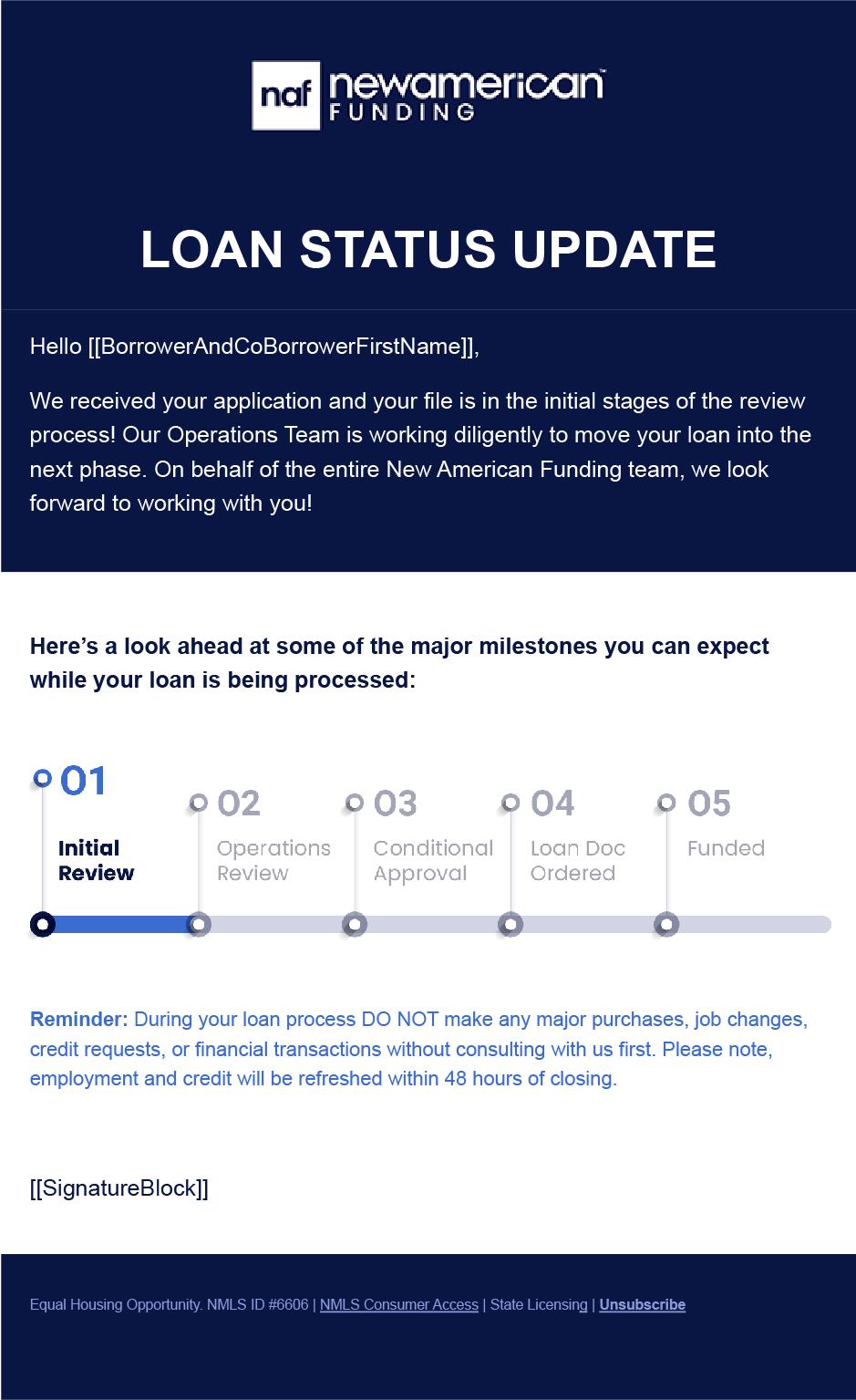

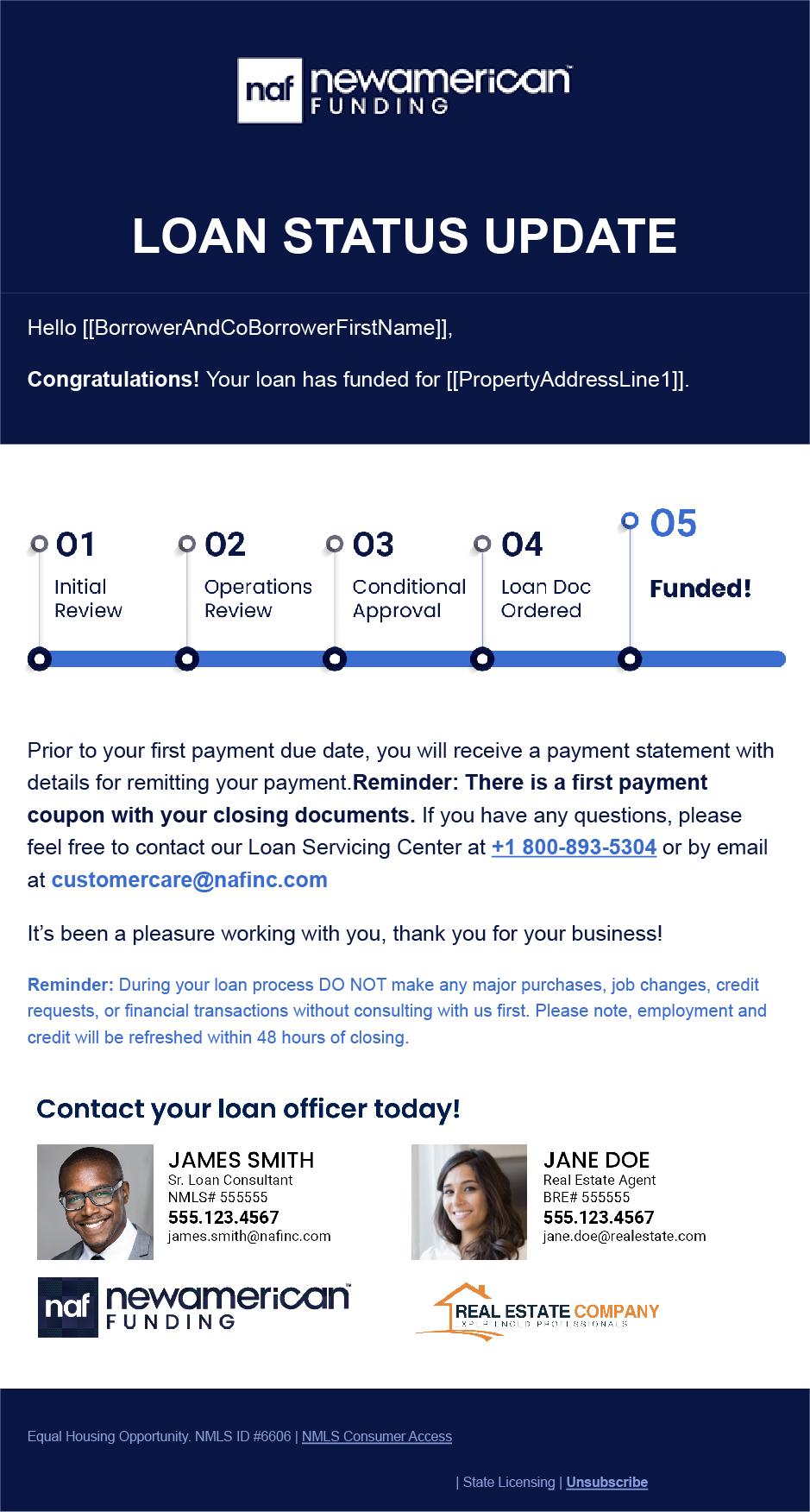

New American Funding keeps you top of mind with co-branded Loan Status update emails to keep the client in the loop every step of the way.

Co-branded closing cards are mailed to our mutual clients with information on how to download closing documents.

Personalized co-branded greeting cards sent to clients for years after a loan closes on birthdays, holidays and loan anniversaries.

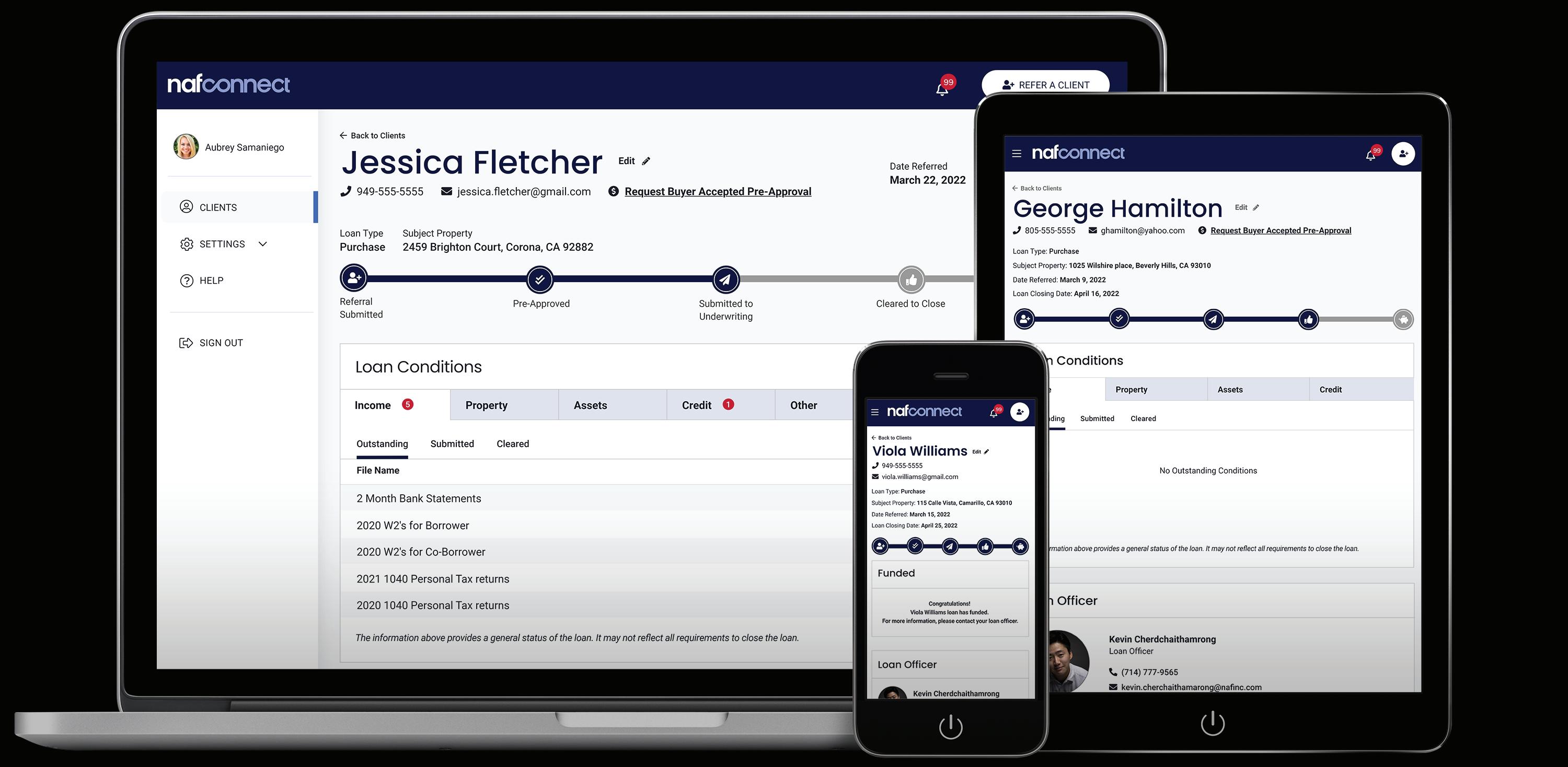

NAFConnect is a platform for Real Estate Agents (REA) to connect to NAF Loan Officers.

Help clients navigate the loan process and communicate with New American Funding.

View your client's loan status and receive notifications as it moves across key milestones.

See documents needed by the New American Funding processing team.

Generate, edit, and download pre-approval letters at the click of a button.

Receive notifications when new milestones are completed and watch real-time loan status updates to keep you and your client up-to-date on the status of their loan.

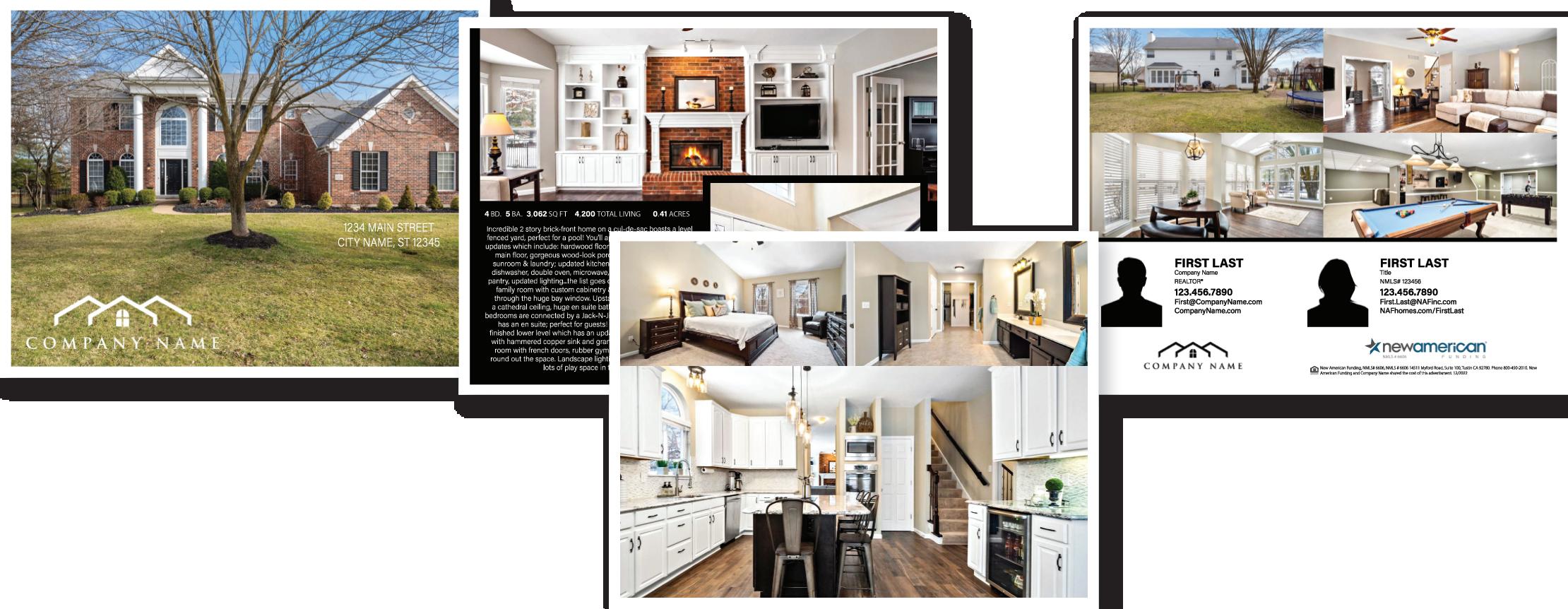

• Print Mail

• Doorhangers

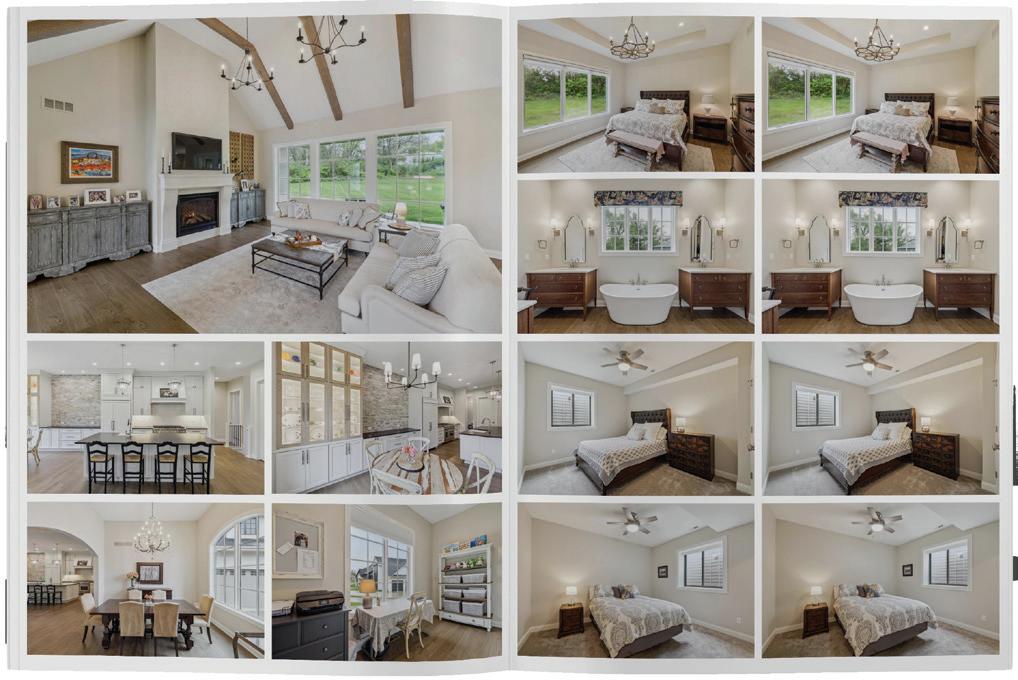

• Listing Booklets

• Flyers

• Luxury Business Cards

• Buyer and Seller Booklets

• Listing/Open House Materials

• Agent Signage

Turn any of our booklets into a virtual flipbook to send digitally to clients via text or email. Scan to see an example.

Every Door Direct Mail® (EDDM) is a USPS® program that allows you to mail marketing pieces to every home on a selected postal route—without needing a mailing list or individual addresses.

This makes it a cost-effective and efficient way to reach entire neighborhoods with consistent, professional messaging.

EDDM is especially effective for real estate professionals because it allows you to focus your marketing on the neighborhoods that matter most to your business.

Whether you’re promoting a new listing, recent sales, open houses, or your personal brand, EDDM helps keep you visible where homeowners live.

With EDDM, you can:

• Target specific neighborhoods or ZIP Codes

• Reach hundreds of homes at once

• Avoid the cost and hassle of purchasing mailing lists

• Build brand recognition through repeated exposure

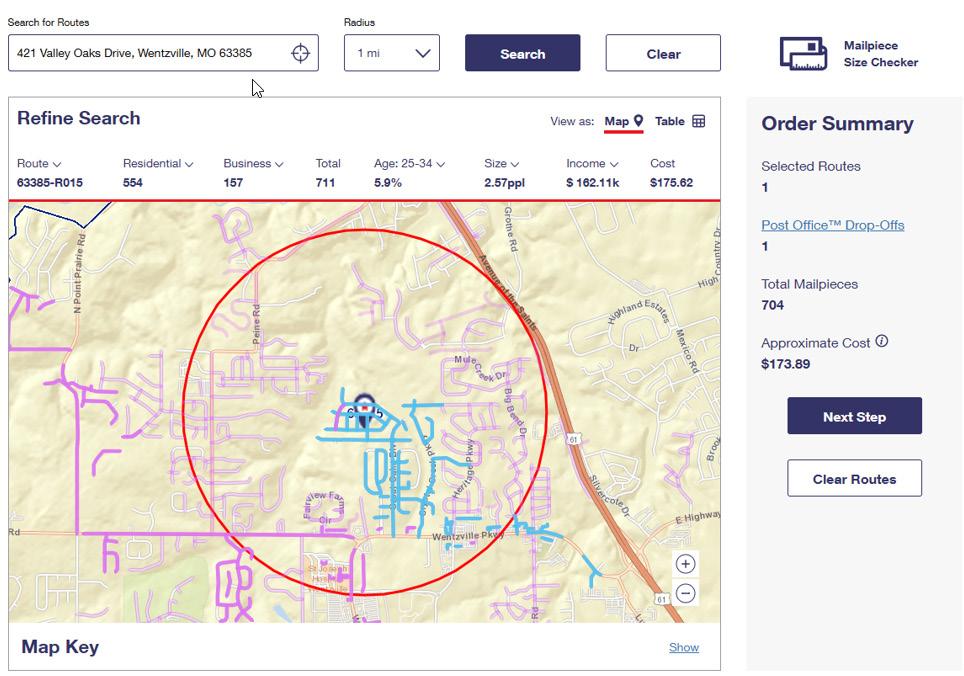

The first step in using Every Door Direct Mail® is identifying the postal routes that best align with your target audience.

This tool allows you to select neighborhoods based on location, delivery count, and demographics.

1. Visit USPS.com

Navigate to Business and select Every Door Direct Mail® from the menu.

2. Enter a Location

Type an address, city and state, or ZIP Code into the search field, then click Search.

3. Locate the Address on the Map

A star icon will appear on the map, indicating the selected address location.

4. Select Available Routes

Once highlighted you will see route information including Demographics, Total Mail Pieces and Cost of Postage.

To complete your Every Door Direct Mail® mailing, USPS® requires postage to be paid online through your USPS® account.

If you already have an account, you can log in and proceed with payment. If not, follow the steps below to create one.

Don’t Have a USPS® Account? Register and Create a Personal Account

1. Go to USPS.com

Click Sign In / Register in the top-right corner of the page.

2. Select “Create an Account”

Choose the option to create a new USPS® account.

3. Choose a Personal Account

When prompted, select Personal as the account type.

4. Enter Your Information

Complete the required fields, including:

• First and last name

• Email address

• Phone number

• Mailing address

5. Create Login Credentials

Set up your username, password, and security questions.

6. Verify Your Email Address

USPS® will send a verification email. Click the link provided to activate your account.

7. Log In to Continue

Once verified, sign in to access Every Door Direct Mail®, submit your mailing, and pay for postage online.

Tip: Save your login information—you’ll use this account for future EDDM® mailings and payment confirmations.

Once you have selected your mailing route(s) and created or logged into your USPS® account, follow the steps below to submit and pay for your EDDM® postage.

Step-by-Step: Submitting and Paying for EDDM® Postage

1. Log In to Your USPS® Account

Visit USPS.com and sign in using your personal account credentials.

2. Access Every Door Direct Mail®

From the USPS® website, navigate to Business and select Every Door Direct Mail®.

3. Review Your Selected Routes

Confirm the mailing route(s) you previously selected. Review the number of deliveries and total postage cost.

4. Choose Mailing Options

Select your mailing date and confirm whether you are mailing Retail EDDM®

5. Proceed to Checkout

Click Checkout to move to the payment screen.

6. Enter Payment Information

Provide your payment details using a credit or debit card.

7. Submit Payment

Review your order summary, then click Submit Payment to complete the transaction.

8. Receive Confirmation

After payment is processed, you will receive a confirmation screen and email receipt from USPS®.

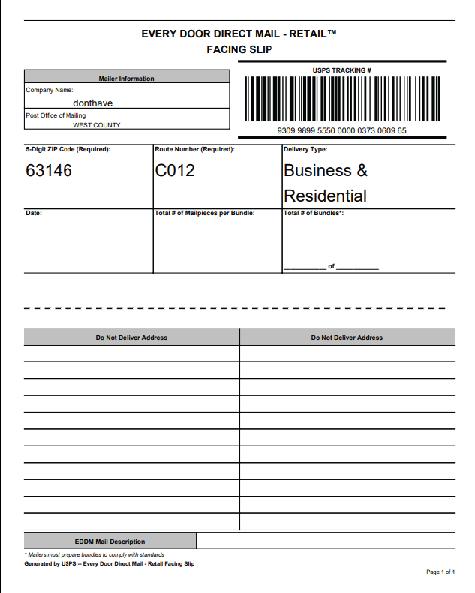

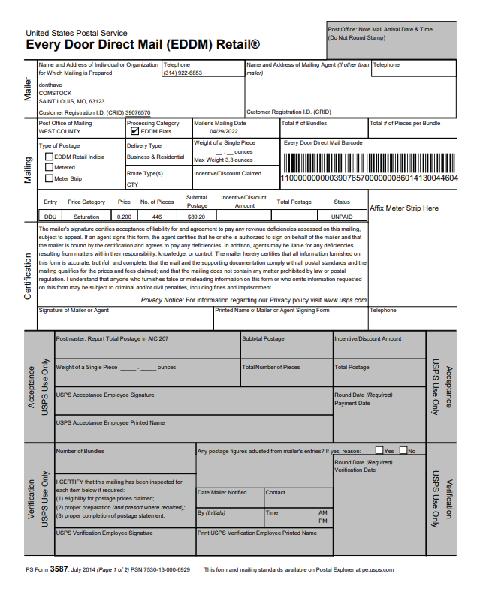

After payment is complete, USPS® will generate the required EDDM® paperwork, including a Mailing Statement and Facing Slips for each selected route.

Both of these documents must be downloaded and sent to the Midwest Marketing Team. Our team will use them to properly bundle, label, and complete your mailer in accordance with USPS® requirements.

Once we receive these documents, we’ll take care of the remaining preparation so your mailer is ready for post office drop-off.

LO Name:

Title:

We cannot start designing until we have received all information.

You will be notified when your design is approved or on-hold

Realtor Name:

Company Name:

Title:

O ce #:

Email:

Website: NMLS#:

Cell #:

SCORE Team 217 Mortgage EHLT

Quantity: Need by Date*:

O ce #:

Email:

Website:

Cell #:

(Please include headshot & logo if first time requesting a design)

Shipping - UPS 2-Day Delivery

Ship Order to: Home O ce Address Type

(Every Door Direct Mail)

Bundle and attach Facing Slips (please send us your USPS paperwork)

with address list**

Door Hanger (4.25x11) Flyer (8.5 x 11)

Listing Booklet

Flipbook Version

4 pg. (20 photos minimum)

8 pg. (40 photos minimum)

Coloring Book Crayon Packs ($0.20 each)

Social Media

Luxury Business Card

Trifold (6”x11” folded; 11”x17” unfolded)

These have an increased turn time.

Corporate Marketing Collateral

Please attach the file or collateral ID#.

Seller Book Template

Please also include a bio and two reviews/link to reviews page.

Buyer Book Template

Please also include a bio and two reviews/link to reviews page.

Did you find an idea on Etsy or Pinterest? Send us a screenshot and we can recreate!

(Please note we can NOT use realtor.com, zillow.com, or similar site links because of RESPA to pull information or photos)

If sending photographer files, please include the description, beds/baths/sqft/etc. below.

Description/Design Explanation:

Beds: Baths: SQFT: Garage Spots:

(NOTE: The team does not write descriptions. Please review your verbiage carefully for spelling and grammar mistakes. The team are not LO’s or Realtors and will need as much information as possible to complete your requests.)

Turn times vary. PROOF turn times and PRINT turn times are not always the same.

* Any design request sent after 2:30pm CST will count as next work-day submittal. These turn times begin at 9am CST next work day, M-F.

** If providing addresses, please include an Excel spreadsheet file with headers such as Name, Address, City, State, Zip.

***All New Designs will need to be sent to OL A Marketing for compliance approval which can increase turn around time.

Please review all design proofs carefully Edits after approval will incur a charge of $0.20 p/p for reprints.

PRINTING WILL NOT BEGIN UNTIL WE RECEIVE EXPRESS APPROVAL TO PRINT.

• Down Payment as Low as 3%

• Fixed or Adjustable Rates

• Down Payment Assistance Programs Available

• Non-Occupying Co-Borrowers Allowed

• Down Payment as Low as 3.5%

• Lower Credit Score Flexibility

• Higher Allowable Debt to Income Ratios

• 100% Financing with DPA

VA

• 100% Financing

• No Monthly Mortgage Insurance Premiums

• Flexible Underwriting Guidelines

USDA

• 100% Financing

• Lower Credit Score Flexibility

• Gifts for Closing Costs Allowed

• Borrow up to $3 Million

• Credit Score as Low as 700

• Eligible for Primary Residence, Second Home or Investment Property

• Warrantable and Non-Warrantable Condos Permitted

• FHA and Conventional Programs

• Purchase or Refinance

• Principal Residence, Second Home or Investment Property

• Ability to Finance Repairs and Home Improvements

• Allows Buyer to Become a Cash Buyer

• Buyer Can Purchase New Home Without Selling Current Home

• Conventional and VA Loans Allowable

• Lock In Your Rate - Rate Can’t Increase

• If Rates Improve during Locked Period, You Can Float Down to a Better Rate

• Self Employed Borrowers can use Business Bank Statements to Qualify

• Purchase New Home Without Selling Current Home –Exclude Payment in Debt to Income Ratio

• Purchase, Refinance or Cash-Out

• Primary, Second Home or Investment Property Eligible

• Use Equity From Your Existing Home Towards the Purchase of a New Home

• Ability to Present a Strong Non-Contingent Offer, Giving You a Competitive Edge in the Market

• No Monthly Payments During the Loan Term Reducing the Financial Stress of managing Two Mortgage Payments

• Lower Interest Rate for the First Few Years of Mortgage

• Available on Conventional, FHA VA and USDA Loan Products

• 1/0, 1/1/1, 2/1, and 3/2/1 Buydown Options Available

• Additional Funds for Down Payment and Closing Costs

• Chenoa

• NAF Pathway Product Suite

• Borrower can Reduce the Principal Balance

• New American Funding will Re-Amortize the Loan based on the Remaining Term and Payments will be Reduced

• Multiple Recasts can be Completed during the Life of the Loan

• PMI can be Eliminated in Some Scenarios

Buying in cash means convenience, cer tainty, and may mean cost savings too. In fact, buying in cash may help your clients save up to 11% over those using a traditional mor tgage.1

With NAF Cash, an affiliated company of New American Funding, your buyer can make a competitive, true cash offer that is not contingent on financing and close in as little as seven days. You know what that means for you.

• Clients can buy their new home before selling their current home

• Sellers may be more likely to offer concessions to cash buyers

• Get commissions quickly

• Use potential savings to buy down interest rate

• No fees for agents

• Close on more homes faster

Follow these steps to make your buyer a cash buyer with NAF Cash!

STEP 1

Get Cer tified

Join a FR EE 4 5 - minu te N A F Cash LLC training

STEP 2

Get Your Clie nt Pre -A pproved

Get your client pre - approved with New A merican Funding!

STEP 3

Complete N A F Cash Docume nts

Work with your N A F Cash Transac tion Coordinator to submit the required documents.

STEP 4

Get Ready to Write Cash Of fers

Your N A F Cash Transac tion Coordinator will notif y you once the client has been approved and they can begin making a cash of fer

STEP 5

O f fer Accepted

Close and move in quickly! At this point , you will work closely with your N A F Cash Transac tion Coordinator

Elite Interest Assist: The seller-paid interest program that makes listings stand out

With Elite Interes t Assis t , the seller covers 100% of the buyer’s interest for the first 3 or 5 months af ter closing ( buyer s till pays principal, ta xes , and insurance as usual) It ’s clean , no deferred interes t , and it helps move inventor y noticeably fas ter.

Eligible borrowers can now get up to $6,000 in assistance toward the down payment and closing costs. Let’s connect to see if our Pathway Programs could be the solution you're looking for.

This is a quick reference guide only- ask your trusted LO for more information and specifics

G row Your Business & H elp Clients Achieve H ome ownership.

N A F Pathway 10 0 Program helps eligible buyers cover their down payment , closing cos ts, and prepaid expenses with program not only provides your buyers with an accessible path to homeownership, bu t also expands your business by

• Up to 10 0% Financing

• 3.5% or 5% in Down Payment Assis tance

• Owner- Occupied Only

PROPE RT Y T YPES H I GH L I G HT S

• Minimum Credit S core of 5 80

• No Income Restric tions

• 2-1 temporar y buydown available

• 10 - year repayable second lien

A renovation mortgage offers your clients the financial flexibility to meet their home improvement needs for a wide variety of renovation projects, from repairs and energy updates to landscaping and luxury upgrades. This renovation loan includes financing in their conventional purchase or refinanced home loan.

• Purchase the home and include rehabilitation costs in the same transaction

• Finance up to 97% of the “After Improved” appraised value

• Occupancy types include primary residence, second home, or investment properties

• No minimum repair amount

• The maximum repair amount is 75% of the “After Improved” appraised value of the property

We can help your buyers with J umb o Ho m e L oan s from New American Funding

I f your c lients want a h ome in a pre mi u m nei gh bor h oo d , a re read y to buy a va c ati o n h ome , or w ant to ex pand thei r real estate po r t fo li o, ou r fl ex i b le Jumb o loans cou ld b e ju st what th e y need . W ith l oans up to $5 milli on and alte rnati ve qu ali fy in g in com e opti o ns , your c lients can bu y more w ith Ne w Ame ri c an Fu ndin g!

OUR JUMBO HOME LOANS DELIVER MORE!

Up to $5 million

Down payments of as little as 10%

Debt-to-income ratio up to 50%

Credit score as low as 620

Cash-out Refi up to 85%

Options for bank statements, 1099, asset verification, and DSCR

Primary, secondary, & investment proper ties

Available for 1 - 4 unit single-family, condos, modular homes, and townhomes

Do You Have Buyers Ready For a Bi gg er Home , Investment Property, or Vacation Home?

$0 Down Payment – No Mortgage Insurance

$2 Million Maximum Loan Amount

Fixed Rate and ARM Options Available

• Medical Doctor (MD)

• Doctor of Osteopathy (DO)

• Doctor of Dental Science or Surgery (DDS)

• Doctor of Dental Medicine (DMD)

• Doctor of Ophthalmology (MD or DO)

• Doctor of Psychiatry (MD or DO)

• Doctor of Pharmacy (PharmD)

• Doctor of Veterinary Medicine (DVM)

• Doctor of Podiatric Medicine (DPM)

• Certified Registered Nurse Anesthetist (CRNA)

• Medical residents, fellows, or interns with one of the above degrees

A mortgage recasting, or loan recast, is when a borrower makes a large, lump-sum payment toward the principal balance of their mortgage and the lender, in turn, reamortizes the loan. This means that your loan and payments are reduced to reflect the new balance. It allows borrowers the opportunity to close with just 5% down. Once the current home is sold, borrower can recast to use the proceeds from the sale to buy down the principle balance to reduce monthly payment and eliminate PMI.

Recasting Highlights:

• Minimum of $5000 principal reduction

• $300 Nominal fee

• Borrower can reduce the principal balance

• New American Funding will re-amortize the loan based on the remaining term and payments will be reduced

• Recast for Conventional Loan (Freddie Mac and Fannie Mae)

• Multiple Recasts can be completed during the life of the loan

• Only one document is needed for recast: Borrowers must provide a Recast Modification Agreement which they will execute and have notarized

• The first principal and interest payment must be made on the original note

• PMI can be eliminated in some scenarios

A temporary buydown lowers the effective interest rate for the first few years of the mortgage. This reduction is a result of the deposit of a lump sum into an escrow account, a portion of which is released each month to reduce the borrower’s payments. Temporary Buydowns can be used on Conventional, FHA, VA, and USDA Loan Products.

These pages will focus on the Seller Paid Buydown.

Year 1 - Monthly Payment calculated using a Rate 1% below Note Rate

Year 2-30 - Monthly Payment would be calculated at the Note Rate

EXAMPLE:

Note Rate 6.625%

Year 1 Rate 5.625%

Year 2-30 Rate 6.625%

Year 1 - Monthly Payment calculated using a Rate 2% below Note Rate

Year 2 - Monthly Payment would be calculated at 1% below Note Rate

Year 3-30 - Monthly Payment would be calculated at the Note Rate

EXAMPLE:

Note Rate 6.625%

Year 1 Rate 4.625%

Year 2 Rate 5.625%

Year 3-30 Rate 6.625%

Year 1-3 - Monthly Payment calculated using a Rate 1% below Note Rate

Year 4-30 - Monthly Payment would be calculated at the Note Rate

EXAMPLE:

Note Rate 6.625%

Year 1-3 Rate 5.625%

Year 4-30 Rate 6.625%

Year 1 - Monthly Payment calculated using a Rate 3% below Note Rate

Year 2 - Monthly Payment calculated using a Rate 2% below Note Rate

Year 3 - Monthly Payment calculated using a Rate 1% below Note Rate

Year 4-30 - Monthly Payment would be calculated at the Note Rate

EXAMPLE:

Note Rate 6.625%

Year 1 Rate 3.625%

Year 2 Rate 4.625%

Year 3 Rate 5.625%

Year 4-30 Rate 6.625%

The cost of the Buydown is simply the difference between the BUYDOWN PAYMENT and the P&I PAYMENT using the Note Rate.

The COST for the Seller is equal to the SAVINGS for the Buyer.

See examples below.

1st Year - Buyer of House B is saving $403.75 per month Compared to Buyer of House A Savings of $51.23 per month

2nd Year - Buyer of House B is saving $206.90 per month Compared to Buyer of House A Savings of $51.23 per month

Our entire team is on-call and available to assist you & your clients with their lending needs!

• Fast Preapprovals

• Rate & Program Flyers

• Open House Materials

• Attend Open House

• Broker Previews

How much can a seller pay towards closing costs?

The more you save, the lower your monthly mor tgage payment will be. Link your bank account, monitor your spending, gain spending insights, and create a budget.

strengthen your credit and correct any errors. Work with a loan coach who knows credit like their ABCs.

The amount of debt you have compared to your income is one of the most impor tant factors for

• Get a $500 lender credit if you close on a home with New American Funding within two years of signing up with Uqual.

• Get access to 1:1 coaching from a team of exper ts who is obsessed with your loan success.

• Gain access to a Loan Readiness Score that shows you how close you are to reaching your loan goal.

It star ts with a 1:1 call with an exper t, giving you a clear path forward. Using ar tificial intelligence, we analyze your finances to create a strategy that will guide you on your path to loan readiness.

When we’re on your side, you’re on your way. We include an Action Plan that shows you step by step what you need to do to progress towards your goals. Plus, we accompany you to encourage and coach you throughout your journey

We don’t just help you achieve your mor tgage, we empower your financial future. As you progress in our program, you open new doors of oppor tunity to create wealth and be the best version of you, relieved of financial stress.

Talk to your New American Funding loan officer today

to Max. Conforming/High Balance Loan Limits

Up to Max. Conforming/High Balance Loan Limits

Total financed renovations cannot exceed 10% of the lesser of purchase price + total renovation cost, or “as completed” appraised value. If property is located in a Duty to Serve High Needs Area, this can be increased to 15%. For manufactured homes this is limited to the lesser of $50,000 or 10% of the “as completed” appraised value (increase to 15% if property located in Duty to Serve High Needs area). No minimum Must be completed within 120 days of closing. Not required

Up to allowable loan limits including cost of home repairs/ improvements. Total financed renovations cannot exceed 75% of the lesser of purchase price + total renovation cost, or “as completed” appraised value. For manufactured homes this is limited to the lesser of $50,000 or 50% of the “as completed” appraised value. No minimum Must be completed within 9 months of closing. Not required

Up to allowable loan limits including cost of home repairs/ improvements. Total financed renovations cannot exceed 75% of the lesser of purchase price + total renovation cost, or “as completed” appraised value. For manufactured homes this is limited to the lesser of $50,000 or 50% of the “as completed” appraised value. No minimum

which will include the

Must be completed within 12 months of closing. Required

on FHA County Loan

Up to allowable loan limits including cost of home upgrades, contingency reserves and allowable fees.

$5,000 Must commence within 30 days of closing and be completed within 6 mos. Required to review contractor bid and complete formal write up on the project. completing all progress inspections throughout project.

Required. Ranges from 10-20% depending on the project. May be financed or paid in cash.

Required. Ranges from 10-20% depending on the project. May be financed or paid in cash.

Manufactured home provided subject remains in compliance with

Manufactured home provided subject remains in compliance with HUD’s property acceptability criteria and all Freddie Mac requirements Accessory Dwelling Unit (ADU), including a manufactured home ADU

Required. Ranges from 10-15% depending on the project. May be financed or paid in cash. 1-4 Units 1 Unit 2nd Home 1 Unit Investment Condo/PUD Manufactured Home (provided improvements do not require structural changes) Newly built home when the home is at least 90% complete. The remaining improvements must be related to completing non-structural items the original builder was unable to finish.

Required. Ranges from 10-20% depending on the project. May be financed or paid in cash.

Required. Ranges from 10-20% depending on the project. May be financed or paid in cash.

Same as FHA Standard 203(k)

Complete tear down & reconstruction. Alterations to allow for commercial or business use. New construction. Purchase of personal property (built in appliances allowed).

Complete tear down & reconstruction. Alterations to allow for commercial or business use. New construction. Purchase of personal property (built in appliances allowed).

Complete tear down & reconstruction.

Alterations to allow for commercial or business use. New construction. Purchase of personal property (built in appliances allowed).

Same as FHA 203k Standard, plus no structural alterations or foundation repair.

FHA Approved Condo Bank owned REO All properties must be completed with a min. of 12 mos. since Certificate of Occupancy Manufactured home double wide or larger Luxury items, including new swimming pools, hot tubs, outdoor fireplaces, gazebos. Existing inground swimming pools may be repaired. Complete tear down & reconstruction. Alterations to allow for commercial or business use. New construction. Purchase of personal property (built in appliances allowed).

cations.

Disclaimer: Equal Housing Opportunity. Terms and conditions apply. Subject to borrower and property qualifications. Not all applicants will qualify. This is not a loan commitment or guarantee of any kind. Rates and terms are subject to change without notice. NMLS #6606. 2025 © New American Funding, LLC. NAF. com. Corporate office 14511 Myford Rd., Suite 100 Tustin, CA 92780. Phone (800) 450-2010. http://nmlsconsumeraccess.org.

Buydown Program Disclaimer: Rate and payment information for example purposes only.

Lock In & Float Disclaimer: Float Down options subject to additional terms and conditions, ask a New American Funding Loan Officer for more information. Borrower must pay required taxes and insurance.

Renovation Loan Disclaimer: Homestyle ® is a registered trademark of Fannie Mae. Homeownership education required by one borrower if all borrowers are first-time homebuyers.

NAF Cash® Disclaimer: https://www.newamericanfunding.com/legal/statelicensing/. NAF Cash® is fulfilled by NAF Cash®, LLC, an affiliated real estate company of New American Funding that is managed and operated in compliance with applicable legal and regulatory requirements. NAF Cash®, LLC. MI Real Estate Broker #6502431375. NAF Cash®, LLC does not originate loans or issue loan commitments. NAF Cash®, LLC charges a Transaction Fee of 1.5%-3.5% of purchase price for its service (fee varies by state). Terms and conditions apply, not available in all states. 41050 W 11 Mile Rd, Ste 220, Novi, MI, 48375. Phone 844-344-0531.

NAF Bridge Loan not available in TX or MA.

Medical Professionals Disclaimer: Must hold a minimum of an M.D., D.O., D.D.S., DNP, DNAP, D.M.D, PharmD, VMD, DPM or CRNA degree and have an active employment contract or verification of terms of employment acceptance.

NAF Pathway: Equal Housing Opportunity. This is not a loan commitment or guarantee of any kind. Terms and conditions apply. Subject to borrower and property qualifications. Not all applicants will qualify. Rates and terms are subject to change without notice. All mortgage loan products are subject to credit and property approval. © 2025 New American Funding, LLC. NMLS #6606. nmlsconsumeraccess.org. Corporate office 14511 Myford Rd., Ste 100, Tustin, CA 92780. www.newamericanfunding.com. Phone: (800) 450-2010. Credit up to $6,000 maximum. Due to maximum seller concession rules applicable to purchase loan transactions, this credit could be less than $6,000 in some cases where other concessions have been made to the consumer. Credit up to $7,500 maximum. Due to maximum seller concession rules applicable to purchase loan transactions, this credit could be less than $7,500 in some cases where other concessions have been made to the consumer. NMLS #6606

1/2026.