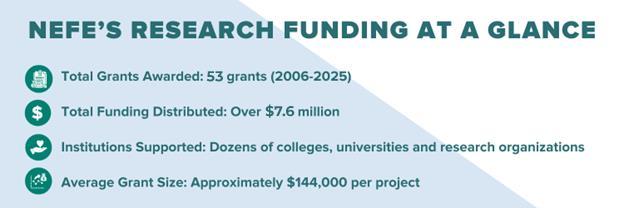

For over two decades, the National Endowment for Financial Education (NEFE) has been a catalyst for advancing effective financial education through its research funding. Since 2006, NEFE has awarded 53 research grants totaling over $7.6 million in funding. This substantial investment underscores NEFE’s commitment to improving the public’s financial well-being by supporting evidence-based insights and innovations in the field of personal finance as it relates to our Personal Finance Ecosystem. Each project funded by NEFE is presented as rigorous, innovative and actionable, adding to the collective understanding of what works in financial education and empowering policymakers, educators and practitioners with data-driven strategies. In addition, each study was funded based on relevance and ability to impact the field at the time of funding. Not all research will align with NEFE’s current rigor and standards. As the field continues to evolve, NEFE strives to answer crucial questions and contribute to the field’s understanding of effective education practices.

Key Research Themes Supported

NEFE-funded projects span a wide range of research areas and themes, which have been most recently aligned with the organization’s strategic funding priorities. Although the funded studies are diverse in focus, most can be grouped into a few broad themes that have helped to define our current research agenda:

▪ Financial Capability and Financial Education Effectiveness: Many grants examine how to improve financial capability across various populations. This includes evaluating the impact and outcomes of financial education programs (for example, high school personal finance courses) and developing better

measures of financial knowledge and skills. By re-evaluating financial literacy metrics and educational practices, NEFE-backed research helps identify what truly works in teaching personal finance. These projects inform best practices for educators and policymakers, ensuring that financial education efforts are evidence-based and effective.

▪ Behavioral Finance and Financial Decision Making: A core theme in NEFE’s portfolio is understanding the behaviors and decisions behind personal finance. Projects in this area probe into how people make financial choices, what influences those choices (such as biases or cognitive factors) and how interventions can lead to better outcomes. By providing insight into financial behavior, NEFE-supported studies on financial decision making shed light on topics like savings habits, debt management and investment behaviors. This research helps uncover strategies to help nudge positive financial behaviors and improve overall financial well-being.

▪ Underserved Populations and Equity: NEFE emphasizes that financial education must work for everyone, and many funded projects focus on underserved or historically disadvantaged groups. NEFE-funded initiatives have explored issues such as racial and gender wealth gaps, the financial challenges of low-income communities, and the unique needs of first-generation college students and other underserved populations. For example, NEFE-funded studies examine viable solutions to address crucial gaps in high school financial education, and how financial knowledge impacts college students facing barriers and challenges. By studying systemic inequality and tailoring research to assist diverse groups, NEFE’s funding elevates knowledge of how to make financial education more inclusive and effective for all.

▪ Youth Financial Education: A significant portion of NEFE’s research funding is dedicated to youth, recognizing the long-term impact of early financial education. Projects in this theme investigate K-12 financial education requirements, youth savings behaviors and the role of family or school/peer socialization in shaping young people’s financial skills. NEFE’s focus on youth financial education reflects the belief that building good financial habits early can have profound effects on a lifetime of financial outcomes. Supporting research on youth ensures that the next generation is better prepared and financially secure.

Broad Impacts of NEFE-Funded Research

The collective impact of NEFE’s research funding is evident in the growth of knowledge and tangible changes it has fostered in the financial education field. NEFE-funded studies have expanded the body of knowledge on financial capability, producing insights that are widely cited and serving as resources for other scholars and practitioners. As of 2025, NEFE’s research portfolio has been referenced in over 1,700 peer-reviewed publications, underscoring the organization’s influence in academia and beyond. This growing evidence base helps drive informed decision making among policymakers, who turn to NEFE’s research when considering financial education legislation, and educators use the findings to refine curricula and teaching methods. Importantly, NEFE’s grants have spurred innovation and critical dialogue by funding research that investigates emerging issues and challenging questions.

Each project is selected for its academic rigor and its potential to make a profound contribution to the field of financial education, thereby improving public financial wellbeing. The outcomes of these projects often include practical recommendations for example, identifying more effective ways to deliver financial training or highlighting gaps where certain communities are left behind—which can be acted upon through additional research inquiries and by practitioners.

The overarching impact themes across NEFE’s funded research include:

▪ Building Evidence for What Works: NEFE’s investment ensures that interventions and inquiries across the Personal Finance Ecosystem are backed by sound research. This strengthens the case for financial education by demonstrating measurable benefits when these interventions are evaluated with rigor. Also, it reveals which approaches are less effective and guides the field toward more promising strategies.

▪ Informing Policy and Practice: Findings from NEFE-funded studies have informed state education requirements, program design and national discussions on financial education. For instance, evidence from NEFE research on K-12 education outcomes is informing how states implement personal finance requirements, ensuring those policies truly benefit students. By contributing data and analysis, NEFE empowers leaders to craft initiatives that better serve the financial needs of their communities.

▪ Advancing Equity and Inclusion: Through its focus on underserved groups, NEFE’s research funding has elevated the understanding of financial challenges faced by minorities, women and other marginalized populations, both at the individual and systems levels. This has helped shift the field toward more inclusive practices acknowledging that financial education isn’t working unless it is working for everyone. As a result, new programs and curricula are increasingly designed with cultural relevance and accessibility in mind, and stakeholders are more aware of closing pervasive gaps (such as disparities in financial outcomes) as a measure of success.

▪ Cultivating a Culture of Rigor: NEFE has fostered higher standards in financial education research. Emphasizing robust methodology and measurement, NEFEfunded projects encourage the use of validated metrics and long-term evaluation of outcomes, when feasible. This commitment to rigor improves the credibility of our field. Researchers supported by NEFE often collaborate across disciplines (economics, psychology, education, social work, family and consumer sciences, etc.) and bring cutting-edge approaches to their studies, setting new benchmarks for quality. The emphasis on continuous improvement of research design and data (including examining biases in data collection) helps ensure that future financial education efforts rest on a solid, scientific foundation.

NEFE’s research funding has had a transformational effect on the landscape of financial education, contributing to our understanding of complex topics such as financial capability, effective teaching of financial knowledge and its practical applications, as well as how to better support financial well-being across the nation. The grants highlighted in this catalog stand as testament to NEFE’s vision: A nation where everyone has the knowledge, confidence and opportunity to live their best financial life

This introduction celebrates the scale of that vision and the inspiring impact it continues to have on researchers, educators, policymakers, advocates and the individuals who ultimately benefit from a stronger foundation in personal finance and advancing greater levels of financial well-being

Financial Management Practices of College Students from States with Varying Financial Education Mandates

Institution University of Wisconsin—Madison

Principal Investigator Michael Gutter, Ph.D.

Research Team Wendy L. Way, Ph.D., Allen Phelps, Ph.D.

Grant Details Amount

Short Summary

Methodology

Approximate Duration

$112,552 July 2006-December 2009

This study used three categories of financial outcome indicators (financial knowledge, financial dispositions and financial behaviors) to assess the effectiveness of state policies regarding high school financial education.

Analysis of prior college student studies, analysis of financial literacy standards in all 50 states and Washington, D.C., and online surveys of more than 15,000 land grant college students across the U.S.

Key Findings Overall, this study shows that financial behaviors of college students vary by state policy on financial education, even when controlling demographics, financial resources, financial education and financial knowledge. Social learning is an important determinant of dispositions. As such, it is possible that the behavioral impact of financial education would wane if not reinforced through social learning.

In addition, college students engage in various financial transactions out of necessity. Thus, regardless of having had a class, many students will need checking accounts and will opt to learn to use them through self-education, social learning opportunities or simply from trial and error (experience).

Publications Copur, Z., & Gutter, M.S. (2010). Social learning opportunities and the financial behaviors of college students. Family and Consumer Sciences Research Journal, 38(4), 387–404. Link to article: https://www.academia.edu/27944194/ Social_Learning_Opportunities_and_the_Financial_Behaviors_of_College_Students

303-741-6333

La Tercera Edad: Latinos’ Financial Literacy, Pensions & Impact on Families

Institution University of Notre Dame du Lac

Principal Investigator Gilberto Càrdenas, Ph.D.

Research Team Karen Richman, Ph.D., Teresa Ghilarducci, Ph.D.

Grant Details Amount

Short Summary

Methodology

Key Findings

Approximate Duration

$100,000 August 2006-August 2008

This project, under NEFE's now-retired Innovative Thinking Program, examined the retirement behavior of Latinos as a continuum, by focusing on current Latino workers, the Latino elderly and their families, and how their behavior differs from that of other various demographics. Three issues were explored: Latino workers' retirement readiness and how their financial literacy affects planning for retirement, retirement savings and wealth accumulation; why Latinos are not covered by pensions and why they are less likely to participate in 401(k) types of plans; and how Latino elderly support their retirement life, including the types of support adult children provide to retired parents and the impacts on families that provide such financial support.

Comparative analysis of data from the 1996 and 2000 Survey of Income Program Participants (SIPP), analysis of core and supplemental data from the 2004 Health and Retirement Survey (HRS), focus groups with Latino retirees and working adults.

Based on the sample, Latinos are less likely to be eligible for pension participation due to their disadvantaged position in the labor market. Since Latinos were more likely to be lowwage workers, they are likely to be more concerned about maximizing their cash income and less willing to spend on pension security. A large percentage of Latino participants were immigrants or of Mexican origin (67% of Latinos are of Mexican origin and 40% of Latinos are foreign born) and have several reasons to be estranged from the U.S. financial system. This study found that in 1996, about 12% of Latinos indicated that they had not thought about pension plans and the EBRI survey (2000) found that only 20% of Latinos know how much they will need to save for retirement.

Publications Richman, K. E., Barboza, G., Ghilarducci, T., & Sun, W. (2008). La Tercera Edad: Latinos' pensions, retirement and impact on families. University of Notre Dame, Institute for Latino Studies. Link to article: https://curate.nd.edu/articles/report/La_Tercera_Edad_ Latinos_Pensions_Retirement_and_Impact_on_Families/24831021?file=43680012

303-741-6333

Teacher's Background and Capacity to Teach Personal Finance: Results of a National Study

Institution University of Wisconsin

Principal Investigator Wendy L. Way, Ph.D.

Research Team Karen Holden,

Ph.D.

Grant Details Amount

$104,807

Approximate Duration

October 2006-December 2009

Short Summary In Spring 2006, NEFE convened education and family economics deans and chairs from six universities to discuss the capability of new teachers to manage their own finances and their preparedness to teach financial literacy. The group determined that a study was needed to survey faculty, K-12 teachers and student teachers. NEFE developed an RFP and vetted it with the six universities, which agreed to cooperate in the study with the University of Wisconsin taking the lead. Dr. Way collaborated with universities to conduct a national survey of education faculty, K-12 teachers and student teachers to learn what it will take to teach new teachers (TNT) to provide effective financial education in the classroom. This is the first national study of teacher preparedness and interest in K-12 classroom financial education.

Methodology

Key Findings

Two phases:

1. Comprehensive literature review to determine what is known about a) financial issues experienced by pre-service and in-service K-12 teachers, and b) teachers’ capacity for teaching financial education

2. National surveys of more than 100 teaching faculty in eight universities, 678 preservice teacher education students and nearly 500 K-12 teachers

There is evidence that teacher pay is not commensurate with that of other professionals with similar levels of education. Given this disparity, it seems somewhat inadequate to recommend simply that teachers be given an opportunity to learn how to supplement their income as a teacher or learn how to manage their finances more wisely so they will have sufficient income to meet their needs (two of teachers’ top personal finance concerns). Instead, what it points to is a need for additional dialogue about the forms, adequacy and equity of compensation for those who perform what is arguably one of the most critical tasks for our nation’s future the education of our children.

Publications Way, W. L., & Holden, K. (2009). Teachers' background and capacity to teach personal finance: Results of a national study. Journal of Financial Counseling and Planning, 20(2), 64–78. Link to article: https://www.researchgate.net/publication/281549521

303-741-6333

Arizona Pathways to Life Success for University Students (APLUS):

Cultivating Positive Financial Attitudes and Behaviors (APLUS – Wave 1)

Institution University of Arizona

Principal Investigator Soyeon Shim, Ph.D.

Research Team Joyce Serido, Ph.D., Jing Jian Xiao, Ph.D., Bonnie Barber, Ph.D., Noel Card, Ph.D.

Grant Details

Amount

$207,078

Approximate Duration

January 2007-December 2008

Short Summary Shim and her research team at the University of Arizona embarked upon a landmark project (APLUS) to better understand the financial behaviors of college-aged students. Wave 1, “The Formation of Positive Financial Behaviors Among Young Adults and the Effects on Their Life Successes,” surveyed more than 2,000 freshman students about how they spend their time and money, their financial literacy and practices, and their debt management and well-being. Subsequent waves help researchers better understand, for instance, who has the greatest influence on college students’ financial decision processes as they move through university. Knowing this information helps educators tailor more effective financial education messages and educational opportunities.

Methodology Online and paper-based surveys of more than 2,000 incoming freshman students.

Key Findings

There are three factors that create an effective solution to avoiding financial problems when students start college:

1. Parental involvement (has the most influence)

2. Education (formal financial education in high school)

3. Work experience (part-time job)

73% reported engaging in at least one of the following risky financial behaviors within the preceding six months:

• Not paying bills on time

• Not making full payments on credit cards

• Maxing out credit cards

• Borrowing from credit cards

• Taking out payday loans

On average, students surveyed received a failing grade (59%) when tested on financial literacy.

Publications Shim, S., reSerido, J., & Xiao, J. J. (2009). Cultivating positive financial attitudes and behaviors for healthy adulthood: Wave 1 report. Arizona Pathways to Life Success for University Students (APLUS). Link to article: https://aplus.arizona.edu/sites/aplus.arizona.edu/files/2022-06/wave1_report.pdf

303-741-6333

Economic Impact Study: Financial Well-Being, Coping Behaviors and Trust Among Young Adults (APLUS – Wave 1.5)

Institution University of Arizona

Principal Investigator Soyeon Shim, Ph.D.

Research Team Jing Jian Xiao, Ph.D., Bonnie Barber, Ph.D.

Grant Details Amount

$48,911

Short Summary

Methodology

Key Findings

Approximate Duration

September 2009-February 2010

Building on the student survey conducted in Wave 1 of the APLUS longitudinal study, Wave 1.5 was designed to study the immediate impacts of the 2008 economic crisis. The researchers identified and profiled those most likely to suffer financial difficulties as a result of the economic recession. Additionally, a literature review was conducted alongside data analysis of results from the just-in-time survey. The researchers also examined the nature and dynamics of trust that these young adults have in financial systems via focus groups.

Survey of 500 college students, focus groups

• More women, African Americans, students with lower academic achievement and those from lower- and middle-socioeconomic status (SES) families reported a greater immediate impact of the recession.

• Financial self-confidence (subjective knowledge), especially of women and minority students, declined substantially. The impact was more evident in financial areas for women, while men were more affected academically.

• Financial strain (the combination of declining financial self-confidence and increasing debt) was most evident among minority students, particularly African American and Hispanic students.

• An expected increase in the use of cost-cutting strategies was overshadowed by a dramatic increase in extreme financial coping strategies (dropped classes, leaves of absence and postponed health care), with the potential for future financial hardship.

Publications Shim, S., Serido, J., Card, N., Barber, B., Xiao, J. J., Staten, M., Lanza, R., Tang, C., Ahn, S.-Y., & Mittal, C. (2010). Wave 1.5 economic impact study: Financial well-being, coping behaviors, and trust among young adults. Arizona Pathways to Life Success for University Students (APLUS). Link to article: https://aplus.arizona.edu/sites/aplus.arizona.edu/files/2022-06/wave1_5_report.pdf

303-741-6333

Young Adult's Financial Capability (APLUS – Wave 2)

Institution University of Arizona

Principal Investigator Soyeon Shim, Ph.D., Joyce Serido, Ph.D.

Research Team Jing Jian Xiao, Ph.D., Bonnie Barber, Ph.D., Mike Staten, Ph.D., Noel Card, Ph.D.

Grant Details

Short Summary

Amount

Approximate Duration

$150,000 March 2010-February 2012

The purpose of the project was to assess the cohorts’ Senior years of college: 1) changes in personal values, personal finance knowledge and behaviors; 2) the development of financial identity; 3) the impact of academic and work experiences and financial education on financial development; and 4) the role and impact of changing relationships with others on financial decision making.

Methodology Resurveyed

Key Findings

Financial Socialization:

Parents play a key socializing role during college years, helping their young adult children to become financially capable adults. Parents’ influence is 1.5 times greater than that of financial education and more than twice that of friends.

Cumulative Education:

When it comes to financial education, ongoing education is critical to better outcomes. Participants with cumulative education know more and report more positive behaviors. Also, a snowball effect was documented, with earlier financial education exponentially increasing the likelihood of later financial education, including informal learning through books, magazines and seminars.

Followers, Drifters & Pathfinders:

APLUS participants cluster into three groups by financial management style:

o Followers: Those who mostly just accept what their parents say is best.

o Pathfinders: Those actively building a self-chosen style of financial management.

o Drifters: Those who don’t follow their parents’ style but have no individual approach.

Pathfinders have significantly greater financial capability, knowing more about personal finance, having more positive financial attitudes and making better financial decisions.

Publications Shim, S., & Serido, J. (2011). Young adults’ financial capability: Wave 2 report. Arizona Pathways to Life Success for University Students (APLUS). Link to article: https://aplus.arizona.edu/sites/aplus.arizona.edu/files/2022-06/Wave-2-Report.pdf

303-741-6333

Life After College: Drivers for Young Adult Success (APLUS –Wave 3)

Institution University of Arizona

Principal Investigator Joyce Serido, Ph.D.

Research Team Soyeon Shim, Ph.D., Bonnie Barber, Ph.D., Mike Staten, Ph.D., Noel Card, Ph.D.

Grant Details Amount

$75,000

Short Summary

Methodology

Key Findings

Approximate Duration

June 2012-June 2014

For the first time, most of the APLUS participants had shifted their focus from school to career, and many will have also formed romantic relationships and might have begun cohabitating. Many also achieved financial independence from their parents. Therefore, Wave 3 focused on the effects of a cumulative financial education on financial capabilities and the changing roles of socialization agents such as parents and romantic partners. As young adults enter the workforce, the researchers were also able to study the ways in which new agents, such as employers, influence a young adult’s financial behaviors and determine why some young adults achieve higher financial capabilities than others.

Resurvey 75%-80% of the original cohort.

More than half the participants overall (50.6%) reported relying on financial support from family to meet current financial demands, including nearly half (48.9%) of those employed full-time. This finding raises concerns for both young adults trying to become self-sufficient and for their parents as they prepare for retirement.

For participants with debt, financial well-being was 17% lower, 19% lower and 31% lower for those employed full-time, employed part-time and unemployed, respectively. Debt was associated with 4%, 8% and 10% lower life satisfaction for those same groups. These findings suggest that more than a financial burden, debt undermines well-being. Furthermore, carrying debt seems to erode the benefits of even full-time employment.

Our findings showed that patterns of financial behaviors practiced during the college years were drivers for three distinct pathways to young adulthood:

• High-functioning participants (12%) maintained consistently high levels of responsible financial behavior across all three waves.

• Rebounding participants (61%) started college with moderately responsible financial behaviors that had declined by year four but rebounded by Wave 3 two years later.

• Struggling participants (26%) started college with poor financial behaviors, which had further declined by year four. Although their behaviors had improved two years later, they were still worse than during their first year of college and significantly lower than those of all other participants.

Publications Serido, J., & Shim, S. (2014). Life after college: Drivers for young adult success (Wave 3 report). Arizona Pathways to Life Success for University Students (APLUS).

Link to article: https://aplus.arizona.edu/sites/aplus.arizona.edu/files/2022-06/wave-3report.pdf

303-741-6333

Adult Fiscal Competency: An Analysis of Financial Behavior During the Transition to Adulthood (APLUS – Wave 4)

Institution University of Minnesota

Principal Investigator Joyce Serido, Ph.D.

Research Team Soyeon Shim, Ph.D

Grant Details Amount

$75,000

Short Summary

Methodology

Key Findings

Approximate Duration

February 2016-May 2017

Beginning in 2008, the APLUS project surveyed and followed a unique group of young adults, members of the millennial generation who were then freshmen in college. In this report, the researchers provide a glimpse into the progress of the participants, looking at several domains of adult achievement: employment, financial capability, life goals and well-being. Perhaps the most striking finding is that, despite challenging economic and social conditions, most of the young adults in the study are doing well

Resurvey 75%-80% of original cohort

In terms of financial capability and differences in knowledge, agency and behavior, men scored higher than women in both what they knew and their confidence in what they knew and reported better financial behaviors in some areas.

Participants from lower-socioeconomic status (SES) families felt less control over their finances, less confident about their finances and reported less healthy financial coping behaviors despite having been on par with their peers in past data. Well-being was significantly correlated with financial capability, particularly financial self-confidence. Employment status is also strongly correlated with well-being. Fewer young adults were receiving financial support from parents and family at Wave 4. Those who were, including those from higher-SES backgrounds, reported lower well-being compared to their peers. Finances were a bigger threat to goals for more vulnerable populations: non-white participants, those from lower-SES families and those whose parents hadn’t attended college. Ethnic minorities, those from lower-SES families and first-generation participants, were more likely to be carrying student loan debt and were more negatively affected by it. While participants from lower-SES families noted financial strain as a key barrier, participants cited issues related to navigating repayment as more challenging than the lack of finances.

Publications Serido, J., & Shim, S. (2017). Approaching 30: Adult financial capability, stability, and wellbeing (Wave 4 report). Arizona Pathways to Life Success for University Students (APLUS). Link to article: https://aplus.arizona.edu/sites/aplus.arizona.edu/files/202206/APLUS_WAVE4.pdf

303-741-6333

Increasing The Effectiveness of Retirement Saving Programs Among Female and Low-Income Workers: A Marketing Approach

Institution Dartmouth College

Principal Investigator Annamaria Lusardi, Ph.D.

Research Team Punam Keller, Ph.D., Adam Keller, Ph.D.

Grant Details Amount

$174,776

Approximate Duration

January 2007-June 2010

Short Summary Seeking ways to increase the retirement plan enrollment of low-income and female employees, economics professor Annamaria Lusardi, Ph.D., and social marketing expert Punam Keller, Ph.D., focused on new employees at Dartmouth in the fall of 2008 to understand their perceptions about the program. The low-cost marketing campaign included videos and a simple brochure. As a result, these materials were added to the new employee orientation, which aided in significant retirement plan participation over prior years.

Methodology

Key Findings

183 employees in the control group and 166 employees in the treatment group. The treatment group utilized the modified planning aid while the control group did not. Observations, focus groups, in-depth interviews and surveys with young, low-income, lowtenure new employees at Dartmouth were conducted to determine barriers to enrolling in retirement plans.

HR Toolkit – Retirement TLC

A comprehensive toolkit was developed to aid human resource professionals to increase employees’ participation in company-sponsored retirement plans. The step-by-step guide included timelines, instructions and helpful hints, all based on the study’s research. Resources provided include surveys, flyers and videos. The program was presented at the SHRM Annual Conference in June 2011.

Publications Lusardi, A., Keller, P. A., & Keller, A. M. (2009). New ways to make people save: A social marketing approach (NBER Working Paper No. 14715). National Bureau of Economic Research Link to article: https://www.nber.org/papers/w14715

303-741-6333

Helping Consumers Respond Responsibly to the Advertising and Availability of Debt Consolidation Loans

Institution Duke University

Principal Investigator Paul Bloom, Ph.D.

Research Team Lisa Bolton, Joel Cohen, Ph.D.

Grant Details Amount

Short Summary

Methodology

Key Findings

Approximate Duration

$175,549 May 2008-December 2011

The purpose of this project was to determine which consumers, if any, react to the advertising and availability of debt consolidation programs by maintaining or increasing risky financial behaviors that have the potential to increase their indebtedness, and to develop an intervention that would reduce the likelihood of consumers reacting to the advertising.

Samples of 1,801 college students and adult consumers drawn from a commercial panel.

The researchers found that creating loan literacy and lender literacy together, using an attractive video presentation, seems to have promising effects on the knowledge, attitudes and intentions of real consumers in real settings showing the capability of undoing the boomerang effect created by debt consolidation loan advertising.

Publications Bolton, L. E., Bloom, P. N., & Cohen, J. B. (2011). Using loan plus lender literacy information to combat one-sided marketing of debt consolidation loans. Journal of Marketing Research, 48(SPL), S51–S59. Link to Article: https://www.researchgate.net/publication/259888971_Using_Loan_Plus_Lender_ Literacy_Information_to_Combat_OneSided_Marketing_of_Debt_Consolidation_Loans

Financial Literacy Education for Adult Learners in CommunityBased Programs

Institution Penn State University

Principal Investigator Elizabeth Tisdell, Ed.D.

Research Team Edward W. Taylor, Ed.D.

Grant Details Amount

$149,852

Short Summary

Methodology

Key Findings

Approximate Duration

February 2009-July 2010

While many studies have explored adult learning, and many others have looked at financial literacy, little research has focused on where those disciplines overlap. This study helps fill that gap by looking at financial literacy programs for adult learners delivered through community resources rather than formal education settings. The goals of the research included identifying strategies and techniques that educators use today and exploring how they work in financial literacy programs across the country.

A literature search and review of documented, successful financial education strategies was conducted, along with a survey of financial education practitioners.

• 95.5% of adult educators (including all people of color) agreed that teaching should take into account the differences among learners.

• 98% of adult educators indicate that the purpose of financial education is to help students learn, understand basic financial information and make informed choices.

• Many educators also indicated that they need to recognize family legacies of attitudes, emotions and beliefs around money to help them change behaviors.

• More than half of the educators said they use curricula they personally adapted from published sources or developed completely on their own, often to meet the needs of their learners, whose diverse circumstances are not reflected in available materials.

Publications Taylor, E. W., Tisdell, E. J., & Forté, K. S. (2012). Teaching financial literacy: A survey of community-based educators. International Journal of Consumer Studies, 36(5), 531–538. Link to article: https://www.researchgate.net/publication/263251707_Teaching_financial_literacy_ A_survey_of_community-based_educators

303-741-6333

Understanding and Increasing Mexican Immigrants' Financial and Retirement Security

Institution University of Notre Dame Du Lac

Principal Investigator Gilberto Càrdenas, Ph.D.

Research Team Edward W. Taylor, Ed.D.

Grant Details Amount

$124,999

Short Summary

Methodology

Key Findings

Approximate Duration

September 2009-July 2011

This case study examines the social, cultural and economic factors influencing Mexican immigrants’ savings and preparedness for retirement. The research was conducted in Chicago, where people of Mexican origin account(ed) for 17% of the population. The study builds upon previous research undertaken with support from NEFE (Richman, Barboza, Ghilarducci, Sun 2008 and Ghilarducci and Richman 2008). The previous study called attention to the looming crisis in Latinos’ preparation for retirement. In just three years, this critical point has arrived.

Ethnographic data collection (focus groups, interviews), comparative and regression analysis

Latino workers in the United States are far less likely than other groups to be covered by employer-provided pensions or to be contributing to employer-based retirement savings plans. With limited individual assets, Latinos, who (at the time) constitute 15% of the population, remain more vulnerable than other groups to a life of low income and poverty. Even when Latino employees are working for an employer who sponsors a pension plan, they are less likely than white and Black people to be included. Financial literacy is essential to individual workers' investment decision making. Financial illiteracy, however, is widespread throughout the population, but is of particular concern for Latinos

Immigrants’ culture of interdependence, extended families and transnational networks appear to be key aspects of how they define investment and prepare for retirement. Though Mexican immigrants arrive as members of multigenerational, interdependent, transnationally dispersed families, as they integrate into U.S. society these immigrants are pressured to become more independent, abandoning past norms of reciprocity (e.g., women enter the workforce, family mobility leaves more elderly parents without children [support] nearby and families are smaller).

Publications Jelm, E., Saad-Lesser, J., Richman, K., Knight, R., & Ghilarducci, T. (2016). Confianza, savings, and retirement: A study of Mexican immigrants. University of Notre Dame, Institute for Latino Studies. Link to article: https://curate.nd.edu/articles/report/Confianza_Savings_and_Retirement_ A_Study_of_Mexican_Immigrants/24823755/1?file=43663926

303-741-6333

Financial Behavior, Debt, and Early Life Transitions: Insights from the National Longitudinal Survey of Youth, 1997

Institution The Ohio State University

Principal Investigator Randy Hodson, Ph.D.

Research Team Rachel Dwyer, Ph.D.

Grant Details Amount

Short Summary

Methodology

Key Findings

Approximate Duration

$193,047 January 2012-June 2014

Debt is emerging as a typical accompaniment to early life transitions, such as college attendance, leaving the parental home, and establishing an independent household and family. Debt and challenges of financial management are thus becoming deeply embedded in the lived experiences of young Americans as they transition toward adulthood. Randy Hodson and Rachel E. Dwyer, professors at the Ohio State University, gathered a team of researchers, including several doctoral students, to study the effects of debt on these transitions.

The data that informs the study of young adult transitions is “The National Longitudinal Survey of Youth-1997” cohort (NLSY-97). The NLSY-97 asks a wide range of questions on both family background and current situation, including questions asked of respondents as far back as their mid-teens and questions asked directly of their parents at that time.

• Young adults expressed declining acceptance of credit cards after 2004.

• The number of young adults with credit cards dropped to below 60% between 1992 and 2010.

• After the Great Recession (2007–2009), fewer young adults held credit card debt, but those who did had more and held it longer compared to earlier generations.

• Compared to Gen X, millennials took on greater amounts of debt at an earlier age.

• Millennials with greater incomes took on exponentially more debt as they aged compared to their lower-income peers

Publications Dwyer, R. E., & DeMarco, L. M. (2024). Unequally indebted: Debt by education, race, and ethnicity and the accumulation of inequality in emerging adulthood. Emerging Adulthood, 12(5), 878–893. Link to article: https://pmc.ncbi.nlm.nih.gov/articles/PMC11600330/pdf/nihms-2013949.pdf

303-741-6333

A Meta-Analytic and Psychometric Investigation of the Effect of Financial Literacy on Downstream Financial Behaviors

Institution University of Colorado Boulder

Principal Investigator John Lynch, Ph.D.

Research Team Daniel Fernandes, Richard G. Netemeyer

Grant Details Amount

Short Summary

Methodology

Approximate Duration

$159,990 June 2011-May 2013

Policymakers have embraced financial education as a necessary antidote to the increasing complexity of consumers’ financial decisions over the last generation. Academic work has concluded that financial literacy is an antecedent to various healthy financial behaviors. John Lynch, Ph.D., and his team conducted a meta-analysis of the effects of financial literacy and of financial education on financial behavior in 155 papers to test the magnitude of the average effect of an independent variable, whether there is systematic variation in effect-sizes across studies and, if so, what differences among the studies could explain this variation.

Phase 1, Meta-Analysis. The researchers chose which studies to include. Studies of interventions must have at least a month interval between the intervention and testing the effect on financial behavior. If multiple papers make use of the same dataset, they include only the paper with the most complete report of the dataset. Data was coded for the type of measured literacy, manipulated literacy intervention and content of intervention. Phase 2 of the project was a large-scale national survey in which researchers included the following measures: personality traits, such as propensity to plan and numeracy, and financial behaviors such as borrowing, saving and debt.

Key Findings Behaviors and literacy as measured today are weakly linked. Educational interventions and financial literacy, as measured to date, are only weakly linked to behaviors much less so than in comparable domains, such as workplace education or career counseling interventions.

The amount and timing of financial education matters. When it comes to attempts at building financial literacy to shape behavior, education that closely precedes a financial decision has more impact. Diminishing returns means that more education isn’t always better unless timed close to points of decision.

Findings from past investigations merit revisiting. Different classes of studies have yielded such disparate results more varied than good science would predict that we must question to what extent those differences stem from the need for better research designs and analyses.

Publications Dwyer, R. E., & DeMarco, L. M. (2024). Unequally indebted: Debt by education, race, and ethnicity and the accumulation of inequality in emerging adulthood. Emerging Adulthood, 12(5), 878–893. Link to article: https://journals.sagepub.com/doi/10.1177/21676968241241560

The Significance of Gender for Savings and Retirement

Institution University of Notre Dame Du Lac

Principal Investigator Karen Richman,

Ph.D.

Research Team Wei Sun, Justin Sena and Sung David Chun

Grant Details Amount

$129,000

Short Summary

Methodology

Key Findings

Approximate Duration

September 2011-September 2015

Gender ideologies and norms powerfully influence financial investments, savings and commitments. Yet, the financial industry, organizations advocating for vulnerable populations, and many researchers in the field know little about how gender affects Latino men’s and women’s savings in general or savings for retirement. This project has “married” economics and the related field of consumer science with anthropology by integrating the respective disciplines’ methods and quantitative and qualitative approaches. In previous research supported by NEFE, “La Tercera Edad: Latinos’ Pensions, Retirement and Impact on Families” (2008) and “Confianza, Savings and Retirement: A Study of Mexican Immigrants” (2012), the researchers showed how collectivism the affective and material interdependence between the members of families and social networks could hold powerful sway over Mexican immigrants’ ideas about savings. This project informs solutions for increasing men’s and women’s financial security and economic independence.

Qualitative research: Ethnographic research using in-depth methodologies to reach a deepened understanding of how gender affects savings and retirement. Methods include focus groups, interviews and observations, and a review of the existing literature and secondary analysis of other ethnographic studies.

Quantitative research: Analysis of summary and inferential statistics, as well as hypothesis testing of data sets at national, regional and local levels. Statistical analysis controls for variables that women’s and men’s savings, including marital status, family composition, number of children, age, socioeconomic status/profession and immigrant generation.

Regardless of their nativity, Latino men and Latino women have lower educational attainment, are more likely to work in service and construction industries and are less likely to be in management and professional occupations. All of these characteristics negatively affect Latinos’ pension participation.

Job tenure plays a significant role in pension participation. Latino workers’ shorter job tenure contributes to their inability to take full advantage of defined contribution plans. When Latinos leave jobs or retire, they are less likely than whites, Blacks and Asians to preserve their capital by leaving it in the plan or rolling it over into other retirement plans.

Publications Sena, J., Richman, K., Chun, S. D., & Sun, W. (2015). The significance of gender for Latina/o savings and retirement. Institute for Latino Studies, University of Notre Dame.

Cognitive Capabilities, Decision-Making Ability, and Financial Outcomes Across the Lifespan

Institution Columbia University

Principal Investigator Eric Johnson, Ph.D.

Research Team Ye Li, Ph.D.

Grant Details Amount

Short Summary

Methodology

Key Findings

Approximate Duration

$164,996 August 2012-January 2014

This study was the first to combine credit report data with multiple standard measures of fluid intelligence, crystallized intelligence (including financial literacy) and economic preference assessments, such as how much risk people are willing to take and how patient they are in making decisions. The researchers sought to understand how a person’s accumulation of knowledge and experience, particularly in the financial domain, can provide an alternative pathway to making sound financial decisions.

To analyze how cognitive abilities relate to financial decision quality across the lifespan, the researchers used regression models to examine the relationships between fluid cognitive ability (such as reasoning and problem solving) and accumulated knowledge or expertise, and their impact on financial outcomes, primarily credit scores. They tested whether these two types of intelligence predicted credit scores independently and whether accumulated knowledge could buffer the negative effects of declining reasoning ability. The models also controlled for factors like age, education, income, risk tolerance, patience and personality traits.

The brain slows with age, but this NEFE-funded study shows that when it comes to financial decision making, financial literacy can offset the decline associated with normal aging. Three factors were shown to affect credit scores: age, fluid intelligence and financial literacy a domain-specific measurement of financial crystallized intelligence. By far, financial literacy had the greatest impact.

Publications Li, Y., Gao, J., Enkavi, A. Z., Zaval, L., Weber, E. U., & Johnson, E. J. (2015). Sound credit scores and financial decisions despite cognitive aging. Proceedings of the National Academy of Sciences of the United States of America, 112(1), 65–69 Link to article: https://www.researchgate.net/publication/269986753_ Sound_credit_scores_and_financial_decisions_despite_cognitive_aging

303-741-6333

Online Learning and Financial Decision Making

Institution Purdue University

Principal Investigator Geralyn Miller, Ph.D.

Research Team Lawrence A. Kuznar, Ph.D., Maneesh Sharma,

Grant Details Amount

Short Summary

Methodology

Key Findings

Ph.D.,

Rodrigo Ruiz Huidobro

Approximate Duration

$40,000 December 2012-August 2013

The fundamental purpose of this study is to understand the utilization of financial education tools and resources in American families by employing an ethnographic methodology. While ethnographic observation is labor intensive and reduces the number of cases one can investigate, the hope is that in-depth conversations and observations of online financial information seeking will yield deeper insights into consumer needs and behavior than other social science methods (focus groups, surveys, etc.).

An ethnographic approach was used to interview six middle-income families in the U.S. Subjects were visited where they most often conducted their online financial information seeking (typically their homes). Participants were asked questions concerning their financial behavior, their financial information needs, and how they used online sources to meet those information needs. The study emphasized what subjects said about their financial experiences and information seeking, and made minimum assumptions about what would matter, providing a ground-up view of the realities of online financial information use among middle class Americans

General Issues:

• The key background issue that impacted use of online sources was concern over internet security and the credibility of online sources.

Sources and Uses of Financial Information:

• TV and family input

• Professionals consulted, but suspected of ulterior motives

• Online sources used, but trust and credibility remain hurdles, especially for older subjects

• Online sources primarily used for banking, investment research, tax filing and some budgeting

• Some subjects used and were interested in expanding their use of mobile apps

• Younger subjects used online sources primarily to manage mortgages and student loans

• Older subjects used online sources primarily to research investments and gather news about the economy and social issues that they felt impacted their finances

• Expressed needs for online resources

• Mortgage and student loan calculators

• Investment education

Publications Miller, G., Kuznar, L. A., & Sharma, M. Online learning and financial decision making: A pilot study. National Endowment for Financial Education. https://www.nefe.org/_files/research/Online-Learning-and-Financial-Decision-Making.pdf

Financial Capability Among Young Adults

Institution George Washinton University

Principal Investigator Annamaria Lusardi,

Ph.D.

Research Team Carlo de Bassa Scheresberg, Ph.D.

Grant Details Amount

$124,965

Short Summary

Methodology

Key Findings

Approximate Duration

January 2014-June 2015

This study was conducted to better understand the factors that shape young adults’ financial behaviors at a time when individuals are increasingly responsible for their own financial security. Building on concerns raised by previous research such as widespread financial illiteracy, high debt burdens and poor financial decision making among young Americans the researchers aimed to identify key determinants of financial outcomes in early adulthood. The central focus of the study was to explore how financial literacy, along with demographic and contextual factors, influences financial behavior. Of particular interest was how educational quality and socioeconomic background contribute to disparities in financial capability, with implications for both policy and the intergenerational transmission of inequality in the United States.

The study expanded on the 2009 National Financial Capability Study (NFCS) by incorporating new survey questions to more precisely assess the financial experiences of young adults. These additions included measures of student loan use, perceived debt burden and financial fragility operationalized as the respondent’s ability to raise $2,000 in 30 days in the event of an emergency. The researchers analyzed this updated dataset to investigate the relationship between financial literacy and financial behavior, while also examining the influence of demographic characteristics and unexpected income shocks. Special attention was given to the role of educational environments in shaping financial knowledge and behavior, allowing the researchers to evaluate how differences in school resources and teaching practices contribute to disparities in financial outcomes.

The researchers found that students who attended schools with adequate educational materials, strong classroom management and engaged teachers demonstrated higher levels of financial literacy. These findings suggest that school quality has a measurable impact on students’ financial preparedness and that such factors can be shaped through policy. Without targeted educational interventions, disparities in financial knowledge may continue to reinforce broader patterns of intergenerational inequality.

Publications de Bassa Scheresberg, C. (2014). Financial capability among young adults. George Washington University, Global Financial Literacy Excellence Center. Link to article: https://www.nefe.org/_images/research/GWU-Financial-Capability-Young-Adults/GWUFinancial-Capability-Young-Adults-Final-Report.pdf

Early Warning Signs of Impaired Financial Skills in Older Adults

Institution University of Alabama–Birmingham

Principal Investigator Daniel Marson, Ph.D.

Research Team

Grant Details Amount

$137,951

Short Summary

Methodology

Key Findings

Approximate Duration

July 2013-July 2015

The study used the Financial Capacity Instrument (FCI) to assess and track how well older adults manage everyday financial tasks over time. The research identifies some of the earliest financial skill impairments in cognitively typical older adults. Because older adults become disproportionately vulnerable to declines in financial abilities and potential exploitation, the researchers sought to empower individuals and families by increasing awareness of these early shifts in financial functioning.

The FCI was used to track both stability and change in these financial skills over time in the samples of control-normal and control-decliners. Using the Cognitive Observations in Seniors (COINS) dataset, the research team used mixed statistical models to identify these early changes and trajectories.

The main outcome of the study is a clear set of “early warning signs” to help family members, caregivers, doctors and older adults themselves recognize when financial abilities may be declining.

The set of early warning signs incudes: Taking longer to complete financial tasks, missing key details in financial documents, experiencing difficulty with everyday math, showing decreased understanding of financial concepts, and identifying risks in investment opportunities.

The complete checklist and corresponding examples can be found at: https://www.nefe.org/_images/research/Early-Warning-Signs-Impaired-FinancialSkills/Early-Warning-Signs-Impaired-Financial-Skills-Checklist.pdf

Publications Marson, D. C., McPherson, T., Falola, M., Cutter, G., Triebel, K., Martin, R., Kerr, D., & Gerstenecker, A. (2015). Early warning signs of impaired financial skills in older adults (Final report). University of Alabama at Birmingham. Link to article: https://www.nefe.org/_images/research/Early-Warning-Signs-Impaired-FinancialSkills/Early-Warning-Signs-Impaired-Financial-Skills-Final-Report.pdf

Social Influences on Financial Decision Making

Institution Duke University

Principal Investigator Scott Huettel, Ph.D.

Research Team Dianna Amasino, Nicolette Sullivan, Rachel E. Kranton

Grant Details Amount

$104,541

Short Summary

Methodology

Key Findings

Approximate Duration

November 2014-October 2018

Intertemporal choices involve tradeoffs between value and time, as when someone chooses between spending a smaller amount of money now or investing to receive a larger amount of money later. This study uses real-time eye tracking alongside computational modeling to investigate how individuals evaluate monetary rewards varying in amount and delay, aiming to better understand the mechanisms that distinguish patient and impatient choices.

In two experiments, young adults made financial decisions about monetary rewards that varied in amount and time until receipt. During the choice process, the position of their eye gaze was tracked in real time. Computational modeling was used to analyze these decision dynamics and to compare these temporal patterns between more patient and more impatient individuals.

The results indicate that reward amount and delay are evaluated through separate processes during intertemporal choice. Patient individuals incorporate information about reward magnitude earlier than impatient ones, indicating differences in attention over time. Eye tracking revealed that patient participants frequently shifted their gaze between monetary amounts, actively comparing values. Impatient individuals focused less on amounts and weighted delay information sooner, leading to preferences for immediate rewards. These findings challenge the idea that patience comes from a fully rational integration of all information and instead highlight the role of attentional strategies especially early focus on reward amounts in promoting patience. This suggests new directions for interventions targeting attention to encourage more patient decisions.

Publications Amasino, D. R., Sullivan, N. J., Kranton, R. E., & Huettel, S. A. (2019). Amount and time exert independent influences on intertemporal choice. Nature Human Behaviour, 3(4), 383–392. Link to article: https://pmc.ncbi.nlm.nih.gov/articles/PMC8020819/pdf/nihms1686516.pdf

Untangling the Determinants of Retirement Savings Balances

Institution New School for Social Research

Principal Investigator Teresa Ghilarducci,

Ph.D

Research Team Joelle Saad Lessler, Ph.D., Bridget Fisher

Grant Details Amount

Short Summary

Methodology

Key Findings

Approximate Duration

$120,000 January 2015-December 2016

Job loss, sickness, divorce: These are the kinds of life and economic events that derail even the most disciplined of savers. People want to believe, “It won’t happen to me.” The truth is that almost no one is safe from these shocks, and low-income individuals are disproportionately affected. With limited means to finance these shocks, they withdraw from their 401(k) if they are fortunate enough to have access to employer-provided retirement plans at all.

However, this study considers the reality that while sometimes unpredictable, changes in peoples’ lives do not occur independently, and that the magnitude of the impact on retirement savings depends on gender, race and socioeconomic status. By evaluating each factor’s relative impact on defined contribution retirement savings accumulations for different age and income groups, it becomes clearer who is at risk of not having enough retirement savings (and why).

The researchers linked data from the Survey of Income and Program Participation (SIPP) with individual earnings records from the Social Security Administration (SSA) and the Internal Revenue Service (IRS). The SIPP contains information on retirement savings, education, demographic characteristics, marital history, fertility history, health status and government transfer payment beneficiary history. The SSA and IRS data allow researchers to track lifetime earnings and variability, and also to study actual records of contributions to retirement plans.

Researchers identified which factors were related to increased or decreased retirement savings, and identified specific dollar amounts by which each factor affected account balances.

Factors related to higher savings include: Having a college degree, participating in defined benefit and/or defined contribution retirement plans at work, good health, being married and U.S. citizenship.

Factors related to lower savings include: Poor health and disability, income shocks, being non-white, being divorced and belonging to a union (which may signal greater likelihood of having a traditional defined benefit pension).

Publications Ghilarducci, T., Fisher, B., Radpour, S., & Webb, A. (2016). Policy options for cutting retirement plan leakages (Policy Note Series). Schwartz Center for Economic Policy Analysis and Department of Economics, The New School for Social Research. Link to article: https://www.economicpolicyresearch.org/media/k2/attachments/ Policy_Options_for_Cutting_Retirement_Plan_Leakages.pdf

Building Financial Self-Efficacy in Low-Income Young Children

Institution University of Kansas

Principal Investigator Barbara Phipps

Research

Team Terri Friedline, Ph.D., Nadia Kardash

Grant Details Amount

$134,997

Short Summary

Methodology

Key Findings

Approximate Duration

August 2014-July 2017

The purpose of the three-year research project, “Building Financial Efficacy in Low-Income Young Children,” was to gain insight into the effects of financial education and Child Savings Accounts (CSAs) on the financial knowledge and emerging identities of financial and educational capability in five- to eight-year-old children It was designed to answer the following research question: How do children’s knowledge, aspirations and identities change as they participate in financial education and/or CSAs over a three-year period?

Beginning in the fall of 2014, children in 10 kindergarten classrooms at three elementary schools were assigned randomly by classroom to one of three groups. Children in one group received financial education and had an opportunity to open and contribute to a savings account throughout the year (FE&CSA). Children in the second group were taught financial education only (FE), and children in the third group served as controls. Initially, 40 families consented to participate in our qualitative project. The researchers developed and used a semi-structured interview protocol. In years two and three, financial education was continued through instructional packets sent by regular mail to the parents of each of the children in the two financial education groups, and the interviews began two weeks after the last packet was mailed. The interviews were audio recorded and transcribed.

In analyzing the children’s responses to questions about money, spending, saving and banking, findings suggest that a financial capability identity developed in the FE and FE&CSA groups. The data show that children’s knowledge improved faster among the children who received financial education than among those who did not. This can be attributed to both the direct effect of the lessons on the child and to changes in the parents’ financial socialization of the child through the parent letters sent home after each lesson.

Many of the parents, even some in the control group, stated that being a part of the study and responding to our interview questions made them more aware of the need for helping their children develop financial awareness and savings behaviors.

An unexpected finding was that several parents stated that, because of being a part of our study, they had thought more about their own financial capability and were working to improve it.

Publications Banerjee, M., Friedline, T., & Phipps, B. (2017). Financial capability of parents of kindergarteners. Children and Youth Services Review, 81, 178–187.Link to article: https://www.sciencedirect.com/science/article/abs/pii/S0190740916304789?via%3Dihub

Enhancing Retirement Savings with School-Based Financial Education

Institution George Washington University

Principal Investigator Annamaria Lusardi, Ph.D.

Research Team Carlo de Bassa Scheresberg

Grant Details Amount

Short Summary

Approximate Duration

$110,000 January 2016-August 2016

Young adults in the U.S. are particularly vulnerable to the risks associated with greater responsibility for financial security. A previous report showed that young Americans have very low levels of financial literacy, are heavily indebted, are frequent users of high-cost borrowing methods and are already raiding their retirement accounts (de Bassa Scheresberg and Lusardi, 2014). Given these findings, the development of financial literacy skills among young people is increasingly perceived by policymakers as essential. This report analyzed data from the 2012 OECD PISA Financial Literacy Assessment to explore how financial literacy among U.S. high school students may impact the sustainability of the U.S. retirement system. The authors found that many U.S. teens lacked adequate financial literacy, which is crucial in a retirement system increasingly reliant on individual decision making. Financial literacy was strongly linked to socioeconomic status, school quality and teacher effectiveness.

Methodology In this paper, the researchers use data from the 2012 Programme for International Student Assessment (PISA) to analyze key factors and determinants of financial literacy among young individuals and assess the long-term implications for the robustness of the U.S. retirement system. The researchers used data from the 2012 PISA Financial Literacy Assessment, which tested over 29,000 15-year-old students across 18 countries, including 1,133 students from 158 U.S. schools. The study employed both univariate and multivariate statistical analyses to explore the relationship between students' financial literacy scores and various factors grouped into five categories: (1) demographic characteristics, (2) socioeconomic status, (3) parental involvement, (4) school characteristics and (5) teacher characteristics. The multivariate analysis used ordinary least squares (OLS) regression to isolate the effect of each variable while controlling other variables. This allowed researchers to identify which factors most strongly influenced financial literacy outcomes.

Key Findings

The researchers found that the average performance of U.S. students was not statistically different from the average performance of students in Organization for Economic Co-operation and Development (OECD) countries. However, a large variation in student performance within the U.S. was seen: Only about one in 10 students scored in the highest level of financial literacy. They also found that performance on the financial literacy assessment was strongly positively associated with variables denoting high family socioeconomic status, well-functioning schools and competent math teachers.

Publications Lusardi, A., & de Bassa Scheresberg, C. (2016). Enhancing retirement savings with school-based financial education (Final Report). Global Financial Literacy Excellence Center, The George Washington University School of Business

Link to article: https://www.nefe.org/_images/research/Enhancing-Retirement-Savingswith-School-Based-Fin-Ed/Enhancing-Retirement-Savings-with-School-Based-Fin-EdFinal-Report.pdf

303-741-6333

Diverging Paths: Youth Debt, College, and Family Background

Institution Ohio State University

Principal Investigator Rachel Dwyer, Ph.D.

Research Team Laura DeMarco, Ph.D., Emily Shrider, Ph.D.

Grant Details Amount

Short Summary

Methodology

Key Findings

Approximate Duration

$183,492 July 2015-June 2018

The purpose of this research was to extend prior research on when and why debt becomes problematic, versus when loans facilitate educational investments and the transition to adulthood, focusing specifically on populations such as community college students that have received too little scholarly attention. The study examines student loan debt, along with secured and unsecured consumer debt, to illustrate the broader financial risks experienced by young adults with education ranging from high school diplomas to graduate degrees.

Two nationally representative samples were analyzed for this research: “The National Longitudinal Survey of Youth – 1997” from the U.S. Bureau of Labor Statistics and “The Survey of Consumer Finances from the Federal Reserve Board.”

The researchers found that millennial emerging adults carry significant but unevenly distributed debt, with less educated groups facing riskier debts and Black and Hispanic young adults encountering barriers to credit. These findings emphasize the need to understand financial risk within broader social and institutional contexts. Financial advice is most effective when considering structural barriers alongside individual circumstances. The findings also underscore the importance of public investment in education to support upward mobility and reduce financial risks for individuals and society.

Publications Dwyer, R. E., & DeMarco, L. M. (2024). Unequally indebted: Debt by education, race, and ethnicity and the accumulation of inequality in emerging adulthood. Emerging Adulthood, 12(5), 878–893. Link to article: https://pmc.ncbi.nlm.nih.gov/articles/PMC11600330/pdf/nihms-2013949.pdf

Financial Fragility in the U.S.: Evidence and Implications

Institution George Washington University

Principal Investigator Annamaria Lusardi, Ph.D.

Research Team Raveesha Gupta, M.A., Andrea Hasler, Ph.D., and Noemi Oggero, M.Sc.

Grant Details

Short Summary

Methodology

Key Findings

Amount

$179,599

Approximate Duration

January 2017-February 2018

This project assesses the financial fragility of American households (e.g., the inability to cope with emergency expenses within a short timeframe). The researchers build upon previous work to understand further the nature and underlying factors of the problem expenses in a short time frame.

The financial fragility measure is based on the following question, asked in the National Financial Capability Study (NFCS): “How confident are you that you could come up with $2,000 if the need arose within the next month?” Answers to this question enable the researchers to assess respondents’ financial capabilities.

The researchers use data from two national surveys the 2015 NFCS and the 2015 Survey of Household Decision-making (SHED) and complement the data with qualitative information from focus groups conducted in three American cities: Austin, Baltimore and Cincinnati.

This study shows that even during a time of higher economic stability, 36% of Americans cannot come up with $2,000 within a month to cover an emergency expense. Fragility is, thus, highly prevalent even in good economic times. Moreover, financial fragility is highly pervasive in the broad working-age population. People in all age groups are comparably likely to be financially fragile, and although the likelihood decreases with increasing income, it is still relatively high among high-income workers. Specifically, we find that according to the 2015 NFCS, almost 30% of households in the median income category ($50K–$75K) are financially fragile and so are 20% of households in the next income band up to $100K

Publications Hasler, A., Lusardi, A., & Oggero, N. (2018, April 16). Financial fragility in the US: Evidence and implications. Global Financial Literacy Excellence Center. Link to article: https://cygnetinstitute.org/wp-content/uploads/2021/02/ Financial-Fragility-Research-Paper-04-16-2018-Final.pdf

303-741-6333

Understanding Financial Literacy Decay to Improve Financial Behaviors of Young Adults

Institution University of Rhode Island

Principal Investigator Stephen Atlas, Ph.D.

Research Team Nilton Porto, Ph.D., Jing Jian Xiao, Ph.D.

Grant Details Amount

$176,522

Short Summary

Methodology

Key Findings

Approximate Duration

September 2016-August 2017

This study extends the research done by Fernandes et al. (2014) and addresses the decay of financial knowledge after financial education interventions. The researchers reported results of two studies, first from a longitudinal study following a sample of college students after receiving a financial education intervention, followed by an online experiment study to examine the effects of financial education on financial capability variables.

Study 1: Tracking a Cohort of Young Adults for 12 Months

• 245 advanced college students nearing graduation

• Over-sampled disadvantaged populations

• Participants either completed online verified financial education or did not

• Data collected once before financial education and five times post-financial education throughout the following year Study 2: Manipulating Confidence

• 500 young adult participants from validated online panel of Amazon Mechanical Turk participants ages 18-25 years old

• Participants were randomly assigned to one of two knowledge conditions (watch a six-minute video on emergency savings or no video), one of three confidence conditions (recall two experiences with high confidence moderate or low confidence).

Results of the longitudinal study show that a single education intervention affects financial confidence and financial behavioral intention but not financial knowledge. Results of the experimental study show that the education intervention directly influences confidence and that confidence manipulations cause behavioral change.

Publications Atlas, S., Porto, N., & Xiao, J. J. (2018, September). Financial education and confidence in financial knowledge. [Conference paper]. ResearchGate. Link to article: https://www.researchgate.net/publication/323856184_ Financial_literacy_overconfidence_and_financial_advice_seeking

Financial Capability and Asset Building: Preparing Social Workers to Reach Millions of Households

Institution Washington University in St. Louis

Principal Investigator Michael Sherradon, Ph.D.

Research Team Margaret S. Sherraden, Ph.D., Jin Huang, Ph.D., Lissa Johnson MBA, MSW, LCSW, Peter Dore, M.A., Julie Birkenmaier, Ph.D., Vernon Loke, Ph.D., and Sally Hageman, Ph.D.

Grant Details Amount

$150,000

Short Summary

Methodology

Key Findings

Approximate Duration

June 2016-February 2018

This research study was part of a large effort called the Financial Capability and Asset Building (FCAB) initiative, which is housed at Washington University’s Center for Social Development (CSD). The initiative envisions social work and human-service practitioners who are prepared to improve financial capability and promote asset accumulation in financially vulnerable households. This study informs efforts to prepare social workers for FCAB practice. It creates a baseline measure of the amount of financial and economic (F&E) content currently covered in social work education, identifies F&E topics from the perspective of social work educators, and contributes to understanding the opportunities, barriers and directions for expanding F&E content in social work.

The survey instrument has four main sections: (1) The amount of F&E content taught, (2) Perceptions concerning the usefulness of F&E topics, (3) Barriers and recommendations on including F&E content and (4) Preferred ways to learn more about F&E content for teaching.

The survey also included questions about respondents’ demographic characteristics and prior financial education, the courses they teach and their institutions.

The most cited barrier to including F&E content in the curriculum is lack of flexibility and time to teach more content. In other words, time constraints and competition for limited teaching time make it imperative to clarify the connection between FCAB practice requirements and education. Emphasizing the importance of FCAB in conjunction with other topics, and perhaps over other topics, can be part of the solution. Eventually, practice needs for FCAB services should be reflected in the accreditation guidelines spelled out in EPAS (CSWE, 2015)

Publications Leiker, C., Clancy, M. M., & Sherraden, M. (2020, October). Insights from state treasurers: Developing and implementing statewide Child Development Account policies (CSD Policy Summary No. 20-19). Washington University in St. Louis, Center for Social Development.

Link to article: https://openscholarship.wustl.edu/cgi/viewcontent.cgi? article=1633&context=csd_research

303-741-6333

Making it Stick: Using Cognitive Science and Technology to Enhance the Impact of Financial Education

Institution Dartmouth College

Principal Investigator Sean Kang, Ph.D.

Research Team

Grant Details Amount

$168,431

Short Summary

Methodology

Key Findings

Approximate Duration

September 2017-July 2019

This study was designed to compare the knowledge, self-efficacy and credit management behaviors of participants following a workshop about personal credit. The study activities were designed to test the effectiveness of certain cognitive science learning principles when applied in a post-instruction setting. Reflecting the principles that testing can enhance learning and explanatory feedback following incorrect answers can improve understanding, participants completed two sessions of study activities that included practice quizzes. To test the principle that spacing out the review of information over time (“spaced retrieval practice”) can enhance learning and retention, some participants completed the study activities on a spaced schedule.

275 sophomore students at Champlain College (Burlington, VT) elected to participate in the study, and 175 students ultimately completed the study and had usable data. Study participants used a smartphone application to complete study activities on certain timelines.

This study suggests the effectiveness of spaced retrieval practice in the financial education field. When tested on their knowledge recall five to six months after an informational workshop on credit, college students who performed brief retrieval exercises (e.g., 10-minute practice quizzes) in spaced intervals after the workshop scored higher than students who did not do any retrieval or experienced retrieval only immediately after the workshop. This suggests that cognitive learning principles like spaced retrieval that are effective in other subject areas may also be effective for college financial education programming.

Publications Kang, S. H. K., Eglington, L. G., Schuetze, B. A., Lu, X., Hinterstoisser, T. M., & Huaco, J. (2023). Using cognitive science and technology to enhance financial education: The effect of spaced retrieval practice. Journal of Financial Counseling and Planning, 34(1), 20–31. Link to article: https://openscholarship.wustl.edu/cgi/viewcontent.cgi?article=1633&context=csd_researc h

Working Longer: Evidence and Implications for a Heterogeneous Workforce

Institution George Washington University

Principal Investigator Annamaria Lusardi, Ph.D.

Research Team Andrea Hasler, Ramon Perez

Grant Details Amount

$195,000

Short Summary

Methodology

Key Findings

Approximate Duration

December 2017-March 2019

Phased retirement programs offer employees who want to extend their years of work greater flexibility as they approach and pass the age of traditional retirement, and in the process, they provide employers with a valuable workforce planning tool. This research offers insight and perspectives on the challenges and benefits that employers and employees face, and ways to design formal programs that enable those who would like to work longer to gradually reduce their hours as they reach retirement