DAIRY MARKET REPORT VOLUME 29 | ISSUE 3

3/30/2026

EXECUTIVE SUMMARY After starting the year in a funk, dairy product prices have noticeably improved even as milk production remains robust, increasing 3.4% in January on a liquid basis. While the milking herd continues to grow, component growth surprisingly decelerated to start 2026, indicating that producers are responding to strong economic incentives from beef-on-dairy but not pushing for maximum milkfat tests with the fall in butter prices. Despite heavy milk production, dairy product supplies and inventories are not overly burdensome. In fact, nonfat dry milk prices are rising due to limited supply, and butter is finding support due to reported low inventories. Domestic demand for dairy proteins remains remarkable, as consumers turn to products like cottage cheese, Greek yogurt and high protein beverages to support health goals. With vigorous domestic protein demand and growing milkfat exports, signs are indicating that the U.S. is moving back towards balance. While DMC margins dipped to $7.81/cwt in January, recent commodity price increases should provide a much-needed boost to margins in the coming months.

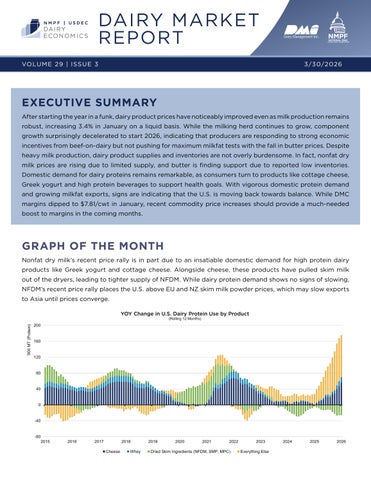

GRAPH OF THE MONTH Nonfat dry milk’s recent price rally is in part due to an insatiable domestic demand for high protein dairy products like Greek yogurt and cottage cheese. Alongside cheese, these products have pulled skim milk out of the dryers, leading to tighter supply of NFDM. While dairy protein demand shows no signs of slowing, NFDM’s recent price rally places the U.S. above EU and NZ skim milk powder prices, which may slow exports to Asia until prices converge.