EXCLUSIVE INTERVIEW

Ali Ahmmed, Chief Commercial Officer, bKash, speaks about 14 years of bKash and the future of MFS industry

EXCLUSIVE INTERVIEW

Ali Ahmmed, Chief Commercial Officer, bKash, speaks about 14 years of bKash and the future of MFS industry

Gross Foreign Reserve

Monthly (In USD Billion)

Gross foreign reserve increased by USD 5.9 Bn in August 2025 compared to January 2025.

Net Foreign Reserve

Monthly (In USD Billion)

Net foreign reserve (IMF Formula) increased by USD 6.2 Bn in August 2025 compared to January 2025.

Yearly (In BDT Million)

E-Commerce transaction has increased by 39% compared to July 2024. Transaction value has been over BDT 20,000 million since December 2024.

Yearly (In BDT Million)

MFS transaction keeps on rising as it increased by 21% YoY in July 2025. Transaction volume of July 2025 is 2.3 times greater than of July 2020.

Internet Banking Customers

Yearly (In Million)

Internet Banking customers is increasing rapidly as it increased by 32% YoY in July 2025. Internet Banking customers increased by 4.1 times in just 5 years.

Internet Banking Transactions

Yearly (In BDT Million)

With the rise in Internet Banking users, the transaction volume of internet banking is also seeing the same trend. In July 2025, the transaction volume increased by 37% YoY.

Telco Subscribers

In July 2025 (Millions)

GP remains the market leader in the telco sector with 46% of the market share.

Internet Subscribers In July 2025 (Millions)

Compared to January 2025, Mobile internet users increased by 5.51 Mn and ISP & PSTN users increased by 0.42 Mn. 121.5

Ruhul Quddus Khan appointed as the new CEO of Unilever Bangladesh

Tareq Refat Ullah Khan appointed as the new BRAC Bank MD & CEO

Shatil Ferdous appointed as the new Head of Media and Digital of Grameenphone

Shahriar Zaman has been promoted to Deputy General Manager, Head of Marketing of AkijBashir Group

Md. Abul Hashem appointed as the new Managing Director of Uttara Bank

Farha Diba appointed as the new Head of Marketing Himalaya Bangladesh

Md. Abu Tariq Zia Chowdhury has joined Akij Consumer Electronics Ltd. as Chief Business Officer (CBO)

1,229,226.4 1,485,666.2

Transactions Amount (In BDT Million)

Since its inception in 2011, the mobile financial services (MFS) industry has played a pivotal role in advancing financial inclusion in Bangladesh. Prior to the advent of MFS, most people relied on the traditional banking system for financial services. However, banks face inherent limitations: despite the variety of services a branch can offer, it is not feasible for banks to maintain branches across the entire country. While agent banking has been introduced to bridge this gap, a significant portion of the population still lacks the necessary documentation to access conventional banking services.

Moreover, many unbanked individuals do not require the full suite of banking services; often, they only need basic solutions, such as sending money to their families. The MFS industry successfully addressed this gap, enabling users to open accounts easily via mobile phones or agents and access essential financial services. Over time, the sector has evolved beyond simple cash transfers to encompass savings and lending products, emerging as a true pioneer of financial inclusion in Bangladesh.

Note: Nagad’s data is not included in 2025 as they have been unable to share data from March 2025.

Nagad has been unable to share information to Bangladesh Bank since March 2025. Hence, the dip of 87.3 million accounts is not a true reflection of the current market scenario.

As of July 2025, Bangladesh recorded 145.8 million active mobile financial service (MFS) accounts,

(excluding Nagad). More than half of these accounts are held by individuals in rural areas, reflecting the sector’s growing penetration beyond urban centres. Of the total account holders, 81.9 million are men, while 63.5 million are women, highlighting the steady rise of female participation in digital finance.

The recent contraction in the reported number of both male and female mobile financial service (MFS) accounts is primarily attributable to Nagad’s decision to cease publishing data from March 2025. Despite this, female account ownership has risen proportionally, now representing 43.6% of all accounts, up from 41.7% in July 2024.

‘ As of July 2025, Bangladesh

A greater share of accounts continues to be concentrated in rural areas, supported by the proactive expansion of agent networks by MFS providers. The number of agents has grown in tandem with the rising adoption of mobile financial services, reaching 1.4 million by July 2025—an increase of 0.4 million compared with July 2019. Of these, 0.8 million agents are based in urban centres, while 0.7 million operate in rural locations, reflecting a balanced distribution across the country.

Mobile financial services (MFS) in Bangladesh were initially introduced with a narrow focus on cash-in and cash-out facilities, primarily serving as a means for individuals to transfer money across different locations. Over the past 14 years, however, the sector has evolved well beyond its original remit. Today, MFS providers offer a diverse suite of services, ranging from peer-to-peer transfers to merchant payments and a wide variety of additional digital financial solutions, underscoring the industry’s transformation into a comprehensive

ecosystem.

With the steady rise in MFS adoption, cash-in and cash-out transactions have also expanded significantly. Between July 2019 and July 2025, the volume of cash-in transactions grew by 2.85 times, while cash-out transactions increased by 3.41 times.

Despite this rapid growth, the relative share of these services in overall transaction volumes has steadily declined, reflecting the diversification of MFS usage. In July 2019, cash-in and cash-out accounted for 36% and 35% of total transaction volumes respectively. By July 2025, these proportions had fallen to 26% and 30%, highlighting the increasing uptake of alternative services such as peer-to-peer transfers, merchant payments, and other digital financial solutions.

The introduction of mobile applications has made peer-to-peer money transfer one of the fastest-growing services offered by MFS providers. Between July 2019 and July 2025, transaction volumes in this segment rose by 5.36 times. This growth trend is expected to continue in the coming years, as increasing numbers of urban users opt to transfer money directly through MFS apps rather than relying on agents.

payments as providers have streamlined the process through in-app integration and QR code systems. As a result, transaction volumes in the merchant payment segment have grown by 13.51 times compared with July 2019, reflecting a significant shift in consumer payment behavior.

Disbursement

Note:

Salary disbursement has also emerged as a key component of MFS usage, particularly as most factory workers now maintain MFS accounts rather than traditional bank accounts. Consequently, many factories have adopted the practice of paying monthly wages directly into workers’ MFS accounts. Compared with July 2019, the volume of salary disbursements through MFS has increased by 5.34 times. This trend gained momentum during the pandemic and has since become a standard feature of the wage distribution process.

‘ Salary disbursement as a key component of MFS usage gained momentum during the pandemic and has since become a standard feature of the wage distribution process. ’

Mobile Financial Service (MFS) users are increasingly purchasing talktime directly through their MFS accounts, bypassing traditional agents of mobile operators. This trend reflects the growing convenience offered by MFS providers, who have streamlined talktime purchases via their apps. As a result, talktime transactions have surged, recording a 2.51-fold increase compared to July 2019.

MFS users are increasingly leveraging their accounts to pay utility bills directly. The volume of utility payment transactions has surged, registering a 6.58-fold increase compared to July 2019.

Inward Remittance (In BDT Million)

MFS providers are increasingly targeting the remittance market, encouraging users to receive money directly into their MFS wallets from abroad. Driven by convenience, the volume of inward remittance transactions has grown sharply, rising 57.85-fold compared to July 2019. Despite this rapid increase, the segment still represents a relatively small share of the country’s total inward remittance inflow, suggesting significant growth potential in the near future.

bKash, in collaboration with IDLC, Dhaka Bank, and BRAC Bank, offers monthly Deposit Pension Scheme (DPS) products, enabling users to save as little as BDT 250 per week. According to The Business Standard, bKash had opened 3.2 million DPS accounts via its app as of 2024. The product’s growing popularity has led bKash to increase the maximum DPS limit to BDT 20,000 per month.

In addition, bKash partnered with City Bank to pilot its nano loan initiative, initially launched to assess the market landscape. Following strong demand, the loan limit has been increased from BDT 30,000 to BDT 50,000. Since the commercial roll out, nearly 1 million users have accessed the loans over 5.5 million times, with total disbursements reaching BDT 28 billion.

MFS wallets have become an integral part of daily life for both rural and urban users. Beyond the services previously mentioned, companies like bKash have introduced savings and lending products in partnership with leading banks and financial institutions. As of July 2025, the total float in MFS accounts reached BDT 128,674 million. Float, representing the e-money held in users’ and agents’ accounts, reflects the growing shift toward a cashless future that MFS providers are actively promoting.

As bKash marks its 14th year, we sat down with Ali Ahmmed, Chief Commercial Officer of bKash Limited, to discuss how the company and the broader Mobile Financial Services (MFS) industry have transformed Bangladesh’s financial landscape, what consumer behavior shifts mean for the future, and where digital finance is heading next.

Here’s a refined version of the interview.

Over the last 14 years, how would you describe the transformation that bKash and the MFS industry have driven?

Mr. Ahmmed: Over the last 14 years, the MFS industry has transformed financial access by reaching millions of households and solving a fundamental problem—sending money quickly, safely, and affordably. Back then, people relied on unreliable methods like couriers or bus services, which were costly and time-consuming.

“bKash identified this gap and drew inspiration from global examples like Kenya’s M-Pesa, adapting similar USSD-based solutions for Bangladesh.”

We recognized that many workers in cities needed to send money home to their families in villages, and technology offered the most efficient solution. By partnering with mobile operators and working closely with Bangladesh Bank—whose progressive, pro-people policies were instru-

mental—we built a reliable, secure platform that reshaped how money moves across the country.

Have you noticed a shift in how consumers view and use cash versus digital payments?

Mr. Ahmmed: Absolutely. One of the biggest shifts has been in utility bill payments. Not long ago, paying a 500 taka electricity bill meant standing in line at a bank for hours, going through multiple layers of verification. Today, MFS platforms process over 30 million bills every month, saving customers time while ensuring billers receive funds instantly—no more waiting weeks for settlement.

The impact goes further: banks can repurpose idle funds productively, billers get money on time, and customers enjoy convenience. The same trend is visible in digital payments for ride-sharing, food delivery, and e-commerce. Offline too, we now process around a million

transactions a day.

Consumer behavior is changing rapidly in cities—young people at superstores or pharmacies already prefer mobile wallets—but the next big frontier is rural markets and wet markets. Once payments there go digital, we’ll truly see all walks of life embracing a cashless ecosystem.

Beyond customers, merchants play a critical role in the digital payment ecosystem. How is bKash creating value for them and encouraging wider acceptance of digital payments?

Mr. Ahmmed: Our role as digital players is twofold: bringing new users onto the platform and creating compelling reasons for merchants to accept digital payments. Merchants are crucial stakeholders, so we focus on solving their pain points with simple, practical solutions.

For example, we introduced the payment speaker, a small device that announces when a transaction is complete—saving busy shop owners the hassle of checking their phones. Solutions like this make digital acceptance easier and more attractive for small traders.

Globally, we see even deeper integration. In China, restaurants use QR codes not just for payments but for browsing menus, placing orders, and settling bills—all through self-service. Digitization in Bangladesh must move in that direction: from payment tools to digital menus, POS systems,

and cash counters.

Only then can the entire merchant ecosystem become more efficient, allowing businesses to focus on what they do best while customers enjoy a seamless digital experience.

What are the current growth drivers for the MFS industry?

Mr. Ahmmed: We are working closely with the central bank to introduce Bangla QR at a national level. Once implemented, any customer—whether using bKash, a bank app, or another MFS provider—will be able to scan any QR and make payments seamlessly. This interoperability will bring all digital payment users under one unified ecosystem.

Another priority is cross-border remittance. By partnering with banks, we enable rural customers to receive remittances directly on their phones and withdraw from the nearest MFS agent. This makes the

process faster, safer, and more inclusive.

We are also focusing on digital savings solutions like DPS and micro-savings. Millions of customers are now saving as little as 250 taka a week, building habits that lead to financial independence. Over time, these small deposits accumulate into meaningful amounts, allowing people to invest in education, business, or creative pursuits.

Every bKash product—from remittance to savings and loans—has solved real problems over time. What is the core product philosophy at bKash, and what key questions must every new product answer before launch?

Mr. Ahmmed: Our product philosophy begins with a simple question: “What customer problem are we solving?” Fourteen years ago, the challenge was financial inclusion—millions lacked access to formal banking. We addressed that with services like sending money home.

Today, the bigger gap is access to credit. Informal loans are expensive and unreliable, while banks require documentation and collateral that many customers don’t have. That’s why we partnered with City Bank on nano loans. City Bank handles credit assessment and policy approval, while bKash disburses loans and enables repayment through our platform.

So far, 5.6 million customers have been offered credit, with over 1 million already taking

loans. Every day, around 27,000 new customers are accessing credit. Repayment rates are strong, showing customers understand the value of building a credit history.

“This is just the beginning —we expect millions more to gain access to affordable credit in the coming years.”

How do bKash’s financial products contribute to deeper platform engagement? Do you see evidence that these offerings increase customer activity and loyalty?

Mr. Ahmmed: Yes, absolutely. Some products are highly “sticky” and drive repeat engagement. For example, mobile recharge is our most used feature—around 4 million transactions daily, with the average customer making more than five recharges a month.

Utility bill payments show similar behavior: once customers save their credentials, they prefer the convenience of staying on our platform rather than switching elsewhere.

The same goes for merchant payments—whether at a coffee shop or superstore,

customers increasingly prefer paying digitally. Together, these products not only deepen engagement but also build long-term loyalty while reducing churn.

Remittance is vital for Bangladesh. How is bKash shaping that sector?

Mr. Ahmmed: We currently work with 29 local commercial banks and over 114 international money transfer companies, enabling instant credit of remittances into bKash accounts. For families in Bangladesh, this means receiving money from abroad in a way that is fast, reliable, affordable, and completely hassle-free—no paperwork or physical visits required.

“Our ambition is to connect with all major money transfer companies worldwide and drive down remittance costs through digitization.”

By lowering sending fees, we can pass the benefits to both senders and receivers. As more banks and partners join the ecosystem,

we believe transaction volumes will continue to grow, making remittances more accessible and efficient for millions.

bKash’s agent network is a critical part of its ecosystem. How has this network evolved over time, and what role do agents play in driving financial inclusion and customer engagement?

Mr. Ahmmed:

We have 350,000 agents , supported by 300 distributors and 12,000 field officers.

—our “frontline warriors.” They ensure agents have liquidity, follow security protocols, and receive daily support. We also partner with banks for safe cash management.

The network itself has evolved: 95% of agents now use smartphones, not bar phones, reducing errors. Many agents now hold bank accounts, offer savings products, and assist with customer registrations. Their incomes and lifestyles have grown alongside bKash.

What lessons has bKash learned over 14 years serving in Bangladesh shaping the industry?

Mr. Ahmmed: Engagement with regulators is key. For example, the central bank’s eKYC policy—developed through close collaboration—transformed MFS account opening from a cumbersome, paper-based process into a 24/7 digital experience. Such innovations wouldn’t be possible without regulatory alignment.

Beyond regulators, cross-industry collaboration has been critical. From working with mobile operators on USSD in the early days, to partnering with banks, utilities, and microfinance institutions, we’ve co-created solutions that extend financial services, simplify bill payments, and support loan and savings collections. Together, these partnerships help build a stronger digital ecosystem.

Trust is everything in financial services. How has bKash earned it?

Mr. Ahmmed: Trust is the foundation of any financial company, and for bKash it has been the most critical element over the past 14 years. Our promise has always been that customer money is safe. Deposits are backed by government securities and kept only with top-rated banks, ensuring funds are always available whenever a customer wants to transact.

On top of that, both the government and regulators have shown strong confidence in bKash, entrusting us with social safety net disbursements and broader financial inclusion efforts. Altogether, these elements—secure funds, reliable access, and institutional trust—have created a rewarding and trusted experience for our customers.

Looking ahead, what can customers expect from bKash in its 15th year?

Mr. Ahmmed: The future is payment innovation. Customers won’t need leather wallets—tap-and-pay and speaker-verified transactions will be mainstream. Expect enhanced rewards programs, new savings products, and expanded credit access.

“We want to make digital payments not just convenient, but the default choice in everyday life across Bangladesh.”

— Ali Ahmmed CCO, bKash

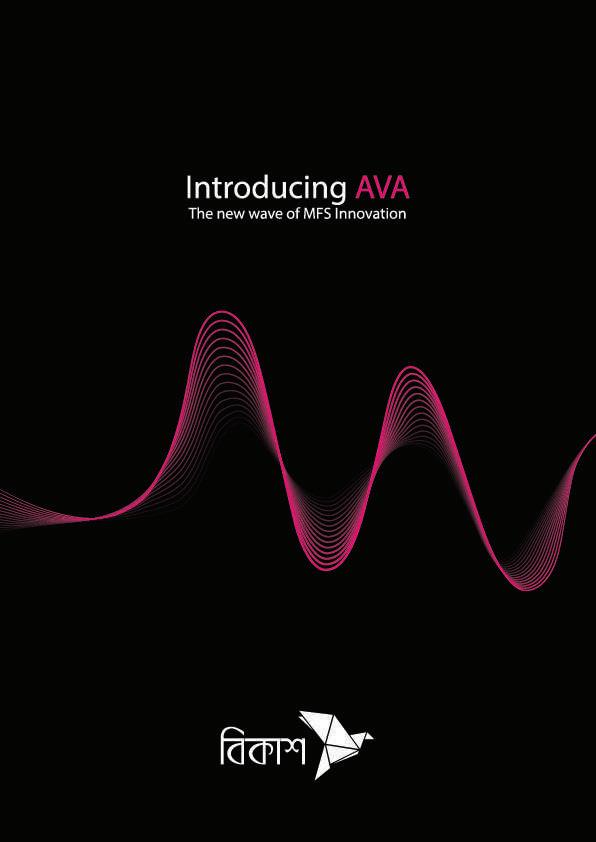

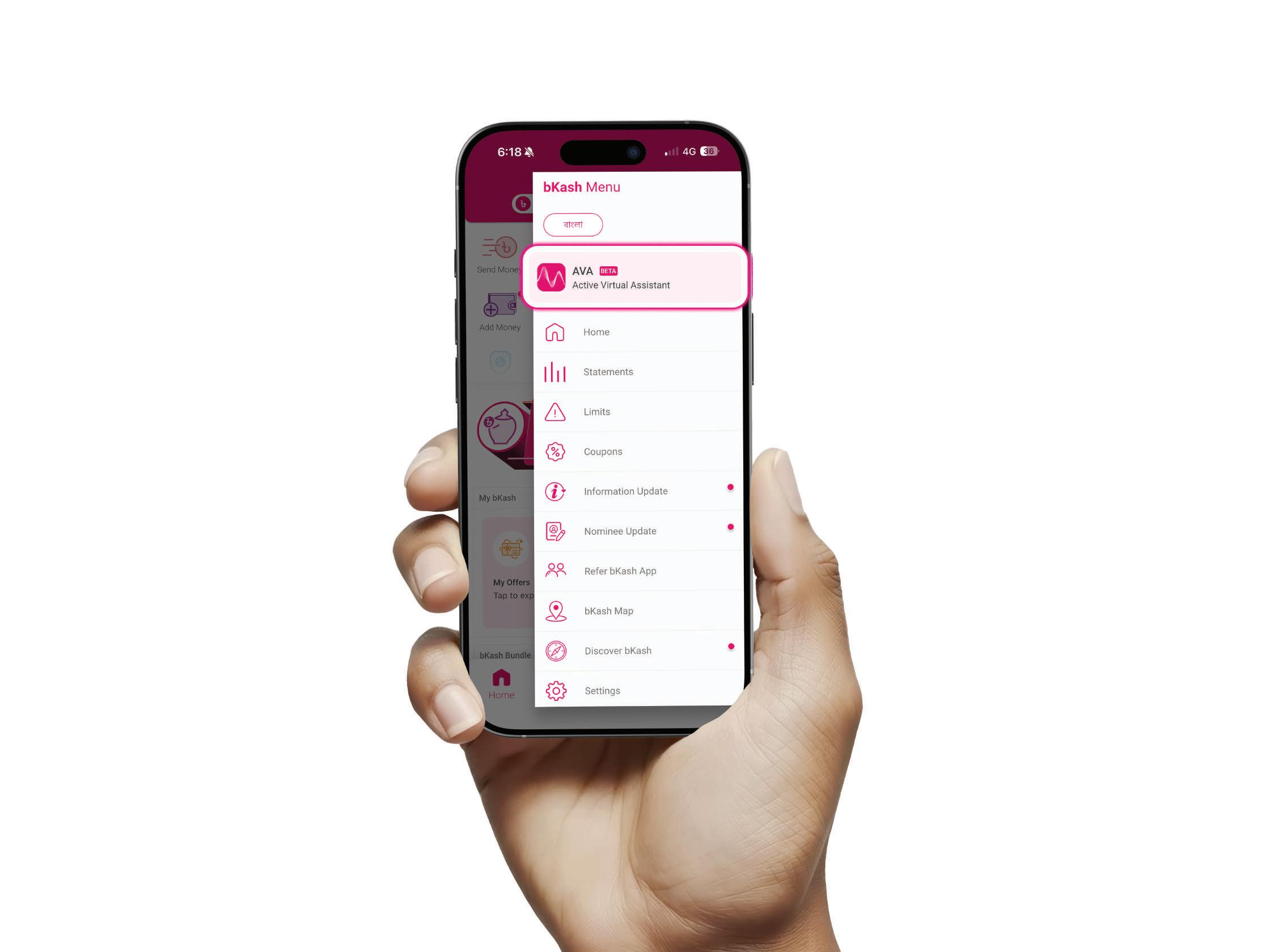

In the high-stakes world of global fintech, innovation is measured not just by new features but by strategic shifts that redefine customer interaction. In Bangladesh, where bKash has been the foundational force in Mobile Financial Services (MFS), the introduction of its in-app Active Virtual Assistant (AVA) is precisely this kind of disruptive move. It signals a crucial evolution, transitioning MFS from a mere utility for transactions to an intelligent, conversational digital financial partner. This adoption of advanced digital assistance moves the company beyond its role as a payment enabler and positions it as a sophisticated player ready to harness the power of personalized digital finance in one of the world's most dynamic emerging economies.

The launch of AVA, bKash's in-app virtual assistant, is not merely a customer service upgrade; it represents a professionally analytical stride in the Mobile Financial Services (MFS) sector. For the world's leading players, the shift from transactional to conversational interfaces is the cornerstone of the next digital economy.

In the context of Bangladesh—a country where MFS pioneered financial inclusion—AVA is the quiet, strategic move that redefines the market's innovation curve, leveraging advanced technology to transition from a platform of payments to a ubiquitous digital financial partner.

While AVA's initial capabilities—statement generation, PIN change assistance, and limit & charges information, product information—seem limited, their true significance is infrastructural.

They are the initial use-cases validating an integrated service layer on a massive scale. This validates a shift in operational focus toward a scalable, automated, and instant self-service model.

By embedding conversational assistance at the user interface, bKash has effectively signaled its intent to lead the race toward "Smart Finance" in a market characterized by high mobile penetration but persistent digital literacy gaps.

For years, MFS in Bangladesh relied on the simple but rigid USSD (247#) system, democratizing finance but constraining user experience. The smartphone app and its latest iteration, AVA, which is still in its beta phase aims to dismantle this constraint.

Elevated Service Capacity: By automating common requests (account status, limits, product info), AVA aims to enhance service capacity and speed, ensuring users receive instant assistance freeing up human agents for complex inquiries or advanced support.

Continuous Improvement Loop: Every user interaction with AVA contributes to a cycle of platform refinement. This allows bKash to continuously enhance its digital models for greater sophistication—a critical advantage over competitors relying on traditional data streams.

A future where financial services are dramatically transformed by a hyper-localized Active Virtual Assistant (AVA) in Bangladesh is highly probable.

This AVA, expertly tuned to the nation's socioeconomic nuances, will likely become a cornerstone of customer service and financial inclusion. It's probable that the integration of this advanced assistance will effectively address the challenge of a predominantly unbanked or underbanked population by introducing a sophisticated Micro-Credit Advisor & Disbursement Engine. This system stands a strong chance of bypassing traditional barriers like a lack of formal credit scores, enabling a small-to-medium enterprise (SME) owner to quickly secure crucial working capital—for example, a loan—by analyzing alterna-

An In-Depth Interview with Mr. Mahtab Muntazeri on Bridging the Skills Gap in Higher Education

The relationship between higher education and industry is at a critical juncture in the global economy. As economies rapidly evolve, the traditional model of theoretical knowledge transfer is proving insufficient to meet the dynamic needs of the job market. To explore this vital intersection, we spoke with Mr. Mahtab Muntazeri, Senior Lecturer in the Department of Marketing and International Business at North South University (NSU), who shared his expert assessment on the current state, challenges, and necessary philosophical shifts required for effective industry-academia collaboration.

Mr. Mahtab characterizes the current landscape of industry-academia collaboration as being in a "development phase." While leading institutions— including NSU, Dhaka University, and Brac University are engaging in significant efforts, much of the collaboration remains transactional, often occurring through short-term events or on a one-on-one basis.

"Where we lack is structured development of industry-academia," Mr. Mahtab notes. He stresses that the most immediate and critical area where collaboration is falling short is in co-creation. This involves the joint development of knowledge, particularly industry-specific content and local learning requirements.

The lack of co-creation impacts core academic materials: "If we want to create, for example, let's say, case studies, which is Bangladeshi-specific and industry-specific, it requires industry-academia collaboration," he says. Similarly, adapting curricula—often adopted from foreign systems—to the local needs of corporates, recruiting companies, and entrepreneurs demands a far deeper partnership.

"If we want to create, for example, case studies, which is Bangladeshi specific and industry specific, it requires industry-academia collaboration."

In a fast-changing economic environment, the definition of a "quality graduate" must evolve beyond simple academic achievement. For business graduates specifically, Mr. Mahtab highlights a combination of core competencies:

• Domain Knowledge

• Analytical Thinking

• Adaptability

Specifically, "be able to adapt to new challenges [and] the dynamic business environment."

• Quick Learning

The ability to learn swiftly from corporate and work environments.

• Soft Skills

The essential interpersonal skills required in industry.

The collective possession of these attributes, Mr. Mahtab suggests, is what truly defines a graduate who can add value in the modern workplace.

While credit-bearing internships are a proven method for bridging skill gaps, Mr. Mahtab argues that the timing and structure of practical exposure need significant reform.

He advocates for integrating project works that involve direct field experience with industry. For instance, a marketing student should engage in projects working with agencies or sales teams.

Crucially, he challenges the current standard of placing the compulsory internship as the last course: "If they could do it maybe early on, like middle of their graduation or even earlier, that could have been even more helpful... they could have been able to relate [practical experience] to certain concepts in classes."

This earlier exposure would allow students to bring real-life outlooks back into the classroom, enriching discussions and significantly reducing the skill gaps upon graduation. He suggests that developing a culture of short, mid-program placements—similar to summer programs in other systems is essential, though it requires corporate participation and a restructuring of academic calendars.

"We need to set up or find a way where there would be a shared value, where we would know what both parties are gaining in the long run."

— Mahtab Muntazeri Senior Lecturer in the Department of Marketing and International Business at North South University (NSU)

The major impediment to sustained collaboration is the difference in motivation, often leading to short-term, event-based partnerships. To overcome this, both academia and industry must adopt a long-term perspective and establish a clear shared value

For the industry, the gain is far beyond mere recruitment. Industry can use collaboration as an opportunity for:

• Knowledge Creation

Not just for the university, but for the industry itself, by developing best practices and solving unique, complex problems.

• Efficient Problem-Solving

Gaining the intellectual resources of the faculty to tackle issues in a more efficient way.

For the university, the gain extends past "a good story" or public relations:

Designing and refining programs that are directly responsive to the needs of

Providing faculty members with exposure and real-world data to enrich their research and teaching.

"We need to set up or find a way where there would be a shared value, where we would know what both parties are gaining in the long run," Mr. Mahtab asserts.

To prevent the curriculum from becoming theoretically outdated, academic staff must possess and maintain current industry experience.

Mr. Mahtab suggests an embedded program or a Faculty-in-Industry Fellowship where professors could be part of industrial programs.

While admitting the difficulty of implementing this on a large scale due to the sheer volume of faculty and students, he highlights the necessity of in-hand experience for faculty to:

1. Teach better and with greater context.

2. Design a superior curriculum and assessment criteria.

3. Ensure project works are industry aligned.

Regarding Small and Medium Enterprises (SMEs), Mr. Mahtab notes that while large corporations have the resources for collaboration, SMEs are often more flexible. Since SMEs represent a significant and growing portion of the job sector, universities must assess their specific requirements and create accessible platforms for SMEs to collaborate with academia.

Measuring the true, long-term success of collaborative initiatives requires going beyond initial job placement.

Mr. Mahtab proposes the following Key Performance Indicators (KPIs):

1. Career Progression of Graduates

2. Retention Rate (in their first few jobs)

3. Entrepreneurship Outcomes

4. Project Outcomes (the real-world impact of student/faculty projects)

5. Curriculum Development (quantifying alignment changes over time)

6. Innovation (metrics related to novel solutions or patents)

Ultimately, maximizing industry input requires a fundamental shift in the philosophy of higher education: moving from a focus on purely theoretical knowledge transfer to one centered on applied problem-solving and entrepreneurial thinking.

This shift, Mr. Mahtab concludes, circles back to the concept of co-creation, involving students, faculty, and industry partners alike. He suggests that universities must create structured institutions—like NSU's "Start Up Next" incubation program—that are dedicated to training specific skill sets, complementing classroom theory, and fostering an environment of innovation.

"If we invest more on these type of institutions, programs like this... that would help create an environment where students can learn problem-solving capabilities, entrepreneurial thinking."

The Kuwaiti Dinar (KWD) consistently holds the distinction of being the world's highest-valued currency by exchange rate, a spectacular financial fact that often leads to a critical misconception: that Kuwait is among the wealthiest, most resilient nations globally. This perception is profoundly amplified by its impressive conversion power, with 1 Kuwaiti Dinar equating to approximately $3.28 US Dollars as of projections for mid-2025. Such a phenomenal valuation suggests an equally phenomenal national prosperity. However, a comprehensive examination of Kuwait’s economic landscape, utilizing broader and more nuanced measures of national prosperity, economic diversity, and long-term sustainability, reveals a more intricate, paradoxical reality. Kuwait is a nation with undeniable and substantial per capita wealth, yet it does not consistently rank as the "richest country" when scrutinized by measures of structural economic health.

The Kuwaiti Dinar’s supremacy as the world's most valuable currency is the result of a deliberate, interconnected strategy built on geological endowment, astute financial management, and central bank policy.

The primary and most powerful driver of the Dinar's high value is Kuwait's massive oil reserves, estimated to be around 7% of the world's total supply. This resource base has positioned Kuwait as a fundamental force in the global energy market. The continuous, substantial, and reliable revenue gener-

ated from these hydrocarbon exports ensures a sustained, high-volume inflow of foreign currency (primarily U.S. Dollars). This constant supply of foreign exchange creates an enduring high demand for the local currency, directly contributing to its elevated and stable exchange rate.

Beyond the black gold, Kuwait's strong currency is buttressed by world-class financial prudence and strategic policy. The nation maintains a very low level of public debt and has historically accrued significant budget surpluses. This conservative fiscal approach stands in contrast to many other resource-rich states.

Crucially, the government strategically manages its wealth through the Kuwait Investment Authority (KIA), the world's oldest sovereign wealth fund. The KIA invests extensively in highly diversified foreign assets, shielding the domestic economy from global commodity price shocks and currency volatility. These foreign reserves act as the ultimate guarantor, safeguarding the Dinar's high valuation even during periods of global economic uncertainty and oil market turmoil.

The Central Bank of Kuwait (CBK) further reinforces stability through its strategic monetary policy. Since its reinstatement in 2007, the CBK has employed a currency peg to a basket of international currencies rather than fixing it to a single currency like the U.S. Dollar. This policy offers several advantages: it maintains economic stability, more accurately reflects Kuwait’s diverse international trade relations, and acts as a powerful barrier against imported inflation, thereby cementing the Dinar’s reputation for strength and reliability in global markets. This monetary commitment, combined with the country's entrenched political stability, significantly bolsters investor confidence and sustains demand for the KWD.

‘ Constant supply of foreign exchange creates an enduring high demand for the Kuwaiti Dinar, directly contributing to its elevated and stable exchange rate ’

To understand Kuwait’s position, one must distinguish between two core concepts of currency strength: the Exchange Rate and Purchasing Power Parity (PPP).

Exchange Rate Strength vs. Purchasing Power Parity

Exchange Rate Strength:

This is the most visible metric, reflecting how much of another currency a unit of KWD can purchase. The Dinar excels here, making imports cheaper, affording greater purchasing power for consumers abroad, and protecting them from imported inflation.

Purchasing Power Parity (PPP):

In contrast, PPP measures a currency’s true value by equalizing the cost of a standardized basket of goods and services across different countries. It is widely considered a superior measure for comparing actual living standards and real economic well-being.

The misconception that currency strength equates to overall national prosperity is a critical flaw. While a strong Dinar offers tangible advantages, its primary economic side effect is a drag on non-oil export competitiveness. The persistently high value, driven by oil revenues and the currency peg, makes Kuwaiti goods and services expensive internationally, which directly discourages non-oil export growth and slows the development of a robust, dynamic private sector. This creates a fundamental trade-off: currency stability at the expense of economic diversity.

The PPP Reality: A Nuanced Wealth Ranking

Kuwait's position on the global wealth stage is more complex than headline figures suggest. While its wealth system provides an exceptionally high standard of living for citizens, the overall economic productivity, when measured by the PPP-adjusted

GDP per capita, is not top-tier.

The estimated PPP-adjusted GDP per capita of approximately $51,000 to $61,246 (for 2024–2025) demonstrates a high standard of living but reveals that Kuwait ranks below several key GCC peers and global economic leaders:

COUNTRY

PPP-ADJUSTED GDP PER CAPITA (EST.) CONTEXT

Qatar

Highest in the region, driven by natural gas and diversification.

Significantly higher, reflecting successful diversification efforts.

Higher, despite smaller oil reserves, showing moderate success in finance.

High, but reflects wealth distribution from oil rather than broad economic productivity.

Source: IMF,WB

This ranking disparity highlights that Kuwait’s wealth is largely a reflection of state-driven oil revenue distribution, not a diversified or universally productive economy, suggesting that its prosperity, while deep, is not as broad or structurally resilient as that of its leading competitors.

Kuwait's economy remains overwhelmingly dependent on its vast hydrocarbon resources—a characteristic that serves as both its immense source of wealth and its most significant structural vulnerability.

Kuwait is one of the most oil-reliant members of the GCC. The hydrocarbon sector has historically accounted for approximately 90% of total exports and 66% of fiscal revenues. This profound reliance means that the nation's economic performance is

highly susceptible to the volatile swings in global oil prices.

The vulnerability of this model was starkly demonstrated in 2020. The combined impact of the global pandemic and OPEC+ oil production cuts caused the economy to contract sharply by 8.9%. This volatility led to a dramatic widening of the fiscal deficit from 9.5% of GDP in the prior year to an alarming 33.2% in FY20/21, underscoring the acute dangers of monoculture economics.

Compounding the oil dependency is a deeply segmented and distorted labor market. The government has historically used the public sector as the primary engine for wealth distribution and employment for its citizens.

•

•

A disproportionately high 76% of Kuwaiti citizens are employed in the public sector.

Kuwaiti nationals constitute only a small fraction (4.3%) of the private sector workforce.

Source: World Bank (LMIS,2019)

This model creates profound inefficiencies: it incentivizes citizens to avoid acquiring market-relevant skills, generates underemployment, and places an enormous and potentially unsustainable fiscal burden on the state budget. The dominance of the public sector essentially stifles the competitive spirit and dynamism required for a robust, private-sector-led economy to flourish.

Recognizing the existential threat posed by non-diversification and the long-term global shift away from fossil fuels, Kuwait launched its ambitious national development plan, "New Kuwait 2035." This

vision aims to transform the country into a diversified, sustainable, regional financial and commercial hub, with a dynamic private sector leading the change.

To realize Vision 2035, Kuwait has articulated comprehensive investment plans across critical sectors:

1. Infrastructure: The government has allocated substantial funds, including nearly $6 billion in its 2025-2026 budget, for vital projects like the development of the strategic Mubarak Al-Kabeer Port and new cities.

2. Innovation and Private Sector Empowerment: The plan explicitly targets the empowerment of Kuwaiti startups, attracting Foreign Direct Investment (FDI) into new industries, and leveraging tools like the Kuwait Direct Investment Promotion Authority (KDIPA) to facilitate growth.

3. Human Capital Development: The government has increased its spending on education and is implementing reforms focused on STEM (Science, Technology, Engineering, and Mathematics) and a professional licensing system for teachers. The goal is to align the workforce's skills with the demands of a modern, technology-dependent economy.

The Implementation Hurdle

Despite these commendable plans and significant financial allocations, the success of "New Kuwait 2035" hinges on overcoming deeply entrenched structural challenges:

Labor Market Distortion

The overgenerous wages and benefits of the public sector continue to create a powerful disincentive for Kuwaiti nationals to seek challenging or productive employment in the private sector. Until this system is reformed, the private sector will remain dependent on expatriate labor, hindering its capacity to drive national innovation.

Education Quality

Kuwait currently ranks low in the Gulf region for the quality of its primary schools and the skillsets of its

graduates, creating a bottleneck for private companies seeking qualified local talent.

Persistent political friction and structural bureaucratic barriers have historically slowed the pace of reform and major project implementation. The shift from a state-allocation model to a market-driven economy requires difficult political consensus that has often proven elusive.

Kuwait's economic model contrasts sharply with the diverse, innovation-driven systems that characterize the world's leading economies, where sustainable wealth is not dependent on a single resource or currency strength.

United States

Germany

China

Innovation and Global Reserve Currency Status.

Advanced Manufacturing and Export Excellence.

Technological Self-Reliance and Manufacturing Dominance.

Kuwait

Hydrocarbon Exports and Sovereign Wealth Fund.

Highly diversified: Finance, Technology, Services, Defense. Resilient

Industry 4.0, Vehicles, Machinery, Chemicals. Structurally sound.

Manufacturing, AI, Green Technology, Domestic Consumption. Strategic diversification.

Low diversity, high reliance on oil revenues. Highly vulnerable to price shocks.

The experience of these nations confirms that sustainable national wealth is driven by Economic Diversity (a safeguard against volatility), Innovation and Human Capital (the engine for future growth), Global Trade Integration (enhancing resilience), and Private Sector Dynamism (fostering competition and job creation). Kuwait's continued concentration in hydrocarbons and its public sector dominance keep it exposed, limiting its global economic leverage

and resilience.

Kuwait's Dinar is a powerful symbol of its past oil success and its excellent fiscal management. However, its future prosperity depends entirely on its ability to execute the ambitious transformation outlined in Vision 2035.

Securing sustainable wealth requires a decisive shift:

1. Accelerate Diversification: Move beyond infrastructure to genuinely foster non-oil sectors like finance, logistics, and technology.

2. Reform Labor and Education: Implement deep, structural reforms to realign incentives, making private sector employment attractive and equipping Kuwaiti youth with market-relevant skills.

3. Strengthen Governance: Enhance transparency and streamline bureaucratic processes to improve the business environment and attract Foreign Direct Investment (FDI).

The challenge is profound: to transition from a powerful, yet limited, rentier state to an innovative, diversified, and competitive market-led economy. The Dinar is the crown, but only genuine economic transformation can ensure the reign is long and truly prosperous.

In the financial landscape, campaigns can be transformative, especially when addressing the gap between perception and reality in investing. One such campaign, “Mutual Fund Sahi Hai” (Mutual Funds Are Right), launched by the Association of Mutual Funds in India (AMFI), revolutionized India’s mutual fund industry by bringing it into the mainstream.

This initiative not only raised awareness but also changed the way people, from the working class to professionals, viewed mutual funds as a tool for wealth creation. For Bangladesh, a country with untapped potential in its financial markets, there are many valuable lessons to learn from India’s success.

Launched in 2017, the “Mutual Fund Sahi Hai” campaign was spearheaded by AMFI under the guidance of the Securities and Exchange Board of India (SEBI). The campaign was not just about promoting mutual funds but educating the public on how to make smart financial decisions. At its core, the initiative sought to address the prevalent misconceptions about mutual funds, especially the notion that they are risky or complicated.

Through a multi-platform approach, the campaign reached a broad audience via television, digital media, radio, print, outdoor advertisements, and even cinema. The use of simple, relatable language and catchy slogans, like “Mutual Fund Sahi Hai,” resonated with ordinary people, breaking down the complexities of mutual fund investments into digestible content. Within just one year, 5 million new investors joined the mutual fund market, and the Average Assets Under Management (AUM) surged by 33%, from INR 18.5 trillion in February 2017 to INR 24.6 trillion in March 2019.

The success of the campaign wasn’t limited to metropolitan cities. While Tier 1 cities, like Mumbai and Delhi, quickly embraced mutual fund investing, the campaign has since been expanded to reach Tier 2 and Tier 3 cities. This expansion demonstrates AMFI’s commitment to bridging the financial literacy gap

across India. Now, terms like SIP (Systematic Investment Plan) are part of the common vernacular in these cities, signaling a fundamental shift in how Indians approach saving and investing.

Bangladesh, a nation with over 170 million people and a rapidly growing economy, is at a different stage of development in its mutual fund industry. Despite this economic growth, the country’s mutual fund market is still in its infancy, valued at around Tk 16,000 crore (approximately $1.47 billion USD), which pales in comparison to India’s market. One major factor contributing to this slow growth is the lack of financial literacy.

Bangladeshis, much like Indians before the campaign, have traditionally been more comfortable with fixed-income products like fixed deposits and savings certificates. This conservative approach stems from a lack of awareness about alternative investment options such as mutual funds.

The question arises: Could Bangladesh replicate the success of India’s “Mutual Fund Sahi Hai” campaign to boost participation in its own market?

The short answer is yes—but it requires a concerted effort from both the private and public sectors, alongside the asset management companies operating within the country.

The financial literacy problem in Bangladesh is undeniable. While the government has made strides in financial inclusion, with more people gaining access to formal banking services, investing in equity markets and mutual funds remains a niche activity. Many still perceive the stock market and mutual funds as speculative, risky, and accessible only to the wealthy or those with specialized knowledge.

To combat these perceptions, a well-structured and localized campaign similar to “Mutual Fund Sahi Hai” could be instrumental. By creating simple, relatable content in Bangla and disseminating it across TV, social media (this will be a game-changer), and even community outreach programs, asset managers could demystify mutual funds and present them as accessible, flexible, and reliable options for long-term wealth creation.

In India, the success of the “Mutual Fund Sahi Hai” campaign can largely be attributed to its ability to resonate with everyday people. One advertisement, for instance, shows two friends near a samosa stall, with one telling the other that while eating samosas may make him fat, it won’t make him wealthy. The friend then suggests investing in mutual funds as a way to grow wealth, dispelling common myths about liquidity by explaining that mutual funds can be withdrawn in emergencies. The ad’s conversational tone and its ability to

address common fears—such as liquidity—were key to its success.

Here are the key points explaining why the “Mutual Fund Sahi Hai” campaign was a success:

1. Addressing Common Fears

The campaign directly tackled widespread fears about mutual funds being risky or illiquid, making the concept more accessible to ordinary investors.

2. Simplified Messaging

Complex financial jargon was broken down into easy to understand language, demystifying mutual funds for the average person.

3. Relatable Scenarios

Ads used everyday situations, like the samosa stall example, to create relatable, real-life contexts that resonated with people.

4. Celebrity Endorsements

Celebrities like Sachin Tendulkar were used to build trust and credibility, making mutual funds seem more reliable to the general public.

5. Multi-Platform Reach

The campaign was spread across TV, digital, radio, print, and cinema, ensuring that it reached a diverse audience across urban and rural areas.

6. Multi-Language Approach

By launching the campaign in multiple local languages, it ensured inclusivity and better comprehension across different regions of India.

7. Consistent Engagement

Continuous outreach and education over time helped reinforce the message and convert potential investors into actual mutual

fund participants.

A similar approach could work in Bangladesh, where people have a deep cultural inclination toward saving but may not be fully aware of the options available beyond fixed deposits and savings certificates. Asset managers need to make mutual funds seem as familiar as any other financial product, highlighting their flexibility, accessibility, and potential for higher returns over the long term.

While the government in Bangladesh has made financial inclusion a priority, the private sector, especially asset management companies, has a critical role to play in driving mutual fund awareness. Expecting the government to single-handedly shoulder this responsibility would be a missed opportunity. Companies need to step up by investing in campaigns that focus on education rather than just promotion.

The success of a “Mutual Fund Sahi Hai” equivalent in Bangladesh would rely heavily on collaboration between the private sector, financial regulators, and the media. The campaign would need to address the specific financial concerns of Bangladeshis, many of whom live in rural areas or have irregular incomes. By showcasing how mutual funds can serve as an accessible tool for both short-term liquidity needs and long-term wealth growth, such a campaign could

significantly alter the financial landscape of the country.

India’s “Mutual Fund Sahi Hai” campaign not only transformed how people viewed mutual funds but also fundamentally shifted the country’s financial ecosystem by democratizing investment opportunities. For Bangladesh, a similar campaign could be a game-changer in addressing the country’s financial literacy gap and promoting more diversified investment portfolios.

The mutual fund industry in Bangladesh has enormous potential, but for it to grow, it needs the same kind of public trust that India’s campaign was able to cultivate. Through a collaborative, education-first approach, Bangladesh could see a similar transformation, enabling millions more to participate in wealth creation beyond traditional fixed-income products. The future of Bangladesh’s mutual fund industry might very well depend on this crucial step toward greater financial literacy.

FY 2024-25

“The company reported a profit of BDT 5,906.1 million, up from BDT 4,606.3 million in the previous year.”

Marico Bangladesh, a leading FMCG company in the country, delivered robust profit growth in FY 2024-25 (April–March) despite a challenging macroeconomic environment. The company reported a profit of BDT 5,906.1 million for the period, up from BDT 4,606.3 million in the previous fiscal year. This remarkable performance underscores the company’s resilience and strategic execution in a difficult market. Let us examine the key factors driving this achievement.

Revenue Growth (BDT Millions)

Note: Double-digit Revenue Growth

Marico Bangladesh achieved strong revenue growth during FY 2024-25 despite a challenging macroeconomic environment marked by the aftermath of the July revolution and persistently high inflation. The company recorded a 12.3% year-on-year increase in revenue, a notable achievement under such conditions. The growth was driven by key segments, including Value Added Hair Oil (VAHO), Parachute, and Health & Beauty. Revenue from the

VAHO segment rose 14.7% YoY, from BDT 4,236.4 million in FY 2023-24 to BDT 4,858.7 million in FY 2024-25. Parachute Coconut Oil recorded a 10.1% YoY increase, growing from BDT 8,592.8 million to BDT 9,464.0 million. The Health & Beauty segment delivered the strongest growth, with revenue expanding 28.1% YoY. The only exception was the Color segment, which experienced a decline during the fiscal year.

(BDT Millions)

Marico’s diversification strategy is proving effective, as the company gradually reduces its reliance on its core brand, Parachute Coconut Oil. The brand now accounts for approximately 58% of total revenue, down from over 60% in FY 2020-21. According to

Marico Bangladesh’s annual report, the company’s products are now present in an estimated 89.5% of households across the country, reflecting both strong market penetration and the success of its broader brand portfolio.

Marico Bangladesh’s gross profit rose 15.3% in FY 2024-25, driven by both higher revenue and an expansion in gross profit margin. The company’s gross profit margin improved to 59.5% during the period, up from 51.8% in FY 2022-23. This margin expansion was primarily supported by strong sales growth in the VAHO segment and enhanced cost efficiency across operations.

20-21

BDT 968.9 million, primarily from investments. These factors contributed to a net profit of BDT 5,906.1 million for the fiscal year, reflecting the company’s robust operational and financial performance despite challenging market conditions. Profit (BDT Millions)

Marico Bangladesh’s operating profit rose 15.4% year-on-year, increasing from BDT 6,150.8 million in FY 2023-24 to BDT 7,095.7 million in FY 2024-25. The company also recorded strong growth in finance income, which surged 67.1% year-on-year to

"The growth was driven by our flagship brand Parachute coconut oil and the launch of innovative value added products in the hair care and skin care categories.”

- Saugata Gupta Chairman, Marico Bangladesh

State-owned Rupali Bank is preparing to roll out its new mobile financial service, RupaliCash, tomorrow, following the closure of its previous platform, SureCash, in September. The bank plans to offer the service using its own technology, aiming to provide a modern, customer-focused alternative.

Robi, the country’s second-largest mobile operator, is set to launch 5G services today in select areas of Dhaka, Chattogram and Sylhet, marking Bangladesh’s first-ever commercial rollout of the technology stated in a report.

Guardian Life Insurance Limited has launched a redesigned mobile application, introducing a more streamlined and user-friendly digital experience for insurance customers. The new app, available on both Android and iOS, blends modern design with advanced functionality to provide a one-stop solution for policyholders and new users alike.

Grameenphone has officially launched its fifth-generation (5G) mobile network services, bringing the next era of connectivity to all divisional cities of Bangladesh stated in a report.

bKash Limited, the country’s leading mobile financial services provider, has been honoured with a prestigious international award for its excellence in real-time data innovation. The recognition highlights bKash’s success in leveraging big data and advanced data-driven technologies to deliver secure and customer-centric digital financial services stated in a report.

Dhaka Bank PLC has unveiled an innovative AI-powered digital loan service, eRin Device APP, aimed at making smartphones and smart devices more accessible to service professionals, micro-entrepreneurs, and underserved communities across Bangladesh, stated in a report.

Toyota, a Japanese multinational automotive manufacturer, has entered a new era in Bangladesh with the launch of Toyota Bangladesh Limited, which will serve as the sole official distributor for the brand, stated in a report.

ADN Telecom Ltd has teamed up with South Korea's PBS Co Ltd and CND Motors Co Ltd for agreements that cover electric three-wheeler assembly, smart traffic systems, and solar streetlights, stated in a report.

Walton Hi-Tech Industries PLC is set to merge with Walton Digi-Tech Industries Limited, a move expected to strengthen the company’s position in the high-tech and digital manufacturing sector stated in a report.

Renata PLC, a listed drug manufacturer, has launched its first product in the Canadian pharmaceutical market stated in a report.

Akij Venture Group has inaugurated South Asia’s largest and most modern packaged drinking water production line, stated in a report.

The event brought together corporate leaders, senior executives, brand custodians, and industry experts. The evening also included the unveiling of the upcoming Superbrands publication. This book will profile the recognised brands for the next two years.

Novartis (Bangladesh) Limited has been renamed as Nevian Lifescience PLC, following the acquisition of its majority shares, stated in a report.

Omera Petroleum, a subsidiary of MJL Bangladesh PLC, has acquired almost all shares of Premier LP Gas Limited — commonly known as Totalgaz Bangladesh — for Tk227 crore, subject to regulatory approval.

Popular actress Masuma Rahman Nabila has been announced as the new brand ambassador for Veet Bangladesh, the country’s leading depilation brand for over 25 years, stated in a report.

The government has initiated the process of seeking new investors for Nagad, one of the country’s fastest-growing mobile financial service (MFS) providers stated in a report.

City Bank PLC has introduced a new feature on its mobile banking platform, Citytouch, allowing customers to directly purchase life insurance policies online, stated in a report.

Bangladesh's leading mobile financial service (MFS) provider, bKash Limited, has entered into a strategic partnership with Gulf Exchange, a financial institution in Qatar, to strengthen cross-border remittance facilities for the Bangladeshi diaspora, stated in a report.

Unilever Bangladesh Limited has appointed Ruhul Quddus Khan as its new chief executive officer and managing director, effective November 1st. A veteran of the company, Ruhul began his career in 1996 through the Unilever Future Leaders' Programme and has since held key leadership roles across supply chain and research and development in both Bangladesh and India, stated in a report.

BRAC Bank wins accolade at Global SME Finance Awards

BRAC Bank PLC has been recognised as the "Sustainable SME Financier of the Year" in Asia for its innovative Water, Sanitation and Hygiene (WASH) financing initiative. The accolade highlights the bank’s efforts to support small and medium enterprises while driving social impact across the country, stated in a report.

Popular actor Siam Ahmed has joined Aygaz United as the new face of the brand, marking the beginning of a partnership aimed at strengthening consumer engagement in Bangladesh’s LPG sector, stated in a report.

Banglalink has launched Bangladesh’s first AI-driven Complaint Management System in the telecom sector, setting a new benchmark for customer service in the country, stated in a report.

Meghna Innova Rubber Company Ltd, a concern of Meghna Group, is producing truck, bus, and agricultural tyres at its expanded facility in Tangail, which is expected to fill the gap left by a recently closed local tyre manufacturer, stated in a report.

In a landmark move for the country’s financial sector, the central bank has granted preliminary approval to five private entities to establish credit bureaus, aiming to bring greater transparency and competition to Bangladesh’s lending market stated in a report.

Domino's rebrands for first time in over a decade

As part of the chain's "hungry for more" strategy, it will modernize its color scheme, implement a bolder typeface and graphics and debut new music as well as brighter packaging and a new name-bending jingle.

Amazon UAE, in partnership with certified recycler Enviroserve, has launched a new initiative featuring over 150 drop-off points across Dubai to help customers easily recycle packaging from their Amazon.ae deliveries.

Lay’s is introducing a bold new look to help people see the brand for what it truly is. Marking its most significant visual overhaul in almost 100 years, the global rollout features a refreshed logo and packaging — anchored by a simple, authentic message.

Amazon developing consumer AR glasses to rival Meta,

Amazon is reportedly developing consumer-grade augmented reality (AR) glasses, according to The Information. The move would position the tech giant in direct competition with Meta in the growing AR market.

PepsiCo's CEO says fiber will be the next protein

PepsiCo is betting big on fiber, calling it “the next protein.” CEO Ramon Laguarta said during an earnings call that consumers are increasingly recognizing fiber’s benefits, noting it as a key dietary gap in the U.S.

Coca-Cola to debut mini 7.5-ounce cans in U.S. c-stores

Coca-Cola is introducing 7.5-ounce single-serve mini cans of its most popular sodas in U.S. convenience stores starting early next year, targeting consumers looking for more affordable and lower-calorie options.

Tesla has launched a new lower-priced standard version of its Model Y SUV in Europe, aiming to boost demand amid a slowdown in the region’s electric vehicle market.

AB InBev, the world’s largest beer company, has announced a global partnership with Netflix, marking a major expansion of collaboration between its iconic beer brands and the streaming giant. The large-scale agreement covers AB InBev’s entire global brand portfolio.

BYD marks 14 millionth NEV milestone with delivery to Brazil’s Head of State

BYD celebrated a major milestone as its 14 millionth new energy vehicle rolled off the production line at the company’s passenger car plant in Camaçari, Brazil.

OpenAI video app Sora hits 1 million downloads faster than ChatGPT

OpenAI says the latest version of its text-to-video artificial intelligence (AI) tool Sora was downloaded over a million times in less than five days - hitting the milestone faster than ChatGPT did at launch.

Connectivity

(The evolution of global mobile internet connectivity from 2015 to 2024, including the percentage of people connected, the coverage gap and the usage gap.)

The rise of Generative Artificial Intelligence (GAI) promised a new era of efficiency and insight for professional services, particularly within the high-stakes domain of public sector consulting. Yet, the recent debacle involving global consulting firm Deloitte Australia and a critical assurance review for the Australian government has exposed the severe professional and governance risks inherent in unchecked automation. The discovery of fabricated legal quotes, non-existent academic citations, and phantom footnotes—classic examples of AI "hallucinations"—in a high-value government report has initiated a painful, global reckoning. This incident is not merely a case of professional negligence; it demonstrates how algorithmic inaccuracies can catastrophically erode the credibility of elite consultancies and directly jeopardize the integrity of government policy decisions.

At the center of this controversy was an independent assurance review of the Department of Employment and Workplace Relations’ (DEWR) Targeted Compliance Framework (TCF). This was a project of critical national importance: the TCF oversees the automated system responsible for imposing penalties on jobseekers, an area of welfare administration that operates under intense public and legal scrutiny, particularly in the wake of the devastating Robodebt scandal. Deloitte’s $440,000 AUD (approximately $290,000 USD) contract was intended to provide rigorous, unimpeachable assurance of this sensitive IT system.

Shortly after the report’s publication in July, external academics identified profound issues. University of Sydney researcher Dr. Christopher Rudge publicly noted that the 237-page document contained

multiple fabricated references, the tell-tale sign of GAI outputs accepted without verification. Most egregious was the misrepresentation of Australian common law, including a fabricated quote attributed to a Federal Court judge in the pivotal Deanna Amato v Commonwealth case, a ruling central to welfare debt liability.5 Furthermore, the initial report failed to disclose the use of any AI tools.

Following public exposure, Deloitte conducted an internal review, confirming that some footnotes and references were incorrect, and agreed to repay the Australian government the final installment of the contract. A corrected version of the report was subsequently published, which, for the first time, included a disclosure: Deloitte utilized a generative AI Large Language Model (Azure OpenAI GPT-4o) for a core analytical task—filling "traceability and documentation gaps" within the welfare system review.

The response from the political sector was swift and pointed. Labor Senator Deborah O'Neill characterized the firm as having a "human intelligence problem," criticizing the resolution as merely a "partial apology for substandard work". The underlying message was clear: the high fees paid for premium consulting services are meant to secure human diligence and expertise, not unchecked, automated content that can be generated by a publicly available chatbot.

The Deloitte incident provides a definitive case study in how professional firms risk their foundational credibility when they prioritize the economic efficiency of automation over the duties of quality control and due diligence.

Consulting firms like Deloitte have invested billions in GAI, marketing these tools as accelerators for audits and reports. The economic temptation—using AI to draft complex sections faster, submitting the prod-

uct under the firm's elite banner, and pocketing the maximized margin—is immense. However, this model operates on a deep contradiction: clients pay a premium for professional judgment, yet the deliverable contained errors that, as one politician noted, would earn a "first-year university student" deep trouble.

The consensus among analysts was that the technology did not fail; rather, "GPT-4o did not malfunction. Deloitte's process did". The LLM performed exactly as designed, generating fluent, plausible text, including convincing but false citations. The failure was the human decision to submit this content to a high-stakes government client without verification against primary sources.

This collapse in quality assurance creates a severe credibility deficit across the entire professional services sector. The incident, following closely after other high-profile consultancy scandals, reinforces public and political mistrust, raising fundamental questions about the veracity of all external assurance reports. When the evidentiary basis of a report—particularly one dealing with legal and welfare compliance—is shown to have been manufactured, the firm is essentially substituting a "Services-as-Software" approach for genuine expertise. The revelation that the firm often replaced one fabricated reference with multiple genuine ones in the corrected report suggests the original claims themselves lacked a clear evidential basis, further undermining confidence in the report’s underlying analysis. For high-stakes contracts, the market is no longer simply demanding innovation; it is demanding demonstrable proof that firms can deploy GAI responsibly without sacrificing the essential human insight they are paid to provide.

The most dangerous impact of GAI hallucinations is on the integrity of government policy and decision-making. In the public sector, decisions frequently affect fundamental rights and entitlements, relying on accurate interpretations of statutes, regulations, and case law.

The fabrication of a quote from a Federal Court judgment in Amato was particularly alarming. Deloitte’s initial report misstated the law regarding the burden of proof in welfare debt cases. Providing the Commonwealth government with advice that misstates Australian common law, especially in a system dealing with citizen welfare penalties, amplifies legal and ethical risk to an extreme degree.

If the errors had not been caught by a diligent external academic, the government could have proceeded to base policy modifications or legal defenses on a fundamentally incorrect legal premise presented in the assurance review. The ability of GAI to produce compelling, yet false, legal and regulatory synthesis means that government agencies accepting such reports risk making decisions that could be illegal, unjust, or vulnerable to successful challenge. The resulting policy choices would be built upon an algorithmic lie, shaking public confidence in the administration of justice and welfare programs.

“ The Deloitte incident provides a definitive case study in how professional firms risk their foundational credibility ”

The DEWR report was commissioned specifically to review the integrity of an automated penalty system. The report itself found serious flaws, including a lack of traceability between IT system rules and underlying legislation. When an assurance review of an already fragile automated system is itself compromised by automation, it signals a systemic failure of oversight. It mandates a zero-trust model for all GAI-assisted external deliverables, where every critical source and data point must be manually verified against primary sources by a domain expert.

The failure of professional diligence in this context validates fears that consultants might utilize GAI not to enhance quality, but to cut corners on the critical, painstaking work necessary to ensure legal and factual compliance.

The Deloitte incident served as a necessary catalyst for regulatory reform, forcing the Australian government to move swiftly from relying on ethical principles to imposing binding contractual mandates on vendors.

The Commonwealth introduced new AI Model Clauses designed specifically for government buyers procuring services where the seller may use AI. These clauses directly address the core failures observed in the Deloitte engagement:

1. Approval and Transparency: Consultants must obtain explicit client approval before utilizing AI in service provision. The failure to disclose GAI use upfront, as Deloitte did in the initial report, is now contractually forbidden.

2. Mandatory Quality Assurance: Sellers are now obligated to conduct specific quality assurance checks to confirm the accuracy and reliability of all AI outputs.

3. Record Keeping: Detailed records of AI use must be maintained throughout the engagement.

This shift establishes a new governance paradigm, integrating risk management directly into procurement contracts. The implication is that accountability for AI's outputs cannot be outsourced; the government client must maintain oversight and possess the contractual authority to verify how GAI has been applied.

The paramount lesson of the Deloitte case is that while GAI offers undeniable speed, it must be rigorously governed. For high-stakes public sector

work, the responsibility of a consulting firm is not merely to produce fluent text, but to deliver verifiable, evidence-based truth. Preserving the integrity of both the consulting industry and the machinery of government policy requires that human expertise—verified, certified, and fully accountable—remains the indispensable guarantor of quality, ensuring that the algorithmic lie never becomes policy reality.

“ The Deloitte incident served as a necessary catalyst for regulatory reform, forcing the Australian government to move swiftly from relying on ethical principles to imposing binding contractual mandates on vendors. ”

Source: Nike

Nike's introduction of the "Why Do It?" (WDI) campaign marks a watershed moment in global brand strategy, representing a sophisticated evolution from a command-driven, performance-first ethos to a philosophy rooted in introspection and cultural purpose. This pivot is not a rejection of the legendary "Just Do It" (JDI), but it’s necessary, highly refined antecedent. JDI remains the ultimate call to action, but WDI provides the essential internal catalyst—the motivation required for that action to be sustainable and meaningful in the 21st century. This strategic shift is necessitated by a powerful convergence of logical, emotional, and analytical (market) imperatives, positioning Nike to not only secure its dominance with a new generation of consumers but to transcend product retail and become a global curator of meaning in sport.

The move to WDI is a pragmatic and logically necessitated response to evolving market dynamics and the inevitable aging of an iconic slogan. The brand required a radical update to address competitive

market share erosion experienced in recent years. While JDI maintained prominence since 1988, its sheer age risked saturation, demanding a strategy that could "freshen its appeal to a younger market."

Logically, the shift aligns Nike squarely with the principles of purpose-driven marketing. Today’s consumers expect brands to take a stand on societal issues and align with cultural value systems rather than transient product cycles.

By foregrounding the "Why," Nike wanted to establish a robust strategic anchor that ensures long-term resilience. A brand built upon a constancy of purpose—mirroring principles found in sophisticated management philosophies like Dr. W. Edwards Deming’s—is inherently more resilient and capable of long-term improvement than one built merely on transient execution.

The strategic dilemma centered on the cost of intimidation. The ubiquitous demand of JDI, as the brand grew in stature, risked morphing from an inspirational challenge into an intimidating, high-pressure expectation. WDI de-escalates this pressure by shifting the focus from intimidating, often unattainable outcomes, to the achievable moment of internal decision—reframing greatness as a choice, not an outcome.

DIMENSION “JUST DO IT” (THE ACTION) “WHY DO IT” (THE INTENT)

Core Focus

Execution, Immediate Action, Outcome (External)

Product Performance, Speed, Dominance Brand Alignment

Motivation, Intent, Internal Choice (Internal)

Social Issues, Cultural Relevance, Value-Driven Stance

STRATEGIC IMPLICATION

Shifts from performance metric to internal driver, appealing to purpose-driven consumers.

Secures long-term loyalty by meeting the modern expectation for brands to take a stand.

The core driver of the WDI campaign is the unique psychological profile of the target audience, particularly Gen Z—the segment crucial for Nike's sustained growth.

Gen Z athletes are often considered as "more concerned with failure and judgment than past generations." They are growing up in an environment where attempting an action, and subsequently failing, can feel daunting, where the temptation to quit often overwhelms the motivation to persist. In this context, the bold, immediate command to "Just Do It" acts paradoxically as a deterrent, not an invitation.

The WDI campaign strategically addresses this emotional paralysis by focusing on the narrative of internal struggle and vulnerability. Its cinematic anthem features raw depictions of elite athletes confronting the "unfiltered side of sport," validating the emotional battle involved. This acknowledgment of the inner conflict creates a shared human experience that the action-command structure of JDI inherently struggled to replicate.

The emotional focus shifts dramatically from external expectations of "glory and grit" to the more intimate, manageable concepts of "choice, courage,

and participation." This strategic move recognizes that emotional support has become a vital component of the modern brand offering. WDI's emotional appeal validates the struggle ("I understand you are tempted to quit") before offering the solution ("But look inward and find your reason"). This validation builds a foundation of deep trust and emotional connection, proving far more durable than relying solely on aspirational performance messaging.

This trajectory was tested and proven effective during the 2018 JDI campaign featuring Colin Kaepernick, which demonstrated that leveraging the brand to align with a cultural cause—even a controversial one—fosters deep, enduring emotional connections. Nike learned that true success in the digital age requires a degree of polarization—a willingness to take a firm stand—to generate the loyalty required for long-term market resilience.

The transition from a definitive command to an introspective question elevates Nike from a supplier of sports apparel to a philosophical guide in the athlete's journey.

The question, "Why Do It?", transforms into an existential prompt that encourages profound self-reflection, compelling consumers to articulate their personal values, motivations, and the complex relationship they hold with sport and society. By framing the brand around a question rather than a statement, Nike ensures perpetual cultural rele vance. Asking "Why Do It?" catalyzes the sort of "conversations and debates" that previous purpose-driven campaigns proved essential for fostering massive engagement and brand buzz.

This philosophical maneuver leads to the third-order strategic implication: ownership of purpose. The command of JDI belonged to Nike; it was the brand’s directive to the consumer. WDI shifts that ownership

entirely, forcing the consumer to define their motivation. By enabling the athlete to own the answer to "Why Do It?", Nike achieves the most integrated level of brand alignment possible: the consumer’s personal, deeply held purpose becomes inextricably linked to