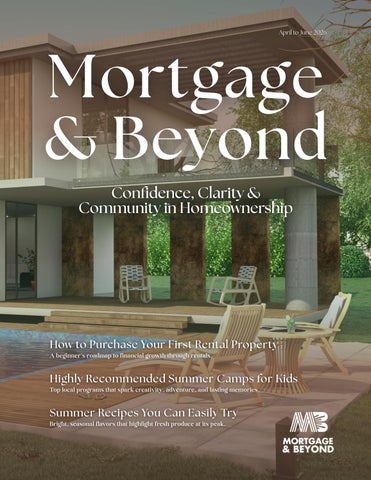

Highly Recommended Summer Camps for Kids

Top local programs that spark creativity, adventure, and lasting memories.

Top local programs that spark creativity, adventure, and lasting memories.

As we welcome the warmth and energy of summer, it’s the perfect time to reflect on what homeownership truly represents not just a place to live, but a foundation for building wealth, creating memories, and expanding opportunities.

At Mortgage and Beyond, we believe homeownership is just the beginning of the journey For many families, the next step is learning how real estate can become a powerful tool for financial growth. In this issue, we’re excited to share guidance on purchasing your first rental property, understanding financing options if you own a business, and exploring how the right mortgage strategy can help you build a long-term real estate portfolio.

Summer is also about time with family and community. That’s why we’ve included a curated list of local summer events and camps across North Texas to help you make the most of the season with the people who matter most.

Our mission has always been simple to empower tools they need to make confident decisions. Whe future, or simply enjoying the summer with your fam

Here’s to sunshine, opportunity, and building something meaningful this summer.

With gratitude,

Founder, Mortgage & Beyond

A welcome message from our founder

Practical steps to safeguard your mortgage approval during the process

Breaking down the key components of what you pay each month

A closer look at the M&B Loan Program for self employed borrowers

First rental property? Here are strategies to set you up for success

L

Spotlight on community highlights and happenings near you

Exciting camps and local outings for kids and families to enjoy together

Important deadlines to keep your finances on track

A quick review to realign your budget and goals

N T E N T S

Easy, everyday changes that make your home more sustainable

Boost your credit score and make the most of your tax refund

Expert insights on loans, equity, and financing explained simply

Two delicious seasonal dishes to enjoy and share E C

Congratulations you’re under contract! That’s a big milestone. Now comes the quiet phase most buyers don’t think about: protecting the approval you’ve already worked hard to earn.

Between contract and closing, your lender is verifying that your financial picture hasn’t changed. The numbers that qualified you must still qualify you. Underwriting isn’t emotional. It’s formula-driven. And formulas don’t care how excited we are about new furniture.

Keep your job steady

Employment is verified before closing. Even positive changes may need documentation. Speak with your lender before making a move.

Respond quickly to document requests.

IDs, pay stubs, bank statements, and tax returns are normal at this stage Prompt responses keep your file moving toward closing

Document larger deposits.

Be ready to log any incoming funds. Clear records prevent delays.

Make every payment on time.

Credit will be checked again One late payment can affect your score and approval terms Stay consistent until closing

Maintain your savings.

Keep your closing funds available. Avoid large transfers or unusual activity without consulting your loan team.

Once you’re under a purchase contract, consistency is everything. Your loan is still being reviewed, and even small changes can affect the final approval.

Agreeing to co‑sign means you’re liable for the debt, and your financial profile is affected right away.

Cash deposits can be hard to verify and may prompt extra underwriting review. Keep your accounts consistent and well-documented.

Your income structure matters Any employment change should be reviewed with your lender first.

New credit can shift your score and debt-to-income (DTI) ratio — even small accounts may impact final underwriting.

New monthly payments change your qualifying numbers What feels manageable now could affect your loan approval

Scenario: A buyer once financed new furniture after going under contract. The added monthly payment increased their debt just enough to complicate the approval. Nothing dramatic just numbers shifting.

Reminder: Stay steady for a few more weeks, and you’ll cross the finish line with confidence!

When most people hear “mortgage payment,” they think it’s just paying a loan In reality, it covers several parts that protect your home, investment, and lender

Knowing each piece makes budgeting easier From reducing your loan balance to covering taxes, insurance, and optional community fees, every dollar has a purpose

MOST MORTGAGE PAYMENTS CON SI ST OF FOUR PRIMARY PARTS:

— COMMONLY CALLED PITI

p r i n c i p a l

Paying Down What You Borrowed

Principal is the part of your payment that reduces the loan balance For example, each payment gradually chips away at a $300,000 loan, building equity the portion of the home you own. Early in the loan, less goes toward principal, but this grows over time. Think of principal as measurable progress toward full ownership.

Interest is what the lender charges on your loan Calculated as a percentage of your balance, it’s higher at the start and decreases as the balance drops Your rate significantly affects the total mortgage cost Interest isn’t a penalty it’s the cost of accessing funds to buy your home

P r o p e r t y Ta x e s

Property taxes fund local services like schools, roads, and emergency services

Lenders often collect part of your annual taxes monthly and pay them via escrow

Tax amounts vary by location and property value, and may change over time

Homeowners insurance covers your home against fire, storms, theft, and other damage Lenders require insurance because the home is collateral for the loan Premiums are often collected monthly via escrow, and rates can change based on claims history or different market factors

Depending on your situation, your payment may also include:

Homeowners Association Fees

Living in an HOA community means paying dues for shared amenities, maintenance, and neighborhood services These fees are billed monthly or quarterly, and lenders would factor them into your overall housing budget to give a full picture of affordability

Mortgage Insurance

If your down payment is under 20% on a conventional loan, PMI may be required It protects the lender in case of default, while helping make homeownership possible sooner The good news once you build enough equity, it can usually be removed

Many buyers assume their mortgage payment will always stay the same With a fixed-rate mortgage, principal and interest remain steady, but taxes, insurance, and HOA/association fees may increase (or decrease) over time

Adjustable-rate mortgages (ARMs) can also change your interest portion after an initial fixed period. Knowing what can change helps you plan without surprises.

Profit and Loss (P&L) Statements NOT required

Loan amounts as high as $3,000,000

Up to 90% loan-to-value (LTV) with no mortgage insurance, depending on loan size and purpose

Multiple business bank accounts permitted

Business bank statements and personal bank statements permitted

Business expense ratio as low as10%

Borrower does not have to be100% owner ofthe business

Common-sense consideration of Non-Sufficient Funds (NSFs) and overdrafts

Highly competitive rates and unsurpassed funding times

12- and 24-Month BankStatement Program Features: Shows your

Are you thinking about buying your first rental property? It’s an exciting step and for many people, it’s the beginning of long-term financial growth Rental real estate can provide steady income and build wealth over time But like any investment, it works best when you go in prepared Here’s a clear, practical look at what to expect and how to do it right

Rental property appeals to investors seeking both immediate income and long term growth

RENTAL PROPERTY OFFERS SEVERAL ADVANTAGES:

If your rent covers your expenses and leaves money left over, you create positive cash flow each month

Property values tend to increase over time, especially in areas with job and population growth

Landlords can deduct many expenses, including mortgage interest, maintenance, and insurance

As the cost of living rises, rents often rise too while a fixed mortgage payment stays the same

You don t need to pay the full price in cash Financing allows you to control a valuable asset with a smaller upfront investment

Rental property is not completely passive It requires attention and planning

Repairs are inevitable, and unexpected costs are part of ownership Tenants also require careful screening, since choosing reliable renters is one of the most important ways to protect your investment Vacancies can be costly, because even when the property is empty you ’ re still responsible for covering the bills And above all, rental property is a business Even if you hire a property manager, you remain accountable for the decisions and financial performance Being a landlord can be rewarding but it requires a professional mindset

Here’s a clear, practical look at what to expect and how to do it right

Before buying:

Aim for strong credit

Pay down high-interest debt

Save for:

15–25% down payment

Closing costs

3–6 mo emergency funds

Having cash reserves reduces stress when surprises happen

While appreciation can increase the value of your property over time, cash flow is what provides immediate stability Your first rental should be able to cover its expenses and generate steady profit each month Monthly income creates security

For your first property, keep it manageable A single-family home is often easier to maintain and resell A small duplex can also work well, especially if you live in one unit and rent the other Avoid major renovation projects at the beginning Stability matters more than speed

Make sure rent realistically covers: Mortgage Taxes and insurance Maintenance (5–10% of rent) Vacancy (5–8%)

If the deal only works under “perfect” conditions, it’s probably too risky.

Buying your first rental property can be a powerful move toward financial independence The key is preparation, patience, and treating the property like a business

Start small Run the numbers carefully Keep reserves

Done the right way, your first rental won’t just generate income it will lay the foundation for long-term wealth

APR 3

APR 4

APR 4-12

AAGD2026TradeShow

At Dallas Market Hall, this annual expo connects multifamily property owners, managers, and on site teams with suppliers and service providers, featuring themed booths, networking, and the latest industry resources

SoleToSole

A premier sneaker, vintage, and streetwear expo, bringing together 80+ vendors and enthusiasts in a vibrant marketplace of trading, shopping, and style

MusicHallatFairParkEvents

Some Like It Hot - lively musical comedy running through early April

APR 16-19 APR 22-23

MAY 1-3 (Apartment Association of Greater Dallas)

MainStreetFortWorthArtsFestival

Downtown Fort Worth transforms into a vibrant showcase of juried artists, multiple music stages, and gourmet food vendors, making it one of the largest cultural events in Texas each spring

DallasBuildExpo

A regional construction showcase with 250 exhibitors, classes, and networking at Dallas Market Hall

DallasInternationalGuitarFestival

At Dallas Market Hall, this expo features buy sell trade booths, exhibitor showcases, and live performances, capped by a Saturday night jam

MAY6 -JUN14

MusicHallatFairParkEvents

Wicked - The blockbuster Broadway hit returns for an extended run in May and June

JUNE 6-7

Richardson’s three day festival blends national touring bands, local art displays, and family friendly activities, creating a lively celebration of music and creativity

A colorful expo showcasing aquatics, reptiles, aquascaping, and interactive displays, all under one roof at Dallas Market Hall JUNE 10-12

This annual commercial real estate networking event features exhibitors, themed booths, cocktails, and food, connecting industry professionals with building service providers in a lively “Under the Big Top” showcase (Building Owners and Managers Association of Greater Dallas)

At Keyrenter, we transform your investment into a seamless, stressfree experience. Our full-service property management approach ensures your rental property is not just maintained but optimized for maximum profitability

21 Point Tenant Screening

Full-Service Property Management

Transparent Financial Reporting

Proactive Maintenance Planning

Efficient Rent Collection

Low Eviction Rate (469) 414-1000

Schedule a Call

6565 N MacArthur Blvd #225, Irving, TX 75039, United States info@keyrenterdfwmidcities.com Why Keyrenter

Marble Falls, Texas Hill Country

Good to know:

Overnight spots go fast; check first‑time camper sessions and bus options.

Carrollton, DFW Area

Classic day camp fun focused on character, teamwork, and adventure High‑energy games, creative challenges, and confidence‑building activities led by seasoned counselors. Great for first time campers and busy families

Lake time, ropes courses, and campfire nights make summer unforgettable Counselors build independence and leadership through cabins, color wars, and unplugged play Perfect for kids ready to stretch their wings.

Good to know: Multiple DFW locations; weekly themes and sibling discounts

Good to know: Sessions fill early; check age tracks and half‑ vs. full‑day options.

Hands‑on garden labs, scavenger hunts, and STEAM projects turn the Arboretum into a living classroom. Outdoor time, art with natural materials, and friendly science make spring and summer bloom Best for curious kids who love plants and wildlife.

White Rock Lake Area

ACROSS DFW ACROSS DFW

Grand Prairie — EpicCentral District

Zip lines, climbing nets, and sky high obstacles deliver thrills for all ages, with beginner zones easing first timers in. Summer energy finds its outlet here, as families cheer each other on from one challenge to the next

Tip: Book timed tickets and pack grippy socks if required

Plano — Oak Point Park

Swing, climb, and zip through rope ladders, Tarzan swings, and canopy crossings. With courses for every level, it’s a treetop escape that blends adrenaline with family fun.

Bring: Closed toe shoes, water, bug spray.

Dallas — Victory Park

Cool off indoors with puzzles that test teamwork and spark laughter Pick a theme, race the clock, and celebrate together when the final lock clicks open

Tip: Choose an age appropriate room and book a private slot.

From high energy fun to quiet escapes, summer reminds families that the best adventure is time spent together

April

Tax Season Essentials & Key Filing Dates

SEC 10 Q filing deadline for accelerated filers; large public companies must submit Q1 reports

SEC 10 Q filing deadline for non accelerated filers; smaller public companies submit Q1 reports

June

Property tax payment deadline in many Texas counties; late payments may trigger fees or liens

Mid‑Year Checkpoint & Education Milestones

Tax Day; federal income tax returns due and deadline to file Form 4868 for a six month extension (extends filing time not payment)

IRA (Individual Retirement Account) & HSA (Health Savings Account) Contribution Deadline; last day to make 2025 tax year contributions toward retirement or medical savings

Property tax installment deadline; counties require spring payments to avoid late fees

May

Quarterly Reporting & Homeowner Obligations

Estimated tax payment due (Q2); self employed and small businesses submit their second quarterly installment to avoid penalties

Mid year financial checkpoint; a good time to review budgets and savings progress

Final day to submit the Free Application for Federal Student Aid for the 2026–27 academic year

June marks the halfway point of the year a natural time to pause and review your financial progress.

Financial progress rarely comes from one big decision. It’s usually built through small, consistent adjustments.

Many people begin January with clear goals: saving more, reducing debt, improving credit, or preparing for homeownership. But as the months pass, daily expenses and busy schedules can make it easy for those plans to drift.

A quick mid-year review helps you see what’s working, identify what needs adjustment, and refocus your financial goals while there’s still plenty of time left in the year.

Your budget anchors your financial plan, and mid‐year is the time to check where your money is going.

(Take10minutestoreview):

Currentmonthlyincome

Fixedexpenses(mortgage,rent, insurance,propertytaxes)

Variableexpenses(food,utilities, entertainment,transportation)

Subscriptionsorunusedservices

Areaswheresavingscouldaddup

Ask yourself:

Are you staying within your planned spending limits? Have new expenses appeared that weren’t in your January budget?

F I N A N C I A L C H E C K P O I N T

Mid-year is a natural moment to check how your savings are progressing. Many people set goals at the start of the year, such as saving for a home down payment, building an emergency fund, reducing debt, or preparing for a future investment property. Reviewing these goals now helps you see where adjustments may be needed to stay on track

It’s also a good time to revisit your broader financial priorities.

Ask yourself:

Are my goals still the same as they were in January?

Have my priorities shifted?

Is my current plan helping me move closer to those goals?

A time to strengthen your financial habits:

• Increase automatic savings contributions

• Direct bonuses or extra income to savings

• Reduce high-interest debt balances

• Continue building emergency reserves

The second half of the year offers a fresh opportunity to refocus. With a clearer view of your budget, savings, and goals, you can move forward with confidence Whether you’re preparing for homeownership, planning an investment, or building better habits, small adjustments now can lead to meaningful results by year‐end.

Need guidance?

Scan the QR to connect with us at Mortgage & Beyond for a quick call about your financial or mortgage questions.

ckpoint as a course correction rather than a olve, and reviewing them regularly helps you oach, and stay on track toward future goals.

company to restore your home and help protect your personal property From soaked floors to smoky walls, we return your property to its predamageconditionquicklyandefficiently.

We’recallingonprofessionalsinthese

Membership Tier

Vendor Type

To keep the list vetted and high value to our clients, we ask for an annual partnershipfee We are not looking to make a profit from the partnershipfee, thefee simply covers onboarding, quality control, and getting our partners to be visible to as many as good referral partners as possible. Here is the info:

Membership Tier

Vendor Type Scale

Pest Control

Home Staging

Smart Home Install

Movers

Packers

Home

Water

Membership Tier

Foundation

Vendor Type

Real Estate Photographers

Drone Videographers

Marketing & Creative Vendors (flyers, websites, social media)

Event Planning

If you run a reputable service-based business and want to be considered for the next round of partners, your company will receive the following benefits:

1. Ad Placement in Mortgage and Beyond Magazine

A half-page or full-page ad featuring your current specials in our Magazine (published quarterly), mailed to 6,000 clients annually.

2. Direct Introductions to Top Agents

Connect with 150 high-producing realtors who closed 1,000+ transactions last year and get access to their partner group.

3. Marketing Opportunities With Builders & Offices

Get your flyers and promos into the hands of national builders and major local real estate teams through our partner network.

4. Monthly Homebuyer Guide Placement

Show up in a printed guide mailed to 200–300 new mortgage applicants every month.

5. Featured on Our Website

Your business will be listed as a trusted vendor visible to 10,000+ monthly visitors.

6. Newsletter Exposure

Be seen by 8,500+ homeowners and real estate pros through our weekly newsletter

PRACTICAL WAYS TO GO GREEN.

Making your home sustainable and planet-friendly saves money, reduces your carbon footprint, and keeps things comfortable. You don’t need a full remodel small, smart changes add up.

Switch to LED bulbs – use up to 80% less energy.

Install a smart thermostat – adjusts heating/cooling automatically.

Use timed power strips – cut phantom energy from idle devices.

Seal drafts and insulate – keeps your home efficient year-round.

Opt for low-VOC paints – healthier indoor air

Choose recycled or responsibly-sourced materials (bamboo, FSC wood)

Use eco-friendly cleaning supplies – safer for you and the environment

Look for ENERGY STAR® or GREENGUARD® certifications when buying appliances

3 GREEN BUILDING & UPGRADES

Passive solar design & high-efficiency insulation – save energy naturally.

Consider solar panels or battery storage – store energy and cut bills

Add rainwater harvesting or composting systems – reduce water waste

Explore living walls or green roofs – improve air quality and insulation

4 EVERYDAY HABITS THAT HELP

Turn off lights when leaving rooms

Air-dry clothes instead of using the dryer

Track energy use with smart home apps

Compost kitchen waste to reduce landfill impact.

PRO TIP

Start small: Pick one upgrade or habit this week and build from there Every step counts!

rates Higher scores qualify for lower interest rates.

options Strong scores increase your borrowing power.

Review all three bureaus for errors and dispute inaccuracies

Your payment history has the biggest impact late payments can drop your score

Length of credit history strengthens your score

Keep balances low and pay down high-interest accounts first Aim for under 30% credit utilization

Too many inquiries can temporarily lower your score Apply only when needed

A

Avoid unnecessary fees like Private Mortgage Insurance (PMI).

Think of your credit score as a plant — small, consistent actions help it grow and stay healthy.

Improving your credit takes patience, but steady effort pays off. Strong credit gives you confidence, more mortgage options, and long-term financial flexibility. Start now, stay consistent, and watch your score rise

For many people, a tax refund feels like a bonus In reality, it’s money you ’ ve already earned — simply returned to you And if you ’ re thinking about buying a home, that refund can become more than spending money It can become a strategic step forward For first-time buyers especially, even a few thousand dollars can meaningfully impact your homeownership journey The key is using it with intention

Adding your refund to your down payment can lower your loan amount, reduce payments, and possibly eliminate PMI Even small increases can create long-term savings

Deposit your refund directly into your home savings account to avoid impulse spending

Closing costs are separate from your down payment and include lender and title fees, taxes, and insurance Using your refund here can ease upfront expenses

Reducing credit card or loan balances may improve your credit score and debt-to-income ratio, strengthening your loan approval

Target high-interest credit cards first to maximize score improvement.

Unexpected repairs happen. Setting aside your refund as reserves provides stability and reassurance after closing

Keep reserves in a separate savings account to prevent accidental spending

For current homeowners, applying refunds toward future investment savings can steadily build purchasing power over time

Treat each tax refund as a scheduled contribution toward your long-term investment goal

A tax refund offers flexibility, but how it’s used can shape your financial future Instead of viewing it as temporary spending money, consider how it can move you closer to stability, homeownership, or longterm wealth building

Smart financial progress often happens in steady, intentional steps Your tax refund is simply one of them

I’DLIKETOREMODELMYHOMEANDUSEITSEQUITYTO COVERTHECOSTS.WHICHLOANPROGRAMISBESTFORME?

Remodelingwithhomeequityusuallycomesdowntotwo mainloanoptions:aHomeEquityLineofCredit(HELOC)or aCashOutRefinance.

HELOC(HomeEquityLineofCredit)

Workslikeacreditcardtiedtoyourhome borrow,repay,andborrow again.Greatforprojectsinstages.Youonlypayinterestonwhatyouuse, butratesareusuallyvariable,andyou’llmanagetwoloans.

CashOutRefinance

Replacesyourmortgagewithalargerone,givingyoualumpsumatclosing. Bestforbigremodelsneedingallfundsupfront,especiallyifyoucanlockina lowerrate Downsides:higherclosingcostsandalongermortgageterm

AHELOCsuitsphasedupdates,whileacashoutrefinanceworksbetterforone largerenovation.Bothletyouleverageyourhome’sequity thechoice dependsonwhetheryouvalueflexibilityorasinglepayout

Homeownership can be more than just a roofoveryourhead;it’salsoawaytobuild value and create financial opportunities. Whether through borrowing against equity orinvestinginproperty,therightmortgage decisions can help you strengthen your longtermfinancialoutlook.

MYCHILDWILLBEATTENDINGTEXASA&M,ANDI’MCONSIDERING PURCHASINGAHOMEFORHIMTOLIVEINWHILERENTINGOUTA FEWROOMSTOCLASSMATES.ISTHISAGOODIDEA?

Purchasing a property near a college campus can be a practical waytocombinehousingwithalong-terminvestment

Insteadofpayingrentforseveralyears,owningthehomeallowsyoutobuildequity, andrentingafewroomstoclassmatesmayhelpoffsetthemonthlymortgage.

There are a couple of ways this can be structured. If your child is 18 or older and has established credit, they may be able to apply for the loanasthemainapplicant,withyou co-signing on the loan In this case, your income can be used to help qualifyforthemortgage.

Another option is purchasing the home as an investment property, whichtypicallyrequiresabouta20% down payment, and renting the extra rooms to your child and their classmates.

By the time your child graduates, this strategy may allow you to build equity in the property while gaining experience with rental property ownership.

Whetheryou’reremodelingwithequityorbuyingaproperty,therightloan dependsonyourgoals.AHELOCoffersflexibility,acashoutrefinanceprovides certainty,andinvestmentfinancingcansupportlongtermownership.

Bell peppers and tomatoes are in season May–September, making this a perfect early‐summer main dish.

HOW TO DO IT:

TIME TO MAKE: 55 MIN

SERVES: 8

8 large bell peppers (any color)

2 tbsp olive oil

1 medium onion, finely chopped

6 cloves garlic, minced

2 cups cooked brown rice

2 cups cherry

tomatoes, halved

2 cups chickpeas, drained

1 cup crumbled feta

½ cup chopped parsley

2 tsp dried oregano

1 tsp smoked paprika

1 tsp salt

½ tsp black pepper

Optional: 1 lb ground turkey or beef, browned

Top with extra feta and parsley.

Pair with a simple cucumber‐yogurt salad

1 Preheat oven to 375°F (190°C) Slice the tops off 8 peppers and remove the seeds

2. Sauté aromatics. Heat olive oil, cook onion until soft, then add garlic.

3. Build the filling by stirring in rice, tomatoes, chickpeas, oregano, paprika, salt, and pepper.

4 Remove from heat and fold in feta and parsley (Optional: add cooked meat if using )

5. Spoon the filling into peppers. Place upright in a baking dish with ½ cup water at the bottom Cover with foil and bake for about 30 minutes

6 Remove foil and bake for 10–15 minutes more, until peppers are tender

Blueberries peak May–June, lemons are year‐round, and the flavor profile is bright, fresh, and early‐summer friendly

Cake

2 ½ cups all‐purpose flour

2 tsp baking powder

½ tsp baking soda

½ tsp fine salt

1 cup granulated sugar

½ cup unsalted butter, softened

3 large eggs, room temperature

1 cup Greek yogurt

¼ cup fresh lemon juice

2 tbsp lemon zest

1 tsp vanilla extract

1 ½ cups fresh blueberries

1 tbsp flour (for tossing blueberries)

Lemon Glaze

1 cup powdered sugar

2–3 tbsp fresh lemon juice

1 tsp lemon zest

1 Prepare the pan Preheat oven to 350°F (175°C)

Grease and flour a 10‐cup Bundt pan

2 Whisk dry: flour, baking powder, baking soda, salt

3. In a separate bowl, cream butter and sugar until pale and fluffy Beat in eggs one at a time

4 Mix in yogurt, lemon juice, zest, and vanilla

5 Combine dry ingredients to wet, stir until smooth

6. Toss blueberries with flour, fold into batter.

7. Bake 45–55 min, until toothpick comes out clean.

8 Cool for 15 min, invert onto a rack, and drizzle glaze