needs another 4 000 financial advisers – highlighting the opportunity for well-positioned firms.

Your value must be obvious

Can your clients explain what makes you worth the fee? If they cannot articulate your value, you have a pricing problem waiting to happen.

then find tools that support them. According to industry analysis, advisers who have the best control of their data will be the winners, with artificial intelligence serving as a mechanism to extract data more efficiently.

Strip away the noise

What really matters in your business? Most firms chase activity instead of creating impact. Choose three metrics: recurring revenue growth, client retention rate, and profit per client. Ignore vanity metrics unless they connect directly to profitability.

“Advice-led businesses earn recurring revenue from ongoing relationships”

According to a 2024 report by Old Mutual’s Savings and Investment Monitor, more than 70% of South African households cannot cover an unexpected expense equal to one month’s income. Yet, many advisers struggle to communicate their value clearly. Make your value visible through three actions. First, show clients what they gain beyond investment returns: tax strategies, estate plans, decisions simplified. Second, create a one-page annual summary listing every service delivered. Third, ask clients to describe your value in their own words, then use that language.

Research by PwC South Africa reveals that women are 30% less likely to work with financial advisers, despite often needing more robust retirement strategies. This gap represents both a communication failure and an opportunity.

Technology: Enhancing without replacing

Research shows that advisers who outsource business functions to specialised providers promote efficiency and scalability. Start with your strategy and process,

According to Ninety One’s tracking of 35 independent wealth advisory firms in South Africa, well-established advice firms focus on what they can control: highquality engagements with clients seeking guidance. Block two hours each month to review these numbers with your team. If a metric is not improving, change one thing and measure again.

Ask yourself two questions:

• What small shifts could you make this year that would create long-term change? Perhaps moving one service from reactive to proactive, or training one team member to handle reviews independently.

• What would happen if you stayed the same for five years? Research shows that 66% of heirs of older South African clients are likely to leave the country. Inaction is a decision with consequences.

Building a business instead of a practice requires intentional choices about revenue models, relationships, value communication, technology, and focus. Make those choices by design, not by default. The smallest viable next step: pick one of the five decisions above and review it with your team this quarter. Measure where you are, decide where you want to be, and document three actions that will close the gap.

Stay curious!

Get ready for a noisy year!

In 2026, rewards will come to those who are willing to rebalance boldly but thoughtfully; who diversify globally without abandoning local conviction; and who help clients embrace the entrepreneurial mindset required to navigate the next chapter in global investing. That was the overall message from Morningstar’s Outlook for 2026, presented by Morningstar’s Global Chief Research and Investment Officer, Dan Kemp.

A different kind of outlook

Kemp was quick to make one thing clear: Forecasting with confidence is not only misleading; it actively harms clients. Predictions create expectations and expectations create surprise – a powerful behavioural trigger that prompts investors to freeze, fight or flee. Freezing is manageable. Fighting, trying to trade one’s way out of volatility, rarely works. Fleeing can destroy long-term outcomes.

Staying invested, no matter what

The behavioural research behind the Outlook reinforces three adviser imperatives for 2026: Prepare clients for volatility before it arrives, arm them with clear information, and prioritise education over reaction. When clients expect turbulence, they’re less likely to be shocked by it. When they understand the forces shaping markets, they’re less likely to abandon a well-built plan. And when portfolios are constructed for robustness, investors are better equipped to stay invested and seize opportunity. The year ahead will be noisy. But advisers who anchor clients will give them the best possible chance of reaching their goals.

The AI arms race and the problem of concentration

The global AI narrative has lifted the ‘Magnificent Seven’ to near-mythical status, and with it, investor exposure to a narrow segment of the US market. While concentration alone doesn’t guarantee a correction, it does erode diversification benefits and leaves portfolios vulnerable to sudden sentiment shifts.

It’s worth noting that US small caps remain materially undervalued compared to their large-cap peers, after years of underperformance. Likewise, US healthcare presents attractive entry points in an otherwise fully valued US sector landscape. For clients reluctant to step away from

the familiar comfort of US equities, these represent credible pathways to rebalance without abandoning the market entirely.

The case for looking offshore

Much of the real excitement, however, lies outside the US. Emerging markets have delivered strongly, supported by both local performance and a softer dollar. Markets such as Brazil, Mexico and South Korea stand out for their mix of strong economic momentum, structural reform and valuations that still imply upside. China, despite perennial debate, remains a meaningful opportunity set, particularly for tech exposure that is both broad and high quality.

For South African advisers, the offshore diversification message remains essential. But 2026 will require more nuance: not all emerging markets are created equal, and not every undervalued market is undervalued for the right reasons. Country selection matters more than ever.

“When clients expect turbulence, they’re less likely to be shocked by it”

The dollar will be discounted, but not cheap

One of the trickiest dynamics clients will be grappling with heading into 2026 is the behaviour of the US dollar. After years of dominance, 2025 delivered an uncomfortable reversal. But a weaker dollar doesn’t automatically signal a collapse in reservecurrency status.

The more grounded interpretation is that the dollar is cheaper than it was, but it’s still overvalued. Tools like the Big Mac Index still suggest the rand is more than 40% undervalued relative to the dollar.

For advisers, the message is not to build narratives around the dollar’s demise, but to help clients understand:

• Why a weaker dollar impacts offshore returns

• Why speculation around gold or cryptocurrency often rides on shaky assumptions, and How to avoid overreacting to currency cycles.

Most importantly, advisers should caution against DIY currency hedging. Correct hedging depends on client perspective, asset mix, base currency and long-term investment goals, which are variables too complex to manage in isolation.

South Africa, the quiet outperformer

Amid the global narrative, South Africa delivered a surprisingly strong US dollar performance in 2025, largely unnoticed because the country represents just 3% of emerging market indices. It did so without foreign investor inflows, which have continued to trend negative. This means that local returns have been driven by fundamentals, not sentiment.

Much of the JSE’s strength came from a concentrated group of precious-metal miners benefiting from elevated gold and platinum prices. But looking ahead to 2026, the sector-level picture tells a more interesting story:

• Resources as a broad category now screen as relatively low-return prospects, especially gold and platinum miners, which appear fully priced

Global diversified miners listed locally, including BHP, Anglo American and Glencore, still show reasonable valuationbased upside

South African financials offer the most compelling real return expectations for rand-based investors. The major banks remain well capitalised, prudently managed, and benefit from valuations that still sit at attractive levels despite economic headwinds.

For local, rand-based investors, SA equities remain priced to deliver higher expected returns than developed and emerging market peers. For international investors, however, South Africa is a tougher sell. The benefits of cheap valuations are offset by liquidity constraints, currency volatility and opportunity costs versus larger emerging markets offering broader exposure.

Guiding clients through the transition

As 2026 unfolds, advisers will play a critical role in helping clients move from passive participation to intentional positioning. The transition resembles a shift from corporate security to entrepreneurial freedom. Clients can’t rely on one dominant market (the US) to do the heavy lifting

Finally, questions around the dollar, US debt and gold serve as a reminder that markets often price in risks long before they appear in the headlines. For advisers, the role in 2026 is clear. Guide your clients away from speculation and toward durable, evidence-based strategy.

Why 2026 could be the year Africa rewrites its investment story

Speaking at the SuperReturn Africa Conference, John McDermott, Chief Africa Correspondent for The Economist, examined what experts are predicting from Africa for the coming year and how inflation, currency and interest rate trends are shaping investment decisions.

For years, Africa’s economic narrative has been shaped by volatility, uneven reforms and political fragility. Yet beneath the noise, the continent’s fundamentals have been shifting, quietly at first, then unmistakably in 2024 and 2025. As we move toward 2026, investors with an eye on long-term opportunity may find that Africa is no longer a peripheral consideration, but a region entering a new phase of geopolitical relevance and economic resilience.

A front-row seat to multipolar geopolitics

Africa today offers perhaps the clearest view of the world’s accelerating multipolarity. It is the place where East and West, and increasingly the ‘Rest’, intersect most visibly. A striking representation of this is a multicoloured map of trade, investment and scientific flows into Africa. The picture is unmistakable: Africa trades more with China but finances more with the West, and across nearly every category, the diversity of partners has surged in just two decades. Multipolarity brings risk but also diversification, competition and interest from new players.

US–China rivalry brings risk and opportunity

In previous cycles, African fortunes swung on the dominance of a single big partner – first China in the 2000s, and then the US in earlier decades. But in today’s geopolitical shuffle, Africa is not a bystander. If anything, the return of a more transactional US foreign policy is driving fresh commercial diplomacy. Agencies like US Exim Bank and the Development Finance Corporation (DFC) are stepping up financing in strategic corridors such as Angola’s Lobito project.

China, meanwhile, has moved from the ‘1.0 era’ of large infrastructure loans to a ‘2.0 era’ rooted

For financial advisers, Africa in 2026 is not just a frontier, it is a region in transformation. Those who understand its shifting dynamics will be best placed to guide clients toward opportunities that balance risk with long-term potential.

Three forces converge next year:

1 Geopolitical competition that increases investment options, partners and financing

2 Structural economic momentum, including AfCFTA, stronger capital markets and ongoing reforms in key economies

in investment and consumer penetration. Chinese companies, from smartphone giants to solar technology firms, are expanding briskly across African markets. Exports from China to Africa have surged precisely because other regions are turning inward.

The rise of middle powers

More intriguing still is the growing influence of middle powers, including the UAE, Saudi Arabia, Qatar, Türkiye, India, Vietnam and Brazil. The UAE is now the fourth-largest investor in Africa. Türkiye is fast becoming a dominant infrastructure builder. Indian tech firms are laying digital foundations in emerging African markets. Vietnamese and Southeast Asian firms are pushing into agro-processing. Brazil’s agricultural research agency has opened new offices on the continent. This widening of partners creates competition –and competition improves financing, terms and long-term opportunities for investors.

“Africa may not yet have fully arrived, but the direction of travel is clear”

African responses are more strategic than ever Against this backdrop, African governments are not acting passively. Three responses define the current moment:

1. A strategic ‘scramble’ for US market access Initial panic following tariff threats gave way to more coordinated diplomacy. As political relationships stabilise, bilateral deals, and possibly a reworked AGOA, are again feasible.

2. Portfolio diversification

African leaders are increasingly widening their networks to include Gulf, Asian and alternative Western partners. Deals are being struck quickly, with countries like Zambia and Ethiopia successfully pulling investment from new and agile players.

3. The African Continental Free Trade Area (AfCFTA)

The AfCFTA has become the symbol of Africa’s resolve to reduce fragmentation and build resilience. Nearly every country has

3 A demographic and political push from increasingly vocal citizens demanding accountability, opportunity and growth.

ratified the agreement, and implementation momentum is building. AfCFTA has the potential to enable regional value chains, reduce commodity dependency, attract more manufacturing and investment, and create a unified market of 1.4 billion people.

This is the type of structural reform that changes long-term investment cases.

Macroeconomic resilience equals a turnaround Geopolitics sets the scene, but macroeconomics drives the investment story. Here, too, Africa is signalling a shift. According to the IMF, subSaharan Africa is set to be the fastest-growing region globally in 2026. Ten of the world’s 20 fastest-growing economies are African. Inflation is cooling, currencies are stabilising, and several capital markets have reached record highs. Portfolio flows are turning positive, partly because global reallocations away from China are creating openings that more agile African markets can capture. South Africa and Nigeria, the region’s largest economies, are finally pushing through long-awaited structural reforms. If sustained, these reforms could unlock substantial investment momentum.

Debt remains a challenge

The biggest headwind is debt. Twenty countries are in or near distress. Many governments are increasingly relying on expensive domestic borrowing, which strains banks and crowds out private investment. Without reforms in debt management, capital markets and revenue systems, growth could stagnate.

Still, advisers should recognise that Africa’s debt problem is partly a story of underinvestment. Investment as a share of GDP lags behind Asian peers, not due to lack of opportunity, but due to demographics, underdeveloped markets and risk perceptions.

Encouragingly, new research is helping close information gaps. A recent analysis of IFC private equity returns from 1961 to 2020 shows that African returns, over the long term, outperform both MSCI EM and the S&P 500. Data like this helps correct the ‘perception premium’ that inflates Africa’s cost of capital.

Schroders’ Crystal Ball 2026

As 2025 draws to a close, financial advisers are preparing clients for another year defined by complexity. Debt, artificial intelligence, geopolitics and central bank independence shaped the investment conversation this year, and according to experts at Schroders’ recent Crystal Ball 2026 briefing, the variables may shift but the uncertainty isn’t going anywhere.

The session brought together two key voices: Johanna Kyrklund, Group Chief Investment Officer, and Nils Rode, Chief Investment Officer of Schroders Capital to unpack the global landscape and identify where advisers should focus for 2026.

A new political and economic reality

Kyrklund said that while market sentiment has been surprisingly resilient, especially in the United States, the drivers behind that strength point to a deeper political and economic shift, and not just the impact of a US election cycle.

She described the last decade as a turning point away from globalisation and tight fiscal policy – which were hallmarks of the 1990s and 2000s – towards an era defined by anti-globalisation, looser budgets and higher inflationary pressures. “Nominal growth has been phenomenal in the US, and nominal growth supports corporate earnings,” she noted. This is the backdrop against which 2026 must be viewed.

Populist policies may be supporting growth for now, but advisers should remain mindful of their ultimate constraint: the bond market’s tolerance. While debt levels continue to climb, current inflation dynamics are keeping yields under control. A more dovish Federal Reserve is helping too, though Kyrklund warned that its stance may be too dovish in the long term.

Bubbles,

froth and the limits of

valuation

A major concern for investors heading into 2026 is valuation risk. Kyrklund pointed to widening signs of exuberance reminiscent of the late 1990s, though not yet at extremes.

The US equity-bond yield gap sits firmly in ‘expensive, but not bubble’ territory. Meanwhile, the outperformance of non-revenue tech companies and the rise of leveraged equity ETFs signal froth in certain parts of the market.

The takeaway? Selectivity matters more than ever. Kyrklund emphasised that while bottom-up opportunities remain, thanks to strong free cashflow in key tech names, passive exposure to mega-cap dominance is risky this late in the cycle. Active management and disciplined position sizing will be essential.

Rethinking diversification in an inflationary era

One of the most meaningful structural shifts is the changing role of fixed income. In a de-globalised, more inflation-prone world, bonds no longer reliably deliver the equity diversification investors enjoyed from 2008 to 2020. The return to a positive stock-bond correlation means that advisers should once again treat fixed income primarily as a yield generator, not a hedge.

Instead, Kyrklund recommended looking to: Gold and select commodities

Emerging markets, where more orthodox fiscal policies and attractive real yields create opportunity

• Geographic diversification, as markets such as China and European financials show renewed strength

Fixed income alternatives such as catastrophe bonds, which offer uncorrelated yield.

Another key concern is the weakening diversifying power of the US dollar. Historically, the dollar has risen when equities fall, but this year both declined together. Advisers planning global allocations should keep a close eye on Fed credibility and future inflation cycles.

Preparing for a ‘resilient first’ era

Switching to the private markets outlook, Rode emphasised the need for resilience rather than momentum-driven investing. With holding periods often extending well beyond five years, private market investors must focus on themes that endure through cyclical shocks, not just those that look attractive in a single calendar year.

Rode highlighted several important dynamics: 1. A four-year slowdown and a bottom in sight

Private markets have been cooling since 2021, with declines in fundraising, deal flow,

exits and valuations. While painful for existing allocations, this environment is creating more attractive vintage years for 2024–2026. Lower competition and healthier valuations, especially in small and mid-cap buyouts, present long-term opportunities.

2. Small and mid-cap buyouts: Quiet outperformers

Contrary to assumptions that smaller companies carry higher risk, data across 25 years shows these buyouts consistently outperform large-cap strategies during crisis periods. Their lower leverage and predominantly local revenue bases shield them from global trade tensions and geopolitical volatility.

3. Continuation funds are here to stay

Continuation vehicles, where an asset remains with the same private equity sponsor for an extended period, are growing structurally, not just cyclically. They offer lower fees, fewer surprises, and faster liquidity, which make them a compelling tool for advisers seeking stability in private equity exposure.

4. Diversified private debt remains attractive

Private debt has weathered the slowdown better than any other private market segment, thanks to floating-rate structures. Rode highlighted: Insurance-linked securities (cat bonds) for uncorrelated returns

• Real estate and infrastructure debt, supported by strong collateral and defensive characteristics

Opportunistic income strategies able to move across asset classes.

5. Real estate and renewables: A reset, then recovery

Real estate has seen the steepest correction, especially office assets in the US and UK, but Rode believes a floor is forming. Higher construction costs and rental inflation are improving fundamentals for new deployments. Renewable infrastructure, especially in Europe and Asia, remains supported by strong economic and political tailwinds.

What’s under the radar for 2026?

Asked where opportunities may be overlooked today, both CIOs pointed to areas beyond the dominant US tech narrative: International equities such as European banks, China’s growing tech ecosystem, and value styles outside the US.

Small and mid-market private equity

Early-stage innovation globally, with India standing out as the least-correlated major market.

Rode underscored a subtle but crucial trend in private markets: while quarterly data suggested an uptick in investment activity, the reality for most of the market painted a different picture. This apparent

“One of the most meaningful structural shifts is the changing role of fixed income”

increase was largely skewed by a handful of very large transactions, masking a broader slowdown affecting most of the private equity, venture capital and innovation deals. Rode also addressed concerns around AI-related investments, particularly in sectors like data centres and energy. He noted that while exposure exists, it is selective and spread across value chains rather than concentrated. The bulk of these investments are early-stage companies with significant growth potential, alleviating fears that a late-cycle correction in AI could ripple broadly across private markets. According to Rode, these strategic investments are grounded in fundamental growth rather than speculative momentum, providing resilience in an otherwise highvolatility environment.

The situation in Europe

When discussing opportunities in European equities, Kyrklund highlighted European banks and mid-cap value stocks as areas of potential outperformance, contrasting the US where mega-cap technology dominates. Rode complemented this perspective, pointing to healthcare, particularly biotech, as a contrarian opportunity, noting that the sector had cooled after peaking in 2021. He stressed that private market investors should consider these underappreciated segments for resilient, long-term growth, rather than chasing the headline-grabbing sectors.

Absolute return strategies and hedge funds also drew attention. Kyrklund observed that with yields in traditional assets declining and gold becoming more correlated with equities, liquid alternatives and absolute return vehicles now present a compelling avenue for diversification. Investors should focus on liquid, transparent exposures to manage risk effectively while capturing returns from less conventional strategies.

Energy transition and infrastructure investments, particularly in Europe and Asia, continue to offer strong entry points despite fundraising slowdowns. Long-term demand, political support, and attractive valuations make these investments appealing for patient capital. Similarly, semi-liquid structures and continuation funds are expanding access to private markets for a broader investor base, allowing individuals to participate in highquality, resilient assets while accommodating liquidity needs.

What financial advisers should keep in mind

The outlook for 2026 is one of paradox: a benign macroeconomic backdrop paired with late-cycle valuations and rising geopolitical risk. The consensus from Schroders’ leadership is clear: Stay invested, but be selective. Manage exposure to mega-cap tech actively. Prioritise resilience, diversification and real sources of yield. Look beyond the US because opportunity is broader than the headlines suggest.

By Sean Hanlon Executive Director at BrightRock

TCrafting clientcentric insurance for the year ahead

he core of insurance has always been protection, but the very definition of what constitutes effective protection is undergoing a seismic shift. As we look into 2026, our industry stands at a pivotal intersection: static, one-size-fits-all policies are rapidly becoming relics of the past. Today’s consumers, navigating an increasingly complex and unpredictable world, demand solutions that are dynamic and can change with them as their lives change.

Here are some essential insights to consider when getting your clients cover.

1. Insurance that evolves with life

Static, one-size-fits-all insurance is becoming obsolete. Consumers are demanding products that adapt dynamically to their evolving circumstances – not policies that remain frozen in time while their lives move forward. The growing demand for innovative, flexible and highly customisable insurance solutions is driven by several shifts in the life insurance landscape.

South Africa’s insurance market is one of the most competitive globally, prompting insurers to differentiate through customer-centric product design. At the same time, digital transformation and the expansion of new distribution channels have raised consumer expectations for convenience, adaptability and seamless service. The industry’s increasing focus on transparency, fair treatment and simplified underwriting has also encouraged the development of products that better match people’s evolving financial needs. Together, these trends underscore a clear market appetite for more personalised and adaptable insurance offerings. This is where needs-matched cover, such as BrightRock’s offering, becomes especially relevant.

2. Income protection is at the heart of financial protection

With inflationary pressures and economic volatility affecting households across Africa, ensuring a steady income flow during times of illness and injury is paramount. Futurefocused insurers can track an individual’s earnings trajectory, rather than static lump-sum benefits. Tracking the number of pay cheques a client has left to earn until retirement ensures that their cover precisely matches their needs, is more affordable, and eliminates unnecessary waste.

3. AI, data and technology

Just as in other industries, we expect to see new applications for AI emerge over the next year. Many industry commentators fear that AI may replace human connection, but studies show that consumers increasingly value personal interactions and expert advice, especially in areas of complexity. The true power of digital technologies is in supporting, not replacing, human connection. In this context, advisers will look to personalised product technologies that integrate the advice process with the product solution, freeing them up to focus on what really matters: understanding their clients’ needs and helping them make informed risk protection choices that can meet those needs in the long term.

Three things for advisers to note about insurance of the future

1 Protection must be personal and it must be adaptable

Clients no longer accept static, generic cover. The future of protection is dynamic, needs-matched and flexible enough to shift with life’s milestones. Advisers who prioritise adaptable solutions, rather than traditional one-size-fits-all policies, will be better positioned to provide meaningful, futureproof advice.

4. Affordability through intelligent precision

The industry’s biggest challenge remains accessibility. With household budgets under pressure, traditional cover structures often leave clients either underinsured or overpaying. The future lies in precisionbased affordability, dynamically adjusting premiums and benefits to ensure clients pay only for what they need, when they need it. BrightRock’s needs-matched model embodies this thinking. By aligning cover to financial obligations month-by-month, clients can maintain meaningful protection without the burden of excess cost. This creates a smarter, more sustainable insurance ecosystem that supports retention and longterm client value.

5. The adviser of the future

The role of the financial adviser is being reimagined. Automation can quote a premium, but it can’t interpret human emotion or anticipate how life events ripple through a family’s finances. The adviser of 2026 is no longer a salesperson, they’re a life-stage strategist. They translate complex financial data into decisions that protect futures. As cover becomes more dynamic and client-centric, advisers will be central to ensuring it remains relevant and human.

6. The pillars of client-centric cover

To truly deliver client-centric protection, insurers and advisers must build on three core pillars: Efficiency, ensuring clients only pay for the precise cover they need, exactly when they

2

Income protection is the foundation of real financial security

In an environment of rising costs and economic uncertainty, safeguarding a client’s income matters more than ever. Advisers should focus on solutions that track an individual’s earning journey to retirement, ensuring cover aligns precisely with real needs, avoids waste, and provides genuine financial resilience.

3

Technology enhances advice but human insight remains irreplaceable

AI and digital tools can streamline processes and personalise product design, but they cannot replace empathy, context or judgment. The adviser of the future uses technology to deepen the human connection, enabling smarter conversations, more precise cover and better long-term outcomes for clients.

need it, thereby maximising premium value and fostering trust.

Flexibility, meaning the cover must be capable of easily changing – by both client and adviser – as their lives change; this is paramount for maintaining relevance. And finally, certainty, providing clients with absolute clarity on what is covered and when, as this transparency is crucial for building confidence and alleviating the anxiety often linked with complex financial products.

By Herman van Papendorp Head of Asset Allocation at Momentum Investments Group

2Markets will continue to rewrite the rulebook

025 was the year of Trump for global financial markets. The unpredictability of Trump’s policy pronouncements since his inauguration on 20 January last year has forced global financial markets to continually re-evaluate the basic principles underlying investment thinking and portfolio positioning. What market participants have come to realise is that in the Trump era, nothing is sacrosanct or safe – not policy, not institutions and certainly not historical alliances.

Trump’s unpredictable policies reshape global markets

It is quite ironic (and probably an unintended consequence) that Trump’s alienation of the rest of the world has caused the rest of the world to move closer together in a unified play on the adage that ‘the enemy of my enemy is my friend’. Trump 2.0 has turned out to be Trump 1.0 on steroids. The 2017-2021 period of Trump’s first term was characterised by Trump’s regular postings on then Twitter (now X) that often changed the investment world from the previous status quo. In his second term, Trump has been even more aggressive and more frequent in his utterances about market-moving issues on his own Truth Social media platform.

Record-breaking executive order activity

Trump has also so far in his second term been the second-most active ever of all US presidents with the issuance of executive orders, with his order frequency outpacing those of Hoover (who presided during the early part of the Great Depression, 1929-’33) and only second to FD Roosevelt (whose terms included the latter part of the Great Depression as well as World War II, 1933-’45).

In our view, the combination of anticipated rising US inflation, forthcoming fiscal stimulus measures, and a potential threat to US central bank independence from the Trump administration to force policy rates lower are all risks to the US bond market, while at the very least less negative for US equities than bonds, if not outright equities positive.

“EM earnings revisions have turned positive”

What is expected from the equity market

Research by Morgan Stanley shows that the US equity market historically performed best when US policy rates were in a falling cycle. This is expected to continue in 2026, even though the magnitude of future Fed rate cuts is heavily debated. In addition, analysis by Citi illustrates that when US rate cuts took place during softlanding economic growth periods historically, global equity returns were particularly strong, pointing to potential further equity upside from current levels. Although equity markets in Europe, Japan and EM outpaced the US historically in these soft-landing rate-cutting periods, we think the rest of the world outperformance of the US may be less pronounced this time due to the current large weighting of technology in the US equity market, and with technology historically being a large outperforming sector in softlanding rate-cut cycles.

The threats that remain

Anticipated rising United States (US) inflation, fiscal stimulus measures, Federal Reserve (Fed) rate cuts amid a potential threat to Fed independence, together with higher and more synchronised global regional profit growth in 2026, fundamentally favour global equities over

solid in a soft-landing scenario. However, the magnitude of future US equity returns should be constrained by high valuations that have little room for disappointment.

Key issues to note

In terms of the impact of all of this on South Africa, the following points are salient:

A weaker US dollar, driven by structural and cyclical factors, will likely have positive implications for emerging market (EM) equities relative to developed market (DM) equities, as has been the case in the past. In addition, EM earnings revisions have turned positive, while EM has also become an attractive way to access the global artificial intelligence (AI) investment theme.

We are cautiously confident about the prospective trajectory of the South African (SA) economy and local asset class returns in 2026, with further local rate cuts and some growth acceleration expected from a low base. SA’s recent strong equity performance may help rekindle long-dormant foreign investor interest in SA equities, as has already been the case for SA bonds. An increased global allocation to EM equities could simultaneously result in material global inflows supporting SA equities, particularly given that SA is a high-beta play on EM equities. Due to strong profit momentum, SA equities remain attractively valued against global peers and its own history.

Although the SA nominal bond spread with the US has fallen to levels last seen in 2013, the real ex-ante SA bond yield is still above its historical average, providing an underpin for the asset class. While the absolute level of SA inflationlinked bond (ILB) yields is still high, the absence of inflationary pressures in the coming year points to a lack of fundamental support for ILBs. The combination of moderately rising inflation in 2025 and 150 basis points of SA Reserve Bank (SARB) rate cuts since September 2024 has pushed available real SA cash rates down towards its long-term average, making local cash an inferior investment alternative among the SA asset classes, in our view. In contrast, SA listed property fundamentals continue to improve, with reported net operating income growth the strongest since 2018, and the earnings recovery guided to continue in 2026.

Risks to global markets would be: a deterioration in the AI theme, less Fed rate cuts than expected, a hard landing for the US economy, or geopolitical risk escalation. The main local risk would be the disintegration of the coalition Government of National Unity.

By Carla de Waal Head: Multi Management & Manager Selection at FNB Wealth & Investments

DBuilding winning portfolios for real-world markets

elivering consistent, risk-adjusted returns that meet clients’ medium to longterm goals remains the fundamental challenge for any investment manager. This has nothing to do with prediction, but everything to do with process. That’s why we’ve built a disciplined investment approach focused on delivering specific outcomes, supported by a robust multi-manager framework – a structure that combines the expertise of multiple specialist managers under one coordinated strategy to provide clarity, confidence and stability for clients in an uncertain world.

This approach has not only built our reputation for consistency and innovation, but also for helping our clients navigate uncertainty and reach their goals. Our success is shown not only by strong fund performance since inception, but also by the careful, risk-aware way we achieved it – delivering superior risk-adjusted returns that have earned industry recognition.

As Renzi Thirumalai, CIO at FNB Wealth & Investments, explains: “These achievements reflect the disciplined process behind our investment philosophy. Our focus has always been on delivering consistent, risk-adjusted returns through a robust, outcomes-based approach. This disciplined framework gives clients confidence that their longterm objectives remain on track, even in uncertain markets.”

Furthermore, these wins reflect not only disciplined process but also the collaborative strength of FNB, RMB and Ashburton, combined with our multi-management expertise. This means our clients benefit from top skills and experience in multiple investment disciplines, where each selected team is an expert in their field – yet, combining these is where the total becomes far more than the sum of the parts.

Beyond managing portfolios, our role is to help clients stay invested and focused on long-term goals – particularly when behavioural biases threaten to derail outcomes. Overconfidence, for example, can lead investors to believe they can time markets, herding and recency bias can drive them to chase what’s ‘hot’ now, and loss aversion causes panic selling during downturns. These emotional responses carry real costs.

For example, a R1 000 investment five years ago in the FNB Growth Fund of Funds would now be worth just over

R2 000 (after fees, before tax). However, if you exited during the Covid-19 crash and stayed in cash, even with recent high interest rates, your investment would only have grown to slightly above R1 300. This illustrates why staying invested matters, once you have selected the appropriate fund for your investment needs.

Our task is to build solutions that can help clients overcome such behavioural biases to become better investors. This is why our investment process is built on three interconnected principles designed to mitigate these risks.

The first step is strategic asset allocation – the long-term foundation that helps us stay on track to meet return objectives. This provides stability, but because markets change, we also use tactical asset allocation. This lets us adjust positions when we see opportunities, adding flexibility without losing sight of our long-term goals.

However, these decisions are only as effective as the managers we choose to execute them. Effective manager selection represents perhaps the most critical component of our process, requiring a disciplined framework that screens, analyses and blends managers across different styles, market caps and asset classes.

Our multi-management approach offers key benefits: true diversification across investment styles, portfolios built to withstand different market conditions, flexibility to adapt when markets change, and strong governance

“Our role is to help clients stay invested and focused on long-term goals”

through our investment committee and oversight process.

For our award-winning FNB Horizon funds, we also draw on the collective investment capabilities of FNB, RMB and Ashburton, allowing our FNB Multi Management team access to world-class, institutional-grade resources and expertise. Our investment committee brings together deep experience across asset allocation, quantitative research and portfolio management, with team members whose combined experience spans multiple market cycles. Having navigated previous periods of market stress, from financial crises to bear markets, this experience is particularly valuable when disciplined adherence to process becomes most critical. It’s precisely during these challenging periods that the benefit of a structured, repeatable process becomes evident – when emotion might otherwise drive individual decisions, our framework keeps portfolios aligned with longterm objectives.

Of course, the proof of any strategy ultimately lies in its successful execution, and FNB Multi Management has this proof. The FNB Multi Manager Equity Fund has delivered strong performance relative to peers in the ASISA South African Equity General category, while the FNB Multi Manager Balanced Fund has delivered competitive returns in the ASISA SA Multi Asset High Equity space.

Our Horizon series of funds has met or exceeded return objectives across different risk profiles and over their intended minimum investment horizons. These outcomes don’t come from market timing or concentrated bets; they’re the result of an ability to stick to the same proven, disciplined process.

For financial advisers and intermediaries, this provides practical value. We do the heavy investment lifting, allowing advisers to focus on client relationships and financial planning. In a world of noise, uncertainty and complexity, this provides the clarity, confidence and stability that their clients need.

There is no doubt that market environments will continue to change in the years to come, presenting both opportunities and challenges. But what will remain constant is the need for disciplined investment management, grounded in sound process, and delivered consistently irrespective of market conditions.

That remains our strength and our unwavering focus.

By Kobus Kleyn Liberty Financial Adviser and Certified Financial Planner

AAn RA is the very foundation of advice

s a foundation for all good financial planning for every new client, whatever their age or ambitions, they should be guided to a Retirement Annuity (RA). I like to think of the RA as a plan A in every case. Put a retirement plan in place first, and it contributes to a client’s value and remains as a failsafe should other things not work out as desired in their life. There have been many discussions around seeking alternatives to RAs, because of a belief that these savings vehicles are old-fashioned or that they take time to grow, or perhaps because people apparently can’t access their money during the savings period.

Many advisers have likely encountered clients who have toyed with the idea that their house or business, or even their investments, will be their retirement plan. This is, of course, not something any ordinary adviser would recommend.

As advisers understand too well, many people in this position find that a house can be expensive to maintain, along with monthly mortgage payments, and may not accumulate in value as hoped. And a business may not be profitable or long lasting enough to provide for a future retirement. And, of course, ordinary investments are taxed at substantial rates.

The tax savings are significant

Here are some key points to remind clients about the key benefits of an RA, which makes it a unique tool and must-have lifestyle product for a successful financial future.

• Immediate tax relief: Contributions up to 27.5% of income, capped at R350 000 a year, are fully tax deductible

• RA growth is tax-sheltered: No Capital Gains Tax or Dividends Withholding Tax applies, so growth remains untouched

• Retirement tax benefit: First R550 000 lump sum at retirement is tax-free – a major planning tool.

An RA provides lifestyle security

Moving beyond the tax advantages, an RA offers a series of lifestyle enhancements that focuses on the discipline and advantages of saving. As an adviser, convincing clients to save whenever possible is another important foundation of good advice.

• Estate and creditor protection: RA assets fall outside the estate and are protected under the Pension Funds Act

• Access via two-pot system: These reforms allow limited withdrawals, while maintaining the key savings component

• Controlled income: Here clients have a wide choice of living annuity or life annuity options that allow for tailored incomes in retirement

• Compound interest effect: Starting earlier multiplies growth, thanks to time in the market.

What to do about it

The RA sits as a cornerstone of product selection for a financial needs analysis. It provides tax savings, lifestyle support, and security for when clients retire. Its advantages begin well before retirement and become even more evident once this life stage is reached.

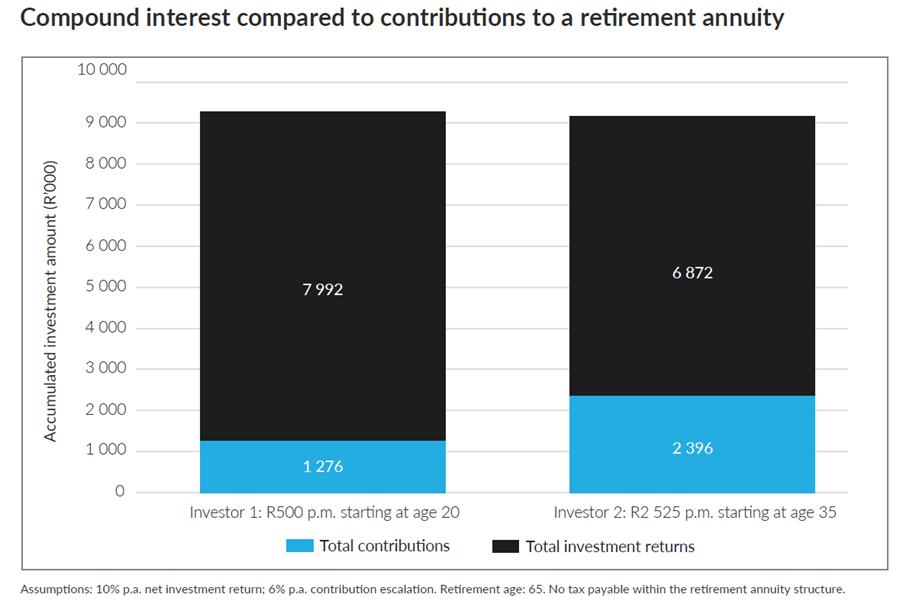

Advisers should emphasise that at any age, an RA is a proven retirement savings vehicle that has the support of government legislation, and offers generous tax advantages and a savings component. This is not to mention the extraordinary power of compound interest over time – the more you give, the more you get.

Some like to argue that the traditional RA has had its day. It is, however, continually evolving, along with the products that enable it. And here the skill of the adviser in deciding what is best for every client comes into play.

RAs remain the most efficient retirement savings vehicles out there, and the test of time continues to prove this after all other options have been exhausted.

By Cassidy Nydahl Head of Growth, Franc App

RHow goal-based investing can help clients reach future financial goals

esearch shows that most investors don’t fail because they choose the wrong fund, they fail because they lose sight of their goals. Defining a clear purpose for your money is what keeps you on track when life throws curveballs. This is the idea behind goal-based investing. You define the outcome first, then determine your contributions and the risk to fit the time you have. In practice, that means mapping short, medium, and long-term horizons, setting a target rand amount for each, and giving every goal a name and an image so it feels concrete enough to stick with when your motivation dips.

“The real shift happens when you understand how much risk you can take”

This approach helps people move beyond the indecision that often comes with too many choices. Once a goal has a time frame and a number, the asset mix follows naturally. A holiday next year needs capital preservation and daily liquidity, so a money market allocation makes sense. A home deposit in five years can take on some equity exposure to grow more over time. The result is fewer second-guessing moments and

less temptation to chase whatever is trending on social media. The plan fits the goal, not the other way around.

Even though a clear goal gives you something to aim at, the real shift happens when you understand how much risk you can take and how long you have to reach it. That alignment builds confidence. It also removes the fear of ‘getting it wrong’, which is one of the biggest psychological barriers to investing.

However, there are three obstacles that stop people from following through: decision fatigue, willpower and isolation. Fortunately, there are practical fixes.

• Automate contributions. If a debit order deducts R100 on payday, the decision has already been made. Automation protects the plan from month-to-month trade-offs. Build accountability. Savings challenges create light social pressure that helps people show up. Shared Goals – available with Franc – do the same. Up to 10 people can contribute to a single goal with complete visibility into deposits, turning good intentions into habits.

• Lower the threshold to start. Start with small amounts and increase later. For this purpose, Franc has no minimums to start investing with on the platform.

Creating financial goals that last

Compiled by Sandy Welch Editor, MoneyMarketing

For advisers, January offers an opportunity to assist your clients to create financial plans they can commit to over the long term. It’s not about New Year resolutions, it’s about setting the groundwork for solid, thoughtful targets that are achievable. With that in mind, MoneyMarketing explored the five most effective ways advisers can guide their clients toward a financially successful 2026.

1

Start with a life-first approach, not a numbers-first one

Great financial goals aren’t built from balance sheets, they’re built from clients’ lived

realities. Advisers should begin by uncovering what clients want their money to do for them: their aspirations, obligations, anxieties and life transitions. Framing finances around life events such as education, home ownership, business ambitions, retirement and lifestyle creates goals that feel meaningful and therefore stick.

2

Translate dreams into measurable, time-bound targets

Clients often describe vague ambitions (“I want to retire comfortably”, “I want to travel more”). Advisers add value by turning these into clear, quantified, time-bound goals. Whether it’s “retire at 65 with

Once the barriers have been overcome, think of a wealth plan like a champagne glass tower. The top glass must fill first, i.e. emergency savings. This is the buffer that keeps a bad month from derailing everything else. Once that is healthy, the champagne flows over to the other glasses (goals), depending on their priority.

Some months, it is a trickle. Other months it is more. The point is sequence and flow. The mix for each goal is set to the timeline. Short horizons stay in cash-like instruments. Longer horizons earn their keep with diversified equity. This picture helps people decide what to fund now, what to pause, and what deserves more risk because there is time to recover.

We are currently working on developing a digital wealth coach (an evolution of the current Franc robo-advice) to help users define a plan across products, choose suitable strategies for each goal, and build the habits to stay on track.

The idea is to have a conversational guide that can adjust recommendations as life changes and keep the focus on the goals. Remind your clients to start with the goal, match the risk to the time, and automate the habit. The rest will follow.

Franc App is a goal-based platform for saving and investing that offers personalised strategies and wealth habit coaching.

R40 000 per month in today’s rand value” or “save R250 000 for a deposit in three years,” measurable targets allow for transparent planning, progress tracking and realistic prioritisation.

3 Build goal hierarchies to manage trade-offs

Not all goals can be funded equally. Advisers should help clients categorise goals into essential, important, and aspirational. This creates a natural decision-making framework when budgets are tight or circumstances change. By ranking goals, advisers can guide clients through tradeoffs without emotional friction and ensure scarce resources are allocated with purpose.

4

Stress-test the plan against real-world risks

A goal is only as good as its resilience. Advisers should model

scenarios that include inflation shocks, market volatility, job loss, longevity risk and healthcare costs. This not only protects clients from unforeseen events but also builds confidence in the plan. Clients who see their goals survive stress tests are more likely to stay invested and avoid panic-driven decisions.

5 Create a dynamic review process that celebrates milestones

Goal setting is not a once-off conversation. Advisers should implement a structured review cycle, annual or semi-annual, where clients’ progress is checked, assumptions updated, and life changes incorporated. Equally important is celebrating milestones: paying off debt, reaching an emergency fund target or hitting a savings landmark. Recognition builds motivation and strengthens adviser–client engagement.

How to get your clients to buy into TFSAs

MoneyMarketing asked Ryan Basdeo, Head: Index Portfolio Management at 1nvest, to unpack the Tax-Free Savings Account, one of the simplest yet most powerful tools available to South African savers. Despite being around for nearly a decade, TFSAs remain widely misunderstood and often underutilised.

What is a TFSA and why should the average saver consider opening one?

A Tax-Free Savings Account (TFSA) is an investment vehicle introduced by the government to encourage saving. The big advantage? All returns, including interest, dividends and capital gains, are completely tax-free. This means your money compounds at a much faster rate. TFSAs are ideal for anyone wanting to grow wealth efficiently for goals such as retirement or education.

How should clients go about deciding which one to choose? Is it worthwhile having more than one?

When choosing a TFSA, clients should be aware of fees and platform costs. High fees erode returns (compounding negatively). It's best to aim for fees below 0.5% where possible. Some providers offer ETFs (low-cost, passive), others unit trusts or fixed deposits. There should be specific TFSA-enabled instruments which are more diversified investments and give exposure to broader themes than concentrated exposures. You can have multiple TFSAs across providers, but the annual (R36 000) and lifetime (R500 000) limits apply across all accounts combined. So, splitting accounts doesn’t increase your allowance. There is a hefty penalty of 40% of the value contributed above the allowed limit. Clients must be very careful not to exceed the limit.

Does 1nvest have any TFSA compliant funds?

Yes, we do - most of our funds are TFSA compliant for example, 1nvest S&P500 Index Feeder or 1nvest MSCI World Index Feeder, however, please refer to the 1nvest website for more information.

One of the biggest advantages of a TFSA is the tax benefit. Can you explain exactly what investors are not taxed on, and how this impacts long-term growth?

Clients pay zero tax on interest income, dividends and capital gains. This means every rand earned stays invested, compounding over time. Let’s assume that you invest the maximum R3 000 per month into a tax-free savings account (TFSA) over 25 years. You achieve an average annual return of 6% after inflation compounded monthly. After roughly 14 years, you will have invested the maximum R500 000. Your investment will continue to grow untouched for the remaining years, even though contributions have stopped. At a 6% average annual return, compounded monthly, your final balance after 25 years would equate to just over R1.5m. You can withdraw the full amount, entirely tax free.

Why should a young person choose to put extra money into a TFSA as opposed to topping up a retirement annuity?

Contribution limits are often seen as a drawback of TFSAs. How should investors approach these limits, and do smaller regular contributions still make a meaningful difference?

Even small monthly contributions (such as R500) matter because of compounded growth. Starting early is key. Think of it this way: If you plant a tree today, it has decades to grow tall and strong, providing shade and fruit. If you wait 20 years, you’ll still get a tree, but it will never be as big or as fruitful as the one planted earlier. Time is the sunlight and water for your money. The longer it has, the more it compounds and grows. Warren Buffett famously said it: “The best time to plant a tree was 20 years ago. The second best time is now.”

Some people think TFSAs should only be used for short-term goals. Is that accurate, or can they play a powerful role in long-term wealth creation as well?

No, it’s seriously flawed to think so. While withdrawals are allowed anytime, the real power is in long-term compounding. Using a TFSA for short-term savings wastes its tax advantage. Remember, withdrawals also eat up your R500 000 limit.

What are some common mistakes you see people making with TFSAs, and how can investors avoid them?

Ryan Basdeo, Head: Index Portfolio Management at 1nvest

The pros of a TFSA include full flexibility. Investors can withdraw at any time while enjoying tax-free growth and no restrictions on asset allocation. The pros of an RA is that they are tax-deductible (up to 27.5% of income), but funds are locked until age 55. For young investors, a TFSA offers liquidity and global investment options without Regulation 28 limits. Ideally, do both: max RA for tax deductions, then use TFSA for extra savings.

“While withdrawals are allowed anytime, the real power is long-term compounding”

Over-contributing: Exceeding limits triggers a 40% penalty

• Using TFSA as an emergency fund: Withdrawals reduce lifetime allowance permanently

• Waiting until year-end to invest: Delays compounding; start early or set up debit orders

• Choosing low-growth products (e.g. fixed deposits): Misses out on equity growth potential.

For South Africans feeling financially stretched, why is it still worth prioritising a TFSA, even with a small monthly debit order, and is January a good time to start?

January is ideal: you capture growth for the full tax year and avoid the last-minute rush. Consistency beats lump sums at year-end. Even if you start small, compounding is your friend and works best over time.

Seniors lead the charge in Tax-Free Savings growth

FNB is seeing a surge in tax-free savings account uptake, with senior customers leading the way. Usage among seniors has jumped by 35.91%, compared to 6.57% growth among youth, highlighting a growing awareness of the power of tax-free investing for long-term financial security. At the start of the financial year, 4% of FNB customers had already fully funded their tax-free savings accounts, positioning themselves to maximise returns through early contributions and compound growth. “Clients who make lump-sum payments early in the year benefit most from compound interest, accelerating their wealth creation,” says Himal Parbhoo, CEO of Retail Cash Investments at FNB. Since launch, tax-free savings accounts have become a cornerstone of wealth creation for FNB clients. Parbhoo adds, “The appeal lies in their simplicity and effectiveness. All returns, including interest, dividends, and capital gains, are completely tax-free. In contrast, traditional savings and investment accounts are subject to tax on returns, which can significantly slow down growth over time.

“Tax-free savings accounts have become a cornerstone of wealth creation”

“With tax-free savings, every rand earned stays invested and continues to grow. It’s one of the most efficient ways to build wealth over the long term,” says Parbhoo.