Issue 05 February 2026

Issue 05 February 2026

INT RO D U CIN G

Presenting our Sharif Kitchen Sinks for hassle-free everyday kitchen work. Non-magnetic, scratch-resistant stainless steel sink of international-standard, designed for your stress-free kitchen moments

For the February edition of Market Script, we return to fundamentals.

We begin by examining the macroeconomic signals and key leadership movements shaping the months ahead. Our Spotlight explores a defining global paradox: gold prices climbing sharply while the US dollar so�ens—unpacking what this divergence reveals about investor psychology and global confidence.

Capital markets take center stage, supported by analytical insights and a conversation with leaders from BRAC EPL Stock Brokerage Limited. Beyond equities, we expand the lens—from global shipbuilding dynamics to disciplined personal investment allocation— balancing structural perspective with financial strategy.

We revisit the legacy of Sheikh Akij Uddin, place Olympic Industries Limited under focused review, and explore how Pepsi challenges CocaCola on the Super Bowl stage.Through Urban Echo, we also decode the growing nursery business economy shaping our cities.

As markets fluctuate and industries evolve, Market Script remains committed to delivering clarity through rigorous, contextual insight.

Mar-25 Feb-25

Export (In USD Billions)

E-Commerce Transactions (In BDT Millions)

Internet Banking Customers (In Millions)

Internet Banking Transactions (In BDT Millions)

Internet Subscribers - December 2025 (Millions) Telco Subscribers - December 2025 (Millions)

HumairaSultana has been appointed as the Chief Executive Officer (CEO) and Managing Director (MD) of Biman Bangladesh Airlines.

Monzula Morshed has been appointed as Deputy Managing Director and Chief Human Resources Officer (CHRO) of BRAC Bank PLC.

and Chief Executive Officer of

Md

been appointed as the Managing Director and Chief Executive Officer of

G.M.KamrulHassan has officially been appointed as the Chief Executive Officer of the Igloo Category at Abdul Monem Ltd.

The Dhaka Stock Exchange (DSE) has appointed SnehashishBarua as an Independent Director.

MuidurRahmanTanvirhas been appointed as the Chief Executive Officer of Mitsubishi Motors Rangs Limited.

Md.LatifHasan has been appointed as Deputy Managing Director of United Commercial Bank.

The global economic architecture, long anchored by American financial hegemony and post-war institutions, is currently undergoing a seismic shi�. As reported by Al Jazeeraʼs Counting the Cost, a confluence of economic volatility and geopolitical realignment is reshaping the world map.

From the soaring price of gold to Indiaʼs high-stakes trade pivots and the nearbankruptcy of the United Nations, a clear pattern emerges: the "Guardians of the Global Order" are retreating, and the rest of the world is scrambling to hedge its bets.

This analysis examines the three pillars of this transition— the decline of the dollar, Indiaʼs strategic trade recalibration, and the erosion of multilateral governance.

"The rise in gold prices is not just a market trend; it is a vote of no confidence in the current geopolitical stability."

The most visible barometer of global anxiety is the inverse relationship between the US dollar and gold.The dollar, historically the worldʼs reserve currency and the backbone of global growth, is under severe pressure. Over the past year, greenback has lost approximately 10% of its value against a basket of global currencies, marking its worst annual performance since 2017.

This decline is not merely an accident of market volatility; it appears to be partly a matter of policy. President DonaldTrump has historically viewed a strong dollar as a disadvantage, arguing that it hampers American competitiveness. As noted in the transcripts, Trump has previously fought against countries

like China and Japan for devaluing their currencies, asserting that a weaker dollar makes US exports cheaper and aids the onshoring of manufacturing. However, this "weak currency policy" is a double-edged sword.While it may assist exporters, it risks fueling inflation and reducing the purchasing power of American consumers.

As the dollar wobbles, investors are fleeing toward safe havens. Gold prices have been on a leak, hitting record highs, fueled by a "hedging strategy" where investors seek assets that perform well across multiple negative scenarios. The catalyst for this flight is twofold: uncertainty regarding US policy and the Federal Reserveʼs interest rate trajectory.

With interest rates effectively cut, the opportunity cost of holding non-yielding assets like gold has decreased, making the metal more

attractive than USTreasury bills. Furthermore, the weaponization of the dollar through tariffs and sanctions has unnerved global investors, prompting central banks to diversify their reserves.

However, analysts caution against declaring the immediate death of the dollar. While there is a shi� in investor flows, argumentatively this is not yet "true debasement".The creation of a viable alternative reserve currency—such as one proposed by the BRICS nations—remains a distant prospect. Building a currency settlement system takes decades, as evidenced by the slow international adoption of the Chinese RMB. For now, the dollar weakens, but it lacks a singular successor, leaving gold to serve as the primary beneficiary of American financial instability.

While the US grapples with currency valuation, India is aggressively positioning itself to fill the vacuum le� by shi�ing supply chains. New Delhi is attempting to transform into a global manufacturing hub and a democratic alternative to China.To achieve this, India has engaged in a flurry of diplomatic activity, concluding major trade agreements with both the European Union and the United States.

The agreement with the EU, described by officials as the "mother of all deals," was twenty years in the making. It promises to lower tariffs and open European markets to Indian textiles, leather, jewelry, and increasingly, electronic goods like mobile phones. Conversely, it opens Indiaʼs protected markets to high-value European agricultural products and wines. Analysts suggest that the "hidden hand" of DonaldTrumpʼs protectionism catalyzed this deal; both Brussels and New Delhi felt the urgent need to diversify export markets beyond a volatile United States. However, Indiaʼs subsequent arrangement with the United States—dubbed by some as the "father of all deals"—reveals the stark geopolitical costs of this economic expansion.The US has agreed to slash tariffs on Indian goods to 18% (down from 50%), but this economic boon comes with a "geopolitical catch": India must stop buying Russian oil.

This condition places India in a precarious macroeconomic position. Since the invasion of Ukraine in 2022, India had dramatically increased its reliance on Russian energy,

importing over a third of its oil from Moscow at discounts of up to 25%.This cheap energy was instrumental in helping India manage inflation and stabilize its economy during global turmoil.

This pivot could have severe consequences. Replacing discounted Russian crude with oil from theWestern hemisphere or the US will be considerably more expensive.While the trade deal promises increased exports to the US, the inflationary pressure of higher energy costs could destabilize India's domestic economy. Furthermore, the US expectation that India will purchase up to $500 billion in American energy and technology represents a massive financial commitment. India is thus attempting a difficult balancing act: alienating a traditional ally (Russia) to appease a new strategic partner (the US), all while trying to protect its domestic manufacturing ambition from the shocks of energy inflation.

While India's trade agreement with the EU is described as the "mother of all deals," its arrangement with the US—the "father of all deals"—comes with a "geopolitical catch": India must stop buying Russian oil.

Beyond currency markets and trade wars, the crisis of global order is manifesting institutionally at the United Nations.The UN is currently warning of a "race to bankruptcy," facing a record shortfall of over $2 billion.This financial crisis is existential, threatening the organization's ability to maintain peacekeeping missions and humanitarian aid.

The primary driver of this liquidity crisis is the United States. As the UNʼs largest donor, the US is responsible for approximately 95% of the money currently owed to the organization.This is not a matter of economic inability but of political will.TheTrump administration has

openly questioned the value and efficiency of the UN, viewing it as an impediment to American interests rather than a vehicle for them. By withholding dues,Washington aims to exert pressure, steer the UNʼs direction, or simply weaken the institution entirely.

The consequences of this "defunding" strategy are tangible and tragic.The UN Secretariat has been forced to cut its budget by 15% and reduce its workforce by 2,600 staff. More critically, theWorld Health Organization reported that 6,000 health centers had to shut down due to funding cuts, directly depriving millions of people in conflict regions of lifesaving assistance.

The UN, designed as the only inclusive body where all nations have a seat at the table, is being undermined in favor of exclusive clubs like the G7 or G20. However, the international community is attempting to adapt.There is an ongoing trend of "multilateralism minus one," where other nations continue to negotiate and cooperate on issues like international tax conventions without US participation.While the system survives, it is significantly frailer, forcing the UN to consider desperate measures such as accessing financial markets or implementing international taxes on maritime transport to bypass reliance on member state contributions.

The United States, once the guarantor of the global system, is becoming its primary source of instability—through the volatility of its currency, the protectionism of its trade policies, and the financial starvation of multilateral institutions. Investors are reacting by fleeing the dollar for gold. India is reacting by pivoting toward the West, even at the cost of its energy security and historical alliances.The international community is reacting by attempting to sustain global governance mechanisms despite American disengagement.

While there is currently no single viable alternative to the dollar-based system, the friction is palpable.The rise in gold prices is not just a market trend; it is a vote of no confidence in the current geopolitical stability.Whether it is the devaluation of the dollar, the coercion of Indian trade policy, or the bankruptcy of the UN, the message is consistent: the era of a unified, predictable global order is ending, replaced by a landscape of transactional diplomacy and economic survivalism.

THE CHANGING ARCHITECTURE OF BANGLADESH’S CAPITAL MARKET

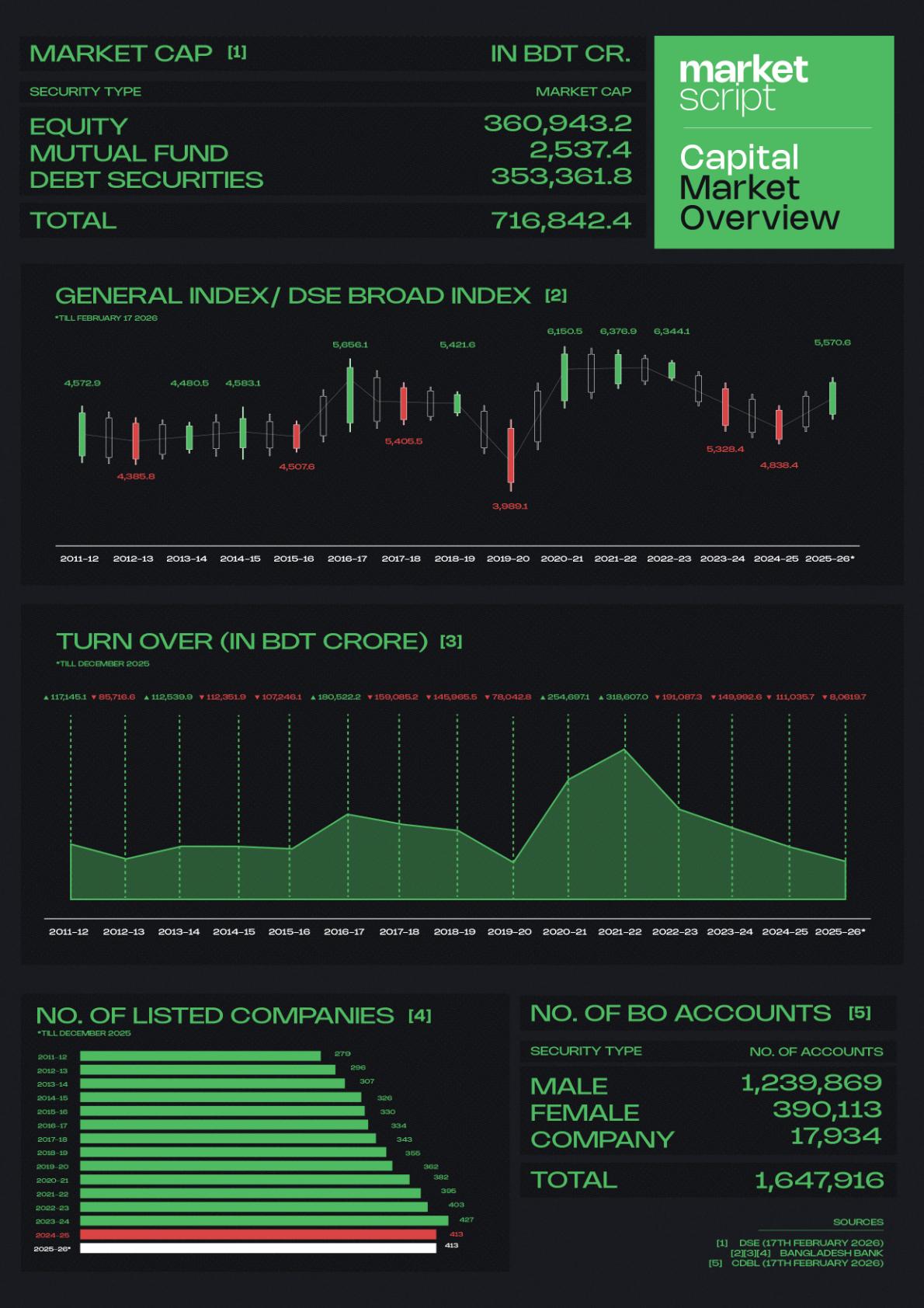

The evolution of the Bangladesh capital market over the last seventeen years provides a compelling case study of a frontier market navigating the peaks of speculative exuberance and the troughs of systemic correction. Dominated by the Dhaka Stock Exchange (DSE), the market has served as a barometer for the nationʼs broader economic transitions, reflecting shi�s in regulatory philosophy, global headwinds, and domestic stability.

The narrative of the modern Bangladesh stock market began with an unprecedented, meteoric rise in 2010. During this period, a confluence of liberal credit policies and a massive influx of retail investors created a "perfect storm" of speculation. Monetary policy at the time allowed for significant liquidity, and merchant banks aggressively provided margin loans to investors, many of whom possessed limited financial literacy.

By late 2010, the DSE General Index (DGEN) shattered historical records, surpassing the 8,900-point mark.This valuation was widely considered untethered from reality; price-toearnings (P/E) ratios reached levels that lacked any fundamental justification.The market was driven not by corporate earnings or dividends, but by a cycle of speculation and suspected manipulation.

In early 2011, the bubble burst with devastating speed.The index shed over 50% of its value within months.The crash was not merely a financial event but a social one.Thousands of retail investors, who had invested their

life savings or borrowed heavily to enter the market, faced total financial ruin.Widespread street protests erupted in Dhakaʼs Motijheel commercial area, prompting the government to intervene with bailout packages and a restructuring of the Bangladesh Securities and Exchange Commission (BSEC). A critical technical takeaway from this era was the realization that the DGEN index was flawed; it lacked free-float adjustment, making it easily manipulated. Consequently, it was discontinued in 2013 and replaced by the DSEX.

The years following the 2011 crash were marked by a "sideways" movement. Although the national economy maintained a steady GDP growth rate, the capital market failed to mirror this momentum. Investor trauma from the crash ran deep, and the market struggled with a persistent lack of "depth"—a term referring to the absence of large, high-quality blue-chip companies.

During this period, the market remained dominated by the financial sector, specifically

banks and non-bank financial institutions (NBFIs). Between 2012 and 2017, turnover stayed low, and foreign portfolio investment remained minimal. While the BSEC introduced some corporate governance reforms and pushed for the demutualization of the exchanges (separating ownership from trading rights), these structural changes did not immediately translate into market vibrance. A brief rally occurred in late 2017 and early 2018, spurred by Bangladeshʼs impending graduation from the United Nations' Least Developed Country (LDC) category.The DSEX crossed 6,300 points, but the euphoria was short-lived. Concerns over rising non-performing loans (NPLs) in the banking sector and a tightening liquidity environment caused the market to retreat once more by mid-2018.

By

September 2021,

the DSEX reached an all-time high of over 7,300 points.

The year 2025 has emerged as one of the most challenging periods for Bangladesh's capital market,

defined by a persistent erosion of investor confidence and significant structural shi�s. Operating under the interim government, the market has faced a "bearish" reality where reform-oriented regulatory moves have yet to translate into price recovery or increased trading activity.

administration faced bans and heavy fines.

The benchmark DSEX index concluded the year 2025 at 4,865 points, representing a decline of 6.73% from the previous year. This downturn was accompanied by a sharp 18% drop in average daily turnover, which fell toTk 521 crore.The shrinking role of equities in the national economy was further highlighted by the market capitalization-to-GDP ratio, which dipped to 12.21%. Despite technically attractive valuations with the price-toearnings (P/E) ratio sitting at a low 8.59 investors remained largely on the sidelines, spooked by volatility and a lack of fresh high-quality listings.

A hallmark of the interim government era has been a "cleanup" of the regulatory landscape.The reconstituted Bangladesh Securities and Exchange Commission (BSEC) took unprecedented punitive actions against influential figures and market manipulators. Highprofile investors and former officials including those linked to the previous

While these measures were welcomed by advocates for transparency, they initially contributed to a "freeze" in trading activity. Market insiders noted that the abrupt nature of these enforcement actions, combined with the formation of various task forces and focus groups, created a period of policy uncertainty where intermediaries and institutional players preferred to wait for stability.

The human cost of this turbulent year is visible in the departure of small investors. Approximately 66,500 Beneficiary Owner (BO) accounts were emptied of shareholdings in 2025, leaving only 12.05 lakh accounts with active shares.This exit reflects a deep-seated "investor fatigue" and a growing distrust in the marketʼs ability to protect the savings of retail participants a�er years of instability.

Despite the immediate gloom, 2025 laid significant groundwork for long-term recovery.The BSEC introduced new

margin loan and mutual fund rules, reduced BO account maintenance fees, and initiated efforts to bring state-owned enterprises and reputable multinational companies to the exchange.

Market analysts suggest that while 2025 was a year of "bitter medicine" and reform, the benefits may only materialize in 2026.The consensus among

market experts is that a genuine turnaround depends on three factors:

1. PoliticalClarity:The return of an elected government and a stable political roadmap.

2. MacroeconomicStability: Improvements in the broader economy, including law and order and private investment.

3. QualityIPOs: Moving away from a secondary market

dominated by speculative "junk" stocks toward fundamentally strong corporate listings. Ultimately, the interim government era will be remembered as a transitional phase that prioritized institutional integrity over shortterm price gains, leaving the market in a state of cautious anticipation for a new economic chapter.

Market analysts suggest that while 2025 was a year of "bitter medicine" and reform, the benefits may only materialize in 2026.

In Conversation with

Mr. Ahsanur Rahman

Bangladeshʼs capital market has been in a prolonged bearish phase. With the national election scheduled for February, how do you assess the post-election outlook for the market? What structural or sentiment-driven changes do you anticipate in the near to medium term?

Mr. Rahman: Post-election, markets typically react first to sentiment rather than fundamentals. If the outcome is credible and the transition is orderly, we should see a reduction in the political risk premium, which could trigger a relief rally. Early indicators would include stronger liquidity and improving trading volumes, as investors shi� from a risk-off to a risk-on stance. However, if uncertainty persists, sentiment can quickly reverse back into a risk-off phase.

In my view, among the structural changes that may follow the election—such as an increase in quality listings and stronger disclosure requirements, the most impactful will be the shi� toward technology-driven market access. As confidence returns and the government stabilizes, we should see faster adoption of digital trading infrastructure, smoother investor onboarding, and improved access to market information.

"While the 2025 IPO Rules have largely addressed the supply side by easing the pathway for quality companies to list, attention must now pivot decisively toward the demand side. A healthy capital market requires a strong, long-term institutional investor base"

From a policy perspective, which priority areas should the incoming government focus on restoring investor confidence and stimulate sustainable growth in the capital market?

Mr. Rahman:The incoming government should prioritise capital market reforms centred on stability, governance, and market depth. For us,

this translates into improving regulatory consistency, increasing the supply of quality listed companies, and developing a long-term institutional investor base. Without these elements, the market will remain retail-heavy, volatile, and unable to mobilise long-term capital effectively.

While the 2025 IPO Rules have largely addressed the supply side by easing the pathway for quality companies to list, attention must now pivot decisively toward the demand side. A healthy capital market requires a strong, longterm institutional investor base. Foreign portfolio investment in Bangladesh remains insignificant compared to regional peers. To strengthen our institutional base, we must actively attract foreign investment—and to do so, we must focus seriously on reclassifying our market status from Frontier to Emerging. This shi� is essential for foreign institutional investors to feel sufficiently secure to deploy long-term capital.

The new government should aim to transform Bangladeshʼs capital market and attract sustainable foreign investment. One of its highest priorities should be securing market reclassification by global index providers from frontier to emerging market status.

I would strongly advocate for the immediate formation of a National Task Force for Market Reclassification to align our regulatory and operational standards with global benchmarks. This effort must be guided by a clear, time-bound roadmap. To achieve our ambition of becoming a trillion-dollar economy, we must move beyond a bank-centric financing model. Transitioning from Frontier to Emerging Market status should be treated as a national economic priority. Vietnam offers a compelling example—its government made reclassification a core policy objective, coordinating closely between the central bank and the ministry of finance to remove technical barriers.

This reclassification is expected to unlock billions of dollars in foreign capital inflows, deepen market liquidity, and integrate Bangladesh more fully into global investment portfolios. I am prepared to assist the government in dra�ing the initial Terms of Reference (ToR) for this proposed Task Force. We have the IPO rules, and we have the potential. What we need now is the political will to synchronise our institutions and clearly signal to the world that Bangladesh is open for institutional business.

Despite its importance in developed markets, Bangladeshʼs listed bond market remains largely underdeveloped. What, in your view, are the key constraints behind this? How can regulators and policymakers incentivize corporates and institutions to issue and list bonds?

Mr. Rahman: Bangladeshʼs listed bond market remains underdeveloped primarily because incentives on both the supply and demand sides are weak. From a corporate perspective, bank loans are easier, faster, and more convenient, which naturally makes bank financing the preferred option. In contrast, issuing listed bonds is still perceived as complex, time-consuming, and costly due to multiple approval layers and the involvement of numerous intermediaries.

A further structural constraint is the lack of market infrastructure, particularly the absence of an official benchmark yield curve and robust valuation standards. Without reliable pricing benchmarks, bonds cannot be priced efficiently, which suppresses trading activity.

Consequently, secondary market liquidity remains thin, and a functioning ecosystem of market makers has yet to emerge. On the investor side, long-term institutional funds continue to remain parked in fixed deposit receipts (FDRs), awareness of bond products is limited, and confidence in credit ratings and issuer credit quality remains weak.

To address these challenges, regulators could simplify issuance by introducing fast-track approvals for repeat and high-rated issuers, alongside shelf registration or medium-term note programs.

Policymakers should also publish a benchmark yield curve, ensure regular bond price dissemination through exchanges, and introduce measures to stimulate institutional demand. In addition, targeted tax incentives, stronger oversight of credit rating agencies, and enabling bond repos or collateral eligibility at Bangladesh Bank would significantly enhance market liquidity and investor confidence.

"Our ultimate goal is to cultivate an investor base that is not just larger, but more resilient—"

BRAC EPL Stockbrokerage Ltd has emerged as the market leader in foreign portfolio trading. Could you share the strategic pillars, operational strengths, or institutional practices that enabled the company to achieve this leadership position?

Mr. Rahman: First, trust and governance. We place a premium on transparency, robust internal controls, and the strict confidentiality of client information.

Second, uncompromised research. At BRAC EPL, we focus on independent, high-integrity research—our views are driven by fundamentals and data, not short-term market narratives. We emphasize transparency of assumptions, consistency in methodology, and clear articulation of risks, enabling investors to understand not just our recommendations but the rationale behind them.

Third, execution excellence. We treat execution as a product in itself—fast, accurate, and consistent, particularly in a market where microstructure frictions can materially affect outcomes.

Fourth, operational strength and client service. Foreign institutional investors value seamless onboarding, responsive communication, clean trade allocations, and dependable posttrade support, all of which are core to our operating model.

We also take pride in our long-standing partnerships with leading global brokers. Beyond business, these relationships have helped elevate our internal standards, as we have learned directly from their best practices across markets. As a result, we have aligned ourselves more closely with international expectations in execution quality, compliance, and investor servicing.

"Our objective is not merely to digitize brokerage services, but to build a true fintech bridge—one that enables every Bangladeshi with a smartphone to participate in the countryʼs growth story."

The company has recently placed strong emphasis on financial literacy through initiatives such as “Jene Bujhey Binoyog” and its MoU with BICM. What long-term objectives underpin this focus, and how do you see financial literacy shaping the future investor base?

Mr. Rahman: Our long-term objective behind initiatives such as Jene Bujhey Binoyog and the MoU with BICM is very clear: to help build a stronger, safer, and more mature investor base in Bangladesh.

Market volatility in Bangladesh is driven not only by macroeconomic factors, but also by a persistent education gap. The capital market remains heavily retail-dominated, and when investors lack financial literacy, they become more vulnerable to rumors, panic-driven behavior, and, unfortunately, manipulation.

For us, financial literacy is therefore not a CSR initiative, it is a long-term market development strategy. A better-informed investor base encourages more rational participation, healthier long-term savings behavior, and ultimately a more stable and resilient capital market.

We also believe that financial literacy today must be complemented by digital literacy. Many potential investors are losing money not only in the stock market, but even before entering it—through online scams, fake platforms, and widespread misinformation. Our aim is to redirect these individuals toward the regulated capital market by providing proper guidance, access to verified platforms, and education rooted in responsible investing.

Importantly, we do not view investor education through a traditional lens. The future lies in scalable, technology-driven learning—microlearning formats, mobile-first modules, practical investor safety training, and structured programs capable of reaching new communities beyond the usual urban and metropolitan circles.

Our ultimate goal is to cultivate an investor base that is not just larger, but more resilient investors who understand risk, avoid shortcuts, and participate with knowledge and discipline

In mid-2025, BRAC EPL Stockbrokerage partnered with BRAC Bank to enable BO account opening via the Astha app. How has the market responded, and how does this integration advance your broader digital transformation and client acquisition strategy?

Mr. Rahman: Todayʼs investors prioritize convenience, speed, and seamless digital access. At BRAC EPL Stockbrokerage, our digital transformation initiatives have been deliberately designed to deliver exactly that. Our core focus has been on building an end-to-end digital ecosystem that makes the investing experience simpler, faster, and more reliable for both new and existing investors.

A major milestone in this journey has been the launch of our proprietary trading platform across both web and mobile—BRAC EPL Trade. This has significantly strengthened our execution capabilities and enabled us to deliver more consistent investor experience through improved speed, transparency, and service quality. The platform allows investors to access trading and account services anytime, anywhere—capabilities that are now a baseline expectation for modern market participants.

Another critical pillar of our transformation has been integration with trusted financial platforms. By connecting our services with BRAC Bankʼs Astha app and bKash, we have made transactions easier, safer, and more convenient, while reducing friction across the investor journey.

Our objective is not merely to digitize brokerage services, but to build a true fintech bridge—one that enables every Bangladeshi with a smartphone to participate in the countryʼs growth story. We are increasingly focused on empowering investors through data, analytics, and intelligent tools, evolving from a traditional service provider into an essential part of our clientsʼ everyday financial lives.

You assumed the role of CEO at BRAC EPL Stockbrokerage with 18 years of professional experience. Could you briefly walk us through your career journey and the leadership principles that have shaped your growth in the capital market?

Mr. Rahman: My 18-year career in the capital market has evolved through distinct phases. I began by building a strong foundation in market fundamentals—understanding valuation, investor behaviour, and the workings of Bangladeshʼs market microstructure. In the early years of my career, I worked in the back office, before transitioning to the front office as a fulltime trader.

During my eight years as Head of International Trade & Sales, I had the opportunity to participate in multiple international roadshows and global investor conferences—exposure that relatively few professionals in our market experience. These engagements allowed me to interact directly with global fund managers, frontiermarket specialists, and institutional traders, and to understand first-hand how they assess markets like ours. More importantly, they gave me a clear view of the standards global investors expect in governance, transparency, research quality, and execution discipline—insights that continue to shape the way I think and operate today.

Over time, my role expanded into leadership—building teams, strengthening execution and operational processes, and contributing to institutional partnerships and digital transformation initiatives, including improvements in

platform access and transaction convenience for investors. Having worked across both the back office and the trading floor, I understand the business end-to-end. This perspective has been invaluable in leadership roles, as it enables me to align strategy with operational realities and execution discipline.

The leadership principles that have shaped my growth are straightforward: integrity and transparency. I operate with a client-first mindset, believe strongly in research-led and datadriven decision-making, and place a high priority on developing people. I focus on empowering teams with full ownership—giving them the freedom, confidence, and accountability to make decisions and deliver results.

Mr. Ahsanur Rahman CEO, BRAC EPL STOCK BROKERAGE LIMITED

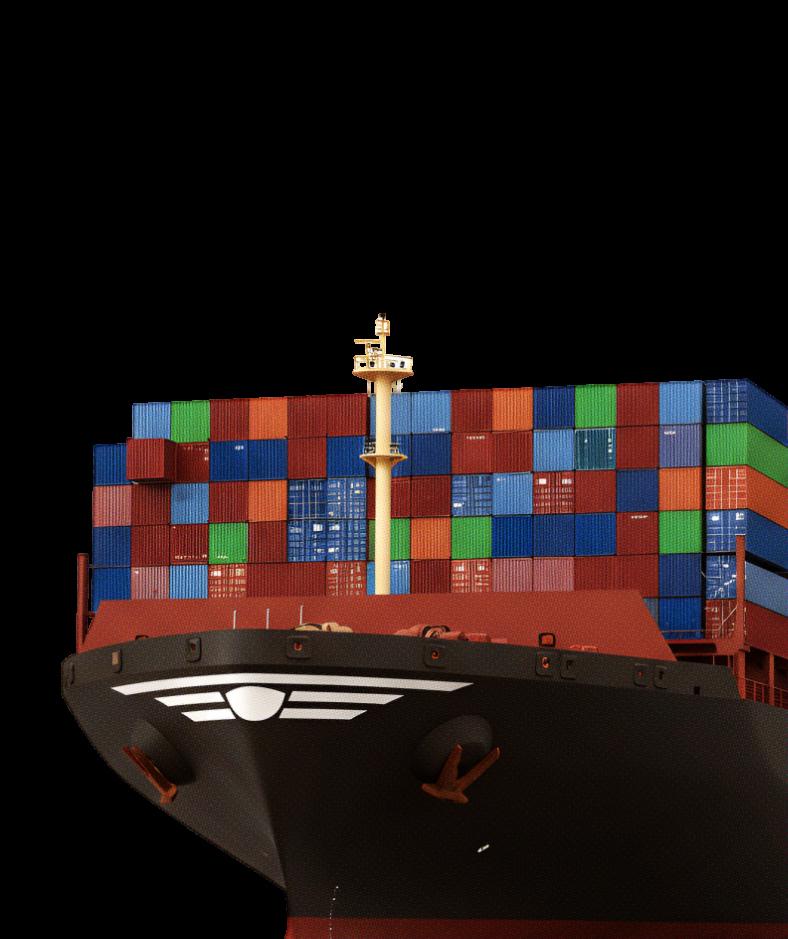

In the modern global economy, the movement of physical goods is the silent engine of commerce. From bicycles and couches to automobiles and childrenʼs toys, the vast majority of consumer products cross oceans to reach their destinations. For decades, the

provenance of the ships carrying these goods was a diverse mix of industrial powers. However, in the 21st century, a singular shi� has occurred: the infrastructure of global trade has become overwhelmingly Chinese.

China is now, by a significant margin, the world’s largest shipbuilding nation.

The statistics are staggering, approximately 34% of all ships currently on the water were manufactured in China. Even more telling for the future of the industry is the order book, where China holds 57.1% of all ships currently under construction. This dominance extends beyond the vessels themselves to the wider ecosystem of logistics; today, 95% of shipping container production is owned and operated by China.

As the United States contemplates a strategic "reset" to reclaim its maritime capabilities, it faces an economic and logistical chasm that may be impossible to bridge.

China's rise to the top of the shipbuilding hierarchy was neither accidental nor sudden. It was the result of a calculated convergence of state planning, economic timing, and resource management.

The historical trajectory of shipbuilding shows a migration of power fromWest to East. FollowingWorldWar II, the United States saw its shipbuilding capacity decline, ceding ground to Japan in the 1970s and South Korea in the 1980s. By the 2000s, China entered the fray, eventually overtaking its Asian neighbors to become the top shipbuilding nation.

Several key factors fueled this ascension:

1. StrategicStatePlanning:The Chinese government identified shipbuilding as a strategic sector essential for upgrading its economy from basic manufacturing to sophisticated production.This vision was codified in Beijingʼs 10th Five-Year Plan, which laid the foundation for

growing ports and the shipbuilding industry.

2. VerticalIntegrationand Infrastructure: China possesses a "strong domestic economy that is export-oriented," which naturally generates demand for ships. Furthermore, China owns the infrastructure required for the entire supply chain, including steel, aluminum, parts, components, and final assembly. This vertical integration allows for massive economies of scale.

3. SubsidiesandFinance: Shipbuilding is an incredibly capital- and labor-intensive industry.To overcome the barriers to entry, the Chinese government provided immense financial support. Between 2010 and 2018 alone, broad support for shipbuilding totaled $132 billion. This figure does not even account

In stark contrast to Chinaʼs industrial focus, the United States has evolved into a serviceoriented economy.

Manufacturing currently accounts for only 8% of total US employment.While the US was once the predominant force in shipbuilding, specifically during WorldWar II, when it built thousands of "Liberty" ships to support the Allied war effort— that capacity has all but evaporated over the last 80 years.

The degradation of US shipbuilding capability is illustrated by a precipitous drop in market share. In 2024, the United States built a mere 0.01% of the world's commercial ships.

million, whereas estimates for a comparable US-built ship hover around $330 million.This massive price difference explains why, between 2020 and 2022, China had over 4,000 large oceangoing ships on its order books, while the US had just 12.

Faced with this imbalance, political figures like Donald Trump have proposed aggressive measures to "resurrect" the American shipbuilding industry. The proposed strategy relies heavily on protectionism and punitive fees rather than organic market growth.

The central proposal involves raising revenue to boost US ship production through fresh levies on Chinese-built, owned, and operated ships.The suggested fees are exorbitant: starting at $1 million and potentially reaching $3.5 million every time a Chinese-built ship docks in the United States. Crucially, this policy would target not just Chinese companies, but any ship owner worldwide that includes Chinese vessels in their fleet.

The goal of these measures is to "even the playing field" and reduce dependence on a geopolitical rival. However, the economic consensus suggests that such a "reset" would have farreaching and potentially destructive consequences.

Industry experts have warned that the proposed levies could lead to a "trade apocalypse".The

immediate effect of taxing docking ships by millions of dollars would be a spike in freight rates.These costs would invariably be passed down to the consumer, driving up the cost of goods and exacerbating inflation.

Beyond direct costs, the logistical implications are profound.

• SupplyChainDisruption: Extreme levies could cause a ripple effect across US supply chains. Ships might reorient their current routing to make fewer stops in the United States to avoid the fees.

• ModalShi�s: A reduction in maritime stops would force a change in the distribution of goods, leading to increased reliance on road and rail transport between fewer ports, potentially clogging terrestrial infrastructure.

• TradeDiversion: Ultimately, this policy could divert trade away from US hubs entirely, altering the landscape of global trade economics.

The challenge is that the US is attempting to subsidize an industry that "isn't gonna make any money" and will cost taxpayers significantly, solely to achieve a strategic transition.

The push for US shipbuilding is not motivated by profit, but by national security and geopolitics. There is a growing concern in Washington regarding the strategic vulnerability of being unable to build ships or move goods independently of Chinese infrastructure.The argument posits that it is a security risk for the US to rely on a rival nation to transport its goods.

However, the "America First" approach of going it alone

ignores the existing assets of US allies. Japan and South Korea remain the other two dominant players in the shipbuilding triumvirate, alongside China. While the US lacks capacity, its allies possess the infrastructure and technical ability to produce high volumes of ships. A collaborative strategy involving these allies might be more feasible than a complete domestic overhaul, but current political rhetoric favors a solitary, manufacturing-centric approach.

The data suggests that a "grand restoration" of US shipyards is unlikely.The gap between the US and the Asian shipbuilding giants—China, Japan, and Korea— is so vast that a return to the dominance of theWorldWar II era is difficult to envision.

Chinaʼs dominance is built on decades of infrastructure investment, a skilled but affordable labor force, and hundreds of billions of dollars in state subsidies. For the US to compete, it would require a massive, sustained transfer of public wealth into private industry to bridge a $275 million per-ship price gap.

While tariffs and levies may serve as political tools to signal a "reset" in relations with China, the economic reality is that the US has transformed into a service economy. Reverting to a heavy manufacturing model for shipbuilding involves fighting against decades of economic evolution and the entrenched, subsidized dominance of Chinese industry. As the US weighs its national security anxieties against economic efficiency, the consumer is likely to pay the price for any attempt to turn the tide.

The Capital Market Deserves a Place in Your Financial Planning.

Ask a typical Bangladeshi saver where their money is parked, and the answer is almost always the same – Fixed Deposit Receipt (or FDR) It feels safe. It feels familiar. And for decades, it has been treated as the default option for anyone who wants to reduce investment risk, assuming one has placed money into a wellgoverned bank or non-bank financial institution. But safety can o�en be the nemesis of opportunity.

Here is an uncomfortable reality. Over the past few years, inflation in Bangladesh has frequently remained above 9% per annum, meaning that most FDRs have struggled to deliver positive real returns to their holders.

Over the past few years, inflation in Bangladesh has frequently remained above 9% per annum, meaning that most FDRs have struggled to deliver positive real returns to their holders.

Over the last three years, average gross FDR returns were around 8.35%* per annum, while the average inflation rate hovered at 9.38% per annum. Net returns from FDRs are further reduced by taxes and additional costs such as bank charges and excise duties, as applicable.

This is not to say that FDRs are not an important short-term investment tool.They are both easy to evaluate and offer a defined return, but a complete allocation of your investment portfolio to FDRs may not produce an optimal result, especially over the long term.

While no financial option is a panacea to wealth, long-term investment into the ownership of reputable, growing blue chip companies via the capital market is an optional tool to the achievement of positive real returns over time.

When Bangladeshʼs GDP grows, investment and consumption increases, and Bangladeshʼs quality companies typically experience a marked enhancement in their financial results. As a shareholder in such companies, you stand to directly benefit from increased dividend distributions and gain in company valuation.

The capital market represents ownership in real businesses:

• You participate in strategic ownership decisions

• Your investment return is two-fold –recurring dividend distribution and valuation gain

• Tax on dividends received is 20%, while capital gains tax is 15%, comparable to or lower than that applied to most other investment returns

• You may also benefit from tax incentives, including a 15% tax rebate on share investment or 3% of taxable income, whichever is lower (subject to prevailing tax rules).

More likely than not, there is an outstanding company in Bangladesh with proven sponsor backing that you truly admire based on past performance and future growth prospects. Or perhaps there are several companies that you admire and would like to diversify into for a portion of your savings investment. Dedicating a long-term allocation to shares or a mutual fund that coincides to your investment philosophy introduces potential upside return opportunity to enhance the yield of your savings portfolio. This is not just theory. Over long periods, wellgoverned companies in Bangladesh have rewarded patient investors through consistent earnings growth and dividends, even during volatile market cycles.

Over the past 15 years, for instance, Square Pharmaceuticals has delivered a compound annual growth rate (CAGR) of approximately 12%, while BRAC Bank has generated around 18%. Such long-term performance illustrates how patient investors in well-governed companies can benefit from compounding and sustained value creation, reinforcing the potential rewards of a carefully considered equity allocation within a diversified savings portfolio.

Patient investors in well-governed companies can benefit from compounding and sustained value creation, reinforcing the potential rewards of a carefully considered equity allocation within a diversified savings portfolio.

So, how big could a potential allocation of your savings portfolio to equities be and how can it be executed?

An appropriate allocation depends on the overall size of your savings portfolio and your comfort in the ability to hold a long-term investment. If you are a more aggressive investor, you may wish to consider a higher allocation as a percentage of the portfolio. If you are simply looking to enhance your overall portfolio yield, you may wish to consider a smaller allocation. In any case, unless you are an experienced professional investor, I would strongly discourage the assumption of debt to make an investment into the capital market due to the potential mismatch in the timing and quantity of returns. In addition, the purchase/sale of shares or mutual fund units over time permits an investor to average his purchase/sale price within the allocation, rather than depend on a singular price point.

The decision to invest directly or indirectly via a mutual fund depends on several key questions:

• Do you wish to diversify your capital market investments?

• Is it difficult for you to track macroeconomic and sectoral trends?

• Would you likely have limitations/time constraints when assessing and monitoring your capital market investments?

• Do you anticipate that you may be emotional when experiencing price volatility?

• Is there a fund offering available with structure and holdings composition that shares your investment philosophy?

• And if so, is it your view that the asset manager, trustee and custodian of the fund are experienced and reliable?

If you respond affirmatively to the afore mentioned questions, you may wish to consider investing through the mutual fund you favor rather than direct investment.

MUMITUL ISLAM Manager, Investment and Trade, Green Delta Dragon Asset Management

Mumitul Islam is an investment professional with over eight years of experience in investment research and portfolio management. He currently serves as a Manager in the Investment andTrade Department at Green Delta Dragon Asset Management Company Ltd.

Mr. Islam holds a Bachelor of Business Administration (BBA) degree from North South University and has completed Level I of the CFA Program. He is currently pursuing CFA Level II.

Bangladesh has officially perfected the art of safe marketing. Our brands are polite, predictable, and positively boring. Discounts? Check. Celebrity endorsements? Check. Generic slogans that make you yawn? Double check.

But hereʼs the kicker—weʼre avoiding the one thing that makes marketing fun: revenge.

Yes, revenge marketing. Not bitter. Not toxic. Just smart, cheeky, and unforgettable. Itʼs the kind of marketing that makes people talk, share, and smile at ads instead of scrolling past them while muttering, “meh.”

"Marketing doesnʼt have to be a boardroom lecture. It can be a game. A joke. A story worth retelling... Right now, weʼre dying of boredom while the world laughs without us"

Globally, brands do this all the time. A competitor slips up. A campaign flops. Criticism hits. Instead of hiding, brands respond with wit and swagger. In Bangladesh?We retreat, whisper “letʼs not make waves,” and return to yet another billboard of a smiling celebrity holding a product. Riveting.

By avoiding this, our brands arenʼt just playing it safe, theyʼre turning marketing into a chore. Social media campaigns could be memorable, daring, even funny. Instead, theyʼre… polite. And politeness doesnʼt sell. Polite doesnʼt make you the topic of conversation at tea stalls orWhatsApp groups. Polite doesnʼt make a 20-year-old repost your ad because it made them laugh. Imagine this: a competitor is launching a flashy new product. A Bangladeshi brand says, “Uh… maybe we should respond next month.”

A brand that embraces revenge marketing? Instant memeworthy content, clever social media zingers, and headlines people remember.Thatʼs the difference between being forgettable and being unforgettable.

Hereʼs the irony: we spend millions trying to look cool—but refuse to be bold.We chase perfection, avoid controversy, and call it strategy. Meanwhile, brands that play a little, joke a little, and strike back in good humor?They win hearts, minds, and wallets. Bangladesh, itʼs time to admit it: marketing doesnʼt have to be a boardroom lecture. It can be a game. A joke. A story worth retelling. Revenge marketing isnʼt spite—itʼs strategy with personality.

And right now, weʼre dying of boredom while the world laughs without us.

So, hereʼs a radical thought: maybe itʼs time to stop being polite and start being unforgettable. Because in marketing, if youʼre not having fun, neither is anyone else.

And guess what, this is a revenge write up as well!

TASMIA

AHMED Directory of Strategy & Planning, MastheadPR

Bornon22August1929in Madhyadangavillage, FultalaUpazila,Khulna (thenBritishIndia).Hewas theonlychildofSheikh MofizUddinandMatina Begum.

Economichardshipforced himtodiscontinueformal schooling.Hele�home duringtheBengalfamine andtraveledtoCalcutta (nowKolkata)insearchof work,survivinghardships includingsleepingat Sealdahrailwaystationand takingsmalljobstoearn money.

Beganbusinessactivitiesin beedi(hand-rolled cigarette)manufacturing withhelpfromafamily friend.Healsoranasmall grocerystore.

By1954–55,hemarketed productsundertheAkij Beedilabel

SheikhAkijUddinformally organizedhisgrowing enterprisesintoAkijGroup, layingthefoundationsfor whatwouldbecomeoneof Bangladeshʼslargest industrialconglomerates.

Workedandsavedsome capitalinPeshawarbefore returningtohisvillagewith amodestamounttostart entrepreneurialventures.

1980s-

1990s

AkijGroupexpandedinto multiplesectorsincluding textiles,cement,jute, pharmaceuticals, ceramics,printing& packaging,andfood& beverages.

Underhisleadership,Akij Groupbecameamajor employerinBangladesh withoperationsacross diverseindustries.

2006

10 October

SheikhAkijuddinpassed awayatage77in Singapore.Atthetimeof hisdeath,AkijGrouphad becomeacornerstoneof Bangladeshʼsindustrial landscape.

Banglalink Digital has launched a new suite of data portfolios aimed at rewarding long-term users with repurchase bonuses and quarterly advance packs, the operator has announced. Launched on January 30, these initiatives aim to provide additional data to customers who regularly purchase specific high-value packs. Under the repurchase bonus program, customers who buy a new pack within the validity period will receive a 25GB bonus with theTk699 pack and a 35GB bonus with theTk819 pack.

BRAC Bank PLC has introduced Google Pay for itsVisa credit cardholders, enabling fast, secure, contactless payments using Android smartphones, locally and internationally. Cardholders can add their cards to Google Wallet for use at millions of Google Paysupported merchants.This eliminates the need for physical cards and offers greater convenience and security through advanced encryption.

PRAN-RFL Group has entered Bangladesh's motorcycle market, with plans to invest approximatelyTk 500 crore over the next three years.The company aims to establish a manufacturing and assembly facility at Habiganj Industrial Park, which is expected to create direct and indirect employment opportunities for around 5,000 people.

SCB

EBL have formalized a strategic

Standard Chartered Bangladesh and Eastern Bank PLC. have formalized a strategic agreement to expand access to export receivables financing across Bangladesh.This partnership combines Standard Chartered's extensive global network with Eastern Bank's deep local market expertise, creating enhanced opportunities for the country's exporters.

Eastern Bank PLC. recently signed an agreement with Zantrik Limited, an automobile repair and maintenance service provider in Dhaka, to offer financing facilities for car purchases.

Grameenphone is taking connectivity beyond borders with its new 5G roaming service—designed for travelers who donʼt want their internet to slow down when theyʼre on the move. Now live inThailand, Malaysia, Norway, Sweden, and Denmark, the service will expand to more destinations over time.With a compatible 5G smartphone and a GP SIM, customers can stream without buffering, work seamlessly on the go, share moments instantly, and travel with confidence—knowing their internet is always ready to keep up, wherever the journey takes them.

PRAN-RFL Group , Bangladesh's leading food processor, secured approximately $5.5 million in export orders at the fiveday Gulf Food Fair 2026, one of the world's largest food exhibitions, which concluded on January 30 at the DubaiWorld Trade Centre. Orders for biscuits, noodles, beverages, and confectionery came from the USA, China, Saudi Arabia, Iraq, Syria, Ethiopia, Kenya, Somalia, and other markets.

Tanveer Food Ltd, a subsidiary of the Meghna Group of Industries (MGI), has launched “Fresh Coffee” in the Bangladesh market.The new brand was officially introduced on Saturday, February 7, at a local hotel in Dhaka.

In a recent conversation with Mr. Sohail Hamid Khan, CEO of Junaid Jamshed (J.), Markedium sought to understand the brandʼs vision, market entry rationale, expansion route, go-to-market strategy, similarities and differences between Bangladesh and Pakistan, and the broader market opportunity in Bangladesh. Below is a summarized version of the interview.

Mr. Sohail Hamid Khan

CEO,

JUNAID JAMSHED (J.)

J. has built a strong footprint across Pakistan and international markets. Why was Bangladesh selected as the next strategic destination, and what factors made this expansion timely from a business and brand perspective?

Sohail Hamid Khan: Bangladesh represents one of South Asiaʼs most dynamic consumer markets, driven by a growing middle class, strong cultural identity, and increasing appetite for structured retail. From a strategic standpoint, the timing aligns with our regional expansion roadmap and the brandʼs maturity to scale into markets that share cultural affinities while offering new growth headroom.

What specific gap in the Bangladeshi fashion and lifestyle market does J. aim to fill? In simple terms, why should a Bangladeshi consumer choose J. over existing local and international brands?

Sohail Hamid Khan: We see a gap in the organized modest lifestyle segment that integrates fashion, fragrance, and accessories under one cohesive brand. J. offers a complete lifestyle ecosystem built on quality, affordability, and cultural relevance providing a consistent retail experience that blends tradition with contemporary design.

"While our core brand DNA remains consistent, the Bangladesh rollout emphasizes faster consumer feedback loops and omni- channel integration compared to earlier international expansions."

Could you walk us through your Bangladesh expansion model physical retail, partnerships, supply chain localization, or digital touchpoints and how it differs from your previous international rollouts?

Sohail Hamid Khan: Our entry model combines flagship physical retail with a strong digital presence, supported by localized supply chain partnerships to ensure agility and efficiency. While our core brand DNA remains consistent, the Bangladesh rollout emphasizes faster consumer feedback loops and omni- channel integration compared to earlier international expansions.

How do you read the Bangladeshi fashion consumer in terms of taste, price sensitivity, lifestyle aspirations, and cultural influence? What insights stood out most during your market assessment?

Sohail Hamid Khan: The Bangladeshi consumer is culturally rooted yet globally aware. There is a strong appreciation for modest fashion, cra�smanship, and value-driven purchasing, balanced with rising lifestyle aspirations. One key insight was the demand for quality and authenticity at accessible price points.

From a fashion, retail, and consumer behavior standpoint, where do you see the strongest similarities between the Bangladeshi and Pakistani markets and where do they fundamentally diverge?

Sohail Hamid Khan: Both markets share strong cultural foundations and festive-driven purchasing behaviour. However, Bangladesh has its own textile heritage, climate considerations, and distinct aesthetic preferences. Understanding these nuances allows us to respect similarities while tailoring execution thoughtfully.

J. is widely known for its values-driven, Islamic-inspired branding and marketing approach. Will this philosophy remain consistent in Bangladesh, or do you anticipate adapting it to local cultural nuances?

Sohail Hamid Khan: Our values driven philosophy remains central to the brand. However, we approach every market with cultural sensitivity. The core principles of modesty, integrity, and family orientation will remain intact, while communication styles may adapt to reflect local narratives.

To what extent will J.ʼs collections in Bangladesh be localized—whether in fabric choice, silhouettes, pricing tiers, or seasonal relevance versus maintaining a unified global design language?

Sohail Hamid Khan: We intend to maintain a unified global design language while adapting fabric weights, seasonal collections, and pricing tiers to local preferences. Localization will be strategic rather than cosmetic ensuring relevance without diluting brand identity.

Where do you see J. Bangladesh in the next five years—in terms of store footprint, category expansion, brand equity, and contribution to the local fashion ecosystem?

Sohail Hamid Khan: Over the next five years, we aim to establish a strong retail footprint in key metropolitan cities, expand into multiple adjacent product categories, and build a brand that is trusted for both quality and consistency. Alongside we are keen on leveraging the ecommerce landscape in Bangladesh and look to establish a strong online sales channel to reach consumers beyond the metropolitan areas. All in all, we see Bangladesh becoming a meaningful contributor to our regional growth story.

Beyond consumers, what opportunities does J.ʼs entry create for local stakeholders such as suppliers, artisans, talent, and the broader retail ecosystem in Bangladesh?

Sohail Hamid Khan: Our entry creates opportunities for collaboration with local suppliers, retail professionals, and creative talent. We aim to contribute positively to the ecosystem by fostering employment, knowledge exchange, and long-term partnerships that strengthen the broader retail infrastructure.

As J. begins its journey in Bangladesh, what promise are you making to Bangladeshi customers and business partners and how should they define success for J. in this market?

Sohail Hamid Khan: Our promise is simple: consistency, quality, and respect for culture. Success for us will not only be measured in store count or revenue, but in the trust we build with customers and partners over time.

Olympic Industries, one of the leading biscuit and confectionery manufacturers in Bangladesh, posted a 9.6% profit growth in FY2024–25. Despite the adverse macroeconomic environment in Bangladesh, the company also recorded revenue growth during the fiscal year.

Olympic Industries strengthened its export performance in FY2024–25, with export revenue reachingTk 430.8 million.

During FY2024–25, the country faced a volatile macroeconomic environment, largely driven by the July revolution and persistently high inflation. Despite these challenges, Olympic Industries recorded revenue growth of 6.9% in FY2024–25.

The Biscuit & Confectionery segment, which contributes approximately 98% of total sales, grew by 6.4% compared to the same period last year. In volume terms, the segment expanded by 9.8%, reaching 127,581.6 metric tonnes (MT).

Meanwhile, the Battery segment posted a 36.2% increase in sales compared to the same period last year. In terms of volume, the company sold 57.3 million batteries, reflecting a 21.8% year-on-year growth.

Particulars

Olympic Industries strengthened its export performance in FY2024–25, with export revenue reachingTk 430.8 million. Domestic operations remained the primary revenue driver, generating Tk 27,290.2 million, up 6.7% year-on-year.

Gross profit rose by 7.5% year-on-year, supported by lower raw material costs, which enabled margin expansion despite moderate revenue growth.The gross profit margin improved marginally to 23.93% in FY2024–25 from 23.80% in the previous fiscal year.

Olympic Industries recorded a 9.6% growth in profit in FY2024–25, primarily driven by significantly lower finance costs and higher other income. However, operating profit increased by only 0.2% year-on-year, as higher administrative and selling expenses weighed on operating performance.

Administrative expenses rose by 9%YoY, while selling expenses increased by 12.2%YoY. Within selling expenses, salaries and allowances grew by 19.1%YoY, and advertising and promotional expenses rose by 6.5%YoY.

Finance costs declined sharply by 57.8% YoYtoTk 59.9 million. Meanwhile, other income—comprising cash incentives and investment income—increased by 88.4%YoYto Tk 576.0 million.

As a result, the company posted a net profit ofTk 2,010.4 million in FY2024–25, up fromTk 1,834.1 million in FY2023–24.

In the crowded marketplace of consumer goods, a bottle of soda or a jar of hot sauce usually competes for attention on a supermarket shelf. However, a significant shi� is underway. Food and beverage (F&B) giants are increasingly stepping out of the kitchen and into the makeup bag. From CocaCola teaming up with Brazilian beauty creators to Tajín adding spice to Rare Beauty, these collaborations are redefining brand relevance. This trend raises critical questions:Why are consumable brands pivoting to cosmetics? How do they leverage culture to drive sales? And what role do beauty creators play in legitimizing these unusual partnerships?

At first glance, the union of cola and cosmetics or hot sauce and lip gloss might seem like a random marketing stunt. However, the source material suggests this is a calculated strategic move designed to secure longevity in a market where consumer attention is scarce and loyalty is fragile.

The primary driver for this shi� is the desire to move a brand from a moment of consumption to a daily ritual. As the sources note, F&B brands typically "live in crowded aisles". By entering the beauty space, they gain a new stage.When a consumer applies a lip gloss inspired by their favorite soda or sauce, the brand effectively transcends its category, becoming a part of the consumer's personal routine rather than just a product they eat or drink.

The primary driver for this shi� is the desire to move a brand from a moment of consumption to a daily ritual.

Furthermore, these brands are not attempting to become full-fledged beauty companies or replace established beauty giants. Instead, they are prioritizing cultural relevance over category expansion.The goal is to stay part of the cultural conversation. By launching limited-edition collections, brands create a sense of urgency, buzz, and shareability that standard product advertising rarely achieves.

This transition allows brands to sell more than just taste; they begin selling "mood, identity, and selfexpression". Beauty is inherently personal and expressive, offering a way for F&B brands to tap into fashion and lifestyle sectors without abandoning their core identities. As one source poignantly summarizes, for these brands, "relevance isnʼt just tasted, itʼs worn".

The success of these collaborations hinges on their ability to be "culturally sharp" and visually arresting on digital platforms.The source material highlights that social media is th e real marketplace for these cross-industry partnerships.

Food-inspired makeup is designed specifically for the visual-heavy nature of platforms like Instagram, TikTok, and Reels.The "visual drama" of a chilli-red gloss or the vintage aesthetic of Coke-themed packaging travels much faster online than traditional product advertisements. For example, the Coca-Cola x BrunaTavares collection utilizes the brandʼs signature red-and-white palette and vintage visual language to turn everyday makeup into "Coca-Cola memorabilia".This visual distinctiveness makes the products collectible rather than clinical, encouraging consumers to showcase them on their own social feeds.

These collaborations also succeed by rooting themselves in pop culture. A prime example is Selena Gomezʼs Rare Beauty collaborating withTajín to create a chilli-inspired lip and cheek set.The partnership worked because it tapped intoTajínʼs existing "cult status," particularly among Gen Z, resulting in a product that felt "deeply rooted in pop

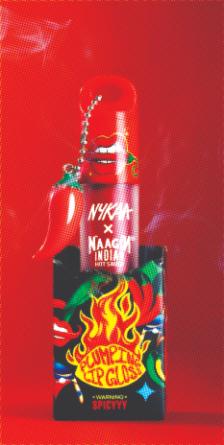

culture rather than product innovation alone". Similarly, in the Indian market, Nykaa Cosmetics collaborated with Naagin, a hot sauce brand, to launch a spicy lip-plumping gloss.This move capitalized on the local market's growing love for "heat, humour, and homegrown brands with personality".The collaboration wasn't just about the functional benefit of plump lips; it was about projecting an attitude that resonated with the cultural zeitgeist.

By engaging in these collaborations, brands show they are listening to younger audiences. Consumers today prefer brands that "experiment, collaborate, and show cultural awareness," finding them to be more human and relevant than those that stay strictly within their lanes.

Perhaps the most critical component of these partnerships is the role of beauty creators and established retailers.When a soda brand tries to sell mascara, it risks feeling out of place or gimmicky.To mitigate this, F&B brands utilize a strategy of "borrowed credibility".

Partnerships with established figures or platforms provide the trust that F&B brands lack in the cosmetic space. For instance, the Coca-Cola collection was not a solo venture; it was a team effort with BrunaTavares, a Brazilian beauty creator. Tavares brought "makeup credibility" to the table, ensuring that the products—ranging from eyeshadows to blush sticks—were viewed as

legitimate beauty items rather than cheap novelties. Retailers play a similar role.WhenTabasco partnered with Sephora for a heat-infused lip gloss, Sephoraʼs involvement brought "trust" to the experiment. Sephora has the unique ability to turn "novelty into desire," signaling to consumers that the product is

worth their money. Similarly, Nykaa provided the hot sauce brand Naagin with a powerful, mainstream beauty platform, elevating a condiment brand into the world of high-visibility cosmetics.

These creators and platforms act as the bridge between the kitchen and the vanity.They ensure that while the product may be inspired by a flavor, it performs like a cosmetic.The resulting products— whether it is a spicy lip plumper or a Coke-red mascara—allow the F&B brand to leverage the creator's authority to avoid the risk of their experiment failing or being perceived as a mere joke.

The trend of food and beverage brands entering the beauty space is "more than a gimmick". It represents a fundamental shi� in how companies view brand boundaries. By borrowing credibility from beauty creators and designing products that thrive on the visual drama of social media, brands like Coca-Cola andTajín are securing their places in the modern cultural landscape.

We can expect to see more of this in the future: "More flavours turning into finishes" as brands realize that the best way to stay fresh and visible is to step completely outside of their designated aisle. In doing so, they transform their identity from something you simply consume into something you proudly wear, ensuring they remain part of the conversation long a�er the bottle is empty.

A CASE STUDY ON OOH INNOVATION BY JARVIS AND BKASH LIMITED

When bKash - the number one mobile financial service (MFS) brand in Bangladesh onboarded Hamza Choudhury as its brand ambassador, it signaled far more than a routine endorsement announcement.

When bKash - the number one mobile financial service (MFS) brand in Bangladesh onboarded Hamza Choudhury as its brand ambassador, it signaled far more than a routine endorsement announcement.

As the countryʼs number one MFS platform, bKash has consistently shaped culture through its strong portfolio of top-tier brand ambassadors of Bangladesh, including celebrated actors like Afran Nisho and Mehazabien Chowdhury.These collaborations reflect the brandʼs stature, credibility, and deep integration into the everyday lives of millions of Bangladeshis. Its communication platform, “Ekshathe bKash Hobe,” is rooted in the belief that collective progress drives national growth.

At the same time, Hamza Choudhury: a Bangladeshi descendant who built his professional career at Leicester City F.C. made a decision that transcended club football. Choosing to represent Bangladesh from a lens of patriotism and identity, he became a symbol of aspiration for a football-loving nation that has long followed the global stage while yearning for meaningful representation of its own.

For a country where football passion runs deep but global visibility has been limited, Hamza represented hope, pride, and renewed belief.

Recognizing this cultural moment, bKash saw an opportunity not just to onboard a footballer, but to amplify the re-emergence of football in Bangladesh aligning its philosophy of collective growth with a national resurgence powered by identity, unity, and shared ambition.

But alignment in spirit is easy. Execution is not.

“Ekshathe bKash Hobe” -Together,We Grow - is a powerful line.Yet, in a world where celebrity announcements dominate attention, the question was critical:

How do you make togetherness real? How do you move beyond symbolic messaging and literally involve people in the celebration?

Jarvis was tasked with transforming a beautiful communication line into an experience that users could actively participate in.

The challenge wasnʼt visibility. It wasnʼt reach. It wasnʼt even relevance.The real challenge was participation.

“Ekshathe bKash Hobe” sounds simple. But in practice, most brand campaigns remain one-directional. A celebrity announces. The brand publishes.The audience watches. But this moment demanded something more.

Footballʼs re-emergence is not about one player. Itʼs about the

In a country where football passion runs deep but global visibility has been limited, Hamza represented hope, pride, and renewed belief.

fans.The streets.The children who dream.The collective belief that football belongs to Bangladesh again.

If the communication was about collective growth, then users couldnʼt remain spectators. They had to become part of the story.

The challenge was to design an idea where people didnʼt just see Hamza, they stood beside him. Not metaphorically. Literally.

bKash and Jarvis flipped the narrative. Instead of chasing celebrity-centric engagement, we made the audience the hero.

Rather than positioning Hamza as the sole face of the campaign, we built a system where every user could co-exist with him inside the same visual universe.

The idea was simple yet powerful: Bring “Ekshathe bKash Hobe” to life by allowing users to create their own moment with Hamza.

Not through static posts. Not through comment contests. Not through traditional digital mechanics. But through immersive technology. We leveraged augmented reality to collapse the distance between icon and individual.

If footballʼs resurgence belongs to everyone, then everyone deserves to be in the frame.

Bring “Ekshathe bKash Hobe” to life by allowing users to create their own moment with Hamza.

Jarvis created a custom AR filter experience that transformed users into co-creators.

Through the AR interface, users could:

• Generate dynamic images alongside Hamza

• Personalize their celebratory visuals

• Create their own branded football moment

• Download and share with their communities

The AR experience wasnʼt just a filter: it was a participation engine. Instead of watching a campaign unfold, users inserted themselves into it.

They werenʼt amplifying a celebrity.They were celebrating their own connection to football.

The personalization aspect added emotional ownership. Each image generated was unique. Each download carried pride. Each share extended the campaign organically.

The technology acted as a bridge between aspiration and access.

For the first time in a bKash ambassador announcement, users werenʼt reacting to content — they were generating it. But we didnʼt stop at digital participation.We extended it into the physical world.

To take co-creation beyond social media, Jarvis introduced Bangladeshʼs first AR-powered live billboard activation.

Hereʼs how it worked:

• Users clicked photos with Hamza using the AR filter.

• Their personalized ad sets were generated in real time.

• Selected visuals were pushed live onto billboards.

In that moment, something powerful happened. A user wasnʼt just posting online.They were standing tall on a billboard alongside Hamza in real time.

This blurred the boundary between digital and outdoor advertising.The campaign moved from phone screens to city skylines. And most importantly, it reinforced the core message: “Ekshathe bKash Hobe” isnʼt a slogan. Itʼs an action.

The personalization aspect added emotional ownership.

The billboard activation turned passive engagement into public pride. Users didnʼt just see the brand.They saw themselves inside the brand.

The campaign was launched during the time of a football match between Bangladesh and India which translated to traction even a�er the match had ended.

The impact was measurable, participatory, and scalable.Together with bKash, we successfully made users a literal part of the campaign.

• 14,661 Photos Generated

• 34,142 Downloads

• 5,979 Shares

• 1,679 Billboard Appearances

These numbers represent more than metrics.They represent co-creation at scale. Each photo generated signified ownership. Each download reflected emotional investment. Each share extended community engagement. Each billboard appearance validated participation in the most public way possible.

The campaign didnʼt just announce a brand ambassador. It built a movement around collective pride.

And it demonstrated that when technology enables access, people are eager to participate.

The campaign built a movement around collective pride.

Beyond impressions and downloads, the true success of this campaign lies in what it symbolized. Jarvis enabled bKash and its users to co-create.

We transformed a communication line into an interactive ecosystem.

“Ekshathe bKash Hobe” stopped being a promise and became an experience. Instead of placing Hamza on a pedestal, we placed users beside him.

Instead of telling people to celebrate footballʼs return, we gave them a platform to celebrate it themselves.

Instead of chasing attention, we designed participation.

In doing so, we demonstrated that modern brand building is no longer about broadcasting messages itʼs about building systems where audiences can step in and shape the narrative. Football re-emerged. But more importantly, belief re-emerged. And this time, it belonged to everyone.

Pepsi has decided to bypass subtlety entirely, launching an aggressive and playful salvo in the cola wars

In the high-stakes world of Super Bowl advertising, subtlety is rarely the strategy of choice. For Super Bowl LX, Pepsi has decided to bypass subtlety entirely, launching an aggressive and playful salvo in the cola wars by co-opting one of its rivalʼs most beloved symbols: the polar bear. By reviving the legendary Pepsi Challenge and aiming it squarely at CocaColaʼs mascot, Pepsi is looking to turn a cultural icon into a defector for its Pepsi Zero Sugar brand.

The centerpiece of the campaign is a 30-second spot that reimagines the classic blind taste test.The ad features a polar bear—an animal synonymous with Coca-Cola advertising since 1922 and a staple of their holiday marketing since 1993—making a shocking discovery. In the spot, the bear selects Pepsi Zero Sugar over Coke Zero in a blind test. This choice triggers an identity crisis for the mascot, leading him to a psychiatristʼs office to process his world-shaking realization.

The creative execution brings significant star power to the screen.The spot was directed by filmmakerTaikaWaititi, who also cameos as the bearʼs psychiatrist. Soundtracked by Queenʼs anthem "IWantTo Break Free," the ad follows the bear as he explores a new world populated by Pepsi Zero Sugar drinkers.The commercial also includes pop culture easter eggs, such as a nod to a viral Coldplay "kiss cam" moment from the previous summer.The creative work was led by BBDO and the PepsiCo Content Studio.

Pepsi views this campaign as a "big reset moment" intended to resonate throughout the year.The core strategy relies on the heritage of the Pepsi Challenge, a marketing promotion that first launched in 1975 to ask consumers to compare colas without brand bias.

According to PepsiVice President of Marketing Gustavo Reyna, the use of the polar bear is a method of highlighting consumer data in an entertaining way. Reyna notes that the company aims to prove Pepsi is the "best-tasting cola in the

market," a claim they state is confirmed by 66% of Americans based on 2025 Pepsi Challenge results. By showing even a polar bear—the ultimate Coke loyalist— reassessing his choice, Pepsi is encouraging consumers to "rethink their choice of cola".

Reyna describes this approach as a way to embrace the brand's "challenger DNA," utilizing a proven historical tactic to drive modern engagement.

The aggressive creative direction is underpinned by specific market realities.While Pepsi Zero Sugar currently lags behind Coke Zero in total market share (holding 1.4% compared to Coke Zeroʼs 4.6% of the carbonated so� drink market in the first nine months of 2025), Pepsi possesses the momentum.

Data indicates that Pepsi Zero Sugar is growing at a significantly faster rate than its rival.The brand saw its volume increase by 18.1%, overshadowing Coke Zeroʼs 4.8% increase over the same period. Furthermore, Pepsi Zero Sugar reached over one million new households and saw total growth of 30.8%. As Reyna explicitly stated, Pepsi Zero Sugar has become one of the company's "main growth drivers," prompting them to "double down" on the

The "polar bear defection" is designed as a multi-channel campaign rather than a standalone television commercial.The push includes out-of-home advertising, linear TV, podcasts, and creator content. Pepsi plans to lean into "edutainment" to inform consumers about the results of the Pepsi Challenge.

To amplify engagement during Super Bowl week, the campaign features specific activations such as a social giveaway on X, the delivery of complimentary Pepsi Challenge kits via Gopuff, and appearances by the polar bear character in the Bay Area and across social media