NEW JERSEY

REALTOR

®

Winter 2026: VOLUME 12 ISSUE 1

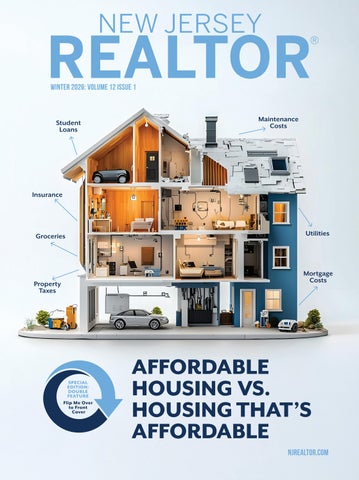

Student Loans

Maintenance Costs

Insurance

Groceries

Utilities

Mortgage Costs

Property Taxes

SPECIAL EDITION: DOUBLE FEATURE Flip Me Over to Front Cover

AFFORDABLE HOUSING VS. HOUSING THAT’S AFFORDABLE NJREALTOR.COM