FINANCIAL EDUCATION: PROGRESS AND POSSIBILITIES

UPDATED APRIL 2025

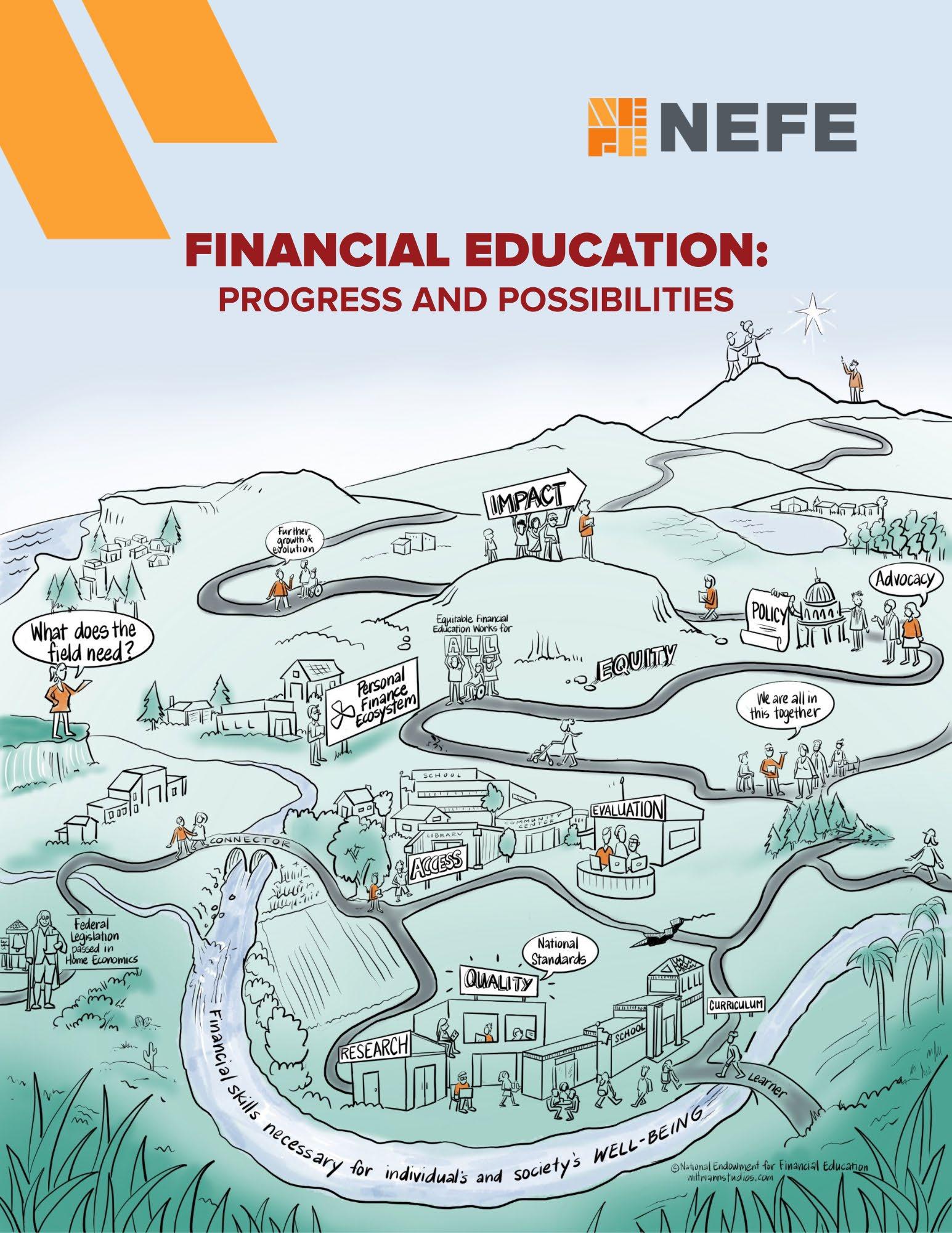

INTRODUCTION

There is growing recognition in the United States about the importance of financial education for individuals, families and society as a whole Especially as financial markets become more complex and economic challenges evolve, understanding the principles of managing money, budgeting, investing and debt is essential for individuals to make informed decisions and secure their financial well-being. Despite this recognition, many Americans lack the foundational knowledge necessary to navigate an increasingly complex economic landscape. Some have access to education and information that enables them to make informed financial decisions, whereas others face systemic challenges and exclusionary barriers that limit their access to economic information, services and resources.

This paper looks briefly at the more recent history of financial education in the United States and how the field has evolved over the decades, going from informal information that was sometimes passed from one family member to another to legislatively mandated course requirements for K-12 students in many states. This paper celebrates current achievements while also identifying challenges and gaps in financial education access and content. In describing the current state of financial education, this paper provides context and suggests priorities for the ongoing work of the National Endowment for Financial Education® (NEFE®) and its many partners and colleagues across the field

A NOTE ABOUT TERMS

As with any field especially one that is evolving and maturing financial education is awash with terms and concepts whose nuanced definitions are not always clear to readers and even practitioners in the field. To ensure clarity and comprehension of the concepts discussed in this paper, a few terms are explained below These descriptions are not definitions per se, but rather how the terms are used by NEFE and in this paper.

■ Financial education is a systematic approach to developing financial knowledge and decision-making skills.

■ Financial capability is an individual's ability to act in their own best interest based on their knowledge, skills and access to financial resources.

■ Financial well-being is a personal state that is self-defined and changes over time. It is not a final destination but rather a continuum.

■ Financial literacy is knowledge of personal finance concepts and is often applied to positive financial behaviors.

■ Financial knowledge is the ability to master financial concepts, terms and definitions.

■ Financial skills are the ability to use knowledge and make decisions. Financial access is having the opportunity and awareness to take action and exercise choice wthin financial markets, the financial services industry and other aspects of financial life.

HISTORICAL CONTEXT AND EVOLUTION OF THE FIELD OF FINANCIAL EDUCATION IN THE U.S.

EARLY AWARENESS OF THE BENEFITS OF FINANCIAL EDUCATION

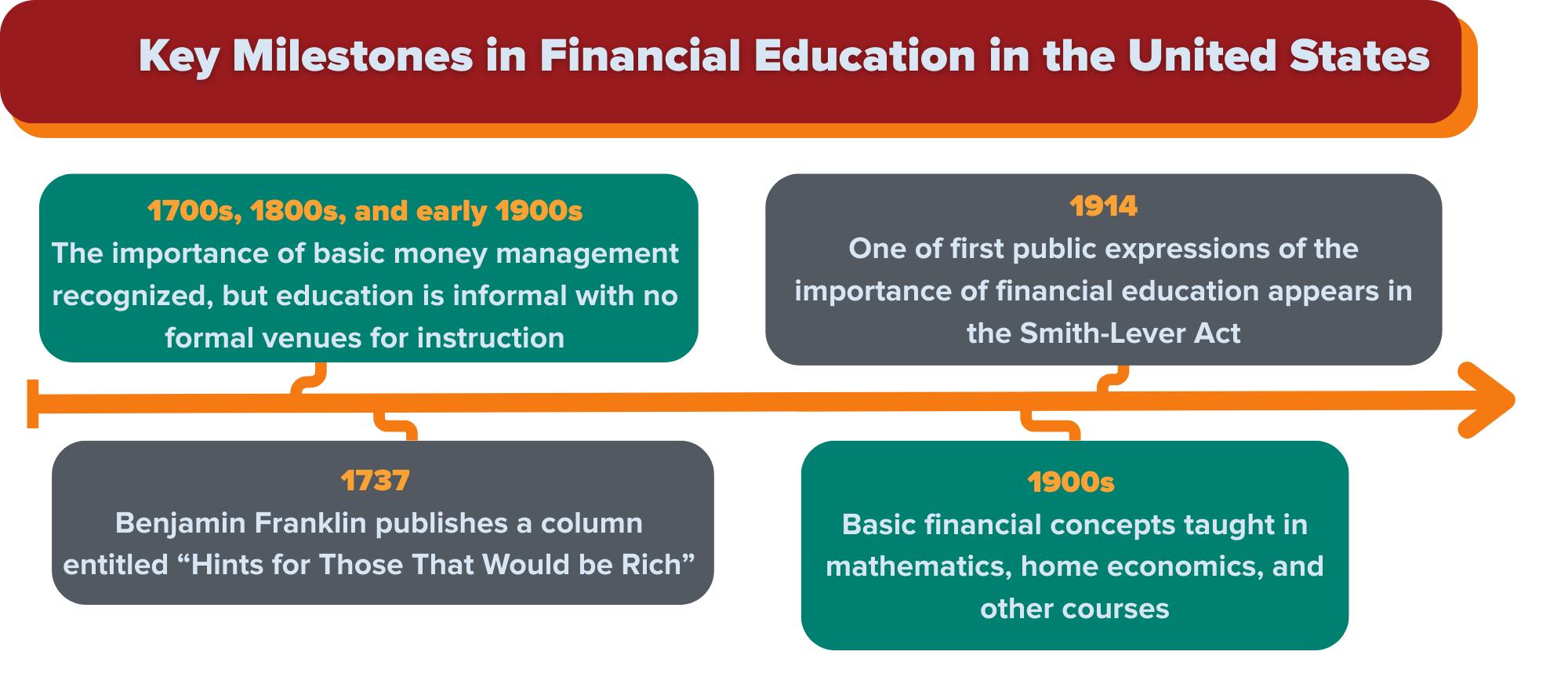

Long before financial literacy emerged as an educational topic in the early 20th century, people recognized the need to understand basic financial concepts to improve their decisionmaking and financial outcomes. Congress passed the Smith-Lever Act of 1914, established the Cooperative Extension Service, as one of the first public acknowledgments of the importance of financial education to individual well-being and society as a whole. In the early 20th century, some schools included financial education concepts in broader optional courses like mathematics and home economics. Even so, throughout much of the 20th century, families primarily taught financial education informally, passing down only basic concepts at home. It took decades before schools and institutions expanded beyond informal instruction. And while financial planners, banks, and other financial institutions expanded their offerings, access to financial knowledge often remained limited to those with significant resources or professional ties to the industry. In other words, people acknowledged the importance of financial education, but its implementation was inconsistent, with many institutions failing to treat it as a necessity for all.

MORE RECENT DEVELOPMENTS AT THE STATE AND FEDERAL LEVELS

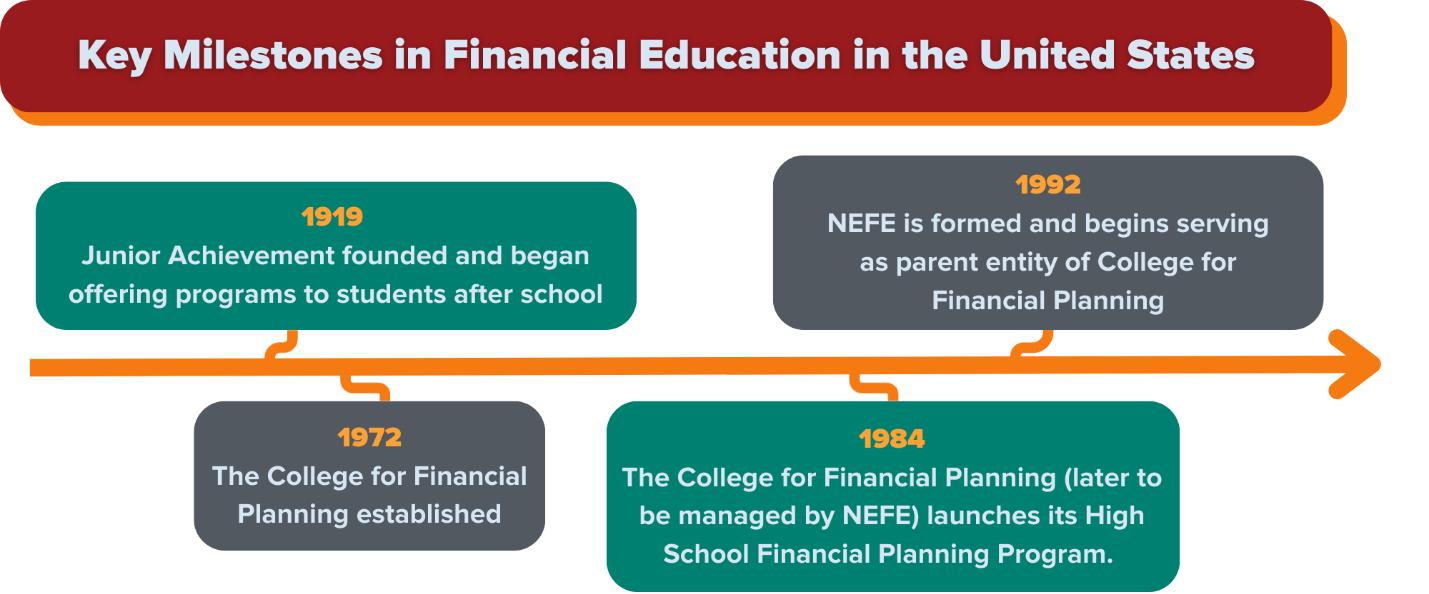

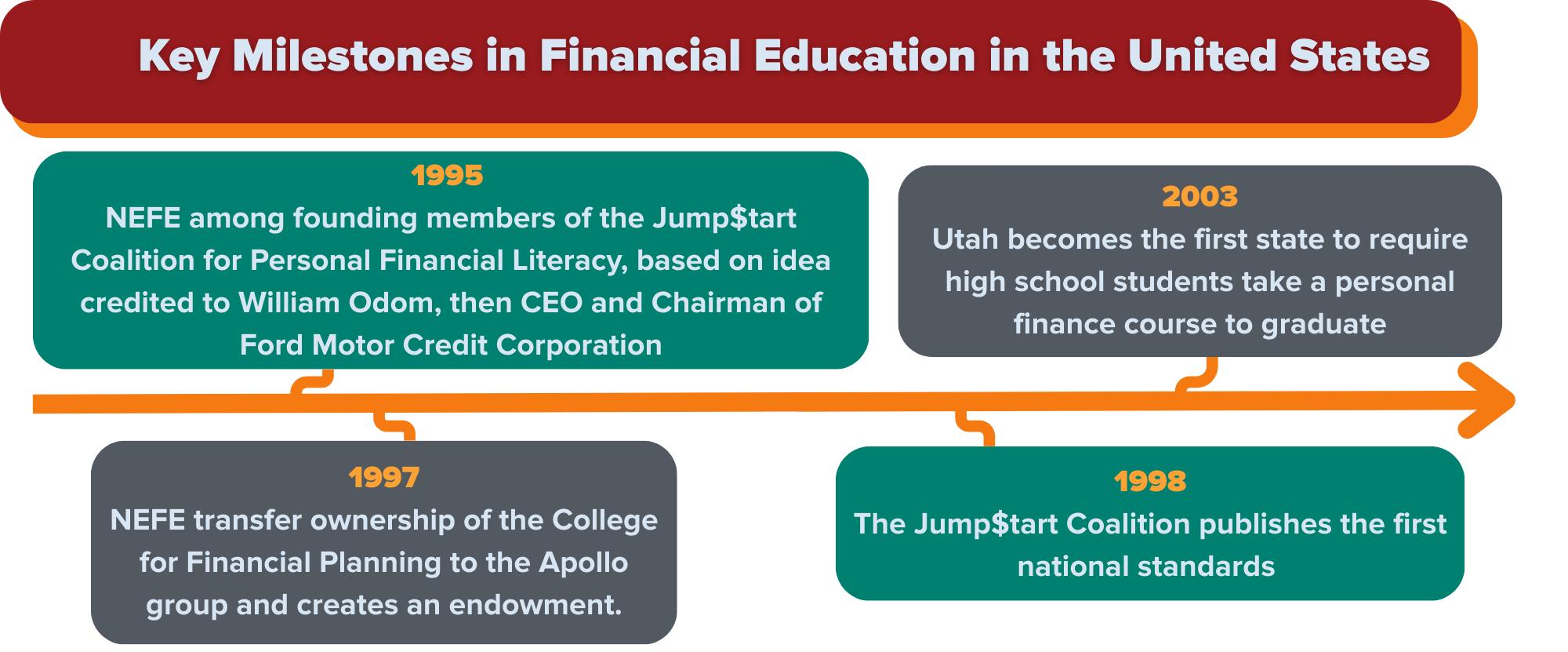

Financial education grew and continued to evolve in the late 20th and into the 21st century. Key milestones include NEFE launching its first financial education program in 1984, the Jump$tart Coalition being formed in 1995, and Jump$tart introducing the first national standards in 1998 (see below). These and other developments occurred as financial products and services (for example, credit and retirement accounts) became more widely available and more complex, and the demand for increased knowledge grew.

The Great Recession from 2007 to 2009 and subsequent growth recession in 2012 led to heightened awareness of the importance of financial education in navigating economic challenges, driving further demand for new programs, expansion of existing programs and the entry of new organizations into the field. At the same time, technological advances allowed for more innovative approaches to teaching and online courses expanded access.

Another factor that drove the demand and expansion of financial education was the rise in defined contribution plans, which shifted the responsibility of retirement savings and investment decisions from the employer to individuals. These plans which include 401(k) plans, Employee Stock Ownership Plans (ESOP) and profit-sharing plans overtook defined benefit plans as the predominant form of private pension arrangement by the 1990s. Understanding how to effectively manage their accounts, including investment choices and withdrawal strategies, became essential for individuals to enjoy financial security in retirement.

As the number of organizations developing curricula and/or offering financial education programs increased, practitioners and others recognized an increased need for standards to promote consistency and quality

The Jump$tart Coalition published the first national standards in 1998, with revised versions published in 2001, 2006 and 2015. The most recent set of standards, published in 2021, is the first co-published version and collaboration with partner organization, the Council for Economic Education (CEE). These standards are intended to guide educators, curriculum writers, policymakers and myriad others to ensure some consistency in financial education in K-12 classrooms.

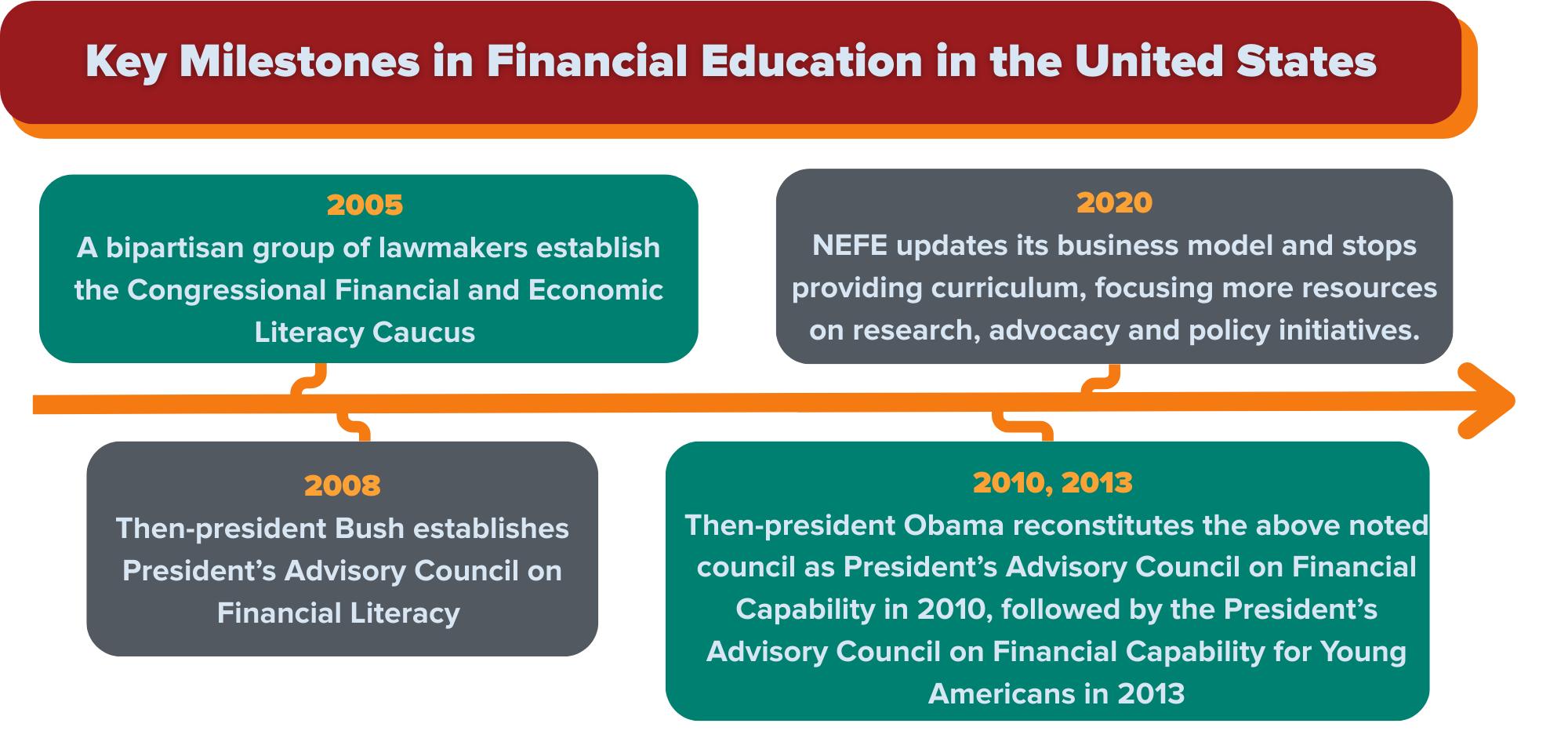

The federal government also took steps throughout the early 2000s and 2010s to support financial education for all Americans. The Financial Literacy and Education Commission (FLEC) was established in 2003 to develop a national strategy and coordinate financial education activities of over 20 federal agencies. FLEC’s establishment was followed by the formation of the President’s Advisory Council on Financial Literacy by then-President Bush in 2008 to make recommendations on improving financial education nationwide. The council was reconstituted by then-President Obama as the President’s Council on Financial Capability in 2010 and as the President’s Council on Financial Capability for Young Americans in 2013. While the latter council submitted its final report in 2015, its work encouraging a focus on four key strategies of building stronger partnerships, utilizing pilot programs, leveraging technology, and supporting research and evaluation continues to have a positive influence today. As demonstrated by the establishment of the councils by presidents Bush and Obama, financial education has benefited from bipartisan support at the federal level, as well as at the state level.

Figure 1 – Photos from 2024 Financial Literacy Day on Capitol Hill

Congressional committees and caucuses have held hearings and conducted studies over the years, and bipartisan caucuses in both houses seek to bring visibility to the importance of increased financial education and literacy: the Financial Literacy Caucus in the Senate and the Financial and Wealth Creation Caucus in the House of Representatives (first established in 2005 as the Financial and Economic Literacy Caucus), aims to “equip Americans with the skills and resources they need for economic stability, wealth-building, and prosperity”

Further complementing the federal efforts described, the Federal Reserve, Federal Deposit Insurance Corporation, and the office of the Comptroller of the Currency modernized regulations to the Community Reinvestment Act in 2023. This civil rights law is aimed at countering racial discrimination in lending and plays a significant role in promoting financial education, especially for low- and moderate-income communities. And more recently, in late 2024, the U.S. Treasury released a National Strategy for Financial Inclusion, which includes specific and actionable recommendations related to financial education.

The combined actions by the federal government over recent decades have motivated action and contributed to progress. But ongoing support and further action by the federal government is needed to promote consistent policies and equitable access to resources across all states and all populations, as discussed more below.

FINANCIAL EDUCATION TODAY

Today, with an increasingly complex financial system and unequal access to reliable information, there is widespread recognition of financial education as essential for everyone not just for those focused on securing their wealth. Just as society recognizes the need for math and reading skills to make informed decisions, it also acknowledges that financial skills are crucial for both individual and societal well-being. A 2024 survey carried out by NEFE showed overwhelming support for personal finance to be required in high school. According to the survey, more than 8 out of 10 adults surveyed support a high school requirement:

• 83% said their state should require a semester- or year-long financial education course for graduation.

• 82% whose high school did not offer financial education said they wished they were required to take a semester- or year-long financial education course during high school.

As financial markets and economic activity have become more complex, financial education has come to encompass a broad range of topics, including budgeting, saving, investing, credit and risk management, and retirement planning. The topics also have evolved with the changing financial landscape to encompass modern financial processes and approaches, including fintech, digital currencies and more. Courses and curriculum are increasingly geared to diverse populations and varying levels of financial knowledge and experience, with approaches often integrating technology to provide real-time advice and a more personalized learning experience. Moreover, many educators are taking a more holistic approach, addressing behavioral aspects of financial decision-making. And just as social media has taken over other aspects of daily life, so-called “finfluencers,” or influencers who share financial advice on social media, are finding receptive audiences especially among younger populations. But even if well-meaning, not all financial advice on social media is fact-based or appropriate to the learner; it is important for the learner to cross-check information with reliable sources and be aware of biases.

K - 12 HIGH SCHOOL GRADUATION REQUIREMENTS

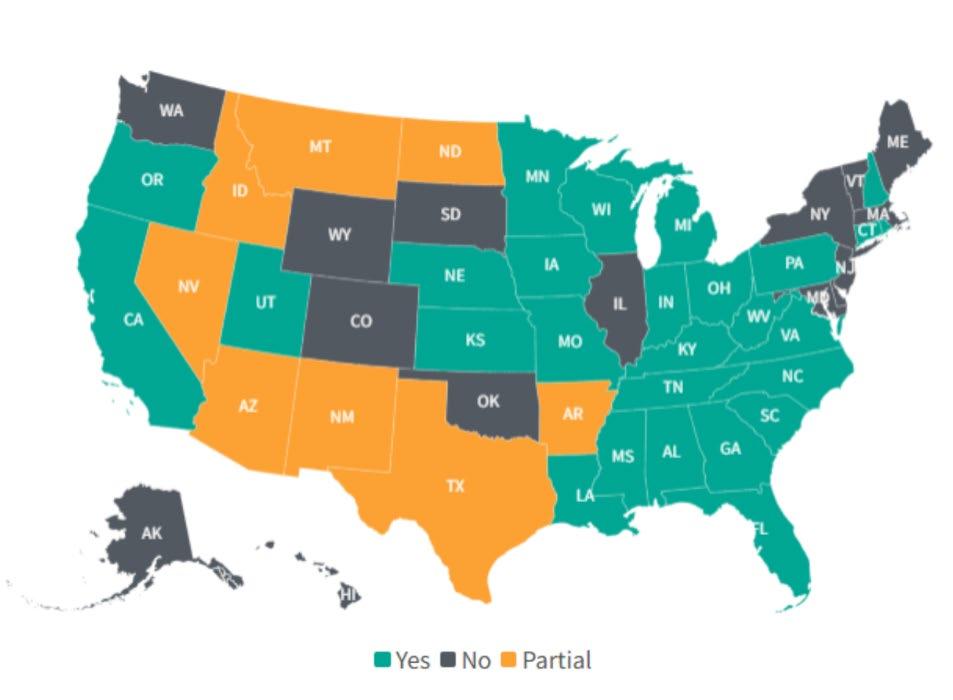

Americans now have more access to financial information and education, with workplace programs, community-based initiatives, faith-based organizations, and online and selfdirected learning resources Among the most significant developments in terms of broad access to financial education has been the work done by NEFE, Jump$tart Coalition (and its many partners), the Council for Economic Education, NextGen Personal Finance, the FinEd50 coalition and countless others to advocate for financial education requirements at the state level in K-12 education across the nation. As of 2024, according to NEFE (see NEFE’s map in the figure above), 27 states require a stand-alone semester course in financial literacy that every student must take to graduate. (Under this approach, states may have an integrated course if it is a year-long and 50% or more of the coursework hours are devoted to financial literacy.)

Even more states have slightly less stringent requirements: the Council for Economic Education (CEE) found in its 2024 survey that 35 states require students to take a course that includes personal finance to graduate (not necessarily stand-alone), and 28 states require all students to have some study of economics for graduation.

A slightly different approach to measuring state progress is the National Report Card on State Efforts to Improve Financial Literacy in High Schools issued every few years by Champlain College’s Center for Financial Literacy. In addition to reporting on how many and which states require a stand-alone personal finance course, the report grades states on how well they are implementing personal finance education policy, providing a more nuanced picture and state-by-state assessment.

The COVID-19 pandemic played a role in the significant growth in state legislative action over the past few years. Just as the recessions in 2008 and 2012 had driven expansion of programs COVID and its accompanying economic impacts also spurred increased action on the part of state legislators, who were faced with constituents experiencing severe economic hardships and challenging economic decisions.

The 27 states with requirements noted above is a significant increase from just six years ago when in 2019, pre-COVID, only six states had course requirements. Moreover, it is noteworthy that just as efforts at the federal level have enjoyed bipartisan support, so have most state requirements, contributing to their relatively rapid expansion among states.

RESEARCH

IMPACTS OF FINANCIAL EDUCATION AMONG STUDENTS: SOME RESEARCH EXAMPLES

The Effects of Financial Education on Student Financial Aid Choices (Stoddard & Urban, Economics Education, 2018)

The increase in state legislative action regarding K-12 requirements and related developments in the field has propelled, informed and been bolstered by an increasingly sophisticated body of research. Among recent studies that have driven progress are several on the impacts of financial education on student knowledge and behaviors. A 2018 meta-analysis showed that financial education has sizable impacts on knowledge but lesser impacts on behavior. A follow-up 2022 robust meta-analysis found significant impacts on both knowledge and behavior, suggesting that 1) the 2018 study confirming the positive impacts of financial education contributed to momentum in the field and led to practitioners and others addressing gaps and making positive changes and 2) the 2022 study benefited from the increasing sophistication in practice, research methodologies and approaches, enabling better analyses of downstream behavioral effects. These and similar studies provide foundational evidence of the benefits of financial education and have informed subsequent and increasingly sophisticated research. The collective growing research showing positive benefits of financial education has also contributed to the policy momentum seen in states passing requirement legislation.

A MORE NUANCED FIELD TODAY

Financial education in schools: A meta-analysis of experimental studies (Kaiser & Meinkhoff, Economics of Education Review, 2019)

Financial Education Affects Financial Knowledge and Downstream Behaviors (Kaiser, Lusardi, Menkoff, & Urban, Journal of Financial Economics, 2022.

As the field has grown and matured, it also has become more complex and nuanced. Progress today is not merely about more educators passing on knowledge to more learners; it is about ensuring that work is based on research- and data-based policies and practices; incorporating goals, measures of impact, and evaluation; and broadening and deepening the field to include behavior and practical applications. Most importantly, progress today is about learning from research and emerging practices to adopt new models and approaches that embed equity and inclusivity.

Until the last few years, not enough thought and resources centered culture and identity in materials and curricula. Content was often designed and delivered through a narrow lens and its success was assumed (or alternately its irrelevance was assumed by those who do not believe in financial education). Missing was the intentional and consistent consideration of an individual’s life circumstances, individual identity, cultural frameworks, and contextual understanding of societal systemic factors that shape and/or contribute to one’s position in the financial ecosystem all factors that shape the success or failure of any educational experience.

As the field embraces this broader and deeper approach that seeks to equip all populations to more effectively navigate the financial system, there is a recognition today that financial education is not a dichotomy as in, an individual is either financially educated or not. Whereas earlier approaches to financial education merely focused on providing information (and as noted above, usually the same information, irrespective of the audience), today’s educators understand that financial education occurs over an individual’s lifetime. At any given time, individuals must be able to relate to and apply what they learn for the information to be beneficial.

FINANCIAL EDUCATION AS A FIELD

While there are no hard and fast rules of what constitutes a field, most practitioners, policy makers, and financial educators agree that financial education evolved into a field over the past several decades and that today, it can be considered a field beyond infancy but not yet fully mature.

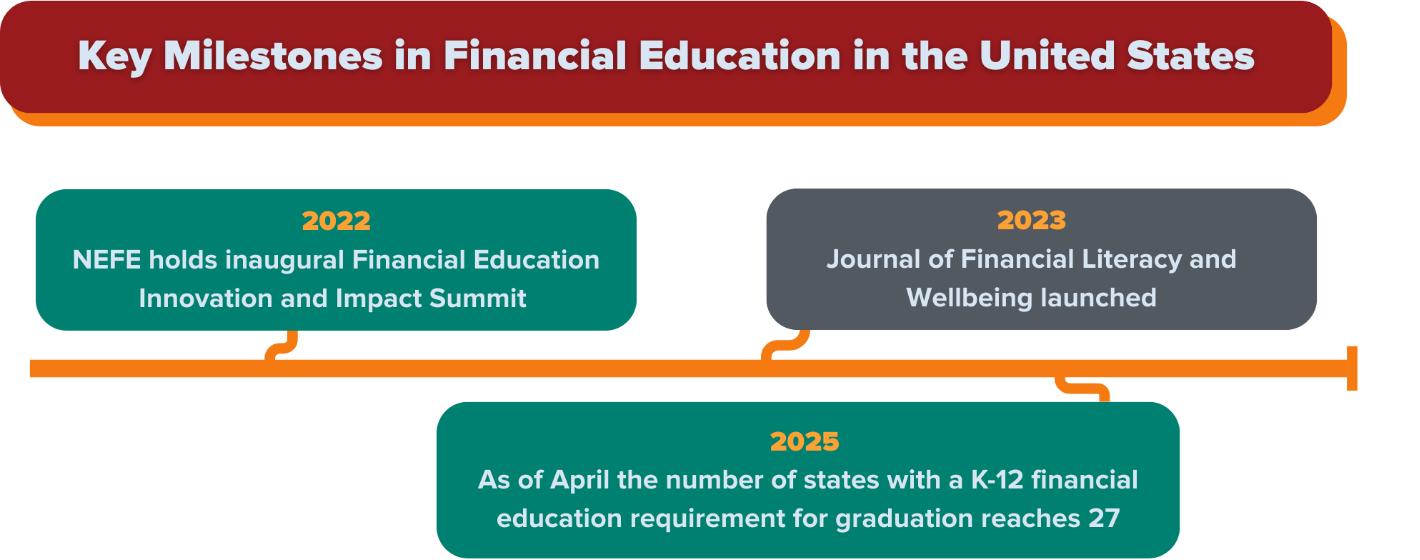

Fields are typically made up of like-minded people and organizations, are taught and researched, and have their own methodologies, theories, and bodies of knowledge. Financial education possesses these attributes, especially with the 2023 launch of the academic Journal of Financial Literacy and Wellbeing.

Unlike more mature fields, however, financial education remains somewhat fragmented with disparate information; and forward progress is sometimes as much led by like-minded organizations as by individual passions.

Finally, and perhaps most importantly, is the recognition that financial education cannot solve every problem. As noted on its website, “NEFE acknowledges that financial education alone cannot solve the economic inequity that exists across socioeconomic status, race and gender within the U.S. We see financial education as one piece of a broader ecosystem that affects individual financial capability and well-being.” Income inequality, systemic poverty, the racial wealth gap and other interrelated societal inequities require policy interventions and changes. This recognition is important in countering the pessimistic view that because financial education has not solved poverty in the nation, it must be ineffective.

As the field continues to mature, further growth and evolution is both appropriate and needed.

NEFE’S ROLE IN THE FIELD

Many individuals and organizations have contributed to making financial education what it is today. In addition to those already mentioned are countless educators, curriculum providers, advocacy organizations, and other individuals and organizations, all committed to improving financial well-being for all Americans.

NEFE’S FIVE KEY FACTORS FOR EFFECTIVE FINANCIAL EDUCATION

Well-trained financial educator (and/or tested financial elearning protocol)

Vetted/evaluated financial education program materials

Timely personal finance instruction

Relevant subject matter

Evaluating impact

Since its founding, NEFE has consistently sought to innovate, excel and drive progress in financial education, not just further its own position in that field. In 2020, NEFE recognized there were several effective, high-quality curriculum providers and saw value in further focusing on research, advocacy and policy. The decision to sunset its curricular offerings, a well-known part of its business model, allowed NEFE to focus additional financial and personnel resources toward efforts that strengthen our community of practice and to advocate for more access to financial education, fund more research, and facilitate robust conversations about issues like quality, access, equity and impact.

NEFE’s policy and advocacy work focuses on both the state and federal levels and utilizes research and historical data to drive conversations, convene thought leaders and amplify information. Core to NEFE’s mission is promoting and advocating for quality financial education. Recently this work has centered on ensuring high school graduation requirements are implemented with quality and effective financial education to best serve learners. This work included crystalizing what is meant by effective financial education and developing the “Five Key Factors for Effective Financial Education”. To be reviewed and revised in 2025, NEFE’s factors are intended as a guide for educators and as minimal requirements for interventions to be successful.

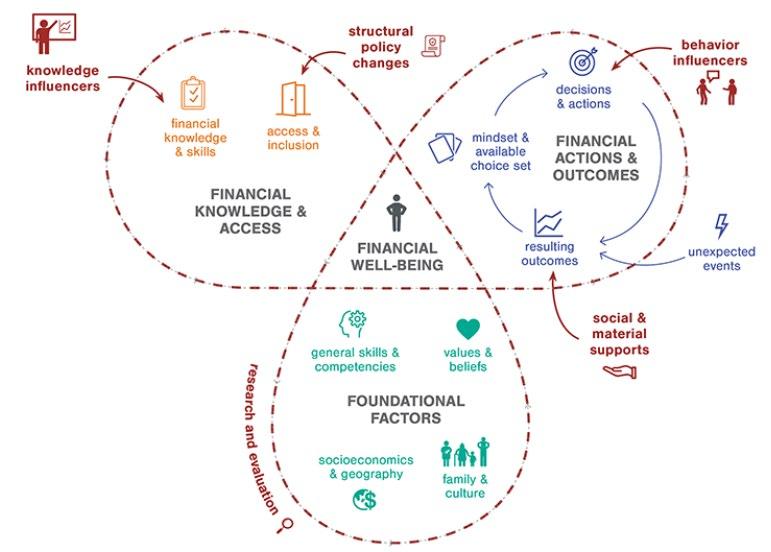

Another of NEFE’s most utilized contributions is the creation of the Personal Finance Ecosystem. The Ecosystem (see figure 2) is a visual framework informed by NEFE’s years in the field and the evolution of its own work in curriculum, adult learning programs, research and advocacy. It shows financial education’s role in an individual’s well-being and the many other factors that influence financial well-being.

It is intended to be used by practitioners, researchers, and policy makers to contextualize financial education among many other interventions, and to manage expectations of what can be achieved by any single intervention as well as model what can be achieved when we think and act collectively.

Building on experience convening thought leaders for over two decades, NEFE held the inaugural FEII Summit in 2022, a first-of-its-kind gathering in the field of financial education. The Summit provided an opportunity for both long-time financial industry experts and newcomers to celebrate progress and discuss challenges; and it offered strategically planned presentations and discussion around access, quality and impact. The 2024 Summit solidified NEFE’s role as convener and built on the success of the first convening, with participants and keynote presentations, panels and breakouts that further explored financial education quality, access and impact.

NEFE continues to carry out and support innovative and much-needed research. Reflecting the growth in the financial education field over the past two decades and its increase in complexity, NEFE’s research agenda has similarly grown both in quantity and complexity. Since 2006, when NEFE made the decision to focus its grants program solely on research, to 2024, NEFE has awarded 43 research grants totaling close to $7 million dollars. Many early research grants sought to understand the foundational aspects of financial literacy; today, mirroring the progression of research in the field, NEFE’s supported research agenda has become much more focused on broader implications of financial education’s quality and outcomes. The current research agenda includes a scale validation project that is addressing the lack of rigorous testing and validation of survey assessments in the financial services industry and longitudinal studies that demonstrate how financial literacy evolves over time and impacts financial decisions

NEFE-FUNDED RESEARCH: SOME RECENT EXAMPLES

University of Tennessee

Extension: Listening to LearnAssessing the Needs of Personal Finance High School Teachers

Lewis and Clark College: Exploring Racial Ideologies within the National Standards for Personal Finance Education

Morgan State University: Creating Identity Responsive Financial Education

UCLA: The Power of Second Sight: Measuring the Impact of Political Financial Education on Inequality

OTHER RECENT DEVELOPMENTS IN THE FIELD

Like most fields, financial education does not have neat lines or clear boundaries defining what it includes and what it doesn’t. As financial markets and supporting technology evolve and the landscape becomes even more complex, the field continues to incorporate new ideas and concepts.

The integration of fintech has expanded access to financial services and education; AI is providing personalized learning experiences and real-time feedback; online courses, apps, and interactive tools offer flexible and engaging learning opportunities; financial literacy games make learning about money management more interactive and enjoyable, particularly for younger audiences; and as already noted, “finfluencers” are reaching new audiences and changing how learners interact and engage with financial educators and curriculum. While expanded access to financial information and concepts can be a benefit for individuals and the field, unless properly vetted they also carry the increased risk of doing more harm than good.

In addition to expanding with fintech, financial education is evolving to encompass other areas of health and wellness as well as concepts like sustainability, behavioral finance and financial therapy. Behavioral finance looks at psychological influences on investors, consumers and financial markets. And financial therapy is a type of therapy that combines financial and emotional support and hopefully will deepen our understanding of the Personal Finance Ecosystem (PFE).

CHALLENGES

Recognition of the importance of financial education and the growth in expectations and requirements is cause for celebration. But significant recent successes have not fully overcome the challenges that the field faces, and with successes have come new challenges. For K-12 students and adults alike, consideration must be given to the quality and relevance of the curriculum. Financial education content must evolve to keep pace with changes in the financial landscape, such as the rise of digital banking, cryptocurrencies and the gig economy.

Even more, as already noted, the field has come to understand that financial education must center the needs and experiences of the learner to ensure materials and practices are accessible and inclusive. Whereas the historical approach had been based on an overly simplified assumption that more financial education will lead to more positive outcomes for individuals, more research is needed to better understand current literacy levels and differences by demographic groups including age, gender, socioeconomic status and other differentiating factors.

“Financial education plays a vital role in the personal finance ecosystem. It helps individuals better understand and access appropriate financial services, increase decision-making confidence, and avoid exploitation and predatory practices. By promoting financial literacy, we can empower underserved communities and promote economic equality, contributing to a more inclusive financial system.”

BETH BEAN, PH.D

Senior Vice President, Research and Policy

The recent increase in state-level financial education requirements has been widely (and rightly) celebrated, but requirements alone aren’t enough. Equal attention is now given to the importance and associated challenges associated with implementing those requirements in a meaningful and impactful manner. Some of the main obstacles are a lack of trained educators and the limited amount of support from states to mitigate this gap. In a recent NEFE funded research study exploring the implementation of Nevada’s requirement implementation, “teachers reported a need for more and better financial literacy instructional materials, including culturally relevant teaching materials” (Mulhern, Kennedy, and Okuda-Lim, 2024). Addressing this gap will require investment in educator training programs, time to appropriately scale the implementation of personal finance graduation requirements, and deployment of comprehensive, responsive curricula that can be easily implemented in schools across the country.

Thus, while financial education has come a long way and made great strides in improving curriculum and understanding impact, until financial education is available to and works for everyone, the field must temper any celebratory announcements with an acknowledgement that those who do not have access are not benefiting. And those who are in locations that have poor implementation may even be harmed or at best, the education has no impact. These systemic issues perpetuate a cycle of financial illiteracy among disadvantaged populations.

GOING FORWARD:

WHERE IS THE MOMENTUM TODAY?

The challenges identified above most notably ones associated with implementing K-12 requirements and the need for more research, along with the larger, interrelated issues of quality, access, equity and impact are driving NEFE’s and its partners’ priorities and work going forward.

The rapid rise in the number of states requiring financial education as a condition of graduation offers an opportunity to improve financial education at scale. But just doing more is not enough: Implementation on a large scale must not sacrifice excellence. Quality financial education is accurate, timely and relevant that is, content and delivery modalities consider the learner’s context and life experiences and adapt to how the information is being consumed. And while the increase in the number of states with financial education requirements at the K-12 level is encouraging, these bills rarely provide support for teacher training and redeployment, causing many practitioners to describe the requirements as “unfunded mandates.” While continuing to push states that have not passed K-12 financial education requirements to do so, a high priority should be placed on providing training and tools for educators and supporting implementation of existing state mandates by refining curriculum to be relevant and effective for the learner and elevating the need for teacher training. NEFE recognizes many of our peers provide high-quality training and applauds their commitment to delivering national and local professional development. Yet, solidifying these graduation requirements with guaranteed dollars to cover issues such as teacher training will assure not only access to a financial education but also access to confident and well-resourced educators.

The work focused on K-12 requirements is integral to the field’s commitment to advancing equitable and inclusive practices to address the disparities in access to quality financial education across all communities and individuals of all ages. With the hiring of its first position solely focused on equity in 2023, NEFE doubled down on its commitment to highlight equity as a top challenge and a top priority. NEFE is working with peers to define and fully understand what is meant by equity and inclusivity in financial education. As such, key concepts and questions center on: ways to make financial education relatable and relevant to myriad audiences; who currently does not have access to high-quality financial education; understanding those who have been left out of the opportunities that financial education offers; defining the desired outcomes we hope to see across all populations and recipients of financial education; and defining the calls to action that will influence practicebased and systemic issues.

These and other questions require rigorous evaluation and research as well as lots of listening. Even as we tout a growing field and its many advances, there is far too little evaluation data on what constitutes quality financial education, how it impacts individuals, and even what metrics and measurements are most effective. More research is needed to better understand impacts on population subsets and how the field can advance effective, population-specific practices. And research is needed not just on small groups at a single point in time but also through longitudinal studies that track many participants over several years.

Financial education occurs over a lifetime, at different ages and in differing circumstances. For many, it starts at home and in K-12 education. For some it extends into higher education, and it is needed by all in the workforce and retirement. Wherein, research must delve into the causal mechanisms between financial education, positive financial behaviors, and financial well-being and other individual and societal characteristics. Only by significantly expanding research will the field be able to identify the most effective methods and programs to improve financial literacy among different demographics.

Of course, in calling for further research, we cannot fall victim to analysis paralysis the research itself must continue to grow and evolve, benefiting from ongoing scrutiny of existing practices even as we adopt new models and approaches. NEFE is positioned to lead progress in many of these areas by our commitment to collaborating with partners to improve evaluation methods and tools while advancing large-scale national research on financial education’s long-term impact, including its effects on different population subsets.

Perhaps most important for the financial education field is the need to remain connected and unified as it grows. NEFE has been a leader in convening stakeholders to ensure that efforts are aligned, and resources are used efficiently. Going forward, this coalescence is even more important. It will foster collaborative opportunities and is the best defense against ineffective approaches, inadequate curriculum, and poorly trained or untrained instructors. Agreement on evaluation metrics and measures will lead to better outcomes, the surest path to scalability and sustainability for long-time players and newcomers to the field alike. No organization in this community has the resources alone to solve this issue, thus NEFE’s vested interest in collaborative, researchinformed approaches to both financial education practice and advocacy.

Financial education has experienced tremendous momentum and success over the past three decades, but there still is much to do. A true spirit of collaboration within our community is necessary to unlock the doors to improved financial well-being for all Americans. Anything less than fully embracing our synergy is a disservice to those we all aim to serve. We are stronger together than as one.”

BILLY J. HENSLEY, PH.D PRESIDENT AND CHIEF EXECUTIVE OFFICER

CONCLUSION

As the field of financial education steps into young adulthood, it has seen remarkable progress and achievements both highlighting and confirming its potential; we all have much to celebrate. NEFE is proud of the progress made and our role in it. Yet, much as a young adult faces new challenges and responsibilities, this field has significant growth and maturation ahead to achieve even greater impact. As the focus now is on ensuring quality curriculum along with effective pedagogy that centers the learner, rigorous evaluation, and innovation based on robust research, we must not forget that disparities in access to effective financial education persist among underrepresented and low-income communities. We face this next era of work alongside our partners and hope that in the years to come many more organizations and policymakers will be working to champion effective financial education.

NEFE continues its service of research, expertise and collaboration at such a critical moment in time. Highquality financial education plays an especially pivotal role in changing someone's life and can impact the trajectory of entire generations. NEFE has a distinguished and impressive legacy of leadership and thought partnership and continues to make a difference in improving the quality of financial lives for all Americans.

DIONNE BLUE, PH.D. 2025 CHAIR, NEFE BOARD OF TRUSTEES

As NEFE staff are fond of saying, until financial education works for all, it doesn’t work. Through its convening power and its advocacy work and by prioritizing rigorous, actionable research, NEFE is driving the field to focus on access, quality and impact concepts that will require significant work by all and NEFE is seeking to lead by example and make decisions that will continue to create positive change.

Momentum requires a unified approach. All financial education organizations whether advocates, practitioners, evaluators or researchers must leverage each other's strengths, avoid unnecessary duplication of efforts and address challenges with a unified front. Such a cohesive and collaborative approach will ensure that scarce resources are used efficiently and effectively and best practices shared. Only through sustained commitment and collaboration will we see successful outcomes for all individuals.

© 2025 National Endowment for Financial Education® (NEFE®)