Proposed Budget for Fiscal Year 2027

Proposed Budget for Fiscal Year 2027

Fijalkowski

Angela M. Hill | County Administrator

Christopher S. Lawrence | Deputy County Administrator

Scott A. Woodrum | Assistant County Administrator

Terri T. Mitchell | Chief Financial Officer

Marc M. Magruder | Director of Management and Budget

Robin C. Meade | Budget Manager

Jody R. Parsons | Budget Manager

Scenic view of eastern Montgomery County.

Proposed Budget for Fiscal Year 2027

March 9, 2026

Dear Honorable Members of the Board of Supervisors:

This annual message provides an opportunity to outline the proposed budget for your review. More than ever, the proposed Fiscal Year 2026–2027 (FY 27) budget reflects the collaborative efforts of leadership teams from both the County and Montgomery County Public Schools to address identified needs while remaining fiscally responsible.

Our community’s population has experienced consistent growth over the past several years. As the County continues to grow, so too does the demand for services that support our citizens.

In total, budget requests for FY 27 amounted to $16.6 million. To fully meet these requests, the real estate tax rate would need to increase by 12 cents, to 88 cents per $100 of assessed value, and the annual budget would need to increase by nine percent, allocating $99.3 million for County functions (34 percent of the total budget) and $194.9 million for Montgomery County Public Schools (66 percent of the total budget).

While it is not possible to fund all budget requests each year, I am pleased to present a balanced and financially sound proposed budget for FY 27. The proposed budget and tax rate prioritize the most critical needs identified, with a strong emphasis on public education, public safety, and the growing demand for essential citizen services.

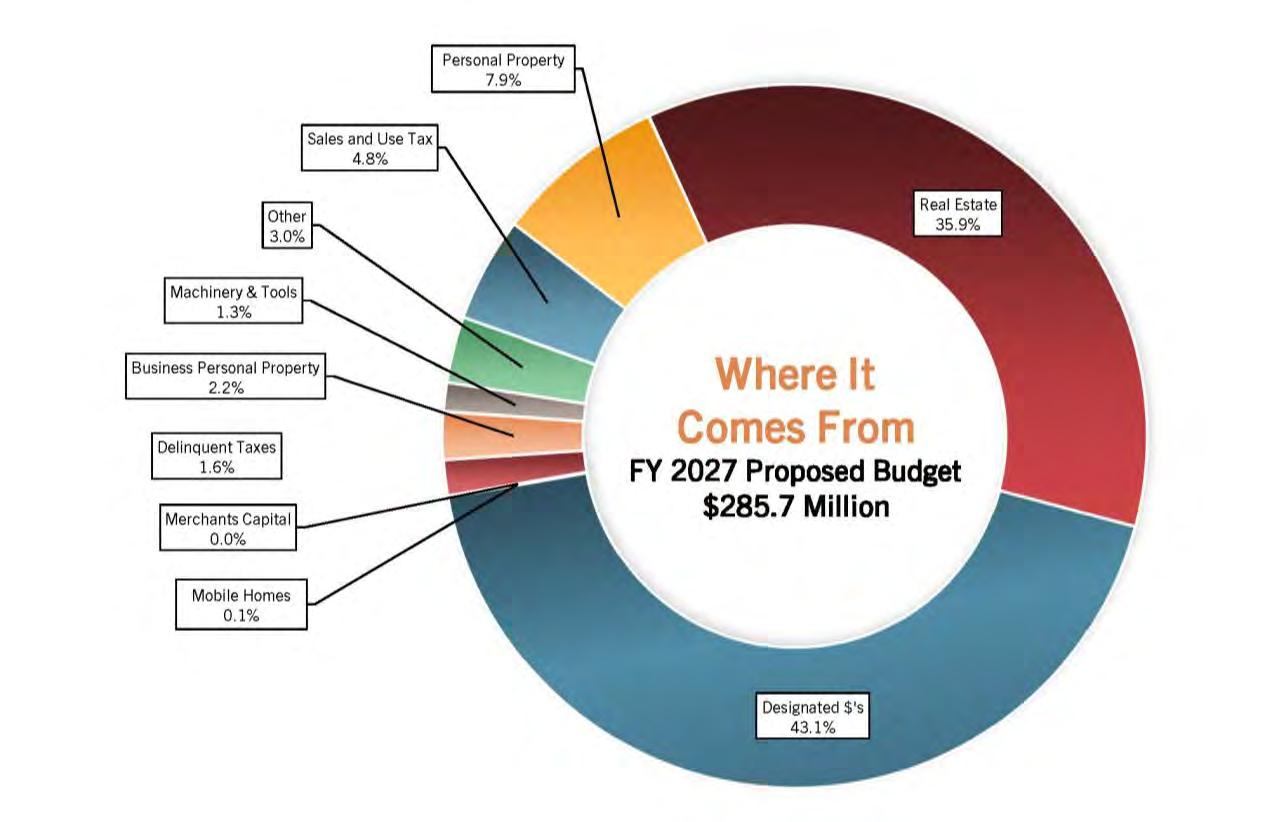

For FY 27, I am proposing a total budget of $285.7 million, an increase of $14.9 million, or 5.5 percent over the originally adopted Fiscal Year 2025-2026 (FY 26) budget, establishing a real estate tax rate of 81 cents per $100 of assessed value, a five-cent increase over FY 26.

Of the total proposed budget amount, I am recommending $190.7 million, 67 percent, be allocated to Montgomery County Public Schools ($160.8 million for school operating; $3.2 million school capital; $7 million for school nutrition funds; and $19.7 million for school debt service). This reflects a $4.1 million increase in County funding I am recommending the remaining $95 million (33 percent) be used to fund public safety; general government administration; judicial administration; general services; health and welfare; parks, recreation, and cultural; community development; and other agencies. Of the new undesignated revenue, I am recommending the allocation of 56 percent to public schools, six percent to public safety, and 38 percent to general County functions.

Funding Sources: $14.9 million in New Revenue

Currently, $1 million is projected in new undesignated revenue for FY 27. The proposed five-cent tax rate increase will provide an additional $6.4 million in new undesignated revenue for a total of $7.4 million.

Each one-cent increase in the real estate tax rate generates approximately $1.3 million in additional revenue. The proposed five-cent real estate tax rate increase provides the additional funding necessary to strategically support identified priorities, including Montgomery County Public Schools, public safety, general County operations, and 51 other agencies that deliver human services, public safety, education, cultural, environmental, and economic development programs throughout our community.

County designated funds, which include local fees, state funding, and federal grants, are projected to increase by $3 million New designated state revenue in the amount of $3.8 million for the school operating fund, combined with $0.7 million in designated school nutrition funds, result in a total increase of $4.5 million in FY 27.

It is important to note, funding from the Montgomery County Public Service Authority (PSA) is included in the County’s FY 27 designated funds to support the newly established Utilities Department. This funding facilitates the transition of PSA employees to County Utilities Department employees and results in an increase of $2.4 million in the County’s general fund. While this change increases the overall general fund within the County’s budget, it does not represent an increase in taxpayer dollars, as these costs are fully funded with revenue from the PSA.

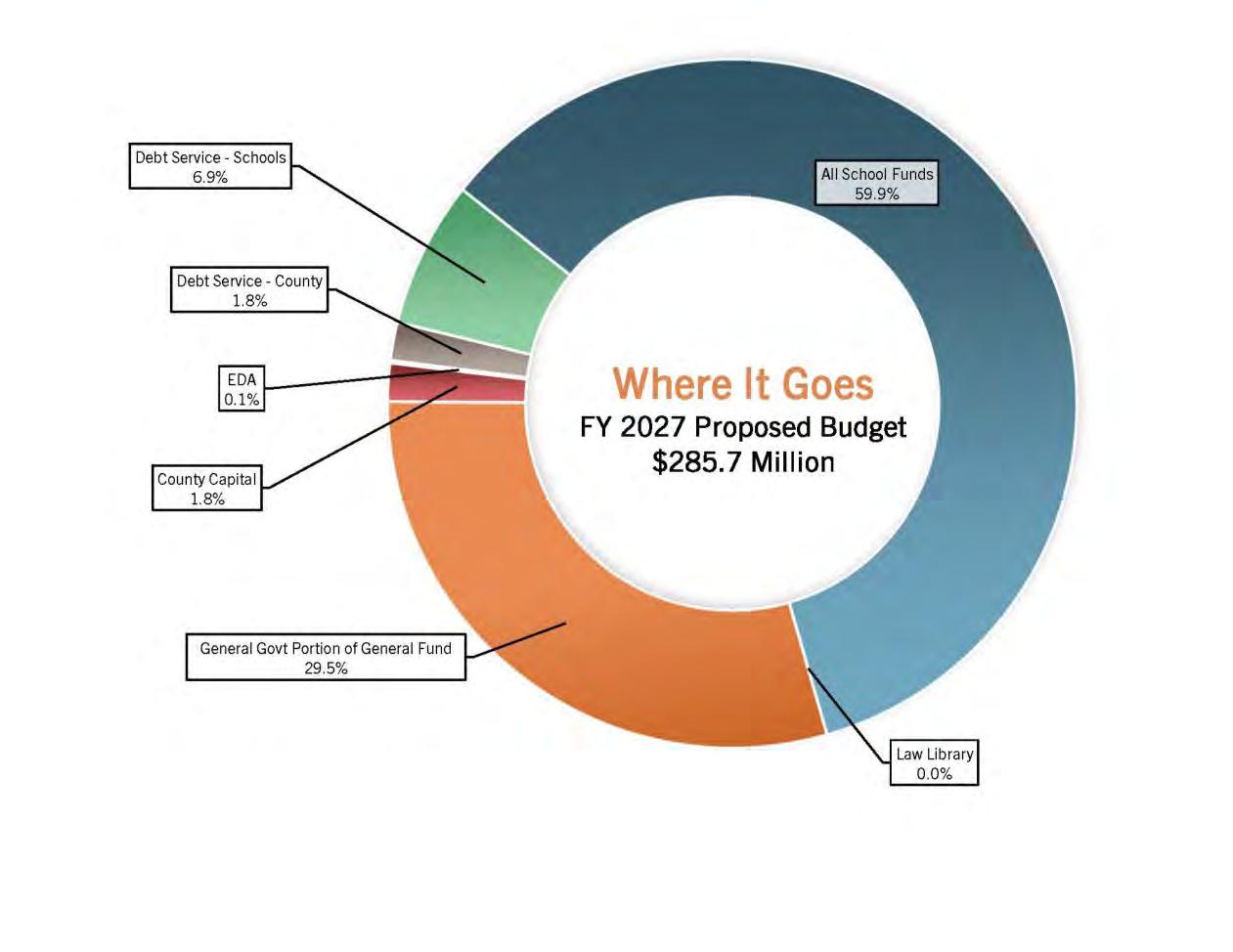

Proposed Funding: $285.7 Million

We worked intentionally together throughout the year to bring clarity to the County’s vision and priorities. In addition, both County and MCPS staff members have made adjustments this year to improve coordination, communication and overall budget planning. One example of this is the collaborative budget process calendar and timeline that outlines both key deadlines for the County and public schools as shown in the “Understanding the Budget” section (Appendix A) of the FY 27 proposed budget book.

The proposed FY 27 budget is a direct result of our collaborative work and shared direction. Our priorities remain consistent, yet we understand the need to adapt where and when appropriate to compensate for our community's growth.

Of the proposed $285.7 million budget, I am recommending:

• $190.7 million for Montgomery County Public Schools to include the school operating budget; the school nutrition fund; the school capital fund; and school debt service;

• $30.5 million for public safety, which includes the Sheriff’s Office; Western Virginia Regional Jail Authority; Montgomery County Fire and EMS Department; Volunteer Fire and Rescue Agencies; and the Animal Care and Adoption Center;

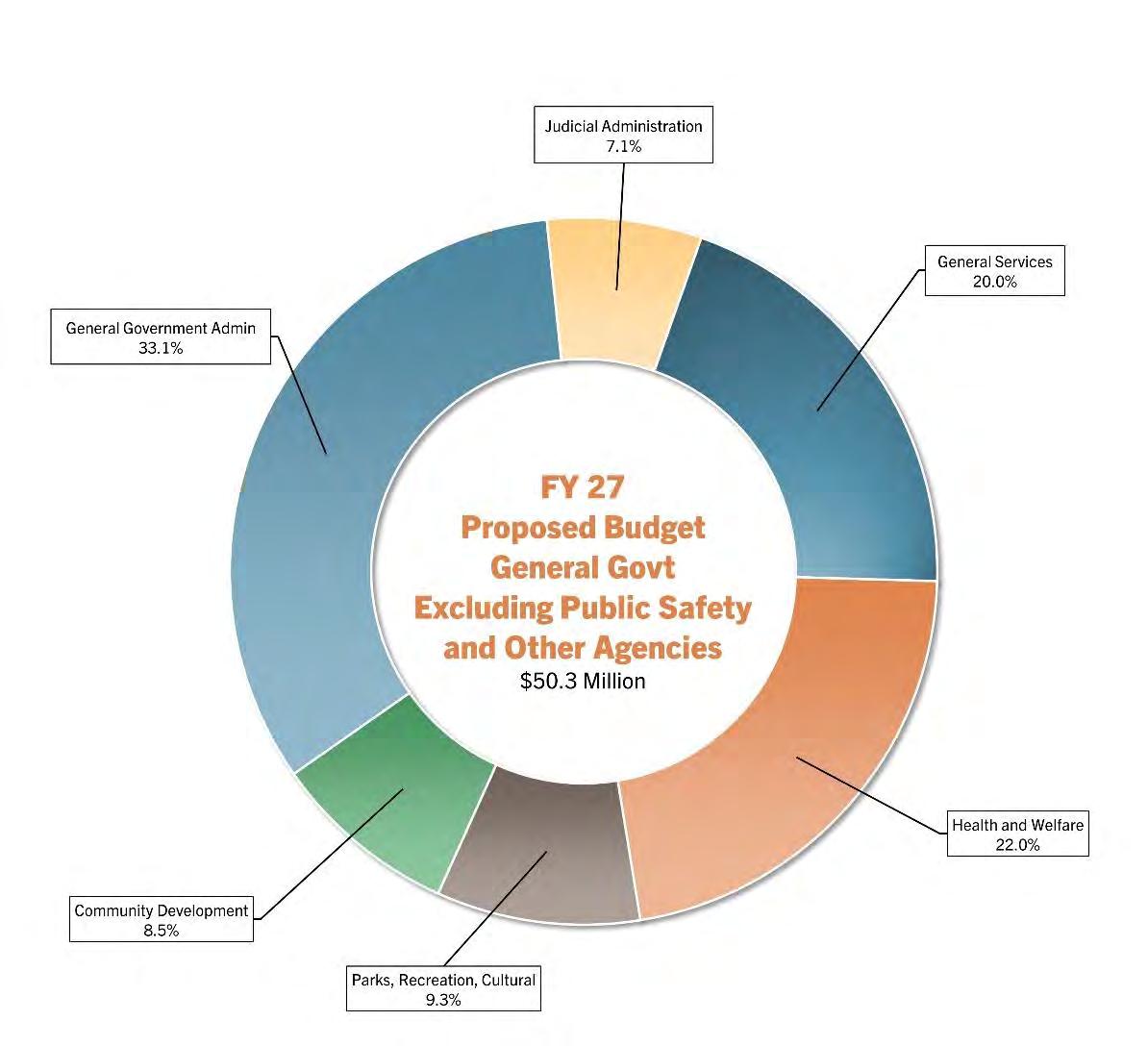

• $50.3 million for general government functions to include funding for general government administration; judicial administration; general services; health and welfare; parks, recreation, and cultural; and community development;

• $5.1 million for the County Capital Fund;

• $5.1 million for County debt service;

• $3.6 million for other agencies; and

• $0.4 million for EDA incentives

During the County’s budget analysis, we identified $0.8 million in one-time funding requests. These include equipment for the following functions: fire and EMS, technology, planning and GIS, library, the office of elections, solid waste and landfill remediation. These costs align with our priorities and support our commitment to providing superior customer service. They are outlined in the “Budget Summary” (Appendix C) of the proposed budget document and will be presented to the Board for approval

following adoption of the budget. With the proposed five-cent real estate tax rate increase, the County will receive approximately $3.2 million in unbudgeted revenue with the June 5, 2026, tax collection, a portion of which could be used to fund these items.

Public education continues to represent the largest share of the County’s annual budget. The proposed FY 27 budget allocates more than two-thirds of total County funding to Montgomery County Public Schools (MCPS), with the remaining portion supporting essential County services, including public safety, general government and judicial administration, health and welfare, parks, recreation and cultural programs, community development, and other agencies. This funding approach allocating more than two-thirds of the overall budget to public schools has been a long-standing practice for Montgomery County for many decades.

Because public education remains one of the Board’s highest priorities, the FY 27 proposed budget continues to dedicate a significant portion of County resources to MCPS. The proposed budget includes $4.1 million in new County undesignated funding for the MCPS operating fund. In addition, the budget reflects an estimated $3.8 million in increased state and federal funding for MCPS for a total proposed funding increase to the Schools Operating fund of $7.9 million.

Historically, the Board of Supervisors has demonstrated their dedication to public education by providing significantly more funding than the state’s required local effort for the Standards of Quality (SOQ) as demonstrated in the table below.

Source: Virginia Department of Education, Actual FY25 Required Local Effort and Required Local Match Report

The proposed budget also includes a dedicated 2.5 cent allocation of the real estate tax rate, generating approximately $3.2 million, to support MCPS capital projects.

Continued collaboration between the County and MCPS remains a key component of the budget development process. A joint meeting of the Board of Supervisors and the School Board is scheduled for Monday, March 16, 2026, to further discuss the FY 27 budget and to collectively address the needs of both the public schools and other government functions This meeting was strategically scheduled to provide an opportunity for further collaboration prior to setting the advertised tax rate. This meeting will occur after the March 9, 2026, presentation of the proposed budget and before the March 23, 2026, meeting at which the Board of Supervisors will set the advertised tax rate for the April 9, 2026, public hearing.

The accompanying chart illustrates the allocation of new designated and undesignated revenue and highlights the County’s consistent commitment to directing a substantial portion of new funding to MCPS. It is important to note that the Commonwealth provides significantly more designated funding to public schools than to local governments. While public education remains a top priority, the County must also balance limited undesignated revenue to address other critical needs, including public safety and core County services.

$14,000,000

$12,000,000

$10,000,000

$8,000,000

$6,000,000

$4,000,000

$2,000,000

Please note on the chart provided the increases in public safety funding over the past five years. In FY 22, the County began funding career EMS personnel for the first time ever, providing 24/7 coverage in the Eastern Montgomery and Riner areas In FY 25, the County responded to growing public safety needs in Eastern Montgomery by providing career firefighters from 7 a.m. to 7 p.m., seven days a week. In FY 26 the Board approved funding for eight deputies for the Montgomery County Jail; one investigator for the Sheriff’s Office; and 12 additional career firefighters to provide 24-hour fire service in Eastern Montgomery.

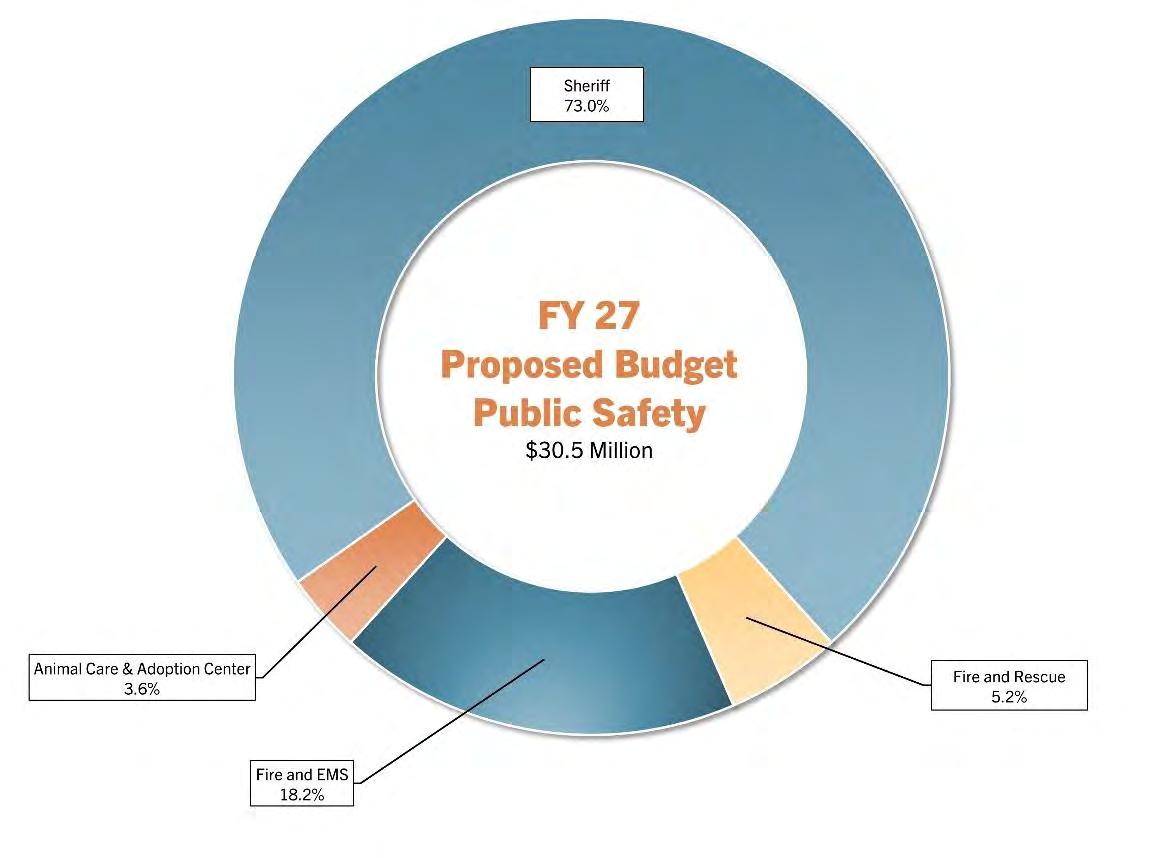

Public Safety: $30.5 Million

Public safety includes the Sheriff’s Office; Western Virginia Regional Jail Authority; Fire and EMS Department; Volunteer Fire and Rescue Agencies; and the Animal Care and Adoption Center In FY 27, 11 percent of the overall budget is proposed to be allocated to fund public safety needs. In total, I am recommending $30.5 million in funding to address identified public safety needs in FY 27.

In the fall of 2025, Montgomery County partnered with Mission CIT, LLC to complete a comprehensive study of the County’s Fire and Rescue/EMS system, including services provided in the towns of Blacksburg and Christiansburg and by the Virginia Tech Rescue Squad. The study will evaluate the current volunteer-career model and develop strategic recommendations for the future, with the goal of strengthening the volunteer system and enhancing coordination between the County and the towns to ensure the delivery of high-quality emergency services throughout the community.

The study will provide the information necessary to determine appropriate funding levels for the towns’ fire and rescue volunteer agencies. Funding requests received for FY 27 will be considered upon completion of the study.

The FY 27 proposed budget allocates $22.3 million for the Montgomery County Sheriff’s Office. This includes funding for School Resource Officers at all County schools, as well as deputies who provide law enforcement, civil process service, corrections, courthouse security, and conduct motor vehicle accident and criminal investigations. Special contingencies includes $200,000 to address deputy recruitment and retention.

Included in the Sheriff’s Office budget is an allocation of $5.6 million for the Western Virginia Regional Jail Authority Of that total, I am proposing additional funding of $301,772 to cover debt service and per diem costs based on the number of inmates housed at the jail. Both the debt service and per diem cost and the number of inmates are estimated to increase in FY 27.

One identified critical need is the County’s responsibility to deliver timely emergency assistance through trained professionals. The total amount budgeted for the Fire and EMS Department is $5.6 million. I am proposing $32,200 to fund basic operating increases such as motor vehicle insurance, counseling services, training and uniforms

Volunteer Fire and Rescue Agencies

The County provides annual operating funds to nine volunteer fire and rescue agencies. For FY 27, I am recommending $1.6 million for fire and rescue operational needs, which includes $20,626 in additional funding.

I am recommending a total FY 27 budget of $1.1 million for the Animal Care and Adoption Center (ACAC), which includes funding for one new position to address increasing service demands. The ACAC remains committed to operating as a no-kill facility amid a sustained rise in animal intake and a decline in animal adoptions. The proposed position is essential to expanding foster placement efforts, relieving capacity constraints and ensuring animals can continue to be accepted into care.

General Government Functions; General Government Administration; Judicial Administration; General Services; Health and Welfare; Parks, Recreation, and Cultural; and Community Development: $50.3 Million

The FY 27 proposed budget includes $50.3 million for general government functions, encompassing general government administration, judicial administration, general services, health and welfare, parks, recreation and cultural programs, and community development.

This proposed funding reflects a thorough internal budget review process that requires each department to present and justify its budget requests to the County’s leadership team. This process ensures all requests undergo rigorous evaluation before recommendations for general government functions are presented to the Board.

Guided by the Board of Supervisors’ priorities and a shared commitment to providing high-quality services to County citizens, the review process promotes interdepartmental collaboration, encourages discussion of operational challenges, and fosters a better understanding of departmental responsibilities. These efforts often lead to innovative solutions that balance limited resources with identified needs.

Beginning with the FY 25 budget, the County developed a strategic multi-year staffing approach to address the growing needs of our community and demonstrate our commitment to providing superior services to our citizens This plan recognizes that meeting growing service demands requires a phased and sustainable approach to staffing, rather than one-time or reactive position growth. As part of this effort, the County has identified the need for additional staff over multiple years to align workforce capacity with operational demand.

The Board has supported this strategic staffing approach, approving a significant number of requested new positions over the past three fiscal years. Position requests are evaluated annually and prioritized into the appropriate budget cycle. While each request reflects a legitimate operational need, it remains essential that workforce expansion be approached in a measured and purposeful manner. Balancing service demands with available funding, facility capacity, and long-term sustainability requires thoughtful prioritization to ensure continued fiscal responsibility while maintaining service levels.

For FY 27, departments submitted requests for 22.75 new positions. Consistent with the strategic approach, I am proposing funding for six new full-time positions and one part-time position in FY 27, including:

• Director of Real Estate Assessment in County Administration;

• Finance Manager in Finance;

• Solid Waste Manager, HVAC Technician, and a part-time Building Inspector in General Services;

• Adoption Foster Coordinator at the Animal Care and Adoption Center; and

• Family Services Specialist in Social Services.

The total cost associated with these proposed new positions is $625,522 for salaries and benefits, along with $16,800 for equipment and related expenses.

Annually, both the towns of Blacksburg and Christiansburg and MCPS typically provide two pay increases for employees an across-the-board adjustment combined with a step or merit-based increase. While the County does not currently provide a formal step or merit increase, we are in the process of designing and implementing a system for the next fiscal year. To remain

competitive with neighboring localities, I am recommending $1.3 million to fund a three percent pay increase for County employees in FY 27

As healthcare costs continue to increase, it is important to monitor and maintain adequate funding to cover the County’s self-funded employee health insurance program. For FY 27, the County is taking a two-step approach to provide additional funding in the health insurance fund.

Since the Human Resources department is the County interface with the service provider for the County’s on-site employee clinic, the clinic operating fees along with annual flu vaccinations and health plan consultant fees will now be charged to the Human Resources department rather than to the health insurance fund beginning in FY 27. Since FY 22, these costs have been paid from the fund; this change will make an additional $301,437 available to cover claims costs The same amount is added to the Human Resources budget for FY 27 to cover costs related to employee clinic fees and annual flu vaccinations, reinforcing the County’s commitment to employee wellness and preventive care.

The second step that will increase the health insurance fund is the addition of $250,000 to Special Contingencies. Both of these actions generate a total of $551,437 of additional funding in the health insurance fund for FY 27.

For FY 27, the County received funding requests totaling $0.6 million from 30 other agencies. I am recommending an additional $55,167 to support these requests. The FY 27 proposed budget includes a total of $3.6 million in funding for 51 outside agencies that support the Board’s priorities. A detailed listing of proposed allocations for these agencies begins on page 267 of the FY 27 proposed budget document.

The County’s annual proposed budget is developed by a dedicated and highly skilled financial team that carefully analyzes local, regional, and national trends and projections. The FY 27 proposed budget builds upon the County’s established financial practices and policies, which have contributed to a AA+ bond rating.

This budget reflects a continued commitment to financial strength and long-term stability through sustainable and responsible fiscal management by both the Board of Supervisors and County staff. While not all budget requests could be accommodated, the proposed FY 27 budget represents meaningful progress in supporting public education, public safety, and core County functions while balancing limited resources with identified needs.

In summary, the proposed FY 27 budget totals $285.7 million, with a real estate tax rate of 81 cents per $100 of assessed value. This budget addresses the needs of a growing community while remaining fiscally responsible, allocating 56 percent of new undesignated revenue to public schools, six percent to public safety, and 38 percent to general County functions.

A detailed budget timeline and calendar are included on page 63 of the proposed budget document. Key dates include work sessions in March and a public hearing scheduled for April 9, 2026 The deadline for

x

adoption of the FY 27 budget and tax rate is April 20, 2026, to accommodate the spring tax billing schedule.

I appreciate your continued leadership and support and welcome any questions as you review the proposed FY 27 budget.

Sincerely,

Angela M. Hill, CPA, CGMA County Administrator

Proposed Budget for Fiscal Year 2027

Proposed Budget for Fiscal Year 2027

Since its founding in the eighteenth century, Montgomery County has experienced a rich history in agriculture, manufacturing, and technology with ties to notable historical figures to include George Washington and even Daniel Boone. The county has experienced consistent growth throughout the years.

Montgomery County – which is home to two of the state’s four largest towns, Blacksburg and Christiansburg – is a high-tech community strategically located on the Interstate 81 corridor.

The county provides a full range of services to its approximately 102,000 residents to include: law enforcement; fire and rescue; planning and GIS; economic development; social services; courts; parks and recreation; general services; environmental services; animal control; libraries; and schools.

Montgomery County traces its origin to 1776 when it was formed and named after General Richard Montgomery, an American hero of the French and Indian War and the American Revolution. The first settlement, Draper’s Meadow, was established in the 1740s but was destroyed by Shawnee Indians during the French and Indian War.

Christiansburg, the county seat, was incorporated in 1792 and named in honor of Colonel William Christian. This community was an important stop on the Wilderness Road, which roughly corresponds to the present day U.S. Route 11. As the retail hub of the county, Christiansburg is host to several shopping centers and restaurants.

Blacksburg was incorporated in 1871. The town originated on tracts of land donated by William Black – for whom it was named – and was established at the same site as the previous settlement of Draper’s Meadow. Blacksburg is home to Virginia Tech, one of the nation’s leading educational institutions and research universities. The

town is also home to the Virginia Tech Corporate Research Center.

Graduates from area colleges and universities add to the abundant, educated workforce to make a probusiness community with a solid mix of high-tech, manufacturing, retail and professional services –including a variety of Fortune 500 firms.

The graphics and charts provided below have been obtained from the Labor Market Information report provided by the Virginia Employment Commission.

Status of our Economy: Expected to outgrow our urban neighbor by 2030.

Source: Weldon Cooper Center for Public Service, U.Va., 2017.

Population by Gender

Source: 2020 Census.

Source: 2020 Census.

30-39 years 20-29 years 10-19 years 0-9 years

40-49 years

50-59 years

60-69 years

80 years and over 70-79 years

Projected Population Change

Source: U.S. Census Bureau, Virginia Employment Commission.

Projected Population Change: Montgomer y County

Montgomery County maintains a few of the very industries that were popular at its inception including agriculture and manufacturing. In addition, technology, health care, education, retail, hospitality, and food service are now among popular industries throughout the county. According to the Local Area Unemployment Statistics by the Virginia Employment Commission, Montgomery County consistently maintains an average unemployment rate that is lower than the national average, with a recorded rate of 4.4 percent compared to the national rate of 4.6 percent as of July 2025.

Source: Virginia Employment Commission, Economic Information & Analytics, Local Area Unemployment Statistics.

Source: Virginia Employment Commission, Economic Information & Analytics, Quarterly Census of Employment and Wages (QCEW), 1st Quarter (January, February, March) 2025.

Proposed Budget for Fiscal Year 2027

The FY 27 County budget for all funds (net of transfers) totals $285.7 million. The General Fund budget totals $185.1 million, including transfers to other funds, such as the School Operating Fund. The School Operating Fund totals $161.6 million, including the transfer from the County of $69.4 million. The general government portion of the General Fund (net of transfers to other funds) totals $84.4 million and the School Operating Fund (net of transfers) totals $160.8 million. The total County budget also includes the Debt Service Fund ($24.8 million), the Law Library Fund ($17,600), the School Nutrition Fund ($7 million), funding for County Capital ($5.1 million), School Capital ($3.2 million), and the Economic Development Authority Incentive Program ($0.4 million).

The FY 27 proposed real estate tax rate is 81 cents per $100 of assessed value. The FY 26 approved rate was 76 cents. The FY 27 proposed budget includes a five-cent real estate tax rate increase.

P r o p o s ed Bud get

$285.7 Million

The following highlights major changes in expenditure areas. Detailed explanations of the expenditure recommendations can be found in the Expenditure Plan section of the document. A recap of expenditures by fund, County dollars by division, position (FTE) listing, and a graphic summary of the FY 27 proposed budget are included in the Appendices.

The FY 27 proposed budget includes funding to cover the cost of a 3% compensation increase for classified and part-time non-classified County employees July 1, 2026, and funding to maintain the County’s Compensation and Classification Pay Plan.

In the area of General Administration, the following major budget changes were made for FY 27:

Revenue Sharing – funds are added to cover the increased Transient Occupancy, Sales, and Meals Taxes collected in the 177 Corridor based on the agreement with the City of Radford.

County Administration – funds are added for a Director of Real Estate Assessments (one FTE) to oversee the valuation of real property for tax purposes.

Public Relations and Community Engagement – funds are added to support annual software maintenance costs and an increased number of Canva software licenses.

Human Resources – funds for the Employee Health Clinic are moved from the self-funded health insurance fund to the Human Resources division to more effectively monitor and maintain adequate funding to cover the employee insurance program.

Management and Budget – funds are added to cover the increased cost of producing the proposed and approved budget books and approved CIP book.

Finance – funds are added for one Finance Manager position (one FTE) to supplement existing staff and assist in completing financial statement audits, which have increasingly complex regulatory requirements, in a timely manner.

Information Technology – funds are added to cover new software programs, software maintenance service contracts, and hardware costs for new positions.

Treasurer – funds are added for DMV administrative fees charged to the County and increases in printing, binding, and postage costs.

Electoral Board – funds are added to purchase additional equipment to assist with same day registration needs in the largest voting precincts, as well as for increased postage costs.

General Contingencies – funds are added to the General Contingency Budget to meet the County’s financial policies of retaining 1% of the County’s general government portion of the General Fund to cover contingency needs.

Special Contingencies – funds are added to the Special Contingency Budget to cover the cost of a 3% compensation increase for classified and part-time non-classified County employees July 1, 2026. An additional $250,000 is added to cover potential increases in County health insurance costs for FY 27, $225,000 is added to offset increased Worker’s Compensation insurance premiums, $200,000 is added to evaluate the compensation structure for the Sheriff’s office, and $200,000 is also included in the base to maintain the County’s compensation and classification plan for all other employees throughout the County.

Other small changes to the Board of Supervisors, County Attorney, and Commissioner of Revenue are due to changes in personnel costs due to turnover savings and benefit changes between FY 26 and FY 27.

In the area of Judicial Administration, the following major budget changes were made for FY 27:

Commonwealth Attorney – funds are added to the base budget to cover one Assistant Commonwealth Attorney that was added by the state in FY 26. Funds are also added to supplement the current office supplies budget in FY 27.

Circuit Court – funds are added for recurring costs associated with the courtroom evidence presentation system.

Clerk of the Circuit Court – funds are added to the base budget to cover one Deputy Court Clerk position that was added by the state in FY 26.

In the area of Public Safety, the following major budget changes were made for FY 27:

Sheriff – funds are added to cover the costs for debt service and inmate per diem expenses at the Western Virginia Regional Jail.

Fire and EMS – funds are added for increased vehicle insurance premiums, training, professional services, purchase of outerwear for EMS staff, and software maintenance increases. The slight reduction in the Fire and EMS division is due to staff turnover savings from FY 26 to FY 27.

Fire and Rescue – funds are added for Riner Fire Department to offset cost increases in training, repairs, and maintenance and to the Special Operations Team for uniforms for new members. The slight reduction in Fire and Rescue is due to a transfer of funds from Elliston Fire Department to General Services to cover the cost of utilities and repairs and maintenance to that facility.

Animal Care and Adoption Center – funds are added for one Adoption/Foster Coordinator position (one FTE) to focus on dog fosters and adoptions.

In the area of General Services, the following major budget changes were made for FY 27:

General Services – funds are added to cover the costs of one part-time Building Inspector position (.75 FTE), one Solid Waste Manager (one FTE), and one HVAC Technician position (one FTE). Funds are also added for trash and recycle container replacements, groundwater monitoring and corrective actions at Thompson and Mid-County landfills, housekeeping supplies, utilities, fee payments, uniform costs for new staff, training, and agricultural supplies for additional acreage gained.

In the area of Health and Welfare, the following major budget changes were made for FY 27:

Public Health – funds are added for the New River Health District based on projected state funding and local matching requirements.

Social Services – funds are added to the base budget to cover one Family Services Specialist position that was added due to the Resource Family Collaborative grant program awarded for FY 26. In addition, funds are added for an additional Family Services Specialist (one FTE) to provide services and assistance to the adult population as a result of new guardianship requirements, and for assessment needs of the elderly for nursing home placement.

Other small changes to the Human Services and Social Services are due to changes in personnel costs due to turnover savings and benefit changes between FY 26 and FY 27.

In the area of Parks, Recreation, and Cultural, there were no significant budget changes for FY 27. The small reductions in both divisions are due to changes in personnel costs due to turnover savings and benefit changes between FY 26 and FY 27.

In the area of Community Development, the following major budget changes were made for FY 27.

Economic Development – funds are added for mowing costs for additional acreage in Falling Branch, Phase II.

Utilities Division – PSA staff and daily operations officially transitioned to Montgomery County October 1, 2025. The integration of utilities services into a County department provides multiple opportunities for improvement including streamlined administration to support stronger customer service.

The small reduction in Planning and GIS is due to changes in personnel costs due to turnover savings and benefit changes between FY 26 and FY 27.

Other Agencies requests are evaluated each year based on existing funding agreements, board directives, and funding alignment between local government support in the New River Valley. Significant increases were provided to the New River Valley Emergency Communications Regional Authority, the Virginia Cooperative Extension, and the Community Services Board for FY 27. The large reduction in Economic Development Agencies is due to a local match requirement for federal grant funds supporting station facility construction improvements for the New River Valley Passenger Rail that is no longer needed in FY 27.

Transfer to the School Operating Fund

County funding in the FY 27 budget for the School Operating Fund totals $69.4 million, which is an increase of $4.1 million over the FY 26 approved budget.

Transfer to the Debt Service Fund

Funds are transferred to the Debt Service fund to cover the cost of County and School debt service.

Transfer to the School Capital Fund

2.5 cents of the real estate tax rate are earmarked for the School Capital Fund.

Transfer to the Economic Development Authority (EDA) Funds are transferred to the EDA for economic development incentives.

Transfer to the County Capital Fund

1.5 cents of the real estate tax rate are included for Fire and Rescue capital needs and 1 cent of the real estate tax rate is earmarked for future capital projects, which includes $100,000 for the Valley to Valley Trail project. In addition, $1,300,000 is transferred to address County capital maintenance needs. Other monies include $425,000 for the Parks Revitalization project and $210,000 to address technology infrastructure issues.

Proposed Budget for Fiscal Year 2027

Proposed Budget for Fiscal Year 2027

BUDGET SUMMARY, APPENDIX

Proposed Budget for Fiscal Year 2027

During the FY 27 budget process, County divisions made several one-time funding requests. These one-time funding items were excluded in the FY 27 Proposed Budget because they can be funded with one-time only money, which would reduce the overall cost of the budget and avoid any impact on the tax rate for FY 27. One-time funding of $832,434 will be requested in July 2026. Following are the specific items to be addressed.

• $71,000 in One-Time Funding for Information Technology Needs – $71,000 in one-time funding is needed in FY 27 for one-time labor costs to improve the network infrastructure, increasing reliability and connectivity.

• $21,960 In One-Time Funding for Office of Elections Needs – $21,960 in one-time funding is needed in FY 27 for twelve additional Poll Pads for the County’s largest precincts to accomodate same day registration. The associated recurring costs total $3,600 and are included in the FY 27 proposed budget.

• $148,869 In One-Time Funding for Sheriff’s Department Needs – $148,869 in one-time funding is needed in FY 27 to pay down Montgomery County Sheriff’s Office employees’ compensatory time balances to 240 hours, for those whose balances currently exceed that amount. Currently, employees are not compensated for this time until they either leave the department or reach the maximum federal limit of 480 hours. Allowing this option will have a positive and measurable impact on departmental performance by improving morale, job satisfaction, and engagement. Moreover, adding this option would bring MCSO more in line with surrounding law enforcement agencies who pay for overtime, as well as reduce the number of compensatory leave hours carried on the books for future payout by the County.

• $337,700 In One-Time Funding for Fire and EMS Needs:

• $187,700 in one-time funding is needed in FY 27 to purchase equipment for a Whole-Blood Program capable of storing and administering whole blood to trauma patients who need it, replace and upgrade three cardiac monitors, and purchase a stairchair to assist with moving patients out of areas with steps.

• $150,000 in one-time funding is needed in FY 27 to replace and upgrade stabilization equipment carried on the department’s heavy rescue truck to address reliability, safety, and capability gaps when responding to heavy vehicle crashes, industrial/agricultural entrapments, and other complex rescue incidents.

• $195,000 in One-Time Funding for General Services Needs:

• $65,000 in one-time funding is needed in FY 27 to replace aging and failing compactor equipment at the Merrimac Consolidated Site.

• $130,000 in one-time funding is needed in FY 27 for professional groundwater monitoring services at Thompson Landfill to stay in compliance with DEQ and implementation of a corrective action plan, including well drilling and media injection for three new wells and additional reporting. The recurring costs total $23,000 and are included in the FY 27 proposed budget.

• $32,000 in One-Time Funding for Library Needs – $32,000 in one-time funding is needed in FY 27 to replace outdated routers. The current hardware will no longer be supported after October 2026. This purchase will preserve current connection capability and network security for the branches. Without licensed vendor supported routers, no online services except public wireless would function. The library automated system, office applications, cataloging and acquisitions, calendaring and scheduling, public catalog, public internet, and staff internet all rely on these routers to function.

• $25,905 in One-Time Funding for Planning and GIS Needs:

• $8,000 in one-time funding is needed in FY 27 for the purchase of a large-format plotter to improve efficiency, accuracy, and service delivery for both the Planning and GIS Department and other County departments. The current plotter is nearing the end of its expected lifespan.

• $17,905 in one-time funding is needed in FY 27 begin the implementation of the Montgomery Matters Comprehensive Plan’s land use recommendations. This work will assist in coordinating the recommendations and outcomes of the Comprehensive Plan into the Zoning Ordinance update project.

One-time Items Removed from FY 2027 Proposed Budget

Proposed Budget for Fiscal Year 2027

Summary of Full-Time Employees/Equivalents

Proposed Budget for Fiscal Year 2027

Graphs

G ener a l G o v er nment

C o unt y F und i ng f o r S cho o l O p er at i ng

S cho o l Fund s F Y 2 0 2 7 P r o pos ed Budget $ 1 7 1 . 1 mi l l i o n

Proposed Budget for Fiscal Year 2027

Proposed Budget for Fiscal Year 2027

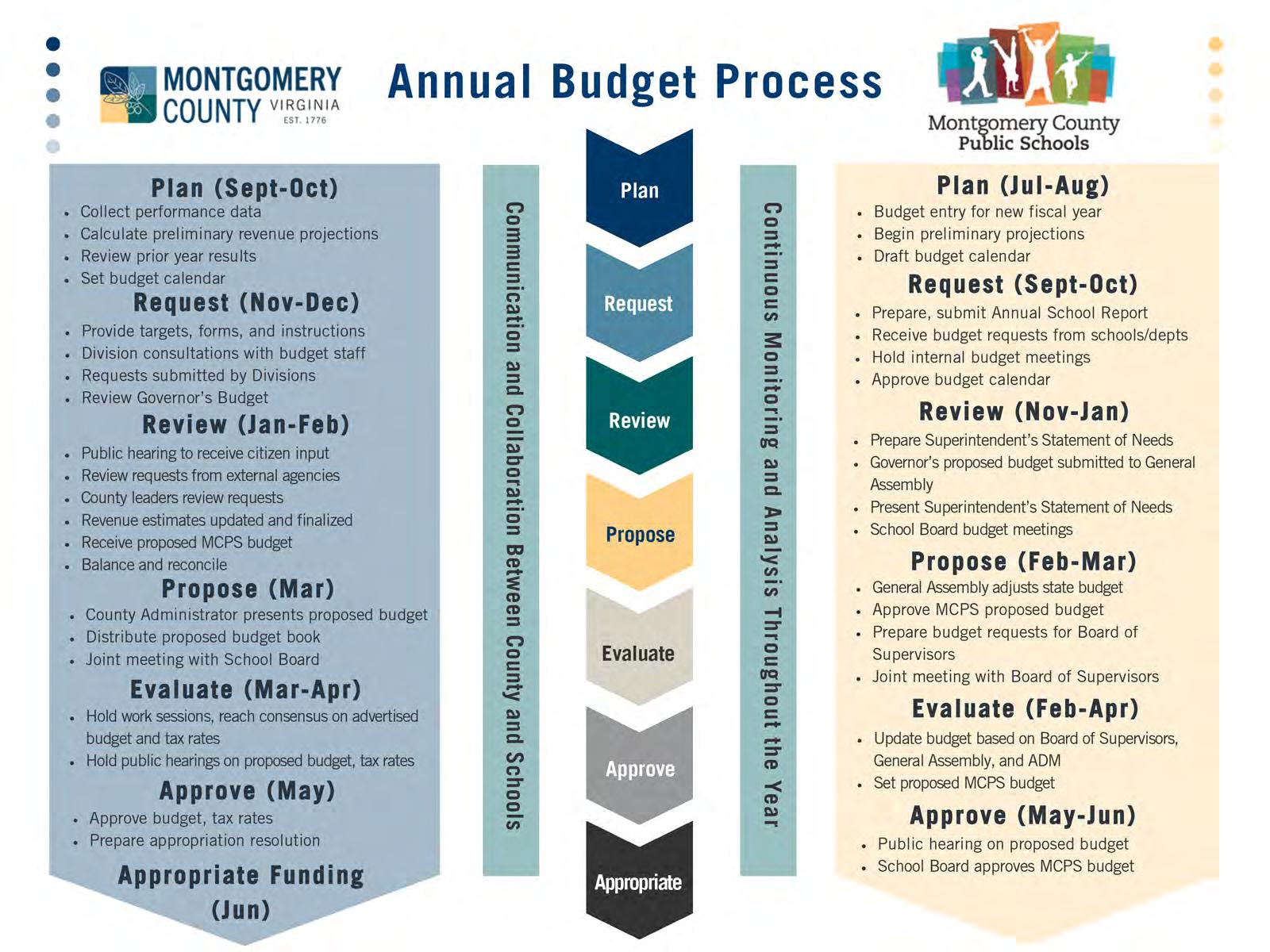

Montgomery County’s annual budget begins with the development of the proposed budget, the budget recommended by the County Administrator, and ends with the approved budget, which has been reviewed, adjusted and approved by the Board of Supervisors (Board).

The County’s annual budget process begins in the fall of each year, when divisions, departments and agencies submit budget requests for the upcoming fiscal year. In January and February, County staff develop the proposed budget. The proposed budget and budget document are presented to the Board in March of each year. During that time, the Board begins deliberations to adjust the budget and develop the County’s approved budget. During budget deliberations, the Board holds public hearings for citizen comments and conducts work sessions. Citizen comments assist the Board of Supervisors in making decisions regarding spending. After budget adjustments, the final approved budget is adopted in April and becomes effective July 1. The budget runs on a fiscal year basis and is effective July 1 through June 30. The County’s 2027 Budget Calendar is shown below (some changes may occur during the process):

July - August 2025

Prior year-end expenditure and revenue analysis; revenue analysis for FY 2027 begins.

SeptemberOctober 2025 Budget targets and budget instructions are developed for FY 2027 Proposed Budget.

November 2025 FY 2027 budget forms and instructions are sent to county divisions and external agencies.

December 2025

Budget requests for FY 2027 are due.

January - February 2026 Staff begins the development of the FY 2027 Proposed Budget.

Jan. 26, 2026 7:15 PM Public Hearing for citizen input.

Feb. 9, 2026 7:15 PM Revenue estimates. (Work Session)

Feb. 23, 2026 7:15 PM Superintendent presents the Proposed FY 2027 MCPS budget to the Board of Supervisors. (Work Session)

Mar. 9, 2026 7:15 PM Presentation of the FY 2027 Proposed Budget.

Mar. 16, 2026 7:00 PM Joint meeting with MCPS. (Special Meeting)

Mar. 23, 2026 7:15 PM Establish advertised tax rate and advertised budget. (Work Session)

Apr. 9, 2026 6:30 PM Public Hearing on advertised tax rate and budget. (Special Meeting)

Apr. 20, 2026 6:30 PM Adopt budget and establish tax rate. (Special Meeting)

May - June 2026

Year-end revenue and expenditure estimates are finalized for FY 2026 and transfers are made to close the year.

July 1, 2026 New Fiscal Year begins.

JANUARY

CALENDAR KEY: Regular Meeting Work Session

The County’s budget is the government’s estimated revenues and expenditures for the fiscal year that begins on July 1 and ends on June 30. It consists of operating and capital budgets for county programs and services. The budget also allocates funds for the operating and capital needs of the public school system and contributes to a number of other agencies.

The County’s budget consists of the following funds:

• General Fund – which provides funding for the day-to-day operations of the County government.

• Law Library Fund – which provides funding for the day-to-day operations of the law library.

• School Operating Fund – which provides funding for the day-to-day operations of the School system.

• School Nutrition Fund – which provides funding for the day-to-day operations of the School food program.

• County and School Capital Funds – which provides an annual cash-to-capital allocation for new county and school capital needs.

• Debt Service Funds – which provides funding to cover the County and School’s outstanding debt obligations.

• EDA Incentive Fund – which provides funding for economic development initiatives.

In November of each year, County divisions are provided with budget targets for the upcoming fiscal year. The base budget target represents the base of personnel and operating costs anticipated for the upcoming year based on the prior year approved budget with adjustments made for personnel changes and mandates. One-time only funding from the prior year is excluded from the base budget. Along with the base budget target, County divisions are also provided the opportunity to request addenda items, which represent dollars over and above the base budget.

Base Budget Targets allow for the delineation between previously approved funding levels and requested increases.

Base Budget Targets are established as follows:

• Personal Services - Includes all positions approved up to the issuance of the proposed budget and covers the estimated costs in fringe benefits.

• Operations and Maintenance - Caps funding at the level of the prior year approved budget, less adjustments for one-time only expenditure items.

• Capital Outlay - Most capital outlay is removed from the base budget target as typically it is a nonrecurring expense. Some divisions maintain a permanent capital outlay allocation as they utilize the funding on a yearly basis to replace equipment on an existing replacement plan. Examples include motor vehicle and computer replacements.

Addenda Requests are increased funding over and above the Base Budget Targets. They must be presented as Addenda to the Base Budget. This means that additional justification for increased funding or the inclusion of capital outlay dollars must be provided with the request.

These adjustments are designed to clearly identify increases to operations and initiatives proposed by departments. The chart below illustrates the process.

Estimated costs for continued operations

Based on prior year approved budget with adjustments

Excludes: Office Furniture Other Equipment

over and above the base budget target for operating and capital items

Dollars requested for new or expanded services (initiatives)

All budget requests (base budget request and addenda) are due in December of each year and are evaluated for inclusion in the upcoming budget. When making budget requests, County divisions must address the following:

• Is there sufficient workload to justify the request?

• Is there sufficient need to justify the request?

• Is the request related to a state or federal mandate?

• Are there legal requirements that will not be met if the request is not funded?

• Is the request linked to a specified outcome that is community or board driven?

• What tangible benefits can the County expect to experience as a result of funding the request?

All budget requests are evaluated based on available funding and the justification listed above.

With the goal of allowing decision-makers to focus on broader issues, the budget document consolidates similar

functions. The FY 2027 budget continues to consolidate information and array budget data in ways that facilitate a broader understanding.

This budget document includes both the County’s general government operating budget, the Montgomery County Public Schools’ operating and nutrition budgets, the law library budget, County and School capital budgets, the debt service budget, and the economic development incentive budget.

The FY 2027 budget document is organized into 20 major headings, each of which is separated by a large divider tab:

• Budget Message

• Table of Contents

• Budget Summary

• Understanding the Budget

• Revenue Summary

• Summary by Function

• Expenditure Plans

• General Government Administration

• Judicial Administration

• Public Safety

• General Services

• Health and Welfare

• Parks, Recreation, and Cultural

• Community Development

• Other Agencies

• Transfers

• Law Library

• Education

• Debt Service

• County Capital

Included under the last section; Expenditure Plans, are the 34 major County Divisions or budget categories, which include Division expenditures, revenues earmarked for use by the specific Division, and County funding provided. Each of these sub-sections includes the Division’s Organizational Chart, Financial Data, Personnel, Key Performance Indicators (KPIs), Description of the Division, Base Budget Discussion, Addenda Discussion, which includes the County Administrator’s recommendation. Also included are each Department’s Description and Financial Data.

Division Financial Data - Provides a recap of the Division’s funding history, including the Base Budget and addenda requests, and recommended funding by three categories:

• Personal Services

• Operations and Maintenance

• Capital Outlay

Department Description and Financial Data - Presents historical budget data by major category for each department. The following column headings are used:

• FY 25 Revised Budget

• FY 25 Actual Budget

• FY 26 Approved Budget

• FY 27 Base Budget

• FY 27 County Administrator’s Recommended Addenda

• FY 27 County Administrator’s Recommended Total

The County Administrator’s Recommendation column identifies the amount of funding recommended for each major cost category by base budget and addenda.

Revenue that has been designated to offset expenditures in divisions is also presented. These sources include State Compensation Board funding, fees and permit charges collected by the respective divisions and other sources related to each specific function. In the presentation format, designated revenues are totaled and subtracted from the expenditures, identifying the amount of the County’s undesignated general fund revenue needed to support the division’s expenditures.

The County’s General Government portion of the General Fund (which consists of individual county divisions) have been further consolidated into 8 functional areas: General Government Administration; Judicial Administration; Public Safety; General Services; Health and Welfare; Parks, Recreation, Cultural; Community Development; and Other Agencies. Appropriation control is set at these functional areas.

After the budget is approved by the Board, the final approved budget is appropriated and becomes effective July 1. After July 1, the Board makes adjustments through additional appropriations. The budget is an estimate; therefore, as revenues and expenditure needs change, the appropriation may be adjusted. This can mean additional appropriations or reductions of appropriations. If the budget amendment exceeds 1% of the total expenditures shown in the currently adopted budget, the Board will hold a public hearing to gather citizen input. These adjustments are approved at the Board level.

Each month, the Board holds public meetings where appropriations are approved if necessary. After these approvals, the appropriations are entered into the County’s financial system. Expenditures can then be made by the division using the budget adjustment. The County’s accounting system separately keeps track of the County’s original and revised budget. The revised budget changes throughout the year as appropriations are adjusted.

The County’s accounting system is organized and controlled on a fund basis. The basis of accounting refers to the accounting method the County utilizes to recognize revenues and expenses. There are three ways in which a governmental entity can recognize revenue and expenses: cash, accrual, modified accrual basis. Under the cash basis method, revenue is recognized when cash is received and expenses are recognized when paid. Under accrual basis, revenue is recognized when earned and expenses are recognized when incurred. Modified accrual basis is a hybrid of cash basis and accrual basis. It recognizes revenues when they become both measurable and available. Expenditures are generally recognized when the related fund liability is incurred.

The County operates on the modified accrual basis of accounting for both budgetary and accounting purposes.

This means that the County recognizes revenues when they become both measurable and available. Expenditures are generally recognized when the related fund liability is incurred.

Division directors are responsible for individual budgetary compliance. Divisions are required to monitor and adjust their individual budgets and spending habits as needed throughout the year. They are required to stay within their approved expenditure authority.

The County’s Office of Management and Budget monitors budgetary compliance at the macro level to ensure compliance with the County’s financial policies. With the consolidation of County divisions into the 8 major functional areas: General Government Administration; Judicial Administration; Public Safety; General Services; Health and Welfare; Parks, Recreation, Cultural; Community Development; and Other Agencies; budgetary control has been set at each major functional area. Division directors are still required to stay within their approved division expenditure authority; however, the County Administrator has the ability to approve transfers within each major function without board approval. Within each division, directors can move funds between individual line items, with the exception of salary line items, which require approval of the Finance Director or the Budget Director.

Allowing the County Administrator to approve transfers within each major function without board approval provides better operational efficiency and reduces the number of budget amendments required annually.

The Board of Supervisors uses this combination of documents and information to review and approve the annual budget. It is available as public information for review by any citizen who requests access to it and is found on the County’s web site at www.montva.com. A glossary of financial terms begins in the following section in an effort to assist citizens in reviewing and understanding the County’s budget. If you have any questions about the County’s budget or the budget process, please contact Montgomery County’s Office of Public Relations and Community Engagement at 540-382-5700.

Addenda Request

The request for funding amounts over and above the designated Base Budget targets.

Appropriation

An approval by the Board of Supervisors for County staff to make an expenditure or to incur debt using government resources. These are usually for specific, stated amounts over a one-year period.

Appropriation Resolution

An official act by the Board of Supervisors providing staff the legal authority to obligate or spend County funds.

Approved Budget

The budget enacted by the Board of Supervisors.

Assessed Value

The fair market value placed by the Commissioner of Revenue on personal and real property owned by County citizens. Real estate values are reassessed every four years.

Base Budget

A budget that shows how much it would cost in the next fiscal year to operate the same programs approved in the current year.

Basis of Accounting

The basis of accounting refers to the accounting method the County utilizes to recognize revenues and expenses.

Budget

A financial plan for operating the County using estimates of costs (expenditures) and proposed methods for offsetting those costs (revenues).

Budget Calendar

The County’s schedule of deadlines and events related to preparing and adopting the next year’s budget.

Budget Document

The County staff’s official report, which presents the proposed budget to the Board of Supervisors.

Budget Message

The County Administrator’s written synopsis of the proposed budget. This message analyzes budgeting issues and specific programs within the context of the County’s economic climate. In addition, it gives the County Administrator an opportunity to highlight certain noteworthy recommendations.

Fixed assets with a value of at least $5,000 and an anticipated useful life of more than one year. Furniture and equipment are examples of fixed assets.

Capital Improvement Program

The County’s five-year plan for completing capital projects on an annual basis, with tentative beginning and ending dates for each, and anticipated costs and options for financing them.

Large one-time construction projects or purchases that are expected to provide services to citizens over a period of time. Examples of capital projects are the construction of new schools, fire stations, etc.

Special monies set aside for unforeseen costs or emergencies, or for special purposes that may require further analysis.

The repayment of County debt, including principal and interest.

Expenditures

The cost of, or payment for, goods and services used in County operations.

Full Time Employee or Full Time Equivalent.

Fiscal Year

The County’s financial reporting year, which begins on July 1 and ends on June 30 of the next calendar year.

An overall activity performed by a division or organization. The County’s budgets are divided into personal services, operations and maintenance, and capital outlay.

The part of the budget that accounts for day-to-day operating expenses for the County, including dollars transferred from the General Fund for support of the School System.

A promise from County government to pay for bonded debt (essentially a loan) based on its full faith and credit or basic power to pay debts with tax revenue. These bonds are used to finance long-term projects through payments of principal and interest over a period of years.

Grant

A gift of assets, usually cash, by one source to another organization. The County receives most of its grants for specific projects or programs from the federal or state government. However, private foundations sometimes contribute funds to the County.

The initial budget prepared for and proposed to the Board of Supervisors by the County Administrator.

Income or increased assets for a specific fund.

Under the lease revenue method, the County transfers a “lease hold interest” (the legal right to use the property) to the Economic Development Authority (EDA). The EDA then “leases back” these facilities and projects to the County for a term equal to the debt service term. The lease payments cover the debt service term. These issuances

are also structured with a Trustee, who must enforce all obligations. Consequently, the Trustee collects rental payments, pays bondholders, and monitors requisitions on the use of funds and issues checks to vendors from the proceeds.

The total dollar amount of tax that should be collected based on existing tax rates and assessed values of personal and real properties.

The level at which taxes are imposed or charged for certain property owned by citizens and businesses.

The Virginia Employment Commission’s (VEC’s) report of persons who are actively filed as not holding, but are seeking, a job for which they would receive compensation. This does not include persons who have no job, but do not consult the VEC for job placement services.

Proposed Budget for Fiscal Year 2027

Proposed Budget for Fiscal Year 2027

Montgomery County’s general revenue forecast is developed based on past revenue trends, current revenue collections, and current and future local growth patterns. The County’s local economy, along with state and federal influences, contributes to the revenue picture. Budget staff, with data from the Commissioner of the Revenue and Treasurer offices, work throughout the year evaluating revenue trends, collection rates, and growth patterns to determine the revenue projection.

Local, state, and national economic conditions all influence the local fiscal environment. The County’s revenue structure, job base, and major economic contributors provide a strong foundation for sustained growth. Montgomery County is home to Virginia Tech, the second largest public university in Virginia. Virginia Tech is also the largest employer in the County, providing jobs for approximately 13,000 employees. Montgomery County is fairly unique in that Virginia Tech’s presence in the community provides a stable foundation for economic growth. However, even with the presence of a stable and large employer, the local economy remains heavily dependent on the broader state and national economies. These broader economies are some of the most important factors in predicting increased revenue growth, even at the local level.

The sudden onset of the pandemic in March of 2020 created a host of challenges for the economy and revenue forecasting. In March of 2020, the Coronavirus Aid, Relief, and Economic Security Act, also known as the CARES Act, provided direct cash stimulus payments to individuals, as well as economic assistance to workers, businesses and state and local governments. In December of 2020, a second pandemic relief package provided direct cash stimulus payments to individuals, as well as economic assistance to workers and businesses. In March of 2021, the Federal Government passed the American Rescue Plan Act, a third round of legislation totaling $1.9 trillion, that provided additional direct aid, added unemployment benefits, and $350 billion of aid to state and local governments.

As the government responded to the pandemic, the Federal Reserve (America’s Central Bank) decreased interest rates sharply to near zero and increased its balance sheet through Quantitative Easing (QE) to increase the money supply. Easy money, coupled with supply chain issues and increased demand for goods and services, created inflationary pressure. Inflation started to rise in November of 2021 and hit 40-year highs, peaking in June of 2022. To address this surge in inflation, the Federal Reserve began increasing interest rates in March of 2022. The Federal Reserve increased the federal funds rate from near zero to a peak target rate of 5.25% to 5.5% in July of 2023. As inflation eased and the economy cooled over 2023 and 2024, the Federal Reserve began reducing rates. The current federal funds target rate (as of February 2026) is 3.5% to 3.75% and represents a 1.75% reduction since the peak rate in July of 2023. The Fed has signaled the potential of two additional rate reductions in 2026, targeting a federal funds rate of around 3% to 3.25%. The Neutral Rate, the rate at which monetary policy is neither contractionary nor expansionary, is estimated at 3%.

The condition of the County economy is greatly affected by national and state economic conditions.

National Economic Outlook

Evaluating the current state of the economy is difficult as there is often a lag between when information and data are available and the County’s ability to evaluate the impact of that information and data. The U.S. economy continues to remain strong. Some economists suggest that the US is in a K-shaped economy in which the top 20% of Americans are spending and keeping the economy strong, while the bottom 80% of Americans are struggling. This K-shaped economic growth is likely to continue throughout 2026.

While there is some uncertainty around fiscal and monetary policy decisions, the overall US economic outlook for

2026 is positive with moderate growth projected. The labor market is expected to stabilize and GDP is projected to expand as the drag from tariffs subsides. Inflation, however, is still above the Fed’s 2% target rate and is projected to remain above that target through 2028. Most analysts agree that a recession is unlikely in 2026; however, there are still risks to the economy. Labor market uncertainty, higher unemployment and inflation above the targeted 2% could create a drag on the economy.

GDP is one of the broadest measures of the economy. This measure affects interest rates, fiscal budgeting, and U.S. monetary policy. According to the Bureau of Economic Analysis, the real GDP of the U.S. increased at a rate of 1.4% in the fourth quarter of 2025. In the third quarter, real GDP increased 4.4%. Analysts expect the economy to grow by 1.4% to 2.6% for 2026 and 1.8% to 2.6% for 2027. The ideal range for manageable GDP growth is in the 2% to 3% range.

The unemployment rate is a second measure of the broader economy. According to the Bureau of Labor Statistics, the national unemployment rate for 2025 was 3.9%, down from 4% reported in 2024. Comparing the latest information, the unemployment rate for December 2025 was 4.4%, up from 4.1% in December 2024. Economists estimate that the unemployment rate will be between 4.2% and 4.6% in 2026 and 4.0% and 4.5% in 2027.

The Consumer Price Index (CPI) is a measure of inflation. The CPI is also a measure that personally impacts most Americans. Unlike recent years, when the U.S. experienced low inflation, the annual rate of inflation accelerated in 2021 and 2022 to a near 40-year high. As a result of interest rate increases in 2022 and 2023, the percentage change (inflation rate) cooled. According to the Bureau of Labor Statistics, for 2025, the CPI was 2.6%, down from 2.9% in 2024. Comparing the latest information, the inflation rate for December 2025 was 2.7%, down from 2.9% in December 2024. High inflation rates mean that purchasing power is being degraded and the costs of goods and services are rising. Economists expect inflation to fall to between 2.1% and 2.7% in 2026 and 2.1% and 2.5% in 2027. The Federal Reserve’s target rate for inflation is 2%.

The housing market slowed in 2025 with fewer housing starts in 2025 compared to 2024. Housing shortages are still an issue, which has kept housing prices high. Total housing starts in 2025 were 1.35 million. Analysts expect a 1% decrease in housing starts in 2026. While homebuilder sentiment weakened in January of 2026, analysts predict that the housing market is likely to experience a gradual recovery in 2026 as interest rates fall and home affordability improves.

For the auto industry, an estimated 16.2 million new vehicles were sold in 2025 compared to approximately 15.8 million units in 2024. Forecasters estimate that U.S. auto sales are likely to decrease back to the 2024 level of 15.8 million units in 2026. The biggest issue facing the auto industry in 2026 is affordability. While high income families are likely to help new vehicle sales, middle and low income families are still expected to struggle with the cost of new vehicles. While forecasters predict lower sales, auto manufacturers are focusing on lower priced models with less expensive trims to boost sales.

According to economists, Virginia’s economic outlook is consistent with national trends which indicate moderate growth for 2026.

According to the Virginia Department of Workforce Development and Advancement, the unemployment rate for the Commonwealth of Virginia for 2024 was 2.9%, up from 2.7% in 2023. Comparing the latest information, the unemployment rate for December 2025 was 3.4%, up from 2.5% in December 2024. Virginia unemployment rates are lower than the national rates.

State General Fund revenues for FY 25 grew by 6.1%. State General Fund revenue projections for FY 26 and FY 27 are expected to increase by 3.05% and 3.03%. Sales tax collections are estimated to grow at 3.24% for FY 26 and 2.24% in FY 27.

More than half of the State’s revenues are non-general fund revenues, which are designated funds earmarked for specific purposes. These funds include federal grants, institutional revenue, transportation funds, and Master Tobacco Settlement Agreement funds. Non-general fund revenues are expected to increase by 23.6% in 2026 and increase by 5% in 2027.

Like the U.S. and State economic outlooks, Montgomery County’s economic outlook is expected to see moderate growth. The County’s unique qualities and job base provide a strong foundation for sustained growth. Local employment rates are consistent with state and federal trends.

According to the Virginia Department of Workforce Development and Advancement, the unemployment rate for Montgomery County for 2024 was 3.0%, up from 2.8% in 2023. Comparing the latest information, the unemployment rate for November 2025 was 3.9%, up from 3.0% in November 2024. Like the national and state trends, the local unemployment rate is still extremely low and will likely increase in FY 26. The ideal unemployment rate is 3% to 5%.

Resources within the County budget are classified as either designated or undesignated.

• Designated Resources represent revenue accounts that are mandated for specific uses including:

• Support from the State Compensation Board for constitutional officers, court fees, fees for services and programs;

• Direct state aid for public assistance payments;

• State and federal funds for schools; and

• Support for human services programs.

• Undesignated Resources fall into two categories: undesignated revenue and fund balance. Undesignated revenue represents dollars which may be used in the budget at the Board’s discretion. These include property taxes, sales taxes, and similar local sources of revenue. Total budgeted revenue for FY 27 is $285.7 million with $123.1 million considered designated. Of this designated amount, $98.5 million or 80% is earmarked for public schools. Undesignated revenue dollars that may be used in the budget at the Board’s discretion total $162.6 million. Of this amount, $69.4 million goes to the public schools for operations, and $22.7 million supports debt service costs for county and public school facilities.

Local revenue growth is heavily dependent on property taxes, especially the real estate tax, which is the County’s single largest local revenue source. Real estate revenues (real property) represent 60% of the County’s total undesignated revenue. Personal Property tax revenue (motor vehicles) is the County’s second largest local revenue source and it represents 14% of the County’s undesignated revenue. Sales and Use Tax is the third largest local revenue source, representing 8% of the County’s undesignated revenue. Together these three revenue sources account for 82% of the County’s undesignated revenue and represent the bulk of revenue growth the County experiences on a yearly basis.

Since the pandemic, the County has experienced strong yearly revenue growth. This growth has started to slow as consumers and businesses are beginning to spend and invest less. In FY 25, total undesignated revenue collections exceeded estimates by $4.3 million (net of $0.6 million for ½ year of a 1-cent tax rate increase). Areas of strong growth were found in personal property ($2.2 million), interest earnings ($0.8 million), real estate and public service corporation taxes ($0.4 million), delinquent taxes ($0.3 million) and recordation taxes ($0.3 million). All other categories of revenue exceeded estimates by $0.3 million.

In FY 26, the County’s revenue growth is slowing with some revenues showing weak to limited growth; while other revenues are exceeding estimates. On the negative side, personal property taxes are down as several large businesses closed and businesses are investing less; sales tax collections are estimated to be down as consumers are spending less; interest earnings are down as the Federal Reserve continues to lower the Fed Funds rate. On the positive side, real estate and public service corporation taxes are up and will exceed estimates. For FY 26, the County expects to meet overall revenue estimates with a $1.1 million surplus of funds expected at the end of FY 26. Most revenue categories are trending back to normal levels. With the Federal Reserve planning several interest rate reductions in 2026, and with one-time revenue from the pipeline disappearing in FY 27, revenue growth for FY 27 is limited.

The County estimates a $1.3 million base revenue shortfall in FY 27 before new revenue growth is added. The chart shows a breakdown of the revenue by category:

*Calculated in Millions

Of the $1.1 million projected surplus in FY 26, $1.3 million is the result of one-time monies provided in FY 26 that were unbudgeted for the Mountain Valley Pipeline. These funds, along with increases in real estate, recurring increases in the pipeline’s valuation, and other miscellaneous revenues are being offset by shortfalls in personal property, sales tax and interest earnings. The shortfalls from FY 26 will carry over into FY 27. Some additional decreases in FY 27 result from reduced sales tax revenue due to a change in school age population estimates in the towns, lower interest earnings based on the Federal Reserve rate reductions in FY 26, and less pipeline related revenue as a result of a one-time payment in FY 26. The County expects to lose additional one-time revenues in all other revenues for FY 27. The County is estimating a total FY 27 base revenue decrease of approximately $1.3 million.

For FY 27, the County projects an increase of approximately $2.3 million in new undesignated revenue growth. This increase is made up of $1.2 million in new real estate construction, $0.8 million in personal property motor vehicles and other personal property categories, and $0.3 million in sales tax revenues. Adding the base revenue shortfall of $1.3 million to the new revenue growth of $2.3 million provides approximately $1.0 in new revenues without a tax rate increase for FY 27.

The FY 27 budget includes a 5-cent real estate tax increase from 76 cents to 81 cents. This tax increase adds $6.4 million in additional real estate tax revenue to address operational needs. Total undesignated revenues are estimated to provide $7.4 million in new money for FY 27.

General Fund designated revenues are estimated to increase by $3 million. $2.4 million is due to the addition of reimbursements from the Public Service Authority from the creation of the Utilities Division, $0.3 million is due to additional state funding increases for constitutional officers provided in FY 26 and FY 27, $0.1 million is due to the Social Services reconciliation in FY 26 and added to the base in FY 27, and $0.2 million is due to an increase in the local user fees in FY 27. Total County General Fund revenue growth including the five-cent real estate tax increase for FY 27 is expected to be $10.4 million.

Real estate values are based on the actual assessed value as of January 1, 2025, and estimated increases for new construction. Based on building permit data, from January 1, 2025 to January 1, 2026, assessed values are expected to increase $174 million. Growth from January 1, 2026 to January 1, 2027, is estimated at $160 million.

Real estate values totaled $12.5 billion for the CY 25 land book, including land use. The CY 26 land book is estimated to be $12.7 billion. The CY 27 land book is estimated at $12.8 billion. Total real estate revenues are estimated at $97.2 million, which is $7.3 million more than the FY 26 estimate.

Personal Personal property tax collections are based on the 2025 tax book, which is the most current documentation of assessed values. From this data, the 2026 property values are estimated. The estimated values, along with historical collection rates, are used to predict future personal property tax collections. Collection rates for FY 25 and FY 26 were used to estimate the rate for FY 27. The tax rate for personal property categories is $2.55 per $100 of assessed value.

This category includes motor vehicles (the County’s second largest source of revenue) and business personal property. FY 27 estimated taxes on motor vehicles total $22.4 million; business personal property taxes total $6.3 million.

Taxes on motor vehicles are estimated to grow by $0.6 million over the FY 26 estimate. Business personal property revenue is expected to decrease ($0.6) million. In total, personal property revenue categories are expected to remain flat.

New car registrations for CY 2025 were up 18% compared to CY 2024, while new truck registrations were up 10%. This resulted in a net increase in new vehicle registrations of 17%, as 369 more vehicles were purchased in 2025 as compared to 2024.

Source: Commissioner of Revenue’s Office

Montgomery County’s third largest category of undesignated revenues is sales and use tax. Sales and use tax is a consumption tax paid for sales of certain goods and services. For FY 25, the County collected $13.5 million and is estimated to collect $13.6 million for FY 26. For FY 27, the County estimates $13.8 million, which is a ($0.3) million decrease from what was budgeted in FY 26.

FY 08

FY 09

FY 10

FY 11

FY 12

FY 13

FY 14

FY 15

FY 16

$7,333,314

$7,205,999

$6,885,153

$7,184,055

$7,639,848

$7,986,545

$7,939,087

$8,467,926

$8,857,514

FY 17 $9,048,892

FY 18

FY 19

FY 20

FY 21

FY 22

FY 23

FY 24

FY 25

FY 26

FY 27

$9,423,190

$9,489,392

$10,013,089

$10,701,631

$12,443,543

$12,997,571

$13,463,283

$13,494,911

$14,109,401

$13,767,548

Historically, the County’s other undesignated revenues grow at a modest level; however, for FY 26 all other categories of undesignated revenue are expected to increase by $0.4 million. The County expects machinery and tools revenues to increase $0.1 million. Public Service Corporation taxes are expected to increase $0.9 million. Delinquent taxes are estimated to increase $0.2 million. Due to expected changes in interest rates, the County’s interest on savings is expected to decrease ($0.9) million. All other categories of undesignated revenue in total are estimated to increase by $0.1 million.

Machinery and tools is a tax on businesses at $1.82 per $100 of value, which is assessed at 60%/50%/40%, depending on the number of years an asset has been owned. Revenue collections were relatively flat for many

years; however, the County has experienced more growth in the last 10 years. The County estimates $3.7 million in collections for FY 26. The FY 27 estimate is set at $3.8 million.

Over the past several fiscal years, the state has reduced the amount of funding provided to local governments. Public education, public safety, Constitutional Officers, local libraries, and other local services have all been affected. In many areas, the state has shifted the burden of revenue generation to local governments. For the Montgomery County Public School System, the State’s budget includes an additional $3,619,579 in new funding for general school operational needs. $151,142 in new state funding is included for Constitutional Officers and their staff for FY 27.

The FY 27 budget increases the real estate tax rate from last year’s approved rate of 76 cents to 81 cents. This represents a five-cent tax rate increase. All tax rates are per $100 of assessed value.

The FY 27 budget increases the real estate tax rate from 76 cents to 81 cents, which is a five-cent tax rate increase over the FY 26 approved rate.

No General Fund balance dollars have been used to balance the FY 27 budget.

Reserve funds are dollars set aside that are either not required for expenditure in the current year or are earmarked for a specific future purpose.

Why Does the County Need Reserve Funds?

The financial health of a locality is determined based on its “operating position,” which refers to three factors:

• The County’s ability to balance the budget using current revenue (not using fund balance in the operating budget);

• The County’s ability to maintain reserves for emergencies (establishing reserve funds for specific purposes); and

• The County’s ability to maintain sufficient cash to pay expenses on a timely basis (ensuring an adequate level of cash flow reserves).

Why Shouldn’t the County Use Reserve Money to Balance the Budget?