How systemic weakness in SME lending leads to poor outcomes

14 Rewiring the network

From the branch up

Trust is the differentiator

Asset finance refinance

Broking the right deal for your client

Search HSBC UK Commercial Brokers or scan the QR code to find out more

Ask the expert

Special features

18 NACFB: Beneath the surface

22 acceptcards®: Cashflow control

24 Cambridge & Counties Bank: Strong foundations

26 UK Agricultural Finance: Seeds of change

28 Proplend: Navigating lease events

30 FOLK2FOLK: The hospitality myth

33 The big interview: Aldermore’s Danielle Soto

38 Allica Bank: The survey says

40 Roma Finance: Tailored solutions

44 Keystone Property Finance: Striking a balance

46 Mercantile Trust: Deal diligence

Industry insights

48 Skipton Business Finance: Shapeshifter

50 Hampshire Trust Bank: Leverage with purpose

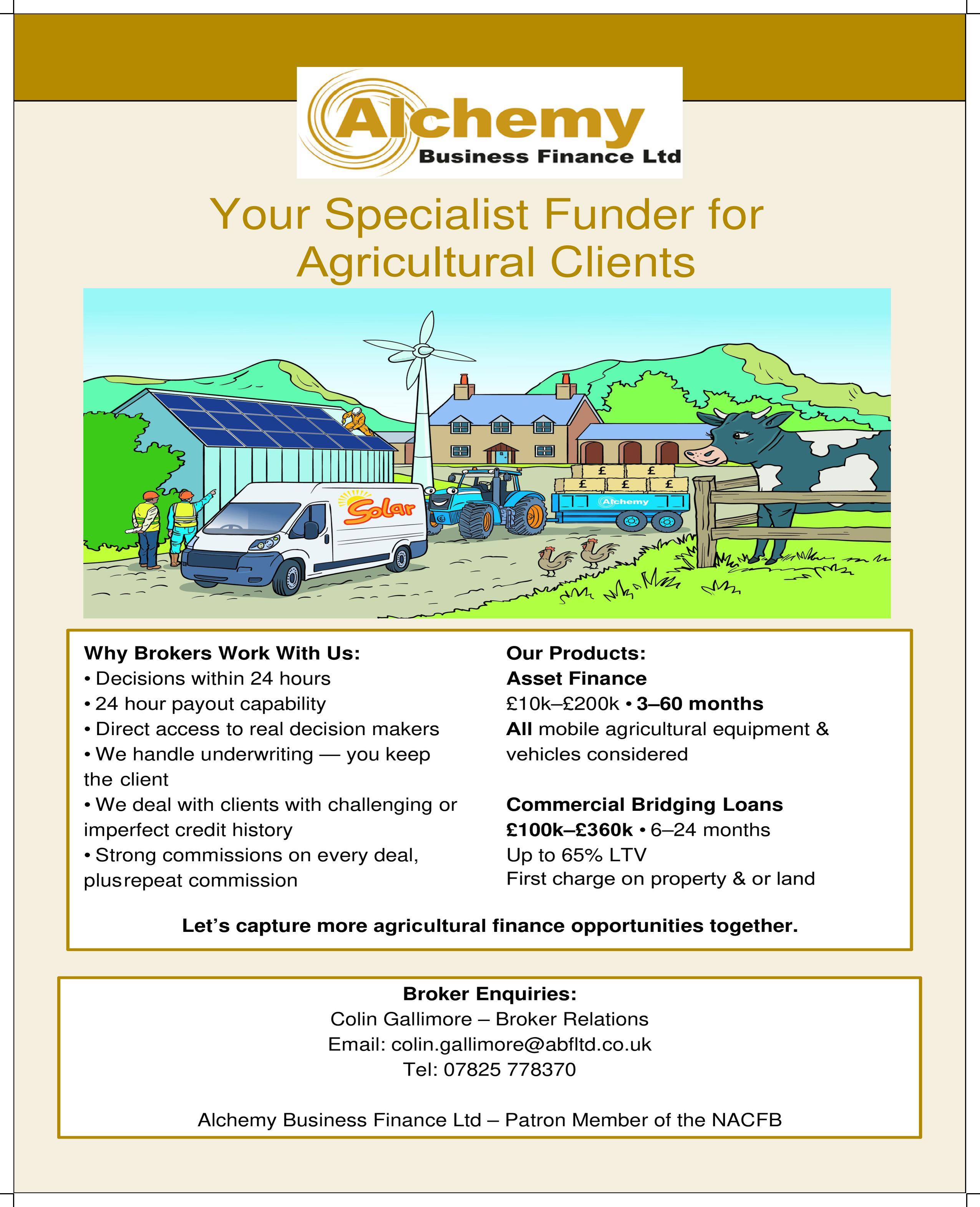

52 Alchemy Business Finance: Harvesting solutions

54 Alternative Bridging Corporation: Welcome home

56 Blacks Solicitors: A new era

58 Reward Funding: System gridlock

Opinion & commentary

60 UMi: Trust is the differentiator

62 Somo: The defining moment

64 Glenhawk: Outside the box

66 LHV Bank: Debt reset

68 Brickflow: Capital errors

70 Ultimate Finance: Asset finance refinance

72 NACFB: Five ways the NACFB can support your business

74 Five minutes with: Lee Simms, AFS (UK)

Meet Danielle Soto

Jim Higginbotham Chief Executive Officer

NACFB

Positive energy

There is a real sense of movement around the NACFB at the moment. Across the broker market, you can feel the pace picking up. There is growth, there is ambition, and there is a growing recognition that brokers are playing an ever more important role in helping businesses find the right funding in a market that is rarely simple. That is all positive. But as our market grows in influence, it also draws more attention. More scrutiny. More questions. And that is no bad thing.

Because if brokers want to remain a central and trusted part of the SME finance journey, we have to keep earning that position. That is why this month’s cover feature feels really timely. In it, I seek to address head on an issue that is not always easy to talk about: the role of short-term finance, and what happens when speed, pressure and commercial incentives begin to work against good customer outcomes. This is not about finger-pointing or pretending there is a simple villain in the story. Short-term finance can be a vital tool. But like any tool, it matters how it is used, when it is used, and whether the customer truly understands what sits behind it. Good brokers make that difference. They bring judgement, perspective and challenge, not just access.

In this issue you can also see that same approach in our work on Appointed Representative networks. Over recent weeks, we have been supporting this important part of our membership in two ways: practically, through direct guidance and discussion, and representatively, through our response to HM Treasury on proposed reform of the AR regime. We want firms in this space to feel both supported and properly represented.

This month’s magazine also carries a story that is deeply important on a human level. We are proud to be backing The Sam West Foundation as the NACFB’s charity partner for 2026/27. It is a charity doing meaningful work in support of children, young people and families affected by mental health challenges, and I hope our community will get behind it wholeheartedly.

Taken together, these stories say something important about the kind of trade body we want to be: active, thoughtful, warm, and willing to engage with the hard yards as well as the good news. There is some brilliant work happening across the NACFB at the moment, and a huge amount of that comes down to the energy, care and commitment of the people behind it.

That gives me real confidence for what comes next.

Drive The Dream

From modern classics to the latest supercar, we take a personal approach to prestige vehicle asset finance.

Dedicated sales team supported by specialist PV underwriters for a commercial can-do approach.

In-house valuation team, using the latest valuation tools and independent valuers.

Flexible funding structures with tailored balloon payments and deposits to suit your client's profile.

Products that fuel ambition:

•Hire Purchase

Dedicated support:

Refinance

Equity Release

TNACFB names The Sam West Foundation as charity partner

The NACFB has named The Sam West Foundation as its official charity partner for 2026/27, committing to a fundraising target of £30,000 while also pledging to raise awareness of the charity’s work supporting children, young people, and families affected by mental health challenges.

Founded in 2018 by Sam’s parents, Chris and Michelle, The Sam West Foundation was established in memory of their son, who tragically took his life at the age of 15 following a short period of clinical depression. The charity is dedicated to improving awareness, diagnosis, and treatment of mental health issues affecting young people, while also advancing education in music and the arts.

Sam grew up in Kent in a close and loving family with his parents and two brothers, Ben and Tom. He was deeply valued by the many friends around him, who knew him for his gentleness, kindness, quick wit and playful sense of humour. He was also gifted in music and the arts, with a bright future ahead of him.

The Foundation was recommended to the NACFB by a team member who attended school with Sam and felt the impact of his loss within the school and the wider community. The NACFB selected the charity not only because of this personal connection, but also in part due to its small size, recognising the potential for a greater impact.

Sam’s parents, Chris and Michelle, shared: “The Sam West Foundation is deeply grateful to have been selected as the charity partner of the NACFB this year. We hope that this will not only enable us to continue our broader work to promote awareness, diagnosis and treatment of mental health issues affecting children, young adults and their families, but also to explore ways by which such support could be offered to the NACFB community.”

Since its inception, the Foundation has already demonstrated the tangible impact that targeted funding can achieve. For example, £9,300 enabled the training of four school staff as mental health first aid instructors, which in turn led to in-house training for 590 staff and 100 sixth form students. This would have cost schools £94,780 to deliver independently. As a result, hundreds of staff

and students are now equipped with the skills to identify young people in need, break down stigma, and guide them towards appropriate support.

In addition, £23,000 invested across four schools in Kent funded mental health practitioners to provide one-to-one counselling for 172 children. A further 487 children accessed drop-in support sessions, while 592 sessions were delivered to staff to strengthen their ability to support emotionally vulnerable students. The programme also extended to families, with 351 parent sessions helping equip parents with the tools to support their children. Alongside this, £4,000 has contributed to cofunding wider counselling services in schools.

Fundraising will take place across several NACFB events in 2026, including NACFB Expo, the Summer Party, the Commercial Broker Awards, and the Commercial Lender Awards. The wider NACFB community is also invited to support the cause through its own fundraising efforts.

The NACFB community has raised in excess of £160,000 for good causes over the last seven years, including The Unbeatable Eva Foundation, Air Ambulances UK, The Newman Holiday Trust and Young Lives vs Cancer (formerly CLIC Sargent).

Anyone wishing to donate, can do so by scanning the QR code or visiting justgiving.com/page/ nacfb-supports-the-sam-westfoundation

NACFB strengthens support for AR networks amid reform debate

The NACFB has stepped up its support for Appointed Representative (AR) networks, combining practical guidance for firms on the ground with direct representation to government as debate over reform of the regime gathers pace.

The trade body has now submitted its response to HM Treasury’s consultation on proposed changes to the AR framework, arguing that reform should be proportionate, risk-based and properly reflect the operational realities of the commercial finance intermediary market. The submission drew on both a targeted survey of NACFB principal firms and AR networks, and feedback gathered in person from network leaders.

That feedback was shaped in part by the NACFB’s recent Rewiring the Network session in Birmingham, hosted by headline sponsor HSBC UK, which brought together AR principals from across the UK for a full day of discussion around governance, oversight, regulatory expectations and good practice.

Led by head of compliance Sarah Cunningham, the session also gave firms the opportunity to share live operational challenges and learn from peers facing similar demands. Following strong engagement, the NACFB is now looking to host a second session for AR networks and firms considering establishing one.

Key dates for 2026

NACFB Funding Future Growth: Supporting brokers across Wales: 15th April I Cardiff I 10:00 – 13:00

NACFB Funding Future Growth: Supporting brokers across the East of England: 12th May I Cambridge I 10:00 – 13:00

NACFB Commercial Finance Expo: 10th June I NEC Birmingham I 09:30 – 16:30

NACFB Summer Party – July I London

NACFB Funding Future Growth: Supporting brokers across Scotland: 3rd September I Glasgow I 10:00 – 13:00

NACFB Commercial Broker Awards: 11th September I Manchester I 13:00 – 19:00

NACFB Commercial Lender Awards: 26th November I London I 18:00 – 01:30

NACFB Funding Future Growth: Supporting brokers across the South East: 14th October I Canterbury I 10:00 – 13:00 NACFB Funding Future Growth: Supporting brokers across the South: 2nd December I London I 10:00 – 13:00

A strong commitment

Empowering brokers and businesses to thrive in a changing world

Ian Coulson Head of Commercial Brokerage HSBC UK

For businesses, finding the right funding structure is as important as being able to access finance. In today’s fast-evolving business landscape, the ability to manage working capital effectively is more than a financial necessity – it’s a strategic advantage. As headline sponsor of the NACFB, HSBC UK is proud to support our broker community, ensuring we enable, educate and incentivise to ensure businesses find the right solutions.

Commercial finance brokers are increasingly called upon to help clients manage risk and seize new opportunities. At HSBC, we recognise that supporting businesses as they expand isn’t just about providing products – it’s about offering insight, partnership, and practical solutions that build confidence.

This ethos is at the heart of our working capital proposition. We know that brokers are trusted advisors, guiding clients through complex decisions and helping them anticipate market changes, fund growth, and respond with agility. Our approach is to empower brokers with the knowledge and resources they need to hold stronger, value-driven conversations with their clients. By sharing market insights and best practices, we help brokers and their clients stay ahead of the curve, ready to respond to both challenges and opportunities as they arise.

As businesses look beyond borders for growth, the challenges become more nuanced – from navigating payment uncertainty to understanding regulatory complexity. HSBC’s international network means we’re uniquely positioned to help brokers and their clients access expertise and insights from around the world, while remaining firmly rooted in the UK market. Our global perspective allows us to support businesses with global working capital needs, ensuring they are equipped to manage risks and capitalise on opportunities. We believe that the journey into new

markets should be an opportunity, not an obstacle, and we’re committed to making that journey as smooth as possible for brokers and their clients.

Our commitment to supporting brokers is stronger than ever. We’re delighted to announce we are expanding our team with the appointment of two additional business development managers in the London area. Taryn Robertson, regional director for London at HSBC UK, said: “This expansion reflects our belief in the region’s vibrant business community and our determination to provide brokers with even greater access to support, expertise, and partnership. Our new team members will bring a wealth of experience and a passion for helping businesses succeed, further strengthening our presence in the capital.”

Across the UK, our business development managers are on hand to help brokers navigate the intricacies of working capital and international trade, ensuring that businesses can thrive – no matter what the future holds. Together, we can help businesses succeed – locally, nationally, and internationally.

To find out more about how we could support you, email us on uk.broker.scheme@hsbc.com

We believe that the journey into new markets should be an opportunity, not an obstacle, and we’re committed to making that journey as smooth as possible for brokers and their clients

Fuel opportunity

We’re championing brokers to go further, unlocking more choice and flexibility for property focused clients.

Î Lending from £500k to £100m

Î Commercial, residential & semi commercial

Î Investment & development

Î Up to 75% LTV

Î Terms from 2 to 20 years

FOR INTERMEDIARY USE

to status. Security

Any

or

as security may be at risk if you do not repay any

on it.

No bridge too far

Establishing a market-leading bridging division

Jamie Jolly

Head of Bridging Secure Trust Bank

In our industry, the term “market leader” is often bandied about. How can two words mean so much yet be so ambiguous at the same time? I’ve been asking myself that question since joining Secure Trust Bank (STB) at the start of the year to lead our expansion into bridging finance.

Without the broker community, there wouldn’t be a property market, let alone a bridging one

There isn’t one correct answer, but I believe the key to making us a “market-leading” bridging lender is ensuring that both brokers and clients can benefit from genuine expertise, clarity and accountability at every stage of the journey.

After over two decades in the specialist lending and bridging spaces, I have experienced enough success stories and failures to know those three aspects are simply non-negotiable.

The goal

Our ambition is simple: to build a bridging business that complements and enhances STB’s established real estate finance division.

The aim is for the sector to associate us with the same level of trust, certainty and consistency affiliated with the bank’s heritage. With over 70 years of stability, a strong balance sheet and a reputation for reliability, it lays the foundations to build a best-in-class bridging division. That, however, is just a starting point.

To achieve this, introducing key routes to market and consistent engagement with internal and external stakeholders is essential. Without the broker community, there wouldn’t be a property market, let alone a bridging one. These relationships are genuine partnerships built on mutual interest and shared success. Intermediaries increasingly want lenders that can deliver, communicate well and understand the nuances of the market. This is exactly the space we intend to occupy, delivering strong conversion rates and high levels of repeat business in the process. This is also why we are building a team weighted towards experience across all key functions.

The approach

Our model combines a highly intuitive broker portal with a personal, relationship-driven approach. This is underpinned by our view that brokers should have direct access to decision makers from day one. The portal will be user-friendly but not a barrier to direct communication, balancing digital efficiency and personal contact.

Over the past 25 years, I have played far too many games of “email tennis” where queries retrospectively fall at the first hurdle – or game. Digitalisation has an important role to play in our industry, but it should never replace invaluable face-to-face conversations between all parties. Whether it’s to quickly resolve a challenge or to discuss and share ideas for product enhancements, you can’t beat regular and open communication.

The journey begins with an initial conversation with one of STB’s relationship directors, where the enquiry is reviewed and indicative terms are agreed upon. The former is then sent through the broker hub for a deeper, more robust underwrite. Formal terms are issued with a clear and agreed list of outstanding items, then our valuation and legal partners are instructed. That blend of experience and clear lines of dialogue ultimately supports all parties as we move on to completion.

Too often, lenders design generic processes that aren’t tailored around bridging and expect everything to run smoothly.

The reality, however, is that no bridging case is the same and can involve challenges. Our portal allows a process that blends ease and accessibility with experience and the ability to communicate with a team that have operated within this space for decades. That is what I class as market leading.

The result

Despite the recent, well-documented challenges facing the industry and its key players, the bridging sector remains robust, resilient and full of opportunity. Our portfolio has been built to offer a suite of products that lead the market segments we choose to operate in.

It encompasses land bank and development exit loans for residential and mixed-use properties, while the former extends to purpose-built student accommodation (PBSA) schemes. Loan sizes range between £2 million and £20 million and have a term of three to 24 months, meaning the right product can be supplied to the right project.

If there’s one thing that my career has taught me, it’s that bridging works best when lenders and brokers operate as true partners. That belief underpins everything we are crafting at STB. With experienced people, a bespoke product suite and processes designed to enhance communication, rather than hinder, we will earn trust by delivering consistently. If that makes us a market leader in the eyes of our partners, then we’ll know that we’re doing things right.

Bridging works best when lenders and brokers operate as true partners

Rewiring the network

Growth, oversight and the shape of what comes next

Sarah Cunningham Head of Compliance NACFB

The AR model continues to appeal for a simple reason: it offers a practical route to growth on both sides of the relationship.

Regulators do not simply want assurance that monitoring is taking place; they expect to see the process, the outputs and the follow-up actions

For principal firms, a well-run network can extend reach and create scale without employing every broker directly. It allows firms to broaden coverage and bring together different specialisms under a shared framework of systems, controls and oversight. For firms joining a network, the appeal is equally clear. It offers a route to market that can be quicker and more commercially realistic than direct authorisation, as the AR is not directly authorised, it is the responsibility of the principal to make sure the network is compliant, up to date with the latest regulation and make regulatory submissions.

Among NACFB Member firms, property-led brokers make up 68% of the community, with 49% operating within AR networks. In asset finance, the proportion is higher still, with 67% of firms working under AR arrangements. At the same time, the number of single-person firms is falling, now standing at 53%, down from 59% over the last two years. Taken together, this points to a market where scale, structure and shared oversight are becoming more attractive. It also helps explain why the AR model is now under a brighter regulatory light.

Oversight is key

Regulators are paying closer attention to how principal firms oversee their ARs in practice. That scrutiny has sharpened further through HM Treasury’s consultation on the Appointed Representatives regime. Importantly, this is not a challenge to the model itself. The consultation recognises the AR regime as a proportionate and cost-effective way for firms to undertake regulated activity, promote competition and support innovation.

Against that backdrop, the NACFB recently brought together a group of AR network leaders for a peer-to-peer working session focused on what good looks like in practice. Delegates worked through the construction of a fictional principal firm from the ground up, exploring the governance, compliance and operational foundations required. One of the clearest themes to emerge was that effective oversight starts well before a firm is ever appointed.

A credible AR network begins with a properly considered regulated business plan, not a sales document. It should clearly articulate how the firm is structured, what activities it undertakes, how responsibility is allocated and how risks are identified and managed. A defined risk appetite is equally important, ensuring the principal is clear on what it will and will not accept, and how that position evolves as the network grows. These documents should be supported with the firm’s policies and procedures.

The same discipline applies to onboarding. Selecting an AR is not simply about production potential. It requires thorough due diligence across the individuals involved, the business model and their regulatory background. Principals need to understand not only what an AR intends to do, but how it operates and whether it can be effectively overseen. The written AR agreement is central to this, clearly defining the scope of permitted activity and where responsibility sits.

Once an AR is appointed, the real work begins. Smaller networks cannot assume that a lighter structure allows for looser control. Clear reporting lines, defined responsibilities and appropriate separation between commercial activity and compliance oversight are essential. A principal does not need to be large to be well governed, but it must be able to demonstrate what it is doing and why within their policies and procedures.

That emphasis on evidence is critical. Regulators do not simply want assurance that monitoring is taking place; they expect to see the process, the outputs and the follow-up actions. Regular site visits remain an important part of that oversight, providing a clear line of sight into how ARs are operating in practice. These reviews should cover core areas such as file quality, complaints

handling, training, record-keeping and financial resilience, alongside any remediation required.

Ongoing oversight should also track key indicators, including complaint trends, revenue patterns and the balance between regulated and non-regulated activity. Financial monitoring remains important, particularly where there are signs of deterioration or changes in ownership or structure.

The session also highlighted several blind spots that can emerge if oversight is not sufficiently robust. These include ARs accepting regulated introductions from non-regulated sources, weak approaches to commission disclosure and inconsistent financial crime controls. Individually, these issues can appear manageable; collectively, they can present material risk.

What comes next

HM Treasury’s consultation raises a number of important questions. These include whether principal firms should require specific FCA permission to operate as a principal, whether the Financial Ombudsman Service should be able to consider complaints directly against ARs in certain circumstances, and whether ARs themselves should fall within scope of the Senior Managers and Certification Regime.

The NACFB has already engaged its network and will be responding to the consultation. The central point is straightforward. The AR model works best when it remains proportionate, commercially viable and grounded in real-world brokerage activity, while still demanding high standards of oversight.

AR networks are not a shortcut. They are a responsibility. But for many firms, they remain one of the most effective ways to combine entrepreneurial freedom with structured governance. That is why they continue to matter, and why getting them right is essential. If your firm needs support as an existing AR network or AR, or is considering adopting the model, get in touch with the NACFB compliance team.

Regulators are paying closer attention to how principal firms oversee their ARs in practice

AI in action

How SMEs are saving time and working smarter

Artificial intelligence (AI), we’ve all heard of it and are likely all using it in some form or other, helping us save time, improve efficiency and make better use of data. From marketing and customer service to administration and planning, AI is starting to reshape how many SMEs operate day-to-day. We spoke to Alan Watkins, managing director at NACFB Partner CETSAT, who works closely with SME clients, to hear how small businesses are using AI and where they’re seeing the biggest gains, and where the limitations still lie.

What are the most common AI tools you’re currently seeing small business clients adopt?

Most small businesses start with AI tools that fit into the systems they already use every day. Features within Microsoft 365 and Google Workspace are becoming popular for drafting emails, summarising meetings, and organising information. Tools such as ChatGPT are also widely used for generating ideas or helping structure documents.

In practice, businesses are using AI to save time on everyday tasks. That includes writing proposals, producing marketing content, summarising documents, extracting information from PDFs, and helping respond to customer enquiries more efficiently. It is less about replacing people and more about removing repetitive work that slows teams down.

Where are you seeing the biggest productivity gains?

Administration is where most companies see benefits first. Drafting emails, summarising meeting notes, and preparing documents can take up a surprising amount of time each week. AI can produce a starting point very quickly, allowing staff to review and refine the final output.

Customer service is another area where improvements are noticeable, particularly in helping teams respond to enquiries more quickly. Marketing teams are also using AI to generate campaign ideas, social media posts, and website copy more efficiently. Finance teams are seeing steady gains through tools that help extract information from invoices and receipts.

Can you share a practical example of this in action?

One example is a professional services company with around 30 staff. They introduced AI tools to help prepare proposals and summarise meetings so that actions could be captured clearly.

What previously took several days could often be completed within a single day. This meant the team could respond to opportunities more quickly and spend more time focusing on their clients. They estimate the change has saved around 20 to 25 hours of staff time each week while improving their overall service.

Alan Watkins Managing Director CETSAT

What misconceptions do business owners often have about AI?

A common belief is that AI is designed to replace people. In reality, the most successful uses simply help employees work more efficiently by supporting them with routine tasks.

Another misconception is that businesses need complex systems or huge amounts of data before they can start. In many cases, companies can see benefits from small improvements using tools they already have.

What should SMEs be cautious about?

Businesses should be mindful of data protection and avoid sharing sensitive information with unmanaged tools. It is also important to remember that AI can sometimes produce inaccurate information, so human review remains essential.

With sensible policies, staff training, and clear oversight, AI can become a practical tool that helps businesses work smarter rather than harder.

Administration is where most companies see benefits first

Beneath the surface

Why poor SME borrowing outcomes are rarely the product of one bad choice

Jim Higginbotham CEO NACFB

Anyone who spends enough time driving on British roads knows the feeling. You hit a pothole you did not see in time and the instinct is immediate: blame the hole. It is the thing that jolts to the core of you, the thing that causes the damage, the thing right in front of you. Yet potholes rarely appear overnight. They are what happens when pressure has been building beneath the surface for some time, when wear and strain and patchwork repairs gradually weaken the road until one day the damage becomes impossible to ignore. I have found myself thinking about that in relation to the current debate around short-term finance.

There is a real issue here. There are an increasing number of SME borrowers who for a multitude of potential reasons are finding themselves burdened with excessive debt which doesn’t meet the medium to long-term needs of their business. This debt is typically short-term in nature and in many cases more expensive than more appropriate forms of debt that would meet the longer-term needs of the borrower. In extreme cases this is leading to such a drain on operational cash flow in otherwise viable businesses that debt service is compromised resulting in defaults and business failures.

What worries me slightly is the speed at which people move from recognising the problem to claiming they already understand it. A few striking examples emerge, a villain is identified, a familiar argument takes shape, and before long a wider market issue is being treated as though it has one simple cause and one simple answer. That may be politically effective, but it is rarely the same thing as being right.

A useful product, used badly

Short-term finance is not inherently the problem. In many cases, it is a useful and legitimate part of the funding

mix. For some businesses it provides quick access to working capital when speed genuinely matters. For others it offers flexibility at a point where other forms of finance are not available or not appropriate. Used properly, it can be exactly the right product at exactly the right moment. I think the difficulty really begins when speed starts to crowd out judgement.

Most small business owners are not planning their funding needs with the benefit of long-time horizons. They are managing staff, suppliers, tax bills, customer delays, rising costs and the daily demands of keeping a business moving. When a cash squeeze appears, their focus is naturally on solving the immediate problem in front of them. This is not really failing, more often it is the reality of running a small business.

Years ago, some of those short-term pressures might have been absorbed by an overdraft or a long-established bank relationship. In many cases that route is now less available, so borrowers look elsewhere. When they do, the market presents plenty of options. Some are entirely suitable. Some are expensive but fairly reflect the risk involved. Some are less appropriate than they first appear. For a borrower under pressure, though, the appeal of speed and ease can easily override everything else.

That is when a short-term facility can start doing a job it was never really designed to do. Instead of bridging a temporary gap, it becomes a stand-in for a longer-term funding need. Once that mismatch sets in, the risk of poor outcomes rises quickly.

The intermediary role

This is where responsible brokers

add real value. At their best, they do not merely fulfil requests. They bring perspective. They help borrowers distinguish between the funding they think they need and the funding that actually fits the business.

That is especially important in the short-term space because when all some brokers have is a hammer, everything looks like a nail. It is a bit of a blunt phrase, but it captures something important. Product familiarity shapes behaviour. Distribution models shape behaviour. Incentives shape behaviour. If a broker’s world narrows around one route, one product type or one commercial rhythm, it becomes harder to step back and ask the more important question: is this genuinely the right solution for this client?

A broker should not simply act on instruction. They should test it. What is the money actually for? Is this a temporary gap or a sign of a deeper working capital issue? What happens when the facility matures? What will the repayment burden do to trading headroom over the months ahead? Are there alternatives that may be slower or less straightforward, but more suitable in the round? We all know that this is the real work of intermediation.

Commission also has to be part of this conversation. Again, commission is not inherently a problem. Brokers are entitled to be paid and lenders will often be the party making that payment. The issue arises when remuneration is opaque, disproportionate or capable of distorting judgement. If a borrower cannot understand how their broker is

What worries me slightly is the speed at which people move from recognising the problem to claiming they already understand it

being paid, or whether that payment is fair in the context of the service provided, trust in the process begins to weaken. A market that wants to present broking as a professional, value-adding activity cannot afford to be vague about incentives.

Shared responsibility

Lenders are just as much a part of this picture. There is no single universally fair price in business lending. Pricing reflects risk, capital treatment, operational cost and the profile of the borrower. Higher-cost funding is not automatically unfair funding. But lenders do have a responsibility to communicate cost clearly, explain structure properly and ensure that the product being offered makes sense for the borrower in question.

That last point matters because affordability and suitability are not the same thing. A business may be able, on paper, to service a facility, at least initially. That does not necessarily mean it is the right answer to the problem being solved. A market that asks only whether a borrower can afford the repayments risks missing the more important question of whether the facility is actually suitable over the life of the arrangement.

This is why I do not think the answer lies in demonising one product type or one part of the market. The truth is more complicated. This is a systemic and multifaceted problem. That is not a way of hiding behind broad responsibility or

If we want to improve outcomes, we need to understand the whole chain rather than fixate only on the point where it snaps

making everyone a bit to blame so that nobody is accountable. It is simply an acknowledgement that poor outcomes usually arise when several pressures combine at once: borrower urgency, limited financial awareness, patchy product understanding, commission structures, price opacity, lender appetite and underwriting that may focus more on immediate affordability rather than longer-term suitability. If we want to improve outcomes, we need to understand the whole chain rather than fixate only on the point where it snaps.

That is also why it matters that the NACFB was invited earlier this year by Blair McDougall, the Small Business Minister, to join a session examining this issue. It reflects the fact that all participants in the commercial finance ecosystem have a role to play in solving for good customer outcomes. That working together as a cohesive body with common purpose is infinitely more effective than demonising or overly lauding any one part of the ecosystem.

A better response

The encouraging part is that these issues are not beyond repair. SME

borrowers need better support to distinguish between an immediate cash need and a longer-term funding requirement. Brokers need to continue proving their value through judgement, challenge and guidance rather than simply speed of execution. Commission needs to be transparent and proportionate. Lenders need to communicate cost and structure in ways that busy business owners can genuinely understand. Underwriting needs to give proper weight to suitability alongside affordability.

None of this is beyond the industry to address, but it does require a more mature response than the one public debate often produces. We have a choice as an industry, to address these issues ourselves or have the regulator try and do it for us. The market does not need louder accusations nearly as much as it needs better judgement.

If we want stronger outcomes for SMEs, then the answer is not to stare at the pothole and declare the case solved. It is to look beneath the surface, understand why the road gave way, and then do the harder, more useful work of putting it right.

Cashflow control

How payment processing impacts SME liquidity

Richard Bradley CEO acceptcards®

Cashflow is the lifeblood of a business, yet many SMEs are unknowingly restricting it through the way they process card and cash payments.

While brokers naturally focus on funding structures, affordability and credit profiles, the mechanics of how money enters a business are frequently overlooked, despite their direct impact on liquidity, stability and growth potential.

We know that cashflow pressure remains one of the leading causes of SME concern in the UK, even among profitable businesses. Recent data from Intuit QuickBooks’ SME insight report shows that 51% of UK SMEs say cashflow is currently a problem. For many, the issue is not a lack of revenue, but timing and efficiency. Payment processes within businesses often evolved reactively over time, rather than strategically, leaving them with legacy arrangements that no longer reflect how they trade today.

Transaction fees and charges are an obvious consideration, but they are only part of the picture. Studies into SME payments behaviour indicate that settlement delays of even a few days can have a material effect on working capital, particularly for businesses operating with high transaction volumes or thin margins. When funds land in their bank accounts several days after a sale, businesses are effectively creating a cash gap that must be funded elsewhere.

This gap frequently manifests as increased reliance on overdrafts or other short-term facilities. While these tools have an important role to play, over time the cost of bridging these gaps can erode

margins and affect affordability calculations when businesses seek new or renewed funding. There is also another behavioural impact. Research into SME financial decision-making shows that unpredictable cashflow reduces confidence and slows investment. Business owners delay or avoid taking on new recruits, limit purchases and postpone capital expenditure when visibility over incoming funds is poor. The flipside of this means that predictable and easy access to cash improves planning and supports more confident growth decisions.

This presents an opportunity to take a more holistic view of cashflow. By understanding how clients take cash and card payments, settlement times and the cumulative cost of transactions, brokers can identify whether cashflow could be improved operationally as well as financially. Improved cashflow has a direct impact on access to finance. Stronger liquidity can enhance affordability, reduce perceived risk and in some cases broaden the range of funding options available to an SME, leading to more sustainable outcomes for both brokers and their clients.

As the SME landscape becomes increasingly data driven, payment processing should be viewed as a core component of financial health rather than a peripheral operational detail. Encouraging clients to review how money moves through their business can help unlock more efficient cashflow, improve funding outcomes and support long term growth all without fundamentally changing how they trade day-to-day.

Improved cashflow has a direct impact on access to finance

Markets may We still deliver.

OBBLE.

Funds ready. Clear credit appetite. Our mandate doesn’t change with the headlines.

Strong foundations

Why

smaller sites deserve specialist lending

Jayne Follows Head of Real Estate Finance

Cambridge & Counties Bank

Much of the conversation around property development finance continues to focus on scale: large sites, national developers and multi-phase schemes running well into double-digit millions. Yet across the UK, SME housebuilders delivering smaller, local schemes play a vital role in meeting housing demand – often operating quietly, efficiently and under the radar.

These are experienced builders working with a single plot, an infill site, or a modest area of land. They may be delivering two, five or 10 homes rather than hundreds, but collectively their contribution is significant. Despite this, many still face challenges accessing finance, particularly where borrowing requirements sit below the £5-10 million mark and fall outside the appetite of larger development lenders.

Smaller housebuilders often don’t fit neatly into mainstream development funding models. Their projects may be modest in size but no less complex, and they frequently require lenders who understand the nuances of local planning, phased cashflow and hands-on delivery. Many are experienced operators with strong track records yet still find themselves underserved because their deal size is considered “too small” or “too niche”.

From a lender perspective, these smaller schemes demand the same level of care and due diligence as larger developments, but with greater flexibility, pragmatism and a genuine understanding of SME businesses. This includes recognising that developers may be looking to fund a single site, refinance land with planning, or progress a first development beyond their core contracting activity.

For brokers, this presents a clear opportunity. The challenge is rarely the viability of the project, but finding funding solutions that reflect the commercial reality of smaller schemes. SME housebuilders value relationships, clarity and speed of decision-making. They want to work with lenders who take the time to understand their business model and how a project will evolve, rather than forcing it into a structure designed for much larger developments.

Brokers who can connect these clients with lenders that actively support smaller schemes are not only adding immediate value, but also helping sustain local housebuilding and regional growth. These projects may be delivered one site at a time, but their cumulative impact is meaningful – unlocking small sites, supporting experienced builders and turning viable land into new homes.

As the market continues to evolve, it’s essential that SME housebuilders are not overlooked. Supporting them isn’t just about funding bricks and mortar; it’s about recognising their role in the wider housing ecosystem.

At Cambridge & Counties Bank, we continue to see strong demand from experienced SME developers delivering smaller schemes. For these builders, deliverability is key: certainty of commitment, pragmatic decision-making and a lender who remains engaged throughout the project can be transformational.

SME housebuilders value relationships, clarity and speed of decision-making

Seeds of change

How agricultural inheritance tax changes are impacting farm borrowing

Mark Thompson CEO UK Agricultural Finance

Britain’s farming sector is, once again, entering a period of significant adjustment. Changes to Agricultural Property Relief (APR) and Business Property Relief (BPR) are coming into force, shaking up the established reliance on family farms passing from one generation to the next, without any tax consequences.

It represents one of the most consequential structural shifts in rural finance requirements for decades

For decades the practical reality was that qualifying farms transferred land and business assets with little or no inheritance tax. That certainty shaped how farming families thought about succession, ownership structures and borrowing. The new regime changes all of this.

Consider a 300-acre mixed farm in Herefordshire, representative of a typical family operation. Previously, the expectation was that the farm could transfer to the next generation tax free and the only discussion was around which of the children would farm. Under the revised APR/BPR framework, the same farm could now face an inheritance tax bill of around £350,000.

For many families that liability cannot be met from income alone. For lenders and brokers, this is more than a tax adjustment. It represents one of the most consequential structural shifts in rural finance requirements for decades.

The new framework

From 6th April 2026, a £2.5 million cap per individual applies to assets eligible for 100% APR or BPR relief. Above that level, qualifying assets receive 50% relief, creating an effective 20% inheritance tax charge on the excess value. The allowance is

transferable between spouses or civil partners, meaning couples may pass on up to £5 million of qualifying agricultural or business assets free of tax, in addition to their normal nil-rate bands.

These reforms particularly affect asset-rich but cash-poor farming families, many of whom relied on APR and BPR to transfer land across generations without triggering a tax bill.

Liquidity pressures

The new inheritance tax can be paid in ten equal annual interest-free instalments, but the liability still requires a source of liquidity to fund this. For many farms this presents an unfamiliar problem.

Land values have risen steadily, pushing increasing numbers of farms above the new thresholds. At the same time, the profitability of many farming businesses remains modest, relative to the value of the underlying land. The result is a growing number of farms that are valuable on paper but generate limited distributable cash.

Evidence of financial pressure is already visible. Around 27% of family farm sales in 2024 were attributed to debt pressures or financial restructuring, a notable shift in a sector historically cautious about leverage. What is changing is the source of risk.

Historically farmers worried about losing their farm due to commodity prices, bad weather, or subsidy changes. Increasingly, tax policy is now driving financial decisions.

For brokers, this creates a new advisory opportunity. Farmers who avoided debt are now exploring refinancing, restructuring or short-term borrowing to manage their tax exposure.

Ownership changes

Inheritance tax reform is also intersecting other tax changes, including the increase in capital gains tax on non-residential land to 24% from October 2024.

Families are increasingly having the difficult but necessary conversations about how to organise ownership across generations. In many cases, restructuring itself requires capital, whether to fund buying family members out, trust structures or asset reallocation. That in turn creates new demand for specialist agricultural finance.

One unintended consequence of the reforms may be earlier generational transition within farming businesses. From a lending perspective, this is already encouraging

multi-generational borrowing structures, where both generations participate in financing arrangements.

Real-world impact

The government argues that the revised £2.5 million threshold will shield most farms, with around 85% of agricultural estates expected to avoid additional inheritance tax. In practice, the picture is more complex. Analysis indicates that, between 480 and 600 estates each year could face new liabilities, including around 200 farms valued below £5 million. The greatest increases are likely to fall on farms worth over £7.5 million, while roughly 70 estates annually may struggle to meet liabilities using non-farm assets alone.

For lenders and brokers, these changes are likely to reshape credit demand, security structures and loan design across the sector. There is expected to be increased need for short-term inheritance tax funding, alongside greater demand for longer-term lending secured against land and buildings. Refinancing to support generational restructuring may become more common, as well as working capital facilities where farm income is redirected towards meeting tax instalments.

A pivotal moment

The reforms to APR and BPR represent more than a technical tax change. They are likely to trigger a restructuring cycle across British agriculture.

For brokers and lenders, the opportunity lies in helping clients navigate that transition, structuring finance that avoids forced land sales, supports generational transfer and maintains long-term resilience.

Those who position themselves as informed advisers working alongside accountants, solicitors and estate planners can become indispensable partners, during what could prove to be the most significant financial restructuring period agriculture has experienced in decades.

For lenders and brokers, this is more than a tax adjustment

Navigating lease events

What brokers need to know about break clauses and rent reviews

Theo Theodosiadis Head of Credit Proplend

Commercial property lenders pay close attention to lease events when assessing loan applications. While some brokers typically focus on headline terms like rent and lease length, understanding how break clauses and rent reviews affect lending decisions can significantly improve application outcomes. This article explores these critical lease events and their impact on underwriting.

Break clauses and their implications

A break clause gives either the landlord or tenant the right to terminate the lease early, typically at specified intervals. From a lender’s perspective, tenant break clauses represent a key risk factor that directly influences loan terms.

When assessing break clauses, lenders consider:

• The timing of the break relative to the loan term;

• Whether the break is mutual, tenant-only, or landlord-only;

• Conditions attached to exercising the break (e.g. no arrears, reinstatement);

• The impact on property value if the break is exercised;

• The likelihood of the tenant exercising the break based on their business performance.

Rent review mechanisms

Rent reviews provide opportunities for rental income to increase during the lease term, which can enhance property value and improve debt service coverage. However, the type of review mechanism matters significantly to lenders when assessing long-term income security.

Common rent review types include:

• Open market reviews – rent adjusted to current market levels;

• Index-linked reviews – rent increases tied to RPI (Retail Prices Index) or CPI (Consumer Prices Index);

• Fixed uplifts – predetermined increases at set intervals;

• Upward-only clauses – rent can only increase, never decrease.

Lenders generally favour upward-only open market reviews, as these protect against rental decline while allowing participation in market growth. Index-linked reviews provide predictable income growth but may lag behind strong market performance. The timing of reviews relative to the loan term is also carefully assessed.

Practical considerations

When preparing loan applications, brokers should obtain and review the full lease documentation early in the process. Key dates should be clearly identified, including any upcoming break clauses or rent reviews within the proposed loan term. Providing lenders with a clear timeline of lease events, along with analysis of how these might affect the property’s income and value, demonstrates thorough preparation. Where break clauses exist, information about the tenant’s trading performance and likelihood of remaining in occupation can help mitigate lender concerns.

By understanding how lenders assess these lease events, brokers can anticipate questions, structure applications more effectively, and ultimately secure better terms for their clients’ commercial property financing.

Tenant break clauses represent a key risk factor

From the branch up

From Coventry High Street to Aldermore’s senior ranks, Danielle Soto on leadership, perspective and purposeful growth

We first ask Danielle Soto for an interview back in January at Villa Park, where she is hosting an Aldermore event for colleagues – the sort of setting that tells you quite a lot before a formal question has even been asked. There is pace to the day, certainly, but also ease. Danielle moves through it with the calm attentiveness of someone used to holding a lot at once: people, logistics, mood and message. She is warm without being performative, focused without seeming hurried, and plainly enjoys bringing people together. She says yes to the interview readily enough, though over the weeks that follow, it becomes clear that finding a gap in her diary is less straightforward. That feels less like executive theatre than the reality of a life being lived at full tilt.

When we do finally make it work over breakfast in Spitalfields, she arrives exactly as you might expect: engaged, thoughtful and entirely present. By then, she is balancing one of Aldermore’s broader leadership briefs – spanning business finance and savings – alongside a house move, two teenage daughters and Seve, the family dog (named after

Ballesteros). It is a lot to hold in view at once, and perhaps that is part of what makes her so immediately readable in person. There is no sense of someone trying to project authority. If anything, the impression is of someone long past needing to.

Looking over her career to date, one might assume Danielle came up through one of banking’s more polished talent pipelines. In fact, her story is more grounded than that. She started at Barclays on Coventry High Street and spent almost two decades there, working her way through the business and building the kind of practical, hard-earned understanding that cannot really be faked. It still shows – in the way she talks about customers, in the value she places on people, and in the instinctive tendency to bring the conversation back to what matters in the real world. At Aldermore, where she has been since 2022, that grounding now sits within a role that stretches across deposits and lending, brokers and customers, people and performance. Over our breakfast, what comes through most clearly is not just seniority, but substance: experience, perspective, and a firm sense of what really matters.

You spent almost two decades at Barclays before joining Aldermore in 2022. What shaped you most during those years?

I had a fantastic time at Barclays. I really did. I started out as a personal banker in a branch on Coventry High Street, selling current accounts, loans and credit cards, and I stayed there for almost two decades, eventually leaving as a managing director. When I look back on that period, what shaped me most was the combination of opportunity, strong

leadership, leadership development, and some very important sponsors along the way. I was fortunate in that respect, but I also worked incredibly hard for it.

Those early years in the branch network gave me a grounding that has never left me. You learn the technical side of banking, yes, but you also learn about people very quickly. You learn what customers worry about, what they value, what frustrates them, how trust is built, and how much difference a good conversation can make. When you are face-to-face with customers every day, you develop instincts that stay with you. I genuinely believe that has made me a better leader all these years later.

There is also something about having come up that way which keeps you grounded. Retail banking was not always seen as the glamorous route, but it gave me a very broad base and a real understanding of what banking is actually for. I feel very lucky to have had that start.

You did not come through a graduate scheme route. Do you think taking the harder road has shaped how you lead?

It’s a matter of perspective. I have had an incredible career to date, watching and learning from many of the best leaders in the industry. You often miss that through other routes but practical hands-on experience always wins for me.

Having visible role models was hugely important for me, and I recognise that being that role model for others is now a big part of my own responsibility

If you start from the shop floor, so to speak, you understand how things really work. You understand customers, but you also understand colleagues, pressure, pace, systems, and how decisions made at the top land in the real world. I think that has stayed with me. It means I naturally try to anchor things in what will actually work, not just what sounds good in theory.

What did Aldermore offer that was different enough to make you move?

What really attracted me was the chance to make change happen in a business that is big enough to matter but small enough that you can get your arms around it. In a very large organisation, change can take a long time and be harder to feel. At Aldermore, you can move at pace and see the effect of your decisions more directly. For someone like me, that was very appealing.

Aldermore often talks about being close to customers and brokers. What does that actually mean in practice?

I have lived through the era when relationship banking was a real anchor of the high street proposition, when

bank managers were visible and known locally, and then through all the transformation that followed as those models changed. Branch footprints reduced, footfall changed, more activity moved into pooled and telephony-based structures, and the shape of banking shifted quite significantly.

What is interesting, is that the need for relationships did not disappear. In some parts of the market it may have become less visible, but it never stopped mattering. At a specialist lender like Aldermore, that relationship side of the proposition is still really important. Our ability to work closely with brokers, introducers and clients is part of what makes us distinct.

Now, that does not mean resisting automation or clinging to old models for sentimental reasons. Quite the opposite. What is incumbent on us is making that journey as efficient as possible. We should absolutely be investing in automation, in better journeys, in making it easier to do business with us. But I do not see that as being in conflict with relationships. I think the better you automate the right parts of the process, the more space you create for the human part to add value.

For me, that is what being close to brokers and customers really means in practice. It means they can have real, meaningful conversations with us when they need to. It gives us a deeper understanding of their context. And it creates a genuine sense of partnership, rather than just transaction.

How do you view the broker channel?

Definitely as a strategic partner. It is a really critical part of our business and it has to be a genuine two-way relationship built on mutual respect. It has to feel adult to adult. It has to be mutually beneficial. If we aren’t regularly engaging with brokers, hearing what is on their minds, understanding how we can support them and how they can support us, then we are missing a massive trick.

We’re deeply engaged with our most valuable broker partners, bringing them in, sharing market insight, hearing what is on their clients’ minds, talking about our propositions and where we are investing. Those sessions have landed really well, and I think that sort of engagement matters.

You have led transformation programmes at scale. What is the emotional reality of transformation that people do not always see?

Transformation is a word that most people find scary; when in fact what is really happening is that a business is changing because it needs to stay relevant. How you take people with you is where leaders make a difference. It asks a lot of people. It asks them to keep delivering while also changing how they work, and I have learnt that being open and honest without losing who you are as a leader is crucial.

What gives me energy is being around people who are driven and ambitious. I’m lucky in that respect. I have a great team here, and when you are surrounded by people who are motivated, driven and genuinely want to make things better, that gives you a huge lift. There is also a real sense of achievement when a team sees a difficult piece of work all the way through.

As a leader, though, you have to watch very carefully for saturation point. That is one of the biggest responsibilities.

People cannot do everything, all at once, indefinitely. So, part of leadership is not just setting direction, it is creating clarity. It is being able to say: this is what matters most now, and this is something we’re going to stop doing because the priorities have changed. That can be incredibly powerful for a team.

What grounds you when things feel in flux?

A boss said to me many years ago, “Danielle, it’s just banking,” and that has

If you start from the shop floor, so to speak, you understand how things really work. You understand customers, but you also understand colleagues, pressure, pace, systems, and how decisions made at the top land in the real world

always stayed with me. Not because the work doesn’t matter, because of course it does, but because perspective matters. You can get caught up in things very easily, and sometimes you need to remind yourself what is really important.

Outside of work, life looks very different. I’m married with two daughters who are both very keen horse riders, something they definitely got from me. So weekends are very outdoorsy, surrounded by ponies and doing plenty of driving around between events. And if I’m honest, there’s a lot of terror on my part because they’re now jumping solid fences over a metre high. That definitely grounds you very quickly.

Even the commute helps in its own strange way. I live a few hours away from the office, and while of course there are times when I would love to be home sooner, it can also be useful decompression time. Then you walk through the front door and teenage daughters bring you back down to earth immediately.

You have been closely involved in female talent development. Has the sector genuinely progressed?

Yes, but there is still a long way to go.

There have been targeted interventions, and they have made a difference, but the biggest issue for me is still pipeline. I’ve been hiring in business finance for more than a year now, and the reality is, there just isn’t enough female pipeline coming through. That means you have to be very intentional.

The advice I would give women coming into financial services is to find good sponsors and invest in those relationships. A lot has been written over the years about mentoring, and that has its place, but sponsorship matters enormously. Looking back, some of the pivotal moments in my own career happened because more senior women were quietly looking out for me and opening doors at the right moment. Having visible role models was hugely important for

me, and I recognise that being that role model for others is now a big part of my own responsibility. Those relationships and that visibility really matter.

What excites you most about the next chapter at Aldermore?

We’ve recently welcomed a new CEO and CFO, which naturally marks the start of a new chapter. That has re-galvanised us as a team and created a real sense of momentum. We’re in the process of resetting our strategic ambitions and there are some genuinely exciting prospects on the horizon, particularly around client-focused solutions and how we continue to evolve the business in a way that’s truly centred around our customers.

We’re deeply engaged with our most valuable broker partners, bringing them in, sharing market insight, hearing what is on their clients’ minds

SemiCommercial Lending that delivers more

LTV up to 75% including interest only Can include small HMOs (up to 6 bed), AST or Holiday Lets

Tiered rates at 55%, 65% and 75%

property up to £5m

The survey says

How brokers are solving a decades-old issue for established businesses

Danny McMurdo Business Relationship Manager Allica Bank

Every six months, Allica surveys a panel of brokers from across the industry. It’s a brilliant way to get honest feedback about how we’re doing. We also get a unique perspective on the state of lending – past, present, and future – across the country.

Running an established business can be complex, so it’s critical business owners have access to the right kind of expertise

580 brokers shared their perspectives in our survey at the end of 2025. It’s clear that there’s momentum in the market. More importantly, we can see that brokers are overdelivering for the good of the established British business community.

The data itself is interesting, but it becomes fascinating when seen as part of a bigger picture.

Headline stats from brokers

Overall, the outlook from brokers was really positive. With interest rates having eased up, it’s unlocking opportunities to use finance in different ways.

44% of reported demand was for commercial mortgages and 38% for refinancing. With borrowing becoming (relatively) more affordable, the numbers are more attractive. For some businesses, growth plans that were previously stuck now look more viable.

Year-over-year, the number of businesses seeking finance to stay afloat has dropped by 72% (from 22% to 6%).

Things are picking up across the board, with 56% of commercial mortgage brokers and 55% of bridging brokers saying they had been busier as the year went on.

Brokers are more important than ever

The results of the survey make for positive reading. When we put them in the wider context of the SME lending gap, things get really interesting.

Our own research project found that finance for established businesses is about £65 billion behind where it should be, based on historic data. Since the millennium, banks have focused on residential property, rather than productivity. As a result, access to finance has become a major barrier to growth for established businesses.

As I see it, brokers are essential in changing this situation. Your knowledge and relationships make the impossible possible for your clients.

Brokers are bridging the gap

At Allica, we’ve seen the vital work of brokers first-hand since opening our loan book in 2020. Two recent deal examples perfectly showcase this. In both cases, the business owner couldn’t have accessed mission-critical finance without the expertise of their broker.

Firstly, Capitalise.com helped new owners purchase and refurb Penarth’s Holm House. The iconic spa hotel was once frequented by the likes of Daniel Craig and Harry Styles, but struggled to recover post-pandemic. New co-owner, Kashif Ahmed, said: “We’re fortunate that Capitalise.com connected us with Allica Bank, who were willing to listen and understand our vision. High-street banks didn’t even give us a look in.”

Thanks to their broker George, “what could have been a stressful, uncertain process… turned into something simple and straightforward.”

Secondly, Mark Standley of StandOut Capital Solutions and his dedication to keeping the operators of The Three Horseshoes

in-situ. Barely one year after taking on the lease, landlady Monika was rocked by the owner selling the pub in Peterston-super-Ely. Monika wanted to take ownership herself, but couldn’t find a lender that would offer them a mortgage after only a year of trading, so the community rallied with a crowdfunding campaign and raised enough for a commercial mortgage deposit with Allica.

Mark navigated the nuances of their application, specifically the challenge of proving the source of the deposit. “It was heartwarming, but complex,” he said.

Without their brokers, these businesses would have fallen into the lending gap.

Stable footing builds successful businesses

Running an established business can be complex, so it’s critical business owners have access to the right kind of expertise.

That’s why Allica is committed to investing in and really deepening our broker relationships. You’re the ones at the frontline of business growth. Established business owners turn to you for your expertise and support; we want to play the same role for you.

We’ve lent close to £4 billion to established businesses since 2020 and, as our survey shows, the brokers we partner with see lots of opportunities for more growth in the year ahead. Together, we’ll close the lending gap and get British business booming again.

Without their brokers, these businesses would have fallen into the lending gap

Sonia Mann Head of Sales

Roma Finance

Tailored solutions

FLOW, GROW, and PRO with Roma Finance

In a market defined by tighter underwriting, margin sensitivity and time-critical transactions, brokers need funding partners who can move quickly, structure intelligently, and understand the full property lifecycle.

Roma Finance provides a suite of tailored solutions – FLOW, GROW, and PRO – each designed to support investors and developers at different stages of their property journey. Recent case studies illustrate how these products are being applied in practice.

FLOW: Commercial bridge for fast-paced opportunities

Bridging finance remains essential when timing is critical and competitive assets are on the market. RomaFLOW is designed for experienced investors who require speed and certainty.

A recent example involved a £1.9 million bridging loan to fund the acquisition of a 10-floor office building in Stockport. The property, purchased below market value at £2.6 million and with a current market value of £3.8 million, is fully leased to a corporate tenant and generates approximately £860,000 of annual rental income.

The borrower, an investor with a 21-property portfolio, required fast execution to secure the discounted acquisition. Roma delivered funding in just nine days, structuring a 12-month facility that preserved flexibility for the client’s exit strategy. This case demonstrates the importance of lenders who can combine speed with structured oversight, enabling investors to secure assets that standard finance may not accommodate.

GROW: Supporting development and ground-up schemes

Development finance continues to present opportunities, particularly for regional commercial and industrial schemes. RomaGROW is designed to fund new builds, refurbishments, and mixed-use developments.

In Market Harborough, Leicestershire, Roma provided a £2.3 million 12-month loan for an 11-unit light industrial and warehouse scheme at Hermitage Business Park, with day one funding of £350,000 released to allow works to start promptly. While the customer had prior experience in refurbishment

Specialist lending is not just about product availability –it is about matching the borrower and the asset with the appropriate facility, providing certainty where mainstream finance may be slower or less flexible

projects, this was their first ground-up development. Detailed costings, clear evidence of demand, and a robust business plan were key to securing the loan. The projected GDV of £4.3 million highlights both the potential commercial return and the local market benefit of the scheme.

The case illustrates how specialist lenders can support first-time developers as well as experienced sponsors, provided the project is well-prepared and risks are properly evidenced. Strong communication between broker, borrower, and lender contributes to a smooth and efficient funding process.

PRO: Bridge to term for transitional assets

Investors often require a bridge between acquisition, development or conversion, and long-term income generation. RomaPRO is designed to facilitate this transition.

In one case, a property entrepreneur acquired a former care home intending to convert it into a mixed scheme of HMO units and self-contained flats. Roma provided a £627,800 facility over 60 months, enabling both purchase and conversion. Upon completion, the borrower refinanced onto a buy-to-let product. The flats are now fully tenanted, providing stable rental income and adding value to the borrower’s portfolio.

This example demonstrates how bridge-to-term solutions can reduce refinance risk by providing a clear exit plan from the outset. Specialist lenders are able to structure facilities that reflect both asset potential and borrower strategy, rather than relying solely on standard affordability models.

Key considerations

Across FLOW, GROW, and PRO, the consistent themes are speed of execution, sponsor quality, structured flexibility, and clear communication. In a market balancing modest economic growth with cost pressures and regulatory change, experienced investors remain active but require lenders who understand complex income structures, SPVs, mixed-use schemes, and staged delivery.

Specialist lending is not just about product availability – it is about matching the borrower and the asset with the appropriate facility, providing certainty where mainstream finance may be slower or less flexible. Brokers play a crucial role in preparing and presenting cases that demonstrate strong viability, clear exit strategies, and robust project planning.

Working together

For brokers, the role of a specialist lender is increasingly important. FLOW, GROW, and PRO demonstrate how carefully structured facilities can support time-sensitive acquisitions, development projects, and transitional assets. By combining speed, flexibility, and a relationship-led approach, Roma Finance enables brokers to help investors and developers capitalise on opportunities that might otherwise be missed.

In a market where timing, preparation, and clarity of strategy are critical, having a lender who understands the nuances of different property types and individual customer requirements can make the difference between a completed transaction and a missed opportunity.

...purpose led the interest rate

Where the majority of rental income in a semi-commercial property comes from residential tenants, we can offer residential interest rates.

Semi-commercial case study

A two-property refinance with a 56% LTV, 15-year interest-only term and fixed for 5 years at 6.49 per cent.

Property 1

• Former fire station

• Developed into 12 residential units, commercial unit and office

• Residential units let to supported living provider

• £2.805m loan.

Property 2

• Grade II Listed

• 9 commercial units and 13 residential above

• Established tenancy base

• £1.122m loan.

Striking a balance

Lenders should think twice before sidelining brokers

David Whittaker CEO Keystone Property Finance

Brokers have always been a key component of UK mortgage distribution, but they have become the dominant distribution channel over the past decade.

From a market share of less than 50% in 2009, they now write nearly nine in 10 new mortgages, according to the Intermediary Mortgage Lenders Association. Yet a mix of regulatory change, advancing technology and commercial pressure appears to be prompting some lenders to reassess that relationship. If the industry is not careful, it risks repeating mistakes it has already made.

The intermediary channel did not become dominant by chance. The Mortgage Market Review pushed most borrowers toward advice from 2014 onwards, while growing complexity in buy-to-let lending made brokers absolutely vital. Together, these forces created a system that delivered both scale for lenders and support for borrowers.

Recently, however, there are signs that parts of the market are testing the limits of that model, particularly in the product transfer space. Dual pricing, reduced procuration fees and more direct engagement with existing customers suggest some lenders are exploring ways to reduce reliance on intermediaries.

On paper, the logic is understandable. Product transfer (PT) customers are already on lenders’ books and new technology makes them easier to reach directly. But convenience should not be confused with suitability. Advice is important even for those who take out a PT, if only to ensure they aren’t missing out on a better deal elsewhere.

More broadly, a sustained shift toward direct distribution risks weakening the infrastructure that supports both residential and buy-to-let lending. We’ve been here before. After the financial

crisis, several lenders attempted to push business through direct channels, only to find volumes difficult to sustain without brokers. When they returned, the intermediary market had lost capacity and took years to rebuild.

With the advent of AI, many people may think this time is different – that the technology is finally there to disintermediate the mortgage process.

Used well, AI will be able to streamline admin and enhance decision-making. But it will never replace human underwriters – at least in the specialist lending arena – or reduce the need for professional advice. I can’t see borrowers ever fully trusting an algorithm for such a large financial decision, especially one that is so complex, like buy-to-let.

If technology is a threat, regulation is another concern. The FCA’s decision to drop the need for mandatory advice may give borrowers more flexibility. However, it may also act as the catalyst for mainstream lenders to push their direct channels, in the hope that advancing technology will be able to drive the volumes that brokers once did. I suspect they will be bitterly disappointed with the outcome.