CHARTING A COURSE FOR GROWTH

Playbook

December 2025

Playbook

December 2025

Discover Boating partnered with Ipsos, a Market Research and Consultancy specialist, to gain strategic insights on the evolving dynamics of recreational boating. This collaboration aimed to help Discover Boating understand the landscape today, trends that will shape recreational boating, and actions to take to retain and grow the category.

Uncover macro forces affecting today’s consumer that will impact the boating category and broader operating context #2

Highlight how the Boat Owner has changed, focusing on how they access boating, learn, are influenced, and make purchases & who the Owner of Tomorrow will be & Objectives

To achieve these objectives, Ipsos conducted qualitative interviews with industry leaders and quantitative research with current and potential boat owners.

Explore and identify predictive factors that indicate likelihood to own a recreational boat #3

This playbook synthesizes our comprehensive insights for Discover Boating into two sections of practical insights and recommendations:

1) Today's Boating Landscape: An overview of who current and potential boaters are, with detailed profiles on the most promising prospects

2) Futureproofing analysis and recommendations for Discover Boating, OEMs, and Dealers to connect more effectively with boaters over the next 3 years.

We recommend that OEMs and Dealers begin by reviewing the Executive Summary, followed by the "Today's Boating Landscape" section. They can then proceed to explore the profiles, insights, and strategic recommendations relevant to their specific interests.

Selection of key insights from the Playbook

To understand how to reach our target audiences and grow the recreational boating category, the industry needs to know who today's boat owners are and who could become owners in the future. Through our research, we have defined two primary groups of targets: Current Owners and Prospective Owners.

These groups are fundamentally different in their relationship with boating: one group already participates in the category while the other represents our high potential new buyers to grow the category. Each group has distinct needs, motivations, barriers that require tailored approaches to effectively engage them.

Across these two primary groups, we have identified further clusters (6 in total) that allow for even more precise targeting at specific touchpoints in the consumer’s boating journey.

Target Boaters clusters include both Current and Prospective Owners, and are mapped to Discover Boating, Dealers, and/or OEMs for targeted action

People who currently own at least one boat

RECENT BUYERS

People who may be interested in owning a boat in the future

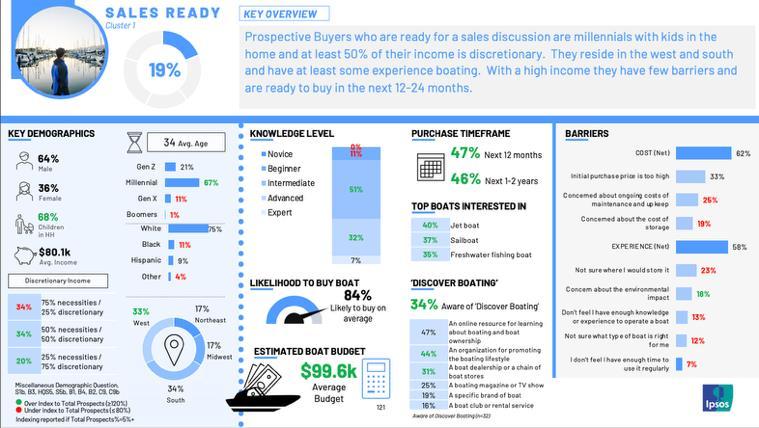

SALES READY

INEXPERIENCED TIME-PRESSED COST-CONSCIOUS

Purchased their main boat prior to 2020

Focus for..

Dealers

Purchased their main boat after 2020

Fewest barriers experienced; ready to buy

Focus for..

OEMs Discover Boating

Dealers OEMs

Have the means, but feel they need more experience, support and knowledge

Core barrier is lack of time; open to alternative access models

Interested, but are not as financially ready; open to alternative access models

OEMs

*A fifth Prospective Owners cluster, Priced Out, is excluded due to it being a low-opportunity target

Prospective Owners tend to be younger, have lower income, and turn to peer-driven digital channels to engage with boating

People who currently own at least one boat

• Older, higher income, more educated

• Have more positive outlook on personal finances

• Value boat manufacturer websites, online articles/reviews, dealer websites as main resources

People who may be interested in owning a boat in the future

• Younger, lower income, less educated

• Higher engagement with boats via charters and rentals

• Friends and family, YouTube, and social media play a bigger role when it comes to key information resources

Data overviews for each Prospective Owner Target are presented in the following pages, with more data available in the appendix

Fewest barriers experienced; ready to buy

Have the means, but feel they need more experience, support and knowledge

Core barrier is lack of time; open to alternative access models COST-CONSCIOUS

Interested, but are not as financially ready; open to alternative access models

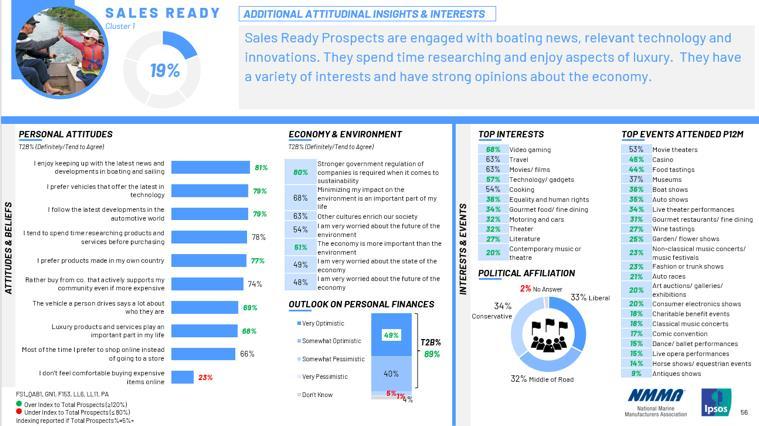

Prospects who are ready for a sales discussion are millennials with kids in the home and at least 50% of their income is discretionary. They reside in the west and south and have at least some experience boating.

Prospects who are ready for a sales discussion are Gen Z or Boomers with 25% of their income as discretionary. They reside mainly in the Northeast and have novice to beginner boating experience.

Prospects are Millennials and Gen X, majority living in the South. They are less concerned about the cost or their experience with boating, and more concerned having enough time to use the boat.

Prospects who are looking to purchase in the next 1-5 years. They are less likely to be advance or expert boaters and are mostly concerned with costs, considering not only the initial cost of the boat but also the storage and ongoing maintenance for the vehicle.

Sales Ready are prospects who are ready for a sales discussion are millennials with kids in the home and at least 50% of their income is discretionary. They reside in the west and south and have at least some experience boating. With a high income they have few barriers and are ready to buy in the next 12-24 months.

Concerned about ongoing costs of maintenance and upkeep

Concerned about the cost of storage

(Net)

Not sure where I would store it

Concern about the environmental impact

Don’t feel I have enough knowledge or experience to operate a boat

Not sure what type of boat is right for me

I don’t feel I have enough time to

Inexperienced are prospects who are ready for a sales discussion are Gen Z or Boomers with 25% of their income as discretionary. They reside mainly in the Northeast and have novice to beginner boating experience. They are still trying to decide what type of boat to buy and are ready to buy in the next 1-2 years.

Not sure what type of boat is right for me

Don’t feel I have enough knowledge or experience to operate a boat

Not sure where I would store it

Concern about the environmental impact COST (Net)

Concerned about ongoing costs of maintenance and upkeep

Concerned about the cost of storage

Initial purchase price is too high

Don’t feel I have enough time to use it regularly

Time Pressed Prospects are Millennials and Gen X, majority living in the South. They are less concerned about the cost or their experience with boating, and more concerned having enough time to use the boat. They have an estimated budget of $66K for their purchase; average with other prospects.

Concerned about ongoing costs of maintenance and upkeep

Concerned about the cost of storage

Don’t

Cost Conscious Prospects are looking to purchase in the next 1-5 years. They are less likely to be advance or expert boaters and are mostly concerned with costs, considering not only the initial cost of the boat but also the storage and ongoing maintenance for the vehicle and fear they won’t have time to use it.

Concerned about the cost of storage

Concerned about ongoing costs of maintenance and upkeep

Initial purchase price is too high

(Net)

Concern about the environmental impact

Not sure where I would store it

Don’t feel I have enough knowledge or experience to operate a boat

Not sure what type of boat is right for me

Don’t feel I have enough time to use it regularly

These Macro Forces will also have implications on how OEMs, Dealers, and Discover Boating connect with their Target Boaters

Forces and its resulting Drivers of Change

Increasing Cost of Living and Fragmented Labor Market

Economic Optimism and Luxury Spending

Changing Definition of Ownership

Growing Diversity and Generational Shift

Value Reprioritization and Delay in Traditional Milestones

Mindful and Purposeful Living

Increased Digital Usage in All Aspects of Life

Openness to

Social Media as a Source of Influence

• Current Owners (Established & Recent)

• Sales-ready

• Inexperienced

• Communicate boating as an activity that can be enjoyed within a moderate budget and serve as a trusted mentor by offering clear, easy-to-understand guides

• Provide resources on how boating can be enjoyed in sustainable ways, and for better mental health

• Actively promote boats designed for enjoyable family and kid-friendly experiences

• Position new boat tech features as enablers of efficiency, safety, and connectivity

• Develop standardized digital assets (e.g., video tutorials, interactive calculators) for dealers to use in the research phase of the purchase journey

• Offer immersive digital experiences of boat interiors and exteriors, and invest in professional video walk-throughs of high-interest models

• Strategically partner with influencers on social media and post videos on YouTube to gain more visibility and interest

Further implications are detailed within the individual Target Cluster profiles in the Futureproofing section.

• Current Owners (Established & Recent)

• Sales-ready

• Inexperienced

• Improve transparency through clear service and maintenance plans that offer a fixed, predictable cost for routine maintenance

• Collaborate with local organizations and provide owners opportunities to engage

• Host fun and low-commitment local on-water events that give prospective boaters a firsthand taste of the boating experience

• Offer introductory boating and safety courses in accessible local areas, open to anyone interested in getting into boating

• Ensure the digital experience is seamlessly connected to the in-person journey, and be prepared to engage highly informed customers

• Develop highly engaging, mobile-friendly website tools that allow users to easily compare models or guide them to the best fit for their needs

Further implications are detailed within the individual Target Cluster profiles in the Futureproofing section.

• Current Owners (Established & Recent)

• Inexperienced

• Time-Pressed

• Cost-Conscious

• Position boating as an investment in family memories, relaxation, and life experiences

• Normalize access as an important steppingstone to becoming a boat owner for prospective boaters

• Develop owner spotlight campaigns that highlight their personal stories

• Develop content and videos that tie back to the core motivations for each group (e.g., relaxing time in nature, with family, and being outdoors)

• Leverage the power of existing owners by hosting events such as owner testimonials that introduce people into boating

• Create online forums and communities where owners can connect, and a feature that helps new boaters find local, active, and welcoming boating clubs or social groups

• Provide short and quick YouTube videos that provide quick summaries of key boat types, ownership costs, and features

Further implications are detailed within the individual Target Cluster profiles in the Futureproofing section.

Profiles of who they are today, their needs and motivations

People who currently own at least one boat

RECENT BUYERS

People who may be interested in owning a boat in the future

INEXPERIENCED TIME-PRESSED COST-CONSCIOUS

Purchased their main boat prior to 2020

Focus for..

Dealers

Purchased their main boat after 2020

Fewest barriers experienced; ready to buy

Focus for..

OEMs Discover Boating

Dealers OEMs

Have the means, but feel they need more experience, support and knowledge

Focus for..

Dealers OEMs

Discover Boating (Handoff)

Core barrier is lack of time; open to alternative access models interested, but are not as financially ready; open to alternative access models

Focus for..

Discover Boating

*A fifth Prospective Owners cluster, Priced Out, is excluded due to it being a low-opportunity target

Focus for..

Discover Boating

There are two main segments of Current Owners, distinguished by how recently they purchased a boat

Purchased their main boat prior to 2020

Purchased their main boat after to 2020

Purchased their main boat between 2021-2023

TWO YEARS BUYERS

Purchased their main boat between 2024-2025

Recent First Time Buyers (40%) are more likely to use Inland lakes than RepeatBuyers

Almosthalf of More Recent Buyers (Past Two Years) are more likely to use their boats forWatersports and Entertaining Guest or Clients

Not enough free time

Health or age-related reasons

Effort of preparing boat for use and cleaning after Unpredictable weather

Ongoing costs of fuel

Ongoing costs of maintenance

Finding other people to go with me

Ongoing costs of insurance

Stress and responsibility of being the primary operator Ongoing

A prevailing theme across all Boat Owners is ‘the water gene,’ suggesting that exposure and experience to boating and water correlate with ownership

Outdoor Activities

A Desire to be on the Water Boating-adjacent Activities Childhood Experiences

Engagement with boats via charters and rentals jumps from 17% to 27% among 2020 vs 2024 Buyers and is significantly higher among Prospects

Such as paddle boarding, fishing, canoeing or kayaking are more common among Owners

Specifically skiing, snowboarding, rock climbing, backpacking are more common among Owners

Buyers who purchased post 2020 are more likely to say they had frequent exposure as a child and have some of their best memories on the water

But exposure to the water gene does not have to be through your immediate family nor childhood – it can also come from friends or outdoor

Base: Established Owners (n=82), Recent Buyers (n=418) QD3. Still thinking about your childhood and teenage years, how often, if at all, did you go boating in the following ways?

shows need to as well. They are no longer a place

for brokering deals, but an opportunity for enthusiasm, experience, and

63% of Established Owners have attended a boat show BOAT SHOW

A wide selection of boats and brands

A wide range of price points, including affordable options

Showcases of the latest technology and innovations A fun, family-friendly atmosphere Easy access to dealers for pricing and financing information A

Educational seminars and learning opportunities

On-water experiences and test drives

Perceptions Wants

69% of Recent Buyers have attended a boat show

About the same % of First Time Buyers have also attended

Showcases of the latest technology and innovations A fun, family-friendly atmosphere

A wide selection of boats and brands A wide range of price points, including affordable options Easy access to dealers for pricing and financing information Educational seminars and learning opportunities A low-pressure, relaxed environment

On-water experiences and test drives

Perceptions

Wants

Online purchases were even more common Past Two Years Buyers (27%), and Recent Repeat Buyers (25%)

Past Two Years Buyers are looking a dealer that has the specific boat brand they are looking for (41%) vs. 27% among Less Recent Buyers.

The

increased price of boat ownership is evident with Recent Buyers spending almost 30% more on a vessel in the past 5 years, and over double annually

$50,000-$74,999

$75,000-$99,999

$100,000-$149,999

$150,000-$249,999

$250,000-$499,999

$500,000+ I

Agree Agree

Agree

Disagree Disagree Strongly Disagree

Buyers prioritize knowing and having the ‘latest and greatest’, more so than Established Owners, and demonstrate significant comfort buying online

-T2B% (Definitely/Tend to Agree)-

I tend to spend time researching products and services before purchasing.

I enjoy keeping up with the latest news and developments in boating and sailing. I prefer products made in my own country. I would rather buy from a company that actively supports my community even if it would be more expensive to.

prefer vehicles that

Established Owners

Recent Buyers

In addition to comfort buying online, Recent Buyers are generally more ‘online’ than Established Owners – especially on social media

Established Owners

Recent Buyers

-T2B% (Definitely/Tend to Agree)-

Social mediahelps me connect with people with similar interests.

I regularly follow the social media posts of brands or companies that I'm interested in.

I check social media to see what others are up to, but do not post much myself.

I am constantly using social media to learn.

My online identity is an important part of who I am.

I rely on social media news to keep me informed.

I tend to believe a post on social media if it is shared by one of my friends.

Social mediaputs me in a better mood.

I'm uncomfortable with receiving ads in my social media feeds.

Social mediais a waste of time.

Purchased their main boat prior to 2020

RECENT BUYERS Focus for..

People who currently own at least one boat OEMs Discover Boating

Purchased their main boat after 2020

People who may be interested in owning a boat in the future

Fewest barriers experienced; ready to buy

Have the means, but feel they need more experience, support and knowledge

Dealers OEMs

Core barrier is lack of time; open to alternative access models interested, but are not as financially ready; open to alternative access models Dealers OEMs

*A fifth Prospective Owners cluster, Priced Out, is excluded due to it being a low-opportunity target

There are 3 key themes that represent the fundamental mindset of the Prospective Owner; understanding these can help prepare for tomorrow

1

2

3

Whether affluent or not, all prospects are concerned about their own particular financial situation and how boating can be affordable for them

For most prospects, there are appealing alternative models for gaining access to on the water experiences

Similar to the changes observed among Recent Buyers, Prospects demonstrate interest and use of new touchpoints and key considerations for making a purchase

Owners tend to be younger, have a lower income and are less educated than Current Owners, but have a similar distribution of discretionary income

highlight their different needs,

of the 5, all except the ’Priced Out’

These prospects are in their 40s-50s and live in the south. Their desire for a boat is high but they feel strapped for time – uncertain if it is worth the investment. We need to maintain engagement and connection to the sport through alternative models until they are ready to buy or consider other avenues for monetizing the experience.

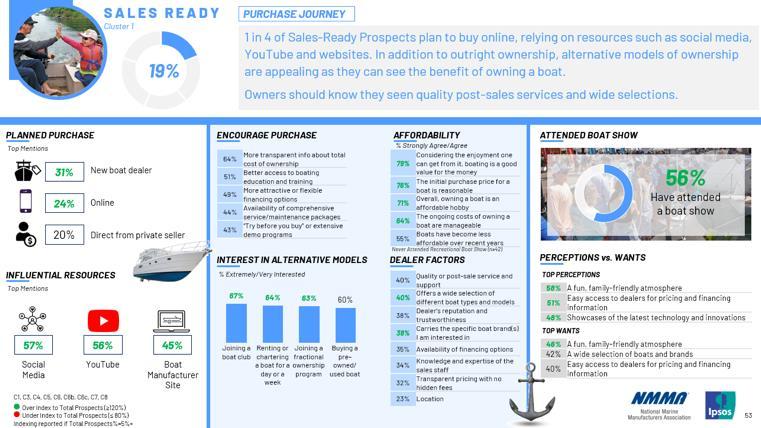

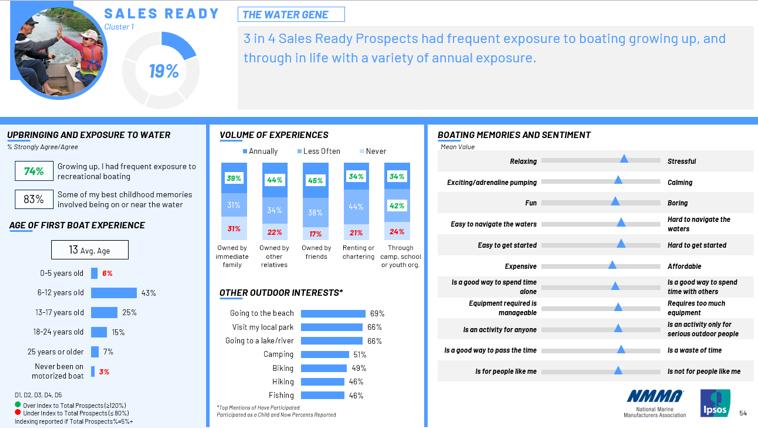

19%

These prospects are Millennials with kids in the West– they have the money and want to buy in the next 1-2 years. They are familyfocused, so conversations should highlight the family-friendliness of the sport and also provide them with a mix of boat options.

18%

These consumers have the desire but are further-out financially from being able to buy. They are in their 30s-40s and skew multi-cultural, and are concerned about all financial aspects of ownership, making alternatives to outright owning attractive ways to provide exposure and access.

These prospects are younger and multicultural, living in the south and northeast. They are beginners – and still too inexperienced to buy; our opportunity is to maintain connection with them, providing access to boating in alternative ways –educating them and keeping them involved until they are ready to buy.

Overview: Demographics, budget, knowledge level, readiness and barriers to purchase

Purchase Journey: How and who they plan to buy from, information sources, purchase motivations, boat show perceptions, etc.

Attitudes & Insights: General attitudes and values, top interests, etc. In the appendix, you will

Milestones & Media: Milestones achieved, and social media behavior usage & attitudes, etc.

The Water Gene: Exposure to water, age of first boat experience, how often, outdoor interests, boating memories, etc.

How are the expectations and needs of these prospects likely to change in the next 3 years?

The world has changed significantly in recent years, and will continue to shape the needs and expectations of consumers and our Target Boaters

We identified three key Macro Forces that will shape the world of tomorrow

Macro Forces and its resulting Drivers of Change

Increasing Cost of Living and Fragmented Labor Market

Economic Optimism and Luxury Spending 3. Changing Definition of Ownership 1. Growing Diversity and Generational Shift 2. Value Reprioritization and Delay in Traditional Milestones 3. Mindful and Purposeful Living

Increased Digital Usage in All Aspects of Life 2. Openness to New Technology 3. Social Media as a Source of Influence

With rising living costs and a fragmented labor market, consumers are growing more cautious with their spending

Decrease in points for U.S. Consumer Confidence Index as of March 2025, its lowest level since January 2021

Percentage of U.S. adults who said they spent more on experiences in the past year vs. they did in the year before

Percentage of U.S. consumers who state inflation as their main worry, standing as the country’s most pressing concern

Increase in the U.S. resale and thrift market (USD $56 billion) up from ~USD $49 billion in 2024, suggesting that consumers seek for value in their purchases

CBS News, March 2025

Morning Consult, 2025

Ipsos What Worries the World, September, 2025

2025

With global economics driving up the cost of everyday goods and housing prices outpacing wage growth, U.S. consumers are feeling the financial squeeze, leading to more cautious, value-driven spending habits amidst an uneven job market.

Financial realities are fueling a widespread “live for today” sentiment where consumers, feeling powerless over their future, channel a YOLO (You Only Live Once) mindset into spending on immediate experiential rewards like travel and dining.

Access is overtaking ownership as consumers rethink what it means to “have” something. From rentals to subscription models, low-commitment flexibility (cost, time, energy) and convenience now define modern value over ownership, driven by new economic and social pressures.

Amidst the financial pressure, adjusted consumer spending is fueling the demand for accessible, experience-driven boating

As rising costs and job insecurity squeeze discretionary income, new boat sales are softening as consumers become highly selective. Boat buyers may prioritize value and utility as they look to maximize every dollar they spend..

As financial constraints push consumers to prioritize rewarding experiences over large asset purchases, the success of the boating industry will depend on strategically repositioning boating as an attainable luxury and emphasizing the instant gratification on the water.

As consumers seek low-commitment flexibility and convenience, sharedservice models open a new gateway to boating, providing accessible time on water without the significant financial and logistical commitment of ownership.

being reshaped by a more

Drop in 25-to-34-year-olds (vs. 1975) who achieved four most common milestones (moving out of parents’ home, working, married, with children), reflecting a bigger focus on economic security California, Hawaii, New Mexico, Texas, Nevada, Maryland, Georgia now have no racial or ethnic group forming a majority, signaling a “majority-minority” dynamic

Percentage of purchasing decisions women influence, with women’s median discretionary spending up 0.9% year-over-year, outpacing men and underscoring their growing economic power

The World Data, October 2025 Bank of America, Capital One, 2025

United States Census Bureau, 2025

Percentage of US and Canadian consumers who said they would pay more for products and services that are ethical and sustainable

Ipsos Conscious Consumer Report, 2025 Edition

diversity and changing life

are reshaping how Americans define identity, success, and their well-being

Social Reconfiguration: What does it entail?

Growing Diversity with Generational Changeover

1 Value Shift & Delay in Traditional Milestones

2

America is undergoing a demographic transformation, driven by generational shifts, increasing diversity, and international and urban migration. Gen Z and Millennials are actively reshaping cultural norms around identity, representation, and inclusion.

Consumers, especially those who are younger, are redefining success and stability. They are delaying marriage, homeownership, and parenthood in favor of financial security, personal growth, and flexibility.

3

Mindful Living and Spending

Consumers are becoming more intentional about how they spend their time, money, and energy, seeking products and experiences that align with their health, ethics, and environmental values.

The changing values and lifestyles present new avenues for boating to become more diverse, mindful, and inclusive across generations

The generational and demographic shift is redefining today’s boater from a traditional owner to a diverse and digital consumer. It is reshaping the industry to pivot towards lowered skill barriers, urban access, and to authentically champion diversity to capture the new growing market.

While delayed milestones free up discretionary income, this capital is less likely to translate into outright boat purchases. Instead, the consumer demand for financial security and flexibility is transforming the boating market, creating a structural shift from a focus on boat ownership to one centered on financial agility and flexible access models.

As consumers favor lifestyles prioritizing emotional well-being and restorative experiences, recreational boating can be repositioned as a way of “blue therapy” that offers mental clarity, sensory restoration, and sense of calm.

Technology has become essential to consumers’ lives, yet remains a doubleedged sword of innovation and apprehension

89%

Percentage of U.S. adults who say they are comfortable adapting new technology in daily life, suggesting that using technology has become second nature

Ipsos

42%

Percentage of U.S. consumers who used phones as part of their latest retail purchase, suggesting that phones have become central to the shopping experience

53%

Percentage of Gen Z who say socialvideo content is more relevant to them than traditional video content, with 50% saying they feel stronger connection to social-media creators than actors on TV

64%

Percentage of U.S. adults who say that products and services using AI make them nervous, while only 38% say it makes them excited

2025 Visa’s Global Digital Shopping Index: US Edition, 2025 The Ipsos AI Montor 2025

The rapid integration of AI is driving changes in how consumers perceive technology and what they expect to get from it

Tech-Celeration What does it entail?

Increased Digital Usage

Digital tools are now seamlessly integrated into every facet of consumer life, creating an expectation for instant, mobile access for everything from communication and transactions to information gathering via smart devices and apps.

2

As technology becomes woven into daily life, consumers are more willing to adopt it across work, leisure, health, and home. Growing comfort is speeding up adoption, and expectations for efficiency and personalization are rising, though trust concerns remain.

3

Influence

Social platforms have evolved into powerful discovery engines, shaping opinions and driving purchases. Authenticity, creator credibility, and community validation now matter more than traditional advertising. Consumers are increasingly relying on peers, influencers, and independent creators to make sense of the world around them.

Consumer demand for accessible boating brings the need for the industry to effectively balance digital utilization with authenticity

Tech-Celeration What does this mean for all Target Boaters?

Increased Digital Usage

The pervasive use of digital tools creates a consumer expectation for a seamless digital journey across all touchpoints, from initial research to the moment of purchase and ownership. Consumers now demand a fully connected and intuitive experience, from online platforms to the moment they are on the water.

2

As digital technology rapidly evolves, consumers (especially younger generations) are seeking a boating experience that integrates technology to solve friction points (e.g., assisted docking, intuitive navigation) and helps make the experience safer, easier, and more accessible.

3

Social Media as a Source of Influence

Social media has evolved into a primary channel where consumers go for product information, serving as a key source of inspiration, education, and sales for boating. It is now a platform where authentic storytelling can be strategically used to connect the industry with the consumer base.

What do these Macro Forces mean for our Targets and how we connect with them?

To understand how to better connect with our Target Boaters in the next 3 years, we analyzed each prospective boater target through the lens of the Macro Forces

Each futureproofing profile features:

Target Overview: One-page snapshot for each target, showing selected survey data points organized by how they align with each of the three macro forces

Target x Macro Force Analysis: Likely impact of a macro force on each target - how each target consumer behaves and what it means for tomorrow

Ways to Connect: Actionable recommendations detailing who acts (DB, Dealers, OEMs), what to do, and how to engage the target boater, for each Macro Force

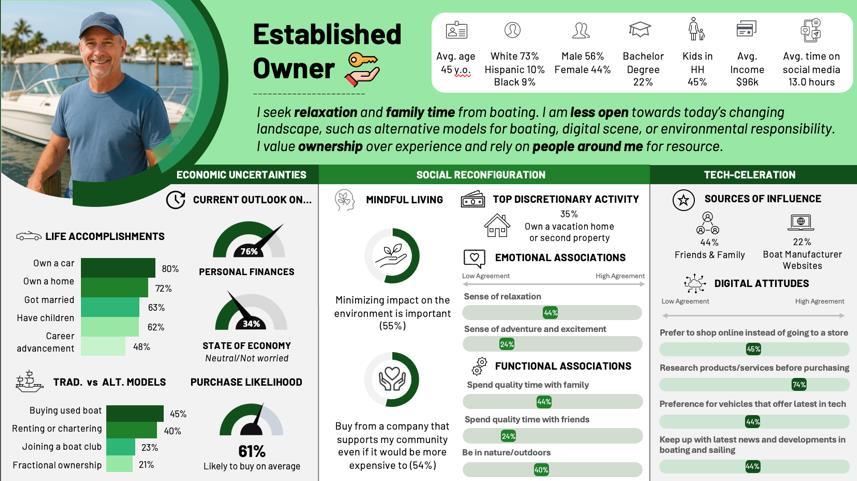

I seek relaxation and family time from boating. I am less open towards today’s changing landscape, such as alternative models for boating, digital scene, or environmental responsibility.

I value ownership over experience and rely on people around me for resource.

the environment is important (55%)

from a company that supports my community even if it would be more expensive to (54%) SOURCES

Manufacturer Websites

Prefer to shop online instead of going to a store

Researchproducts/services before purchasing

Preference for vehiclesthat offerlatest in tech

Keep up with latest news and developments in boating and sailing

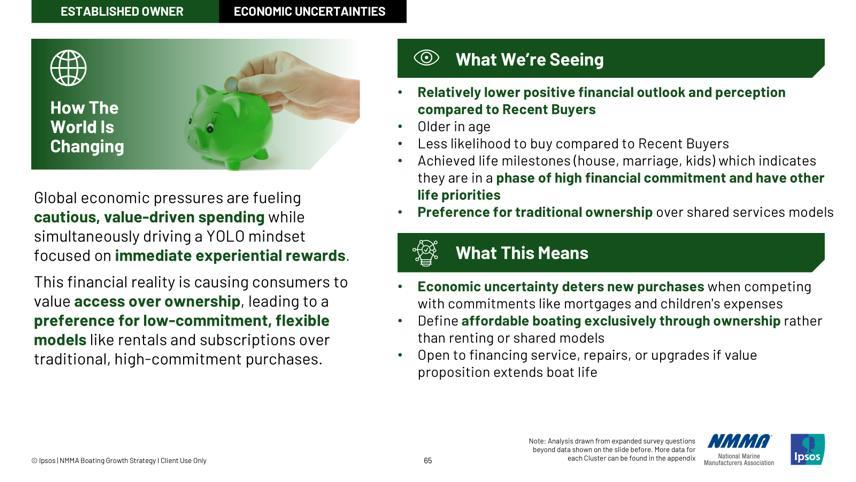

Global economic pressures are fueling cautious, value-driven spending while simultaneously driving a “-Live-Once” mindset focused on immediate experiential rewards

What We’re Seeing With This Target

• Relatively lower positive financial outlook and perception compared to Recent Buyers

• Older in age

• Less likelihood to buy compared to Recent Buyers

• Achieved life milestones (house, marriage, kids) which indicates they are in a phase of high financial commitment and have other life priorities

• Preference for traditional ownership over shared services models

• Economic uncertainty deters new purchases when competing with commitments like mortgages and children’s tuition

• Define affordable boating exclusively through ownership rather than renting or shared models

• Open to financing service, repairs, or upgrades if value proposition extends boat life

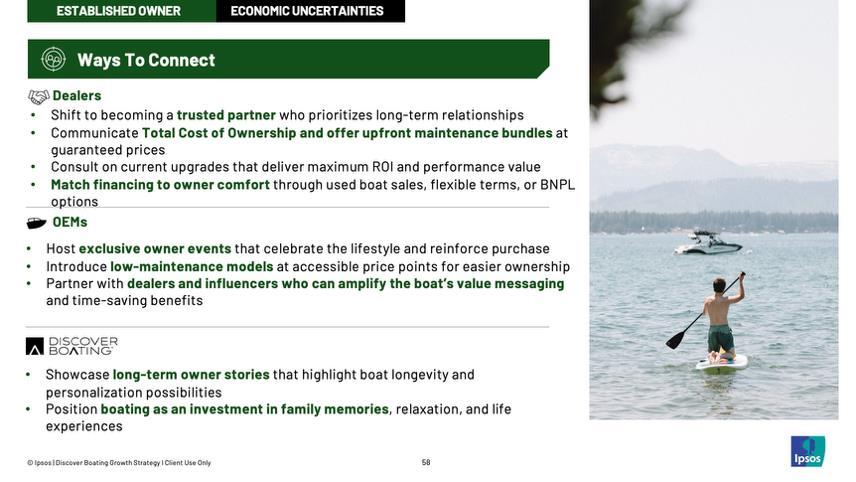

• Shift to becoming a trusted partner who prioritizes long-term relationships

• Communicate Total Cost of Ownership and offer upfront maintenance bundles at guaranteed prices

• Consult on current upgrades that deliver maximum ROI and performance value

• Match financing to owner comfort through used boat sales, flexible terms, or BNPL options

• Host exclusive owner events that celebrate the lifestyle and reinforce purchase

• Introduce low-maintenance models at accessible price points for easier ownership

• Partner with dealers and influencers who can amplify the boat’s value messaging and time-saving benefits

• Showcase long-term owner stories that highlight boat longevity and personalization possibilities

• Position boating as an investment in family memories, relaxation, and life experiences

Driven by generational and demographic shifts, America is seeing cultural norms being redefined around identity and inclusion.

Younger consumers are delaying major milestones in favor of financial security and flexibility, becoming intentional spenders who prioritize products and experiences aligning with their health, ethical, and environmental values.

• Traditional demographics (skew older, white), with preference for home ownership over experiences

• Around average consensus that reducing environmental impact matters

• Core motivations are centered around relaxation, family, and nature

• Industry pivot towards more diverse consumers and urban access may be less relevant to them

• Core motivations are well aligned with industry’s messaging around “blue therapy”, focused on emotional well-being

• While not the primary drivers of ethical and environmental values, they are aware of their role as stewards of environment

• View boat shows as an extension of validating the sense of relaxation they seek from boating

• Host small, local, family-focused gatherings (e.g., dock parties) that build a sense of exclusive, close-knit community that create opportunities for owners and their friends & families to connect

• Clearly present boat options tailored to their desire for experiences that include relaxing time in nature, with family, and being outdoors

• Offer services and features that cater to multi-generational use (e.g., open layouts, accessibility features, new electronics or accessories)

• Ensure product communication continues to emphasize the practical utility, family experiences, and time in nature that established owners value most

• Develop content and videos that tie back to their core motivations (e.g., relaxing time in nature, with family, and being outdoors)

• Position boating as a meaningful way for the next generation to connect with nature

• Develop owner spotlight campaigns that highlight personal stories around family traditions, favorite cruising routes, and the restorative value of time on the water

• Design boat show experiences to feel low-pressure, relaxed, and owner-centric

Digital tools are now seamlessly integrated into consumer life, driving an expectation for instant, mobile access and increased adoption across all sectors.

This has elevated expectations for efficiency and personalization. Social platforms have also evolved into powerful discovery engines where community validation now drive purchases and shape opinions more than traditional advertising.

• Low engagement with social media and reliance on traditional sources

• Friends and family play a big role in source of influence, and prefers them over other online resources or boat manufacturer's website

• Likely to research products and services before purchasing

• More likely to shop in store than online

• Less inclined to be enticed by the latest and greatest in tech, even in boating

• Digital friction can deter boat purchases

• May miss out on product information and inspiration as it becomes harder to reach through primary social channels

• More likely to be influenced by community and validated experiences from peers than digital channels

• Advanced boat features are not a priority for them

• Provide a consistent, seamless experience across digital and physical channels, ensuring all critical product information is easy to find wherever customers engage

• Assess their digital comfort level and offer personalized, one-on-one training to help them navigate the new tech features on boats in a meaningful way

OEMs

• Develop standardized digital assets (e.g., video tutorials, interactive calculators) for dealers to use in the research phase of the purchase journey

• Position new boat tech features as enablers of efficiency, safety, and connectivity

• Provide Word-of-Mouth referral programs that reward established owners for bringing in friends or family

• Do not underestimate the continued importance of trusted, non-digital channels such as in-person events, magazines, direct mail, personalized emails, and dealerships

• Leverage the power of existing owners by hosting events such as owner testimonials that introduce people into boating

I seek for both relaxation and adventure from boating. I am more open towards today’s changing landscape, such as alternative models for boating, digital scene, or environmental responsibility. I am more heavily influenced by social media and online than people around me.

Minimizing impact on the environment is important (74%)

Buy from a company that supports my community even if it would be more expensive to (75%)

Prefer to shop online instead of going to a store Researchproducts/services before purchasing

Preference for vehicles that offer latest in tech

Keep up with latest news and developments in boating and sailing

Global economic pressures are fueling cautious, value-driven spending while simultaneously driving a “-Live-Once” mindset focused on immediate experiential rewards

• Relatively positive financial outlook and perception (higher than Established Owners)

• Prioritize traditional milestones like parenthood, while also valuing career advancement and international travel

• Higher likelihood to purchase compared to Established Owners, but also open-minded towards alternative models

• Despite their relatively positive outlook, economic pressure may impact financial confidence and make them hyper-aware of the Cost of Ownership, requiring them to find justification for their investment

• Will expect the boat to deliver high-reward, low-hassle experiences, whether they’re investing in a new purchase or exploring shared-access options

• Likely to be early adopter of changing access models

• Improve transparency through clear service and maintenance plans that offer a fixed, predictable cost for routine maintenance

• Increase touchpoints with recent buyers to reinforce confidence in their vessel and maintenance plan, offering advice and reassurance—including guidance on used boats and alternative models when appropriate

• Leverage loyal owners as brand advocates and micro-influencers, turning their experiences into authentic touchpoints to engage recent buyers before and after their purchase

• Offer transparent pricing, flexible financing options, and strong warranties to make purchase process feel more manageable

• Offer educational content and guidance on how different boat models can enable new experiences, encouraging owners to explore ways to enjoy boating beyond what they currently have

Driven by generational and demographic shifts, America is seeing cultural norms being redefined around identity and inclusion. Younger consumers are delaying major milestones in favor of financial security and flexibility, becoming intentional spenders who prioritize products and experiences aligning with their values.

• More diverse in demographics (higher share of Hispanics, Black compared to the Established Owners)

• Values sustainability and environmental responsibility

• High willingness to pay more for brands that align with their values

• Views boating as balanced mix of relaxation, adventure, and social connection

• Likely to expect greater diversity in marketing, boating communities, and dealership representation

• Messages highlighting sustainability, local community impact, and ethical practices serve as key differentiators

• Core motivations align closely with the industry’s “blue therapy” messaging, emphasizing emotional well-being

• Place greater emphasis on cultural competency for staff training, and look to reflect the growing diversity of the consumer base in sales floor staff

• Collaborate with local organizations and provide owners opportunities to engage (e.g., small percentage of service fees going to a local water preservation group)

• Demonstrate transparency and authentic commitment through active community involvement and clear, consistent communication

• Offer educational content on eco-friendly options, highlighting sustainable brand practices and environmentally conscious options (e.g. electric motors)

• Identify social media influencer partnerships that authentically represent the brand and engage diverse audiences

• Expand content showcasing diverse types of families and individuals enjoying boating lifestyle

• Create content that resonates with motivations around adventure, relaxation, and nature (e.g., “blue therapy” wellness retreats, eco-tours)

Digital tools are now seamlessly integrated into consumer life, driving an expectation for instant, mobile access and increased adoption across all sectors.

This has elevated expectations for efficiency and personalization. Social platforms have also evolved into powerful discovery engines where community validation now drive purchases and shape opinions more than traditional advertising.

• Digital adopters who value technology and prefer vehicles and boats equipped with the latest features

• Active online and on social media

• Social media, websites, and online reviews are top information sources

• Prefers to shop online than in store

• Expect to use digital channels for their consumer journey, from research to moment of purchase

• Likely to be highly informed as they receive information related to boating online and from social media

• More likely influenced by digital channels compared to off-line

• Expect instant, mobile-optimized information and efficient, personalized interactions

• View boat technology as a necessary component for safety, connectivity, performance

• Respond quickly and professionally to all feedback across digital channels

• Ensure the digital experience is seamlessly connected to the in-person journey, and be prepared to engage highly informed customers

• Clearly highlight boats with advanced, integrated technologies, emphasizing how these features serve as meaningful upgrades to their existing boats

• Make sure websites are up-to-date with extensive photo galleries and video tours of boats and new features

• Strategically partner with influencers or online sources beyond the boating world (e.g., tech YouTubers) to gain more visibility and interest to new boat models

• Utilize digital platforms (e.g., short-form video (Instagram reels/TikTok) for quick tips, YouTube for in-depth reviews/safety guides

• Create online forums and communities where recent owners can connect

Although I am younger, I have a relatively positive outlook on both my personal finance and the current economy. I’ve achieved many milestones, and I am open towards different alternative models boating offer. I am very active on social media and get most of my resources from there.

Minimizing impact on the environment is important (68%)

Buy from a company that supports my community even if it would be more expensive to (74%)

Other cultures enrich our society (63%)

Prefer to shop online instead of going to a store

Researchproducts/services before purchasing

Preference for vehicles that offer latest in tech

Keep up with latest news and developments in boating and sailing

Global economic pressures are fueling cautious, value-driven spending while simultaneously driving a “-Live-Once” mindset focused on immediate experiential rewards.

• Relatively positive financial outlook and perception (highest among all prospect groups) but high cost of ownership is biggest point of hesitation

• Achieved many life milestones, approximately 2 in 3 have kids

• High likelihood to purchase but also open-minded towards different shared services models

• Shows the highest likelihood to purchase among all prospect groups

• Highest average income among all prospect groups

• Likely in a financially-stable state of life where they are able to enjoy boating

• Boats are the last major discretionary commitment after achieving milestones, and will seek to get the most value out of the purchase

• Likely to be early adopter of changing access models

• Financially ready to purchase a boat but resources on lower financial entry points will help

• Offer simple, transparent materials and consultations that break down Total Cost of Ownership

• Provide information on financing (e.g., affordable monthly payment) so they can gain confidence in moving towards act of purchase

• Promote used, certified pre-owned models as an alternative to new boat purchase

• Communicate boating as an activity that can be enjoyed within a moderate budget

• Create content that reframes the cost of a boat against the rising costs of competing family activities to highlight the value gained from time on the water

• Sell the family experience, connecting the boat directly to their achieved milestones and making great memories with kids, relatives and friends

• Extend invitations of select owner meet-ups where current owners address concerns and showcase the lifestyle and community awaiting them

Driven by generational and demographic shifts, America is seeing cultural norms being redefined around identity and inclusion.

Younger consumers are delaying major milestones in favor of financial security and flexibility, becoming intentional spenders who prioritize products and experiences aligning with their health, ethical, and environmental values.

• Skews White compared to other prospect groups

• Youngest demographics among all prospect groups

• Values sustainability and environmental responsibility

• Willing to pay more for brands that align with their values

• Exhibits highest spend on experiences and travel among all prospect groups

• Many, as young parents, will likely look for ways boating can offer fun family experiences with their children

• Demand information on sustainable boating, and sensitive to ecological footprint and ethical practices

• Seek Dealers/OEMs that demonstrate proactive commitment to local conservation and ethical community engagement

• View recreational boating as an immersive experience they can have, rather than something they own

• Provide personalized, dealer-curated guides to local low-impact cruising areas or nature preserves

• Create resources to help them research boat brands that have transparent, environmental and ethical commitments

• Host local, family-focused gatherings (e.g., dock parties for prospective boaters) that give families opportunities to connect and engage

• Place greater emphasis on the experience of being on water over being a boat owner

OEMs

• Provide resources on how boating can be enjoyed in sustainable ways

• Use articles and visuals that connect boating directly to mental health, stress reduction, and digital detox

• Actively promote boats designed for enjoyable family and kid-friendly experiences

Digital tools are now seamlessly integrated into consumer life, driving an expectation for instant, mobile access and increased adoption across all sectors. This has elevated expectations for efficiency and personalization. Social platforms have also evolved into powerful discovery engines where community validation now drive purchases and shape opinions more than traditional advertising.

• Digital adopters who value technology and prefer vehicles equipped with the latest features

• Active on social media, with highest social media usage among all prospects

• Social media and YouTube are top information sources and get influenced from them

• Regularly follows social media posts of brands or companies of interest, as well as latest news in boating

• Expect to use digital channels for their consumer journey, from research to moment of purchase, and expect it to be fast, mobile-friendly, and transparent

• Social media and YouTube are not just a research engine, but also a virtual showroom and tool for validation

• View technology as a core part of boat’s value proposition

• Content creators and YouTubers are highly influential to this cluster

• Ensure the digital experience is seamlessly connected to the in-person journey with live chat, linked social media, text communication, online appointments, and transparent pricing

• Invest in professional video walk-throughs (both short-form and long-form) of highinterest models so they can visualize every element of them

• Develop highly engaging, mobile-friendly website tools that allow users to easily compare models or guide them to the best fit for their needs (e.g., a fun interactive assessment)

OEMs

• Strategically partner with influencers on social media and post videos on YouTube to gain more visibility and interest

• Maintain an active social media presence, being selective with content to ensure it accurately reflects brand values and resonates with their focus on family time and immersive experiences

• Offer immersive digital experiences of boat interiors and exteriors, and invest in professional video walk-throughs of high-interest models, allowing potential buyers to fully explore and experience the boats before visiting the dealership to satisfy their research needs

I have a moderate outlook on both my personal finance and the current economy. I value different cultures and rely on my friends and family more than the digital sources. Although I have interest in boating, I lack experience and knowledge.

Minimizing impact on the environment is important (57%)

Buy from a company that supports my community even if it would be more expensive to (51%)

Other cultures enrich our society (65%)

Prefer to shop online instead of going to a store

Researchproducts/services before purchasing

Preference for vehicles that offer latest in tech

Keep up with latest news and developments in boating and sailing

Global economic pressures are fueling cautious, value-driven spending while simultaneously driving a “-Live-Once” mindset focused on immediate experiential rewards.

• Relatively positive financial outlook and perception (on par with other prospect groups)

• Lower income level and lower percentage of those with bachelor’s degrees

• Experience is the main barrier when it comes to ownership, but cost of entry is also a challenge with the lower income

• High likelihood to purchase but also open-minded towards different shared services models

• With the lack of experience and lower income, shared service models provide a risk-free gateway to address their two biggest concerns

• Hands-on exposure or trial opportunities (rentals, boat clubs, test rides) will be crucial for them to build confidence –particularly where education and instruction are offered

Note:

• Focus on guiding them through used and affordable boats that provide lower initial investment but bring them into the category

• Host fun and low-commitment local on-water events that give them a firsthand taste of the boating experience

• Serve as a trusted financial and educational mentor by offering clear, easy-tounderstand resources, such as working with dealers to offer a first-time boater safety kit, on-water training, and a step-by-step ownership and financial guide

• Normalize access as an important steppingstone to becoming a boat owner

• Offer an interactive online calculator or comparison tool that clearly shows the financial tipping point where ownership becomes more cost-effective than a boat club or rental model

• Provide clear, non-intimidating information or videos that break down financial steps to becoming a boater (e.g., “Budgeting for Boating Life”)

Driven by generational and demographic shifts, America is seeing cultural norms being redefined around identity and inclusion. Younger consumers are delaying major milestones in favor of financial security and flexibility, becoming intentional spenders who prioritize products and experiences aligning with their health, ethical, and environmental values.

• More diverse in demographics (higher share of Black and Hispanics across all prospects)

• Experience followed by cost are the key barriers to boat ownership

• Environmental or ethical responsibility falls slightly lower than the average of prospect clusters

• High percentage recall boating or have impressions of boating being a way to spend time alone

• Will likely want to see more diverse representation in the boating landscape (across boat shows, dealers, marketing content, etc.)

• Environmental and ethical messages are not as relevant to them compared to other clusters, and the decision is driven more by practicality, safety, and personal relevance

• Boating should be positioned as a flexible, welcoming activity that fits diverse cultural norms and social gatherings

• Offer introductory boating and safety courses in accessible local areas, open to anyone interested in getting into boating

• Place greater emphasis on cultural competency on staff training, and actively ensure dealership teams reflect the growing diversity of the consumer base

• Use simple and easy-to-understand language to explain features, emphasizing why they matter, not just how they work

OEMs

• Serve as confidence builders and offer introductory courses on boating skills and safety such as on-water training sessions, and a step-by-step ownership guide

• Ensure different demographics are represented in marketing communications and campaigns

• Create a feature that helps new boaters find local, active, and welcoming boating clubs or social groups

Digital tools are now seamlessly integrated into consumer life, driving an expectation for instant, mobile access and increased adoption across all sectors.

This has elevated expectations for efficiency and personalization. Social platforms have also evolved into powerful discovery engines where community validation now drive purchases and shape opinions more than traditional advertising.

• Relatively open to technology, showing similar level of interest with other prospect groups

• YouTube is the one of the top sources of information, but still value friends & family as an important resource

• Lowest social media usage among all prospects

• Feels equally comfortable shopping online and in-person

• Likes to research products or services before purchasing, including the latest tech developments

• YouTube is an essential educational platform and tool

• Views technology as a nice-to-have, rather than the main deciding factor for purchase

• Digital and mobile experiences must reinforce the trust they get from friends and family and still provide the personal validation they need

• Ensure digital experience is seamlessly connected to the in-person journey, allowing them to switch between the method they feel most comfortable with

• Host in-person events and share YouTube and social content where loyal customers discuss their first-time experiences to reinforce trust

• Strategically collaborate with YouTubers to create engaging content such as “A Day in the Life of a Boater” or “Boating 101 tutorials” that feature different boats

• Ensure all educational content on the website and YouTube is designed for quick social sharing for easy validation with the trusted network

• Provide authentic testimonials that feature new boaters, so the content feels relevant for them

I have a relatively positive view towards both my personal finance and the economy. Although I have interest in boating, time is an issue for me. I rely on my friends and family more than the digital sources.

Minimizing impact on the environment is important (61%) Buy from a company that supports my community even if it would be more expensive to (69%)

cultures enrich our society (67%)

Prefer to shop online instead of going to a store

Researchproducts/services before purchasing

Preference for vehiclesthat offerlatest in tech

Keep up with latest news and developments in boating and sailing

Global economic pressures are fueling cautious, value-driven spending while simultaneously driving a “-Live-Once” mindset focused on immediate experiential rewards.

• Relatively positive financial outlook and perception (relative to other prospect groups)

• Oldest in age among all prospect groups

• Average for both likelihood to purchase and openness towards different alternative models

• Accomplished major traditional life milestones, especially those that require high commitment like car ownership and raising a family

• Time-poor individuals who are hyper-aware of the longer-term costs associated with boat ownership beyond the purchase price

• Ease of use, convenience, and streamlined experience will be the most important for them

• Will likely view alternative models as ways to get time on water without administrative commitment of ownership

• Validate the investment by creating compelling content that positions boating as efficient, guaranteed way to spend high-quality time with family and friends

• Provide simple guides that help them navigate best course of action based on time-for-cost ratio on expected usage

• Deliver experience over logistics by shifting the focus on what they can get from boating

• Introduce more content on boat clubs, fractional ownership, and rentals that allow for flexibility and lower commitment

Driven by generational and demographic shifts, America is seeing cultural norms being redefined around identity and inclusion. Younger consumers are delaying major milestones in favor of financial security and flexibility, becoming intentional spenders who prioritize products and experiences aligning with their health, ethical, and environmental values.

• High willingness to purchase from a company that supports their community

• Time is the main barrier when it comes to ownership

• Around average when it comes to environmental or ethical responsibility compared to other prospect groups

• High percentage claim that some of best childhood memories involve being on or near the water, and have impressions of it being associated with excitement and fun

• Will seek for high emotional ROI as every experience on water matters with limited time

• Will likely buy a boat from a brand with aligned personal values

• Will likely seek for the boating life as long as time allows, since they have positive memories associated with life on water

• Create content that focuses on high-end, low-effort social experiences on a boat

• Publish community-driven narratives such as people who use their boats for charitable activities or mentorship, providing aspirational examples of how to combine their passion with their desire for social contribution

• Provide exciting pre-planned itineraries and guide on how to enjoy boating (e.g.,

Thrill & Chill: A Guide to Boating Experiences) that eliminate the time barrier

• Provide time-efficient education or quick-read guides that are brief and concise

Digital tools are now seamlessly integrated into consumer life, driving an expectation for instant, mobile access and increased adoption across all sectors.

This has elevated expectations for efficiency and personalization. Social platforms have also evolved into powerful discovery engines where community validation now drive purchases and shape opinions more than traditional advertising.

• Relatively open to technology and prefer vehicles equipped with the latest features

• YouTube is the one of the top sources of information, but still value friends & family as important resource

• Actively researches products and services before purchasing

• Tries to keep up with latest news in boating

• YouTube is very important educational tool

• Likely view technology on the boat as ways to make things efficient

• Digital and mobile experiences must reinforce the trust they get from friends and family and still provide the personal validation they need

• Integrate virtual tours and product comparisons to reduce friction in the decisionmaking process

• Provide short and quick YouTube videos that provide quick summaries of key boat types, ownership costs, and features

• Ensure all educational content on website and YouTube is designed for quick social sharing for easy validation via trusted networks of boaters and prospects

• Feature video testimonials from accomplished and busy professionals who discuss how boating improved their quality of life

• Collaborate with influencers or YouTubers who focus on practical, lifestyleoriented boating content (e.g., “A

Day in the Life of a Boating Family”)

I hold a more pessimistic view on my personal finances and the state of economy. Although I have interest in boating, cost is my barrier. I care about sustainability and minimizing impact on environment. I rely both on social media and people around me for resources.

Minimizing impact on the environment is important (67%)

Buy from a company that supports my community even if it would be more expensive to (61%)

Other cultures enrich our society (67%)

Prefer to shop online instead of going to a store

Researchproducts/services before purchasing

Preference for vehicles that offer latest in tech

Keep up with latest news and developments in boating and sailing

Global economic pressures are fueling cautious, value-driven spending while simultaneously driving a YOLO mindset focused on immediate experiential rewards.

What

• Less optimistic on the outlook of the economy

• Values career advancement (highest among all clusters, including owners)

• Average when it comes to likelihood to purchase, and open towards alternative models

• Financially-sensitive cluster with a majority owning a car

• Hyper-aware of the ongoing costs of maintaining a vehicle, likely to be calculated spenders

• Career-driven individuals who seek to maximize income/wealth, and boat expenditures will need to support this financial goal

• Will seek for transparent, low-cost options where the total cost is fully known upfront

• Offer easy-to-understand financial education, including budgeting tips for boating and comparisons of ownership vs. shared-access models

• Create step-by-step guides for first-time buyers that cover financing, insurance, and ongoing costs (e.g., fuel surcharge, late fees)

• Position ownership as a long-term financial goal but emphasize access as the necessary current solution for immediate enjoyment

• Create content that validates and celebrates boat clubs and rentals as the best first step for cost-conscious prospects

• Provide trial memberships for boat clubs or shared-access programs they can get through Discover Boating, or offer scholarships or discounts for first-time boaters in training courses or boating workshops to encourage them

Driven by generational and demographic shifts, America is seeing cultural norms being redefined around identity and inclusion. Younger consumers are delaying major milestones in favor of financial security and flexibility, becoming intentional spenders who prioritize products and experiences aligning with their health, ethical, and environmental values.

• High willingness to purchase from a company that supports community

• Cost is the main barrier when it comes to ownership

• Around average when it comes to environmental or ethical responsibility

• High percentage perceive boating as not being for people like themselves

• Since cost is the primary barrier and their ethical responsibility is average, they are likely to prioritize affordability and accessibility over premium eco-friendly features

• Given that financially pressed individuals often represent a wide array of racial background, inclusive representation may be important to them

• Will likely seek communication that makes them feel financially included

• Show boating as a lower-carbon footprint, higher-freedom form of travel compared to air travel and international trips

• Provide marketing and communications that emphasize inclusivity and belonging, showing that boating is for everyone, not just wealthy or experienced individuals

Digital tools are now seamlessly integrated into consumer life, driving an expectation for instant, mobile access and increased adoption across all sectors.

This has elevated expectations for efficiency and personalization. Social platforms have also evolved into powerful discovery engines where community validation now drive purchases and shape opinions more than traditional advertising.

What We’re Seeing With This Target

• Relatively open to technology

• Social Media is the top source of information

• Still value friends & family as important resource

• Actively researches products and services before purchasing

• Prefers to shop online than in-person

• What they see on social media has high influence on their perceptions and decisions

• Digital and mobile experiences must reinforce the trust they get from friends and family and still provide the personal validation they need

• Strategically partner with lifestyle influencers on social media who can share relatable experiences and demonstrate that boating is accessible

• Highlight diverse stories and testimonials on website and social media from boaters of different backgrounds and financial situations

• Publish short and concise educational content on social media that can easily be shared for validation with trusted network

Stephanie Don Vice President, Ipsos Market Strategy & Understanding

Rachel Kelley

Sr. Account Manager, Ipsos Market Strategy & Understanding

Jennifer Bender Associate Partner, Ipsos Strategy3

Andrew Ang Engagement Manager, Ipsos Strategy3

Rachel Song Consultant, Ipsos Strategy3